bcb.gov.br Brazil’s Economic Outlook and Agenda BC# Roberto Campos Neto Governor of Banco Central do Brasil October 15, 2021 Goldman Sachs

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

bcb.gov.br

Brazil’s Economic Outlook and Agenda BC#

Roberto Campos NetoGovernor of Banco Central do Brasil

October 15, 2021

Goldman Sachs

- 10 20 30 40 50 60 70 80 90

Chile

Canada

Japan

Brazil

United Kingdom

Israel

Australia

United States

Turkey

Europe ex UK

South America ex Brazil

Colombia

IndiaUK

Europe ex. UK

2

COVID-19

Covid-19: New deaths and vaccination

Sources: (1) Our World in Data. Last data: 13 Oct. 2021. (2) Localiza SUS for Brazilian booster doses.

South Am. ex BrazilBrazil

U.S.

New deaths/million(7-day rolling average)

New deaths fall as vaccination advances

At least one dose Fully vaccinated Booster dose

Share of population vaccinated (% of population)

Brazil

0

2

4

6

8

10

12

14

16

18

20

Mar-20 Sep-20 Mar-21 Sep-21

3

COVID-19

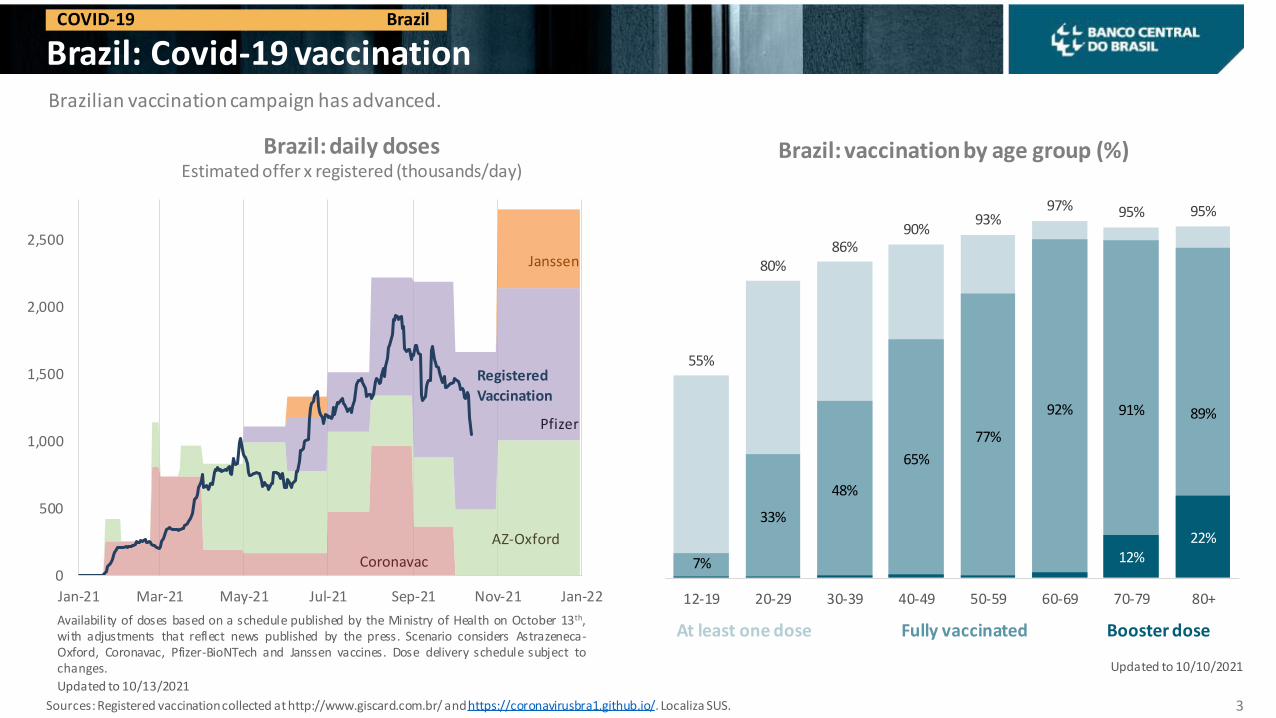

Brazil: Covid-19 vaccination

Sources: Registered vaccinationcollected at http://www.giscard.com.br/ andhttps://coronavirusbra1.github.io/. Localiza SUS.

Brazil

Brazilian vaccination campaign has advanced.

Brazil: daily dosesEstimated offer x registered (thousands/day)

Brazil: vaccination by age group (%)

Availability of doses based on a schedule published by the Ministry of Health on October 13th,with adjustments that reflect news published by the press. Scenario considers Astrazeneca-Oxford, Coronavac, Pfizer-BioNTech and Janssen vaccines. Dose delivery schedule subject tochanges.

At least one dose Fully vaccinated Booster dose

Updated to 10/10/2021

Updated to 10/13/2021

55%

80%86%

90%93%

97% 95% 95%

7%

33%

48%

65%

77%

92% 91% 89%

12%22%

12-19 20-29 30-39 40-49 50-59 60-69 70-79 80+

Coronavac

AZ-Oxford

Registered

Vaccination

0

500

1,000

1,500

2,000

2,500

Jan-21 Mar-21 May-21 Jul-21 Sep-21 Nov-21 Jan-22

Pfizer

Janssen

4

GLOBAL ECONOMY

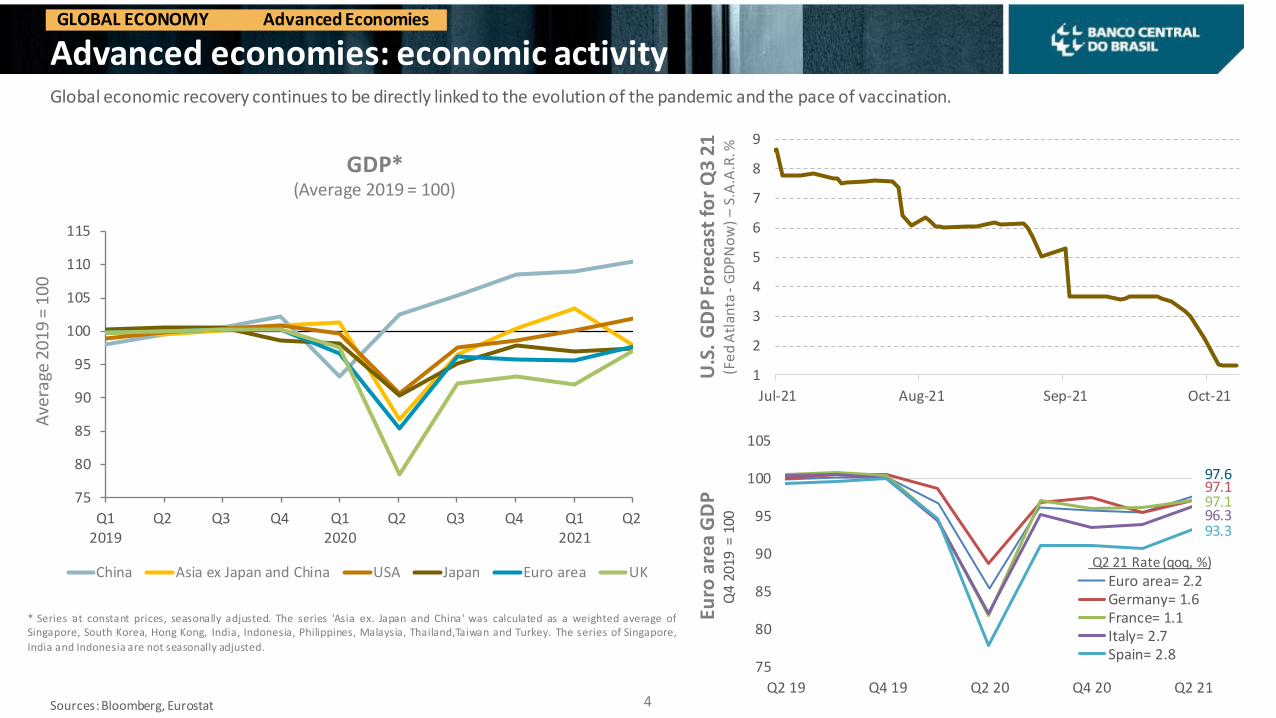

Advanced economies: economic activity Global economic recovery continues to be directly linked to the evolution of the pandemic and the pace of vaccination.

Sources: Bloomberg, Eurostat

Advanced Economies

. Euro

are

a G

DP

U.S

. G

DP

Fo

reca

st f

or

Q3

21

(Fe

d A

tlan

ta -

GD

PN

ow

) –

S.A

.A.R

. %

97.697.197.196.393.3

75

80

85

90

95

100

105

Q2 19 Q4 19 Q2 20 Q4 20 Q2 21

Q4

2019

= 1

00

Euro area= 2.2Germany= 1.6France= 1.1Italy= 2.7Spain= 2.8

Q2 21 Rate (qoq, %)

75

80

85

90

95

100

105

110

115

Q12019

Q2 Q3 Q4 Q12020

Q2 Q3 Q4 Q12021

Q2

Ave

rage

20

19

= 1

00

China Asia ex Japan and China USA Japan Euro area UK

GDP* (Average 2019 = 100)

* Series at constant prices, seasonally adjusted. The series 'Asia ex. Japan and China' was calculated as a weighted average ofSingapore, South Korea, Hong Kong, India, Indonesia, Philippines, Malaysia, Thailand,Taiwan and Turkey. The series of Singapore,

India and Indonesia are not seasonally adjusted.

1

2

3

4

5

6

7

8

9

Jul-21 Aug-21 Sep-21 Oct-21

82%

100%

69%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21

Total Advanced Countries Emerging Countries

Brazil below

50

Total 28 countries, 12 advanced and 16 emerging

5

Economic activity

Sources: Refinitiv, Bloomberg.

Eco

no

mic

Su

rpri

ses

(Cit

i Eco

no

mic

Su

rpri

ses

Ind

ex

–C

ESI)

GLOBAL ECONOMY

PMI Manufacturing: % countries above 50 points

PM

I Se

rvic

es

(% o

f co

un

trie

s ab

ove

50

po

ints

)

-80

-40

0

40

80

120

Oct-16 Oct-17 Oct-18 Oct-19 Oct-20 Oct-21

Global EM

83%

0%

20%

40%

60%

80%

100%

Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Sep-21

Brazil above 50

Total 12 countries

6

GLOBAL ECONOMY

China: economic activity

Sources: Caixin-Markit, NBS, Deutsche Bank, Bloomberg

China

PMI Manufacturing - China

47

48

49

50

51

52

53

54

55

Sep-12 Sep-13 Sep-14 Sep-15 Sep-16 Sep-17 Sep-18 Sep-19 Sep-20 Sep-21

Caixin PMI (surveys mainly small, private business)

Official PMI (surveys mainly state-owned companies)

Hang Seng Properties Index

Real estate activity slowing down30%

25%

20%

15%

10%

5%

0%

-5%

-10%

30%

25%

20%

15%

10%

5%

0%

-5%

-10%

Jul-12 Jul-15 Jul-18 Jul-21

Property Investiment in Real Estate - Total Steel Production - rhs

000s

25

30

35

40

45

50

Oct-18 Apr-19 Oct-19 Apr-20 Oct-20 Apr-21 Oct-21

53

63

73

83

93

103

113

123

133

143

53

63

73

83

93

103

113

123

133

143

Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21

Chile Mexico South Africa Colombia Brazil

7

GLOBAL ECONOMY

Emerging economies: economic activity

Sources: Bloomberg, IBGE and BCB (Focus Report).

Emerging Economies

Re

tail

sale

s(j

an/2

02

0=1

00

)

Rus

sia

Mal

aysi

a

Sou

th A

fric

a Bra

zil

Me

xico

Arg

enti

na Colo

mbi

aCh

ina

Chile

-12

-10

-8

-6

-4

-2

0

2

42020 GDP (%)

55

60

65

70

75

80

85

90

95

100

105

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21

SA, j

an/2

020

= 10

0

Economic Activity Index

Argentina Brazil Chile Colombia Mexico Peru

Ma

lays

ia

Mal

aysi

a

Ru

ssia

Rus

sia

Sou

th A

fric

a

Sou

th A

fric

a

Bra

zil

Bra

zil

Mex

ico

Me

xico

Arg

enti

na

Arg

enti

na

Colo

mb

ia

Co

lom

bia

Chin

a

Chin

a

Chile

Chile

0

2

4

6

8

10

12

2021 2022

GDP forecast (%)

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

Angola

Egypt

South Africa

Morocco

Algeria

Nigeria

India

Pakistan

China

Malaysia

Turkey

Kazakhstan

Azerbaijan

Russia

Thailand

Philippines

Croatia

Hungary

Ukraine

Romania

Belarus

Brazil

Uruguay

Bolivia

Colombia

Ecuador

Peru

Chile

Mexico

Dominican Rep.

Oman

Islamic Re. of Iran

Un. Arab Emirates

8

GLOBAL ECONOMY

Fiscal response

Sources: [1] IMF WEO Oct/21. For Brazil, the source is BCB. Brazil’s 2021 figure refers to Aug . [2] IMF Historical Public Debt Database.

Fiscal policy

Gross Debt – emerging markets(% of GDP)

Historical pattern of general government debt(1935-2020, % of GDP)

AFR

ICA

ASI

A E

X M

IDD

LE E

AST

EUR

OP

ELA

TIN

AM

ERIC

AM

IDD

LE E

AST

Brazil

Advanced Emerging Low Income

-10

5

20

35

50

65

80

95

110

125

193

5

194

0

194

5

195

0

195

5

196

0

196

5

197

0

197

5

198

0

198

5

199

0

199

5

200

0

200

5

201

0

201

5

202

0

WWIIGlobal financial

crisis

Covid-19

9

GLOBAL ECONOMY

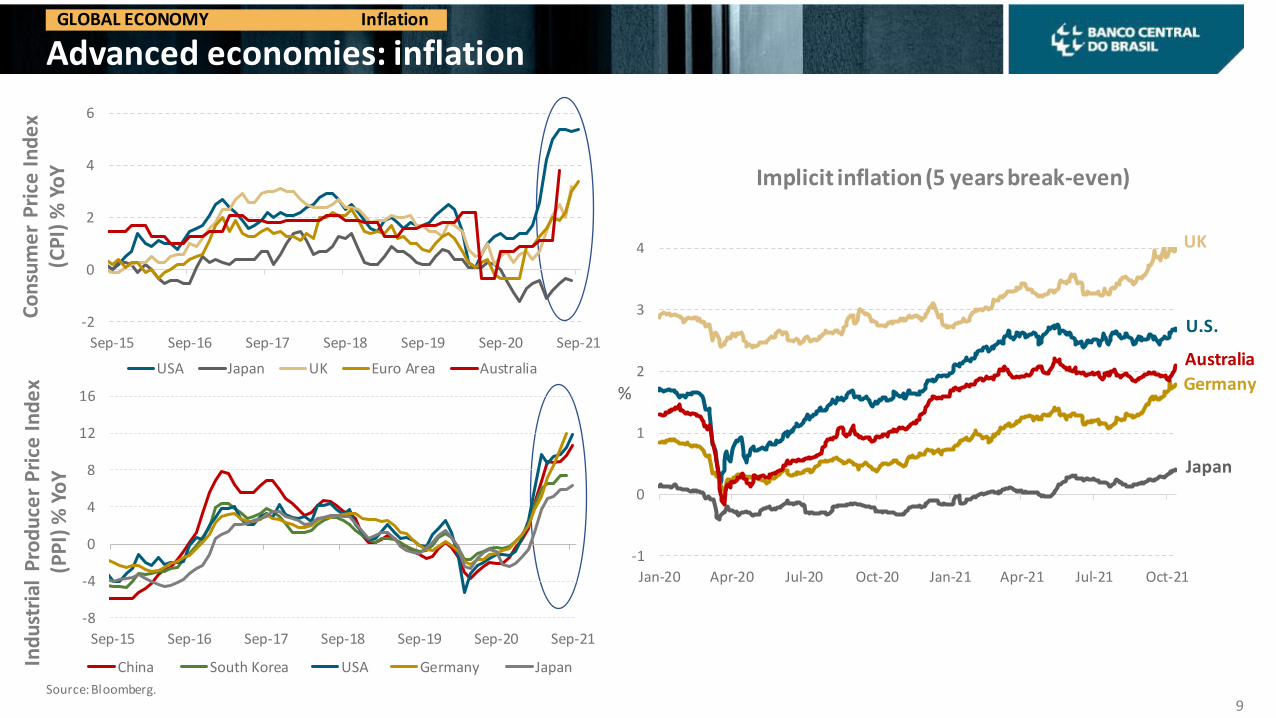

Advanced economies: inflation

Source: Bloomberg.

Inflation

Implicit inflation (5 years break-even)

UK

U.S.

Australia

Germany

Japan

Co

nsu

me

r P

rice

In

de

x(C

PI)

% Y

oY

%

Ind

ust

rial

Pro

du

cer

Pri

ce I

nd

ex

(PP

I) %

Yo

Y

-2

0

2

4

6

Sep-15 Sep-16 Sep-17 Sep-18 Sep-19 Sep-20 Sep-21

USA Japan UK Euro Area Australia

-1

0

1

2

3

4

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

-8

-4

0

4

8

12

16

Sep-15 Sep-16 Sep-17 Sep-18 Sep-19 Sep-20 Sep-21

China South Korea USA Germany Japan

-25

-20

-15

-10

-5

0

5

10

15

20

25

-1

0

1

2

3

4

5

96 98 00 02 04 06 08 10 12 14 16 18 20 22

CPI Owner´s Equivalent Rent

CPI Primary Rents

Case-Shiller Index (advanced 14 months, right axis)

10

GLOBAL ECONOMY

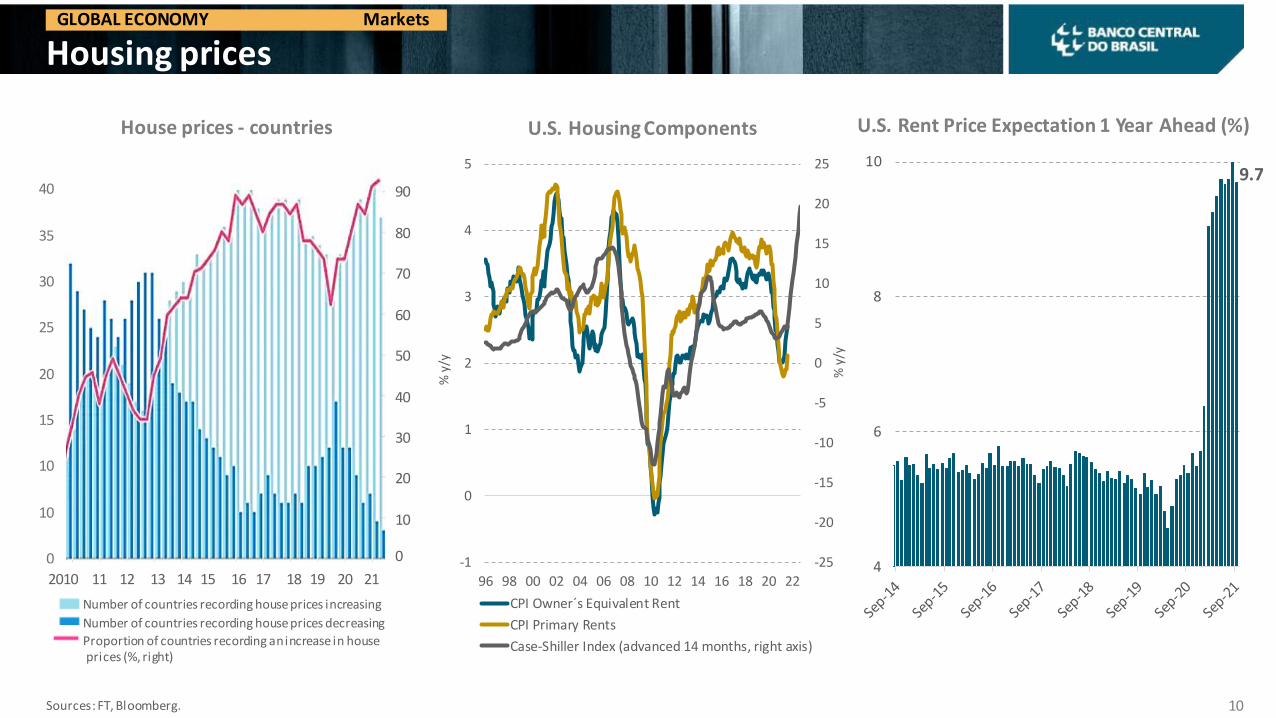

Housing prices

Sources: FT, Bloomberg.

Markets

U.S. Housing Components U.S. Rent Price Expectation 1 Year Ahead (%)

Number of countries recording house prices increasing

Number of countries recording house prices decreasing

Proportion of countries recording an increase in houseprices (%, right)

40

35

30

25

20

15

10

10

0

90

80

70

60

50

40

30

20

10

0

House prices - countries

2010 11 12 13 14 15 16 17 18 19 20 21

% y

/y

% y

/y

9.7

4

6

8

10

11

GLOBAL ECONOMY

Sectoral bottlenecks

Sources: Bloomberg, Refinitiv.

Indicators suggest bottlenecks in the global economy.

Inte

rna

tio

na

l Fre

igh

t C

ost

s(J

an 2

018

= 10

0)

Sem

ico

nd

uct

ors

Ind

ex

(De

c 19

93 =

100

)

Semiconductors = Philadelphia Stock Exchange Semiconductor Index

0

5

10

15

20

25

30

35

40

45

50

US AT UK FR DE EA CZ AU IT CA IE ES GR TW PL JP MX KR BR TR ID RU CN IN

PMI Manufacturing Delivery Times (Smaller numbers represent longer time)

Sep/21 2020 Average0

700

1400

2100

2800

3500

Oct-96 Oct-01 Oct-06 Oct-11 Oct-16 Oct-21

826827

405

0

200

400

600

800

1000

Jan-18 Oct-18 Jul-19 Apr-20 Jan-21 Oct-21

Global Container Index

Harpex Global Charter Rate Index

Baltic Exchange Dry Global Index

12

GLOBAL ECONOMY

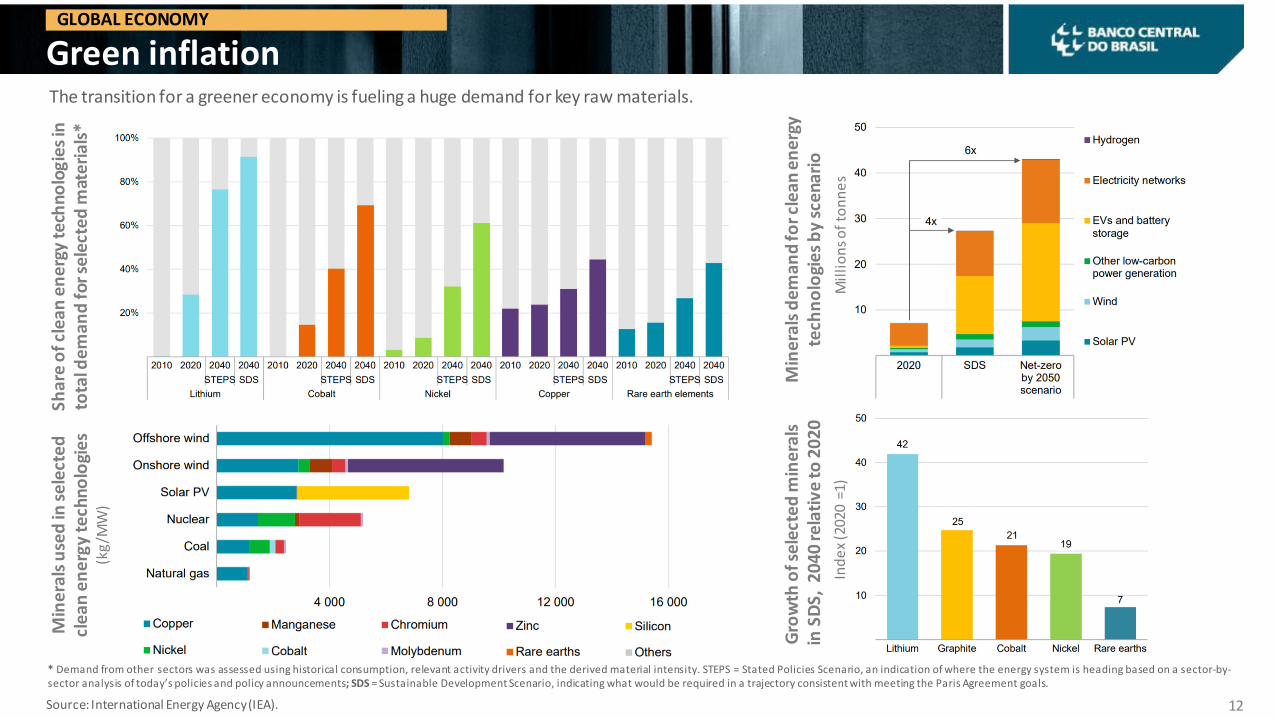

Green inflation

Source: International Energy Agency (IEA).

The transition for a greener economy is fueling a huge demand for key raw materials.

Shar

e o

f cle

an e

ner

gy te

chno

logi

es in

to

tal d

eman

d fo

r sel

ecte

d m

ater

ials

*M

ine

rals

use

d in

se

lect

ed

cl

ean

en

erg

y t

ech

no

logi

es

(kg

/MW

)

Min

eral

s d

eman

d fo

r cle

an e

ner

gy

tech

no

logi

es

by

sce

nari

o

Mil

lio

ns

of

ton

ne

s

Gro

wth

of s

elec

ted

min

eral

sin

SD

S, 2

040

rela

tive

to 2

020

* Demand from other sectors was assessed using historical consumption, relevant activity drivers and the derived material intensity. STEPS = Stated Policies Scenario, an indication of where the energy system is heading based on a sector-by-sector analysis of today’s policies and policy announcements; SDS = Sustainable Development Scenario, indicating what would be required in a trajectory consistent with meeting the Paris Agreement goals.

Ind

ex

(202

0 =1

)

0

200

400

600

800

1000

1200

1400

Oct-14 Oct-15 Oct-16 Oct-17 Oct-18 Oct-19 Oct-20 Oct-21

13

GLOBAL ECONOMY

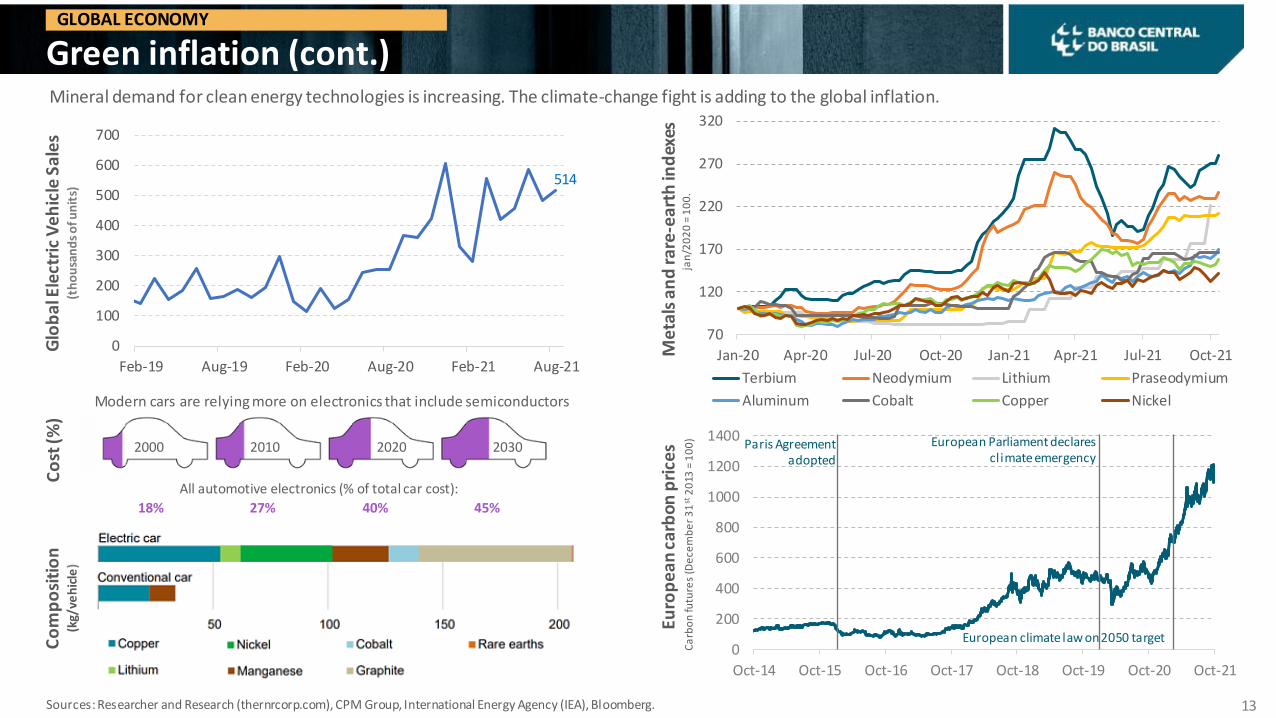

Green inflation (cont.)Mineral demand for clean energy technologies is increasing. The climate-change fight is adding to the global inflation.

Co

st (%

)

Modern cars are relying more on electronics that include semiconductors

2000 2010 2020 2030

All automotive electronics (% of total car cost):

18% 27% 40% 45%

Sources: Researcher and Research (thernrcorp.com), CPM Group, International Energy Agency (IEA), Bloomberg.

Co

mp

osi

tio

n(k

g/ve

hic

le)

jan

/20

20

= 1

00

.

Euro

pea

n ca

rbon

pri

ces

Ca

rbo

n fu

ture

s (D

ece

mb

er

31

st2

013

= 1

00

)

Me

tals

an

d ra

re-e

arth

ind

exes

Cobre

Lítio

Níquel

Manganês

Cobalto

Grafite

50 100 150 200

Carro convencional

Paris Agreement adopted

European Parliament declares climate emergency

Terras-raras

Glo

ba

l Ele

ctri

c V

eh

icle

Sa

les

(th

ou

san

ds

of u

nit

s)

European climate law on 2050 target

514

0

100

200

300

400

500

600

700

Feb-19 Aug-19 Feb-20 Aug-20 Feb-21 Aug-21

70

120

170

220

270

320

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

Terbium Neodymium Lithium Praseodymium

Aluminum Cobalt Copper Nickel

14

GLOBAL ECONOMY

Energy pricesEnergy

Source: Bloomberg.

Energy Prices - Emerging countries (Dec/19=100)

Energy Prices - Advanced countries (Dec/19=100)

133

124

118118

116

109109

104103

80

90

100

110

120

130

140

Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21

Brazil Turkey India

Peru South Africa Chile

Russia Colombia Mexico

111110

107

104

101

75

80

85

90

95

100

105

110

115

Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21

USA United Kingdom Euro area Japan Canada

25

50

75

100

125

150

175

200

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

Jan

20

20

=10

0

15

GLOBAL ECONOMY

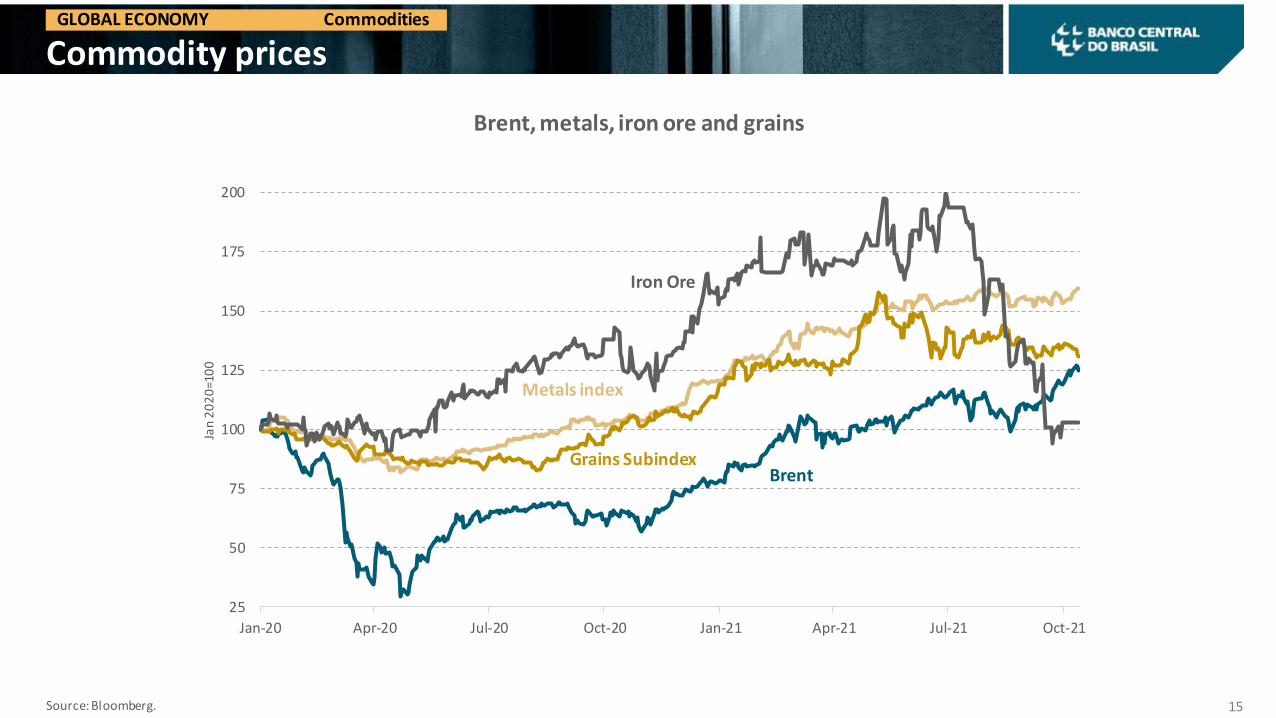

Commodity prices

Source: Bloomberg.

Commodities

Brent, metals, iron ore and grains

Iron Ore

Grains SubindexBrent

Metals index

16

GLOBAL ECONOMY

Emerging economies: inflation

Source: Bloomberg.

Inflation

CPI(jan 2020=100)

CPI Services(jan 2020=100)

130

127

124

121

118

115

112

109

106

103

100

97

126

122

118

114

110

106

102

98

107106

105104104

103

101

124

98

102

106

110

114

118

122

126

98

100

102

104

106

108

110

Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21

Russia

South Africa

Mexico

Chile

Brazil

Colombia

China

Turkey (right)

111

110

109

108107107

107

106

99

128

97

100

103

106

109

112

115

118

121

124

127

130

97

99

101

103

105

107

109

111

113

Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21

BrazilRussiaIndiaMexicoSouth AfricaChilePeruColombiaChinaTurkey (right)

18.00

4.75

6.75

3.50 4.00 3.502.00

4.35

6.25

2.00 1.75 1.650.50

2.751.50

0.50

8.50

0

5

10

15

20

TUR

MEX

RU

S

IDN

IND

ZAF

PH

L

CH

N

BR

A

CO

L

MYS

HU

N

THA

CH

L

PER

PO

L

UKR

Expected for 2021 CurrentP

oli

cy r

ate

s(%

)

17

GLOBAL ECONOMY

EMEs: inflation expectations and monetary policy Inflation expectations and monetary policy in EMEs

Sources: Bloomberg, BCB Focus Report.

Inflation

Several EMEs facing inflation pressures are raising interest rates. Most EMEs remain with inflation expectations anchored.

Inte

rest

rat

e c

han

ge s

ince

Feb

/21

(% Y

oY

)

0.00.51.01.52.02.53.03.54.04.5

Feb-21 Apr-21 Jun-21 Aug-21 Oct-21Brazil +4.25 Russia +2.5 Ukraine +2.5

Chile +2.25 Peru +1.25 Hungary +1.05

Turkey +1 Mexico +0.75 Poland +0.4

Colombia +0.25

18

GLOBAL ECONOMY

Monetary Policy

Sources: Bloomberg, Deutsche Bank.

Monetary Policy

Number of Global Central Bank Decisions - Hikes and Cuts* (rolling 12-month basis)

In terms of global central bank decisions of hikes exceeding cuts, we are now at the highest differential for a decade.

*Sample 21 countries from 1999, 50 from 2005, 60 from 2007, 70 from 2010, 79 from 2013, 80 from 2015.

400

350

300

250

200

150

100

50

0

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Hikes Cuts

0

2

4

6

8

10

12

0 1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y

Rat

es

19

GLOBAL ECONOMY

EMEs: interest rates

Sources: Bloomberg.

Emerging Economies

Yield curves (Jan 20 (dashed lines) - Oct 13 (continuous line), 2021)

10y nominal interest rate (%)

BrazilSouth Africa

MexicoRussia

Colombia

2

4

6

8

10

12

14

Jan-

18

Apr

-18

Jul-

18

Oct

-18

Jan-

19

Apr

-19

Jul-

19

Oct

-19

Jan-

20

Apr

-20

Jul-

20

Oct

-20

Jan-

21

Apr

-21

Jul-

21

Oct

-21

%

Brazil South Africa Russia Mexico

Chile Indonesia Colombia

0

200

400

600

1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y

Cha

nge

sin

ce

Jan

21s

t(b

.p.)

Tenor

20

GLOBAL ECONOMY

Real FX rate and terms of trade

Source: Bloomberg

Indexes of effective foreign exchange rate and terms of trade detached

40

60

80

100

120

-20

-10

0

10

20

Brazil

60

80

100

120

-30

0

30

60

Australia

80

90

100

110

-40

-20

0

20

40

60

Chile

50

70

90

110

-5

10

25

40

South Africa

60

80

100

120

-10

0

10

20Canada

50

70

90

110

130

-10

20

50

80

Colombia

-1040

-840

-640

-440

-240

-40

160

360

Aug-18 Feb-19 Aug-19 Feb-20 Aug-20 Feb-21 Aug-21

88

90

92

94

96

98

100

102

104

I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II

2014 2015 2016 2017 2018 2019 2020 2021

21

DOMESTIC ECONOMY

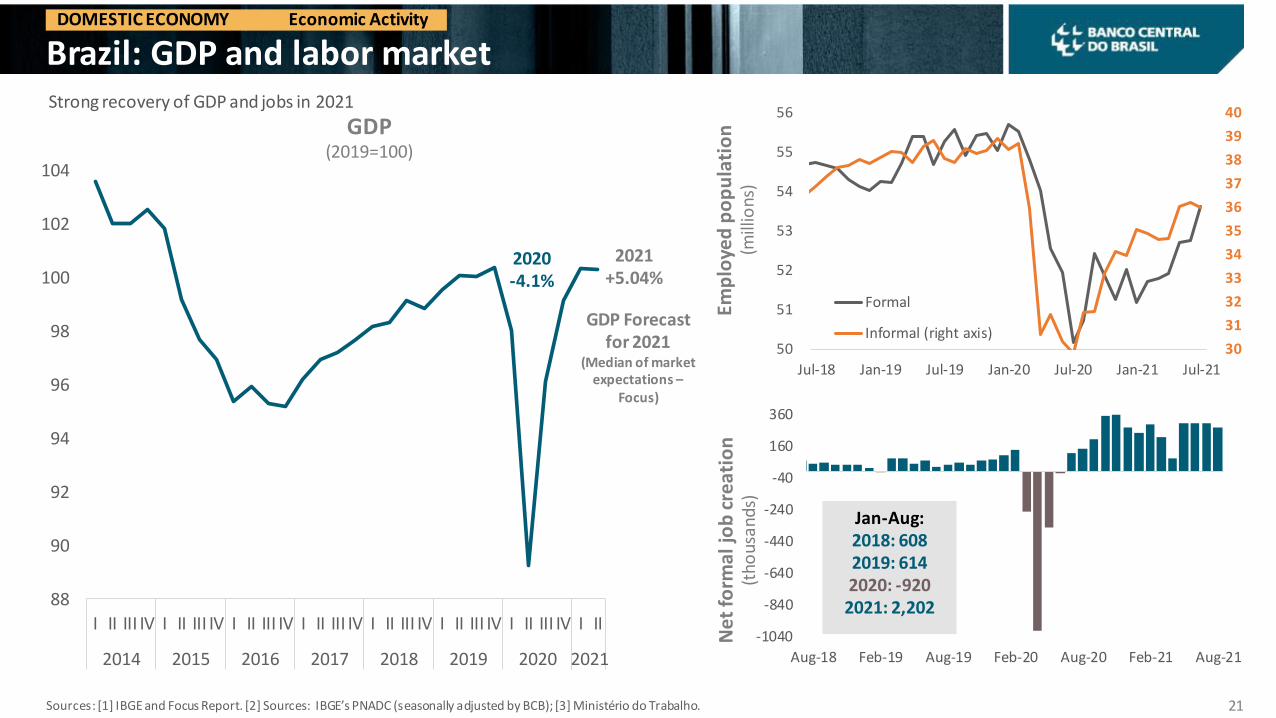

Brazil: GDP and labor market

Sources: [1] IBGE and Focus Report. [2] Sources: IBGE’s PNADC (seasonally adjusted by BCB); [3] Ministério do Trabalho.

Economic Activity

Strong recovery of GDP and jobs in 2021

GDP(2019=100)

2021+5.04%

GDP Forecast for 2021

(Median of market expectations –

Focus)

2020-4.1%

Ne

t fo

rmal

job

cre

atio

n(t

hous

ands

)Em

plo

yed

po

pu

lati

on

(m

illio

ns)

Jan-Aug:2018: 6082019: 6142020: -9202021: 2,202

30

31

32

33

34

35

36

37

38

39

40

50

51

52

53

54

55

56

Jul-18 Jan-19 Jul-19 Jan-20 Jul-20 Jan-21 Jul-21

Formal

Informal (right axis)

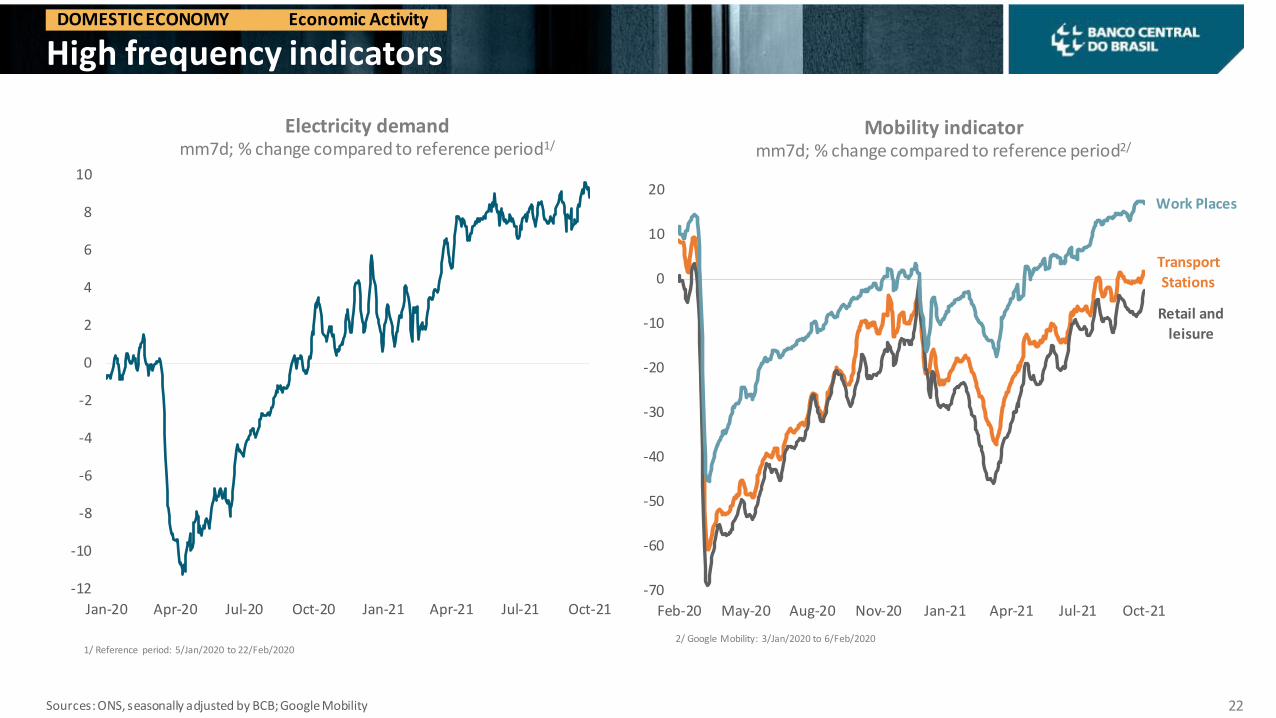

22

DOMESTIC ECONOMY

High frequency indicators

Sources: ONS, seasonally adjusted by BCB; Google Mobility

Economic Activity

Electricity demandmm7d; % change compared to reference period1/

Mobility indicatormm7d; % change compared to reference period2/

Trocar por indicador de mobilidade colado ao lado (Pedir para Depec)

2/ Google Mobility: 3/Jan/2020 to 6/Feb/20201/ Reference period: 5/Jan/2020 to 22/Feb/2020

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21 Oct-21F

Transport

Stations

Retail and

leisure

Work Places

-70

-60

-50

-40

-30

-20

-10

0

10

20

Feb-20 May-20 Aug-20 Nov-20 Jan-21 Apr-21 Jul-21 Oct-21

55

60

65

70

75

80

85

90

95

100

105

110

115

120

Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21

Consumer

Manufacturing

Services

Construction

Retail

50

55

60

65

70

75

80

85

90

95

100

105

110

115

120

Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21

23

DOMESTIC ECONOMY

Confidence indicators

Source: FGV. Seasonally adjusted data.

Economic Activity

Business confidence X consumer confidence Consumer confidenceBy income range (in BRL thousand)

Average 2018-2019=

100

> R$ 9.6 thousand

R$ 4.8 to 9.6 thousand

R$ 2.1 to 4.8 thousand

< R$ 2.1 thousand

Average 2018-2019=

100

24

DOMESTIC ECONOMY

Consumer inflation

Sources: IBGE, BCB.

Inflation

10.25

6.4

0

1

2

3

4

5

6

7

8

9

10

11

Sep-14 Sep-15 Sep-16 Sep-17 Sep-18 Sep-19 Sep-20 Sep-21

IPCA Average of core inflation measures Target

IPCA and target (% YoY) Inflation segments (% YoY)

-6

-2

2

6

10

14

18

22

Sep-14 Sep-15 Sep-16 Sep-17 Sep-18 Sep-19 Sep-20 Sep-21

Administered prices Services

Industrial goods Food at home

Services, 2.73%

Underlying services, 3.77%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Sep-14 Sep-15 Sep-16 Sep-17 Sep-18 Sep-19 Sep-20 Sep-21

25

DOMESTIC ECONOMY

CPI: Services

Source: BCB, based on IBGE.

Inflation

CPI: Services (%) (24-month accumulated, annualized)

26

DOMESTIC ECONOMY

CPI: Surprises and decomposition

Sources: IBGE, BCB.

Inflation

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Sep-20 Nov-20 Jan-21 Mar-21 May-21 Jul-21 Sep-21

Administered

Services

IndustrialGoods

Food athome

CPI surprises (% MoM) Contribution to MoM change (in p.p.)

The date of the projections (in September, December, March and June) corresponds to the cutoff date of the Central Bank of Brazil Inflation Report.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Sep

-20

Oct

-20

No

v-20

Dec

-20

Jan

-21

Feb

-21

Mar

-21

Ap

r-21

May

-21

Jun-

21

Jul-2

1

Au

g-21

Sep

-21

Forecasts in Sep/20 Forecasts in Dec/20 Forecasts in Mar/21 Forecasts in Jun/21 For. InSep/21

IPCA BCB forecast Market expectations (Focus)

27

DOMESTIC ECONOMY

Inflation expectations for CPI

Source: BCB (Focus Report)

Inflation

Market expectations – Focus (% p.y.)

8.59%

4.17%

3.25%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

Aug-19 Jan-20 Jun-20 Nov-20 Apr-21 Sep-21

2021

2022

2023

28

DOMESTIC ECONOMY

Monetary policy

• In its 241st meeting, the Copom unanimously decided to increase the Selic rate by 1.00 p.p. to 6.25%p.a.

• The Committee judges that this decision reflects its baseline scenario for prospective inflation, a higher-than-usual variance in the balance of risks, and is consistent with the convergence of inflation to its target over therelevant horizon for monetary policy, which includes 2022 and, to a lesser extent, 2023.

• The Committee considers that, at the present stage of the tightening cycle, this pace is the most appropriate toguarantee inflation convergence to the target at the relevant horizon and, simultaneously, allow the Committeeto obtain more information regarding the state of the economy and the persistence of shocks.

• At this moment, the Copom's baseline scenario and balance of risks indicate as appropriate to advance theprocess of monetary tightening further into the restrictive territory.

• For the next meeting, the Committee foresees another adjustment of the same magnitude. The Copomemphasizes that its future policy steps could be adjusted to ensure the achievement of the inflation target andwill depend on the evolution of economic activity, on the balance of risks, and on inflation expectations andprojections for the relevant horizon for monetary policy.

241st Copom Meeting – September 2021

15.9%

12.2%

18.8%

-9%

-5%

-1%

3%

7%

11%

15%

19%

23%

Aug-17 Aug-18 Aug-19 Aug-20 Aug-21

29

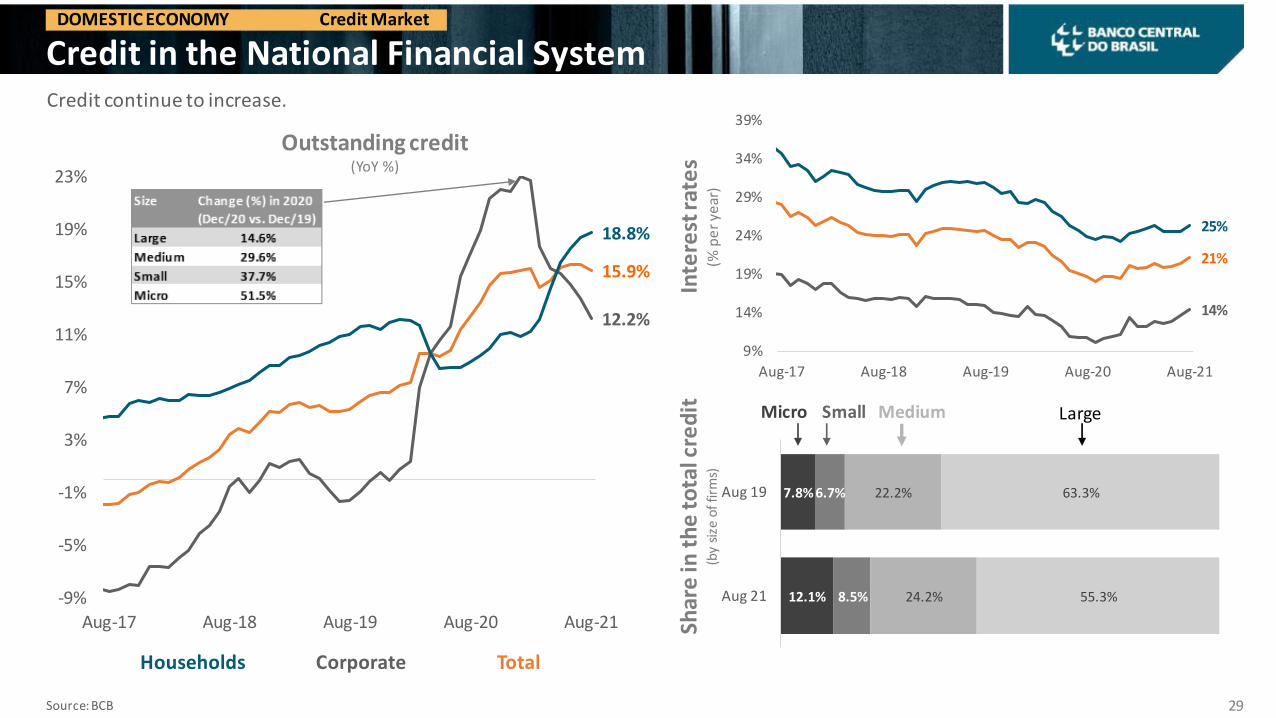

DOMESTIC ECONOMY

Credit in the National Financial System

Source: BCB

Credit Market

Credit continue to increase.

Outstanding credit(YoY %)

Inte

rest

rate

s(%

pe

r ye

ar)

Households Corporate Total

Shar

e in

th

e t

ota

l cre

dit

(by

size

of f

irm

s)

21%

14%

25%

9%

14%

19%

24%

29%

34%

39%

Aug-17 Aug-18 Aug-19 Aug-20 Aug-21

Cen

ten

as

7.8%

12.1%

6.7%

8.5%

22.2%

24.2%

63.3%

55.3%

Aug 19

Aug 21

Micro Small Medium Large

2018

2019

2020

2021

0

40

80

120

160

200

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

30

DOMESTIC ECONOMY

Corporate Credit

Source: B3. (*) until September 27th, 2021.

Spre

ads

Seco

nd

ary

Mar

ket

(%

)

Da

ily v

olu

me

Se

con

dar

y M

arke

t -

(BR

L B

illi

on

s)Accumulated Primary Emissions(BRL Billions)

Emissions Jan-Sep:2018: 119 bi2019: 137 bi2020: 74 bi

2021: 150.4 bi (*)

DOMESTIC ECONOMY Credit Market

0

1

1

2

2

3

3

4

4

5

5

Jan-18 Dec-18 Nov-19 Oct-20 Sep-21

Trading volume MM 60 (without CVRDA6) MM 60

1.51.6

0

1

2

3

4

jan-20 mai-20 set-20 jan-21 mai-21 set-21

AA-A

B-C-D

31

General Government Gross Debt (GGGD)

Source: STN, BCB

Economic ActivityDOMESTIC ECONOMY Fiscal

GGGD/GDP 2021 forecast(Focus median)

%

GGGD/GDP 2021 Focus forecast* (disaggregated)

%

Updated to 10/01/21

* Approximate decomposition of the Focus median forecast evolution for GGGD/GDP. Each variable median isconsidered separately. GDB deflator constructed from Focus CPI forecast. Interest expenditure implicitly calculated

from primary and nominal fiscal results forecast. “Others” are residuals (approximations, methodological compatibility,etc.).

Nov 3rd 2020 Forecast Real GDP

denominatorDenominator

deflator

Primary deficit

reduction forecast

Interests expenditure

increase forecast

OthersSep 19th 2021

Forecast

95.8

-2.3

-6.7

-4.0

1.3

-2.1

82.0

81

83

85

87

89

91

93

95

97

nov-20 jan-21 mar-21 mai-21 jul-21 set-21

9495

100

74

89

82

8382

70

75

80

85

90

95

100

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

20/11/20 1/10/21

32

General Government Gross Debt (GGGD)

Source: BCB (Focus report) – Updated to 10/01/21.

Economic ActivityDOMESTIC ECONOMY Fiscal

%

November 2020 Current

Evolution of GGGD/GDP forecast(median of market analysts forecast – Focus)

33

BCB’s S&E responsabilityRegulationSupervisionPartnerships

Financial education

Rural creditHousing creditRelationship with CongressTransparency of Monetary PolicyCommunication plan for BCB actionsRelationship with foreign investorsDigital Citizenship

InnovationMarket efficiencyInternational reserves

Cooperative creditMicrocreditCurrency convertibilityInitiatives for capital market

34

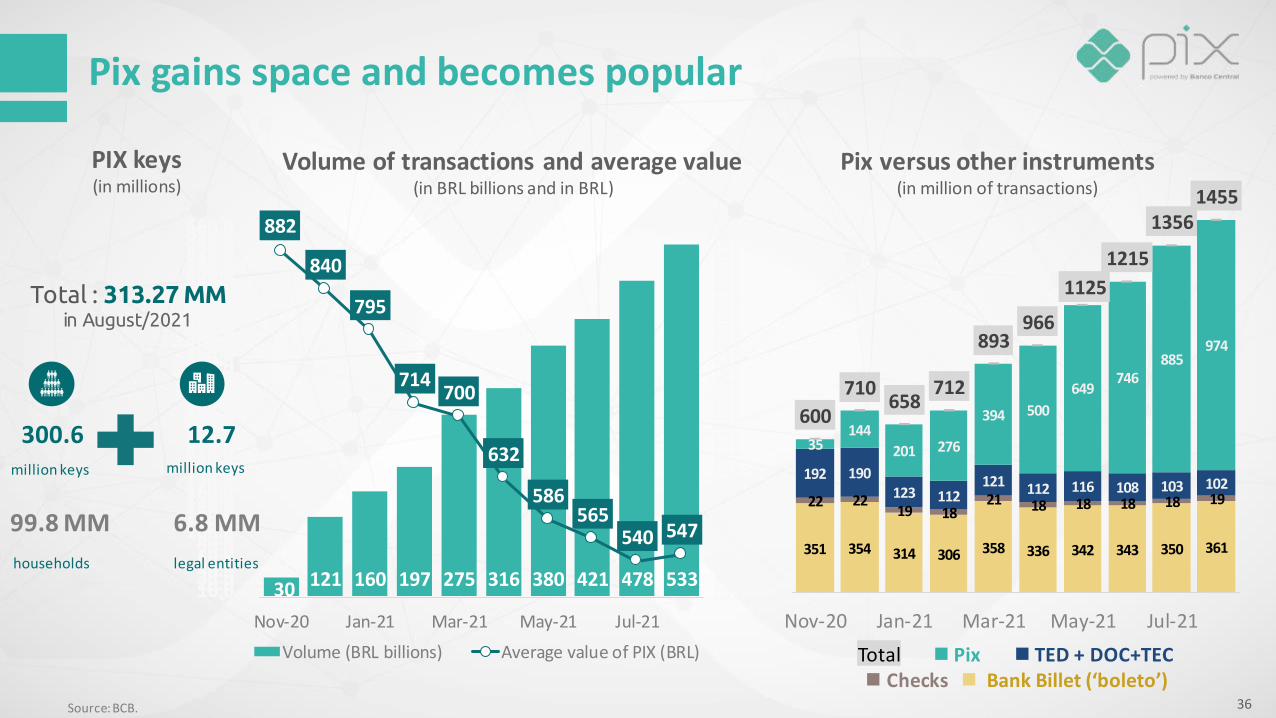

TechnologyAgenda

30 121 160 197 275 316 380 421 478 533

882

840

795

714700

632

586565

540 547

500.0510.0520.0530.0540.0550.0560.0570.0580.0590.0600.0610.0620.0630.0640.0650.0660.0670.0680.0690.0700.0710.0720.0730.0740.0750.0760.0770.0780.0790.0800.0810.0820.0830.0840.0850.0860.0870.0880.0890.0900.0910.0

- 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 190.0 200.0 210.0 220.0 230.0 240.0 250.0 260.0 270.0 280.0 290.0 300.0 310.0 320.0 330.0 340.0 350.0 360.0 370.0 380.0 390.0 400.0 410.0 420.0 430.0 440.0 450.0 460.0 470.0 480.0 490.0 500.0 510.0 520.0 530.0 540.0 550.0 560.0

Nov-20 Jan-21 Mar-21 May-21 Jul-21

Volume (BRL billions) Average value of PIX (BRL)

351 354 314 306 358 336 342 343 350 361

22 2219 18

21 18 18 18 18 19

192 190123 112

121 112 116 108 103 102

35144

201 276

394 500

649746

885974

600

710658

712

893966

1125

1215

13561455

Nov-20 Jan-21 Mar-21 May-21 Jul-21

Pix gains space and becomes popular

36Source: BCB.

households

million keys

Total : 313.27 MMin August/2021

PIX keys(in millions)

99.8 MM

300.6

6.8 MM

12.7

legal entities

Volume of transactions and average value(in BRL billions and in BRL)

Pix versus other instruments(in million of transactions)

Total ◼ Pix ◼ TED + DOC+TEC ◼ Checks ◼ Bank Billet (‘boleto’)

million keys

Pix: Evolution Agenda

3rd quarter 2022

4th quarter

Pix Saque (cash

withdrawal) and Pix Troco (cashback)

Payment Initiation Service Provider –PISP**

Special Return Mechanism(for fraud or operational error)

New ways to initiate• Payer QR Code Technology• Enable contactless transactions• Enable offline payments

Pix Cobrança• Additional Feature Set• Structural Improvements

Direct Debit***

Scheduled guaranteed transactions***

Pix for cross-border payments

[...]

*became mandatory **linked to Open Finance ***Publication of Operating Rules by BCB, Go Live to be defined

Future Agenda

Pix Cobrança

(invoice payments for payments with due date)

2nd quarter

Scheduled payments*

AGENDA BC#

Open Finance

• Implementation will be gradual

Goals: • To promote competition,

efficiency and data safety

• Proper balanced conditions between existing financial institutions and new players

Solutions that can be developed from Open Finance:

Devices to compare services and fees

Apps for financial advice and planning

Payment initiation in social medias

Credit marketplace

• Proposal:

▪ Establishing a modern, compact, and safe legal framework for FX market.

• Objectives:

▪ Simplify the FX legislation and improve the business environment in Brazil.

▪ Ease the connections with payment systems of other countries.

Modernization of exchange rate legislationAGENDA BC#

40

AGENDA BC#

Regulatory Sandbox

BCB’s Regulatory Sandbox starts in 2021 with the Cycle 1.

During the sandbox licensing process, BCB will assess whether the submitted projects comply with the definition of innovative project and whether their development is under the regulatory scope of BCB and CMN, among other criteria.

Legal persons, notary and registration service providers, public companies, and semi-public companies can participate, even when not yet fully licensed by BCB.

Simplified monitoring procedures will be adopted, considering the complexity and risks associated to each innovative project and, should BCB deems appropriate, additional limits and criteria may be applied.

By the end of cycle 1, participants may obtain a permanent license from BCB to operate. The projects may be a stepping stone for the improvement of the regulation issued by BCB and CMN.

TO UNDERSTAND THE REGULATORY SANDBOX

41

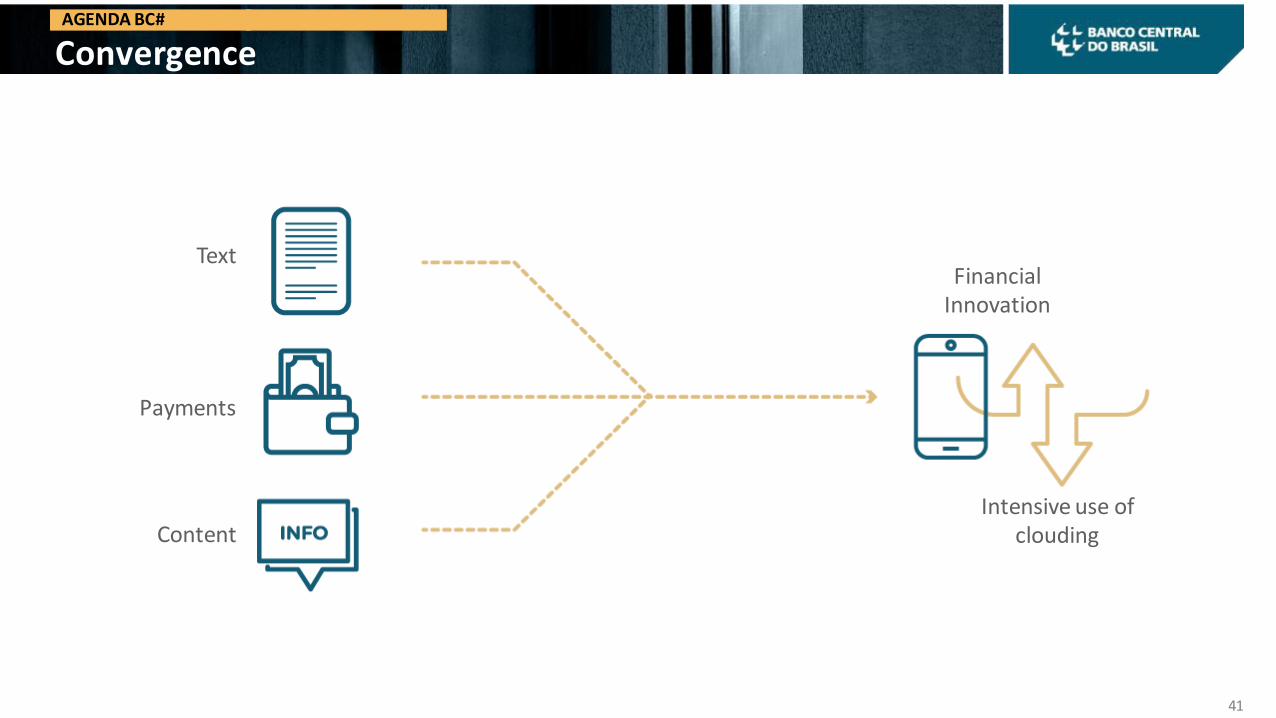

Convergence

Financial Innovation

Intensive use of clouding

Payments

Content

Text

AGENDA BC#

42

Innovation in the financial system

• Simplification• Internationalization• Convertibility

Digital currencyOpen Finance

Innovation in the currency

AGENDA BC#

A CBDC for Brazil:

The Digital Real

Guidelines:

• Extension of the Brazilian real

• Retail payments

• Innovative models development

• Not be interest-bearing

• Guarantee of legal certainty

• Data privacy and security

• Preventing and combating money laundering

• Interoperability and integration

• High cyber security

bcb.gov.br

SustainabilityMeasures:

• BCB’s S&E Responsibility

• Partnerships

• Policies

• Supervision

• Regulation

Common factors in recoveryMore sustainable and more inclusive growth

More technologyThe epidemic has accelerated technological change

in medicine, education, finance, communication

Low interest rates and high liquidity in the world

There are challenges, but also opportunities to reinvent the economy with private resources

Changes in global value chains

World trade

Vision for the future

Impact of possible reflation global conditions on EMEs

bcb.gov.br

Thank you!Roberto Campos Neto

Governor of Banco Central do BrasilOctober 15, 2021

Related Documents