Hedge Fund Activism, Corporate Governance and Firm Performance [Brav, A. / Jiang, W. / Partnoy, F. / Thomas, R. (2008) (Journal of Finance)] Paper Presentation FIN803 – Corporate Finance Christian Schmidt Mannheim, March 18 th , 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Hedge Fund Activism, Corporate Governance and Firm Performance

[Brav, A. / Jiang, W. / Partnoy, F. / Thomas, R. (2008) (Journal of Finance)]

Paper Presentation

FIN803 – Corporate Finance

Christian Schmidt

Mannheim, March 18th, 2016

Mannheim, March 18th, 2016 FIN803 Corporate Finance

MotivationLack of understanding of Hedge Fund Activism

2

MOTIVATION

• Hedge Fund Activism is widely discussed and fundamentally important but remains

poorly understood

• Most commentary is based on supposition or anecdotal evidence

• Hedge Funds are accused of destroying shareholder value (distracting managers;

short-term focus)

• Lack of large-sample evidence and existing samples are plagued with biases (Ref.)

Even the most basic questions about hedge fund activism remain unanswered

Mannheim, March 18th, 2016 FIN803 Corporate Finance

ContributionFive main research questions – Presentation-focus on impact on Shareholder Value

3

MAIN RESEARCH QUESTIONS

Q1) Which firms do activists target?

Q2) How does the market react to the announcement of activism?

Q3) Do activists succeed in implementing their objectives?

Q4) Are activists short term in their focus?

Q5) How does activism impact firm performance?

Mannheim, March 18th, 2016 FIN803 Corporate Finance

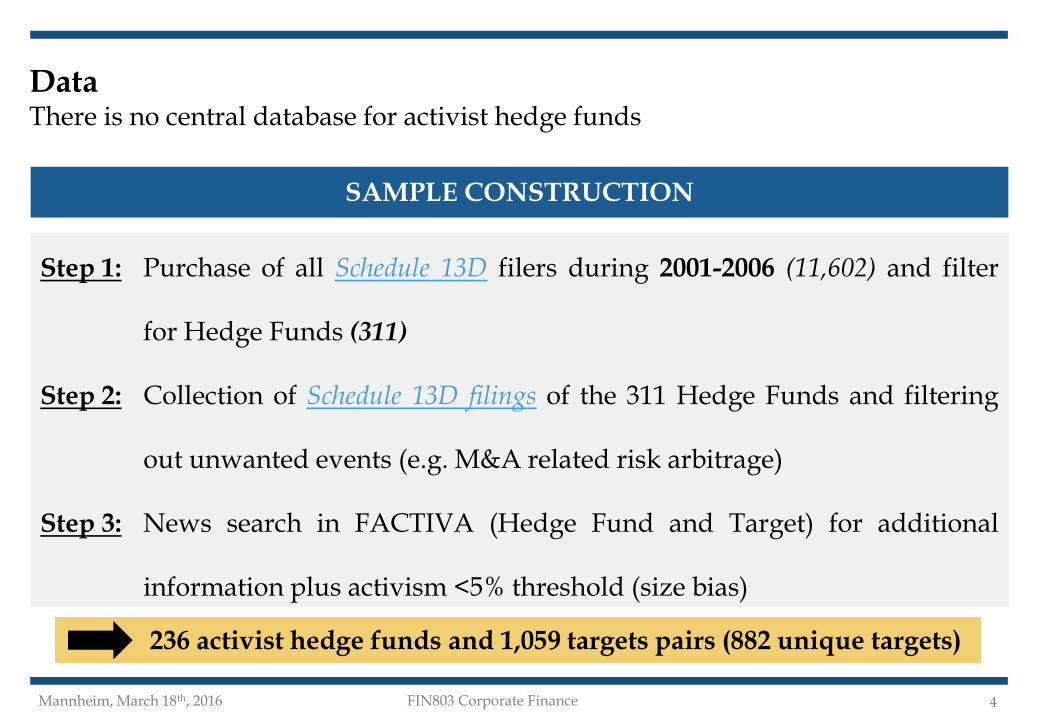

DataThere is no central database for activist hedge funds

4

SAMPLE CONSTRUCTION

Step 1: Purchase of all Schedule 13D filers during 2001-2006 (11,602) and filter

for Hedge Funds (311)

Step 2: Collection of Schedule 13D filings of the 311 Hedge Funds and filtering

out unwanted events (e.g. M&A related risk arbitrage)

Step 3: News search in FACTIVA (Hedge Fund and Target) for additional

information plus activism <5% threshold (size bias)

236 activist hedge funds and 1,059 targets pairs (882 unique targets)

Mannheim, March 18th, 2016 FIN803 Corporate Finance

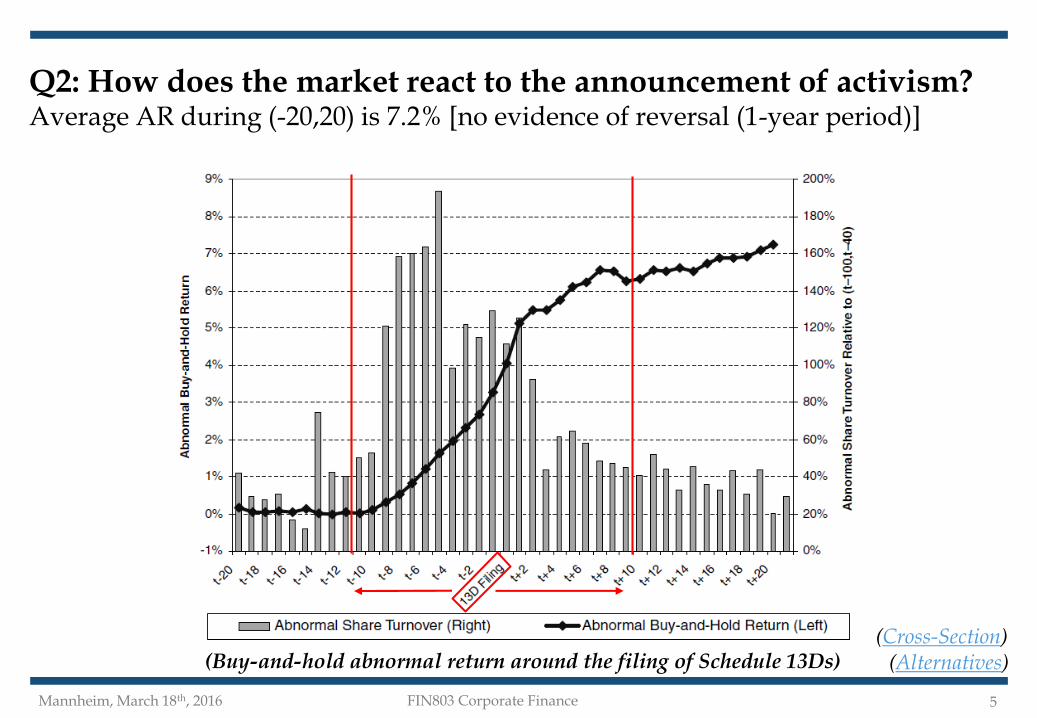

Q2: How does the market react to the announcement of activism?Average AR during (-20,20) is 7.2% [no evidence of reversal (1-year period)]

5

(Buy-and-hold abnormal return around the filing of Schedule 13Ds)(Cross-Section)

(Alternatives)

Mannheim, March 18th, 2016 FIN803 Corporate Finance

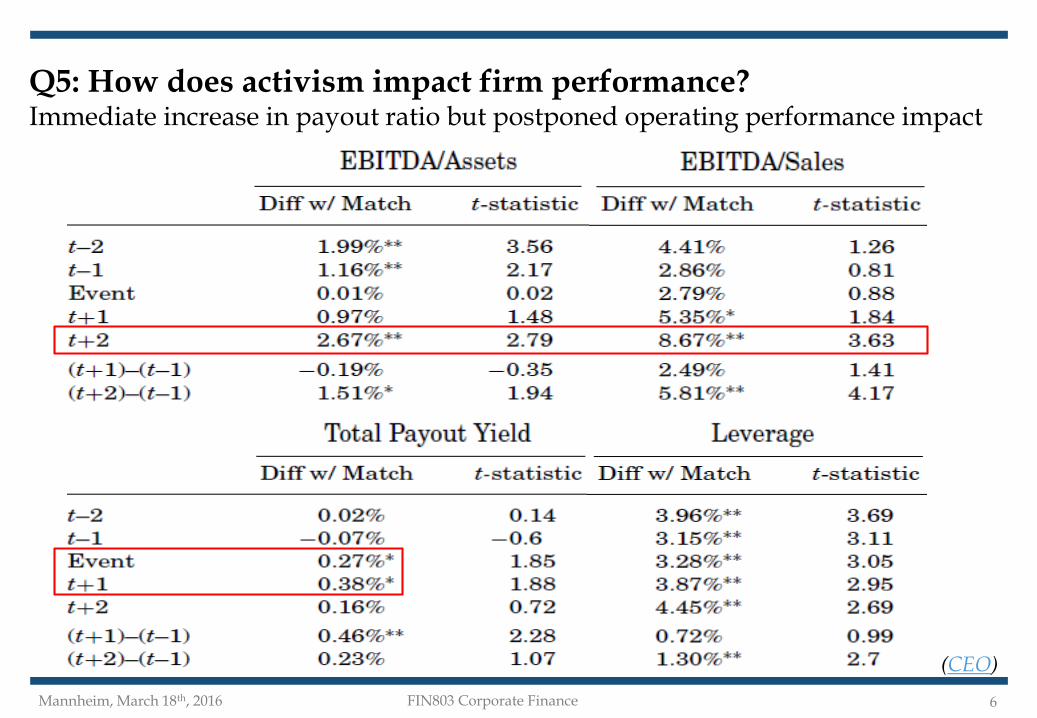

Q5: How does activism impact firm performance?Immediate increase in payout ratio but postponed operating performance impact

6

(CEO)

Mannheim, March 18th, 2016 FIN803 Corporate Finance

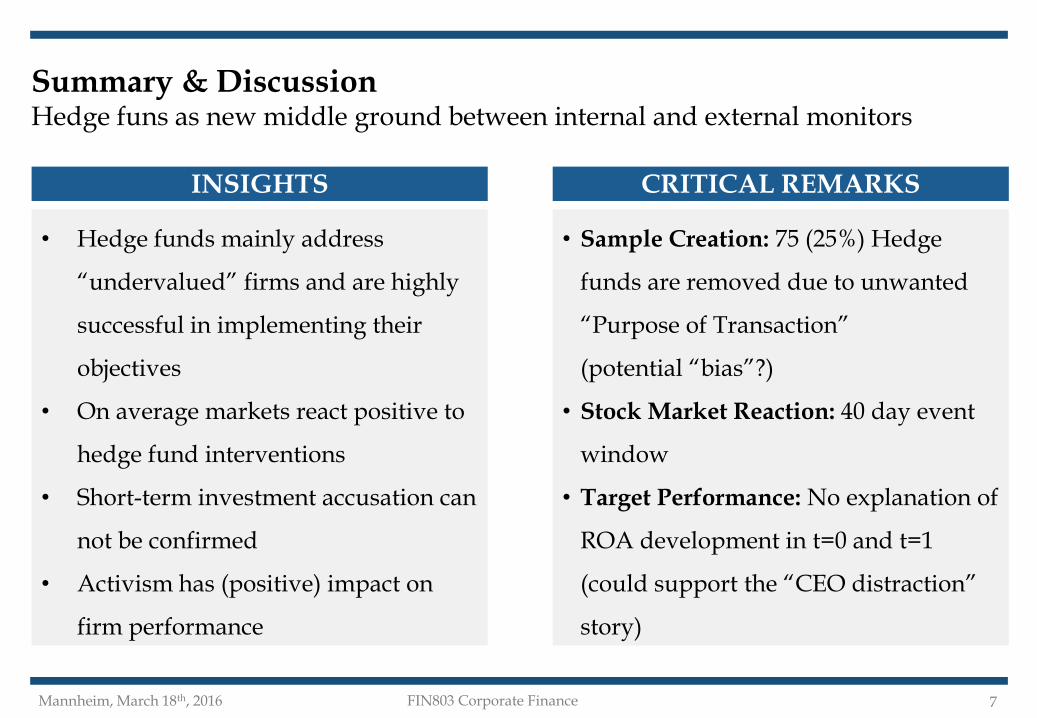

Summary & DiscussionHedge funs as new middle ground between internal and external monitors

INSIGHTS

• Hedge funds mainly address

“undervalued” firms and are highly

successful in implementing their

objectives

• On average markets react positive to

hedge fund interventions

• Short-term investment accusation can

not be confirmed

• Activism has (positive) impact on

firm performance

CRITICAL REMARKS

• Sample Creation: 75 (25%) Hedge

funds are removed due to unwanted

“Purpose of Transaction”

(potential “bias”?)

• Stock Market Reaction: 40 day event

window

• Target Performance: No explanation of

ROA development in t=0 and t=1

(could support the “CEO distraction”

story)

7

Mannheim, March 18th, 2016 FIN803 Corporate Finance

Thank you for you attention!

Mannheim, March 18th, 2016 FIN803 Corporate Finance

AppendixOverview of additional information and analysis

9

APPENDICES

• Hedge Fund “Definition”

• Related Literature

• Schedule 13D Filers / Filing

• Q1: Which firms do activists target?

• Descriptive Analysis

• Probit Regression

• Q2: Cross-Section of Abnormal returns

• Q3: Activist Objectives

• Implementation success

• Tactics

• Q4: Activist Holding Period

• Exit types and holding length

• Ownership

• Q5: Impact on firm performance (CEO)

• Long-term holding returns to activists

• Alternative stock market reaction

explanations

• BHAR analysis around activist exits

Mannheim, March 18th, 2016 FIN803 Corporate Finance

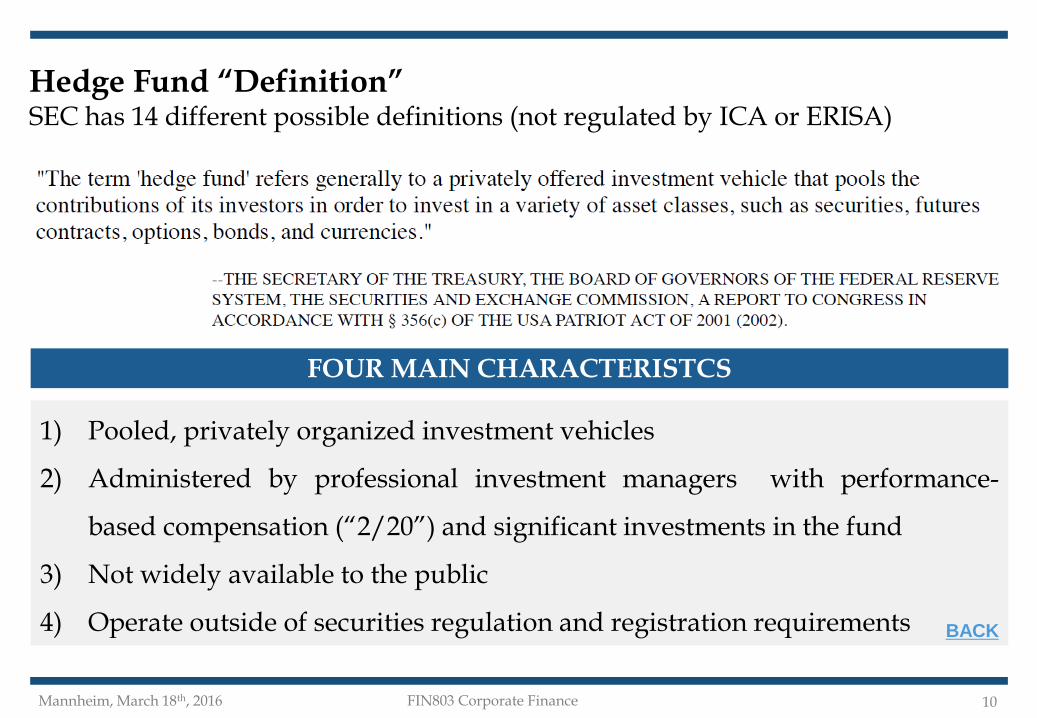

Hedge Fund “Definition”SEC has 14 different possible definitions (not regulated by ICA or ERISA)

10

FOUR MAIN CHARACTERISTCS

1) Pooled, privately organized investment vehicles

2) Administered by professional investment managers with performance-

based compensation (“2/20”) and significant investments in the fund

3) Not widely available to the public

4) Operate outside of securities regulation and registration requirements BACK

Mannheim, March 18th, 2016 FIN803 Corporate Finance

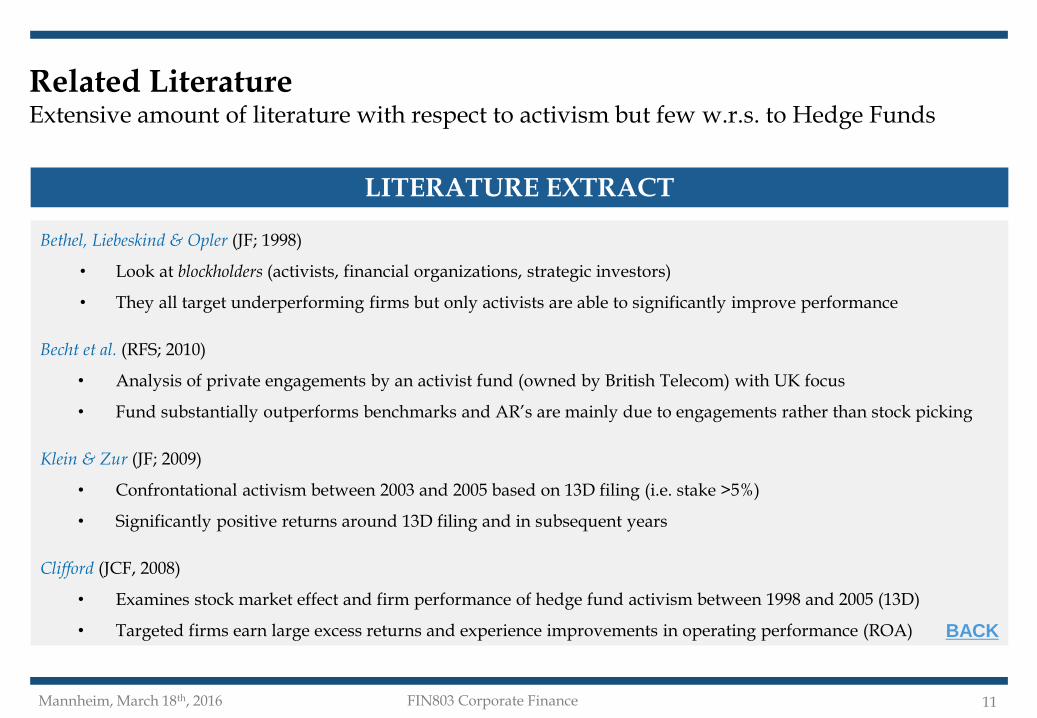

Related LiteratureExtensive amount of literature with respect to activism but few w.r.s. to Hedge Funds

11

LITERATURE EXTRACT

Bethel, Liebeskind & Opler (JF; 1998)

• Look at blockholders (activists, financial organizations, strategic investors)

• They all target underperforming firms but only activists are able to significantly improve performance

Becht et al. (RFS; 2010)

• Analysis of private engagements by an activist fund (owned by British Telecom) with UK focus

• Fund substantially outperforms benchmarks and AR’s are mainly due to engagements rather than stock picking

Klein & Zur (JF; 2009)

• Confrontational activism between 2003 and 2005 based on 13D filing (i.e. stake >5%)

• Significantly positive returns around 13D filing and in subsequent years

Clifford (JCF, 2008)

• Examines stock market effect and firm performance of hedge fund activism between 1998 and 2005 (13D)

• Targeted firms earn large excess returns and experience improvements in operating performance (ROA) BACK

Mannheim, March 18th, 2016 FIN803 Corporate Finance

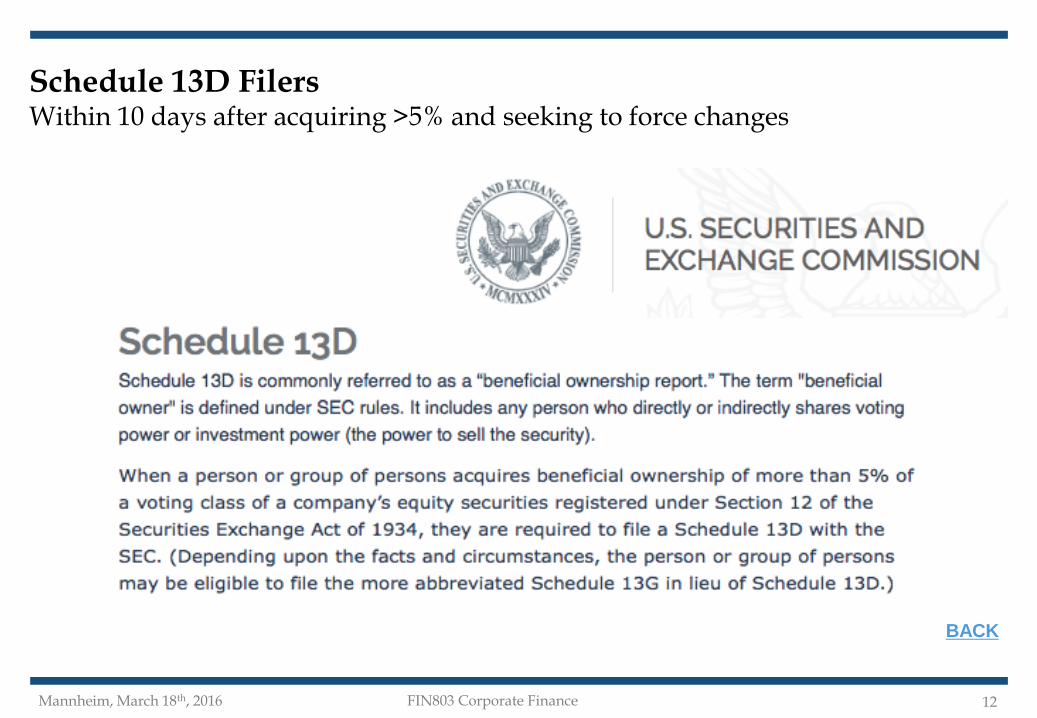

Schedule 13D FilersWithin 10 days after acquiring >5% and seeking to force changes

12

BACK

Mannheim, March 18th, 2016 FIN803 Corporate Finance

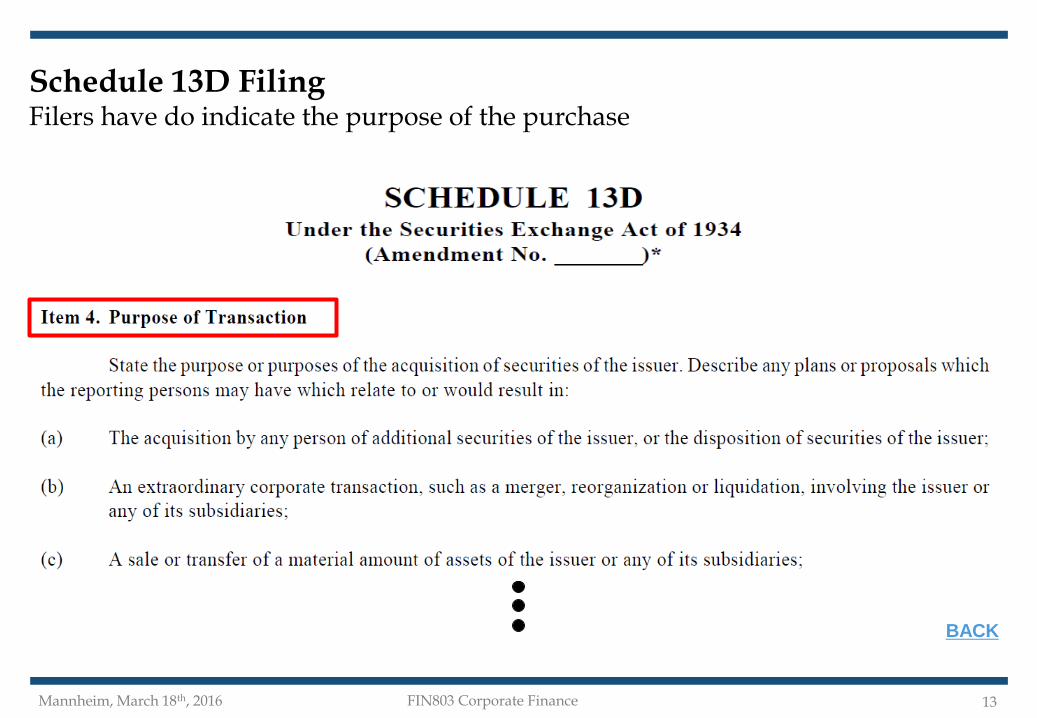

Schedule 13D FilingFilers have do indicate the purpose of the purchase

13

BACK

Mannheim, March 18th, 2016 FIN803 Corporate Finance

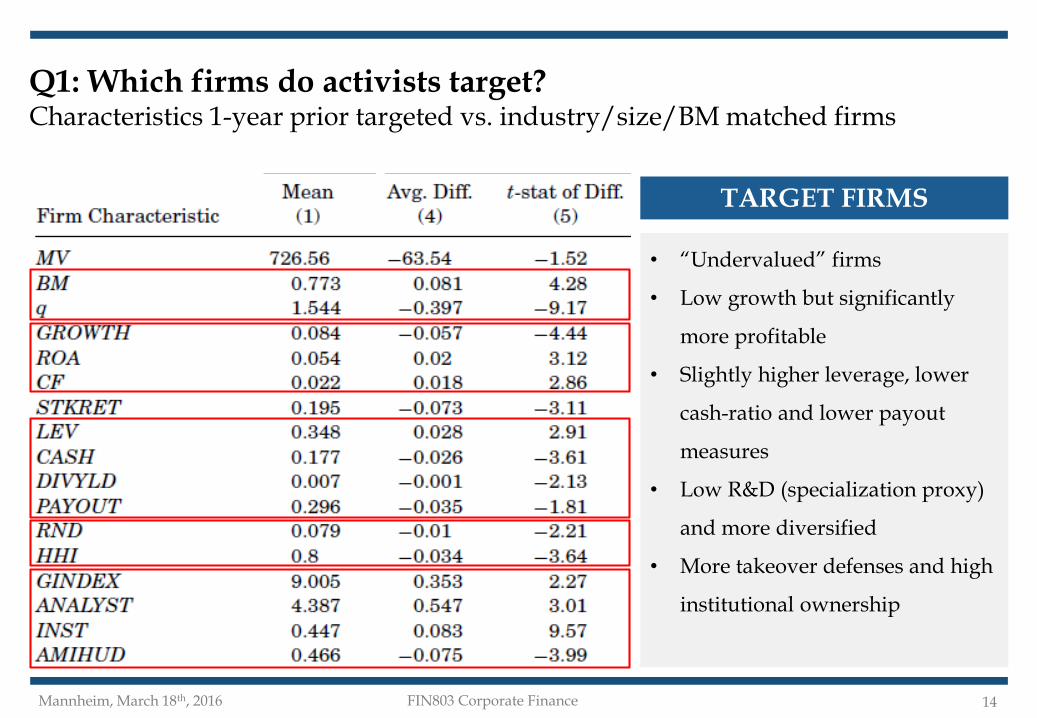

Q1: Which firms do activists target?Characteristics 1-year prior targeted vs. industry/size/BM matched firms

14

TARGET FIRMS

• “Undervalued” firms

• Low growth but significantly

more profitable

• Slightly higher leverage, lower

cash-ratio and lower payout

measures

• Low R&D (specialization proxy)

and more diversified

• More takeover defenses and high

institutional ownership

Mannheim, March 18th, 2016 FIN803 Corporate Finance

Q1: Which firms do activists target?Probit regression estimating likelihood of being targeted confirms previous results

15

BACK

Mannheim, March 18th, 2016 FIN803 Corporate Finance

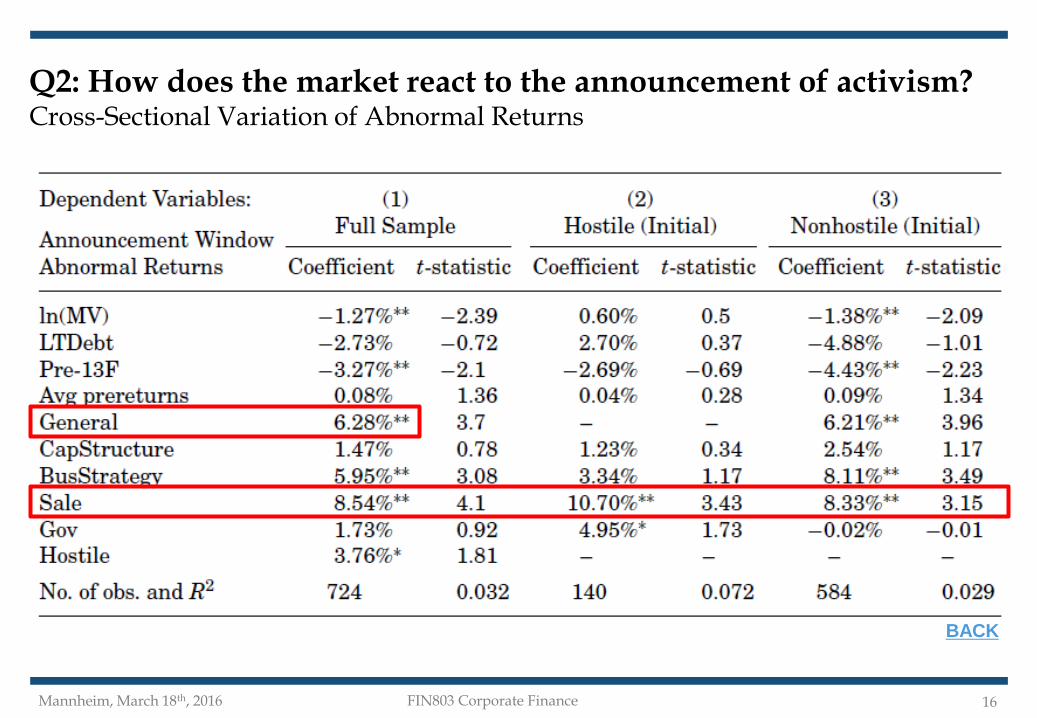

Q2: How does the market react to the announcement of activism?Cross-Sectional Variation of Abnormal Returns

16

BACK

Mannheim, March 18th, 2016 FIN803 Corporate Finance

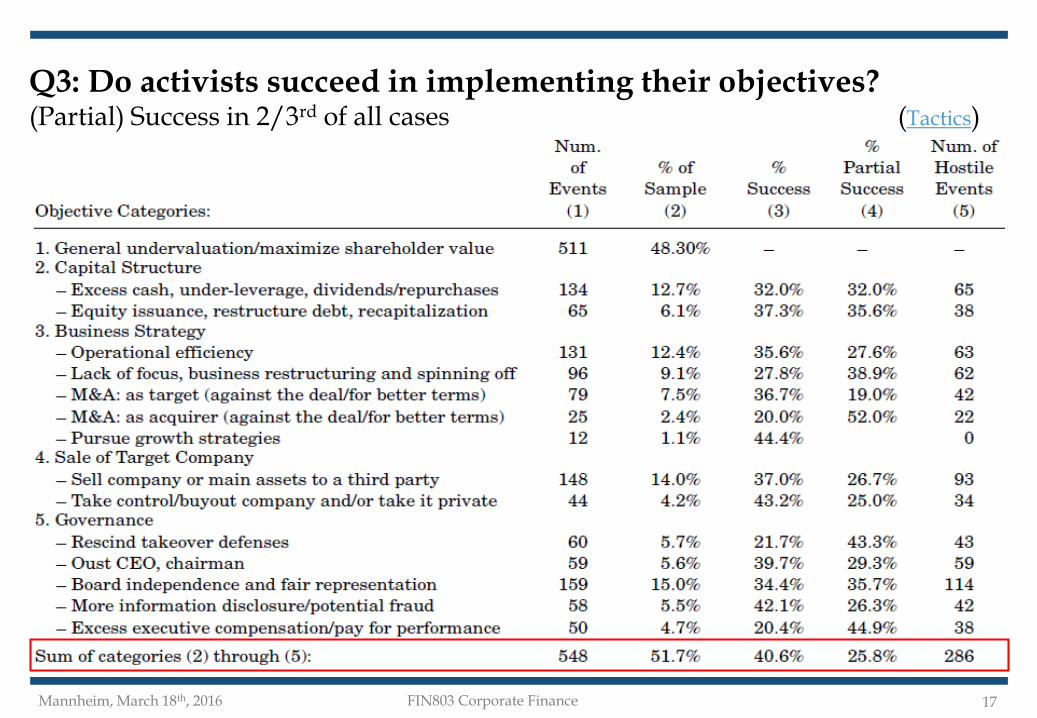

Q3: Do activists succeed in implementing their objectives?(Partial) Success in 2/3rd of all cases (Tactics)

17

Mannheim, March 18th, 2016 FIN803 Corporate Finance

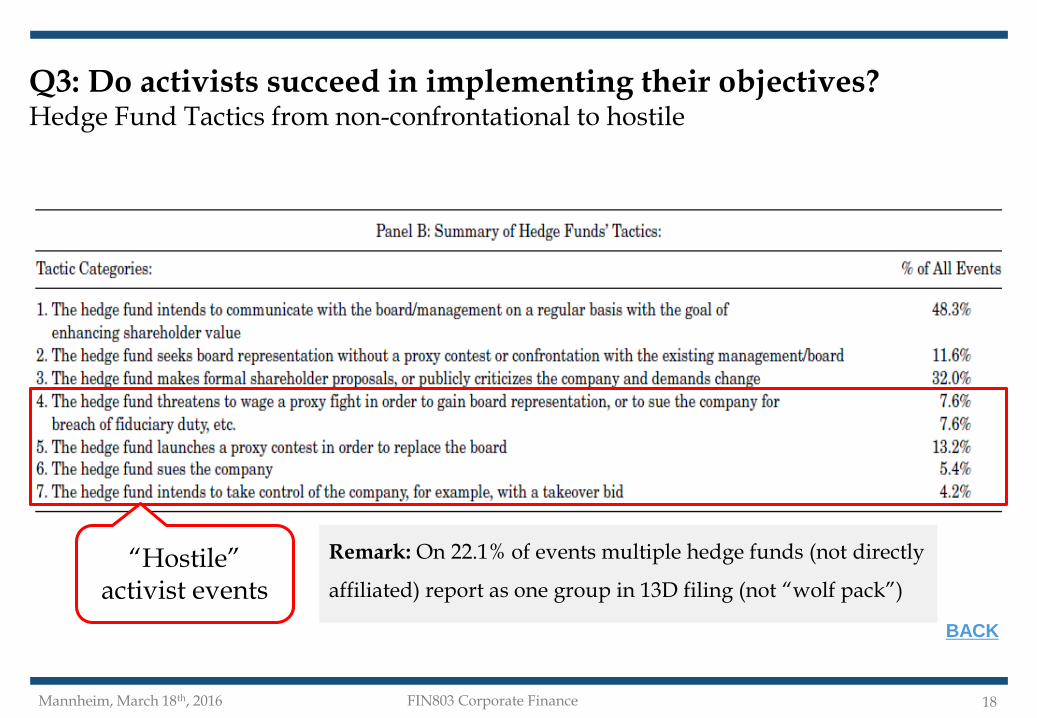

Q3: Do activists succeed in implementing their objectives?Hedge Fund Tactics from non-confrontational to hostile

18

BACK

“Hostile” activist events

Remark: On 22.1% of events multiple hedge funds (not directly

affiliated) report as one group in 13D filing (not “wolf pack”)

Mannheim, March 18th, 2016 FIN803 Corporate Finance

Q4: Are activists short term in their focus?The median duration until the “exit” is 369 days (imputed: 556 or 22 months)

19

(Ownership)

Mannheim, March 18th, 2016 FIN803 Corporate Finance

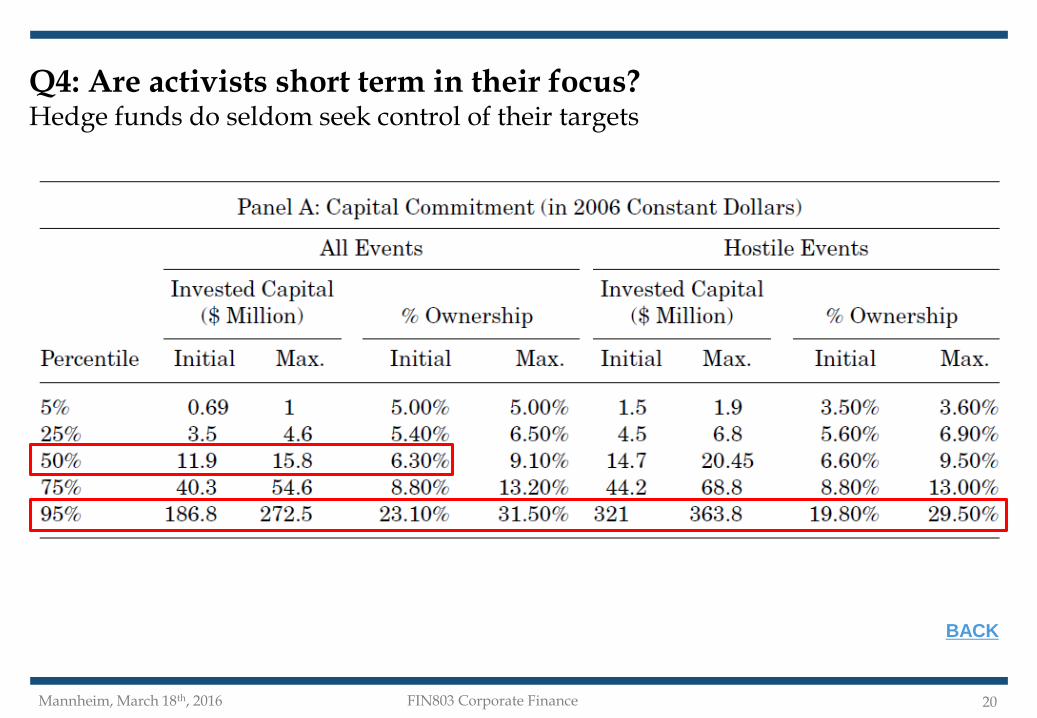

Q4: Are activists short term in their focus?Hedge funds do seldom seek control of their targets

20

BACK

Mannheim, March 18th, 2016 FIN803 Corporate Finance

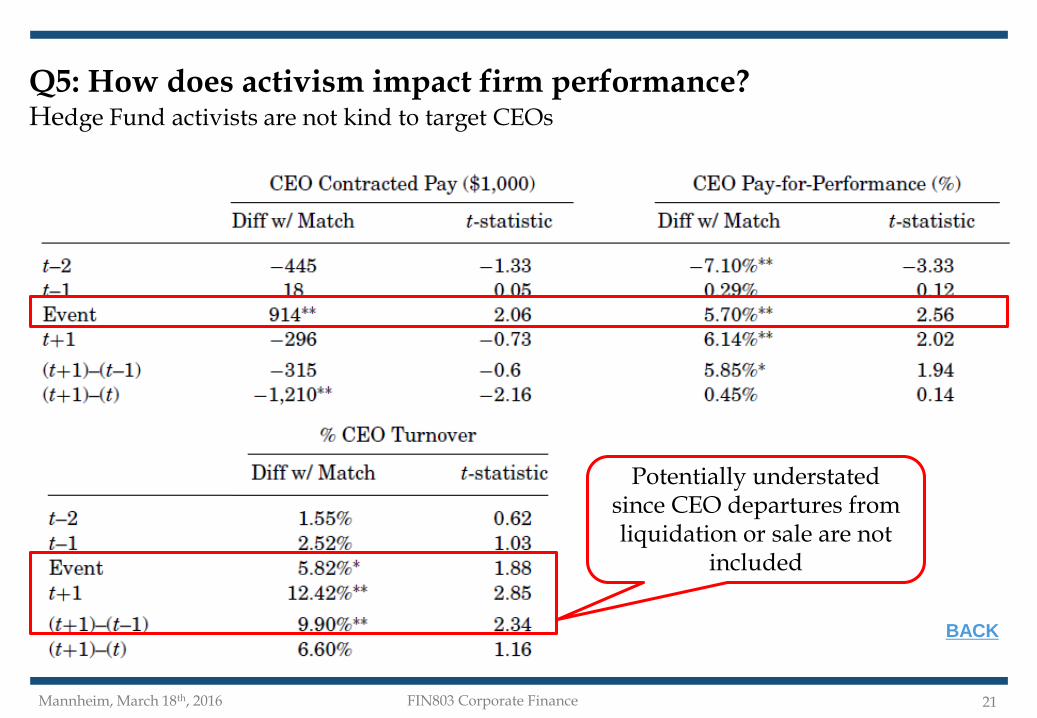

Q5: How does activism impact firm performance?Hedge Fund activists are not kind to target CEOs

21

BACK

Potentially understated since CEO departures from liquidation or sale are not

included

Mannheim, March 18th, 2016 FIN803 Corporate Finance

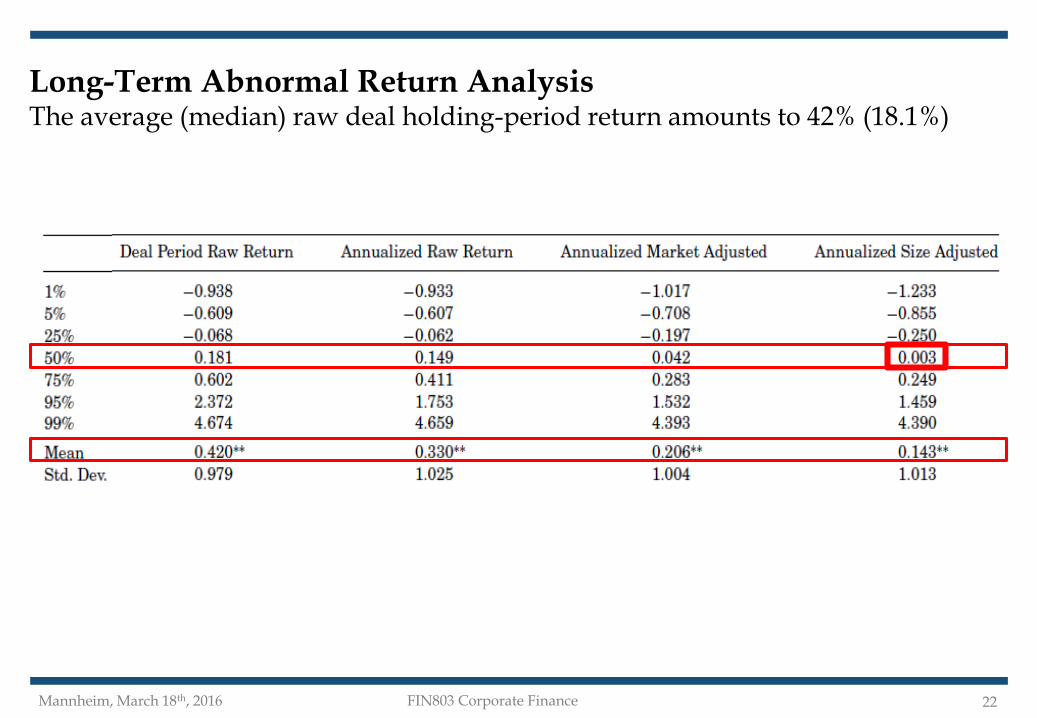

Long-Term Abnormal Return AnalysisThe average (median) raw deal holding-period return amounts to 42% (18.1%)

22

Mannheim, March 18th, 2016 FIN803 Corporate Finance

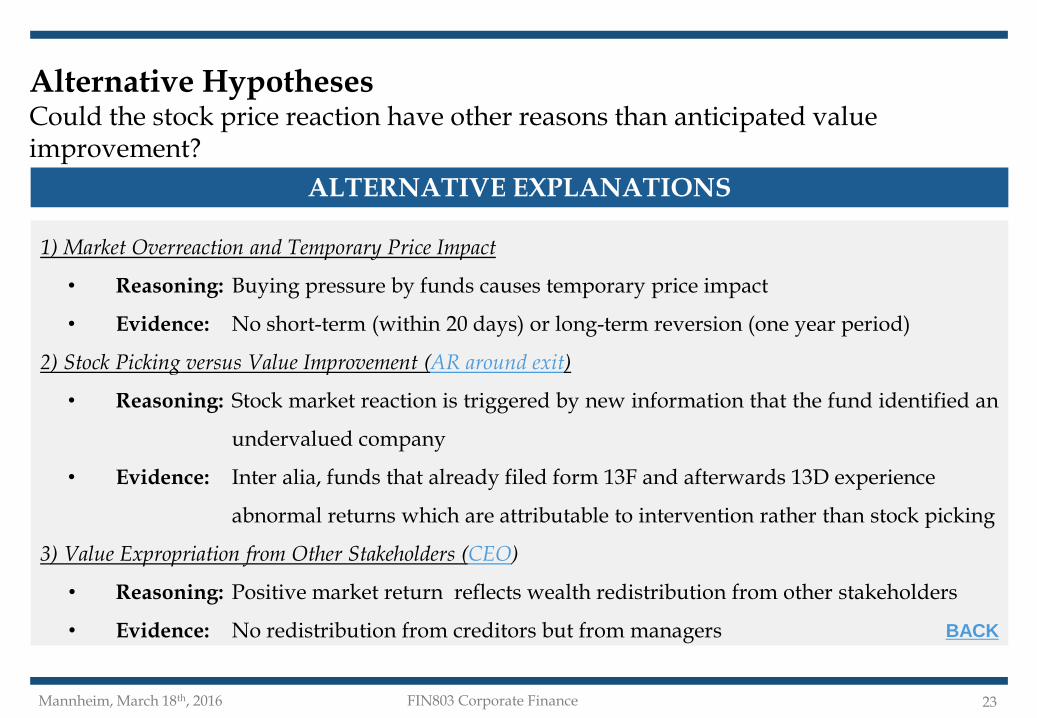

Alternative HypothesesCould the stock price reaction have other reasons than anticipated value improvement?

23

ALTERNATIVE EXPLANATIONS

1) Market Overreaction and Temporary Price Impact

• Reasoning: Buying pressure by funds causes temporary price impact

• Evidence: No short-term (within 20 days) or long-term reversion (one year period)

2) Stock Picking versus Value Improvement (AR around exit)

• Reasoning: Stock market reaction is triggered by new information that the fund identified an

undervalued company

• Evidence: Inter alia, funds that already filed form 13F and afterwards 13D experience

abnormal returns which are attributable to intervention rather than stock picking

3) Value Expropriation from Other Stakeholders (CEO)

• Reasoning: Positive market return reflects wealth redistribution from other stakeholders

• Evidence: No redistribution from creditors but from managers BACK

Mannheim, March 18th, 2016 FIN803 Corporate Finance

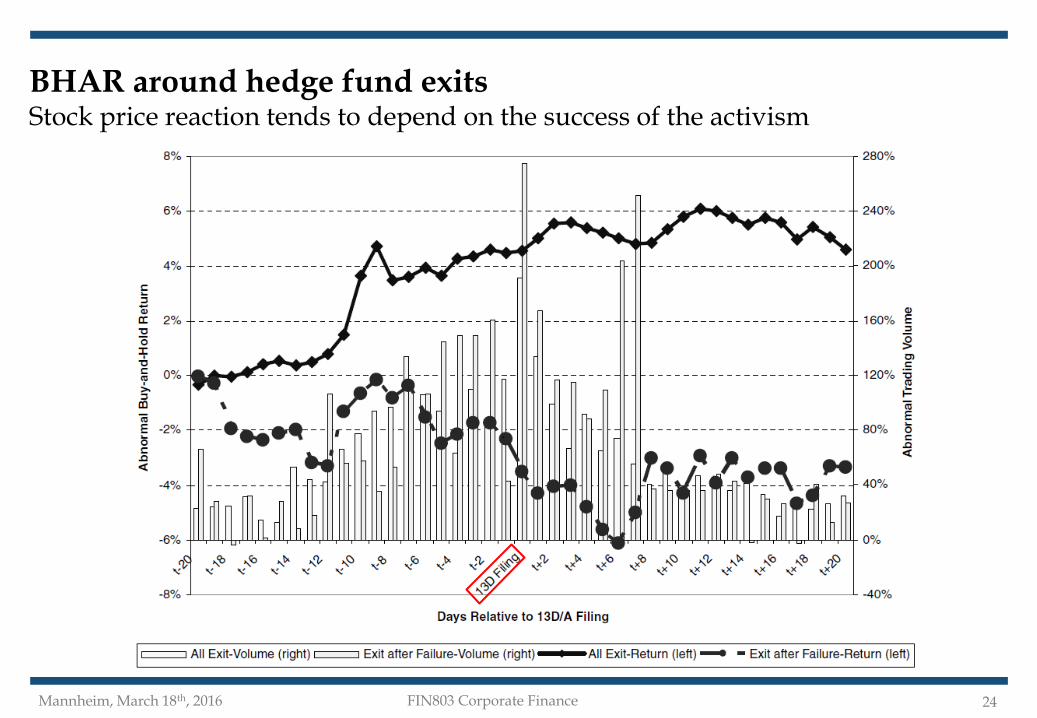

BHAR around hedge fund exitsStock price reaction tends to depend on the success of the activism

24

Related Documents