Guide to Taxation and Investment in Georgia 2018 Tax & Legal

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Guide to Taxation and Investment in Georgia2018Tax & Legal

2

Business and Investment Environment 3 Introduction 3Georgia country key facts 4Deloitte in Georgia 5Forms of Business Organization 5Legal Requirements for Establishing a Company in Georgia 5Establishing a Branch of a Foreign Company in Georgia 6Authorized Capital and Contributions of Partners 7Licensing and Compulsory Notification to State Authorities 7Acquisition of Real Estate in Georgia 7Exchange Controls 7Bank Accounts and Confidentiality of Bank Information in Georgia 8Investment Incentives 8Compulsory Registration with the National Agency of Public Registry of Georgia 9

Taxation in Georgia 13Taxation System 13Definitions of terms in the Tax Code 13Personal Income Tax 13Profit Tax 15Legal entities to whom new profit tax rules do not apply 19Tax Accounting Rules 23Taxation of Nonresidents of Georgia 24Value Added Tax 29VAT Administration 31Excise Tax 32Property Taxes 34Other Taxes 35Transfer Pricing Rules 37Production Sharing Regime 40

Tax & Legal contacts — Georgia 44

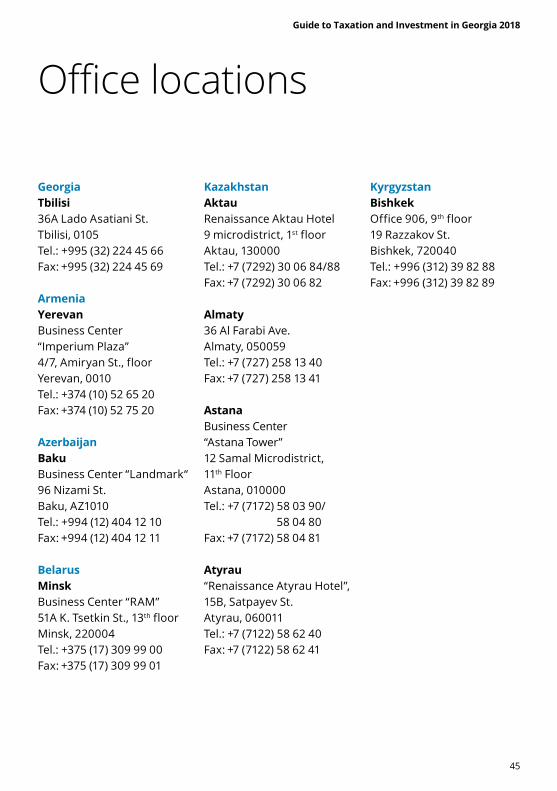

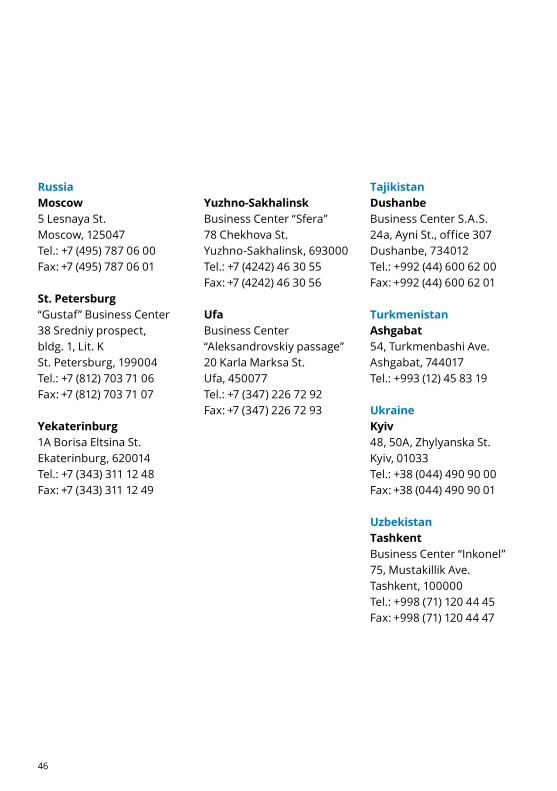

ffice locations 45

Guide to Taxation and Investment in Georgia 2018

3

Business and Investment Environment Introduction Georgia is the aspiring economic center of the Caucasus. It boasts years of robust economic growth, liberal tax and labor legislation, business friendly practices, low corruption, high security and openness to foreign investment. Georgia signed the association agreement with the EU in 2014 and an aspiration to join the EU will guide future policy decisions. On February 2nd 2017, the European Parliament voted in favor of visa-free travel for Georgian citizens to the Schengen Area at the plenary session and the visa-free regime between Georgia and the EU entered into force in April 2017. Georgia has state and private investment funds that welcome foreign investments to implement large scale projects in agriculture, tourism and hydro energy generation.

The World Bank rated Georgia as the 9th easiest place in the world (among 190 countries) to do business in 2018. Heritage Foundation ranked Georgia 13th (among 180 countries) for its economic freedom in 2017. Georgia has a Standard and Poor and Fitch ranking of (BB-) for the 2017 fiscal year. International securities markets showed their confidence in Georgia by the oversubscribed purchase of the state bonds in 2011. The state

securities trade at about 450 bps above the comparable US treasury rates. Georgia has ongoing IMF program as a stand-by, if financial need emerges, considering the tensions in the country’s major trade partners: Russia and Ukraine. The government’s statement of the long term priorities and plans emphasize energy, agriculture, regional trade. Georgia has minerals, water, hydro power and gold resources. Expansion of the financial sector, hydropower, mining, apparel production, telecommunications, on-land and sea transport services significantly enhanced the country’s GDP.

Georgia has a picturesque sea cost and two modern seaports allowing easy access to all the world’s marine centers. Georgia has a track record of prudent macroeconomic management, with low budget deficits and low inflation. Georgia is a small open economy, not immune to the economic trends of the trading partners. On the positive note, the cheaper local currency may facilitate exports. The Central Bank and the Ministry of Finance coordinate their efforts to counteract negative international trends that led to the depreciation of the local currency. Georgia has large unemployment and predominantly young population, which can be a benefit for the firms seeking to enter the market.

4

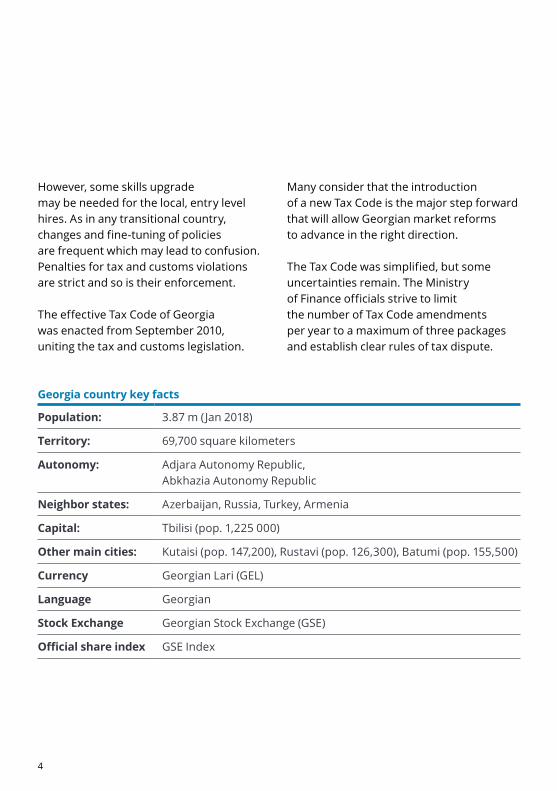

However, some skills upgrade may be needed for the local, entry level hires. As in any transitional country, changes and fine-tuning of policies are frequent which may lead to confusion. Penalties for tax and customs violations are strict and so is their enforcement.

The effective Tax Code of Georgia was enacted from September 2010, uniting the tax and customs legislation.

Many consider that the introduction of a new Tax Code is the major step forward that will allow Georgian market reforms to advance in the right direction.

The Tax Code was simplified, but some uncertainties remain. The Ministry of Finance officials strive to limit the number of Tax Code amendments per year to a maximum of three packages and establish clear rules of tax dispute.

Georgia country key facts

Population: 3.87 m (Jan 2018)

Territory: 69,700 square kilometers

Autonomy: Adjara Autonomy Republic,Abkhazia Autonomy Republic

Neighbor states: Azerbaijan, Russia, Turkey, Armenia

Capital: Tbilisi (pop. 1,225 000)

Other main cities: Kutaisi (pop. 147,200), Rustavi (pop. 126,300), Batumi (pop. 155,500)

Currency Georgian Lari (GEL)

Language Georgian

Stock Exchange Georgian Stock Exchange (GSE)

Official share index GSE Index

Guide to Taxation and Investment in Georgia 2018

5

Deloitte in Georgia Deloitte provides services to Georgian clients and investors in Georgia from its office in Tbilisi. The firm offers accounting, statutory and international auditing, tax consulting, financial and risk advisory and legal services. The Georgian office of Deloitte is part of the Deloitte Touche Tohmatsu global network.

We offer our clients locally oriented, individual services with the background and resources of an international organization. We have the strength, knowledge and expertise to provide sound advice for any business needs, anywhere in the world. When you call on us, you call on the resources of a strong local practice and an integrated global network. For a relatively new marketplace, our experience is wide-ranging and comprehensive. The scope of our services matches the needs of our clients. In this rapidly evolving market, we have to remain flexible and responsive to the needs of our clients.

Forms of Business OrganizationThe main types of business organizations in Georgia are a general partnership, limited partnership, limited liability company, and joint-stock company, cooperative. Foreign organizations can also pursue their business

interests using the registered branches and representative offices. A physical person can also conduct entrepreneurial activities as a sole proprietor.

Legal Requirements for Establishing a Company in GeorgiaIn order to establish an enterprise a number of documents must be submitted to the National Agency of Public Register of Georgia. The documents required are stipulated in the “Law on Entrepreneurs”, in particular, articles of association/a charter which must contain the following information: the company name; the legal form; the legal address; the official email address; the main activity; the name, date, place of birth and place of residence of each founding partner or — where the founding partner is a legal person — the company name, the legal form, the legal address, the date of registration, the identification number; and data on its representatives.

In addition to above, limited liability companies and limited partnerships should submit information on the contributions made by each founder and their shares, accordingly; the name, first name, date and place of birth and address of each director, and each member of supervisory council (if any); full information on the enterprise’s authorized representatives, directors, procurators

6

(if any); obligations related to the limitation of the liability. Limited partnerships should also submit the list of limited partners as well as the list of general (personally liable) partners.

If the partner is a legal entity, submission of the decision of partners on founding a company will also be required.

If a director of the company is not the founding partner, his/her consent to become an authorized representative will also be required.

Notarization of the registration application is not mandatory where the document is signed by authorized persons in person at the registration authority or if the registration application has been duly certified by the administrative authority. It is to be noted that whilst submission of the document confirming contributions to the authorized capital is not required, the document verifying the title to the enterprise’s office premises is required by the state authority.

The National Agency of Public Register of Georgia registers the enterprise within one day after the date of submission of the documents. In case the state authority fails to register the enterprise within the mentioned period, they provide

a substantiated refusal or a reason to the applicant in order for the enterprise to correct an error indicated by the state authorities within 30 calendar days after submission of the application form.

In order to register as a sole proprietor, a physical person must submit to the National Agency of Public Register of Georgia an application. The state authority registers a sole proprietor within one day after the date of submission of the documents. The application form must include the following: the name of sole proprietor; first name and surname, place of residence, ID Number, the date of the submission of the document, signature and e-mail of the sole proprietor.

Establishing a Branch of a Foreign Company in GeorgiaThe foreign company should in the first place inform the National Agency of Public Register of Georgia on the intention to establish a branch. The following documents are required by the state authorities for the registration of a branch: the application on registration of a branch; the decision of the enterprise management on establishment of a branch; a copy of the enterprise’s and a branch’s statutes; the decision on appointment of a branch manager or a power of attorney granting him managerial powers;

Guide to Taxation and Investment in Georgia 2018

7

a copy of the passport and a consent of the person who will be appointed as the director of the Branch.

Authorized Capital and Contributions of PartnersUnder the law of Georgia “On Entrepreneurs”, the authorized capital of a Limited Liability Company may be set at any amount.

A Joint-Stock Company’s authorized capital is divided into shares. The minimum nominal value of the authorized capital may be set at any amount.

Licensing and Compulsory Notification to State AuthoritiesThe law of Georgia “On Licenses and Permits”, adopted on 24 June 2005, defines business activities to be licensed by the corresponding state agencies.

The Code of Administrative Offences of Georgia, adopted on 15 December 1984, provides liability for conducting business activities subject to licensing without a licence or in breach of relevant licence conditions.

Acquisition of Real Estate in GeorgiaThe transfer of title to an immovable property is regulated by the Civil Code of Georgia, adopted on 26 June 1997. The immovable property includes land-plots with minerals, plants and buildings.

In order to purchase immovable property it is necessary to submit a legalized (notarized) document indicating ownership and an extract of the purchaser’s registration to the National Agency of Public Register of Georgia. The seller and purchaser may also submit an application for registration. The title to agricultural land plots is granted to citizens of Georgia and private legal entities registered according to Georgian legislation.

Exchange ControlsGeorgia has adopted a very liberal monetary policy that is investor friendly. There are some legal restrictions for taking foreign currency in or out of Georgia both in cash and credit forms. A loan can be issued in a foreign currency to an individual if the amount of the loan exceeds GEL 100,000 (hundred thousand). In January 2017, the president of the National Bank issued the Order N4/04 that enables commercial banks to issue loans in the amount of up to GEL 100,000 (hundred thousand) in foreign currency if the borrower is not a citizen of Georgia.

The National Bank of Georgia, pursuant to the Law on “The National Bank of Georgia”, dated 7 April 2011, controls the monetary regulations in Georgia.

8

Pursuant to the Decree of the President of Georgia No. 363, dated 16 September 1995, all legal and physical entities are obliged to estimate all prices for products and services, prepare declarations and calculations within the territory of Georgia only in national currency, which is Lari. Therefore, Georgian currency is the only permitted instrument for making payments within the territory of Georgia.

Bank Accounts and Confidentiality of Bank Information in GeorgiaResident and non-resident entities of Georgia have a plenipotentiary power to open and dispose of any accounts in national as well as any other foreign currency. In order to open foreign currency bank accounts, the entities conducting their activities in Georgia are obliged to submit a document confirming their registration with the National Agency of Public Register of Georgia or the tax authorities. As for the branches, in order to open an account, they are required to submit additional documents confirming their registration and foundation.

Cash may be transferred abroad without any limitation, provided that there is a valid order by the non-resident owner of the bank account instructing the bank of this transfer. In order

to transfer foreign currency abroad, residents (entrepreneurs) are required to indicate in the payment order the purpose of operation and present the documents confirming the legality of the operation to be performed.

In the territory of Georgia, payments between residents and non-residents are to be carried out in the national currency of Georgia, except for operations connected with export and import activities that may be performed in any foreign currency acceptable to the parties. According to the Law of Georgia “On Activities of Commercial Banks”, dated 23 February 1996, disclosure of confidential account information is prohibited. Such information may be disclosed only on the basis of a Court decision.

Investment IncentivesObject of Investment Activities and Rights of Foreign InvestorsThe Law of Georgia “On Promotion and Guarantees of Investment”, dated November 12, 1996 determines the legal grounds of making both foreign and domestic investments in Georgia and guarantees their protection. An Investment is any kind of property or intellectual value or right to be contributed and used in the entrepreneurial

Guide to Taxation and Investment in Georgia 2018

9

activity made on the territory of Georgia for earning potential income. An Investor is any physical or legal person, or international organization making investments in Georgia. A Foreign investor may be a citizen of a foreign country (alien), a stateless person not residing in the territory of Georgia, a citizen of Georgia permanently residing abroad, or a legal person registered outside Georgia.

A foreign investor, whilst executing investment and entrepreneurship, is guaranteed and enjoys equal rights to those granted a physical and legal person of Georgia. A foreign investor, after payment of taxes and other mandatory charges is entitled to repatriate the earnings (income) gained from investments as well as other funds abroad without any limitation. This right can be limited only by law, a Court verdict in case of bankruptcy, committing a crime and violation of civil obligations. Besides, a foreign investor has the right to take abroad the property which he owns.

Investment Protection in GeorgiaInvestment in Georgia is entirely and unconditionally protected by the applicable law. Investment may be seized in cases directly specified by the law, by the court decision

or in case of emergency established by the fundamental law, provided there is appropriate compensation thereof.

Compensation to be given to the investor shall correspond to the real market value of the confiscated investment at the moment of the deprivation. Compensation shall be given without any delay and shall account for the losses incurred by the investor from the moment of deprivation until the payment of the compensation.

Compulsory Registration with the National Agency of Public Registry of Georgia A company registered in Georgia or any entity carrying out economic activity in the territory of Georgia should register with the legal entity of public law — National Agency of Public Register of Georgia on a mandatory basis.

The National Agency of Public Register of Georgia shall assign an identification number to each taxpayer to be used for all taxes, including customs tax.

Pursuant to the Tax Code, a taxpayer will be subject to payment of financial penalties in case of performing activities without being registered with the state authorities.

10

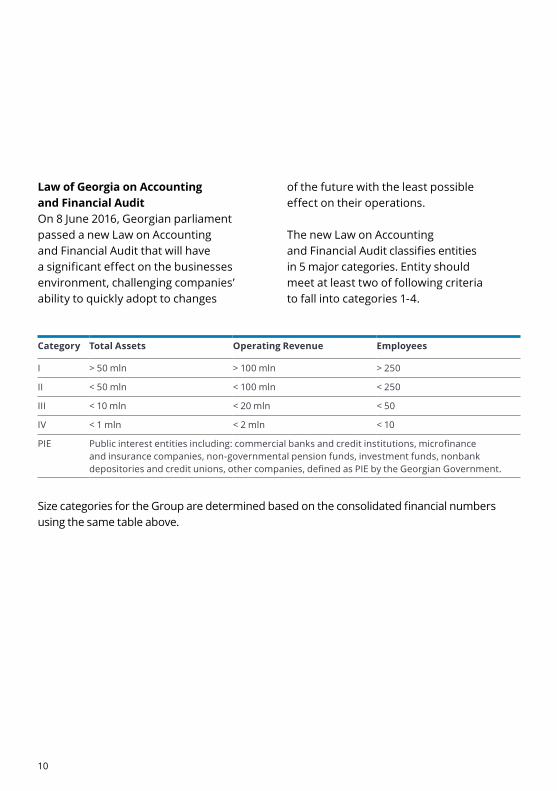

Law of Georgia on Accounting and Financial AuditOn 8 June 2016, Georgian parliament passed a new Law on Accounting and Financial Audit that will have a significant effect on the businesses environment, challenging companies’ ability to quickly adopt to changes

of the future with the least possible effect on their operations.

The new Law on Accounting and Financial Audit classifies entities in 5 major categories. Entity should meet at least two of following criteria to fall into categories 1-4.

Category Total Assets Operating Revenue Employees

I > 50 mln > 100 mln > 250

II < 50 mln < 100 mln < 250

III < 10 mln < 20 mln < 50

IV < 1 mln < 2 mln < 10

PIE Public interest entities including: commercial banks and credit institutions, microfinance and insurance companies, non-governmental pension funds, investment funds, nonbank depositories and credit unions, other companies, defined as PIE by the Georgian Government.

Size categories for the Group are determined based on the consolidated financial numbers using the same table above.

Guide to Taxation and Investment in Georgia 2018

11

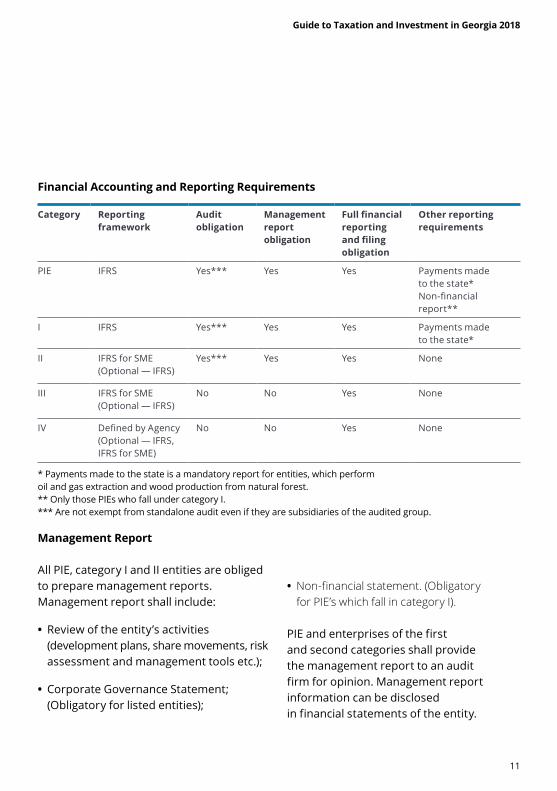

Financial Accounting and Reporting Requirements

Category Reporting framework

Audit obligation

Management report obligation

Full financial reporting and filing obligation

Other reporting requirements

PIE IFRS Yes*** Yes Yes Payments made to the state*Non-financial report**

I IFRS Yes*** Yes Yes Payments made to the state*

II IFRS for SME (Optional — IFRS)

Yes*** Yes Yes None

III IFRS for SME (Optional — IFRS)

No No Yes None

IV Defined by Agency(Optional — IFRS, IFRS for SME)

No No Yes None

* Payments made to the state is a mandatory report for entities, which perform oil and gas extraction and wood production from natural forest.** Only those PIEs who fall under category I.*** Are not exempt from standalone audit even if they are subsidiaries of the audited group.

Management Report

All PIE, category I and II entities are obliged to prepare management reports.Management report shall include:

• Review of the entity’s activities (development plans, share movements, risk assessment and management tools etc.);

• Corporate Governance Statement; (Obligatory for listed entities);

• Non-financial statement. (Obligatory for PIE’s which fall in category I).

PIE and enterprises of the first and second categories shall provide the management report to an audit firm for opinion. Management report information can be disclosed in financial statements of the entity.

12

Management report should include: review of the entity’s activities (development plans, share movements, risk assessment, management tools etc.)

Filing and Publishing Financial Statements and Enforcement DatesNew regulation will enter into force from January 2017 for category I, II and PIE and from January 2018 for category III and IV.

Following statements should be filled no later than October 1st following the reporting period:

• Financial Statements

• Management Report

• Statement on payments made to the state

• Audit Opinion

Other important requirements

• An entity shall prepare financial statements at least once a year and should disclose the comparative numbers as well;

• PIEs shall publish financial statements (including consolidated financial statements) at their webpages;

• Where an entity / group after an end of the two successive reporting periods no longer meets at least two criteria from the size category table the size category of an entity / group shall change and requirements of a new category apply;

• The entity shall be entitled to use only a standard permitted for entities belonging to a larger size category;

• Entities that fall under PIE, category I and II are also obliged to have audit of their financial statements done in accordance with the law even if they are part of the Group that has been audited;

• Financial statements and supporting documents should be maintained for 6 years after the end of the financial year.

Guide to Taxation and Investment in Georgia 2018

13

Taxation SystemThe Tax Code of Georgia is the principal source of tax law and is referred to as a normative act. The Tax Code has been amended several times since it was published on December 22, 2004. With effect from January 1, 2011 the Parliament of Georgia adopted the new Tax Code of Georgia. While other laws may affect taxation, they may not contradict the provisions of the Tax Code. Tax exemptions and concessions may be granted only through amendments to the Tax Code. Tax issues cannot be regulated by other legislation, except for administrative offenses (included in the Administrative Offense Code), tax crimes (included in the Criminal Code), priority of tax obligations (included in the bankruptcy laws), levies, and provisions pertaining to the Law “on Tax Liabilities and State Loans Restructuring”.

Definitions of terms in the Tax CodeThe Tax Code contains a number of definitions, many of them having a specific meaning that may differ from their common meaning, in some cases they are adopted from other laws by reference. However, in some cases the definitions of the terms used in Tax Code are not provided at all. Therefore, it is very important to understand and apply the terms provided in the Tax Code correctly.

Personal Income TaxTax JurisdictionNon-residents and tax resident individuals are subject to Georgian income tax only on income received from Georgian sources.

An individual is considered to be a resident of Georgia for personal income tax purposes if he or she is present in Georgia for more than 183 days in any 12-month period ending in a tax (calendar) year.

The personal income tax is imposed on wages and other forms of compensation paid to employees as well as income earned by physical person, entrepreneurs from their economic activities. Payers of income taxes are:

• employers (except free economic zone enterprise) who are paying wages (both in monetary or non -monetary forms) to physical persons or employees in Georgia;

• physical persons entrepreneurs, organizations and permanent establishments who make payments to physical persons who render services in Georgia and are not registered as a sole proprietor at the tax agency;

• Physical person, entrepreneurs and partnerships who are conducting entrepreneurial activity in Georgia.

Taxation in Georgia

14

Taxable Income and ExemptionsResident individuals are taxable on their domestic income, i.e., on income “received” from Georgian sources. Income is taxable irrespective of whether it is received in cash or in-kind. The following benefits received by a resident individual are specifically excluded from the taxable base of personal income tax: dividends, interests and royalties (except for the case when the receiver has benefited from the input right) received from resident companies, which were previously taxed at the source of income.

Tax RatesUnless other rates apply (for example, for dividends and interest), income of a physical person is taxed at the flat rate of 20%.

Income from renting out the residential space to a person for only residential purposes and not making any deductions from this income shall be taxed at 5%.

Income from sale of vehicle or a residential apartment (house) with attached land plot are taxed at 5%.

Payment of Income Taxes

Generally, income taxes are withheld at the source from payments of wages, dividends, interest, and some other types of payments to nonresidents.

The physical or legal person (including branches and other structural units of Georgian legal entities) making such payments must, as a tax agent, withhold the income tax and pay it to the budget. Any person (sole proprietors, foreign or Georgian companies) who makes a payment to a physical person not registered at the tax agency as a sole proprietor for work performed and services rendered is required to withhold income tax at the source of payment.

The following tax agents withhold income taxes at the source of payment:

• Physical person — entrepreneur who makes payments to physical persons working as employees in his sole proprietorship;

– a legal person who makes payments to physical persons working as employees;

– a physical or legal person paying pensions to physical persons, with the exception of pensions paid under the state social security system;

– a resident legal person paying dividends to physical persons;

– a physical or legal person (except licensed financial institution) paying interest to physical persons;

– a physical or legal persons making payments to non-residents; branches and other separate units of foreign companies.

Guide to Taxation and Investment in Georgia 2018

15

Profit TaxTax Jurisdiction and Payers of Profit TaxLegal entities incorporated in Georgia are normally treated as tax residents and are taxable on their worldwide income. Legal entities incorporated abroad are normally treated as foreign tax residents (“nonresidents”) and are taxable on income from Georgian sources or income from performing business activities through their permanent establishment in Georgia. The profit tax is imposed on profits earned by Georgian and foreign enterprises.

Branches of Georgian companies do not pay profit tax independently, but consolidate their profit (or loss) with the main enterprise, which pays the total profit tax.

New Profit Tax Rules in force from January 2017Georgia is actively looking for ways how to stimulate economic growth and attract more investments from foreign and local investors. Georgian government considered the Estonian 16 year experience with different corporate model as one of the potential ways forward.

Following protracted negotiations and discussions, the Georgian parliament adopted and the president signed into law amendments and an addendum

to the Tax Code in May 2016, which fundamentally reformed the profit tax regime for Georgian companies and permanent establishments (PEs) of nonresident companies. The profit tax regime, under which companies are subject to tax on their annual taxable profits, is changed to a system where tax has to be paid only if corporate profits are distributed, similar to the system adopted by Estonia.

In conjunction with the reform, certain tax rules cease to apply to resident entities and PEs of nonresident entities as from 1 January 2017, including the tax depreciation rules, the thin capitalization rules and the tax loss carry forward rules.

Objects of TaxationThe new profit tax rules are effective as of 1 January 2017, however these rules do not apply to commercial banks, credit unions, insurance organizations, microfinance organizations and pawnshops until January 2019. The new profit tax system apply only to Georgian resident companies and PE of nonresident companies and the tax base comprise both actual and deemed profit distributions, including the following:

• Distributed profits;

16

• Expenses incurred or other payments not related to economic activities;

• Gratuitous supplies of goods/services and/or transfers of funds; and

• Representation expenses that exceed the maximum amount defined in the tax code.

Special rules apply to profits arising from transactions related to Baku-Tbilisi-Ceyhan (“BTC”) and South Caucasus Pipeline (“SCP”), under the Host Government Agreements, and oil and gas operations, under current agreements to engage in these activities that were concluded before 1 January 1998 in line with Georgian laws; these profits are taxed according to the provisions and tax norms that applied before 1 January 2017.

Tax Filing and Payment Due DatesThe profit tax rate remained unchanged at 15%, however, to calculate the taxable amount, the amount of a distribution subject to taxation must be divided by 0.85. In the case of a gratuitous supply of goods/services, the taxable amount shall be determined based on the market value of the goods/services.

The tax reporting period is a calendar month. Tax returns have to be filed, and tax paid, no later than the 15th day of the month following the reporting calendar month.

Items subject to taxDistributed profits: Under the law, amounts distributed to shareholders as dividends in a monetary or nonmonetary form is considered taxable distributed profits. Dividends paid between Georgian companies are excluded from the taxable base (except for dividends paid out of net profits earned from 1 January 2008 to 1 January 2017). This effectively means that further distributions of the taxed dividends by Georgian company (except for a sole proprietor and a person that is exempt from profit tax under the Tax Code) is not deemed to be a profit distribution. However, further distribution of the taxed dividends received from commercial banks, credit unions, insurance organizations, microfinance organizations and pawnshops is not deemed to be a profit distribution barely for net profits earned between 1 January 2008 and 1 January 2017.

Net profits earned from 1 January 2008 to 1 January 2017, as well as the dividends of net profits earned between 1 January 2017 and 1 January 2019, if distributed until 1 January 2019, paid to commercial banks, credit unions, insurance organizations, microfinance organizations and pawnshops are deemed to be a profit distribution.

An allocation of dividends received from foreign enterprises (with the exception of entities resident in a low-tax jurisdiction) is not considered to be distributed profits.

Guide to Taxation and Investment in Georgia 2018

17

Payments made to a nonresident enterprise, whether in a monetary or nonmonetary form, from profits earned from a PE’s activities are treated as distributed profits of the PE (except the profits of PE earned till 1 January 2017). The profits attributable to a PE is the profits that it would be possible for the PE to generate as an independent enterprise engaged in the same or similar activities, operating under the same or similar conditions.

The following items also should be treated as profit distributions:

• Transactions carried out by an enterprise with related parties that are not subject to profit tax and if the value of the transaction agreed to between the parties is different from the market value and their interdependence affects the result of the transaction;

• Cross-border transactions with related parties, if the conditions established for such transactions do not comply with the arm’s length principle; and

• Transactions carried out by an enterprise with a party exempt from income/profit tax (except for a budgetary organization, legal entity under public law — the Deposit Insurance Agency and the National Bank of Georgia), if the value of the transaction is different from the market value.

If resident enterprises distribute dividends on or after 1 January 2017 from net profits of the period between 1 January 2008 and 1 January 2017, they have the right to offset the tax paid on the distribution against the profit tax paid in the prior reporting period. The profit tax credit should not exceed the tax paid on the profit distribution, as envisaged in the Tax Code. The amount of tax credit is calculated according to the following formula: A×B / (C-D), whereby:

A — The amount of dividend subject to distribution;

B — The profit tax accrued and paid during a reporting period from 1 January 2008 to 1 January 2017;

C — The net profit earned within a reporting period from 1 January 2008 to 1 January 2017;

D — The value of shares/stakes of the enterprise transferred to its partner in exchange for dividends from the net profit earned by such enterprise during the time from 1 January 2008 to 1 January 2017.

Expenses incurred or other payments not related to economic activities: The law provides a list of expenses that are not be considered to be related to economic activities, which are treated as deemed profit distributions, and the key categories of such expenses are the following:

• Undocumented expenses;

• Expenses that are not incurred for the purpose of deriving profit, income or compensation; and

18

• Interest payments on loans at a rate higher than the annual threshold rate defined by the Georgia Minister of Finance.

The new profit tax rules also set forth other types of payments that are subject to profit tax as deemed profit distributions, and the key categories of such payments are the following:

• Payments made for the acquisition of a debt security issued by a person resident in a low-tax jurisdiction, or by a person exempt from profit tax under Georgia’s Tax Code (except a budgetary organization, legal entity of public law — the Deposit Insurance Agency and the National Bank of Georgia);

• Payments of penalties/fines arising from contractual relationships or advance payments made to a person resident in a low-tax jurisdiction, or to a person exempt from profit tax under Georgia’s tax code (except a budgetary organization, legal entity of public law — the Deposit Insurance Agency and the National Bank of Georgia);

• Capital contributions or payments made to purchase share/interest (excluding the purchase of the share/interest placed at the stock exchange recognized by a foreign country), for the right to participate in the equity

of a nonresident or a person exempt from profit tax under the tax code;

• Issuance of loans or payments made for the acquisition of a claim toward a person resident in a low-tax jurisdiction, or a person exempt from profit tax under Georgia’s tax code (except a legal entity of public law — the Deposit Insurance Agency and the National Bank of Georgia). This rule will not apply to commercial banks, credit unions, insurance organizations, microfinance organizations and pawnshops; and

• Issuance of loans to a resident individual or a nonresident, or (excluding the purchase of the debt securities placed at the stock exchange recognized by a foreign country) is subject to profit tax. Herewith, the funds available on bank account for securing loans issued by third party to partner individual or partner nonresident is also subject to profit tax.

In this case the amount of the tax base is defined by the amount of such funds available on bank account for securing the loan (this rule will not apply to commercial banks, credit unions, insurance organizations, microfinance organizations and pawnshops).

However, where actual payments are made in relation to an acquired debt security, equity participation or claim

Guide to Taxation and Investment in Georgia 2018

19

transfer or, in the case of loans/advance payments, where the provision of the funds available on bank account for securing loans is cancelled or goods/services are delivered in exchange for the advance payments, the entity that was subject to tax on the deemed profit distribution is entitled to claim an offset and refund of the profit tax incurred in the reporting period of the deemed distribution.

The list of countries that shall be deemed low-tax jurisdictions is defined by a decree N615, issued by the government on 29 December 2016.

Gratuitous supplies of goods/services and/or transfers of funds: According to the law, a supply of goods/services that is not made for the purpose of deriving profit, income or compensation are considered to be a gratuitous supply that is subject to tax as a deemed profit distribution. A shortage of inventory or fixed assets also are deemed to be a gratuitous supply of such goods at the time when the shortage is identified.

The following are major exceptions to the gratuitous supply of goods/services rules, which are not be subject to profit tax:

• Donations made to a charitable organization during a calendar year, which do not exceed 10% of the net profit derived during the previous calendar year;

• Gratuitous transfers of goods or funds that already have been taxed at source, and

• Gratuitous supplies of goods/services or transfers of financial resources to the government, municipalities or legal entities under public law.

Representation expenses: According to the law, the maximum amount of representation costs incurred during the calendar year shall be 1% of the income received during the previous year (1% of expenses incurred, if the expenses exceed the income); any excess costs shall be treated as a deemed distribution of profits. The maximum amount of representation costs incurred in the year of incorporation shall be 1% of expenses incurred by the end of the current calendar year.

Legal entities to whom new profit tax rules do not apply

Old profit tax rules will continue to apply to Organizations according to the Tax Code, BTC and SCP participants, Production Sharing Agreement (PSA) contractors and to a person on profit gained in case of organizing a betting house in a systemic-electronic form. Herewith Commercial banks, credit unions, insurance organizations, microfinance organizations and pawnshops will shift to new profit tax rules as from January 2019.

20

Taxable Income Legal entities to whom new profit tax rules do not apply are taxed on profit, which is determined as gross income from economic activities less allowable deductions, at a flat rate of 15 percent. For Georgian enterprises gross income includes all income, regardless of its source or place of payment, except for income specifically exempt under the Tax Code.

Deductible ExpensesThe Tax Code allows some expenses incurred in the course of economic activities to be deducted from gross income earned from such activities. Expenses not connected with economic activities, personal expenses, and entertainment expenses are not deductible (unless entertainment is considered to be the taxpayer’s economic activity and the expenses are connected therewith). In addition to the limitations of deductibility provided in the Tax Code, the norms issued by the Ministry of Finance of Georgia also limit the extent of business trip expenses.

The Tax Code provides rules and limitations relating to specific deductions. A list of some specific allowable deductions is as follows: interest subject to limitations, doubtful debts, insurance reserve funds, scientific research, depreciation of fixed and intangible assets, repairs, insurance payments, prospecting and extraction

of resources, taxes and fines subject to limitations, representative expenses and losses on the sale of property.

Deductibility of Interest ExpenseAny interest expense paid or incurred by the taxpayer in the course of his business activities is generally deductible. However, there are some interest deductibility limitations. The interest expense paid and/or payable (using the accruals method) on credit (loan) did not exceed 24 % of the credit (loan) per annum is deductible.

Depreciation and Amortization AllowanceThe Tax Code provides general rules for the calculation of depreciation charges and the deductibility of fixed assets for corporate income tax purposes. The tax legislation gives a taxpayer an option either to deduct depreciation charges calculated on fixed assets over a period of time or fully deduct the cost of purchase (production) of such assets immediately.

In the event that the taxpayer employs the above mentioned right in respect of fully deduction of cost of fixed assets, it should continue to use the same method in the future during five years, for all purchased or produced fixed assets for the corporate income tax purposes. Taxpayers are entitled to deduct from gross income the full purchase or production cost of a purchased or produced fixed

Guide to Taxation and Investment in Georgia 2018

21

asset in the year when they were put into exploitation.

Generally, depreciation allowances are permitted for all capital assets, including fixed and intangible property, except for land, art (including but not limited to paintings, jewelry and antiques), museum items, historical objects (except for buildings), biological assets and any other assets that are not subject to wear and tear. In addition, a fixed asset with a value lower than 1,000 GEL is not subject to depreciation. Such assets should be fully deducted from gross income in the accounting year when they are purchased or produced.

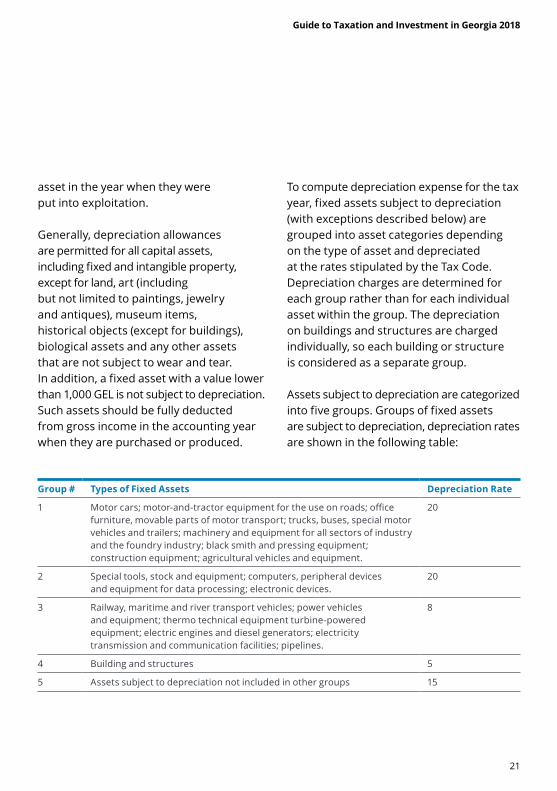

To compute depreciation expense for the tax year, fixed assets subject to depreciation (with exceptions described below) are grouped into asset categories depending on the type of asset and depreciated at the rates stipulated by the Tax Code. Depreciation charges are determined for each group rather than for each individual asset within the group. The depreciation on buildings and structures are charged individually, so each building or structure is considered as a separate group.

Assets subject to depreciation are categorized into five groups. Groups of fixed assets are subject to depreciation, depreciation rates are shown in the following table:

Group # Types of Fixed Assets Depreciation Rate

1 Motor cars; motor-and-tractor equipment for the use on roads; office furniture, movable parts of motor transport; trucks, buses, special motor vehicles and trailers; machinery and equipment for all sectors of industry and the foundry industry; black smith and pressing equipment; construction equipment; agricultural vehicles and equipment.

20

2 Special tools, stock and equipment; computers, peripheral devices and equipment for data processing; electronic devices.

20

3 Railway, maritime and river transport vehicles; power vehicles and equipment; thermo technical equipment turbine-powered equipment; electric engines and diesel generators; electricity transmission and communication facilities; pipelines.

8

4 Building and structures 5

5 Assets subject to depreciation not included in other groups 15

22

In accordance with the Tax Code, taxpayers are allowed to use an accelerated depreciation method for asset groups 2 and 3, provided that the accelerated depreciation rates do not exceed the rates specified for these groups, more than twofold.

Expenses related to intangible assets should be deducted in the form of depreciation (amortization) charges in proportion to their limited useful life. If it is impossible to determine the useful life of an intangible asset, such an asset should be depreciated at the rate of 15%. Intangible assets should be recorded as a separate group. Expenses related to the purchase or production of intangible assets should not be included in the value of intangible assets subject to depreciation, provided that they were deducted from the taxable income (profit) of a taxpayer.

Deductibility of Repair ExpensesThe Tax Code provides a deduction for expenses incurred in connection with the repair of fixed assets. Repairs, which neither add material value to the asset, nor significantly prolong its life, but keep it in an efficient operating condition, are considered repairs for tax legislation purposes. Conversely, repairs that are in the nature of replacements, to the extent that they slow deterioration and significantly prolong the life of the property, must be

capitalized and depreciated in accordance with the provisions of the Tax Code. The maximum deduction for repair expenses is 5 percent of the balance of each asset group at the end of the tax year, provided adequate documentation of the expenses is provided. Any repairs incurred that exceed 5 percent are added to the balance of the asset group and depreciated. However, if an entity uses a 100% depreciation deduction method, then repair expenses should be deducted in full from taxable gross income.

As we have mentioned above, expenses that do not increase the standard (normative, original) performance of fixed assets are considered to be general expenditure. As such, these expenses do not represent repair expenses for taxation purposes and therefore can be deducted in full from gross income.

Statute of limitation The statute of limitation for taxes is three years, however, it is extended by one year if a taxpayer files a tax return (including, an amended one), or submits a taxpayer’s claim within one year that is remaining before expiration of the statute of limitation period. In case of carrying forward the loss for three or more years, the statute of limitation is extended by more than 1 year of the loss carry forward period.

Guide to Taxation and Investment in Georgia 2018

23

The limitations on Carrying Forward of LossesIn accordance with the Tax Code, legal entities to whom new profit tax rules do not apply are entitled to carry forward prior year losses for a period of up to five years and set off losses against gross income of future periods.

Further, a taxpayer can elect a 10-year loss carry forward period, where the statute of limitation is increased from 5 to 11 years. A 10-year carry forward period can still be changed to a 5-year carry forward period when the losses carried forward are used up.

The Tax Code limits the loss carry forward if it occurs in the period of using status of the international financial company by the financial institution.

Tax Accounting RulesThe Tax Code requires that legal entities should maintain accurate records of their income and expenses under a cash or an accrual method of accounting. However, the taxpayer must use the same method for both financial and tax purposes, and be consistent in using the chosen method throughout the tax year. The taxpayer has to record all transactions connected with its activities. At the same time, the contents of a transaction,

its subject, amount and the titles of parties participating in this transaction are to be described completely and clearly in the primary reporting documentation.

Any primary accounting document for taxation purposes is considered to be a document if it has a date and amount of the transaction, reflects the requisites of the parties to the transaction and contains a description of the transaction, there should be at least two identical copies of any such document. A taxpayer is required to keep primary accounting documents for at least three years following the year when the document was issued.

Cash methodUsing the cash method of accounting a taxpayer is required to record income upon its actual receipt, regardless of when the income was earned. Expenses are recorded when payment is made rather than when the expense was incurred.

Accruals methodContrary to the cash method, the general rule under the accruals method of accounting requires a taxpayer to record income when it is earned (a moment of supply of goods/service) regardless of when it is actually received. Expenses are recorded when incurred rather than when the expense is paid.

24

Taxation of Nonresidents of GeorgiaTax Jurisdiction over NonresidentsForeign enterprises may also be subject to profit tax in Georgia. The extent to which a foreign enterprise is subject to profit tax depends on whether it conducts its activities through a permanent establishment or not.

Taxation of Nonresident’s Permanent Establishment in GeorgiaForeign enterprises carrying out economic activities through a permanent establishment in Georgia are subject to profit tax on distributed income received from Georgian sources relating to the activities performed by its permanent establishment.

Permanent Establishment (PE)Pursuant to the Tax Code a permanent establishment of a foreign enterprise or non-resident individual in Georgia is recognized as a defined location on the territory of Georgia, through which they fully or partially carry out an entrepreneurial activity, including activity conducted through an authorized person.

The following are specifically considered to create a permanent establishment: construction sites, assembly or building facilities, and the exercise of controlling activities connected with such facilities; installations or sites, drilling equipment

or ships used for surveying of natural resources, as well as the exercise of controlling activities connected with such facilities; a permanent base where a non-resident physical person carries out entrepreneurial activity; place of management of a foreign enterprise, branch, representative office, department, bureau, office, agency, workshop, mine, pit, other place for extraction of natural resources, any other separate unit or place of such enterprise’s activity.

If a foreign enterprise or non-resident physical person carries out entrepreneurial activity in Georgia through an intermediary, agent or broker having professional status defined by the Georgian legislation who is not authorized to conduct negotiations or sign agreements (contracts) on behalf of this foreign enterprise or non-resident physical person, then the activities of such an intermediary, agent or broker do not create a permanent establishment of this foreign enterprise or non-resident physical person in Georgia.

The possession of securities and shares in capital, ownership of property on the territory of Georgia by a foreign enterprise, if other features of a permanent establishment do not exist, cannot be regarded as a basis for the creation of a permanent establishment.

Guide to Taxation and Investment in Georgia 2018

25

The fact of execution of an agreement by a foreign company, which envisages the joint activity of parties to the contract being performed, fully or partly, on the territory of Georgia, cannot be regarded as a basis for the creation of a permanent establishment.

The mere fact of the assignment by a foreign enterprise of its staff for employment in another enterprise or organization on the territory of Georgia, if other features of a permanent establishment do not exist, does not lead to the creation of permanent establishment, if such employees will act on behalf of that enterprise and protect the rights of the enterprise where they are assigned.

An establishment of a Georgian enterprise in Georgia is not considered a PE of foreign company if it is used only to do the following: store or demonstrate goods or products belonging to the foreign enterprise; keep a stock of goods or products belonging to the foreign enterprise only for the purpose of their processing by another person; purchase goods or products or collect information for the foreign enterprise; any other activities that are preparatory or auxiliary in nature coming from the interests of the foreign enterprise; on behalf of a foreign company for the preparation and/or merely signature of loan agreements, contracts for the supply of goods or which have the nature of technical services.

A permanent establishment of a foreign enterprise in Georgia is considered as such from the time of its registration with the tax agency, providing it with relevant authority or commencing of representational activities. The responsibility to register a permanent establishment of a foreign enterprise lies with the tax authority, which is responsible for creating the relevant registry. The procedure for running the registration and a registry is developed by the Ministry of Finance of Georgia.

Taxation of Income Not Related to a Permanent EstablishmentForeign companies not engaged in economic activities through a permanent establishment are subject to withholding tax on gross income from Georgian sources. No deductions from this income are allowed, and the tax is withheld at the source of payment. However, the Tax Code allows non-resident taxpayers who receive certain types of income to file a return and claim any deductions allowable as if this income was connected with a permanent establishment.

The following withholding tax rates normally apply to the following items of income from Georgian sources payable to nonresidents, provided that such income is not attributable to a nonresident’s permanent establishment in Georgia:

26

Income from Georgian Sources Current Tax Rate

Dividends 5%

Interest 5%

Oil and gas subcontractors 4%

International telecommunication and transportation services 10%

Royalties 5%

Management fees 10%

Income received in the form of wages 20%

Payments to non-residents of other Georgian source service related income not connected to their PE in Georgia

10%

If a non-resident is registered in an offshore or low tax jurisdiction, interest, royalty and service fee payments will be subject to withholding tax at the rate of 15%.

Dividends are subject to withholding tax if they are paid to individuals or foreign entities. It should be mentioned that dividends paid to Georgian legal entities are exempt from withholding tax at the source of payment and dividends received by entrepreneurial legal entities should not be included in their taxable gross income.

Georgian Source IncomeFor profit tax purposes, the following income types are treated as received from Georgian sources:

Interest Income — interest on debt obligations issued by a resident entity

or permanent establishment of foreign company;

Dividends Income — dividends from a resident entity;

Royalty Income — royalties received from a resident entity;

Income from Immovable Property — income from the sale of immovable property located in Georgia;

Other Income — some other types of income.

Taxation of Cross-Border TransactionsOutbound TransactionsSince resident entities are taxable on their worldwide income in Georgia and may also be taxable by foreign states on their income

Guide to Taxation and Investment in Georgia 2018

27

derived from sources or from carrying on business in such states, the same income is potentially subject to double taxation. In terms of domestic tax law, profit tax paid outside Georgia is credited upon payment of tax in Georgia. Excess foreign tax credit may neither be offset against resident taxpayer’s Georgian tax liabilities on any domestic source income, nor can they be carried forward or backward.

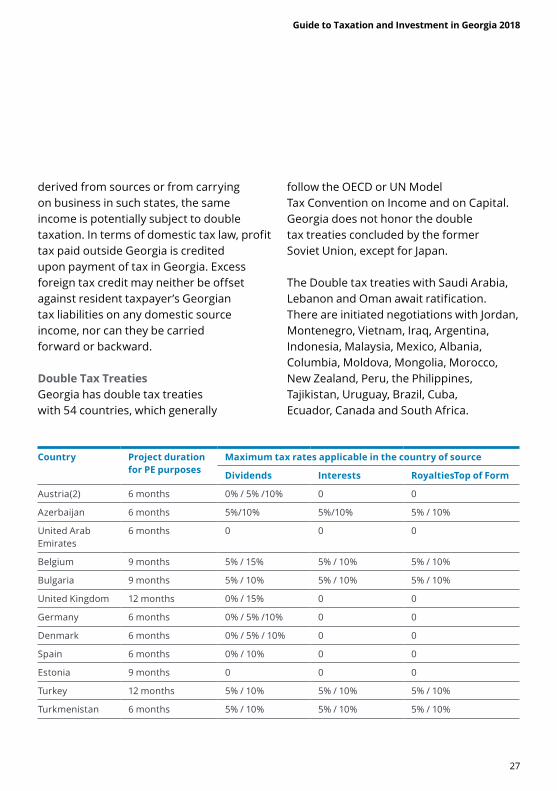

Double Tax TreatiesGeorgia has double tax treaties with 54 countries, which generally

follow the OECD or UN Model Tax Convention on Income and on Capital. Georgia does not honor the double tax treaties concluded by the former Soviet Union, except for Japan.

The Double tax treaties with Saudi Arabia, Lebanon and Oman await ratification. There are initiated negotiations with Jordan, Montenegro, Vietnam, Iraq, Argentina, Indonesia, Malaysia, Mexico, Albania, Columbia, Moldova, Mongolia, Morocco, New Zealand, Peru, the Philippines, Tajikistan, Uruguay, Brazil, Cuba, Ecuador, Canada and South Africa.

Country Project duration for PE purposes

Maximum tax rates applicable in the country of source

Dividends Interests RoyaltiesTop of Form

Austria(2) 6 months 0% / 5% /10% 0 0

Azerbaijan 6 months 5%/10% 5%/10% 5% / 10%

United Arab Emirates

6 months 0 0 0

Belgium 9 months 5% / 15% 5% / 10% 5% / 10%

Bulgaria 9 months 5% / 10% 5% / 10% 5% / 10%

United Kingdom 12 months 0% / 15% 0 0

Germany 6 months 0% / 5% /10% 0 0

Denmark 6 months 0% / 5% / 10% 0 0

Spain 6 months 0% / 10% 0 0

Estonia 9 months 0 0 0

Turkey 12 months 5% / 10% 5% / 10% 5% / 10%

Turkmenistan 6 months 5% / 10% 5% / 10% 5% / 10%

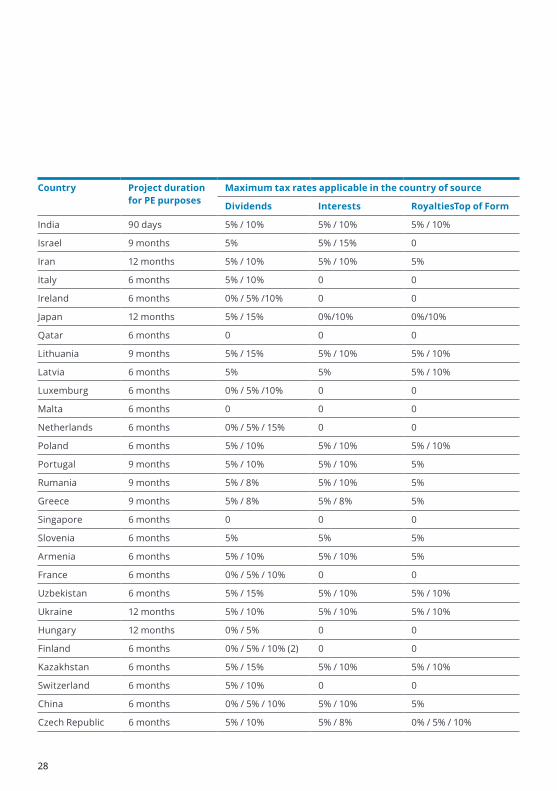

28

Country Project duration for PE purposes

Maximum tax rates applicable in the country of source

Dividends Interests RoyaltiesTop of Form

India 90 days 5% / 10% 5% / 10% 5% / 10%

Israel 9 months 5% 5% / 15% 0

Iran 12 months 5% / 10% 5% / 10% 5%

Italy 6 months 5% / 10% 0 0

Ireland 6 months 0% / 5% /10% 0 0

Japan 12 months 5% / 15% 0%/10% 0%/10%

Qatar 6 months 0 0 0

Lithuania 9 months 5% / 15% 5% / 10% 5% / 10%

Latvia 6 months 5% 5% 5% / 10%

Luxemburg 6 months 0% / 5% /10% 0 0

Malta 6 months 0 0 0

Netherlands 6 months 0% / 5% / 15% 0 0

Poland 6 months 5% / 10% 5% / 10% 5% / 10%

Portugal 9 months 5% / 10% 5% / 10% 5%

Rumania 9 months 5% / 8% 5% / 10% 5%

Greece 9 months 5% / 8% 5% / 8% 5%

Singapore 6 months 0 0 0

Slovenia 6 months 5% 5% 5%

Armenia 6 months 5% / 10% 5% / 10% 5%

France 6 months 0% / 5% / 10% 0 0

Uzbekistan 6 months 5% / 15% 5% / 10% 5% / 10%

Ukraine 12 months 5% / 10% 5% / 10% 5% / 10%

Hungary 12 months 0% / 5% 0 0

Finland 6 months 0% / 5% / 10% (2) 0 0

Kazakhstan 6 months 5% / 15% 5% / 10% 5% / 10%

Switzerland 6 months 5% / 10% 0 0

China 6 months 0% / 5% / 10% 5% / 10% 5%

Czech Republic 6 months 5% / 10% 5% / 8% 0% / 5% / 10%

Guide to Taxation and Investment in Georgia 2018

29

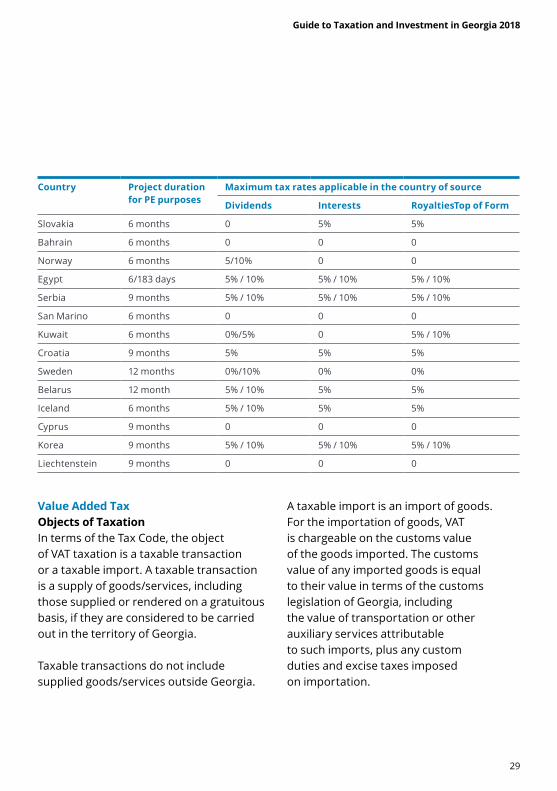

Country Project duration for PE purposes

Maximum tax rates applicable in the country of source

Dividends Interests RoyaltiesTop of Form

Slovakia 6 months 0 5% 5%

Bahrain 6 months 0 0 0

Norway 6 months 5/10% 0 0

Egypt 6/183 days 5% / 10% 5% / 10% 5% / 10%

Serbia 9 months 5% / 10% 5% / 10% 5% / 10%

San Marino 6 months 0 0 0

Kuwait 6 months 0%/5% 0 5% / 10%

Croatia 9 months 5% 5% 5%

Sweden 12 months 0%/10% 0% 0%

Belarus 12 month 5% / 10% 5% 5%

Iceland 6 months 5% / 10% 5% 5%

Cyprus 9 months 0 0 0

Korea 9 months 5% / 10% 5% / 10% 5% / 10%

Liechtenstein 9 months 0 0 0

Value Added TaxObjects of TaxationIn terms of the Tax Code, the object of VAT taxation is a taxable transaction or a taxable import. A taxable transaction is a supply of goods/services, including those supplied or rendered on a gratuitous basis, if they are considered to be carried out in the territory of Georgia.

Taxable transactions do not include supplied goods/services outside Georgia.

A taxable import is an import of goods. For the importation of goods, VAT is chargeable on the customs value of the goods imported. The customs value of any imported goods is equal to their value in terms of the customs legislation of Georgia, including the value of transportation or other auxiliary services attributable to such imports, plus any custom duties and excise taxes imposed on importation.

30

VAT RatesThe VAT rate applicable in Georgia is 18%, referred to as the standard rate, which is applied to most goods/services. Certain transactions are exempt from taxation. There are two types of exempted transactions: transaction exempted with or without the right to recover input VAT. The export of goods is exempted with the right to recover input VAT, while import of certain medicine, passenger cars, publications, mass media and baby products are exempted without the right to recover input VAT.

Time of Taxable TransactionPursuant to the Tax Code, a VATable transaction occurs at the time of a supply of goods (services) and in the case of a supply of goods involving loading, the time of loading. However, it should not be later than the time when compensation was paid to a supplier of goods/services in advance.

If goods or services are supplied on a regular or a continuous basis, the time when a tax invoice for any part of such a transaction was issued or payment was made should be deemed to be the time of the supply of goods or services, but no later than the last working day of the reporting month.

Place of Taxable TransactionA taxable transaction for VAT purposes is a supply of goods (rendering of services) that is performed on the territory of Georgia.

According to the Tax Code, if the recipient and supplier of services are located in different countries, the place of supply for VAT purposes includes the following: a place of registration of the recipient of services or the place of management or the location of a permanent establishment of the recipient of services, assuming that the services are directly related to such permanent establishment. The mentioned provision of the tax law is applicable to supply of intangible assets, consulting, legal, accounting, engineering, advertising and staffing services, as well as telecommunication, radio and television broadcasting, data processing, electronically provided services, and other similar services.

VAT InvoiceVAT payers making taxable supply are required to issue a VAT invoice to customers no later than 30 calendar days after the customers’ notice. The VAT invoice is a strict reporting document approved by the Ministry of Finance of Georgia that confirms the fact of carrying out of VATable transaction. A tax invoice is issued in electronic form.

Guide to Taxation and Investment in Georgia 2018

31

VAT AdministrationRemittanceVAT on domestic supplies and the importation of goods/services is administered by the tax authorities.

Any taxable person should assess the amount of VAT to be remitted to the budget by reducing (“crediting”) its output VAT liability (VAT collected on outward taxable supplies) with input VAT credit (VAT incurred on inward taxable supplies and import supplies).

VAT Credit Any input VAT incurred by a taxable person on inward domestic supplies and imported supplies is creditable against its output VAT liabilities, provided the such input VAT was incurred for taxable imports and taxable transactions where the goods or services are used or to be used for the purposes of the taxpayer’s economic activity, even if they are not included in production costs.

In case VAT taxpayers have taxable transactions and VAT exempt transactions in accordance with the Tax Code, the VAT credit is determined in accordance with the amount of goods (services) which were used in the taxable transactions.

If such differentiation is impossible, the VAT credit is determined on the basis

of the ratio of the exempt supplies, with the right to reclaim input VAT to the total turnover of the month. VAT creditable on the ratio basis should be adjusted pursuant to the December tax return of the current year, when the exact ratio of annual taxable and exempt turnover must be determined.

If fixed assets are used in exempt transactions both with or without the right to reclaim input VAT, and the input VAT cannot be directly attributed to these transactions, in this case the input VAT is recoverable in full in the first reporting period, if exempt supplies without the right to reclaim input VAT are less than 20% of total turnover of the previous tax year. The recoverable VAT is adjusted by the end of each calendar year in proportion to the exempt supplies, with the right to reclaim input VAT in total turnover of the respective calendar year.

If exempt supplies without the right to reclaim input VAT are more than 20% of total turnover of the previous tax year, input VAT on fixed assets is recoverable only in the last reporting period of a tax year, in proportion to the exempt supplies with the right to reclaim input VAT in total turnover of this calendar year.

It should be noted that VAT credit is not allowed if it was paid out for: charity,

32

social and entertainment events; goods / services are used to produce VAT exempt goods / services; on tax invoice that was not reported to a tax agency.

Tax RefundsSince export supplies are exempt with VAT input right, any taxable person making supplies for use or consumption outside of Georgia may claim as a credit its input VAT incurred in connection with exported supplies. Although the excess credit is refundable, in fact, VAT refunds are difficult to obtain in Georgia.

A surplus of the VAT creditable over the VAT assessed in the reporting period can be offset against the future tax liabilities or be refunded within one month period.

VAT Refund Procedures for VAT payer of EU State Member

• A foreign enterprise registered as a VAT payer in EU member state can reclaim VAT incurred for purchase of services/goods (except immovable property) or for import of goods in Georgia provided that:

– the services/goods are carried out in VATable transaction;

– the foreign enterprise is not engaged in economic activity in Georgia through its PE or its fixed place of activity or PE is not Georgia;

– engaged in the same or similar activities, Georgian enterprise registered as a VAT payer would be entitled to reclaim the input VAT.

VAT Refund Procedures for Foreign NationalsForeign nationals are entitled to claim a VAT refund paid on goods purchased in the territory of Georgia at the time of the export of the goods out of Georgian borders, provided that the goods are exported within 3 months after the purchase and the value of the goods per one receipt exceeds GEL 200 (excluding VAT).

To receive the tax refund, foreign individuals have to submit to the tax authorities a receipt in the form officially approved by the Ministry of Finance of Georgia. The refund procedures, a list of goods subject to VAT refund, and criteria for sellers to be entitled to issue the receipts are determined by the Ministry of Finance of Georgia.

Excise TaxGeneral RulesAll physical and legal persons producing excisable goods in the territory of Georgia, or importing excisable goods are subject to excise taxes. For the excisable goods produced or manufactured in the territory of Georgia from raw materials supplied by customers, the producer of the goods is subject to excise taxes.

Guide to Taxation and Investment in Georgia 2018

33

Since excise duty is an indirect tax, any excise duty paid in connection with exported items produced in Georgia may normally be refunded to the exporter. Excise tax is imposed on wine, beer and liquors (whiskey, vodka, etc.); cigarettes and other tobacco products; cars; natural gas, oils, oil distillates, and other products produced from oil and bituminous minerals. International calls received in mobile and home phones are subject to GEL 0.15 and GEL 0.08 per minute respectively.

Time of Taxable TransactionIn respect of the production of the excisable goods in Georgia, the time of a taxable transaction is considered to be the time of a supply (transfer) of goods. In the case of import, the tax point is deemed to be the time of import. The moment of supply of goods is deemed to be the time of a taxable transaction in respect of the excisable goods subject to stamping.

Excise StampsUnder domestic tax law, the mandatory affixing of excise stamps is required for the imported and locally produced alcoholic beverages designated for consumption in Georgia, including beer, with a strength of higher than 1.15 degrees (other than beverages of 50 grams and less as well as those bottled in vessels of 10 liters and more), and tobacco products except for pipe tobacco.

According to the Tax Code, it is prohibited to supply and import the excisable goods without excise stamps under a free circulation regime into the territory of Georgia. The tax authorities controlling excise payments shall seize unstamped imported goods and provided for the sale of excise goods in accordance with the established procedure. From the moment of seizure the goods are deemed to be state property.

In case goods are imported or/and supplied without excise stamps (due to loss, destruction, etc., except for force major circumstances), the goods are considered to be imported or/and supplied and shall be taxed in accordance with the legislation of Georgia. In case of failure to import goods during six months after having received the excise stamps, an importer is required to return them.

Failure to return excise stamps within the mentioned period shall be deemed as an import or supply of the excisable goods subject to excise stamping in the territory of Georgia and shall be taxed accordingly. In the following period when importing the excisable goods marked with non-returned excise stamps, the amount of taxes due must be calculated pro rata to the amount of actually imported goods.

34

Local TaxesThe property tax is a local tax and comprises land tax and property tax of individuals and enterprises.

Local self-government bodies are entitled within their authority to establish local taxes in the respective territory within the maximum limit stipulated by the Tax Code.

Property TaxesProperty Tax of Physical PersonsPhysical persons’ taxable object of the property tax (except for land) includes fixed assets used for economic activities, immovable property (building or a part of it) and construction in progress, also yachts (motor boats), helicopters, airplanes and vehicles under Code 8703 of the National Commodity Nomenclature of Foreign Economic Activities.

The property tax rates are differential and are based on the amount of annual income of the physical person, regardless of his/her tax residency status, from sources in Georgia and outside the country. Property tax rate is between 0.05- 0.2% of the fair market value of the property that is located in Georgia if the individual’s family worldwide income will be from GEL 40,000 to GEL 100,000 during

the reporting calendar year. If, however, such annual income will exceed GEL 100,000 the tax rate will be between 0.8- 1 percent.

The individual is required to submit the tax return before the 1st of November following the reporting calendar (tax) year and pay the tax to the tax authorities before 15th of November of the same year.

Property Tax of Georgian enterprisesPayers of property tax, other than physical persons, include Georgian enterprises, and foreign enterprises engaged in economic activity in Georgia through permanent establishments, organizations whose property or part of property is used for economic activity. For foreign enterprises, property tax is imposed only on property located in Georgia.

The fixed assets, investment property, uninstalled equipment and construction in progress that are listed on the balance sheet of the enterprise, as well as similar property listed on the balance sheet of an organization and utilized for economic activity are, unless specifically exempt, subject to property tax at a flat 1% rate of the average annual net book value of the property.

Guide to Taxation and Investment in Georgia 2018

35

In order to arrive at the taxable base, the net book value of immovable property recorded in the balance sheet of a company at the beginning and end of the year 2018, which were purchased before the year 2000, between 2000-2004 and in 2004 should be multiplied by 3, 2 and 1.5 respectively. However these coefficients are not applicable to the certain state owned companies and to a Georgian company if the company records its immovable property based on revaluation method and the financial statements are audited by an audit company that is included in the list published by the Government.

Land Tax Physical and legal persons, who are owners or users of state owned land plots, including land used for agricultural and non-agricultural purposes, are subject to land tax. The land tax depends on the quality and location of land and is not based on the taxpayer’s economic results.

The base maximum annual rate for the non-agricultural land amounts to GEL 0.24 per one square meter. The tax must be calculated by multiplying the annual base tax rate by the territorial coefficient and the land area. The differentiation of the land tax by territorial coefficient is made in accordance with location and zones of the land plot.

Tax returns should be submitted by a physical person and legal entity no later than 1st of November and 1st of April of reporting year respectively.

Other TaxesFee for the Use of Natural ResourcesPhysical and legal persons (including branches of foreign companies) engaged in any activity that requires a license for the use of natural resources (except for land) owned by the state as well as persons engaged in the timber industry are subject to a fee for the use of natural resources.

The fee is imposed on the volume of natural resources (such as minerals and timber) extracted, and the tax rates are based on the resources extracted. Pursuant to the Law of Georgia “On Fee for the Use of Natural Resources”, some types of activities are granted a 70% reduction in the fee rate.

Fee on Gambling BusinessThe fee on gambling is paid by persons that carry out entrepreneurial activities by organizing lotteries, operating casinos, and other gambling business and are granted permits and/or licenses to carry out such activities by virtue of the Georgian legislation.

36

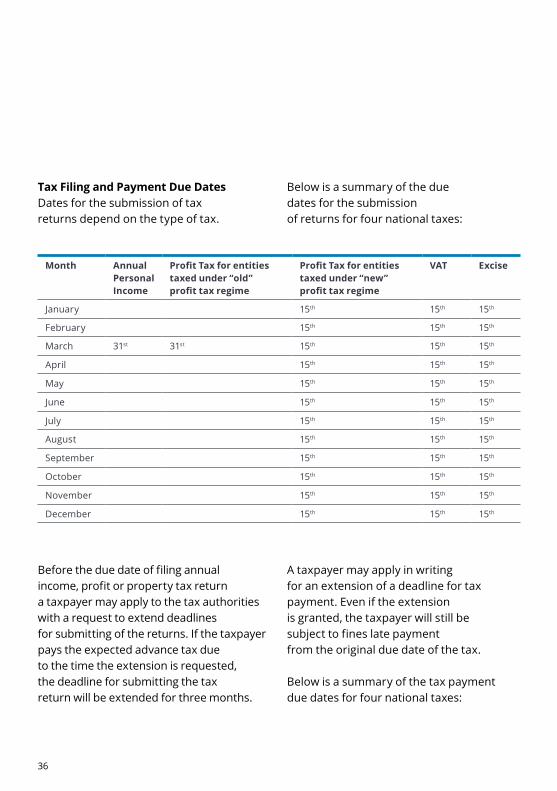

Before the due date of filing annual income, profit or property tax return a taxpayer may apply to the tax authorities with a request to extend deadlines for submitting of the returns. If the taxpayer pays the expected advance tax due to the time the extension is requested, the deadline for submitting the tax return will be extended for three months.

A taxpayer may apply in writing for an extension of a deadline for tax payment. Even if the extension is granted, the taxpayer will still be subject to fines late payment from the original due date of the tax.

Below is a summary of the tax payment due dates for four national taxes:

Tax Filing and Payment Due DatesDates for the submission of tax returns depend on the type of tax.

Below is a summary of the due dates for the submission of returns for four national taxes:

Month Annual Personal Income

Profit Tax for entities taxed under “old” profit tax regime

Profit Tax for entities taxed under “new” profit tax regime

VAT Excise

January 15th 15th 15th

February 15th 15th 15th

March 31st 31st 15th 15th 15th

April 15th 15th 15th

May 15th 15th 15th

June 15th 15th 15th

July 15th 15th 15th

August 15th 15th 15th

September 15th 15th 15th

October 15th 15th 15th

November 15th 15th 15th

December 15th 15th 15th

Guide to Taxation and Investment in Georgia 2018

37

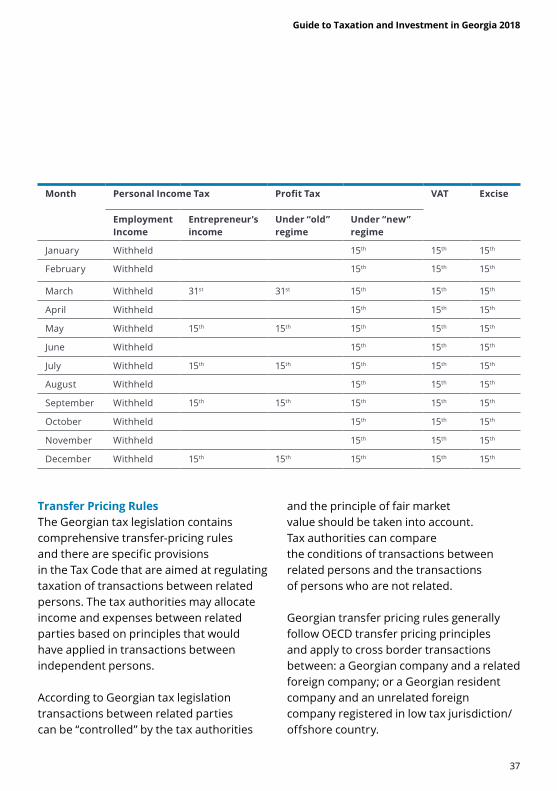

Month Personal Income Tax Profit Tax VAT Excise

Employment Income

Entrepreneur’s income

Under “old” regime

Under “new” regime

January Withheld 15th 15th 15th

February Withheld 15th 15th 15th

March Withheld 31st 31st 15th 15th 15th

April Withheld 15th 15th 15th

May Withheld 15th 15th 15th 15th 15th

June Withheld 15th 15th 15th

July Withheld 15th 15th 15th 15th 15th

August Withheld 15th 15th 15th

September Withheld 15th 15th 15th 15th 15th

October Withheld 15th 15th 15th

November Withheld 15th 15th 15th

December Withheld 15th 15th 15th 15th 15th

Transfer Pricing RulesThe Georgian tax legislation contains comprehensive transfer-pricing rules and there are specific provisions in the Tax Code that are aimed at regulating taxation of transactions between related persons. The tax authorities may allocate income and expenses between related parties based on principles that would have applied in transactions between independent persons.

According to Georgian tax legislation transactions between related parties can be “controlled” by the tax authorities

and the principle of fair market value should be taken into account. Tax authorities can compare the conditions of transactions between related persons and the transactions of persons who are not related.

Georgian transfer pricing rules generally follow OECD transfer pricing principles and apply to cross border transactions between: a Georgian company and a related foreign company; or a Georgian resident company and an unrelated foreign company registered in low tax jurisdiction/offshore country.

38

According to the Instructions a taxpayer should maintain contemporaneous transfer pricing documentations and submit them to the tax authorities upon their request within 30 calendar days. Georgia recognizes five pricing methods for evaluating whether prices are at arm’s length: comparable uncontrolled (independent) price; resale price; cost plus; net profit margin; and profit split. These pricing rules are based on the OECD transfer pricing methods.

Related PersonsPersons are recognized as related if special relations that exist among them may affect the conditions or economic results of their activities or activities of persons represented by them.

The tax authority is authorized to make a reasonable written decision on the use of the market price for taxation purposes if the parties involved in the transaction are related persons, except for cases when their relationship does not affect results of such transactions.

Market valueGeorgian Tax Legislation provides various rules to be employed by the tax authorities for defining the market value (price) of supplied services/goods.

The tax agency is also entitled to utilize state authorities’ official sources of information regarding market prices, information submitted by taxpayers to the tax administration and any other reliable information to determine the market price of goods (services).

Customs DutiesThe Tax Code regulates the taxation of the import and export of goods. Customs duties are payable upon the release of goods by Customs officials. In accordance with the Tax Code, the following fees are paid on the importation of goods:

Import taxGoods transferred through the customs of Georgia are subject to customs tax at the rates 0%, 5% or 12%. The customs tax depends on the type of goods being imported.

VATGoods imported into Georgia are subject to VAT in accordance with the Tax Code. The rate of VAT is 18 percent of the value of the imported goods.