GROUP MEMBER GROUP MEMBER HENRY EBUN - 801984 HENRY EBUN - 801984 ASMARAH RIKUN - 801979 ASMARAH RIKUN - 801979 NOORINA ABD HAMID - 805015 NOORINA ABD HAMID - 805015 BUDIRMAN DAUD - 805014 BUDIRMAN DAUD - 805014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

GROUP MEMBERGROUP MEMBERGROUP MEMBERGROUP MEMBER

HENRY EBUN - 801984HENRY EBUN - 801984ASMARAH RIKUN - 801979ASMARAH RIKUN - 801979

NOORINA ABD HAMID - 805015NOORINA ABD HAMID - 805015BUDIRMAN DAUD - 805014BUDIRMAN DAUD - 805014

Capital Structure: Basic Concepts

Chapter 15

Chapter outline

15.1 The capital structure question and the pie theory.

15.2 Maximizing Firm value Vs Maximizing Stockholder Interests.

15.3 Financial Leverage and Firm Value: An Example.

15.4 Modigliani and Miler:Proposition II (No Taxes).15.5 Taxes.

Question And Answer

15.1 The Capital Structure Question and The Pie Theory

Definition: Capital Structure is the mix of financial securities used to finance the firm.

The value of a firm is defined to be the sum of the value of the firm’s debt and the firm’s equity.

V = B + S If the goal of the management of the firm is to make the firm as

valuable as possible, then the firm should pick the debt-equity ratio that makes the pie as big as possible.

SBS Value of the FirmS

15.2 M&M No Tax: Result

A change in capital structure does not matter to the overall value of the firm.

Total Firm Value = S+BDoes not change (the pie is the same size in each case, just the slices are different).

Equity,$1000,100%

Equity,$700,70%,

Debt$300,30%,

Equity,$400,40%,

Debt$600,60%,

There are really two important questions:1. Why should the stockholders care about maximizing firm value? Perhaps they should be interested in strategies that maximize shareholder value.

2. What is the ratio of debt-to-equity that maximizes the shareholder’s value?

As it turns out, changes in capital structure benefit the stockholders if and only if the value of the firm increases.

Note: When we talk about a change in capital structure, we usually hold other things constant. Thus, an increase in debt financing implies that equity will be repurchased (and vice versa) so that overall assets remain unchanged.

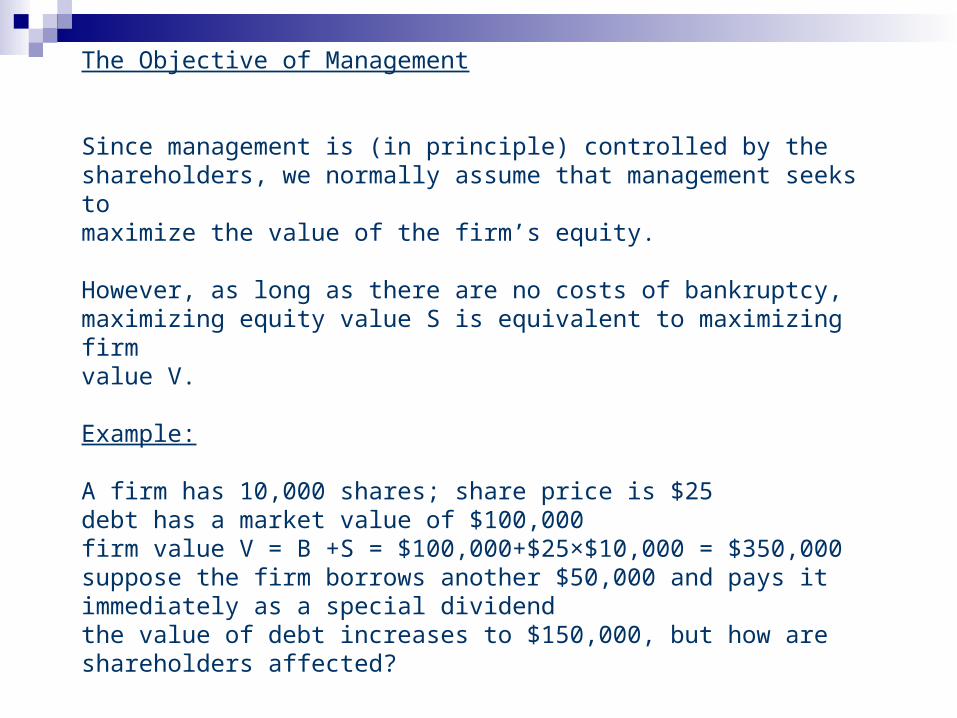

The Objective of Management

Since management is (in principle) controlled by theshareholders, we normally assume that management seeks tomaximize the value of the firm’s equity.

However, as long as there are no costs of bankruptcy,maximizing equity value S is equivalent to maximizing firmvalue V.

Example:

A firm has 10,000 shares; share price is $25debt has a market value of $100,000firm value V = B +S = $100,000+$25×$10,000 = $350,000suppose the firm borrows another $50,000 and pays itimmediately as a special dividendthe value of debt increases to $150,000, but how areshareholders affected?

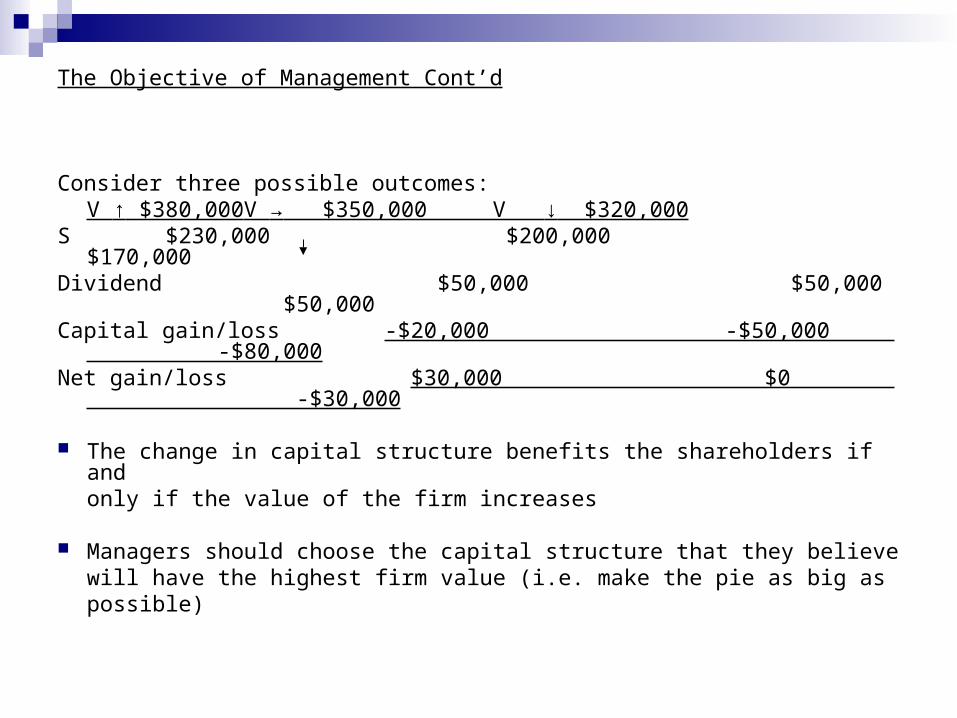

The Objective of Management Cont’d

Consider three possible outcomes:V ↑ $380,000 V → $350,000 V ↓ $320,000

S $230,000 $200,000 $170,000

Dividend $50,000 $50,000 $50,000Capital gain/loss -$20,000 -$50,000 -$80,000Net gain/loss $30,000 $0 -$30,000

The change in capital structure benefits the shareholders if andonly if the value of the firm increases

Managers should choose the capital structure that they believewill have the highest firm value (i.e. make the pie as big aspossible)

CurrentAssets $8000 $8000Debt $0 $4000Equity $8000 $4000Interest rate 10% 10%Market value/share $20 $20Shares outstanding 400 200

Proposed

Consider an all-equity firm that is contemplating going into debt. (Maybe some of the original shareholders want to cash out.)

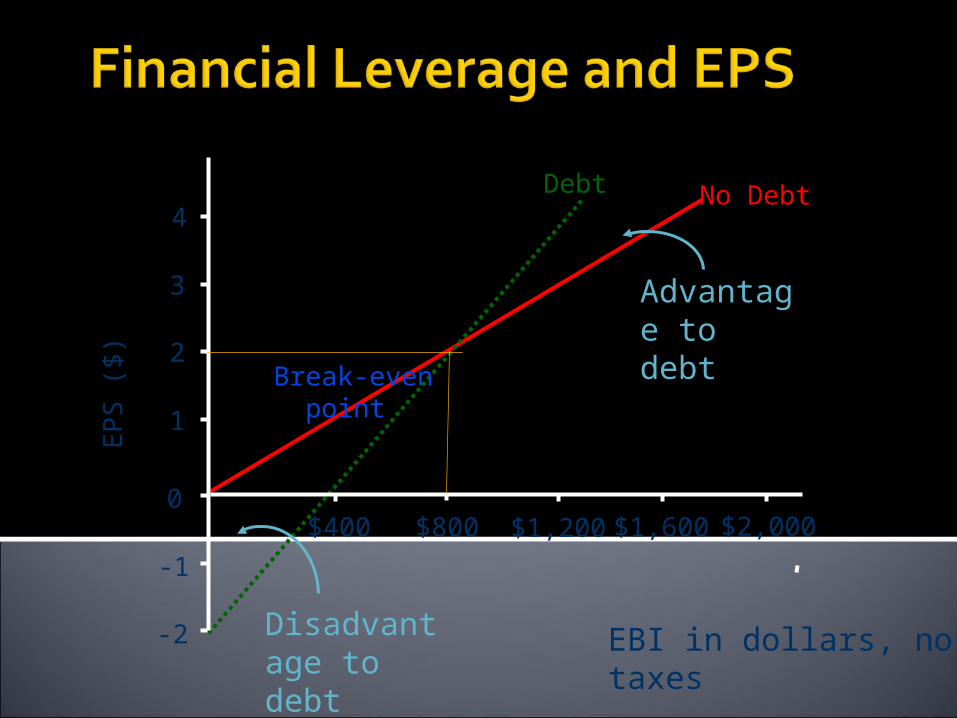

RecessionExpectedExpansionROA 5% 15% 25%Earnings $400 $1,200 $2,000ROE 5% 15% 25%EPS $1 $3 $5

Debt = $4,000

RecessionExpected ExpansionROA 5% 15% 25%EBI $400 $1,200 $2,000Interest -400 -400 -400EAI $0 $800 $1,600ROE 0 20% 40%EPS 0 $4 $8

-2

-1

0

1

2

3

4

$400 $800 $1,600

EP

S (

$)

Debt No Debt

Break-even point

EBI in dollars, no taxes

Advantage to debt

Disadvantage to debt

$1,200 $2,000

Strategy A: Buy 100 Shares of Levered Equity

RecessionExpected ExpansionEPS $0 $4 $8Earnings 0 400 800

Initial cost = 100 shares@$20/share=$200

• MM Proposition I (No Taxes)

Strategy B: Homemade Leverage

RecessionExpected ExpansionEPS 200 600 1,000Interest -200 -200 -200

Net earnings $0 $400 $800 Initial cost = 200 shares@$20/share $2,000 = $2,000

15.4 MM PROPOSITION II 15.4 MM PROPOSITION II (NO TAXES)(NO TAXES)

Proposition IIProposition IILeverage increases the risk and return to stockholdersLeverage increases the risk and return to stockholders

RRS S = R= ROO + (B/S + (B/SLL) (R) (ROO-R-RBB))

RRBB is the interest rate (cost of debt) is the interest rate (cost of debt)RRSS is the return on (levered) equity (cost of equity) is the return on (levered) equity (cost of equity)RROO is the return on unlevered equity (cost of capital) is the return on unlevered equity (cost of capital)B is the value of debtB is the value of debtSSLL is the value of levered equity is the value of levered equity

A higher debt-to- equity ratio leads to a higher required A higher debt-to- equity ratio leads to a higher required return on equity, because of the higher risk involved for return on equity, because of the higher risk involved for equity-holders in a company with debt. The formula is equity-holders in a company with debt. The formula is derived from the theory of Weighted Average Cost of derived from the theory of Weighted Average Cost of Capital (WACC)Capital (WACC)

The derivation is straightforward:The derivation is straightforward:RRWACCWACC= S/B + S x R= S/B + S x RSS + B/B + S x R + B/B + S x RBB

Where Where

RRBB is the cost of debtis the cost of debt

RRSS is the expected return on equity or stock, also called the cost of equity or the required return is the expected return on equity or stock, also called the cost of equity or the required return on equityon equity

RRWACCWACC

is the firm’s weighted average cost of capitalis the firm’s weighted average cost of capital

BB is the value of the firm’s debt or bondsis the value of the firm’s debt or bonds

SS is the value of the firm’s stock or equityis the value of the firm’s stock or equity

A firm’s weighted average cost of capital is a weighted average of its cost ofA firm’s weighted average cost of capital is a weighted average of its cost of

debt and its cost of equity. The weight applied to debt is proportion of thedebt and its cost of equity. The weight applied to debt is proportion of the

debt in the capital structure, and the weight applied to equity is the debt in the capital structure, and the weight applied to equity is the

proportion of equity in the capital structure.proportion of equity in the capital structure.

NoteNote: : RRWACCWACC means an average representing the expected return on all of a company’s securities, each means an average representing the expected return on all of a company’s securities, each source of capital, such as stocks bonds and other debt is weighted in the calculation according to its source of capital, such as stocks bonds and other debt is weighted in the calculation according to its prominence in the company’s capital structureprominence in the company’s capital structure

GRAPHGRAPHC

ost

of

capit

al :

R (

%)

R0

RS

RWAC

RBDebt – equity ratio (B/S)

RRSS == RROO + (R + (ROO – R – RBB) B/S) B/S

RRSS is the cost of equity is the cost of equity

RRBB is the cost of debt is the cost of debt

RROO is the cost of capital for an all-equity firm is the cost of capital for an all-equity firm

RRWACCWACC

is a firm’s weighted average cost of capital. In ais a firm’s weighted average cost of capital. In a

world with no taxes, Rworld with no taxes, RWACCWACC for a levered firm is equal to for a levered firm is equal to

RRO O

RROO is a single point whereas R is a single point whereas RSS, R, RBB and R and RWACCWACC are all are all

entire linesentire lines

Summary of MM Propositions without taxesSummary of MM Propositions without taxes

1.1. AssumptionsAssumptions -No taxes-No taxes -No transaction costs-No transaction costs -Individuals and corporations borrow at same rate-Individuals and corporations borrow at same rate

2.2. Results Results Proposition I = VProposition I = VLL = V = VUU (Value of levered firm equals value of unlevered (Value of levered firm equals value of unlevered

firm) firm) Proposition II = RProposition II = RSS = R = ROO = B / S (R = B / S (ROO–R–RBB))

3. Intuition3. Intuition Proposition I :Through homemade leverage individuals can either duplicate Proposition I :Through homemade leverage individuals can either duplicate

or undo the effects of corporate leverageor undo the effects of corporate leverage Proposition II : The cost of equity rises with leverage because the risk to Proposition II : The cost of equity rises with leverage because the risk to

equity rises with leverageequity rises with leverage

1. Tax definition : Tax is to impose a financial charge or other levy upon a taxpayer by a state or the functional equivalent of a state.

2. The value of the levered firm is the sum of the value of the debt and the value of the equity.

3. The firm value is positively related to debt within tax .

4. MM Proposition I (with corporate taxes) - Firm value increases with leverage : VL = Vu + TcB

VL is the value of a levered firm VU is the value of an un levered firm TCB is the present value of tax shield is the tax rate (TC) x the

value of debt (B)

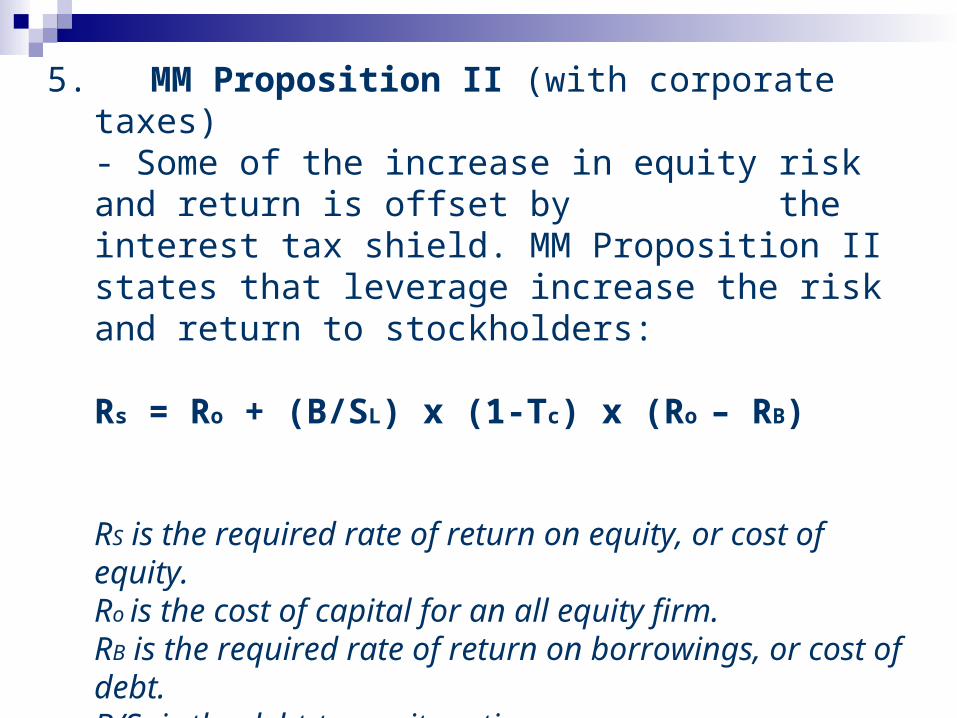

5. MM Proposition II (with corporate taxes)- Some of the increase in equity risk and return is offset by the interest tax shield. MM Proposition II states that leverage increase the risk and return to stockholders:

Rs = Ro + (B/SL) x (1-Tc) x (Ro – RB)

RS is the required rate of return on equity, or cost of equity.Ro is the cost of capital for an all equity firm.RB is the required rate of return on borrowings, or cost of debt.B/SL is the debt-to-equity ratio.Tc is the tax rate.

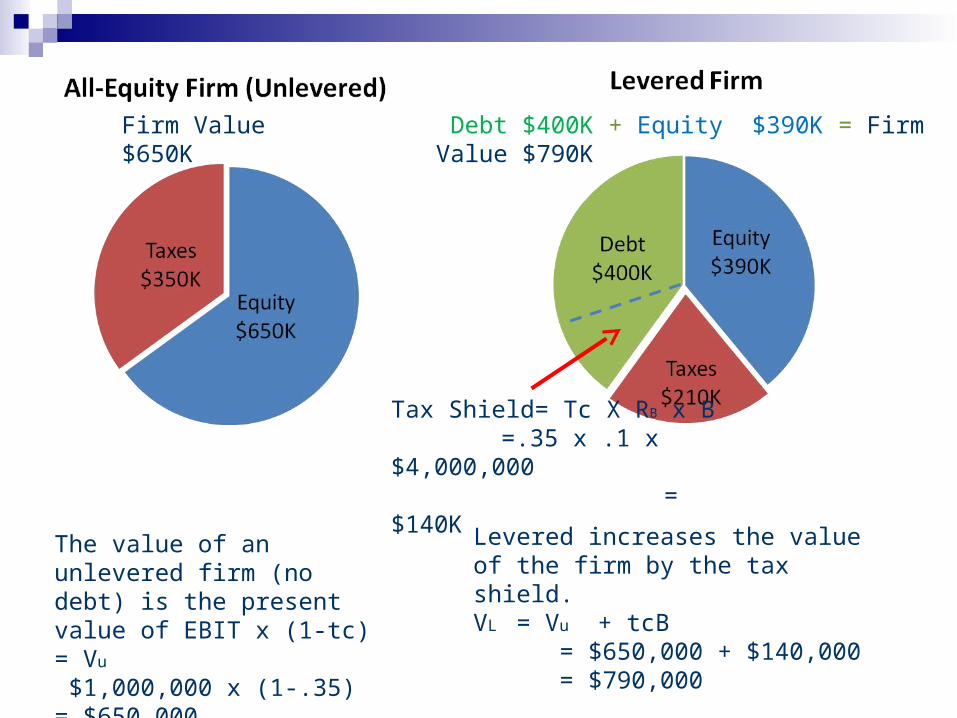

Example: The Water Products CompanyEarnings before interest and taxes (EBIT) = $1,000,000Corporate Tax rate (tc) = 35%Debt (B) = $4,000,000Cost of debt (RB) = 10% Interest (RBB) = $400,000 (.10 x $4,000,000)

Plan 1 (Unlevered)

Plan 2 (Levered)

Earnings before interest and corporate taxes (EBIT)

1,000,000 1,000,000

Interest (RBB) 0 400,000

Earnings before taxes (EBT) 1,000,000 600,000

Taxes (Tc = .35) 350,000 210,000

Earning after corporate taxes 650,000 390,000

Total cash flow (Stockholder + bondholder)

650,000 790,000

The levered firm pays less in taxes than does the unlevered firm about $140K ($350-$210). Thus the sum of the debt plus the equity ($400K + $390K) of the levered firm is greater than the equity of the unlevered firm ($650K).

MM PROPOSITION I (WITH TAXES)

Debt $400K + Equity $390K = Firm Value $790KFirm Value $650K

Tax Shield= Tc X RB x B =.35 x .1 x $4,000,000

= $140K

The value of an unlevered firm (no debt) is the present value of EBIT x (1-tc) = Vu

$1,000,000 x (1-.35) = $650,000

Levered increases the value of the firm by the tax shield.VL = Vu + tcB = $650,000 + $140,000 = $790,000

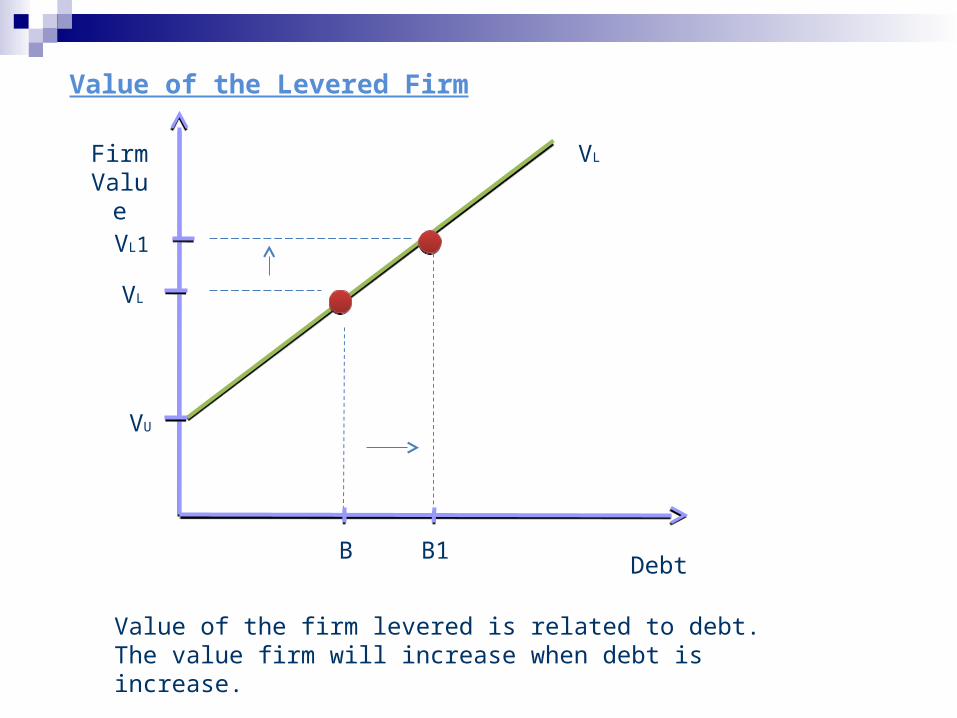

Value of the Levered Firm

VLFirm Value

DebtB

VL

Value of the firm levered is related to debt. The value firm will increase when debt is increase.

VU

B1

VL1

MM PROPOSITION II ( WITH TAXES)

Expected Return and Leverage under Corporate Taxes

1.Expected return on equity and leverage is positive relationship.2.The expected on equity increase with leverage.3.The expected on earning per share increase with leverage.4.The risk of equity increase with Leverage.

The Weighted Average Cost of Capital, RWACC, and corporate Taxes

1.In the no-tax case, RWACC is not affected by leverage.2.But, RWACC will decline with leverage in a world with corporate taxes.

Stock Price and Leverage under Corporate Taxes

1. The price of the stock increase with levered firm.

R0

RB

)()1( 00 BCL

S RRTS

BRR

SL

LCB

LWACC R

SB

STR

SB

BR

)1(

)( 00 BL

S RRS

BRR Cost of capital: R

(%)

Debt-to-equityratio (B/S)

The Effect of Financial Leverage

THANK YOU

Related Documents