Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature Government Safety Net, Stock Market Participation and Asset Prices Danilo Lopomo Beteto November 18, 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Government Safety Net, Stock Market

Participation and Asset Prices

Danilo Lopomo Beteto

November 18, 2011

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Introduction

◮ Goal: study of the effects on prices of government intervention duringcrises

◮ Question: does government intervention sow the seeds of crises thatthe intention is to prevent in the first place?

◮ Motivation: financial crisis of 2007-2009

◮ Object of study: equilibrium prices resulting from the investmentdecision on assets characterized by different degrees of informationabout future returns

◮ Contribution: comparison of prices across different frameworks (withand without government intervention) for different classes of assets;example of a situation where a government safety net increases thelikelihood of crises

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Example: Mortgage-Backed Securities

Figure: Impact of government intervention and feedback.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Comparison of Equilibrium Prices

Figure: Effects from government intervention.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Model

◮ Economy with a government sector, populated by a continuum ofagents (investors), I = [0, 1], four dates, t = 0, 1, 2, 3;

◮ 1 consumption good (money) and 2 financial assets:

◮ Riskless asset in infinite supply, yielding interest rate normalizedto r = 0;

◮ Risky asset in supply of K units, with payoff (in money units)

given by a uniform random variable, θ ∼ U [0, 1];

◮ Agents are initially endowed with A units of money;

◮ Preferences: agents are risk-neutral and utility derives from the payoffof the investment strategy at the final date;

◮ Investment strategy: agents decide whether or not to pay p to buy asingle unit of the risky security, Xi = 1 or Xi = 0, with the remainingsbeing allocated to the riskless asset;

◮ Consumption occurs in the final period, at which point the risky assetis liquidated at the cost t.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Timeline of Events

Figure: Timeline of events.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Government Intervention

◮ For any agent i ∈ I, the payoff of the investment strategy is

Ri (Xi, θ, A, t) ≡ Xi (θ − t) + A − Xip = Xi (θ − p − t) + A;

◮ Social welfare is defined as the sum across investors of theirportfolios’s payoff,

S (θ, A, t) ≡

∫ 1

0

[Xi (θ − p − t) + A] di;

◮ Government intervention policy: there’s intervention if and only ifsocial welfare goes below a certain threshold C,

S (θ, A, t) < C.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Government Intervention

◮ Using the market clearing condition,∫ 1

0Xidi = K, the condition for

government intervention can be written as

S (θ, A, t) < C

⇔∫ 1

0[Xi (θ − p − t) + A] di < C

⇔ (θ − p − t)∫ 1

0Xidi + A

∫ 1

0di < C

⇔ (θ − p − t) K + A < C

⇔ θ < C−A

K+ p + t ≡ θ∗;

◮ In the event of government intervention, social welfare is restored toits minimum acceptable level, C, which implies the asset’s returnbeing as if θ = θ∗;

◮ Investors’s beliefs about government intervention are, therefore,translated as beliefs of θ being smaller than θ∗.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Informational Scenarios

◮ Imperfect information: investors receive a signal, ξi, uniformlydistributed around θ, ξ ∼ U [θ − τ, θ + τ ], with τ > 0. Conditional onξi, agents know that θ is at most τ units away from the signalreceived, i.e., θ ∈ [ξi − τ, ξi + τ ], ∀i ∈ I;

◮ Perfect information: investors know the true θ;

◮ Common prior: the only information investors have is that θ ∼ U [0, 1];

◮ Informational scenarios are meant to be proxies for different classes ofassets, to the extent that their returns can be forecasted.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Investors’ Problem with Govt & Imperfect Information

◮ With the payoff from the investment strategy beingRi (Xi, θ, A, t) = Xi (θ − p − t) + A, investors solve

maxXi

Xi

[E

(θ | ξi

)− p − t

]+ A

s.t. A ≥ p if Xi = 1, ∀i ∈ I.

◮ With θ∗ = (C − A) /K + p + t and government intervention happeningonly for θ < θ∗, the fact that agents face the same price p but receivedifferent signals ξi mean that their outlooks on the possibility ofintervention will be different, according to (recall thatθ ∈ [ξi − τ, ξi + τ ])

(I) θ∗ ≤ ξi − τ (intervention is ruled out);(II) ξi − τ < θ∗ ≤ ξi + τ (intervention is possible);

(III) ξi + τ < θ∗ (intervention is certain).

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Investment in the Risky Asset and Equilibrium Price

◮ Investors’ heterogenous beliefs about the possibility of interventionimply that they have different expectations about the asset’s payoff,

E

(θ | ξi

), so that

Xi

[E

(θ | ξi

)− p − t

]+ A

= Xi

{I(I)ξi

+I(II)1

2τ

{(C − A

K+ p + t

) [1

2

(C − A

K+ p + t

)− (ξi − τ)

]+

1

2(ξi + τ)2

}

+I(III)

(C − A

K+ p + t

)− p − t } + A

≡ Ui (Xi, ξi, A, p) , ∀i ∈ I.

◮ If the asset is affordable, i.e., A ≥ p, investor i is willing to buy therisky asset if Ui (1, ξi, A, p) ≥ A. The equilibrium price P will be suchthat the fraction of investors satisfying this condition equals thesupply, K.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

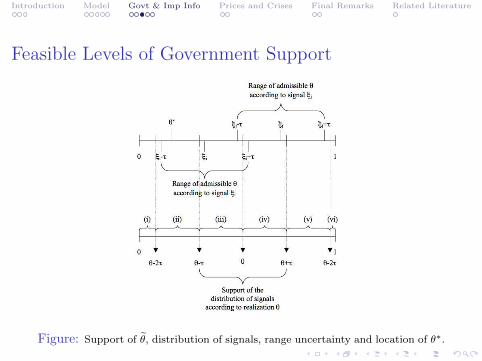

Feasible Levels of Government Support

Figure: Support of θ, distribution of signals, range uncertainty and location of θ∗.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

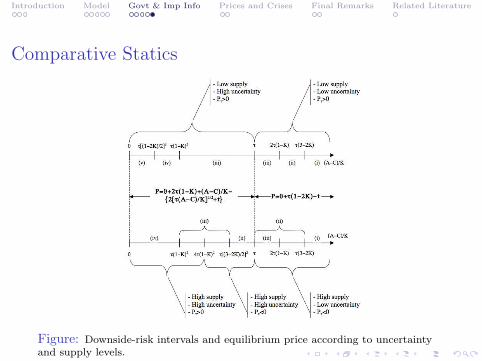

Equilibrium Prices

Main factors determining equilibrium prices:

(i) The magnitude of τ (degree of uncertainty) relative to the downsiderisk, (A − C) /K;

(ii) The supply level of the asset, K.

Figure: Asset price characterization in terms of uncertainty and supply level.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Comparative Statics

Figure: Downside-risk intervals and equilibrium price according to uncertaintyand supply levels.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Effects of Government on Equilibrium Prices

◮ Imperfect Information: equilibrium price when the government isabsent corresponds to the one with the lowest level of support in thegovernment intervention framework: ⇒ P G ≥ P NG;

◮ Perfect Information: equilibrium prices in both frameworks are thesame since the payoff of the asset is known: ⇒ P G = P NG;

◮ Common Prior: government intervention truncates the distribution ofθ, leading to a higher expected value in the government framework asopposed to the case where there’s no safety net: ⇒ P G ≥ P NG

CorollaryRegardless of the informational scenario faced by investors being one of

imperfect, perfect, or common prior information, the resulting equilibrium

price is at least as high in the framework with the presence of the

government relative to the one where the government’s safety net is absent.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Effects of Government on the Likelihood of Crises

◮ Recall that the government intervenes in the economy only if socialwelfare goes below a specific threshold, i.e., if S (θ, A, t) < C, which isequivalent to the realized payoff of the asset being such that

θ < (C − A) /K + p + t ≡ θ∗

◮ A higher price p, therefore, implies a higher likelihood of intervention.

CorollaryIf crises are to be defined as events demanding intervention, the existence of

a government safety net increases the likelihood of them happening, as a

result of the government intervention policy leading to undoubtedly higher

prices - regardless of the informational scenario at hand.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Testable Implications

◮ Assets with some sort of guarantee from the government (implicit orexplicit) should be traded at a premium over otherwise similarsecurities;

◮ With the possibility of government intervention, an increase inuncertainty is beneficial for assets in low supply (less liquid) butdetrimental for the ones in high supply (more liquid);

◮ Prices associated with a high possibility of intervention are supportedto the extent that there’s still some ambiguity related to the decisionof the government: intervention is sure to occur only at extremelyhigh prices, at which a rational investor wouldn’t be willing to trade;

◮ Crises are more likely to happen in economies with strongergovernment support, or safety net.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Extensions

◮ Market participation is affected only by heterogeneity in the signalsinvestors receive, not initial wealth. Introducing heterogeneity in theendowment of investors would allow one to study the effects on pricesof the distribution of wealth too;

◮ The measure of social welfare considered abstracts from thegovernment itself and does not provide any clue regarding what theoptimal level of intervention should be. Such a question couldpotentially be addressed by adding a real sector to the model.

Introduction Model Govt & Imp Info Prices and Crises Final Remarks Related Literature

Related LiteratureEffects of different types of intervention:

◮ Farhi and Tirole (2011): strategic complementarity betweengovernment intervention (interest rate) and maturity transformation;

◮ Diamond and Rajan (2011): undirect intervention (interest rate) morepreferable than direct intervention (bailout);

◮ Acharya and Yorulmazer (2007): government intervention only insystemic crises leads to a too-many-to-fail type of guarantee;

◮ Acharya, Shin and Yorulmazer (2010): effects of different policies onbanks’ choice of liquidity;

◮ Ennis and Keister (2009): efficient government intervention policiesmigh lead to self-fulfilling bank runs;

◮ Morris and Shin (2006), Corsetti, Guimaraes and Roubini (2006):circumstances under which an IMF bailout induces creditors toroll-over their loans.

Market participation effect:

◮ Allen and Gale (1994): model with incomplete market participationand heterogenous liquidity preferences leading to a multiplicity ofequilibrium prices.

Related Documents