FHLBank Pittsburgh Mortgage Asset Management Spring 2005 Seminar Residential Mortgage Loans Hold or Sell? Hold or Sell Page 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FHLBank Pittsburgh

Mortgage Asset Management

Spring 2005 Seminar

Residential Mortgage Loans Hold or Sell?

Hold or Sell

Page 1

Reasons to make residential

mortgage loans:

• Important customer relationships

• Business opportunity

Hold or Sell

Page 2

Once an institution has committed to

making residential mortgage

loans it has two choices:

• Hold the loans

• Sell the loans

Hold or Sell

Page 3

Benefits of Holding

• Relatively low credit risk

• Higher yield than MBS

• GSE loans are fungible

Hold or Sell

Page 4

Mortgage Servicing Rights

Benefits of holding

Page 5

Hold or Sell

FDIC-Insured Office of

Mortgage Lenders* Thrift Supervision

Net interest margin 2004 3.05% 2.89%

Net interest margin 2003 3.36% 2.90%

ROA 2004 1.18% 1.17%

ROA 2003 1.38% 1.29%

ROA 2001 1.05% 1.07%

ROA 1999 1.03% 0.98%

ROE 2004 11.61% 12.79%

ROE 2003 15.08% 14.29%

* Institutions whose residential mortgage loans, plus mortgage backed securities, exceed 50%

of total assets

Mortgage Servicing Rights

Risks of holding

Page 6

Hold or Sell

Financial risks

Interest rate risk

Credit risk

Liquidity risk

Operations risk

Reputation risk

Legal risk

Repricing risk

Basis risk

Yield curve risk

Option risk

Interest rate risk for residential mortgages

• Potential for a gap or mismatch between assetsand liabilities because of the longer term andmarket volatility

• Difficult to estimate prepayment speeds andunderstand the optional component in residentialmortgages

• Be aware of interest rate caps on ARMs

Mortgage Servicing Rights

Page 7

Hold or Sell

Option risk

• High coupon residential mortgage loanshave more call risk

• Low coupon mortgage loans have moreextension risk

Mortgage Servicing Rights

Page 8

Hold or Sell

FDIC roundtable discussion on IRR management

“From an investor’s perspective, there is a “flaw” in the basic mortgage that is usedhere in the United States: it has an option in it”.

“When you invest in a mortgage, there are three things that can happen-and two ofthem are bad. One event is that rates go up and the value of the loan goesdown. A second event is that rates go down and the customer pays off the loan.A third event is that rates stay exactly the same and you earn exactly what youthought you were going to earn”.

“…asset liability management is an art, not a science. I think you have to look atyour models as a series of tools that help you build a circle around what your realexposures are and what your opportunities are.”

Mortgage Servicing Rights

Page 9

Hold or Sell

Managing the risks

• Utilize forecasting models and understand thesensitivity of model assumptions

• Partially fund the longer term loans with longerterm advances◦ Ladder medium term and long term fixed rate

advances◦ Use fixed rate amortizing or prepayment advances

• Use off balance sheet derivatives

Mortgage Servicing Rights

Page 10

Hold or Sell

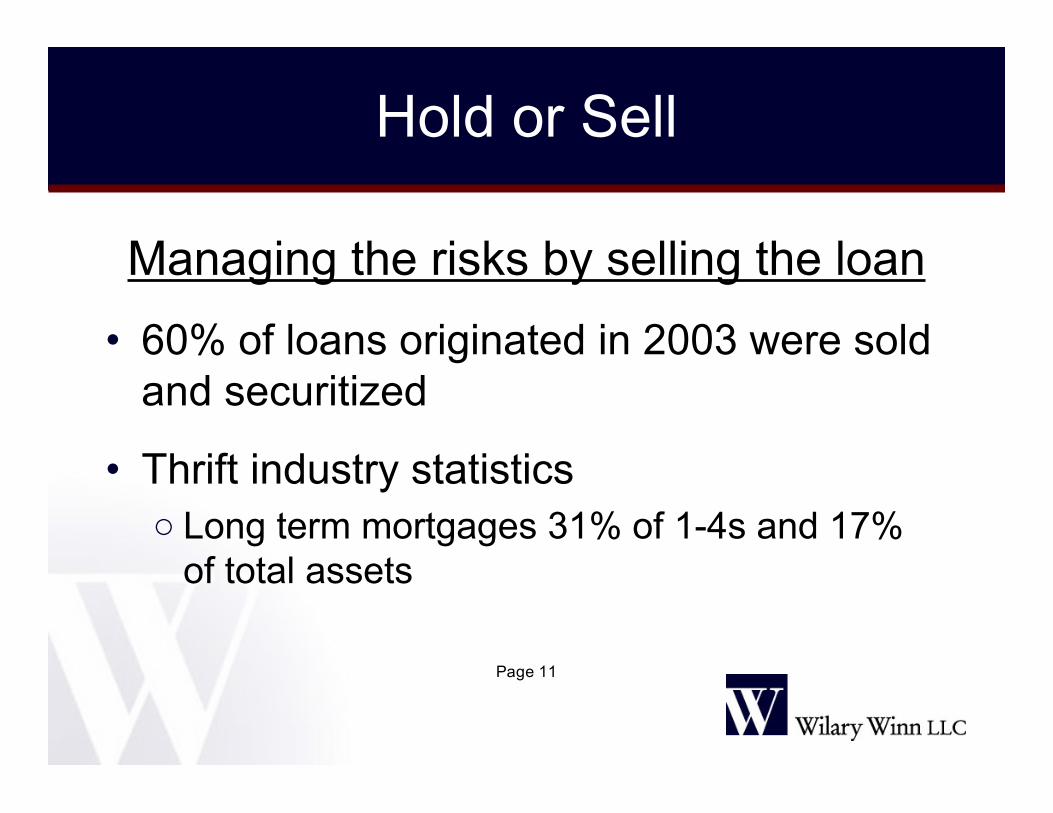

Managing the risks by selling the loan

• 60% of loans originated in 2003 were soldand securitized

• Thrift industry statistics◦ Long term mortgages 31% of 1-4s and 17%

of total assets

Mortgage Servicing Rights

Page 11

Hold or Sell

Sales have benefits and risks• Benefits◦ Reduce interest rate and credit risks◦ Generate potential gains

• Risks◦ Reinvestment risk◦ Generate potential losses if the loan sales are not

hedged or loans have been priced incorrectly◦ Potential loss of customer relationships if the loan is

sold servicing released

Mortgage Servicing Rights

Page 12

Hold or Sell

Sales decision should be based on abest execution analysis

• Where do I sell?

• How do I sell?

• What is my true economic sales price?

Mortgage Servicing Rights

Page 13

Hold or Sell

Where do I sell?

• FHLB

• Fannie Mae

• Freddie Mac

• Correspondent

Mortgage Servicing Rights

Page 14

Hold or Sell

How do I sell?

• Cash vs. MBS security

• Best efforts vs. mandatory and hedgingimplications

Hold or Sell

Page 15

Secondary MarketingBest efforts cash vs. mandatory MBS security

Page 16

Best efforts Mandatory

30 day MBS forward

cash price FNMA price

(SRP excluded) (Feb. settlement)

6.00% loan price 100.994

6.00% loan / 5.50% security price 101.6875

Adjustment for days -0.1319

Price 100.994 101.5556

Difference -0.5616

Note:

The MBS forward assumes a 25 basis point guarantee fee & a 25 basis point servicing fee

Hold or Sell

Best efforts

• Lower price

• Less risk

• Less control

Hold or Sell

Page 17

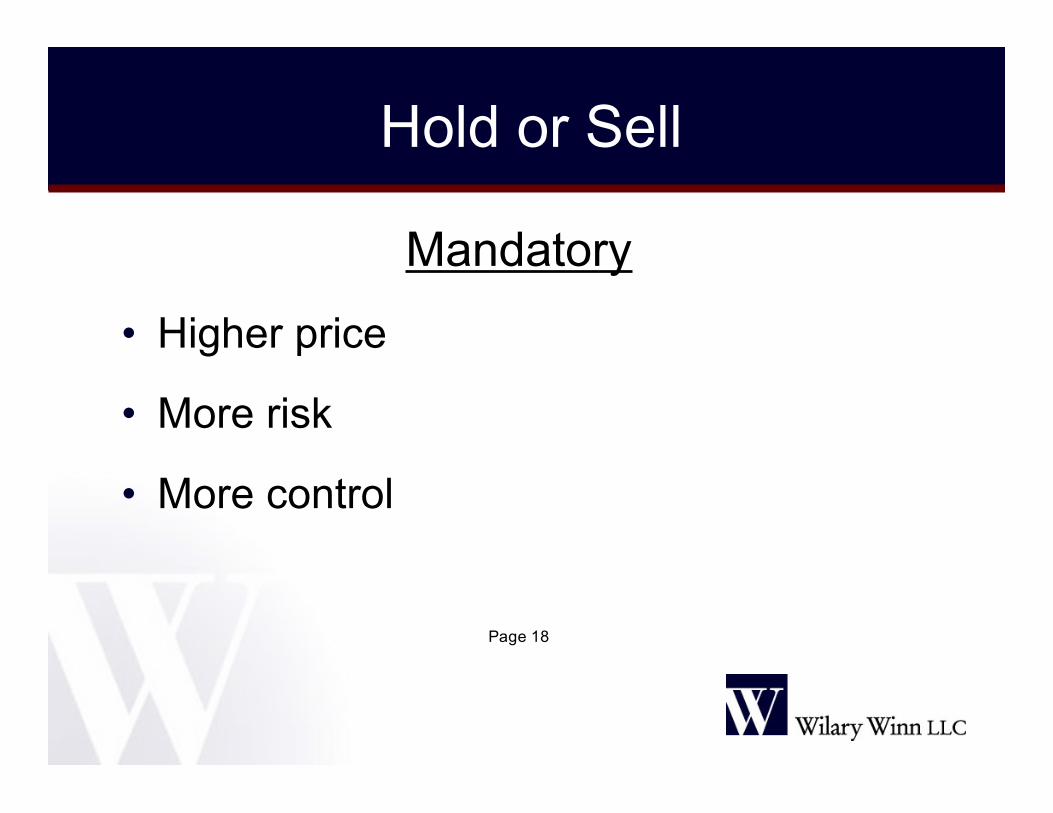

Mandatory

• Higher price

• More risk

• More control

Hold or Sell

Page 18

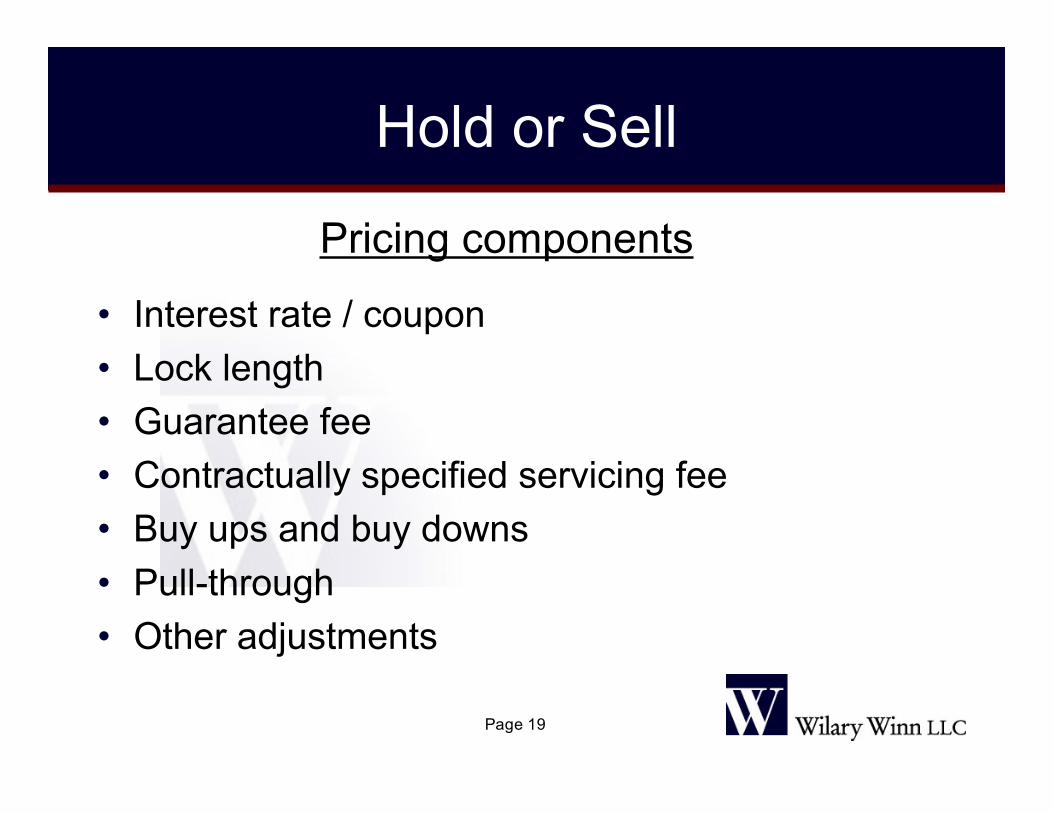

Pricing components

• Interest rate / coupon

• Lock length

• Guarantee fee

• Contractually specified servicing fee

• Buy ups and buy downs

• Pull-through

• Other adjustments

Hold or Sell

Page 19

Secondary MarketingPricing comparison

Page 20

Best efforts FHLB - sch./sch.

30 day 20 business daycash price cash price

(separate SRP) (retained servicing)5.875% loan price - $200,000 loan 101.285 101.498

Adjustment for day difference -0.029Fees to investor -0.175 0.000

SRP / Model Servicing Value 1.700 1.200SRP adjustment for non-escrows -0.250 N/A

Volume bonus 0.100 0.050PV of CE fee N/A 0.370

PV of CE obligation N/A 0.000Price 102.660 103.089

Difference -0.429

Conforming Fixed Rate

Hold or Sell

What is my true economic sales price?

• Value of servicing – retained or released

• Value of servicing remittance method

• Value of credit enhancement fee

• Value of credit enhancement obligation

• Value of interest carry on delivery

Hold or Sell

Page 21

Retained mortgage servicing rights

• MSRs are a modified interest only strip

• Many types of underlying loans

• Value varies significantly by type ofMSR

Hold or Sell

Page 22

MPF credit enhancement fee

• Paid to member for assuming a portion of thecredit risk (credit obligation) on mortgagedefaults

• Determined by the quality of the loans at thepool level and the MPF program selected

• Fee paid monthly over the life of the loans

• Sensitive to prepayments

Hold or Sell

Page 23

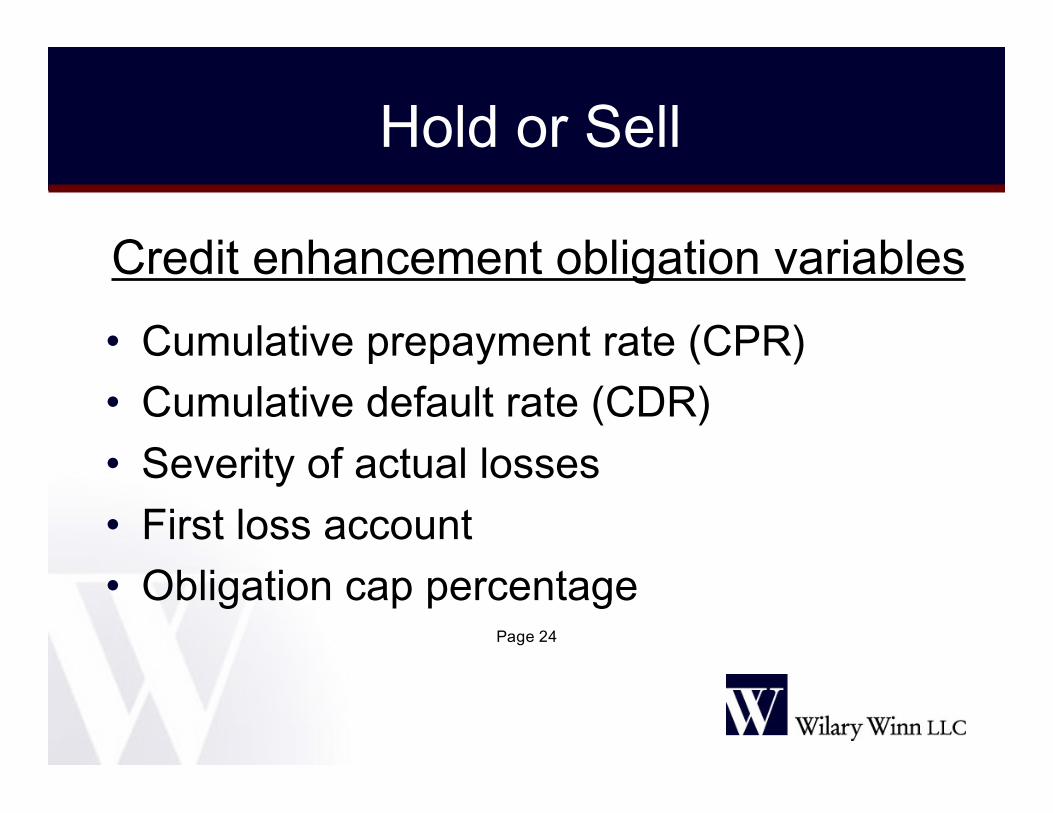

Credit enhancement obligation variables

• Cumulative prepayment rate (CPR)

• Cumulative default rate (CDR)

• Severity of actual losses

• First loss account

• Obligation cap percentage

Hold or Sell

Page 24

Credit enhancement obligation

Hold or Sell

PSA 0.00% 0.02% 0.04% 0.07% 0.15% 0.25%

150 0.51% 0.41% 0.32% 0.18% -0.20% -0.67%

200 0.48% 0.39% 0.30% 0.17% -0.19% -0.63%

250 0.41% 0.33% 0.26% 0.14% -0.16% -0.54%

300 0.37% 0.30% 0.23% 0.13% -0.15% -0.49%

500 0.26% 0.21% 0.17% 0.09% -0.10% -0.35%

700 0.21% 0.17% 0.13% 0.07% -0.08% -0.27%

Annual Losses After First Loss Account

Page 25

Value of interest carry on delivery

• Choose appropriate delivery datebased on actual cycle times

Hold or Sell

Page 26

Hedging

• An interest rate lock commitment (IRLC) is a crossbetween an option and a forward commitment

• Pricing and risk

• Mitigate risk by hedging

◦ Estimate fall-out on locked pipeline

◦ Control interest rate lock-in agreements

◦ Manage pair-offs and market movement

◦ Prepare mark-to-market and position reports

Hold or Sell

Page 27

Fallout risk

• Rate lock does not close

• Borrower renegotiates rate or discountpoints

• Loan closing date is extended

Hold or Sell

Page 28

Factors affecting fallout

• Market interest rates• Type of origination• Length of lock• Purpose of loan• Type of loan• Processing status of loan

Hold or Sell

Page 29

Hedging methodologies

• Pull-through

• Delta

• Modified Delta

Hold or Sell

Page 30

Secondary Marketing

Position and mark-to-market reporting

Page 31

Pipeline

Wavg Gain Gain Probabilty

Principal Interest Probability Days to Buy Sell (Loss) (Loss) * gain

Product Balance Rate of Close Close Price Price % $ (loss)

30 YR FIX 3,000,000 5.882% 84% 37 100.50 101.50 1.00 30,000 25,200

20 YR FIX 2,000,000 5.512% 81% 21 100.25 101.30 1.05 21,000 17,010

15 YR FIX 1,000,000 5.289% 87% 25 99.75 100.85 1.10 11,000 9,570

7 YR Bal. 1,200,000 5.127% 81% 30 100.75 101.25 0.50 6,000 4,860

ARMS 1,000,000 4.230% 89% 25 100.10 101.75 1.65 16,500 14,685

Total Pipeline 8,200,000 5.407% 84% 29 100.34 101.37 1.03 84,500 71,325

Hold or Sell

Background on Wilary Winn LLC

• Wilary Winn provides independent, fee-basedadvice to financial intermediaries, includingbanks, credit unions, finance companies, andmortgage bankers.

• Our services include assessments and valuationof complex financial assets, including mortgageservicing rights and credit enhancement feesreceivable, as well as the development andimplementation of interest rate risk managementprograms.

Hold or Sell

Page 32

Wilary Winn LLC

First National Bank Building

332 Minnesota Street, Suite W-1420

St. Paul, MN 55101-1314

651-224-1200

Frank Wilary [email protected]

Douglas Winn [email protected]

Hold or Sell

Page 33

Related Documents