Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

HDFC MUDARABAH SUKUK Issue No. 02

PROSPECTUS TO THE ISSUE HDFC MUDARABAH SUKUK ISSUE NO.2

Public offer of 150,000 Sukuk of Maldivian Rufiyaa (MVR) 1000 per Sukuk, to the

total value of MVR 150,000,000 (One Hundred and Fifty Million), with a semi-annual

profit share in the ratio 65:35

Issuer/Offeror

HOUSING DEVELOPMENT FINANCE CORPORATION PLC.

Issue date of the prospectus 06/07/2017

Opening date for application/subscription 24/08/2017

Closing date for subscription 18/10/2017

BANKERS

Maldives Islamic Bank

Bank of Maldives Plc

Bank of Ceylon

Registered Address: 4th Floor, H.Mialani, Sosun Magu, Male', Rep. Of Maldives.

Telephone: 3334666 / 3338810 // 3315897 Fax: 3315138

Email: [email protected]

SHARIAH ADVISOR

Dr. Aishath Muneeza

LEGAL COUNSEL

Mazlan & Murad Law

Associates

AUDITORS

KPMG

HDFC Plc. [incorporated as a state owned enterprise on 28 January 2004 by a Presi-

dential Decree under the Companies Act, Law No: 10/96 ,registered as a public com-

pany on the 9th of February 2006 and privatized with the signing of a shareholders’

agreement for privatization between the GOM (49%), IFC (18%), ADB (18%) and

HDFC-Investments Ltd.-India (15%) on July 23, 2008 and incorporated in the Repub-

lic of Maldives as a Privatized Company- Registration Number C-107/2006]

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

HDFC PLC. PROSPECTUS TO THE ISSUE

HDFC MUDARABAH SUKUK

Issue no.2

Published: July 2017

Housing Development Finance Corporation Plc.

4th Floor, H. Mialani

Sosun Magu

Male’, Republic of Maldives

Tel: 3334666

Fax: 3315138

Email: [email protected]

www.hdfc.com.mv

HDFC MUDARABAH SUKUK Issue No. 02

This Issue Prospectus has been drawn up in accordance with

the laws of Maldives. The main aim of this Prospectus is to pro-

vide all the information necessary for the investors to make the

right decision regarding this Sukuk Issue. Each investor must

study this Prospectus carefully in order to decide whether it is

appropriate to invest in it by taking into consideration all the

factors relating to the status and circumstances. It is solely the

responsibility of the Issuer to include any essential and accu-

rate information or data in this Prospectus.

If any investor is in doubt about the contents of this document

he/she should consult a person licensed under the Securities

Act who specializes in advising on the acquisition of shares and

other securities.

Mudarabah Sukuk

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

HDFC MUDARABAH SUKUK Issue No. 02

Table of Contents

1. Introduction 10

1.1. Presentation of Financial Information 11

1.2. Law & Exclusive Jurisdiction 11

1.3. Absolute Responsibility 11

2. Responsibility Statement 12

3. Report by the directors to confirm due inquiry 13

4. Notice to investors 14

5. About the prospectus 14

6. Details of the Sukuk offered 15

7. Mudaraba Sukuk Structure 18

8. Terms & Conditions 19

8.1. Representation and Warrants 20

8.2. Participation in Profits 20

8.3. Loss 20

8.4. Taxation 21

8.5. Management and Control 21

8.6. General Covenants of Mudarib 21

8.7. Transfers 22

8.8. Limited Recourse 22

8.9. Negative Pledge 22

8.10. Termination 22

8.11. Meeting of Sukuk Holders 22

8.12. Force Majeure 22

9. Eligible participants 23

10. Procedure for application 24

10.1. Subscription List 24

10.2. Mode of payment 24

10.3. Dematerialized offering 25

10.4. Allotment 25

10.5. Acceptance and refunds 25

10.6. Payment of Money at Redemption 25

10.7. Rejection of applications 26

10.8. Underwriting and issue costs 26

10.9. Paying Agent 26

11. The Project 27

12. Security 28

13. Listing 28

14. Rights of the Sukuk holder 29

15. The Issuer 29

15.1 HDFC Plc. 29

15.2 Company Overview 30

15.3 Board, Advisory Committees and Senior Management 31

16. Company’s Growth 42

17. HDFC’s Corporate Governance 50

18. Inspection of documents 51

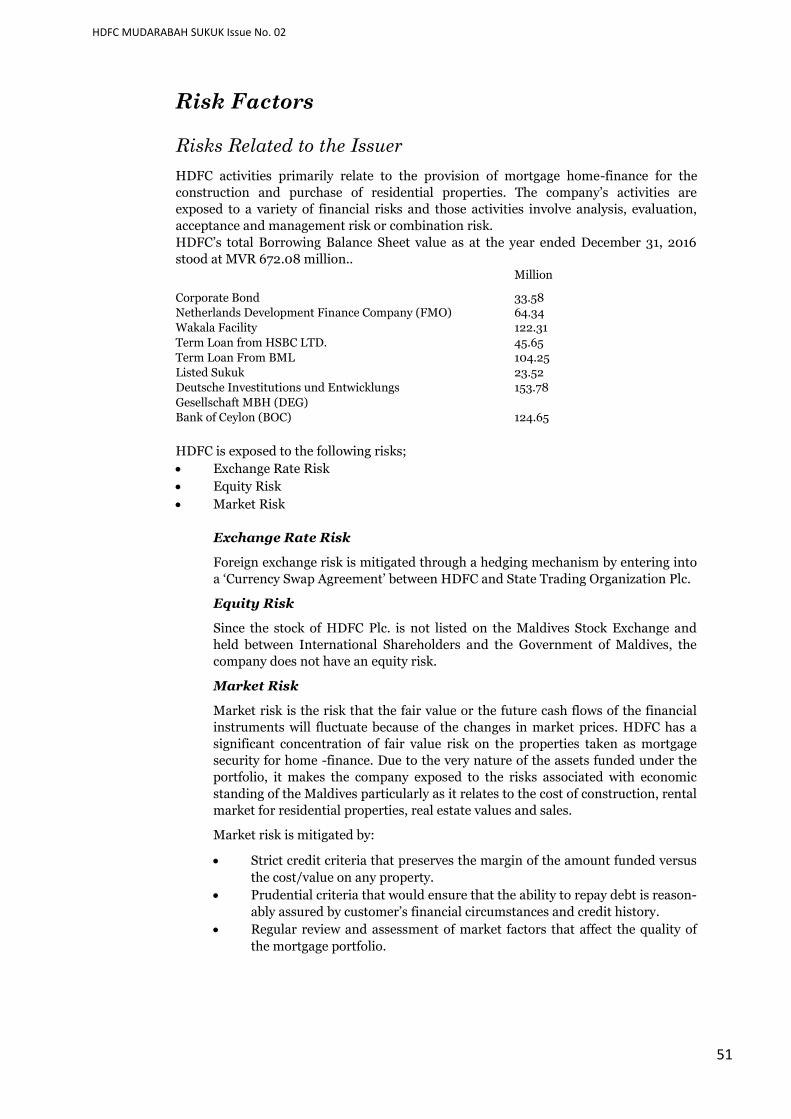

19. Risk Factors 52

20. Material outstanding indebtedness in relation

to the issue 55

21. Litigation and disputes 55

22. Details of shareholding in the company 55

23. Staff Details 55

24. Disclosure of material contracts & conflict of

interest of directors 56

25. Annexes

25.1. Annex - 1. Legal due diligence

25.2. Annex - 2. Accountant’s report

25.3. Annex - 3. Extract of Articles of Association

25.4. Annex - 4. Performance Guarantee Letter by HDFC

25.5. Annex - 5. Audited financial statements for the year ended 31.12.2016

25.6. Annex - 6. Extract of Corporate Governance Code

25.7. Annex - 7. Declaration of Shariah Advisor & Endorsement of HDFC Shariah Committee

25.8. Annex - 8. Glossary of Islamic Financial Terms

HDFC MUDARABAH SUKUK Issue No. 02

9

Prospectus to the Issue HDFC MUDARABAH SUKUK ISSUE NO.2

Introduction

We, at HDFC Plc. Maldives believe that safe and secure housing is

the no.1 priority for the progressive Maldivian society. Therefore, we

wish to offer you an investment opportunity to share in our mission

to make every Maldivian’s dream home a reality through innovative

housing finance products.

Housing Development Finance Corporation (HDFC) Plc. was estab-

lished as a specialized Housing Finance Company in the Maldives in

2004 under state ownership and privatized in July 2008 through a

Public Private Partnership with a joint foreign investment of 51%

shares held by International Finance Corporation (IFC) of the World

Bank Group, Asian Development Bank (ADB) and HDFC Invest-

ments of India. HDFC Plc. is the only specialized Housing Finance

Institution in the Republic of Maldives.

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

10

Presentation of Financial Information

The only sources of Company-specific financial infor-

mation used in this Prospectus are audited financial

statements of the Company prepared in accordance with

the Companies Act (10/96) and International Financial

Reporting Standards (IFRS) except for the financial

years 31 December 2007 and 31 December 2008, which

were prepared with a modification of the requirements of

IAS 39 - Financial Instrument: Recognition and meas-

urement in respect of loan loss provisioning by MMA’s

circular No- GM-9/96 dated 25 April 1996 on Credit Risk

Grading System and Loss Provision Requirements. The

financial statements for years ended December 31, 2004

to 2008 were audited by Ernst & Young Chartered Ac-

countants and by PricewaterhouseCoopers Chartered Ac-

countants for years ended December 31, 2009-2012. For

years ended December 31, 2013-2016, KPMG audited the

financial statements.

Law and Exclusive Jurisdiction

This Prospectus and the Sukuk shall be governed by and

construed in accordance with the laws and regulations of

the Maldives. Each of the parties hereto irrevocably

agrees that the courts in the Maldives shall have exclu-

sive jurisdiction to hear and determine any suit, action or

proceeding, and to settle any disputes, which may arise

out of or in connection with this Prospectus and the

Sukuk, and for such purposes irrevocably submits to the

jurisdiction of such courts. However, before going to the

Court, the dispute shall be first taken to an arbitration

proceeding.

Absolute Responsibility

Approval to issue these securities has been obtained from

the Registrar of Companies under the companies Act

(10/96). Further HDFC has also obtained consent from

the Capital Market Development Authority (CMDA) to

issue these securities under the Securities Act (2/2006).

However, neither the Registrar of the Companies nor the

Capital Market Development Authority takes any respon-

sibility for the accuracy of any statement made thereof or

for the financial soundness of the Company or the value

of securities concerned. HDFC Plc. takes absolute re-

sponsibility for the accuracy of the information disclosed

in the document.

HDFC MUDARABAH SUKUK Issue No. 02

11

Responsibility Statement

Name Address Passport/ID No

Designa-tion

Signature

Ms. Renu Sud Karnad

HDFC Limited Ramon House 169 Backbay Recla-mation HT Parekh Marg Mumbai 400 020, India

Z 1877392 Nominee Director, –Non Exec-utive

Mr. Conrad D’Souza

HUL House, 6th Floor, A Wing, HT Parekh Marg, 165-166, Backbay Rec-lamation, Churchgate, Mum-bai 400 020, India

Z 2480661 Chairman 30th April 2017 on-wards

Mr. Gaurav Agarwal

PO BOX 939505, Villa 6, Street 8, Springs 14, Dubai, UAE

M2306225 Director—Non– Ex-ecutive

Mr. Asif Cheema

Oakwood Preimi-er, Suite 2211, 17 ADB Avenue, Orti-gas Center, Pasig City 16000, Philip-pines

AG4154424 Alternate Director, Non-Executive

Mr. Nihal Senanayake Welikala

9/1 Hyde Park Res-idencies, 79 Hyde Park Corner, Co-lombo 2, Sri Lanka

N2773623 Director, Non—Executive

Mr. Ismail Ali Manik

HDFC Plc H. Mialani Sosun Magu Male’ Maldives

A045786 Chairman Until 19th April 2017

Mr. Mo-hamed Mauroof Jameel

M. Dhoores, Orchid Magu Male’ Maldives

A039093 Director, Non– Ex-ecutive

Ms. Ra-heema Saleem

HDFC Plc H. Mialani Sosun Magu Male’ Maldives

A033318 Managing Director—Executive

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

12

Report by the directors to confirm due inquiry

We, the undersigned as Directors of the Company hereby confirm performance of due in-

quiry in relation to the interval between 31st December 2016 (the date to which the last ac-

counts have been made up) and 06th July 2017 (the date which prospectus is being issued)

that:

a. The business of the Company has in our opinion been satisfactorily main-

tained;

b. There have not, in our opinion, arisen since the last Annual General Meet-

ing of the Company any circumstances adversely affecting the trading or

the value of the assets of the Company or any of its subsidiaries;

c. The current assets of the Company and of its subsidiaries appear in its

books at values which are believed to be realizable in the ordinary course

of business;

d. There are no contingent liabilities by reason of any guarantees given by

the Company or any of its subsidiaries; or

e. There are, since the last annual report, no changes in published reserves

or any unusual factors affecting the profit of the Company and its subsidi-

aries.

Name Designation Signature

Ms. Renu Sud Kar-nad

Nominee Director, Non-Executive

Mr. Conrad D’Souza

Alternate Director, Non-Executive

Mr. Gaurav Agarwal

Director, Non - Executive

Mr. Asif Cheema

Alternate Director, Non-Executive

Mr. Nihal Sena-nayake Welikala

Director, Non-Executive

Mr. Ismail Ali Manik

Chairman—Non– Executive

Mr. Mohamed Mauroof Jameel

Director, Non-Executive

Ms. Raheema Saleem

Managing Director—Executive

HDFC MUDARABAH SUKUK Issue No. 02

13

Notice to investors

The Board of Directors of Housing Development Finance Corporation

Plc. (HDFC PLC) on May 21, 2016 passed a resolution approving the

company to raise MVR 150 million through a Sukuk Issuance to the pub-

lic, financial institutions, public corporations, private entities and other

institutions.

About the prospectus

This Issue Prospectus has been drawn up in accordance with the laws of

Maldives. The main aim of this Prospectus is to provide all the infor-

mation necessary for the investors to make the right decision regarding

this Sukuk Issue. Each investor must study this Prospectus carefully in

order to decide whether it is appropriate to invest in it by taking into

consideration all the factors relating to the status and circumstances. It

is solely the responsibility of the Issuer to include any essential and accu-

rate information or data in this Prospectus.

If any investor is in doubt about the contents of this document he/she

should consult a person licensed under the Securities Act who specializes

in advising on the acquisition of shares and other securities.

Invitation to Subscribe

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

14

Details of the Sukuk offered

The following summary should be read in conjunction with, and is

qualified in its entirety by the detailed information elsewhere in the

Prospectus. Prospective investors in this Sukuk should see the section

in the prospectus under “Risk Factors” that discusses certain factors

that should be considered in connection with an investment in the

Sukuk.

Issuer: Housing Development Finance Corporation Plc.

Issue Price: MVR 1000.00 per Sukuk

Issue Date: 06th July 2017

Subscription Opening: 24th August 2017, 0900hrs

Subscription Closing: 18th October 2017, 1300hrs

Settlement Date: Date of Subscription

Allotment: Within 05 business days from the closure of sub-

scription

Total Issue:

MVR. 150,000,000.00 (One Hundred and Fifty

Million Rufiyaa) (150,000) [One Hundred and Fif-

ty Thousand] Sukuk)

The Project: To fund shari'ah compliant mortgage housing fi-

nance operations under HDFC Amna

Tenure / Maturity

Date: Ten (10) years from the allotment date

Profit: 65% of the gross profit distributed to Sukuk hold-

ers

Profit Payment Dates: Every six months after the date of allotment, until

the Maturity Date

Next Business Day: The first day following a non-working day.

Type of Issue: Dematerialized

MVR1000S U K U K

HDFC MUDARABAH SUKUK Issue No. 02

15

Details of the Previous Sukuk offered

Issuer: Housing Development Finance Corpora-

tion Plc.

Issue Price: MVR 500.00 per Sukuk

Issue Date: 11 September 2013

No. of sukuk issued 45,132

No. of sukuk holders 467

Total value of sukuk issued 22,566,000

Total investments in housing facilities 22,566,000

Profit sharing ratio 65 : 35

Tenure (years) (Maturity Date) 10

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

16

HDFC MUDARABAH SUKUK Issue No. 02

17

Mudaraba Sukuk Structure

The structure of this Sukuk issuance is based on the Shariáh principle of

Mudaraba (Money Management). In the Mudarabah concept, one party will be

providing the capital (the Rabb al Maal) and the other party will be managing

the capital (the Mudarib) in a proposed Shariáh compliant project. For the pur-

poses of this Sukuk, the Sukuk holders are collectively the providers of capital

(the Rabb al Maal) that purchase Sukuk certificates from the Issuer. HDFC Plc

is the manager of the capital (the Mudarib). The project managed by the

Mudarib is known as the Mudaraba.

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

18

8 - Terms & Conditions

All the relevant requirements and approvals from the regulatory authori-

ties in the Republic of the Maldives in relation to the issue of this Sukuk

have been obtained. Each Sukuk Certificate evidences an undivided own-

ership interest in the investment made, subject to the terms herein and

has a limited recourse obligation of the Issuer. Each Sukuk Certificate

ranks pari passu, without any preference or priority, with all other Sukuk

Certificates. Proceeds from the Mudaraba are the sole source of payments

to Sukuk holders pursuant to the Certificates. The Sukuk Certificates do

not represent an interest in the Issuer or any of its affiliates. A meeting

with the Sukuk holders can be convened at the discretion of the Issuer to

discuss matters regarding the Mudaraba.

By purchasing Sukuk certificates, the investors/Sukuk holders agree to

accept and abide by the following terms and conditions:

8.1 Representation & Warranties

The Mudarib hereby represents and warrants to the Rabb al Mal, as fol-

lows:

a. The Mudarib possesses all necessary powers and licenses to

conduct its present business and the Project.

b. The Mudarib Information provided under ‘The Issu-

er’ (section 15) is true and correct.

c. The Mudarib is experienced and knowledgeable in all busi-

ness matters relating to the Project.

d. The Mudarib has prepared with all due care the information

provided under ‘The Project’ on his/her experience and

knowledge and has completed all reasonable investigation to

assure that such are true and correct and disclose all facts

relevant to the Rabb al Mal’s evaluation of the Project.

e. The Mudarib Financials are true and correct according to

generally accepted accounting principles consistently ap-

plied accurately representing the Mudarib’s financial status

on the dates and the profit and loss for the periods indicat-

ed, and no liabilities, fixed or contingent exist at the indicat-

ed dates other than as appear in the Mudarib Financials;

f. All transactions for the purpose of which this Sukuk proceed

will be utilized are Shariah-compliant mortgage financing;

and

g. All regulatory, governmental and corporate approvals and

consents (including exchange control approvals) for the due

execution and delivery of, and performance of the work in-

tended to be carried out.

HDFC MUDARABAH SUKUK Issue No. 02

19

8.2 Participation in profit

a. The participation by Sukuk holders in the profit generated by the Mudaraba will be in

accordance with the following ratio:

i. 35% of the profit will be for Management Services and payable to the

Mudarib.

ii. 65% of the profit will be payable to the Rabb al Mal collectively.

b. Profit will be distributed out of the gross profit generated from the sukuk fund.

c. The profits generated by the Mudaraba will be paid by the Mudarib to Rabb al Maal col-

lectively twice every calendar year; until the earlier of the Termination Date and the Ma-

turity Date.

d. Profit calculation date is Six months from the date of allotment, to be payable to Rabb-Al

Mal not less than One month from the profit calculation date.

e. Profit amount to be distributed will be calculated using the formula below:

Distributable Profit = P × r × w

Where:

P = Profit from the Sharia Complaint Housing Mortgage Facilities

r = Profit Sharing Ratio

w = Weighting Factor

f. Profit from Sharia Compliant Housing Mortgage Facilities is calculated using the formu-

la below:

P = RI - TI

Where:

RI = Return on Investment received from Sharia Compliant Mortgage housing as on a

monthly basis. (ie - Revenue)

TI = Total Investment (ie. Principal Amount)

8.3 Losses

a. 100% of any losses in the Project will be borne by the Rabb al Mal except in case of negli-

gence, breach of obligation or willful default by the Mudarib.

b. The Mudarib will receive no compensation for his Management Services, and will be lia-

ble for any loss in the Project if it is proven that he/she has breached his/her obligations

or is proven to be failing in the discharge of his/her obligations under these terms.

c. In the event of the Project showing losses during the continuity of this Sukuk issuance,

the Mudarib shall forthwith give notice of such losses to the Rabb al Mal together with all

accounts and details pertaining thereto and such other information and records as may

be required by the Rabb al Mal.

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

20

8.4 Taxation

On behalf of the Project, the Mudarib shall be liable for and shall punctual-

ly and regularly pay all taxes, duties and other charges relating to the Pro-

ject’s business and operations.

8.5 Management & Control

The complete management and control of the Project is exclusively vested

in the Mudarib and the Mudarib shall be solely responsible for the man-

agement and control of the Project.

8.6 General Covenants of Mudarib

THE MUDARIB covenants to the the Rabb al Mal that the Mudarib shall:

a. promptly give notice to the Rabb al Mal of any change in the

information disclosed in the section ‘The Issuer’.

b. undertake the Management Services such as providing Islam-

ic financing facilities to third parties with due care and all rea-

sonable commercial diligence expected of an experienced

businessman to ensure the success of the Project according to

the description of The Project.

c. utilize the Project assets exclusively for purposes of the Pro-

ject

d. collect all receivables from third parties arising from the Pro-

ject or the transfer of Project assets or other documents re-

quiring payment from third parties directly to the Account

opened specifically for that purpose.

e. maintain all Project assets in the name of the Mudarib, but

physically segregated from other assets of the Mudarib and

free and clear of all liens and encumbrances except those in

favour of the Rabb al Mal.

f. maintain true and correct books of account relating to the

Project together with all invoices, records contracts and all

other documentation.

g. supply to the Rabb al Mal any information, material or docu-

ment relating to the Project or to Mudarib’s financial status,

and grant access to the Rabb al Mal or its agents to all books

and materials relating to the Project and to the Mudarib’s fi-

nancial statements.

h. immediately disclose in writing to material or document the

Rabb al Mal any business factors of which the Mudarib be-

comes aware and which might adversely affect the success of

the Project.

i. not effect directly or indirectly any transaction on behalf of

the Project in which the Mudarib or any shareholder of the

Mudarib, if a corporation, is interested directly or indirectly

without consent of the Rabb al Mal.

HDFC MUDARABAH SUKUK Issue No. 02

21

J. under its sole responsibility, conduct the Project in conformi

ty with all applicable civil and criminal laws.

K. conduct the Project without violation of the principles of Is

lamic Shariah.

8.7 Transfers

The Issuer makes no representation that the Sukuk may at any time lawful-

ly be sold in compliance with any applicable registration or other require-

ments in any jurisdiction, or pursuant to any exemption available thereun-

der, or assumes any responsibility for facilitating any such sale. Persons

into whose possession this Prospectus or any Sukuk may come must in-

form themselves about, and observe, any applicable restrictions on the dis-

tribution of this Prospectus and the offering and sale of the Sukuk.

8.8 Limited Recourse

By subscribing for or acquiring the Sukuk, Sukuk holders acknowledge that

they will have no recourse to any of the assets of the Issuer (other than the

Mudaraba) to the extent that the Issuer fulfils all of its obligations under

Sukuk. The net proceeds of the realisation of the Mudaraba may not be

sufficient to make all payments due in respect of the Sukuk. If, following

the distribution of such proceeds, there remains a shortfall in payments

due under the Sukuk, no Sukuk holder will have any claim against the Issu-

er to the extent the Mudaraba has been exhausted.

8.9 Negative Pledge

For so long as any payment remains outstanding under any Sukuk, the Is-

suer undertakes not to create or have outstanding any mortgage, charge,

lien, pledge or other security interest upon the whole or any part of the

Mudaraba.

No Sukuk holder can declare anything except at the event of default

8.10 Termination

a. Subject to other provisions of these terms, it is agreed that

upon full payment on Termination Date, if proceeds have

been received, the Mudaraba shall be redeemed.

b. The occurrence of an event of default would entitle the Sukuk

holders to declare the Sukuk immediately due and payable

without any provision for period of grace, while provision for

remedy may be negotiated to the extent appropriate.

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

22

c. An event of default here means:

(i) No payment is made on the payment of any Periodic Distribution

Amount on the due date mentioned on 8.2 (d) and, such failure to

make a payment continues for a period of three months (90 Calen

dar Days) with out any lawful justification;

(ii) the Issuer is (or is deemed by law or a court to be) insolvent or

bankrupt or unable to pay its debts or a moratorium is agreed or

declared or comes into effect in respect of all or any part of the

debts of the Issuer;

(iii) It is or will become unlawful for the Issuer to perform or comply

with any one or more of its obligations under the Sukuk;

(jjj) The default date is the date where an event of default occurs as

stated in subsection C of this article.

d. While the amount invested by the Rabb al Mal must be repaid on the ma-

turity date, mentioned above, the accounts of the Mudarabah will be

drawn up within 15 days thereof and the agreed share of the Rabb al

Mal’s profit will be paid promptly.

e. The Capital amount will be paid in no less than 30 days after the ac-

counts of Mudarabah have been drawn upon maturity date.

8.11 Meeting of Sukuk holders

The Sukuk holders may convene meetings of Sukuk holders to consider any matter

affecting their interests, including the sanctioning by Extraordinary Resolution of a

modification of the Mudaraba Sukuk, those Conditions which are also approved by

the Issuer. Such a meeting may be convened by the Issuer and shall be convened by

the Issuer upon the request in writing of Sukuk holders holding not less than one-

tenth of the aggregate Nominal Amount of such of the Mudaraba Sukuk as are current

as of such date. The quorum at any meeting convened to vote on an Extraordinary

Resolution will be two or more Persons holding or representing at least half of the

aggregate Nominal Amount of such of the Mudaraba Sukuk as are current as of such

date or, at any adjourned meeting, one-quarter of the aggregate Nominal Amount of

such of the Mudaraba Sukuk as are current as of such date.

An Extraordinary Resolution requires the affirmative vote of at least one more Sukuk

holder holding more than half of those represented in the relevant meeting in order

for it to be passed. Any Extraordinary Resolution duly passed at any such meeting

subject to Sukuk regulations shall be binding on all Sukuk holders, whether present or

not.

8.12 Force Majeure

a. Any delays in or failure by a Party hereto in the performance of the obli-

gations hereunder if and to the extent it is caused by the occurrences or

circumstances beyond such Party’s reasonable control, including but not

limited to, acts of God, fire, strikes or other labour disturbances, riots,

civil commotion, war (declared or not) sabotage, any other causes, simi-

lar to those herein specified which cannot be controlled by such Party.

HDFC MUDARABAH SUKUK Issue No. 02

23

b. The Party affected by such events shall promptly inform the other

Party of the occurrence of such events and shall furnish proof of details

of the occurrence and reasons for its non-performance of whole or part

of these terms agreed. The Parties shall consult each other to decide

whether to terminate these conditions or to discharge part of the obliga-

tions of the affected Party or extend its obligations on a best effort and

on an arm’s length basis.

9 - Eligible participants

This issue is open to any individual and any legal entity that is established ac-

cording to the laws of the Maldives. This would include Public Limited Liabil-

ity Companies, Commercial Banks, Pension Authority, Public Corporations

and Insurance Companies.

All supporting documents accompanied with the application should be valid;

this includes copies of national identity cards, passport copies, birth certifi-

cates validating the name and date of birth of the applicant.

For Individuals:

A copy of the National Identity Card (only for Maldivians).

A copy of the birth certificate for minors not having their

national identity card.

For Legal Entities:

A copy of the Certificate of Registration.

A board resolution authorizing the investment in HDFC

MUDARABAH SUKUK- Issue No. 2 and the opening and

operation of an account including appointing authorized

signatory of the account with MSD.

A copy of the Memorandum & Articles of Association and

bylaws that govern the operations of the entity, if any

A copy of the National Identity Card of the authorized sig-

natories

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

24

Procedure for application

Applications must be made on the Application Form supplied with this Prospectus.

Application can be also be downloaded from our website http://www.hdfc.com.mv.

Applicants using downloaded forms are requested to inspect the Prospectus, which is

on the company website whilst hard copies will be available at HDFC PLC’s Head Of-

fice. All the Application should be submitted directly to HDFC PLC at the following

address;

Housing Development Finance Corporation Plc

4th Floor, H. Mialani

Sosun Magu

Male’, Republic of Maldives

Subscription List

The subscription list will open at 0900 hours on 24 August 2017 and remain open for

35 market days and close at 1300 hours on 18 October 2017. The prospectus will be

available upon issuance for 33 market days before subscription will be opened. HDFC

reserves the right to close the issue prior to the closing date in the event of an oversub-

scription following due notice to the public.

Duly completed Application Forms will be accepted by HDFC PLC at its office of busi-

ness. The Prospectus and Application Forms will be made available 14 (fourteen) mar-

ket days prior to the opening of the subscription list.

Subscription via online applications

Online applicants can apply for the offer by accessing the online electronic application

system in https://infinity.depository.mv/

Special consideration must be given to strictly follow the instructions on the website in

filling the online application form.

Mode of payment

Each application should accompany a check/cash/pay-in-slip for the full

payment of the Sukuk applied. The amount payable should be calculated

as per the following formula:

V = Sn

Where V = full payment of Sukuk applied for

S = price per Sukuk (i.e. MVR 1000)

n = number of Sukuk applied for

Payments should be made by check, crossed as “Account Payee Only” and

made payable to Housing Development Finance Corp. PLC or cash

to Housing Development Finance Corp. PLC (7770000007011, Bank

of Maldives Islamic, 9901-01-48000372-101, Maldives Islamic Bank),

where the pay-in slip should be attached to the application form sent to

HDFC head office.

HDFC MUDARABAH SUKUK Issue No. 02

25

All such subscription payments will be deposited to HDFC -

Sukuk 2 account on the ‘Subscription Closing’ date and HDFC Plc

has all the rights to reject the application if a check is not honored

on its first presentation.

An acknowledgement receipt will be issued for the checks/cash/

pay-in-slip received and Application Forms accepted.

Application Forms and the accompanying checks and cash pay-

ments which are incomplete in any way and/or not in accordance

with the terms, conditions and instructions set out in this Pro-

spectus, and application forms which are illegible will be rejected.

Dematerialized offering

This offering of Sukuk will be carried out in a dematerialized environment.

This means that the Sukuk certificates issued by HDFC Plc. will be deposited

with the Maldives Securities Depository (MSD). A record of each Sukuk holder

and Sukuk held shall be maintained by MSD, and statements shall be issued

upon request from time to time to evidence the holding. An MSD account

opening form is enclosed with each Sukuk application form, and must be per-

fected by every applicant subscribing to the Sukuk Issue.

Allotment

The Sukuk will be allotted within 05 (five) business days from the

‘Subscription Closing’ date. All the applications shall be considered for allot-

ment in order of first come first serve basis. The project is for Mortgage Hous-

ing Financing Facilities of HDFC Amna and will continue even if the target

amount is not raised. Over subscription of shares will be allotted on a pro rata

basis.

Acceptance and refunds

Where an application is not accepted in full or in part, the balance of the appli-

cation money, shall be refunded to the applicant within 15 (fifteen) working

days from the closure of the issue. The HDFC PLC reserves the right to accept

subscriptions in full or in part from any subscriber.

Payment of Money at Redemption

The Sukuk holder, whose ownership of the Sukuk is registered

with the MSD, will receive half yearly profit shared in accordance

with the pre-agreed profit sharing ratio.

Profit will only be deposited to the bank account given in the ap-

plication form. The bank account should be in his/her/entity’s

name and should be in a local bank in Maldives Rufiyaa (MVR).

This account must be live and operational all the time during the

tenure of the Sukuk.

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

26

After the Sukuk allotment, MSD should be contacted for any update to the partic-

ulars provided earlier.

If any Sukuk holder fails to update his/her particulars or refuses to claim and re-

ceive payment of the profit payable to such Sukuk holder, the amount due to such

Sukuk holder shall be deposited by the Paying Agent to a separate bank account at

the end of thirty days after the date of maturity and shall be paid to the holder of

such Sukuk when a claim is lodged no later than six months from the date of final

maturity.

No sukuk, partly or in full, may be redeemed prematurely. It will be redeemed in

full upon maturity.

Rejection of applications

Incomplete applications will be rejected at HDFC’s absolute discretion.

Late Applications (delivered after the closure of the Subscription Period) will be

rejected.

Online Applications which does not conform with the instructions and conditions

set out will be deemed incomplete and be rejected.

Applications considered as ‘oversubscription’ will be rejected and refunded within

15 working days following the closure of the issue.

All applications rejected after having received the payments, will be refunded 15

working days after the closure of subscription period.

The Management and Board of Directors reserve the right to refuse or accept any

application owing to a valid reason.

Underwriting and issue costs

No underwriter has been appointed for this series of Sukuk issue.

All expenses and fees attributable to this series of Sukuk issue, including legal fees, authority

fees, advisory charges, Paying Agent fees and bank charges will be borne by the Issuer.

Paying Agent

Maldives Securities Depository Company Pvt. Ltd. will be appointed as the Paying Agent whose

address is given below;

Maldives Securities Depository Company Pvt Ltd

H. Gadhamoo Building, 3rd Floor,

Boduthakurufaanu Magu,

Male’, Maldives.

Tel: (+960) 3307878, Fax: (+960) 3305034,

Email: [email protected]

Websites: www.mse.com.mv, www.msd.com.mv

HDFC MUDARABAH SUKUK Issue No. 02

27

The Project

The funds raised by the issue of Sukuk will be utilized to give Shariah

compliant mortgage financing facilities under the HDFC Islamic window

HDFC AMNA and no amount of the proceeds will be utilized for any oth-

er purpose other than what is stated in the prospectus. More infor-

mation about this operation can be obtained through the following link:

<http://www.hdfc.com.mv/hdfc/index.php/islamic-finance/amna>.

HDFC Amna was launched in May 2012

in a ceremony held at Nasandura Palace

Hotel, Maldives. “Amna” is an Arabic

word which refers to “security”. Amna is

stated in al Quran to connote peaceful,

protected and secure. HDFC Amna is

neither a separate company detached

from HDFC nor a subsidiary of HDFC.

HDFC Amna is simply and solely an Is-

lamic window of HDFC offering Islamic

home financing facilities to the custom-

ers under the existing license of HDFC to

offer home financing products to Maldiv-

ians in an affordable manner.

This Islamic window can be defined as a department of a conventional

financial institution offering Islamic financial services. Hence, HDFC

Amna will operate as a department of HDFC. HDFC Amna will observe

the following standards to achieve Shari'ah compliance:

Complete Segregation of Funds

Shari’ah Supervisory Board (Shari’ah Committee)

Products fully based on Islamic Concepts including the contracts

Management in accordance with Islamic principles

HDFC – Amna has started its operation in December 2012. As at the

ended of the financial year 2016, HDFC Amna has a housing portfolio of

MVR247 million.

The Sukuk Issue is part of HDFC PLC’s intention to leverage its capital

base with a diversified portfolio of Shariah compliant debt instruments

that would include local investors as well.

Another objective of issuing Sukuk to the public by HDFC is to create a

secured low-risk long-term Shariah compliant investment avenue for the

local takaful /insurance companies, pension authority, government cor-

porations, companies and the members of public. HDFC has embraced

principles of sustainable and responsible finance in all aspects of opera-

tions. HDFC Sukuk with a listing in the Maldives Stock Exchange will

increase vibrancy in the market by giving opportunities for varying in-

vestors to take part in the national housing development endeavor.

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

28

Security

The purpose of this Sukuk as mentioned is for Sharia Compliant Mort-

gage Housing Facilities, hence the fund is secured by underlying securi-

ty/assets of the facilities it is invested in. HDFC acknowledges that the

Sukuk offered under this prospectus is not given a third party guarantee.

However, Kafalah Performance guarantee from HDFC Plc. is given to

this offer in Annex 4.

Listing

The Sukuk offered under this prospectus will be eligible for trading in

the Maldives Stock Exchange. Application for listing has been made.

Rights of the Sukuk holder

The Sukuk Holder will be entitled to a half yearly profit in accordance

with the terms given in this prospectus. In the event the Sukuk holder

needs liquidity before the Sukuk’s date of maturity, the Sukuk will be

eligible for trading in the Maldives Stock Exchange and the holder has

the right to transfer ownership through secondary markets.

HDFC MUDARABAH SUKUK Issue No. 02

29

Issuer

Housing Development Finance Corporation Plc.

Our Vision

Our vision is to provide decent and affordable homes in a safe and healthy en-

vironment, and work towards uplifting the living standards of all Maldivians by

becoming the market leader for financial services in the Maldives.

Our Mission

Our mission is to offer financial and social strength to all Maldivians by provid-

ing home finance and other savings and investment products managed profes-

sionally and profitably to the highest International Standards and to the com-

plete satisfaction of all stakeholders.

Our Pledge

HDFC would strive hard and explore all avenues to:

Provide a solution to every single customer.

Process home-finance applications to the highest professional

standard to give a speedy and effective service.

Manage all aspects of customer relationship with due care, com-

munication and sensitivity to ensure 100% home-finance perfor-

mance.

To conduct all affairs as a responsible corporate citizen with good

governance, accountability and transparency.

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

30

Company Overview

Housing Development Finance Corporation (HDFC) Limited was incor-

porated as a state owned enterprise on 28 January 2004 by a Presiden-

tial Decree under the Companies Act, Law No: 10/96. The commercial

operations commenced on March 29, 2004. HDFC was established with

technical assistance from the World Bank, and initially all shares were

held by the Government of Maldives (GOM).

HDFC Plc. was registered as a public company on the 9th of February

2006.

The HDFC Plc. was privatized with the signing of a shareholders’ agree-

ment for privatization between the GOM, IFC, ADB and HDFC-

Investments Ltd.-India on July 23, 2008. This Public Private Partner-

ship has a joint foreign investment in 51% shares by International Fi-

nance Corporation (IFC) of the World Bank Group, Asian Development

Bank (ADB) and HDFC Investments Ltd of India. The structure of the

shareholding in the privatized HDFC Plc. is given in clause 21 (Detail of

shareholding in the company).

The July 2008 initiative to restructure the capital and recommence the

business of HDFC Plc. became effective on February 10, 2009 with the

first equity disbursement by the International Shareholders. IFC and

ADB’s commitment extended to a multi-lateral funding facility with sev-

en-year tenure. HDFC Ltd of India, with over thirty years of experience

in mortgage finance, is the technical partner of HDFC Plc. With assis-

tance from IFC’s Advisory Service performance based Grant (ASPBG).

In March 2013, the company has issued a listed bond of MVR

51.97million at interest rate of 7.5.p.a. Eight Individuals and one institu-

tion invested with this bonds issue.

Having restructured its capital, and with new lines of long-term credit,

Housing Development Finance Corporation Plc., Maldives (HDFC) re-

entered the market for mortgage home-finance for housing needs of

Maldivian Citizens. HDFC is unique as the only specialized housing fi-

nance institution in the Maldives. In a market where seven commercial

banks too are offering mortgage housing loan, HDFC’s competitive rates

and long repayment terms and income pooled home loans enabled the

achievement of a 50% market share by the end of 2016. Today the com-

pany’s loan portfolio stands over at MVR. 1.3 billion. The demand for

home-finance continues at a rate of growth that outstrips the supply of

matching funds, and long-term Sukuk denominated in MVR is seen as

the way forward to create sustainable housing finance in the Maldives.

The GOM’s policy of improving the infrastructure in focus islands to

facilitate economic development through zonal investment opportuni-

ties for Public, Private, Partnership (PPP) ventures is viewed as a posi-

tive factor in going forward with the development of housing finance.

Such an approach would assist sustainable growth in home ownership

based on mortgage security over properties that will appreciate in value.

HDFC MUDARABAH SUKUK Issue No. 02

31

HDFC Plc’s Board, Advisory Committees

and Senior Management

Board of Directors*

Nominee Directors

Mr. Ismail Ali Manik Government of Maldives (Chairman Feb 2016—April 2017)

Mr. Mohamed Mauroof Jameel Government of Maldives

Ms. Renu Sud Karnad HDFC Investments Ltd. (India)

Mr. Gaurav Agarwal Asian Development Bank

Mr. Nihal Senanayake Welikala International Finance Corporation

Alternate Directors

Mr. Conrad D'Souza HDFC Investment Ltd (India)

Mr. Asif Cheema Asian Development Bank

Managing Director

Ms Raheema Saleem

Company Secretary

Mr. Adam Athif

*Only the Managing Director holds a qualifying share in the stock of HDFC. The Chairman and

Board Directors function in a non-executive capacity.

Shari-ah Committee

Dr. Ibrahim Zakariyya Moosa Chairman

Dr. Rusni Hassan Member

Dr.. Aishath Muneeza Member

Mr. Azmeen Rasheed Secretary

Senior Management

Ms Raheema Saleem Managing Director

Mr. Mohamed Shafeeq Head of Finance and Business Development

Mr. Mohamed Fathy Senior Manager, Information Technology

Mrs. Aishath Rasheedha Senior Manager, Credit

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

32

Profile of HDFC Plc’s Board

The Board of HDFC comprises five Nominee Directors from the shareholders; the

Government of Maldives, 2 Directors; Asian Development Bank; International Fi-

nance Corporation and HDFC Investments Ltd. (India), each represented by a nomi-

nee Director; and the Managing Director (non-voting) functions in an executive ca-

pacity. The Shareholders’ also have the right to nominate Alternate Directors who

may partake in the Board Meetings but can only vote in the absence of the Nominee

Director representing the Shareholder. As per the shareholders agreement, the Chair-

man of the Board is appointed on rotation from the experienced and qualified Board

of Directors.

Mr. Ismail Ali Manik was appointed as a non-executive Director by

the Government of Maldives on 6 February, 2016.

Mr. Ismail Ali Manik, has represented the Government of Maldives,

as a Nominee Director since privatization of HDFC. He served as

the Chairman of the Board in 2013 before retiring due to his ap-

pointment to the Board of the Maldives Monetary Authority.

He started his professional career in the Ministry of Finance and

Treasury and worked on fiscal policy, public financial management

and economic policy matters. He has served in the government pub-

lic service for over twenty years. In addition he has also severed in

the World Bank, Washington DC office. He also served as Perma-

nent Secretary of the Ministry of Finance and Treasury and as

Board Director of Maldives Monetary Authority.

Mr. Ali Manik did his Master’s Degree in Public Administration ma-

joring in Economic Policy Management from the Columbia Univer-

sity, New York. In addition, he holds a Bachelor of Economics De-

gree from the University of Adelaide, Australia. Further, he has par-

ticipated at various international seminars and workshops conduct-

ed by the World Bank, ADB and other multilateral agencies.

Other appointments - Managing Partner at A2I Consulting LLP, a

Business and Management Consultancy Firm.

HDFC Board Committees - Audit Committee (Since 6 February

2016)

He does not hold any shares in any company in the Maldives that

has or will be perceived as a conflict of interest with HDFC PLC.

Mr. Ismail Ali Manik Chairman since Feb 6, 2016 - April 19, 2017

Non-Executive

HDFC MUDARABAH SUKUK Issue No. 02

33

Ms. Renu Sud Karnad, was appointed as the non-executive Director

by HDFC Investments Ltd. India, on 9 September, 2008.

Ms. Karnad has more than 38 years of experience in Housing Mort-

gage Finance.

She joined HDFC India in 1978. Having spent 20 years in various

post of the Company, Ms. Karnad was instated on to the Board as

Executive Director in 2000 and was re-designated as Managing Di-

rector from January 1st 2010. She is a Pravin Fellow-, Woodrow

Wilson School of International Affairs, Princeton, and University,

USA. She holds Master’s Degree in Economics from Delhi Universi-

ty and is also a Law Graduate from the University of Mumbai.

Over the years, Ms. Karnad has received numerous awards and ac-

colades.

Other appointments - Managing Director at Housing Development

Finance Corp. Ltd, Mrs. Karnad is a member on the following Com-

mittees of the Board of the Bank:

Stakeholders’ Relationship Committee

Corporate Social Responsibility Committee (Chairperson)

Risk Policy and Monitoring Committee (Chairperson)

Premises Committee (Chairperson)

HDFC Board Committees – None

She does not hold any shares in any company in the Maldives that

has or will be perceived as a conflict of interest with HDFC PLC.

Ms. Renu Sud Karnad Nominee Director

Non-Executive

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

34

Mr. Mauroof Jameel was appointed as the Director by the Government of Maldives on September 2016.

Mauroof Jameel is an architect and specialist on the architectural heritage of Mal-dives. He has wide ranging experience in design and development as well as project and institution management. He holds MSc Architecture, University of Malaysia, Pg Dip Architecture, University of Sheffield, UD and Ba (Hons) Architecture, Manches-ter Metropolitan University, UK. He has been associated with projects such as Hulhumale’, resorts and numerous buildings. Mauroof also served the Maldives gov-ernment in high-level posts and as a cabinet minister and has contributed to the de-velopment of the housing and construction industry. Since 2009 Mauroof has been researching and working in the filed of architectural heritage in both Maldives and Malaysia. At present he works as an architectural consultant, educator and a re-searcher. He is a member of Charted Architect of the Royal Institute of British Archi-tects (RIBA), UK, since 2004.

Mr.Mauroof has received numerous awards and accolades including MACI award for

the service t construction indiusty, President’s and hdc award of appreciation for the

service in development of Hulhumale and British Gas College Award for the Energy

Efficient Design in Housing , UK.

Mr. Mauroof Jameel Director

Non-Executive

Mr. Agarwal started his professional career as a senior officer at Grindwell Norton

Ltd / Saint Gobain (French Co), Bangalore, India in 1995. He then served at Unistar

Internernational LLC, United Arab Emirates (UAE) (Now renamed as Scion)as a

financial analyst in from 1997 to 2000. He has worked in various positions in finan-

cial sector of UAE, including Commercial Bank of Dubai, Ernst & Young / Arthur

Andersen, and as CFO of TAMWELL PJSC, Dubai Islamic Bank. Currently, Mr.

Agarwal works as the CFO of Emirates Investment Bank Pjsc, Dubai.

He holds a Global Executive MBA from INSEAD, France and a Master of Business

Administration from Kurukshetra University, Haryana, India. He received CFA

training from Institute of Chartered Financial Analyst of India (ICFAI), Hyderabad,

and is also a trained Associate of Cost and Works Accountant from Institute of Cost

and Works Accountant of India (ICWA) Calcutta.

Mr. Gaurav Agarwal Director,

Non-Executive

HDFC MUDARABAH SUKUK Issue No. 02

35

Mr. Nihal was appointed as the nominee Director by the IFC on November 2016.

Nihal is a well experienced and respected Senior Banker, having served as the 1st Sri Lankan CEO of Citi Bank, Sri Lanka Branch and CEO of National Development Bank. Currently he works as pro bono Consultant to the Ministry of Public Enterprise Devel-opment of the Government of Sri Lanka and as team leader of the Ministry project to monitor and reform eight state owned banks. He also serves as the Chairman, AMW Capital Leasing Ltd which is owned by the Al-futaim group of Dubai. He is a Non-executive Director of National Development Bank(NDB Bank), Bartleet & Co Ltd and Bartleet Transcapital Ltd. He also work as an independent consultant in the financial sector.

Prior to his retirement in 2008, Nihal was the CEO of NDB Bank group for nearly seven years as Chief Executive Officer and sub-sequently worked for the Group as senior Adviser and Board director until 2011. At NDB he played a leadership role in the complex strategic repositioning of the Group from development bank to a commercial bank with an integrated project finance and capital markets business. Nihal also served as NDB’s nomi-nee Director at MFLC, Maldives and NDB Housing, a housing bank established in 2001 by NDB, IFC, HDFC, India, ADB and FMO in Sri Lanka, which was subsequently merged in to NDB Bank.

Nihal trained as a Chartered Accountant with Ernst & Young in

London. He holds a Bachelor of Law degree of the University of

Sri Lanka and a Fellow member of the Institute of Chartered Ac-

countants in England & Wales and Institute of Chartered Ac-

countants of Sri Lanka

Mr. Nihal S. Welikala Nominee Director

Non-Executive

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

36

Mr. Asif Cheema was appointed as the Alternate Director by the Asian Develop-

ment Bank on April 2015.

Mr. Cheema started his career at Deutsche Bank Securities, New York as an Equi-

ty Research Associate in 1996. Before joining ADB Asif has worked in various fi-

nancial institutions including J.P. Morgan Securities, New York, HSBC Invest-

ment Bank, Dubai and London, Nomura International, Dubai as Executive Direc-

tor, Corporate Finance and Investment Banking. He also has worked at Alpen

Capital, Dubai, and UAE. Mr. Asif, holds a Master’s degree in Business Admin-

istration (MBA) from Yale University and course work in International Affairs

from Colombia University and Bachelor of Science in accounting and finance

from New York Institute of Technology, New York

Other Appointments- Financial Institutions Investment Specialist at the Asian

Development Bank.

HDFC Board Committees – None

He does not hold any shares in any company of the Maldives that has or will be

perceived as a conflict of interest with HDFC Plc.

Mr. Asif Cheema Alternate Director,

Non-Executive

Mr. Conrad D’Souza was appointed as the Alternate Director by the HDFC Invest-

ments Ltd. India on 9 September 2008.

Mr. D’Souza has more than 30 years of experience in the field of Housing Finance.

He joined HDFC Investment ltd. (India) in 1984 and he was the Treasure of

HDFC India and was responsible for resource mobilization for both domestic and

international and asset liability management. Mr. D’Souza has been a consultant

in the housing finance to UNAID/UNDP and IFC (Washington) and has under-

taken assignments in Asia, Africa and Eastern Europe. He is a member of the Na-

tional Stock Exchange of India Limited’s Committee on Currency Derivatives and

a member of the Association of Finance Professionals of India. Mr. D’Souza has

Masters’ Degree in Commerce and MBA and is a Senior Executive Program (SEP)

graduate of the London Business School.

Other appointments: Senior General Manager, Management Services and Inves-

tor Relations. He also is a Board Director in the following companies.

HDFC Holding Ltd., HDFC Investments Ltd., Chalet Hotels Pvt. Ltd, HDFC Edu-

cation & Development Services Pvt. Ltd. HDFC Sales Pvt. Ltd., Association of Fi-

nance Professionals of India. Kooh Sports Pvt. Ltd., and Nationals Trust Bank Plc.

Sri Lanka. HDFC Board Committees - Audit Committee

He does not hold any shares in any company in the Maldives that has a conflict of

interest with HDFC PLC.

Mr. Conrad D’Souza Alternate Director, Chairman Since April 30, 2017

Non-Executive

HDFC MUDARABAH SUKUK Issue No. 02

37

She was the Operations Director and the Company Secretary since 1

October 2014. She is now the Managing Director of the company from

26th February 2017. Prior to privatization of the Company she was the

founding Managing Director. Ms. Raheema has served the Ministry of

Finance and Treasury for more than 16 years at various senior posi-

tions. She had served as the Chairperson of the National Oil Company

and Board of Director at the State Trading Organization and also as a

Board Director at HDFC before and after privatization. She holds Mas-

ter of Management from Monash University and Master of Tourism

from Monash University Australia and Bachelor of Commerce in Ac-

counting and Marketing (Double Major) from Curtin University, Aus-

tralia.

She does not hold any shares in any company in the Maldives that has

or will be perceived as a conflict of interest with HDFC PLC.

Ms. Raheema Saleem Managing Director

HDFC PLC.

Mr. Adam Athif, joined HDFC Plc. in December 2004. Mr. Athif

started his career in the Government of Maldives in 1990 as a Secre-

tary since then he has worked his way up the ladder and has worked

in areas related to Administration and Human Resources in the Pri-

vate Sector as well as the Government. He holds a Diploma in Busi-

ness Administration and is well versed with local Housing Market

having attended various workshops in relation to Housing Finance.

He has declared that he does not hold any shares in any company of

the Maldives that has or will be perceived as a conflict of interest

with HDFC Plc.

Mr. Adam Athif Company Secretary

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

38

Profile of HDFC Plc’s Shariah Advisory Committee

The HDFC Amna department is managed and systematized to ensure proper Shari’ah

governance mechanisms both within the department and among its stakeholders. A

Shari'ah Committee consisting of three members will be established to advise the

Board of Directors of HDFC on Shari'ah related matters. The members of the Shariah

Committee are:

Dr Ibrahim Zakariyya Moosa holds a PhD in Fiqh and Usulul Fiqh

and a M.A in Islamic Revealed Knowledge from International Islamic

University Malaysia. He obtained his Bachelor’s Degree in Islamic

Shariáh from Islamic University of Medina, Saudi Arabia. He was the

former Rector of College of Islamic Studies of Maldives. Currently he

is the Dean of Center for Post Graduate Studies of Islamic University

of Maldives. He also served as a Parliament Member for nine years

(from 1989 to 1999); was a Member of the Special Majlis for thirteen

years (from1990 to 2004); was a Member, Supreme council of Islam-

ic Affairs. (from 1995 to 2004); and also was a Member of Quran

translation committee (from 1995 to 2004). He has attended semi-

nars and published articles on different matters related to Shariáh.

Dr. Ibrahim Zakariyya Moosa Shariáh Advisory Committee

Chairman

Assoc. Professor Dr Rusni Hassan is an Associate Professor at the

Ahmad Ibrahim Kulliyyah of Laws (AIKOL), International Islamic

University Malaysia (IIUM). She graduated with LLB (Honours)

and LLB (Shariah) (First Class), Master of Comparative Laws

(MCL) and Ph.D. in Law. Her area of specialization includes Islamic

Banking, Finance and Islamic Documentations, Islamic Capital

Market, Takaful and Islamic Law of Transactions. She is a Board

Member and PhD Selection Committee at IIUM Institute of Islamic

Banking and Finance. Presently she is a member of Shariah Adviso-

ry Council of Central Bank of Malaysia (Bank Negara Malaysia). She

was a member of Shariah Committee for HSBC Amanah Malaysia,

HSBC Amanah (Takaful) Malaysia and a registered Shariah Unit

Trust Advisor with the Securities Commission. She has presented

numerous research papers on Islamic finance in national and inter-

national conferences and she has also written books of Islamic fi-

nance related subjects. She is the co- author of the winning essay of

the worldwide Islamic finance essay competition organized in Kuala

Lumpur Islamic Finance forum (KLIFF) of 2010 for research: “Take

It or Leave It! The Iniquitous Islamic Banking Documents” and has

won a gold medal and a silver medal in IIUM Research Invention

and Innovation Exhibition 2012 for her research on Islamic banking

and finance.

Dr. Rusni Hassan Member

HDFC MUDARABAH SUKUK Issue No. 02

39

Dr Aishath Muneeza is among the key founders of Islamic finance in

Maldives, a small island nation with a hundred percent Muslim popula-

tion. She has experience in multiple aspects of Islamic finance industry.

She is a member of capital market Sharia Advisory Council of CMDA,

an Islamic Finance Consultant, a researcher, a presenter, a regulator, a

speaker, a trainer, an Associate Professor and an attorney who is active-

ly involved in promoting Islamic finance. She is the driving force behind

the establishment of Maldives Hajj Corporation, the Tabung Haji of

Maldives and she has facilitated the establishment of more than ten

financial institutions offering Islamic finance services. She structured

the first corporate sukuk offered in Maldives and she also structured

the Islamic Treasury Instruments for the government of Maldives. The

Islamic Capital Market framework of Maldives has been shaped under

her guidance and the legal framework of Islamic Capital Market in Mal-

dives was developed by her. She has published numerous books on Is-

lamic finance, available in all major bookstores across Malaysia and she

is the first to publish comprehensive books on Islamic finance in

Dhivehi language. She is the co-author of the winning essay of the

worldwide Islamic finance essay competition organized in Kuala-

Lumpur Islamic Finance forum (KLIFF) of 2010. She had won gold and

silver medals in international research exhibitions for research con-

ducted on disciplines related to Islamic banking and finance. Her con-

tribution to Islamic finance industry has been recognised international-

ly and has been conferred several awards of recognition. She has re-

ceived the prestigious “Rehendhi Award” highest award for women,

conferred by the government of Maldives for her contribution in the

development of Islamic finance industry. Currently she is an Associate

Professor at INCEIF & the chairwomen of Maldives Centre for Islamic

Finance that was set up by the government of Maldives to position the

country as the hub of Islamic finance and Halal industry in the South

Asia region.

Dr. Aishath Muneeza Member

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

40

Mr. Azmeen Rasheed joined HDFC in April 2016, he holds a Juris

Doctor Degree J.D (hons) from Kingdom of Saudi-Arabia, majoring

in Sharia Law and Jurisprudence. He also holds a masters Degree in

the field of Common Law, (Banking and Taxation). He is a regis-

tered attorney in the Maldives. He is currently pursuing his PhD in

Economics from Malaysia.

Prior to his First Professional degree, he worked in State Trading

Organization, Handling Projects related to bids. He is currently the

Manager for HDFC Islamic Window Amna. He has conducted work-

shops and lectures in IUM, MNU and Villa College on Governance

and Sharia Related Subjects as well as Sharia Compliant Finance.

He does not hold shares in any company of Maldives that has or will

be perceived as a conflict of interest with HDFC PLC.

Mr. Azmeen Rasheed Manager - Islamic Finance / Sharia Compliance Officer

HDFC MUDARABAH SUKUK Issue No. 02

41

Mr. Mohamed Shafeeq joined HDFC in 2009. Prior to joining the company he

was the Finance Director at the Society for Health Education (SHE). He holds

MBA from the University of Ballarat, Australia through Unity College Interna-

tional, Malaysia, in addition to a BA (Hons) Accounting and Finance by Univer-

sity of East London, UK, obtained through HELP University College, Malaysia,

he also holds Association of Chartered Certified Accounts (ACCA) through In-

thi International University of Malaysia. He is a member of ACCA and a senior

member of the Certified Practicing Accountants of Maldives (CPA Maldives).

He is also the Information Officer of this Company. He does not hold any

shares in any company in the Maldives that has or will be perceived as a con-

flict of interest with HDFC PLC.

Mr. Mohamed Shafeeq Head of Finance

She joined the HDFC Plc. in March 2004 as part of the initial team. Ms.

Rasheeda began her career with the Maldives Monetary Authority, 1990 and

spend 14 years serving as a Banking Officer in the Banking Section of the Au-

thority. She joined HDFC as a credit officer in 2004 and promoted as a Credit

Manager in 2008, and as a Senior Credit Manager in 2012. She holds Master of

Business Administration from Cardiff Metropolitan University, UK through

International College of Business Technology (ICBT)

Mount Lavinia, Sri Lanka. She is also the Anti Money Laundry (AML) Officer of

the Company.

She does not hold any shares in any company in the Maldives that has or will

Ms. Aishath Rasheedha Senior Manager, Credit

Mr. Fathy joined HDFC Plc. in March 2004 as part of the initial team. He be-

gan his career 2001 in the field of audit and gained experience at local firms

and with the experience gained got engaged in providing consultancy services

as a freelance consultant. While at HDFC he headed the Internal Audit Division

as well as the IT Division, in addition he has provided numerous contributions

in the development of internal controls and systems. He holds M.Sc. in IT Man-

agement from Asia Pacific University Malaysia and Bachelor of Commerce

from Bangalore University of India.

He does not hold any shares in any company in Maldives that has a conflict of

interest with HDFC PLC., except at Bank of Maldives PLC. at which he holds 50

Shares.

Mr. Mohamed Fathy Senior Manager, IT

Profile of other members of the Senior Management

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

42

Company’s Growth

We are pleased to present this report to the Sukuk prospectus of HDFC Plc. with extracts from the

Audited Accounts for the year ended December 31, 2016 while the full audited financial statements

complete with the auditor’s report is annexed:

The twelve-year financial landscape shows that HDFC has grown with each passing year to reach sta-

bility and sustainability.

The continued success of the Housing Development Finance Corporation PLC of the Maldives

(HDFC) with a strong performance in 2016 reflects the strength of the foundation laid by the share-

holders, led by the International Finance Corporation, upon privatization in July 2008.

The Company made an operating profit of MVR 85.7 million (USD 5.6 million) for 2016, continuing

its upward trajectory. The theme we established in 2015, continued onto 2016 “REWARDING LOY-

ALTY & MOVING FORWARD TO GREATER AFFORDABILITY speaks volumes about what HDFC

stands for in terms of proven resilience, customer centrality and innovation of products for invest-

ment and lending. HDFC’s ability to transform ahead of the trends in the most proactive manner

made it possible for the Company to survive and prosper in the Maldives economy considered to be

an emerging market in the global arena. We have built a strong brand image grounded on trust and

confidence so that, to the thousands of our loyal customers, HDFC represents the best and the most

appealing Housing Finance solution in the Maldives to make their dream of living in a decent home

come true.

FINANCIAL HIGHLIGHTS (MVR million)

Year 2014 2015 2016

Total Income 122.7 130.6 151.9

Profit Before Tax 64.6 71.5 85.7

Profit After Tax 54.9 60.5 72.3

Net worth 434.5 455.2 467.8

Loans and Advances to customers 941.5 1,086.50 1,302.00

FINANCIAL RATIOS

ROAE 13% 14% 19%

Earnings/(loss) per share 34.44 37.99 45.36

Dividend Per Share 25.00 17.50 20.00

Dividend (%) 73% 46% 44%

Net Assets value per Share 272.65 285.63 293.5

Debt/Equity ratio 154% 172% 192%

HDFC MUDARABAH SUKUK Issue No. 02

43

HDFC has been a significant contributor to the economic growth and the

quality of life for the people of Maldives, and this Annual General Meet-

ing 2016 is a significant milestone on the path of progress of our organi-

zation.

The reporting year of 2016 also marked the first year after the Golden

Jubilee of National independence in the Republic of Maldives, and

therefore, an extremely eventful year for the country as well as the finan-

cial services industry of the Maldives. There were many events of finan-

cial significance carried out to coincide with the celebrations, and the

HDFC participated in all the relevant events. Maldives Monetary Au-

thority (MMA) released new polymer banknotes to the market, attrac-

tively designed to reflect the cultural and natural appeal of the Maldives

as one of the prime tourist destinations in the world.

The MMA reduced the minimum reserve requirement (MRR) for com-

mercial banks from 20% to 10% in August 2015, and also brought down

the T-Bill rates by almost 30% with caps introduced in October of the

same year. Both these events had a positive impact on the Rufiyaa li-

quidity and enhanced competitiveness among financial institutions,

which will in time; translate to better access to finance with greater af-

fordability for the people of Maldives.

Based on Census 2014, the resident Maldivian population was 338,434

and 30% of the total population live in the Male’ City Region. However,

when it comes to the number of households, Census 2014 showed a total

of 68,249 households in Maldives, out of which 26,739 or almost 40%

were in Male’ and 40,887 households in the 187 administrative islands

in the Atolls. HDFC PLC estimates that there is a deficit of minimum

15,000 units of housing in the capital region alone. Based on the statis-

tics for approvals and certificates of completion issued over the last sev-

en years, the addition to the housing stock has been less than 500 units

on average per annum. The demand led pricing and rentals have been a

major concern for mortgage lending institutions dominated by HDFC

PLC and Bank of Maldives, but given the current trend, unless the sec-

ond phase of Hulhumale’ and the bridge project, which has already com-

menced to connect Male’ and Hulhumale’ add the necessary momentum

for the annual delivery of greater numbers to swell the housing stock,

the house prices will not go into decline to create a negative equity sce-

nario, which has been the bane of the financial sector in the developed

countries.

With the expansion of the economy, the construction industry marked a

revival by an estimated YOY growth of over 20% compared to the slug-

gish performance of the past. Although the major part of this rebound

was due to new resort projects, many real estate development projects

too contributed in 2016, mainly in Hulhumale’. A landmark residential

development project, Amin Avenue, with 279 apartments constructed by

Amin Construction Pvt. Ltd. took the centre stage with HDFC PLC as its

sole Mortgage Finance Partner. The other major developers that part-

nered HDFC PLC to help relive population congestion in the capital city,

Male’ were Rainbow Construction, Damas Company, Jausa Construction

Maldives, Wiz Company and state-owned Maldives Real Estate Develop-

ment Corporation Pvt Ltd. This new trend of real estate development

companies augmenting family-based construction projects on their own-

land augurs well for the housing finance industry, and offers greater po-

tential for HDFC’s future growth.

PROSPECTUS 2016

Housing Development Finance Corporation PLC.

44

Lending Operations and the Social Impact

HDFC’s inclusive business model has developed a range of products and

services that involve the cottage industries in the value chain as suppli-

ers of building material such as compressed cement blocks and car-

pentry work carried out at an island level to reduce the cost of construc-

tion. The total number of beneficiaries at the bottom of the pyramid ex-

ceeds 15,000 during the 13-year existence of HDFC. A comprehensive

range of products and services have been innovated to serve the custom-

ers better. Effective counseling service and CRM have helped in achiev-

ing best-fit product development through customer feedback.

Total loans approved and disbursed under various product categories

serve to profile HDFC’s direct contribution to the housing finance mar-

ket. Since its inception, total housing finance injected to the market

stood over MVR 2.4 billion as at the year ended on December 31, 2016.

Approximately 8000, customers under the pooled application process

participated in HDFC’s growth. As at the year end, the total outstanding

capital stood about MVR 1.4 Billion profiled as below:

0

20

40

60

80

100

120

2015 2016

Islamic Mortgages

Home Loan

HDFC MUDARABAH SUKUK Issue No. 02

45

Maldives Country Report on Housing and Housing Finance

Having re-structured its capital in February 2009, and with new lines of long-term

credit, HDFC has re-entered the market for mortgage loans for housing needs of indi-

viduals and families. HDFC is able to offer long repayment terms in a market where

the demand has grown at a pace outstripping the supply of matching funds. The pri-

vatization has transformed the institution to face the future as a commercially viable,

private sector-led company that can grow and develop effective solutions to the ur-

gent housing problems of the Maldives.

The Maldives consist of approximately 1,200 islands covering an area of

90,000 sq. km. of the Indian Ocean, set in an Exclusive Economic Zone

(EEZ) covering 859,000sq km. The island nation has 196 administrative

islands designated for habitation, in addition to which over 100 islands

are allocated as resort properties and 35 islands designated for industry

and agriculture. Maldives is home to approximately 350,000 citizens

living in a dispersed manner with only thirteen islands outside of Male’

region recording a population of more than 5,000 inhabitants. This pre-

sents a formidable challenge to a housing finance institution which in-

tends to operate at a national level due to the diverse needs

of the population that is thinly spread in some regions, with the excep-

tion of the post-tsunami phenomenon of concentration through in-

migration, where the stress of housing is felt the most in the Male’ Atoll.

The nation’s capital Malé, with around 2.5 sq. km. of total land area, has

over one third of the entire population, while approximately seventy per-

cent of the rest of the inhabited islands have less than 1,000 inhabitants

each. Maldives has a relatively young population with almost forty per-

cent under 15 years of age and around three percent over 65 years of age.

This demographic profile translates to a growth in demand for housing

in the foreseeable future as the young population matures to full-fledged