Heterogeneity in Professional Service Firms Namrata Malhotra and Timothy Morris Imperial College; University of Oxford abstract Research on professional service firms emphasizes similarities in their organization and management and distinctiveness from other types of organization. In this paper we take a different tack and focus on the differences between professional service firms, that is, on heterogeneity across different professional sectors. We argue that differences between professions on a number of dimensions affect the nature of professionals’ work and, in turn, the organization and management of firms across different professional sectors. Drawing on the sociology of professions literature we focus on three key dimensions of knowledge, jurisdictional control and client relationships to compare legal, auditing and engineering consulting firms. We consider how differences in these dimensions across the three professional services sectors impact upon the way firms are organized. We offer a number of propositions explicating how differences in the nature of knowledge, jurisdictional control and client relationships have implications for organizational form, team-working and pricing systems. INTRODUCTION Inherent to the work of all professionals is a claim over some area of expert knowledge applied in work settings (Abbott, 1988; Freidson, 2001; Larson, 1977; Sharma, 1997). This general proposition has been the basis for developing generic frameworks appli- cable to the organization of professional service firms across many sectors or professions, especially distinguishing from manufacturing firms (e.g. Greenwood et al., 1990). However, in recent years differences across professions have become more apparent in terms of their evolution and responses to various external market and institutional changes. Substantial differences at the organizational level are evident, including internal structure, human resource policies and practices, and relations with contiguous occupa- tions, clients, and even pricing systems. For example, the up or out model of promotion is used widely in large law firms but is much less common in other professions such as engineering consulting and architecture (Blau, 1984; Galanter and Palay, 1991; Sherer, 1995; Sherer and Lee, 2002). Some work does draw attention to heterogeneity among different types of professional services (e.g. Covaleski et al., 2003; Morris and Empson, 1998; Reed, 1996; Suddaby and Greenwood, 2005) but the notion of similarity or Address for reprints: Namrata Malhotra, Imperial College Business School, Imperial College, London SW7 2AZ, UK ([email protected]). © Blackwell Publishing Ltd 2009. Published by Blackwell Publishing, 9600 Garsington Road, Oxford, OX4 2DQ, UK and 350 Main Street, Malden, MA 02148, USA. Journal of Management Studies 46:6 September 2009 doi: 10.1111/j.1467-6486.2009.00826.x

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Heterogeneity in Professional Service Firms

Namrata Malhotra and Timothy MorrisImperial College; University of Oxford

abstract Research on professional service firms emphasizes similarities in their organizationand management and distinctiveness from other types of organization. In this paper we takea different tack and focus on the differences between professional service firms, that is, onheterogeneity across different professional sectors. We argue that differences betweenprofessions on a number of dimensions affect the nature of professionals’ work and, in turn,the organization and management of firms across different professional sectors. Drawing onthe sociology of professions literature we focus on three key dimensions of knowledge,jurisdictional control and client relationships to compare legal, auditing and engineeringconsulting firms. We consider how differences in these dimensions across the three professionalservices sectors impact upon the way firms are organized. We offer a number of propositionsexplicating how differences in the nature of knowledge, jurisdictional control and clientrelationships have implications for organizational form, team-working and pricing systems.

INTRODUCTION

Inherent to the work of all professionals is a claim over some area of expert knowledgeapplied in work settings (Abbott, 1988; Freidson, 2001; Larson, 1977; Sharma, 1997).This general proposition has been the basis for developing generic frameworks appli-cable to the organization of professional service firms across many sectors or professions,especially distinguishing from manufacturing firms (e.g. Greenwood et al., 1990).However, in recent years differences across professions have become more apparent interms of their evolution and responses to various external market and institutionalchanges. Substantial differences at the organizational level are evident, including internalstructure, human resource policies and practices, and relations with contiguous occupa-tions, clients, and even pricing systems. For example, the up or out model of promotionis used widely in large law firms but is much less common in other professions such asengineering consulting and architecture (Blau, 1984; Galanter and Palay, 1991; Sherer,1995; Sherer and Lee, 2002). Some work does draw attention to heterogeneity amongdifferent types of professional services (e.g. Covaleski et al., 2003; Morris and Empson,1998; Reed, 1996; Suddaby and Greenwood, 2005) but the notion of similarity or

Address for reprints: Namrata Malhotra, Imperial College Business School, Imperial College, LondonSW7 2AZ, UK ([email protected]).

© Blackwell Publishing Ltd 2009. Published by Blackwell Publishing, 9600 Garsington Road, Oxford, OX4 2DQ, UKand 350 Main Street, Malden, MA 02148, USA.

Journal of Management Studies 46:6 September 2009doi: 10.1111/j.1467-6486.2009.00826.x

homogeneity predominates much of the organization studies literature on professionalservice firms. Systematic inter-profession comparisons of firms are non-existent: studiesare generally based on a single professional sector, such as accounting, law, architecture,engineering consulting or management consulting (Cooper et al., 1996; Greenwood andHinings, 1993; Greenwood et al., 1990, 2002; Lowendahl, 2005; Malhotra, 2003; Malosand Campion, 2000; Morris and Pinnington, 1998; Pinnington and Morris, 2002).

On the other hand, research grounded in the sociology of professions has consistentlydrawn attention to differences between professions. In particular, sociological researchhas explained these differences among professions in terms of the nature of knowledgethey deploy, contests occurring around rival jurisdictional claims and the nature of therelationship with other actors including the state and clients (e.g. Abbott, 1988; Collins,1979; Freidson, 1986). Abbott (1988) proposed that differences in professions’ work,relations to clients and to other professions, and the ability to adapt to developments inexpert knowledge, determined the dynamics of professional competition for attractivejurisdictional spaces. Halliday (1987) distinguished between various kinds of knowledgeto differentiate between professions. Johnson (1972) differentiated between professionsbased on their power base vis-à-vis client groups.

In this paper, we argue that differences between professions on the three dimensions,namely the nature of knowledge, jurisdictional control, and the nature of client relation-ships, affect the conduct of professional work and, in turn, the organization of firms. Wetherefore reconnect the sociology of professions literature with research in the area oforganization and management to develop a clearer and more systematic understandingof firm-level heterogeneity across professions. It is important to note that the threesociological dimensions are related but our focus is on the independent influence of eachdimension on the organization of professional firms. Although expert knowledge under-pins jurisdictional claims and the conduct of client relationships, we argue that each alsohas a direct and independent effect on heterogeneity in how firms across the professionsare organized. The nature of a profession’s knowledge base does not wholly determine allfeatures of a profession’s activities. As we argue below, successful jurisdictional controlalso results from mobilizing activities, institutional arrangements and relations with otherpowerful actors. Client relationships depend upon the nature and power of the client aswell as the knowledge base of the profession.

We compare professional services firms in three sectors – law, accounting, and engi-neering consulting – to illustrate heterogeneity in the organization of different profes-sional firms, and we develop a number of propositions based on our comparativeanalysis. Various typologies of professions suggest that they have underlying similarities,but along certain dimensions there are differences that allow sub-categories to bedefined. For example, Etzioni (1969) contrasts professions and semi-professions. Reed’s(1996) typology distinguishes between traditional, organized and entrepreneurial profes-sions. The professions we select are similar in terms of being traditionally accredited,business-based professions, with the institutional apparatus to support them, but becausethey differ in terms of knowledge bases, jurisdictional control, and client relations(Collins, 1990; Freidson, 2001) they allow us to illustrate our argument that inter-profession differences help to explain heterogeneity at the level of the firm. Our sampleis not exhaustive but it is representative of the wider population of professions in

N. Malhotra and T. Morris896

© Blackwell Publishing Ltd 2009

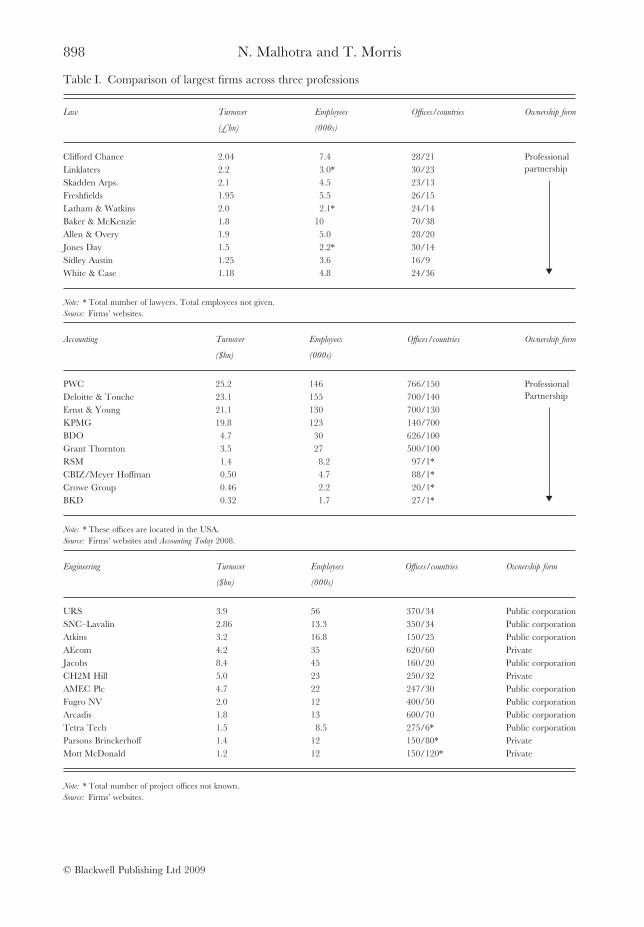

reflecting variation. Our aim is to capture how the differences translate into heteroge-neity at the firm level and our choice of professions serves this purpose. Table I illustratesthis heterogeneity between firms across the three professions. It demonstrates variation inownership, size and the number of offices across the top ten firms in each sector. Lawfirms are clearly much smaller than engineering consulting and accounting firms both interms of number of employees and the number of offices. Further, all the Top 10engineering consulting firms are corporations (public or private) while the legal andaccounting firms are partnerships.

The paper contributes to research in the management of professional service firms(PSFs) and to organization theory more generally. First, having raised questions aboutthe generalizability of sector-specific studies in PSF research, it develops a basis forexplaining heterogeneity by reference to the nature of professional work and its conse-quences for the organization of professional firms. Second, it reconnects research on thesociology of professions with studies of the management of professional firms, a connec-tion that has weakened in recent years. Third, our paper responds to Barley and Kunda’s(2001) call for research to bring work back into organization studies. These authors havedrawn attention to the way work has slipped into the background as organization theoryhas become increasingly concerned with the study of strategy, structures and environ-ments, noting that ‘significant shifts in the nature of work should coincide with significantshifts in the way organizations are structured and in how people experience work’ (2001,p. 77). Barley and Kunda (2001) emphasize that human action generates organizationalvariation. This is particularly pertinent to research on professions and professionals, aswe argue below, because it is their claims to expertise applied in work settings that haveformed the basis of their power and privilege and have been a means of limiting theinfluence of rational-bureaucratic forms of organizing (Freidson, 1986; Leicht andFennel, 2001). We argue that it is through the conduct of professional work that corecharacteristics of the professions translate into specific organizational effects at the levelof the professional firm.

We demonstrate how key dimensions characterizing the professions (macro levelfactors) influence organizational characteristics (micro level factors) through the situ-ational mechanism (Anderson et al., 2006) of the conduct of professional work.

In the next section, we briefly summarize the relevant literature on the sociology ofprofessions, and the organization of professional service firms. In the following section wecompare the work of firms in the selected professions along the three dimensions notedabove and develop propositions explicating how differences on these dimensions trans-late into different organizational implications. Finally, we offer conclusions and direc-tions for future research.

PROFESSIONS AND PROFESSIONAL ORGANIZATIONS

Sociology of Professions

Central to theories of professions is the idea that they are occupationally distinctivebecause of their control and use of what is socially constructed as expert knowledge(Abbott, 1988; Reed, 1996). Formal knowledge is institutionalized into disciplines

Heterogeneity in Professional Service Firms 897

© Blackwell Publishing Ltd 2009

Table I. Comparison of largest firms across three professions

Law Turnover

(£bn)

Employees

(000s)

Offices/countries Ownership form

Clifford Chance 2.04 7.4 28/21 ProfessionalpartnershipLinklaters 2.2 3.0* 30/23

Skadden Arps. 2.1 4.5 23/13Freshfields 1.95 5.5 26/15Latham & Watkins 2.0 2.1* 24/14Baker & McKenzie 1.8 10 70/38Allen & Overy 1.9 5.0 28/20Jones Day 1.5 2.2* 30/14Sidley Austin 1.25 3.6 16/9White & Case 1.18 4.8 24/36

Note: * Total number of lawyers. Total employees not given.Source: Firms’ websites.

Accounting Turnover

($bn)

Employees

(000s)

Offices/countries Ownership form

PWC 25.2 146 766/150 ProfessionalPartnershipDeloitte & Touche 23.1 155 700/140

Ernst & Young 21.1 130 700/130KPMG 19.8 123 140/700BDO 4.7 30 626/100Grant Thornton 3.5 27 500/100RSM 1.4 8.2 97/1*CBIZ/Meyer Hoffman 0.50 4.7 88/1*Crowe Group 0.46 2.2 20/1*BKD 0.32 1.7 27/1*

Note: * These offices are located in the USA.Source: Firms’ websites and Accounting Today 2008.

Engineering Turnover

($bn)

Employees

(000s)

Offices/countries Ownership form

URS 3.9 56 370/34 Public corporationSNC–Lavalin 2.86 13.3 350/34 Public corporationAtkins 3.2 16.8 150/25 Public corporationAEcom 4.2 35 620/60 PrivateJacobs 8.4 45 160/20 Public corporationCH2M Hill 5.0 23 250/32 PrivateAMEC Plc 4.7 22 247/30 Public corporationFugro NV 2.0 12 400/50 Public corporationArcadis 1.8 13 600/70 Public corporationTetra Tech 1.5 8.5 275/6* Public corporationParsons Brinckerhoff 1.4 12 150/80* PrivateMott McDonald 1.2 12 150/120* Private

Note: * Total number of project offices not known.Source: Firms’ websites.

N. Malhotra and T. Morris898

© Blackwell Publishing Ltd 2009

(Foucault, 1980) forming the basis on which credentials are awarded. To be the basis ofa sustainable claim to professional status, knowledge usually relates to some form of skillthat is difficult enough to require training and reliable enough to produce results (Collins,1979, p. 132). Freidson (2001) calls this discretionary intangible skill. He also states thatformal knowledge based on abstract concepts is identified with the historic professionswho have asserted a status of monopoly or control over their work. Professions codifytheir expertise but this creates its own problems because knowledge becomes susceptibleto wider understanding and critique. In order to sustain professional power, some degreeof mystique and impenetrability has to be sustained (Larson, 1977) or, as Jamous andPeloille (1970) express it, the ratio of indeterminacy to technical rules in professionalwork has to remain at a high level.

Although every profession lays exclusive claim to an area of knowledge, the extent towhich this translates into market control of a domain of work activities varies. Partly thisis because of the nature of expert knowledge itself. For example, Collins draws anunflattering contrast between the work of lawyers and doctors and that of engineers:‘Engineers and technicians work is productive labor; that of lawyers and doctors isprimarily political labor. The one produces real outcomes; the other tends to manipulateappearances and beliefs’ (1979, p. 175). Halliday (1987) has argued that differencesamong professions can be understood in terms of the epistemological bases of profes-sional knowledge. Scientific professions are concerned primarily with matter of fact (whatis the case) and normative professions are concerned primarily with matters of value(what ought to be the case) (Halliday, 1987, p. 424). He contrasts engineering as anexample of a scientific profession and law as that of a normative profession. He points tosome professions such as the military and academe that incorporate both epistemic bases,scientific and normative, assuming a syncretistic epistemological foundation (p. 426).Based on these epistemological foundations, different types of professional knowledgecan be described as technical, normative and syncretic.

Our sample of professions reflects Halliday’s typology of professions. Law draws on abody of knowledge that is based on jurisprudence and concepts of justice, property andsocial contracts (Abel, 1989; Heinz and Laumann, 1982). It is predominantly normativein nature. Engineering has a core of knowledge derived from the sciences. The knowl-edge is empirically derived from observation and experimental inquiry (Halliday, 1987).It is predominantly technical in nature. The knowledge underpinning auditing derivesfrom the underlying economics of capitalist production in seeking to identify the rate ofprofit and value of firms. Auditing has increased its reliance on procedures such asstatistical sampling that carry mathematical credentials. Power (2003) notes that there isa tendency to couch the audit process in rational technical terms to produce legitimacyand generate trust in the audit of financial accounts, but underpinning this technicaldimension is a normative dimension as financial statements are perceived as morereliable than they would be without audits. Rose and Miller (1992) identify both pro-grammatic and technical aspects of auditing practice. The programmatic aspect encom-passes the normative image of what an audit ought to be in terms of ideals and goals ofaccountability and verification while the technical aspect concerns specific proceduresand practices (Power, 2000). Extrapolating Halliday’s (1987) epistemological distinctionsto accounting, the profession can be described as syncretic, spanning both the normative

Heterogeneity in Professional Service Firms 899

© Blackwell Publishing Ltd 2009

and scientific epistemological bases. Its core knowledge is therefore an amalgam ofboth normative and technical. There is no clear understanding in the literature of howthe core knowledge base of a profession might affect the organization of professionalfirms.

Success in controlling a jurisdiction requires that the profession withstands challengesfrom other occupations and, where necessary, mobilizes to confront new problems in itsdomain of work. Continuing domination of a domain of work activities, a jurisdiction, iscentral to professional power. Larson (1977) calls this the professional mobility project.Such a project is a continuing process in which a collective actor, a profession, seeks tosecure a monopoly of a market, both by restricting supply and legitimizing statusinequality. Using a Weberian framework, Larson argues that professions must be seen asinterest groups simultaneously pursuing economic and social goals: in this pursuit pro-fessions seek social closure, or the exclusion of rivals, protection of their privileges,defence against incursions into their territory and, in some cases, attempts to usurp theterritory of other groups (Macdonald, 1985, 1995). Similarly, Abbott (1988, p. 20) usesthe concept of jurisdictions which he defines as the link between a profession and itswork. Jurisdictional power follows from the possession of expertise and control of work,but because professional legitimacy is socially constructed (Abbott, 1988; Freidson,2001), there is no simple link between the nature of a profession’s knowledge base and itsjurisdictional power.

Consistent with Weberian arguments that stress how actors have to organize to pursuetheir interests, closure or jurisdictional control cannot be seen automatically to followfrom possession of knowledge: professional status and influence is a continuing project(Halliday, 1987; Macdonald, 1995). Engineering has been unable to develop a strongjurisdiction despite being grounded in scientific knowledge that provides an adequatedegree of abstraction to sustain social closure. The engineering profession has failed togain social closure due to several historical contingencies. Freidson argues that becauseengineering was always reliant on large capital infusions, engineers became employees inorganizations rather than self-employed like auditors and other professions who had lowlevels of capital requirements. Abbott (1988, p. 165) notes that its ‘distinct professionalheritages and tasks prevent a unified cognitive and social structure’. Larson (1977) arguesthat engineering did not gain social closure for two reasons: (1) the engineering professiondid not arise out of one specialty area but ‘different specializations which separately gaverise to the present-day engineering specialty’ (p. 26); (2) engineering work is mediated bya buyer who may not be the consumer (e.g. government as the purveyor of roads andbridges that the public uses). Thus, jurisdictional control or social closure is not justincumbent upon the nature of knowledge base but historical contingencies matter.

Challenges to jurisdictions, or turf wars, occur when occupational groups can assertrights to undertake professional tasks, achieving incursions into new areas of work(Abbott, 1988). This may result from a successful challenge to another profession’smonopoly, or where there is no clearly established monopoly. Therefore, jurisdictionalcontrol will follow partly from the nature of the knowledge base of the profession and toa large extent depend upon how it exercises jurisdictional control. However, it is not clearhow such jurisdictional control strategies impact upon the ways in which firms in aprofession are organized.

N. Malhotra and T. Morris900

© Blackwell Publishing Ltd 2009

In many professional services clients participate in the processes of diagnosis, inferenceand treatment (Abbott, 1988; Fosstenlokken et al., 2003; Mills et al., 1983), but there isa difference in the extent to which the client is consulted during, or has control over, theproduction process ( Johnson, 1972). At one extreme, in the case of medicine, clients havetraditionally had relatively little influence or involvement in these processes (Freidson,1986). At the other extreme, clients have been able to influence virtually all professionalactivities, as in architecture where traditionally powerful patrons subordinated the role ofthe architect (Blau, 1984). When clients can control or influence the process of produc-tion of a professional service and, therefore, judge how to value and pay for it, thesituation is characterized by a high degree of ‘client capture’ (Leicht and Fennel, 2001).The extent to which client capture exists will partly depend on the profession’s knowl-edge base and jurisdictional control and partly on the power of clients themselves but,again, it is not clear how the role and power of clients in the production of servicesimpacts upon professional firms organizationally.

Organization of Professional Firms

Research in the organization and management of professional firms developed in par-allel, especially since the late 1980s. Generally, it has been argued that the nature of theprofessional task, characterized by a high degree of discretion in the ability to diagnoseand solve client problems, is consistent with a professional partnership form in whichthere is a minimal hierarchy, high degree of task autonomy, decentralization of author-ity, and consensus in decision making (Greenwood et al., 1990). There is a greaterreliance on the use of ‘professional’ systems of control through peer pressure. Since themid-1990s, there has been increasing discussion about the pressures on these firms tobecome more managerial and bureaucratic to meet the demands for greater efficiencygenerated by growing competition and deregulation (e.g. Cooper et al., 1996). There isan emphasis on bureaucratic methods creating elaborate hierarchies; centralization ofauthority over key areas like client activities, allocation of resources and performance;and greater specialization and formal integration mechanisms such as coordinationcommittees or partners with control over client relationships and the selection of pro-fessional and managerial tasks (Cooper et al., 1996). Professional organizations maytherefore operate with professional or bureaucratic models of organizing or seek tocombine these in the professional bureaucracy (Mintzberg, 1979). However, there hasbeen a tendency to generalize across professions this movement towards a more mana-gerial and bureaucratic organizational form.

Around the same time, the mid-1990s, we find a resurgence of interest in addressingthe professional–bureaucratic conflict (e.g. Cohen, 2002; Gunz and Gunz, 1994;Wallace, 1995) after the initial impetus in the 1960s (e.g. Hall, 1968; Montagna, 1968;Smigel, 1964). In a study examining how different structural arrangements of profes-sional and non-professional organizations relate to lawyers’ organizational and profes-sional commitment, Wallace (1995) found that in fact very few structural characteristicswere important in explaining professional commitment. Rather the study suggests thatprofessionals have adapted to the non-professional organization while maintainingautonomy over their professional work. Cohen’s (2002) work on multiple commitments

Heterogeneity in Professional Service Firms 901

© Blackwell Publishing Ltd 2009

among employees also indicates that this organizational–professional conflict is notborne out empirically (see Gunz and Gunz (2006) for a discussion of the organization-profession conflict literature). There is an inclination even in this literature to generalizeacross different professions.

Recent studies have pointed to variations in the way different professional firms areorganized (e.g. Brock et al., 1999; Malhotra et al., 2006; Suddaby and Greenwood,2005). Suddaby and Greenwood (2005) point to the emergence of the multidisciplinarypartnership form among the Big Four accounting firms. Malhotra et al. (2006) drawattention to differences in structural responses of accounting and law firms to variousenvironmental pressures. All of these studies call for a systematic analysis of why suchorganizational variations are occurring; a disconnection between the management andorganization of PSFs literature and the sociology of professions literature is conspicuous.There is no reference in the former to differences between professions discussed in thesociology of professions literature and to possible repercussions of those differences forthe organization and management of professional firms. We attempt to build thatconnection.

In summary, while comparative analysis points to the importance of understandingdifferences in the work of professionals that stem from their expertise, jurisdiction andclient relations, there is no systematic understanding of how this translates into differ-ences in the organization of professional firms. In the following sections we explore howdifferences in professional work derived from the three dimensions of the nature ofknowledge, jurisdictional control and client relations create heterogeneity in the organi-zation of firms in different professions.

NATURE OF KNOWLEDGE

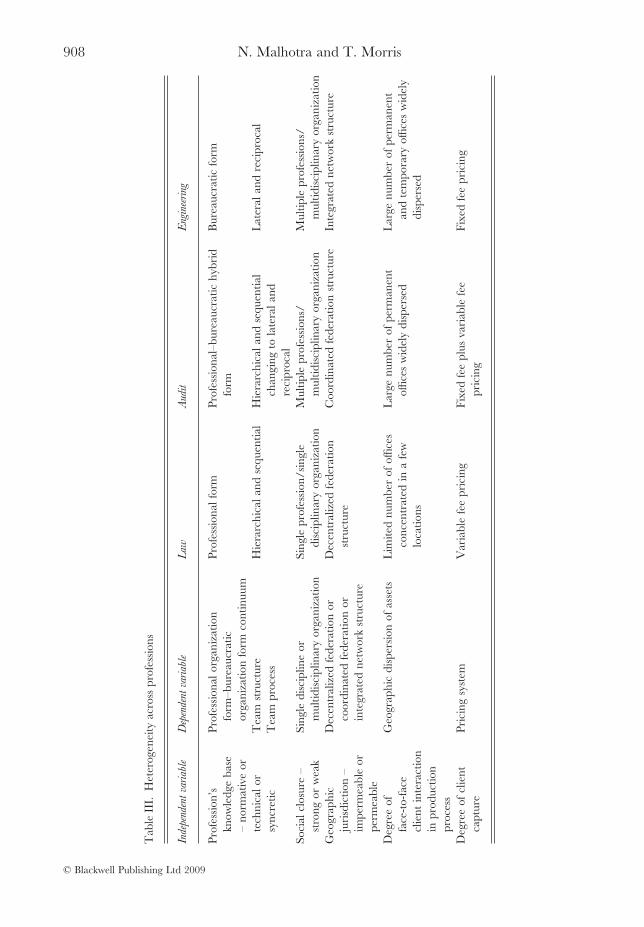

Differences in the nature of the knowledge base underpinning the three professions, interms of being normative, syncretic or technical, have implications for the actual conductof professional tasks and organization form. How does the application of knowledge inday-to-day conduct of professional work influence organization form in the three pro-fessions? By organization form we refer to professional or bureaucratic forms of orga-nizing the work of professionals. Table II summarizes the variables and measures fororganization form.

Law primarily draws on a normative knowledge base. The professional task is centredon the interpretation and application of statute or case based law which may or may notbe tested in court ( Jones, 2000). Lawyers seek to define and exploit areas of uncertaintyor similarity in relation to the case on which they are working: interpreting the extant lawand deploying arguments using appropriate forms of logic or persuasion in relation to thespecific problem-case are core tasks (Halpin, 2000; Schon, 1987). There is a high degreeof reliance on interpretation and judgment based on encoded legal knowledge (Robert-son et al., 2003). To this end, lawyers execute their tasks and manage relationships withthe clients with minimal use of formal procedural rules governing work processes; rather,there is an emphasis on professional norms and standards to guide their actions. Typi-cally, lawyers work on cases with support from juniors and paralegals and with limitedprocedural control (Hillyer, 2000). Structurally, the nature of the professional task fits

N. Malhotra and T. Morris902

© Blackwell Publishing Ltd 2009

with a professional mode of organizing with a minimal hierarchy, high degree of taskautonomy, decentralization of authority, and consensus in decision making amongpartners and senior lawyers (Cooper et al., 1996). Professional principles dominate tosupport the conduct of professional work in law firms.

As noted earlier, the knowledge base of auditing is an amalgam of the normativeaspect of what an audit ought to be in terms of ideals and goals of accountability andverification and the technical aspect encompassed in elaborate procedures and practices.In practice, a continuing challenge has been the evaluation of the outcome of an auditdecision. In the absence of independent criteria of a correct solution, there tends to be agreater emphasis on the process dimension of auditor expertise (Bedard, 1989). This iswhere the procedural criteria of performance or how work is done becomes critical(Power, 1995). The centrality of procedure has in a sense been an impetus for aproliferation of systems and methodologies underpinning the knowledge base of audit-ing. Simultaneously, clients’ expectations of the traditional audit service have changedand how the service is delivered. In particular, efficiency and consistency have become akey source of competitive advantage for accounting firms. Examples of systems includeinter-office instructions that specify the scope of audit, what is to be audited, criticalelements and timelines for major reporting (Barrett et al., 2005, p. 3). Another exampleis risk based audit technologies or methodologies introduced by the big four accountingfirms to facilitate greater efficiency of audit processes across offices, and also to developand offer other business services to audit clients (Barrett et al., 2005). Such detailedprocedural requirements call for an organization form that emphasizes bureaucraticprinciples. However, there is another aspect of the application of knowledge to an audittask: the role of auditors’ judgment.

Table II. Constructs, variables, measures

Construct Variable Measure

Organization form Professional organization form –bureaucratic organization formcontinuum

Degree of hierarchyDegree of task autonomyDegree of decentralization of authorityDegree of consensus in decision making

Nature of teamproduction

Team structureTeam process

Hierarchical–lateralSequential–reciprocal

Organizationaldiversification

Single discipline or multidisciplinaryorganization

Number of professional specializationsoutside core profession

Internationalorganizationform

Decentralized federation or coordinatedfederation or integrated networkstructure

Frequency of movement of peoplebetween offices

Frequency of joint meetingsExtent of reciprocal communication flows

between officesGeographic

dispersionof assets

Number of officesSpatial distribution of offices

Number of officesSpatial dispersion measure

Pricing system Fixed fee basis–variable fee basiscontinuum

0–100% fixed

Heterogeneity in Professional Service Firms 903

© Blackwell Publishing Ltd 2009

Although the purpose of formal systems in audit work has been to increase the degreeof systematic control it has not completely replaced the role of auditors’ judgment inaudit work. In their examination of coordinating systems such as inter-office instructions,Barrett et al. (2005) found that the application of such systems is influenced by theauditors’ judgment of the reasonableness of the client’s statements, client relationshipsdeveloped between local engagement partners and managers of the client subsidiariesand the auditor’s own knowledge of similar businesses. This confirms Power’s (1995)observation that the procedural knowledge base of auditing remains ambiguous. Theformal structure of an audit process encompassed in audit-manuals provides a looseframework for the exercise of judgment (Humphrey and Moizer, 1990) but the applica-tion of technical manuals requires some background cultural knowledge in order to knowhow and when to ‘invoke certain bodies of knowledge and invoke certain symbols ofperformance to generate public confidence in the application of technique’ (Power, 1995,p. 327). In a nutshell, techniques do not encompass all possible rules for application,but a sufficient degree of uncertainty persists in the nature of the knowledge and appliedskill, attributed to the complexity of task, to call for the use of discretionary judgment(Freidson, 2001). Structurally, this has meant organizing in a way that balances andsupports the professionals’ active role in exercising situated judgment in the audit processalong with the need for greater thoroughness and efficiency in following due process. Wepropose that this requires a hybrid of a professional mode of organizing and a morebureaucratic form characterized by medium degrees of hierarchy, task autonomy,decentralization of authority and consensus in decision making. A hybrid balancesprofessional and bureaucratic principles to suit the conduct of the audit task.

Engineering consulting draws on a knowledge base that is primarily technical to dealwith material problems (Collins, 1979). The application of such technical knowledge isamenable to greater analysability (e.g. Perrow, 1967; Withey et al., 1983) and wellunderstood formulas and processes. Engineering consulting work involves connectingdifferent pieces of engineering expertise meticulously to arrive at a technically feasiblesolution for the client (e.g. Fosstenlokken et al., 2003; Rimmer, 1988). Structurally,engineering design work is compatible with greater bureaucratic control over profes-sional activities and has been seen as an important reason why engineers have becomesalaried employees in bureaucratic settings (Collins, 1979). In addition to the technicalengineering work a critical part of the engineering consulting task is project manage-ment. Engineering consultants are all essentially project managers as well. To deliver aproject efficiently, on spec, on time, on budget, again calls for efficiencies facilitated bymore bureaucratic organizational principles (Lowendahl, 2005; Malhotra, 2003).

In sum, the profession’s knowledge base – normative, syncretic or technical – hasimplications for what organization form is appropriate. Law’s normative knowledge baseis compatible with low levels of hierarchy, high levels of task autonomy, high decentrali-zation of authority and high consensus in decision making, resulting in a predominantlyprofessional form of organization. Audit’s syncretic knowledge base results in a hybrid ofa professional form and a bureaucratic form. Engineering has a predominantly technicalknowledge base. Its application in engineering consulting firms is likely to be supportedby the highest levels of hierarchy, relatively less task autonomy, and a balance betweencentralization (firm level) and decentralization (project level), resulting in a more bureau-

N. Malhotra and T. Morris904

© Blackwell Publishing Ltd 2009

cratic form. This is supported by evidence that, unlike accounting and law, engineeringconsulting firms are largely organized as corporations rather than partnerships. The topten engineering design firms are all incorporated, either publicly or privately (Hoover’sDirectory; http://www.hoovers.com).

This leads to our first proposition:

Proposition 1a: Firms in professions with a normative knowledge base are more likely tohave a professional organization form.

Proposition 1b: Firms in professions with a syncretic knowledge base are more likely tohave a professional–bureaucratic hybrid organization form.

Proposition 1c: Firms in professions where the knowledge base is technical are morelikely to have a bureaucratic organization form.

A profession’s knowledge base also influences the nature of team production withinfirms. It is widely argued that profitability in professional firms comes from effectiveleveraging of seniors’ expertise in teams of more junior professionals (Hitt et al., 2001;Maister, 1993; Sherer, 1995) and that team production by professionals of different levelsof experience and seniority is acknowledged to be important to the organization ofprofessional work (Gilson and Mnookin, 1989). However, the literature provides noindication of how specific team structures and processes relate to specific professionaltasks or how these might facilitate or impede the application of professional knowledge.We consider how the application of knowledge in the conduct of the professional task inour three selected professions influences the nature of team production. The nature ofteam production is encapsulated by two dimensions: team structure and process.Table II summarizes the variables and measures that capture the nature of teamproduction.

In law firms, teams may comprise several lawyers from the same specialty or mayinvolve multiple specialisms. For example, an investment bank requiring legal servicesfor underwriting an initial public offering for a corporation will draw on the expertise ofcorporate finance lawyers and at certain points draw on ancillary specialists such as taxlawyers. Normative underpinnings of the knowledge base make partners, or very senior,experienced lawyers, pivotal in the task of exercising professional judgment, interpretingand developing arguments in a case. Junior lawyers do the legwork drawing up routinedocuments and research; the more complex drafting and interpretive work is takenon by senior assistants or by partners (Hillyer, 2000). Juniors take instructions from theseniors: the team structure has a clear hierarchy and definition of roles. Within theteam, the process of interaction is primarily sequential (e.g. Saavedra et al., 1993;Thompson, 1967), where work is delegated by the senior partner to juniors and checkedon completion.

The application of procedural knowledge in an auditing task is not just a cognitiveprocess ( Johnson et al., 1989). Auditing is a collective team-based activity comprisingintensive ongoing interactions within a cohesive, tightly knit engagement team in theprocess of framing an audit opinion (Pentland, 1993). While the interaction in teams has

Heterogeneity in Professional Service Firms 905

© Blackwell Publishing Ltd 2009

a rational programmatic function, there is also a ritualistic purpose; what Collins (1981)refers to as ‘interaction rituals’ form the foundation for constructing institutional trust inthe audit practice. The nature of team level interaction mirrors the syncretic knowledgebase embracing both technical and normative characteristics. Pentland (1993, p. 609)quoted auditors using a much more emotional language to describe an apparentlyrational process; for example: ‘You are not going to finish that job until the senior’scomfortable, the manager’s comfortable and the partner’s comfortable’. Within theteam, comfort is passed up the chain of command from the staff auditor to the partner(Pentland, 1993). What emerges is a team structure with a clear hierarchy and asequential process of interaction. However, recent advances in audit methodologies haveenhanced the importance of teamwork but also changed the nature of interaction withinthe team of auditors. The interaction among junior and senior auditors has become morereciprocal (e.g. Barrett et al., 2005). For example, risk based audit technologies andmethodologies have reduced the documentation including detailed review notes in theaudit process and been replaced by intensive face-to-face oral communication betweenpartners, senior auditors and junior auditors (Barrett et al., 2005; Bell et al., 1997;Winograd et al., 2000). This change has been accompanied by greater horizontal com-munication between team members of differing seniority, breaking down the verticalhierarchy embedded within a team of auditors. Thus, new audit methodologies inclineteams towards more lateral team structures and more reciprocal processes of interaction.

Engineering consulting work is mostly organized around the unique requirementsof each project (Fenton and Pettigrew, 2000; Lowendahl, 2005). In other words, thetechnical knowledge underlying engineering consulting is applied project by project. Anengineering project usually draws on diverse engineering specialties, and sometimesnon-engineering disciplines. Work in a typical project is organized in a team that weavestogether specific technical skills and experience through closely interdependent tasks(Boxall and Steeneveld, 1999; Malhotra, 2003). The process of creating an engineeringdesign involves a series of iterative and overlapping phases of articulating the require-ment, developing different conceptual solutions and then designing and detailing thepreferred solution (Hacker, 1997). Given the technical and precise nature of knowledge,any decision in a specific aspect of the design can have radical consequences for otherareas. For example, the interfaces between structural engineering, services engineeringand architectural design aspects typically require negotiation and compromise. Differentengineering and non-engineering specialists interact, communicating iteratively. Con-sequently, the team structure is lateral and the process of interaction with the teamis reciprocal (e.g. Saavedra et al., 1993; Salter and Gann, 2003; Thompson, 1967;Wageman, 1995). In a sense engineering consulting firms have a paradoxical structurethat embraces highly flexible team structures within an overall bureaucratic organizationform. Examples of paradoxical organizational structures that attempt to meet contra-dictory organizational demands are not uncommon among contemporary organizations(e.g. Gibson and Birkinshaw, 2004; Lewis, 2000). Studies have shown that the successfulimplementation of practices such as total quality management (e.g. Klein, 1994) andjust-in-time management (e.g. Eisenhardt and Westcott, 1988) simultaneously requirestructures that support employee autonomy to foster creativity and monitoring controlsto ensure efficiency standards. Similarly, engineering consulting firms require a structure

N. Malhotra and T. Morris906

© Blackwell Publishing Ltd 2009

that enhances efficiency on the one hand, to be able to deliver a project on spec and ontime, and support creativity on the other hand, to develop customized solutions forclients. Therefore, these firms have an overarching structure underpinned by bureau-cratic principles, but nested within it are project teams with flexible structures.

In sum, we argue that the knowledge bases of the three professional disciplines areapplied to daily professional tasks in different ways with implications for organizingteamwork, especially team structure and process. In law, typically, the team structure ishierarchical and the process of interaction is sequential. In auditing, the chain ofcommand dictating the process of interaction is critical for rigour in forming an auditopinion and creating an image of a hierarchical audit process. Recent innovations inaudit methodologies have had a counterbalancing influence by encouraging more hori-zontal and reciprocal processes of interaction among members of different seniority. Inengineering consulting, team structure and process are dictated more by the need tonegotiate and coordinate specialized technical expertise rather than seniority or hierar-chy. The team structure is lateral and the interaction process among project teammembers is reciprocal. This leads to our second proposition:

Proposition 2a: Firms in a profession with a normative knowledge base are more likelyto have team structures that are hierarchical and team processes that are sequential.

Proposition 2b: Firms in professions with a technical or syncretic knowledge base aremore likely to have team structures that are lateral and team processes that arereciprocal.

Table III summarizes the heterogeneity in organizational form across the three pro-fessions on account of differences in the nature of knowledge bases.

JURISDICTIONS

In this section we discuss the relationship between jurisdictions of work and organiza-tional form. We highlight two aspects of jurisdictional control that, we argue, impactupon the organization of professional firms. First, we refer to jurisdictions as control overareas of work within the broad division of labour establishing a degree of social closure,as the term is used by Abbott (1988). Second, we discuss jurisdictional control in termsof the spatial boundary of control by particular professions, or geographic jurisdictions.For example, divisions between nation states (or, occasionally, agglomerations of statessuch as the European Union, where a single set of rules governing the rights andresponsibilities of occupational groups is enforced) form a spatial boundary for control byparticular professions.

Jurisdictions and Social Closure

Professions are in competition for jurisdictional spaces within a system of work(Abbott, 1988). They seek to occupy areas that are materially attractive and offer statusbenefits as well as to repel incursions from other groups. This has been described as a

Heterogeneity in Professional Service Firms 907

© Blackwell Publishing Ltd 2009

Tab

leII

I.H

eter

ogen

eity

acro

sspr

ofes

sion

s

Inde

pend

ent

vari

able

Dep

ende

ntva

riab

leL

awA

udit

Eng

inee

ring

Prof

essi

on’s

know

ledg

eba

se–

norm

ativ

eor

tech

nica

lor

sync

retic

Prof

essi

onal

orga

niza

tion

form

–bur

eauc

ratic

orga

niza

tion

form

cont

inuu

m

Prof

essi

onal

form

Prof

essi

onal

–bur

eauc

ratic

hybr

idfo

rmB

urea

ucra

ticfo

rm

Tea

mst

ruct

ure

Tea

mpr

oces

sH

iera

rchi

cala

ndse

quen

tial

Hie

rarc

hica

land

sequ

entia

lch

angi

ngto

late

rala

ndre

cipr

ocal

Lat

eral

and

reci

proc

al

Soci

alcl

osur

e–

stro

ngor

wea

kSi

ngle

disc

iplin

eor

mul

tidis

cipl

inar

yor

gani

zatio

nSi

ngle

prof

essi

on/s

ingl

edi

scip

linar

yor

gani

zatio

nM

ultip

lepr

ofes

sion

s/m

ultid

isci

plin

ary

orga

niza

tion

Mul

tiple

prof

essi

ons/

mul

tidis

cipl

inar

yor

gani

zatio

nG

eogr

aphi

cju

risd

ictio

n–

impe

rmea

ble

orpe

rmea

ble

Dec

entr

aliz

edfe

dera

tion

orco

ordi

nate

dfe

dera

tion

orin

tegr

ated

netw

ork

stru

ctur

e

Dec

entr

aliz

edfe

dera

tion

stru

ctur

eC

oord

inat

edfe

dera

tion

stru

ctur

eIn

tegr

ated

netw

ork

stru

ctur

e

Deg

ree

offa

ce-t

o-fa

cecl

ient

inte

ract

ion

inpr

oduc

tion

proc

ess

Geo

grap

hic

disp

ersi

onof

asse

tsL

imite

dnu

mbe

rof

offic

esco

ncen

trat

edin

afe

wlo

catio

ns

Lar

genu

mbe

rof

perm

anen

tof

fices

wid

ely

disp

erse

dL

arge

num

ber

ofpe

rman

ent

and

tem

pora

ryof

fices

wid

ely

disp

erse

d

Deg

ree

ofcl

ient

capt

ure

Pric

ing

syst

emV

aria

ble

fee

pric

ing

Fixe

dfe

epl

usva

riab

lefe

epr

icin

gFi

xed

fee

pric

ing

N. Malhotra and T. Morris908

© Blackwell Publishing Ltd 2009

process of establishing social closure (Macdonald, 1995). Where professions seek toachieve social closure, the aim is to consolidate their boundaries; to exclude othergroups from an existing area of work in order to secure the economic and statusbenefits that flow from monopoly control. Those professions that aim for completesocial closure are disinclined to try and colonize new or different areas of expertisecontrolled by other occupations. Those professions that aim to expand beyond thecore or existing jurisdiction into areas controlled by other professions or areas that aresubject to contested control between several occupations have low social closure. Thesedifferent degrees of social closure have implications for the organization of professionalfirms. Specifically, the degree of social closure influences the extent of organizationaldiversification of a professional firm that is reflected in the number of professionalspecializations it encompasses outside the core profession. It may be a single or mul-tidisciplinary organization. Table II summarizes the variables and measures thatcapture the extent of organizational diversification.

The legal profession has many specialties but it has generally maintained high socialclosure. Its normative authority concerning rights and justice has sustained its internalsolidarity and its ability to defend its jurisdictional boundaries (Abel, 1989). In maintaininga unified jurisdiction lawyers have strictly policed the role of other occupations in legalwork to limit incursions into their jurisdiction. Where they do collaborate with otheroccupations this is likely to be on their own terms, ensuring that these other occupationsare in subordinate roles performing work that supports the lawyer. Routine documenta-tion tasks on cases or control of certain types of lower status legal areas are examples ofwork undertaken by paralegal occupations (e.g. Suddaby and Greenwood, 2001). Lawfirms may have multiple practices but these are within the jurisdiction of a single professionand do not extend into areas of work which lie outside the boundaries of the profession.Structurally, these firms are organized around a single professional specialization.

Auditing has a lower level of social closure than law. It has aimed to expand intonumerous new areas mainly on the basis of the methodology underlying audit tasks.Audit’s expansionary approach has two dimensions. The first is into contiguous non-audit areas by claims that audit’s knowledge base is sufficiently relevant to legitimize awider range of activities, such as consulting. In pursuing this, audit professionals havetransferred into these areas to work alongside non-auditors on problems that strictly lieoutside of their professional domain. The second is into areas where the audit method-ology is applied. Examples of this include efficiency audits in the public sector, environ-mental audits, energy audits, and medical audits (Pentland, 2000). The profession hasmade efforts to highlight similarities in the work involved in these different areas tounderpin its claims to expertise in these new domains (Power, 1997). These efforts havebeen initiated by the largest accounting firms rather than by the profession’s institutions,but these firms co-opted their associations to legitimize this expansion (Suddaby andGreenwood, 2005). The argument is that the profession is best placed to deploy itsknowledge to resolve client problems in the novel domain of activity which may well lieoutside the boundaries of the core profession. An expansionary jurisdictional approachreduces the degree of social closure legitimating the presence of multidisciplinary pro-fessional specializations in accounting firms. Structurally, these firms therefore combineinto multidisciplinary organizational forms.

Heterogeneity in Professional Service Firms 909

© Blackwell Publishing Ltd 2009

As noted earlier, several historical contingencies have made it difficult for engineersto maintain exclusive jurisdiction over their profession, resulting in a very low degreeof social closure. The fact that the engineering specialization has arisen out of severalsub-specialties has limited the profession’s ability to establish unified professionalcontrol of a well defined jurisdiction (Abbott, 1988; Larson, 1977). Fragmentation ofthe profession limits the scope for solidarity. As a consequence, engineers work withindivisions of labour that are frequently organized by managers and owners rather thanby engineers themselves (Leicht and Fennel, 2001). In the Anglo-American context,engineering has also been unable or unwilling to co-opt support from the state forjurisdictional exclusivity. In a nutshell, engineering has a jurisdiction that is internallyfragmented and boundaries that are so open and permeable that the profession has notbeen able to sustain deliberate jurisdictional control. Engineering firms have pursuedopportunistic expansion into related areas such as risk management and health andsafety consulting that also lie outside the boundaries of the engineering profession. OveArup, one of the Top 20 engineering design firms, for example, describes itself as aglobal design and business consulting firm. Structurally, engineering firms haveassumed multidisciplinary organizational forms. Unlike audit, engineering firms havenot co-opted the professional associations to support expansion. We summarize thesedifferences in jurisdictional control and their implications for organizational diversifi-cation as follows:

Proposition 3a: The stronger the social closure of a profession, the more likely that firmswithin the profession will limit the range of specializations to the core professionresisting diversification into multidisciplinary organizations.

Proposition 3b: The weaker the social closure of a profession, the more likely that firmswithin the profession will expand the range of specializations beyond the core profes-sion diversifying into multidisciplinary organizations.

Geographic Jurisdictions

Jurisdiction of work as a spatial boundary of control has different implications fororganizational form in different professions. It is important to note that the notion ofgeographic jurisdictions is intertwined with the nature of the knowledge base of aprofession. Some professions are subject to spatial limits on their knowledge base that inturn create jurisdictional barriers. Others possess forms of knowledge that are more orless universal, usually based on scientific laws. In practice, local variations in custom,practice or regulation are likely to present some degree of limitation on spatial expansionto any profession, but these limitations may not be prohibitive. In Halliday’s terms, anormative knowledge base is likely to geographically bind a profession while technicalknowledge is more universal (Halliday, 1987). Syncretic knowledge will incur somelimitation. Variations in the spatial limits to the application of a profession’s knowledgeinfluence how the professional firm is organized globally. Table II summarizes themeasures that capture the international organization form of the professional serviceorganization.

N. Malhotra and T. Morris910

© Blackwell Publishing Ltd 2009

Lawyers are primarily educated, regulated and controlled by national associations(Morgan and Quack, 2006). Different national jurisdictions reflect different statutoryframeworks so that a lawyer is conventionally expert in the law of one country orjurisdiction. More broadly, there are systemic differences between common and civil lawcodes that limit the transferability of lawyers’ expertise. Anglo-American codes are basedon common law and rely heavily on case based precedents determined by courts whichare then made publicly available. Civil codes are based on a set of fundamental principlesthat are constitutionally enshrined. Thus, geographic jurisdictional barriers generallyreflect substantive differences in legal codes, creating impermeable jurisdictional bound-aries. There are instances where lawyers may have the requisite knowledge to transact indifferent national jurisdictions but are barred from practice unless formally qualified. Inother words, geographic jurisdictional controls trump knowledge. For example, onlylawyers qualified in India can practice in that country and foreign firms are barred fromoperating in that jurisdiction.

Jurisdictional barriers emanating from nationally bounded legal systems have organi-zational implications, requiring firms to organize globally in ways that allow them toadjust to different national systems but also deliver a trans-national service effectively. Amajority of law firms operating globally maintain their autonomy in their nationaljurisdictions but become a part of a network of relationships with firms in other juris-dictions. These loose networks could range from international referral networks to ‘bestfriend’ networks among law firms in which there is some co-investment in infrastructureand methods of service delivery (Morgan and Quack, 2006). In this model, which isbroadly consistent with the decentralized federation outlined by Bartlett et al. (2004),knowledge of the client and documentation to facilitate transactions (for example, termsheets) are developed and retained in national partnerships. In a study of large US lawfirms, Morgan and Quack (2006) found what they described as an exporting global firmmodel. In this model, the firm’s overseas offices primarily support its home-based clientsthrough the application of its home-based system of law in another jurisdiction (Morganand Quack, 2006).

The auditing profession does not experience the same geographic jurisdictional con-straints as law. Furthermore, standardized professional knowledge, in the form of Gen-erally Accepted Accounting Principles, has made audit practices transferable acrossborders albeit with adaptations to specific country contexts. Greater permeability ofgeographic boundaries was certainly conducive to the rapid global expansion of the BigEight accounting firms in the late 1980s and into the 1990s. Suddaby et al. (2006, p. 8)observe that the Big Eight became even more ‘international’ than the corporations theyaudited. They also point out that by 1999 more than 65 per cent of the Big Five’s totalrevenue came from non-US countries. The scale of global expansion of the Big Eight(Five) is telling in the rapidly increasing number of offices and partners worldwide.Between 1982 and 1995 there was a 66 per cent increase in the number of offices KPMGhad worldwide and a 25 per cent increase in its number of partners worldwide (CIFAR,1995). Similar trends were observed among the other elite firms. Highly permeablegeographic boundaries permit a global structure in which national offices can collaborateclosely to deliver services to global clients seeking standardized methodologies andquality. Empirical work on the organization of the Big Five accounting firms suggests

Heterogeneity in Professional Service Firms 911

© Blackwell Publishing Ltd 2009

that these partnerships establish global coordination across semi-autonomous memberfirms to be able to offer consistent quality services across multiple locations (Greenwoodet al., 1999; Rose and Hinings, 1999). What emerges is a structure that is similar to thecoordinated federation model (Bartlett et al., 2004).

Engineering consulting involves the application of universal engineering principlesthat are standard across jurisdictions or country contexts. Customization is required tothe extent that it is necessary to adapt to specific host country government regulationsand to different social and physical environments of the country (Gann and Salter, 2000;Malhotra, 2003). Although, engineers may need a licence to practise in a specific state orprovince to ensure knowledge of local building codes and regulations, this has not led tothe creation of impermeable national jurisdictions in engineering, which has had impor-tant implications for the global structure of engineering consulting firms. Permeablejurisdictional boundaries have allowed these firms to have widely dispersed project andsubsidiary offices globally. The project-based nature of work of engineering firmsrequires a high degree of interdependence and cooperation among offices (Fenton andPettigrew, 2000). Over time, as projects have become bigger and more complex, theyrequire multifarious interfaces and draw on multiple diversely skilled parties acrossoffices. Permeable boundaries permit such integration and coordination across multiplelocations by supporting an unrestricted flow of people, ideas and information. Structur-ally, what emerges is an integrated network form (Fenton and Pettigrew, 2000; Joneset al., 1997).

Proposition 4a: Firms in professions with impermeable national jurisdictional bound-aries are more likely to internationalize by adopting a decentralized federationstructure.

Proposition 4b: Firms in professions with more permeable jurisdictional boundaries aremore likely to internationalize by adopting a coordinated federation or an integratednetwork structure.

Table IV summarizes the heterogeneity in organizational form across the three pro-fessions on account of differences in jurisdictional control manifested in different degreesof social closure and different degrees of permeability in geographic jurisdictions.

Relations with Clients

A distinctive feature of professional service firms is that their products are customizedsolutions that take the form of intangible applications of complex knowledge in which theclient participates to some extent in the production process (Broschak, 2004; Mills et al.,1983; Morris and Empson, 1998). Clients participate with the professional in the pro-cesses of diagnosis, inference and treatment (Abbott, 1988; Fosstenlokken et al., 2003).There are two aspects of client participation in the process of production of service. Oneis the frequency of face-to-face interaction between the client and service provider. Thesecond is the extent to which the client has control over or can influence the productionprocess ( Johnson, 1972). The latter is called client capture. The nature of interaction in

N. Malhotra and T. Morris912

© Blackwell Publishing Ltd 2009

Tab

leIV

.Su

mm

ary

ofpr

opos

ition

s

Dim

ensi

on

(ind

epen

dent

)

Var

iabl

e(i

ndep

ende

nt)

Var

iabl

e(d

epen

dent

)P

ropo

sition

Know

ledge

•N

orm

ativ

e,te

chnic

al,sy

ncr

etic

•Pro

fessio

nal

org

aniz

atio

n

form

–bure

aucr

atic

org

aniz

atio

nfo

rm

•T

eam

stru

cture

(hie

rarc

hic

alorla

tera

l)

•T

eam

pro

cess

(seq

uen

tial

orre

cipro

cal)

P1a:

Firm

sin

pro

fessio

nsw

ith

anorm

ativ

ekn

ow

ledge

bas

ear

em

ore

likel

yto

hav

e

apro

fessio

nal

org

aniz

atio

nfo

rm.

P1b:

Firm

sin

pro

fessio

nsw

ith

asy

ncr

etic

know

ledge

bas

ear

em

ore

likel

yto

hav

ea

pro

fessio

nal

–bure

aucr

atic

hyb

rid

org

aniz

atio

nfo

rm.

P1c:

Firm

sin

pro

fessio

nsw

her

eth

ekn

ow

ledge

bas

eis

tech

nic

alar

em

ore

likel

yto

hav

ea

bure

aucr

atic

org

aniz

atio

nfo

rm.

P2a:

Firm

sin

apro

fessio

nw

ith

anorm

ativ

ekn

ow

ledge

bas

ear

em

ore

likel

yto

hav

e

team

stru

cture

sth

atar

ehie

rarc

hic

alan

dte

ampro

cesses

that

are

sequen

tial

.

P2b:

Firm

sin

pro

fessio

nsw

ith

ate

chnic

alorsy

ncr

etic

know

ledge

bas

ear

em

ore

likel

yto

hav

ete

amstru

cture

sth

atar

ela

tera

lan

dte

ampro

cesses

that

are

reci

pro

cal.

Jurisd

ictional

control

Soci

alcl

osu

re

•Strong

orw

eak

Geo

grap

hic

jurisd

ictional

boundar

ies

•Im

per

mea

ble

orper

mea

ble

•Sin

gle

orm

ultid

isci

plin

ary

org

aniz

atio

n

•D

ecen

tral

ized

feder

atio

norce

ntral

ized

feder

atio

norin

tegr

ated

net

work

stru

cture

P3a:

The

stro

nge

rth

eso

cial

closu

reofa

pro

fessio

nth

em

ore

likel

yth

atfirm

sw

ithin

the

pro

fessio

nw

illlim

itth

era

nge

ofsp

ecia

lizat

ionsto

the

core

pro

fessio

nre

sistin

g

div

ersifica

tion

into

multid

isci

plin

ary

org

aniz

atio

ns.

P3b:

The

wea

kerth

eso

cial

closu

reofa

pro

fessio

nth

em

ore

likel

yth

atfirm

sw

ithin

the

pro

fessio

nw

illex

pan

dth

era

nge

ofsp

ecia

lizat

ionsbey

ond

the

core

pro

fessio

n

div

ersify

ing

into

multid

isci

plin

ary

org

aniz

atio

ns.

P4a:

Firm

sin

pro

fessio

nsw

ith

imper

mea

ble

nat

ional

jurisd

ictional

boundar

iesar

e

more

likel

yto

inte

rnat

ional

ize

by

adopting

adec

entral

ized

feder

atio

nstru

cture

.

P4b:

Firm

sin

pro

fessio

nsw

ith

more

per

mea

ble

jurisd

ictional

boundar

iesar

em

ore

likel

yto

inte

rnat

ional

ize

by

adopting

aco

ord

inat

edfe

der

atio

noran

inte

grat

ed

net

work

stru

cture

.gl

obal

net

work

stru

cture

.

Clie

ntre

lations

•D

egre

eoffa

ce-to-fac

ecl

ient

inte

ract

ion

inpro

duct

ion

pro

cess

•D

egre

eofcl

ientca

ptu

re

•G

eogr

aphic

disper

sion

ofas

sets

(num

ber

and

spat

ialdistrib

ution

of

offi

ces)

•Fix

edfe

eprici

ng

orva

riab

leprici

ng

P5a:

Firm

sin

pro

fessio

nsw

her

eth

ere

isa

hig

hdeg

ree

offa

ce-to-fac

ecl

ient

inte

ract

ion

inth

epro

duct

ion

pro

cess

are

more

likel

yto

hav

ea

larg

enum

ber

of

wid

ely

disper

sed

per

man

entan

dte

mpora

ryoffi

ces.

P5b:

Firm

sin

pro

fessio

nsw

her

eth

ere

isa

low

deg

ree

offa

ce-to-fac

ecl

ient

inte

ract

ion

inth

epro

duct

ion

pro

cess

are

more

likel

yto

hav

ea

smal

lnum

ber

of

offi

cesco

nce

ntrat

edin

afe

wlo

cations.

P6a:

Firm

sin

pro

fessio

nsw

her

eth

ere

isa

hig

hdeg

ree

ofcl

ientca

ptu

rear

em

ore

likel

yex

ante

tohav

efixe

dfe

eprici

ng

impose

dby

thei

rcl

ients.

P6b:

Firm

sin

pro

fessio

nsw

ith

alo

wdeg

ree

ofcl

ientca

ptu

rear

em

ore

likel

yto

hav

e

ava

riab

leprici

ng

system

bas

edon

the

inputofpro

fessio

nal

s’tim

e.

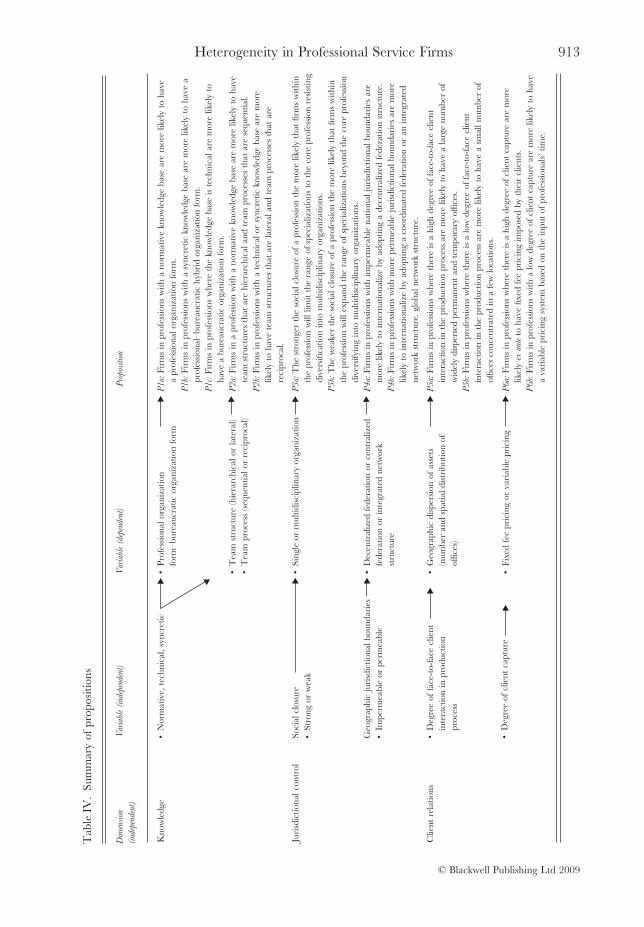

Heterogeneity in Professional Service Firms 913

© Blackwell Publishing Ltd 2009

the production process has implications for the geographic dispersion of assets of theprofessional firm. The degree of client capture, we argue, has ramifications for thepricing system in the professional firm.

The extent to which the client interacts face-to-face with the service provider has adirect impact on the geographic dispersion of assets indicated by the number and spatialdistribution of offices of the professional firm. There is variation across the three profes-sions in the nature of interaction with the client in the process of completing a profes-sional task. In law, face-to-face interaction between the client and the lawyers is relativelylimited. As providers of advice and solutions to clients facing legal risks, lawyers’ tech-nical skills are based on the ability to absorb and make sense of large amounts of writtendocumentation, to draft with great attention to detail and legal precision, and to assessthe logic and implications of legal propositions and develop arguments (e.g. Halpin,2000). Thus, lawyers are largely desk bound and need to engage in face-to-face interac-tion with the client relatively infrequently. Lawyers can perform their tasks spatiallyseparated from the client. This partly explains why, typically, law firms have a limitednumber of offices concentrated in a few locations.

In the case of auditing, technically, audit and tax work are to do with compliance toexternally defined rules, thus minimizing the role of the client in the delivery of thatservice even though the process of conducting an audit task occurs on the client’spremises. Audit rituals have to be validly performed and only professionals of the auditfirm can be trusted (Gambling, 1987). Over time, however, collaboration and interactionwith the client has become important in delivering audit services. This change has partlycome about as the domain of accounting expanded to include non-audit services thatrequired greater interaction with the client, but this permeated into the audit side of thebusiness as well. In a field study of an audit, Barrett et al. (2005, p. 17) observed thatyoung auditors were encouraged to keep a learning journal to document ideas aboutimprovements that could be made to the way the audit was carried out; these improve-ments were in turn proposed to clients as potential business advisory services. Auditingfirms balance the need to maintain a distance from the client while being on the premisesin the course of an audit task and the need to interact with the client outside of the audittask. The frequency of face-to-face interaction is likely to be higher in the conduct of theirprofessional work compared to lawyers. Structurally, this implies that they need to belocated near the client’s office which is reflected in the large number of offices that theaccounting firms have both domestically and globally. The ratio of number of offices tothe number countries is five times, on average, in the largest accounting firms comparedto it being less than twice in the case of the largest law firms as Table I indicates.Accounting firms generally have a widely dispersed network of permanent offices atclient locations along with regional offices and headquarters.

The process of applying engineering knowledge through a consulting project involvesseveral phases including bidding, conceptual design, detailed engineering, and supervi-sion and management of construction. A firm may be involved in either all phases of aproject or only the design phase; this has implications for the extent to which face-to-faceinteraction is required with the client. Design and detailed engineering work can be doneat the head office or another subsidiary design office depending on the needs of a specificproject. However, supervision and management of construction require that the engi-

N. Malhotra and T. Morris914

© Blackwell Publishing Ltd 2009

neers be on the project site. Most importantly, clients often demand that the engineeringconsultants be present in close proximity. Overall, engineering consulting firms requirehigher levels of interaction with clients relative to audit and law firms. The diversetechnical expertise, spatially dispersed distribution of projects, and the need for client–consultant interaction in specific phases of a project increase the likelihood of an engi-neering consulting firm setting up a network of project based and regional offices (e.g.Fenton and Pettigrew, 2000). Consequently, engineering consulting firms have an elabo-rate network of offices like audit firms but with one difference. The structure of an auditfirm comprises permanent offices at client locations along with regional offices andheadquarters. On the other hand, an engineering firm typically has permanent officesand many temporary project offices. The ratio of total number of offices to countries isnearly ten times at any given time for engineering consulting firms (Table I). As a result,the structure of an engineering firm is relatively more dynamic because it shifts andchanges as new projects emerge and others are completed. The more permanent natureof offices in audit firms is attributable to a large extent to the repetitive nature of the audittask. In sum, at any given employment scale, law firms will operate out of a smallernumber of offices compared to accounting and engineering. Table II summarizes vari-ables and measures that capture the geographic dispersion of assets.

Proposition 5a: Firms in professions where there is a high degree of face-to-face inter-action with the client in the production process are more likely to have a large numberof widely dispersed permanent and temporary offices.

Proposition 5b: Firms in professions where there is low degree of face-to-face interactionwith the client in the production process are more likely to have a small number ofoffices concentrated in a few locations.

The second aspect of relations with clients that is critical to the conduct of professionalwork is the degree of client capture. It is generally argued that the expert knowledge ofthe professional creates a dependency relationship with the consumer or client (Green-wood et al., 2005; Starbuck, 1992). However, an inversion of this argument in thesociological literature is that powerful clients can control professions ( Johnson, 1972).This has been called client capture and refers to the degree to which clients can controlor influence the process of production of a professional service, including its costs, timingand delivery (Leicht and Fennel, 2001). Client capture is most likely to occur where theprofessional works for large corporate clients or important brokers in a network and iseither dependent on maintaining good relations to secure further work or finds that theresource expertise of the client matches that of the professional adviser.