1 Growth Opportunities in Soft Drinks Innovation, new product development and detailed market analysis Reference Code: BI00049-008 Publication Date: December 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Growth Opportunities in Soft Drinks

Innovation, new product development and detailed market analysis Reference Code: BI00049-008

Publication Date: December 2011

2

John Band John Band is an experienced FMCG analyst, writer and consultant, with a particular focus on the drinks

industry. He has led consulting projects for major clients across the drinks sector, has presented on drinks

topics at key industry forums, and has been quoted on drinks marketing topics by publications including the

BBC, the Economist and the Wall Street Journal.

John holds a BA and MA from the University of Oxford in Philosophy, Politics & Economics, and a Master of

Digital Communications from the University of Sydney.

Disclaimer Copyright © 2011 Business Insights Ltd

This Management Report is published by Business Insights Ltd. All rights reserved. Reproduction or

redistribution of this Management Report in any form for any purpose is expressly prohibited without the prior

consent of Business Insights Ltd.

The views expressed in this Management Report are those of the publisher, not of Business Insights.

Business Insights Ltd accepts no liability for the accuracy or completeness of the information, advice or

comment contained in this Management Report or for any actions taken in reliance thereon.

While information, advice or comment is believed to be correct at the time of publication, no responsibility

can be accepted by Business Insights Ltd for its completeness or accuracy.

3

Table of Contents

John Band 2

Disclaimer 2

Executive summary 12

Growth opportunities in soft drinks 12 Innovation and new product development 13 Consumer trends driving innovation 14 The future of innovations in soft drinks 15

Chapter 1 Introduction 16

Introduction 16 Market definitions 16 What this report is about 17 Scope of report 17

Chapter 2 Growth opportunities in soft drinks 19

Summary 19 Introduction 20 Market overview 20 Soft drinks overview by category 20

Soft drinks overview by region 25

Category breakdown 30 Bottled water 30

Carbonates 32

Concentrates 33

Functional drinks 34

Juices 36

RTD tea & coffee 38

Smoothies 39

Major country profiles 40

4

Brazil 44

China 45

France 47

Germany 49

India 50

Italy 52

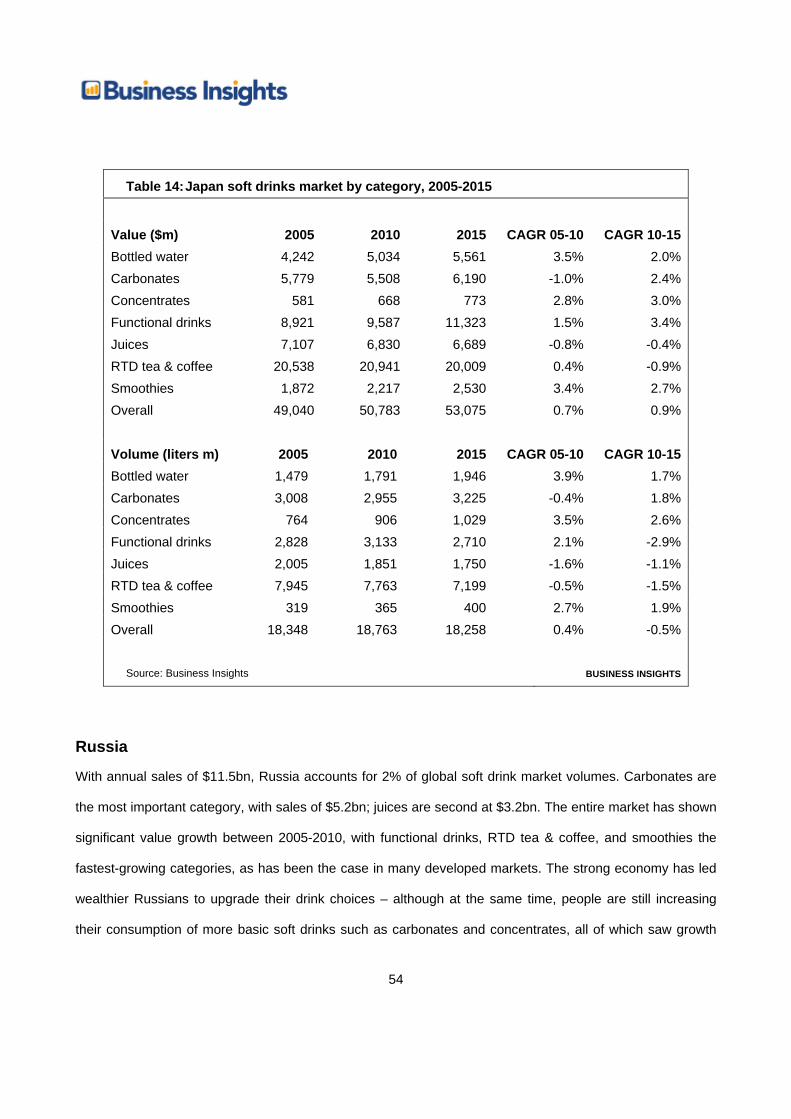

Japan 53

Russia 54

United Kingdom 56

United States 57

Chapter 3 Innovation & new product development 60

Summary 60 Introduction 61 Major soft drinks NPD trends 61 Product claim trends 63

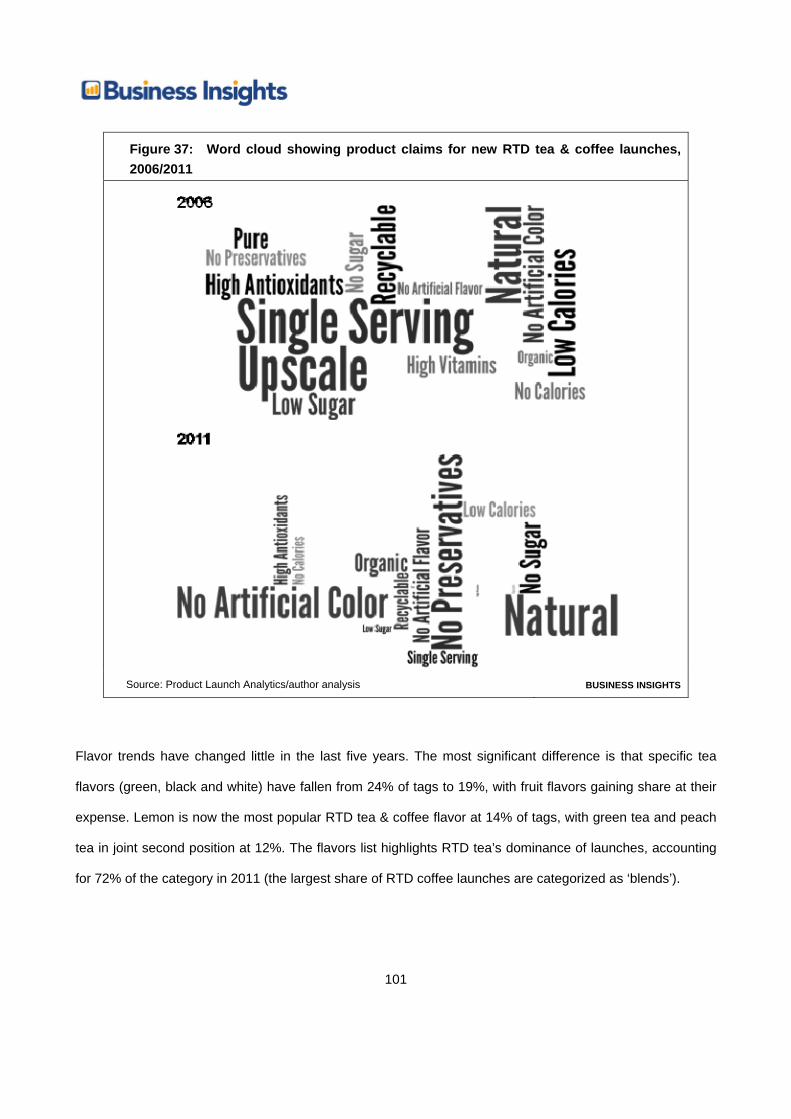

Flavor trends 65

Packaging trends 66

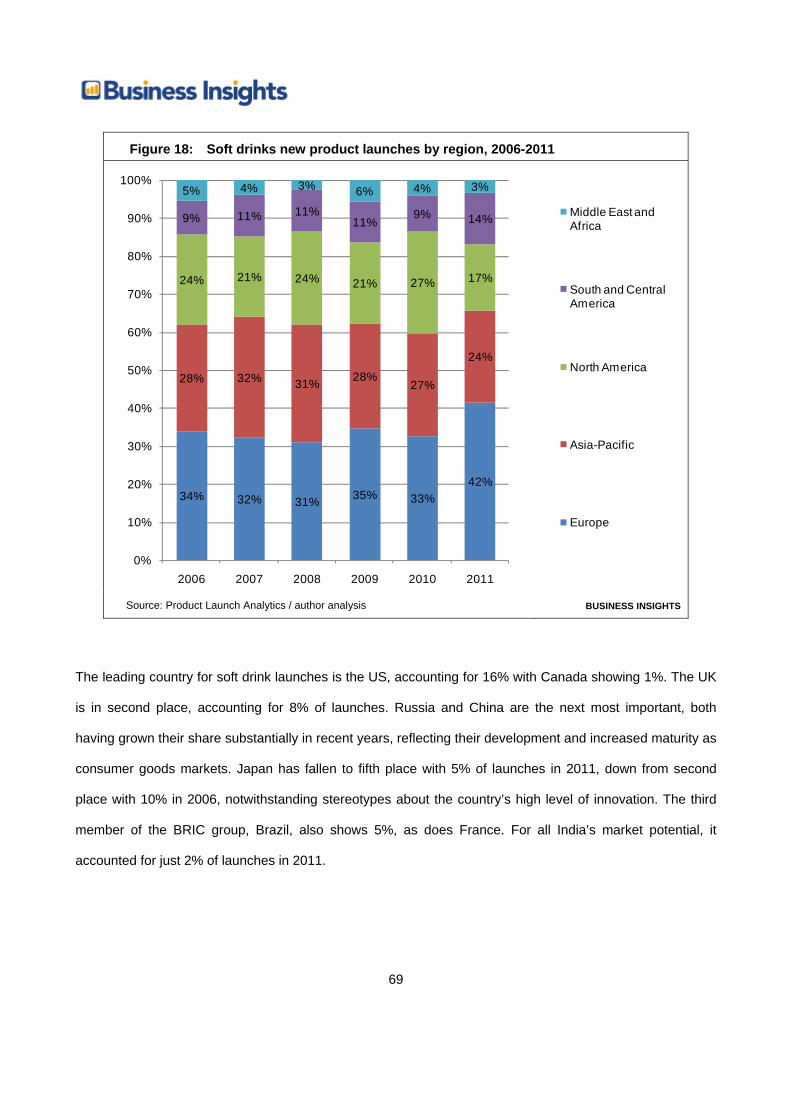

Country and regional trends 68

Innovative products 70

Category-level analysis 74 Bottled water 74

Carbonates 79

Concentrates 84

Functional drinks 89

Juices 94

RTD tea & coffee 99

Smoothies 104

Chapter 4 Consumer trends driving innovation 109

5

Summary 109 Introduction 110 Austerity will drive closer connections with consumers 110 Growth of private label and value brands 111

Mass-premium products are still relevant, although constrained 112

Mass customization will become an important marketing strategy 113

Some austerity trends fit better than others with emerging markets 117

Health and wellness will continue to be a major trend 117 Major drinks players are growing the market but cutting prices 118

New types of functionality can attract non-traditional consumers 119

Regulation and consumer skepticism will remain obstacles 121

Health is becoming important in developing markets 121

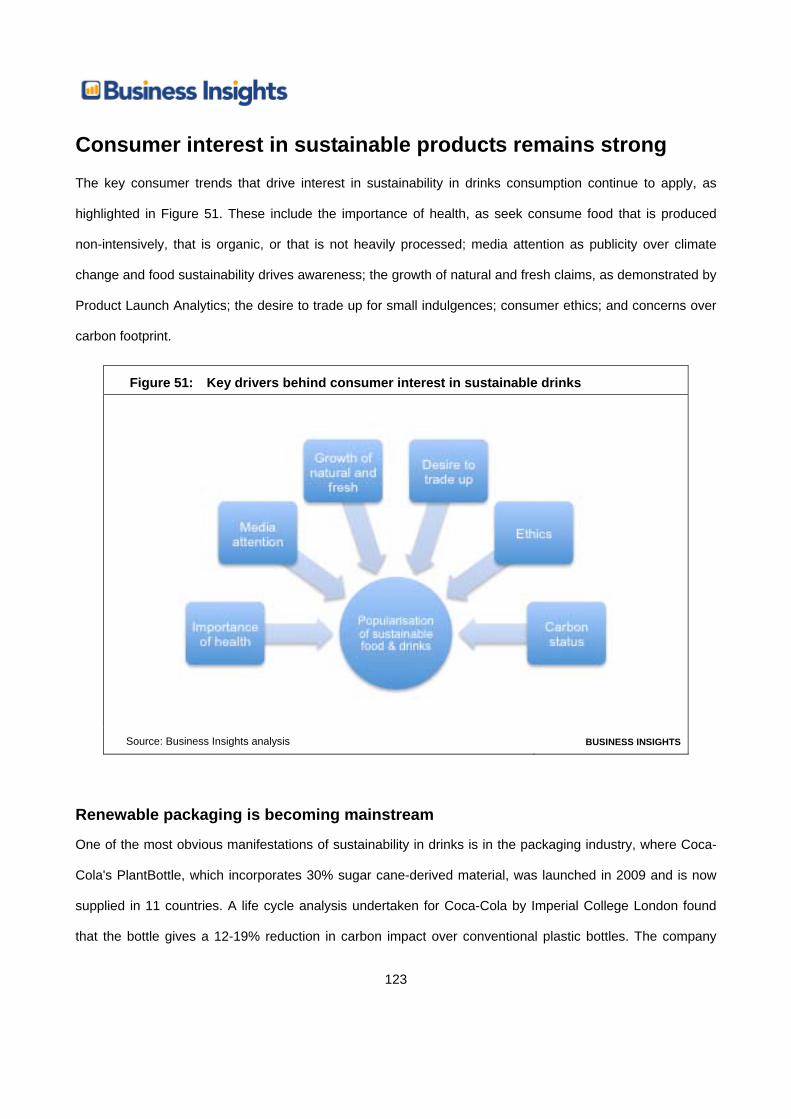

Consumer interest in sustainable products remains strong 123 Renewable packaging is becoming mainstream 123

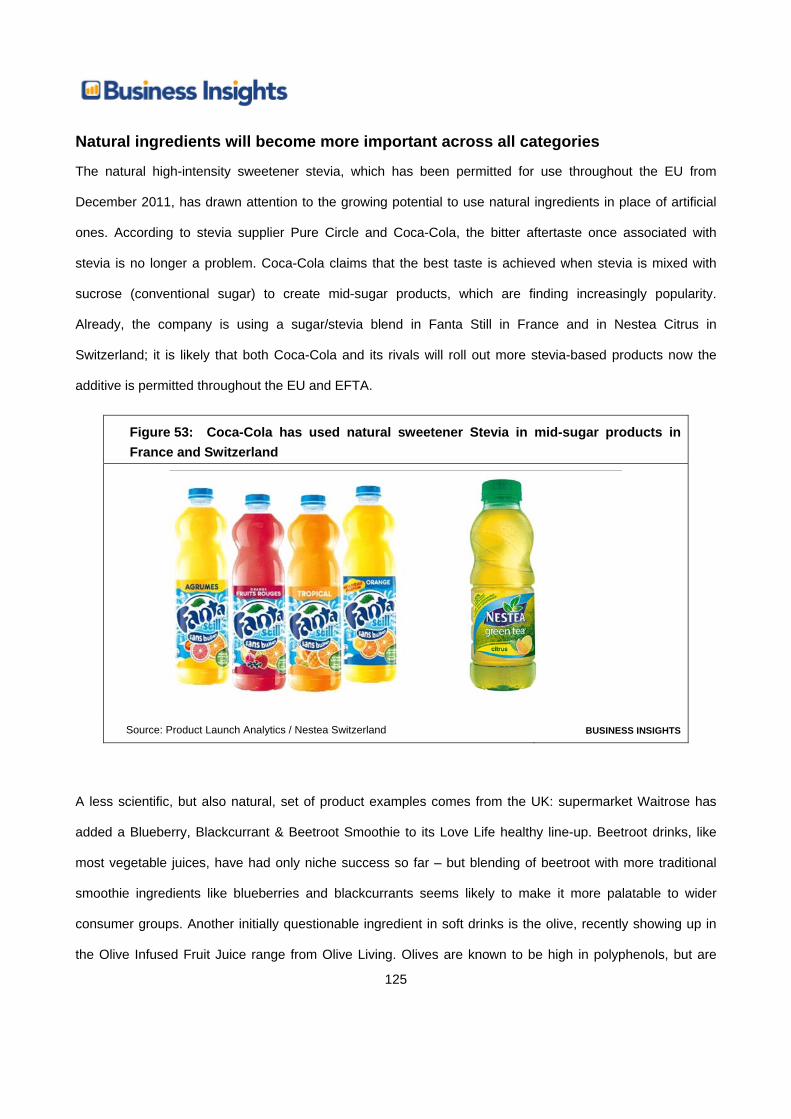

Natural ingredients will become more important across all categories 125

New packaging types allow delivery of active ingredients 126

Convenience remains important, despite economic changes 127 Functional convenience is a powerful trend overlap 127

Convenience needs to be balanced against brand image 128

Convenience is spreading to non-traditional categories and occasions 129

Chapter 5 The future of innovations in soft drinks 131

Summary 131 Introduction 132 Future regional trends 133 The stagnation of western markets 133

China’s shift towards consumption and global power 133

India’s slow, painful journey to consumer capitalism 134

Other developing countries continue to develop 134

Future marketing trends 135 The breakdown of big brands 135

6

The blurring of retailer and manufacturer 135

Personalization will become increasingly important 136

Future consumer trends 136 Demographics will favor health drinks in both west and east 136

Demographic positioning is becoming more complex 137

Novel non-fruit flavors will continue to launch, but will remain unloved 138

Future packaging trends 139 Sustainability will become second nature in packaging 139

Health concerns will also spread into packaging 140

New technologies will deliver consumer benefits 140

Appendix 142

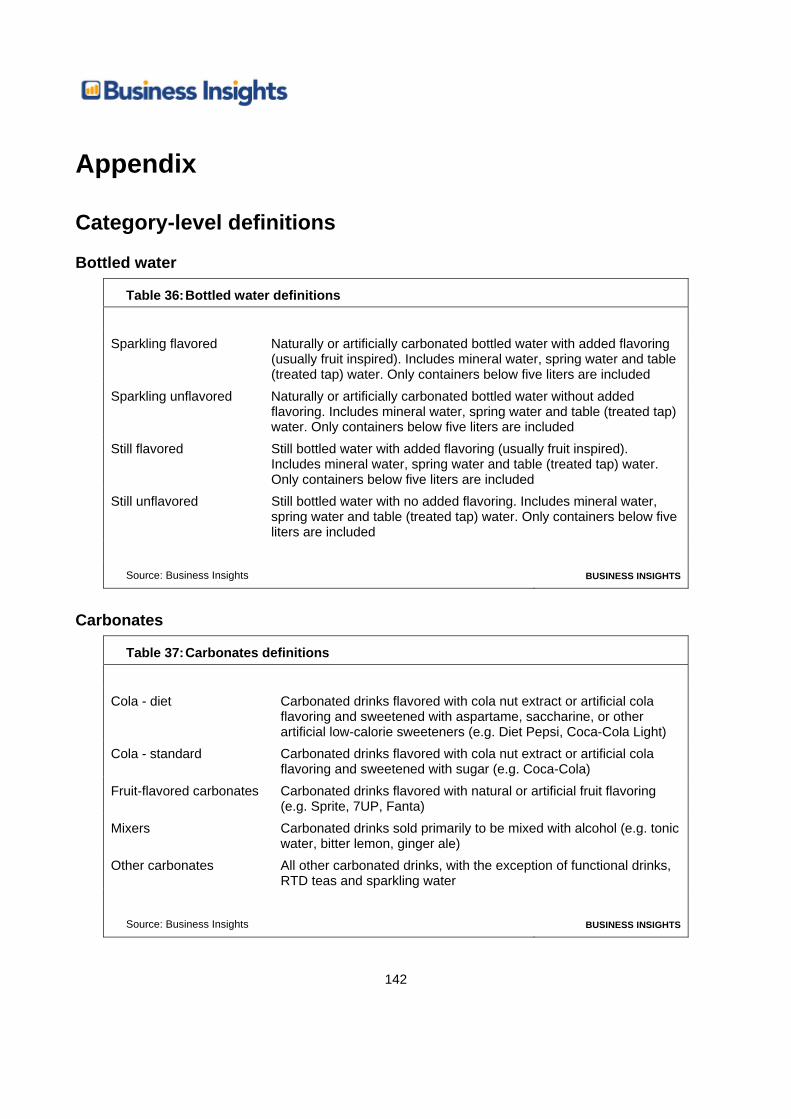

Category-level definitions 142 Bottled water 142

Carbonates 142

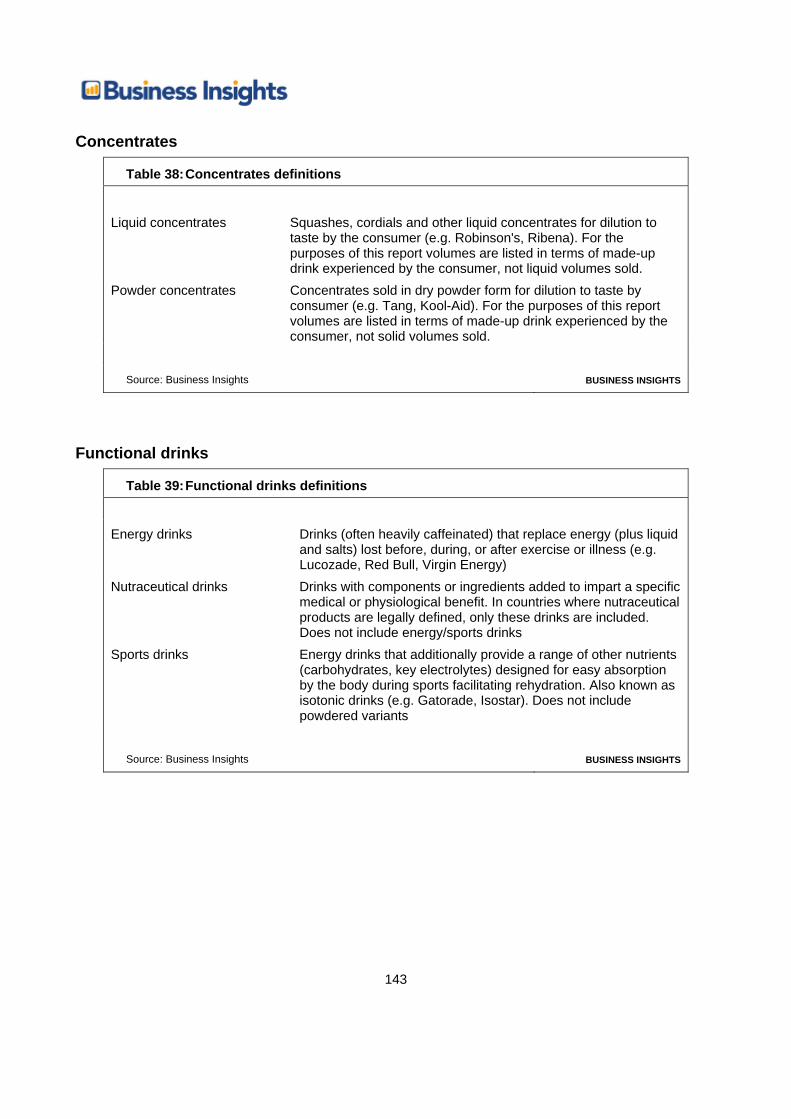

Concentrates 143

Functional drinks 143

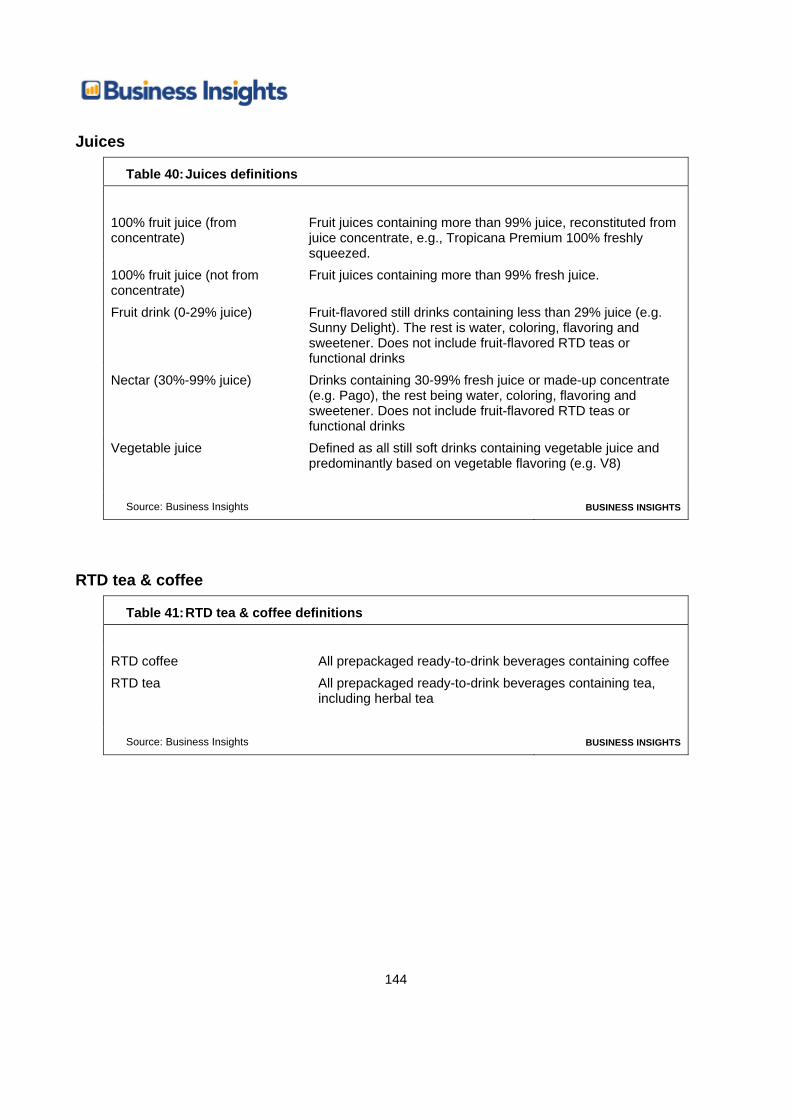

Juices 144

RTD tea & coffee 144

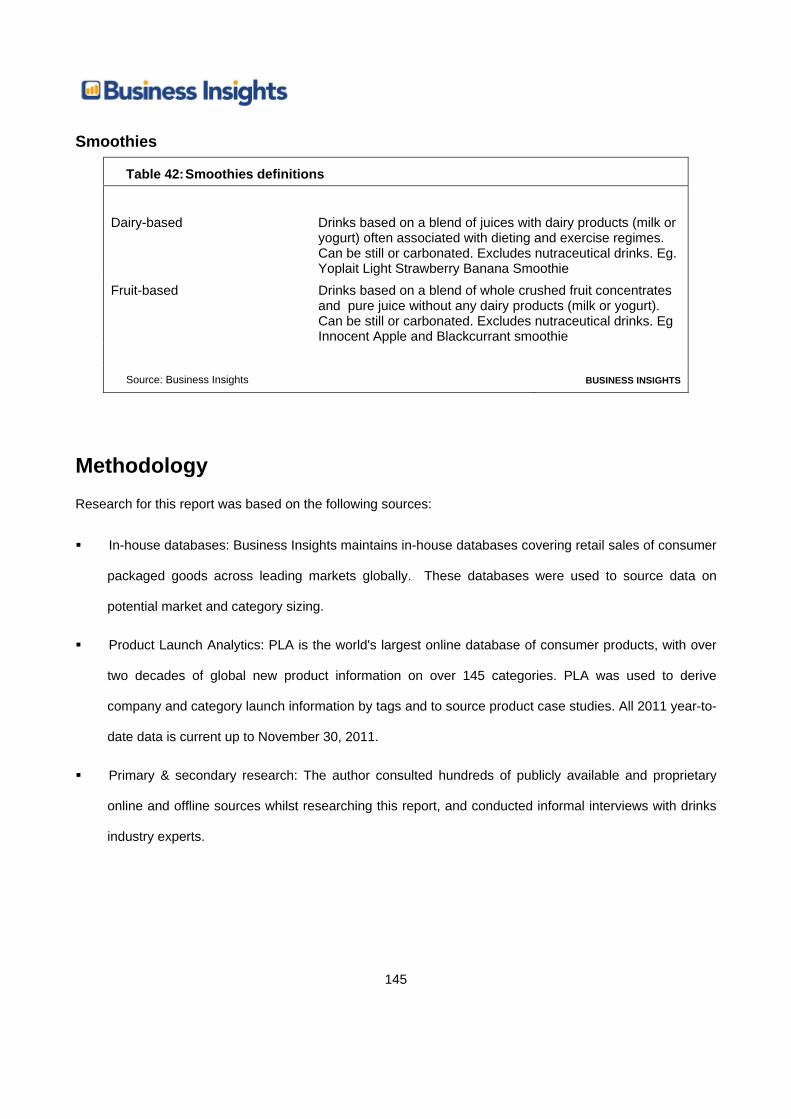

Smoothies 145

Methodology 145

7

Table of figures Figure 1: Global soft drinks value by category ($ bn), 2005-2015 21

Figure 2: Global soft drinks volume by category (liters bn), 2005-2015 22

Figure 3: Global soft drinks value & volume growth by category, 2005-10 23

Figure 4: Global soft drinks value & volume growth forecast by category, 2010-15 24

Figure 5: Global soft drinks price growth by category, 2005-2015 25

Figure 6: Global soft drinks value by region ($ bn), 2005-2015 26

Figure 7: Global soft drinks volume by region (liters bn), 2005-2015 27

Figure 8: Global soft drinks value & volume growth by region, 2005-2010 28

Figure 9: Global soft drinks forecast value & volume growth by region, 2010-2015 29

Figure 10: Global soft drinks price growth by region, 2005-2015 30

Figure 11: Soft drinks value growth by major country, 2005-2015 41

Figure 12: Soft drinks volume growth by major country, 2005-2015 42

Figure 13: Soft drinks price growth by major country, 2005-2015 43

Figure 14: Coca-Cola’s Minute Maid Pulpy was developed in China and rolled out worldwide 47

Figure 15: Soft drinks new product launches by category, 2006-2011 62

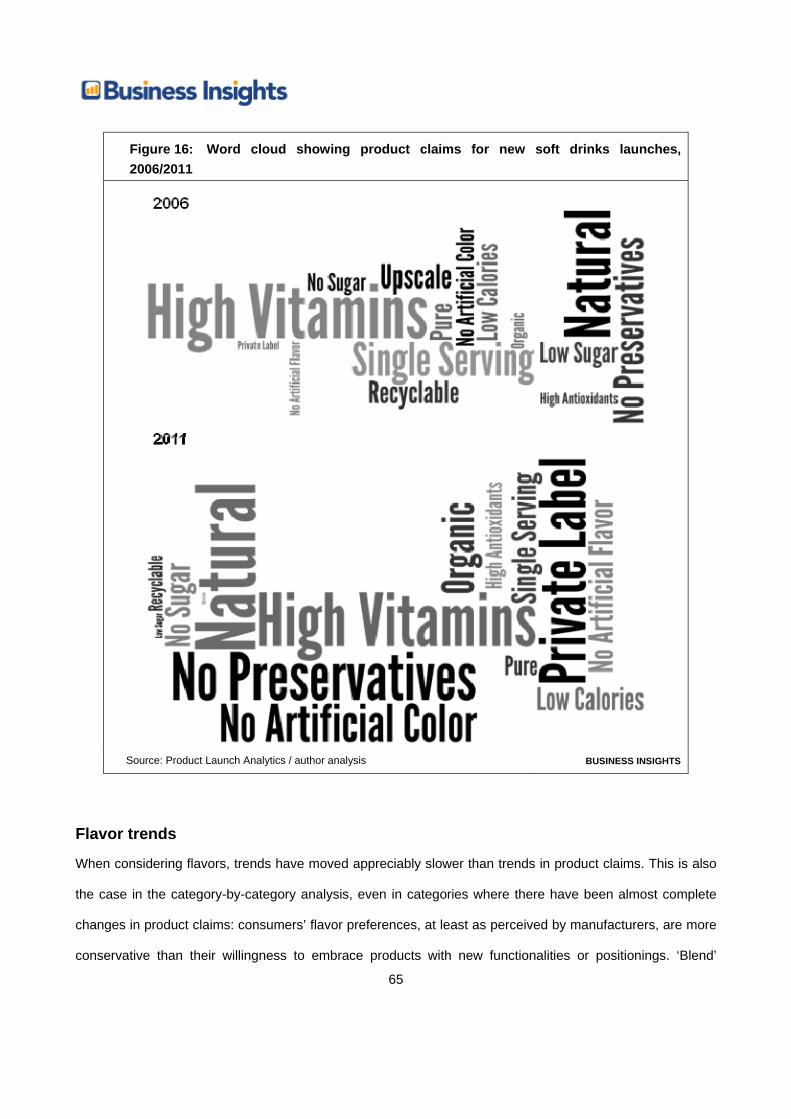

Figure 16: Word cloud showing product claims for new soft drinks launches, 2006/2011 65

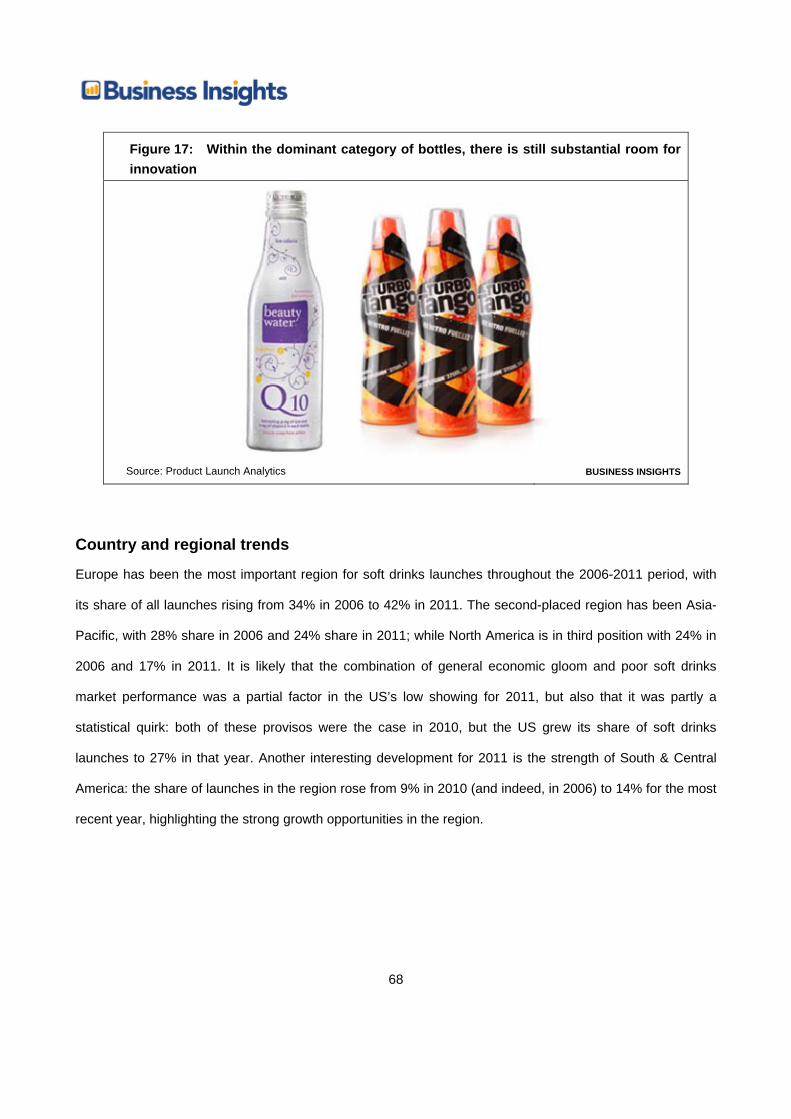

Figure 17: Within the dominant category of bottles, there is still substantial room for innovation 68

Figure 18: Soft drinks new product launches by region, 2006-2011 69

Figure 19: Innovative new product launches by innovation type, 2006-2011 71

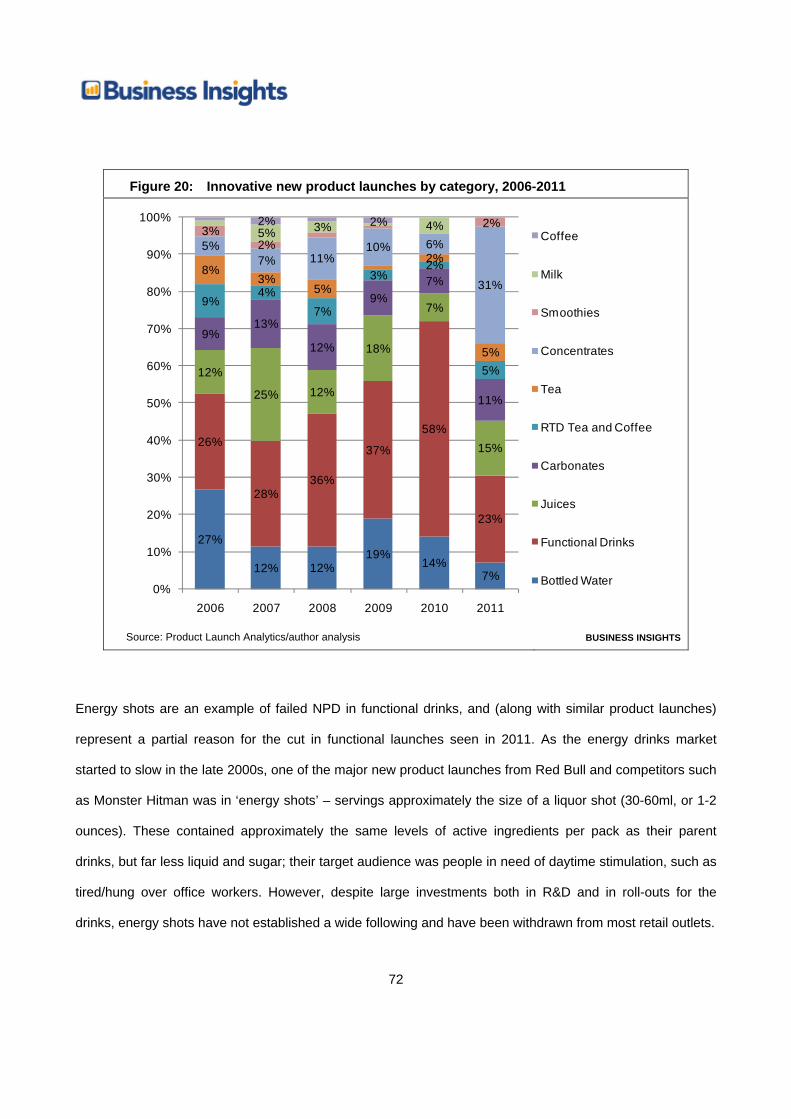

Figure 20: Innovative new product launches by category, 2006-2011 72

Figure 21: Innovative ‘energy shots’ from Red Bull and Monster Hitman were ultimately unsuccessful 73

Figure 22: Word cloud showing product claims for new bottled water launches, 2006/2011 76

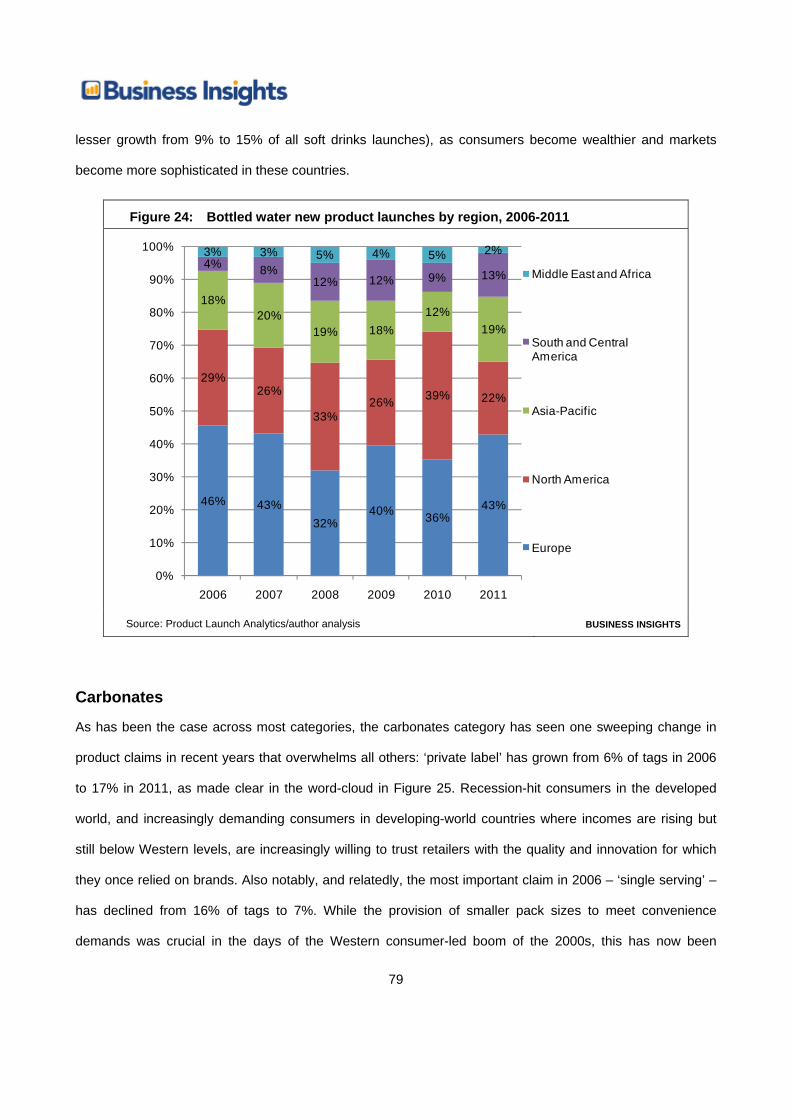

Figure 23: Many North American retailers have launched ranges of premium private label flavored bottled waters 77

Figure 24: Bottled water new product launches by region, 2006-2011 79

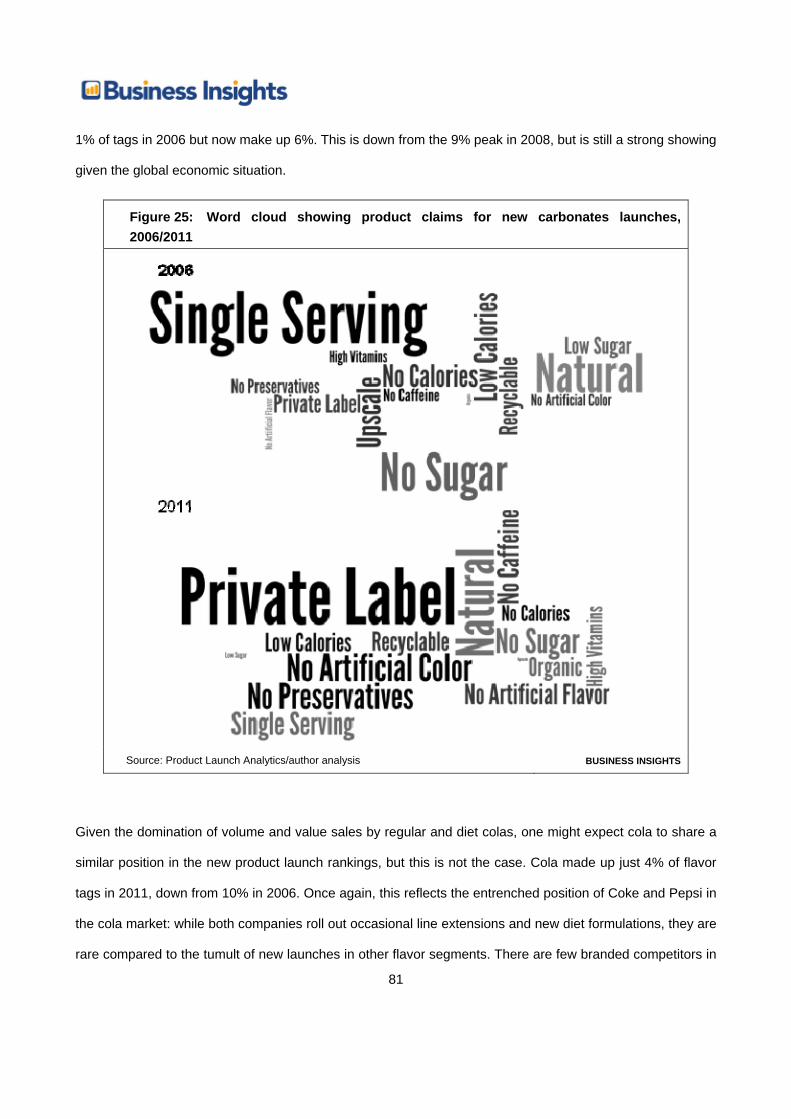

Figure 25: Word cloud showing product claims for new carbonates launches, 2006/2011 81

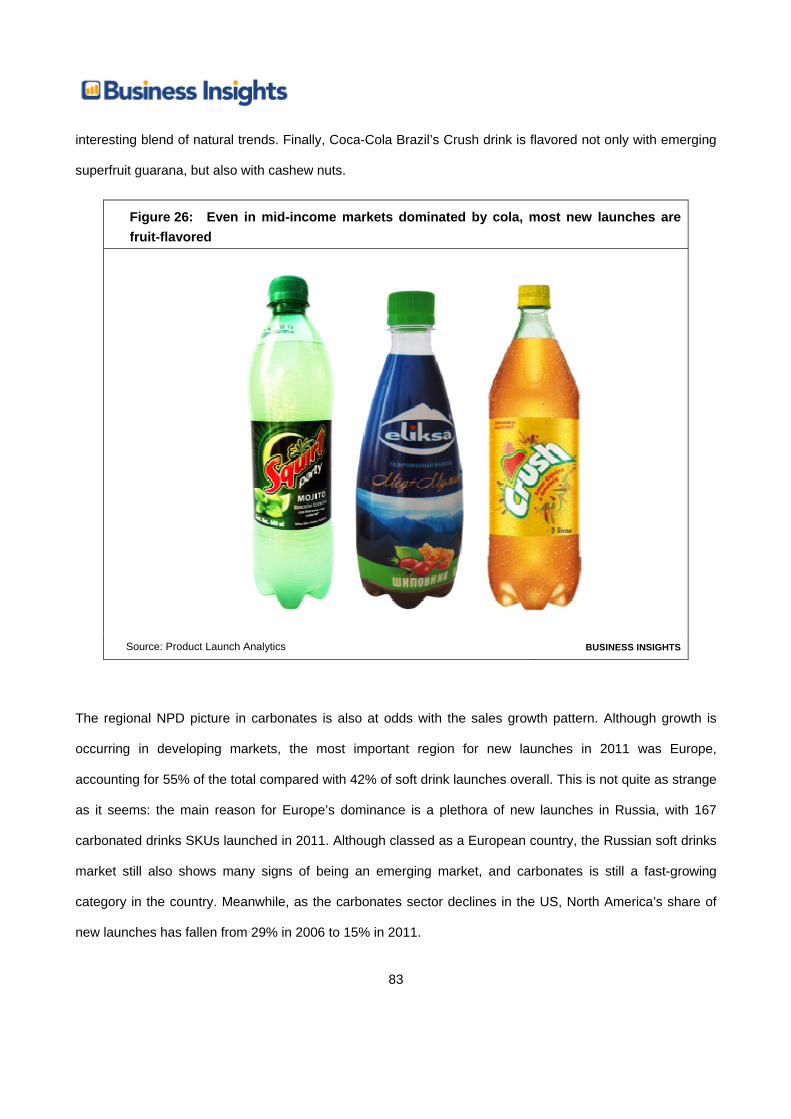

Figure 26: Even in mid-income markets dominated by cola, most new launches are fruit-flavored 83

Figure 27: Carbonates new product launches by region, 2006-2011 84

Figure 28: Word cloud showing product claims for new concentrates launches, 2006/2011 86

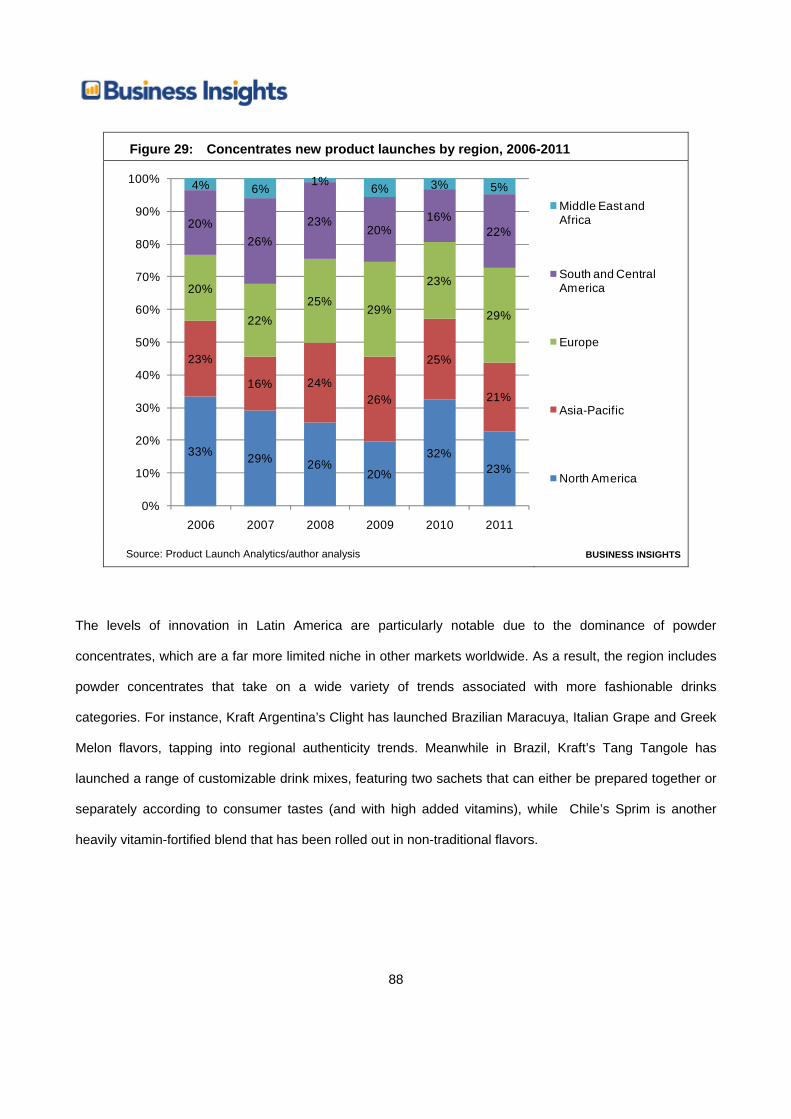

Figure 29: Concentrates new product launches by region, 2006-2011 88

8

Figure 30: Powder concentrates dominate in Latin America, including premium on-trend variants 89

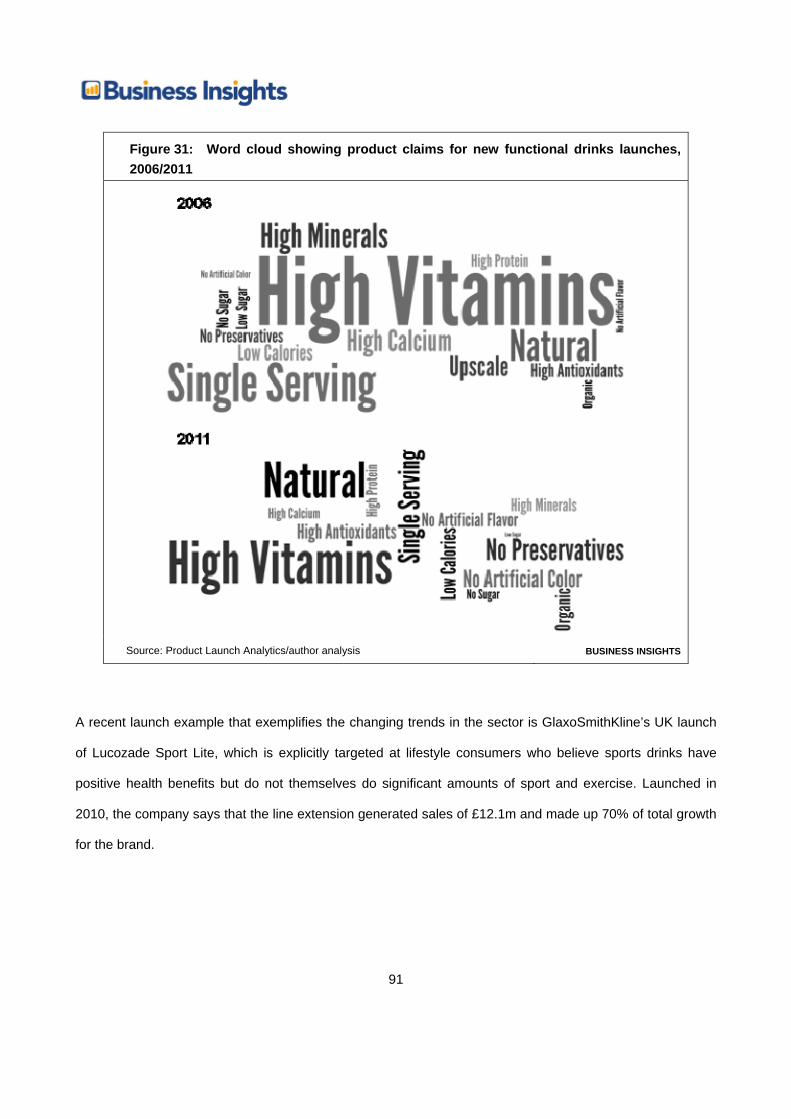

Figure 31: Word cloud showing product claims for new functional drinks launches, 2006/201191

Figure 32: Lucozade Sports Lite has a superficial sports positioning, but is primarily aimed at lifestyle users 92

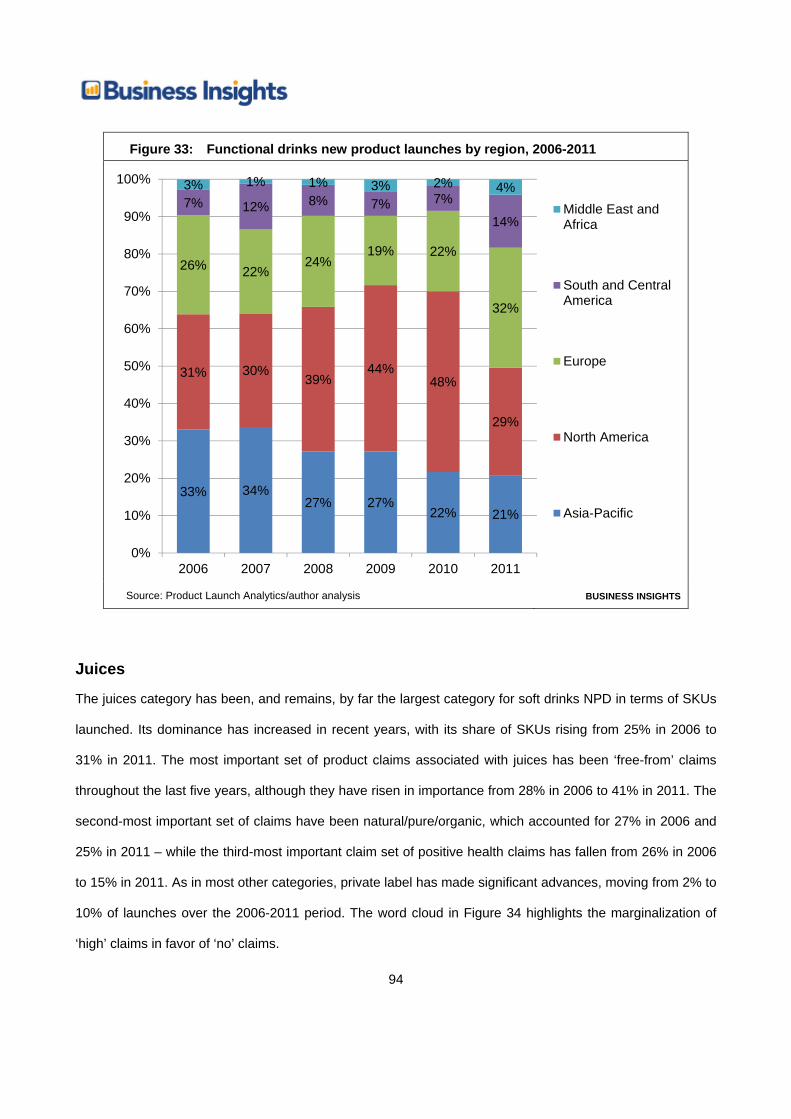

Figure 33: Functional drinks new product launches by region, 2006-2011 94

Figure 34: Word cloud showing product claims for new juices launches, 2006/2011 96

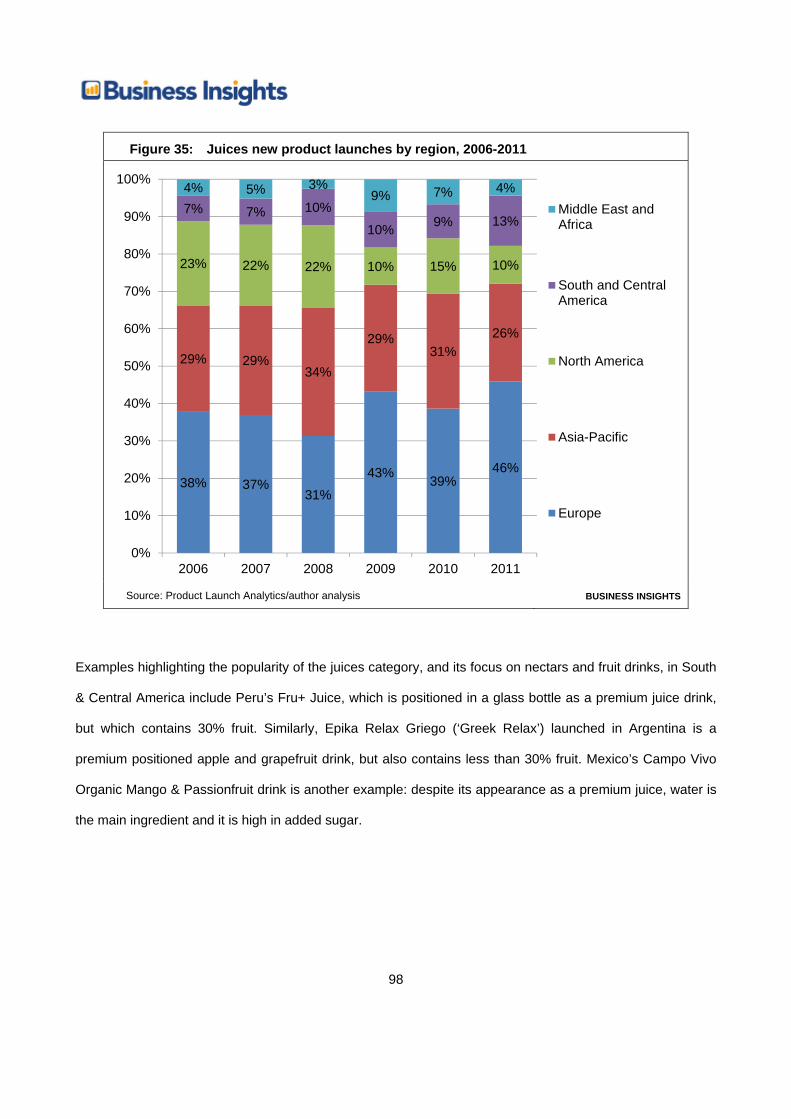

Figure 35: Juices new product launches by region, 2006-2011 98

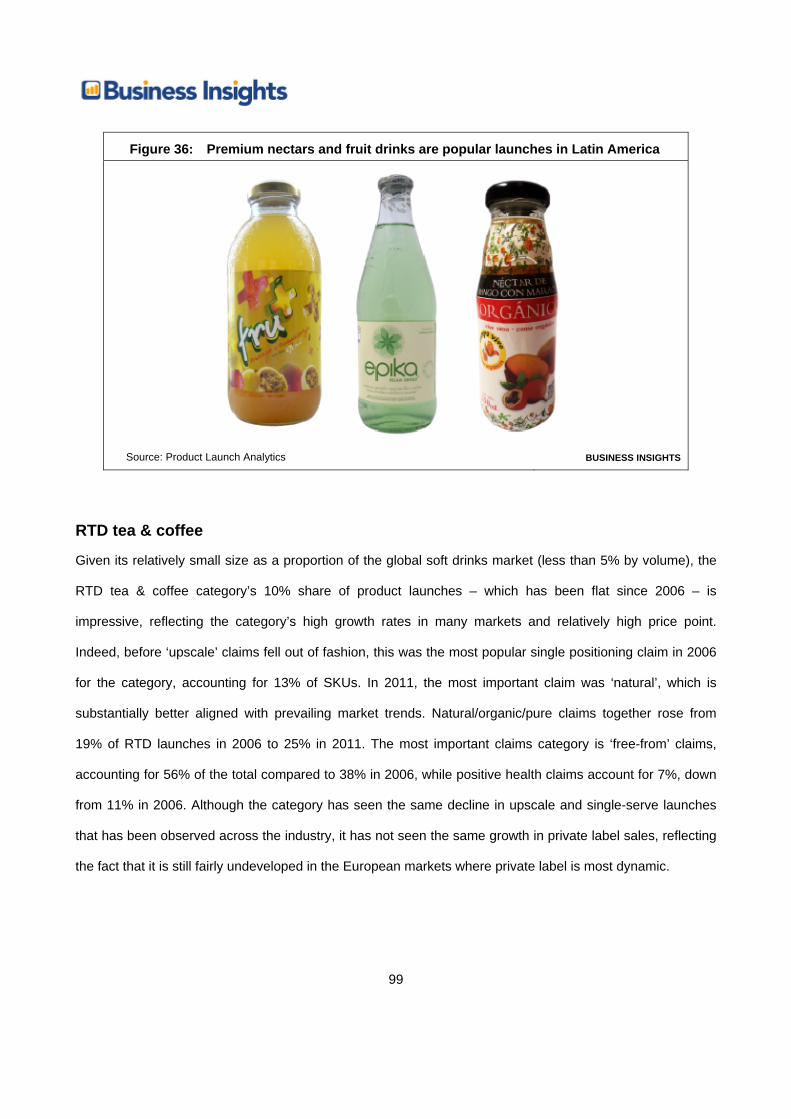

Figure 36: Premium nectars and fruit drinks are popular launches in Latin America 99

Figure 37: Word cloud showing product claims for new RTD tea & coffee launches, 2006/2011 101

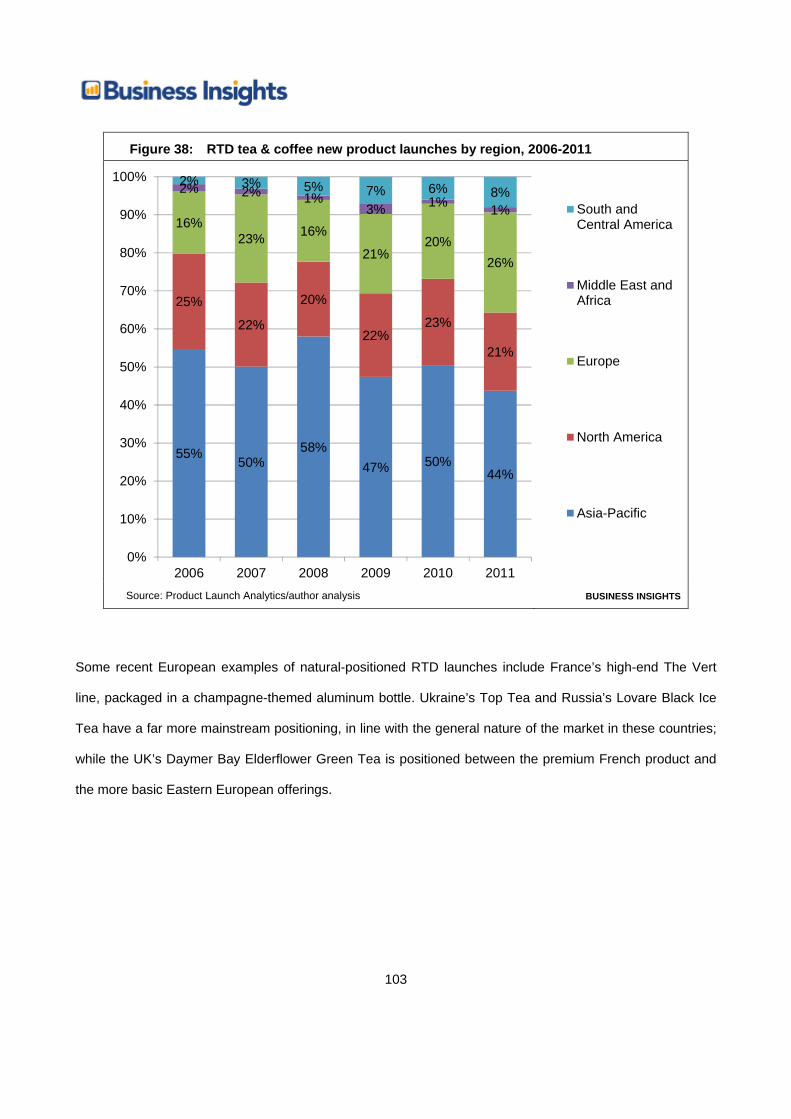

Figure 38: RTD tea & coffee new product launches by region, 2006-2011 103

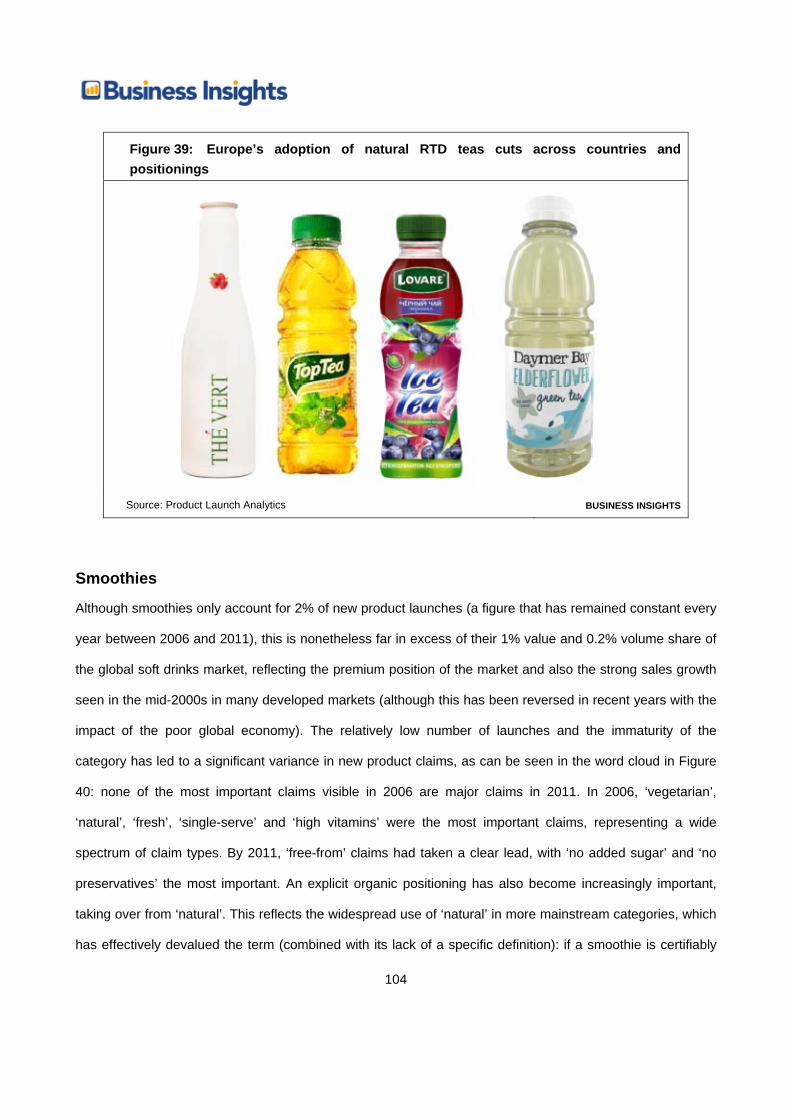

Figure 39: Europe’s adoption of natural RTD teas cuts across countries and positionings 104

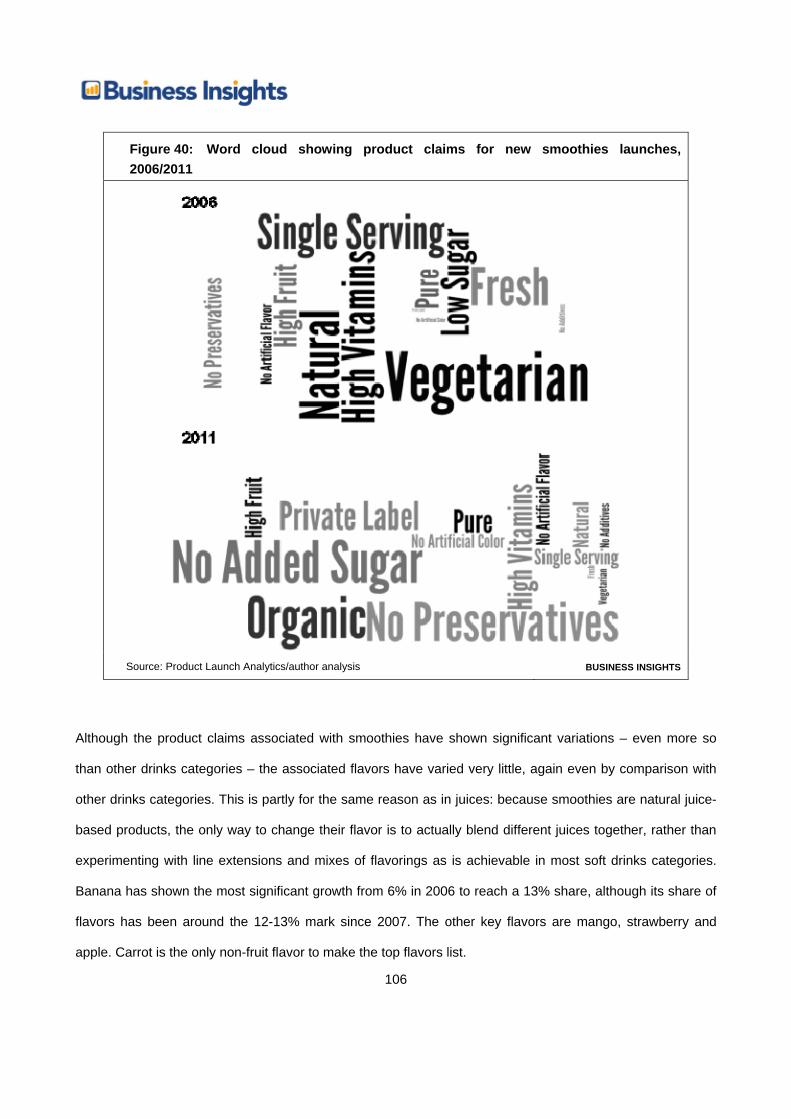

Figure 40: Word cloud showing product claims for new smoothies launches, 2006/2011 106

Figure 41: Protein Plus Parfait Smoothie is a novel formulation, but a conventional strawberry flavor 108

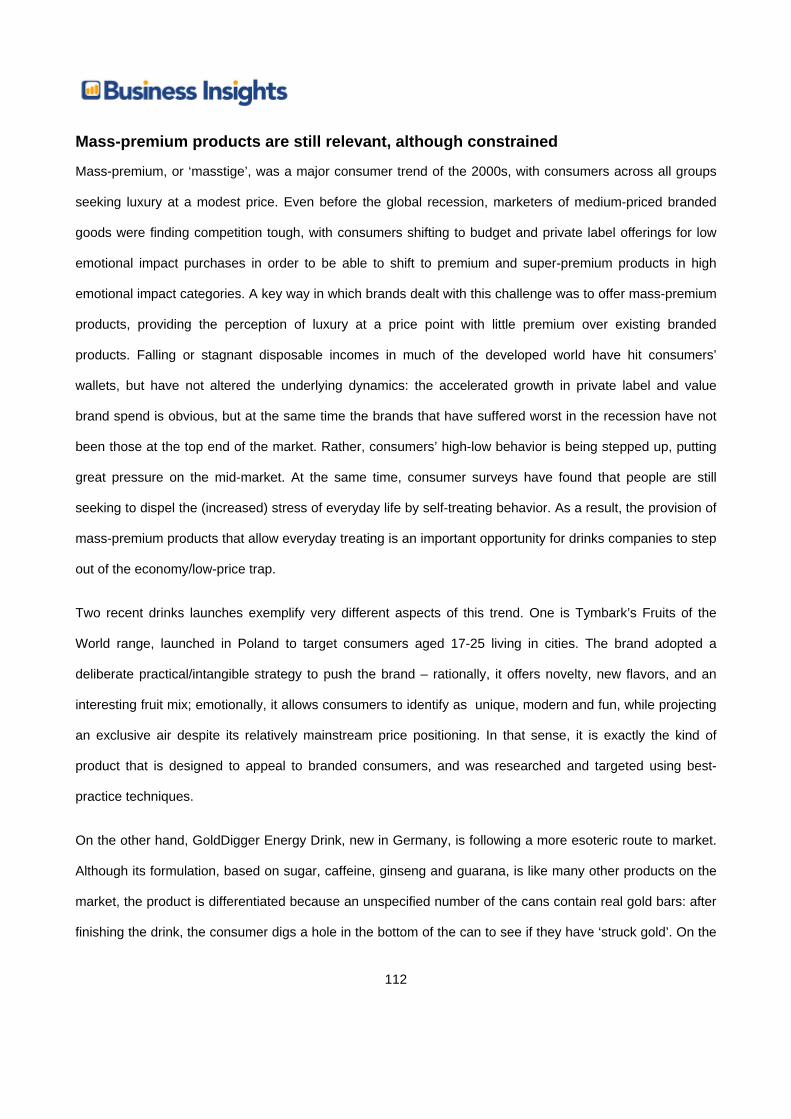

Figure 42: Tymark Fruit of the World and Gold Digger tap into the mass-premium trend in very different ways 113

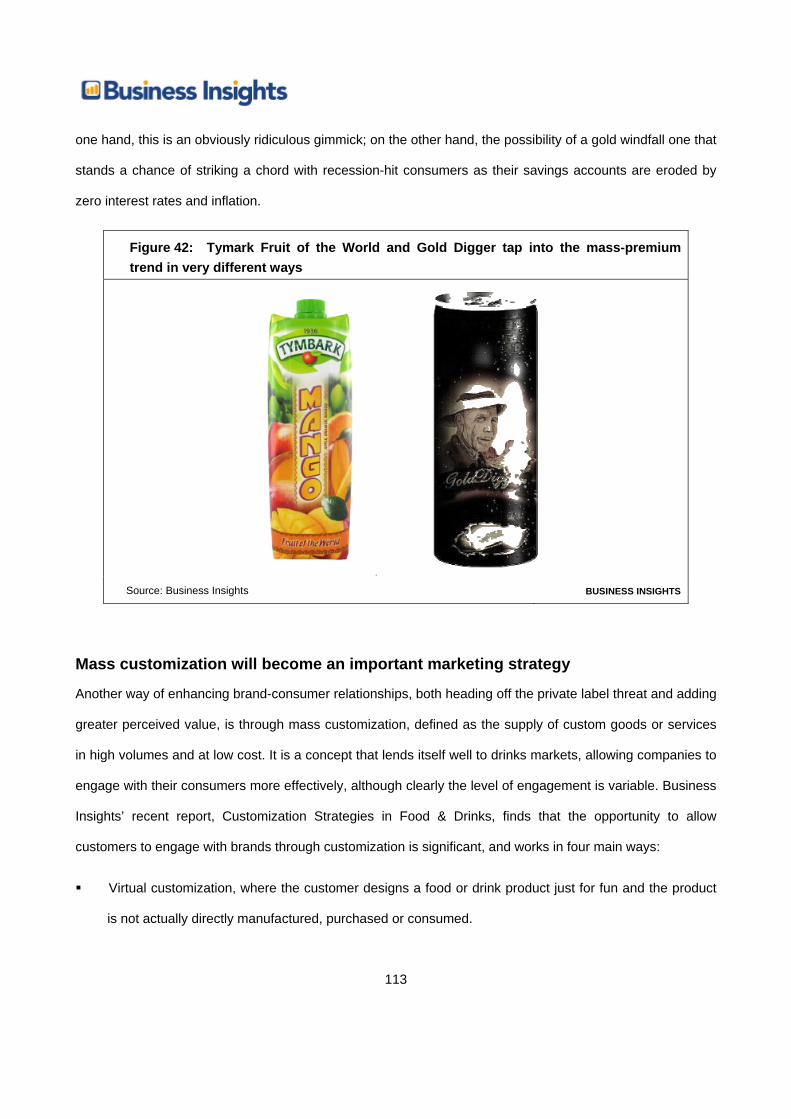

Figure 43: Starbucks’ Frappuccino website allows customers to create their own virtual drink114

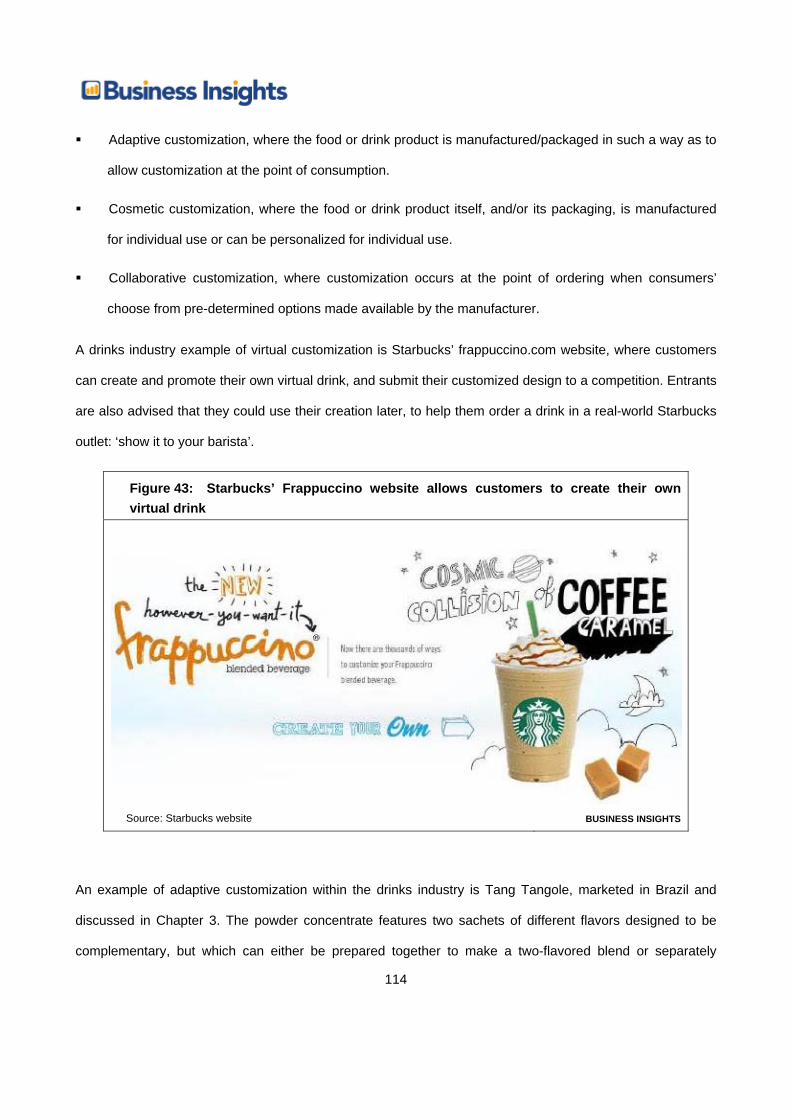

Figure 44: VitaSoy launched 70 limited edition packs with greeting messages, and also allowed full customization via its website 115

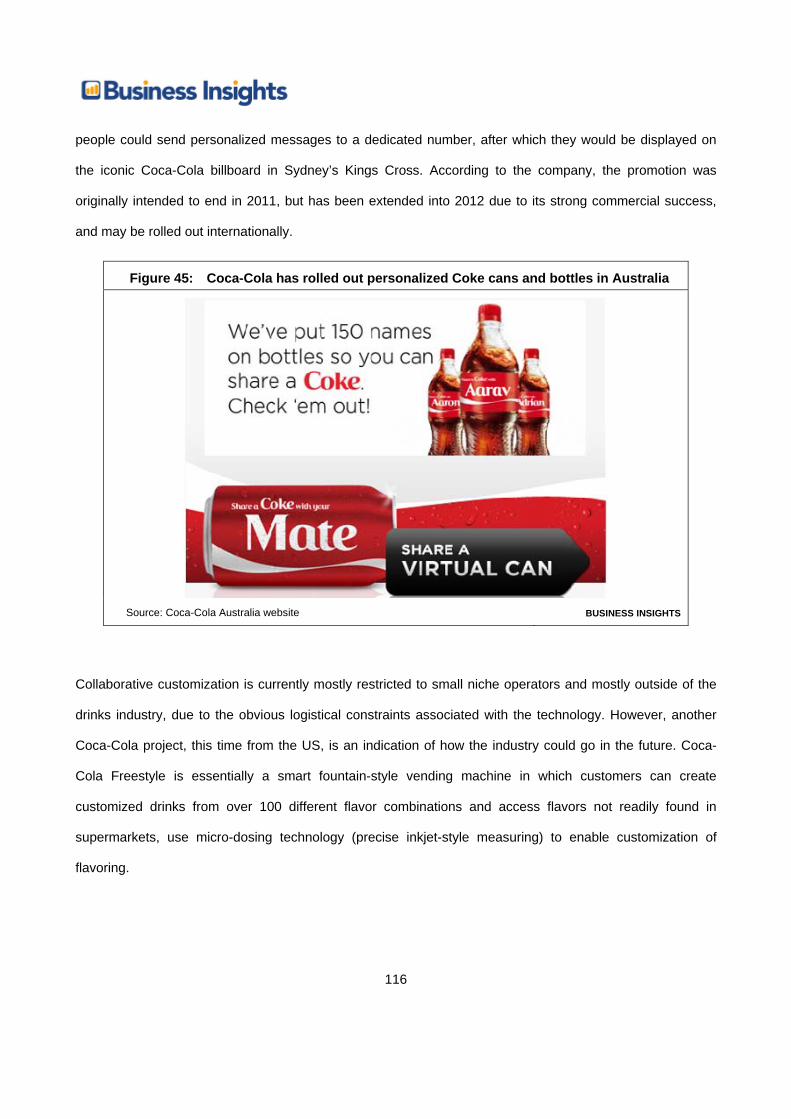

Figure 45: Coca-Cola has rolled out personalized Coke cans and bottles in Australia 116

Figure 46: The Tropicana Essentials range is PepsiCo’s attempt to enter the functional drinks market 118

Figure 47: Drinkoff Sobering Jam and Mind Essential Confidence Shot both offer unusual functional benefits 119

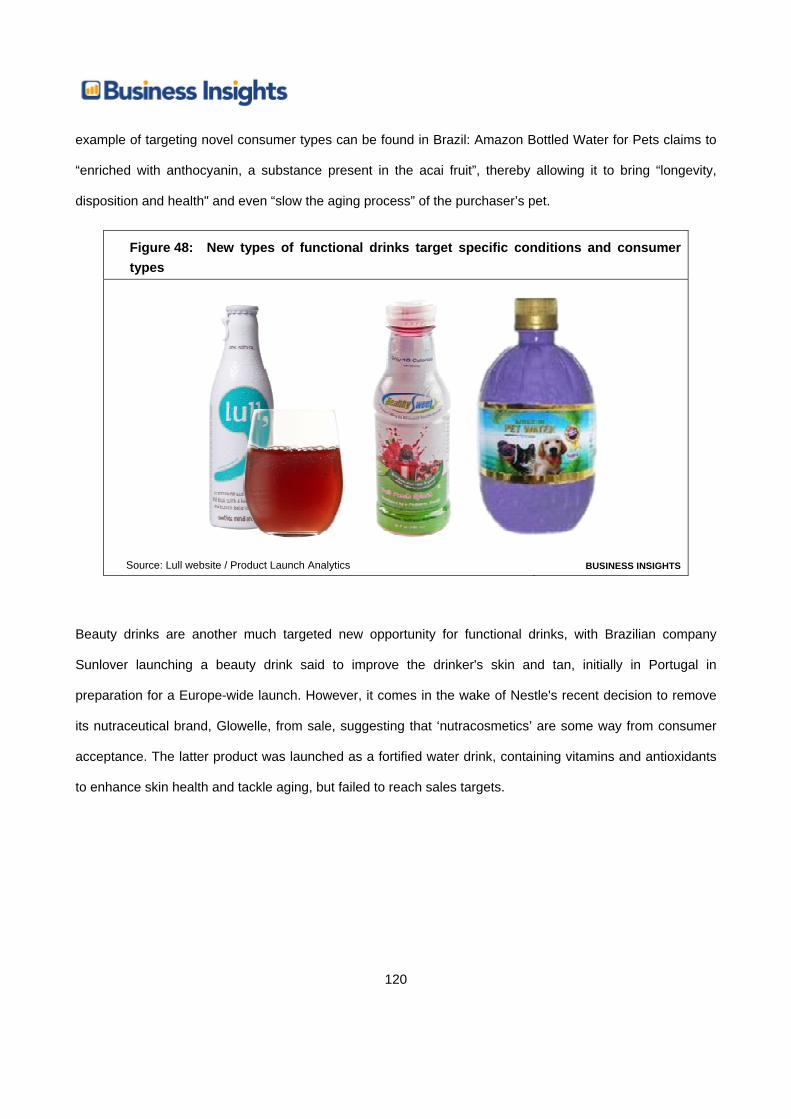

Figure 48: New types of functional drinks target specific conditions and consumer types 120

Figure 49: Brazilian brand Sunlover is hoping to succeed where Nestle’s Glowelle failed 121

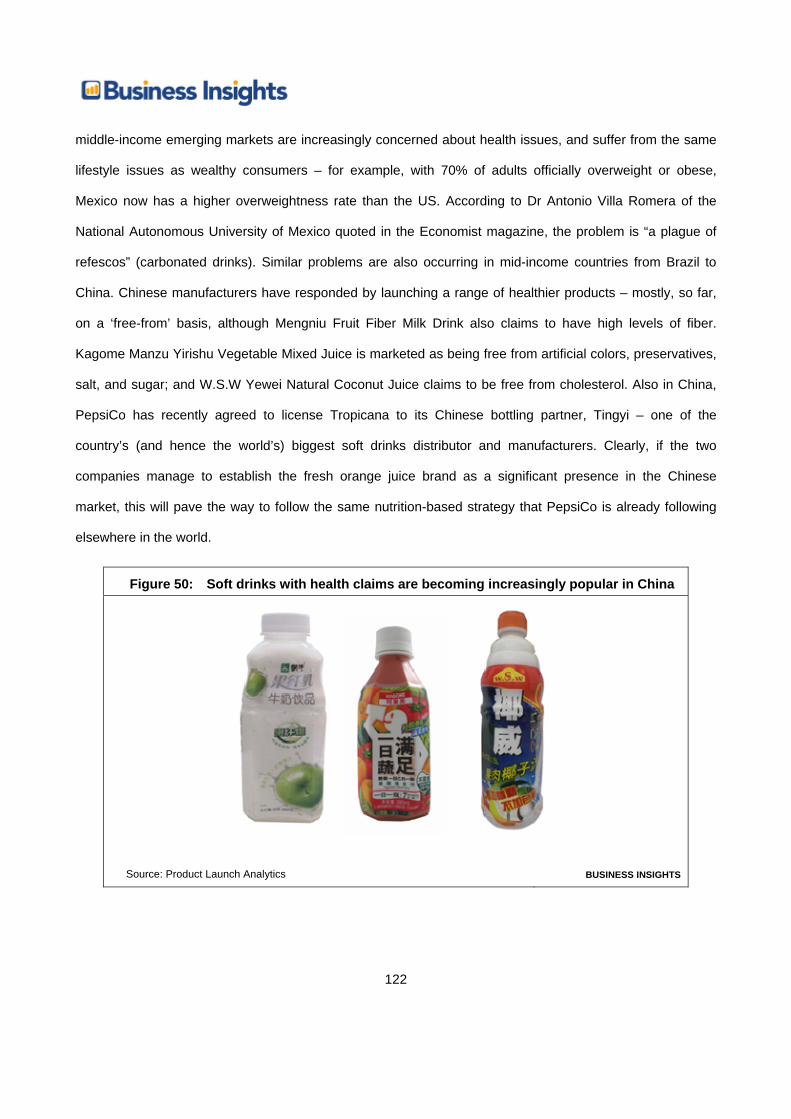

Figure 50: Soft drinks with health claims are becoming increasingly popular in China 122

Figure 51: Key drivers behind consumer interest in sustainable drinks 123

Figure 52: Coca-Cola and Pepsi have both launched sustainably-positioned recyclable bottle types 124

Figure 53: Coca-Cola has used natural sweetener Stevia in mid-sugar products in France and Switzerland 125

Figure 54: Beetroot and olives are examples of non-traditional naturally functional drinks ingredients 126

9

Figure 55: Activate Workout and Boost Kid Essentials are both finally mixed as part of the consumer’s drinking process 127

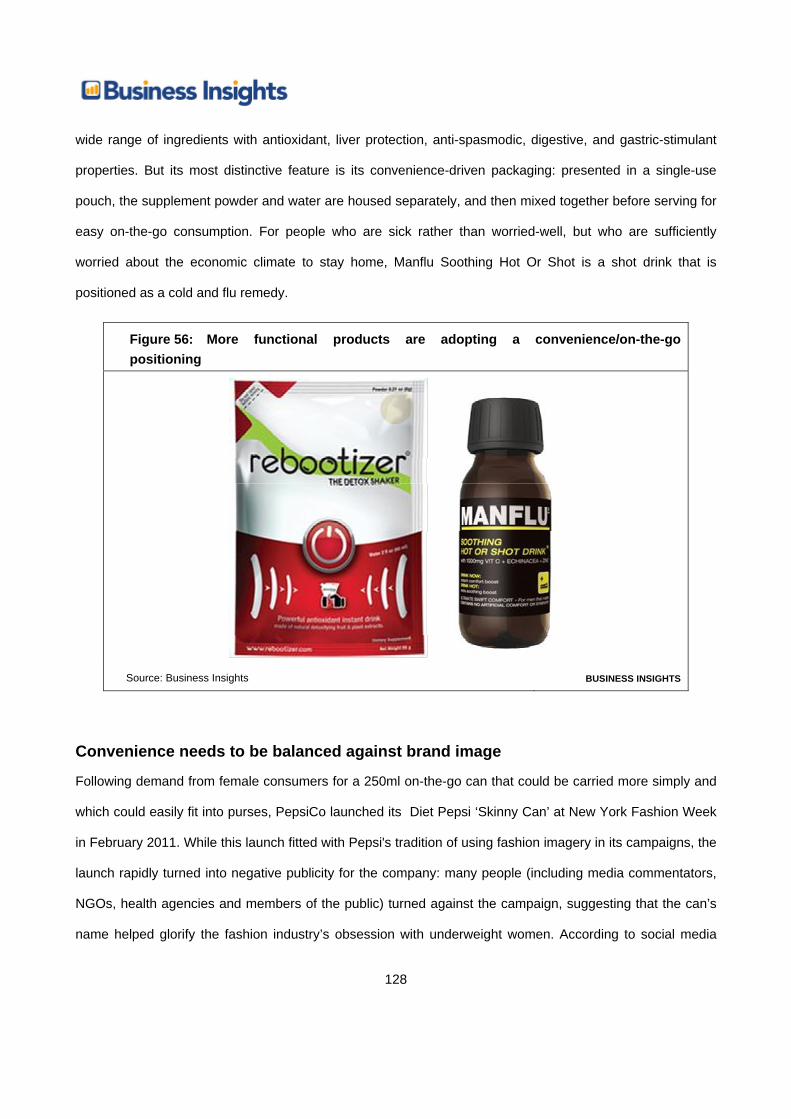

Figure 56: More functional products are adopting a convenience/on-the-go positioning 128

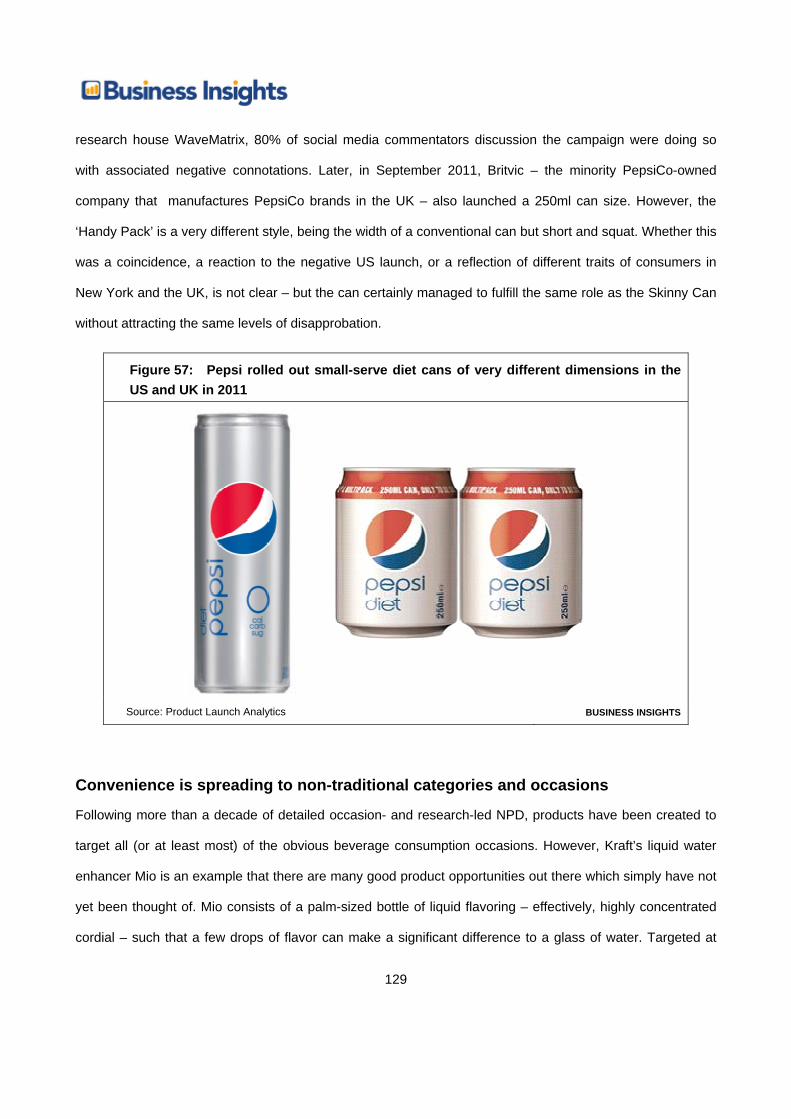

Figure 57: Pepsi rolled out small-serve diet cans of very different dimensions in the US and UK in 2011 129

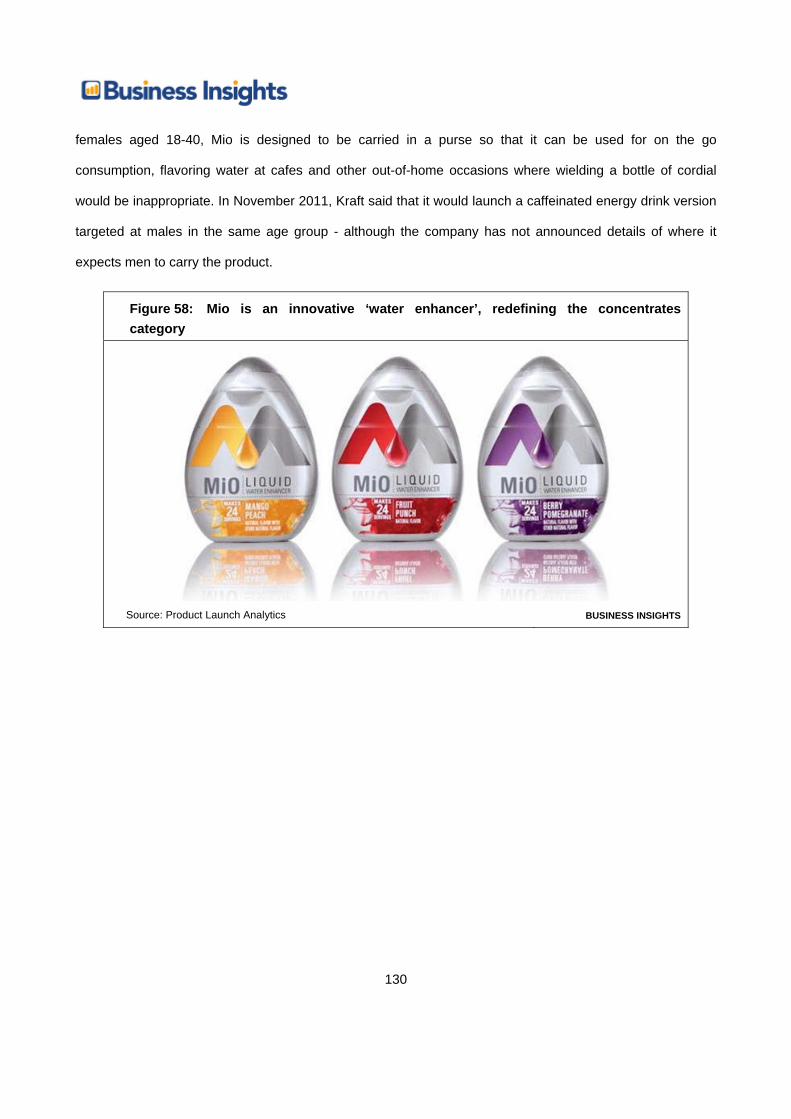

Figure 58: Mio is an innovative ‘water enhancer’, redefining the concentrates category 130

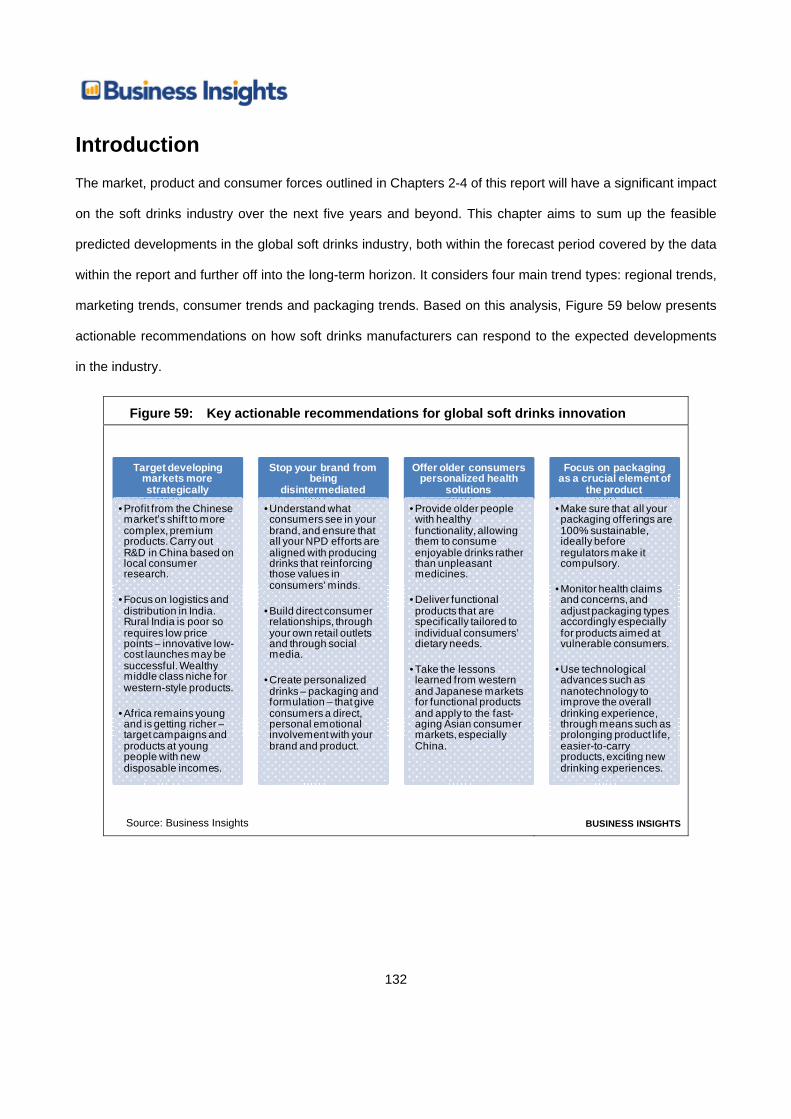

Figure 59: Key actionable recommendations for global soft drinks innovation 132

Figure 60: Child-focused Bot Water was relaunched as a drink without a specific demographic positioning 138

Figure 61: It seems unlikely that these salt-based soft drinks will reach the mainstream 139

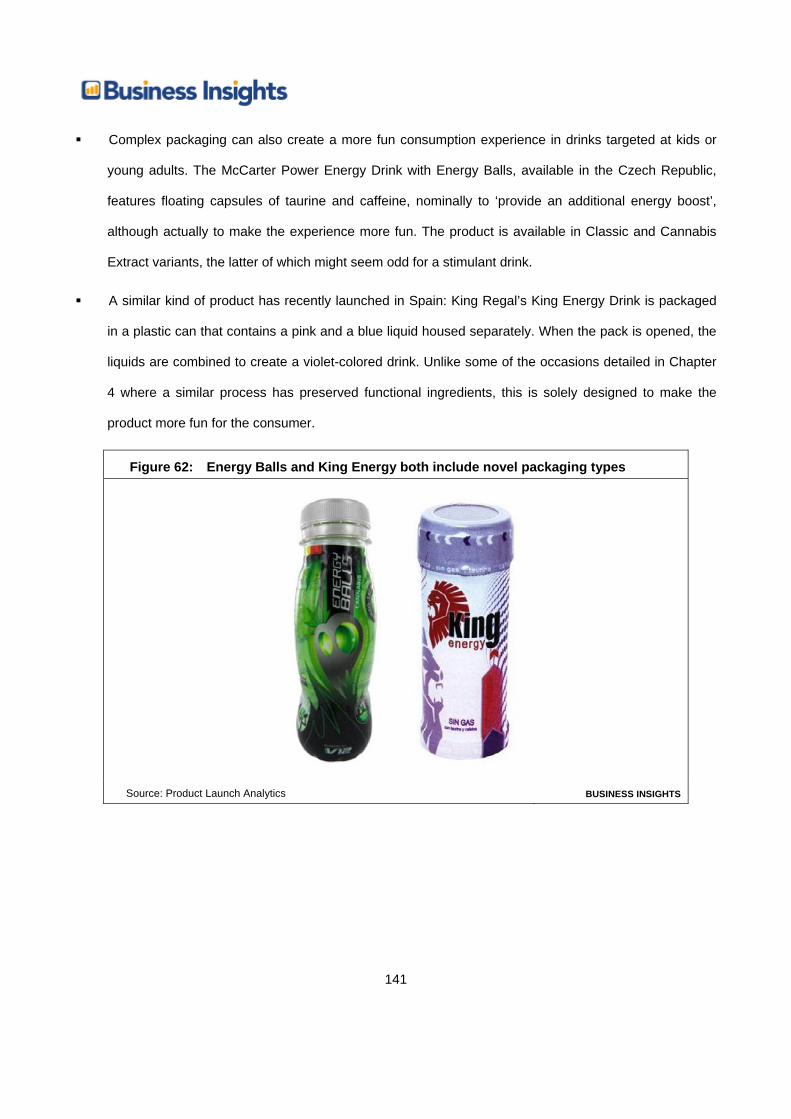

Figure 62: Energy Balls and King Energy both include novel packaging types 141

10

Table of tables Table 1: Global bottled water market by category, 2005-2015 31

Table 2: Global carbonates market by category, 2005-2015 33

Table 3: Global concentrates market by category, 2005-2015 34

Table 4: Global functional drinks market by category, 2005-2015 35

Table 5: Global juices market by category, 2005-2015 37

Table 6: Global RTD tea & coffee market by category, 2005-2015 39

Table 7: Global smoothies market by category, 2005-2015 40

Table 8: Brazil soft drinks market by category, 2005-2015 45

Table 9: China soft drinks market by category, 2005-2015 46

Table 10: France soft drinks market by category, 2005-2015 48

Table 11: Germany soft drinks market by category, 2005-2015 50

Table 12: India soft drinks market by category, 2005-2015 51

Table 13: Italy soft drinks market by category, 2005-2015 52

Table 14: Japan soft drinks market by category, 2005-2015 54

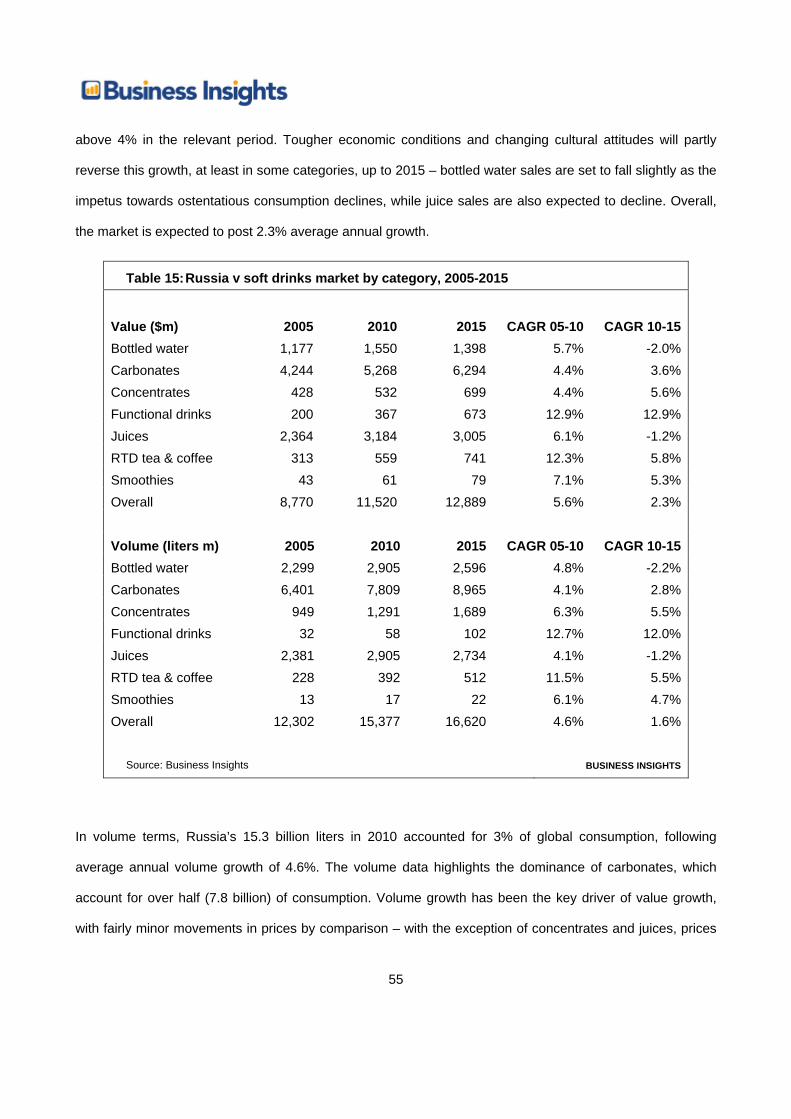

Table 15: Russia v soft drinks market by category, 2005-2015 55

Table 16: United Kingdom soft drinks market by category, 2005-2015 57

Table 17: United States soft drinks market by category, 2005-2015 59

Table 18: Soft drinks new product launches by product claim, 2006-2011 63

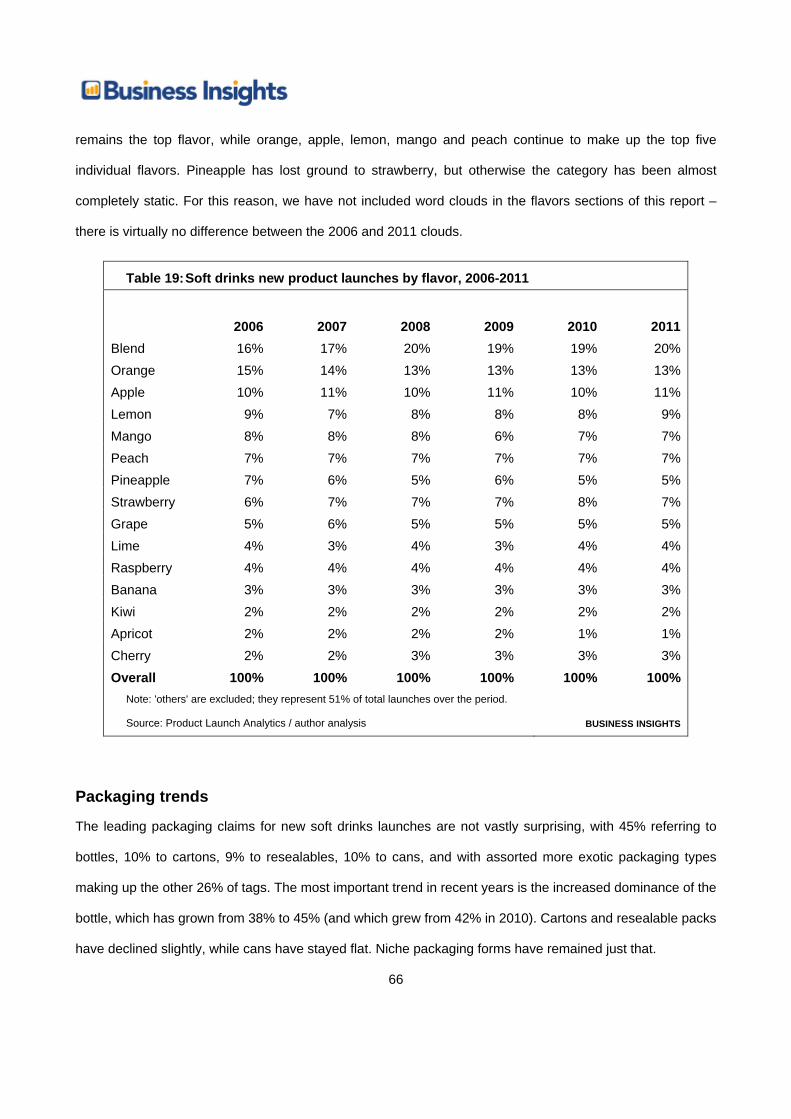

Table 19: Soft drinks new product launches by flavor, 2006-2011 66

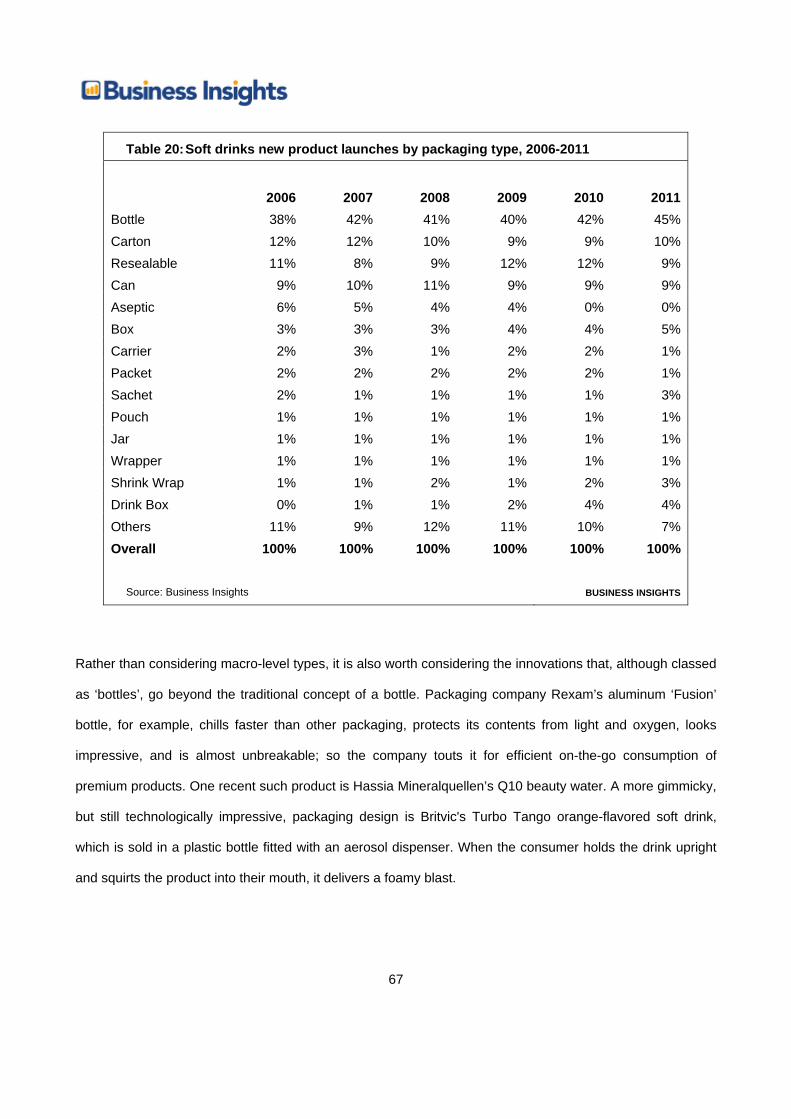

Table 20: Soft drinks new product launches by packaging type, 2006-2011 67

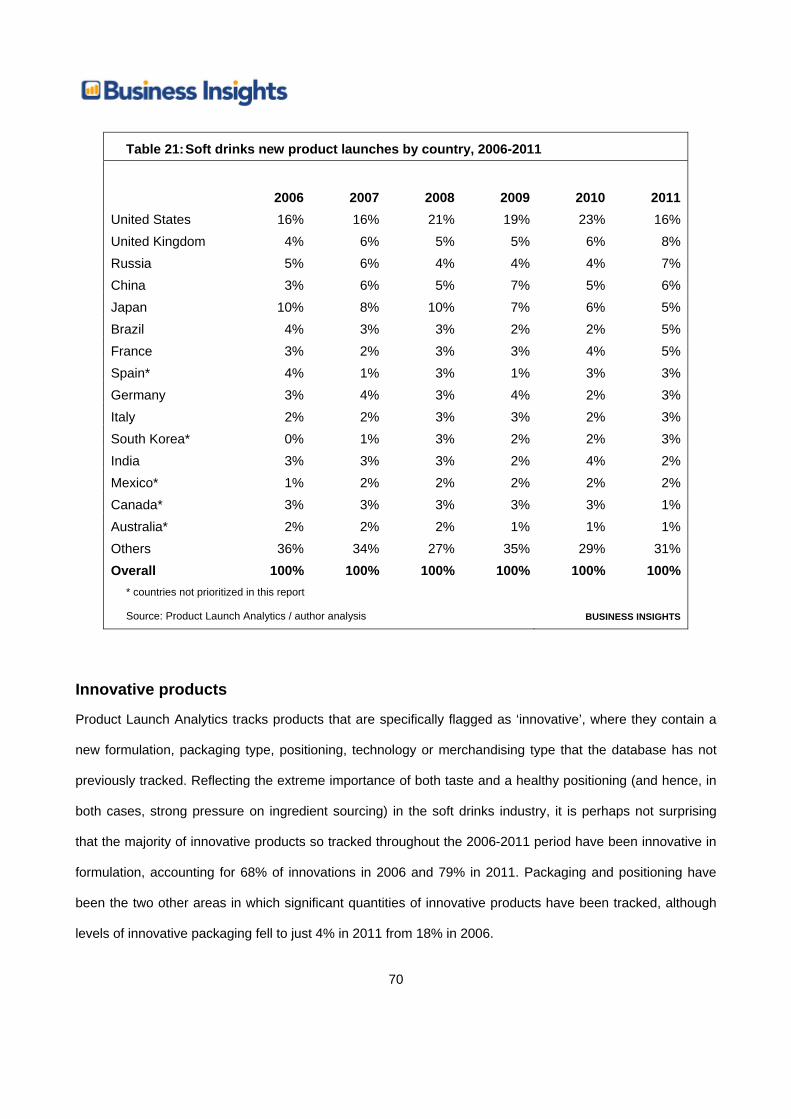

Table 21: Soft drinks new product launches by country, 2006-2011 70

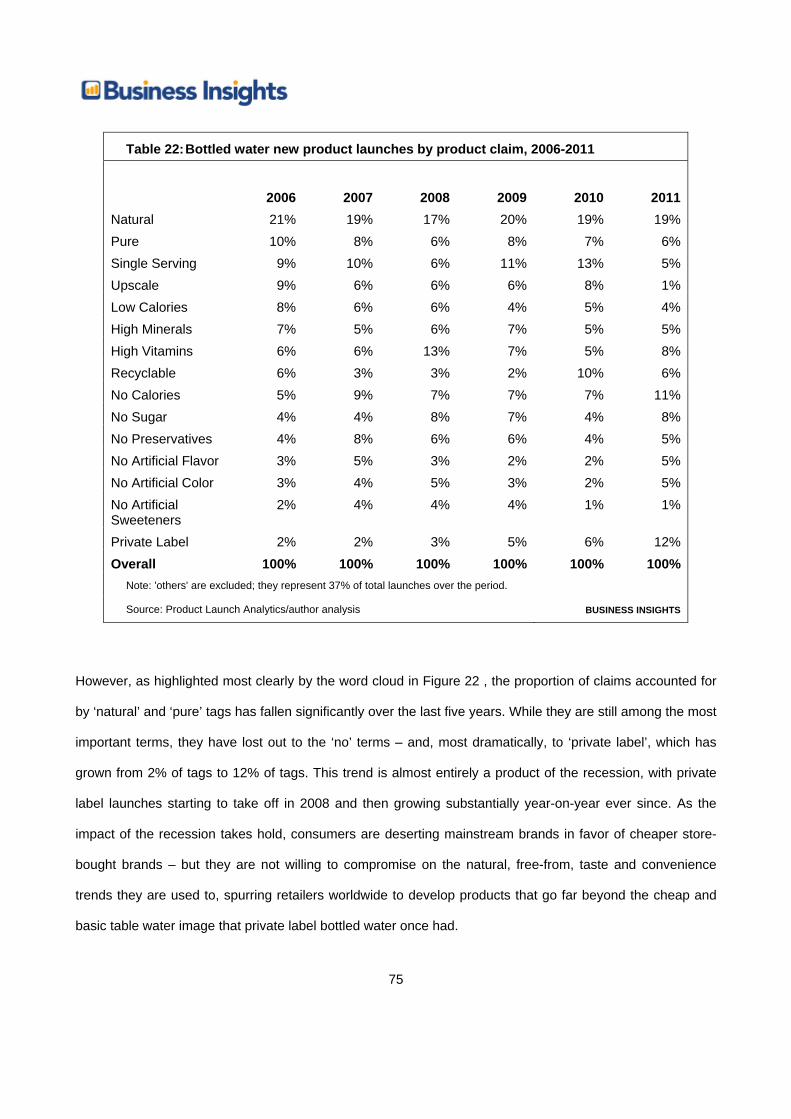

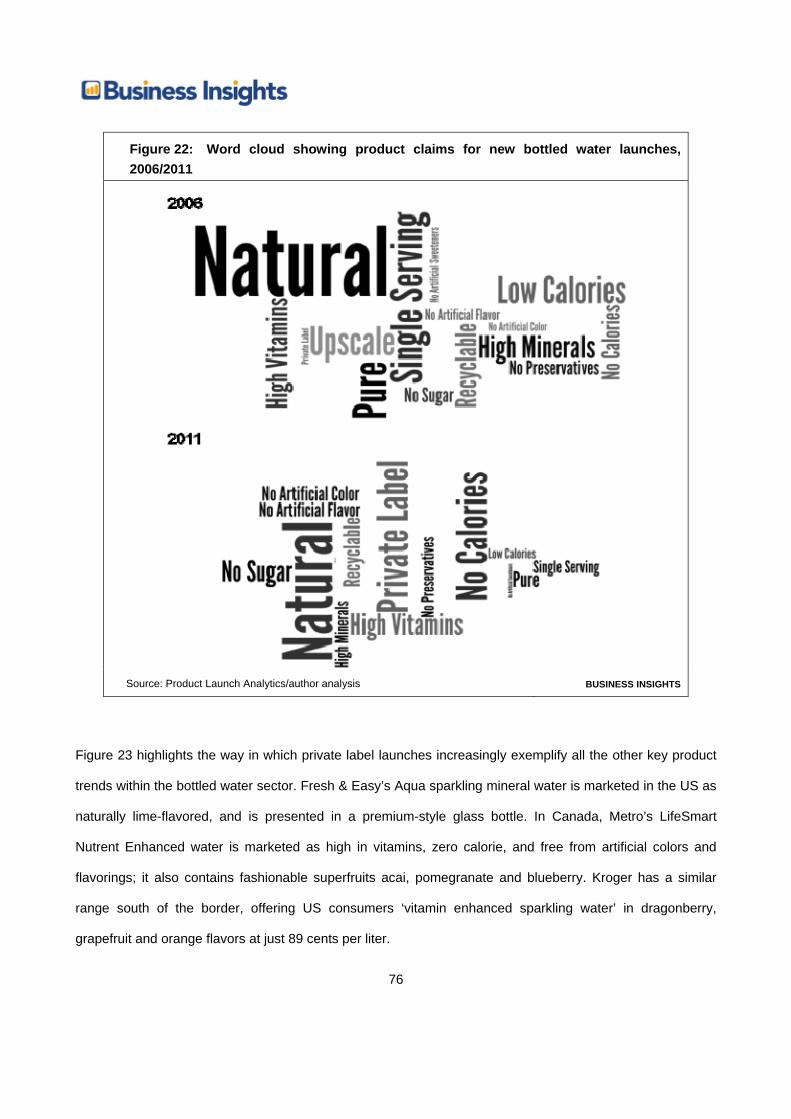

Table 22: Bottled water new product launches by product claim, 2006-2011 75

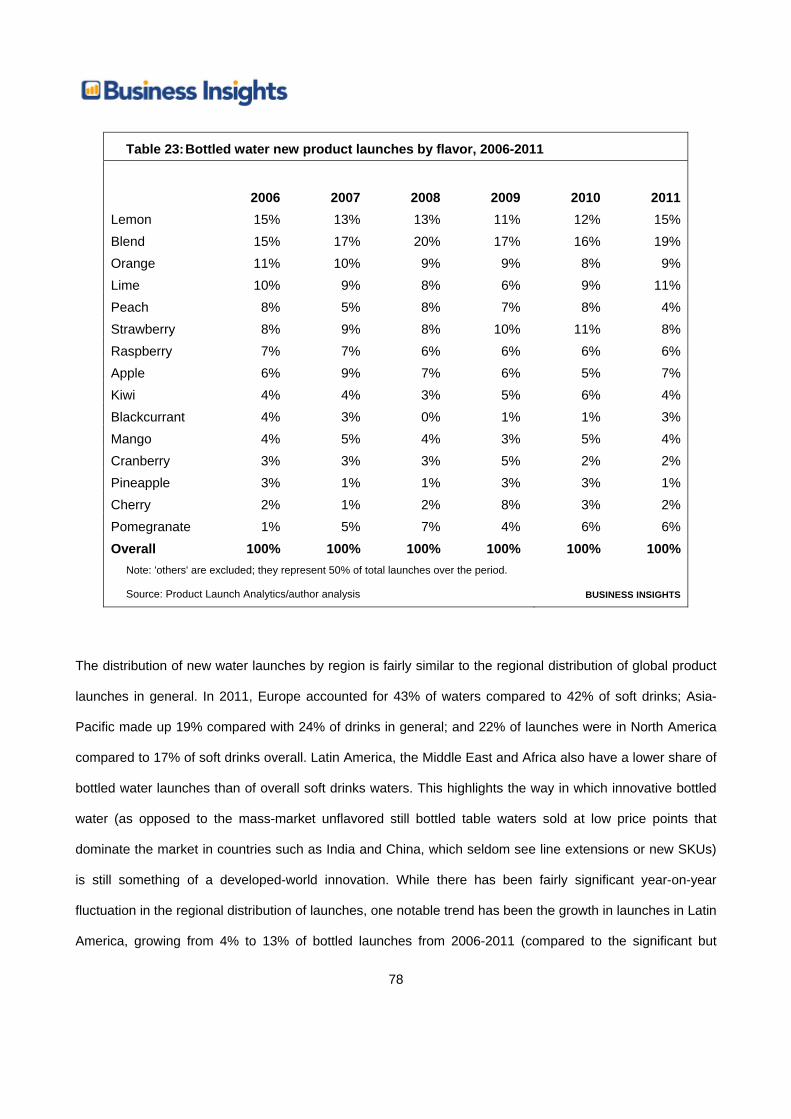

Table 23: Bottled water new product launches by flavor, 2006-2011 78

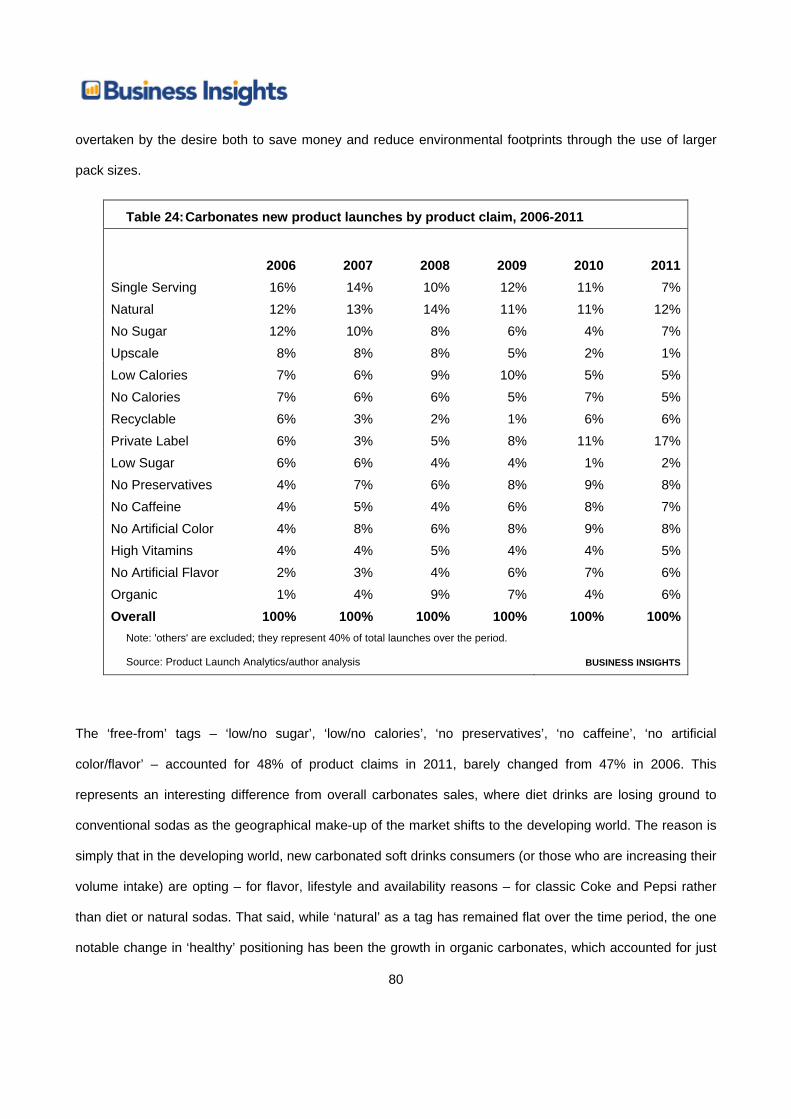

Table 24: Carbonates new product launches by product claim, 2006-2011 80

Table 25: Carbonates new product launches by flavor, 2006-2011 82

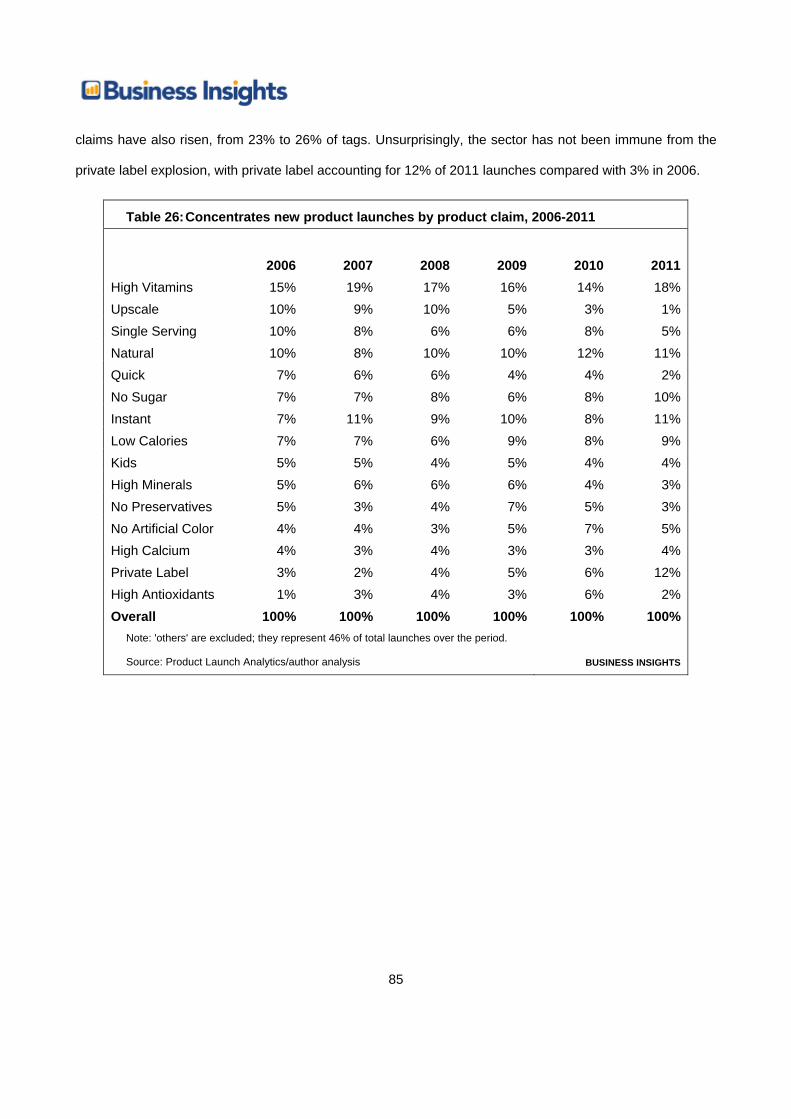

Table 26: Concentrates new product launches by product claim, 2006-2011 85

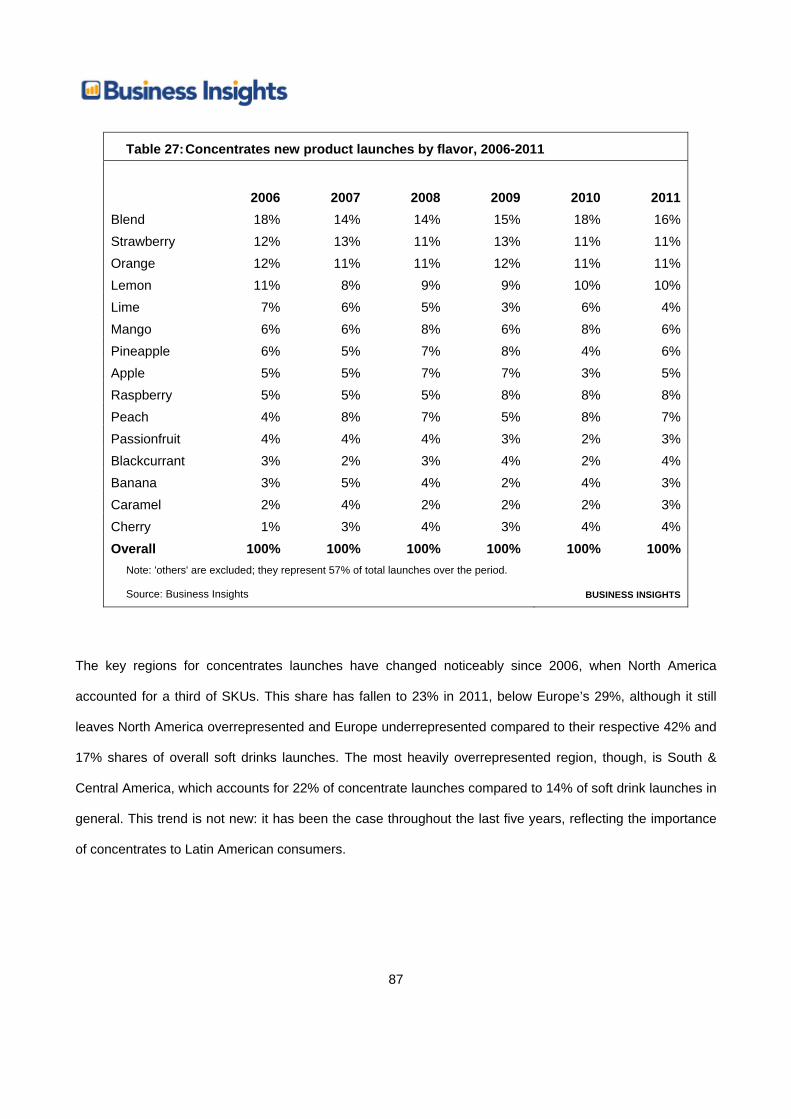

Table 27: Concentrates new product launches by flavor, 2006-2011 87

Table 28: Functional drinks new product launches by product claim, 2006-2011 90

Table 29: Functional drinks new product launches by flavor, 2006-2011 93

Table 30: Juices new product launches by product claim, 2006-2011 95

Table 31: Juices new product launches by flavor, 2006-2011 97

Table 32: RTD tea & coffee new product launches by product claim, 2006-2011 100

Table 33: RTD tea & coffee new product launches by flavor, 2006-2011 102

11

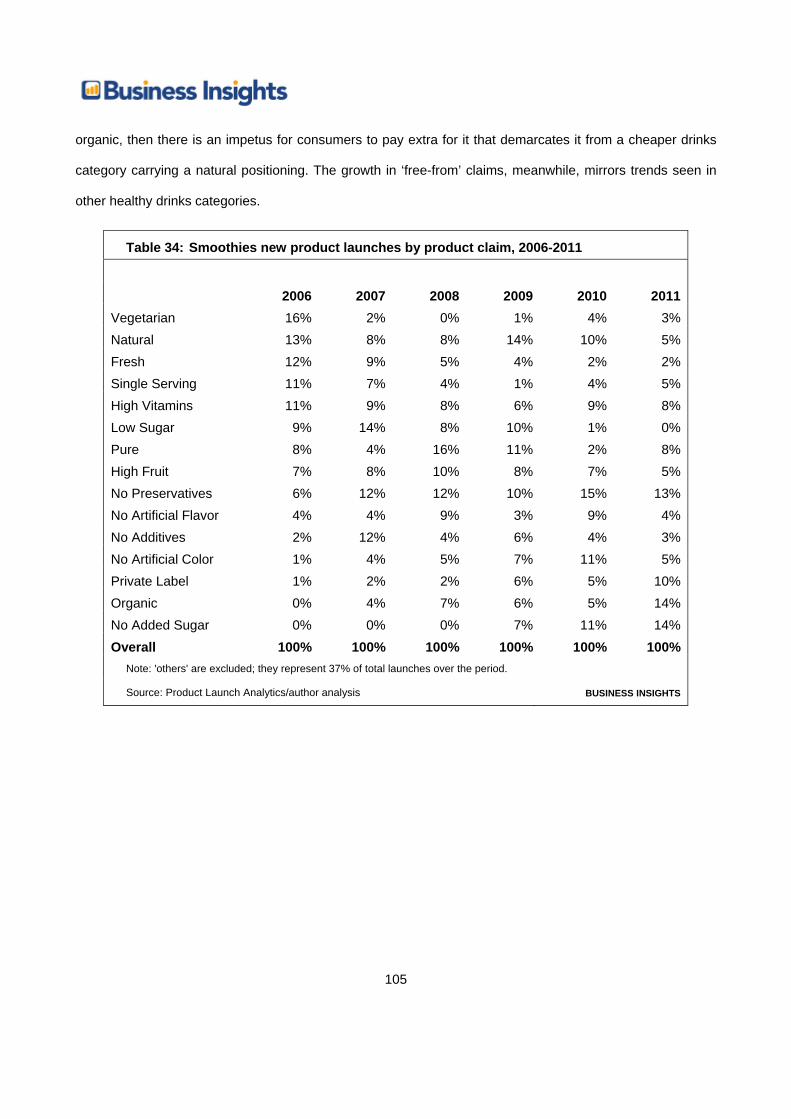

Table 34: Smoothies new product launches by product claim, 2006-2011 105

Table 35: Smoothies new product launches by flavor, 2006-2011 107

Table 36: Bottled water definitions 142

Table 37: Carbonates definitions 142

Table 38: Concentrates definitions 143

Table 39: Functional drinks definitions 143

Table 40: Juices definitions 144

Table 41: RTD tea & coffee definitions 144

Table 42: Smoothies definitions 145

12

Executive summary

Growth opportunities in soft drinks Total global retail soft drinks sales were $504bn in 2010, having risen from $435bn in 2005 at a

compound annual growth rate (CAGR) of 3.0%. The largest category at $191bn was carbonates, with

bottled water second at $99bn and juices third at $84bn.

The fastest growing category from 2010-2015 will be functional drinks, which will grow at 5.0% per year

to reach $61bn. Bottled water will grow at 4.8% driving the total market to $125bn, while concentrates

will be the third-fastest-growing category at 3.3%.

Europe is the largest soft drinks region worldwide, with sales of $188bn (37% of total) worldwide in

2010, followed by North America with sales of $132bn (26%) and Asia-Pacific with $111bn (22%).

The Asia-Pacific market will overtake North America by 2015, with 5.3% annual growth versus 0.4%

annual growth driving Asia-Pacific to $144bn, while North America reaches $135bn. The fastest-

growing market will be South & Central America, with 5.7% annual growth. Europe will remain the

largest market, growing at 2.4% a year to reach $212bn.

Despite the wide disparities in income between different regions, there is surprisingly little variation in

price across regions. In terms of price growth, Asia-Pacific and Africa & Middle East are expected to

modest average price rises in the 2010-2015 period; in North America, average prices will rise just over

1%, while in South & Central America, prices will rise at 0.8%.

The only category that is predicted to see a significant fall in average price per liter between 2010 and

2015 is RTD tea & coffee, with all other categories either showing a flat price or flat growth, compared

to four categories (RTD tea & coffee, carbonates, concentrates and juices) in which average prices fell

in 2005-2010.

13

Innovation and new product development In order to understand and target the most important innovation niches within the soft drinks category, it

is important to have a detailed comprehension of current key innovations: both in the regions and

markets that you are targeting; and innovations from other areas.

Juices have been by far the most important category for NPD innovations within the soft drinks industry

in recent years, making up 31% of new launches despite accounting for a small proportion of total sales

and not being a particularly high growth category in terms of market value or volume.

Concentrates are now the second most important area for soft drinks development, despite their

relatively unfashionable image and relatively low share in many markets, due not least to the strong

position of powder concentrates in fast-growing emerging markets and associated strong levels of

research investment.

‘Upscale’ has fallen from 7% of soft drink product claims to 1% since 2008, while ‘single-serve’ has

fallen from 10% to 6%; on the other hand, private label applied to 2% of launches in 2006 but now

applies to 11%. This is likely driven by consumer reactions to the financial situation.

Positive health claims on soft drink launches have fallen from 19% in 2006 to 16% in 2011; natural,

fresh & organic have risen from 23% to 26%, and free-from claims have risen from 33% to 38%.

Europe has been the most important region for soft drinks launches throughout the 2006-2011 period,

with its share of launches rising to 42% in 2011. The second-placed region is Asia-Pacific, with 24%

share in 2011, and North America is in third position with 17%.

Most ‘innovative’ products tracked are innovative in formulation, accounting for 68% of innovations in

2006 and 79% in 2011. Packaging and positioning are the two other areas in which significant

quantities of innovative products have been tracked, although innovative packaging fell to just 4% in

2011 from 18% in 2006.

14

Consumer trends driving innovation The recessionary behaviors that consumers exhibited in 2009-10 during what appeared to be a

temporary downturn now appear likely to continue to impact on the drinks industry up to the 2015

horizon of this report. The growth in product launches of private label brands, and the decline in

upscale product positioning, are directly related to the global economic situation.

Mass customization, defined as the supply of custom goods in high volumes and at low cost, is a good

way of enhancing brand-consumer relationships, heading off the private label threat, adding greater

perceived value and allowing drinks companies to engage with their consumers more effectively.

Many of the principles required to prosper in recessionary economies can also be applied to staying

ahead in emerging economies. However, although incomes are low, the trend away from conspicuous

consumption is not something that links recessionary and emerging economies.

Although the boom in dedicated functional drinks that characterized the 2000s is no longer such a

major force in the soft drinks market, with over 65s expected to outnumber five to 14 year olds for the

first time in the US by 2014, aging baby boomers with a continued desire to remain young and active,

will be crucial drivers of preventative medicine including healthy drinks.

Several key consumer trends continue to drive interest in sustainable drinks: the importance of health,

as people seek to consume food that is produced non-intensively; media attention as publicity over

climate change and food sustainability drives awareness; the growth of natural & fresh product claims;

the desire to trade up for small indulgences; consumer ethics; and concerns over carbon footprint.

Convenience remains as important to consumers’ lives as it was before the world environment

changed. People who are employed continue to work long hours with long commutes at the beginning

and end; the pressure on working parents remains as strong as ever; and the need – whether real or

imagined – to fit as many hours as possible into the day remains.

15

The future of innovations in soft drinks Low or no growth in most western economies is a given for the next three years and quite possibly

longer; and even when western markets recover, their growth rates will still look stagnant compared to

the rest of the world.

In the short term, rising Chinese consumer spending creates opportunities in the beverage sector, but

in the long run it is likely to lead to Chinese drinks companies that represent serious competition to

existing market players, not just in China but worldwide.

It has become conventional wisdom that major, mass-market drinks are likely to break down, with

consumers no longer displaying the kind of brand loyalty that they once did. This is particularly often

cited for younger consumers, but does not tell the whole story: rather, consumers dip into a portfolio of

brands based on their specific needs at the time.

In the B2C media industry, personalization and disintermediation have become the most important

trends facing the market. It is likely that a similar approach will ultimately reach the drinks industry, as it

gradually becomes more of a technically feasible achievement rather than a pipedream

Functional drinks will be an important way for aging consumers in west and east alike to consume

medications. As the regulatory regime matures, it will be increasingly common for functional ingredients

to be delivered in drinks format, possibly combined with the personalization trend to the point where

people can consume drinks that are directly personalized to their lifestyle needs.

Within the next 10-20 years, drinks packaging will end up becoming 100% recycled and recyclable, and

that this will be accepted by consumers and by the industry as a matter of course.

Packaging will evolve to incorporate new technologies – most notably nanotechnology, but also

advances in cheap electronics, in ergonomics, and in materials science. The main impact of new

packaging technology will be to add functionality to the consumer’s drinking experience.

16

Chapter 1 Introduction

Introduction The soft drinks industry is a large, fast-growing and yet also rapidly maturing industry. In developed-world

markets, traditional categories such as carbonates are stagnating, while the trend of upselling consumers to

premium categories such as energy drinks and smoothies that thrived during the 2000s has been impacted

by recession and discretionary consumer spending cuts in many developed economies. The provision of

novel, value-added but lower-cost innovations has become a key way to win consumer loyalty in these tough

markets. Meanwhile, as per capita consumption levels in mid-income markets rise to developed-world levels,

it is becoming increasingly important for marketers in these countries to offer innovative new products rather

than relying in growth on overall consumption.

Market definitions Business Insights defines the soft drinks industry on a globally consistent basis across market data and

product innovation data. It consists of the following categories:

Bottled water

Carbonates

Concentrates

Functional drinks

Juices

RTD tea & coffee

Smoothies

Detailed category and segment level definitions are included in the Appendix.

17

Only off-trade (retail) sales of packaged soft drinks are included; juices and smoothies made to order on the

premises are not included, and bottled water excludes containers above five liters in size. All volume data is

listed in liters; all value data is listed in US$ at real (i.e. excluding the impact of inflation) prices and constant

2010 exchange rates. Innovations data is based on the Product Launch Analytics database, which aims to

capture key launches consistently across all countries and categories.

What this report is about The soft drinks industry is a more challenging environment than ever before, with a renewed focus on value

for money coupled with continued desires among consumers for premium products that meet their health,

indulgence and convenience needs. This report highlights best-practice across all global markets in meeting

this challenge, helping soft drinks manufacturers to target new product development (NPD) budget to the

most effective uses. It is targeted at marketing and brand managers, strategic decision makers and senior

executives, consultants and researcher working for soft drinks manufacturers, distributors, importers,

marketers and retailers, and consultancy and research firms covering the soft drinks industry.

The report is designed to help companies target appropriate categories and geographies as part of a

channeled new product strategy. It highlights worldwide product innovations, providing inspiration and

examples of best-practice; allows manufacturers to shape regional and global NPD strategy; provides an

analysis of the relationship between socioeconomic trends, category trends and product innovation; and

projects global soft drinks market and category growth over the next five years.

Scope of report The report summarizes innovative and novel product launches across the global soft drinks industry between

January 2006 and November 2011, as reported by Business Insights’ in-house Product Launch Analytics

database of new product launches across the FMCG industry. It analyzes market value and volume data

across the soft drinks industry by value and volume, segmented by region and category. In addition to

considering the market on a regional basis, this report also looks at 10 major countries on a detailed in-depth

18

basis. While they are not necessarily the largest in value or volume terms, they are the markets which

combine the strongest potential, the fastest current growth, the highest current sales, and the most important

centers of innovation. Based on this data, the report presents an analysis of the most important innovation,

new product development and growth trends, globally and on a region/category basis. The information

presented allows industry players to identify the most important growth opportunities and trends to target

within the soft drinks industry.

19

Chapter 2 Growth opportunities in soft drinks

Summary Total global retail soft drinks sales were $504bn in 2010, having risen from $435bn in 2005 at a

compound annual growth rate (CAGR) of 3.0%. The largest category at $191bn was carbonates, with

bottled water second at $99bn and juices third at $84bn.

The fastest growing category from 2010-2015 will be functional drinks, which will grow at 5.0% per year

to reach $61bn. Bottled water will grow at 4.8% driving the total market to $125bn, while concentrates

will be the third-fastest-growing category at 3.3%.

Europe is the largest soft drinks region worldwide, with sales of $188bn (37% of total) worldwide in

2010, followed by North America with sales of $132bn (26%) and Asia-Pacific with $111bn (22%).

The Asia-Pacific market will overtake North America by 2015, with 5.3% annual growth versus 0.4%

annual growth driving Asia-Pacific to $144bn, while North America reaches $135bn. The fastest-

growing market will be South & Central America, with 5.7% annual growth. Europe will remain the

largest market, growing at 2.4% a year to reach $212bn.

Despite the wide disparities in income between different regions, there is surprisingly little variation in

price across regions. In terms of price growth, Asia-Pacific and Africa & Middle East are expected to

modest average price rises in the 2010-2015 period; in North America, average prices will rise just over

1%, while in South & Central America, prices will rise at 0.8%.

The only category that is predicted to see a significant fall in average price per liter between 2010 and

2015 is RTD tea & coffee, with all other categories either showing a flat price or flat growth, compared

to four categories (RTD tea & coffee, carbonates, concentrates and juices) in which average prices fell

in 2005-2010.

20

Introduction The global soft drinks market has shown strong growth in recent years in both value and volume terms, and

is expected to carry on doing so between now and 2015. However, there is significant variation between

different categories and different countries, and indeed between different categories within the same country.

While it is fair to generalize that carbonates are performing better in the developing world than in developed

markets, this is only part of the story: there are some developed markets where carbonates are still a growth

story, and some developing markets where they are not particularly favored.

As a result, a detailed overview of key category, regional and country trends in volume, value and pricing

terms is required to understand how best to target innovations in the soft drinks market. To this end, this

chapter first presents an overview of the global soft drinks market, looking at value, volume and pricing

trends on a category-by-category and region-by-region basis. It then presents a detailed breakdown and

analysis of each category globally on the same basis, followed by a breakdown and analysis of the

performance of the soft drinks markets in 10 major economies.

Market overview This report section provides top-level insight into global soft drinks industry trends, highlighting overall market

dynamics on a category and regional basis. It highlights the most important categories in terms of volume,

value and price growth and explains some of the key macro-level drivers that are impacting on these

categories, and then follows the same approach for major regions.

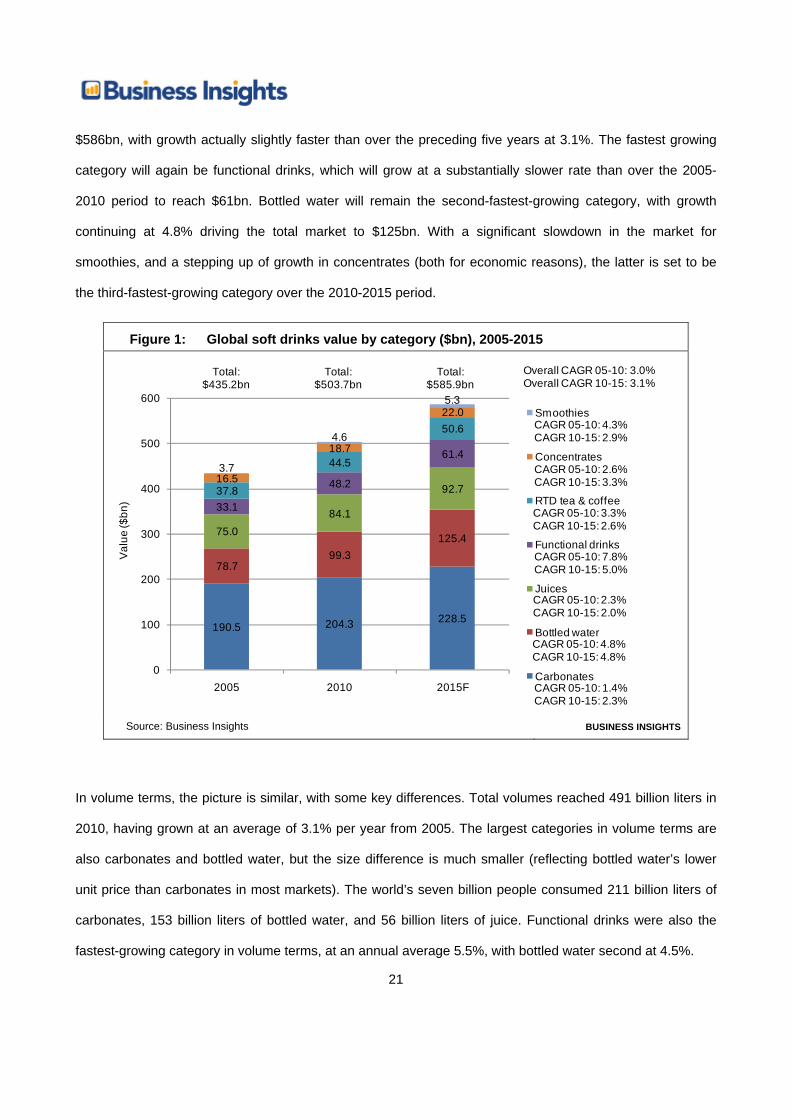

Soft drinks overview by category

Total global retail soft drinks sales were $504bn in 2010, having risen from $435bn in 2005 at a compound

annual growth rate (CAGR) of 3.0%. The largest category at $191bn was carbonates, with bottled water

second at $99bn and juices third at $84bn. The fastest-growing category was functional drinks, having grown

at a global average rate of 7.8%. Bottled water showed the second-fastest growth at 4.8%, and the third-

fastest-growing category was smoothies, which grew at 4.3% to reach a still-minor value of $4.6bn. By 2015,

despite slow economic growth in developed economies, the global market is forecast to reach a value of

21

$586bn, with growth actually slightly faster than over the preceding five years at 3.1%. The fastest growing

category will again be functional drinks, which will grow at a substantially slower rate than over the 2005-

2010 period to reach $61bn. Bottled water will remain the second-fastest-growing category, with growth

continuing at 4.8% driving the total market to $125bn. With a significant slowdown in the market for

smoothies, and a stepping up of growth in concentrates (both for economic reasons), the latter is set to be

the third-fastest-growing category over the 2010-2015 period.

Figure 1: Global soft drinks value by category ($bn), 2005-2015

Total: $435.2bn

Total: $503.7bn

Total: $585.9bn

CAGR 05-10: 4.3%CAGR 10-15: 2.9%

CAGR 05-10: 2.6%CAGR 10-15: 3.3%

CAGR 05-10: 3.3%CAGR 10-15: 2.6%

CAGR 05-10: 7.8%CAGR 10-15: 5.0%

CAGR 05-10: 2.3%CAGR 10-15: 2.0%

CAGR 05-10: 4.8%CAGR 10-15: 4.8%

CAGR 05-10: 1.4%CAGR 10-15: 2.3%

Val

ue ($

bn)

Overall CAGR 05-10: 3.0%Overall CAGR 10-15: 3.1%

190.5 204.3 228.5

78.799.3

125.475.084.1

92.733.1

48.2

61.4

37.8

44.5

50.6

16.5

18.7

22.0

3.7

4.6

5.3

0

100

200

300

400

500

600

2005 2010 2015F

Smoothies

Concentrates

RTD tea & coffee

Functional drinks

Juices

Bottled water

Carbonates

Source: Business Insights BUSINESS INSIGHTS

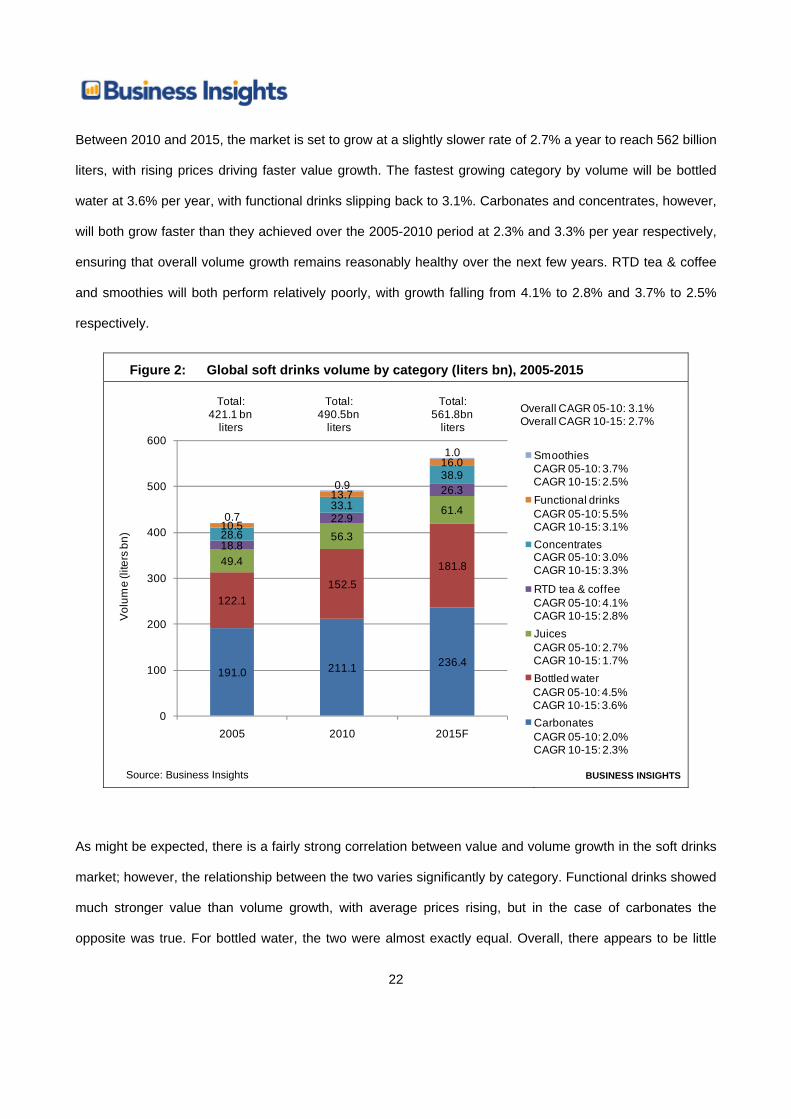

In volume terms, the picture is similar, with some key differences. Total volumes reached 491 billion liters in

2010, having grown at an average of 3.1% per year from 2005. The largest categories in volume terms are

also carbonates and bottled water, but the size difference is much smaller (reflecting bottled water’s lower

unit price than carbonates in most markets). The world’s seven billion people consumed 211 billion liters of

carbonates, 153 billion liters of bottled water, and 56 billion liters of juice. Functional drinks were also the

fastest-growing category in volume terms, at an annual average 5.5%, with bottled water second at 4.5%.

22

Between 2010 and 2015, the market is set to grow at a slightly slower rate of 2.7% a year to reach 562 billion

liters, with rising prices driving faster value growth. The fastest growing category by volume will be bottled

water at 3.6% per year, with functional drinks slipping back to 3.1%. Carbonates and concentrates, however,

will both grow faster than they achieved over the 2005-2010 period at 2.3% and 3.3% per year respectively,

ensuring that overall volume growth remains reasonably healthy over the next few years. RTD tea & coffee

and smoothies will both perform relatively poorly, with growth falling from 4.1% to 2.8% and 3.7% to 2.5%

respectively.

Figure 2: Global soft drinks volume by category (liters bn), 2005-2015

Total: 421.1 bn

liters

Total: 490.5bn

liters

Total: 561.8bn

liters

CAGR 05-10: 3.7%CAGR 10-15: 2.5%

CAGR 05-10: 5.5%CAGR 10-15: 3.1%

CAGR 05-10: 3.0%CAGR 10-15: 3.3%

CAGR 05-10: 4.1%CAGR 10-15: 2.8%

CAGR 05-10: 2.7%CAGR 10-15: 1.7%

CAGR 05-10: 4.5%CAGR 10-15: 3.6%

CAGR 05-10: 2.0%CAGR 10-15: 2.3%

Volu

me

(lite

rsbn

)

Overall CAGR 05-10: 3.1%Overall CAGR 10-15: 2.7%

191.0 211.1 236.4

122.1152.5

181.849.4

56.3

61.4

18.8

22.9

26.3

28.6

33.1

38.9

10.5

13.7

16.0

0.7

0.9

1.0

0

100

200

300

400

500

600

2005 2010 2015F

Smoothies

Functional drinks

Concentrates

RTD tea & coffee

Juices

Bottled water

Carbonates

Source: Business Insights BUSINESS INSIGHTS

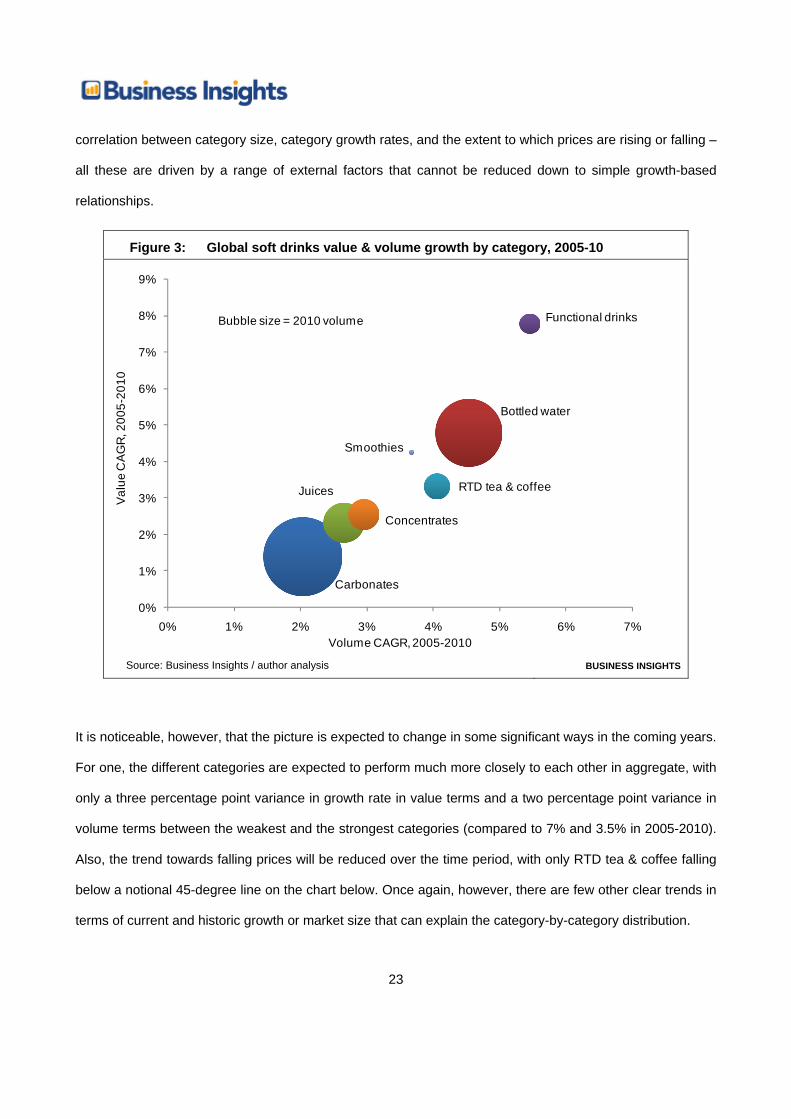

As might be expected, there is a fairly strong correlation between value and volume growth in the soft drinks

market; however, the relationship between the two varies significantly by category. Functional drinks showed

much stronger value than volume growth, with average prices rising, but in the case of carbonates the

opposite was true. For bottled water, the two were almost exactly equal. Overall, there appears to be little

23

correlation between category size, category growth rates, and the extent to which prices are rising or falling –

all these are driven by a range of external factors that cannot be reduced down to simple growth-based

relationships.

Figure 3: Global soft drinks value & volume growth by category, 2005-10

Carbonates

Bottled water

Juices

Functional drinks

RTD tea & coffee

Concentrates

Smoothies

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0% 1% 2% 3% 4% 5% 6% 7%

Val

ue C

AG

R, 2

005-

2010

Volume CAGR, 2005-2010

Bubble size = 2010 volume

Source: Business Insights / author analysis BUSINESS INSIGHTS

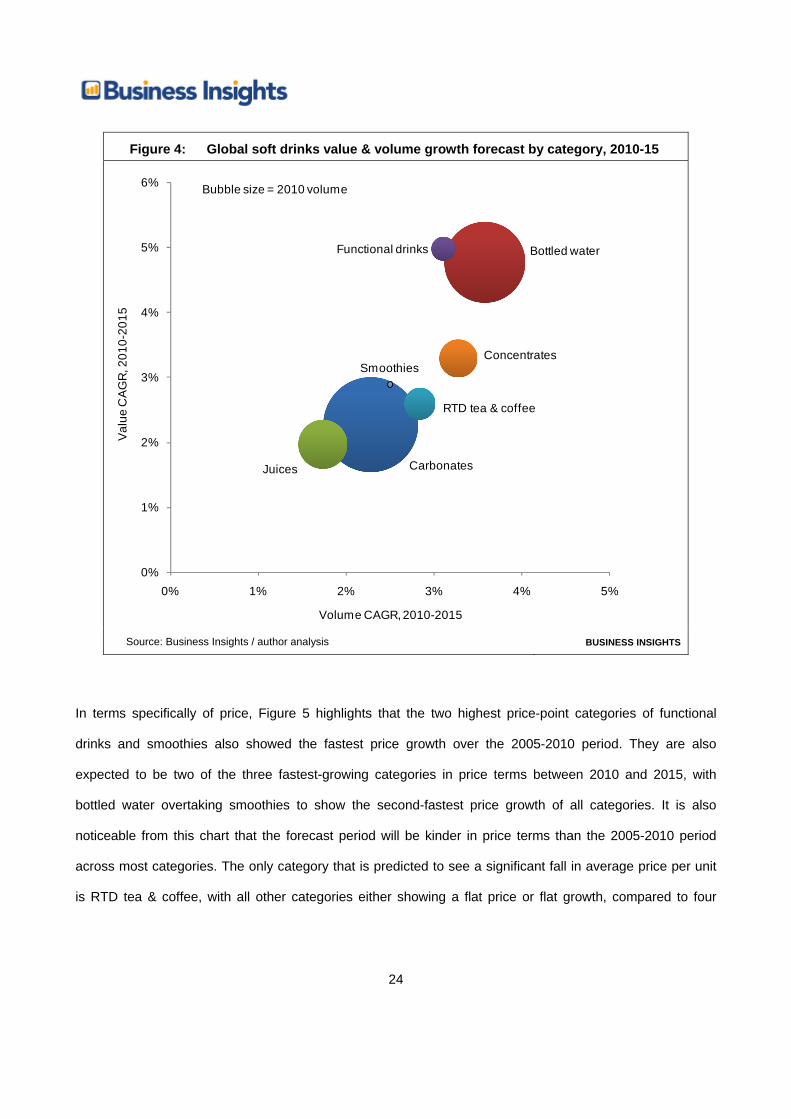

It is noticeable, however, that the picture is expected to change in some significant ways in the coming years.

For one, the different categories are expected to perform much more closely to each other in aggregate, with

only a three percentage point variance in growth rate in value terms and a two percentage point variance in

volume terms between the weakest and the strongest categories (compared to 7% and 3.5% in 2005-2010).

Also, the trend towards falling prices will be reduced over the time period, with only RTD tea & coffee falling

below a notional 45-degree line on the chart below. Once again, however, there are few other clear trends in

terms of current and historic growth or market size that can explain the category-by-category distribution.

24

Figure 4: Global soft drinks value & volume growth forecast by category, 2010-15

Carbonates

Bottled water

Juices

Functional drinks

RTD tea & coffee

ConcentratesSmoothies

0%

1%

2%

3%

4%

5%

6%

0% 1% 2% 3% 4% 5%

Val

ue C

AG

R, 2

010-

2015

Volume CAGR, 2010-2015

Bubble size = 2010 volume

Source: Business Insights / author analysis BUSINESS INSIGHTS

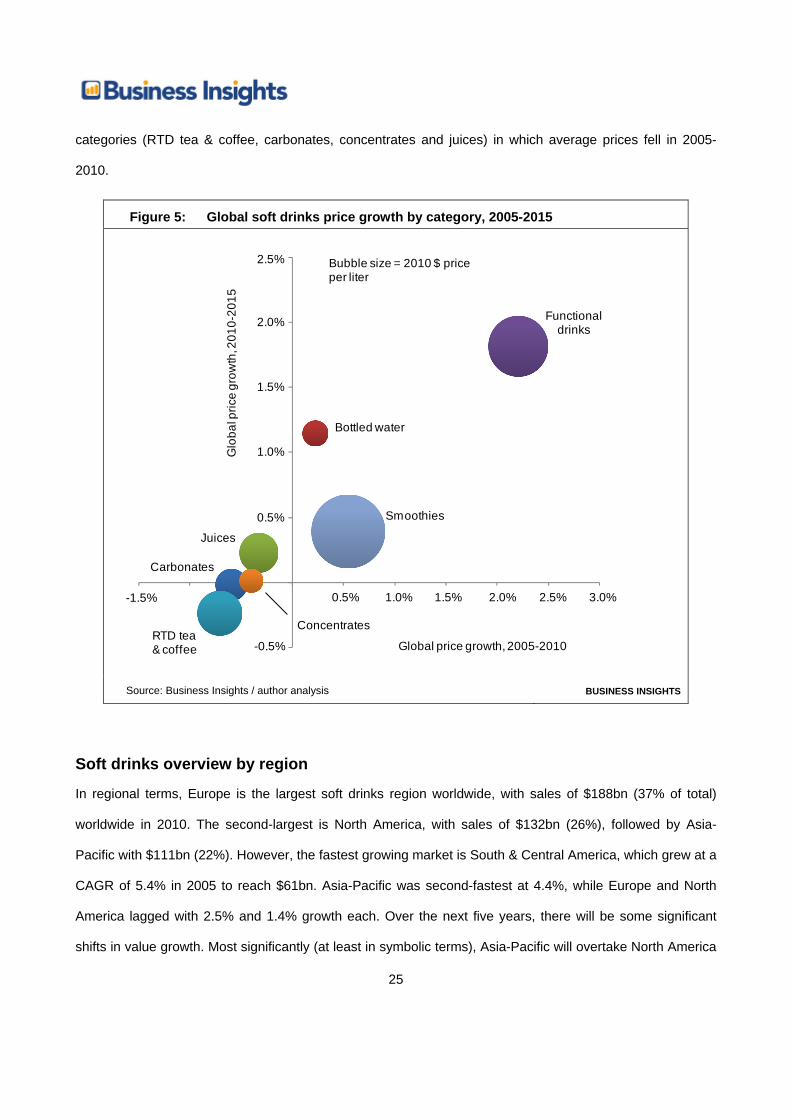

In terms specifically of price, Figure 5 highlights that the two highest price-point categories of functional

drinks and smoothies also showed the fastest price growth over the 2005-2010 period. They are also

expected to be two of the three fastest-growing categories in price terms between 2010 and 2015, with

bottled water overtaking smoothies to show the second-fastest price growth of all categories. It is also

noticeable from this chart that the forecast period will be kinder in price terms than the 2005-2010 period

across most categories. The only category that is predicted to see a significant fall in average price per unit

is RTD tea & coffee, with all other categories either showing a flat price or flat growth, compared to four

25

categories (RTD tea & coffee, carbonates, concentrates and juices) in which average prices fell in 2005-

2010.

Figure 5: Global soft drinks price growth by category, 2005-2015

Carbonates

Bottled water

Juices

Functional drinks

RTD tea & coffee

Concentrates

Smoothies

Glo

bal p

rice

grow

th, 2

010-

2015

Global price growth, 2005-2010

-1.5% 1.0% 1.5% 2.0% 2.5%0.5% 3.0%

1.0%

1.5%

2.0%

2.5%

0.5%

-0.5%

Bubble size = 2010 $ price per liter

Source: Business Insights / author analysis BUSINESS INSIGHTS

Soft drinks overview by region

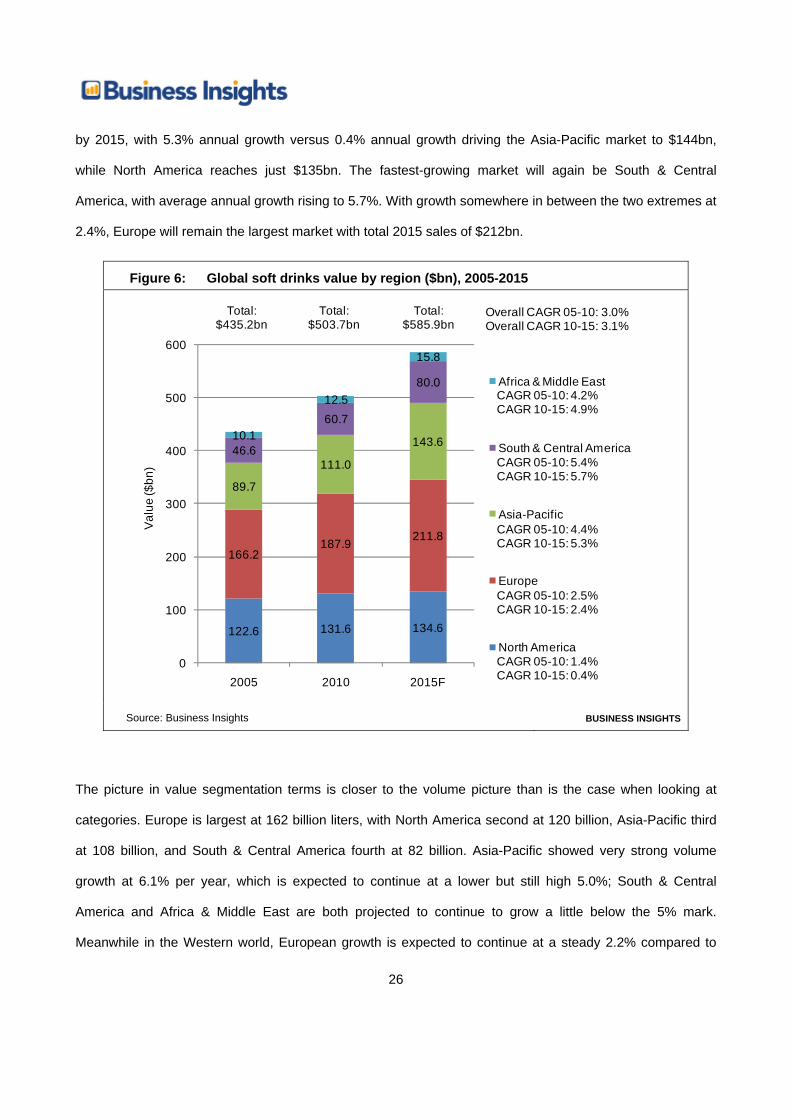

In regional terms, Europe is the largest soft drinks region worldwide, with sales of $188bn (37% of total)

worldwide in 2010. The second-largest is North America, with sales of $132bn (26%), followed by Asia-

Pacific with $111bn (22%). However, the fastest growing market is South & Central America, which grew at a

CAGR of 5.4% in 2005 to reach $61bn. Asia-Pacific was second-fastest at 4.4%, while Europe and North

America lagged with 2.5% and 1.4% growth each. Over the next five years, there will be some significant

shifts in value growth. Most significantly (at least in symbolic terms), Asia-Pacific will overtake North America

26

by 2015, with 5.3% annual growth versus 0.4% annual growth driving the Asia-Pacific market to $144bn,

while North America reaches just $135bn. The fastest-growing market will again be South & Central

America, with average annual growth rising to 5.7%. With growth somewhere in between the two extremes at

2.4%, Europe will remain the largest market with total 2015 sales of $212bn.

Figure 6: Global soft drinks value by region ($bn), 2005-2015

Total: $435.2bn

Total: $503.7bn

Total: $585.9bn

CAGR 05-10: 4.2%CAGR 10-15: 4.9%

CAGR 05-10: 5.4%CAGR 10-15: 5.7%

CAGR 05-10: 4.4%CAGR 10-15: 5.3%

CAGR 05-10: 2.5%CAGR 10-15: 2.4%

CAGR 05-10: 1.4%CAGR 10-15: 0.4%

Val

ue ($

bn)

Overall CAGR 05-10: 3.0%Overall CAGR 10-15: 3.1%

122.6 131.6 134.6

166.2187.9 211.8

89.7

111.0

143.646.6

60.7

80.0

10.1

12.5

15.8

0

100

200

300

400

500

600

2005 2010 2015F

Africa & Middle East

South & Central America

Asia-Pacific

Europe

North America

Source: Business Insights BUSINESS INSIGHTS

The picture in value segmentation terms is closer to the volume picture than is the case when looking at

categories. Europe is largest at 162 billion liters, with North America second at 120 billion, Asia-Pacific third

at 108 billion, and South & Central America fourth at 82 billion. Asia-Pacific showed very strong volume

growth at 6.1% per year, which is expected to continue at a lower but still high 5.0%; South & Central

America and Africa & Middle East are both projected to continue to grow a little below the 5% mark.

Meanwhile in the Western world, European growth is expected to continue at a steady 2.2% compared to

27

2.4% over the previous period. However, North America is expected to go from slow volume growth of 0.4%

to a 0.6% decline in total sales over the same period. As in values, Asia-Pacific will overtake North America

over the time period – but when considered in volume terms, Latin America is also starting to catch up with

its neighbor.

Figure 7: Global soft drinks volume by region (liters bn), 2005-2015

Total: 421.1 bn

liters

Total: 490.5bn

liters

Total: 561.8bn

liters

Vol

ume

(lite

rsbn

)

Overall CAGR 05-10: 3.1%Overall CAGR 10-15: 2.7%

CAGR 05-10: 4.9%CAGR 10-15: 4.6%

CAGR 05-10: 5.0%CAGR 10-15: 4.8%

CAGR 05-10: 6.1%CAGR 10-15: 5.0%

CAGR 05-10: 2.4%CAGR 10-15: 2.2%

CAGR 05-10: 0.4%CAGR 10-15: -0.6%

118.0 120.1 116.8

144.4 162.4 180.9

80.0107.7

137.664.4

82.1

103.6

14.3

18.2

22.8

0

100

200

300

400

500

600

2005 2010 2015F

Africa & Middle East

South & Central America

Asia-Pacific

Europe

North America

Source: Business Insights BUSINESS INSIGHTS

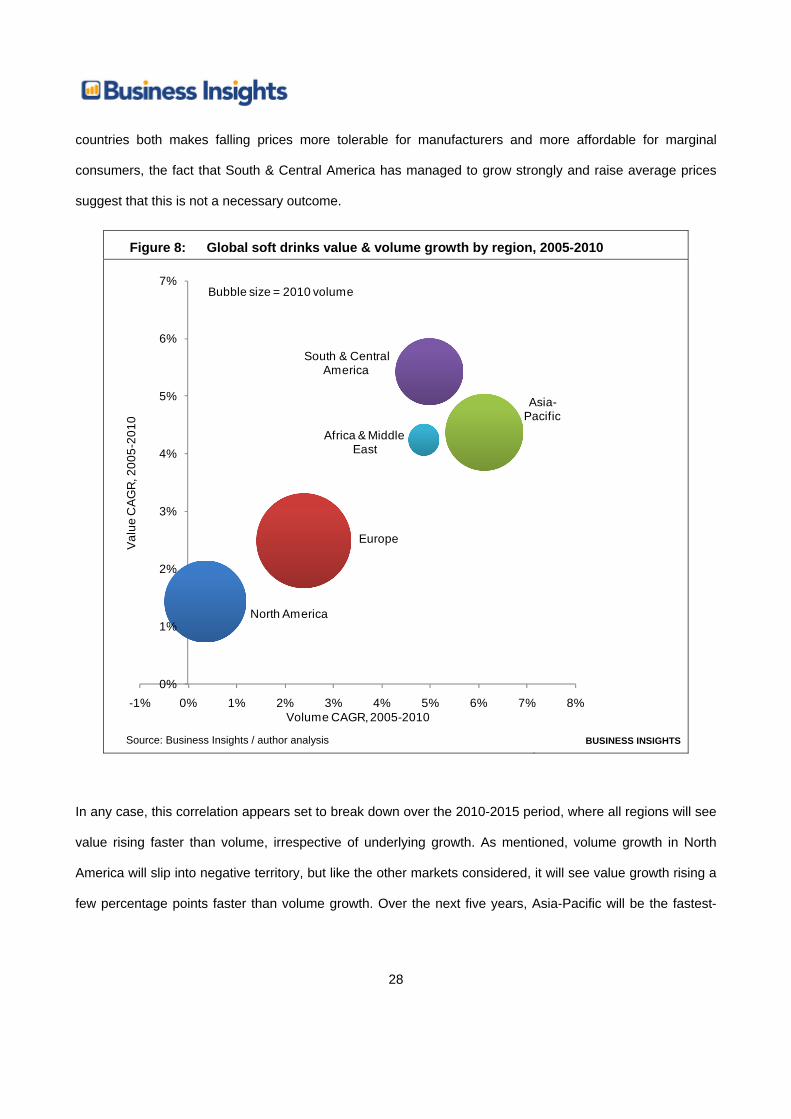

There is a slightly closer relationship between growth rates and the relationship between value and volume

growth when considering the soft drinks market on a regional basis. The slower-growing markets of Europe

and the US saw prices rise faster than volumes in the 2005-2010 period, while the faster-growing Asia-

Pacific and Africa & Middle East markets saw the opposite. However, this correlation does not apply to the

significant South & Central America market, where value growth outstripped volume growth despite the fact

that both were strong. Overall, while it is feasible to assume that strong volume growth in developing

28

countries both makes falling prices more tolerable for manufacturers and more affordable for marginal

consumers, the fact that South & Central America has managed to grow strongly and raise average prices

suggest that this is not a necessary outcome.

Figure 8: Global soft drinks value & volume growth by region, 2005-2010

North America

Europe

Asia-Pacific

South & Central America

Africa & Middle East

0%

1%

2%

3%

4%

5%

6%

7%

-1% 0% 1% 2% 3% 4% 5% 6% 7% 8%

Val

ue C

AG

R, 2

005-

2010

Volume CAGR, 2005-2010

Bubble size = 2010 volume

Source: Business Insights / author analysis BUSINESS INSIGHTS

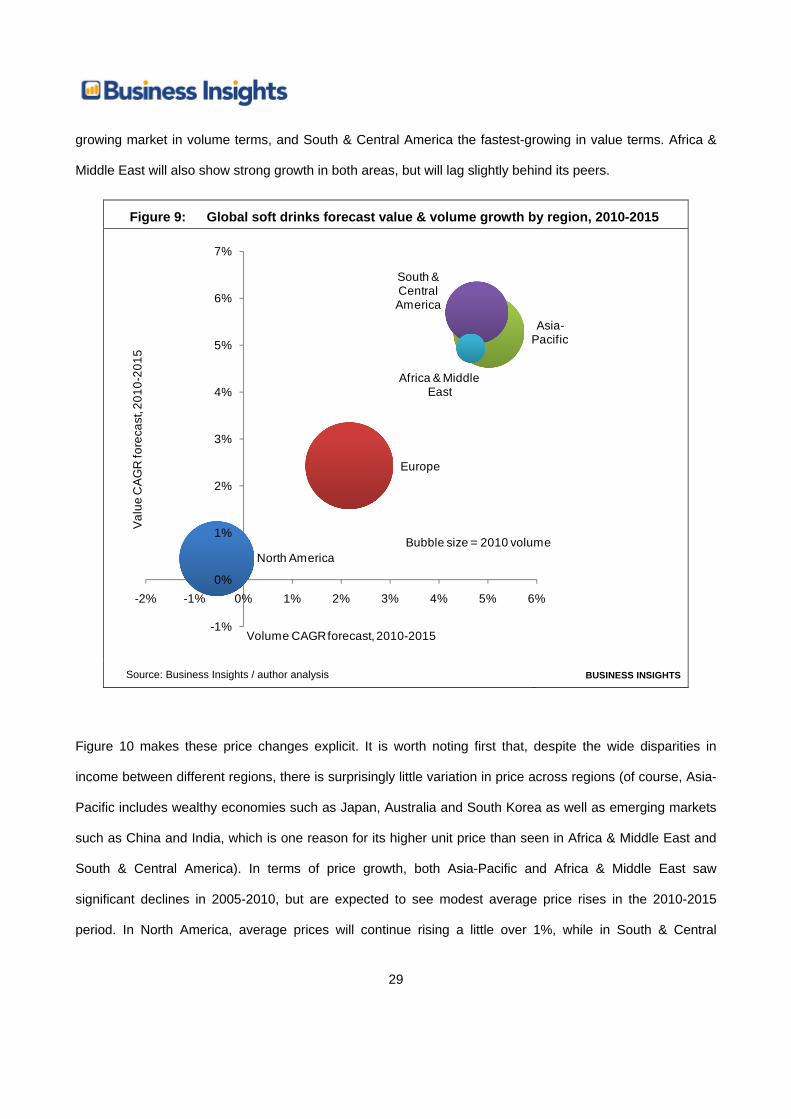

In any case, this correlation appears set to break down over the 2010-2015 period, where all regions will see

value rising faster than volume, irrespective of underlying growth. As mentioned, volume growth in North

America will slip into negative territory, but like the other markets considered, it will see value growth rising a

few percentage points faster than volume growth. Over the next five years, Asia-Pacific will be the fastest-

29

growing market in volume terms, and South & Central America the fastest-growing in value terms. Africa &

Middle East will also show strong growth in both areas, but will lag slightly behind its peers.

Figure 9: Global soft drinks forecast value & volume growth by region, 2010-2015

North America

Europe

Asia-Pacific

South & Central America

Africa & Middle East

-1%

0%

1%

2%

3%

4%

5%

6%

7%

-2% -1% 0% 1% 2% 3% 4% 5% 6%

Val

ue C

AG

R fo

reca

st, 2

010-

2015

Volume CAGR forecast, 2010-2015

Bubble size = 2010 volume

Source: Business Insights / author analysis BUSINESS INSIGHTS

Figure 10 makes these price changes explicit. It is worth noting first that, despite the wide disparities in

income between different regions, there is surprisingly little variation in price across regions (of course, Asia-

Pacific includes wealthy economies such as Japan, Australia and South Korea as well as emerging markets

such as China and India, which is one reason for its higher unit price than seen in Africa & Middle East and

South & Central America). In terms of price growth, both Asia-Pacific and Africa & Middle East saw

significant declines in 2005-2010, but are expected to see modest average price rises in the 2010-2015

period. In North America, average prices will continue rising a little over 1%, while in South & Central

30

America, average soft drinks prices are expected to rise at over 0.8% compared with under 0.5% in the

2005-2010 period. In all cases, these price rises will be driven by premiumization and resource scarcity.

Figure 10: Global soft drinks price growth by region, 2005-2015

North America

Europe

Asia-Pacific

South & Central America

Africa & Middle East

0.0%

0.5%

1.0%

1.5%

-2% -1% 0% 1% 2%

Wei

ghte

d gl

obal

pric

e gr

owth

, 201

0-20

15

Weighted global price growth, 2005-2010

Bubble size = 2010 $ price per liter

Source: Business Insights / author analysis BUSINESS INSIGHTS

Category breakdown It is now worth examining the key categories in the soft drinks market on an individual basis, to provide a

more detailed profile, to clarify what is included and key market dynamics.

Bottled water

Bottled water has shown strong value growth worldwide in recent years, with sales rising at an average

annual rate of 4.8% over the 2005-2010 period to reach $99bn worldwide. It is the second-largest soft drinks

category by both value and volume, behind carbonates on both fronts. The largest single category,

31

accounting for two thirds of sales by value and three quarters of sales by volume, is unflavored still water.

Perhaps surprisingly, this has also been the fastest-growing category in value terms: although developed

market consumers are shifting toward flavored varieties to some extent, this trend has been far outweighed

by the shift from unreliable water supplies in the developing world as incomes and health consciousness rise.

Table 1: Global bottled water market by category, 2005-2015

Value ($bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15Still unflavored 50 65 84 5.1% 5.4%Sparkling unflavored 23 28 34 4.4% 3.7%Sparkling flavored 4 4 5 3.0% 3.0%Still flavored 2 2 3 4.4% 4.7%Overall 79 99 125 4.8% 4.8% Volume (liters bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15Still unflavored 90 113 137 4.8% 3.9%Sparkling unflavored 26 32 36 3.7% 2.5%Sparkling flavored 4 4 5 4.1% 3.6%Still flavored 2 3 3 5.2% 3.8%Overall 122 152 182 4.5% 3.6% Price ($/liter) 2005 2010 2015 CAGR 05-10 CAGR 10-15Still unflavored 0.56 0.57 0.61 0.3% 1.4%Sparkling unflavored 0.85 0.88 0.94 0.7% 1.2%Sparkling flavored 1.06 1.01 0.98 -1.1% -0.6%Still flavored 0.84 0.80 0.84 -0.8% 0.9%Average 0.64 0.65 0.69 0.2% 1.1%

Source: Business Insights BUSINESS INSIGHTS

In volume terms, 152 billion liters of bottled water were consumed in 2010. Still flavored water volume growth

has slightly outpaced unflavored water, with both types outpacing sparkling waters. The global average price

of bottled water is 65 cents a liter, with unflavored water by far the cheapest category, at 57 cents. However,

flavored categories have become cheaper over the last five years as their status has become increasingly

32

mainstream. Prices are expected to show stronger growth over the 2010-2015 period than between 2005-

2010, as markets such as Brazil and China mature to the extent that price rises can be implemented.

Carbonates

Carbonates is the largest soft drinks category in both value and volume terms, with 211 billion liters

consumed and total sales of $204 billion in 2010. Although growth was relatively slow from 2005-2010, it is

expected to rise to 2.3% in value and volume terms from 2010-2015. Cola drinks account for 57%, with a 74-

26 split between regular and diet colas in value terms, although this gap has been narrowing over time. Most

of the rest of the market is made up of fruit-flavored drinks. In volume terms, the category share picture is

similar, but growth trends are reversed between diet and standard colas, and diet colas have a smaller

share. This reflects the fact that diet colas are primarily consumed in developed markets where consumers

are concerned with health issues and are more calorie-conscious, whereas the major growth markets for

carbonates are emerging markets where consumers are (at least for the time being) still actively seeking

energy. These trends are reflected in pricing data. Across most categories, and on average, prices fell in real

terms from 2005-2010, reflecting the shift in consumption from developed to developing markets. Diet cola is

an exception, with prices remaining static in real terms. The trend of falling prices is expected to reverse to a

small extent over the 2010-2015 period.

33

Table 2: Global carbonates market by category, 2005-2015

Value ($ bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15Cola - standard 82 86 95 1.0% 2.1%Fruit-flavored carbonates 55 60 68 1.7% 2.7%Cola - diet 28 30 32 1.3% 1.4%Other carbonates 14 16 18 2.1% 2.6%Mixers 11 13 15 2.9% 3.2%Overall 190 204 228 1.4% 2.3% Volume (liters bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15Cola – standard 84 91 102 1.7% 2.3%Fruit-flavored carbonates 55 61 69 2.3% 2.4%Cola - diet 25 27 29 1.3% 1.1%Other carbonates 16 19 22 3.5% 3.5%Mixers 11 13 14 2.7% 2.7%Overall 191 211 236 2.0% 2.3% Price ($/liter) 2005 2010 2015 CAGR 05-10 CAGR 10-15Cola - standard 0.97 0.94 0.93 -0.7% -0.2%Fruit-flavored carbonates 1.01 0.97 0.99 -0.7% 0.3%Cola - diet 1.11 1.11 1.13 0.0% 0.4%Other carbonates 0.91 0.84 0.81 -1.4% -0.9%Mixers 1.03 1.04 1.07 0.2% 0.5%Average 1.00 0.97 0.97 -0.6% 0.0%

Source: Business Insights BUSINESS INSIGHTS

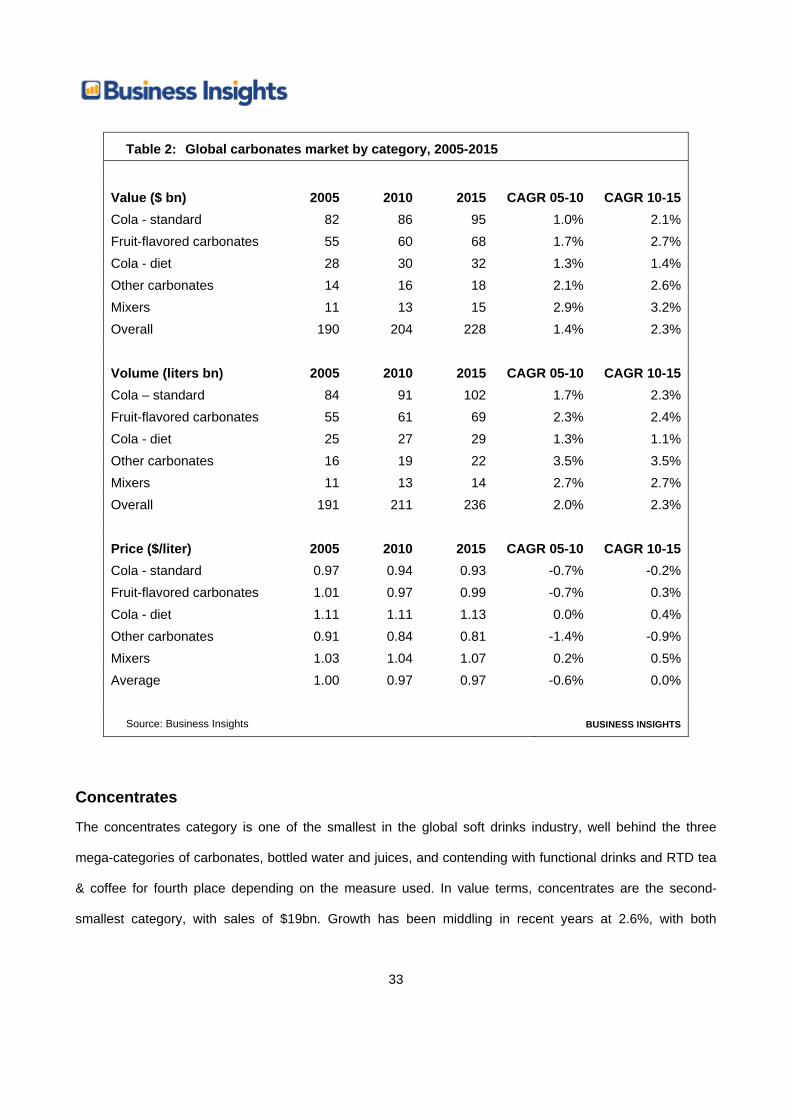

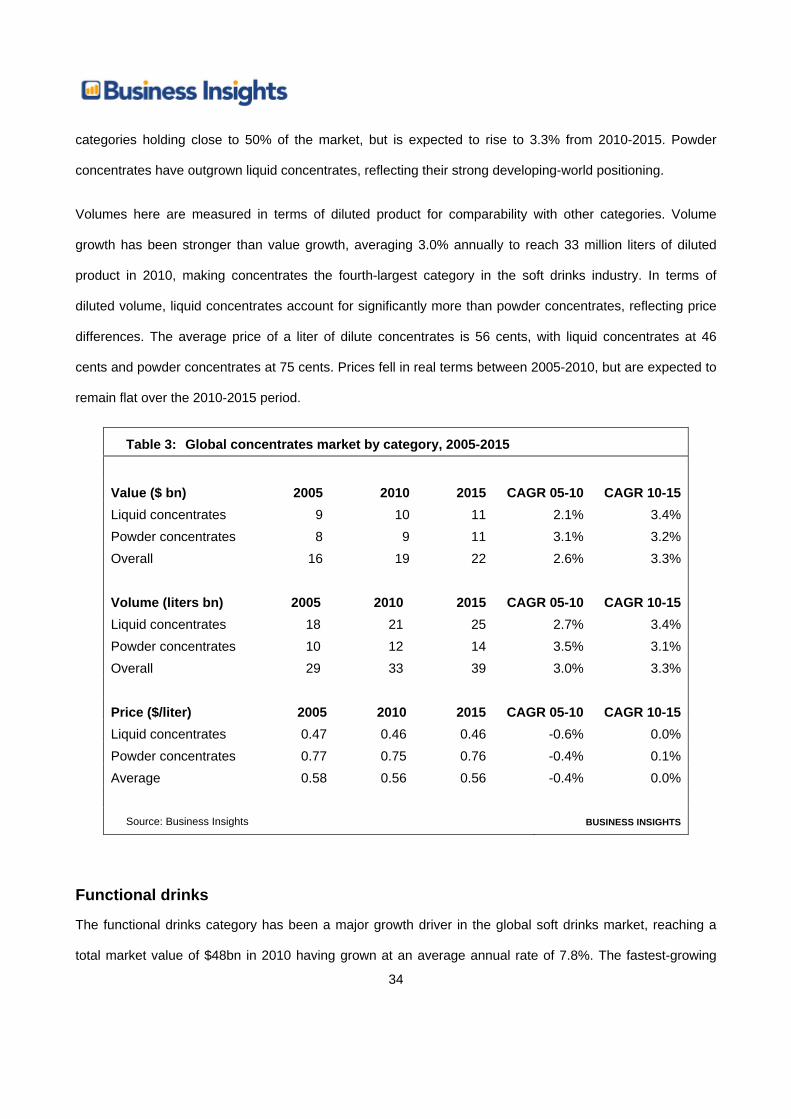

Concentrates

The concentrates category is one of the smallest in the global soft drinks industry, well behind the three

mega-categories of carbonates, bottled water and juices, and contending with functional drinks and RTD tea

& coffee for fourth place depending on the measure used. In value terms, concentrates are the second-

smallest category, with sales of $19bn. Growth has been middling in recent years at 2.6%, with both

34

categories holding close to 50% of the market, but is expected to rise to 3.3% from 2010-2015. Powder

concentrates have outgrown liquid concentrates, reflecting their strong developing-world positioning.

Volumes here are measured in terms of diluted product for comparability with other categories. Volume

growth has been stronger than value growth, averaging 3.0% annually to reach 33 million liters of diluted

product in 2010, making concentrates the fourth-largest category in the soft drinks industry. In terms of

diluted volume, liquid concentrates account for significantly more than powder concentrates, reflecting price

differences. The average price of a liter of dilute concentrates is 56 cents, with liquid concentrates at 46

cents and powder concentrates at 75 cents. Prices fell in real terms between 2005-2010, but are expected to

remain flat over the 2010-2015 period.

Table 3: Global concentrates market by category, 2005-2015

Value ($ bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15Liquid concentrates 9 10 11 2.1% 3.4%Powder concentrates 8 9 11 3.1% 3.2%Overall 16 19 22 2.6% 3.3% Volume (liters bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15Liquid concentrates 18 21 25 2.7% 3.4%Powder concentrates 10 12 14 3.5% 3.1%Overall 29 33 39 3.0% 3.3% Price ($/liter) 2005 2010 2015 CAGR 05-10 CAGR 10-15Liquid concentrates 0.47 0.46 0.46 -0.6% 0.0%Powder concentrates 0.77 0.75 0.76 -0.4% 0.1%Average 0.58 0.56 0.56 -0.4% 0.0%

Source: Business Insights BUSINESS INSIGHTS

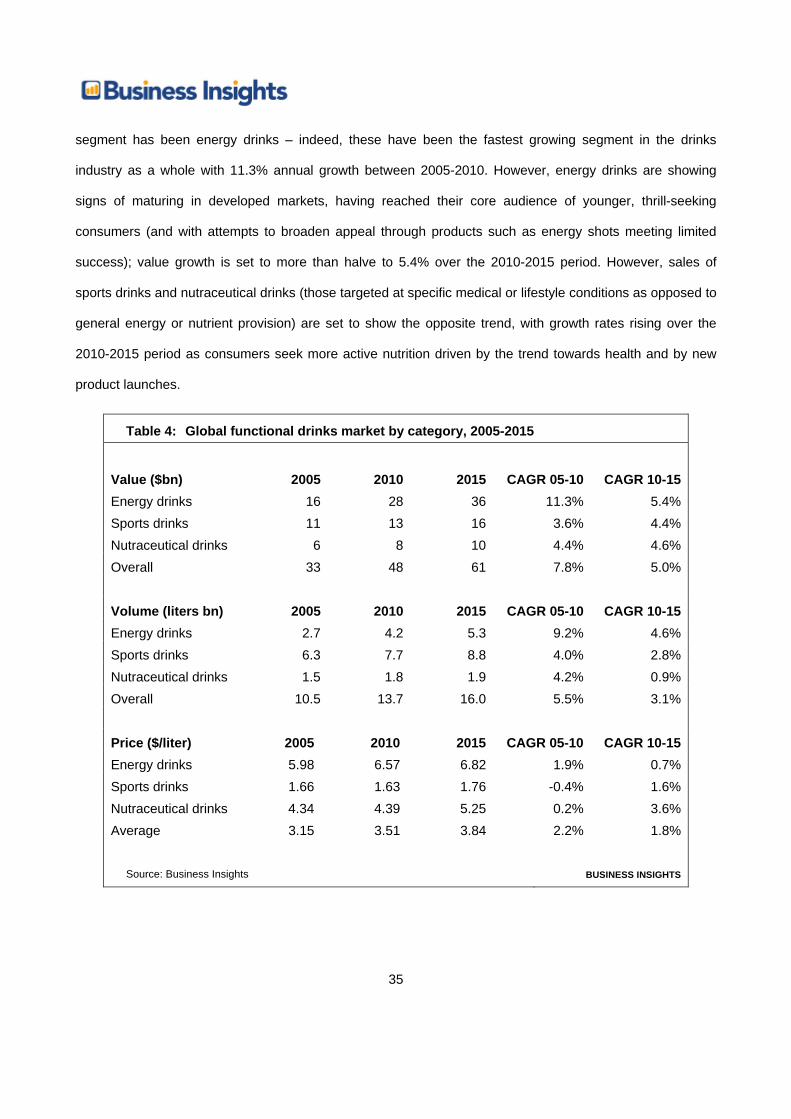

Functional drinks

The functional drinks category has been a major growth driver in the global soft drinks market, reaching a

total market value of $48bn in 2010 having grown at an average annual rate of 7.8%. The fastest-growing

35

segment has been energy drinks – indeed, these have been the fastest growing segment in the drinks

industry as a whole with 11.3% annual growth between 2005-2010. However, energy drinks are showing

signs of maturing in developed markets, having reached their core audience of younger, thrill-seeking

consumers (and with attempts to broaden appeal through products such as energy shots meeting limited

success); value growth is set to more than halve to 5.4% over the 2010-2015 period. However, sales of

sports drinks and nutraceutical drinks (those targeted at specific medical or lifestyle conditions as opposed to

general energy or nutrient provision) are set to show the opposite trend, with growth rates rising over the

2010-2015 period as consumers seek more active nutrition driven by the trend towards health and by new

product launches.

Table 4: Global functional drinks market by category, 2005-2015

Value ($bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15Energy drinks 16 28 36 11.3% 5.4%Sports drinks 11 13 16 3.6% 4.4%Nutraceutical drinks 6 8 10 4.4% 4.6%Overall 33 48 61 7.8% 5.0% Volume (liters bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15Energy drinks 2.7 4.2 5.3 9.2% 4.6%Sports drinks 6.3 7.7 8.8 4.0% 2.8%Nutraceutical drinks 1.5 1.8 1.9 4.2% 0.9%Overall 10.5 13.7 16.0 5.5% 3.1% Price ($/liter) 2005 2010 2015 CAGR 05-10 CAGR 10-15Energy drinks 5.98 6.57 6.82 1.9% 0.7%Sports drinks 1.66 1.63 1.76 -0.4% 1.6%Nutraceutical drinks 4.34 4.39 5.25 0.2% 3.6%Average 3.15 3.51 3.84 2.2% 1.8%

Source: Business Insights BUSINESS INSIGHTS

36

In volume terms, sports drinks are the biggest sellers with just over 50% of the market. This reflects their

position as the most established of the three functional categories, with mainstream sports drinks such as

Gatorade available in most global markets at relatively modest price points. Volume growth in this category is

expected to slow across the board, with all categories seeing substantial falls in volume. The worst-hit

proportionately will be nutraceutical drinks, with growth falling from over 4% to under 1%, reflecting

consumer skepticism over health claims, tighter regulation, and limited scope for these drinks in emerging

markets to date.

The difference between sports drinks and the other two categories is highlighted by their significant price

variance. Sports drinks cost $1.63 a liter on average – still far higher than mainstream soft drinks categories

– compared to $4.39 for nutraceuticals and $6.57 for energy drinks. Energy drinks are expected to show the

slower price growth over the next five years, as manufacturers seek to expand into emerging markets in

central & south America and Asia-Pacific and tap into youth trends; meanwhile, nutraceuticals are expected

to see strong price rises as new formulations are introduced to tackle ever-more-specific conditions at ever-

more-premium price points.

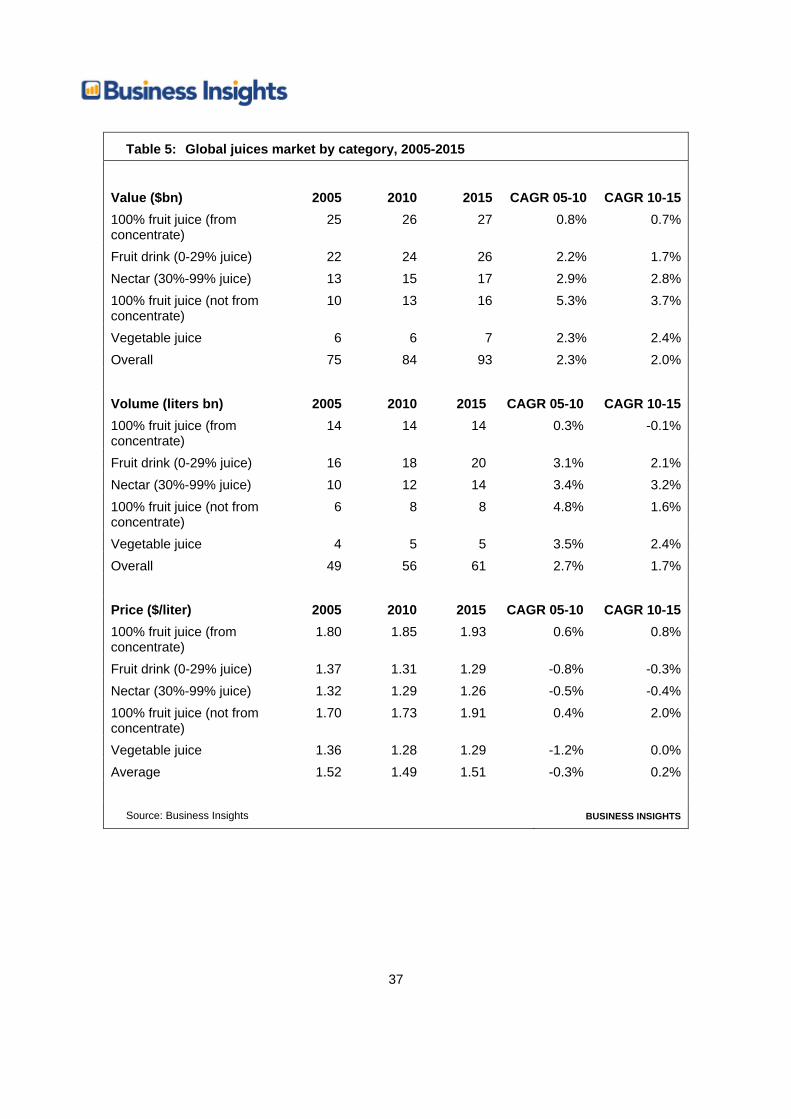

Juices

Juices are the third-largest category in the global soft drinks market in both value and volume terms, with

consumers spending $84bn a year on fruit juices in 2010. 100% juice made from concentrate is the biggest

category in value terms, accounting for $26bn of this spend. In total, 100% juices are worth $41bn, while

part-juice drinks are worth $39m, with vegetable juices accounting for the remainder. From-concentrate juice

has been the slowest-growing category, however, losing developed-world market share to not-from-

concentrate juices such as Tropicana due to their superior perceived taste profile. Meanwhile, sales of fruit

drinks and nectars have grown relatively strongly due to their developing world popularity. These trends are

expected to continue from 2010-2015, although at a slightly slower rate.

37

Table 5: Global juices market by category, 2005-2015

Value ($bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15100% fruit juice (from concentrate)

25 26 27 0.8% 0.7%

Fruit drink (0-29% juice) 22 24 26 2.2% 1.7%Nectar (30%-99% juice) 13 15 17 2.9% 2.8%100% fruit juice (not from concentrate)

10 13 16 5.3% 3.7%

Vegetable juice 6 6 7 2.3% 2.4%Overall 75 84 93 2.3% 2.0% Volume (liters bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15100% fruit juice (from concentrate)

14 14 14 0.3% -0.1%

Fruit drink (0-29% juice) 16 18 20 3.1% 2.1%Nectar (30%-99% juice) 10 12 14 3.4% 3.2%100% fruit juice (not from concentrate)

6 8 8 4.8% 1.6%

Vegetable juice 4 5 5 3.5% 2.4%Overall 49 56 61 2.7% 1.7% Price ($/liter) 2005 2010 2015 CAGR 05-10 CAGR 10-15100% fruit juice (from concentrate)

1.80 1.85 1.93 0.6% 0.8%

Fruit drink (0-29% juice) 1.37 1.31 1.29 -0.8% -0.3%Nectar (30%-99% juice) 1.32 1.29 1.26 -0.5% -0.4%100% fruit juice (not from concentrate)

1.70 1.73 1.91 0.4% 2.0%

Vegetable juice 1.36 1.28 1.29 -1.2% 0.0%Average 1.52 1.49 1.51 -0.3% 0.2%

Source: Business Insights BUSINESS INSIGHTS

38

In volume terms, the picture is rather different. Nectars and fruit drinks account for 30 billion liters of the 56

billion consumed every year, while 100% juices account for 22 billion. Similar growth trends have been

occurring, with from-concentrate juice sales almost flat, while all other categories have posted reasonable

growth. Going forward, sales of nectars and fruit drinks are expected to continue growing strongly, but not-

from-concentrate juices will see a significant fall in growth. While they will continue to win share from 100%

juice, they will struggle to make further inroads into the market. Reflecting their formulation, fruit drinks and

nectars are significantly cheaper than 100% juices, and have been showing falling prices (driven primarily by

geographical mix as developing markets grow) in recent years. This will continue to 2015. The only category

to show significant different pricing trends will be 100% juice: during the 2000s, mass-market products

gained wider distribution and took share away from top-end brands, bringing average prices down, but this

process is now more-or-less complete.

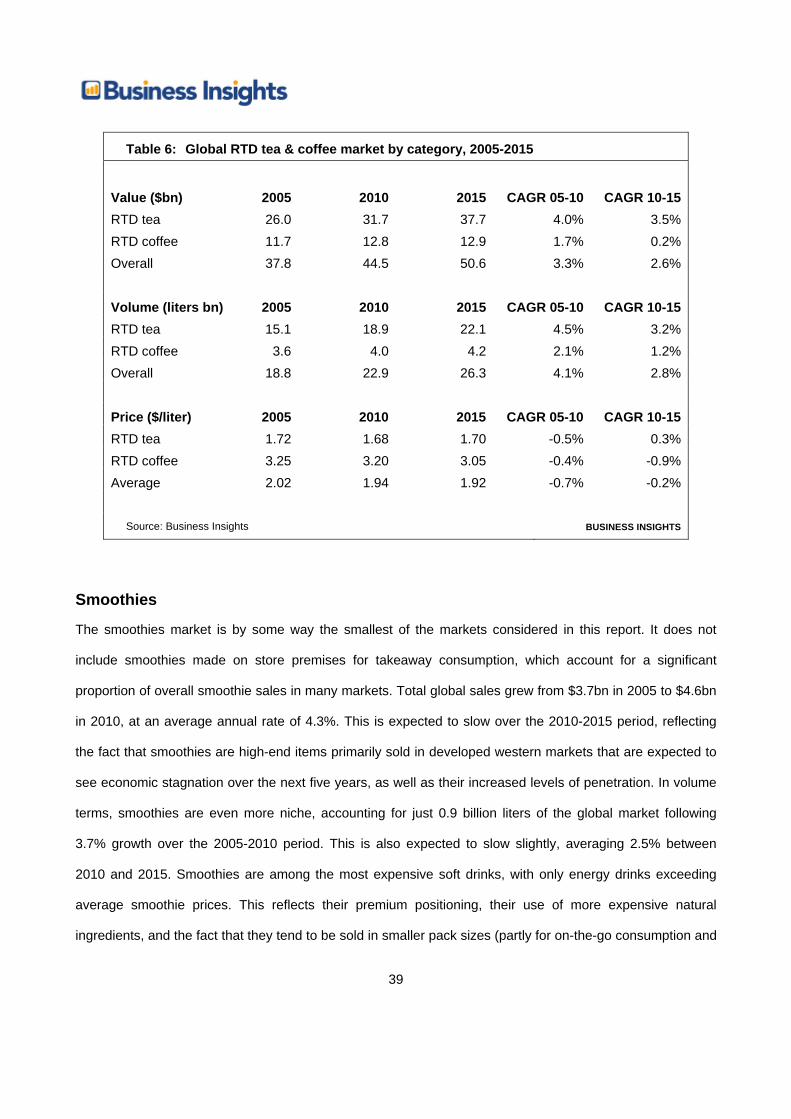

RTD tea & coffee

Sales of ready-to-drink tea & coffee products reached $44bn worldwide in 2010, having shown 3.3% annual

growth over the 2005-2010 period. RTD tea makes up three quarters of the market, and showed the

strongest growth of 4.0% per year, while RTD coffee grew at 1.7%. While RTD tea & coffee is a niche

category in many markets worldwide, it is dominated by the $20bn Japanese market which accounts for 45%

of total sales. Going forward, RTD tea is expected to continue to post strong growth, while RTD coffee

growth is expected to slow significantly. RTD tea dominates the market even more clearly in volume terms,

accounting for over 80% of sales, and has also shown strong volume growth of 4.5% per year. As the market

matures this is expected to slow to 3.2% volume growth between 2010 and 2015. Overall RTD tea & coffee

is a high-priced category, averaging $1.94 per liter; this is due both to its premium nature and to the fact that

the high-priced Japanese market is of such importance. As the market has shifted from niche to mainstream

in many countries worldwide, prices have fallen slightly over the last five years. RTD coffee prices are

expected to continue to fall slightly over the next five years, although RTD tea prices will show slight growth.

39

Table 6: Global RTD tea & coffee market by category, 2005-2015

Value ($bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15RTD tea 26.0 31.7 37.7 4.0% 3.5%RTD coffee 11.7 12.8 12.9 1.7% 0.2%Overall 37.8 44.5 50.6 3.3% 2.6% Volume (liters bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15RTD tea 15.1 18.9 22.1 4.5% 3.2%RTD coffee 3.6 4.0 4.2 2.1% 1.2%Overall 18.8 22.9 26.3 4.1% 2.8% Price ($/liter) 2005 2010 2015 CAGR 05-10 CAGR 10-15RTD tea 1.72 1.68 1.70 -0.5% 0.3%RTD coffee 3.25 3.20 3.05 -0.4% -0.9%Average 2.02 1.94 1.92 -0.7% -0.2%

Source: Business Insights BUSINESS INSIGHTS

Smoothies

The smoothies market is by some way the smallest of the markets considered in this report. It does not

include smoothies made on store premises for takeaway consumption, which account for a significant

proportion of overall smoothie sales in many markets. Total global sales grew from $3.7bn in 2005 to $4.6bn

in 2010, at an average annual rate of 4.3%. This is expected to slow over the 2010-2015 period, reflecting

the fact that smoothies are high-end items primarily sold in developed western markets that are expected to

see economic stagnation over the next five years, as well as their increased levels of penetration. In volume

terms, smoothies are even more niche, accounting for just 0.9 billion liters of the global market following

3.7% growth over the 2005-2010 period. This is also expected to slow slightly, averaging 2.5% between

2010 and 2015. Smoothies are among the most expensive soft drinks, with only energy drinks exceeding

average smoothie prices. This reflects their premium positioning, their use of more expensive natural

ingredients, and the fact that they tend to be sold in smaller pack sizes (partly for on-the-go consumption and

40

partly due to their high prices). Prices have been showing a small upward trend, constrained by the existing

large gap compared to other products and increasingly by the economic situation.

Table 7: Global smoothies market by category, 2005-2015

Value ($bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15Fruit-based 3.4 4.2 4.9 4.3% 2.8%Dairy-based 0.3 0.4 0.5 4.3% 3.4%Overall 3.7 4.6 5.3 4.3% 2.9% Volume (liters bn) 2005 2010 2015 CAGR 05-10 CAGR 10-15Fruit-based 0.7 0.8 0.9 3.7% 2.5%Dairy-based 0.1 0.1 0.1 3.8% 2.8%Overall 0.7 0.9 1.0 3.7% 2.5% Price ($/liter) 2005 2010 2015 CAGR 05-10 CAGR 10-15Fruit-based 5.21 5.35 5.45 0.6% 0.4%Dairy-based 4.58 4.68 4.83 0.4% 0.6%Average 5.15 5.29 5.40 0.6% 0.4%

Source: Business Insights BUSINESS INSIGHTS

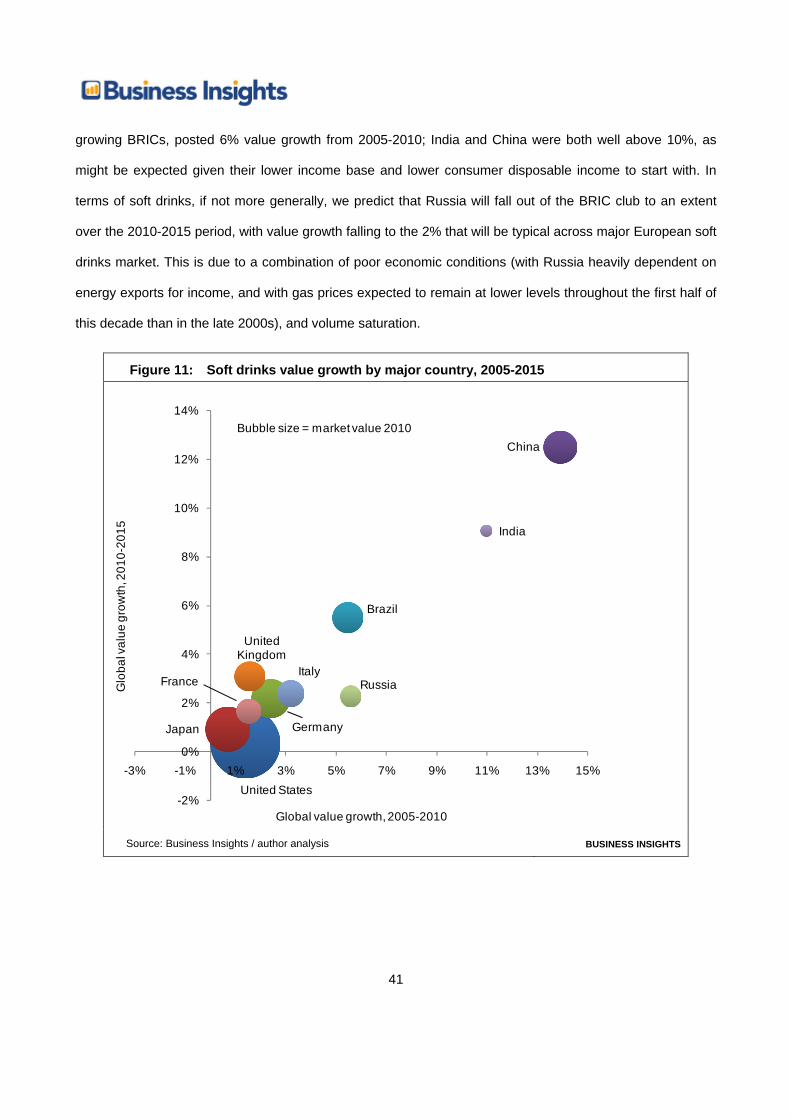

Major country profiles In addition to considering the market on a regional basis, this report also looks at 10 major countries in-

depth. While they are not necessarily the largest in value or volume terms, they are the markets which

combine the strongest potential, the fastest current growth, the highest current sales, and the most important

centers of innovation. In this context, Figure 11 clearly highlights the contrast between the major developed

economies and the BRIC (Brazil, Russia, India and China countries). Although there are significant

differences in market performance between the developed countries in value terms, with the Italian market

growing at three times the speed of the Japanese market from 2005-2010, they are nonetheless dwarfed by

the differences between the BRIC countries and the developed markets. Russia and Brazil, the slowest-

41

growing BRICs, posted 6% value growth from 2005-2010; India and China were both well above 10%, as

might be expected given their lower income base and lower consumer disposable income to start with. In

terms of soft drinks, if not more generally, we predict that Russia will fall out of the BRIC club to an extent

over the 2010-2015 period, with value growth falling to the 2% that will be typical across major European soft

drinks market. This is due to a combination of poor economic conditions (with Russia heavily dependent on

energy exports for income, and with gas prices expected to remain at lower levels throughout the first half of

this decade than in the late 2000s), and volume saturation.

Figure 11: Soft drinks value growth by major country, 2005-2015

United States

Japan Germany

China

Brazil

United Kingdom

ItalyFrance Russia

India

-2%

0%

2%

4%

6%

8%

10%

12%

14%

-3% -1% 1% 3% 5% 7% 9% 11% 13% 15%

Glo

bal v

alue

gro

wth

, 201

0-20

15

Global value growth, 2005-2010

Bubble size = market value 2010

Source: Business Insights / author analysis BUSINESS INSIGHTS

42

Looking at Figure 12's illustration of volume growth, the difference between the BRICs and the developed

economies starts to look more like a continuum. India and China have shown volume growth above 10%,

reflecting their vast populations and very low per capita consumption rates. Meanwhile, with per capita

consumption rates starting to approach those seen in developed markets, volume growth rates in Brazil and

Russia have been respectable rather than exceptional – and Russian volume growth is expected to fall

below 2% in the 2010-2015 period, coming in below Germany, Italy and the UK. The figure also highlights

the contrast between France, Japan and the US, and Germany, Italy and the UK – the former three saw

negligible growth or decline from 2005-2010 and are in the same between 2010 and 2015, whereas the UK,

Italy and Germany are expecting healty volume growth around 2% a year over the next few years.

Figure 12: Soft drinks volume growth by major country, 2005-2015

United States

Japan

Germany

China

Brazil

United Kingdom

ItalyFrance

Russia

India

Glo

bal v

olum

e gr

owth

, 201

0-20

15

Global volume growth, 2005-2010

Bubble size = market volume 201010%

8%

6%

4%

2%

-2%

12%8%6%4% 10%-2%

Source: Business Insights / author analysis BUSINESS INSIGHTS

43

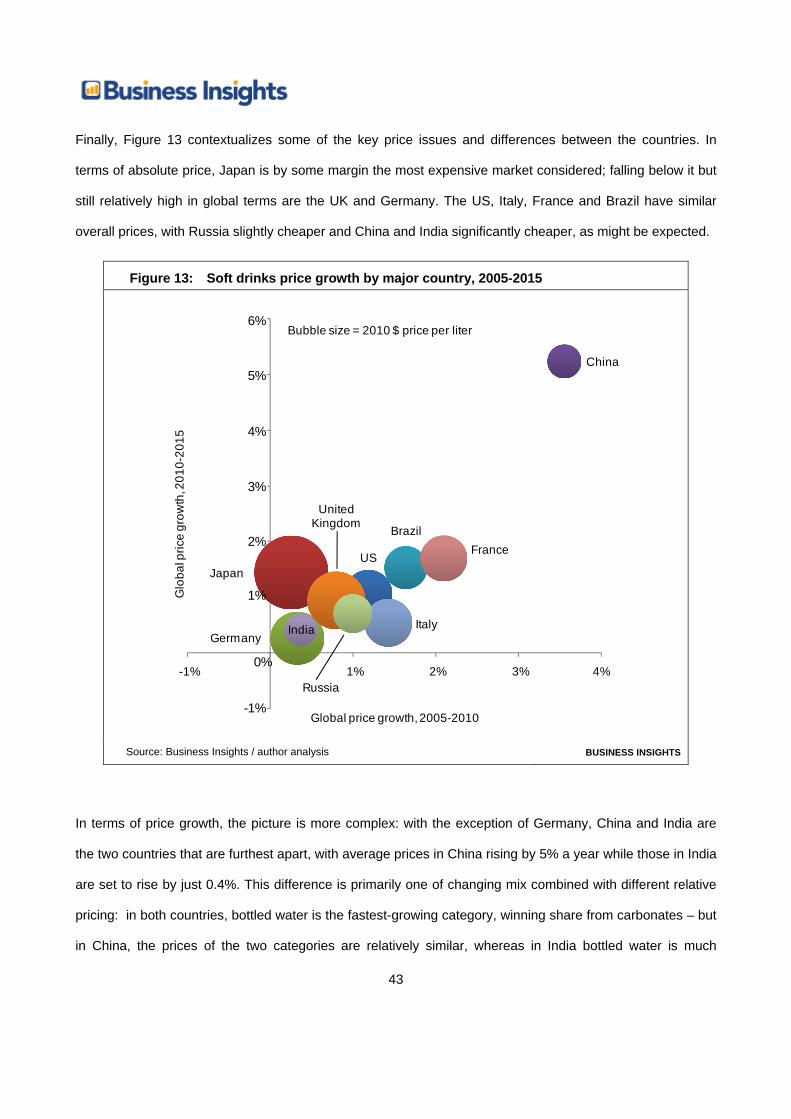

Finally, Figure 13 contextualizes some of the key price issues and differences between the countries. In

terms of absolute price, Japan is by some margin the most expensive market considered; falling below it but

still relatively high in global terms are the UK and Germany. The US, Italy, France and Brazil have similar

overall prices, with Russia slightly cheaper and China and India significantly cheaper, as might be expected.

Figure 13: Soft drinks price growth by major country, 2005-2015

USJapan

Germany

China

Brazil

United Kingdom

Italy

France

Russia

India

Glo

bal p

rice

grow

th, 2

010-

2015

Global price growth, 2005-2010

6%

5%

4%

3%

2%

-1%

1%

0%1% 2% 3% 4%-1%

Bubble size = 2010 $ price per liter

Source: Business Insights / author analysis BUSINESS INSIGHTS

In terms of price growth, the picture is more complex: with the exception of Germany, China and India are

the two countries that are furthest apart, with average prices in China rising by 5% a year while those in India

are set to rise by just 0.4%. This difference is primarily one of changing mix combined with different relative

pricing: in both countries, bottled water is the fastest-growing category, winning share from carbonates – but

in China, the prices of the two categories are relatively similar, whereas in India bottled water is much

44

cheaper than carbonates, driving low average price growth even though Indian bottled water prices are

expected to grow at 2.3% a year. At the same time, though, there is much higher price growth within

categories in China than in India, reflecting a combination of greater premiumization in China and price

controls on the Indian market keeping price rises below inflation.

Brazil

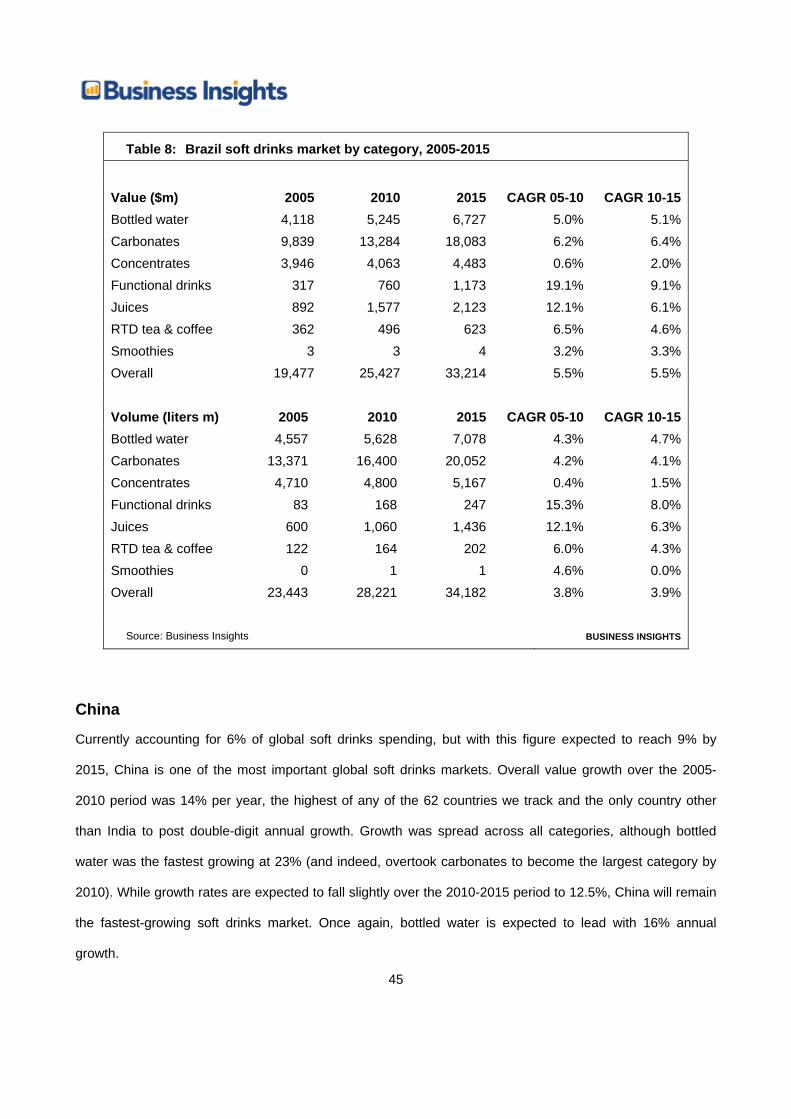

With total spending of $25bn per year, Brazil accounts for 5% of the global soft drinks market by value. In

line with Brazil’s generally strong economic growth, which has led it to be considered part of the BRIC

emerging markets bloc and to be increasingly perceived as a mid-income rather than a developing country,

the country’s soft drinks market has also been performing strongly. Functional drinks and juices have grown

at double-digit rates of 19% and 12% respectively, with all other categories other than concentrates posting

strong growth (the slower growth in concentrates reflects consumers shifting to RTD juices in line with

improvements in income). The market is expected to continue posting strong growth over the next five years,

although now that juices and functional drinks have achieved relatively mainstream positions, their growth

will fall to high single-digit levels between 2010-2015. Brazil’s 28.2 billion liters of soft drinks consumption

make up 6% of total global consumption.

Although not as strong as value growth, volume growth has also been strong across all categories other than

concentrates, with functional drinks and juices again posting particularly significant growth of 15% and 12%

respectively. Concentrates are expected to see something of a revival between 2010-2015, with growth

rising from 0.4% to 1.5%. In volume terms, the three largest categories in the Brazilian market all sell for

similar prices: bottled water, concentrates and carbonates are all priced between 80-90 cents per liter,

driving the country’s 90 cent per liter average price. Juices command a slight premium at $1.49, while

functional drinks are extremely expensive products targeting at Brazil’s growing wealthy middle class

population at $4.52 a liter on average. There has been no clear price trend across categories, with water

and functional drinks rising noticeably while most other categories remain flat. This is broadly likely to

continue between 2010-2015.

45

Table 8: Brazil soft drinks market by category, 2005-2015

Value ($m) 2005 2010 2015 CAGR 05-10 CAGR 10-15Bottled water 4,118 5,245 6,727 5.0% 5.1%Carbonates 9,839 13,284 18,083 6.2% 6.4%Concentrates 3,946 4,063 4,483 0.6% 2.0%Functional drinks 317 760 1,173 19.1% 9.1%Juices 892 1,577 2,123 12.1% 6.1%RTD tea & coffee 362 496 623 6.5% 4.6%Smoothies 3 3 4 3.2% 3.3%Overall 19,477 25,427 33,214 5.5% 5.5% Volume (liters m) 2005 2010 2015 CAGR 05-10 CAGR 10-15Bottled water 4,557 5,628 7,078 4.3% 4.7%Carbonates 13,371 16,400 20,052 4.2% 4.1%Concentrates 4,710 4,800 5,167 0.4% 1.5%Functional drinks 83 168 247 15.3% 8.0%Juices 600 1,060 1,436 12.1% 6.3%RTD tea & coffee 122 164 202 6.0% 4.3%Smoothies 0 1 1 4.6% 0.0%Overall 23,443 28,221 34,182 3.8% 3.9%

Source: Business Insights BUSINESS INSIGHTS

China

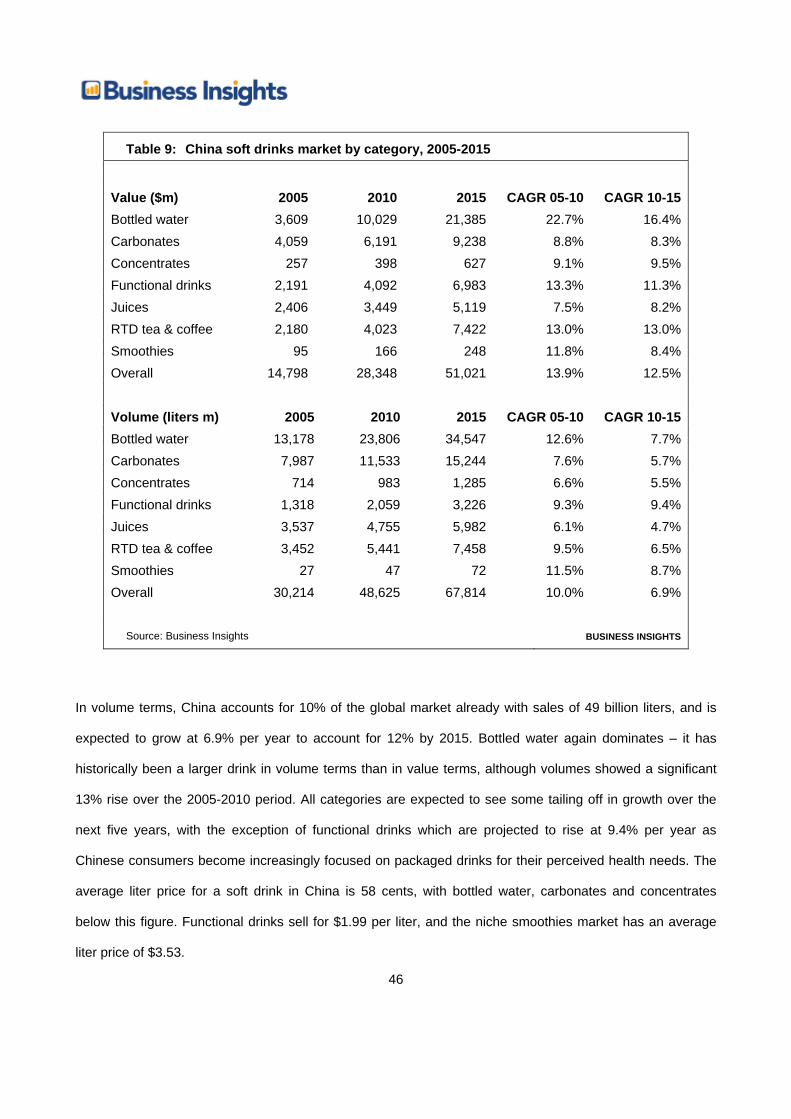

Currently accounting for 6% of global soft drinks spending, but with this figure expected to reach 9% by

2015, China is one of the most important global soft drinks markets. Overall value growth over the 2005-

2010 period was 14% per year, the highest of any of the 62 countries we track and the only country other

than India to post double-digit annual growth. Growth was spread across all categories, although bottled

water was the fastest growing at 23% (and indeed, overtook carbonates to become the largest category by

2010). While growth rates are expected to fall slightly over the 2010-2015 period to 12.5%, China will remain

the fastest-growing soft drinks market. Once again, bottled water is expected to lead with 16% annual

growth.

46

Table 9: China soft drinks market by category, 2005-2015

Value ($m) 2005 2010 2015 CAGR 05-10 CAGR 10-15Bottled water 3,609 10,029 21,385 22.7% 16.4%Carbonates 4,059 6,191 9,238 8.8% 8.3%Concentrates 257 398 627 9.1% 9.5%Functional drinks 2,191 4,092 6,983 13.3% 11.3%Juices 2,406 3,449 5,119 7.5% 8.2%RTD tea & coffee 2,180 4,023 7,422 13.0% 13.0%Smoothies 95 166 248 11.8% 8.4%Overall 14,798 28,348 51,021 13.9% 12.5% Volume (liters m) 2005 2010 2015 CAGR 05-10 CAGR 10-15Bottled water 13,178 23,806 34,547 12.6% 7.7%Carbonates 7,987 11,533 15,244 7.6% 5.7%Concentrates 714 983 1,285 6.6% 5.5%Functional drinks 1,318 2,059 3,226 9.3% 9.4%Juices 3,537 4,755 5,982 6.1% 4.7%RTD tea & coffee 3,452 5,441 7,458 9.5% 6.5%Smoothies 27 47 72 11.5% 8.7%Overall 30,214 48,625 67,814 10.0% 6.9%

Source: Business Insights BUSINESS INSIGHTS

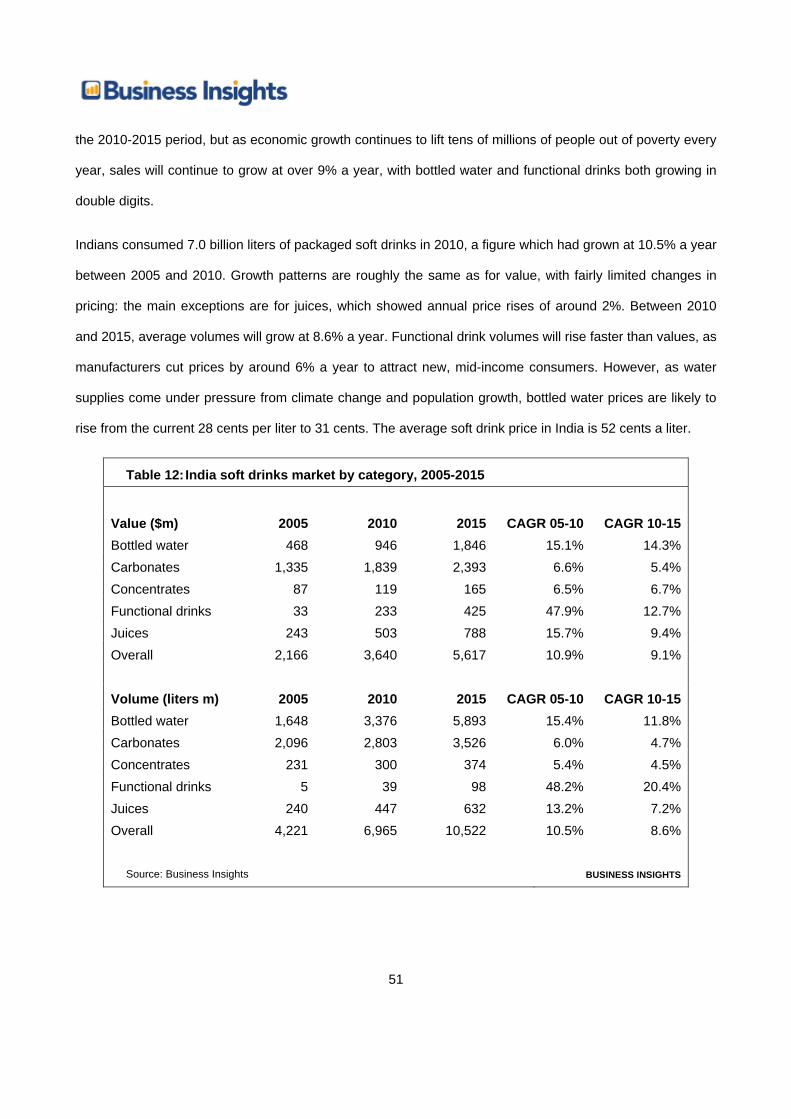

In volume terms, China accounts for 10% of the global market already with sales of 49 billion liters, and is

expected to grow at 6.9% per year to account for 12% by 2015. Bottled water again dominates – it has

historically been a larger drink in volume terms than in value terms, although volumes showed a significant

13% rise over the 2005-2010 period. All categories are expected to see some tailing off in growth over the

next five years, with the exception of functional drinks which are projected to rise at 9.4% per year as

Chinese consumers become increasingly focused on packaged drinks for their perceived health needs. The

average liter price for a soft drink in China is 58 cents, with bottled water, carbonates and concentrates

below this figure. Functional drinks sell for $1.99 per liter, and the niche smoothies market has an average

liter price of $3.53.

47

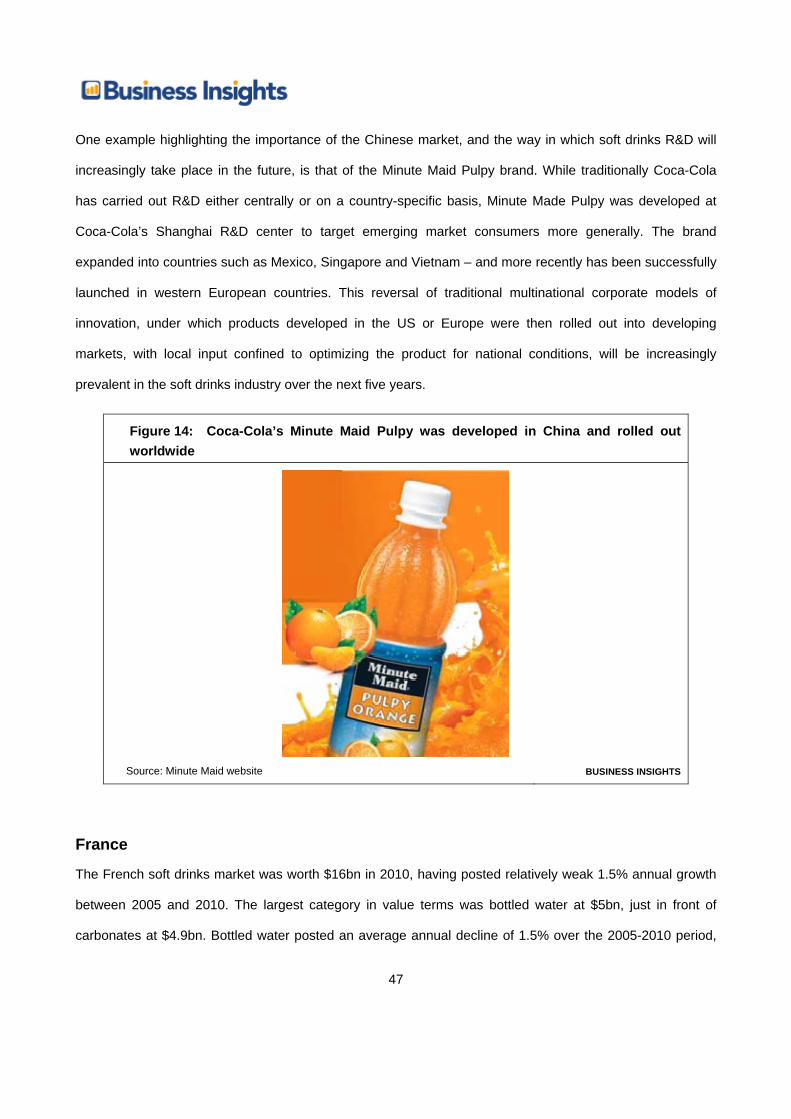

One example highlighting the importance of the Chinese market, and the way in which soft drinks R&D will

increasingly take place in the future, is that of the Minute Maid Pulpy brand. While traditionally Coca-Cola

has carried out R&D either centrally or on a country-specific basis, Minute Made Pulpy was developed at

Coca-Cola’s Shanghai R&D center to target emerging market consumers more generally. The brand

expanded into countries such as Mexico, Singapore and Vietnam – and more recently has been successfully

launched in western European countries. This reversal of traditional multinational corporate models of

innovation, under which products developed in the US or Europe were then rolled out into developing

markets, with local input confined to optimizing the product for national conditions, will be increasingly

prevalent in the soft drinks industry over the next five years.

Figure 14: Coca-Cola’s Minute Maid Pulpy was developed in China and rolled out worldwide

Source: Minute Maid website BUSINESS INSIGHTS

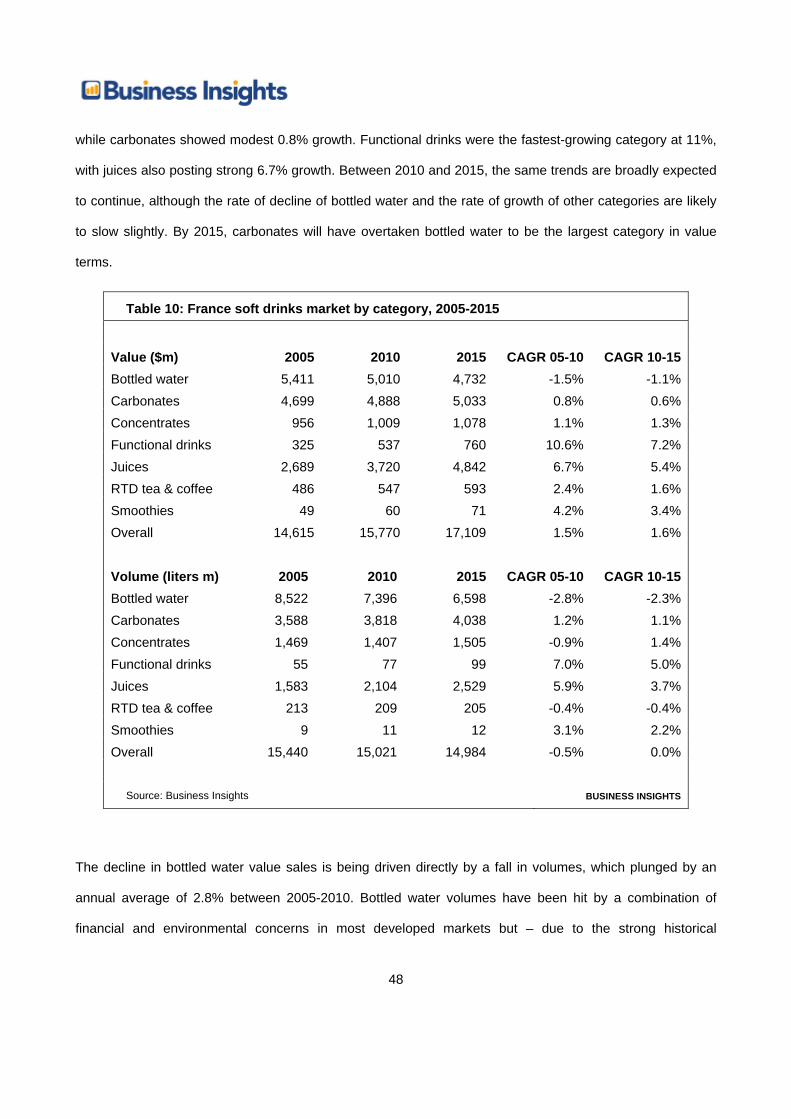

France

The French soft drinks market was worth $16bn in 2010, having posted relatively weak 1.5% annual growth

between 2005 and 2010. The largest category in value terms was bottled water at $5bn, just in front of

carbonates at $4.9bn. Bottled water posted an average annual decline of 1.5% over the 2005-2010 period,

48

while carbonates showed modest 0.8% growth. Functional drinks were the fastest-growing category at 11%,

with juices also posting strong 6.7% growth. Between 2010 and 2015, the same trends are broadly expected

to continue, although the rate of decline of bottled water and the rate of growth of other categories are likely

to slow slightly. By 2015, carbonates will have overtaken bottled water to be the largest category in value

terms.

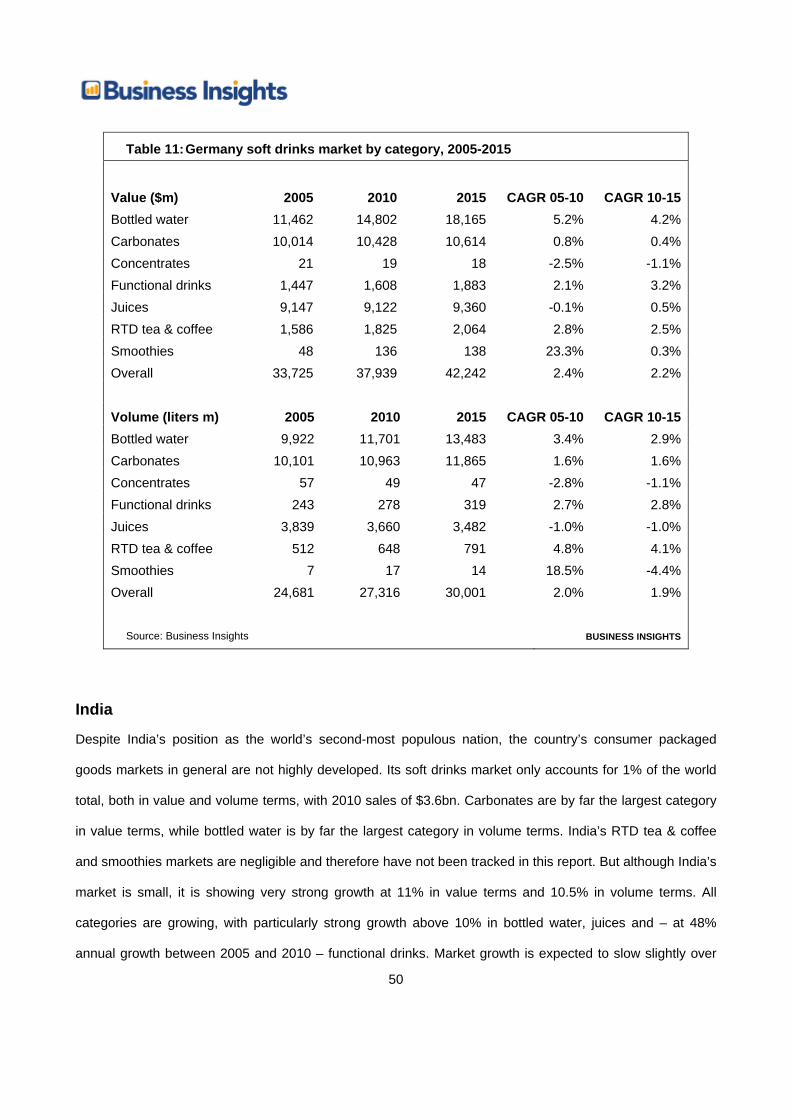

Table 10: France soft drinks market by category, 2005-2015

Value ($m) 2005 2010 2015 CAGR 05-10 CAGR 10-15Bottled water 5,411 5,010 4,732 -1.5% -1.1%Carbonates 4,699 4,888 5,033 0.8% 0.6%Concentrates 956 1,009 1,078 1.1% 1.3%Functional drinks 325 537 760 10.6% 7.2%Juices 2,689 3,720 4,842 6.7% 5.4%RTD tea & coffee 486 547 593 2.4% 1.6%Smoothies 49 60 71 4.2% 3.4%Overall 14,615 15,770 17,109 1.5% 1.6% Volume (liters m) 2005 2010 2015 CAGR 05-10 CAGR 10-15Bottled water 8,522 7,396 6,598 -2.8% -2.3%Carbonates 3,588 3,818 4,038 1.2% 1.1%Concentrates 1,469 1,407 1,505 -0.9% 1.4%Functional drinks 55 77 99 7.0% 5.0%Juices 1,583 2,104 2,529 5.9% 3.7%RTD tea & coffee 213 209 205 -0.4% -0.4%Smoothies 9 11 12 3.1% 2.2%Overall 15,440 15,021 14,984 -0.5% 0.0%

Source: Business Insights BUSINESS INSIGHTS

The decline in bottled water value sales is being driven directly by a fall in volumes, which plunged by an

annual average of 2.8% between 2005-2010. Bottled water volumes have been hit by a combination of

financial and environmental concerns in most developed markets but – due to the strong historical

49

penetration of bottled water in France, and combined with aggressive government marketing campaigns for

tap water – the decline seen in the French market has been particularly significant. The decline in bottled

water sales led directly to an overall decline in French soft drink volumes from 15.4 billion liters to 15.0 billion