High Level Meeting on Customs & Taxation Brussels 19 June 2001

High Level Meeting on Customs & Taxation Brussels 19 June 2001.

Dec 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

High Level Meeting on

Customs & Taxation

Brussels

19 June 2001

ANDREW WEBB

HEAD OF INTERNATIONAL TAX

HM CUSTOMS & EXCISE

VAT & CUSTOMS

WORKING TOGETHER?

1. The Argument

The Argument• Tax and Customs administrations face

many similar demands and challenges• Need for closer co-operation between

managers and officials in the two organisations or departments

• International organisations in the customs and tax areas (eg WCO and OECD) should increase mutual awareness and regularly exchange strategies and work programmes

2. The Environment

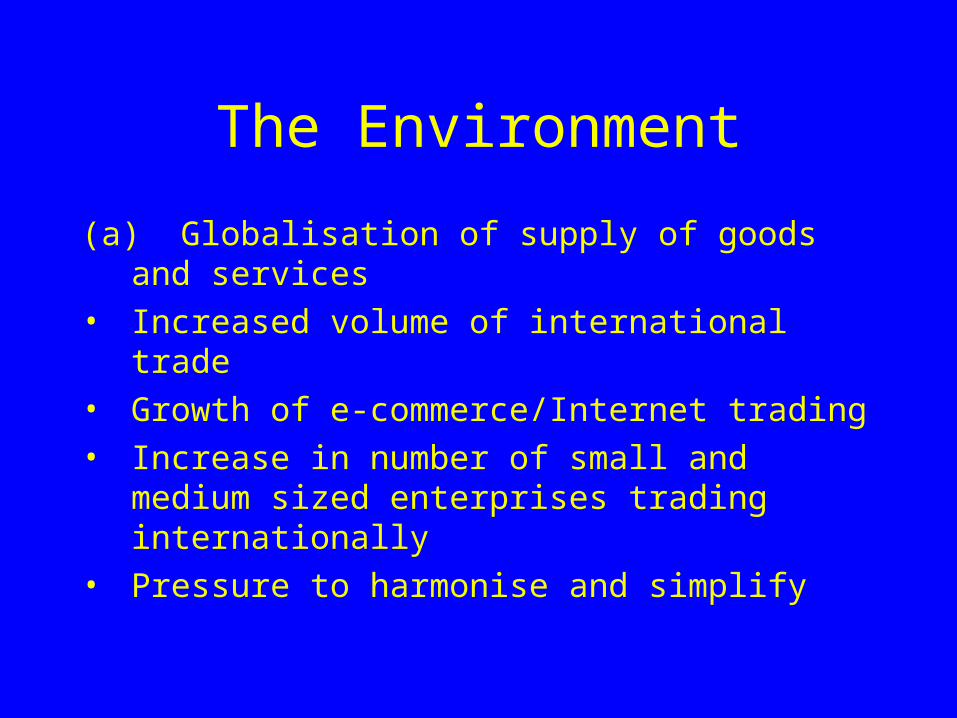

The Environment

(a) Globalisation of supply of goods and services

• Increased volume of international trade

• Growth of e-commerce/Internet trading

• Increase in number of small and medium sized enterprises trading internationally

• Pressure to harmonise and simplify

The Environment

(b) Pressure on administrations to increase revenue and reduce operating costs

• Increase in popularity of VAT• Decrease in importance of import

duties/taxes• International trade agreements/tax

frameworks to manage trade and to prevent double or no taxation

The Environment

(b) Pressure on administrations to increase revenue and reduce operating costs

• Increasing use of electronic systems for taxpayer registration, declarations and revenue accounting

• Use of risk management and audit • Simplification and harmonisation of

systems and procedures

The Environment(c ) Extent of fraud and avoidance• E-commerce/Internet trading creating new

products and methods of delivery• Increased volume, speed and complexity of

trade• Challenges to traditional concepts such as

“borders”, “goods” and “controls”• Exploitation of gaps between countries and

systems

3. The Administrative Response

The Administrative Response(a) System re-design using new technology

and commercial records• Development of integrated (ie taxes and

duties) electronic systems for taxpayer registration, declarations and accounting

• Use of customer service concepts based on single point of contact

• Contracting out and use of trusted third parties

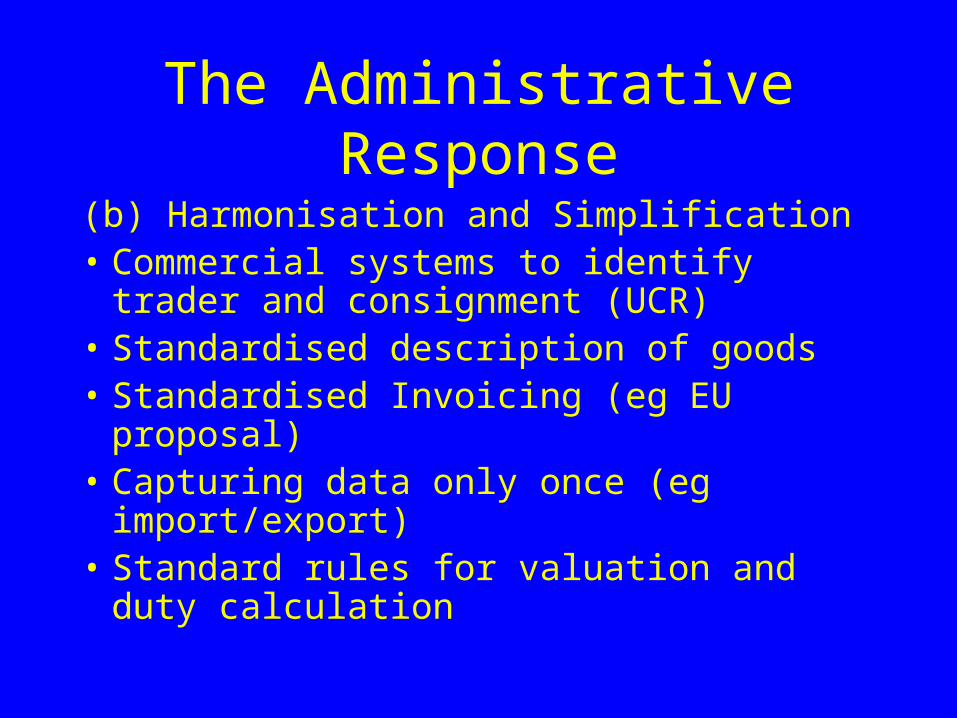

The Administrative Response

(b) Harmonisation and Simplification• Commercial systems to identify trader and

consignment (UCR)• Standardised description of goods• Standardised Invoicing (eg EU proposal)• Capturing data only once (eg import/export)• Standard rules for valuation and duty

calculation

The Administrative Response

(c ) Enhanced Administrative Co-operation• OECD International Taxation Principles (for

e-commerce)• Multi-lateral and Bi-lateral Administrative

Co-operation Agreements (Memorandum of Understanding)

• OECD Mutual Assistance Convention• Information exchange pilots(OECD WP8/9)

The Administrative Response

(d) Development of best practice guidelines

• OECD General Administrative Principles (eg Taxpayer rights and obligations; Risk Management; Compliance Measurement; Principles for managing Ethics in the Public Service)

• EU Fiscal and Customs Blueprints

4 The Case Study

Case study: Fast FreightThe Problem• Vast increase in traffic volume (Internet trading)• Goods subject to both duty and taxes• Different types of operator working to different

legislation (Post Offices/ Express Couriers)• Different administrative requirements • Widespread use of technology v manual

administrative systems

Case Study: Fast Freight

(b) The Express Courier Industry

• Over 6 million shipments per day

• Operates in 220 countries

• Employs 187,000 people

• 1200 aircraft

• Volume of fast freight increasing by 40% a year

Case Study: Fast Freight(c ) Revenue and Customs implications• Manual systems (Post Offices) require

manual risk assessment• Proportion of anti-smuggling and revenue

checks have decreased• Increase in smuggling and revenue loss• Conflict with Post Offices and Express

parcel operators over different laws and requirements (discriminatory?)

Case study: Fast Freight(d) Main Issues• Efficient and effective facilitation of

legitimate parcel trade• Proper account taken to ensure tax and duty

paid• Risk assessment of fraud and smuggling• Equity of treatment between operators• Global, integrated and automated systems

Case Study: Fast Freight

(e ) Vision for the future• Global automation/data capture (bar

coding)• Link automated system to harmonised

system for description, duty/tax calculation and lodgement of declaration

• Changes to legislation • Risk assessment by recipient and transit

countries using global system

Case Study: Fast Freight

(f) Steps to be taken• A solution requires co-operation between customs,

tax, enforcement personnel to research problem, assess revenue loss and identify viable models

• Work closely with operators to make use of their systems and records

• Continue to actively participate in projects looking at the issue (eg SAMPLE-Finland and USA)

5 The Conclusion

The Conclusion• Globalisation of trade and e-commerce has

fundamentally changed the environment• Many of the key issues and challenges faced by

customs and tax administrations are very similar• Current gaps in knowledge and administrative co-

operation arrangements are being exploited • Need for administrations to increase awareness of

each others agendas and work programmes to prevent revenue loss and to find solutions

The Conclusion• Need international organisations working in

the customs and tax areas (eg WCO, OECD) to regularly share strategic visions and objectives

• Need a joint forum (representatives with observer status) where cross cutting issues can be regularly and routinely discussed even though there may not be common solutions

Thank you

Questions?

Related Documents