53 Chapter – 2 GROWTH OF FINANCIAL DERIVATIVES IN INDIA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

53

Chapter – 2

GROWTH OF FINANCIAL

DERIVATIVES IN INDIA

54

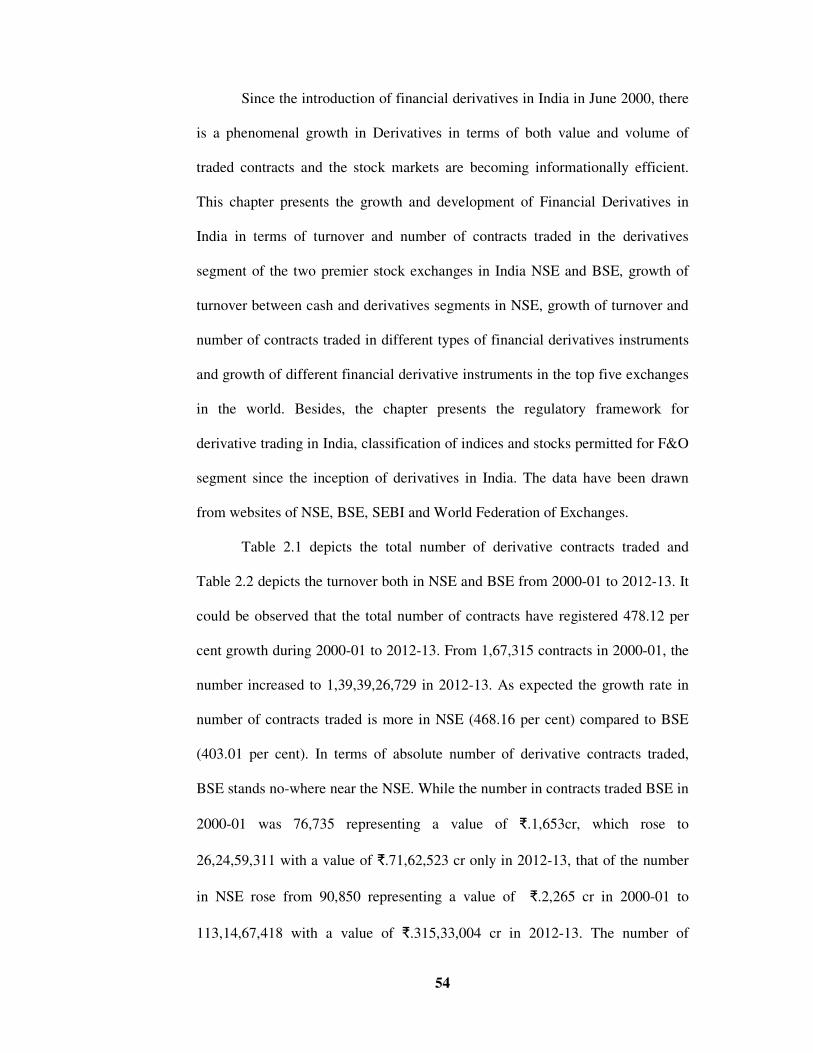

Since the introduction of financial derivatives in India in June 2000, there

is a phenomenal growth in Derivatives in terms of both value and volume of

traded contracts and the stock markets are becoming informationally efficient.

This chapter presents the growth and development of Financial Derivatives in

India in terms of turnover and number of contracts traded in the derivatives

segment of the two premier stock exchanges in India NSE and BSE, growth of

turnover between cash and derivatives segments in NSE, growth of turnover and

number of contracts traded in different types of financial derivatives instruments

and growth of different financial derivative instruments in the top five exchanges

in the world. Besides, the chapter presents the regulatory framework for

derivative trading in India, classification of indices and stocks permitted for F&O

segment since the inception of derivatives in India. The data have been drawn

from websites of NSE, BSE, SEBI and World Federation of Exchanges.

Table 2.1 depicts the total number of derivative contracts traded and

Table 2.2 depicts the turnover both in NSE and BSE from 2000-01 to 2012-13. It

could be observed that the total number of contracts have registered 478.12 per

cent growth during 2000-01 to 2012-13. From 1,67,315 contracts in 2000-01, the

number increased to 1,39,39,26,729 in 2012-13. As expected the growth rate in

number of contracts traded is more in NSE (468.16 per cent) compared to BSE

(403.01 per cent). In terms of absolute number of derivative contracts traded,

BSE stands no-where near the NSE. While the number in contracts traded BSE in

2000-01 was 76,735 representing a value of �.1,653cr, which rose to

26,24,59,311 with a value of �.71,62,523 cr only in 2012-13, that of the number

in NSE rose from 90,850 representing a value of �.2,265 cr in 2000-01 to

113,14,67,418 with a value of �.315,33,004 cr in 2012-13. The number of

55

derivatives contracts in these exchanges reached a milestone of 1,39,39,26,729 in

2013 since the inception of derivatives. These results are presented in Graph 2.1

and Graph 2.2

Table 2.1: Growth of Financial Derivatives in terms of No. of Contracts in

NSE and BSE

Year NSE BSE Total

2000–01 90,580

(54.14)

76,735

(45.86)

1,67,315

(100)

2001-02 41,96,873

(97.55)

1,05,607

(2.45)

43,02,480

(100)

2002-03 1,67,68,909

(99.18)

1,38,037

(0.82)

1,69,06,946

(100)

2003-04 5,68,86,776

(99.33)

3,82,258

(0.67)

5,72,69,034

(100)

2004-05 7,70,17,185

(99.31)

5,31,719

(0.69)

7,75,48,904

(100)

2005-06 15,76,19,271

(99.9999)

203

(0.0001)

15,76,19,474

(100)

2006-07 21,68,83,573

(99.19)

17,81,670

(0.81)

21,86,65,243

(100)

2007-08 42,50,13,200

(98.28)

74,53,371

(1.72)

43,24,66,571

(100)

2008-09 65,73,90,497

(99.92)

4,96,502

(0.08)

65,78,86,999

(100)

2009-10 67,92,93,922

(99.999)

9028

(0.001)

679302950

(100)

2010-11 1,03,42,12,062

(99.999)

5,623

(0.001)

1,03,42,17,685

(100)

2011-12 1,20,50,45,464

(97.40)

3,22,22,825

(2.60)

1,23,72,68,289

(100)

2012-13 1,13,14,67,418

(81.17)

26,24,59,311

(18.83)

1,39,39,26,729

(100)

CAGR 468.16 403.01 478.12

Source: Complied and calculated from the data taken from www.nseindia.com

CAGR: Cumulative Average Growth Rate

Graph 2.1: Percentage of growth in NSE and BSE (No of contracts)

Table 2.2: Growth of Financial Derivatives in terms of Turnover (

Year

2000–01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

CAGR

Source: Complied and calculated from the data taken from

CAGR: Cumulative Average Growth Rate

0.00

20.00

40.00

60.00

80.00

100.00

Ra

te o

f G

row

th

Percentage of growth of No of Contract in NSE and BSE

56

Graph 2.1: Percentage of growth in NSE and BSE (No of contracts)

Table 2.2: Growth of Financial Derivatives in terms of Turnover (

NSE and BSE

NSE BSE Total

2,365

(60.36)

1,653

(41.14)

4,018

(100)

1,01,926

(98.15)

1,923

(1.85)

1,03,849

4,39,862

(99.44)

2,479

(0.56)

4,42,341

(100)

21,30,610

(99.46)

11,620

(0.54)

21,42,230

(100)

25,46,982

(99.33)

17,074

(0.67)

25,64,056

(100)

48,24,174

(99.9998)

8.77

(0.0002)

48,24,183

(100)

73,56,242

(99.20)

59,007

(0.80)

74,15,249

(100)

1,30,90,478

(98.18)

2,42,308

(1.82)

1,33,32,786

1,10,10,482

(99.89)

11,775

(0.11)

1,10,22,257

(100)

1,76,63,665

(99.9987)

234.13

(0.0013)

1,76,63,899

(100)

2,92,48,221

(99.9995)

154.00

(0.0005)

2,92,48,375

(100)

3,13,49,732

(97.49)

8,08,477

(2.51)

3,21,58,209

(100)

3,15,33,004

(81.49)

71,62,523

(18.51)

3,86,95,527

(100)

321.59 272.60 328.85

Source: Complied and calculated from the data taken from www.nseindia.com

CAGR: Cumulative Average Growth Rate

Time Period

Percentage of growth of No of Contract in NSE and BSE

Graph 2.1: Percentage of growth in NSE and BSE (No of contracts)

Table 2.2: Growth of Financial Derivatives in terms of Turnover (�. in Cr) in

Total

4,018

(100)

1,03,849

(100)

4,42,341

(100)

21,42,230

(100)

25,64,056

(100)

48,24,183

(100)

74,15,249

(100)

1,33,32,786

(100)

1,10,22,257

(100)

1,76,63,899

(100)

2,92,48,375

(100)

3,21,58,209

(100)

3,86,95,527

(100)

328.85

www.nseindia.com

Percentage of growth of No of Contract in NSE and BSE

NSE

BSE

Graph 2.2: Percentage of growth of turnover

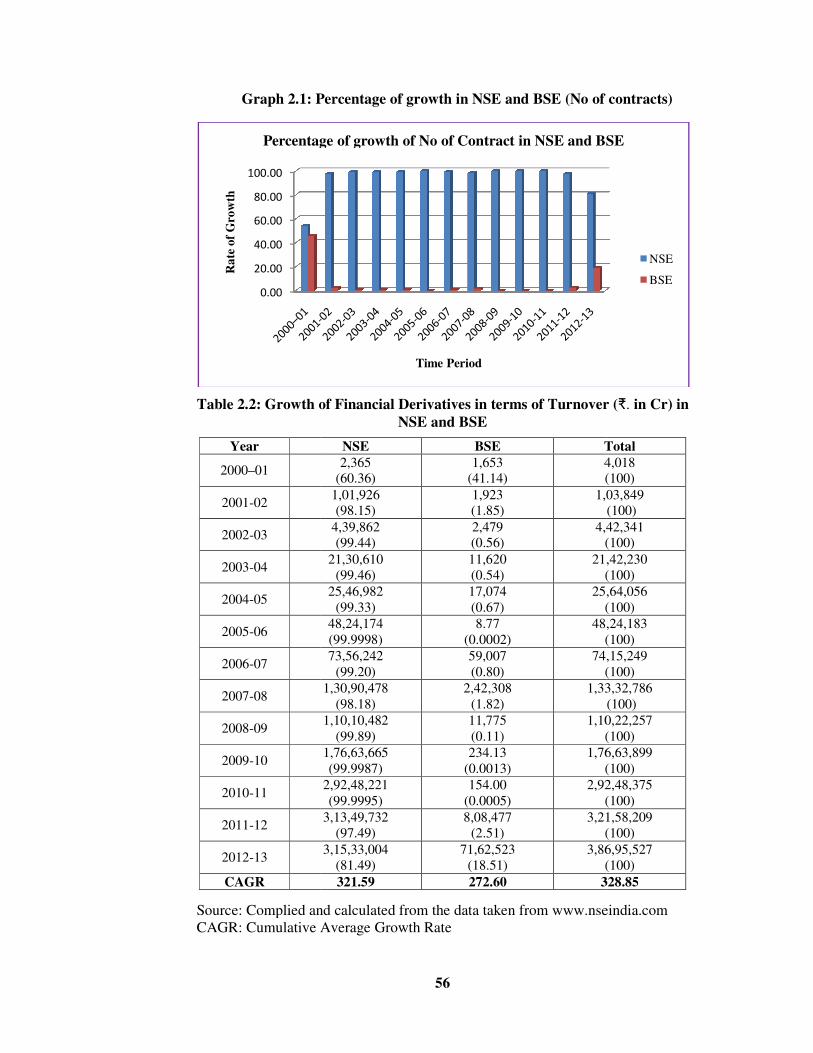

Table 2.3 depicts the explosive growth of Derivative

introduction in Indian Capital Market

share of Derivative segment, which was just 0.18

2000-2001, increased to 92.09

turnover of Cash segment

2001 declined sharply to just 7.91

the total turnover has registered a substantial growth of 31

of 13 years, which could be mainly attributed to the growt

derivatives, which has registered a growth of 120.67

period. From the average daily turnover

shown the table, it is very clear that the daily average

ups and downs in the cash segment. From an average daily turnover of

in 2000-01 it rose to

registered a peak of

consistency in the average daily turnover in the cash segment. On the other

0.0010.0020.0030.0040.0050.0060.0070.0080.0090.00

100.00

Ra

te o

f G

row

th

Percentage of growth of turnover (

57

2.2: Percentage of growth of turnover (�.in Cr) in NSE and BSE

Table 2.3 depicts the explosive growth of Derivative segment

introduction in Indian Capital Market in comparison with Cash segment

share of Derivative segment, which was just 0.18 per cent of total turnover in

2001, increased to 92.09 per cent by 2012-2013. On the other

segment, which was 99.82 per cent in the total turnover in 2000

2001 declined sharply to just 7.91 per cent. An important observation here is that

the total turnover has registered a substantial growth of 31 per cent

of 13 years, which could be mainly attributed to the growth of turnover in

derivatives, which has registered a growth of 120.67 per cent during the same

From the average daily turnover in both cash and derivative

shown the table, it is very clear that the daily average turnover registered many

s and downs in the cash segment. From an average daily turnover of

01 it rose to �.10,833 cr by the end of the year 2012-13. But in between

registered a peak of �.16,959 cr in 2009-10. In other words,

consistency in the average daily turnover in the cash segment. On the other

Time Period

Percentage of growth of turnover (�. in Cr) in NSE and

BSE

in Cr) in NSE and BSE

egment since their

segment. The

of total turnover in

other hand the

in the total turnover in 2000-

. An important observation here is that

over a period

h of turnover in

during the same

in both cash and derivative segments

registered many

s and downs in the cash segment. From an average daily turnover of �.5,337 cr

13. But in between

there is no-

consistency in the average daily turnover in the cash segment. On the other hand,

in Cr) in NSE and

NSE

BSE

58

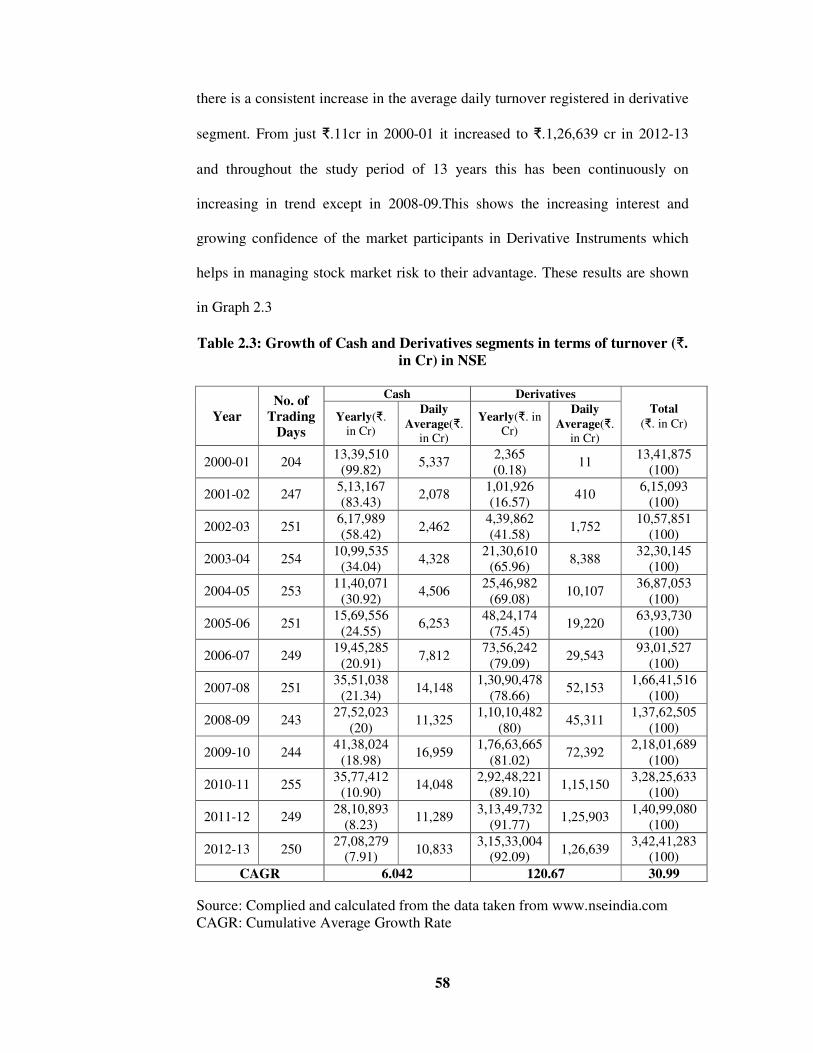

there is a consistent increase in the average daily turnover registered in derivative

segment. From just �.11cr in 2000-01 it increased to �.1,26,639 cr in 2012-13

and throughout the study period of 13 years this has been continuously on

increasing in trend except in 2008-09.This shows the increasing interest and

growing confidence of the market participants in Derivative Instruments which

helps in managing stock market risk to their advantage. These results are shown

in Graph 2.3

Table 2.3: Growth of Cash and Derivatives segments in terms of turnover (�.

in Cr) in NSE

Year

No. of

Trading

Days

Cash Derivatives

Total

(�. in Cr) Yearly(�.

in Cr)

Daily

Average(�.

in Cr)

Yearly(�. in

Cr)

Daily

Average(�.

in Cr)

2000-01 204 13,39,510

(99.82) 5,337

2,365

(0.18) 11

13,41,875

(100)

2001-02 247 5,13,167

(83.43) 2,078

1,01,926

(16.57) 410

6,15,093

(100)

2002-03 251 6,17,989

(58.42) 2,462

4,39,862

(41.58) 1,752

10,57,851

(100)

2003-04 254 10,99,535

(34.04) 4,328

21,30,610

(65.96) 8,388

32,30,145

(100)

2004-05 253 11,40,071

(30.92) 4,506

25,46,982

(69.08) 10,107

36,87,053

(100)

2005-06 251 15,69,556

(24.55) 6,253

48,24,174

(75.45) 19,220

63,93,730

(100)

2006-07 249 19,45,285

(20.91) 7,812

73,56,242

(79.09) 29,543

93,01,527

(100)

2007-08 251 35,51,038

(21.34) 14,148

1,30,90,478

(78.66) 52,153

1,66,41,516

(100)

2008-09 243 27,52,023

(20) 11,325

1,10,10,482

(80) 45,311

1,37,62,505

(100)

2009-10 244 41,38,024

(18.98) 16,959

1,76,63,665

(81.02) 72,392

2,18,01,689

(100)

2010-11 255 35,77,412

(10.90) 14,048

2,92,48,221

(89.10) 1,15,150

3,28,25,633

(100)

2011-12 249 28,10,893

(8.23) 11,289

3,13,49,732

(91.77) 1,25,903

1,40,99,080

(100)

2012-13 250 27,08,279

(7.91) 10,833

3,15,33,004

(92.09) 1,26,639

3,42,41,283

(100)

CAGR 6.042 120.67 30.99

Source: Complied and calculated from the data taken from www.nseindia.com

CAGR: Cumulative Average Growth Rate

59

Graph 2.3: Percentage of growth of turnover in Cash and Derivatives

segments

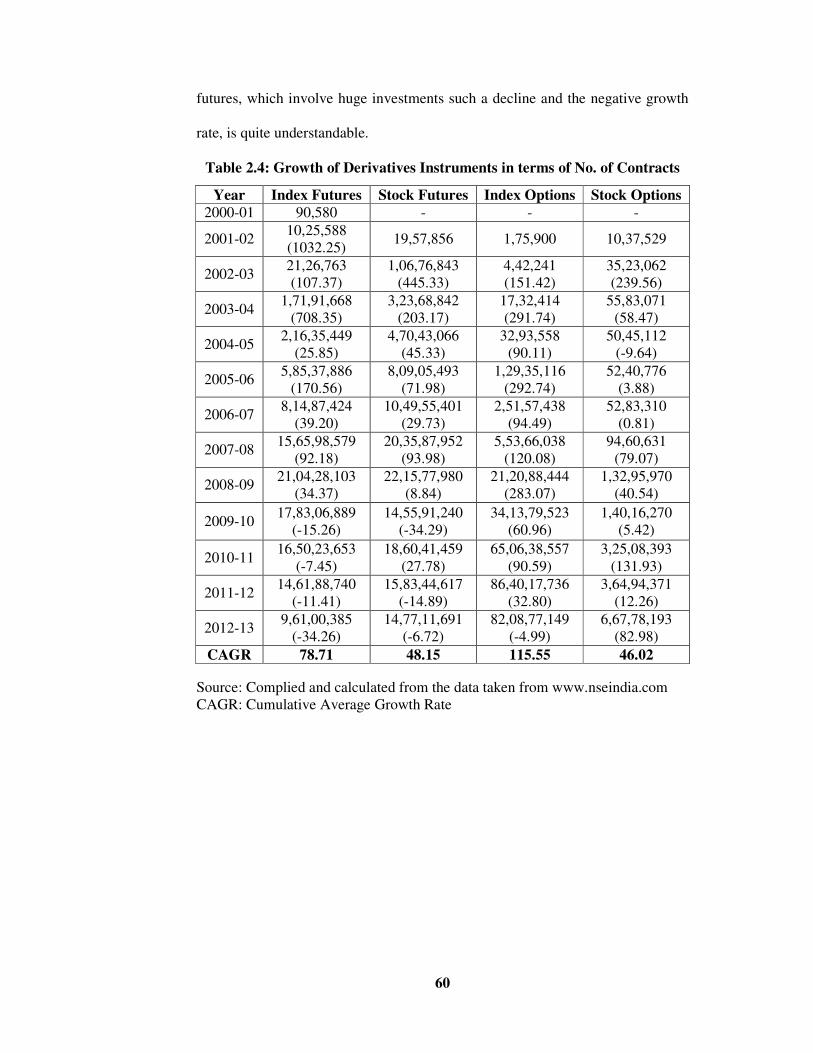

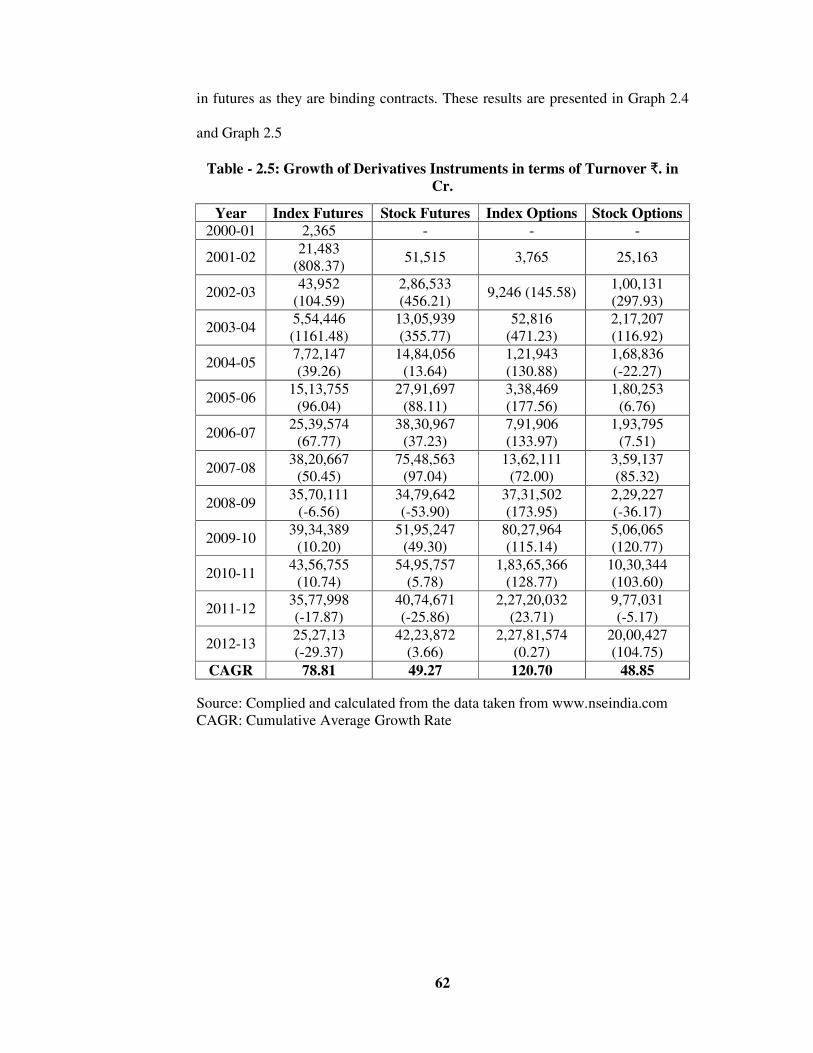

Table 2.4 and 2.5 depicts the growth in number of contracts traded and

turnover for the four major derivative instruments which are also the instruments

covered under the present study – Index Futures, Stock Futures, Index Options

and Stock Options. Instrument-wise, it is observed that stock options have

registered the highest growth rate in 2012-13, in terms of number of contracts and

turnover. The growth rate in this instrument was 82.98 per cent and 104.75 per

cent respectively. The lowest growth rate was registered in Index Futures. In fact,

the growth rate in this instrument started registering negative trend in terms of

number of contracts traded from 2009-10 in which year the growth rate was -

15.26 per cent and by the end of the study period it came down to -34.26 per cent.

In terms of turnover, the negative growth rate registered in this instrument was -

29.37 per cent in 2012-13. Futures being binding contracts and especially Index

0.00

20.00

40.00

60.00

80.00

100.00

120.00R

ate

of

Gro

wth

Time Period

Growth of Cash and Derivatives markets

Cash Market Derivatives Market

60

futures, which involve huge investments such a decline and the negative growth

rate, is quite understandable.

Table 2.4: Growth of Derivatives Instruments in terms of No. of Contracts

Year Index Futures Stock Futures Index Options Stock Options

2000-01 90,580 - - -

2001-02 10,25,588

(1032.25) 19,57,856 1,75,900 10,37,529

2002-03 21,26,763

(107.37)

1,06,76,843

(445.33)

4,42,241

(151.42)

35,23,062

(239.56)

2003-04 1,71,91,668

(708.35)

3,23,68,842

(203.17)

17,32,414

(291.74)

55,83,071

(58.47)

2004-05 2,16,35,449

(25.85)

4,70,43,066

(45.33)

32,93,558

(90.11)

50,45,112

(-9.64)

2005-06 5,85,37,886

(170.56)

8,09,05,493

(71.98)

1,29,35,116

(292.74)

52,40,776

(3.88)

2006-07 8,14,87,424

(39.20)

10,49,55,401

(29.73)

2,51,57,438

(94.49)

52,83,310

(0.81)

2007-08 15,65,98,579

(92.18)

20,35,87,952

(93.98)

5,53,66,038

(120.08)

94,60,631

(79.07)

2008-09 21,04,28,103

(34.37)

22,15,77,980

(8.84)

21,20,88,444

(283.07)

1,32,95,970

(40.54)

2009-10 17,83,06,889

(-15.26)

14,55,91,240

(-34.29)

34,13,79,523

(60.96)

1,40,16,270

(5.42)

2010-11 16,50,23,653

(-7.45)

18,60,41,459

(27.78)

65,06,38,557

(90.59)

3,25,08,393

(131.93)

2011-12 14,61,88,740

(-11.41)

15,83,44,617

(-14.89)

86,40,17,736

(32.80)

3,64,94,371

(12.26)

2012-13 9,61,00,385

(-34.26)

14,77,11,691

(-6.72)

82,08,77,149

(-4.99)

6,67,78,193

(82.98)

CAGR 78.71 48.15 115.55 46.02

Source: Complied and calculated from the data taken from www.nseindia.com

CAGR: Cumulative Average Growth Rate

Graph 2.4: Percentage of Growth of Four Instruments in number of

Category-wise, the growth in options was higher than the growth in

Futures. While the growth rate in Index Options and Stock Options was 115.55

and 46.02 and 120.70 and 48.85 in terms of number of contracts traded and

turnover, the growth rate in Index futures and

and 78.81 and 49.27 in terms of number of contracts traded and turnover

respectively. Thus, the trading activity and frequency was found to be more in

options than in futures.

Another important observation is that in opti

have dominated the stock options in both number and value of contracts. But, in

futures, stock futures have dominated the Index futures. This is quite

understandable because by nature options contracts does not involve any

obligation and hence Index options

unexercised when it is not advantageous to the holder. This leverage is not there

-200

0

200

400

600

800

1000

1200

20

00

-01

20

01

-02

Ra

te o

f g

row

th

Percentage of growth of Four Instruments in terms of No of

61

Graph 2.4: Percentage of Growth of Four Instruments in number of

Contracts in NSE

wise, the growth in options was higher than the growth in

Futures. While the growth rate in Index Options and Stock Options was 115.55

and 46.02 and 120.70 and 48.85 in terms of number of contracts traded and

turnover, the growth rate in Index futures and stock futures was 78.71 and 48.15

and 78.81 and 49.27 in terms of number of contracts traded and turnover

respectively. Thus, the trading activity and frequency was found to be more in

futures.

Another important observation is that in options category Index Options

have dominated the stock options in both number and value of contracts. But, in

futures, stock futures have dominated the Index futures. This is quite

understandable because by nature options contracts does not involve any

tion and hence Index options which involve huge investments can be left

unexercised when it is not advantageous to the holder. This leverage is not there

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

Time Period

Percentage of growth of Four Instruments in terms of No of

contracts in NSE

Index Futures

Stock Futures

Index Options

Stock Options

Graph 2.4: Percentage of Growth of Four Instruments in number of

wise, the growth in options was higher than the growth in

Futures. While the growth rate in Index Options and Stock Options was 115.55

and 46.02 and 120.70 and 48.85 in terms of number of contracts traded and

stock futures was 78.71 and 48.15

and 78.81 and 49.27 in terms of number of contracts traded and turnover

respectively. Thus, the trading activity and frequency was found to be more in

ons category Index Options

have dominated the stock options in both number and value of contracts. But, in

futures, stock futures have dominated the Index futures. This is quite

understandable because by nature options contracts does not involve any

which involve huge investments can be left

unexercised when it is not advantageous to the holder. This leverage is not there

Percentage of growth of Four Instruments in terms of No of

Index Futures

Stock Futures

Index Options

Stock Options

62

in futures as they are binding contracts. These results are presented in Graph 2.4

and Graph 2.5

Table - 2.5: Growth of Derivatives Instruments in terms of Turnover �. in

Cr.

Year Index Futures Stock Futures Index Options Stock Options

2000-01 2,365 - - -

2001-02 21,483

(808.37) 51,515 3,765 25,163

2002-03 43,952

(104.59)

2,86,533

(456.21) 9,246 (145.58)

1,00,131

(297.93)

2003-04 5,54,446

(1161.48)

13,05,939

(355.77)

52,816

(471.23)

2,17,207

(116.92)

2004-05 7,72,147

(39.26)

14,84,056

(13.64)

1,21,943

(130.88)

1,68,836

(-22.27)

2005-06 15,13,755

(96.04)

27,91,697

(88.11)

3,38,469

(177.56)

1,80,253

(6.76)

2006-07 25,39,574

(67.77)

38,30,967

(37.23)

7,91,906

(133.97)

1,93,795

(7.51)

2007-08 38,20,667

(50.45)

75,48,563

(97.04)

13,62,111

(72.00)

3,59,137

(85.32)

2008-09 35,70,111

(-6.56)

34,79,642

(-53.90)

37,31,502

(173.95)

2,29,227

(-36.17)

2009-10 39,34,389

(10.20)

51,95,247

(49.30)

80,27,964

(115.14)

5,06,065

(120.77)

2010-11 43,56,755

(10.74)

54,95,757

(5.78)

1,83,65,366

(128.77)

10,30,344

(103.60)

2011-12 35,77,998

(-17.87)

40,74,671

(-25.86)

2,27,20,032

(23.71)

9,77,031

(-5.17)

2012-13 25,27,13

(-29.37)

42,23,872

(3.66)

2,27,81,574

(0.27)

20,00,427

(104.75)

CAGR 78.81 49.27 120.70 48.85

Source: Complied and calculated from the data taken from www.nseindia.com

CAGR: Cumulative Average Growth Rate

Graph2.5: Percentage of Growth of Four Instruments in terms of Turnover

Graph 2.6 shows an overview of the share of four derivative instruments

covered in the present study in terms of Turnover from the year of their inception

till 2012-13. It is clear from the graph that Index option

derivative instrument

Index Futures (18%

derivative instrument

futures from the point of view of the buyer (call or put) as

Hence, they have become

-200

0

200

400

600

800

1000

1200

20

00

-01

20

01

-02

Ra

te o

f g

row

th

Percentage of Growth of Four Instruments in terms of

63

Percentage of Growth of Four Instruments in terms of Turnover

(�. in Cr)

Graph 2.6 shows an overview of the share of four derivative instruments

in the present study in terms of Turnover from the year of their inception

13. It is clear from the graph that Index option is the

derivative instrument with 52 per cent share followed by stock futures (26%),

Index Futures (18%).Stock options with four per cent are the least preferred

derivative instruments. As stated earlier, by nature options have an

futures from the point of view of the buyer (call or put) as they are not obligatory.

have become the popular derivative instruments among the investors.

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

Time Period

Percentage of Growth of Four Instruments in terms of

Turnover in NSE

Index Futures

Stock Futures

Index Options

Stock Options

Percentage of Growth of Four Instruments in terms of Turnover

Graph 2.6 shows an overview of the share of four derivative instruments

in the present study in terms of Turnover from the year of their inception

the dominating

with 52 per cent share followed by stock futures (26%),

per cent are the least preferred

edge over the

are not obligatory.

the popular derivative instruments among the investors.

Percentage of Growth of Four Instruments in terms of

Index Futures

Stock Futures

Index Options

Stock Options

Graph 2.6: Share of Derivatives Instruments in Turnover (

Source:compiledfrom the data taken from

Table 2.6 exhibits the data on the role of National Stock Exchange vis

vis the top five derivative exchanges in the world in terms of contracts traded

(volume of transactions) in options and futures category. In the Index Options

segment, the National Stock Exchange has occupied the second position in the

world with 820 million contracts traded in 2012. Korean exchange was in the first

position with 1575 million contracts. In the stock options segment, NSE is not

figured in the top five e

Stock Exchange occupied fourth and fifth positions in stock and Index futures

respectively. Surprisingly the three instruments in which the NSE figured in the

top five exchanges in the world,

compared to the previous year.

Index Options

52%

Share of Derivatives Instruments in Turnover (

over the years from 2000

64

Share of Derivatives Instruments in Turnover (�. in Cr.) over the

years from 2000-01 to 2012-13

compiledfrom the data taken from www.nseindia.com

Table 2.6 exhibits the data on the role of National Stock Exchange vis

derivative exchanges in the world in terms of contracts traded

(volume of transactions) in options and futures category. In the Index Options

, the National Stock Exchange has occupied the second position in the

world with 820 million contracts traded in 2012. Korean exchange was in the first

position with 1575 million contracts. In the stock options segment, NSE is not

figured in the top five exchanges in the world. In the Futures category, National

Stock Exchange occupied fourth and fifth positions in stock and Index futures

respectively. Surprisingly the three instruments in which the NSE figured in the

top five exchanges in the world, there is decline in number of contracts traded

compared to the previous year.

Index Futures

18%

Stock Futures

26%

Index Options

Stock Options

4%

Share of Derivatives Instruments in Turnover (�. in Cr.)

over the years from 2000-01 to 2012-13

in Cr.) over the

Table 2.6 exhibits the data on the role of National Stock Exchange vis-à-

derivative exchanges in the world in terms of contracts traded

(volume of transactions) in options and futures category. In the Index Options

, the National Stock Exchange has occupied the second position in the

world with 820 million contracts traded in 2012. Korean exchange was in the first

position with 1575 million contracts. In the stock options segment, NSE is not

xchanges in the world. In the Futures category, National

Stock Exchange occupied fourth and fifth positions in stock and Index futures

respectively. Surprisingly the three instruments in which the NSE figured in the

number of contracts traded

Stock Futures

in Cr.)

65

Table 2.6: Status of National Stock Exchange in the top 5 Derivative

Exchanges in the World (Instrument-wise)

Top 5 Exchanges by number of Index option contracts traded in 2012 (in

million)

Rank Exchange 2012

(inmilns)

2012/2011 growth

rate (in %)

1 Korea Exchange 1575 -57.10

2 National Stock Exchange India 820 -5.90

3 EUREX 383 -18.30

4 Chicago Board Options Exchange 304 -5.00

5 Bombay Stock Exchange 235 0.00

Top 5 Exchanges by number of Stock Future contracts traded in 2012

(in millions)

1 NYSE Liffe Europe 247 -1.60

2 MICEX / RTS 241 -33.40

3 EUREX 196 12.60

4 National Stock Exchange India 153 -4.80

5 Korea Exchange 100 67.60

Top 5 Exchanges by number of Index futures contracts traded in 2012

(in millions)

1 CME Group 588 -20.00

2 EUREX 384 -21.10

3 MICEX / RTS 323 -15.40

4 Osaka SE 150 9.30

5 National Stock Exchange India 112 -27.90

Top 5 Exchanges by number of Stock Option contracts traded in 2012

(in millions)

1 BM&FBOVESPA 929 10.90

2 NASDAQ OMX (US) 639 -8.80

3 NYSE Euronext (US) 595 -6.20

4 Chicago Board Options Exchange 494 -4.20

5 International Securities Exchange 457 6.00

Source: WFE Market Highlights 2012 from www.world-exchanges.org

66

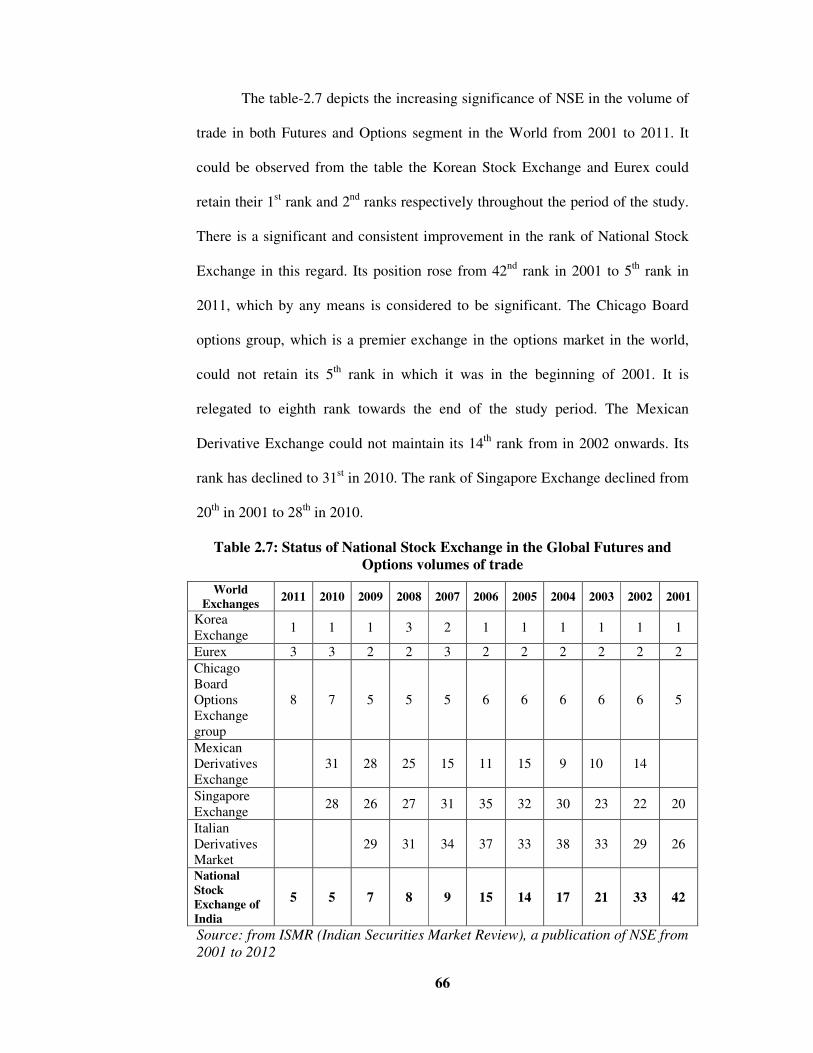

The table-2.7 depicts the increasing significance of NSE in the volume of

trade in both Futures and Options segment in the World from 2001 to 2011. It

could be observed from the table the Korean Stock Exchange and Eurex could

retain their 1st rank and 2

nd ranks respectively throughout the period of the study.

There is a significant and consistent improvement in the rank of National Stock

Exchange in this regard. Its position rose from 42nd

rank in 2001 to 5th

rank in

2011, which by any means is considered to be significant. The Chicago Board

options group, which is a premier exchange in the options market in the world,

could not retain its 5th

rank in which it was in the beginning of 2001. It is

relegated to eighth rank towards the end of the study period. The Mexican

Derivative Exchange could not maintain its 14th

rank from in 2002 onwards. Its

rank has declined to 31st in 2010. The rank of Singapore Exchange declined from

20th

in 2001 to 28th

in 2010.

Table 2.7: Status of National Stock Exchange in the Global Futures and

Options volumes of trade

World

Exchanges 2011 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001

Korea

Exchange 1 1 1 3 2 1 1 1 1 1 1

Eurex 3 3 2 2 3 2 2 2 2 2 2

Chicago

Board

Options

Exchange

group

8 7 5 5 5 6 6 6 6 6 5

Mexican

Derivatives

Exchange

31 28 25 15 11 15 9 10 14

Singapore

Exchange 28 26 27 31 35 32 30 23 22 20

Italian

Derivatives

Market

29 31 34 37 33 38 33 29 26

National

Stock

Exchange of

India

5 5 7 8 9 15 14 17 21 33 42

Source: from ISMR (Indian Securities Market Review), a publication of NSE from

2001 to 2012

67

As depicted in Table 2.8, at present Futures and Options trading is in

operation in 17 Indices in India. Out of these, S&P CNX NIFTY and BSE

SENSEX are the two comprehensive/ broad based Indices. Out of these two, the

turnover of NSE’s S&P CNX NIFTY in F&O segment is about 33 times higher

than that of SENSEX. The present study, which focuses on trading of derivatives

in NSE, assumes significance from this respect also.

Table 2.8: Benchmark Indices in F&O Segment in India as on 2011-12

S.

No Derivative Products on Indices

Turnover

(�. in cr)

1 S&P CNX Nifty Futures & Options 2,62,98,030

2 CNX IT Future & Options 2,162

3 Bank Nifty Futures & Options 5,14,284

4 NIFTY Midcap 50 Futures & Options 264

5 MININIFTY Futures & Options 1,53,763

6 Long term Options on S&P CNX NIFTY (LEAPS) 16,998

7 Dow Jones Industry Average (DJIA) 14,865

8 S&P 500 NA

9 CNXPSE 83

10 CNXINFRA 125

11 FTSE 100 NA

12 BSE SENSEX Futures & Options 7,96,792

13 SENSEX MINI Futures & Options NA

14 BSE TECK Futures & Options NA

15 BSE BANKEX Futures & Options NA

16 BSE OIL & GAS Futures & Options NA

17 BRICSMART indices NA

Source: compiled from data taken from www.nseindia.com and

www.bseindia.com

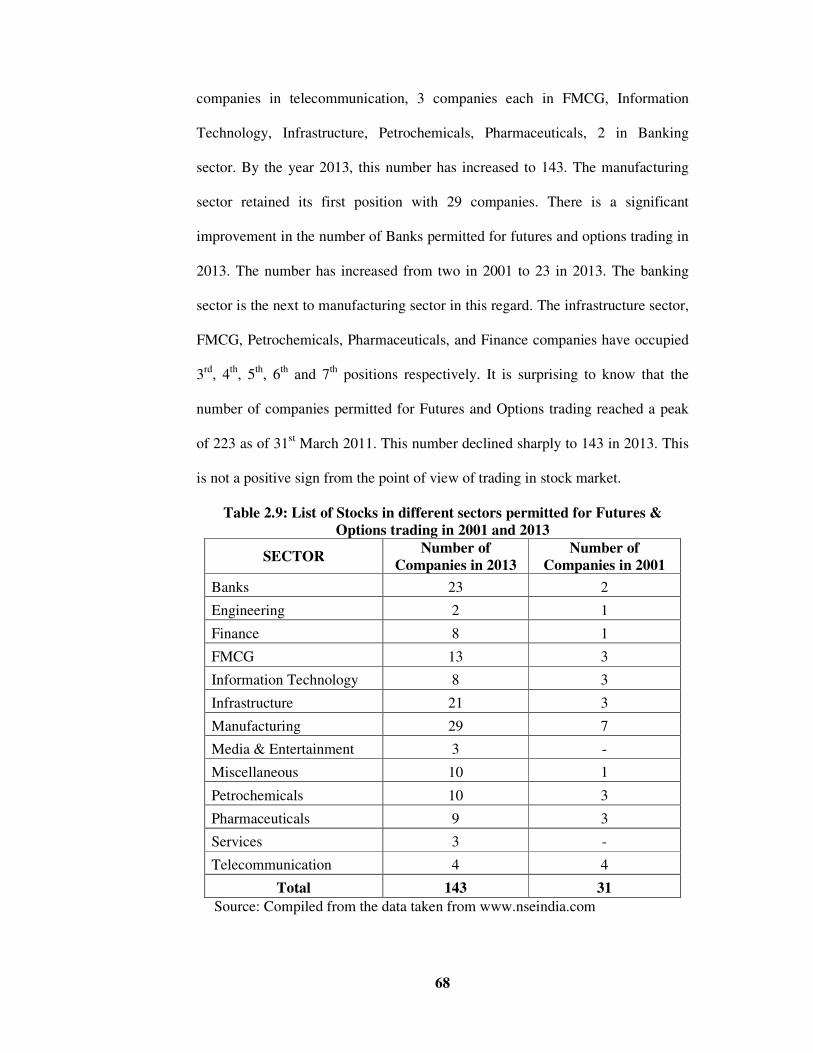

Table 2.9 presents the data on the number of companies permitted for

Futures and Options trading at the time of introduction of derivatives i.e. in 2001

and the number of companies permitted for Futures and Options trading in 2013.

It is clear from the table that only 31 companies could fulfil the criteria laid down

by SEBI in 2001. Out of these 7 companies are in manufacturing sector, 4

68

companies in telecommunication, 3 companies each in FMCG, Information

Technology, Infrastructure, Petrochemicals, Pharmaceuticals, 2 in Banking

sector. By the year 2013, this number has increased to 143. The manufacturing

sector retained its first position with 29 companies. There is a significant

improvement in the number of Banks permitted for futures and options trading in

2013. The number has increased from two in 2001 to 23 in 2013. The banking

sector is the next to manufacturing sector in this regard. The infrastructure sector,

FMCG, Petrochemicals, Pharmaceuticals, and Finance companies have occupied

3rd

, 4th

, 5th

, 6th

and 7th

positions respectively. It is surprising to know that the

number of companies permitted for Futures and Options trading reached a peak

of 223 as of 31st March 2011. This number declined sharply to 143 in 2013. This

is not a positive sign from the point of view of trading in stock market.

Table 2.9: List of Stocks in different sectors permitted for Futures &

Options trading in 2001 and 2013

SECTOR Number of

Companies in 2013

Number of

Companies in 2001

Banks 23 2

Engineering 2 1

Finance 8 1

FMCG 13 3

Information Technology 8 3

Infrastructure 21 3

Manufacturing 29 7

Media & Entertainment 3 -

Miscellaneous 10 1

Petrochemicals 10 3

Pharmaceuticals 9 3

Services 3 -

Telecommunication 4 4

Total 143 31

Source: Compiled from the data taken from www.nseindia.com

69

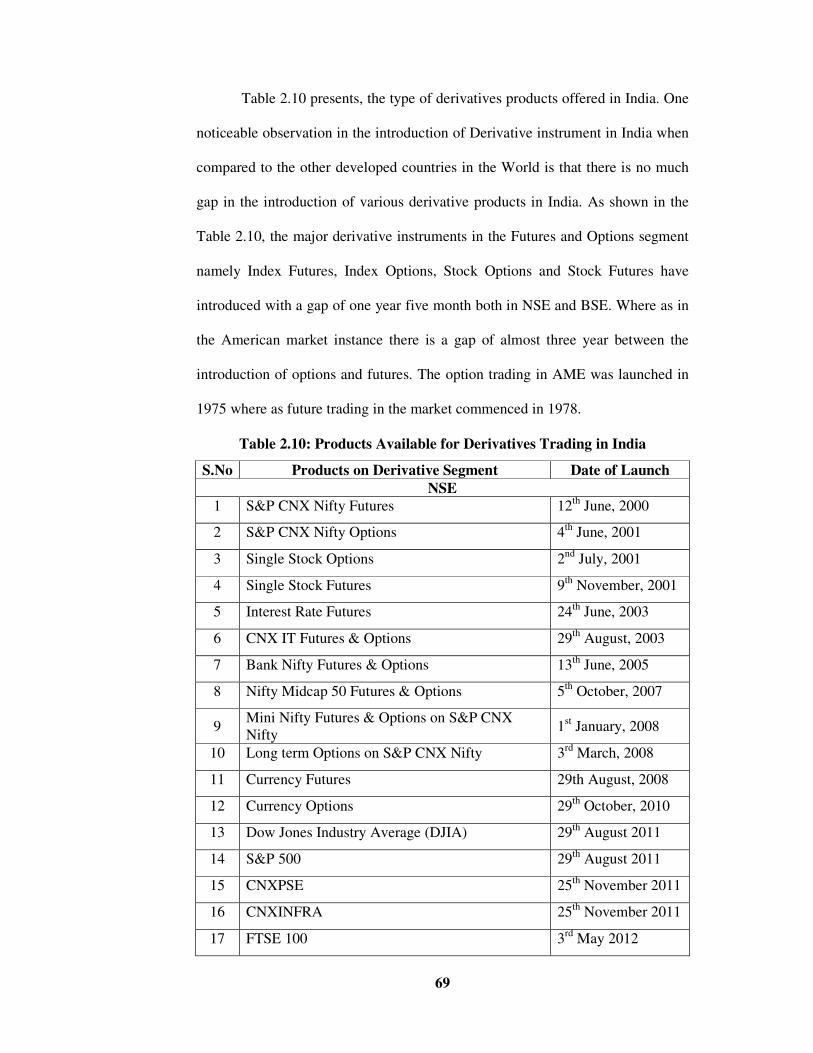

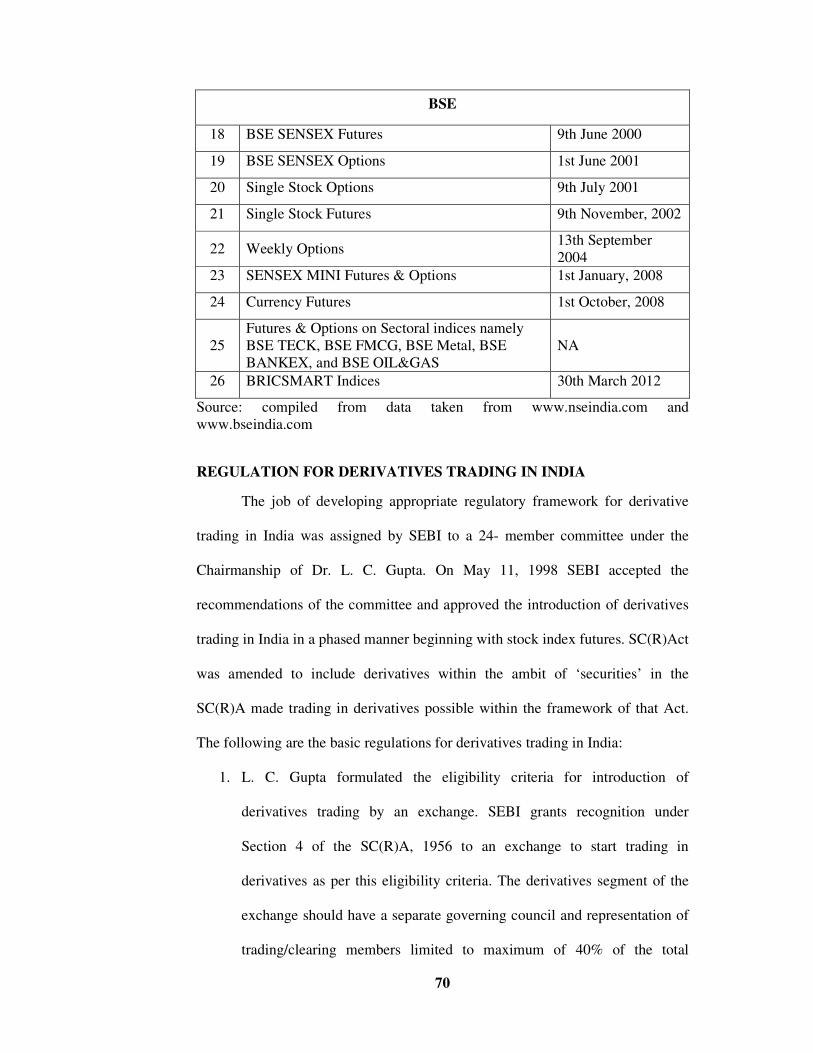

Table 2.10 presents, the type of derivatives products offered in India. One

noticeable observation in the introduction of Derivative instrument in India when

compared to the other developed countries in the World is that there is no much

gap in the introduction of various derivative products in India. As shown in the

Table 2.10, the major derivative instruments in the Futures and Options segment

namely Index Futures, Index Options, Stock Options and Stock Futures have

introduced with a gap of one year five month both in NSE and BSE. Where as in

the American market instance there is a gap of almost three year between the

introduction of options and futures. The option trading in AME was launched in

1975 where as future trading in the market commenced in 1978.

Table 2.10: Products Available for Derivatives Trading in India

S.No Products on Derivative Segment Date of Launch

NSE

1 S&P CNX Nifty Futures 12th

June, 2000

2 S&P CNX Nifty Options 4th

June, 2001

3 Single Stock Options 2nd

July, 2001

4 Single Stock Futures 9th

November, 2001

5 Interest Rate Futures 24th

June, 2003

6 CNX IT Futures & Options 29th

August, 2003

7 Bank Nifty Futures & Options 13th

June, 2005

8 Nifty Midcap 50 Futures & Options 5th

October, 2007

9 Mini Nifty Futures & Options on S&P CNX

Nifty 1

st January, 2008

10 Long term Options on S&P CNX Nifty 3rd

March, 2008

11 Currency Futures 29th August, 2008

12 Currency Options 29th

October, 2010

13 Dow Jones Industry Average (DJIA) 29th

August 2011

14 S&P 500 29th

August 2011

15 CNXPSE 25th

November 2011

16 CNXINFRA 25th

November 2011

17 FTSE 100 3rd

May 2012

70

BSE

18 BSE SENSEX Futures 9th June 2000

19 BSE SENSEX Options 1st June 2001

20 Single Stock Options 9th July 2001

21 Single Stock Futures 9th November, 2002

22 Weekly Options 13th September

2004

23 SENSEX MINI Futures & Options 1st January, 2008

24 Currency Futures 1st October, 2008

25

Futures & Options on Sectoral indices namely

BSE TECK, BSE FMCG, BSE Metal, BSE

BANKEX, and BSE OIL&GAS

NA

26 BRICSMART Indices 30th March 2012

Source: compiled from data taken from www.nseindia.com and

www.bseindia.com

REGULATION FOR DERIVATIVES TRADING IN INDIA

The job of developing appropriate regulatory framework for derivative

trading in India was assigned by SEBI to a 24- member committee under the

Chairmanship of Dr. L. C. Gupta. On May 11, 1998 SEBI accepted the

recommendations of the committee and approved the introduction of derivatives

trading in India in a phased manner beginning with stock index futures. SC(R)Act

was amended to include derivatives within the ambit of ‘securities’ in the

SC(R)A made trading in derivatives possible within the framework of that Act.

The following are the basic regulations for derivatives trading in India:

1. L. C. Gupta formulated the eligibility criteria for introduction of

derivatives trading by an exchange. SEBI grants recognition under

Section 4 of the SC(R)A, 1956 to an exchange to start trading in

derivatives as per this eligibility criteria. The derivatives segment of the

exchange should have a separate governing council and representation of

trading/clearing members limited to maximum of 40% of the total

71

members of the governing council. As per the criteria, the exchange

would have to regulate the sales practices of its members and would have

to obtain prior approval of SEBI before start of trading in any derivative

contract.

2. The Exchange should have minimum 50 members.

3. The members of an existing segment (cash segment) of the exchange

would not automatically become the members of derivative segment. The

members of the derivative segment would need to fulfil the eligibility

conditions separately as laid down by the L. C. Gupta committee.

4. The clearing and settlement of derivatives trades would be through a

SEBI approved clearing corporation/house. Clearing corporations/houses

complying with the eligibility conditions as laid down by the committee

have to apply to SEBI for grant of approval.

5. Derivative brokers/dealers and clearing members are required to seek

registration from SEBI. This is in addition to their registration as brokers

of existing stock exchanges. The minimum net worth for clearing

members of the derivatives clearing corporation/house shall be �.300

Lakh. The net worth of the member shall be computed as follows:

6. Capital + Free reserves Less non-allowable assets viz.,

a) Fixed assets

b) Pledged securities

c) Member’s card

d) Non-allowable securities (unlisted securities)

e) Bad deliveries

f) Doubtful debts and advances

g) Prepaid expenses

h) Intangible assets

72

i) 30% marketable securities

7. The minimum contract value shall not be less than �.2 Lakh. Exchanges

have to submit details of the futures contract they propose to introduce.

8. The initial margin requirement, exposure limits linked to capital adequacy

and margin demands related to the risk of loss on the position will be

prescribed by SEBI/Exchange from time to time.

9. The L. C. Gupta committee report requires strict enforcement of “Know

your customer” rule and requires that every client shall be registered with

the derivatives broker. The members of the derivatives segment are also

required to make their clients aware of the risks involved in derivatives

trading by issuing to the client the Risk Disclosure Document and obtain a

copy of the same duly signed by the client. The trading members are

required to have qualified approved user and sales person who have

passed a certification programme approved by SEBI.

ELIGIBILITY CRITERIA FOR SELECTION OF SECURITIES AND

INDICES FOR DERIVATIVES TRADING

The eligibility of a stock / index for trading in Derivatives segment is

based upon the criteria laid down by SEBI through various circulars issued from

time to time. Based on SEBI guidelines and as a surveillance measure, following

criteria has been adopted by the Exchange for selecting stocks and indices on

which Futures & Options contracts would be introduced.

ELIGIBILITY CRITERIA OF STOCKS:

(i) The stock shall be chosen from amongst the top 500 stocks in terms of

average daily market capitalisation and average daily traded value in the

previous six months on a rolling basis.

73

(ii) The stock's median quarter-sigma order size over the last six months

shall be not less than �.10 lakhs. For this purpose, a stock's quarter-

sigma order size shall mean the order size (in value terms) required to

cause a change in the stock price equal to one-quarter of a standard

deviation.

(iii) The market wide position limit in the stock shall not be less than �.300

crores. The market wide position limit (number of shares) shall be

valued taking the closing prices of stocks in the underlying cash market

on the date of expiry of contract in the month. The market wide position

limit of open position (in terms of the number of underlying stock) on

futures and option contracts on a particular underlying stock shall be

20% of the number of shares held by non-promoters in the relevant

underlying security i.e. free-float holding.

Continued Eligibility :

For an existing F&O stock, the continued eligibility criteria is that market

wide position limit in the stock shall not be less than �.200 crores and stock's

median quarter-sigma order size over the last six months shall not be less than �.5

lakhs. Additionally, the stock’s average monthly turnover in derivative segment

over last three months shall not be less than �.100 crores.

(i) If an existing security fails to meet the eligibility criteria for three

months consecutively, then no fresh month contract shall be issued on

that security. However, the existing unexpired contracts may be

permitted to trade till expiry and new strikes may also be introduced

in the existing contract months.

74

(ii) Further, the members may also refer to circular no.

NSCC/F&O/C&S/365 dated August 26, 2004, issued by NSCCL

regarding Market Wide Position Limit, wherein it is clarified that a

stock which has remained subject to a ban on new position for a

significant part of the month consistently for three months, shall be

phased out from trading in the F&O segment.

Further, once the stock is excluded from the F&O list, it shall not be

considered for re-inclusion for a period of one year.

Re-introduction of excluded stocks

A stock which is excluded from derivatives trading may become eligible

once again. In such instances, the stock is required to fulfil the eligibility criteria

for three consecutive months to be re-introduced for derivatives trading.

ELIGIBILITY CRITERIA OF INDICES

i. Futures & Options contracts on an index can be introduced only if

80% of the index constituents are individually eligible for derivatives

trading. However, no single ineligible stock in the index shall have a

weightage of more than 5% in the index. The index on which futures

and options contracts are permitted shall be required to comply with

the eligibility criteria on a continuous basis.

ii. SEBI has subsequently modified the above criteria, vide its

clarification issued to the Exchange "The Exchange may consider

introducing derivative contracts on an index if the stocks contributing

to 80% weightage of the index are individually eligible for derivative

trading. However, no single ineligible stocks in the index shall have a

weightage of more than 5% in the index.

75

iii. The above criteria is applied every month, if the index fails to meet

the eligibility criteria for three months consecutively, then no fresh

month contract shall be issued on that index, However, the existing

unexpired contacts shall be permitted to trade till expiry and new

strikes may also be introduced in the existing contracts.

PROF. J. R. VARMA COMMITTEE

In June 1998, SEBI set up a committee under the chairmanship of Prof

J.R. Varma, to recommend measures for risk containment in derivatives market

in India. This committee submitted its report in October 1998 giving operational

details of margining system, methodology for charging initial margins, broker net

worth, deposit requirement and real-time monitoring requirement.

The following procedure is adopted for calculating the Quarter Sigma Order

Size:

• The applicable VAR (Value at Risk) is calculated for each security

based on the J.R. Varma Committee guidelines. (The formula

suggested by J. R. Varma for computation of VAR for margin

calculation is statistically known as 'Exponentially weighted moving

average (EWMA)' method. In comparison to the traditional method,

EWMA has the advantage of giving more weight to the recent price

movements and less weight to the historical price movements.)

• Such computed VAR is a value (like 0.03), which is also called

standard deviation or Sigma. (The meaning of this figure is that the

security has the probability to move 3% to the lower side or 3% to the

upper side on the next trading day from the current closing price of the

security).

76

• Such arrived at standard deviation (one sigma), is multiplied by 0.25

to arrive at the quarter sigma

• From the order snapshots (taken four times a day from NSE's Capital

Market Segment order book) the average of best buy price and best

sell price is computed which is called the average price.

• The quarter sigma is then multiplied with the average price to arrive at

quarter sigma price.

• Based on the order snapshot, the value of the order (order size in �.),

which will move the price of the security by quarter sigma price in

buy and sell side is computed. The value of such order size is called

Quarter Sigma order size. Such an exercise is carried out for four

order snapshots per day for all stocks for the previous six months

period.

• From the above determined quarter sigma order size (�.) for each

order book snap shot for each security, the median of the order sizes

(�.) for buy side and sell side separately, are computed for all the

order snapshots taken together for the last six months.

• The average of the median order sizes for buy and sell side are taken

as the median quarter sigma order size for the security.

Futures & Options contracts may be introduced on new securities which

meet the above mentioned eligibility criteria, subject to approval by SEBI.

New securities being introduced in the F&O segment are based on the

eligibility criteria which take into consideration average daily market

capitalization, average daily traded value, the market wide position limit in the

security, the quarter sigma values and as approved by SEBI. The average daily

77

market capitalisation and the average daily traded value would be computed on

the 15th of each month, on a rolling basis, to arrive at the list of top 500

securities. Similarly, the quarter sigma order size in a stock would also be

calculated on the 15th

of each month, on a rolling basis, considering the order

book snap shots of securities in the previous six months and the market wide

position limit (number of shares) shall be valued taking the closing prices of

stocks in the underlying cash market on the date of expiry of contract in the

month.

The number of eligible securities may vary from month to month

depending upon the changes in quarter sigma order sizes, average daily market

capitalisation & average daily traded value calculated every month on a rolling

basis for the past six months and the market wide position limit in that security.

Related Documents

![[Derivatives Consulting Group] Introduction to Equity Derivatives](https://static.cupdf.com/doc/110x72/5525eed15503467c6f8b4b12/derivatives-consulting-group-introduction-to-equity-derivatives.jpg)