Granularity Adjustment for Risk Measures: Systematic vs Unsystematic Risks Patrick Gagliardini ∗ Christian Gouri´ eroux † September 2010 ‡ ∗ Swiss Finance Institute and University of Lugano. † CREST, CEPREMAP and University of Toronto. ‡ Acknowledgements: We thank the participants at the Workshop on Granularity at AXA (Paris) and at the Finance Seminar of HEC Geneva for very useful comments. The first author gratefully acknowledges financial support of the Swiss National Science Foundation through the NCCR FINRISK network. The second author gratefully acknowledges financial support of NSERC Canada and the chair AXA/Risk Foundation: ”Large Risks in Insurance”. 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Granularity Adjustment for Risk Measures:

Systematic vs Unsystematic Risks

Patrick Gagliardini ∗

Christian Gourieroux †

September 2010 ‡

∗Swiss Finance Institute and University of Lugano.†CREST, CEPREMAP and University of Toronto.‡Acknowledgements: We thank the participants at the Workshop on Granularity at AXA (Paris) and at the Finance

Seminar of HEC Geneva for very useful comments. The first author gratefully acknowledges financial support of the

Swiss National Science Foundation through the NCCR FINRISK network. The second author gratefully acknowledges

financial support of NSERC Canada and the chair AXA/Risk Foundation: ”Large Risks in Insurance”.

1

Granularity Adjustment for Risk Measures:

Systematic vs Unsystematic Risks

Abstract

The granularity principle [Gordy (2003)] allows for closed form expressions of the risk mea-

sures of a large portfolio at order 1/n, where n is the portfolio size. The granularity principle

yields a decomposition of such risk measures that highlights the different effects of systematic and

unsystematic risks. This paper derives the granularity adjustment of the Value-at-Risk (VaR), the

Expected Shortfall and the other distortion risk measures for both static and dynamic risk factor

models. The systematic factor can be multidimensional. The methodology is illustrated by several

examples, such as the stochastic drift and volatility model, or the dynamic factor model for joint

analysis of default and loss given default.

Keywords: Value-at-Risk, Granularity, Large Portfolio, Credit Risk, Systematic Risk, Loss Given

Default, Basel 2 Regulation, Credibility Theory.

JEL classification: G12, C23.

2

1 Introduction

Risk measures such as the Value-at-Risk (VaR), the Expected Shortfall (also called Tail VaR) and

more generally the Distortion Risk Measures (DRM) [Wang (2000)] are the basis of the new risk

management policies and regulations in both Finance (Basel 2) and Insurance (Solvency 2). These

measures are used to define the minimum capital required to hedge risky investments (Pillar 1 in

Basel 2). They are also used to monitor the risk by means of internal risk models (Pillar 2 in Basel

2).

These risk measures have in particular to be computed for large portfolios of individual con-

tracts, which can be loans, mortgages, life insurance contracts, or Credit Default Swaps (CDS),

and for derivative assets written on such large portfolios, such as Mortgage Backed Securities,

Collateralized Debt Obligations, derivatives on a CDS index (such as iTraxx, or CDX), Insurance

Linked Securities, or longevity bonds. The value of a portfolio risk measure is often difficult to

derive even numerically due to

i) the large size of the support portfolio, which can include from about one hundred 1 to several

thousands of individual contracts;

ii) the nonlinearity of individual risks, such as default, recovery, claim occurrence, prepayment,

surrender, lapse;

iii) the need to take into account the dependence between individual risks induced by the sys-

tematic components of these risks.

The granularity principle has been introduced for static single factor models during the dis-

cussion on the New Basel Capital Accord [BCBS (2001)], following the contributions by Gordy

(2003) and Wilde (2001). The granularity principle allows for closed form expressions of the risk

measures for large portfolios at order 1/n, where n denotes the portfolio size. More precisely, any

portfolio risk measure can be decomposed as the sum of an asymptotic risk measure corresponding

to an infinite portfolio size and 1/n times an adjustment term. The asymptotic portfolio risk mea-

sure, called Cross-Sectional Asymptotic (CSA) risk measure, captures the non diversifiable effect

of systematic risks on the portfolio. The adjustment term, called Granularity Adjustment (GA),

summarizes the effect of the individual specific risks and their cross-effect with systematic risks,

1This corresponds to the number of names included in the iTraxx, or CDX indexes.

3

when the portfolio size is large, but finite.

Despite its analytical tractability and intuitive appeal, the static single risk factor model is too

restrictive to capture the complexity and dynamics of systematic risks. Multiple dynamic factors

are needed for a joint analysis of stochastic drift and volatility, of default and loss given default,

to model country and industrial sector specific effects, to monitor the risk of loans with guaran-

tees, when the guarantors themselves can default [Ebert, Lutkebohmert (2009)], or to distinguish

between trend and cycle effects. Motivated by these applications, the purpose of our paper is to

extend the granularity approach to a dynamic multiple factor framework.

The static risk factor model is introduced in Section 2, and the granularity adjustment of the

VaR is given in Section 3. The GA for the VaR can be used to derive easily the GA for any

other Distortion Risk Measure, including for instance Expected Shortfall. Section 4 provides the

granularity adjustment for a variety of static single and multiple risk factor models. The analysis is

extended to dynamic risk factor models in Section 5. In the dynamic framework, two granularity

adjustments are required. The first GA concerns the conditional VaR with current factor value

assumed to be observed. The second GA takes into account the unobservability of the current

factor value. This new decomposition relies on recent results on the granularity principle applied

to nonlinearing filtering problems [Gagliardini, Gourieroux (2010)a]. Whereas the initial version

of the Basel 2 regulation has focused on modeling the stochastic probability of default assuming a

deterministic loss given default, the most advanced approaches have to account for the uncertainty

in the recovery rate and its correlation with the probability of default. In Section 6 we introduce a

dynamic two-factor model with stochastic probability of default and loss given default, and derive

the patterns of the granularity adjustment. Section 7 concludes. The theoretical derivations of the

granularity adjustments are done in the Appendices.

2 Static Risk Factor Model

We first consider the static risk factor model to focus on the individual risks and their dependence

structure. We omit the unnecessary time index.

4

2.1 Homogenous Portfolio

Let us assume that the individual risks (e.g. asset values, or default indicators) depend on some

common factors and on individual specific effects:

yi = c(F, ui), i = 1, . . . , n, (2.1)

where yi denotes the individual risk, F the systematic factor and ui the idiosyncratic term. Both

F and ui can be multidimensional, whereas yi is one-dimensional. Variables F and ui satisfy the

following assumptions:

Distributional Assumptions: For any portfolio size n:

A.1: F and (u1, . . . , un) are independent.

A.2: u1, . . . , un are independent and identically distributed.

The portfolio of individual risks is homogenous, since the joint distribution of (y1, . . . , yn) is

invariant by permutation of the n individuals, for any n. This exchangeability property of the indi-

vidual risks is equivalent to the fact that variables y1, . . . , yn are independent, identically distributed

conditional on some factor F [de Finetti (1931), Hewitt, Savage (1955)]. When the unobservable

systematic factor F is integrated out, the individual risks become dependent.

2.2 Examples

We describe below simple examples of static Risk Factor Model (RFM) (see Section 4 for further

examples).

Example 2.1: Linear Single-Factor Model

We have:

yi = F + ui,

where the specific error terms ui are Gaussian N(0, σ2) and the factor F is Gaussian N(μ, η2).

Since Corr (yi, yj) = η2/(η2+σ2), for i �= j, the common factor creates the (positive) dependence

between individual risks, whenever η2 �= 0. This model has been used rather early in the literature

5

on individual risks. For instance, it is the Buhlmann model considered in actuarial science and is

the basis for credibility theory [Buhlmann (1967), Buhlmann, Straub (1970)].

Example 2.2: The Single Risk Factor Model for Default

The individual risk is the default indicator, that is yi = 1, if there is a default of individual i,

and yi = 0, otherwise. This risk variable is given by:

yi =

⎧⎨⎩ 1, if F + ui < 0,

0, otherwise,

where F ∼ N(μ, η2) and ui ∼ N(0, σ2). The quantity F + ui is often interpreted as a log as-

set/liability ratio, when i is a company [see e.g. Merton (1974), Vasicek (1991)]. Thus, the com-

pany defaults when the asset value becomes smaller than the amount of debt.

The basic specifications in Examples 2.1 and 2.2 can be extended by introducing additional

individual heterogeneity, or multiple factors.

Example 2.3: Model with Stochastic Drift and Volatility

The individual risks are such that:

yi = F1 + (exp F2)1/2ui,

where F1 (resp. F2) is a common stochastic drift factor (resp. stochastic volatility factor). When

yi is an asset return, we expect factors F1 and F2 to be dependent, since the (conditional) expected

return generally contains a risk premium.

Example 2.4: Linear Single Risk Factor Model with Beta Heterogeneity

This is a linear factor model, in which the individual risks may have different sensitivities

(called betas) to the systematic factor. The model is:

yi = βiF + vi,

where ui = (βi, vi)′ is bidimensional. In particular, the betas are assumed unobservable and are

included among the idiosyncratic risks. This type of model is the basis of Arbitrage Pricing Theory

(APT) [see e.g. Ross (1976), and Chamberlain, Rothschild (1983), in which similar assumptions

are introduced on the beta coefficients].

6

3 Granularity Adjustment for Portfolio Risk Measures

3.1 Portfolio Risk

Let us consider an homogenous portfolio including n individual risks. The total portfolio risk is:

Wn =n∑

i=1

yi =n∑

i=1

c(F, ui). (3.1)

The total portfolio risk can correspond to a profit and loss (P&L), for instance when yi is an asset

return and Wn/n the equally weighted portfolio return. In other cases, it corresponds to a loss and

profit (L&P), for instance when yi is a default indicator and Wn/n the portfolio default frequency

2. As usual, we pass from a P&L to a L&P by a change of sign 3. The quantile of Wn at a given

risk level is used to define a VaR (resp. the opposite of a VaR), if Wn is a L&P (resp. a P&L).

The distribution of Wn is generally unknown in closed form due to the risks dependence and

the aggregation step. The density of Wn involves integrals with a large dimension, which can reach

dim(F ) + n dim(u) − 1. Therefore, the quantiles of the distribution of Wn, can also be difficult

to compute 4. To address this issue we consider a large portfolio perspective.

3.2 Asymptotic Portfolio Risk

The standard limit theorems such as the Law of Large Numbers (LLN) and the Central Limit

Theorem (CLT) cannot be applied directly to the sequence y1, . . . , yn due to the common factors.

However, LLN and CLT can be applied conditionally on the factor values, under Assumptions

A.1 and A.2. This is the condition of infinitely fine grained portfolio 5 in the Basel 2 terminology

2The results of the paper are easily extended to obligors with different exposures Ai, say. In this case we have

Wn =n∑

i=1

Aiyi =n∑

i=1

Aic(F, ui) =n∑

i=1

c∗(F, u∗i ), where the idiosyncratic risks u∗

i = (ui, Ai) contain the individual

shocks ui and the individual exposures Ai [see e.g. Emmer, Tasche (2005) in a particular case].3This means that asset returns will be replaced by opposite asset returns, that are returns for investors with short

positions.4The VaR can often be approximated by simulations [see e.g. Glasserman, Li (2005)], but these simulations are

very time consuming, if the portfolio size is large and the risk level of the VaR is small, especially in dynamic factor

models.5Loosely speaking, “the portfolio is infinitely fine grained, when the largest individual exposure accounts for an

infinitely small share of the total portfolio exposure” [Ebert, Lutkebohmert (2009)]. This condition is satisfied under

Assumptions A.1 and A.2.

7

[BCBS (2001)].

Let us denote by

m(F ) = E[yi|F ] = E[c(F, ui)|F ], (3.2)

the conditional individual expected risk, and

σ2(F ) = V [yi|F ] = V [c(F, ui)|F ], (3.3)

the conditional individual volatility. By applying the CLT conditional on F , we get:

Wn/n = m(F ) + σ(F )X√n

+ O(1/n), (3.4)

where X is a standard Gaussian variable independent of factor F . The term at order O(1/n) is

zero mean, conditional on F , since Wn/n is a conditionally unbiased estimator of m(F ).

Expansion (3.4) differs from the expansion associated with the standard CLT. Whereas the

first term of the expansion is constant, equal to the unconditional mean in the standard CLT, it is

stochastic in expansion (3.4) and linked with the second term of the expansion by means of factor

F . Moreover, each term in the expansion depends on the factor value, but also on the distribution of

idiosyncratic risk by means of functions m(.) and σ(.). By considering expansion (3.4), the initial

model with dim(F ) + n dim(u) dimensions of uncertainty is approximated by a 3-dimensional

model, with uncertainty summarized by means of m(F ), σ(F ) and X .

3.3 Granularity principle

The granularity principle has been introduced for static single risk factor models by Gordy in

2000 for application in Basel 2 [Gordy (2003)]. We extend below this principle to multiple factor

models. The granularity principle requires several steps, which are presented below for a loss and

profit variable.

i) A standardized risk measure

Instead of the VaR of the portfolio risk, which explodes with the portfolio size, it is preferable to

consider the VaR per individual risk (asset) included in this portfolio. Since by Assumptions A.1-

A.2 the individuals are exchangeable and a quantile function is homothetic, the VaR per individual

8

risk is simply a quantile of Wn/n. The VaR at risk level α∗ = 1 − α is denoted by V aRn(α) and

is defined by the condition:

P [Wn/n < V aRn(α)] = α, (3.5)

where α is a positive number close to 1, typically α = 95%, 99%, 99.5%, which correspond to

probabilities of large losses equal to α∗ = 5%, 1%, 0.5%, respectively.

ii) The CSA risk measure

Vasicek [Vasicek (1991)] proposed to first consider the limiting case of a portfolio with infinite

size. Since

limn→∞

Wn/n = m(F ), a.s., (3.6)

the infinite size portfolio is not riskfree. Indeed, the systematic risk is undiversifiable. We deduce

that the CSA risk measure:

V aR∞(α) = limn→∞

V aRn(α), (3.7)

is the α-quantile associated with the systematic component of the portfolio risk:

P [m(F ) < V aR∞(α)] = α. (3.8)

The CSA risk measure is suggested in the Internal Ratings Based (IRB) approach of Basel 2 for

minimum capital requirement. This approach neglects the effect of unsystematic risks in a portfolio

of finite size.

iii) Granularity Adjustment for the risk measure

The main result in granularity theory applied to risk measures provides the next term in the

asymptotic expansion of V aRn(α) with respect to n, for large n. It is given below for a multiple

factor model.

Proposition 1: In a static RFM, we have:

V aRn(α) = V aR∞(α) +1

nGA(α) + o(1/n),

9

where:

GA(α) = −1

2

{d log g∞

dw[V aR∞(α)]E[σ2(F )|m(F ) = V aR∞(α)]

+d

dwE[σ2(F )|m(F ) = w]

∣∣∣∣w=V aR∞(α)

}

= −1

2E[σ2(F )|m(F ) = V aR∞(α)

]{d log g∞dw

[V aR∞(α)]

+d

dwlog E

[σ2(F )|m(F ) = w

]∣∣∣∣w=V aR∞(α)

},

and g∞ [resp. V aR∞(.)] denotes the probability density function (resp. the quantile function) of

the random variable m(F ).

Proof: See Appendix 1.

The GA in Proposition 1 depends on the tail magnitude of the systematic risk component

m(F ) by means ofd log g∞

dw[V aR∞(α)], which is expected to be negative. The GA depends also

ond

dwlog E

[σ2(F )|m(F ) = w

]∣∣∣∣w=V aR∞(α)

, which is a measure of the reaction of the individual

volatility to shocks on the individual drift. When yi,t is the opposite of an asset return, this reaction

function is expected to be nonlinear and increasing for positive values of m(F ), according to the

leverage effect interpretation [Black (1976)].

When the tail effect is larger than the leverage effect, the GA is positive, which implies an

increase of the required capital compared to the CSA risk measure. In the special case of indepen-

dent stochastic drift and volatility, the GA reduces to GA(α) = −1

2E[σ2(F )|m(F ) = V aR∞(α)

]d log g∞

dw[V aR∞(α)], which is generally positive. The adjustment involves both the tail of the sys-

tematic risk component and the expected conditional variability of the individual risks.

The asymptotic expansion of the VaR in Proposition 1 is important for several reasons. i) The

computation of quantities V aR∞(α) and GA(α) does not require the evaluation of large dimen-

sional integrals. Indeed, V aR∞(α) and GA(α) involve the distribution of transformations m(F )

and σ2(F ) of the systematic factor only, which are independent of the portfolio size n.

ii) The second term in the expansion is of order 1/n, and not 1/√

n as might have been expected

from the Central Limit Theorem. This implies that the approximation V aR∞(α) +1

nGA(α) is

likely rather accurate, even for rather small values of n such as n = 100.

10

iii) The expansion is valid for single as well as multiple factor models.

iv) The expansion is easily extended to the other Distortion Risk Measures, which are weighted

averages of VaR:

DRMn(H) =

∫V aRn(u)dH(u), say,

where H denotes the distortion measure [Wang (2000)]. The granularity adjustment for the DRM

is simply:1

n

∫GA(u)dH(u).

In particular, the Expected Shortfall at confidence level α corresponds to the distortion measure

with cumulative distribution function H(u; α) = (u−α)+/(1−α), and the granularity adjustment

is1

n(1 − α)

∫ 1

α

GA(u)du,

that is an average of the granularity adjustments for VaR above level α.

v) Proposition 1 can be used to investigate the difficult task of aggregation of risk measures.

In Appendix 2 we derive the granularity approximation for the VaR of an heterogeneous portfolio

and relate it to the risk measures of the different homogeneous subpopulations.

4 Examples

This section provides the closed form expressions of the GA for the examples introduced in Section

2. We first consider single factor models, in which the GA formula is greatly simplified, then

models with multiple factor.

4.1 Single Risk Factor Model

In a single factor model, the factor can generally be identified with the expected individual risk:

m(F ) = F. (4.1)

Then, V aR∞(α) is the α-quantile of factor F and g∞ is its density function. The granularity

adjustment of the VaR becomes:

GA(α) = −1

2

{d log g∞

dF[V aR∞(α)]σ2[V aR∞(α)] +

dσ2

dF[V aR∞(α)]

}. (4.2)

11

This formula has been initially derived by Wilde (2001) [see also Martin, Wilde (2002), Gordy

(2003, 2004)], based on the local analysis of the VaR [Gourieroux, Laurent, Scaillet (2000)] and

Expected Shortfall [Tasche (2000)]. 6

Example 4.1: Linear Single Risk Factor Model [Gordy (2004)]

In the linear model yi = F + ui, with F ∼ N(μ, η2) and ui ∼ N(0, σ2), we have m(F ) = F ,

σ2(F ) = σ2, g∞(F ) =1

ηϕ

(F − μ

η

), and V aR∞(α) = μ + ηΦ−1(α), where ϕ (resp. Φ) is the

density function (resp. cumulative distribution function) of the standard normal distribution. We

deduce:

GA(α) = −σ2

2

d log g∞dF

[V aR∞(α)] =σ2

2ηΦ−1(α).

In this simple Gaussian framework, the quantile V aRn(α) is known in closed form, and the

above GA corresponds to the first-order term in a Taylor expansion of V aRn(α) w.r.t. 1/n. Indeed,

we have Wn/n ∼ N (μ, η2 + σ2/n) and:

V aRn(α) = μ +

√η2 +

σ2

nΦ−1(α) = μ + ηΦ−1(α) +

1

n

σ2

2ηΦ−1(α) + o(1/n).

As expected the GA is positive for large α, more precisely for α > 0.5. The GA increases when the

idiosyncratic risk increases, that is, when σ2 increases. Moreover, the GA is a decreasing function

of η, which means that the adjustment is smaller, when systematic risk increases.

Example 4.2: Static RFM for Default

Let us assume that the individual risks follow independent Bernoulli distributions conditional

on factor F :

yi ∼ B(1, F ),

where B(1, p) denotes a Bernoulli distribution with probability p. This is the well-known model

with stochastic probability of default, often called reduced form model or stochastic intensity

model in the Credit Risk literature. In this case Wn/n is the default frequency in the portfolio.

6When the factor F is not identified with the conditional mean m(F ), but the function m(.) is increasing, formula

(4.2) becomes:

GA(α) = −12

⎧⎪⎨⎪⎩

1g∞(F )

d

dF

⎡⎢⎣σ2(F )g∞(F )

dm

dF(F )

⎤⎥⎦⎫⎪⎬⎪⎭

F=m−1(V aR∞(α))

, (4.3)

where g∞ is the density of F (see Appendix 3 for the derivation).

12

It also corresponds to the portfolio loss given default, if the loans have a unitary nominal and a

zero recovery rate. In this model we have m(F ) = F , σ2(F ) = F (1 − F ), and we deduce:

GA(α) = −1

2

{d log g∞

dF[V aR∞(α)]V aR∞(α)[1 − V aR∞(α)] + 1 − 2V aR∞(α)

}. (4.4)

This formula appears for instance in Rau-Bredow (2005).

Different specifications have been considered in the literature for stochastic intensity F . 7 Let

us assume that there exists an increasing transformation A, say, from (−∞, +∞) to (0,1) such

that:

A−1(F ) ∼ N(μ, η2). (4.5)

We get a logit (resp. probit) normal specification, when A is the cumulative distribution function

of the the logistic distribution (resp. the standard normal distribution). A logit specification is used

in CreditPortfolioView by Mc Kinsey, a probit specification is proposed in KMV/Moody’s and

CreditMetrics. Let us denote a(y) =dA(y)

dythe associated derivative. We have:

V aR∞(α) = A[μ + ηΦ−1(α)],

(4.6)d log g∞

dF[V aR∞(α)] = − 1

a[μ + ηΦ−1(α)]

(Φ−1(α)

η+

d log a

dy[μ + ηΦ−1(α)]

).

i) In the logit normal reduced form, the transformation A−1(F ) = log[F/(1−F )] corresponds

to the log of an odd ratio, and the formula for the GA simplifies considerably:

V aR∞(α) =1

1 + exp[−μ − ηΦ−1(α)], GA(α) =

1

2ηΦ−1(α).

In particular, the GA doesn’t depend on parameter μ.

ii) Let us now consider the structural Merton (1974) - Vasicek (1991) model [see Example

2.2]. This model can be written in terms of two structural parameters, that are the unconditional

7Gordy (2004) and Gordy, Lutkebohmert (2007) derive the GA in the CreditRisk+ model [Credit Suisse Financial

Products (1997)], which has been the basis for the granularity adjustment proposed in the New Basel Capital Accord

[see BCBS (2001, Chapter 8) and Wilde (2001)]. The CreditRisk+ model has some limitations. First, it assumes that

the stochastic probability of default F follows a gamma distribution, that admits values of default probability larger

than 1. Second, it assumes a constant expected loss given default. We present a multi-factor model with stochastic

default probability and expected loss given default in Section 6.

13

probability of default PD and the asset correlation ρ, such as:

yi = 1l−Φ−1(PD) +√

ρF ∗ +√

1 − ρu∗i < 0

,

where F ∗ and u∗i , for i = 1, · · · , n, are independent standard Gaussian variables. The structural

factor F ∗ is distinguished from the reduced form factor F which is the stochastic probability of

default. They are related by:

Φ−1(F ) =Φ−1(PD)√

1 − ρ−

√ρ√

1 − ρF ∗.

From (4.5) we deduce that:

μ =Φ−1(PD)√

1 − ρ, η =

√ρ

1 − ρ. (4.7)

Thus, from (4.4)-(4.7) we deduce the CSA VaR [Vasicek (1991)]:

V aR∞(α) = Φ

(Φ−1(PD) +

√ρΦ−1(α)√

1 − ρ

), (4.8)

and the granularity adjustment (see Appendix 4):

GA(α) =1

2

⎧⎪⎪⎨⎪⎪⎩

√1 − ρ

ρΦ−1(α) − Φ−1 [V aR∞(α)]

φ (Φ−1 [V aR∞(α)])V aR∞(α)[1 − V aR∞(α)] + 2V aR∞(α) − 1

⎫⎪⎪⎬⎪⎪⎭ .

(4.9)

Equation (4.9) is similar to formula (2.17) in Emmer, Tasche (2005) [see also Gordy, Marrone

(2010), equation (5)], but is written in a way that shows how the GA depends on the uncondi-

tional probability of default PD and asset correlation ρ. This dependence occurs through the term√(1 − ρ)/ρ and the CSA quantile V aR∞(α).

In Figure 1 we display the CSA quantile V aR∞(α) and the granularity adjustment per contract

1nGA(α) as functions of asset correlation ρ and for different values of the unconditional proba-

bility of default, that are PD = 0.5%, 1%, 5%, and 20%, respectively. These values of PD are

representative for the default probabilities of a firm with rating BBB, BB, B and C, respectively, in

the rating system by S&P. The confidence level is α = 0.99 and the portfolio size is n = 1000.

[Insert Figure 1: CSA CreditVaR and granularity adjustment as functions of the asset correla-

tion in the Merton-Vasicek model.]

14

The CSA VaR is monotone increasing w.r.t. asset correlation ρ when the probability of default is

such that PD ≥ 1−α; for PD < 1−α, the CSA VaR is increasing w.r.t. ρ up to a maximum and

then converges to zero as ρ approaches 1. In the interval of asset correlation values ρ ∈ [0.12, 0.24]

considered for obligors in the Basel 2 regulation [see BCBS(2001)], the CSA VaR is about 0.05

for obligors with PD = 1%, while the GA per contract is about 0.005 for n = 1000 (and 0.05 for

n = 100). Thus, the magnitude of the GA can be significant w.r.t. the CSA VaR. The granularity

adjustment is decreasing w.r.t. asset correlation ρ, when ρ is not close to 1.

In Figure 2 we display the CSA quantile V aR∞(α) and the granularity adjustment per contract

1nGA(α) as functions of probability of default PD and for different values of the asset correlation,

that are ρ = 0.05, 0.12, 0.24, and 0.50, respectively.

[Insert Figure 2: CSA CreditVaR and granularity adjustment as functions of the unconditional

probability of default in the Merton-Vasicek model.]

The CSA VaR is monotone increasing w.r.t. the probability of default PD. The granularity adjust-

ment features an inverse-U shape. The maximum GA occurs for values of PD corresponding to

speculative grade ratings, when ρ is between 0.12 and 0.24.

Example 4.3: Linear Static RFM with Beta Heterogeneity

Let us consider the model of Example 2.4. We have yi = βiF + vi, where F ∼ N(μ, η2),

vi ∼ N(0, σ2), and βi ∼ N(1, γ2), with all these variables independent. Due to a problem of

factor identification, the mean of βi can always be fixed to 1. This also facilitates the comparison

with the model with constant beta of Example 4.1. We get m(F ) = F , σ2(F ) = σ2 + γ2F 2, and:

GA(α) =σ2

2ηΦ−1(α) + γ2

[V aR∞(α)2 Φ−1(α)

2η− V aR∞(α)

], (4.10)

where V aR∞(α) = μ + ηΦ−1(α). Thus, the CSA risk measure V aR∞(α) is computed in the

homogenous model with factor sensitivity β = 1. The granularity adjustment accounts for beta

heterogeneity in the portfolio through the variance γ2 of the heterogeneity distribution. More

precisely, the first term in the RHS of (4.10) is the GA already derived in Example 4.1, whereas

the second term is specific of the beta heterogeneity.

15

4.2 Multiple Risk Factor Model

Example 4.4: Stochastic Drift and Volatility Model

Let us assume that yi ∼ N(F1, exp F2), conditional on the bivariate factor F = (F1, F2)′, and

that

F ∼ N

⎡⎣⎛⎝ μ1

μ2

⎞⎠ ,

⎛⎝ η2

1 ρη1η2

ρη1η2 η22

⎞⎠⎤⎦ .

This type of stochastic volatility model is standard for modelling the dynamic of asset returns, or

equivalently of opposite asset returns.

We can introduce the regression equation:

F2 = μ2 +ρη2

η1

(F1 − μ1) + v,

where v is independent of F1, with Gaussian distribution N [0, η22(1 − ρ2)]. We have m(F ) = F1,

σ2(F ) = exp(F2), and

E[σ2(F )|m(F )] = E[exp F2|F1] = E[exp{μ2 +ρη2

η1

(F1 − μ1) + v}|F1]

= exp

[μ2 +

ρη2

η1

(F1 − μ1)

]E[exp(v)]

= exp

[μ2 +

ρη2

η1

(F1 − μ1) +η2

2(1 − ρ2)

2

].

In particular:

d

dwlog E

[σ2(F )|m(F ) = w

]=

d

dF1

log E [F2|F1] =ρη2

η1

.

When yi is the opposite of an asset return, a positive value ρ > 0, i.e. a negative correlation

between return and volatility, can represent a leverage effect. From Proposition 1, we deduce that:

GA(α) =1

2η1

[Φ−1(α) − ρη2] exp[μ2 + η22/2] exp

[ρη2Φ

−1(α) +ρ2η2

2

2

].

The GA of the linear single-factor RFM (see Example 4.1) is obtained when either factor F2 is

constant (η2 = 0), or factors F1 and F2 are independent (ρ = 0), by noting that E[exp F2] =

exp[μ2 + η22/2].

16

5 Dynamic Risk Factor Model (DRFM)

The static risk factor model implicitly assumes that the past observations are not informative to

predict the future risk. In dynamic factor models, the VaR becomes a function of the available

information. This conditional VaR has to account for the unobservability of the current and lagged

factor values. We show in this section that factor unobservability implies an additional GA for the

VaR. Despite this further layer of complexity in dynamic models, the granularity principle becomes

even more useful compared to the static framework. Indeed, the conditional cdf of the portfolio

value at date t involves an integral that can reach dimension (t+1)dim(F )+n dim(u)−1, which

now depends on t, due to the integration w.r.t. the factor path.

5.1 The Model

Dynamic features can easily be introduced in the following way:

i) We still assume a static relationship between the individual risks and the systematic factors.

This relationship is given by the static measurement equations:

yit = c(Ft, uit), (5.1)

where the idiosyncratic risks (ui,t) are independent, identically distributed across individuals and

dates, and independent of the factor process (Ft).

ii) Then, we allow for factor dynamic. The factor process (Ft) is Markov with transition pdf

g(ft|ft−1), say. Thus, all the dynamics of individual risks pass by means of the factor dynamic.

Let us now consider the future portfolio risk per individual asset defined by Wn,t+1/n =

1

n

n∑i=1

yi,t+1. The (conditional) VaR at horizon 1 is defined by the equation:

P [Wn,t+1/n < V aRn,t(α)|In,t] = α, (5.2)

where the available information In,t includes all current and past individual risks yi,t, yi,t−1, . . .,

for i = 1, . . . , n, but not the current and past factor values. The conditional quantile V aRn,t(α)

depends on date t through the information In,t.

17

5.2 Granularity Adjustment

i) Asymptotic expansion of the portfolio risk

Let us first perform an asymptotic expansion of the portfolio risk. By the cross-sectional CLT

applied conditional on the factor path, we have:

Wn,t+1/n = m(Ft+1) + σ(Ft+1)Xt+1√

n+ O(1/n),

where the variable Xt+1 is standard normal, independent of the factor process, and O(1/n) denotes

a term of order 1/n, which is zero-mean conditional on Ft+1, Ft, · · · . The functions m(.) and σ2(.)

are defined analogously as in (3.2)-(3.3), and depend on Ft+1 only by the static measurement

equations (5.1).

In order to compute the conditional cdf of Wn,t+1/n, it is useful to reintroduce the current

factor value in the conditioning set through the law of iterated expectation. We have:

P [Wn,t+1/n < y|In,t] = E[P (Wn,t+1/n < y|Ft, In,t)|In,t]

= E[P (Wn,t+1/n < y|Ft)|In,t]

= E[P (m(Ft+1) + σ(Ft+1)Xt+1√

n+ O(1/n) < y|Ft)|In,t]

= E[a(y,Xt+1√

n+ O(1/n); Ft)|In,t], (5.3)

where function a is defined by:

a(y, ε; ft) = P [m(Ft+1) + σ(Ft+1)ε < y|Ft = ft]. (5.4)

ii) Cross-sectional approximation of the factor

Function a depends on the unobserved factor value Ft = ft, and we have first to explain how

this value can be approximated from observed individual variables. For this purpose, let us denote

by h(yi,t|ft) the conditional density of yi,t given Ft = ft, deduced from model (5.1), and define

the cross-sectional maximum likelihood approximation of ft given by:

fn,t = arg maxft

n∑i=1

log h(yi,t|ft). (5.5)

18

The factor value ft is treated as an unknown parameter in the cross-sectional conditional model at

date t and is approximated by the maximum likelihood principle. Approximation fnt is a function

of the current individual observations and hence of the available information In,t.

iii) Granularity Adjustment for factor prediction

It might seem natural to replace the unobserved factor value ft by its cross-sectional approxi-

mation fn,t in the expression of function a, and then to use the GA of the static model in Proposition

1, for the distribution of Ft+1 given Ft = fn,t. However, replacing ft by fn,t implies an approxi-

mation error. It has been proved that this error is of order 1/n, that is, the same order expected for

the GA. More precisely, we have the following result which is given in the single factor framework

for expository purpose [Gagliardini, Gourieroux (2010a), Corollary 5.3]:

Proposition 2: Let us consider a dynamic single factor model. For a large homogenous portfolio,

the conditional distribution of Ft given In,t is approximately normal at order 1/n:

N

(fn,t +

1

nμn,t,

1

nJ−1

n,t

),

where:

μn,t = J−1n,t

∂ log g

∂ft

(fn,t|fn,t−1) +1

2J−2

n,t Kn,t,

Jn,t = − 1

n

n∑i=1

∂2 log h

∂f 2t

(yi,t|fn,t),

Kn,t =1

n

n∑i=1

∂3 log h

∂f 3t

(yi,t|fn,t).

Proposition 2 gives an approximation of the filtering distribution of factor Ft given the informa-

tion In,t. Both mean and variance are approximated at order 1/n to apply an Ito’s type correction.

The approximation involves four summary statistics, which are the cross-sectional maximum like-

lihood approximations fn,t and fn,t−1, the Fisher information Jn,t for approximating the factor in

the cross-section at date t, and the statistic Kn,t involved in the bias adjustment.

iii) Expansion of the cdf of portfolio risk

From equation (5.3) and Proposition 2, the conditional cdf of the portfolio risk can be written

as:

P [Wn,t+1/n < y|In,t] = E

[a

(y,

Xt+1√n

+ O(1/n); fn,t +1

nμn,t +

1√n

J−1/2n,t X∗

t

)|In,t

]+ o(1/n),

19

where X∗t is a standard Gaussian variable independent of Xt+1 and O(1/n), of the factor path and

of the available information 8.

Then, we can expand the expression above with respect to n, up to order 1/n. By noting

that fn,t, μn,t, Jn,t are functions of the available information and that E[Xt+1] = E[X∗t ] =

E[O(1/n)] = 0, E[Xt+1X∗t ] = 0, E[X2

t+1] = E[(X∗t )2] = 1, we get:

P [Wn,t+1/n < y|In,t] = a(y, 0; fn,t) +1

n

∂a(y, 0; fnt)

∂ft

μnt

+1

2n

[J−1

n,t

∂2a(y, 0; fn,t)

∂f 2t

+∂2a(y, 0, fnt)

∂ε2

]+ o(1/n).

The CSA conditional cdf of the portfolio risk is a(y, 0; fn,t), where:

a(y, 0; ft) = P [m(Ft+1) < y|Ft = ft]. (5.6)

It corresponds to the conditional cdf of m(Ft+1) given Ft = ft, where the unobservable factor

value ft is replaced by its cross-sectional approximation fn,t. The GA for the cdf is the sum of the

following components:

i) The granularity adjustment for the conditional cdf with known Ft equal to fn,t is

1

2n

∂2a(y, 0; fn,t)

∂ε2. (5.7)

The second-order derivative of function a(y, ε; ft) w.r.t. ε at ε = 0 can be computed by using

Lemma a.1 in Appendix 1, which yields:

∂2a(y, 0; ft)

∂ε2=

d

dy

{g∞(y; ft)E[σ2(Ft+1)|m(Ft+1) = y, Ft = ft]

},

where g∞(y; ft) denotes the pdf of m(Ft+1) conditional on Ft = ft.

ii) The granularity adjustment for filtering is

∂a(y, 0; fn,t)

∂ft

μnt +1

2J−1

n,t

∂2a(y, 0; fnt)

∂f 2t

. (5.8)

It involves the first- and second-order derivatives of the CSA cdf w.r.t. the conditioning factor

value.8The independence between X∗

t and Xt+1 is due to the fact that X∗t simply represents the numerical approximation

of the filtering distribution of Ft given In,t and is not related to the stochastic features of the observations at t + 1 [see

Gagliardini, Gourieroux (2010a)].

20

Due to the independence between variables Xt+1 and X∗t , there is no cross GA.

iv) Granularity Adjustment for the VaR

The CSA cdf is used to define the CSA risk measure V aR∞(α; fn,t) through the condition:

P[m(Ft+1) < V aR∞(α; fn,t)|Ft = fn,t

]= α.

The CSA VaR depends on the current information through the cross-sectional approximation of

the factor value fn,t only. The GA for the (conditional) VaR is directly deduced from the GA of

the (conditional) cdf by applying the Bahadur’s expansion [Bahadur (1966); see Lemma a.3 in

Appendix 1]. We get the next Proposition:

Proposition 3: In a dynamic RFM the (conditional) VaR is such that:

V aRn,t(α) = V aR∞(α; fn,t) +1

n[GArisk,t(α) + GAfilt,t(α)] + o(1/n),

where:

GArisk,t(α) = −1

2

{∂ log g∞(w; fnt)

∂wE[σ2(Ft+1)|m(Ft+1) = w,Ft = fn,t]

+∂

∂wE[σ2(Ft+1)|m(Ft+1) = w,Ft = fn,t]

}w=V aR∞(α;fn,t)

,

and:

GAfilt,t(α) = − 1

g∞[V aR∞(α; fn,t); fn,t]

{∂a[V aR∞(α, fnt), 0; fnt]

∂ft

μnt

+1

2J−1

n,t

∂2a[V aR∞(α; fnt), 0; fnt]

∂f 2t

},

and where g∞(.; ft) [resp. a(., 0; ft) and V aR∞(.; ft)] denotes the pdf (resp. the cdf and quantile)

of m(Ft+1) conditional on Ft = ft.

Thus, the GA for the conditional VaR is the sum of two components. The first one GArisk,t(α)

is the analogue of the GA in the static factor model (see Proposition 1). However, the distribution

of m(Ft+1) and σ2(Ft+1) is now conditional on Ft = ft, and the unobservable factor value ft is

replaced by its cross-sectional approximation fn,t. The second component GAfilt,t(α) is due to the

filtering of the unobservable factor value, and involves first- and second-order derivatives of the

CSA cdf w.r.t. the conditioning factor value.

21

5.3 Linear RFM with AR(1) factor

As an illustration, let us consider the model given by:

yi,t = Ft + ui,t, i = 1, . . . , n,

where:

Ft = μ + ρ(Ft−1 − μ) + vt,

and ui,t, vt are independent, with uit ∼ IIN(0, σ2), vt ∼ IIN(0, η2). In this Gaussian framework

the (conditional) VaR can be computed explicitly, which allows for a comparison with the granu-

larity approximation in order to assess the accuracy of the two GA components and their (relative)

magnitude.

The individual observations can be summarized by their cross-sectional averages 9 and we

have: ⎧⎨⎩ yn,t+1 = Ft+1 + un,t+1,

Ft+1 = μ + ρ(Ft − μ) + vt+1.(5.9)

This implies:

yn,t+1 = μ +1

1 − ρLvt+1 + un,t+1 = μ +

1

1 − ρL(vt+1 + un,t+1 − ρun,t),

where L denotes the lag operator. The process Zt+1 = vt+1 + un,t+1 − ρun,t is a Gaussian MA(1)

process that can be written as Zt+1 = εt+1 − θnεt, where the variables εt are IIN(0, γ2n), say, and

|θn| < 1. The new parameters θn and γn are deduced from the expressions of the variance and

autocovariance at lag 1 of process (Zt). They satisfy:⎧⎪⎨⎪⎩

η2 +σ2

n(1 + ρ2) = γ2

n(1 + θ2n),

ρσ2

n= θnγ

2n.

(5.10)

Hence:

θn =bn −√b2

n − 4ρ2

2ρ, γ2

n =ρσ2

nθn

, (5.11)

9By writing the likelihood of the model, it is seen that the cross-sectional averages are sufficient statistics.

22

where bn = 1 + ρ2 + nη2

σ2and we have selected the root θn such that |θn| < 1. Therefore, variable

yn,t+1 follows a Gaussian ARMA(1,1) process, and we can write:

yn,t+1 = μ +1 − θnL

1 − ρLεt+1

⇐⇒ yn,t+1 = μ +

(1 − 1 − ρL

1 − θnL

)(yn,t+1 − μ) + εt+1

⇐⇒ yn,t+1 = μ +ρ − θn

1 − θnL(yn,t − μ) + εt+1

⇐⇒ yn,t+1 = μ + (ρ − θn)∞∑

j=0

θjn(yn,t−j − μ) + εt+1.

We deduce that the conditional distribution of Wn,t+1/n = yn,t+1 given In,t is Gaussian with mean

μ + (ρ − θn)∞∑

j=0

θjn(yn,t−j − μ) and variance γ2

n.

Proposition 4: In the linear RFM with AR(1) Gaussian factor, the conditional VaR is given by:

V aRn,t(α) = μ + (ρ − θn)∞∑

j=0

θjn(yn,t−j − μ) + γnΦ−1(α),

where θn and γn are given in (5.11).

Thus, the conditional VaR depends on the information In,t through a weighted sum of current and

lagged cross-sectional individual risks averages. The weights decay geometrically with the lag as

powers of parameter θn. Moreover, the information In,t impacts the VaR uniformly in the risk level

α.

Let us now derive the expansion of V aRn,t(α) at order 1/n for large n. From (5.11), the

expansions of parameters θn and γn are:

θn =ρσ2

η2n+ o(1/n), γn = η +

σ2

2nη(1 + ρ2) + o(1/n).

As n → ∞, the MA parameter θn converges to zero and the variance of the shocks γ2n converges

to η2. Hence, the ARMA(1,1) process of the cross-sectional averages yn,t approaches the AR(1)

factor process (Ft) as expected. By plugging the expansions for θn and γn into the expression of

V aRn,t(α) in Proposition 4, we get:

V aRn,t(α) = μ + ρ(yn,t − μ) + ηΦ−1(α)

+1

n

{σ2

2η(1 + ρ2)Φ−1(α) − ρσ2

η2[(yn,t − μ) − ρ(yn,t−1 − μ)]

}+ o(1/n).

23

The first row on the RHS provides the CSA VaR:

V aR∞(α; fn,t) = μ + ρ(yn,t − μ) + ηΦ−1(α). (5.12)

which depends on the information through the cross-sectional maximum likelihood approximation

of the factor fn,t = yn,t. The CSA VaR is the quantile of the normal distribution with mean

μ + ρ(yn,t − μ) and variance η2, that is the conditional distribution of Ft+1 given Ft = yn,t. The

GA involves the information In,t through the current and lagged cross-sectional averages yn,t and

yn,t−1. The other lagged values yn,t−j for j ≥ 2 are irrelevant at order o(1/n).

Let us now identify the risk and filtering GA components. We have:

a(y, 0; ft) = P (Ft+1 < y|Ft = ft) = Φ

(y − μ − ρ(ft − μ)

η

).

We deduce:

g∞(y; ft) =∂a(y, 0; ft)

∂y=

1

ηϕ

[y − μ − ρ(ft − μ)

η

],

and:∂a(y, 0; ft)

∂ft

= −ρ

ηϕ

[y − μ − ρ(ft − μ)

η

],

∂2a(y, 0; ft)

∂f 2t

=ρ2

η2

[y − μ − ρ(ft − μ)

η

]ϕ

(y − μ − ρ(ft − μ)

η

).

Moreover, the statistics involved in the approximate filtering distribution of Ft given In,t (see

Proposition 2) are μn,t = −σ2

η2[(yn,t − μ) − ρ(yn,t−1 − μ)] , Jn,t = 1/σ2 and Kn,t = 0. From

Proposition 2 and equation (5.12), we get:

GArisk(α) =σ2

2ηΦ−1(α),

GAfilt,t(α) =σ2ρ2

2ηΦ−1(α) − ρσ2

η2[(yn,t − μ) − ρ(yn,t−1 − μ)] .

The GA for risk is the same as in the static model for ρ = 0 (see Example 4.1), since in this

Gaussian framework the current factor ft impacts the conditional distribution of m(Ft+1) = Ft+1

given Ft = ft through the mean only, and σ2(Ft+1) = σ2 is constant. The GA for filtering depends

on both the risk level α and the information through (yn,t −μ)−ρ(yn,t−1 −μ). By the latter effect,

GAfilt,t(α) can take any sign. Moreover, this term induces a stabilization effect on the dynamics

of the GA VaR compared to the CSA VaR. To see this, let us assume ρ > 0 and suppose there is

24

a large upward aggregate shock on the individual risks at date t, such that yn,t − μ is positive and

(much) larger than ρ(yn,t−1 − μ). The CSA VaR in (5.12) reacts linearly to the shock and features

a sharp increase. Since (yn,t − μ) − ρ(yn,t−1 − μ) > 0, the GA term for filtering is negative and

reduces the reaction of the VaR.

In Figure 3 we display the patterns of the true, CSA and GA VaR curves as a function of the

risk level for a specific choice of parameters.

[Insert Figure 3: The VaR as a function of the risk level in the linear RFM with AR(1) factor.]

The mean and the autoregressive coefficient of the factor are μ = 0 and ρ = 0.5, respectively.

The idiosyncratic and systematic variance parameters σ2 and η2 are selected in order to imply

an unconditional standard deviation of the individual risks√

η2/(1 − ρ2) + σ2 = 0.15, and an

unconditional correlation between individual risksη2/(1 − ρ2)

σ2 + η2/(1 − ρ2)= 0.10. The portfolio size

is n = 100. The available information In,t is such that yn,t−j = μ = 0 for all lags j ≥ 2, and

we consider four different cases concerning the current and the most recent lagged cross-sectional

averages, yn,t and yn,t−1, respectively. Let us first assume yn,t = yn,t−1 = 0 (upper-left Panel), that

is, both cross-sectional averages are equal to the unconditional mean. As expected, all VaR curves

are increasing w.r.t. the confidence level. The true VaR is about 0.10 at confidence level 99%. The

CSA VaR underestimates the true VaR (that is, underestimates the risk) by about 0.01 uniformly

in the risk level. The GA for risk corrects most of this bias and dominates the GA for filtering.

The situation is different when yn,t = −0.30 and yn,t−1 = 0 (upper-right Panel), that is, when

we have a downward aggregate shock in risk of two standard deviations at date t. The CSA VaR

underestimates the true VaR by about 0.02. The GA for risk corrects only a rather small part of this

bias, while including the GA for filtering allows for a quite accurate approximation. The GA for

filtering is about five times larger than the GA for risk. When yn,t = 0.30 and yn,t−1 = 0 (lower-left

Panel), there is a large upward aggregate shock in risk at date t, and the CSA VaR overestimates

the true VaR (that is, overestimates the risk). The GA correction for risk further increases the VaR

and the bias, while including the GA correction yields a good approximation of the true VaR. The

results are similar in the case yn,t = 0.30 and yn,t−1 = 0.30 (lower-right Panel), that is, in case

of a persistent downward aggregate shock in risk. Finally, by comparing the four panels in Figure

3, it is seen that the CSA risk measure is more sensitive to the current information than the true

25

VaR and the GA VaR. Moreover, the relative importance of the GA correction w.r.t. the CSA VaR

is more pronounced for small values of α, that is, for less extreme risks. To summarize, Figure

3 shows that the CSA VaR can either underestimate or overestimate the risk, the GA for filtering

can dominate the GA for risk, and the complete GA can yield a good approximation of the true

VaR even for portfolio sizes of some hundreds of contracts, at least in the specific linear RFM

considered in this illustration.

6 Stochastic Probability of Default and Expected Loss Given

Default

A careful analysis of default risk has to consider jointly the default indicator and the loss given

default (i.e. one minus the recovery rate). The joint dynamics of the associated dated probability

of default and expected loss given default have been studied in a limited number of papers. A

well-known stylized fact is the positive correlation between probability of default and loss given

default [see e.g. Altman, Brady, Resti, Sironi (2005)]. However, this correlation is a crude sum-

mary statistic of the link between the two variables. This link is better understood by introduc-

ing time-varying determinants. Observable determinants considered in the literature include the

business cycle, the GDP growth rate [see Bruche, Gonzalez-Agrado (2010)], but also the rate of

unemployment [Grunert, Weber (2009)]. In fact there exist arguments for a negative link in some

circumstances. For instance, the bank has the possibility to declare the default of a borrower when

such a default is expected, even if the interest on the debt continues to be regularly paid by the

borrower. A too prudent bank can declare defaulted a borrower able to pay the remaining balance,

and then create artificially a kind of prepayment. In such a case the probability of default increases

and the loss given default decreases, which implies a negative link between the two risk variables.

To capture such complicated effects and their dynamics in the required capital, it is necessary

to consider a model with at least two factors. As in the previous sections, these two factors are

assumed unobservable, since the uncertainty in their future evolution has to be taken into account

in the reserve amount.

26

6.1 Two-factor dynamic model

Let us consider a portfolio invested in zero-coupon corporate bonds with a same time-to-maturity

and identical exposure at default. The loss on the zero-coupon corporate bond maturing at t + 1 is:

yi,t+1 = LGDi,t+1Zi,t+1,

where Zi,t+1 is the default indicator and LGDi,t+1 is the loss given default. Conditional on the

path of the bivariate factor Ft = (F1,t, F2,t)′, the default indicator Zi,t+1 and the loss given default

LGDi,t+1 are independent, such that Zi,t+1 ∼ B(1, F1,t+1) and LGDi,t+1 admits a beta distribution

Beta(at+1, bt+1) with conditional mean and volatility given by:

E [LGDi,t+1|Ft+1] = F2,t+1, V [LGDi,t+1|Ft+1] = γF2,t+1(1 − F2,t+1),

where the concentration parameter γ ∈ (0, 1) is constant. The parameters of the beta conditional

distribution of LGDi,t+1 are at+1 = (1/γ − 1) F2,t+1 and bt+1 = (1/γ − 1) (1 − F2,t+1). The

concentration parameter γ measures the variability of the conditional distribution of LGDi,t+1

given Ft+1 taking into account that the variance of a random variable on [0, 1] with mean μ, say,

is upper bounded by μ (1 − μ). 10 When the conditional concentration parameter γ approaches 0,

the beta distribution degenerates to a point mass; when the conditional concentration parameter γ

approaches 1 the beta distribution converges to a Bernoulli distribution. The dynamic factors F1,t

and F2,t correspond to the conditional Probability of Default and the conditional Expected Loss

Given Default, respectively 11. The effect of factor F2 on the beta distribution of expected loss

given default is illustrated in Figure 4.

[Insert Figure 4: Conditional distribution of LGDi,t given Ft.]

The factor impacts both the location and shape of the distribution.

Both stochastic factors F1,t and F2,t admit values in the interval (0, 1). We assume that the

transformed factors F ∗t = (F ∗

1,t, F∗2,t)

′ defined by F ∗l,t = log[Fl,t/(1 − Fl,t)], for l = 1, 2 (logistic

10This shows that the mean and the variance cannot be fixed independently for the distribution of a random variable

on [0, 1].11In the standard credit risk models, the LGD is often assumed constant. In such a case the LGD coincides with

both its conditional and unconditional expectations. In our framework the LGD is stochastic as well as its conditional

expectation.

27

transformation), follow a bivariate Gaussian VAR(1) process:

F ∗t = c + ΦF ∗

t−1 + εt,

with εt ∼ IIN(0, Ω) and Ω =

⎛⎝ σ2

1 ρσ1σ2

ρσ1σ2 σ22

⎞⎠. The parameters of the factor dynamics are

given in Table 1.

Table 1: Parameters of the factor dynamics

c1 c2 Φ11 Φ12 Φ21 Φ22 σ1 σ2 ρ γ

S1 −1.517 −0.190 0.5 0 0 0.5 0.386 0.655 0.5 0.10

S2 −1.517 −0.032 0.5 0 0 0.5 0.386 0.661 −0.5 0.10

We consider two parameter sets S1 and S2, that correspond to different values of the correlation

ρ between shocks in the two transformed factors, namely 0.5 and −0.5, respectively. Thus, we

cover the cases of positive (resp. negative) dependence between default and loss given default

factors. For both parameter sets, the matrix Φ of the autoregressive coefficients of the transformed

factors is such that the individual series feature a first-order autocorrelation coefficient equal to

Φ11 = Φ22 = 0.5, while the cross effects from the lagged values are Φ12 = Φ21 = 0. Moreover,

parameters c1 and σ1 are such that the unconditional probability of default PD = E[Zi,t] = E[F1,t]

and default correlation:

ρD = corr(Zi,t, Zj,t) =V [F1,t]

E[F1,t](1 − E[F1,t]), i �= j,

are equal to PD = 0.05 and ρD = 0.01, respectively. The PD value corresponds to a rating B [see

e.g. Gourieroux, Jasiak (2010)] and the ρD value is compatible with the Basle formula for asset

correlation and rating B. Both PD and ρD involve the marginal distribution of the default factor

F1,t only, and thus the values of parameters c1 and σ1 are the same across different choices of shock

correlation ρ. The concentration parameter in the conditional distribution of loss given default is

γ = 0.10. Finally, to fix the remaining two parameters c2 and σ2, we use that the unconditional

expected loss given default is (see Appendix 5):

ELGD = E[LGDi,t|Zi,t = 1] = E∗[F2,t],

28

and the unconditional variance of the loss given default is:

V LGD = V [LGDi,t|Zi,t = 1] = γELGD(1 − ELGD) + (1 − γ)V ∗[F2,t],

where E∗[·] and V ∗[·] denote expectation and variance w.r.t. the new probability measure defined

by E∗[W ] = E[WF1,t]/E[F1,t] = E[W |Zi,t = 1], for any random variable W . For both values of

shock correlation ρ, we set c2 and σ2 such that ELGD = 0.45 and V LGD = 0.05. Parameter c2

is negatively related to ρ. Indeed, the larger the correlation between default and loss given default

factors, the smaller the unconditional mean of the loss given default factor that guarantees the same

level of ELGD. Parameter σ2 is slightly decreasing w.r.t. shock correlation ρ.

6.2 CSA VaR and Granularity Adjustment

The CSA VaR and the GA are derived from the results in Section 5.2. Let us first consider the

cross-sectional factor approximations. It is proved in Appendix 5 that:

f1,n,t = Nt/n, (6.1)

where Nt =n∑

i=1

1lyi,t>0 is the number of defaults at date t, and:

f2,n,t = arg maxf2,t

⎧⎨⎩f2,t

(1 − γ

γ

) ∑i:yi,t>0

log

(yi,t

1 − yi,t

)

−Nt log Γ

[(1 − γ

γ

)f2,t

]− Nt log Γ

[(1 − γ

γ

)(1 − f2,t)

]}, (6.2)

where the sum is over the companies that default at date t, and Γ(.) denotes the Gamma function.

Thus, the approximation f1,n,t of the conditional PD is the cross-sectional default frequency at

date t, while the approximation f2,n,t of the conditional ELGD is obtained by maximizing the

cross-sectional likelihood associated with the conditional beta distribution of the LGD at date t.

Proposition 2 on the approximate filtering distribution can be easily extended to multiple factor.

Since the cross-sectional log-likelihood can be written as the sum of a component involving f1,t

only and a component involving f2,t only, the approximate filtering distribution is such that F1,t

and F2,t are independent conditional on information In,t at order 1/n, with Gaussian distributions

29

N

(fl,n,t +

1

nμl,n,t,

1

nJ−1

l,n,t

), for l = 1, 2, where:

μ1,n,t = −e′1Ω−1(f ∗

n,t − c − Φf ∗n,t−1),

(6.3)

μ2,n,t = − J−12,n,t

f2,n,t(1 − f2,n,t)

[e′2Ω

−1(f ∗n,t − c − Φf ∗

n,t−1) + 1 − 2f2,n,t

]+

1

2J−2

2,n,tK2,n,t,

with f ∗n,t =

(log[f1,n,t/(1 − f1,n,t)], log[f2,n,t/(1 − f2,n,t)]

)′and vectors e1 = (1, 0)′, e2 = (0, 1)′,

and:

J1,n,t =1

f1,n,t(1 − f1,n,t),

(6.4)

J2,n,t = f1,n,t

(1 − γ

γ

)2{Ψ′[(

1 − γ

γ

)f2,n,t

]+ Ψ′

[(1 − γ

γ

)(1 − f2,n,t)

]},

with Ψ(s) =d log Γ(s)

dsand:

K2,n,t = −f1,n,t

(1 − γ

γ

)3{Ψ′′[(

1 − γ

γ

)f2,n,t

]− Ψ′′

[(1 − γ

γ

)(1 − f2,n,t)

]}. (6.5)

Let us now derive the CSA VaR and the GA. From the results in Section 5.2 iv), we get the

next Proposition.

Proposition 5: In the model with stochastic conditional PD and ELGD:

i) The CSA VaR at risk level α is the solution of the equation:

a(V aR∞(α; fn,t), 0; fn,t

)= α,

where:

a(w, 0; ft) = Φ

(log[w/(1 − w)] − c1,t

σ1

)

+

∫ 1

w

Φ

⎡⎢⎣ log[w/(y − w)] − c2,t − ρσ2

σ1

(log[y/(1 − y)] − c1,t)

σ2

√1 − ρ2

⎤⎥⎦

· 1

σ1

ϕ

(log[y/(1 − y)] − c1,t

σ1

)1

y(1 − y)dy.

and cl,t = cl + Φl,1 log[f1,t/(1 − f1,t)] + Φl,2 log[f2,t/(1 − f2,t)], for l = 1, 2.

30

ii) The GA at risk level α is GAn,t(α) = GArisk,t(α) + GAfilt,t(α), where GArisk,t(α) is

computed from Proposition 3 with g∞(w; ft) = b(w, 0; ft) and:

E[σ2(Ft+1)|m(Ft+1) = w,Ft = ft] = w(γ − w) + (1 − γ)wb(w, 1; ft)

b(w, 0; ft),

where:

b(w, k; ft) =

∫ 1

w

yk

σ1σ2

ϕ

(log[w/(y − w)] − c1,t

σ1

,log[y/(1 − y)] − c2,t

σ2

; ρ

)1

(1 − y)w(y − w)dy,

and ϕ(., .; ρ) denotes the pdf of the standard bivariate Gaussian distribution with correlation ρ;

the component GAfilt,t(α) is given by:

GAfilt,t(α) = − 1

g∞[V aR∞(α; fn,t); fn,t]

2∑l=1

{∂a[V aR∞(α, fnt), 0; fl,nt]

∂fl,t

μl,nt

+1

2J−1

l,n,t

∂2a[V aR∞(α; fnt), 0; fl,nt]

∂f 2l,t

},

where μl,n,t and Jl,n,t are given in (6.3) and (6.4).

Proof: See Appendix 5.

The CSA and GA VaR in Proposition 5 are given in closed form, up to a few one-dimensional

integrals. We provide the CSA VaR, GA VaR and its risk and filtering components in Figures 5

and 6, for portfolio size n = 500 and risk level α = 99.5%.

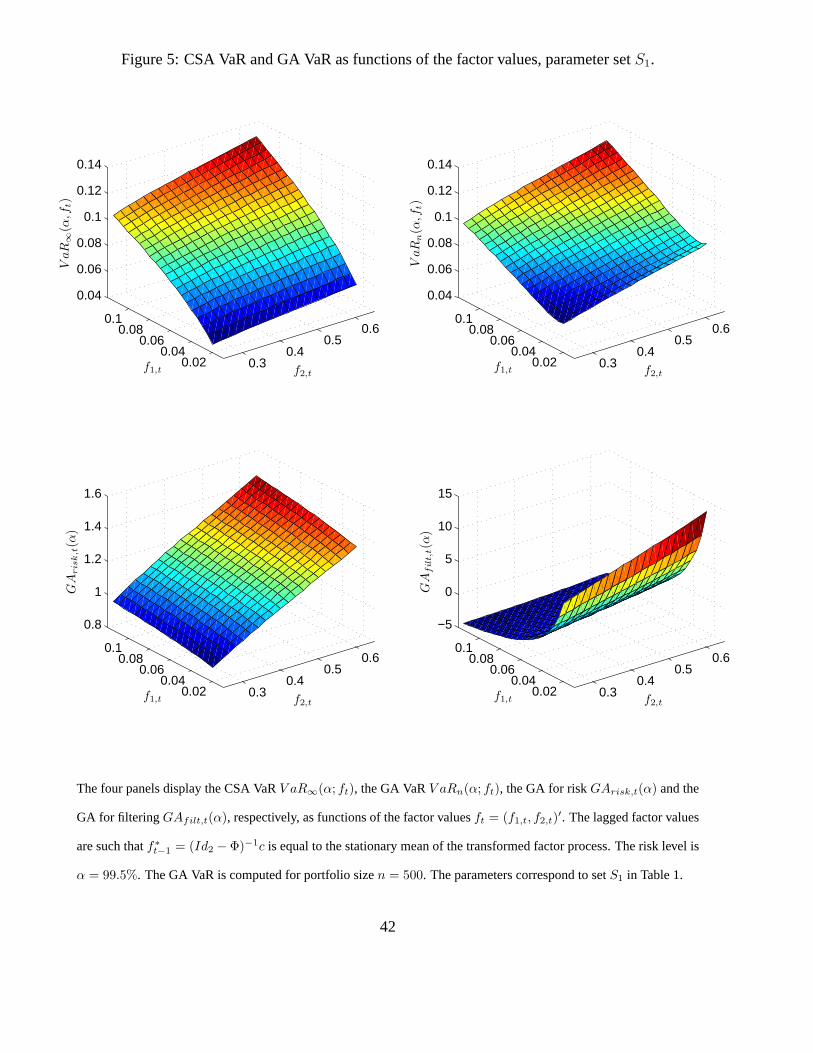

[Insert Figure 5: CSA VaR and GA VaR as functions of the factor values, parameter set S1.]

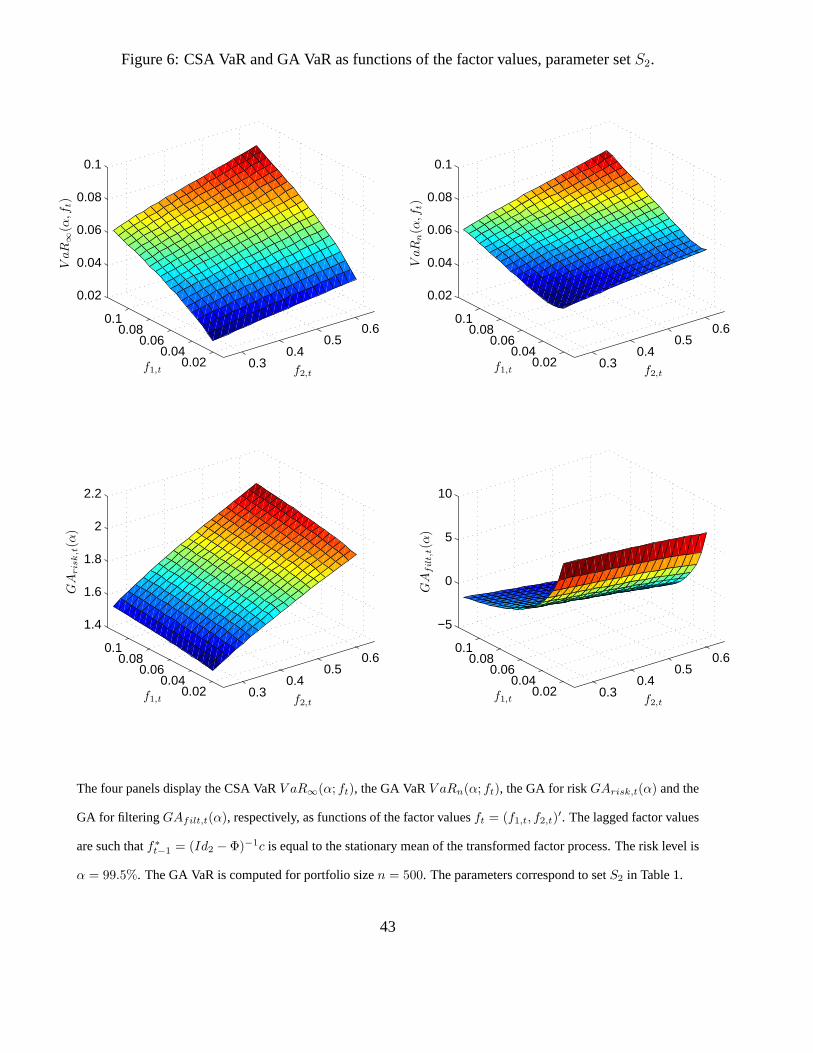

[Insert Figure 6: CSA VaR and GA VaR as functions of the factor values, parameter set S2.]

As expected, the required capital, measured by either CSA VaR, or GA VaR, is increasing with

respect to both factors F1 and F2, with larger sensitivity to factor F1. The risk GA component

(before adjusting for the portfolio size) is always positive, more sensitive to factor F2 and its range

is much smaller than the range of the filtering GA component. The filtering component can take

both positive and negative values and depends nonlinearly on factor F1 in a decreasing way. This

is a consequence of the properties of the ML estimator for the parameter of a Bernoulli distribution

with parameter F1. Indeed, it is known that the estimator is very accurate when F1 is close to 0 (or

31

1). By comparing Figures 5 and 6, we observe immediately that the CSA VaR and the GA VaR

are smaller when the two risks are negatively correlated. We can observe a change in the sign of

dependence of the filtering component with respect to the second factor.

Let us now consider the dynamics of the risk factors and risk measures.

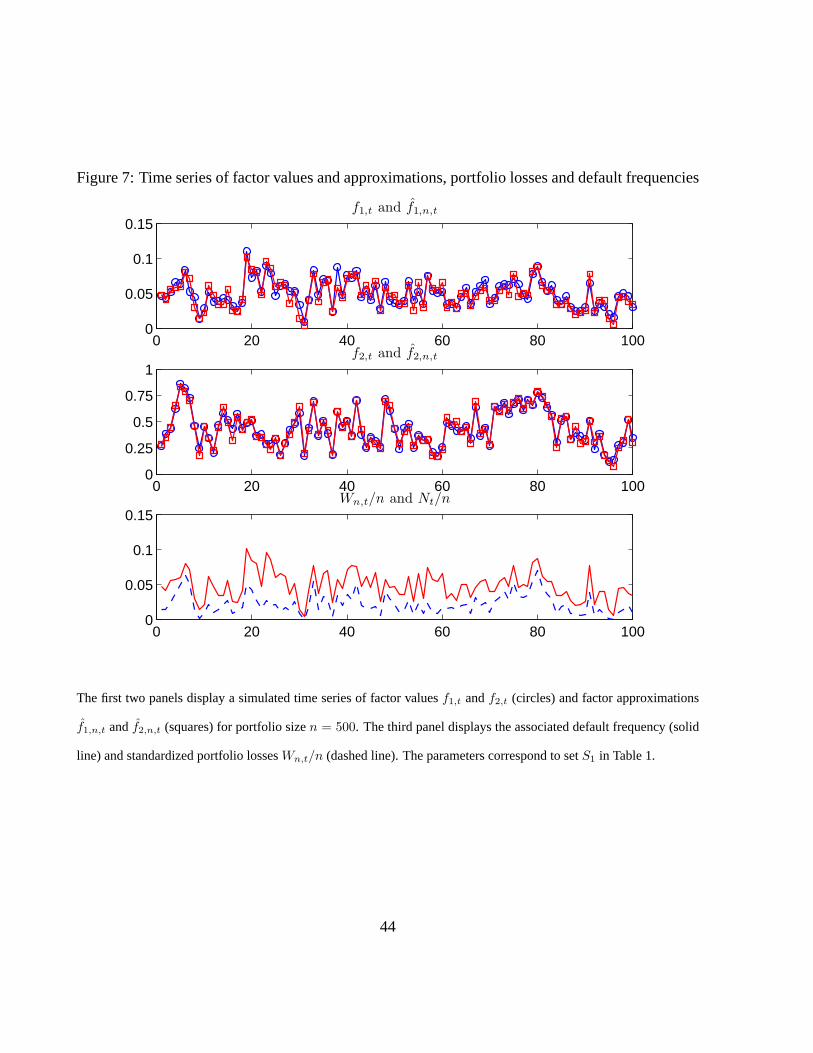

[Insert Figure 7: Time series of factor values and approximations, portfolio losses and default

frequencies.]

[Insert Figure 8: Time series of CSA VaR, GA VaR, GA risk and filtering components.]

The two first panels in Figure 7 provide the factors and their cross-sectional approximations cor-

responding to a simulated path of factors and individual risks, with parameter set S1 and portfolio

size n = 500. The cross-sectional approximations are accurate for both factors, and especially so

for the second factor which is driving the quantitative risk. The third panel provides the series of

percentage portfolio losses and default frequencies. The default frequency is a percentage portfolio

loss with zero recovery rate, which explains why this series is systematically larger. The default

frequency is driven by factor F1 only, and the non parallel evolution of the two series is due to

factor F2, including its dependence with F1. The upper panel of Figure 8 provides the time se-

ries of CSA VaR and GA VaR. The granularity adjustment is in general positive and rather small,

except at dates at which the CSA VaR is low. At these dates the adjustment is mainly due to its

filtering component, as can be deduced from the lower panel of Figure 8. The risk component is

almost constant over time, and (much) smaller in absolute value than the filtering component at

most dates.

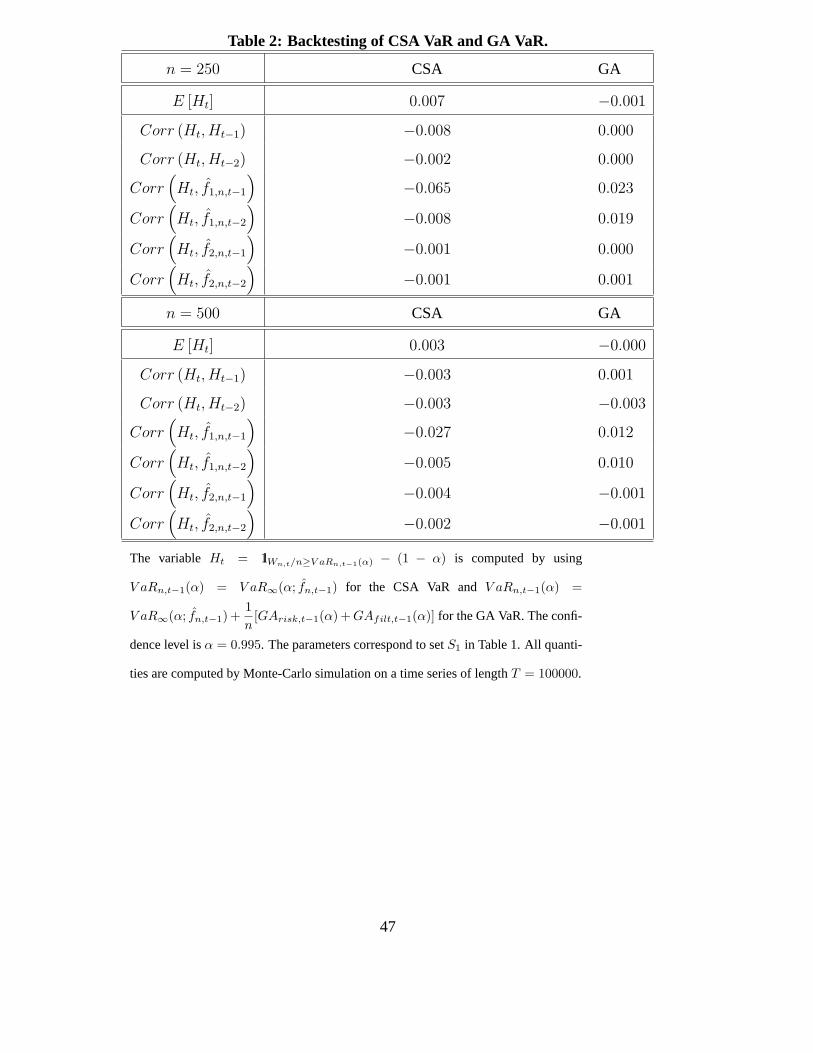

The capital adequacy is usually checked by performing some backtesting. It is known that the

true conditional VaR is such that:

E[Ht|In,t−1] = 0, (6.6)

where Ht = 1lWn,t/n≥V aRn,t−1(α) − (1 − α) [see equation (5.2)]. This is a conditional moment re-

striction, which can be used to construct a battery of specification tests [Giacomini, White (2006)].

More precisely, let us consider an instrument Xt−1, that is a function of information In,t−1, and

deduce from (6.6) the unconditional moment restriction E[HtXt−1] = 0. When Xt−1 = 1, we get

the simple condition E[Ht] = 0, which is the basis for the standard backtesting procedure relying

32

on the number of violations and suggested by the regulator. More secure backtesting is obtained

by considering different instruments. We rewrite the moment condition E[HtXt−1] = 0 in terms

of correlation as corr(Ht, Xt−1) = 0, and provide in Table 2 the true values of the backtesting

moments and correlations for the portfolio sizes n = 250 and n = 500, and the CSA VaR and GA

VaR.

[Insert Table 2: Backtesting of CSA VaR and GA VaR.]

Let us for instance consider the second row of the upper panel (resp. the second row of the lower

panel). With the CSA VaR suggested in the standard regulation the probability of violation is 1.2%

for n = 250 (resp. 0.8% for n = 500) instead of 0.5%. When the granularity adjustment is applied

this probability becomes 0.4% (resp. 0.5%). This shows clearly that the reserve computed with the

CSA approximation is too low on average. The better accuracy of the GA VaR is confirmed when

we consider other instruments such as the lagged factor approximations, or lagged values of H .

We observe that the associated correlations are typically closer to 0 after granularity adjustment.

Finally, it is interesting to discuss the possible effect of the number of factors.

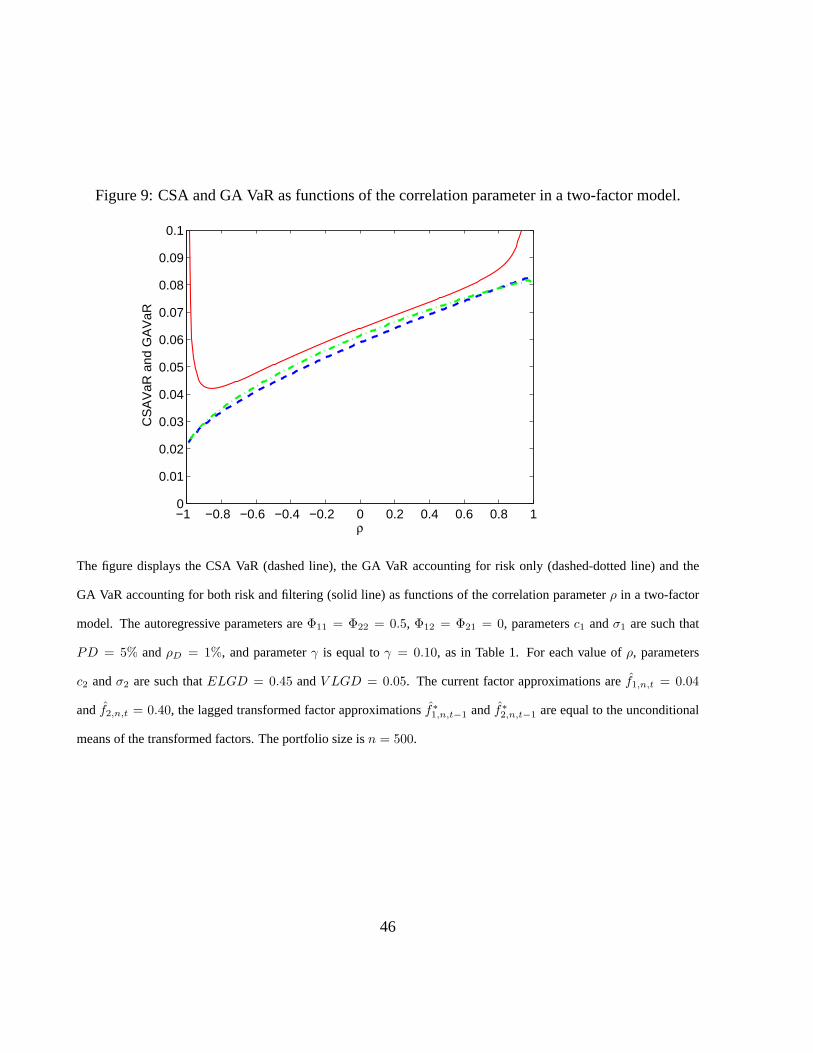

[Insert Figure 9: CSA VaR and GA VaR as functions of the correlation parameter in a two-

factor model.]

In Figure 9 we plot the CSA VaR, the GA VaR accounting for risk only, and the GA VaR with full

correction as functions of the correlation parameter ρ, for ρ ∈ (−1, 1) and portfolio size n = 500.

The limiting values ρ = ±1 correspond to a one-factor model, with the single factor impacting both

the probability of default and the loss given default. We observe that the granularity adjustment

for risk is rather small, and close to zero when the correlation parameter is close to the limiting

values. At the contrary, the adjustment for filtering becomes larger when the absolute value of

the correlation parameter increases. As a result, the total GA is almost independent of ρ when

ρ ∈ (−0.6, 0.6), but the relative contributions of the risk and filtering components varies with ρ.

The total GA explodes when ρ approaches the limiting values ±1. This singularity reflects the

discountinuity in the number of factors.

33

7 Concluding Remarks

For large homogenous portfolios and a variety of both single-factor and multi-factor dynamic risk

models, closed form expressions of the VaR and other distortion risk measures can be derived

at order 1/n. Two granularity adjustments are required. The first GA concerns the conditional

VaR with current factor value assumed to be observed. The second GA takes into account the

unobservability of the current factor value and is specific to dynamic factor models. This explains

why this GA has not been taken into account in the earlier literature which focuses on static models.

These GA assume given the function linking the individual risks to factors and idiosyncratic

risks, and also the distributions of both the factor and idiosyncratic risks. In practice the link

function and the distribution depend on unknown parameters, which have to be estimated. This

creates an additional error on the VaR, which has been considered neither here, nor in the previous

literature. This estimation error can be larger than the GA derived in this paper. However, such

a separate analysis is compatible with the Basel 2 methodology. Indeed, the GA in this paper are

useful to compute the reserves for Credit Risk, whereas the adjustment for estimation concerns

the reserves for Estimation Risk.

The granularity adjustment principle appeared in Pillar 1 of the New Basel Capital Accord in

2001 [BCBS (2001)], concerning the minimum capital requirement. It has been suppressed from

Pillar 1 in the most recent version of the Accord in 2003 [BCBS (2003)], and assigned to Pillar 2

on internal risk models. The recent financial crisis has shown that systematic risks, which include

in particular systemic risks 12, have to be distinguished from unsystematic risk, and in the new

organization these two risks will be supervised by different regulators. This shows the importance

of taking into account this distinction in computing the reserves, that is, also at Pillar 1 level. For

instance, one may fix different risk levels α1 and α2 in the CSA and GA VaR components, and

smooth differently these components over the cycle in the definition of the required capital. The

recent literature on granularity shows that the technology is now in place and can be implemented

not only for static linear factor models, but also for nonlinear dynamic factor models.

12A systemic risk is a systematic risk which can seriously damage the Financial System.

34

References

[1] Altman, E., Brady, B., Resti, A., and A., Sironi (2005): “The Link Between Default and Re-

covery Rate: Theory, Empirical Evidence and Implications”, Journal of Business, 78, 2203-

2227.

[2] Bahadur, R. (1966): ”A Note on Quantiles in Large Samples”, Annals of Mathematical Statis-

tics, 37, 577-580.

[3] Basel Committee on Banking Supervision (2001): ”The New Basel Capital Accord”, Con-

sultative Document of the Bank for International Settlements, April 2001, Part 2: Pillar 1,

Section “Calculation of IRB Granularity Adjustment to Capital”.

[4] Basel Committee on Banking Supervision (2003): ”The New Basel Capital Accord”, Consul-

tative Document of the Bank for International Settlements, April 2003, Part 3: The Second

Pillar.

[5] Black, F. (1976): “Studies of Stock Price Volatility Changes”, Proceedings of the 1976 Meet-

ing of the American Statistical Association, Business and Economics Statistics Section, 177-

181.

[6] Bruche, M., and C., Gonzalez-Aguado (2010): “Recovery Rates, Default Probabilities, and

the Credit Cycle”, Journal of Banking and Finance, 34, 754-764.

[7] Buhlmann, H. (1967): ”Experience Rating and Credibility”, ASTIN Bulletin, 4, 199-207.

[8] Buhlmann, H., and L., Straub (1970): ”Credibility for Loss Ratios”, ARCH, 1972-2.

[9] Chamberlain, G., and M., Rothschild (1983): ”Arbitrage, Factor Structure and Mean-

Variance Analysis in Large Markets”, Econometrica, 51, 1281-1304.

[10] Credit Suisse Financial Products (1997): ”CreditRisk+: A Credit Risk Management Frame-

work“, Credit Suisse Financial Products, London.

[11] de Finetti, B. (1931): ”Funzione Caratteristica di un Fenomeno Aleatorio”, Atti della R.

Accademia dei Lincei, 6, Memorie. Classe di Scienze Fisiche, Matematiche e Naturali, 4,

251-299.

35

[12] Ebert, S., and E., Lutkebohmert (2009): ”Treatment of Double Default Effects Within the

Granularity Adjustment for Basel II“, University of Bonn, Working Paper.

[13] Emmer, S., and D., Tasche (2005): ”Calculating Credit Risk Capital Charges with the One-

Factor Model“, Journal of Risk, 7, 85-103.

[14] Gagliardini, P., and C., Gourieroux (2010a): ”Approximate Derivative Pricing in Large

Classes of Homogeneous Assets with Systematic Risk“, forthcoming in Journal of Finan-

cial Econometrics.

[15] Gagliardini, P., and C., Gourieroux (2010b): ”Granularity Theory”, CREST, DP.

[16] Giacomini, R., and H., White (2006): “Tests of Conditional Predictive Ability”, Economet-

rica, 74, 1545-1578.

[17] Glasserman, P., and J., Li (2005): “Importance Sampling for Portfolio Credit Risk”, Manage-

ment Science, 51, 1643-1656.

[18] Gordy, M. (2003): ”A Risk-Factor Model Foundation for Rating-Based Bank Capital Rules”,

Journal of Financial Intermediation, 12, 199-232.

[19] Gordy, M. (2004): ”Granularity Adjustment in Portfolio Credit Risk Measurement”, in Risk

Measures for the 21.st Century, ed. G. Szego, Wiley, 109-121.

[20] Gordy, M., and E., Lutkebohmert (2007): ”Granularity Adjustment for Basel II”, Deutsche

Bank, DP.

[21] Gordy, M., and J., Marrone (2010): ”Granularity Adjustment for Mark-to-Market Credit Risk

Models“, Federal Reserve Board, DP.

[22] Gourieroux, C., and J., Jasiak (2010): ”Granularity Adjustment for Default Risk Factor

Model with Cohort“, DP York University.

[23] Gourieroux, C., Laurent, J.P., and O., Scaillet (2000): ”Sensitivity Analysis of Value-at-

Risk”, Journal of Empirical Finance, 7, 225-245.

36

[24] Gourieroux, C., and A., Monfort (2009): ”Granularity in a Qualitative Factor Model“, Journal

of Credit Risk, 5, 29-65.

[25] Grunert, J., and M., Weber (2009): ”Recovery Rates of Commercial Lending: Empirical

Evidence for German Companies“, Journal of Banking and Finance, 33, 505-513.

[26] Hewitt, E, and L., Savage (1955): ”Symmetric Measures on Cartesian Products”, Transaction

of the American Mathematical Society, 80, 470-501.

[27] Martin, R., and T., Wilde (2002): ”Unsystematic Credit Risk”, Risk, 15, 123-128.

[28] McNeil, A., Frey, R., and P., Embrechts (2005): Quantitative Risk Management. Concepts,

Techniques, Tools, Princeton Series in Finance, Princeton University Press.

[29] Merton, R. (1974): ”On the Pricing of Corporate Debt: The Risk Structure of Interest Rates”,

Journal of Finance, 29, 449-470.

[30] Rau-Bredow, H. (2005): ”Granularity Adjustment in a General Factor Model“, University of

Wuerzburg, DP.

[31] Ross, S. (1976): ”The Arbitrage Theory of Capital Asset Pricing”, Journal of Economic

Theory, 13, 341-360.

[32] Tasche, D. (2000): ”Conditional Expectation as Quantile Derivative”, Bundesbank, DP.

[33] Vasicek, O. (1991): ”Limiting Loan Loss Probability Distribution”, KMV Corporation, DP.

[34] Vasicek, O. (2002): ”The Distribution of Loan Portfolio Value“, Risk, 15, 160-162.

[35] Wang, S. (2000): ”A Class of Distortion Operators for Pricing Financial and Insurance

Risks”, Journal of Risk and Insurance, 67, 15-36.

[36] Wilde, T. (2001): ”Probing Granularity”, Risk, 14, 103-106.

37

Figure 1: CSA CreditVaR and granularity adjustment as functions of the asset correlation in the

Merton-Vasicek model.

0 0.2 0.4 0.6 0.8 10

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

ρ

V aR∞(0.99)

0 0.2 0.4 0.6 0.8 10

0.005

0.01

0.015

0.02

0.025

0.03

ρ

1nGA(0.99)

PD=0.5%PD=1%PD=5%PD=20%

The panels display the CSA quantile V aR∞(α) (left) and the granularity adjustment per contract 1nGA(α) (right) as

functions of the asset correlation ρ. The confidence level is α = 0.99 and the portfolio size is n = 1000. In each

panel, the curves correspond to different values of the unconditional probability of default, that are PD = 0.5% (solid

line), PD = 1% (dashed dotted line), PD = 5% (dotted line), and PD = 20% (dashed line).

38

Figure 2: CSA CreditVaR and granularity adjustment as a function of the unconditional probability

of default in the Merton-Vasicek model.

0 0.2 0.4 0.6 0.8 10

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

PD

V aR∞(0.99)

0 0.2 0.4 0.6 0.8 1

0

2

4

6

8

10

12

14

16

18

20x 10

−3

PD

1nGA(0.99)

ρ=0.05ρ=0.12ρ=0.24ρ=0.50

The panels display the CSA quantile V aR∞(α) (left) and the granularity adjustment per contract 1nGA(α) (right) as

functions of the unconditional probability of default PD. The confidence level is α = 0.99 and the portfolio size is

n = 1000. In each panel, the curves correspond to different values of the asset correlation, that are ρ = 0.05 (solid

line), ρ = 0.12 (dashed dotted line), ρ = 0.24 (dotted line), and ρ = 0.50 (dashed line).

39

Figure 3: VaR as a function of the risk level in the linear RFM with AR(1) factor.

0.95 0.96 0.97 0.98 0.990.06

0.07

0.08

0.09

0.1

0.11

0.12

α

VaR

n,t(α

)

yn,t = 0, yn,t−1 = 0

0.95 0.96 0.97 0.98 0.99−0.1

−0.08

−0.06

−0.04

−0.02

0

α

VaR

n,t(α

)

yn,t = −0.30, yn,t−1 = 0

0.95 0.96 0.97 0.98 0.990.2

0.22

0.24

0.26

α

VaR

n,t(α

)

yn,t = 0.30, yn,t−1 = 0

0.95 0.96 0.97 0.98 0.990.2

0.22

0.24

0.26

α

VaR

n,t(α

)yn,t = 0.30, yn,t−1 = 0.30

In each Panel we display the true VaR (solid line), the CSA VaR (dashed line), the GA VaR accounting for risk only

(dashed-dotted line) and the GA VaR accounting for both risk and filtering (dotted line), as a function of the confidence

level α. The four Panels correspond to different available information In,t, that are yn,t = yn,t−1 = 0 in the upper

left Panel, yn,t = −0.30, yn,t−1 = 0 in the upper right Panel, yn,t = 0.30, yn,t−1 = 0 in the lower left Panel, and

yn,t = 0.30, yn,t−1 = 0.30 in the lower right Panel, respectively. The portfolio size is n = 100. The model parameters

are such that the unconditional standard deviation of the individual risks is 0.15, the unconditional correlation between

individual risks is 0.10, the factor mean is μ = 0, and the factor autoregressive coefficient is ρ = 0.5.

40