GOOD PRACTICES IN GOOD PRACTICES IN IMPROVING PEOPLE'S IMPROVING PEOPLE'S FINANCIAL CAPABILITY FINANCIAL CAPABILITY Azerbaijan Azerbaijan June 2009 June 2009 Shaun Mundy Shaun Mundy World Bank Consultant and Former Head of World Bank Consultant and Former Head of Financial Capability , Financial Services Financial Capability , Financial Services Authority, UK Authority, UK [email protected] 0044 1883 712045 0044 1883 712045

GOOD PRACTICES IN IMPROVING PEOPLE'S FINANCIAL CAPABILITY Azerbaijan June 2009 Shaun Mundy World Bank Consultant and Former Head of Financial Capability,

Dec 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

GOOD PRACTICES IN GOOD PRACTICES IN IMPROVING PEOPLE'S IMPROVING PEOPLE'S

FINANCIAL CAPABILITY FINANCIAL CAPABILITY

Azerbaijan Azerbaijan

June 2009June 2009

Shaun MundyShaun Mundy

World Bank Consultant and Former Head of Financial World Bank Consultant and Former Head of Financial Capability , Financial Services Authority, UKCapability , Financial Services Authority, UK

[email protected] 0044 1883 7120450044 1883 712045

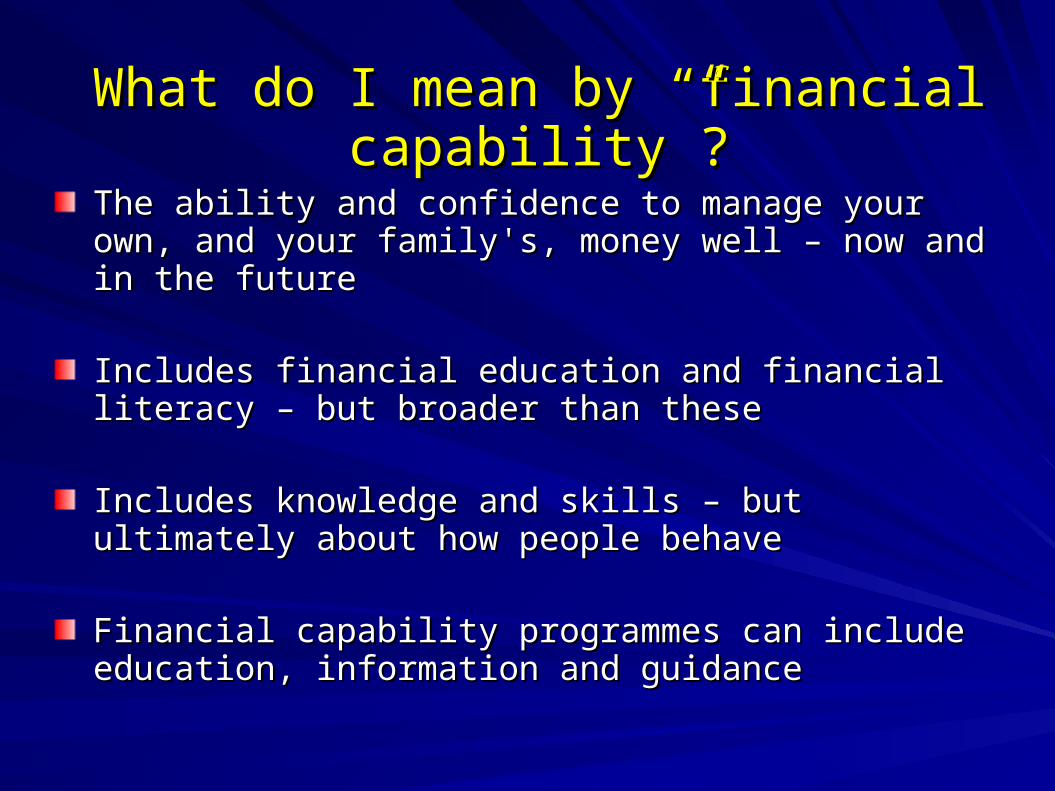

What do I mean by “financial capability”?What do I mean by “financial capability”?

The ability and confidence to manage your own, and The ability and confidence to manage your own, and your family's, money well – now and in the futureyour family's, money well – now and in the future

Includes financial education and financial literacy – but Includes financial education and financial literacy – but broader than thesebroader than these

Includes knowledge and skills – but ultimately about Includes knowledge and skills – but ultimately about how people behavehow people behave

Financial capability programmes can include Financial capability programmes can include education, information and guidance education, information and guidance

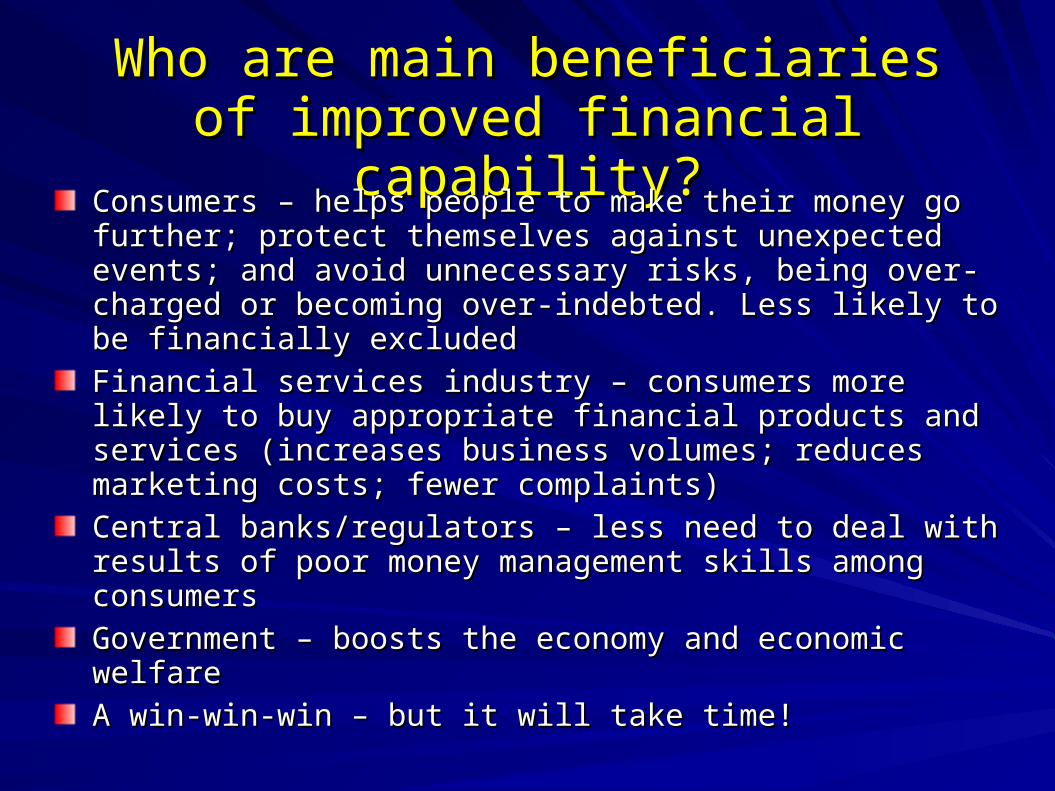

Who are main beneficiaries of Who are main beneficiaries of improved financial capability?improved financial capability?

Consumers – helps people to make their money go further; Consumers – helps people to make their money go further; protect themselves against unexpected events; and avoid protect themselves against unexpected events; and avoid unnecessary risks, being over-charged or becoming over-unnecessary risks, being over-charged or becoming over-indebted. Less likely to be financially excludedindebted. Less likely to be financially excluded

Financial services industry – consumers more likely to buy Financial services industry – consumers more likely to buy appropriate financial products and services (increases appropriate financial products and services (increases business volumes; reduces marketing costs; fewer business volumes; reduces marketing costs; fewer complaints)complaints)

Central banks/regulators – less need to deal with results of Central banks/regulators – less need to deal with results of poor money management skills among consumerspoor money management skills among consumers

Government – boosts the economy and economic welfareGovernment – boosts the economy and economic welfare

A win-win-win – but it will take time!A win-win-win – but it will take time!

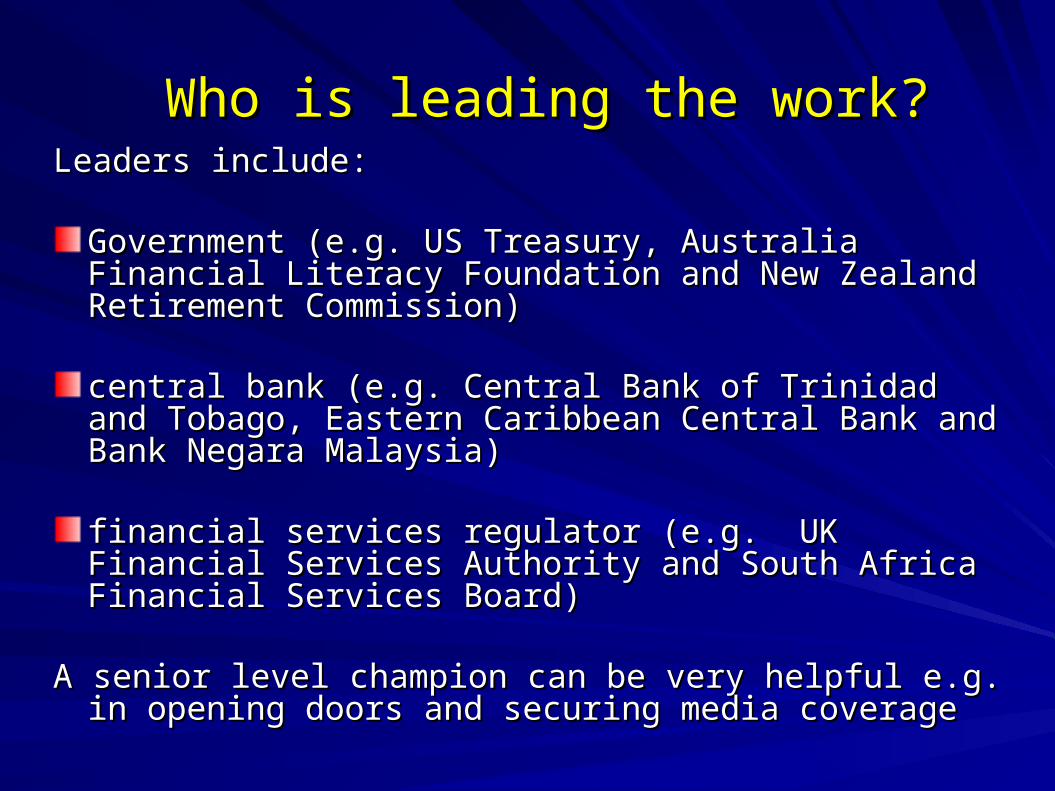

Who is leading the work?Who is leading the work?Leaders include: Leaders include:

Government (e.g. US Treasury, Australia Financial Government (e.g. US Treasury, Australia Financial Literacy Foundation and New Zealand Retirement Literacy Foundation and New Zealand Retirement Commission)Commission)

central bank (e.g. Central Bank of Trinidad and central bank (e.g. Central Bank of Trinidad and Tobago, Eastern Caribbean Central Bank and Bank Tobago, Eastern Caribbean Central Bank and Bank Negara Malaysia)Negara Malaysia)

financial services regulator (e.g. UK Financial Services financial services regulator (e.g. UK Financial Services Authority and South Africa Financial Services Board)Authority and South Africa Financial Services Board)

A senior level champion can be very helpful e.g. in A senior level champion can be very helpful e.g. in opening doors and securing media coverageopening doors and securing media coverage

Who are the potential partners?Who are the potential partners?

Government Government

Central bank and financial Central bank and financial services regulatorsservices regulators

Financial services firms, Financial services firms, MFIs and trade associations MFIs and trade associations + any trusts/foundations+ any trusts/foundations

Employers and trades Employers and trades unionsunions

Consumer organisationsConsumer organisations

MediaMedia

Education bodies (schools; Education bodies (schools; and universities/colleges)and universities/colleges)

Donors, development Donors, development agenciesagencies

Support groups, rural Support groups, rural outreach bodies, cell-phone outreach bodies, cell-phone and utility companies, health and utility companies, health bodies, etc, etcbodies, etc, etc

Wide range of organisations have interest and are Wide range of organisations have interest and are therefore potential partners. For example: therefore potential partners. For example:

How can partners contribute?How can partners contribute?

FundingFunding Developing materialsDeveloping materials Distribution – e.g. of bookletsDistribution – e.g. of booklets Expertise and experience – e.g. in how Expertise and experience – e.g. in how best to reach particular groupsbest to reach particular groups Providing presentersProviding presenters Seconding staffSeconding staff Undertaking projectsUndertaking projects Securing further partners and supportSecuring further partners and support

Need to focus on attitudes – not just Need to focus on attitudes – not just knowledge, information and skillsknowledge, information and skills

Important to focus on people's attitudes, as well Important to focus on people's attitudes, as well as on education, information and skillsas on education, information and skills

Not sufficient, for example, that peopleNot sufficient, for example, that people know know howhow to save. They also need to understand the to save. They also need to understand the benefits that this can bring them and their benefits that this can bring them and their families, to recognise that it is worth deferring families, to recognise that it is worth deferring current expenditure and to be motivated to set current expenditure and to be motivated to set aside money on a regular basisaside money on a regular basis

Behavioural economics insightsBehavioural economics insights

People are liable to be overwhelmed by too much People are liable to be overwhelmed by too much information or by a large number of choices – so, it is information or by a large number of choices – so, it is best to keep things as simple as possiblebest to keep things as simple as possible

People tend to be over-confident and to overlook non-People tend to be over-confident and to overlook non-confirmatory information. Challenging people's views, confirmatory information. Challenging people's views, or getting people to explain their views to others, can or getting people to explain their views to others, can help them to be more objectivehelp them to be more objective

People need to be helped (for example, through People need to be helped (for example, through training and through counselling) to make good training and through counselling) to make good decisions – not merely given training and information decisions – not merely given training and information about financial issuesabout financial issues

Take advantage of teachable momentsTake advantage of teachable moments

For example:For example:

people who are planning to get married people who are planning to get married

couples who are separatingcouples who are separating

parents before/after the birth of a childparents before/after the birth of a child

people whose close relative has recently died people whose close relative has recently died

people starting a new job – particularly if it's their first jobpeople starting a new job – particularly if it's their first job

people coming up for retirementpeople coming up for retirement

households receiving overseas remittanceshouseholds receiving overseas remittances

Use lively and engaging communicationsUse lively and engaging communicationsMany people want to be able to manage their money well, Many people want to be able to manage their money well, but this doesn't necessarily translate into being receptive but this doesn't necessarily translate into being receptive to personal finance messagesto personal finance messages

Use range of lively and engaging methods – avoid “worthy Use range of lively and engaging methods – avoid “worthy but dull”. Trusted intermediaries can be very helpfulbut dull”. Trusted intermediaries can be very helpful

Be positive (e.g. “make the most of your money” – not “this Be positive (e.g. “make the most of your money” – not “this is how to avoid money troubles”)is how to avoid money troubles”)

Keep messages simpleKeep messages simple

Focus groups, consumer testing and pilot exercises help to Focus groups, consumer testing and pilot exercises help to identify what works best identify what works best

Use range of mediaUse range of mediaRadio and television, for example:Radio and television, for example: – soaps soaps – ““edutainment” i.e. use of entertainment and media to edutainment” i.e. use of entertainment and media to

promote educational messages promote educational messages – radio, including call-in shows radio, including call-in shows Helpful to refer to website, call centre number or leaflet line to Helpful to refer to website, call centre number or leaflet line to

get further informationget further information

Publications, e.g. booklets, newspapers (in section which Publications, e.g. booklets, newspapers (in section which has broad appeal, not finance section), magazines, comic has broad appeal, not finance section), magazines, comic books, postersbooks, posters

Consider developing a website (e.g. sorted.org.nz)Consider developing a website (e.g. sorted.org.nz)

Only likely to be successful if perceived as impartial and not Only likely to be successful if perceived as impartial and not as marketing materialas marketing material

Financial education in schoolsFinancial education in schoolsEquipping next generation to manage money well (and Equipping next generation to manage money well (and children who have received financial education can go on children who have received financial education can go on to help their parents)to help their parents)

Curriculums are crowded – but financial education can be Curriculums are crowded – but financial education can be incorporated into a range of other subjects, e.g. incorporated into a range of other subjects, e.g. mathematics, citizenship, languages, social sciencesmathematics, citizenship, languages, social sciences

Schoolchildren find financial education programmes which Schoolchildren find financial education programmes which are experiential and interactive (e.g. researching and are experiential and interactive (e.g. researching and solving problems which students regard as relevant to their solving problems which students regard as relevant to their lives) more engaging lives) more engaging

Many examples of resources for each age group which can Many examples of resources for each age group which can be drawn onbe drawn on

Most teachers don't feel financially capable – they need Most teachers don't feel financially capable – they need training and resourcestraining and resources

Questions and commentsQuestions and comments

Shaun MundyShaun Mundy

0044 1883 7120450044 1883 712045

Related Documents