Hilary Salt Member Trustee Network Conference 2013

Hilary Salt Member Trustee Network Conference 2013.

Dec 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Hilary Salt

Member Trustee Network

Conference 2013

Q: What is the aim of a pension scheme?

To pay the right amount of money, to the right people,

at the right time

A:

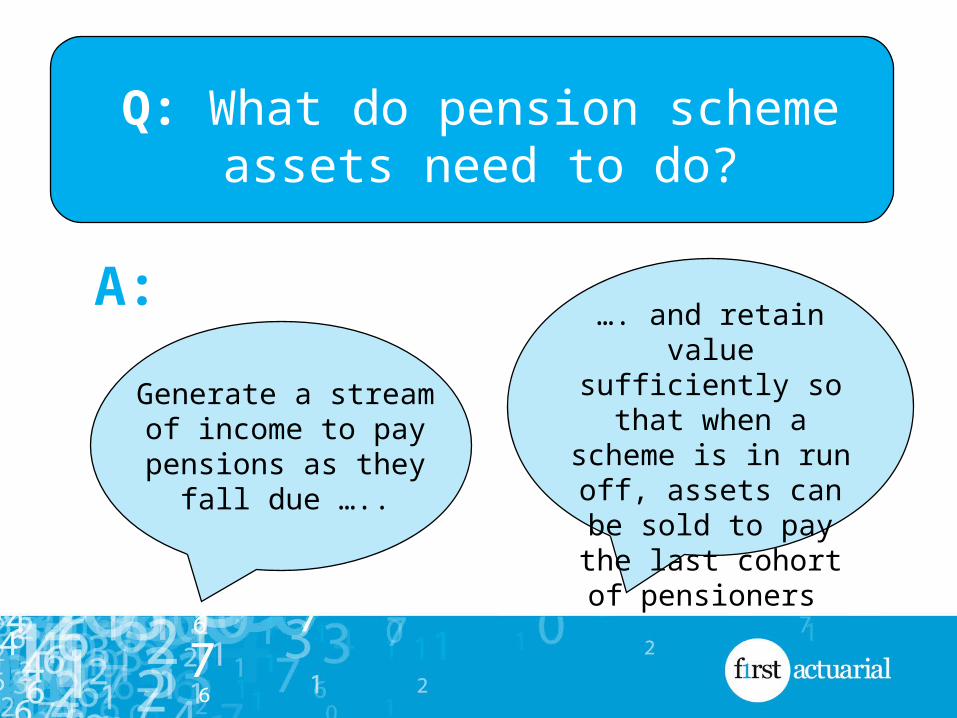

Q: What do pension scheme assets need to do?

A:

Generate a stream of income to pay

pensions as they fall due …..

…. and retain value sufficiently so that

when a scheme is in run off, assets can be

sold to pay the last cohort of pensioners

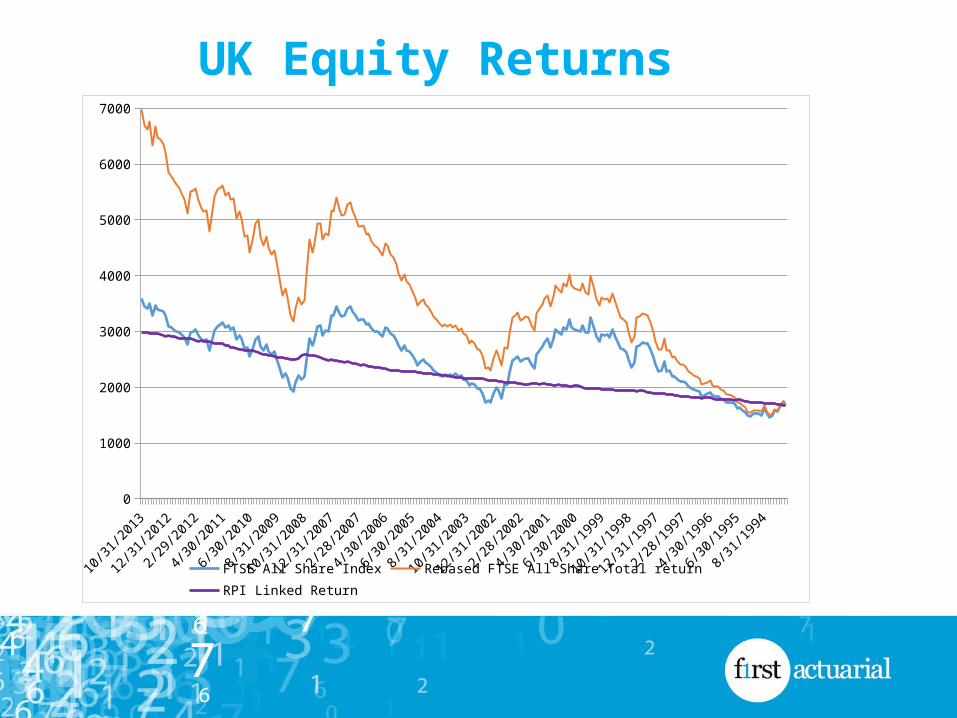

UK Equity Returns

12/1/1

993

12/1/1

994

12/1/1

995

12/1/1

996

12/1/1

997

12/1/1

998

12/1/1

999

12/1/2

000

12/1/2

001

12/1/2

002

12/1/2

003

12/1/2

004

12/1/2

005

12/1/2

006

12/1/2

007

12/1/2

008

12/1/2

009

12/1/2

010

12/1/2

011

12/1/2

0120

1000

2000

3000

4000

5000

6000

7000

FTSE All Share Index Rebased FTSE All Share Total return RPI Linked Return

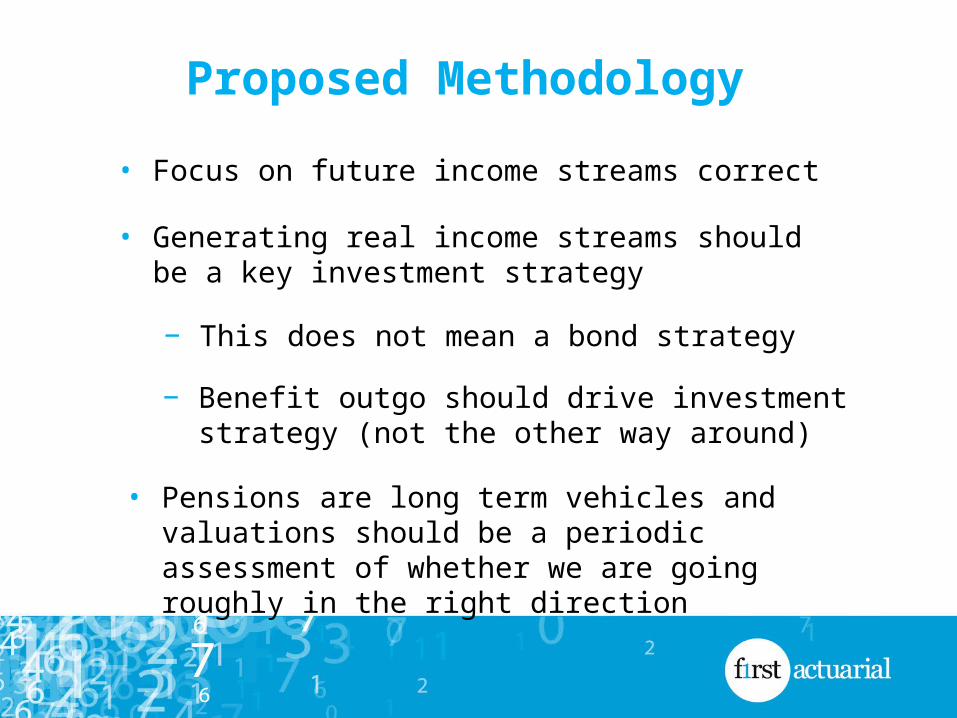

Proposed Methodology

• Focus on future income streams correct

• Generating real income streams should be a key investment strategy

− This does not mean a bond strategy

− Benefit outgo should drive investment strategy (not the other way around)

• Pensions are long term vehicles and valuations should be a periodic assessment of whether we are going roughly in the right direction

Barriers to the Proposed Methodology

• Can we play the ball from where it is?

• Valuations used for all the wrong things

− Accounting valuations

− Funding valuations

− Buy-out valuation – but PPF to cover insolvency

Schemes in Wind Down

• Schemes closed to future accrual using ‘flight plans’

• As funding position improves, move assets into bonds to ‘reduce risk’

• What is the meaning of risk for a pension scheme?

− Risk of falling funding position measured against a bond based valuation measure

− Risk of not meeting the benefits (or the benefit expectation)

• Problems with DC ‘reckless’ caution, funding for buy-out

Things to Watch For

The attitude of the Pensions RegulatorA lucky pair?

Defined ambition

Related Documents