Goldman Sachs Global LNG Seminar

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Goldman SachsGlobal LNG Seminar

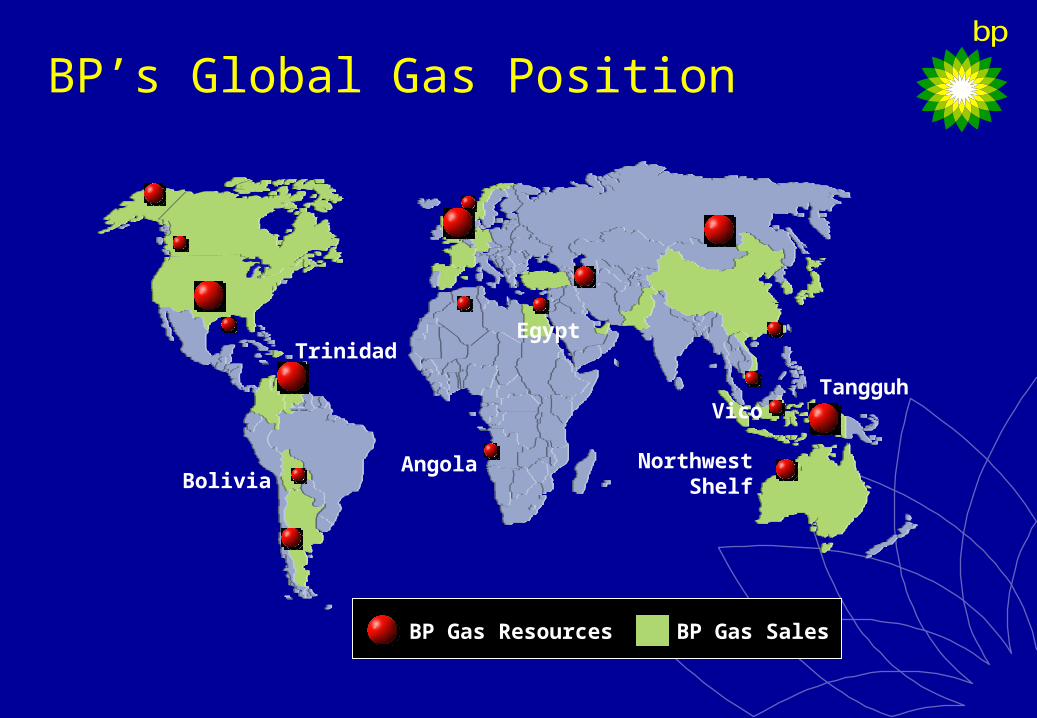

BP’s Global Gas Position

Bolivia

Trinidad

Tangguh

BP Gas Resources BP Gas Sales

NorthwestShelf

Angola

Vico

Egypt

LNG Industry Dynamics Continue to Drive Growth

0

50

100

150

200

250

1964 1973 1980 1990 1996 2000 2010 2010 L 2010 Hi

7% CAGR

Early LNG growth Rise of Asian LNG Plentiful Gas Reserves

JapanKoreaTaiwanOther

EuropeU.S.

Lower growth

LNG gains greater market share of US supply gap

0

50

100

150

200

250

300

350

400

2020

Asia lacksProximal supply

Dri

vers

Dri

versNew M.E Low

Cost Supply

New Atlantic Low Cost Supply

US proximal supply declines

Higher demand growth driven by lower Asian prices

CCGT drives gas demand

New Asian customers

5% CAGR

10% CAGR

Major p/l competition

Gas demand growth continues

Costs allow new smaller markets to be reached

mtpa

mtpa

7% CAGR

US access constraints & low prices

Constrained US access

2002 Sales volume of 111 million tonnes LNG p.a.

•15 bcf/d or 6% of world gas demand of 230 bcf/d

•2.5 million boe/d or 3% of world oil demand

2002 $25b annual sales revenues; 130 LNG ships – cost of $4b per year

Key LNG Markets

Tangguh

Asia PacificTrinidad

USA

NWS

Europe to IndiaAtlanti

c

UK

India

China

Korea

Japan

SpainItaly

USA

Adgas

LNG remains a regional business

• US: deep and liquid market -- gaining access to regas capacity ensures access to market

• Europe: partial liberalisation -- regas capacity and customers generally difficult to secure

• Asia-Pacific: customers prefer long term contracts -- key is securing commitments

Linear business model

High Inertia environment

Gas monetisation priority

Merchant Trader

Early Market access

Portfolio opportunities

Vico

BP LNG Today and Future Developments

Spain, France

Italy, UK

Africa

India

USWC

Asia Pacific

Middle East

Atlantic

USA Japan, Korea, China

Trinidad Trains 2 & 3

Cove Point re-gas capacity

Trinidad Trains 4-6

Build New US East Coast re-gas

Adgas to Spain (3 Years)Qatargas to Spain (3Years)Iran LNG

Kakinanda re-gas & power project, IndiaDabhol, India

NWS supply into Japan/KoreaGuangdong re-gas terminal ownershipFuijan supply contractPhilippines supply (LOI)Vico

NWS Train 5 – Japan/Korea/ChinaTangguh – Japan/Korea/Taiwan/Java,

US West Coast

Nigeria to Spain spot cargoesEgypt Italy re-gas terminalLNG to UK

• Focus is on developing access to key premium markets development/capacity in re-gas.

• Market positions in advance of equity supply managed through short term supply deals & spot.

• Emerging supply network provides new opportunities for LNG trading

Long term economic supply

Short term opportunities

Potential new projects Current activites

British Trader in Trinidad (10/05/03)

Trinidad

Spain

ElbaIsland

CovePoint

Boston

Trains 2 & 340% Spain60% US & Other

Train 140% Spain60% US & Other

Diversion &Back Fill Opportunity

LakeCharles

Trinidad - a New Complex Set of Deliveries to Capture US Market Opportunities

Trains 2 & 3Value Chain Alignment – Repsol acquire upstream interest in BP Trinidad & TobagoPotential Diversion – Trinidadian volumes destined for Spain to more attractive US marketsRisk Management – opportunity to balance supply / demandin Spain

Cove Point Terminal

Dominican Republic

Key LNG Markets

Tangguh

Asia PacificTrinidad

USA

NWS

Europe to IndiaAtlanti

c

UK

India

China

Korea

Japan

SpainItaly

USA

Adgas

LNG remains a regional business

• US: deep and liquid market -- gaining access to regas capacity ensures access to market

• Europe: partial liberalisation -- regas capacity and customers generally difficult to secure

• Asia-Pacific: customers prefer long term contracts -- key is securing commitments

Linear business model

High Inertia environment

Gas monetisation priority

Merchant Trader

Early Market access

Portfolio opportunities

Vico

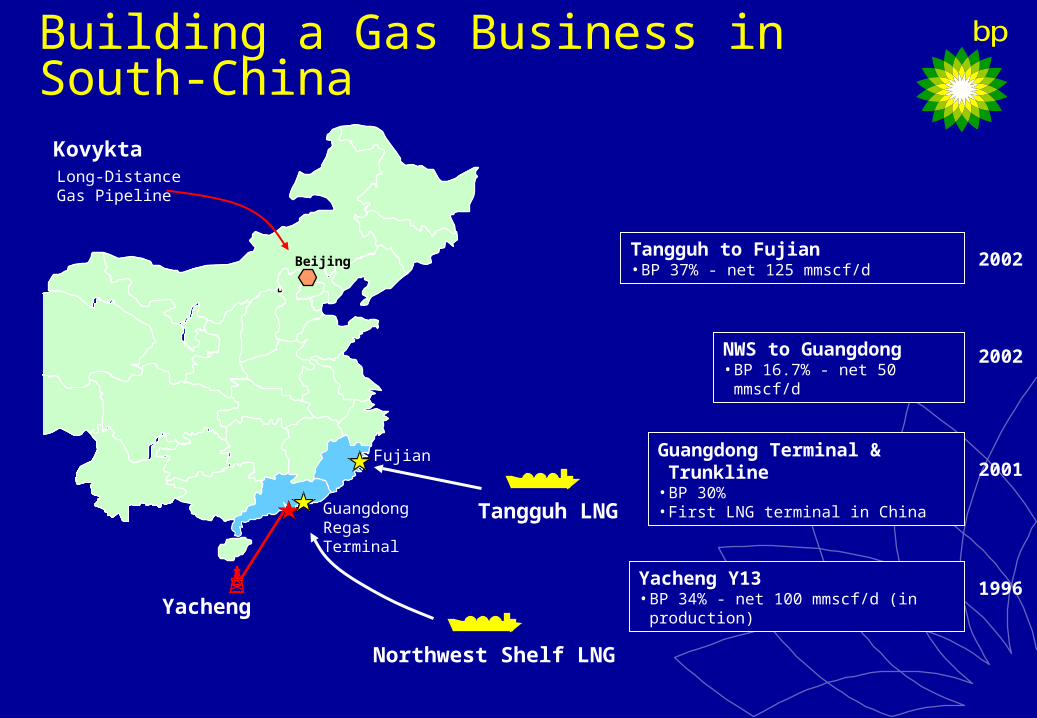

Yacheng

Kovykta

Beijing

Long-Distance Gas Pipeline

Fujian

Guangdong Regas Terminal

Building a Gas Business in South-China

NWS to Guangdong•BP 16.7% - net 50 mmscf/d

Yacheng Y13•BP 34% - net 100 mmscf/d (in

production)

Tangguh to Fujian•BP 37% - net 125 mmscf/d

Guangdong Terminal & Trunkline

•BP 30%•First LNG terminal in China

1996

2001

2002

2002

Northwest Shelf LNG

Tangguh LNG

Tangguh

BP Equity Gas into LNG Plant

0

1,000

2,000

3,000

Sontrach Shell Qatar BP XOM TFE

mmscf/d

2006E

2003

BP internal analysis based on publicly available data

gas supplied to plants

mmscfd

0

500

1000

1500

2000

00 01 02 03 04 05 08

New LNG

~

source: BP projections 03 - 05, 08

markets capturedas of Dec ‘02

0

500

1000

1500

2000

Japan

Americas

Spain

China

Other

mmscfdTrinidad 2&3Trinidad 1 IndonesiaAustralia

Building Markets Ahead of SupplyBP’s growth in equity gas is supported by building key LNG market positions in all three regions ahead of the supply

Related Documents

](https://static.cupdf.com/doc/110x72/577c7d741a28abe0549edc33/lee000966-depth-conversion-of-tangguh-gas-fieldsautosaved.jpg)