Health Savings Accounts and Trends in Employee Health Benefits National Academy of Social Insurance Charles H. Klippel Senior Vice President and Deputy General Counsel Aetna Inc. January 27, 2005

Health Savings Accounts and Trends in Employee Health Benefits National Academy of Social Insurance Charles H. Klippel Senior Vice President and Deputy.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Health Savings Accountsand

Trends in Employee Health Benefits

National Academy of

Social Insurance

Charles H. Klippel

Senior Vice President

and Deputy General Counsel

Aetna Inc.

January 27, 2005

The Emergence and Future of Consumerism

• Drivers of change in plan design– Changes in preferences/ market forces– The role of a deductible – Tax policy

• Impact of change– Findings from Aetna’s experience

• Future directions– Further evolution in plan design– Employer disengagement– Other considerations

Policy follows the market

• HSAs are a consequence, not a cause, of change– Consumerism did not start in Washington– Not a “red” or “blue” idea– Not driven by health industry– Started with employers

• Not radical thinking– Role of deductible in health coverage– Response to employee concerns– Cost pressures– Preserving tax preference of benefit dollars

Deductibles in health plans

• Deductibles have always been a part of health insurance – Standard in almost all other forms of

insurance– Historically plans without a deductible are

the anomaly

• Health Maintenance OrganizationsSelected provider networkCare managed to protocols = Different benefit structure

The Role of a Deductible

Classic role of a deductible in insurance• Reduce “moral hazard”• Avoid high processing costs of smaller claims

Additional consideration in health• Increasing choice in treatment• Differing perceptions of value• Significant cost differences• Efficacy may not correlate with cost

Example: Pharmaceuticals

Supporting choice/ subsidizing risk

Options for the plan sponsor• Manage selection directly or in benefit design• Pay everything regardless of choice• Deductible (with financial assistance)

Focus defined benefit dollars on shared, unanticipated risks• Benefits typically a trade-off for wages• “Regressive” (in tax terms)• An inherent cross-subsidy related to use, not need

Health Reimbursement Accounts

• A portion of benefits structured as “fund”– Unused dollars roll over for future years

• Sanctioned by Treasury in June 2002– Must be employer dollars– No employee contributions– Employer defines rules– Money is not portable

• HRAs in practice– Typically self-funded plans– Accounts generally “first dollar”– May continue for retirees, otherwise lost

when employment ends

HRA

Health Savings Accounts

• Part of MMA in December 2003• Greater flexibility

– Permits employee funding• Consumer protections

– All money belongs to employee– Employer can’t restrict use– Fully portable– HDPH specifies minimum deductible and

maximum out-of-pocket (i.e., plans can be too rich or too limited to qualify)

HSA

Alternatives to fund structure

• Additional wages– Less tax efficient– Does not encourage savings

• Lower deductible, eliminate “fund”– “Doughnut-hole” argument– Less consumer risk (?)

Doughnut-hole Paradox

$0.00

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

0 36% 49% 63% 90%

Source: Medical Expenditure Panel Survey (2002)

Plan with $1000 deductible and $500 “fund”• Would save employer $220 over 1st dollar plan• Savings equivalent to a $300 deductible

$300

Doughnut-hole Paradox

$0.00

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

0 36% 49% 63% 90%

$300 Deductible $1000 w/ $500 Fund

More expenses covered 43% 57%

Average % of expenses covered

45% 86%

% covered of $10,000 99.7% 99.5%

$0.00

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

0 36% 49% 63% 90%

Impact of plan design

• Aetna Health Fund®– HRA plan enrollees in 2003– 13,500 members enrolled in other Aetna

plans in the 2002– One full-replacement plan– Full-year 2002 to 2003 comparison – Also compared to 300,000 cohort-matched

individuals enrolled in other Aetna plans in 2003

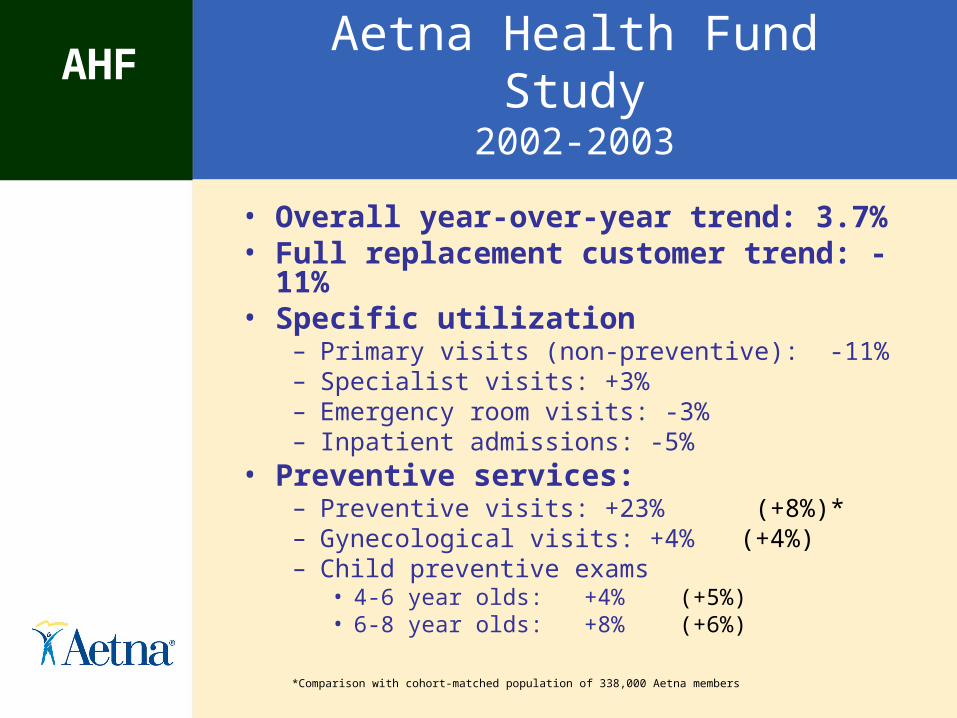

Aetna Health Fund Study2002-2003

• Overall year-over-year trend: 3.7%• Full replacement customer trend: -11%• Specific utilization

– Primary visits (non-preventive): -11%– Specialist visits: +3%– Emergency room visits: -3%– Inpatient admissions: -5%

• Preventive services:– Preventive visits: +23% (+8%)*– Gynecological visits: +4% (+4%)– Child preventive exams

• 4-6 year olds: +4% (+5%)• 6-8 year olds: +8% (+6%)

*Comparison with cohort-matched population of 338,000 Aetna members

AHF

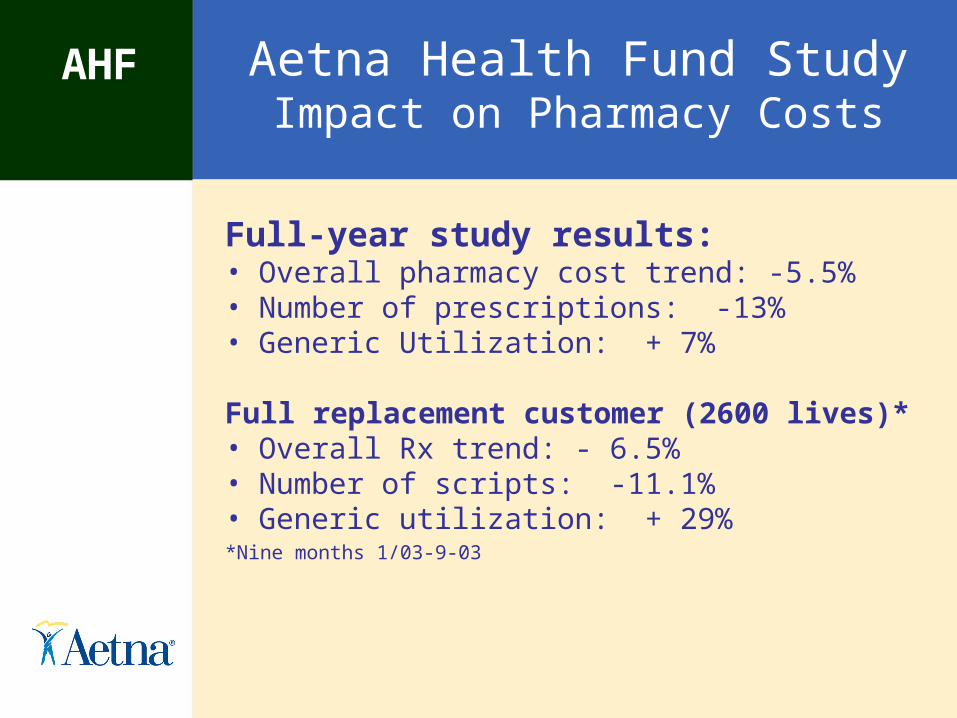

Aetna Health Fund StudyImpact on Pharmacy Costs

Full-year study results:• Overall pharmacy cost trend: -5.5%• Number of prescriptions: -13%• Generic Utilization: + 7%

Full replacement customer (2600 lives)*• Overall Rx trend: - 6.5%• Number of scripts: -11.1%• Generic utilization: + 29%*Nine months 1/03-9-03

AHF

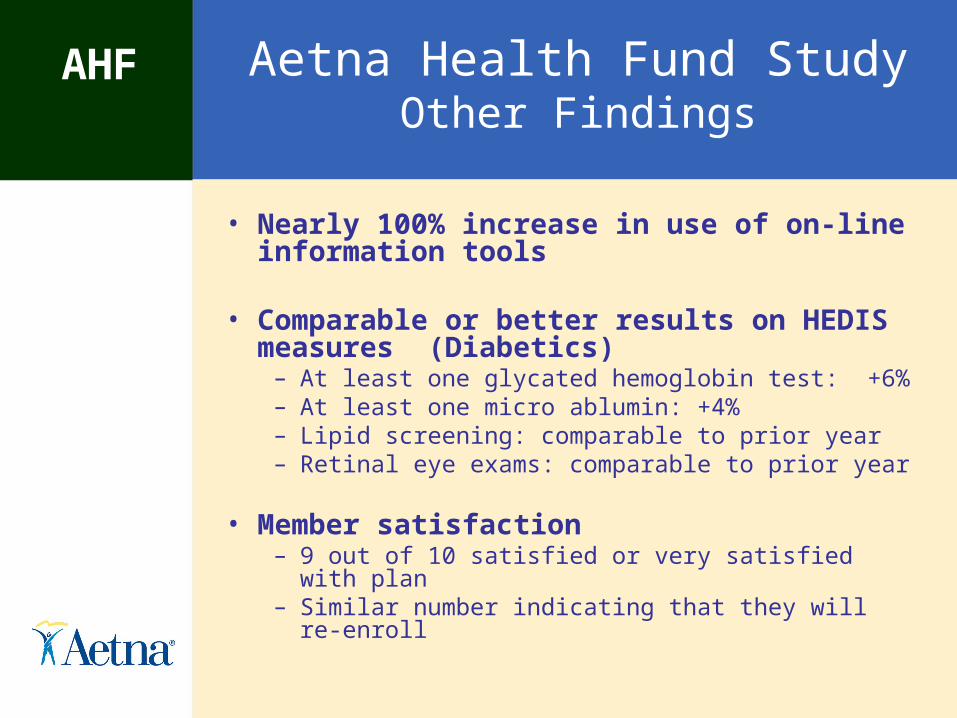

Aetna Health Fund StudyOther Findings

• Nearly 100% increase in use of on-line information tools

• Comparable or better results on HEDIS measures (Diabetics)

– At least one glycated hemoglobin test: +6%– At least one micro ablumin: +4%– Lipid screening: comparable to prior year– Retinal eye exams: comparable to prior year

• Member satisfaction– 9 out of 10 satisfied or very satisfied with plan– Similar number indicating that they will re-enroll

AHF

Looking forward

Where is plan design going from here?

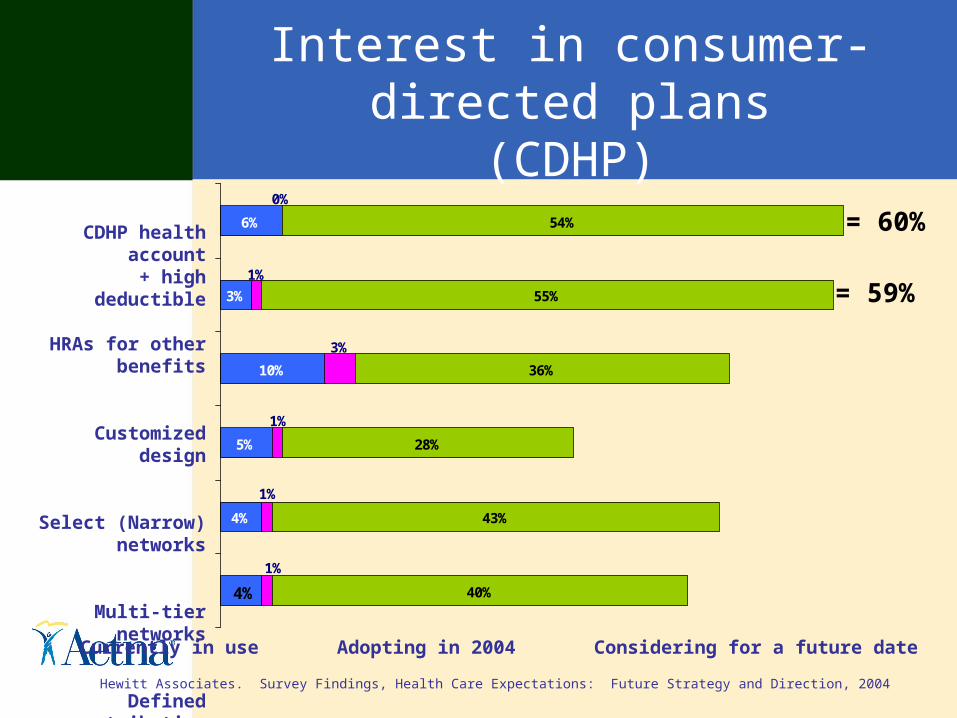

Interest in consumer-directed plans(CDHP)

4%

5%

10%

3%

6%

40%

43%

28%

36%

55%

54%

4%

1%

3%

1%

0%

1%

1%

CDHP health account + high deductible

HRAs for other benefits

Customized design

Select (Narrow) networks

Multi-tier networks

Defined contribution

Currently in use Adopting in 2004 Considering for a future date

Hewitt Associates. Survey Findings, Health Care Expectations: Future Strategy and Direction, 2004

= 59%

= 60%

Estimated CDHP adoption

1% 2% 3% 7% 12% 19% 24%4% 4% 4%

4%4%

4%4%

26% 26% 26%26%

25%

25%24%

52% 51% 49% 47% 43%38%

35%

18% 18% 18% 17% 16% 15% 13%

2004 2005 2006 2007 2008 2009 2010

POSPPOHMOConventionalConsumer-directed health plans

(percentages may not total 100 because of rounding)

Forrester Research, Inc., 2003

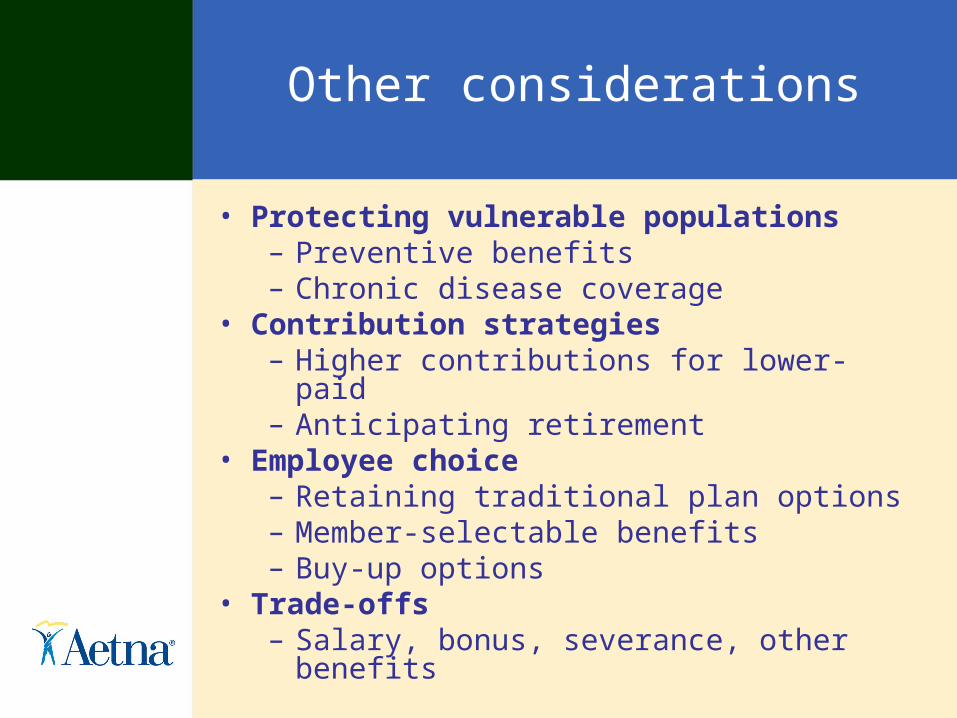

Other considerations

• Protecting vulnerable populations– Preventive benefits– Chronic disease coverage

• Contribution strategies– Higher contributions for lower-paid– Anticipating retirement

• Employee choice– Retaining traditional plan options– Member-selectable benefits – Buy-up options

• Trade-offs– Salary, bonus, severance, other benefits

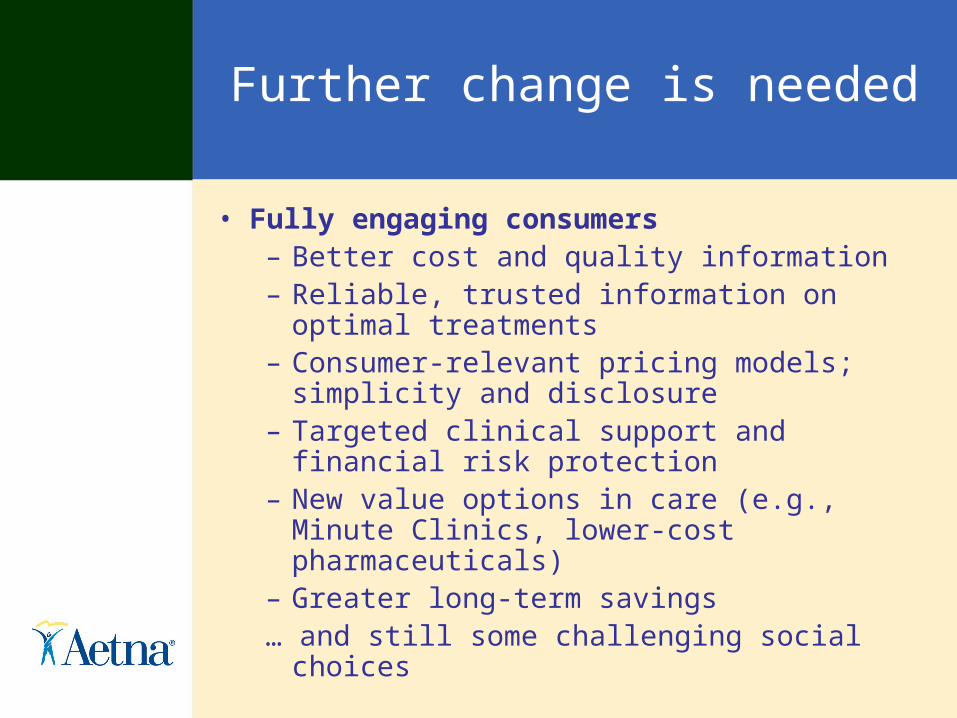

Further change is needed

• Fully engaging consumers– Better cost and quality information– Reliable, trusted information on optimal

treatments– Consumer-relevant pricing models;

simplicity and disclosure– Targeted clinical support and financial risk

protection– New value options in care (e.g., Minute

Clinics, lower-cost pharmaceuticals)– Greater long-term savings… and still some challenging social choices

Related Documents

![[Friederike Klippel] Keep Talking Communicative F(BookFi.org)](https://static.cupdf.com/doc/110x72/56d6bfe01a28ab3016980726/friederike-klippel-keep-talking-communicative-fbookfiorg.jpg)