UMS 20 MAR 2015 MOHD ROZLAN MOHAMED ALI Pengarah Unit Teknikal GST Persatuan Akauntan Percukaian Malaysia (M.A.T.A.) TREATMENT ON EDUCATION INDUSTRY GST Treatment on Education

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

UMS 20 MAR 2015

MOHD ROZLAN MOHAMED ALI Pengarah Unit Teknikal GST Persatuan Akauntan Percukaian Malaysia (M.A.T.A.)

TREATMENT ON

EDUCATION INDUSTRY

GST Treatment on Education

4

Private higher education

1

2

(a) Childcare, preschool, primary and secondary school by:

5

Ministry of Education/ other Ministries

GST IMPLICATION ON EDUCATION

3

4 Public Universities as statutory bodies

Private educational institutions(b) Tertiary education

Ministry of Education/ other Ministries

5

Any childcare, preschool, primary and secondary schools

Registered under the Education Act 1961/ 1996/ Child Centre Act 1984/ State Islamic Religious School Controlled Enactments 1988Follow the National Curriculum/ approved curriculum by Minister

Education sector

6

Tertiary education Establishment of the educational institutions under the Universities and University Colleges Act 1996, Private Higher Education 1996, University Technology Mara 1984, or any other written law

Education sector

3

GST Implication - Childcare, preschool, primary and

secondary school

7

MINISTRY OF EDUCATION/ OTHER MINISTRIES

1. Childcare2. National School / Government assisted school3. National type of school (Chinese) & (Tamil)4. Religious school 5. Boarding School (SBP)6. Technical / Vocational school

OUT OF SCOPE

INPUT(1) No GST charged by supplier on all goods acquired (2) GST charged and paid on services

OUTPUT NO GST charged to students

8

PRIVATE

1. Childcare2. Pre school3. Primary and secondary school4. Religious school 5. Technical / Vocational school

EXEMPT

INPUT(1) No GST charged by supplier on certain approved goods acquired under GST Relief Order 2014(2) To pay GST on goods not listed under the GST Relief Order 2014(3) To pay GST charged on services(4) No ITC claimable on GST paid

OUTPUT NO GST charged to students

9

GST Implication - Tertiary education

10

PUBLIC UNIVERSITIES /IPTA

STATUTORY BODIES

EXEMPT

INCORPORATED

INPUT(1) No GST charged by supplier on certain approved goods acquired under GST Relief Order 2014(2) To pay GST on goods not listed under the GST Relief Order 2014(3) To pay GST charged on services(4) No ITC claimable on GST paid on goods not listed in the GST Relief Order 2014

OUTPUT NO GST charged to students

11

PRIVATE UNIVERSITIES/ COLLEGE UNIVERSITIES/ ACADEMY/ INSTITUTE

EXEMPT

INPUT(1) No GST charged by supplier on certain approved goods acquired under GST Relief Order 2014(2) To pay GST on goods not listed under the GST Relief Order 2014(3) To pay GST charged on services(4) No ITC claimable on GST paid on goods not listed in the GST Relief Order 2014

OUTPUT NO GST charged to students

12

Private Educational Institutions (present treatment)

Private Educational Institutions

Suppliers of goods and services

1. Not listed under Sales Tax Exemption Order 2013 or2. Not listed under the Customs Exemption Order 2013

1.Subject to payment of duty import on any goods

2. Subject to payment of sales tax (5%/ 10% or specific) & services Tax (6%)

No Tax exemptionTo pay all sales tax & Services tax

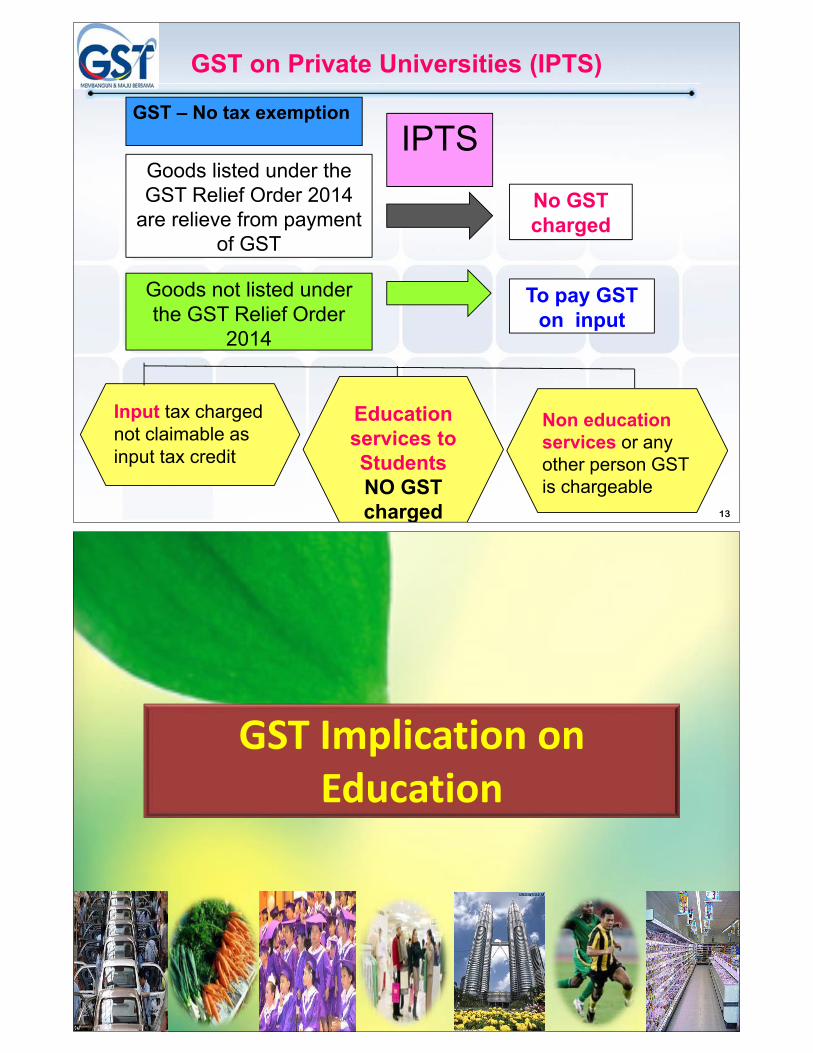

13

GST on Private Universities (IPTS)

IPTS

Input tax charged not claimable as input tax credit

GST No tax exemption

Goods listed under the GST Relief Order 2014

are relieve from payment of GST

No GST charged

Goods not listed under the GST Relief Order

2014

To pay GST on input

Education services to Students NO GST charged

Non education services or any other person GST is chargeable

GST Implication on Education

15

A

GST impacts on many aspects of theoperations of an educational institution

1) Pricing of, and quotes for, supplies of goods and services

2) Promotion of sales of goods and services3) Specific new clauses required when entering into

contractual arrangements4) Documentation received and produced5) The reporting

systems6) Internal control procedures required7) Incorrect handling of GST related matters can

cause financial loss to an organisation8) Staff of an educational body need to be trained

in how GST affects the organisation, and trained in aspects that affect their work.

16

A

The first steps that every educational body needs to take NOW to prepare for GST

1) Identifying all your inputs2) Identifying all your outputs 3) Classifying those inputs and outputsaccording to their GST treatment (that is, are they taxable supplies i.e. standard rate, zero rated , or exempt 4) Read the law, guides and ruling if any and identify any areas of uncertainty, and seek help from a professional adviser if necessary5) Consider your record keeping systems to

to scratchtrack and record all of these transactions6) Consider your accounting system

17

1

2

There are three types of supply transaction

Taxable supplies

SUPPLY OF GOODS AND SERVICES

3

GST is only paid on taxable suppliesSome supplies may be a mixture of transactiontypes and must be separated into identifiablecomponents

Zero rated supplies (exports)

Exempt supplies

18

1 Taxable supplies

SUPPLY OF GOODS AND SERVICES

Educational institutions must pay GST on taxablesupplies but :

a) Cannot claim input tax credit for makingeducation services

a) Can claim input tax credit for purchases usedto make taxable supplies.

19

1 Taxable supplies

SUPPLY OF GOODS AND SERVICES

Educational Institutions makes taxablesupplies if :a) The supply is made for payment;b) The supply is made in the course of

operating its business; andc) The supply is made in Malaysia

20

1 Taxable suppliesSUPPLY OF GOODS AND SERVICES

a) If Educational institution has made ataxable supply, it has to issue a full taxinvoice;

b) If an invoice contains more than onetraction then the invoice must also show :

Each taxable supplyThe amount of GST to be paid andThe amount to be paid for the totalsupply

21

Supply for paymentSUPPLY OF GOODS AND SERVICES

Payment is usually monetary, but has someother form of payment such as :

a) Goods and services provided instead ofmoney such as barter transactions or

b) Payment in the form of refraining fromdoing something

22

Supply made in MalaysiaSUPPLY OF GOODS AND SERVICES

A supply of goods made in Malaysia if the goodsare any of the following:a) Delivered or made available in Malaysia to the

purchaserb) Removed from Malaysia orc) Brought into Malaysia, provided the seller

either imports the goods into Malaysia orinstall or assembles the goods in Malaysia

23

Supply made in MalaysiaSUPPLY OF GOODS AND SERVICES

a) A supply of property eg land, building if theproperty is in Malaysia

b) A supply of something other than goods orproperty eg services, rightis in Malaysia if any of the following apply;

the thing is done in Malaysiathe seller makes the supply through a businessthey carry on in Malaysia orThe supply is of a right to purchase or acquiresomething that is in Malaysia

24

Supply of education services - exempt

Educational institution does notinclude GST in the price of educationservices and cannot claim input taxon taxable purchases used to makeeducation services

25

Education services - exemptItems which are exempt that relate to educationalinstitutions include:

Course of study in childcare, preschool,primary & secondary school;or Course fees for most tertiary courses,masters courses and doctoral coursesEducational course materialsStudents administration services fees directlyrelated to education servicesCompulsory excursions relating to aneducational course

26

Education services - exempt

Health services provided by generalpractitioners;Other health services includingcounselling and dental services;ExportsFinancial supplies e.g. bank interest,consideration on the sale of investmentsandRenting residential premises forresidential accommodation for students

27

Items which do not constitute as a supplySUPPLY OF GOODS AND SERVICES

Government appropriationOther appropriation where the monies received are notconsideration for any supplyResearch grants from government or others (with condition)Donations, prizes, sponsorships and scholarships(provided they are made voluntarily, there is no expectationof receiving anything in return and no material benefit to thedonorDividendsParking fines andInternal transaction between operational units within theschools or higher education

28

Adjusting eventSUPPLY OF GOODS AND SERVICES

Occur to supplies in the following instances:a) When the price of a supply changes after the

tax invoice has been raised or issued;b) When a taxable supply is cancelledc) When a bad debt is written off ord) When a previously written off bad debt is

recoveredWhen an adjusting event occurs it may result in an increase or decrease in the GST liability of educational institution and care should be taken to ensure that GST is correctly accounted for

29

Claiming GST credits for purchasesACQUISITION OF GOODS AND SERVICES

Educational institution can claim input tax creditsfor GST included a purchase if :a) The purchase is used wholly or mainly in

carrying out its business;b) The price includes GSTc) Educational institution is liable to provide

payment to the item purchased andd) Educational institution must have a tax

invoice from the supplier

30

GST credits cannot be claimedACQUISITION OF GOODS AND SERVICES

a) Educational institution cannot claiminput tax credits for GST purchase tomake education services supplies

b) Private use and non deductibleexpenses (entertainment for visitors)

c) Blocked inputs

31

1. If educational institution made taxable supply, it has to issue tax invoice

TAX INVOICE

a) For acquisition on education services, thetax invoice cannot be used to claim input tax

b) For acquisition on taxable supplies made,the tax invoice is used to claim GST paid tothe supplier

2. If educational institution acquire goods or services, it will receives tax invoices in two situations:

32

Tertiary course of study

Course of study is defined in the Education Act 1996

Establishment of the higher educational institutions is under the Universities and University Colleges Act 1996, Private Higher Education 1996, University Technology Mara Act 1984, or any other written law Accredited courses approved by MalaysianQualification Agency

33

The following accredited undergraduate orpostgraduate courses arei. Associate degreeii. Associate diplomasiii. Diplomasiv. Bachelor Degreesv. Bridging study for overseas studentsvi. Graduate study Bachelor degreesvii. Masters qualifying coursesviii. PhD

Tertiary course of study

34

The fees for the supply of educationcourse of study that consists oftuition and facilities and curriculumrelated education supplies, the fee isthe consideration for the exempteducation supply

Related education supplies

35

A single fee charged for the supply ofand education course of study willneed to be apportioned betweentaxable, exempt and zero rate supplyif it includes :a) A supply of membership to a

student organisation

Related education supplies

36

b) Supply by way of sales, lease or hire ofgoods other than course materialsc) Supply of accommodation as part of anexcursion or field trip;d) Supply of accommodation to tertiarystudents by the provider of the education; ore) Supply of food as part of accommodationprovided to tertiary students by the providerof the education

Related education supplies

37

Miscellaneous fees and charges

Educational institution chargesmiscellaneous fees of variousdescriptions.A fee for education course of study isexempt in respect of the provision offacilities and/or the supply ofadministration services directlyrelated to the supply of education

38

Miscellaneous fees and chargesThe provision of facilities which would beexempt include :

a) the provision of maintenance of plant,equipment, buildings and grounds;

b) Access to libraries including the access tolibrary books, periodicals and manuals;

c) Access to computer and sciencelaboratories;

d) Access to computers and other onlineresources

39

Miscellaneous fees and charges

Administration fees which is exemptinclude:a) Program changes and late enrolments;b) Late issue or replacement of student

cards;c) Printing academic transcripts, certificates

and statements;d) Overdue charges or late payments ande) Administration of the library

40

Course materialsIf University A charges a fee for the supply of course materialsas part of subjects undertaken then the supply is an exemptsupply. The following are examples of course materials ifsupplied by University A to students :

a) Photocopied or printed educational materials thatspecifically relate to the course

b) Course notes for a specific subject outlining thecourse contents, reading list, tutorial and seminartopic, assignment and essay questions;

c) Consumables art supplies such as paint, sketchpads

d) Ingredients used in a hospitality course ore) Chemical used in chemistry and related courses

41

The following are not considered to be coursematerials if supplied by educational institutionto students subject to any changes on the GSTOrders:a) Textbooksb) Musical instrumentsc) Computers and calculators andd) Sporting equipment

Course materials

42

SUPPLIES OF EDUCATION

Example:A a 1st year students studying a Bachelor of Economics arerequired to purchase a study guide which has beenrecommended by his lecturer. The guide is a collection ofpreviously published works from journals and other resourcesand other materials and includes the owncontributions. Its effective life is limited to the duration of thecourse which was offered by the University .As the study guide is a collection of materials extracted fromvarious textbooks and its useful life is limited to the durationof the course, the study guide is exempt provided it ispurchased from the University which are no sellable at anybook stores and in accordance with the course offered.

43

SUPPLIES OF EDUCATION

Example:Ahmad is enrolled in a Bachelor of Science course. Aspart of his assignment, he is required to provide 4duplicate copies to his lecturer. He goes to the libraryand is charged RM20 for the photocopying.

The photocopying service is not considered to becourse materials and it would therefore subject to GSTas in most universities photocopying is a business by3rd party.

44

Excursions and Field trips

If an excursion or field trip is directly related to thecourse of study the supply is exempt except for foodand accommodation suppliedAny supply of food as part of the excursion or fieldtrip whether it be supplied by educational institutionas the supplier of the course or by another supplier issubject to GST as it normally provided by caterer or3rd partyAny supply of accommodation as part of theexcursion or field trip whether it be supplied byeducational institution as the supplier of the course orby another supplier is subject to GST

45

Accommodation A supply of accommodation to students providedhalls or sponsored flats by the provider of theeducational institution is a supply of non commercialresidential accommodation.The accommodation provided to the students is anexempt supply. No GST will be payable on the supplyof accommodation provided to tertiary students andeducational institution will not be entitled to input taxfor any acquisition that relate to the supplyWhere food is supplied to students staying at theaccommodation is subject to GST as it is normallyprovided by 3rd party.

46

Exports Questions :1) What is the GST treatment if an employee of

educational institution for example MSU flies toUSA and performs research services in thatcountry?

2) IMU provides research assistance to an ITcompany in Dubai. The research assistancerelates to providing information on IT trends inMalaysia. The research work is carried out atIMU campus. What is the GST treatment?

47

Financial assistance payments

Funding is generally considered to besponsorship if educational institutionprovides advertising and promotionalactivities in return for payment which hasmaterial benefit to the payer.The sponsorship is a standard rated supplyand subject to GST

Sponsorship

48

Question :

1) University A enters into a formal agreement with Maybank. Thebank agrees to provide University A with RM300,000 a year for3 years to complete a project. In return for the paymentMaybank will receive the following benefits:

The University is obliged to acknowledge the sponsorshipon all advertisements, media and promotional materials;The relationship between The University and Maybank isacknowledge on the program websiteThe University is obliged to provide a guest speaker atpromotional events and function.

What is the GST treatment on the sponsorship by Maybank?

Sponsorship

49

Research Grants

Funding is provided to undertakeresearch will be subject to GST if thefindings of the research are of thematerial benefit

QQuueessttiioonnss????

Related Documents