Revenue Law Journal Volume 2 | Issue 1 Article 4 9-1-1991 Green Taxes : Legal and Policy Issues in Using Economic Instruments for Environmental Management Ralf Buckley Griffith University Follow this and additional works at: hp://epublications.bond.edu.au/rlj is Journal Article is brought to you by the Faculty of Law at ePublications@bond. It has been accepted for inclusion in Revenue Law Journal by an authorized administrator of ePublications@bond. For more information, please contact Bond University's Repository Coordinator. Recommended Citation Buckley, Ralf (1991) "Green Taxes : Legal and Policy Issues in Using Economic Instruments for Environmental Management ," Revenue Law Journal: Vol. 2: Iss. 1, Article 4. Available at: hp://epublications.bond.edu.au/rlj/vol2/iss1/4

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Revenue Law Journal

Volume 2 | Issue 1 Article 4

9-1-1991

Green Taxes : Legal and Policy Issues in UsingEconomic Instruments for EnvironmentalManagementRalf BuckleyGriffith University

Follow this and additional works at: http://epublications.bond.edu.au/rlj

This Journal Article is brought to you by the Faculty of Law at ePublications@bond. It has been accepted for inclusion in Revenue Law Journal by anauthorized administrator of ePublications@bond. For more information, please contact Bond University's Repository Coordinator.

Recommended CitationBuckley, Ralf (1991) "Green Taxes : Legal and Policy Issues in Using Economic Instruments for Environmental Management ,"Revenue Law Journal: Vol. 2: Iss. 1, Article 4.Available at: http://epublications.bond.edu.au/rlj/vol2/iss1/4

Green Taxes : Legal and Policy Issues in Using Economic Instruments forEnvironmental Management

AbstractGreen taxes are used widely overseas and increasingly in Australia. There are four main categories. 1. Taxes,levies, fees and other charges, including development taxes, rezoning charges, emission charges, emissionlicence fees, environmental protection charges, input taxes, resource rents and royalties, sliding charges forutilities, and product levies. 2. Tradeable, bankable and marketable rights and credits, including tradeableemission rights, emission reduction credits, transferable development credits, tradeable resource quotas, andtradeable emission leases. 3. Other economic instruments such as refundable deposits, performance bondsand guarantess, and subsidies, 4. Income tax concessions and differential sales taxes and import duties. RecentHigh Court authority suggests that whilst some of these instrucments would be excises and hence could beimposed only by the Commonwealth, most could also be imposed by state government and some also by localgovernment. Their economic and policy advantages and disadvantages are reviewed.

Keywordsgreen taxes, taxation, environmental management

This journal article is available in Revenue Law Journal: http://epublications.bond.edu.au/rlj/vol2/iss1/4

GREEN TAXES: LEGAL AND POLICYISSUES iN USING ECONOMIC

INSTRUMENTS FOR ENVIRONMENTALMANAGEMENT

BA MA PhDMM~CA MAus~MM M~AIA MIBioiProfessor, Science and Technology,Griffith University

~ntroductionBackground

Green taxes are widely used in Europe! and North America.2 In Australiathey have been endorsed by industry,3 and tentatively by conservation

1 OECD, The Application of Economic Instruments for Environmental ,Protection inOECD Member Countries (t988) OECD Report E,W/ECO/87.]2; OECD,Recommendation of the Council on the Use of Economic Instruments in EnvironmentalPolicy (1991a) OECD Report C(90) 177/FINAL; OECD, Guidelines for theApplication of Economic Instruments in Environmental Policy (1991b) 1 EnvironmentCommittee Meeting at Ministerial Level Backgrev~nd Paper; OECD, Resource Pricing(1991c) 2 Environment Committee Meeting at Ministerial Level Background Paper.

2 Stavins, ~Clean Profits~ [1989] (Spring) Policy Review 58.3 Davis, Market Based Approaches to Environmental Management (1990) Australian

Chamber of Commerce.

27

1

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

(199"1) 2 Revenue L J

groups,4 and are under ce!ose scrutiny by governments.5 Their social andeconomic effects are still controversial, but it is legal issues which arecurrently most critical in determining precisely how they will be designedand imposed.

Taxes have significantly different meanings in law, economics, andpolicy. So-called green taxes encompass a range of economic instruments ofenvkonmental policy° Only some of these are taxes in a legal sense. Inaddition, in many cases a particular policy goal could be achieved either byimposing a tax or charge, or by granting a private right which may betradeable or bankable. Such environmental property rights, sometimesknown as marketobased measures of environmenta! policy, therefore need tobe considered along with taxes in the stricter sense° The term green tax isthus used broadly to mean any instrument of fiscal policy withenvironmental applications or implications. This includes both rights andcharges; and charges include taxes, levies, licence fees, and duties.

These economic instruments are only one class of environmental policytoots o Regulatory and technological instruments are the other two°Regulatory instruments specify physical standards to be attained, leavingdecisions on technology and costs to the operating corporations concerned°Technological instruments specify technology to be adopted, but not costs oroutcome. Economic instruments set charges for environmental use ordegradation, but do not specify the equipment used or environmenta! qualityobjectives to be obtained° A given set of policy objectives may require abasket of measures of all three classes, typically employing green taxeswithin a framework of regulated standards or technological requirements.

Reasons for green taxes

Green taxes and retated economic instruments have been advocated fortwo main reasons° The first is economic: in the right circumstances,economic instruments shoutd be able to achieve a given level ofenvironmental quality at lower total cost than regulatory or technologicalinstruments. This applies only if information, metering, transaction andadministration costs are low, however. Recently, economists have suggested

4 Cameron, "An Initial Appraisal of the Effectiveness of Environmental PolicyInstrnments: Forestry, Agriculture and Ecologically Sustainable Development" inPapers, ANU/RAC Conference, Economics of Environmental Policy (1990) AustralianNational University and Resource Assessment Commission.

5 edgers, Economic Instruments for Achieving Environmental Objectives andSustainable Development (199t) Aust, Arts Sp~rt Environment Tourism andTerritories.

28

2

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

Raft I~uckiey Graven Taxes: LegaI and Policy Issues

that these conditions are rarely met.6 Green taxes which have been tried inpractice, however, seem to have performed well.7

The second argument is social: green taxes provide incentives forsocially desirable behaviour without removing individual freedom of choice.By designing appropriate economic incentives for good environmentalmanagement, government can allow many development decisions to bemade by project proponents, rather than passed to government. Some typesof policy instrument can also act to transfer administrative workload frompunic regulatory agencies to private-sector insurance and finance industriesand the courts°

Aims arid effects of green to.xes

Taxes and associated fees and charges levied by government havevarious purposes and effects: to raise revenue, to recover punic sector costs,to achieve social equity, or to modify taxpayer behaviouro

Taxes imposed principa!ly to raise general revenue are by far the largestin relative financial terms, and agencies charged with administering suchtaxes are generally concerned only to raise maximum revenue withminimum administrative cost and social inequity.* How that revenue willultimately be disbursed is not defined at the time it is raised.

There is a targe class of fees and charges imposed by governmentavowedly to recover costs incurred in providing specific rather than generalpublic services. This is the so-called user-pays policy o From both economicand legal perspectives, however, the fees charged and the services providedare highty heterogeneous. Compare, for example, electricity tariffs withstamp duties.

Specific taxes intended principally as instruments of social equity arerare. Social welfare programmes, for instance, are funded from generalrevenue. Economic theorists, however, often postulate such taxes as policytoOlSo9 If a particular policy decision, such as approval for a major resourceor industrial development, would impose costs on some individuals butallow greater gains for others, then in theory a tax could be used to force thelatter to compensate the former and still enjoy a net gain.

6 Vollebergh, "Wishful Thinking About the Effects of Market Incentives inEnvironmental Policy" in Dietz and Heijman (eds), Environmental Policy in a MarketEconomy (1987) 40; Common, Environmental and Resource Economics: AnImroduction (1988) Longman; Common, "~qe Choice of Pollution ControlInstruments: Why is so Little Notice Taken of Economists’ Recommendations?" (1990)21 Environ Plan A 1297o

7 Bressers, "Effluent Charges Can Work: the Case of the Dutch Water Quality Policy" inDietz and Heijman (eds), above n 6 at 40.

8 Preston, "Taxation and the Environment" in Papers, CEDA Conference on FutureDirection of Reform in Corporate Taxation (1990) Committee for the EconomicDevelopment of Australia; Aust, Treasury, "Economic and Regulatory Measures forEcologically Sustainable Development Strategies" [!990] (June) Economic Roundup.

9 Common, above n 6; Barbier, Economics, NaruraLResource Scarcity andDevelopment: Conventiona! and Atternative Views (1989) Earthscan.

3

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

(1991) 2 Revenue L J

All taxes have secondary effects, and some of these have major socialand environmental consequences. One of the main factors influencing thesize of these secondary effects is the relative magnitude of other social andeconomic pressures on the taxpayers affected. For example, the purpose ofincome tax is not to alter taxpayer behaviour, but taxpayers do in fact altertheir behaviour to minimise their tax liabititieso These behavioural changesare heavily constrained, however, by the taxpayers’ pressing requirementsfor continuing income.

Most green taxes, in contrast, are deliberately designed to modifytaxpayer behaviour. Commonly, they are intended to act as a deterrent toenvironmentally damaging behaviour or as an inducement to improveenvironmental management practices. Some are also intended as instrumentsof social equity, or to recover puNic-sector costs, but rarely are theyintended to raise general revenue. For many green taxes, the intention is tohalt or reduce the activities taxed so completely that no revenue is raised atatlo

Classes of instrument

Fiscal instruments with environmental implications fall into two mainclasses. Firstly, many provisions in legislation for general revenue-raisingtaxes may have environmental implications. These include income and salestaxes, customs and import duties, and excises. These taxes are very broad inapplication and revenue base, and a small change in any of their provisionsmay have major economic and social consequences. Relevant provisionsmay in turn be considered in two groups. The first consists of those whoseenvironmental consequences are inadvertent and often negative; the secondof those which are specifically intended as instruments of environmentalpolicy.

The second major category consists of taxes and related instrumentswhose primary purpose is not to raise revenue. These are generally muchnarrower in focus: the proportion of the population or electorate which paysthese taxes is relatively small, as is total revenue raised; but their social andenvironmental implications are large. Again, most of these instruments fallinto one of two groups. The first consists of charges imposed by governmentfor the use of publicly owned environmental goods and services. Theseinclude taxes, levies and licence fees of various types, and they may beapplied to both the private and the public sector. The second group consistsof private rights for the use of publicly owned environmental goods andservices, sold or granted by government and subsequently transferable orbankable o

4

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

F~alf Buckley Green Taxes: Legal and Policy

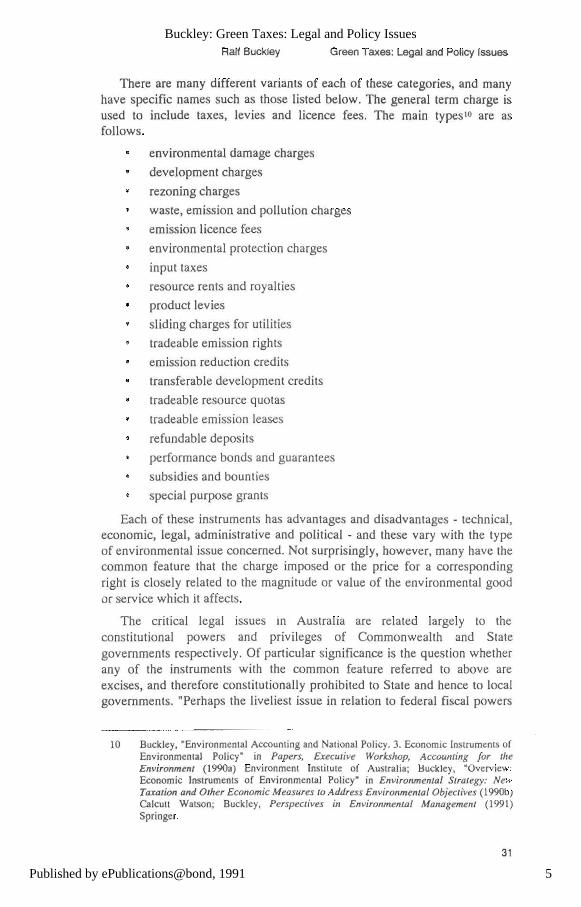

There are many different variants of each of these categories, and manyhave specific names such as those listed below. The general term charge isused to include taxes, levies and licence fees. The main types10 are asfollows.

* environmental damage chargeso development chargeso rezoning chargeso waste, emission and pollution chargeso emission licence feeso environmental protection chargeso input taxeso resource rents and royalties° product levieso sliding charges for utilities° tradeable emission rightso emission reduction creditso transferable development credits° tradeable resource quotaso tradeable emission leases° refundable depositso performance bonds and guarantees° subsidies and bountieso special purpose grants

Each of these instruments has advantages and disadvantages - technical,economic, legal, administrative and political - and these vary with the typeof environmental issue concerned. Not surprisingly, however, many have thecommon feature that the charge imposed or the price for a correspondingright is closely related to the magnitude or value of the environmental goodor sep, dce which it affects.

The critical legal issues in Australia are related largely to theconstitutional powers and privileges of Commonwealth and Stategovernments respectively. Of particular significance is the question whetherany of the instruments with the common feature referred to above areexcises, and therefore constitutionally prohibited to State and hence to locatgovernments. "Perhaps the livetiest issue in relation to federal fiscal powers

10 Buckley, "Environmental Accounting and National Policy. 3. Economic Instruments ofEnvironmental Policy" in Papers, Executive Workshop, Accounting for theEnvironment (1990a) Environment Institute of Australia; Buckley, "Overview:Economic Instruments of Environmental Policy" in Environmental Strategy: .NewTaxation and Other Economic Measures to Address Environmental Objectives (19%9b)Calcutt Watson; Buckley, Perspectives in Environmental Management (t991)Springer.

5

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

(!991) 2 Revenue L J

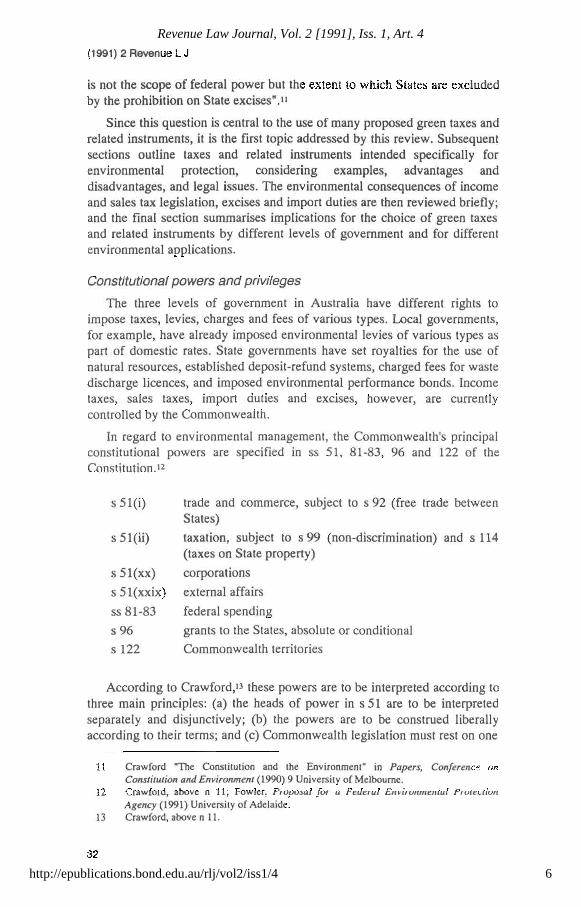

is not the scope of federal power but the extent to which States are excludedby the prohibition on State excises".11

Since this question is central to the use of many proposed green taxes andrelated instruments, it is the first topic addressed by this review. Subsequentsections outline taxes and related instruments intended specifically forenvironmental protection, considering examples, advantages anddisadvantages, and legal issues. The environmental consequences of incomeand sales tax legislation, excises and import duties are then reviewed briefly;and the final section summafises implications for the choice of green taxesand related instruments by different levels of government and for differentenvironmental applications.

Constitutional powers and privileges

The three levels of government in Australia have different rights toimpose taxes, levies, charges and fees of various types. Local governments,for example, have already imposed environmental levies of various types aspart of domestic rates. State governments have set royalties for the use ofnatural resources, established deposit-refund systems, charged fees for wastedischarge licences, and imposed environmental performance bonds. Incometaxes, sales taxes, import duties and excises, however, are currentlycontrolled by the Commonwealth.

In regard to environmental management, the Commonwealth’s principalconstitutional powers are specified in ss 51, 81-83, 96 and 122 of theConstitution.12

s 51(i)

s 5 l(ii)

s 51(xx)s 5 l(xxix)ss 81-83s 96s 122

trade and commerce, subject to s 92 (free trade betweenStates)taxation, subject to s 99 (non-discrimination) and s 114(taxes on State property)corporationsexternal affairsfederal spendinggrants to the States, absolute or conditionalCommonwealth territories

According to Crawford,!3 these powers are to be interpreted according tothree main principles: (a) the heads of power in s 51 are to be interpretedseparately and disjunctively; (b) the powers are to be construed liberallyaccording to their terms; and (c) Commonwealth legislation must rest on one

11 Crawford "The Constitution and the Environment" in Papers, Conference onConstitution and Environment (1990) 9 University of Melbourne.

12 Crawford, above n 11; Fowler, Proposal for a Federal Environmental ProtectionAgency (1991) University of Adelaide.

13 Crawford, above n 11.

32

6

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

F~alf Buckley Green Taxes: Legal and Policy Issues

or more of the granted heads of power in its legal operation, but notnecessarily in its practical effect. Indeed, Commonwealth legislation can bedrafted to derive support cumulatively from a suite of constitutional powers,as for example in the Environment Protection (Nuclear Codes) Act 1978(Cth). Similarly Fowler14 notes that the National Occupational Health andSafety Commission Act 1985 (Cth) draws on all relevant powers to cover:Commonwealth spending, territories, places and agencies; defence;information and communications; trade or commerce; banking; insurance;and corporations, including their financial operations and trading.

The Ozone Protection Act 1989 (Cth), for example, which introduced anational system of licences, levies and tradeable quotas for the production,import and export of ozone depleting substances, relies on the externalaffairs power.15 Presumably, analogous Commonwealth Acts imposingcharges or tradeable quotas for greenhouse gases, acid gases or marinepollution could do likewise.

The Commonwealth has few exclusive powers; but where powers are notassigned exclusively, Commonwealth law overrules State law.16Commonwealth and State laws can interact in various different ways.17 SomeCommonwealth acts have overridden State law, for example; whereas otherscease to operate if the Commonwealth declares that a parallel State law is anadequate substitute. In the particular case of income tax, it might appear thatsince Commonwealth legislation "covers the field" in the sense of s 109 ofthe Constitution, attempts by the States to levy income taxes would beconstitutionally invalid. The current view, however, appears to be that theStates could levy income taxes if they wished, but that political reasons haveprevented them, even when they were specifically invited to do so by theCommonwealth some years ago.

Constitutional contextUnder s 90 of the Australian Constitution, the imposition of excises is an

exclusive prerogative of the Commonwealth. The first limb of s 90 states:"On the imposition of uniform duties of customs the power of the Parliamentto impose duties of customs and of excise, and to grant bounties on theproduction or export of goods, shall become absolute". The intention of s 90was to give the Commonwealth power over taxation of commodities and toprevent the States hampering that power.18 It is important to establish theprecise legal definition of an excise in order to determine whether any of the

14 Fowler, above n 12 at 32.15 Fowler, "Global Change, the Australian Constitution and the Environment" in

Constitution and Environment, above n 11.16 Crawford, above n 11.17 Fowler, above n 12.18 Par�on v Milk Board (Vic) (1949) 80 CLR 229, 260.

33

7

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

991) 2 Revenue L J

various forms of green tax would fall into the category of excises; since ifthey did, they could be imposed only by the Commonwealth.

Originally, an excise was a duty levied on domestically produced goods,notably alcohol, analogous to customs duties levied on imported goods. Suchan interpretation may still hold in the UK.19 At the time of federation, anexcise was conceived of as "a tax on articles produced or manufactured in acountry", and "was intended to mean a duty analogous to a customs dutyimposed upon goods either in relation to quantity or value when produced ormanufactured, and not in the sense of a direct tax or personal tax".z.o Thisdefinition no longer applies in Australia, however; currently ’*the phrase’duties of excise* has no definite meaning".21

With regard to green taxes and related instruments, two different lines ofargument are important. The first defines, or at least circumscribes, thegenera1 meaning of the term excise in Australia. It derives from a long seriesof High Court cases, starting with Peterswald2z and culminating in PhilipMorris z3 and Coasmceo24 The second, which applies to a particular class ofgreen charges, derives from a recent case in Tasmania, Harper.2~ Both arerelevant, since if a particular instrument does not fall under the authority ofHarper, then the more general definition of excise will apply. I shalltherefore examine this general definition first.

General definition of an excise in Australia

There appears to be no unanimous High Court decision still standing thatdefines the term excise unambiguously. Two sets of tests may be identified:those which appear to be generally accepted by the High Court at present,and those which are still contentious, largely as a result of the so-calledfranchise cases considered belowo The generally accepted criteria are asfo110wso

An excise must be a tax: "o.. an excise is a particular form orcategory of tax..An impost will not constitute an excise ~mtess it is atax°o2~ A tax must be "a compulsory exaction of money by a punicauthority for punic purposes, enforceable by taw o..,;27 but not atlsuch exactions are necessarily taxeso~ The list of exactions which

19 Herbert, More Uncommon Law (1952) 269°274°20 Griffith CJ in Peterswald v Bartle~v (1904) 1 CLR 497, 508-509, quoting from Quick

and Garran, Annotated Constitution of the Australian Commonwealth (1991) 837-838.21 Dawson J in Philip Morris Led v Commissioner of Business Franchises (1989) 63

ALJR 520, 541o22 Above n 20.23 Above n 21.24 Coastace Pry Lid v Zhe &ate of New South Wales (1989) 63 AMR 558, (1989) 167

CLR 503.25 Harper v Minister for Sea Fisheries (Tasmania) (1989) 63 ALJR 687.26 Mason CJ and Deane J in Philip Morris, above n 21 at 525.27 Latham CJ in Matthews v Chicory Marketing Board (1938) 60 CLR 263, 276.28 Air CaIedonie Imernadonat v The Commonwealth (1988) 165 CLR 462, 467, fo~owed

in recent excise cases such as Philip Morris, above n 21.

8

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

F~aff Buck~ey Green Taxes: L~al and Policy Issues

do not constitute taxes is not exhaustive, but includes those whichare "a payment for services rendered";z9 "a charge for theacquisition or use of property"; "a fee for a privilege"; "a fine orpenalty imposed for criminal conduct or breach of statutoryobligation"; and any other of "various special types of exaction"o3~

2. An excise must be imposed in relation to goods or commodities:"o o o for constitutional purposes excises are taxes directly related togoods imposed at some step in their production or distributionbefore they reach the hands of consumers".31 It may, however, beimposed at any step in the process of production, manufacture,distribution or sale, before the goods concerned reach the consumer.An excise "embraces all taxes upon, or in respect of, a step in theproduction, manufacture, sale or distribution of goods"?2 and "a taxon a step in the production or distribution of goods to the point ofreceipt by the consumer is a duty of excise"o~ Distribution and salewere included in 1938,34 replacing the narrower definition inPeterswald; and the broader definition has been followedsubsequently o~5 For a brief period, consumption was also includedin the definition;~ but was subsequently excluded?7

3. The effect on the relevant step in (2) can be legal, practical or both;ie it may take effect in either form or substance. 3~ An excise doesnot have to be a "direct" tax.39 "The Court wil! not be restricted toconsidering the statutory criterion of liability atone but willconsider other factors in determining whether the tax is in substancea tax upon a step in production or distribution"o4~

4. Contrary to the original character of an excise, it is now no longernecessary for a tax to be quantified by the amount of thecommodity manufactured or sold in order to qualify as an exciseo41~qis is still a retevant consideration, however, as outlined below.

29 Latham CA in Matthews, above n 27 at 276.30 Air Caledonie, above n 28 at 466-~7.31 Unanimous judgment of the High Court in Bolton v Madsen (t963) 110 CLR 2(~4, 271o32 Mason J in Hematite Petroleum Pry LM v Victoria (1983) 151 CLR 599.33 Brennan J in Philip Morris, above n 21 at 533.34 Dixon J in Matthews, above n 27 at 304.35 Patton, above n 18; Western Australia v Chamberlain Industries Pry Ltd (1970) 121

CLR 1; Hematite, above n 32; Gosford Meats Pry Lid v New South Wales (1985) 155CLR 368; Philip Morris, above n 21o

36 Dixon J in Matthews, above n 27 at 303°37 Dixon J in Parton, above n 18 at 261; Bolton, above n 31; Chamberlain Industries and

later eases cited, above n 35.38 Barwick CJ in Chamberlain Industries, above n 35; Kitto J in Chamberlain Industries,

above n 35; Kitto J in Philip Morris, above n 21.39 sensu Peterswald, above n 20; Dennis Hotels Pry Ltd v Victoria (1960) 104 CLR 529,

554; Philip Morris, above n 21 at 526.40 Brennan J in Philip Morris, above n 21 at 535.41 Matthews, above n 27 at 302-303; Hematite, above n 32 at 657; overruling Pegerswald,

above n 20 and later cases cited.

35

9

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

991) 2 Revenue L J

5. A tax is not an excise if it has "no closer connection withproduction or distribution than that it is exacted for the privilege ofengaging in the process at all" or is "only in respect of the businessgenerally, and not in respect of any particular act done in the courseof the business";’~z but note43 "This is a fine distinction when the feeis calculated on the value of the commodity in which transactions inthe business took place".

6. Charges which are imposed by other names, such as licence fees,may still be taxes and excises. "If an exaction is in truth no morethan a fee for a licence, it does not amount to a tax and,accordingly, is not an excise";4~ but a so-called licence fee may stillbe a tax and an excise, however, if "the statutory description orlabel ’fee for a licence’" is in truth "a cloak for the imposition of a

A number of further propositions have been made, but are not agreedunanimously. The first concerns State government licence fees set inproportion to sales in a period preceding that for which the licence applies,by a "backdating" formula. This is relevant here since similar formulae couldreadily be t~sed in relation to, eg, fees for licences to discharge wastes° In theso-called franchise cases,4~ licence fees calculated by backdated formulaewere held not to be excises. These decisions were upheld in t984,4v albeitprincipally on the rather dubious grounds that "the States have organisedtheir financial affairs in reliance on them". In 1985,4~ however, a feecalculated by a backdated formula was held to be an excise; and in PhilipMorris in 1989, the Court was at pains to point out that decisions in thefranchise cases did not provide authority for the general proposition that abackdated calculation would prevent a tax from being an excise. Indeed, thedecisions themselves have been strongly criticised. The dissenting judgmentof McHugh J in Philip Morris49 was particularly blunt: "t doubt that thefranchise cases were correctly decided". Crawford~0 described the HighCourt’s decision in Dennis Hotds~1 as "indefensible", and Fowlerhz called it"plainly wrong". Currently, therefore, it appears that a licence fee which iscalculated by reference to the value of sales in a period preceding that forwhich the licence applies may be an excise but will not necessarily be SOo~3

42 Kitto J in Dennis Hotels, above n 39 at 560, 563; followed in Philip Morris, above n21.

43 Brennan J in Philip Morris, above n 21 at 533.44 Mason CJ and Deane J in Philip Morris, above n 21 at 525.45 Ibid 525 per Mason CJ and Deane Jo46 Namely Dennis ~otels, above n 39; Dickenson’s Arcade Pry Lid v Tasmania (1974)

130 CLR 177; and HC Sleigh Ltd v South Australia (1977) 136 CLR 475.47 Evda Nominees Pry Ltd v Victoria (1984) 154 CLR 311,316.48 Gosford Meats, above n 35 at 406.49 Above n 21 at 557.50 Crawford 1990, above n 11 at 12.51 Above n 39.52 Fowler, above n 15 at 25.53 .Philip Morris, above n 21 at 529-530.

36

10

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

Ra~f Buck~ey Green Taxes: Legal and Poticy ~ssues

The second proposition is that tobacco and liquor should be treateddifferently from other industries. This is relevant since if it were the basis forthe decision in Philip Morris, that would reduce its relevance in anenvironmental context. It was the position taken by Mason CJ and Dearie Jin both Philip Morris and Coastace: "The licence fees in question were taxesnot amounting to excise duties because, in the special fields of licences tosell alcohol or tobacco, a fee otherwise amounting to an excise duty will notbe so regarded if properly characterised as a fee for carrying on a businesscalculated by reference to sales during a period other than the licence period:a fortiori in the case of a fee being an impost on sale, not on manufacture".This is a remarkable judgment, given that liquor and tobacco were two of theearliest commodities on which excises were imposed. Of the three franchisecases,5’~ Dennis Hotels concerned liquor and Dickenson’s Arcade tobacco, asalso Philip Morris; but HC Sleigh was concerned with petroleum products.In Philip Morris, however, whilst Dawson, Toohey and Gaudron J3concurred with the judgment of Mason CJ and Dearie J, they did so fordifferent reasons; so the case does not provide authority for any generalproposition regarding the special nature of tobacco and liquor.

The third proposition is that taxes -will not be excises if they affect thecommodities concerned "in their character as articles of commerce ratherthan in their character as goods manufactured in Australia";55 ie, "thequestion of whether [the Act] imposes a duty of excise is to be answered byascertaining whether the tax affect tobacco products as subjects of Australianmanufacture".56 Given that the High Court had determined in previous casesthat a tax affecting the distribution and sale of commodities as well as theirproduction and manufacture could still be an excise, and given that PhilipMorris Ltd did in fact manufacture articles in Australia from Australiangrown tobacco, this was also a remarkable distinction. Again, the case doesnot provide authority for this proposition in general.

In assessing the likely outcome of potential challenges to possible futuregreen taxes, the judgment of Brennan J in Philip Morris is particularlyrelevant. He set out a series of propositions which integrated High Courtauthority to date and could be used to establish "whether any particular tax isan excise. Though his was a dissenting judgment, the dissension arose overthe special treatment of tobacco and liquor, and the propositions do nototherwise contradict arguments made in the majority judgment. He identifiedfour criteria57 to determine whether a tax has "a closer connection" as in thetest58 at item 5 in the list above. They may be paraphrased as follows.

54 Above n 46.55 Dawson J in Philip Morris, above n 21 at 550.56 Ibid, Toohey and Gaudron JJ.57 Philip Morris, above n 2t at 540.58 Above n 42.

37

11

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

(1991) 2 Revenue LJ

If it is simply to raise revenue, a tax is more likely to be an excisethan if it is also or principally to regulate a business activity.If it is in substance levied only once in the chain of manufacture,distribution and sale [as in Philip Morris] a tax is also more likelyto be an excise.The higher the rate of tax, the greater the connection between thetax and the transactions which attract it.If a backdafing formula is used, then the closer and shorter theperiod, the greater the connection.

To date, therefore, there is no conclusive authority from the High Oourton the precise definition of an excise. The High Court indicated in PhilipMorris that it may wetl undertake a major review of law relating to s 90 ofthe Constitution in the near future, in the same way that taw relating to s 92was reviewed in Cole v Whitfieldo59 Meanwhile, in cases dealing withtobacco, liquor, or articles of commerce rather than manufacture, we mightperhaps anticipate a similar outcome to Philip Morris and Coastace. Greentaxes, however, generally do not fall into these categories, so it might bereasonable to suppose that authority from other previous cases, assummafised in the discussion above and in Brennan J’s propositions, may befollowed.

Special types of exaction

The precise definition of an excise is irrelevant if a particular economicinstrument of environmental policy, a "green tax" in the economic andpolicy sense, is held not to be a tax in the legal sense. This was the outcomein Harper, which concerned the constitutional validity of a fee for a licenceto take abalone in Tasmania. The High Court held unanimously that ".oo itspurpose being to preserve a finite natural resource, the fee imposed was ofthe same character as a charge for the acquisition of property (analogous tothe price of a profit a prendre) as distinct from a fee payable to be permittedto do an act otherwise prohibited, and therefore did not bear the character ofa tax and was not a duty of excise". The Court held that since the fee is not atax, it is irrelevant whether the seabed concerned was owned by theCommonwealth or Tasmania. The critical argument® was that: "[a] limitednaturat resource which is otherwise available for exploitation by the publiccan be said to be truly punic property whether or not the Crown has theradical or freehold title to the resource. A fee paid to obtain such a privilegeis analogous to the price of a profit a prendre; it is a charge for theacquisition of a right akin to property. Such a fee may be distinguished froma fee exacted for a ticence merely to do some act which is otherwiseprohibited (for example, a fee for a ticence to set1 liquor) "where there is noresource to which a right of access is obtained by payment of the fee"°

59 Cole v WTdtfidd (1988) 165 CLR 360; 78 ALR 42.60 Brennan J in Harper, above n 25 at 693°

38

12

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

Raft Buckley Green Taxes: Legal and Policy Issues

In attempting to assess the potential application of this case to "greentaxes" in general, it may be significant that the natural resource concernedwas (a) limited, and (b) "otherwise available for exploitation by the public".If the High Court considers that the latter is essential for the resource to be"truly public property," that will limit the application of the case. Stateforests, for example, are generally not available for exploitation by thepublic, so the outcome of Harper would not necessarily extend fromfisheries to forestry. The radical title to State forests, however, wouldgenerally be held by the State concerned on behalf of the Crown, so theforests might be held to be public property nevertheless. In the case of aforest whose use was constrained by Commonwealth legislation, such asthose covered by the World Heritage Properties Act or the AustralianHeritage Commission Act, however, the relative significance of legislativepowers and proprietary rights might become significant. This issue wasraised by the defence in Harper, but was not determined by the Court. TheCourt did, however, state specifically, per Dawson, Toohey and McHugh J J,that "[t]he special circumstances of the case would not support a generalconclusion that no exaction of money can constitute a tax if demanded forconserving a punic natural resource".

Several other aspects of Harper are significant to potential future greentaxes. The plaintiff noted that the High Court had previously held~1 that alicence fee for fish prcw..essing was an excise, and argued that taking abalonewas just the first step in a fish production process and that the licence feewas a tax on that step in production and was therefore an excise. Thisargument was not upheld by the Court. Hence it appears that a distinctionwas made between initial acquisition of the raw resource, and its subsequenttransformation as a commodity. A similar approach is commonplace in theforestry industry, where payment for the a lease to log a given area of forestis distinguished from a royalty applied to the value of the logs taken.Similarly, in the petroleum industry, a fee for a petroleum production licenceis quite distinct from a royalty on crude oil, gas or condensate.

A second interesting aspect of Harper is that the State of Tasmania hadused a series of different formulae to calculate abalone ticence fees payablein 1987, 1988 and 1989 respectivetyo In 1987 the fee was a fixed factor timesthe actual tonnage permitted to be taken during the licence period, tn 1988 itwas a fixed factor times the ratio between the value of abalone taken inprevious period, and the tonnage permitted to be taken in current period. In1989, it was a flat fee varying only according to whether the amount takenwas more or less than 15 tonnes. This change in the mode of calculationmight well have been interpreted as a series of moves by the Stategovernment to use formulae which were less likely to be considered asexcises. Had the High Court held that the licence fee was a tax, it seemslikely that the mode of calculation used in 1987 would have rendered it alsoan excise. The formula used in 1988 is a variant of the backdating approach

61 M G Kailis (1962) Pey Led v Western Australia (1974) 130 CLR 245.

39

13

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

(1991) 2 Revenue L J

used in the franchise cases; that in 1989 was a fiat fee whose nearestanalogue would be that in Hematite Petroleum. This suggests that the Stategovernment was by no means confident that the fee was not a tax.

The judgment of Mason CJ, Dearie and Gaudron JJ in Harper is ofespecial interest as an indicator of the High Court’s views on environmentalpolicy, and one section in particular (at 688) is worth quoting at length.

The licensing system o. o is not a mere device for tax collecting. Its basis lies inenvironmental and conser,,ational considerations which require that exploitation,particularly commercial exploitation, of limited public natural resources becarefully monitored and legislatively curtailed if their existence is to bepreserved. Under that licensing system, the general public is deprived of the rightof unfettered exploitation of the Tasmanian abalone fisheries. What was formerlyin the public domain is converted into the exclusive but controlled preserve ofthose who hold licenceso The right of commercial exploitation of a publicresource for personal profit has become a privilege confined to those who holdcommercial ticenceSo This privilege can be compared to a profit a prendreo Intruth, however, it is an entitlement of a new kind created as part of a system forpreserving a limited natural resource in a society which is coming to recognisethat, in so far as such resources are concerned, to fail to protect may destroy andto preserve the right of everyone to take what he or she will may eventuallydeprive that right of all context. In that context, the commercial licence fee isproperly to be seen as the price exacted by the public, through its laws, for theappropriation of a limited public natural resource to the commercial exploitationof those who, by their own choice, acquire or retain commercial licenceso Soseen, the fee is the quid pro quo for the property which may lawfully be takenpursuant to the statutory right or privilege which a commercial licence confersupon its holder. It is not a tax.

Relationship with value of goods

In determining whether a government exaction is a tax, and if so whetherit is an excise, one critica! aspect is the relation between the amount chargedand the value of the goods to which the charge relates. This test operatesdifferently in regard to taxes and excises respectively, however, and also inregard to large and small fees.

A relatively small fee wil! generally not be considered a tax unless itvaries with the quantity or value of the commodity. "When a statute fixes alump sum in a moderate amount as a licence fee there is no necessary reasonto characterise the exaction as a tax or as an excise. On the other hand, whenthe statute exacts, as the fee for a licence to carry on a business ofmanufacturing, producing, selling or distributing a commodity, an amountcalculated by reference to the quantity or value of the commoditymanufactured, produced, sold or distributed by the licensee during aparticular period, the exaction has the attributes of a tax. Although theexaction is expressed to be for the grant of the right to engage in thebusiness, which is collateral to actual manufacture, production, sale or

14

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

F~aff Buckley Green Taxes: Legal and Policy lssues

distribution, the mode of calculation of the fee reveals its character as a taxon the activity carried on by the licensee under the licence".62

For a relatively large fee, however, the test "calculated by reference tothe quantity or value" is not a necessary requirement; as shown by the HighCourt’s judgment in Hematite Petroleum, where a flat fee of $10 million perannum for the use of a petroleum pipeline was held to be both a tax and anexcise. The High Court held63 that "[t]he fee is an exaction of suchmagnitude imposed in respect of a step in production in such circumstancesthat it is explicable only on the footing that it is imposed in virtue and valueof the hydrocarbons produced o. "o Ie, the fee was related to the value of thegoods, even though not calculated by reference to their quantity.

In both Air Caledonie64 and Harper,65 the High C~urt’s judgments appearat first sight to conflict with that of Mason CA and Deane J in Philip .Morris,quoted above. Thus in Air Catedonie (at 457), if an exaction "has nodiscernible relation with the value of what is acquired, the circumstancesmay be such that the exaction is, at least to the extent that it exceeds thatvalue, properly to be seen as a tax". And in Harper,~ one of the mainreasons that the abalone licence fee was not considered a tax is that there is"a relationship between the amount paid and the value of the privilegeconferred by the licence". This apparent discrepancy disappears, however, ifit presumed that the test of a discernible relation is not applicable toexactions which -would not be considered taxes in any event since they are a"speciat type" of exaction, such as those listed in Matthews~7 and AirCaledonieo That is, that the test of exclusion as a special type of exactionmust be applied before the test of a discernible relationship with the quantityor value of goods. In Harper, for example, since the fee was considered to bethe price of a profit a prendre, it was therefore not a tax, and the discerniblerelationship test was therefore not relevant. This presumption of sequentialtesting would overcome the difficulty raised by Crawfordc~ that "[i]t wouldbe curious if [an] air emission licence was held to be a tax because it did notbear a close enough relationship to the value of the resource appropriated,but was then held to be an excise because it did bear a sufficiently closerelationship to the value of the goods produced".

If an exaction qualifies as a tax because (a) it is not considered a specialtype, and (b) it satisfies the discernible relation test either through its size orby being calculated by reference to the quantity or value of goods, then thediscernible relation test is also relevant in determining whether it is anexcise. It is not, however, the only relevant test, as outlined in the generaldefinition of excise as above.

62 Mason CA and Deane J in Philip Morris, above n 21 at 525°63 Mason J in Hematite Petroleum, above n 32.64 Above n 28.65 Above n 25°66 Above n 25 per Dawson, Toohey and McHugh JJ at 693.67 Above n 27.68 Above n 11.

41

15

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

(1991 ) 2 Revenue L J

charges: taxes, |evies and |icence feesEnvironmental damage charges

Definition. Charge for an activity, equal to the value of damage to theenvironment occasioned by that activity.

Basis° Compensation for environmental damage. Damage to theenvironment imposes costs on the public as owner of the environment, andprovides corresponding private benefits for the waste producer. If set at anappropriate level, environmental damage charges transfer these costs fromthe punic back to the private beneficiaries.

Examples° Used in many different forms which rely on differentestimates of environmental damage costs, as outlined below. Chargesimposed by the Environmental Restoration and Rehabilitation Trust Act1990 (NSW), Environmental Research Trust Act 1990 (NSW), andEnvironmental Education Trust Act 1990 (NSW) might be consideredconceptually as environmental damage charges, though as noted by Fowler,69they are phrased as charges for services rather than direct taxes.

Advantages° Socially equitable: compensation for damage to publiclyowned environmental goods and services, providing investment capital tomaintain intergenerational equity. Avoids economic distortions associatedwith so-called negative externalities.

Disadvantages° Accurate valuation of environmental damage isrelatively complex, costly and uncertainoT0

Legal considerations. It would seem likely that environmental damagecharges would be considered as a special type of exaction, probably a fee forthe use of property, and hence neither a tax nor an excise. As such, theycould be levied by any level of government.

Development taxes

Definition. Charges associated with development approvals for some oralt types of development, proportional to or varying with the type, scale orconstruction cost of the development°

Basis° A form of environmental damage charge using development costsas a surrogate measure of environmental damage costs; based on the premisethat all industrial or commercial development causes environmental damage,and that for any given type of development the damage is likely to beapproximately proportional to the cost of the development.

6970

Fowler, above n 15, footnoteBuckley, "Environmental Accounting and National Policy° 1. Techniques andLimitations" in Accounting for the Environment, above n 10 (1991); Buck]ey, above n10 (1991); Bojo, Maler and Unemo, Environment and Development: an EconomicApproach (1990) gduwer.

42

16

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

F~Nf Buck~ey Green Taxes: LegN and Policy ~ssues

Examples. Development taxes are used in some States of the USA.71

Advantages. Easy to administer; provide funds for environmentalmanagement associated with specific developments.

Disadvantages. The ratio between the environmental impacts of adevelopment and its overall cost is not fixed, but varies both "with the type ofdevelopment and with the skill and funds devoted to environmental planningand management. If this is not taken into account, then development costswill be poor estimates of environmental damage costs, and the mode ofcalculation wil! discourage expenditure on environmental protection. If it istaken into account, the advantage of simplicity is reduced.

Legal considerationSo Though they would appear to be taxes primafacie, there are several arguments which might distinguish developmentcharges from taxes within the meaning of s 90 of the Constitution, asfoltowso 1. As a type of environmental damage charge, they might beconsidered as charges for the use of public goods. 2o They might beconsidered as a fee for a privilege, namely the right to undertake a particulardevelopment, and hence a special type of exaction and not a tax. 3. Even ifconsidered to be taxes, they might not be classified as excises since they areimposed for the right to carry on a business, rather than as a tax directlyrelated to goods or commodities. 4. For developments which do not producegoods or commodities, such as those which provide services, infrastructure,accommodation, etc, development taxes would probably not be consideredas excises; but this argument would not apply for charges imposed ondevelopments in primary industries or manufacturing.

Rezor~ir~g charges

De~ni~ien. A charge imposed by a government planning authority forthe rezoning of privately owned land to a more intensive use.

Basis° Such a rezoning corresponds to the grant of a valuable right to aprivate firm or individual, at a potential environmental cost to the punic. Arezoning charge is a means to recover that cost in part or full.

Examples. Not currently used as such in Australia, but under seriousconsideration by State and local governments.

Advantages. Low" administrative costs° Social equity.

Disadvantages. Because of the strong commercial incentives forrezoning, the market would probably bear rezoning charges at a relativelyhigh leveio This might lead to the imposition of unfairly high charges inalready urbanised areas, where the marginal impacts of rezoning areminima!; and indeed, where higher density housing reduces the per capitaenvironmental impacts of residential accommodation. It would be preferable,therefore, if rezoning charges were restricted to the conversion of either (a)

71 Westman, Ecology, ]mpact Assessment and E’nvironmemat Planning (1985) Wiley.

43

17

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

991) 2 Revenue L J

land of high conservation value to land of lower value, or (b) rural land toresidential allotments, resort developments, or urban or industrial use(including subdivision of acreage).

Legal considerations. Could potentially be considered an excise, but thisis unlikely. Could probably be imposed by any level of government, notablyby local government.

Emissior~ charges

Definition. Charges imposed for permission to release wastes off-site,into air, water or landfill; often referred to as pollution taxes. There are manydifferent variants. Most impose a charge per unit emission, either metered orestimated. The charge imposed may be a complex function of the amount,composition and timing of the discharge. Fees for waste discharge licences,either flat or stepped, are a special case which are usually distinguishedunder a separate name.

Basis. A type of environmental damage charge, with the quantity andcomposition of discharges used as an estimate of the environmental damagethey produce.

Examples. Used in many nations, but with considerable variation in theirprecise form; eg as regards thresholds, sliding charge scales, and couplingwith statutory penalties?2 In the Federal Republic of Germany, for example,effluent charges were introduced in 1976 in addition to technology-basedrequirements23 Effluent discharge permits in the FRG specify baselinelevels, discharge standards, monitoring procedures, and maximumpermissible discharge concentrations. If standards are met, charges arediscounted by 50 percent. If they are exceeded, the full charges are payable,plus fines. The actual charges are calculated from the expected dischargeconcentrations as specified by the corporations concerned, using damage-unit rates fixed by law: eg, 1 unit per cubic metre of organic settleable solids,5 units per 100 gm mercury, etc. This gives a total expected number ofdamage units, and charges are then set at a certain fee per unit. The cost ofthese charges to the corporations concerned is less than 2 percent of sales foreven the most heavily polluting industries, excepting only the pulp, yeastand tanning industries.v4 The standards are set by industry-government taskforces. Municipalities are subject to the charges in the same way as privatecorporations. The revenues raised are used to subsidise investment in wastetreatment technology.

72 Bressers, above n 7; OECD, above n 1 (1988); Bongaerts and Kraemer, "Permits andEffluent Charges in the Water Pollution Control Policies of France, West Germany andthe Netherlands" (1989) 12 Environ Monitor Assess 127; Mulet, "Incentives inInternational Environmental Problems" in Economics of Environmental Policy above n4; Lindner, "Effectiveness of Environmental Policy Instruments", ibid.

73 Brown and Johnson, "Pollution Control by Effluent Charges: it Works in the FederalRepublic of Germany, Why Not in the US?" (1984) 24 Nat Res J 929.

74 Ibid.

44

18

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

Raft Buck|ey Green Ta~es: Legal and Policy Issues

In the FRG, the intr~lucfion of emission charges was supported bysectors of industry which had already adopted improved effluent-controlpractices, as the charges gave them a financial edge over their competitors.In Holland, however, both industry and conservation groups opposedpollution charges initially, though both now support them in view of theirsuccess.75

Except for emission licence fees (see below), emission charges as suchdo not yet appear to have been adopted by any of the States or theCommonwealth in Australia; but they are currently under very closeconsideration. Carbon taxes, as proposed to enable Australia to comply withinternational targets for the reduction of greenhouse gas emissions,76 wouldfall into this category. Since carbon taxes would presumably be levied by theCommonwealth, however, s 90 would not be relevant.

Advantages. 1. The quantity and composition of emissions provide arelatively accurate measure of the environmental damage caused by wastedischarges. 2. Emissions are already metered, measured or monitored tocheck compliance with standards, so additional metering and administrativecosts are low. 3. The precise formulae used in calculating emission chargescan be designed and modified to reflect changing scientific opinion on therelationship between discharges and environmental impacts: eg, thresholdscorresponding to the level of discharge below which environmental damageis believed to be negligible. 4. The charging rates can be modified iterativelyto achieve a predetermined ambient environmental quality or to reflect anincreasing number of discharge points. 5. Emission charges can readily beintegrated with existing regulatory standards and penalties. 6. In theory,emission charges can achieve a particular level of environmental quality at alower totat cost than regulatory discharge standards alone. 7. Emissioncharges seem to have worked welt where they have been used overseas.

Disadvantages. 1. The conditions which are required for emissioncharges to achieve the high economic efficiency of which they aretheoretically capable, seldom apply in practice: though note that this may notbe a major disadvantage in reatityo 2. The economic impacts of a given levelof charges are generally not known in advance: though note that this alsoapplies to regulator’.,, and technological instruments.

Legal considerations. Whilst emission charges are generally imposed onprocesses which produce goods and commodities, and are generally have adefined relationship to the quantity of emissions and hence of goodsproduced, it is arguable that they are not taxes and hence not excises, forseveral different reasons. The most fundamental is that they are charges forthe use of public property, namely for the use of the environment as areceptacle for wastes; and as such are a special type of exaction. According

75 Bresse~s, above n 7.76 Bertram, "Tradeable Emission Permits and the Control of Greenhouse Gases" in

Economics of Environmenm! Policy, above n 4.

45

19

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

(199t ) 2 Revenue L J

to Fowler:77 "it might be argued by analogy [with Harper]78 that a State taxon air pollution constitutes a charge for the rig~t to exploit air as a commongood and therefore is also not an excise". It seems likely on current authoritythat this argument would be upheld by the High Court. It would be lessclearcut where discharges were to private land or a privately ownedwaterbody, but even in those cases, governments generally retain legislativepowers over land and water use, and this might be a sufficient criterion forHarper to apply. Note that Harper did not decide this last issue specifically.

For emission charges which incort~rate a discharge threshold belowwhich the charge is zero, it is conceivable that an alternative argument mightapply: namely, that the charge is not a compulsory exaction, since it may beavoided entirely by reducing discharges below that threshold. Income tax isstill a tax even though incomes below a threshold incur zero tax liability,however, so it seems unlikely that this argument would hold unless thethreshold were so high that a zero charge were the norm rather than theexception.

If both these approaches were to fail, then the States could perhaps stillimpose emission charges by exploiting the current technical loophole in thedefinition of an excise, namely the use of a backdating formula incalculating the charge imposed. Since emission charges are not related totobacco or liquor, however, nor to items of commerce rather thanmanufacture, there would be strong grounds for distinction from the majorityjudgments in Philip Morris,79 and the High Court would probably not lookwith favour on such an artifice.

Hence it appears that the strongest approach for the States at present, andone likely to be successfu!, would be to rely on Harper and similarprecedents, and ensure that any legislation imposing emission charges statesexplicitly that they are intended as a charge for the use of the environment asa public good.

Emission licence fees

Definition° Fixed or variable fee for a licence to discharge wastes.

Basis° Small fixed fees: imposed to recover government administrativecosts° Larger and variable fees: a form of emission charge°

Examp~eso Fees for waste discharge licences are common worldwide° InAustralia they are commonly imposed by State legislation regulating air andwater qualityo They were originally intended simply as a means for partialrecovery of public sector administrative costs, tf large enough, however,they might also be viewed as a special type of environmental damagecharge.

77 Fowler, above n 12 at 24°78 Above n 25°79 Above n 21o

20

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

Raft Buckley Green Taxes: Legal and Policy I~sues

Advantages. Already in common use, and accepted by industry.Modifications to formulae for calculating charges can generally be effectedby regulation rather than requiring new legislation.

Disadvantages. 1. There is a significant risk of governmentoverservicing if, as is often the case, (a) these licence fees they are collectedby State government departments responsible for environmentalmanagement; (b) they are retained by those departments rather than passedto Treasury; and (c) those departments are under-funded and underincreasing pressure to raise their own funds from so-called "users" or"clients". This risk exists for any form of green tax where all of (a), (b) and(c) apply, but in practice this is most common for emission licences. 2o Atpresent, licence fees are rarely effective as environmental damage chargessince (a) they are generally small relative to their value to the licensees, whowould otherwise have to reprocess or recycle all wastes on site; and (b) theyare very" small relative to the cost of the environmental damage they permit,as measured by any of the standard environmental accounting techniqueso~

Legal considerations. Legal constraints on emission licence fees dependon the relative size of the fee. If it is small, then the courts will probablyconsider that it is not a tax for that reason alone.81 If large, however, then thearguments given above in relation to emission charges will apply o

Environmental protection charges

Definition. A charge equal to the profit made by breaking ordisregarding an environmental standard, and apptying in addition to anyfines or penalties.

Basis. Essentially an instrument to recover illegal gains. If the profit afirm can make by disregarding environmental standards is greater than thepenalty applied, it will be to the firm’s commercial advantage to ignore thestandard. Environmental protection charges are designed to remove thisincentive.

Examples. Used in Scandinavia82 and the USA.83

Advantages° Removes any commercial incentive to breach standards andrecovers private gains from doing so.

1)isadvantageso High monitoring and enforcement costs.

Lega! considerations° Since environmental protection charges arepenalties imposed for breaching statutory obligations, they are not taxes,~4

80 Above n 70.81 Philip Morris, above n 21 at 525.82 Ware, Fiscal Measures and the Attainment of Environment Objectives: Scandinavian

Ini¢iatives and �heir Applicability ¢o Ausgratia (1985) AGPS.83 Westman, above n 71.84 Air Caledonie, above n 28 at 466-467.

47

21

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

(199t) 2 Revenue LJ

and could hence be imposed by either State or Commonwealth governments.The basis of calculation, however, might be subject to challenge undercommon law.

~’nput taxes

Definition. Charge levied on inputs to environmentally damagingprocesses, rather than outputs or actual damage.

Basis. A tTorm of environmental damage charge, which attempts to avoidthe metering costs associated with emission charges.

ExarnpleSo In some European countries, industries are taxed on theirpetroleum consumption, with revenues being used to subsid~se variousenvironmental projects. Fuels containing over 1 ~rcent sulphur are alsosubject to a sliding tax on sulphur content, to en~urage the use of low-sulphur

Advantages. Few. Outputs from environmentally damaging pr~essesare generally monitored to check compliance. Inputs may be measured moreprecisely, but they are one step further removed from actual environmentaldamage.

~sadvantages. 1. No ~ncenfive to ~mprove pr~esses or pollutioncontrol to redu~ emissions and environmental damage per unit productiveoutput, unless the taxes are related to input quantifies by a factor whichvaries w~th the ratio betweenintroduce economic distortions ~used by attempts at input substitution.

There may wetl be good environmental and economic reasons to imposecharges on publicly owned resources, such as raw materials and energy,which are inputs to industrial processes. However, it will almost always bepreferable to include such charges in the prices demanded by government forthe use of the resources concerned, since that will reduce economicdistortions associated with negative externalities, rather than introducingnew distortions by means of input taxes.

Legal cor~siderafior~s. Even if intended as a form of environmentalprotection charge, input charges would appear to be taxes both in form andsubstance and are likely to fall within the compass of s 90.

Resource rents and royalties

Definition. In practice, resource rents are charges related to the quantityor value of the resource before extraction or use, whereas royalties aredetermined by the quantity or value of the primary commodity afterextraction: crude oil, condensate, sawlogs, etc. In legal terms, however, a

85 Ware t985, above n 82; OECD, above n 1 (1991a, b).

22

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

F~aff Buckley Green Taxes: LegN and Policy ~ssues

royalty is "a payment made to the owner of land for the right to take awaythings which are part of or naturally attached to the soil".86

Basis. Both resource rents and royalties represent prices extracted by thepunic owners of public natural resources for their use by private interests°

Examples. Widely used in mineral, petroleum and forestry industries inAustralia and overseas.87 Rents, royalties and ticence fees for the Australianmineral and petroleum industries in 1989/90 totalled $627 million, forexample.~

Advantages. 1. Mechanism whereby government custodians of publiclyowned resources can obtain a fair return to the public for their use. 2. Avoidseconomic distortions associated with provision of subsidised raw materials.3. Encourages development of valueoadding industry:

Disadvantages. Limited in application by the competitive effects, ondomestic industry, of fluctuations in global commodity markets.

L~gal eor~sideratior~so Royalties and rents can generally only be chargedby the owners of the resource concerned or the 1and on which it is found.This does not present a significant limitation in practice.

Sliding charges for utilities

Definition. A utility, in this sense, is a resource which is delivered toindustrial and domestic consumers as a continuous metered supply accordingto demand. Water, gas and electricity are the most common examples. Asliding charge for such a utility is one where the charge per unit resourceincreases with the number of units consumed in a given charging period: abasic supply would be cheap, but heavy demand would attract higher unitprices.

Basis. Infrastructure for supply of reticulated water, gas and electricity isgenerally large-scale and capital intensive, so differential allocation of coststo individual small consumers is economically difficult and inefficient. Inaddition, social policy considerations generally dictate that basic supplies ofpower and -,,cater should be available throughout densely populated areas. Asmall basic supply, therefore, should be made available at tow cost. Heavyand wasteful consumption, however, incurs unnecessary punic expenditureand environmental damage, and it is reasonable to recover such costs fromindividual heavy consumers. 89

Examples. Not currently used in Australia, where the most commoncharging systems are either fixed unit rates, or fixed total charges which donot vary with the quantity consumed. At present, most differential tariffs for

86 Stanton v Federal Commissioner of Taxation (1955) 92 CLR 630,87 Cameron, above n 4; OECD, above n 1 (1988, 1991c).88 AMtC, Minerals Industry Survey (1990) Australian Mining Industry Council; Gillies,

"Developments in Mining Resource Rent Taxation" (1990) 2 Proc Pac Rim 90 Congr651.

89 C~ombs, The Return of Scarcity (1990) Cambridge.

23

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

(1991) 2 Revenue L J

utilities operate in the opposite direction: large industries typically pay lowerunit prices than domestic consumers. In addition, power and water suppliesare subsidised from general revenue in most areas.

Advantages. Provides economic incentives for resource and energyconsergation; allocates costs of environmental damage to those ultimatelyresponsible. Low administrative costs since supplies to individual consumersare already metered. Precise charging scale can be modified iteratively toestablish effects on consumption. Avoids economic distortions associatedwith subsidisatiOno

Disadvantages. 1. Special concessions may be required for particularheavy consumers such as hospitals and schools o 2. Stiding charges wouldneed to be introduced simultaneously throughout a large region, to avoidcompetition between local areas.

Legal considerations. Few. In Australia, electricity supplies aregenerally controlled by statutory authorities of State governments, and watersupplies by State and local governments. In either case, those authorities arelargely free to determine charges.

Product Jevies

Definition. A charge imposed per item or per unit value on retail sale ofproducts.

Basis. Where resources and energy used in manufacture and distributionof the products concerned, or the use or final disposal of those products, areenvironmentally damaging, and the prices paid by consumers do not fullyreflect those environmental costs, product levies are a means of recoveringthe costs of environmental damage from consumers.

Examples. Used overseaso~ Australian State governments haveconsidered or are currently considering levies on products such as car tyres,motor fuels, batteries, newspapers, fertilisers, pesticides and so on. Levies onmotor vehicle registration have also been considered.

Advantages. 1. Reduces consumption of products whose manufactureand distribution wastes resources and energy or uses subsidised resourcesand energy. 2. Provides additional commercial incentives for recycling andresource recovery. 3o General consumer acceptance. 4o Could be combinedwith sales tax system if levied by Commonwealth.

Disadvantages. Confusion with sales taxes if levied by States; highadministrative costs.

Legal considerations. It would appear that most product levies wouldalmost certainly be classed as excises and so would be subject to challenge ifimposed by State or local government.

90 OECD, above n 1 (1988, 1991b,c),

24

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

Raft E~uck~ey Green Taxes: Lega~ and Policy {ssues

Environmental damage rights and creditsDefinition. Rights to carry out a prescribed level of an environmentally

damaging activity, which are initially granted by government and may then,depending on the conditions of the right, be either (a) held in credit forfuture use, (b) transferred to or traded with other firms carrying out the sameor related activities, or (c) marketed for cash.

Basis. Regulator?" or technological instruments give firms the right toproduce a certain level of environmental damage. These rights are non-rivaland do not limit the total level of environmental damage which can beproduced by all firms. An alternative approach is to create damage rightswhich can be owned and which have a fixed and finite total. Depending onthe precise form of instrument, these rights may either be bankable byindividual firms only, tradeable between firms under various conditions, ormarketable for cash. Options and futures in such rights may also be createdand traded.91

Examples. The main examples are emission or pollution rights, andtransferable development credits. Both of these are currently used in theUSA. They are considered in more detail below o

Advantages. Transferable or bankable environmental damage rightsallow considerable commercial freedom of choice in environmentalmanagement by individual firms, whilst altowing regulatory agencies tocontrot the overall levet of environmental damage in a given area. Neitherregulated standards nor environmental damage charges have the latteradvantage° In addition, by controlling the period for which rights apply,regulatory agencies can use tradeable rights to produce smooth transitions inthe effective price and degree of environmental damage associated withparticular industry sectors°

Disadvantages. One of the most serious difficulties with tradeableenvironmental damage rights is how they should be allocated initially. Theymay be sold to private interests by the State, for example by auction ortender, or they may be distributed gratis to existing industries in proportionto actual past levels of activity, a process known as grandfathering. Theformer means that firms which were using rights provided by regulatoryinstruments effectively have those rights cancelled and have to buy newones. This may be viewed as unjust, since there was a reasonable expectationthat these rights would continue° Grandfathering, however, gives an tmfairadvantage to firms with poor environmental management or outdatedequipment, since it gives them the right to continue high levels ofenvironmental damage, to the detriment of their competitors as well as thecommunity. Some combination of short-term free rights and longer-termpurchased rights with a transition period for adjustment seems optimal.

91 Raufer, Feldman and Jaksch, "Emissions Trading and Acid Deposition Control: theNeed for ERC I_~asing" (1986) 36 J Air Pollut Contr Assoc 574,

25

Buckley: Green Taxes: Legal and Policy Issues

Published by ePublications@bond, 1991

(1991) 2 Revenue L J

Another difficulty with tradeable environmental damage fights is thatthey could be used to corner the market for a particular product, bypreventing competing manufacturers from operating. This does not yet seemto have occurred in practice.

A third disadvantage is that tradeable rights will only be effective whenthere is a well informed, rapidly clearing and competitive market for them.This will only occur when (a) the total amount of environmental damagewhich firms would produce in a given area if unrestricted exceeds the totaldamage rights granted for that area, creating a commercial demand for suchrights; and (b) there are enough firms competing for those rights to avoidmonopolistic and oligopolistic market behaviouro

Legal considerations° It would appear that unless the Commonwealthwere to enact conflicting legislation, there is currently no constitutional orother lega! barrier to the States erecting systems of tradeable rights. Themost likely avenue for legal challenge would be from holders of existingregulatory licences, if their rights under these licences were reduced orabrogated. In practice, however, the main barriers to the use of tradeablerights in Australia are more likely to be economic and political than legal.

Tradeable emission rights and emission reduction credits

Definition. These are environmental damage rights related specifically towaste discharges. Different terminologies are used to distinguish (a) theconditions under which an emission right is granted initially, and (b) theconditions under which it may subsequently be banked, traded or sold. Theterm emission reduction credit (ERC) refers to a right which is granted to afirm which has reduced emissions from existing operations, and which canbe banked by that firm for use in future operations. Different types ofemission rights have different generic names, depending on the degree oftrading permitted. Trading between discharge points within one plant iscalled netting. Rights tradeable between plants and discharge points butwithin one site are called bubbles. Those tradeable between plants, sites andoperations, but within one firm, are called internat offsets; and thosetradeable between firms, within a regional airshed or water catchment, arecalled external offsets.

Basis. Nets and bubbles were introduced to enable a company to cutpollution contro! costs by reducing emissions from sources where it ischeapest to do so, provided the overall net reduction is more than wouldhave been achieved by reducing emissions from each source equally, asrequired to meet overall emission standards. Higher emission rates from onesource are offset by !ow emissions from another. Broader tradingopportunities, including internal and external offsets, were introduced as anextension. In an internal offset, a single corporation is permitted to constructa new plant if it reduces emissions in existing plants by more than the totalnew emissions from the new plant o The number of times this reduction mustexceed the new emission is called the offset factor, and is often high: eg,

52

26

Revenue Law Journal, Vol. 2 [1991], Iss. 1, Art. 4

http://epublications.bond.edu.au/rlj/vol2/iss1/4

Green Ta~es: Legal and Policy Issues

10:1. In an external offset, one company reduces its emissions, giving it anemission-fight credit which it can then trade with or sell to another companyin the same region. A similar offset ratio applies. Evidently this approachworks best where administrative boundaries coincide with airshed orwatershed boundaries: otherwise emissions released in one administrativeregion would affect environmental quality in a second, irrespective of thecontrols applied in the second.

Examples. Tradeable emission rights are most widely used in the USAand West Germany, particularly in regard to air qualityo~z They are also usedin Japan. In the USA, 94 air-quality bubbles and -3000 offsets had beenapproved up to January 1986, with an average cost saving of US$2 millionper bubble.93 In the USA at present, both internal and external offsets arepermitted. In either case, new plants must also use best practicabletechnology. A J1 States within a given airshed impose uniform rules.

Advantages. As for tradeable environmental damage fights ~n general.