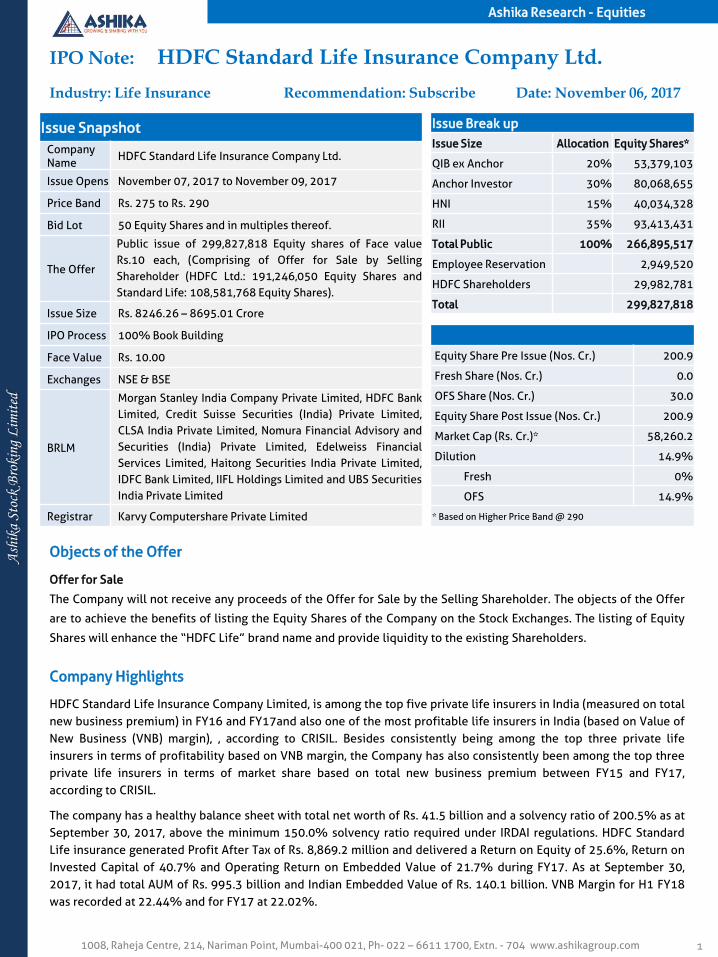

Ashika Stock Broking Limited Ashika Research - Equities 1 IPO Note: HDFC Standard Life Insurance Company Ltd. Issue Snapshot Company Name HDFC Standard Life Insurance Company Ltd. Issue Opens November 07, 2017 to November 09, 2017 Price Band Rs. 275 to Rs. 290 Bid Lot 50 Equity Shares and in multiples thereof. The Offer Public issue of 299,827,818 Equity shares of Face value Rs.10 each, (Comprising of Offer for Sale by Selling Shareholder (HDFC Ltd.: 191,246,050 Equity Shares and Standard Life: 108,581,768 Equity Shares). Issue Size Rs. 8246.26 – 8695.01 Crore IPO Process 100% Book Building Face Value Rs. 10.00 Exchanges NSE & BSE BRLM Morgan Stanley India Company Private Limited, HDFC Bank Limited, Credit Suisse Securities (India) Private Limited, CLSA India Private Limited, Nomura Financial Advisory and Securities (India) Private Limited, Edelweiss Financial Services Limited, Haitong Securities India Private Limited, IDFC Bank Limited, IIFL Holdings Limited and UBS Securities India Private Limited Registrar Karvy Computershare Private Limited Industry: Life Insurance Recommendation: Subscribe Date: November 06, 2017 1008, Raheja Centre, 214, Nariman Point, Mumbai-400 021, Ph- 022 – 6611 1700, Extn. - 704 www.ashikagroup.com Objects of the Offer Offer for Sale The Company will not receive any proceeds of the Offer for Sale by the Selling Shareholder. The objects of the Offer are to achieve the benefits of listing the Equity Shares of the Company on the Stock Exchanges. The listing of Equity Shares will enhance the “HDFC Life” brand name and provide liquidity to the existing Shareholders. Issue Break up Issue Size Allocation Equity Shares* QIB ex Anchor 20% 53,379,103 Anchor Investor 30% 80,068,655 HNI 15% 40,034,328 RII 35% 93,413,431 Total Public 100% 266,895,517 Employee Reservation 2,949,520 HDFC Shareholders 29,982,781 Total 299,827,818 Company Highlights HDFC Standard Life Insurance Company Limited, is among the top five private life insurers in India (measured on total new business premium) in FY16 and FY17and also one of the most profitable life insurers in India (based on Value of New Business (VNB) margin), , according to CRISIL. Besides consistently being among the top three private life insurers in terms of profitability based on VNB margin, the Company has also consistently been among the top three private life insurers in terms of market share based on total new business premium between FY15 and FY17, according to CRISIL. The company has a healthy balance sheet with total net worth of Rs. 41.5 billion and a solvency ratio of 200.5% as at September 30, 2017, above the minimum 150.0% solvency ratio required under IRDAI regulations. HDFC Standard Life insurance generated Profit After Tax of Rs. 8,869.2 million and delivered a Return on Equity of 25.6%, Return on Invested Capital of 40.7% and Operating Return on Embedded Value of 21.7% during FY17. As at September 30, 2017, it had total AUM of Rs. 995.3 billion and Indian Embedded Value of Rs. 140.1 billion. VNB Margin for H1 FY18 was recorded at 22.44% and for FY17 at 22.02%. Equity Share Pre Issue (Nos. Cr.) 200.9 Fresh Share (Nos. Cr.) 0.0 OFS Share (Nos. Cr.) 30.0 Equity Share Post Issue (Nos. Cr.) 200.9 Market Cap (Rs. Cr.)* 58,260.2 Dilution 14.9% Fresh 0% OFS 14.9% * Based on Higher Price Band @ 290

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Ash

ika

Stoc

k B

roki

ng L

imit

edAshika Research - Equities

1

IPO Note: HDFC Standard Life Insurance Company Ltd.

Issue Snapshot

CompanyName

HDFC Standard Life Insurance Company Ltd.

Issue Opens November 07, 2017 to November 09, 2017

Price Band Rs. 275 to Rs. 290

Bid Lot 50 Equity Shares and in multiples thereof.

The Offer

Public issue of 299,827,818 Equity shares of Face value

Rs.10 each, (Comprising of Offer for Sale by Selling

Shareholder (HDFC Ltd.: 191,246,050 Equity Shares and

Standard Life: 108,581,768 Equity Shares).

Issue Size Rs. 8246.26 – 8695.01 Crore

IPO Process 100% Book Building

Face Value Rs. 10.00

Exchanges NSE & BSE

BRLM

Morgan Stanley India Company Private Limited, HDFC Bank

Limited, Credit Suisse Securities (India) Private Limited,

CLSA India Private Limited, Nomura Financial Advisory and

Securities (India) Private Limited, Edelweiss Financial

Services Limited, Haitong Securities India Private Limited,

IDFC Bank Limited, IIFL Holdings Limited and UBS Securities

India Private Limited

Registrar Karvy Computershare Private Limited

Industry: Life Insurance Recommendation: Subscribe Date: November 06, 2017

1008, Raheja Centre, 214, Nariman Point, Mumbai-400 021, Ph- 022 – 6611 1700, Extn. - 704 www.ashikagroup.com

Objects of the Offer

Offer for Sale

The Company will not receive any proceeds of the Offer for Sale by the Selling Shareholder. The objects of the Offer

are to achieve the benefits of listing the Equity Shares of the Company on the Stock Exchanges. The listing of Equity

Shares will enhance the “HDFC Life” brand name and provide liquidity to the existing Shareholders.

Issue Break up

Issue Size Allocation Equity Shares*

QIB ex Anchor 20% 53,379,103

Anchor Investor 30% 80,068,655

HNI 15% 40,034,328

RII 35% 93,413,431

Total Public 100% 266,895,517

Employee Reservation 2,949,520

HDFC Shareholders 29,982,781

Total 299,827,818

Company Highlights

HDFC Standard Life Insurance Company Limited, is among the top five private life insurers in India (measured on total

new business premium) in FY16 and FY17and also one of the most profitable life insurers in India (based on Value of

New Business (VNB) margin), , according to CRISIL. Besides consistently being among the top three private life

insurers in terms of profitability based on VNB margin, the Company has also consistently been among the top three

private life insurers in terms of market share based on total new business premium between FY15 and FY17,

according to CRISIL.

The company has a healthy balance sheet with total net worth of Rs. 41.5 billion and a solvency ratio of 200.5% as at

September 30, 2017, above the minimum 150.0% solvency ratio required under IRDAI regulations. HDFC Standard

Life insurance generated Profit After Tax of Rs. 8,869.2 million and delivered a Return on Equity of 25.6%, Return on

Invested Capital of 40.7% and Operating Return on Embedded Value of 21.7% during FY17. As at September 30,

2017, it had total AUM of Rs. 995.3 billion and Indian Embedded Value of Rs. 140.1 billion. VNB Margin for H1 FY18

was recorded at 22.44% and for FY17 at 22.02%.

Equity Share Pre Issue (Nos. Cr.) 200.9

Fresh Share (Nos. Cr.) 0.0

OFS Share (Nos. Cr.) 30.0

Equity Share Post Issue (Nos. Cr.) 200.9

Market Cap (Rs. Cr.)* 58,260.2

Dilution 14.9%

Fresh 0%

OFS 14.9%

* Based on Higher Price Band @ 290

Ash

ika

Stoc

k B

roki

ng L

imit

edAshika Research - Equities

21008, Raheja Centre, 214, Nariman Point, Mumbai-400 021, Ph- 022 – 6611 1700, Extn. - 704 www.ashikagroup.com

The Company believes that its strong parentage and its trusted brand enhance its appeal to consumers. It was one of

the first private life insurance company to register in India and was established as a joint venture between HDFC (one

of India’s leading housing finance institutions) and Standard Life Aberdeen plc (one of the world’s largest investment

companies), initially through its wholly owned subsidiary The Standard Life Assurance Company and now through its

wholly owned subsidiary, Standard Life Mauritius.

The Company has a broad, diversified product portfolio covering five principal segments across the individual and

group categories, namely participating, non‐participating protection term, non‐participating protection health, other

non‐participating and unit‐linked insurance products. As at September 30, 2017, its product portfolio comprised 32

individual and ten group products, as well as eight optional rider benefits. Its wide product suite caters to specific

needs of customers during each stage of their lives. It also provides with the flexibility to operate successfully across

business cycles, work with diverse sets of distribution partners and serve a range of consumers from mass market to

high net worth individuals.

Company’s prime focuses it to be in highly profitable business model despite stiff competition and to be in top five

ranks. For this, it is keeping ULIP products sale under 50% and from the rest, it does conventional product, tailor

made products and specialized products. The Company has a pan-India presence, comprising 414 branches and

spokes across India as at September 30, 2017, supported by a dedicated workforce of 16,544 full-time employees.

The Company’s bancassurance partners include banks, non-banking financial companies, micro-finance institutions

and small finance banks in India. The number of major bancassurance partners grew from 31 as at March 31, 2015 to

125 as at September 30, 2017. The top 15 bancassurance partners (in terms of total new business premium sourced

for the period ended September 30, 2017) had over 11,200 branches across India as at September 30, 2017.

View

HDFC Life is one of the most profitable life insurers, based on Value of New Business (VNB) margin, among the top 5

private life insurers in India (measured on total new business premium) in FY16 and FY17, according to CRISIL. VNB

margin stood at 22.4% as on 30th Sep, 2017. AUM was Rs. 99,534 cr as on Sep 17, grown at a CAGR of 17% from

FY15-FY17. Total new business premium for FY17 and H1FY18 was Rs. 8,696.4 cr and Rs. 4,402.9 cr respectively.

Between FY15-FY17, their annualised premium equivalent has grown at a CAGR of 14.5%. Its 13th month individual

persistency ratio stood at 80.9% and 82.2% for FY17 and H1FY18 respectively. As on Sep 30, 2017, company has a

pan-India presence, comprising 414 branches spread across India and is supported by a dedicated workforce of

16,544 full-time employees. The company’s bancassurance partners include banks, non-banking financial companies,

micro-finance institutions and small finance banks in India. HDFC Life sells policies through a multi channel network.

This includes direct sales through own branches, Insurance agents, Partner Banks and through other financial

institutions. Company has over 66,372 individual agents.

On performance front, company’s revenue and net profit has grown at a CAGR of 22% and 19% respectively over the

last 5 years. For H1FY18, it has posted net profit of Rs. 554.8 cr on a total income of Rs. 14,415 cr. It has a healthy

balance sheet with total net worth of Rs. 44.6 bn and strong solvency ratio of 2x as on 30th Sep, 2017 as against

regulatory minimum of 1.50x. Its 12.6% expense ratio is slightly lower that the industry average of 13%. Death

Claim Settlement Ratio for HDFC Life is better than peers at 99.2% compared to 98% for SBI Life and 97.2% for ICICI

Prudential, as on FY17. During FY 17 the company reported strong ROE of 25.6%, ROCE of 40.7% and Operating

Return on Embedded Value of 21.7%. As on 30th Sep, 2017, its Indian Embedded Value stood at Rs.14,011.4 cr.

At the higher price band, the issue is valued at 4.2x as on 30th Sep, 2017 embedded value, which is at premium when

considered with 3.9x and 3.6x embedded value for SBI Life and ICICI Prudential respectively. However, considering

robust VNB margins, lower operating expenses ratio and strong persistency ratio coupled with healthy premium

growth, the premium valuations are justified. Considering low insurance penetration in India and improvement in

share of financial savings in household savings, together with strong operational metrics for HDFC Life, we

recommend to “SUBSCRIBE” the issue from long term investment perspective.

Ash

ika

Stoc

k B

roki

ng L

imit

edAshika Research - Equities

31008, Raheja Centre, 214, Nariman Point, Mumbai-400 021, Ph- 022 – 6611 1700, Extn. - 704 www.ashikagroup.com

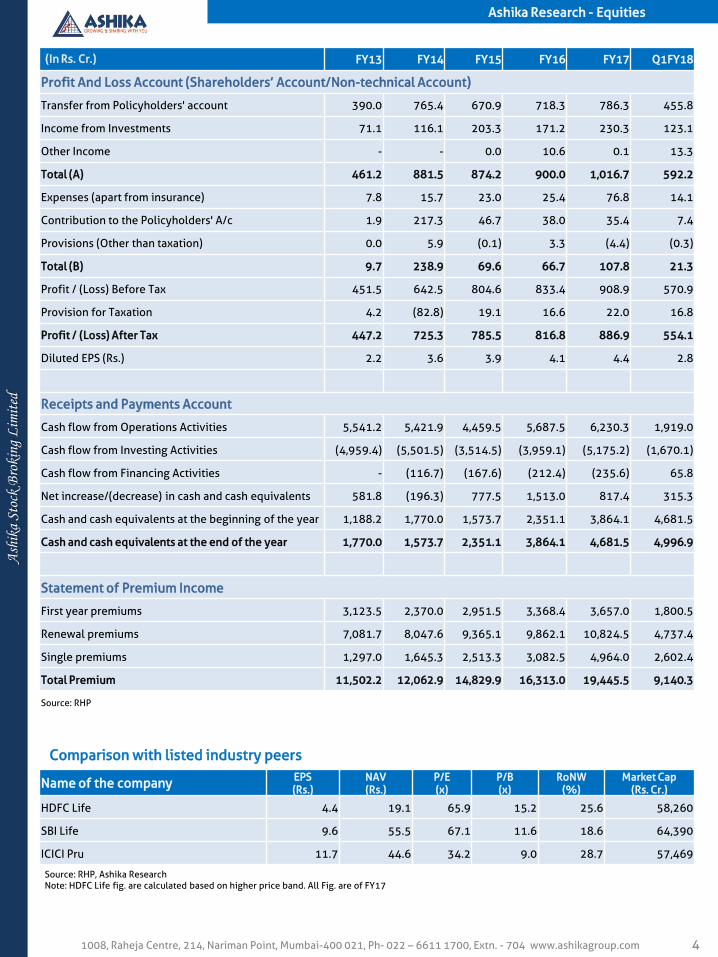

Consolidated Financial Statement

(In Rs. Cr.) FY13 FY14 FY15 FY16 FY17 Q1FY18

Statement of Assets and Liabilities

Shareholders' Funds

Share Capital 1,994.9 1,994.9 1,994.9 1,995.3 1,998.5 2,005.6

Reserves and Surplus 196.2 165.4 548.4 1,149.4 1,795.5 2,409.0

Credit/(Debit) Fair Value Change Account (10.3) 2.7 (2.0) (41.2) 32.3 49.1

Sub-total 2,180.8 2,163.1 2,541.3 3,103.5 3,826.3 4,463.6

Policyholders' Funds

Credit/(Debit) Fair Value Change Account (78.4) 31.1 61.3 53.6 398.1 567.1

Policy Liabilities 10,155.6 14,339.7 19,279.2 24,400.6 32,382.7 36,537.6

Provision for Linked Liabilities 27,794.6 32,735.7 42,140.2 42,753.8 50,806.5 52,938.6

Funds for discontinued policies 538.5 1,471.7 2,780.2 2,973.2 2,994.0 3,192.3

Sub-total 38,410.3 48,578.1 64,260.8 70,181.3 86,581.3 93,235.6

Funds for Future Appropriations 648.6 313.0 464.1 705.5 866.8 929.1

Total Sources of Funds 41,239.6 51,054.1 67,266.2 73,990.2 91,274.4 98,628.3

Investments

- Shareholders' 855.7 1,613.5 2,194.7 2,553.8 3,231.4 3,702.7

- Policyholders' 11,215.2 14,706.2 19,908.5 25,862.9 34,691.5 39,686.2

Assets held to cover Linked Liabilities 28,333.1 34,207.4 44,920.4 45,727.0 53,800.5 56,130.9

Loans 78.2 47.7 125.6 93.1 47.9 16.2

Fixed assets 281.8 289.5 352.5 347.4 353.5 344.0

Current Assets 1,153.9 1,410.6 1,806.9 1,960.3 2,971.8 2,346.9

Current Liabilities 1,521.9 1,455.8 2,042.3 2,554.1 3,822.2 3,598.7

Net Current Assets (368.0) (45.2) (235.4) (593.9) (850.4) (1,251.8)

Total Application of Funds 41,239.6 51,054.1 67,266.2 73,990.2 91,274.4 98,628.3

Revenue Account (Policyholders’ Account/Technical Account)

Premiums earned - Net 11,446.1 11,976.4 14,762.5 16,178.8 19,274.9 9,051.0

Income from Investments 2,542.7 5,073.1 12,249.3 1,790.6 11,140.6 5,278.3

Other Income 27.6 241.2 78.9 97.1 138.9 85.7

Total (A) 14,016.3 17,290.7 27,090.6 18,066.5 30,554.4 14,415.0

Commission 647.3 514.1 623.5 701.9 792.0 403.7

Operating expenses (Insurance Business) 1,216.0 1,280.5 1,488.8 1,871.8 2,385.3 1,282.6

Provision for Tax 50.9 151.6 119.3 174.6 152.0 22.4

Provisions (other than taxation) 0.0 27.5 (2.5) 3.2 6.3 (6.5)

Service Tax on charges 128.0 134.0 153.2 185.4 216.1 131.7

Total (B) 2,042.2 2,107.7 2,382.3 2,936.8 3,551.6 1,834.0

Benefits paid (Net) 3,902.8 4,661.9 8,162.4 8,176.9 9,842.2 5,485.6

Interim & terminal bonuses paid 18.7 32.9 71.4 65.1 158.2 94.7

Change in valuation of liability 7,414.9 10,058.4 15,652.5 5,928.1 16,054.8 6,482.5

Total (C) 11,336.5 14,753.2 23,886.3 14,170.1 26,055.2 12,062.9

Surplus/ (Deficit) (D) = (A) - (B) - (C) 637.6 429.8 822.1 959.6 947.6 518.1

Source: RHP

Ash

ika

Stoc

k B

roki

ng L

imit

edAshika Research - Equities

41008, Raheja Centre, 214, Nariman Point, Mumbai-400 021, Ph- 022 – 6611 1700, Extn. - 704 www.ashikagroup.com

(In Rs. Cr.) FY13 FY14 FY15 FY16 FY17 Q1FY18

Profit And Loss Account (Shareholders’ Account/Non-technical Account)

Transfer from Policyholders' account 390.0 765.4 670.9 718.3 786.3 455.8

Income from Investments 71.1 116.1 203.3 171.2 230.3 123.1

Other Income - - 0.0 10.6 0.1 13.3

Total (A) 461.2 881.5 874.2 900.0 1,016.7 592.2

Expenses (apart from insurance) 7.8 15.7 23.0 25.4 76.8 14.1

Contribution to the Policyholders' A/c 1.9 217.3 46.7 38.0 35.4 7.4

Provisions (Other than taxation) 0.0 5.9 (0.1) 3.3 (4.4) (0.3)

Total (B) 9.7 238.9 69.6 66.7 107.8 21.3

Profit / (Loss) Before Tax 451.5 642.5 804.6 833.4 908.9 570.9

Provision for Taxation 4.2 (82.8) 19.1 16.6 22.0 16.8

Profit / (Loss) After Tax 447.2 725.3 785.5 816.8 886.9 554.1

Diluted EPS (Rs.) 2.2 3.6 3.9 4.1 4.4 2.8

Receipts and Payments Account

Cash flow from Operations Activities 5,541.2 5,421.9 4,459.5 5,687.5 6,230.3 1,919.0

Cash flow from Investing Activities (4,959.4) (5,501.5) (3,514.5) (3,959.1) (5,175.2) (1,670.1)

Cash flow from Financing Activities - (116.7) (167.6) (212.4) (235.6) 65.8

Net increase/(decrease) in cash and cash equivalents 581.8 (196.3) 777.5 1,513.0 817.4 315.3

Cash and cash equivalents at the beginning of the year 1,188.2 1,770.0 1,573.7 2,351.1 3,864.1 4,681.5

Cash and cash equivalents at the end of the year 1,770.0 1,573.7 2,351.1 3,864.1 4,681.5 4,996.9

Statement of Premium Income

First year premiums 3,123.5 2,370.0 2,951.5 3,368.4 3,657.0 1,800.5

Renewal premiums 7,081.7 8,047.6 9,365.1 9,862.1 10,824.5 4,737.4

Single premiums 1,297.0 1,645.3 2,513.3 3,082.5 4,964.0 2,602.4

Total Premium 11,502.2 12,062.9 14,829.9 16,313.0 19,445.5 9,140.3

Source: RHP

Comparison with listed industry peers

Name of the companyEPS(Rs.)

NAV(Rs.)

P/E(x)

P/B(x)

RoNW(%)

Market Cap(Rs. Cr.)

HDFC Life 4.4 19.1 65.9 15.2 25.6 58,260

SBI Life 9.6 55.5 67.1 11.6 18.6 64,390

ICICI Pru 11.7 44.6 34.2 9.0 28.7 57,469

Source: RHP, Ashika ResearchNote: HDFC Life fig. are calculated based on higher price band. All Fig. are of FY17

Ash

ika

Stoc

k B

roki

ng L

imit

edAshika Research - Equities

51008, Raheja Centre, 214, Nariman Point, Mumbai-400 021, Ph- 022 – 6611 1700, Extn. - 704 www.ashikagroup.com

(In Rs. Mn.) FY15 FY16 FY17 Q1FY18

Key Performance Indicators

Total premium 148,299 163,130 194,455 91,403

Net premium 65,752 80,572 94,825 35,752

AUM 670,467 742,472 917,424 995,340

New business sum assured 1,815,761 2,714,860 3,887,575 1,965,449

Embedded value 88,882 102,325 124,705 140,114

VNB 5,915 7,393 9,225 4,782

VNB margin 18.5% 19.9% 22.0% 22.4%

EVOP 16,012 18,372 22,193 12,576

APE* 31,946 37,095 41,882 21,307

Total operating cost ratio 10.2% 11.6% 12.7% 14.2%

13th month persistency 73.3% 78.9% 80.9% 82.2%

61st month persistency 39.8% 50.0% 56.8% 55.4%

Operating Return on Embedded Value 22.9% 20.7% 21.7% 21.2%

Insurance profits 6,242 6,803 7,510 4,484

Profits after tax 7,855 8,168 8,869 5,541

Insurance profit as % of total profit after tax 79.5% 83.3% 84.7% 80.9%

Solvency ratio 196.1% 198.4% 191.6% 200.5%

Return on Net worth 35.2% 28.9% 25.6% 13.4%

Net Asset Value Per share (Rs.) 12.7 15.6 19.1 22.3

Number of lives insured (in millions) 5.7 15.4 20.9 11.7

Persistency Ratio

13th Month 73.3% 78.9% 80.9% 82.2%

25th Month 64.0% 67.5% 73.3% 74.4%

37th Month 65.1% 60.1% 63.9% 65.6%

49th Month 64.2% 63.4% 58.3% 59.3%

61st Month 39.8% 50.0% 56.8% 55.4%

Source: RHP

Ash

ika

Stoc

k B

roki

ng L

imit

edAshika Research - Equities

61008, Raheja Centre, 214, Nariman Point, Mumbai-400 021, Ph- 022 – 6611 1700, Extn. - 704 www.ashikagroup.com

Ashika Stock Broking Limited (“ASBL”) or Research Entity has started its journey in the year 1994 and is engaged in the business of broking services,

depository services, distributor of financial products (Mutual fund, IPO & Bonds). This research report has been prepared and distributed by ASBL in the

sole capacity of a Research Analyst (Reg No. INH000000206) of SEBI (Research Analyst) Regulations 2014. ASBL is a wholly owned subsidiary of Ashika

Global Securities (P) Ltd., a RBI registered non-deposit taking NBFC Company. Ashika group (details is enumerated on our website

www.ashikagroup.com) is an integrated financial service provider inter alia engaged in the business of Investment Banking, Corporate Lending,

Commodity Broking, Debt Syndication & Other Advisory Services.

There were no significant and material disciplinary actions against ASBL taken by any regulatory authority during last three years.

Disclosure

ASBL or its associates, its Research Analysts (including their relatives) may have financial interest in the subject company(ies). However, the said

financial interest is not limited to having an open stock market position in /acting as advisor to /having a loan transaction with the subject company(ies)

apart from registration as clients.

1) ASBL or its Research Analysts (including their relatives) do not have any actual / beneficial ownership of 1% or more of securities of the subject

company(ies) at the end of the month immediately preceding the date of publication of this report or date of the public appearance. However

ASBL's associates may have actual / beneficial ownership of 1% or more of securities of the subject company(ies).

2) ASBL or their Research Analysts (including their relatives) do not have any other material conflict of interest at the time of publication of this

research report or date of the public appearance. However ASBL's associates might have an actual / potential conflict of interest (other than

ownership).

3) ASBL or its associates may have received compensation for investment banking, merchant banking, and brokerage services and for other products

and services from the subject companies during the preceding 12 months. However, ASBL or its associates or its Research analysts (forming part

of Research Desk) have not received any compensation or other benefits from the subject companies or third parties in connection with the

research report. Moreover, Research Analysts have not received any compensation from the companies mentioned herein in the past twelve

months.

4) ASBL or their Research Analysts have not managed or co–managed public offering of securities for the subject company(ies) in the past twelve

months. However ASBL's associates may have managed or co–managed public offering of securities for the subject company(ies) in the past

twelve months.

5) Research Analysts have not served as an officer, director or employee of the companies mentioned in the report.

6) Neither ASBL nor its Research Analysts have been engaged in market making activity for the companies mentioned in the report.

Disclaimer

The research recommendation and information herein are solely for the personal information of the authorized recipient and does not construe to be

an offer documents or any investment, legal or taxation advice or solicitation of any action based upon it. This report is not for public distribution or use

by any person or entity, where such distribution, publication, availability or use would be contrary to law, regulation or subject to any registration or

licensing requirement. We will not treat recipients as customer by virtue of their receiving this report. The report is based upon the information

obtained from public sources that we consider reliable, but we do not guarantee its accuracy or completeness. ASBL shall not be in anyways responsible

for any loss or damage that may arise to any such person from any inadvertent error in the information contained in this report. The recipients of this

report should rely on their own investigations.

Name Designation Email ID Contact No.

Paras Bothra President Equity Research [email protected] +91 22 6611 1704

Krishna Kumar Agarwal Equity Research Analyst [email protected] +91 33 4036 0646

Partha Mazumder Equity Research Analyst [email protected] +91 33 4036 0647

Arijit Malakar Equity Research Analyst [email protected] +91 33 4036 0644

Kapil Jagasia Equity Research Analyst [email protected] +91 22 6611 1715

Tirthankar Das Technical & Derivative Analyst [email protected] +91 33 4036 0645

Research Team

Related Documents