| | Local Wind Industry- Opportunities & Challenges Gökhan Serdar– CFO - EMEA Region 13 November 2018 Company Presentation 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

| |

Local Wind Industry- Opportunities & Challenges

Gökhan Serdar– CFO - EMEA Region

13 November 2018Company Presentation 1

| |

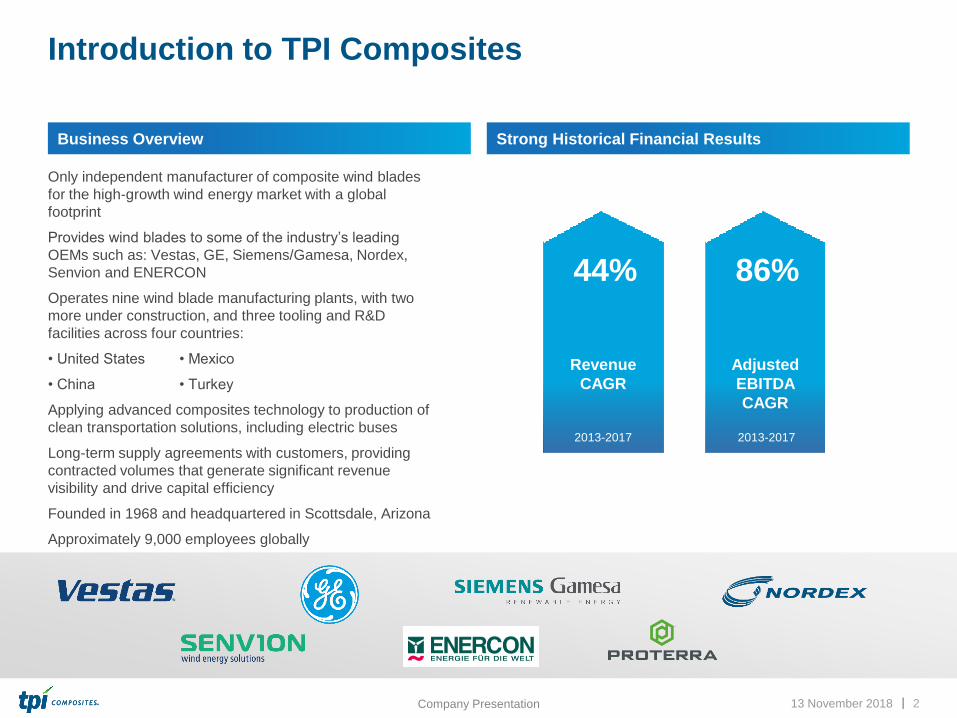

Introduction to TPI Composites

Only independent manufacturer of composite wind blades

for the high-growth wind energy market with a global

footprint

Provides wind blades to some of the industry’s leading

OEMs such as: Vestas, GE, Siemens/Gamesa, Nordex,

Senvion and ENERCON

Operates nine wind blade manufacturing plants, with two

more under construction, and three tooling and R&D

facilities across four countries:

• United States • Mexico

• China • Turkey

Applying advanced composites technology to production of

clean transportation solutions, including electric buses

Long-term supply agreements with customers, providing

contracted volumes that generate significant revenue

visibility and drive capital efficiency

Founded in 1968 and headquartered in Scottsdale, Arizona

Approximately 9,000 employees globally

13 November 2018 2Company Presentation

Business Overview Strong Historical Financial Results

Revenue

CAGR

44%

2013-2017

Adjusted

EBITDA

CAGR

86%

2013-2017

| |

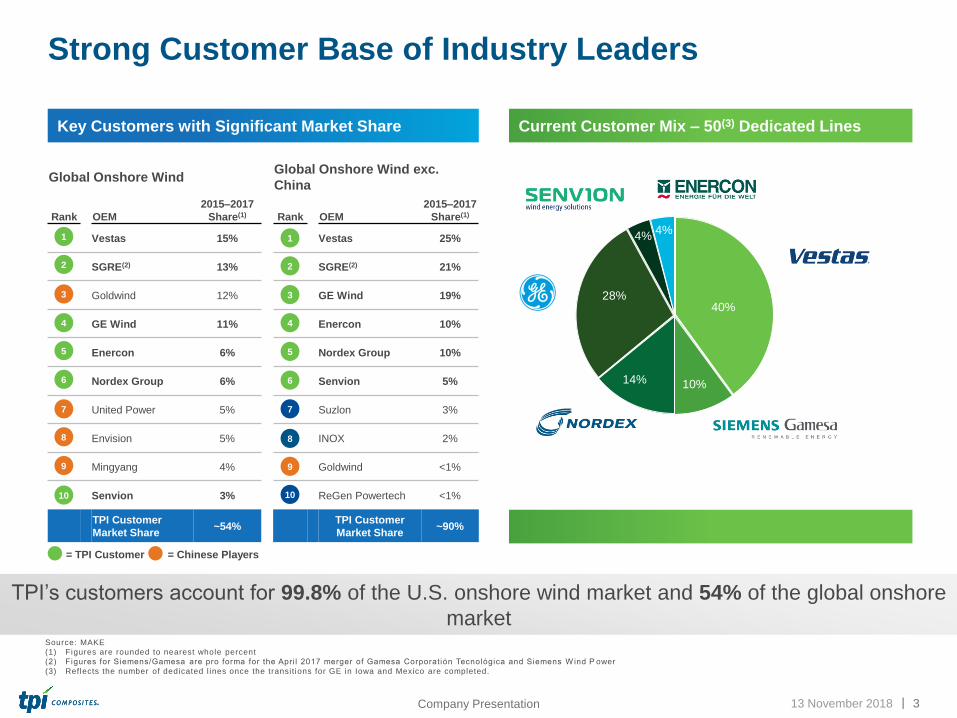

TPI’s customers account for 99.8% of the U.S. onshore wind market and 54% of the global onshore

market

Current Customer Mix – 50(3) Dedicated Lines

3Company Presentation

= TPI Customer

Global Onshore Wind Global Onshore Wind exc.

China

Rank OEM

2015–2017

Share(1) Rank OEM

2015–2017

Share(1)

1 Vestas 15% Vestas 25%

2 SGRE(2) 13% SGRE(2) 21%

3 Goldwind 12% GE Wind 19%

4 GE Wind 11% Enercon 10%

5 Enercon 6% Nordex Group 10%

6 Nordex Group 6% Senvion 5%

7 United Power 5% Suzlon 3%

8 Envision 5% INOX 2%

9 Mingyang 4% Goldwind <1%

Senvion 3% ReGen Powertech <1%

TPI Customer

Market Share ~54%

TPI Customer

Market Share~90%

1

2

4

5

7

3

6

8

9

= Chinese Players

1

2

5

6

3

4

9

7

8

10

Source: MAKE

(1) Figures are rounded to nearest whole percent

(2) Figures for Siemens/Gamesa are pro forma for the Apri l 2017 merger of Gamesa Corporatión Tecnológica and Siemens W ind P ower

(3) Reflects the number of dedicated l ines once the transi tions for GE in Iowa and Mexico are completed.

40%

10%14%

28%

4%4%

Key Customers with Significant Market Share

10

Strong Customer Base of Industry Leaders

13 November 2018

| | September 2018 4Company Presentation

The Industry is Shifting to a Predominantly Outsourced Wind Blade

Manufacturing Model

(1) Source: MAKE – based on % of MW

(2) TPI’s market share based on TPI MW relative to MAKE OEM total onshore MW for 2013, 2016 and 2017

38%51%

62%49%

0%

20%

40%

60%

80%

100%

2009 2017

Outsourced Insourced

Vertically integrated OEMs have begun to outsource wind blade

manufacturing due to:

• global talent constraints

• the need for efficient capital allocation

• the need to accelerate access to emerging markets

• the need for supply chain optimization

Some have sold or shuttered in-house tower and blade manufacturing

facilities in favor of an outsourced manufacturer

Geographically distributed, high precision blade manufacturing is more cost

effective when performed by diversified, specialized manufacturers

TPI is the only independent manufacturer of composite wind blades with a

global footprint and is well positioned to capitalize on global industry trends

Expected to continue to outsource a significant

percentage of blade needs notwithstanding

acquisition of LM Wind Power

TPI selected as manufacturer of Vestas-

designed blades in China, Mexico and Turkey

Currently outsources to TPI in Mexico and

Turkey

3%

9%

13%

2013 2016 2017

TPI Share Increase:

~4X

Future market share increases

expected to be driven by:

✓ Continuation of

outsourcing

✓ LM Wind Power customer

attrition

✓ Advantages from global

footprint

Several of the wind industry’s largest participants have chosen TPI as their leading outsourced blade manufacturer

Outsourcing Trends Global Wind Blade Manufacturing: Outsourced vs. Insourced (1)

TPI Global Wind Blade Market Share 2013 – 2017 (2)

| | TPI CONFIDENTIAL

TPI TR Mile Stones

13 November 2018

2012 2013 2014 2015 2016 2017

◼ Joint venture with AL-KE◼ Signed agreement with 1st

customer (GE for 48,7)◼ TK 1 Hall A construction◼ First blade is delivered

◼ ISO 9001 certificated◼ New blade model

introduction (GE-50,2)

◼ 1000. GE blade is produced.◼ Groundbreaking for TK2

◼ TK2 production started◼ Signed agreement with 3rd

customer (Vestas for V126)◼ 1000. NX blade is produced

◼ TK 1 Hall B construction◼ Signed agreement with 2nd

customer (NX for 58,5)

◼ IMS certification(ISO9001&14001&18001)

◼ New blade model introduction (NX –65.5)

◼ GE production finished◼ Signed agreement with 4th customer

SGRE (G132)

2 Molds

5 Molds

6 Molds

6 Molds

8 Molds

8 Molds

Headcount:375 Headcount:1099 Headcount:1586

Headcount:539 Headcount:1312 Headcount:1637

2018

◼ New blade model introduction (V136)

◼ SA extended for 2nd mold with SGRE

◼ IMS recertification done◼ Signed agreement with 5th

customer Enercon

13 Molds

Headcount:2750

5

| | TPI CONFIDENTIAL 13 November 2018

TR Plant Key Data – TK1 and TK2

6

| | TPI CONFIDENTIAL

Turkey Blade Shipments

November 13, 2018

CANADA

IRELAND

SCOTLAND

ENGLAND

SWEDEN

FINLAND

POLAND ROMANIA

CROATIA

MONTENEGRO

GERMANY

FRANCE

ITALY

TURKEY

AUSTRALIA

URUGUAY

SOUTH AFRICA

US

| | TPI CONFIDENTIAL

Opportunities/ Challenges

Opportunities

• Turkey as the Hub in EMEA for Component Manufacturing

• Potential in Growth in Turkish Wind Market- 1 GW/ Year in Next 10 years

• Continuity of YEKA’s

• Local Sub-Supplier Development in Turkey- Anchor Investment

• Human Capital in Turkey

Challenges

• Uncertainty about Local Component Support Beyond 2020

• Licenses Won with Negative Prices

• Current Financial Outlook- Financing Challenges

• Country Risk Perception

• Competitiveness

813 November 2018

| |

Related Documents