GST – Registration Provisions including Business Process CA LGopal Shah Bhubaneswar, Odisha il l h h@ il Email: ca.lgshah@gmail.com M: 9437124361

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

GST – Registration Provisions including Business Process

CA LGopal ShahBhubaneswar, Odishail l h h@ ilEmail: [email protected]: 9437124361

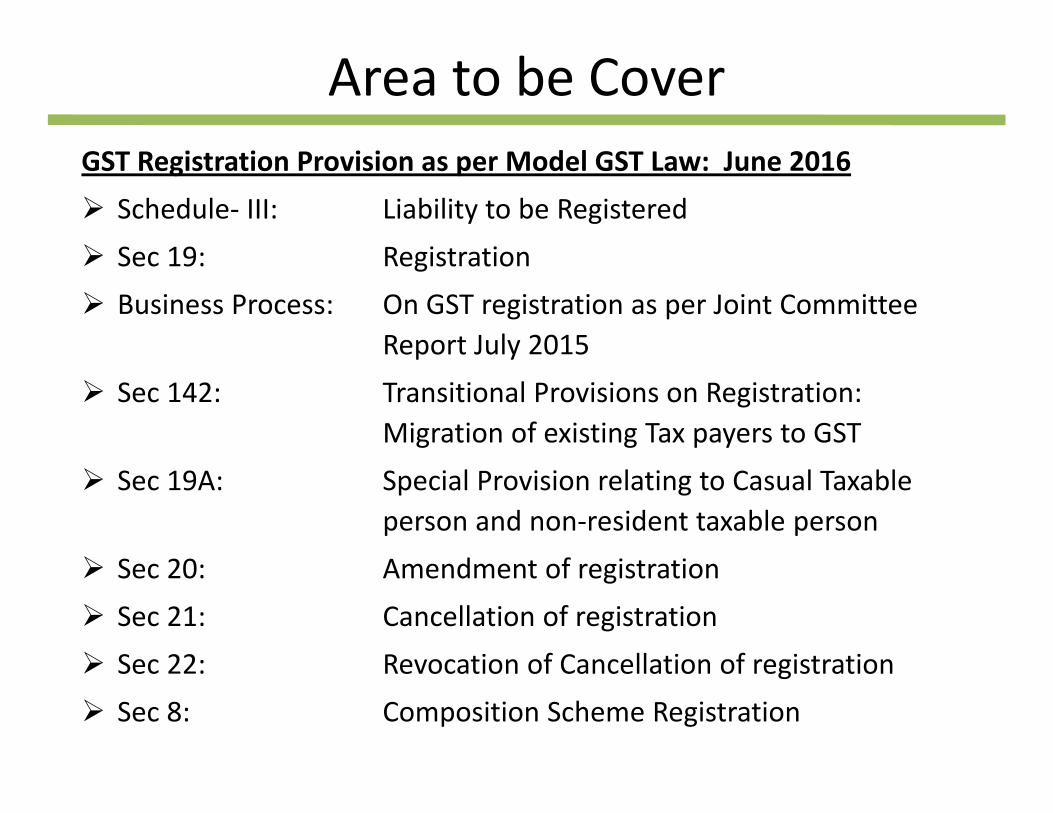

Area to be Coverd lGST Registration Provision as per Model GST Law: June 2016

Schedule‐ III: Liability to be RegisteredSec 19: RegistrationSec 19: Registration Business Process: On GST registration as per Joint Committee

Report July 2015p ySec 142: Transitional Provisions on Registration:

Migration of existing Tax payers to GSTSec 19A: Special Provision relating to Casual Taxable

person and non‐resident taxable personS 20 A d t f i t tiSec 20: Amendment of registrationSec 21: Cancellation of registrationSec 22: Revocation of Cancellation of registrationSec 22: Revocation of Cancellation of registrationSec 8: Composition Scheme Registration

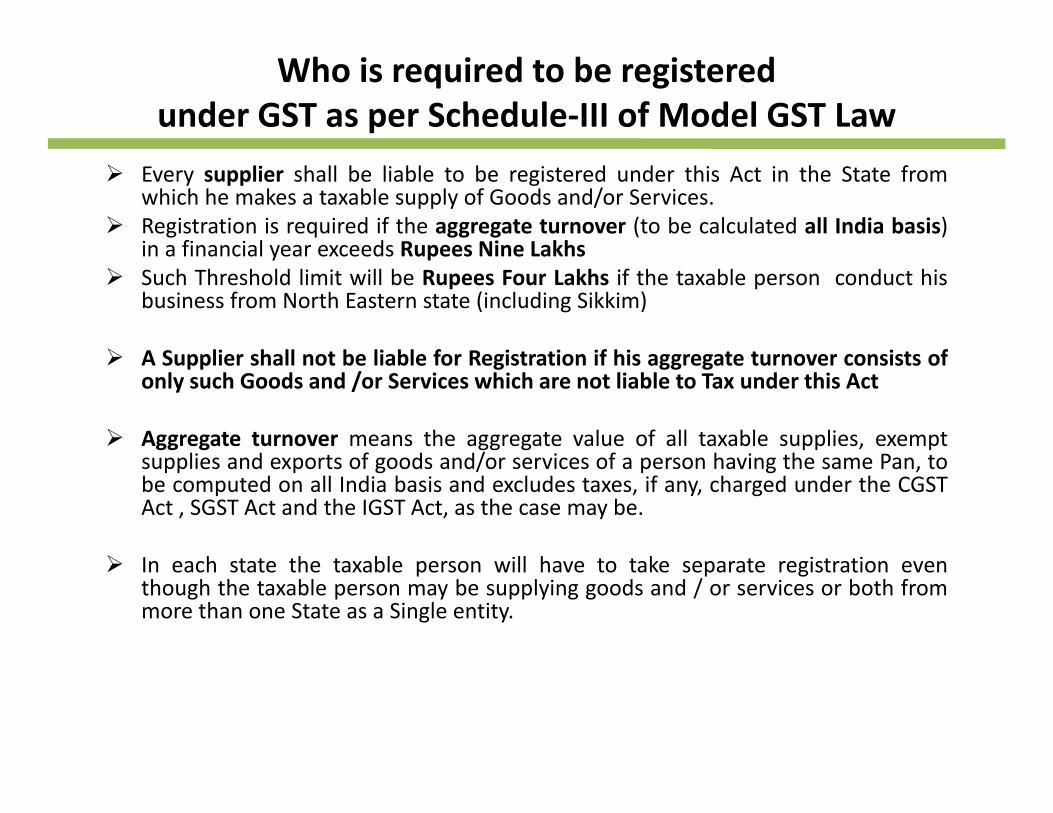

Who is required to be registered under GST as per Schedule‐III of Model GST Law

Every supplier shall be liable to be registered under this Act in the State fromwhich he makes a taxable supply of Goods and/or Services.Registration is required if the aggregate turnover (to be calculated all India basis)in a financial year exceeds Rupees Nine Lakhsin a financial year exceeds Rupees Nine LakhsSuch Threshold limit will be Rupees Four Lakhs if the taxable person conduct hisbusiness from North Eastern state (including Sikkim)

A Supplier shall not be liable for Registration if his aggregate turnover consists ofA Supplier shall not be liable for Registration if his aggregate turnover consists ofonly such Goods and /or Services which are not liable to Tax under this Act

Aggregate turnover means the aggregate value of all taxable supplies, exemptsupplies and exports of goods and/or services of a person having the same Pan tosupplies and exports of goods and/or services of a person having the same Pan, tobe computed on all India basis and excludes taxes, if any, charged under the CGSTAct , SGST Act and the IGST Act, as the case may be.

I h t t th t bl ill h t t k t i t tiIn each state the taxable person will have to take separate registration eventhough the taxable person may be supplying goods and / or services or both frommore than one State as a Single entity.

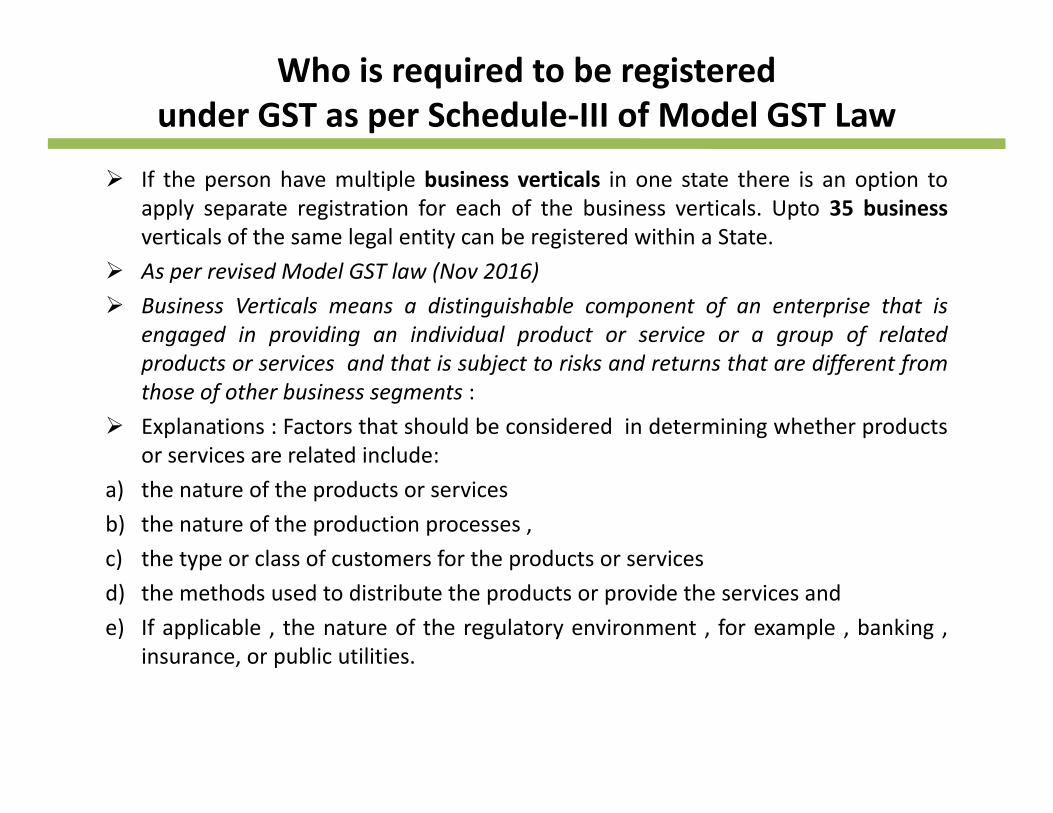

Who is required to be registered under GST as per Schedule‐III of Model GST Law

If the person have multiple business verticals in one state there is an option toapply separate registration for each of the business verticals. Upto 35 businessverticals of the same legal entity can be registered within a State.As per revised Model GST law (Nov 2016)Business Verticals means a distinguishable component of an enterprise that isengaged in providing an individual product or service or a group of related

d i d h i bj i k d h diff fproducts or services and that is subject to risks and returns that are different fromthose of other business segments :Explanations : Factors that should be considered in determining whether productsor services are related include:or services are related include:

a) the nature of the products or servicesb) the nature of the production processes ,c) the type or class of customers for the products or servicesc) the type or class of customers for the products or servicesd) the methods used to distribute the products or provide the services ande) If applicable , the nature of the regulatory environment , for example , banking ,

insurance, or public utilities.insurance, or public utilities.

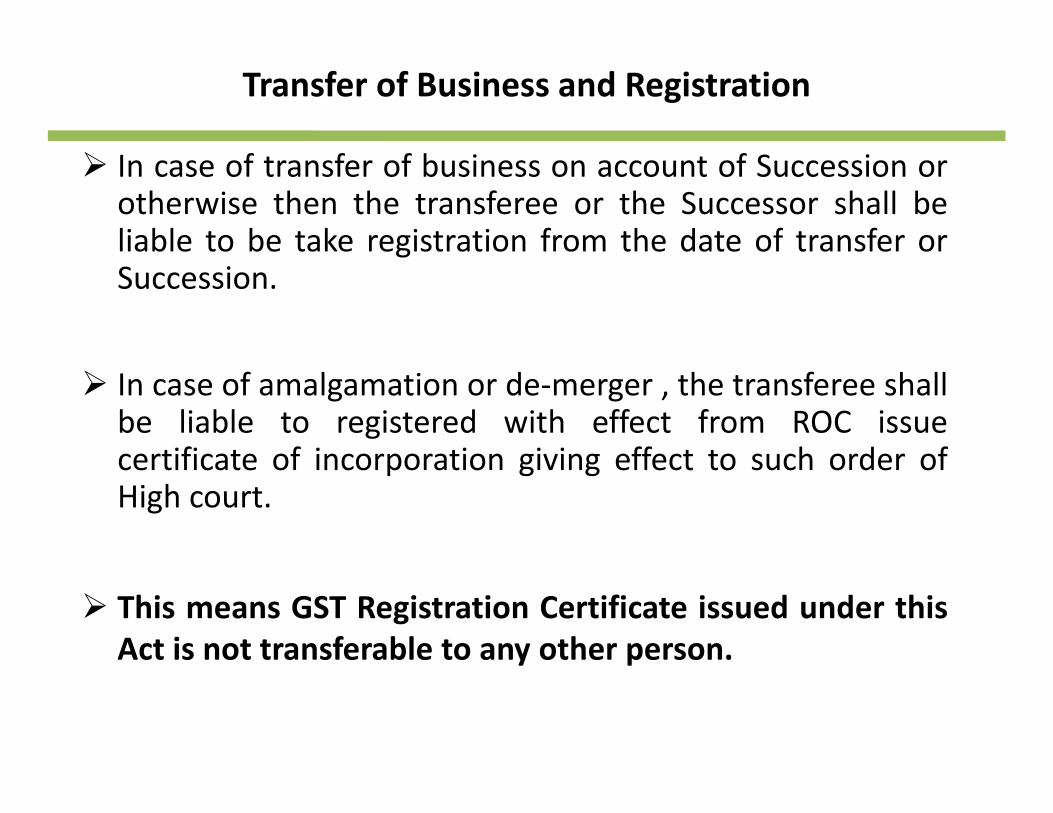

Transfer of Business and Registration

In case of transfer of business on account of Succession orotherwise then the transferee or the Successor shall beliable to be take registration from the date of transfer orgSuccession.

In case of amalgamation or de‐merger , the transferee shallbe liable to registered with effect from ROC issuecertificate of incorporation giving effect to such order ofcertificate of incorporation giving effect to such order ofHigh court.

This means GST Registration Certificate issued under thisAct is not transferable to any other person.y p

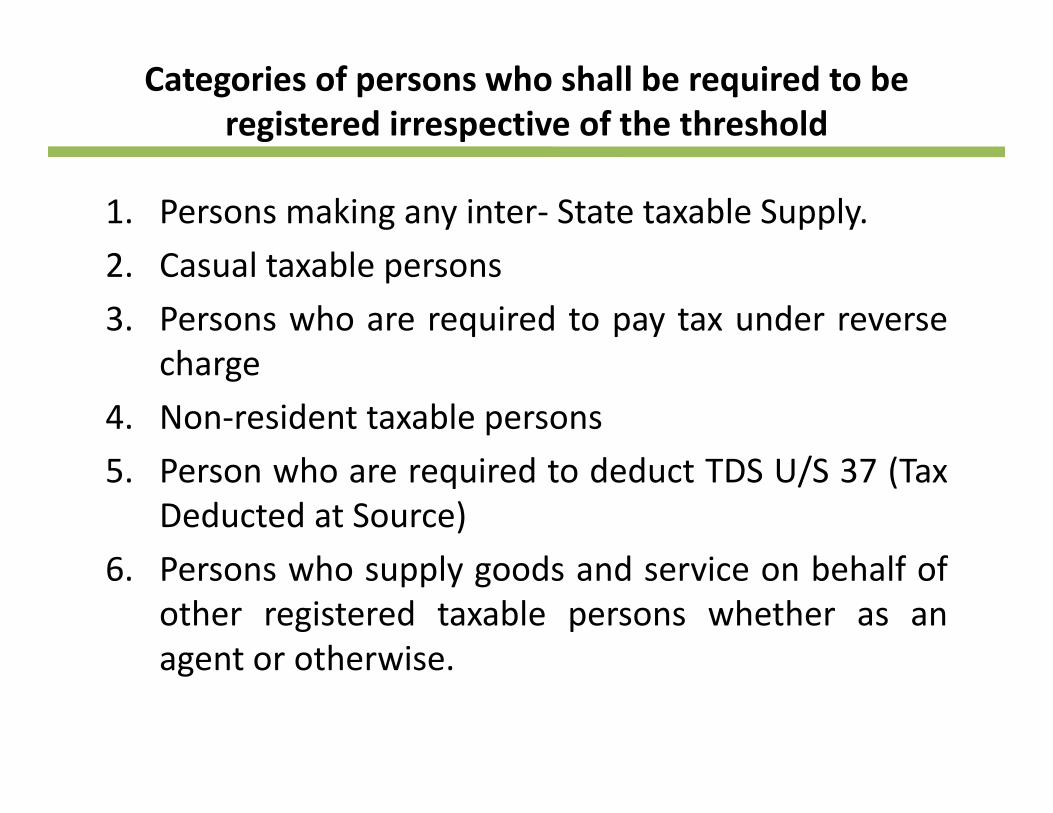

Categories of persons who shall be required to be registered irrespective of the threshold

1. Persons making any inter‐ State taxable Supply.2 l bl2. Casual taxable persons3. Persons who are required to pay tax under reverse

hcharge4. Non‐resident taxable persons

h d d d / (5. Person who are required to deduct TDS U/S 37 (TaxDeducted at Source)

6 P h l d d i b h lf f6. Persons who supply goods and service on behalf ofother registered taxable persons whether as anagent or otherwiseagent or otherwise.

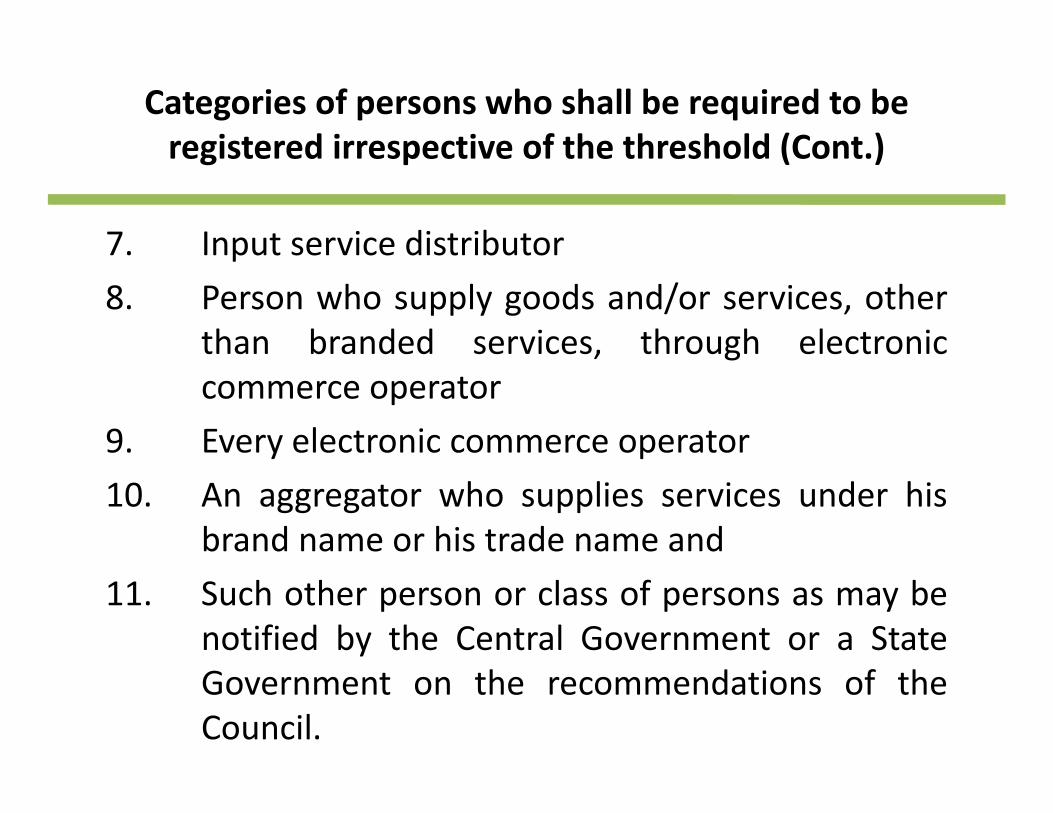

Categories of persons who shall be required to be registered irrespective of the threshold (Cont )registered irrespective of the threshold (Cont.)

7. Input service distributor7. Input service distributor8. Person who supply goods and/or services, other

than branded services, through electronic, gcommerce operator

9. Every electronic commerce operatory p10. An aggregator who supplies services under his

brand name or his trade name and11. Such other person or class of persons as may be

notified by the Central Government or a StateGovernment on the recommendations of theCouncil.

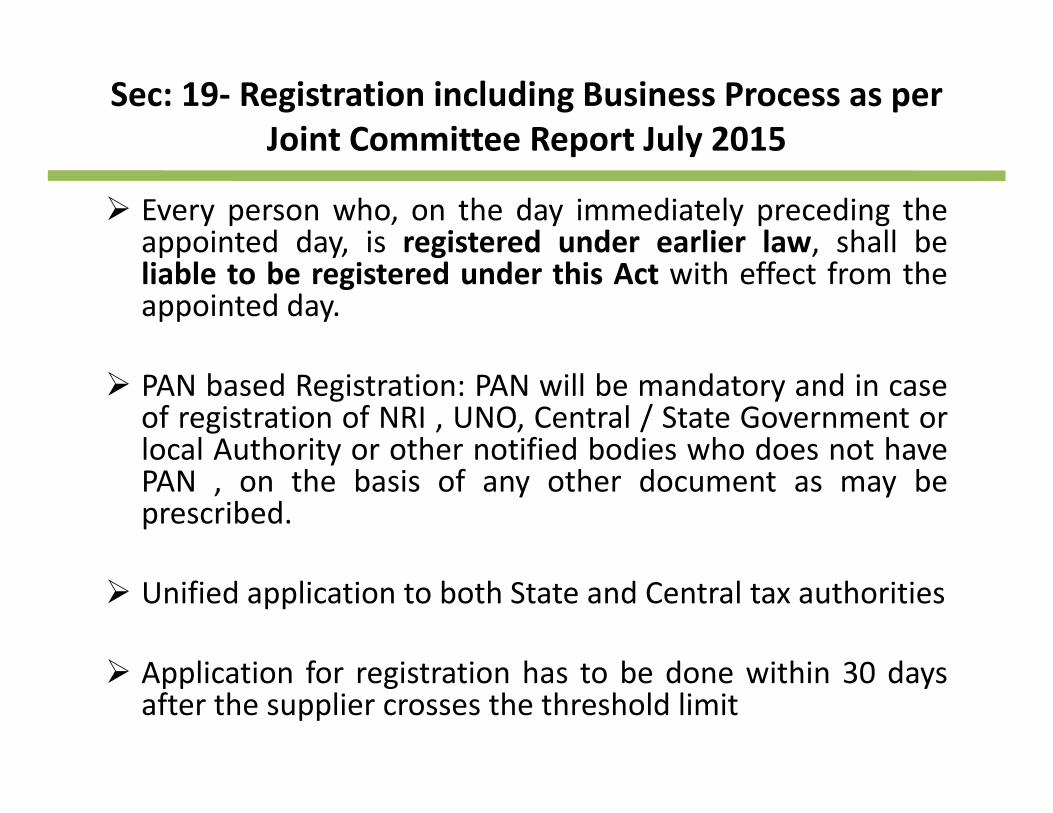

Sec: 19‐ Registration including Business Process as per Joint Committee Report July 2015Joint Committee Report July 2015

Every person who, on the day immediately preceding theappointed day, is registered under earlier law, shall bepp y, g ,liable to be registered under this Act with effect from theappointed day.

PAN based Registration: PAN will be mandatory and in caseof registration of NRI , UNO, Central / State Government orlocal Authority or other notified bodies who does not havelocal Authority or other notified bodies who does not havePAN , on the basis of any other document as may beprescribed.

Unified application to both State and Central tax authorities

A li i f i i h b d i hi 30 dApplication for registration has to be done within 30 daysafter the supplier crosses the threshold limit

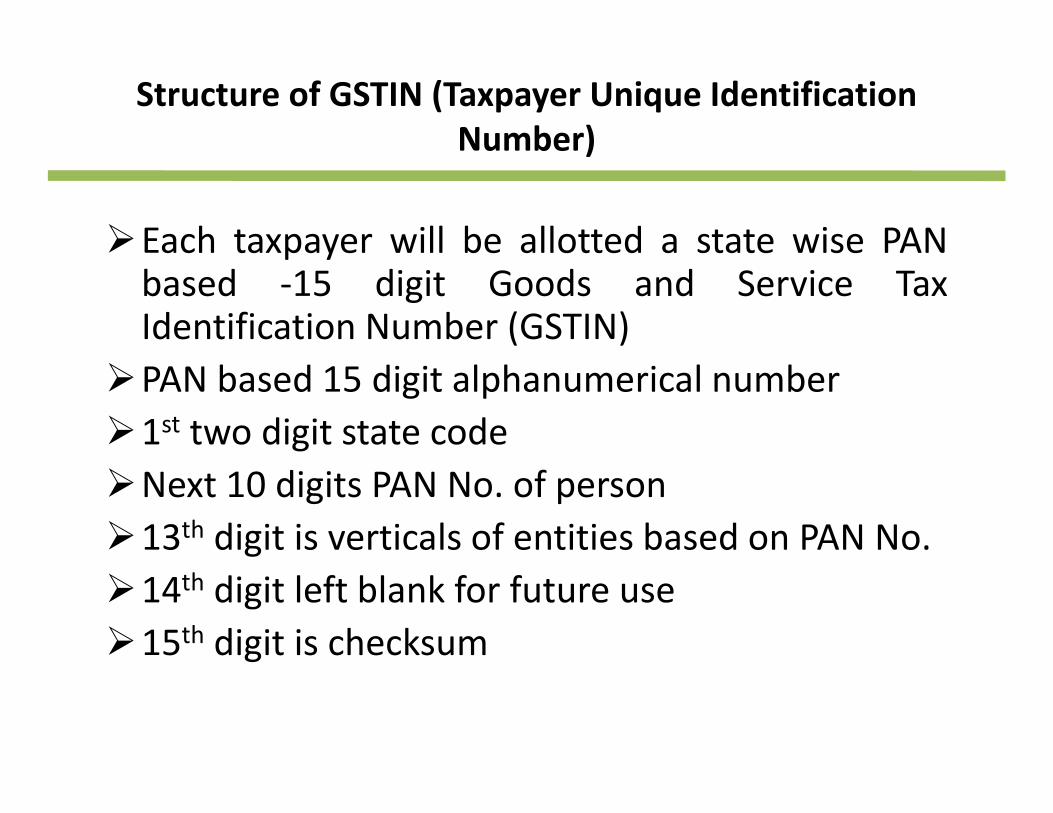

Structure of GSTIN (Taxpayer Unique Identification Number)Number)

Each taxpayer will be allotted a state wise PANac ta paye be a otted a state sebased ‐15 digit Goods and Service TaxIdentification Number (GSTIN)PAN based 15 digit alphanumerical number1st two digit state codeNext 10 digits PAN No. of person13th digit is verticals of entities based on PAN No.14th digit left blank for future use15th digit is checksum

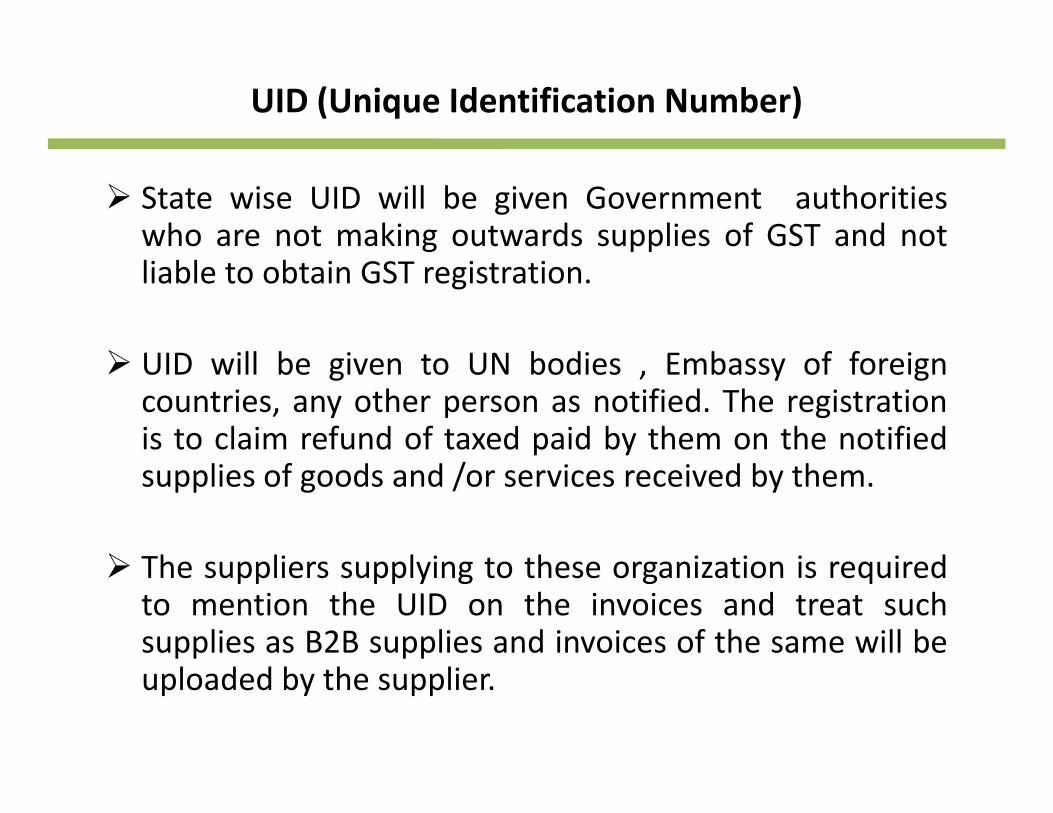

UID (Unique Identification Number)

State wise UID will be given Government authoritieswho are not making outwards supplies of GST and notliable to obtain GST registration.

UID ill b i t UN b di E b f f iUID will be given to UN bodies , Embassy of foreigncountries, any other person as notified. The registrationis to claim refund of taxed paid by them on the notifiedsupplies of goods and /or services received by them.

Th li l i t th i ti i i dThe suppliers supplying to these organization is requiredto mention the UID on the invoices and treat suchsupplies as B2B supplies and invoices of the same will beuploaded by the supplier.

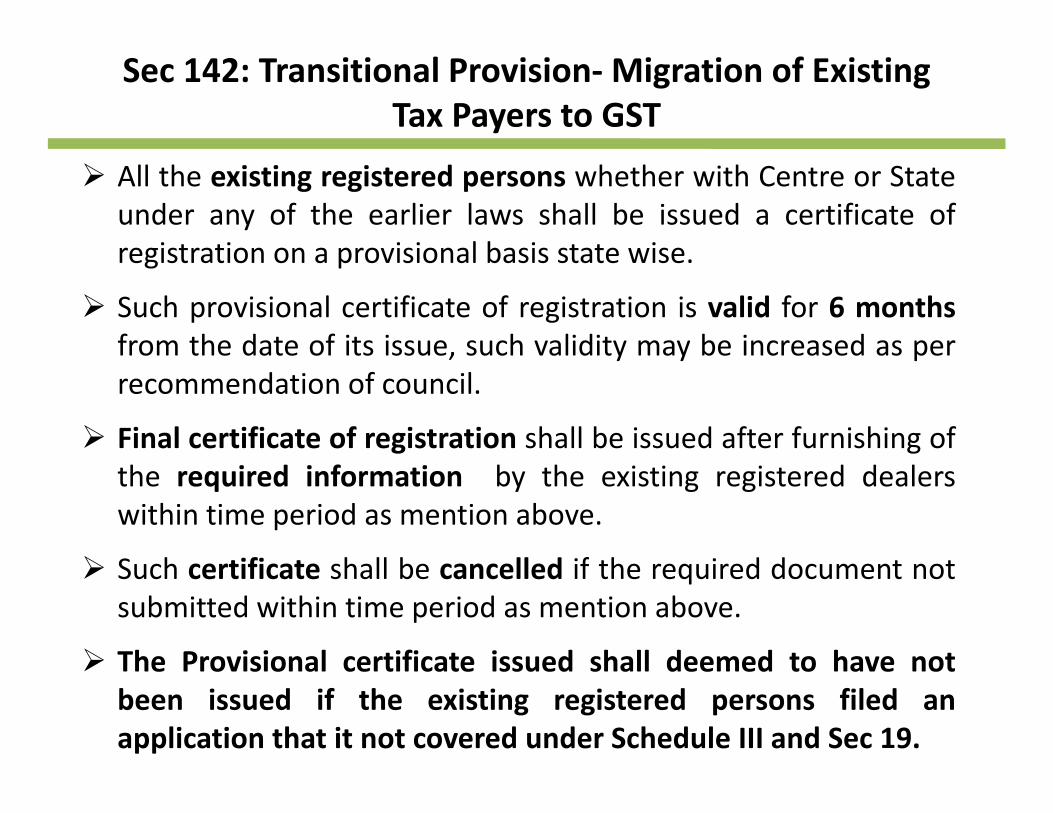

Sec 142: Transitional Provision‐Migration of Existing Tax Payers to GST

All the existing registered persons whether with Centre or Stateunder any of the earlier laws shall be issued a certificate ofregistration on a provisional basis state wiseregistration on a provisional basis state wise.

Such provisional certificate of registration is valid for 6 monthsfrom the date of its issue, such validity may be increased as perfrom the date of its issue, such validity may be increased as perrecommendation of council.

Final certificate of registration shall be issued after furnishing ofthe required information by the existing registered dealerswithin time period as mention above.

S h tifi t h ll b ll d if th i d d t tSuch certificate shall be cancelled if the required document notsubmitted within time period as mention above.

The Provisional certificate issued shall deemed to have notThe Provisional certificate issued shall deemed to have notbeen issued if the existing registered persons filed anapplication that it not covered under Schedule III and Sec 19.

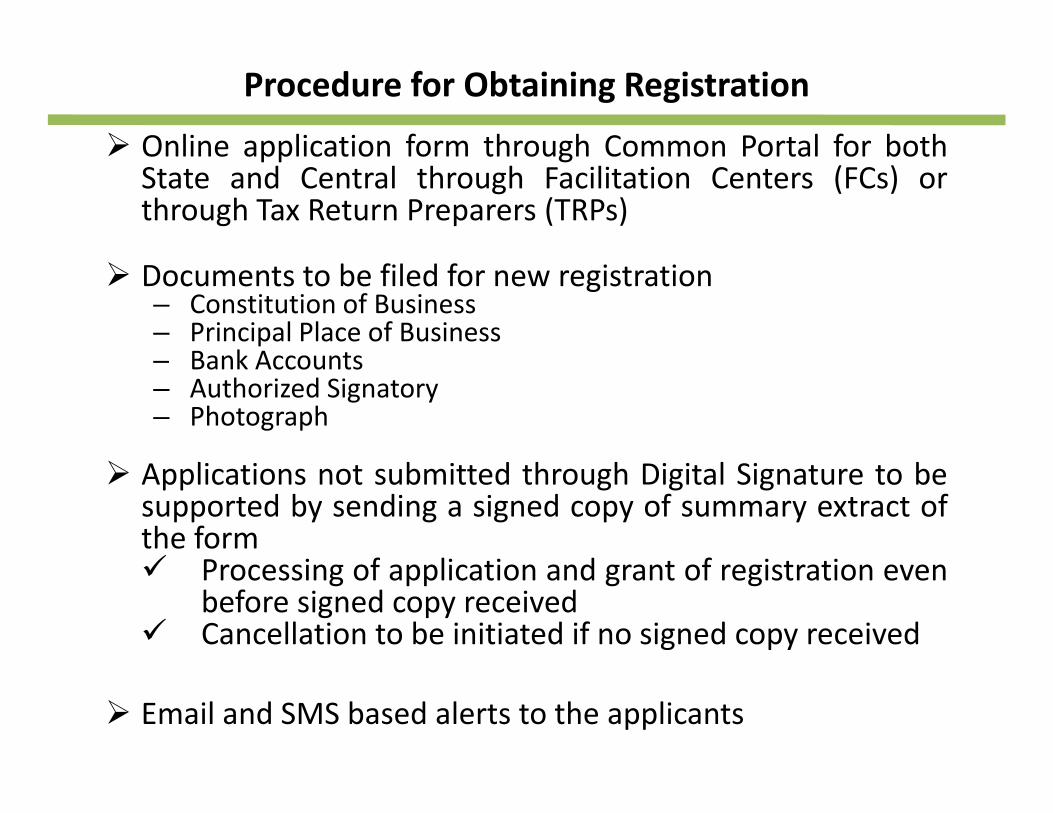

Procedure for Obtaining Registration

Online application form through Common Portal for bothOnline application form through Common Portal for bothState and Central through Facilitation Centers (FCs) orthrough Tax Return Preparers (TRPs)

Documents to be filed for new registration– Constitution of Business– Principal Place of Business

Bank Acco nts– Bank Accounts– Authorized Signatory– Photograph

Applications not submitted through Digital Signature to besupported by sending a signed copy of summary extract ofthe form

P i f li i d f i iProcessing of application and grant of registration evenbefore signed copy receivedCancellation to be initiated if no signed copy received

Email and SMS based alerts to the applicants

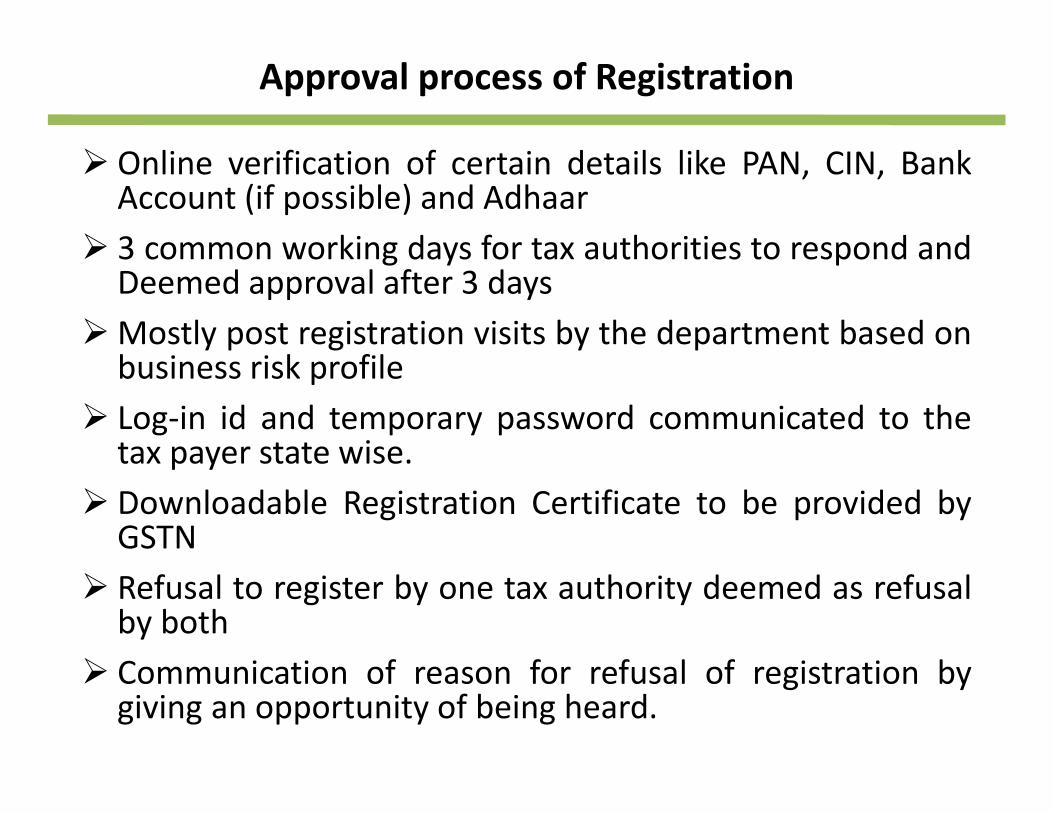

Approval process of Registration

l f f d l l k kOnline verification of certain details like PAN, CIN, BankAccount (if possible) and Adhaar3 common working days for tax authorities to respond and3 common working days for tax authorities to respond andDeemed approval after 3 daysMostly post registration visits by the department based onb i i k filbusiness risk profileLog‐in id and temporary password communicated to thetax payer state wisetax payer state wise.Downloadable Registration Certificate to be provided byGSTNRefusal to register by one tax authority deemed as refusalby bothC i ti f f f l f i t ti bCommunication of reason for refusal of registration bygiving an opportunity of being heard.

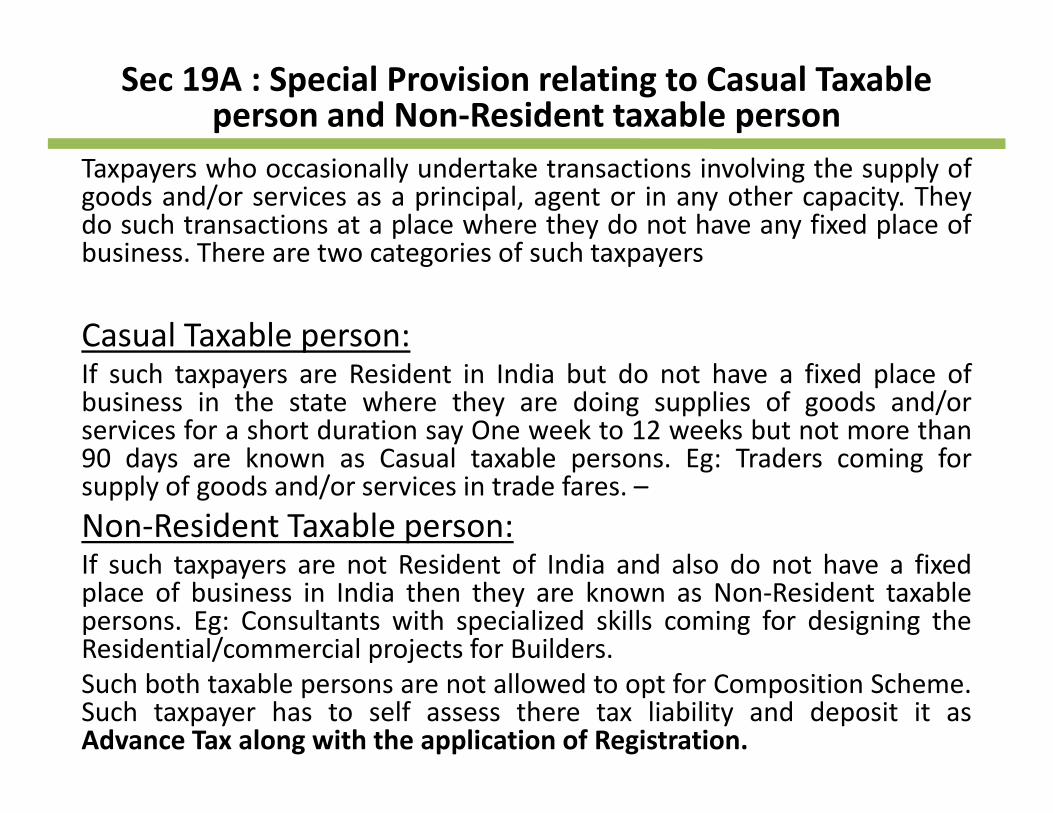

Sec 19A : Special Provision relating to Casual Taxable person and Non‐Resident taxable person

Taxpayers who occasionally undertake transactions involving the supply ofgoods and/or services as a principal, agent or in any other capacity. Theydo such transactions at a place where they do not have any fixed place ofbusiness There are two categories of such taxpayersbusiness. There are two categories of such taxpayers

Casual Taxable person:If such taxpayers are Resident in India but do not have a fixed place ofbusiness in the state where they are doing supplies of goods and/orservices for a short duration say One week to 12 weeks but not more than90 days are known as Casual taxable persons Eg: Traders coming for90 days are known as Casual taxable persons. Eg: Traders coming forsupply of goods and/or services in trade fares. –Non‐Resident Taxable person:If such taxpayers are not Resident of India and also do not have a fixedIf such taxpayers are not Resident of India and also do not have a fixedplace of business in India then they are known as Non‐Resident taxablepersons. Eg: Consultants with specialized skills coming for designing theResidential/commercial projects for Builders.Such both taxable persons are not allowed to opt for Composition Scheme.Such taxpayer has to self assess there tax liability and deposit it asAdvance Tax along with the application of Registration.

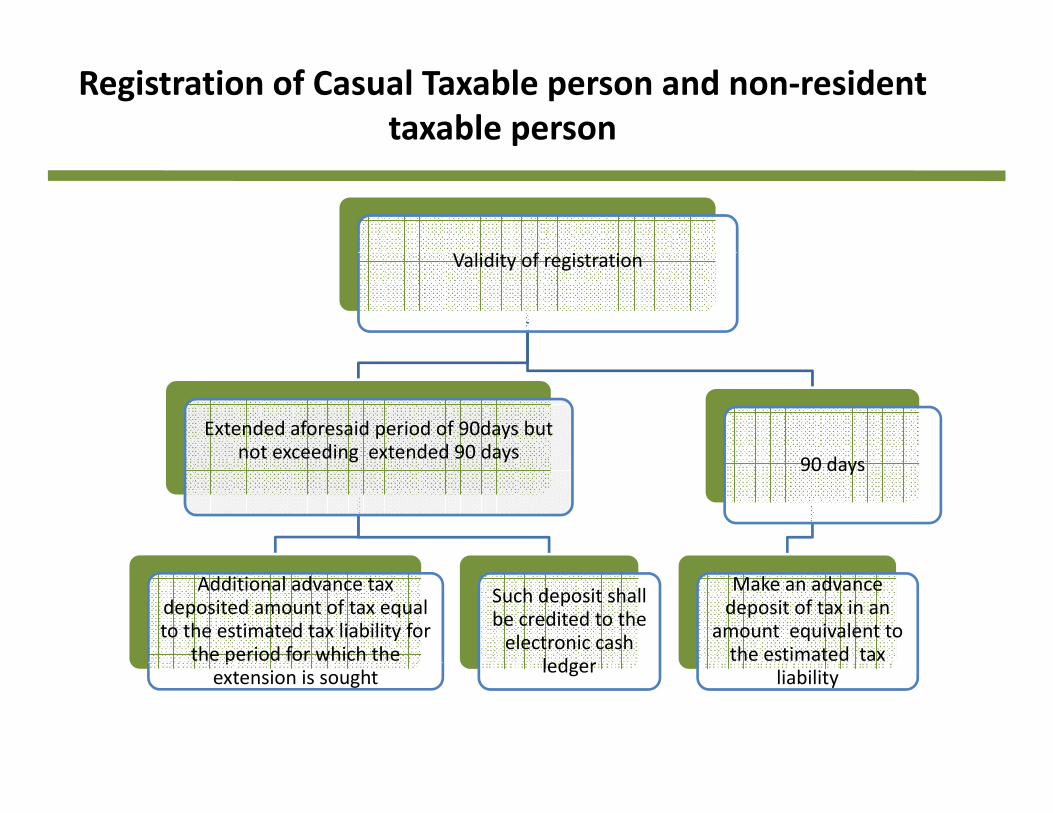

Registration of Casual Taxable person and non‐resident taxable person

l d fValidity of registration

Extended aforesaid period of 90days but not exceeding extended 90 days 90 dnot exceeding extended 90 days 90 days

Additional advance tax deposited amount of tax equal to the estimated tax liability for

the period for which the

Such deposit shall be credited to the electronic cash

ledger

Make an advance deposit of tax in an

amount equivalent to the estimated tax p

extension is sought ledger liability

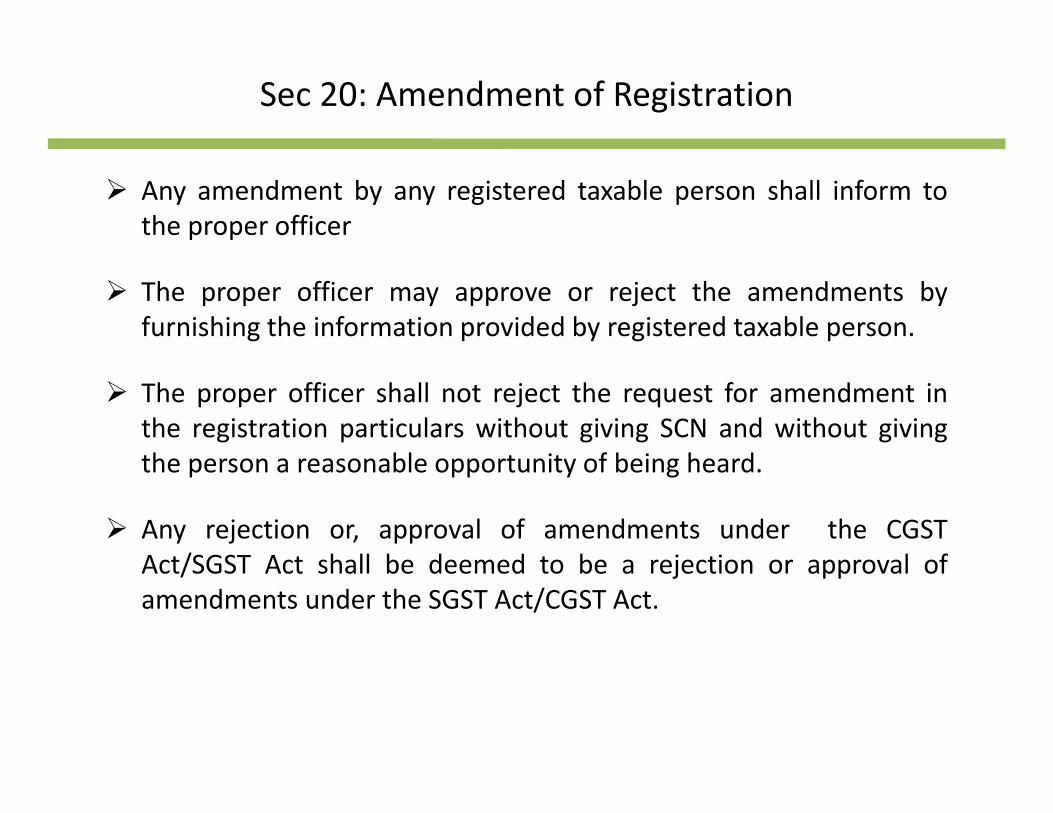

Sec 20: Amendment of Registration

Any amendment by any registered taxable person shall inform tothe proper officer

The proper officer may approve or reject the amendments byfurnishing the information provided by registered taxable person.

The proper officer shall not reject the request for amendment inthe registration particulars without giving SCN and without givingth bl t it f b i h dthe person a reasonable opportunity of being heard.

Any rejection or, approval of amendments under the CGSTAct/SGST Act shall be deemed to be a rejection or approval ofAct/SGST Act shall be deemed to be a rejection or approval ofamendments under the SGST Act/CGST Act.

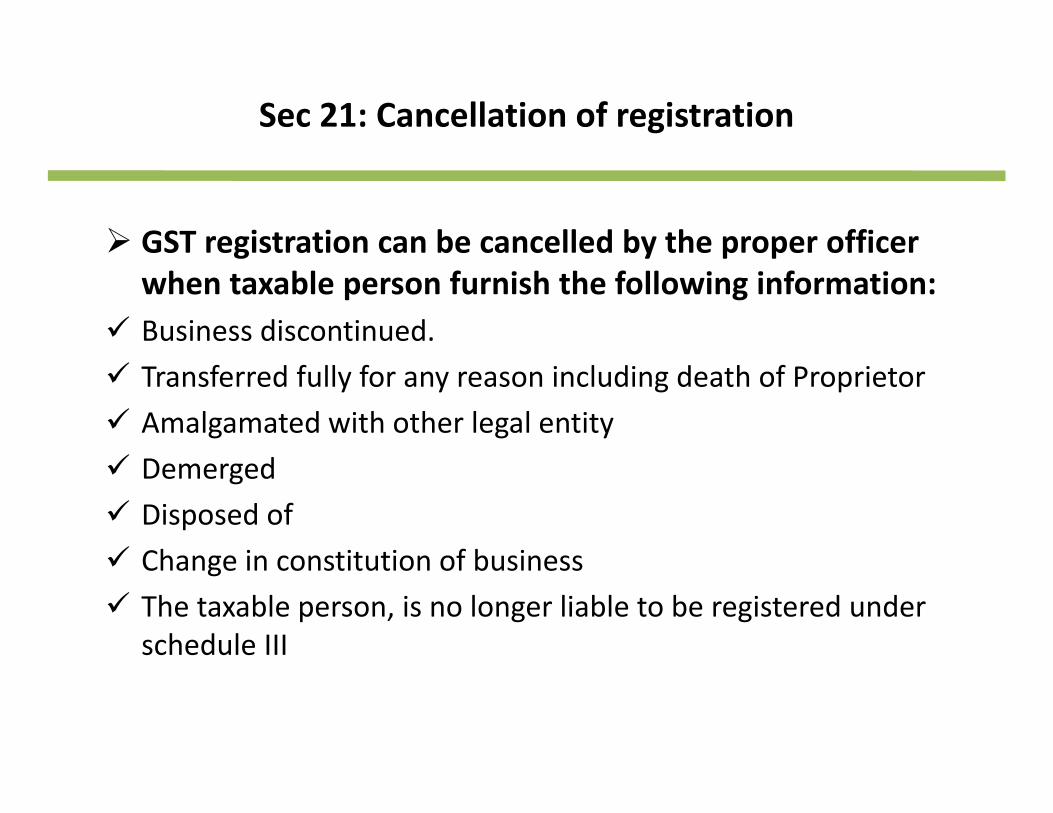

Sec 21: Cancellation of registration

GST registration can be cancelled by the proper officer GS eg st at o ca be ca ce ed by t e p ope o cewhen taxable person furnish the following information:Business discontinued.Transferred fully for any reason including death of ProprietorAmalgamated with other legal entity

dDemergedDisposed ofChange in constitution of businessChange in constitution of businessThe taxable person, is no longer liable to be registered under schedule III

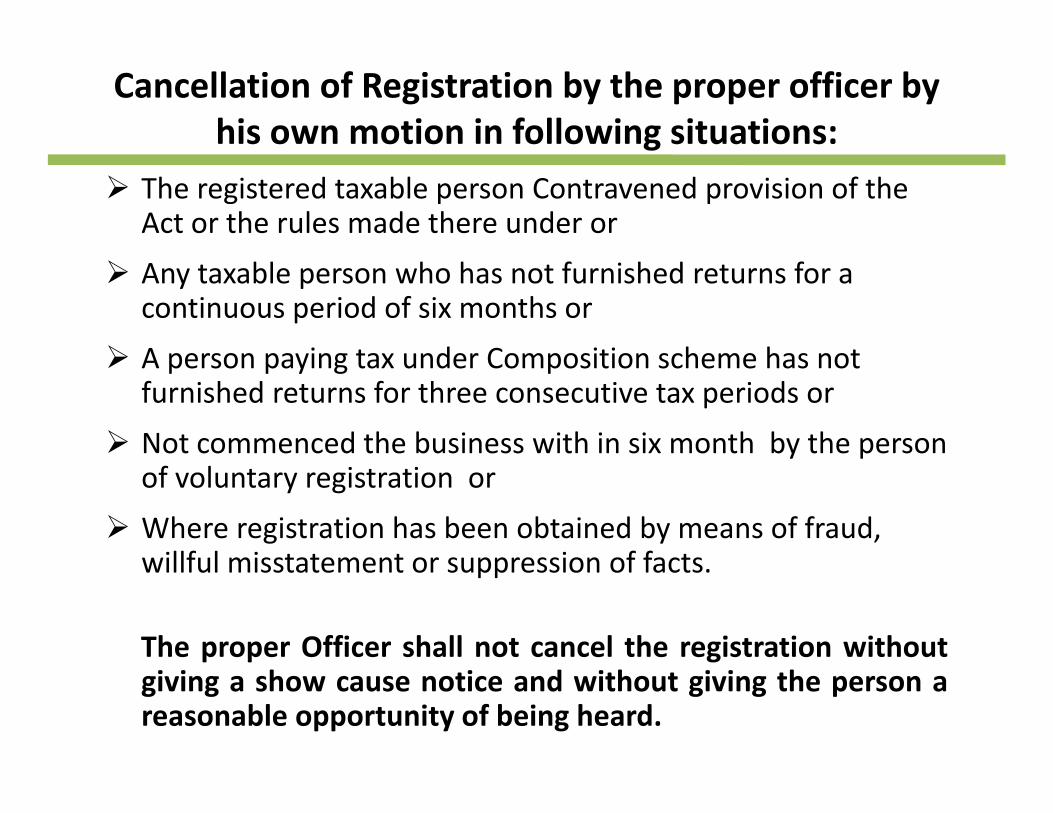

Cancellation of Registration by the proper officer by his own motion in following situations: g

The registered taxable person Contravened provision of the Act or the rules made there under or

Any taxable person who has not furnished returns for a continuous period of six months or

A person paying tax under Composition scheme has notA person paying tax under Composition scheme has not furnished returns for three consecutive tax periods or

Not commenced the business with in six month by the person y pof voluntary registration or

Where registration has been obtained by means of fraud, willful misstatement or suppression of factswillful misstatement or suppression of facts.

The proper Officer shall not cancel the registration withoutgiving a show cause notice and without giving the person areasonable opportunity of being heard.

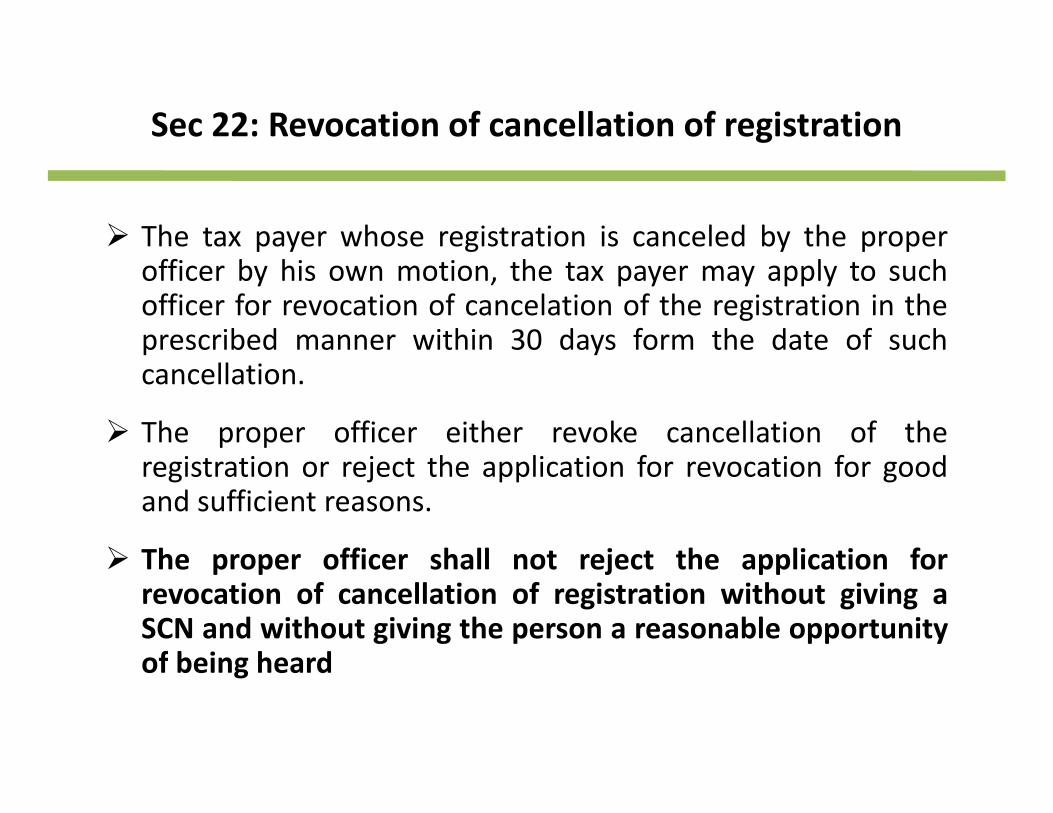

Sec 22: Revocation of cancellation of registration

The tax payer whose registration is canceled by the properofficer by his own motion, the tax payer may apply to suchofficer for revocation of cancelation of the registration in theprescribed manner within 30 days form the date of suchcancellation.

The proper officer either revoke cancellation of thei i j h li i f i f dregistration or reject the application for revocation for good

and sufficient reasons.

The proper officer shall not reject the application forThe proper officer shall not reject the application forrevocation of cancellation of registration without giving aSCN and without giving the person a reasonable opportunityof being heardof being heard

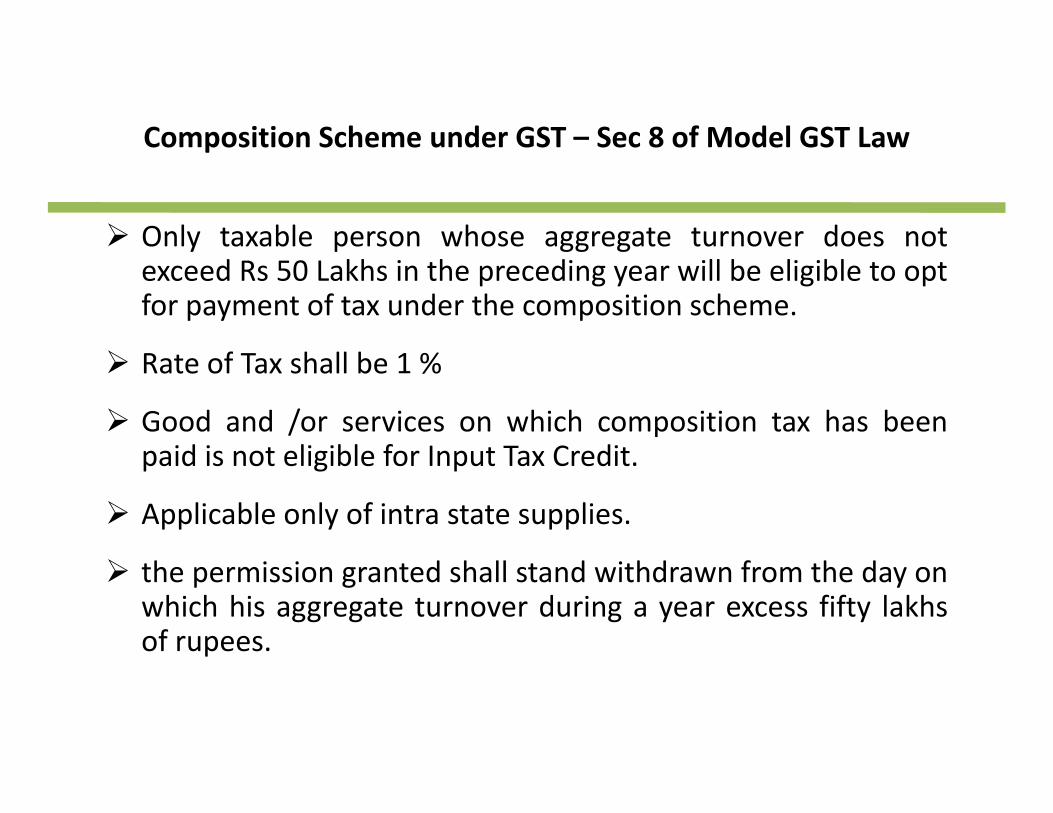

Composition Scheme under GST – Sec 8 of Model GST Lawp

Only taxable person whose aggregate turnover does notexceed Rs 50 Lakhs in the preceding year will be eligible to optfor payment of tax under the composition scheme.

R t f T h ll b 1 %Rate of Tax shall be 1 %

Good and /or services on which composition tax has beenpaid is not eligible for Input Tax Creditpaid is not eligible for Input Tax Credit.

Applicable only of intra state supplies.

h d h ll d hd f h dthe permission granted shall stand withdrawn from the day onwhich his aggregate turnover during a year excess fifty lakhsof rupees.

Composition Scheme not permissible to following persons

who is engaged in the manufacture of goods or supply ofg g g pp yservices; or

who makes any supply of goods which are not leviable to taxy pp y gunder the Act; or

Who makes any inter‐State outward supplies of goods or

who makes any supply of goods through an electroniccommerce operator who is required to collect tax at source

Registration under Composition SchemeRegistration under Composition Scheme

•Normal dealer TOOnly in the beginning

of financial year• Composition Dealer

of financial year

•Composition DealerTO

During the year also with a condition not

TO•Normal dealer

to switch again under composition scheme

in the same FY

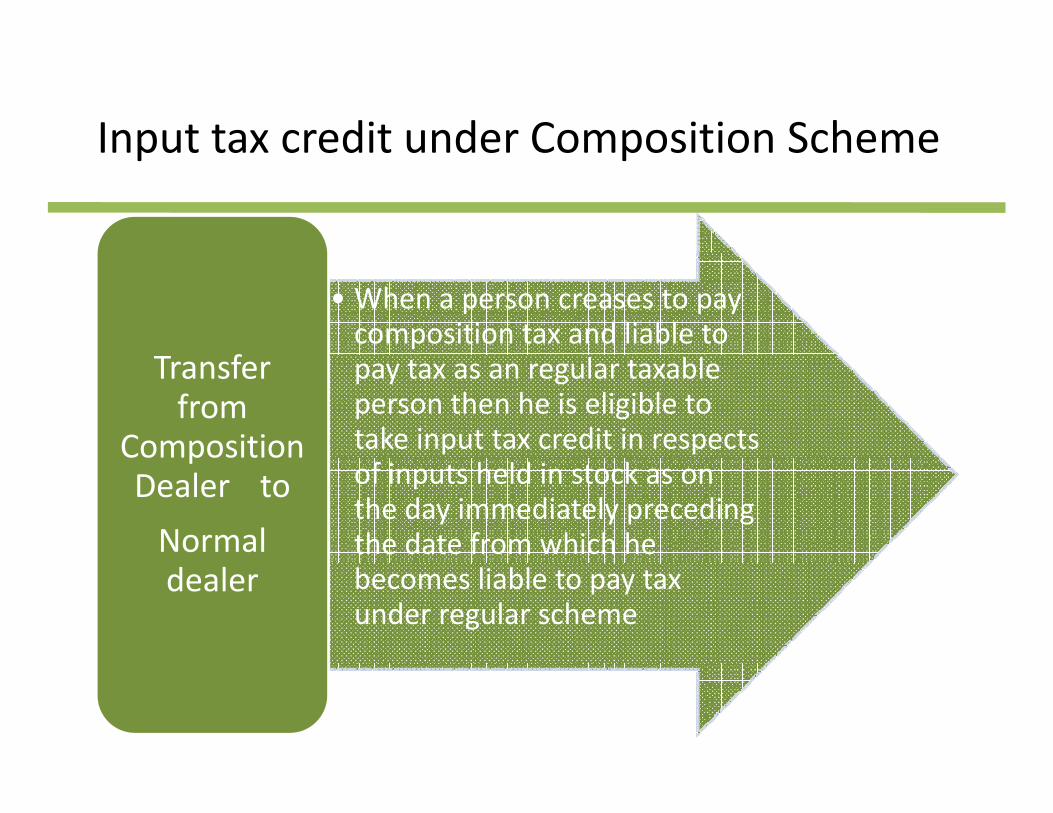

Input tax credit under Composition SchemeInput tax credit under Composition Scheme

• When a person creases to pay composition tax and liable to

f pay tax as an regular taxable person then he is eligible to take input tax credit in respects

Transfer from

Composition of inputs held in stock as on the day immediately preceding the date from which he

pDealer toNormal

becomes liable to pay tax under regular scheme

dealer

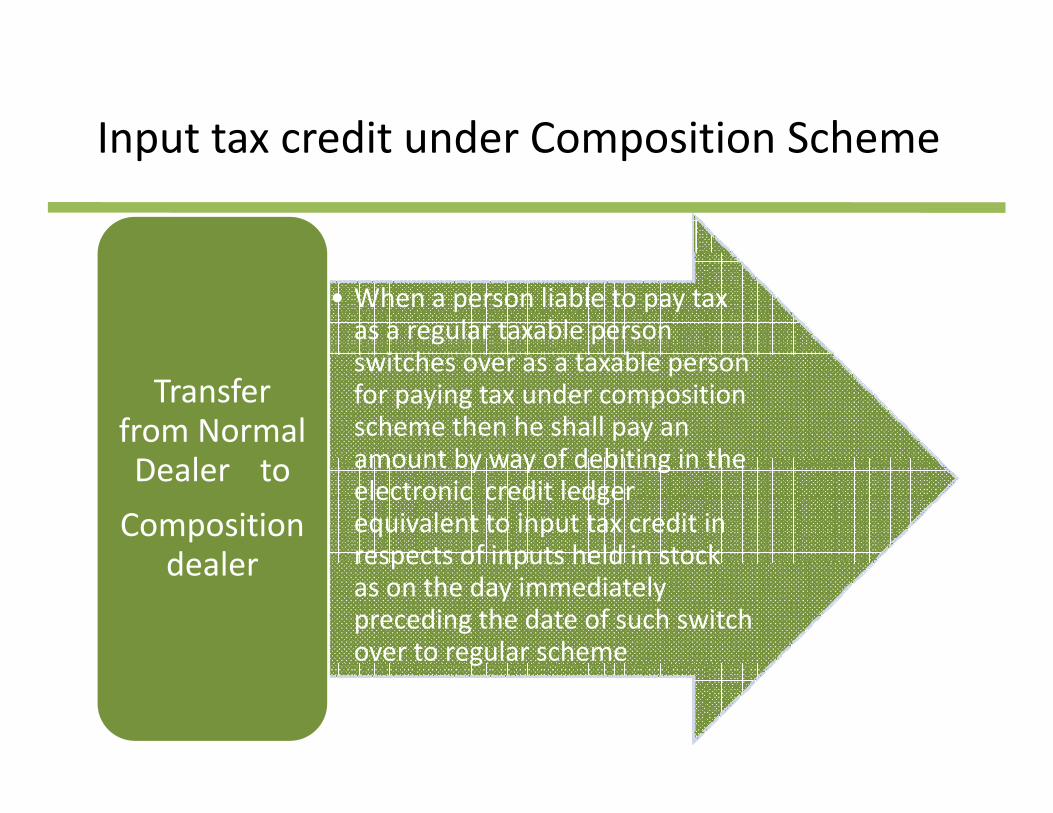

Input tax credit under Composition SchemeInput tax credit under Composition Scheme

• When a person liable to pay tax as a regular taxable person

it h t blswitches over as a taxable person for paying tax under composition scheme then he shall pay an amount by way of debiting in the

Transfer from Normal

l amount by way of debiting in the electronic credit ledger equivalent to input tax credit in respects of inputs held in stock

Dealer toComposition

dealer respects of inputs held in stock as on the day immediately preceding the date of such switch over to regular scheme

dealer

g

Related Documents