Gramm Financial Center Deferred Compensation in the New Millennium Gramm Financial Center http://gfc.pfyfn.com

Gramm Financial Center Deferred Compensation in the New Millennium Gramm Financial Center .

Jan 01, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Gramm Financial Center

Deferred Compensation in the

New Millennium

Gramm Financial Centerhttp://gfc.pfyfn.com

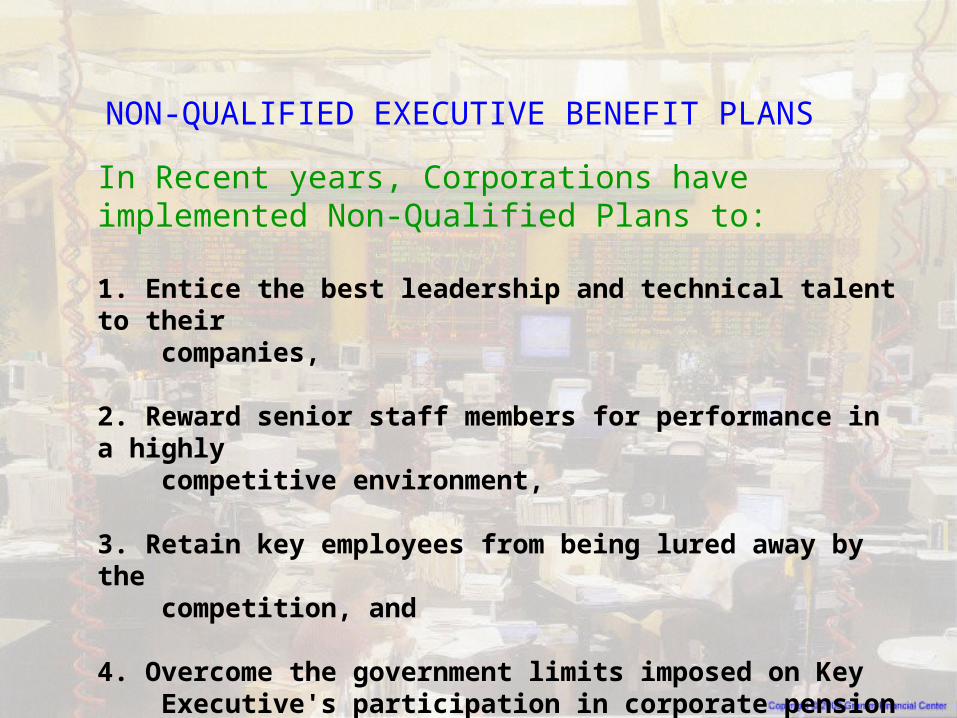

NON-QUALIFIED EXECUTIVE BENEFIT PLANS

In Recent years, Corporations have implemented Non-Qualified Plans to:

1. Entice the best leadership and technical talent to their companies,

2. Reward senior staff members for performance in a highly competitive environment,

3. Retain key employees from being lured away by the competition, and

4. Overcome the government limits imposed on Key Executive's participation in corporate pension and 410-(k) type plans.

The 3 CAN'TS:

•We can't allow you to defer the desired amount of pre-tax compensation (LEGISLATIVE LIMITS).

•We can't provide retirement income commensurate with your final salary (90-100% of final salary).

•We can't provide an adequate level of Survivorship Benefits to protect your family (ERISA requirements).

Companies have been forced to say to their executives...

SUPPLEMENTAL RETIREMENT INCOME

Issues

• Qualified Plan restrictions:• Must be employee to participate; director not eligible.• Limits on benefits and contributions.• $160,000 (as indexed for COLA) Compensation cap in determining qualified pension benefits• Changes in discrimination rules.

• Incentive compensation excluded from pension formulas• Lower income replacement ratios- reduced standard of living after retirement for key employees.• No linkage between benefit level and corporate performance measures.

Copyright © 2000 Gramm Financial Center

SUPPLEMENTAL SURVIVOR BENEFITS

Typical Group Term Issues

• Benefit often less than targeted because:• incentive compensation not used to determine benefit

• Few collect; most deaths occur after retirement when coverage is terminated or substantially reduced.• Poor cost/ benefit ratio:

• High cost to employer with low collection ratio by employees.• Not a retention tool for management• Excessive imputed income to employee

• Government restrictions and compliance requirements on eligibility and benefit amounts.

Copyright © 2000 Gramm Financial Center

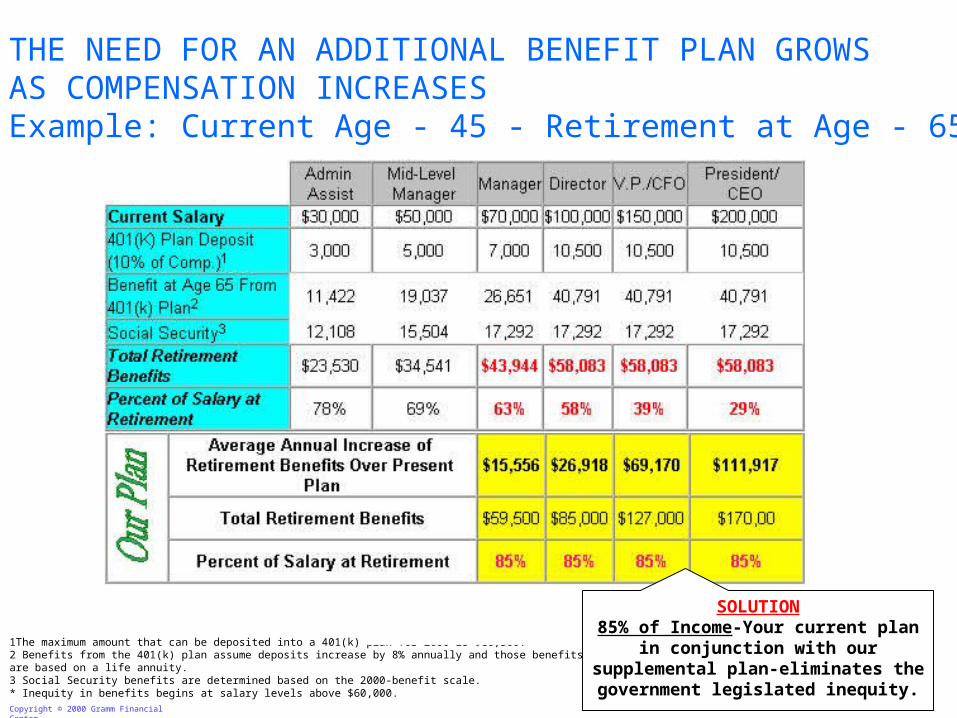

THE NEED FOR AN ADDITIONAL BENEFIT PLAN GROWSAS COMPENSATION INCREASESExample: Current Age - 45 - Retirement at Age - 65

PROBLEMEconomists say you need 75%-85% of income during your retirement.

1The maximum amount that can be deposited into a 401(k) plan for 2000 is $10,500.2 Benefits from the 401(k) plan assume deposits increase by 8% annually and those benefits are based on a life annuity.3 Social Security benefits are determined based on the 2000-benefit scale.* Inequity in benefits begins at salary levels above $60,000.

SOLUTION85% of Income-Your current plan

in conjunction with our supplemental plan-eliminates the government legislated inequity.

Copyright © 2000 Gramm Financial Center

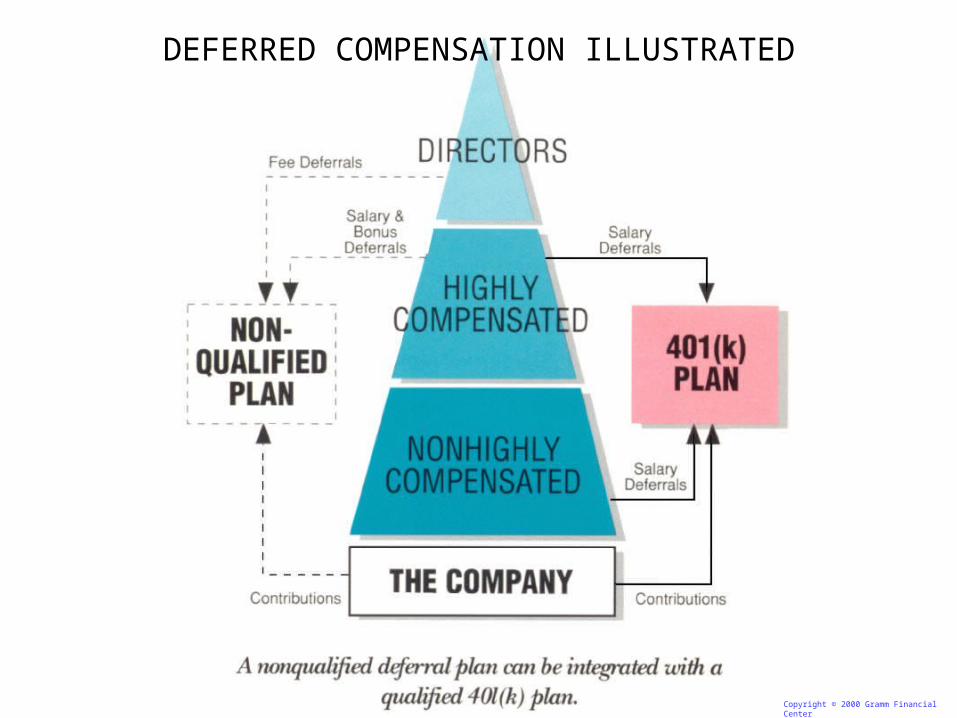

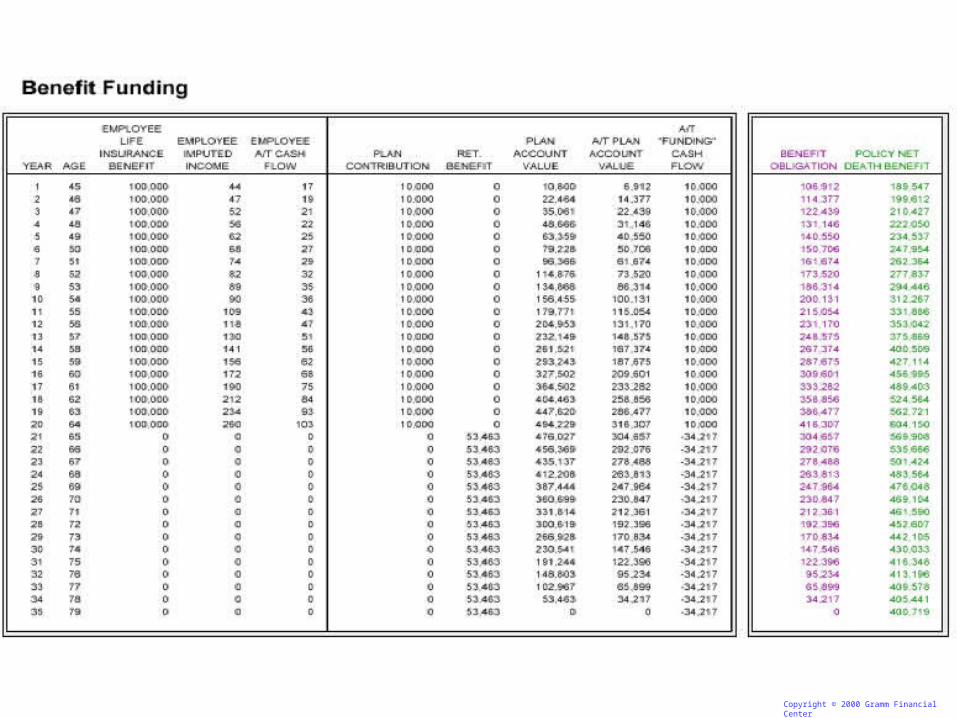

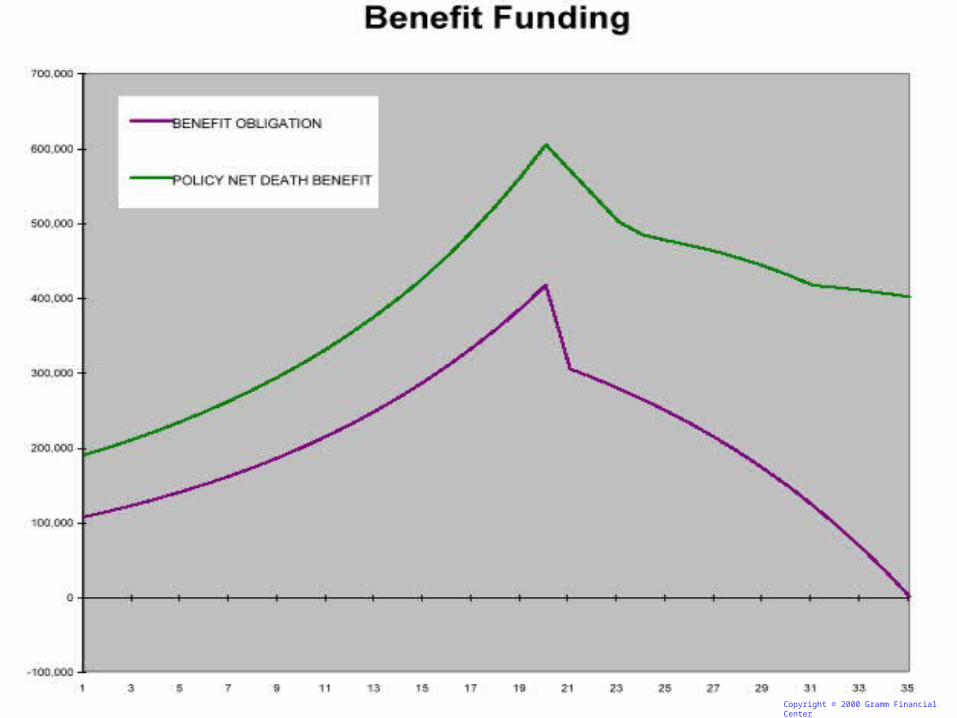

DEFERRED COMPENSATION ILLUSTRATED

Copyright © 2000 Gramm Financial Center

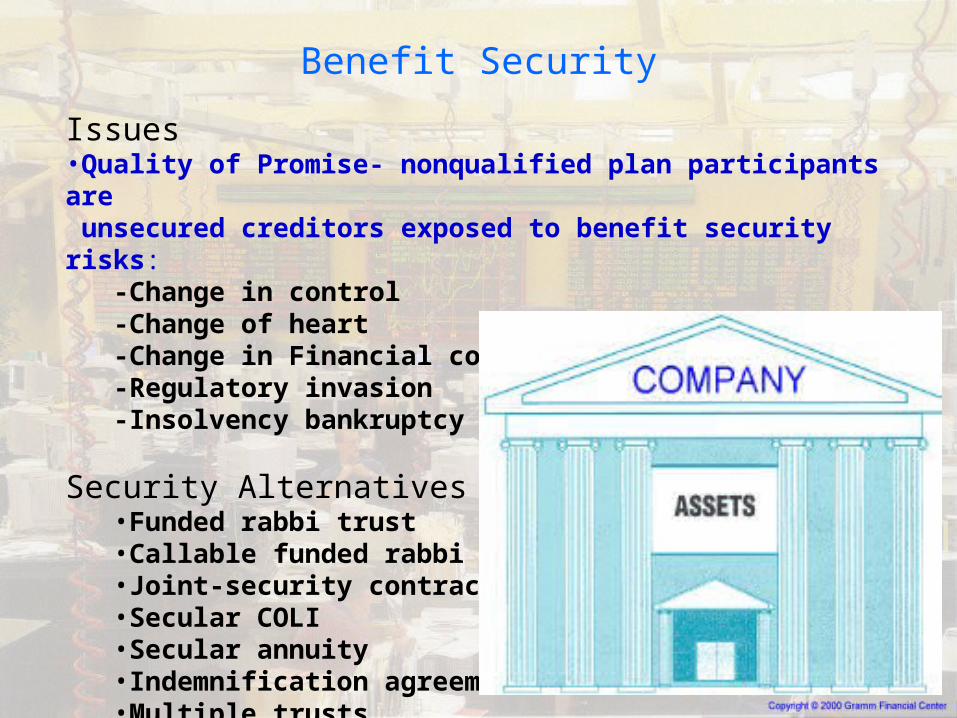

Issues•Quality of Promise- nonqualified plan participants are unsecured creditors exposed to benefit security risks:

-Change in control-Change of heart-Change in Financial condition-Regulatory invasion-Insolvency bankruptcy

Security Alternatives•Funded rabbi trust•Callable funded rabbi trust•Joint-security contract•Secular COLI•Secular annuity•Indemnification agreement•Multiple trusts

Benefit Security

Tax deferred compounding not only greatly increases the value of today's dollar, it also puts the executive back in control of his/her retirement planning. If a 45-year-old defers $1,000 today and begins receiving a benefit at age 65 over a 10-year period, the after-tax return greatly outpaces any outside investment made:

DEFERRAL PLAN VS OUTSIDE INVESTMENT

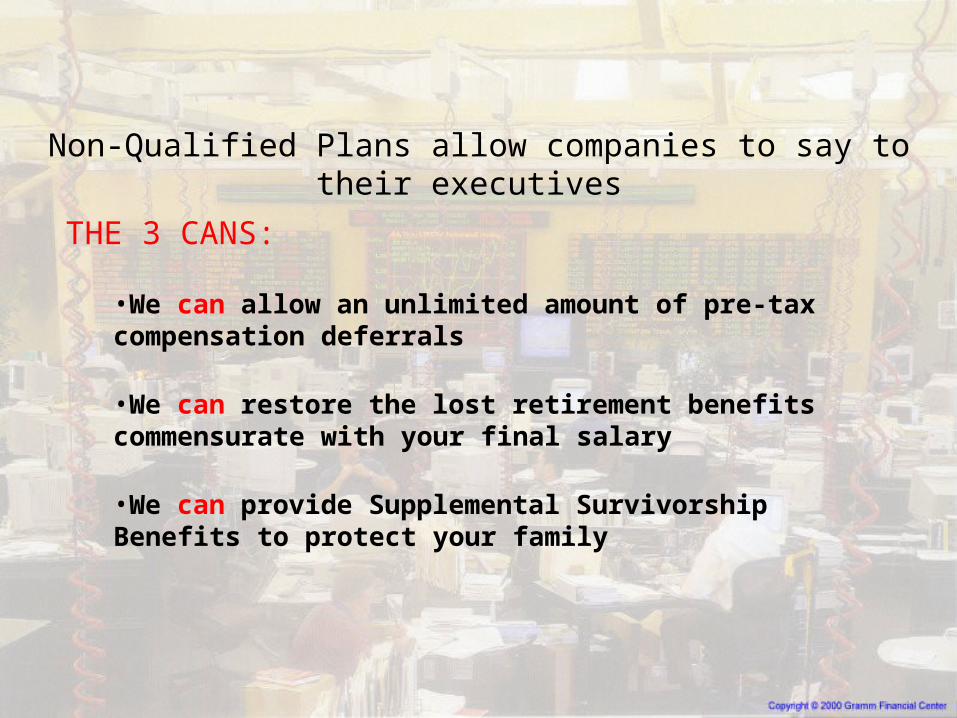

Non-Qualified Plans allow companies to say to their executives

THE 3 CANS:

•We can allow an unlimited amount of pre-tax compensation deferrals

•We can restore the lost retirement benefits commensurate with your final salary

•We can provide Supplemental Survivorship Benefits to protect your family

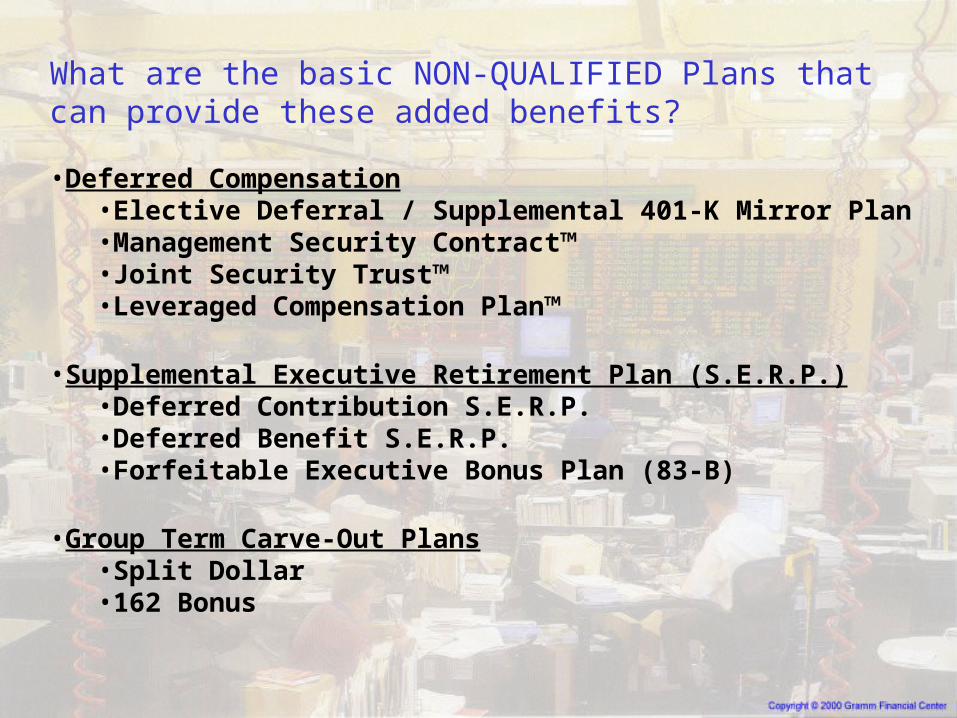

What are the basic NON-QUALIFIED Plans that can provide these added benefits?

•Deferred Compensation•Elective Deferral / Supplemental 401-K Mirror Plan•Management Security Contract™•Joint Security Trust™•Leveraged Compensation Plan™

•Supplemental Executive Retirement Plan (S.E.R.P.)•Deferred Contribution S.E.R.P.•Deferred Benefit S.E.R.P.•Forfeitable Executive Bonus Plan (83-B)

•Group Term Carve-Out Plans•Split Dollar•162 Bonus

Financial Modeling

Gramm Financial Centerhttp://gfc.pfyfn.com

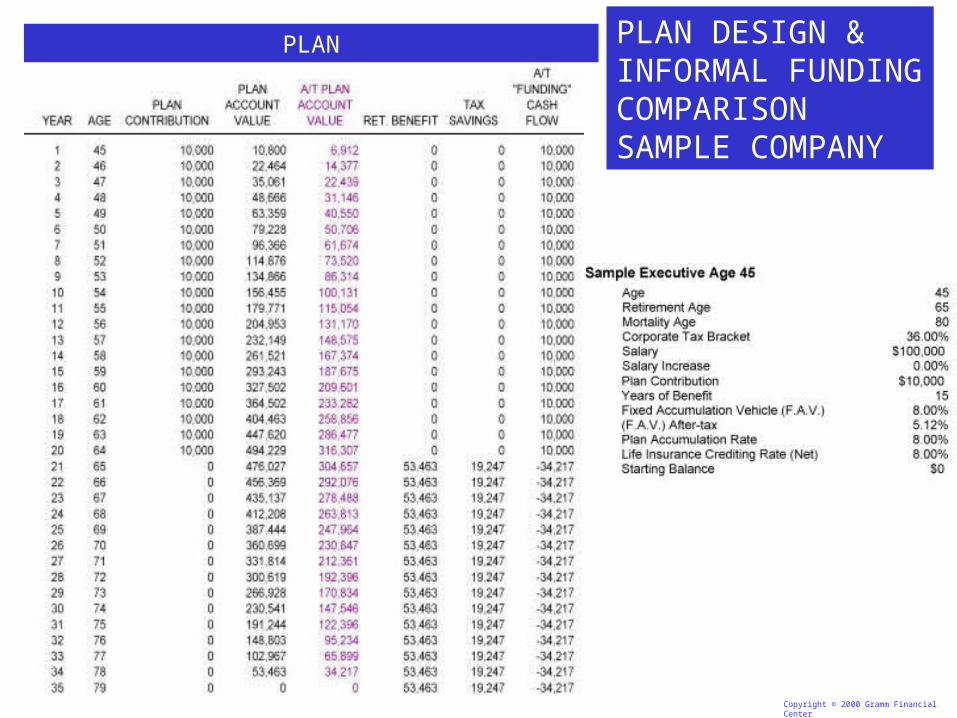

PLAN DESIGN & INFORMAL FUNDING COMPARISON SAMPLE COMPANY

PLAN

Copyright © 2000 Gramm Financial Center

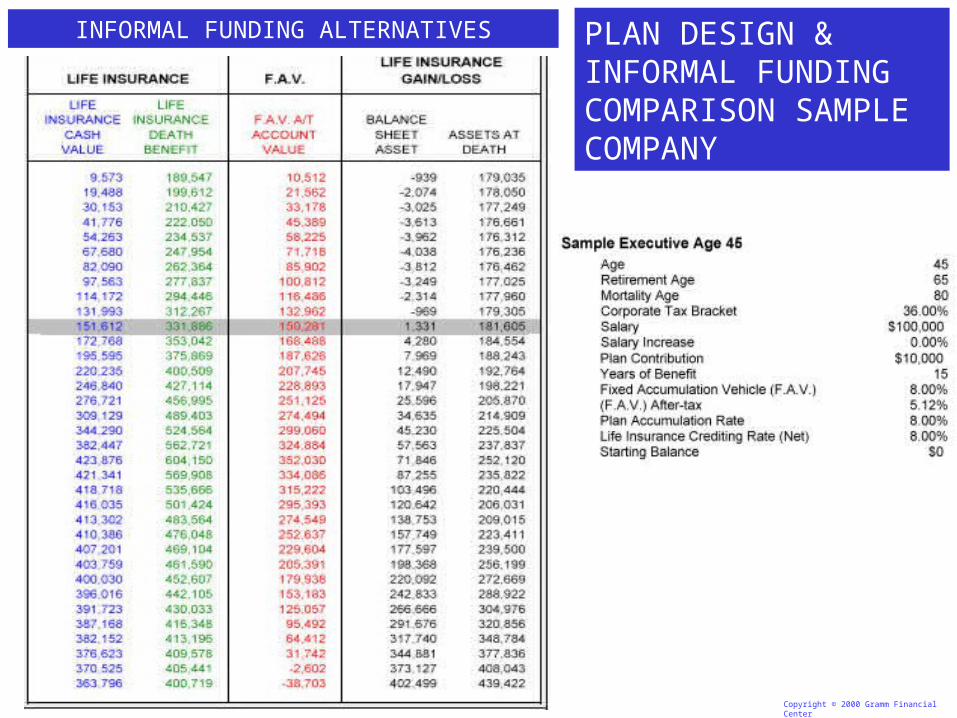

PLAN DESIGN & INFORMAL FUNDING COMPARISON SAMPLE COMPANY

INFORMAL FUNDING ALTERNATIVES

Copyright © 2000 Gramm Financial Center

Copyright © 2000 Gramm Financial Center

Copyright © 2000 Gramm Financial Center

Copyright © 2000 Gramm Financial Center

Related Documents