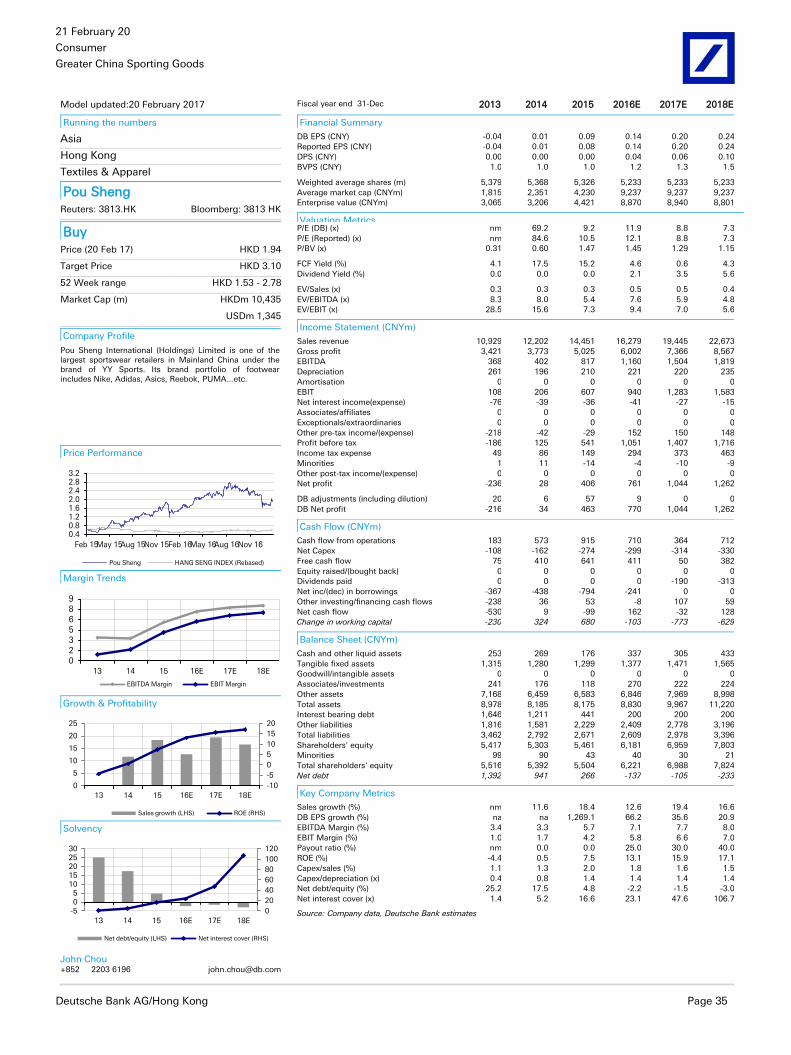

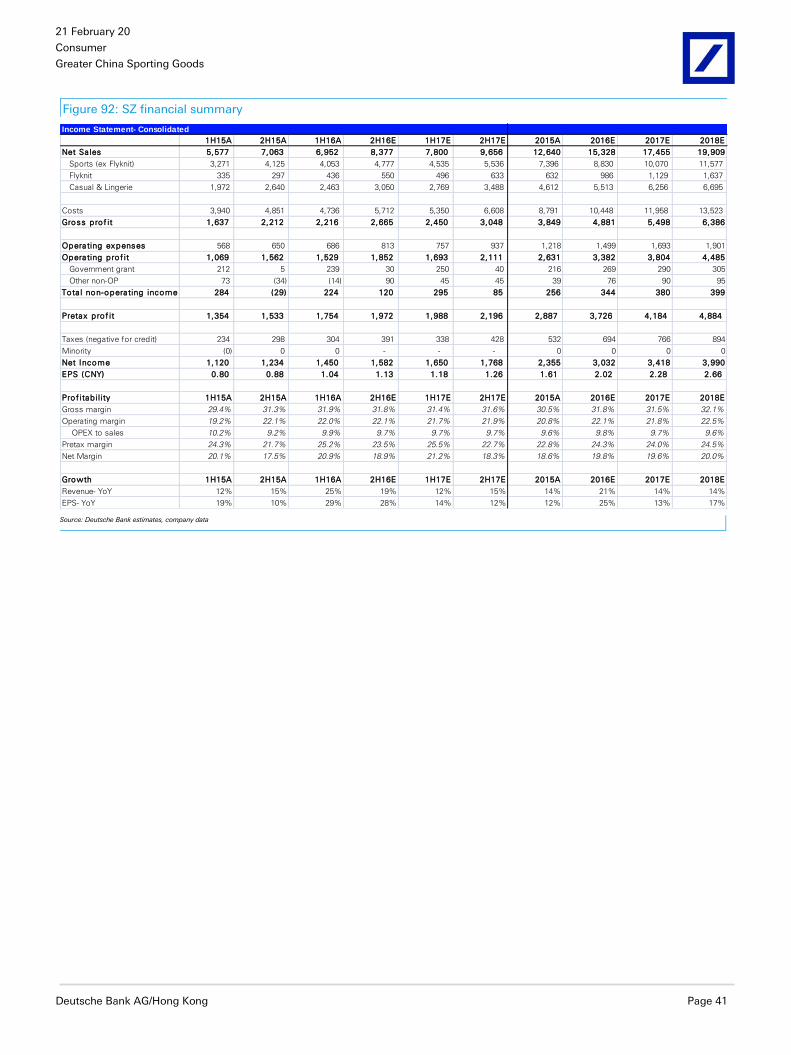

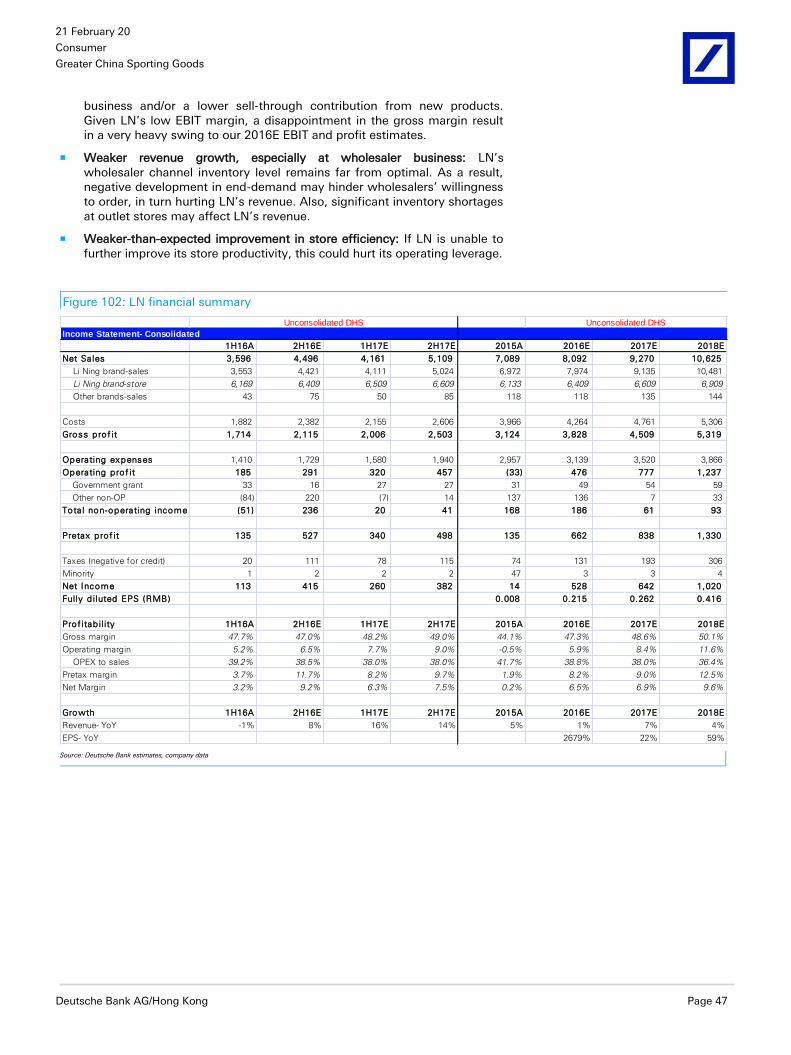

Deutsche Bank Markets Research Asia China Consumer Industry Greater China Sporting Goods Date 21 February 2017 Recommendation Change FY16 preview: Time to buy US- exporting ODMs; upgrading YY to Buy Buy Eclat, YY, FT & PS; stay cautious into Anta’s 2H16 results ________________________________________________________________________________________________________________ Deutsche Bank AG/Hong Kong Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016. John Chou Research Analyst (+852 ) 2203 6196 [email protected] Anne Ling Research Analyst (+852 ) 2203 6177 [email protected] Key Changes Company Target Price Rating 0551.HK 35.00 to 38.00(HKD) Hold to Buy 1476.TW 435.00 to 430.00(TWD) - 2313.HK 62.00 to 56.00(HKD) - 9910.TW 170.00 to 156.00(TWD) - 2020.HK 24.00 to 26.50(HKD) Buy to Hold 2331.HK 6.20 to 5.90(HKD) - Source: Deutsche Bank Top picks Yue Yuen (0551.HK),HKD26.95 Buy Eclat Textile (1476.TW),TWD309.00 Buy Feng Tay (9910.TW),TWD130.00 Buy Pou Sheng (3813.HK),HKD1.94 Buy Source: Deutsche Bank The upcoming earnings could be mixed for the sporting goods space, with YY (Yue Yuen) likely delivering a more meaningful beat. Having said that, we believe the results and management comments will improve the sentiment for US-exporting ODMs. We thus recommend buying Eclat, FT (Feng Tay) and we upgrade YY to Buy. PS’s 2017 growth may surprise to the upside, but its 4Q16 results may miss. Any weakness post results should be a buying opportunity. We expect the market to digest emerging uncertainties on SZ (Shenzhou) and LN (Li Ning). We view Anta’s multi-brand strength as priced-in, with growing uncertainties on the Anta Adult orderbook. We thus downgrade it to Hold. Upcoming results: be selective; US recovery is our best theme For ODMs: YY’s 4Q16 earnings may beat market expectations, while Eclat and FT could be mixed. Nevertheless, we expect the US-driven exporters to deliver positive comments regarding a US market recovery. SZ’s 2H16 results should be in line, but we anticipate more investor questions on its 2017 growth outlook. For domestic sportswear companies: Anta’s 2H16 earnings are likely to beat consensus, thanks to heavier inventory build by wholesalers during 2H16. We lack conviction on LN’s 2H16 earnings but expect positives including off-line and e-commerce sell-through growth. PS’s 4Q16 earnings may miss due to unsuccessful discount in November (highlighted previously). Incremental to our view: higher conviction on US-exporting ODMs Eclat will likely add a new e-commerce private label client in 3Q17. Our recent conversations with Eclat’s private competitors show the strong demand for jacquard fabric and Eclat’s dominant position. YY will likely benefit from Adidas’s order shift from Apache. Our profit analysis uncovers YY’s significant non-recurring loss in 2016 and potential to recover. FT’s anchor basketball shoes have finally entered mass production. This, along with better demand for the Kobe Bryant series, will likely boost FT’s shares. PS should demonstrate stronger-than-expected momentum in 2017. We also detected the first breakeven of PS’s e-commerce business in 2016. Some issues the markets need to digest SZ: 2017 gross margin pressure and a slowdown in Flyknit upper orders may lead to uncertainties. But we argue the negatives are temporary by nature. LN’s 2017 expenses outlook may be higher than some investors’ expectation. But we view the expenses as necessary investments to optimize its channels. Also, LN’s profitable e-commerce business shouldn’t be ignored by investors. Anta: we estimate a slight rise in inventory levels. Although the current level (5-6 months) is far from the crisis level (over 10 months), we anticipate Anta’s wholesalers to reduce orders from the 4Q17 sales fair, to take a breather. Valuation and risks to our positive industry view We value the sporting goods sector using DCF, as we expect investors to focus on the sector’s long-term value creation. For WACC, we follow DB’s view on RFR and ERP while assigning a beta of 0.9 to 1.3 and terminal growth of 1-2%. Downside risks: weaker cyclical recovery, weaker innovation, sports segmentation ad e-commerce failing to drive sector growth. Upside risks (Anta): faster destocking by wholesalers, stronger performance by new brands. Distributed on: 20/02/2017 22:57:48 GMT

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Deutsche Bank Markets Research

Asia

China

Consumer

Industry

Greater China Sporting Goods

Date

21 February 2017

Recommendation Change

FY16 preview: Time to buy US-exporting ODMs; upgrading YY to Buy Buy Eclat, YY, FT & PS; stay cautious into Anta’s 2H16 results

________________________________________________________________________________________________________________

Deutsche Bank AG/Hong Kong

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016.

John Chou

Research Analyst

(+852 ) 2203 6196

Anne Ling

Research Analyst

(+852 ) 2203 6177

Key Changes

Company Target Price Rating

0551.HK 35.00 to 38.00(HKD)

Hold to Buy

1476.TW 435.00 to 430.00(TWD)

-

2313.HK 62.00 to 56.00(HKD)

-

9910.TW 170.00 to 156.00(TWD)

-

2020.HK 24.00 to 26.50(HKD)

Buy to Hold

2331.HK 6.20 to 5.90(HKD) -

Source: Deutsche Bank

Top picks

Yue Yuen (0551.HK),HKD26.95 Buy

Eclat Textile (1476.TW),TWD309.00 Buy

Feng Tay (9910.TW),TWD130.00 Buy

Pou Sheng (3813.HK),HKD1.94 Buy

Source: Deutsche Bank

The upcoming earnings could be mixed for the sporting goods space, with YY (Yue Yuen) likely delivering a more meaningful beat. Having said that, we believe the results and management comments will improve the sentiment for US-exporting ODMs. We thus recommend buying Eclat, FT (Feng Tay) and we upgrade YY to Buy. PS’s 2017 growth may surprise to the upside, but its 4Q16 results may miss. Any weakness post results should be a buying opportunity. We expect the market to digest emerging uncertainties on SZ (Shenzhou) and LN (Li Ning). We view Anta’s multi-brand strength as priced-in, with growing uncertainties on the Anta Adult orderbook. We thus downgrade it to Hold.

Upcoming results: be selective; US recovery is our best theme For ODMs: YY’s 4Q16 earnings may beat market expectations, while Eclat and FT could be mixed. Nevertheless, we expect the US-driven exporters to deliver positive comments regarding a US market recovery. SZ’s 2H16 results should be in line, but we anticipate more investor questions on its 2017 growth outlook. For domestic sportswear companies: Anta’s 2H16 earnings are likely to beat consensus, thanks to heavier inventory build by wholesalers during 2H16. We lack conviction on LN’s 2H16 earnings but expect positives including off-line and e-commerce sell-through growth. PS’s 4Q16 earnings may miss due to unsuccessful discount in November (highlighted previously).

Incremental to our view: higher conviction on US-exporting ODMs Eclat will likely add a new e-commerce private label client in 3Q17. Our recent conversations with Eclat’s private competitors show the strong demand for jacquard fabric and Eclat’s dominant position. YY will likely benefit from Adidas’s order shift from Apache. Our profit analysis uncovers YY’s significant non-recurring loss in 2016 and potential to recover. FT’s anchor basketball shoes have finally entered mass production. This, along with better demand for the Kobe Bryant series, will likely boost FT’s shares. PS should demonstrate stronger-than-expected momentum in 2017. We also detected the first breakeven of PS’s e-commerce business in 2016.

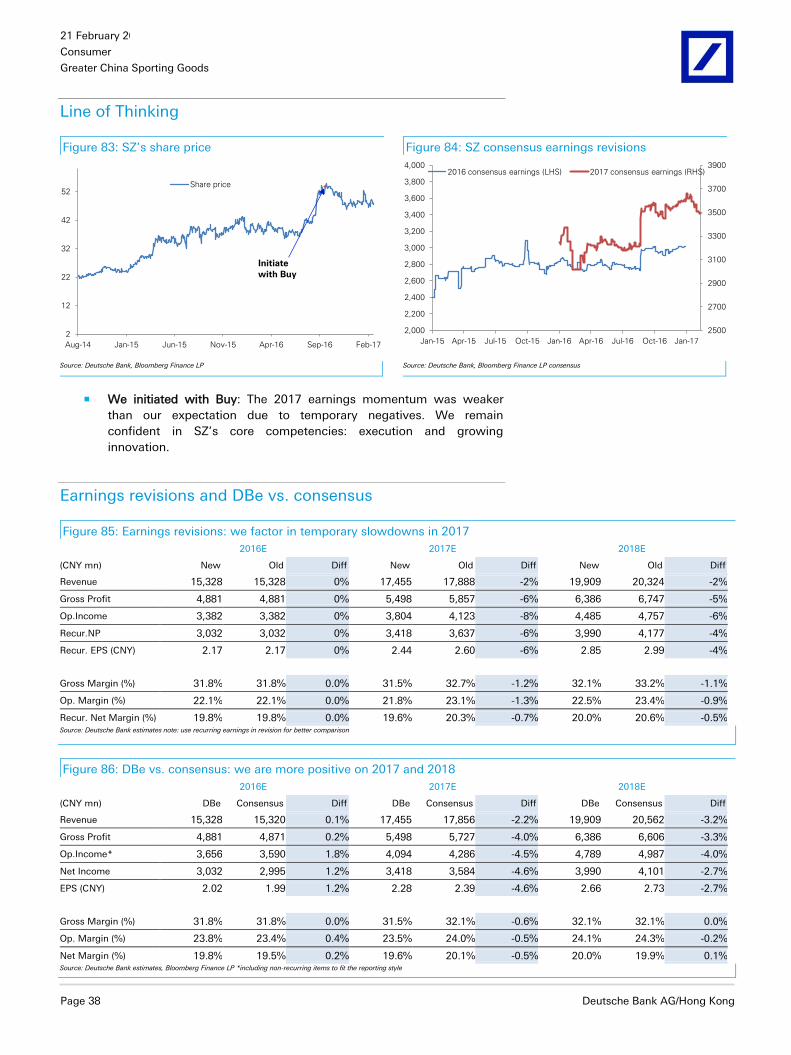

Some issues the markets need to digest SZ: 2017 gross margin pressure and a slowdown in Flyknit upper orders may lead to uncertainties. But we argue the negatives are temporary by nature. LN’s 2017 expenses outlook may be higher than some investors’ expectation. But we view the expenses as necessary investments to optimize its channels. Also, LN’s profitable e-commerce business shouldn’t be ignored by investors. Anta: we estimate a slight rise in inventory levels. Although the current level (5-6 months) is far from the crisis level (over 10 months), we anticipate Anta’s wholesalers to reduce orders from the 4Q17 sales fair, to take a breather.

Valuation and risks to our positive industry view We value the sporting goods sector using DCF, as we expect investors to focus on the sector’s long-term value creation. For WACC, we follow DB’s view on RFR and ERP while assigning a beta of 0.9 to 1.3 and terminal growth of 1-2%. Downside risks: weaker cyclical recovery, weaker innovation, sports segmentation ad e-commerce failing to drive sector growth. Upside risks (Anta): faster destocking by wholesalers, stronger performance by new brands.

Distributed on: 20/02/2017 22:57:48 GMT

21 February 2017

Consumer

Greater China Sporting Goods

Page 2 Deutsche Bank AG/Hong Kong

2H16 /4Q16 preview

Our best ideas and what’s likely to drive the share price

Idea 1: Buy Eclat now New clients: likely including a private activewear label by a major e-

commerce operator (Figure 17).

New products in robust demand: private competitors’ interviews unveil the strong potential of jacquard (Figure 18).

Idea 2: Buy Yue Yuen now; upgrading it to Buy Painful plant shift finally done: The China plants profit analysis points

to significant room for improvement (Figure 31).

Adidas order shift boosts revenue: Apache’s order loss (Figure 39).

Idea 3: Buy Feng Tay now Lebron James Signature has started mass production and Kobe Bryant

line is surprisingly strong (Figure 50).

Nike’s recovery (Figure 52).

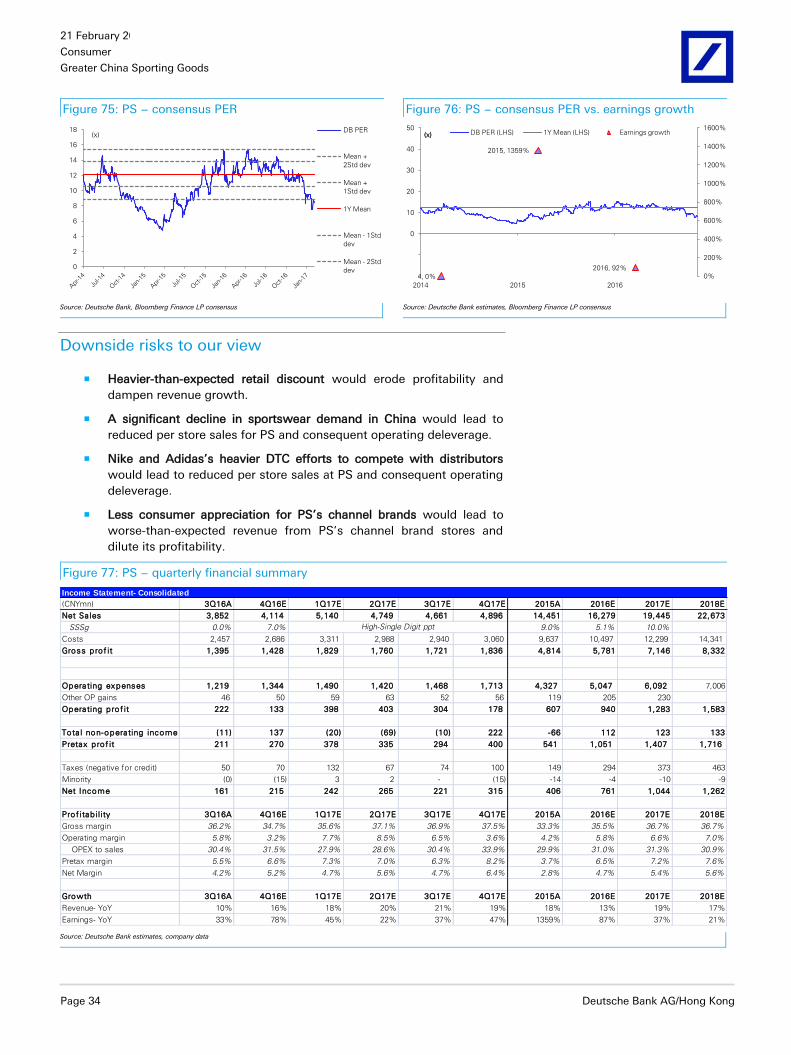

Idea 4: Buy Pou Sheng, any weakness post results should be seen as buying

opportunity 2017 revenue growth to outpace market expectation (Figure 65).

In-house e-commerce likely turned profitable in 2016 (Figure 66).

Concerns on accounting mistreatment soon removed.

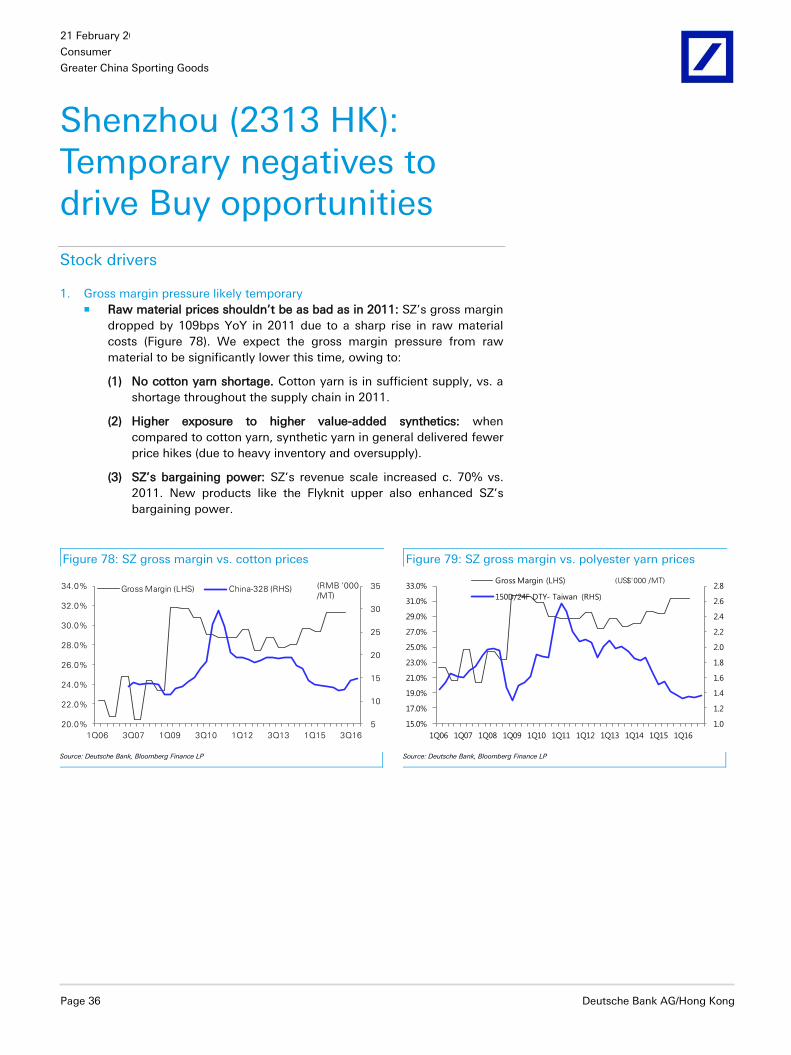

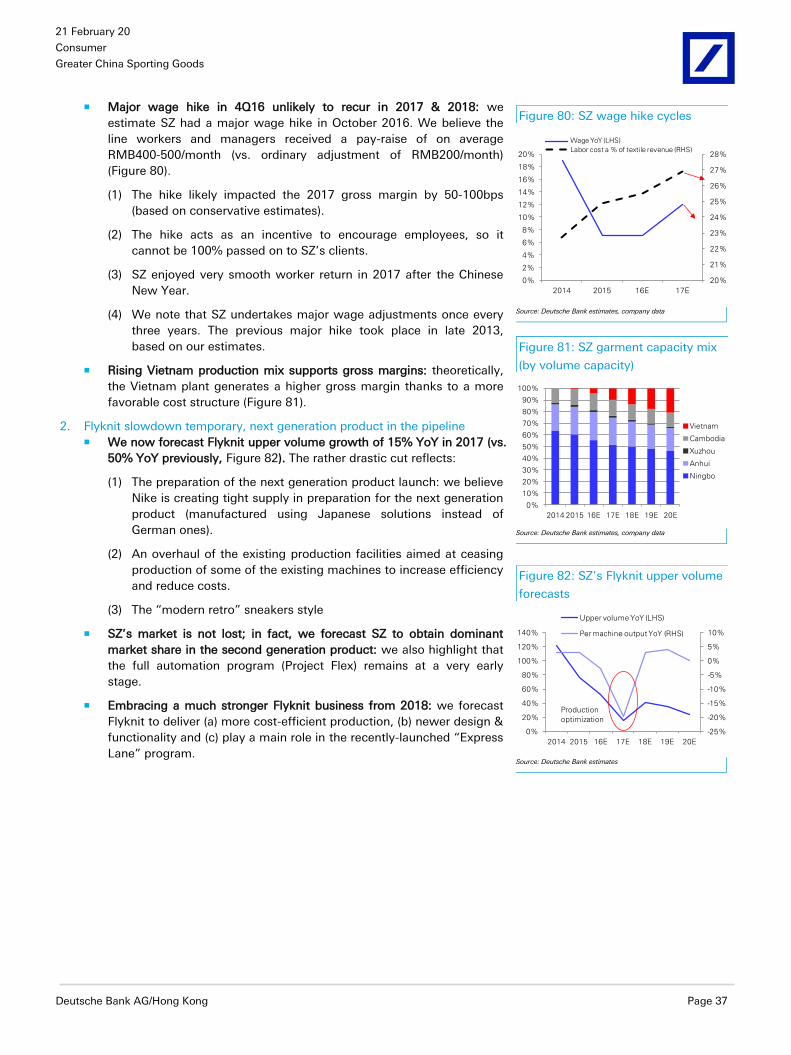

Shenzhou: non-recurring negatives to drive Buy opportunities Gross margin pressure from once-every-three-year wage hike (Figure

80).

Flyknit order slowdown temporary (Figure 82).

Li Ning: constructively increasing 2017 expenses Investment in channels (Figure 93).

Profitable e-commerce business (Figure 96).

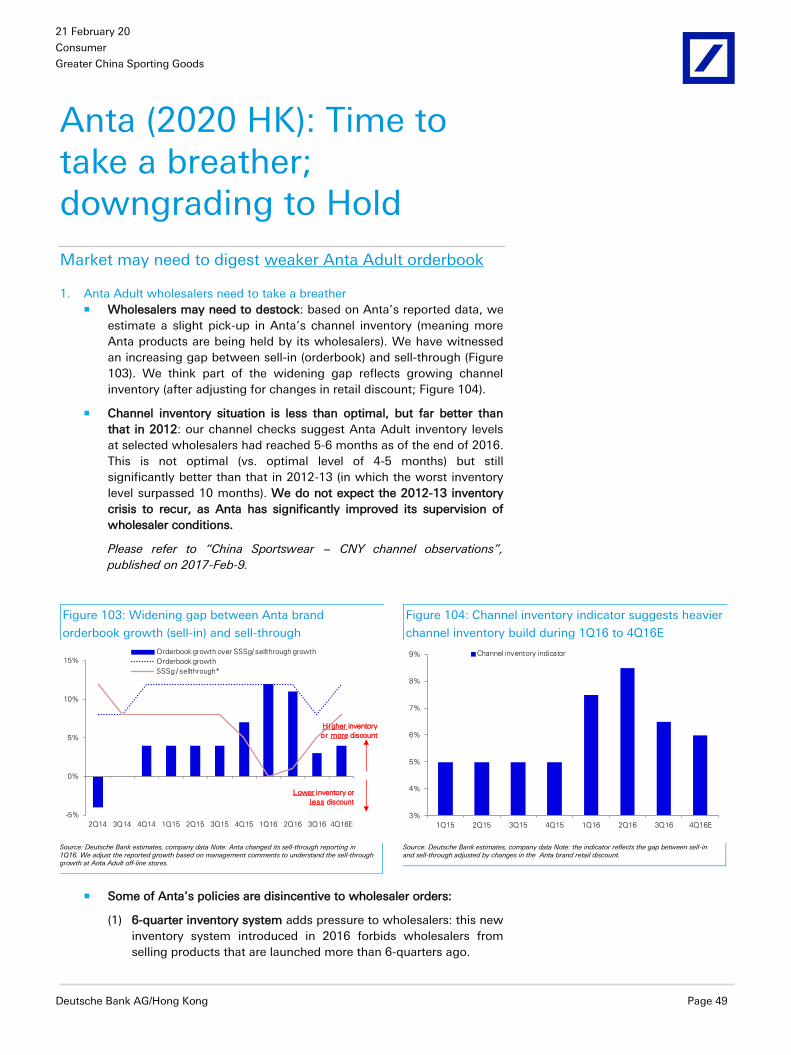

Anta: market may need to digest Anta Adult orderbook; downgrading to Hold Anta Adult wholesalers may need to destock (Figure 103).

Multi-brand strategy performing well (Figure 109).

Figure 1: Top picks – US-exporting ODMs (Eclat, Yue Yuen, Feng Tay), also Pou Sheng

Name Ticker Rating Mkt Cap Close PX Target PX Upside Methodology Revenue mix (2015) 17E PER 17E EPS Dividend

(USDbn) (local) (local) YoY Yield

Eclat 1476 HK Buy 2.5 309 430 39% DCF (25x PER*) Major sports brands (30%)

Private label (30%)

18 23% 3%

Yue Yuen 551 HK Buy 5.7 26.95 38 41% DCF (15x PER*) ODM: NKE (27%), ADS (23%) 11 9% 6%

Feng Tay 9910 TT Buy 2.3 130 156 20% DCF (19x PER*) NKE (81%, basketball shoes) 16 15% 4%

Pou Sheng 3813 HK Buy 1.3 1.94 3.1 60% DCF (14x PER*) Retail (80%), Wholesale (20%) 9 36% 2%

Shenzhou 2313 HK Buy 8.6 47.7

56 17% DCF (21x PER*) Uniqlo (30%), NKE (30%)

ADS (22%)

19 13% 3%

Li Ning 2331 HK Buy 1.5 5.15 5.9 15% DCF (21x PER*) Wholesale (55%), Retail (34%) 17 73% 2%

Anta 2020 HK Hold 8.1 25 26.5 6% DCF (21x PER*) Anta brand (83%), Fila (17%) 19 21% 3%

Source: Deutsche Bank estimates, Bloomberg Finance LP, Company data *2017 PER, Using closing price as of 20 February 2017

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 3

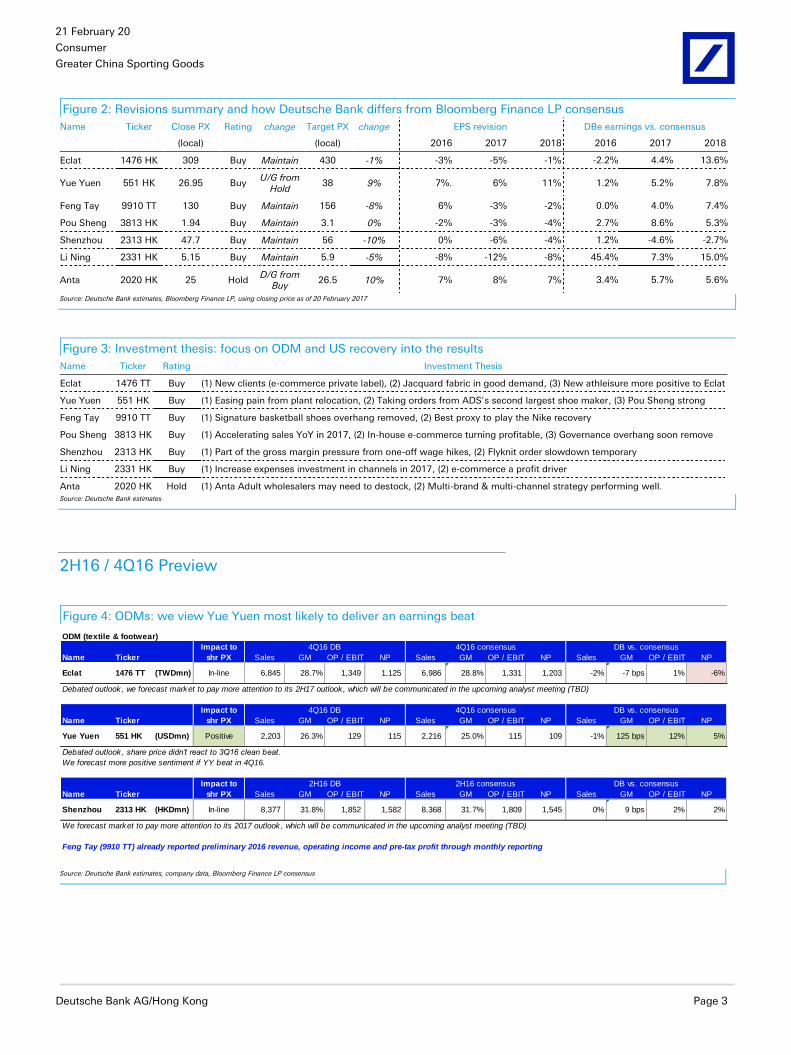

Figure 2: Revisions summary and how Deutsche Bank differs from Bloomberg Finance LP consensus

Name Ticker Close PX Rating change Target PX change EPS revision DBe earnings vs. consensus

(local) (local) 2016 2017 2018 2016 2017 2018

Eclat 1476 HK 309 Buy Maintain 430 -1% -3% -5% -1% -2.2% 4.4% 13.6%

Yue Yuen 551 HK 26.95 Buy U/G from

Hold 38 9% 7%. 6% 11% 1.2% 5.2% 7.8%

Feng Tay 9910 TT 130 Buy Maintain 156 -8% 6% -3% -2% 0.0% 4.0% 7.4%

Pou Sheng 3813 HK 1.94 Buy Maintain 3.1 0% -2% -3% -4% 2.7% 8.6% 5.3%

Shenzhou 2313 HK 47.7 Buy Maintain 56 -10% 0% -6% -4% 1.2% -4.6% -2.7%

Li Ning 2331 HK 5.15 Buy Maintain 5.9 -5% -8% -12% -8% 45.4% 7.3% 15.0%

Anta 2020 HK 25 Hold D/G from

Buy 26.5 10% 7% 8% 7% 3.4% 5.7% 5.6%

Source: Deutsche Bank estimates, Bloomberg Finance LP, using closing price as of 20 February 2017

Figure 3: Investment thesis: focus on ODM and US recovery into the results

Name Ticker Rating Investment Thesis

Eclat 1476 TT Buy (1) New clients (e-commerce private label), (2) Jacquard fabric in good demand, (3) New athleisure more positive to Eclat

Yue Yuen 551 HK Buy (1) Easing pain from plant relocation, (2) Taking orders from ADS’s second largest shoe maker, (3) Pou Sheng strong

Feng Tay 9910 TT Buy (1) Signature basketball shoes overhang removed, (2) Best proxy to play the Nike recovery

Pou Sheng 3813 HK Buy (1) Accelerating sales YoY in 2017, (2) In-house e-commerce turning profitable, (3) Governance overhang soon remove

Shenzhou 2313 HK Buy (1) Part of the gross margin pressure from one-off wage hikes, (2) Flyknit order slowdown temporary

Li Ning 2331 HK Buy (1) Increase expenses investment in channels in 2017, (2) e-commerce a profit driver

Anta 2020 HK Hold (1) Anta Adult wholesalers may need to destock, (2) Multi-brand & multi-channel strategy performing well. Source: Deutsche Bank estimates

2H16 / 4Q16 Preview

Figure 4: ODMs: we view Yue Yuen most likely to deliver an earnings beat

ODM (textile & footwear)

Impact to

Name Ticker shr PX Sales GM OP / EBIT NP Sales GM OP / EBIT NP Sales GM OP / EBIT NP

Eclat 1476 TT (TWDmn) In-line 6,845 28.7% 1,349 1,125 6,986 28.8% 1,331 1,203 -2% -7 bps 1% -6%

Debated outlook, we forecast market to pay more attention to its 2H17 outlook, which will be communicated in the upcoming analyst meeting (TBD)

Impact to

Name Ticker shr PX Sales GM OP / EBIT NP Sales GM OP / EBIT NP Sales GM OP / EBIT NP

Yue Yuen 551 HK (USDmn) Positive 2,203 26.3% 129 115 2,216 25.0% 115 109 -1% 125 bps 12% 5%

Debated outlook, share price didn’t react to 3Q16 clean beat.

We forecast more positive sentiment if YY beat in 4Q16.

Impact to

Name Ticker shr PX Sales GM OP / EBIT NP Sales GM OP / EBIT NP Sales GM OP / EBIT NP

Shenzhou 2313 HK (HKDmn) In-line 8,377 31.8% 1,852 1,582 8,368 31.7% 1,809 1,545 0% 9 bps 2% 2%

We forecast market to pay more attention to its 2017 outlook, which will be communicated in the upcoming analyst meeting (TBD)

Feng Tay (9910 TT) already reported preliminary 2016 revenue, operating income and pre-tax profit through monthly reporting

4Q16 DB 4Q16 consensus DB vs. consensus

4Q16 DB 4Q16 consensus DB vs. consensus

2H16 DB 2H16 consensus DB vs. consensus

Source: Deutsche Bank estimates, company data, Bloomberg Finance LP consensus

21 February 2017

Consumer

Greater China Sporting Goods

Page 4 Deutsche Bank AG/Hong Kong

Figure 5: Sportswear: we expect solid earnings and operation data from Anta, but 2017 orderbook outlook may see

risks. We forecast positive operation data from Li Ning

Sportswear (domestic brands & distributors)

Impact to

Name Ticker shr PX Sales GM OP / EBIT NP Sales GM OP / EBIT NP Sales GM OP / EBIT NP

Anta 2020 HK (CNYmn) Positive 7,637 47.5% 1,785 1,339 7,204 47.8% 1,645 1,257 6% -27 bps 9% 7%

Strong earnings growth in 2H16 likely well-communicated with investors.

Impact to

shr PX +ve / -ve DB Consen. Previous +ve / -ve DB Consen. Previous +ve / -ve DB Consen. Previous*

Anta 2020 HK OP data Mixed +ve +HSD~LDD +HSD +LDD =ve +LSD~MSD +LSD~MSD +MSD -ve Guide dow n No change +MSD~HSD

We see more downside to 4Q17 orderbook YoY

*meaning previous target

Impact to

Name Ticker shr PX Sales GM OP / EBIT NP Sales GM OP / EBIT NP Sales GM OP / EBIT NP

Li Ning 2331 HK (CNYmn)Positive (lack of

conviction)4,496 47.0% 291 415 4,461 45.6% 253 250 1% 138 bps 15% 66%*

We don't have conviction on the 2H16 earnings (due to the vast moving parts), but we remain confident in the turnaround trend

*our forecasts include DHS disposal & revaluation gains

Impact to

shr PX +ve / -ve DB Consen. Prev. +ve / -ve DB Consen. Prev. +ve / -ve DB Consen. Prev.*

Li Ning 2331 HK OP data Positive +ve +HSD~LDD +MSD~HSD +HSD +ve +HSD +MSD +HSD =ve no change n.a. +L-M teen

We expect acceleration in sellthrough driven by (1) off-line and (2) e-commerce

*meaning previous target

Impact to

Name Ticker shr PX Sales GM OP / EBIT NP Sales GM OP / EBIT NP Sales GM OP / EBIT NP

Pou Sheng 3813 HK (CNYmn) Negative 4,114 34.7% 133 215 4,341 36.3% 146 195 -5% -162 bps -9% 10%

2017 consensus forecasts may be somewhat stall:

PS's reported 4Q16 revenue resulted lower than the headline consensus, but actually beat market's latest expectation (evidenced by share price rally).

2H16 DB 2H16 consensus DB vs. consensus

4Q16 DB 4Q16 consensus DB vs. consensus

4Q16 Sellthrough YoY 3Q17 Orderbook YoY 2017 Orderbook YoY

2H16 DB 2H16 consensus DB vs. consensus

4Q16 SSSg 3Q17 Orderbook YoY 2017 Orderbook YoY

Source: Deutsche Bank estimates, company data, Bloomberg Finance LP consensus

Valuation tools

Figure 6: Valuation comps: textile and footwear ODMs

Name Ticker PX_Last Market Cap DB rating

(local cur.) (US$mn) FY16 FY17 FY16 FY17 FY16 FY17 FY16 FY17 FY16 FY17

Textile

Shenzhou 2313 HK 47.7 8,598 Buy 21.0 18.6 25% 13% 4.1 3.8 22.2% 24.3% 3.4% 3.3%

Eclat 1476 TT 309 2,699 Buy 22.8 18.4 -10% 23% 5.5 4.8 26.3% 29.3% 3.4% 3.0%

Texwinca 321 HK 5.15 917 Hold 10.1 13.3 36% -39% 1.9 1.4 18.5% 11.3% 8.1% 7.5%

Best Pacific 2111 HK 6.1 809 NR 14.2 12.0 28% 18% 3.1 2.7 23.1% 23.7% 2.8% 3.2%

Makalot 1477 TT 123 826 NR 13.3 16.1 -12% -17% 2.9 2.7 18.1% 17.5% 6.2% 5.0%

FENC 1402 TT 27.25 4,736 NR 24.3 19.2 -30% 27% 0.8 0.7 3.1% 3.9% 3.3% 3.8%

Formosa Taffeta 1434 TT 31.2 1,707 NR 15.3 13.5 22% 13% 1.0 1.0 6.3% 7.1% 4.6% 5.3%

Youngone 111770 KS 30100 1,163 NR 10.2 9.8 1% 4% 1.1 1.0 10.7% 10.2% 0.7% 0.7%

Hansae 105630 KS 25100 876 NR 14.3 13.2 -23% 8% 2.1 1.8 15.4% 15.0% 1.1% 1.2%

Pacific 1382 HK 8.75 1,631 NR 12.7 12.3 -7% 3% 3.8 3.8 30.0% 31.0% 8.2% 8.2%

Luthai 200726 CH 9.26 1,435 NR 9.7 8.6 13% 13% 1.0 0.9 10.6% 11.0% 6.9% 7.7%

Texhong 2678 HK 11.84 1,396 NR 8.3 7.6 89% 9% 2.0 1.7 25.7% 21.1% 3.6% 3.9%

Average 18.1 15.8 9% 12% 2.8 2.6 17.3% 18.0% 4.0% 4.1%

Footweaer ODM

Feng Tay 9910 TT 130 2,819 Buy 17.5 16.1 8% 8% 5.9 5.3 34.9% 37.8% 3.8% 4.0%

Yue Yuen 551 HK 26.95 5,726 Buy 11.6 10.6 20% 9% 1.2 1.2 10.1% 10.7% 5.2% 5.7%

Stella 1836 HK 10.78 1,103 NR 13.5 11.8 -33% 15% 1.1 1.1 8.1% 9.3% 7.4% 7.6%

Average 13.5 12.3 10% 10% 2.6 2.4 17.1% 18.5% 5.1% 5.4%

PE EPS YoY PB ROE Div. Yield

Source: Deutsche Bank estimates, Bloomberg Finance LP Note: companies under Deutsche Bank coverage use Deutsche Bank estimates; other companies use Bloomberg Finance LP consensus. To determine which companies are under Deutsche Bank coverage, please refer to column “DB rating.” Using closing price as of 17 February 2017.

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 5

Figure 7: Valuation comps: sportswear brands and distributors

Name Ticker PX_Last Market Cap DB rating

(local cur.) (US$mn) FY16 FY17 FY16 FY17 FY16 FY17 FY16 FY17 FY16 FY17

China Sportswear Brands & Distributors

Anta 2020 HK 25 8,061 Hold 22.5 18.5 21% 21% 5.9 5.4 25.2% 27.8% 2.7% 3.2%

Li Ning 2331 HK 5.15 1,443 Buy 21.2 17.4 >100% 73% 1.5 2.1 17.1% 19.0% 2.0% 2.5%

Belle 1880 HK 5.1 5,542 Buy 8.9 10.1 -10% -12% 1.7 1.6 17.2% 14.6% 4.9% 5.9%

Pou Sheng 3813 HK 1.94 1,334 Buy 11.9 8.8 66% 36% 1.5 1.3 13.3% 16.3% 0.0% 2.2%

XTEP 1368 HK 3.58 1,024 NR 10.0 9.0 9% 11% 1.4 1.3 14.1% 14.6% 5.8% 6.5%

CNDX 3818 HK 1.49 1,063 NR 8.6 10.5 5% -18% 0.7 0.7 8.7% 7.2% 6.8% 5.8%

361 Degrees 1361 HK 3.08 821 NR 10.9 9.5 0% 15% 1.0 0.9 9.0% 9.9% 5.8% 4.8%

Average 15.8 14.0 11% 14% 3.3 3.1 19.3% 19.9% 3.6% 4.3%

Global SPA

Inditex ITX SQ 31.245 103,427 Hold 33.8 30.3 15% 12% 8.5 7.8 26.3% 26.8% 2.2% 2.5%

H&M HMB SS 244 45,329 Sell 21.7 19.6 -11% 10% 6.6 6.1 31.2% 32.4% 4.5% 4.5%

Fast Retailing 9983 JP 34990 32,825 Hold 71.2 28.1 -56% 154% 6.0 5.2 7.0% 18.9% 1.1% 1.3%

Average 37.6 27.2 -4% 37% 7.6 6.9 24.0% 26.8% 2.6% 2.8%

Global Sports Brands

Lululemon LULU US 66.73 9,147 Hold 35.8 31.3 -1% 14% 9.1 6.8 24.8% 24.7% 0.0% 0.0%

Under Armour UA US 19.75 9,082 Hold 34.0 n.a. 10% n.a. 4.3 3.9 14.0% 8.7% 0.0% 0.0%

Adidas ADS GR 148.9 33,087 Buy 32.0 25.3 31% 26% 5.0 4.8 17.8% 19.6% 1.4% 1.6%

Amer Sports AMEAS FH 22.4 2,820 Buy 19.0 16.2 9% 17% 2.6 2.4 13.0% 14.8% 3.1% 3.0%

Puma PUM GY 299.75 4,802 Buy 71.9 35.9 68% 100% 2.6 2.5 3.8% 7.1% 0.3% 0.6%

Skechers SKX US 26.28 4,167 NR 16.7 14.9 5% 13% 2.6 2.2 16.6% 15.5% 0.0% 0.0%

VF VFC US 52.68 21,794 NR 16.8 n.a. 3% n.a. 4.3 4.4 25.1% 28.5% 3.1% 3.1%

Columbia COLM US 56.81 3,965 NR 20.9 20.2 11% 3% 2.5 2.3 13.0% 12.0% 1.4% 1.5%

Nike NKE US 56.75 93,892 Buy 26.3 24.2 17% 9% 8.1 7.9 30.1% 32.5% 1.2% 1.3%

Average 27.0 24.8 16% 13% 6.7 6.5 25.6% 27.3% 1.3% 1.4%

Global Apparel Brands

RL RL US 78.39 6,445 NR 12.3 n.a. -19% n.a. 1.8 1.8 13.8% 8.8% 2.8% 2.9%

GAP GPS US 24.47 9,761 Hold 10.1 12.1 -14% -17% 4.0 3.3 33.3% 23.7% 4.2% 4.2%

A&F ANF US 12.2 826 Sell 10.9 n.a. -27% n.a. 0.7 0.7 5.8% -0.9% 7.3% 7.4%

Guess GES US 13.02 1,098 NR 26.2 19.8 -50% 32% 1.1 1.1 5.4% 6.3% 7.8% 8.0%

Average 11.9 12.9 -19% -12% 2.9 2.5 23.4% 16.2% 4.1% 4.1%

Average 32.0 25.8 3% 27% 7.0 6.5 24.5% 26.3% 2.2% 2.4%

PB ROE Div. YieldPER EPS YoY

Source: Deutsche Bank estimates, Bloomberg Finance LP Note: companies under Deutsche Bank coverage use Deutsche Bank estimates; other companies use Bloomberg Finance LP consensus. To determine which companies are under Deutsche Bank coverage, please refer to column “DB rating.” Using closing price as of 17 February 2017.

Figure 8: Eclat: consensus PER (12-month forward) Figure 9: Yue Yuen: consensus PER (12-month forward)

0

5

10

15

20

25

30

35

40

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

DB PER

Mean +

2Std dev

Mean +

1Std dev

2Y Mean

Mean - 1Std

dev

Mean - 2Std

dev

(x)

8

9

10

11

12

13

14

15

2013 2014 2015 2016 2017

DB PER

Mean +

2Std dev

Mean +

1Std dev

2Y Mean

Mean - 1Std

dev

Mean - 2Std

dev

(x)

Source: Deutsche Bank, Bloomberg Finance LP

Source: Deutsche Bank, Bloomberg Finance LP

21 February 2017

Consumer

Greater China Sporting Goods

Page 6 Deutsche Bank AG/Hong Kong

Figure 10: Feng Tay: consensus PER (12-month forward)

Figure 11: Pou Sheng: consensus PER (12-month

forward)

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

DB PER

Mean +

2Std dev

Mean +

1Std dev

2Y Mean

Mean - 1Std

dev

Mean - 2Std

dev

(x)

0

2

4

6

8

10

12

14

16

18 DB PER

Mean +

2Std dev

Mean +

1Std dev

1Y Mean

Mean - 1Std

dev

Mean - 2Std

dev

(x)

Source: Deutsche Bank, Bloomberg Finance LP

Source: Deutsche Bank, Bloomberg Finance LP

Figure 12: Shenzhou: consensus PER (12-month forward) Figure 13: Li Ning: consensus PER (12-month forward)

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

DB PER

Mean +

2Std dev

Mean +

1Std dev

2Y Mean

Mean - 1Std

dev

Mean - 2Std

dev

(x)

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Li Ning PER

Mean +

2Std dev

Mean +

1Std dev

Mean

Mean -

1Std dev

Mean -

2Std dev

(x)

Source: Deutsche Bank, Bloomberg Finance LP

Source: Deutsche Bank, Bloomberg Finance LP

Figure 14: Anta: consensus PER (12-month forward)

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Anta PER

Mean +

2Std dev

Mean +

1Std dev

1Y Mean

Mean -

1Std dev

Mean -

2Std dev

(x)

Source: Deutsche Bank, Bloomberg Finance LP

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 7

Eclat (1476 TT): All about product cycles; Buy

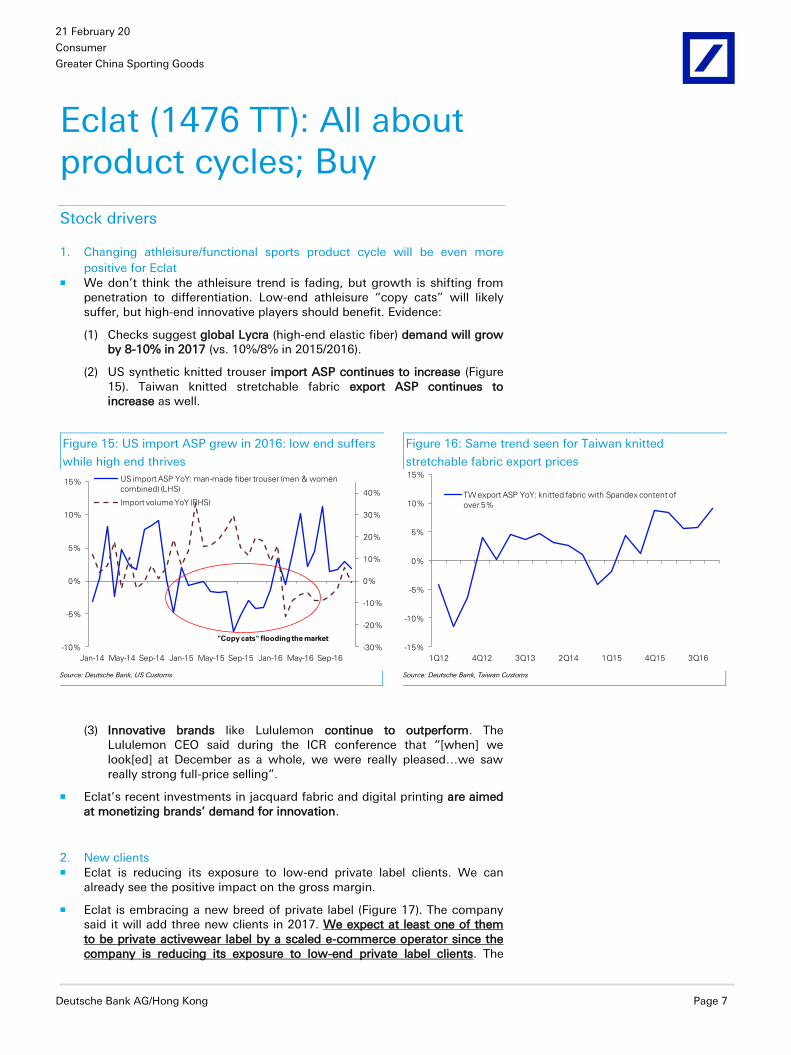

Stock drivers

1. Changing athleisure/functional sports product cycle will be even more

positive for Eclat We don’t think the athleisure trend is fading, but growth is shifting from

penetration to differentiation. Low-end athleisure “copy cats” will likely suffer, but high-end innovative players should benefit. Evidence:

(1) Checks suggest global Lycra (high-end elastic fiber) demand will grow by 8-10% in 2017 (vs. 10%/8% in 2015/2016).

(2) US synthetic knitted trouser import ASP continues to increase (Figure 15). Taiwan knitted stretchable fabric export ASP continues to increase as well.

Figure 15: US import ASP grew in 2016: low end suffers

while high end thrives

Figure 16: Same trend seen for Taiwan knitted

stretchable fabric export prices

-30%

-20%

-10%

0%

10%

20%

30%

40%

-10%

-5%

0%

5%

10%

15%

Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16

US import ASP YoY: man-made fiber trouser (men & women

combined) (LHS)

Import volume YoY (RHS)

"Copy cats" flooding the market

-15%

-10%

-5%

0%

5%

10%

15%

1Q12 4Q12 3Q13 2Q14 1Q15 4Q15 3Q16

TW export ASP YoY: knitted fabric with Spandex content of

over 5%

Source: Deutsche Bank, US Customs Source: Deutsche Bank, Taiwan Customs

(3) Innovative brands like Lululemon continue to outperform. The Lululemon CEO said during the ICR conference that “[when] we look[ed] at December as a whole, we were really pleased…we saw really strong full-price selling”.

Eclat’s recent investments in jacquard fabric and digital printing are aimed at monetizing brands’ demand for innovation.

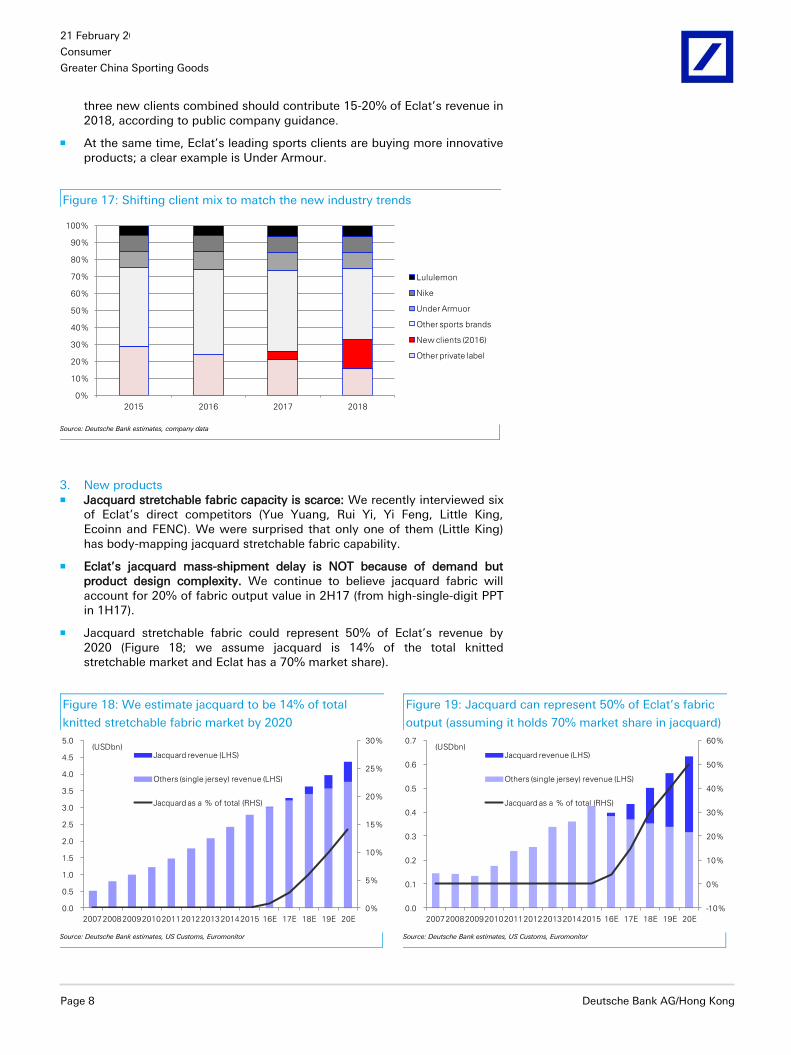

2. New clients Eclat is reducing its exposure to low-end private label clients. We can

already see the positive impact on the gross margin.

Eclat is embracing a new breed of private label (Figure 17). The company said it will add three new clients in 2017. We expect at least one of them to be private activewear label by a scaled e-commerce operator since the company is reducing its exposure to low-end private label clients. The

21 February 2017

Consumer

Greater China Sporting Goods

Page 8 Deutsche Bank AG/Hong Kong

three new clients combined should contribute 15-20% of Eclat’s revenue in 2018, according to public company guidance.

At the same time, Eclat’s leading sports clients are buying more innovative products; a clear example is Under Armour.

Figure 17: Shifting client mix to match the new industry trends

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018

Lululemon

Nike

Under Armuor

Other sports brands

New clients (2016)

Other private label

Source: Deutsche Bank estimates, company data

3. New products Jacquard stretchable fabric capacity is scarce: We recently interviewed six

of Eclat’s direct competitors (Yue Yuang, Rui Yi, Yi Feng, Little King, Ecoinn and FENC). We were surprised that only one of them (Little King) has body-mapping jacquard stretchable fabric capability.

Eclat’s jacquard mass-shipment delay is NOT because of demand but product design complexity. We continue to believe jacquard fabric will account for 20% of fabric output value in 2H17 (from high-single-digit PPT in 1H17).

Jacquard stretchable fabric could represent 50% of Eclat’s revenue by 2020 (Figure 18; we assume jacquard is 14% of the total knitted stretchable market and Eclat has a 70% market share).

Figure 18: We estimate jacquard to be 14% of total

knitted stretchable fabric market by 2020

Figure 19: Jacquard can represent 50% of Eclat’s fabric

output (assuming it holds 70% market share in jacquard)

0%

5%

10%

15%

20%

25%

30%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

200720082009201020112012201320142015 16E 17E 18E 19E 20E

Jacquard revenue (LHS)

Others (single jersey) revenue (LHS)

Jacquard as a % of total (RHS)

(USDbn)

-10%

0%

10%

20%

30%

40%

50%

60%

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

200720082009201020112012201320142015 16E 17E 18E 19E 20E

Jacquard revenue (LHS)

Others (single jersey) revenue (LHS)

Jacquard as a % of total (RHS)

(USDbn)

Source: Deutsche Bank estimates, US Customs, Euromonitor Source: Deutsche Bank estimates, US Customs, Euromonitor

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 9

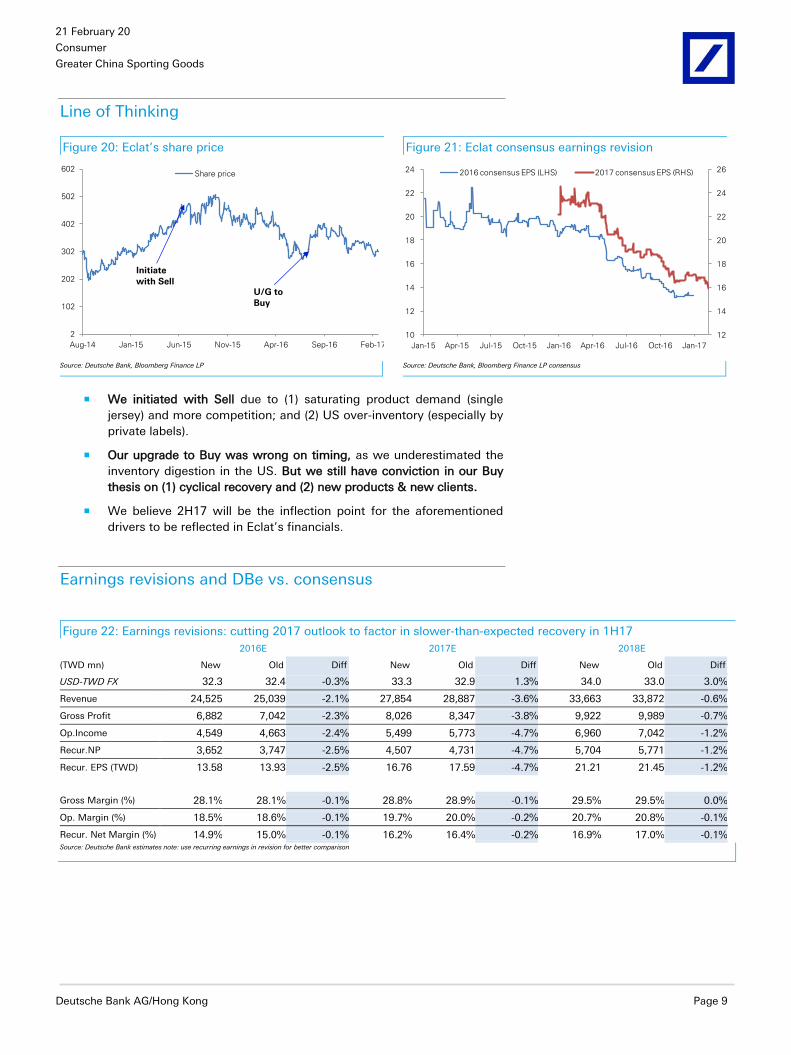

Line of Thinking

Figure 20: Eclat’s share price Figure 21: Eclat consensus earnings revision

2

102

202

302

402

502

602

Aug-14 Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17

Share price

U/G to

Buy

Initiate

with Sell

12

14

16

18

20

22

24

26

10

12

14

16

18

20

22

24

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17

2016 consensus EPS (LHS) 2017 consensus EPS (RHS)

Source: Deutsche Bank, Bloomberg Finance LP

Source: Deutsche Bank, Bloomberg Finance LP consensus

We initiated with Sell due to (1) saturating product demand (single

jersey) and more competition; and (2) US over-inventory (especially by

private labels).

Our upgrade to Buy was wrong on timing, as we underestimated the

inventory digestion in the US. But we still have conviction in our Buy

thesis on (1) cyclical recovery and (2) new products & new clients.

We believe 2H17 will be the inflection point for the aforementioned

drivers to be reflected in Eclat’s financials.

Earnings revisions and DBe vs. consensus

Figure 22: Earnings revisions: cutting 2017 outlook to factor in slower-than-expected recovery in 1H17

2016E 2017E 2018E

(TWD mn) New Old Diff New Old Diff New Old Diff

USD-TWD FX 32.3 32.4 -0.3% 33.3 32.9 1.3% 34.0 33.0 3.0%

Revenue 24,525 25,039 -2.1% 27,854 28,887 -3.6% 33,663 33,872 -0.6%

Gross Profit 6,882 7,042 -2.3% 8,026 8,347 -3.8% 9,922 9,989 -0.7%

Op.Income 4,549 4,663 -2.4% 5,499 5,773 -4.7% 6,960 7,042 -1.2%

Recur.NP 3,652 3,747 -2.5% 4,507 4,731 -4.7% 5,704 5,771 -1.2%

Recur. EPS (TWD) 13.58 13.93 -2.5% 16.76 17.59 -4.7% 21.21 21.45 -1.2%

Gross Margin (%) 28.1% 28.1% -0.1% 28.8% 28.9% -0.1% 29.5% 29.5% 0.0%

Op. Margin (%) 18.5% 18.6% -0.1% 19.7% 20.0% -0.2% 20.7% 20.8% -0.1%

Recur. Net Margin (%) 14.9% 15.0% -0.1% 16.2% 16.4% -0.2% 16.9% 17.0% -0.1% Source: Deutsche Bank estimates note: use recurring earnings in revision for better comparison

21 February 2017

Consumer

Greater China Sporting Goods

Page 10 Deutsche Bank AG/Hong Kong

Figure 23: DBe vs. consensus: we are significantly more positive on 2H17 and 2018

2016E 2017E 2018E

(TWD mn) DBe Consensus Diff DBe Consensus Diff DBe Consensus Diff

Revenue 24,525 24,666 -0.6% 27,854 27,257 2.2% 33,663 30,815 9.2%

Gross Profit 6,882 6,931 -0.7% 8,026 7,795 3.0% 9,922 8,927 11.1%

Op.Income 4,549 4,531 0.4% 5,499 5,278 4.2% 6,960 6,218 11.9%

Net Income 3,425 3,504 -2.2% 4,507 4,319 4.4% 5,704 5,020 13.6%

EPS (TWD) 12.73 13.03 -2.2% 16.76 16.06 4.4% 21.21 18.66 13.6%

Gross Margin (%) 28.1% 28.1% 0.0% 28.8% 28.6% 0.2% 29.5% 29.0% 0.5%

Op. Margin (%) 18.5% 18.4% 0.2% 19.7% 19.4% 0.4% 20.7% 20.2% 0.5%

Net Margin (%) 14.0% 14.2% -0.2% 16.2% 15.8% 0.3% 16.9% 16.3% 0.7% Source: Deutsche Bank estimates, Bloomberg Finance LP

Valuation, risks and financial summary

Cutting target price by 1%, in line with earnings revisions on 2018E

We have trimmed our DCF-based target price to TWD430 to reflect downward

earnings revisions to 2018E. We use the discounted cash flow (DCF) method

as our primary approach to value Eclat’s shares. We adopt DCF as we expect

investors to focus more on Eclat’s long-term innovations. In our DCF model,

we apply a WACC of 6.61% with a cost of equity of 7.08% (risk-free

rate=1.8%, beta=0.94, market risk premium=5.6%) and a cost of debt of

2.43%.

We increased our assumed long-term growth rate to 1%. This is still at the low

end of the 1-2% assumptions we use for other ODMs under our coverage. We

view Eclat’s innovator business model as highly reliant on the new product

cycle. In the past we were skeptical on whether Eclat could innovate beyond

its single jersey category. But with its new jacquard fabric, we are more

positive on Eclat’s ability to sustain its innovation pipeline. We thus increase

the assumption to 1%. Terminal value now represents 45% of Eclat’s total

value.

Figure 24: DCF sales, margin assumptions and sensitivity Figure 25: Free cash flow to equity profile

Two-stage DCF:

1. FCF forecasts from model 2018-2020

2. Explicit forecast period 2021-2030

2018~2021 2022~2025 2026~2030 2018~2030

Revenue CAGR: 20.9% 3.8% 1.0% 6.1%

Average EBIT margin: 21.2% 21.0% 20.1% 20.7%

FCF CAGR: 12.6% 2.1% -0.4% 3.3%

Source: Deutsche Bank estimates

Source: Deutsche Bank estimates, Note: representing free cash flow for equity (in line with Deutsche Bank RTN)

430 7.6% 7.1% 6.6% 6.1% 5.6%

-1.00% 331 351 374 401 431

0.00% 347 371 398 430 467

1.00% 368 397 430 470 519

2.00% 397 433 476 530 599

3.00% 438 486 548 628 740

WACC

Terminal

Growth-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2012 2015 2018 2021 2024 2027 2030

Free Cashflow (LHS)

YoY (RHS)(NT$mn)

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 11

Figure 26: Discounted cash flow valuation – key assumptions

Share & Market Information Note

Valuation date 12 month forward

Current Stock Price 309

Issued Shares (million) 269 Weighted average shares

DCF Target Price 430

Implied Upside (Downside) 39%

Valuation metrics

FY16 PER (recurring) 31.7

FY17 PER (recurring) 25.7

FY16 PBR 7.8

FY17 PBR 6.8

Cost of Equity 7.08%

Risk Free Rate (%) 1.80% Deutsche Bank assumption for Taiwan

Beta 0.94 Bloomberg 1-year beta

Market Risk Premium (%) 5.60% Deutsche Bank assumption for Taiwan

Cost of Debt (after tax) 2.43%

Cost of Debt 3.00% Company long-term borrowing rate

Tax Rate 19.00% Long-term tax rate

Target Debt / (Debt + Equity) 10%

WACC 6.61%

DCF Model LT growth 1.0% We are more positive on Eclat’s ability to sustain innovations.

Source: Deutsche Bank estimates, company data

PE valuation supports our DCF target price; we now shift target multiple to 2-

year mean

Our target price of TWD430 represents c.25x of 2017E recurring EPS. The

multiple is in line with Eclat’s two-year mean forward DB PER. We didn’t

change this implied multiple.

Figure 27: Eclat: consensus PER (12 month forward) Figure 28: Consensus PER vs. earnings growth

0

5

10

15

20

25

30

35

40

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

DB PER

Mean +

2Std dev

Mean +

1Std dev

2Y Mean

Mean - 1Std

dev

Mean - 2Std

dev

(x)

-60%

-10%

40%

90%

140%

-20

-10

0

10

20

30

40

50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

DB PER (LHS) 2Y Mean (LHS) Earnings growth(x)

Source: Deutsche Bank estimates, Bloomberg Finance LP

Source: Deutsche Bank estimates, Bloomberg Finance LP

21 February 2017

Consumer

Greater China Sporting Goods

Page 12 Deutsche Bank AG/Hong Kong

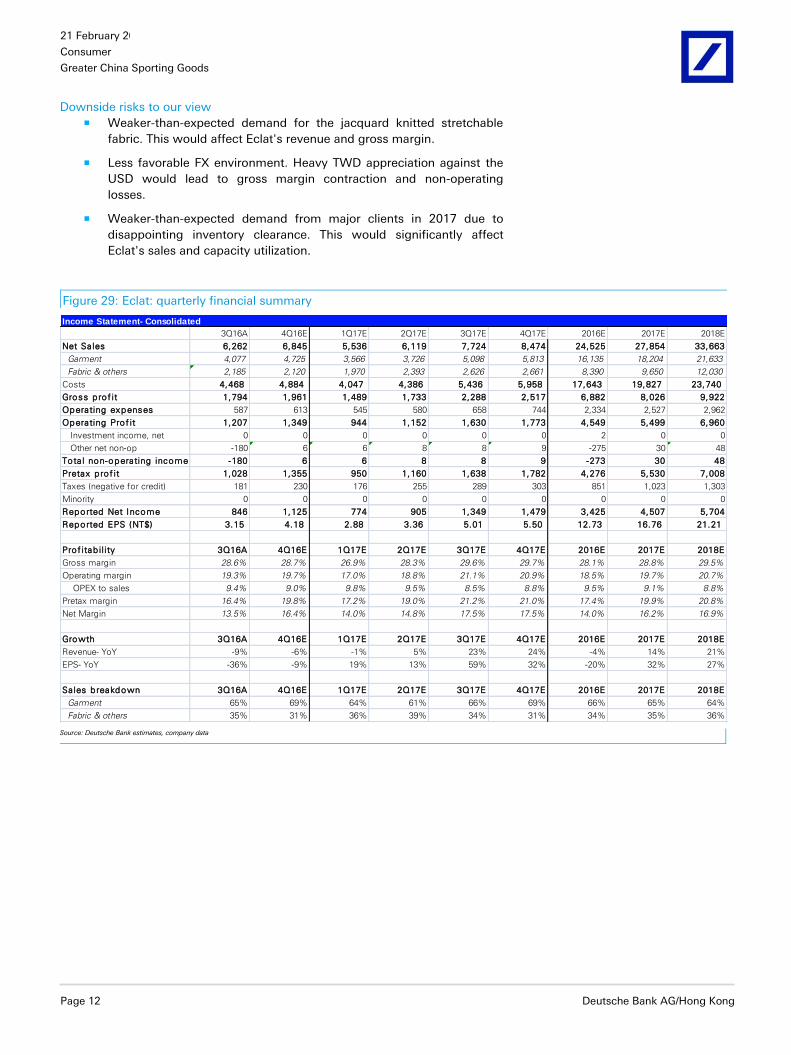

Downside risks to our view Weaker-than-expected demand for the jacquard knitted stretchable

fabric. This would affect Eclat's revenue and gross margin.

Less favorable FX environment. Heavy TWD appreciation against the

USD would lead to gross margin contraction and non-operating

losses.

Weaker-than-expected demand from major clients in 2017 due to

disappointing inventory clearance. This would significantly affect

Eclat's sales and capacity utilization.

Figure 29: Eclat: quarterly financial summary

Income Statement- Consolidated

3Q16A 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 2016E 2017E 2018E

Net Sa les 6,262 6,845 5,536 6,119 7,724 8,474 24,525 27,854 33,663

Garment 4,077 4,725 3,566 3,726 5,098 5,813 16,135 18,204 21,633

Fabric & others 2,185 2,120 1,970 2,393 2,626 2,661 8,390 9,650 12,030

Costs 4,468 4,884 4,047 4,386 5,436 5,958 17,643 19,827 23,740

Gross prof it 1,794 1,961 1,489 1,733 2,288 2,517 6,882 8,026 9,922

Operating expenses 587 613 545 580 658 744 2,334 2,527 2,962

Operating Prof it 1,207 1,349 944 1,152 1,630 1,773 4,549 5,499 6,960

Investment income, net 0 0 0 0 0 0 2 0 0

Other net non-op -180 6 6 8 8 9 -275 30 48

Tota l non-operating income -180 6 6 8 8 9 -273 30 48

Pretax prof it 1,028 1,355 950 1,160 1,638 1,782 4,276 5,530 7,008

Taxes (negative for credit) 181 230 176 255 289 303 851 1,023 1,303

Minority 0 0 0 0 0 0 0 0 0

Reported Net Income 846 1,125 774 905 1,349 1,479 3,425 4,507 5,704

Reported EPS (NT$) 3.15 4.18 2.88 3.36 5.01 5.50 12.73 16.76 21.21

Prof itab il ity 3Q16A 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 2016E 2017E 2018E

Gross margin 28.6% 28.7% 26.9% 28.3% 29.6% 29.7% 28.1% 28.8% 29.5%

Operating margin 19.3% 19.7% 17.0% 18.8% 21.1% 20.9% 18.5% 19.7% 20.7%

OPEX to sales 9.4% 9.0% 9.8% 9.5% 8.5% 8.8% 9.5% 9.1% 8.8%

Pretax margin 16.4% 19.8% 17.2% 19.0% 21.2% 21.0% 17.4% 19.9% 20.8%

Net Margin 13.5% 16.4% 14.0% 14.8% 17.5% 17.5% 14.0% 16.2% 16.9%

Growth 3Q16A 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 2016E 2017E 2018E

Revenue- YoY -9% -6% -1% 5% 23% 24% -4% 14% 21%

EPS- YoY -36% -9% 19% 13% 59% 32% -20% 32% 27%

Sales breakdown 3Q16A 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 2016E 2017E 2018E

Garment 65% 69% 64% 61% 66% 69% 66% 65% 64%

Fabric & others 35% 31% 36% 39% 34% 31% 34% 35% 36% Source: Deutsche Bank estimates, company data

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 13

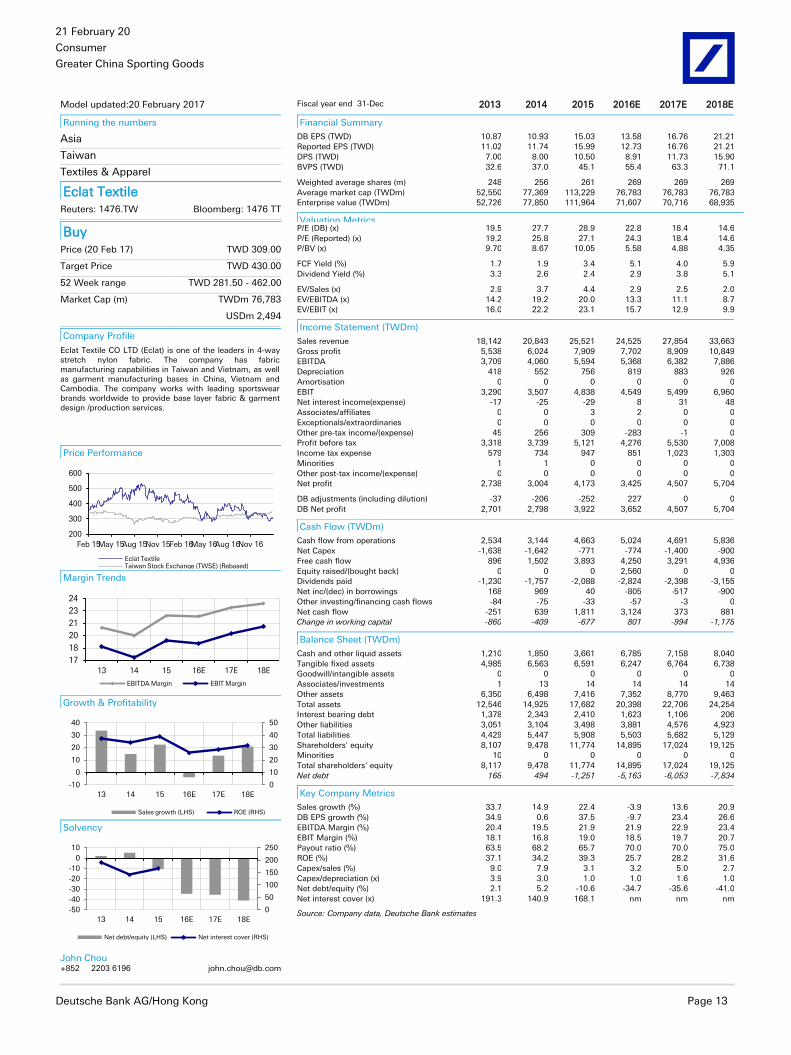

Model updated:20 February 2017

Running the numbers

Asia

Taiwan

Textiles & Apparel

Eclat Textile Reuters: 1476.TW Bloomberg: 1476 TT

Buy Price (20 Feb 17) TWD 309.00

Target Price TWD 430.00

52 Week range TWD 281.50 - 462.00

Market Cap (m) TWDm 76,783

USDm 2,494

Company Profile

Eclat Textile CO LTD (Eclat) is one of the leaders in 4-way stretch nylon fabric. The company has fabric manufacturing capabilities in Taiwan and Vietnam, as well as garment manufacturing bases in China, Vietnam and Cambodia. The company works with leading sportswear brands worldwide to provide base layer fabric & garment design /production services.

Price Performance

200

300

400

500

600

Feb 15May 15Aug 15Nov 15Feb 16May 16Aug 16Nov 16

Eclat TextileTaiwan Stock Exchange (TWSE) (Rebased)

Margin Trends

17

18

20

21

23

24

13 14 15 16E 17E 18E

EBITDA Margin EBIT Margin

Growth & Profitability

0

10

20

30

40

50

-10

0

10

20

30

40

13 14 15 16E 17E 18E

Sales growth (LHS) ROE (RHS)

Solvency

0

50

100

150

200

250

-50

-40

-30

-20

-10

0

10

13 14 15 16E 17E 18E

Net debt/equity (LHS) Net interest cover (RHS)

John Chou

+852 2203 6196 [email protected]

Fiscal year end 31-Dec 2013 2014 2015 2016E 2017E 2018E

Financial Summary

DB EPS (TWD) 10.87 10.93 15.03 13.58 16.76 21.21

Reported EPS (TWD) 11.02 11.74 15.99 12.73 16.76 21.21

DPS (TWD) 7.00 8.00 10.50 8.91 11.73 15.90

BVPS (TWD) 32.6 37.0 45.1 55.4 63.3 71.1

Weighted average shares (m) 248 256 261 269 269 269

Average market cap (TWDm) 52,550 77,369 113,229 76,783 76,783 76,783

Enterprise value (TWDm) 52,726 77,850 111,964 71,607 70,716 68,935

Valuation Metrics P/E (DB) (x) 19.5 27.7 28.9 22.8 18.4 14.6

P/E (Reported) (x) 19.2 25.8 27.1 24.3 18.4 14.6

P/BV (x) 9.70 8.67 10.05 5.58 4.88 4.35

FCF Yield (%) 1.7 1.9 3.4 5.1 4.0 5.9

Dividend Yield (%) 3.3 2.6 2.4 2.9 3.8 5.1

EV/Sales (x) 2.9 3.7 4.4 2.9 2.5 2.0

EV/EBITDA (x) 14.2 19.2 20.0 13.3 11.1 8.7

EV/EBIT (x) 16.0 22.2 23.1 15.7 12.9 9.9

Income Statement (TWDm)

Sales revenue 18,142 20,843 25,521 24,525 27,854 33,663

Gross profit 5,538 6,024 7,909 7,702 8,909 10,849

EBITDA 3,709 4,060 5,594 5,368 6,382 7,886

Depreciation 418 552 756 819 883 926

Amortisation 0 0 0 0 0 0

EBIT 3,290 3,507 4,838 4,549 5,499 6,960

Net interest income(expense) -17 -25 -29 8 31 48

Associates/affiliates 0 0 3 2 0 0

Exceptionals/extraordinaries 0 0 0 0 0 0

Other pre-tax income/(expense) 45 256 309 -283 -1 0

Profit before tax 3,318 3,739 5,121 4,276 5,530 7,008

Income tax expense 579 734 947 851 1,023 1,303

Minorities 1 1 0 0 0 0

Other post-tax income/(expense) 0 0 0 0 0 0

Net profit 2,738 3,004 4,173 3,425 4,507 5,704

DB adjustments (including dilution) -37 -206 -252 227 0 0

DB Net profit 2,701 2,798 3,922 3,652 4,507 5,704

Cash Flow (TWDm)

Cash flow from operations 2,534 3,144 4,663 5,024 4,691 5,836

Net Capex -1,638 -1,642 -771 -774 -1,400 -900

Free cash flow 896 1,502 3,893 4,250 3,291 4,936

Equity raised/(bought back) 0 0 0 2,560 0 0

Dividends paid -1,230 -1,757 -2,088 -2,824 -2,398 -3,155

Net inc/(dec) in borrowings 168 969 40 -805 -517 -900

Other investing/financing cash flows -84 -75 -33 -57 -3 0

Net cash flow -251 639 1,811 3,124 373 881

Change in working capital -860 -409 -677 801 -994 -1,178

Balance Sheet (TWDm)

Cash and other liquid assets 1,210 1,850 3,661 6,785 7,158 8,040

Tangible fixed assets 4,985 6,563 6,591 6,247 6,764 6,738

Goodwill/intangible assets 0 0 0 0 0 0

Associates/investments 1 13 14 14 14 14

Other assets 6,350 6,498 7,416 7,352 8,770 9,463

Total assets 12,546 14,925 17,682 20,398 22,706 24,254

Interest bearing debt 1,378 2,343 2,410 1,623 1,106 206

Other liabilities 3,051 3,104 3,498 3,881 4,576 4,923

Total liabilities 4,429 5,447 5,908 5,503 5,682 5,129

Shareholders' equity 8,107 9,478 11,774 14,895 17,024 19,125

Minorities 10 0 0 0 0 0

Total shareholders' equity 8,117 9,478 11,774 14,895 17,024 19,125

Net debt 168 494 -1,251 -5,163 -6,053 -7,834

Key Company Metrics

Sales growth (%) 33.7 14.9 22.4 -3.9 13.6 20.9

DB EPS growth (%) 34.9 0.6 37.5 -9.7 23.4 26.6

EBITDA Margin (%) 20.4 19.5 21.9 21.9 22.9 23.4

EBIT Margin (%) 18.1 16.8 19.0 18.5 19.7 20.7

Payout ratio (%) 63.5 68.2 65.7 70.0 70.0 75.0

ROE (%) 37.1 34.2 39.3 25.7 28.2 31.6

Capex/sales (%) 9.0 7.9 3.1 3.2 5.0 2.7

Capex/depreciation (x) 3.9 3.0 1.0 1.0 1.6 1.0

Net debt/equity (%) 2.1 5.2 -10.6 -34.7 -35.6 -41.0

Net interest cover (x) 191.3 140.9 168.1 nm nm nm

Source: Company data, Deutsche Bank estimates

21 February 2017

Consumer

Greater China Sporting Goods

Page 14 Deutsche Bank AG/Hong Kong

Yue Yuen (551 HK): Seeing the end to five-year down-cycle; upgrading to Buy

Stock drivers

1. Painful plant shift largely done By early Feb-2017, we estimate that YY had largely completed the

plant relocations of its Guangdong plants.

We adopt a three-step analysis to understand the impact from YY’s

Guangdong plant shutdown and model for the future. We conclude

that there should be a stronger-than-expected profitability recovery for

YY’s ODM operation. We forecast YY’s ODM EBIT margin to deliver a

steady recovery to 7.2%/7.6%/8.4% in 16E/17E/18E, vs. consensus

forecasts of 6.4%/6.0%/6.4%, respectively (Figure 30).

Step 1: obtaining the recurring profit: we adopt the public subsidiary

profit information reported by YY. There has been a surge in losses in

YY’s Guangdong production cluster in YT3Q16 (Figure 31). We

estimate a majority of the additional losses are extraordinary in nature.

Figure 31: Profit (losses) from YY’s China plants

(USDmn) 2010 2011 2012 2013 2014 2015 YT3Q15 YT3Q16

Guangdong 12 16 15 (11) (6) (6) (5) (48)

Hunan (1) 1 1 (2) (4) (9) (9) (2)

Hubei (0) (6) 1 0 (2) (7) (7) (2)

Anhui & Jiangsu 16 9 13 (28) (17) (5) (4) (14)

Jiangxi (10) (17) (8) (15) (2) 3 (1) (5)

Prof it ( loss) 17 3 22 (56) (32) (24) (26) (71)

% of ODM profit 5% 1% n.a. -13% -10% -7% -11% -23%

% of consolidated profit 5% 1% n.a. -13% -10% -6% -8% -17% Source: Deutsche Bank estimates, company data

We can then break down YY’s profit into the below three segments to

simplify our analysis (Figure 32):

(1) China recurring profit

(2) Non-China recurring profit

(3) Extraordinary (non-recurring): USD90m/over USD30m provisions made

in 2014/2015 to compensate employees in the China plants.

Figure 30: Consensus seeing flattish

EBIT margin trend for YY ODM

(YT3Q16= 6.8%, up 1.7 ppt YoY)

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

2014 2015 16E 17E 18E

DB Consensus implied

YY: ODM EBIT margin

Source: Deutsche Bank estimates, Bloomberg Finance LP

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 15

Figure 32: YY: ODM operating profit breakdown

(200)

(100)

-

100

200

300

400

500

600

2010 2011 2012* 2013 2014 2015 YT3Q16

Extraordinary (non-recurring)

Non-China: recurring

China: recurring

(USDmn)

Source: Deutsche Bank estimates, company data *no available disclosure

Step 2: sanity checks of our profit breakdown exercise: We view the

profit estimates as reasonable. Figure 33 suggests YY’s poor

profitability (measured by operating profit per pair) in China due to

plant migrations since 2010. The profitability of YY’s non-China plants

also took a hit as they absorbed production capacity relocated from

China. Nevertheless, we saw a profitability recovery for YY’s non-

China plants in YT3Q16. Figure 34 suggests YY’s non-China plants are

operating at good efficiency (similar to Feng Tay’s plants), while YY’s

China operation remains a profit drag.

Figure 33: The time series is reasonable from an

operating profit per pair perspective

Figure 34: YY’s profit per pair vs. Feng Tay’s

(1.0)

(0.5)

-

0.5

1.0

1.5

2.0

2.5

3.0

2010 2011 2012* 2013 2014 2015 YT3Q16

China

Non China

(USD per pair)

1. Plant migration

started

2. Overseas plants

suffer from inefficiency

3. Overseas plants

regaining efficiency

(1.0)

(0.5)

-

0.5

1.0

1.5

2.0

2.5

3.0

2010 2011 2012* 2013 2014 2015 YT3Q16

YY: China YY: Non China Feng Tay: consolidated

(USD per pair)

Source: Deutsche Bank estimates, company data *No available data for YY

Source: Deutsche Bank estimates, company data *No available data for YY

Step 3: model for the future: We estimate YY’s ODM operating profit

to grow by 11%/12% in 2017/2018, respectively. This implies YY’s

operating profit per pair will increase by 6%/10% in 2017/2018. We

view our assumptions as conservative, considering that we estimate

YY’s profit per pair to increase to USD1.59 by 2020 vs. USD1.96 at

Feng Tay during 2015 (Figure 35). Feng Tay’s historical plant

profitability (Figure 36) points to a significant profitability recovery

(toward 8% operating margin) as plant operations stabilize.

Blue-sky scenario: if YY’s consolidated operating profit per pair

increases to USD1.96 (Feng Tay’s 2015level) in 2017, YY’s ODM

operating profit will reach USD657mn (37% higher than our base case).

Such leads to 28% upside to DB’s consolidated earnings forecasts.

21 February 2017

Consumer

Greater China Sporting Goods

Page 16 Deutsche Bank AG/Hong Kong

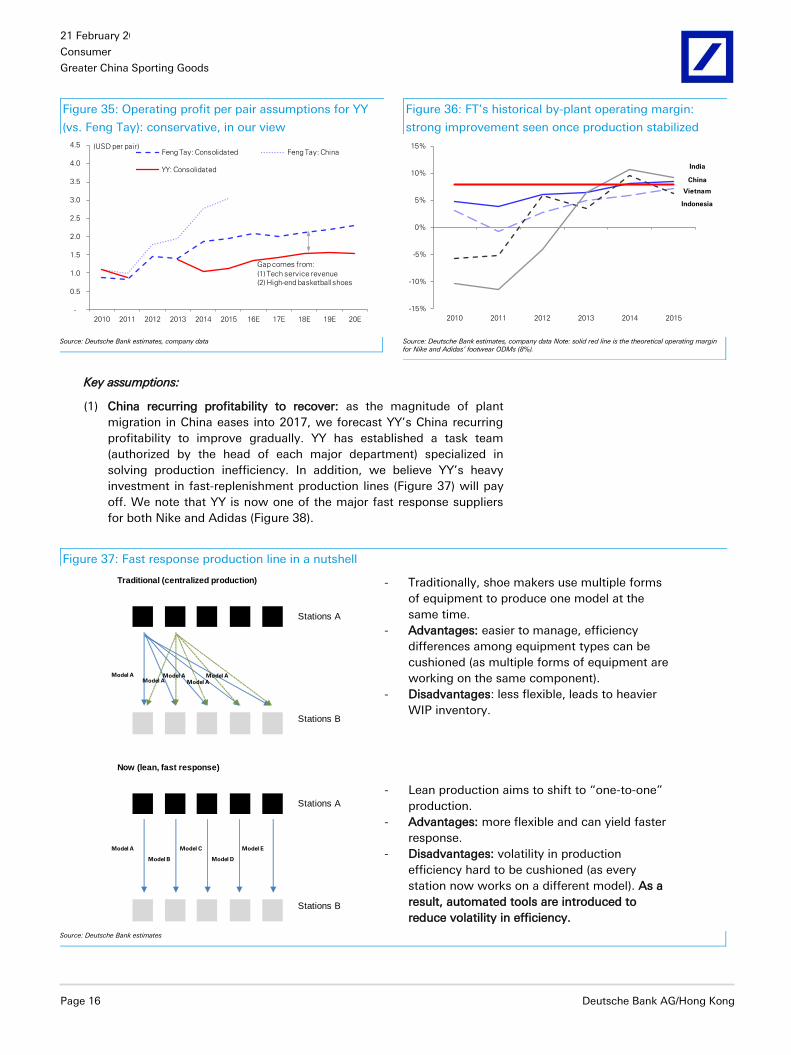

Figure 35: Operating profit per pair assumptions for YY

(vs. Feng Tay): conservative, in our view

Figure 36: FT’s historical by-plant operating margin:

strong improvement seen once production stabilized

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2010 2011 2012 2013 2014 2015 16E 17E 18E 19E 20E

Feng Tay: Consolidated Feng Tay: China

YY: Consolidated

(USD per pair)

Gap comes from:

(1) Tech service revenue

(2) High-end basketball shoes

-15%

-10%

-5%

0%

5%

10%

15%

2010 2011 2012 2013 2014 2015

India

Indonesia

Vietnam

China

Source: Deutsche Bank estimates, company data

Source: Deutsche Bank estimates, company data Note: solid red line is the theoretical operating margin for Nike and Adidas’ footwear ODMs (8%).

Key assumptions:

(1) China recurring profitability to recover: as the magnitude of plant

migration in China eases into 2017, we forecast YY’s China recurring

profitability to improve gradually. YY has established a task team

(authorized by the head of each major department) specialized in

solving production inefficiency. In addition, we believe YY’s heavy

investment in fast-replenishment production lines (Figure 37) will pay

off. We note that YY is now one of the major fast response suppliers

for both Nike and Adidas (Figure 38).

Figure 37: Fast response production line in a nutshell

Traditional (centralized production)

Stations A

Stations B

Now (lean, fast response)

Stations A

Stations B

Model AModel A

Model AModel A

Model A

Model A

Model B

Model C

Model D

Model E

- Traditionally, shoe makers use multiple forms

of equipment to produce one model at the

same time.

- Advantages: easier to manage, efficiency

differences among equipment types can be

cushioned (as multiple forms of equipment are

working on the same component).

- Disadvantages: less flexible, leads to heavier

WIP inventory.

- Lean production aims to shift to “one-to-one”

production.

- Advantages: more flexible and can yield faster

response.

- Disadvantages: volatility in production

efficiency hard to be cushioned (as every

station now works on a different model). As a

result, automated tools are introduced to

reduce volatility in efficiency.

Source: Deutsche Bank estimates

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 17

(2) Non-China recurring profit still has room for improvement: we

witnessed YY’s efforts to further strengthen its raw material supply in

Vietnam. Also, we believe the production in Vietnam has been

stabilizing following the reduced capacity reallocation from China.

(3) Extraordinary (non-recurring) items to reduce: we view YY as still

adjusting its capacity in China, but the amount of extraordinary items

should drop significantly going forward.

2. Adidas order shift to boost revenue According to Ching Luh, (a private competitor of Apache's), Apache (

萬邦鞋業 ) one of Adidas’ major footwear manufacturers, was

reported to have violated its labor welfare compliance protocols in

2016. We forecast Adidas will gradually shift its orders to YY and

Ching Luh.

We conservatively estimate that the shift can boost YY’s 2017 volume

by 1-3% (Figure 39).

YY’s ability to take on additional orders from Adidas also cements its

relationship with the brand, in our view.

Figure 39: Scale comparison among Adidas’ major shoe manufacturers

-

5.0

10.0

15.0

20.0

25.0

30.0

YY Ching Luh Apache

Other brands Adidas

(mn pairs per month)

Source: Deutsche Bank estimates, company data

Figure 38: Major fast response

sports shoes manufacturers

0%

5%

10%

15%

20%

25%

Yue Yuen Feng Tay Ching Luh

Fast replenishment order % of

total orders

Source: Deutsche Bank estimates, company data

21 February 2017

Consumer

Greater China Sporting Goods

Page 18 Deutsche Bank AG/Hong Kong

3. Easing price pressure YY faced heavier pricing pressure in 2016 − partly reflecting the FX

pressure experienced by Adidas, in our view. Nevertheless, with the

USD strengthening against the EUR, we forecast less pricing pressure

from Adidas.

In addition, YY has been strengthening its cooperation with Adidas

through:

(a) Taking on additional footwear orders from Apache,

(b) Preparing knitted upper production for Adidas,

(c) Expanding the “Boost” midsole production in Vietnam, and

(d) Helping Adidas execute growth in China through the retail

operation (Pou Sheng).

We view our ASP growth forecasts as conservative, considering the

rising raw material prices and the “cost-plus” pricing model.

4. Beneficiary of the “modern retro” style A major comeback has been seen for retro sneakers in the production

pipeline: namely, the Nike Air Max series, Air Force 1, etc.

Modern technology with authentic design means better profitability

for ODMs: these retro shoes have been continuously produced by

ODMs, so factory workers are very familiar with the production

process. We estimate the profitability for retro shoes to be higher than

for other shoes, thanks to more advanced production technology and

material science.

Flyknit order cut partly reflects the come-back of retro shoes: we

believe traditional shoe makers will see easing pressure from knitted

uppers in 2017.

Line of Thinking

Figure 41: YY’s share price Figure 42: YY consensus earnings revisions

22.0

24.0

26.0

28.0

30.0

32.0

34.0

36.0

38.0

Aug-14 Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17

Share price

Initiate

with Hold U/G to Buy

450

470

490

510

530

550

570

590

610

450

470

490

510

530

550

570

590

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17

2016 consensus earnings (LHS) 2017 consensus earnings (RHS)

Source: Deutsche Bank, Bloomberg Finance LP

Source: Deutsche Bank, Bloomberg Finance LP consensus

We initiated with Hold as we expected continued challenges with YY’s

ODM business, despite strong growth from the retail business (Pou

Sheng).

We upgraded to Buy as we were more positive on the ODM profit

recovery, as well as incremental positives including order shifts from

Apache.

Figure 40: Our (conservative) ASP

forecasts

-4%

-2%

0%

2%

4%

6%

8%

10%

2010 2012 2014 16E 18E 20E

Blended ASP YoY

Source: Deutsche Bank estimates, company data

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 19

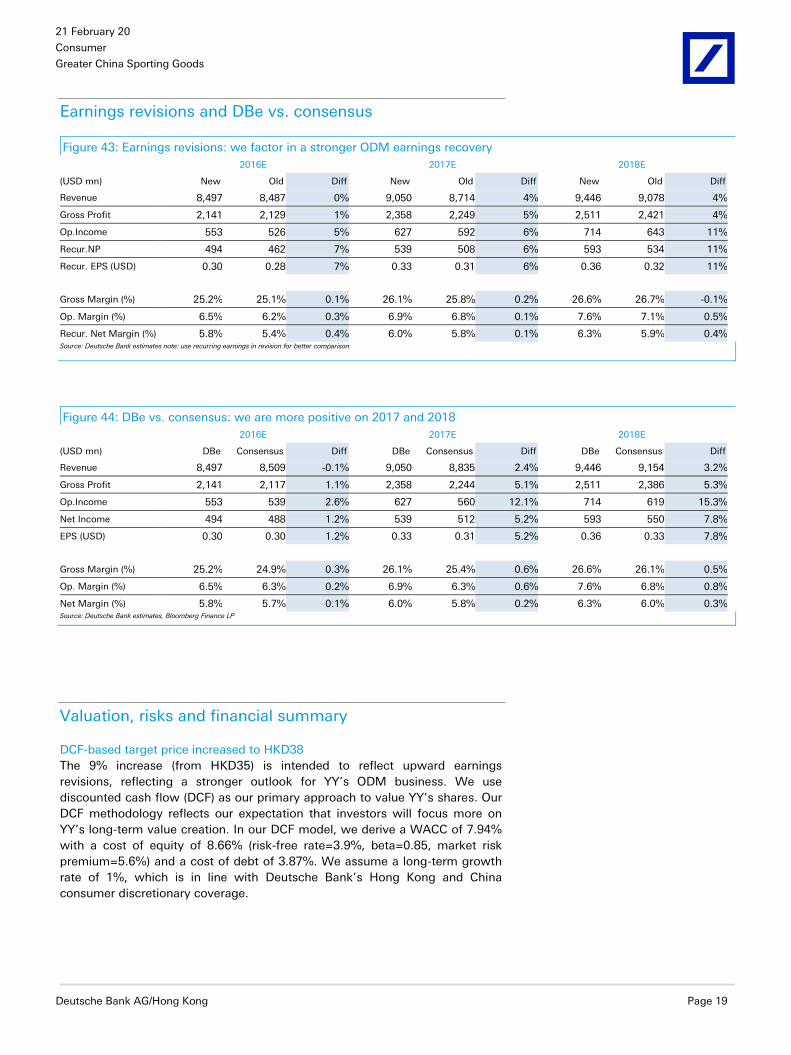

Earnings revisions and DBe vs. consensus

Figure 43: Earnings revisions: we factor in a stronger ODM earnings recovery

2016E 2017E 2018E

(USD mn) New Old Diff New Old Diff New Old Diff

Revenue 8,497 8,487 0% 9,050 8,714 4% 9,446 9,078 4%

Gross Profit 2,141 2,129 1% 2,358 2,249 5% 2,511 2,421 4%

Op.Income 553 526 5% 627 592 6% 714 643 11%

Recur.NP 494 462 7% 539 508 6% 593 534 11%

Recur. EPS (USD) 0.30 0.28 7% 0.33 0.31 6% 0.36 0.32 11%

Gross Margin (%) 25.2% 25.1% 0.1% 26.1% 25.8% 0.2% 26.6% 26.7% -0.1%

Op. Margin (%) 6.5% 6.2% 0.3% 6.9% 6.8% 0.1% 7.6% 7.1% 0.5%

Recur. Net Margin (%) 5.8% 5.4% 0.4% 6.0% 5.8% 0.1% 6.3% 5.9% 0.4% Source: Deutsche Bank estimates note: use recurring earnings in revision for better comparison

Figure 44: DBe vs. consensus: we are more positive on 2017 and 2018

2016E 2017E 2018E

(USD mn) DBe Consensus Diff DBe Consensus Diff DBe Consensus Diff

Revenue 8,497 8,509 -0.1% 9,050 8,835 2.4% 9,446 9,154 3.2%

Gross Profit 2,141 2,117 1.1% 2,358 2,244 5.1% 2,511 2,386 5.3%

Op.Income 553 539 2.6% 627 560 12.1% 714 619 15.3%

Net Income 494 488 1.2% 539 512 5.2% 593 550 7.8%

EPS (USD) 0.30 0.30 1.2% 0.33 0.31 5.2% 0.36 0.33 7.8%

Gross Margin (%) 25.2% 24.9% 0.3% 26.1% 25.4% 0.6% 26.6% 26.1% 0.5%

Op. Margin (%) 6.5% 6.3% 0.2% 6.9% 6.3% 0.6% 7.6% 6.8% 0.8%

Net Margin (%) 5.8% 5.7% 0.1% 6.0% 5.8% 0.2% 6.3% 6.0% 0.3% Source: Deutsche Bank estimates, Bloomberg Finance LP

Valuation, risks and financial summary

DCF-based target price increased to HKD38

The 9% increase (from HKD35) is intended to reflect upward earnings

revisions, reflecting a stronger outlook for YY’s ODM business. We use

discounted cash flow (DCF) as our primary approach to value YY’s shares. Our

DCF methodology reflects our expectation that investors will focus more on

YY’s long-term value creation. In our DCF model, we derive a WACC of 7.94%

with a cost of equity of 8.66% (risk-free rate=3.9%, beta=0.85, market risk

premium=5.6%) and a cost of debt of 3.87%. We assume a long-term growth

rate of 1%, which is in line with Deutsche Bank’s Hong Kong and China

consumer discretionary coverage.

21 February 2017

Consumer

Greater China Sporting Goods

Page 20 Deutsche Bank AG/Hong Kong

Figure 45: DCF sales, margin assumptions and sensitivity Figure 46: Free cash flow to equity profile

Two-stage DCF:

1. FCF forecasts from model 2018-2020

2. Explicit forecast period 2021-2030

2018~2021 2022~2025 2026~2030 2018~2030

Revenue CAGR: 6.6% 4.1% 2.3% 3.7%

Average EBIT margin: 7.5% 7.1% 6.7% 7.1%

FCF CAGR: 17.3% 3.1% 0.8% 5.0%

-70%

-50%

-30%

-10%

10%

30%

50%

-

100

200

300

400

500

600

700

2012 2015 2018 2021 2024 2027 2030

Free Cashflow to Equity (LHS)

YoY (RHS)(USDmn)

Source: Deutsche Bank estimates

Source: Deutsche Bank estimates, Note: representing free cash flow for equity (in line with Deutsche Bank RTN)

Figure 47: Discounted cash flow valuation – key assumptions

Share & Market Information Note

Valuation date 12 month forward

Current Stock Price 26.95

Issued Shares (million) 1,646 Weighted average shares

DCF Target Price 38

Implied Upside (Downside) 41%

Valuation metrics

FY16 PER (recurring) 16.6

FY17 PER (recurring) 14.9

FY16 PBR 1.7

FY17 PBR 1.6

Cost of Equity 8.66%

Risk Free Rate (%) 3.9% Deutsche Bank assumption for China

Beta 0.85 Bloomberg 1-year beta

Market Risk Premium (%) 5.60% Deutsche Bank assumption for China

Cost of Debt (after tax) 3.87%

Cost of Debt 4.50% Company long-term borrowing rate

Tax Rate 14.00% Long-term tax rate

Target Debt / (Debt + Equity) 15%

WACC 7.94%

DCF Model LT growth 1.0% In-line with DB consumer discretionary coverage space

Source: Deutsche Bank estimates, company data

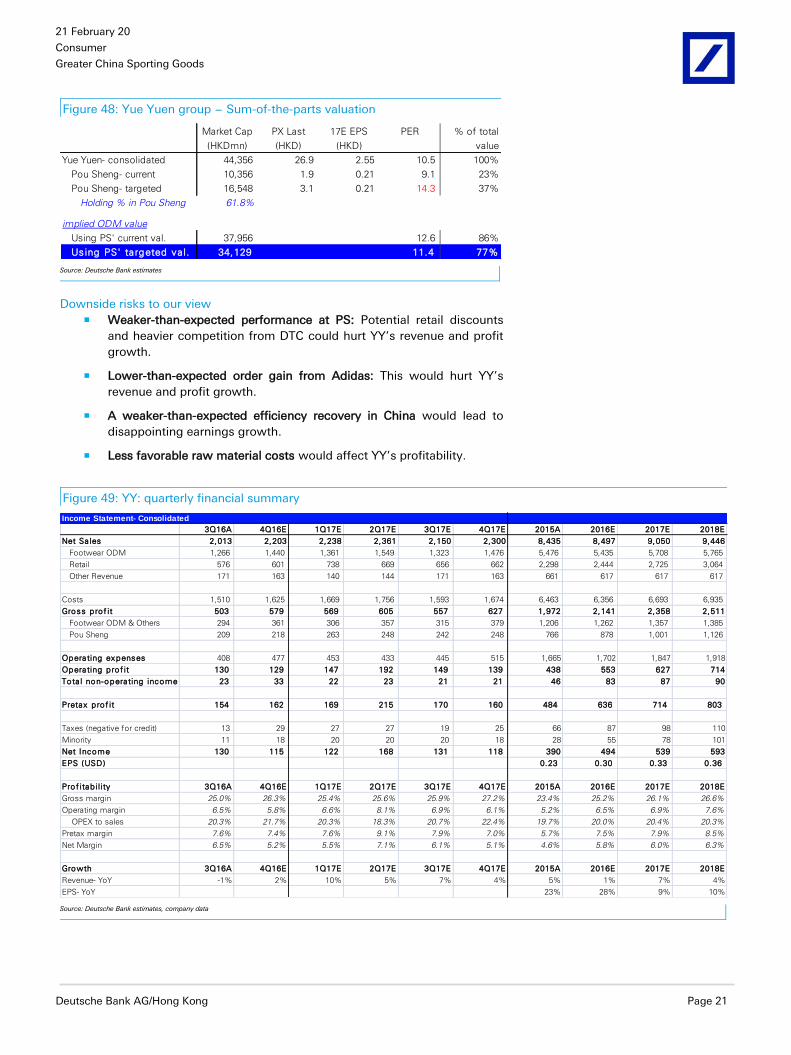

SoTP analysis suggests ODM values not fully priced in

We support our valuation using a sum-of-the-parts (SoTP) analysis. If we derive

YY’s ODM value using the current value of Pou Sheng (the group’s retail

operation), YY’s ODM value is implied at HKD38bn, or 12.6x ODM earnings. If

we assign Pou Sheng’s value using our targeted corporate value (derived from

the target price), ODM business is trading at 11.4x.

38 8.9% 8.4% 7.9% 7.4% 6.9%

-1.00% 30 32 34 36 38

0.00% 31 33 36 38 41

1.00% 33 35 38 41 44

2.00% 35 37 41 44 49

3.00% 37 41 45 49 56

WACC

Terminal

Growth

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 21

Figure 48: Yue Yuen group − Sum-of-the-parts valuation

Market Cap PX Last 17E EPS PER % of total

(HKDmn) (HKD) (HKD) value

Yue Yuen- consolidated 44,356 26.9 2.55 10.5 100%

Pou Sheng- current 10,356 1.9 0.21 9.1 23%

Pou Sheng- targeted 16,548 3.1 0.21 14.3 37%

Holding % in Pou Sheng 61.8%

implied ODM value

Using PS' current val. 37,956 12.6 86%

Using PS' targeted va l. 34,129 11.4 77% Source: Deutsche Bank estimates

Downside risks to our view Weaker-than-expected performance at PS: Potential retail discounts

and heavier competition from DTC could hurt YY’s revenue and profit

growth.

Lower-than-expected order gain from Adidas: This would hurt YY’s

revenue and profit growth.

A weaker-than-expected efficiency recovery in China would lead to

disappointing earnings growth.

Less favorable raw material costs would affect YY’s profitability.

Figure 49: YY: quarterly financial summary

Income Statement- Consolidated

3Q16A 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 2015A 2016E 2017E 2018E

Net Sa les 2,013 2,203 2,238 2,361 2,150 2,300 8,435 8,497 9,050 9,446

Footwear ODM 1,266 1,440 1,361 1,549 1,323 1,476 5,476 5,435 5,708 5,765

Retail 576 601 738 669 656 662 2,298 2,444 2,725 3,064

Other Revenue 171 163 140 144 171 163 661 617 617 617

Costs 1,510 1,625 1,669 1,756 1,593 1,674 6,463 6,356 6,693 6,935

Gross prof it 503 579 569 605 557 627 1,972 2,141 2,358 2,511

Footwear ODM & Others 294 361 306 357 315 379 1,206 1,262 1,357 1,385

Pou Sheng 209 218 263 248 242 248 766 878 1,001 1,126

Operating expenses 408 477 453 433 445 515 1,665 1,702 1,847 1,918

Operating prof it 130 129 147 192 149 139 438 553 627 714

Tota l non-operating income 23 33 22 23 21 21 46 83 87 90

Pretax prof it 154 162 169 215 170 160 484 636 714 803

Taxes (negative for credit) 13 29 27 27 19 25 66 87 98 110

Minority 11 18 20 20 20 18 28 55 78 101

Net Income 130 115 122 168 131 118 390 494 539 593

EPS (USD) 0.23 0.30 0.33 0.36

Prof itab il ity 3Q16A 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 2015A 2016E 2017E 2018E

Gross margin 25.0% 26.3% 25.4% 25.6% 25.9% 27.2% 23.4% 25.2% 26.1% 26.6%

Operating margin 6.5% 5.8% 6.6% 8.1% 6.9% 6.1% 5.2% 6.5% 6.9% 7.6%

OPEX to sales 20.3% 21.7% 20.3% 18.3% 20.7% 22.4% 19.7% 20.0% 20.4% 20.3%

Pretax margin 7.6% 7.4% 7.6% 9.1% 7.9% 7.0% 5.7% 7.5% 7.9% 8.5%

Net Margin 6.5% 5.2% 5.5% 7.1% 6.1% 5.1% 4.6% 5.8% 6.0% 6.3%

Growth 3Q16A 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 2015A 2016E 2017E 2018E

Revenue- YoY -1% 2% 10% 5% 7% 4% 5% 1% 7% 4%

EPS- YoY 23% 28% 9% 10% Source: Deutsche Bank estimates, company data

21 February 2017

Consumer

Greater China Sporting Goods

Page 22 Deutsche Bank AG/Hong Kong

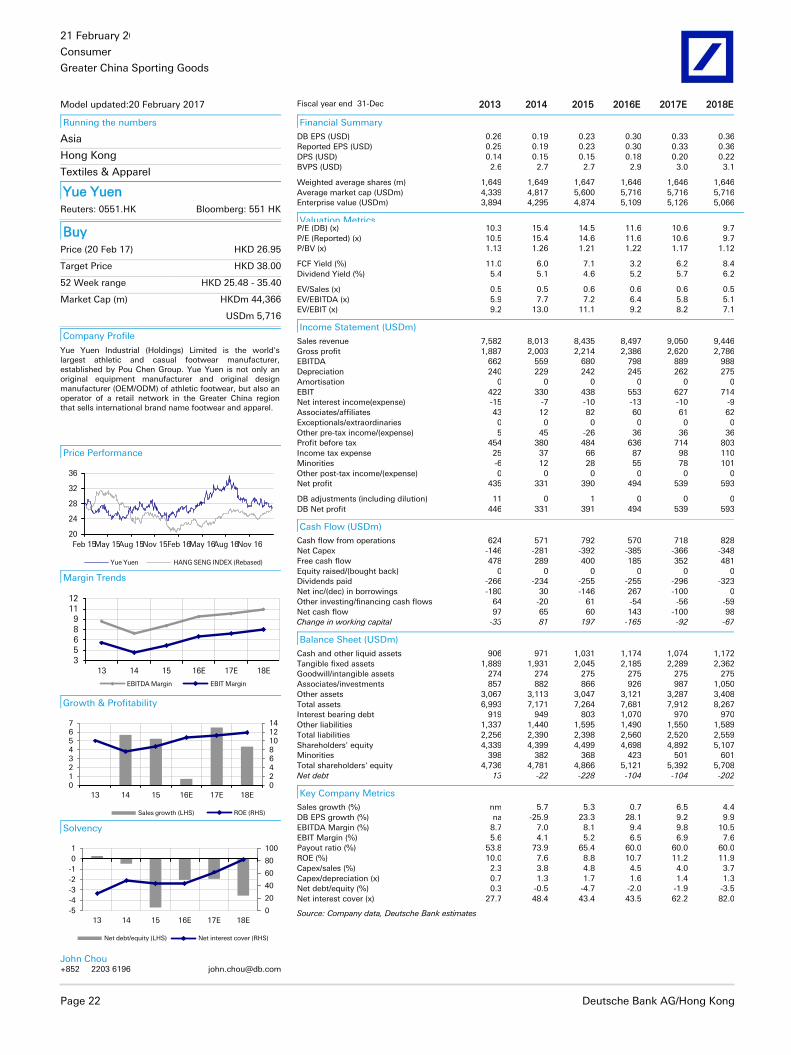

Model updated:20 February 2017

Running the numbers

Asia

Hong Kong

Textiles & Apparel

Yue Yuen Reuters: 0551.HK Bloomberg: 551 HK

Buy Price (20 Feb 17) HKD 26.95

Target Price HKD 38.00

52 Week range HKD 25.48 - 35.40

Market Cap (m) HKDm 44,366

USDm 5,716

Company Profile

Yue Yuen Industrial (Holdings) Limited is the world's largest athletic and casual footwear manufacturer, established by Pou Chen Group. Yue Yuen is not only an original equipment manufacturer and original design manufacturer (OEM/ODM) of athletic footwear, but also an operator of a retail network in the Greater China region that sells international brand name footwear and apparel.

Price Performance

20

24

28

32

36

Feb 15May 15Aug 15Nov 15Feb 16May 16Aug 16Nov 16

Yue Yuen HANG SENG INDEX (Rebased)

Margin Trends

35689

1112

13 14 15 16E 17E 18E

EBITDA Margin EBIT Margin

Growth & Profitability

02468101214

01234567

13 14 15 16E 17E 18E

Sales growth (LHS) ROE (RHS)

Solvency

0

20

40

60

80

100

-5

-4

-3

-2

-1

0

1

13 14 15 16E 17E 18E

Net debt/equity (LHS) Net interest cover (RHS)

John Chou

+852 2203 6196 [email protected]

Fiscal year end 31-Dec 2013 2014 2015 2016E 2017E 2018E

Financial Summary

DB EPS (USD) 0.26 0.19 0.23 0.30 0.33 0.36

Reported EPS (USD) 0.25 0.19 0.23 0.30 0.33 0.36

DPS (USD) 0.14 0.15 0.15 0.18 0.20 0.22

BVPS (USD) 2.6 2.7 2.7 2.9 3.0 3.1

Weighted average shares (m) 1,649 1,649 1,647 1,646 1,646 1,646

Average market cap (USDm) 4,339 4,817 5,600 5,716 5,716 5,716

Enterprise value (USDm) 3,894 4,295 4,874 5,109 5,126 5,066

Valuation Metrics P/E (DB) (x) 10.3 15.4 14.5 11.6 10.6 9.7

P/E (Reported) (x) 10.5 15.4 14.6 11.6 10.6 9.7

P/BV (x) 1.13 1.26 1.21 1.22 1.17 1.12

FCF Yield (%) 11.0 6.0 7.1 3.2 6.2 8.4

Dividend Yield (%) 5.4 5.1 4.6 5.2 5.7 6.2

EV/Sales (x) 0.5 0.5 0.6 0.6 0.6 0.5

EV/EBITDA (x) 5.9 7.7 7.2 6.4 5.8 5.1

EV/EBIT (x) 9.2 13.0 11.1 9.2 8.2 7.1

Income Statement (USDm)

Sales revenue 7,582 8,013 8,435 8,497 9,050 9,446

Gross profit 1,887 2,003 2,214 2,386 2,620 2,786

EBITDA 662 559 680 798 889 988

Depreciation 240 229 242 245 262 275

Amortisation 0 0 0 0 0 0

EBIT 422 330 438 553 627 714

Net interest income(expense) -15 -7 -10 -13 -10 -9

Associates/affiliates 43 12 82 60 61 62

Exceptionals/extraordinaries 0 0 0 0 0 0

Other pre-tax income/(expense) 5 45 -26 36 36 36

Profit before tax 454 380 484 636 714 803

Income tax expense 25 37 66 87 98 110

Minorities -6 12 28 55 78 101

Other post-tax income/(expense) 0 0 0 0 0 0

Net profit 435 331 390 494 539 593

DB adjustments (including dilution) 11 0 1 0 0 0

DB Net profit 446 331 391 494 539 593

Cash Flow (USDm)

Cash flow from operations 624 571 792 570 718 828

Net Capex -146 -281 -392 -385 -366 -348

Free cash flow 478 289 400 185 352 481

Equity raised/(bought back) 0 0 0 0 0 0

Dividends paid -266 -234 -255 -255 -296 -323

Net inc/(dec) in borrowings -180 30 -146 267 -100 0

Other investing/financing cash flows 64 -20 61 -54 -56 -59

Net cash flow 97 65 60 143 -100 98

Change in working capital -33 81 197 -165 -92 -67

Balance Sheet (USDm)

Cash and other liquid assets 906 971 1,031 1,174 1,074 1,172

Tangible fixed assets 1,889 1,931 2,045 2,185 2,289 2,362

Goodwill/intangible assets 274 274 275 275 275 275

Associates/investments 857 882 866 926 987 1,050

Other assets 3,067 3,113 3,047 3,121 3,287 3,408

Total assets 6,993 7,171 7,264 7,681 7,912 8,267

Interest bearing debt 919 949 803 1,070 970 970

Other liabilities 1,337 1,440 1,595 1,490 1,550 1,589

Total liabilities 2,256 2,390 2,398 2,560 2,520 2,559

Shareholders' equity 4,339 4,399 4,499 4,698 4,892 5,107

Minorities 398 382 368 423 501 601

Total shareholders' equity 4,736 4,781 4,866 5,121 5,392 5,708

Net debt 13 -22 -228 -104 -104 -202

Key Company Metrics

Sales growth (%) nm 5.7 5.3 0.7 6.5 4.4

DB EPS growth (%) na -25.9 23.3 28.1 9.2 9.9

EBITDA Margin (%) 8.7 7.0 8.1 9.4 9.8 10.5

EBIT Margin (%) 5.6 4.1 5.2 6.5 6.9 7.6

Payout ratio (%) 53.8 73.9 65.4 60.0 60.0 60.0

ROE (%) 10.0 7.6 8.8 10.7 11.2 11.9

Capex/sales (%) 2.3 3.8 4.8 4.5 4.0 3.7

Capex/depreciation (x) 0.7 1.3 1.7 1.6 1.4 1.3

Net debt/equity (%) 0.3 -0.5 -4.7 -2.0 -1.9 -3.5

Net interest cover (x) 27.7 48.4 43.4 43.5 62.2 82.0

Source: Company data, Deutsche Bank estimates

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 23

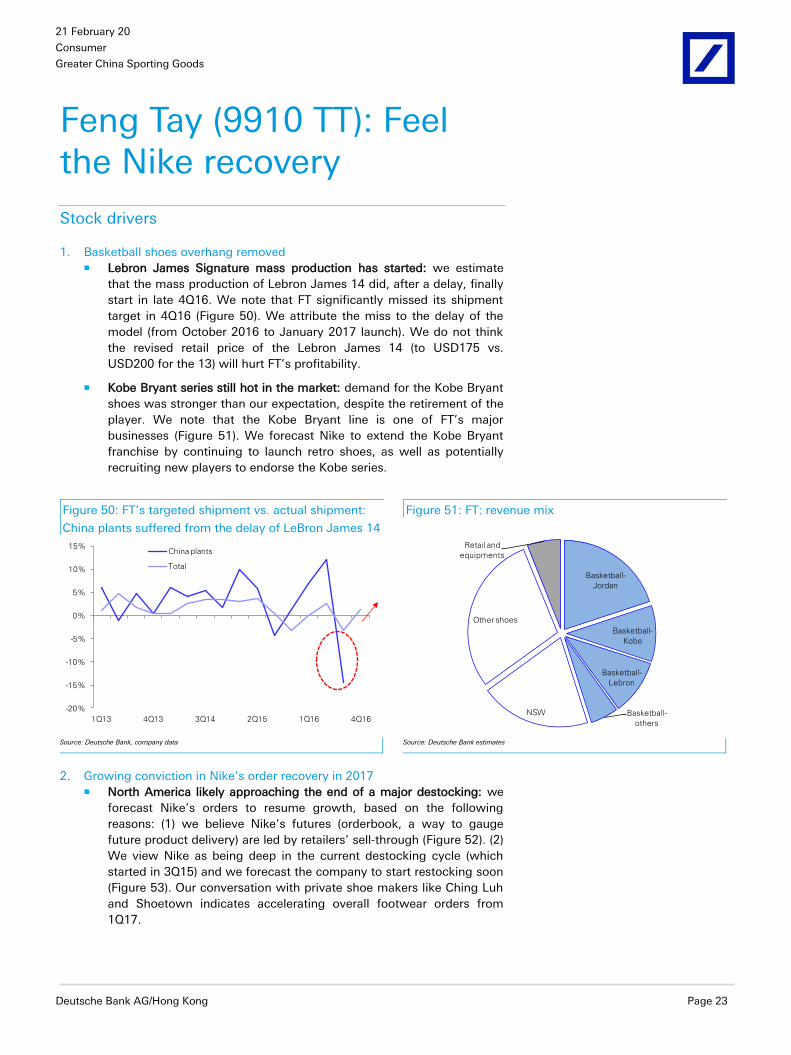

Feng Tay (9910 TT): Feel the Nike recovery

Stock drivers

1. Basketball shoes overhang removed Lebron James Signature mass production has started: we estimate

that the mass production of Lebron James 14 did, after a delay, finally

start in late 4Q16. We note that FT significantly missed its shipment

target in 4Q16 (Figure 50). We attribute the miss to the delay of the

model (from October 2016 to January 2017 launch). We do not think

the revised retail price of the Lebron James 14 (to USD175 vs.

USD200 for the 13) will hurt FT’s profitability.

Kobe Bryant series still hot in the market: demand for the Kobe Bryant

shoes was stronger than our expectation, despite the retirement of the

player. We note that the Kobe Bryant line is one of FT’s major

businesses (Figure 51). We forecast Nike to extend the Kobe Bryant

franchise by continuing to launch retro shoes, as well as potentially

recruiting new players to endorse the Kobe series.

Figure 50: FT’s targeted shipment vs. actual shipment:

China plants suffered from the delay of LeBron James 14

Figure 51: FT: revenue mix

-20%

-15%

-10%

-5%

0%

5%

10%

15%

1Q13 4Q13 3Q14 2Q15 1Q16 4Q16

China plants

Total

Basketball-

Jordan

Basketball-

Kobe

Basketball-

Lebron

Basketball-

others

NSW

Other shoes

Retail and

equipments

Source: Deutsche Bank, company data

Source: Deutsche Bank estimates

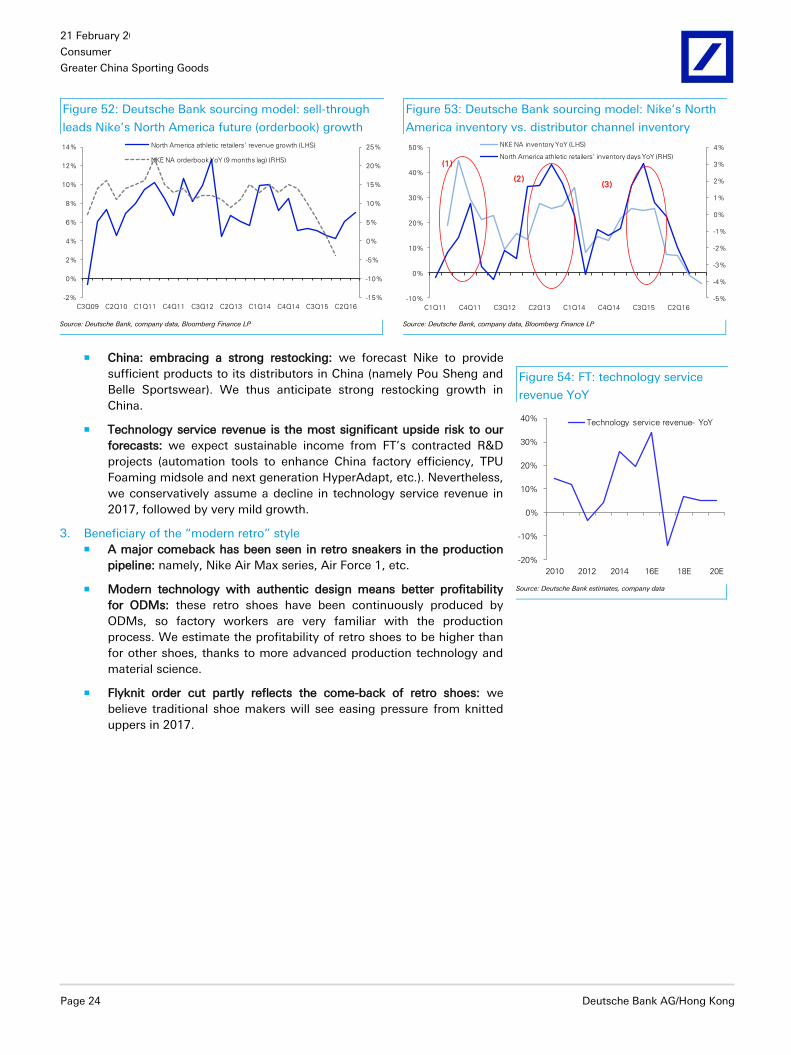

2. Growing conviction in Nike’s order recovery in 2017 North America likely approaching the end of a major destocking: we

forecast Nike’s orders to resume growth, based on the following

reasons: (1) we believe Nike’s futures (orderbook, a way to gauge

future product delivery) are led by retailers’ sell-through (Figure 52). (2)

We view Nike as being deep in the current destocking cycle (which

started in 3Q15) and we forecast the company to start restocking soon

(Figure 53). Our conversation with private shoe makers like Ching Luh

and Shoetown indicates accelerating overall footwear orders from

1Q17.

21 February 2017

Consumer

Greater China Sporting Goods

Page 24 Deutsche Bank AG/Hong Kong

Figure 52: Deutsche Bank sourcing model: sell-through

leads Nike’s North America future (orderbook) growth

Figure 53: Deutsche Bank sourcing model: Nike’s North

America inventory vs. distributor channel inventory

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

C3Q09 C2Q10 C1Q11 C4Q11 C3Q12 C2Q13 C1Q14 C4Q14 C3Q15 C2Q16

North America athletic retailers' revenue growth (LHS)

NKE NA orderbook YoY (9 months lag) (RHS)

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

-10%

0%

10%

20%

30%

40%

50%

C1Q11 C4Q11 C3Q12 C2Q13 C1Q14 C4Q14 C3Q15 C2Q16

NKE NA inventory YoY (LHS)

North America athletic retailers' inventory days YoY (RHS)(1 )

(2 )(3 )

Source: Deutsche Bank, company data, Bloomberg Finance LP

Source: Deutsche Bank, company data, Bloomberg Finance LP

China: embracing a strong restocking: we forecast Nike to provide

sufficient products to its distributors in China (namely Pou Sheng and

Belle Sportswear). We thus anticipate strong restocking growth in

China.

Technology service revenue is the most significant upside risk to our

forecasts: we expect sustainable income from FT’s contracted R&D

projects (automation tools to enhance China factory efficiency, TPU

Foaming midsole and next generation HyperAdapt, etc.). Nevertheless,

we conservatively assume a decline in technology service revenue in

2017, followed by very mild growth.

3. Beneficiary of the “modern retro” style A major comeback has been seen in retro sneakers in the production

pipeline: namely, Nike Air Max series, Air Force 1, etc.

Modern technology with authentic design means better profitability

for ODMs: these retro shoes have been continuously produced by

ODMs, so factory workers are very familiar with the production

process. We estimate the profitability of retro shoes to be higher than

for other shoes, thanks to more advanced production technology and

material science.

Flyknit order cut partly reflects the come-back of retro shoes: we

believe traditional shoe makers will see easing pressure from knitted

uppers in 2017.

Figure 54: FT: technology service

revenue YoY

-20%

-10%

0%

10%

20%

30%

40%

2010 2012 2014 16E 18E 20E

Technology service revenue- YoY

Source: Deutsche Bank estimates, company data

21 February 2017

Consumer

Greater China Sporting Goods

Deutsche Bank AG/Hong Kong Page 25

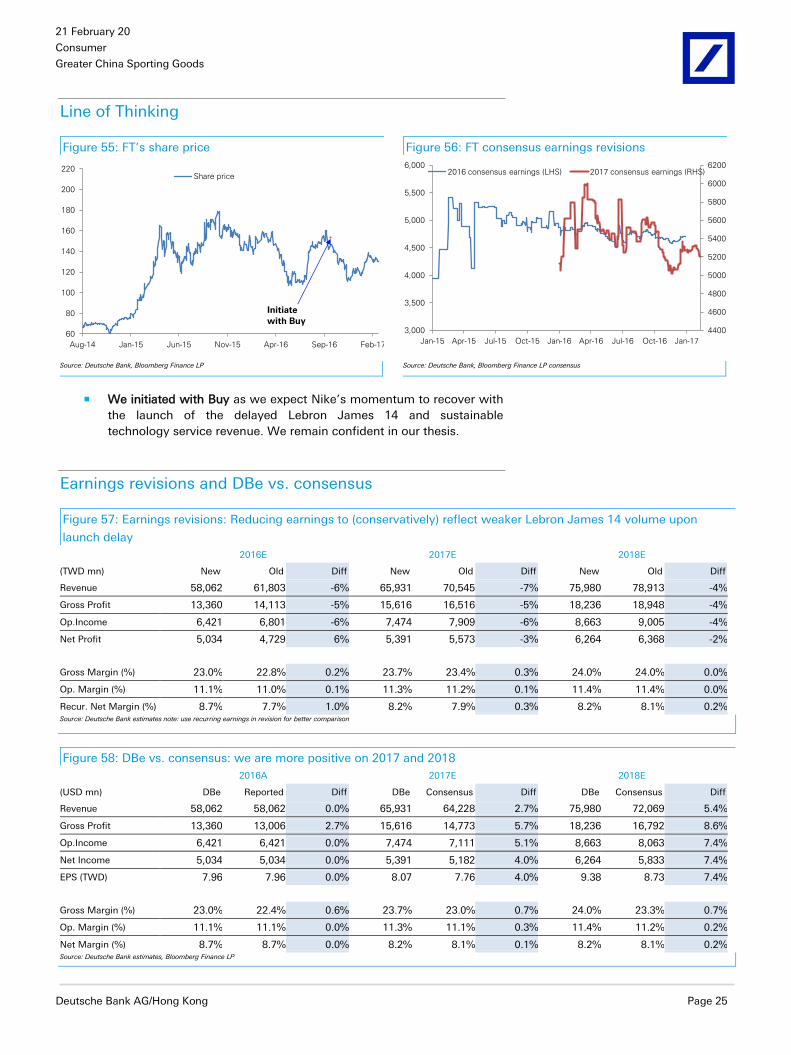

Line of Thinking

Figure 55: FT’s share price Figure 56: FT consensus earnings revisions

60

80

100

120

140

160

180

200

220

Aug-14 Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17

Share price

Initiate

with Buy

4400

4600

4800

5000

5200

5400

5600

5800

6000

6200

3,000

3,500

4,000

4,500

5,000

5,500

6,000

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17

2016 consensus earnings (LHS) 2017 consensus earnings (RHS)

Source: Deutsche Bank, Bloomberg Finance LP

Source: Deutsche Bank, Bloomberg Finance LP consensus

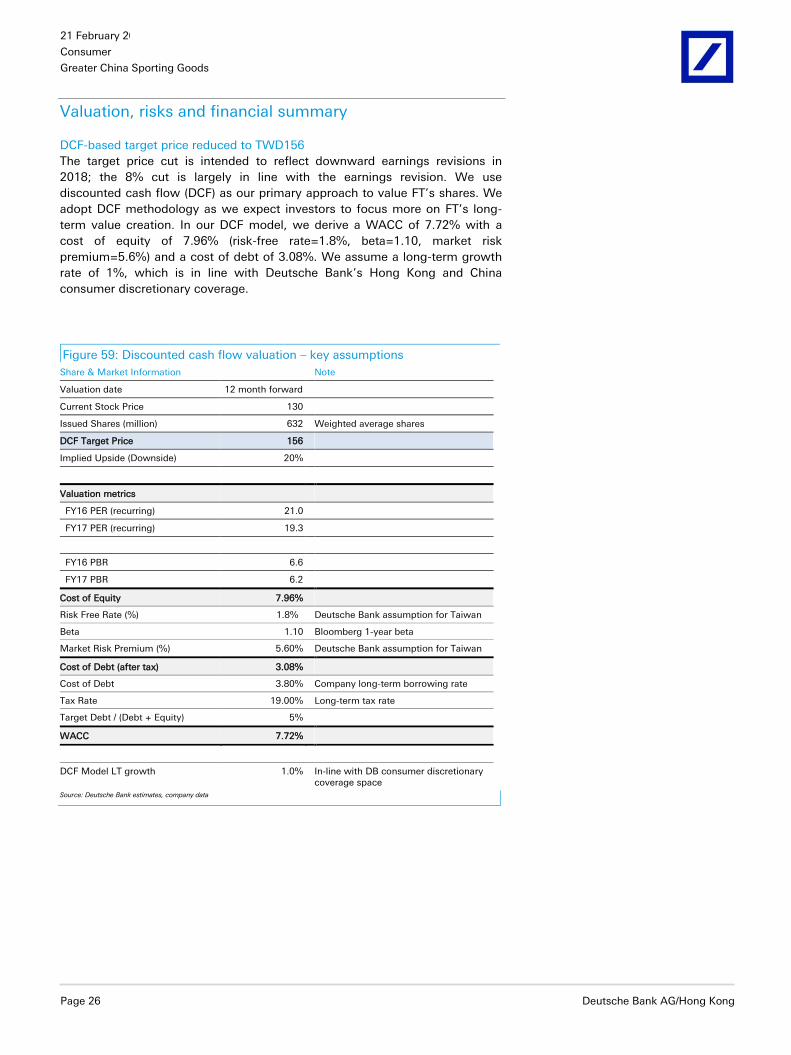

We initiated with Buy as we expect Nike’s momentum to recover with

the launch of the delayed Lebron James 14 and sustainable

technology service revenue. We remain confident in our thesis.

Earnings revisions and DBe vs. consensus

Figure 57: Earnings revisions: Reducing earnings to (conservatively) reflect weaker Lebron James 14 volume upon

launch delay

2016E 2017E 2018E

(TWD mn) New Old Diff New Old Diff New Old Diff

Revenue 58,062 61,803 -6% 65,931 70,545 -7% 75,980 78,913 -4%

Gross Profit 13,360 14,113 -5% 15,616 16,516 -5% 18,236 18,948 -4%

Op.Income 6,421 6,801 -6% 7,474 7,909 -6% 8,663 9,005 -4%

Net Profit 5,034 4,729 6% 5,391 5,573 -3% 6,264 6,368 -2%

Gross Margin (%) 23.0% 22.8% 0.2% 23.7% 23.4% 0.3% 24.0% 24.0% 0.0%

Op. Margin (%) 11.1% 11.0% 0.1% 11.3% 11.2% 0.1% 11.4% 11.4% 0.0%