Consulting Retirement GM Pension Settlement Actions And Considerations for Plan Sponsors June 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Consulting Retirement

GM Pension Settlement Actions

And Considerations for Plan Sponsors

June 2012

Aon Hewitt 1

On June 1, 2012, General Motors Co. (GM) announced a program that will settle approximately $26 billion in pension liabilities for salaried retirees and beneficiaries by the end of 2012. This announcement follows a recent pension settlement announcement by Ford Motor Company, in which they outlined plans to offer lump sum payments to approximately 90,000 retirees, beneficiaries, and deferred vested participants.

This document includes an overview of GM’s June 1 announcement, as well as a comparison of GM’s pension settlement actions to Ford’s. We have also included information on the pension settlement actions contemplated by other plan sponsors during 2012 and Aon Hewitt commentary on considerations associated with pension settlement strategies.

All information summarized in this document relative to the GM and Ford pension settlement programs is based on publicly available information.

“Just the Facts” About GM’s Pension Settlement Program The reduction in GM’s pension obligation will be accomplished through a combination of (1) offering lump sums to 42,000 of the 118,000 impacted salaried retirees and beneficiaries and (2) purchasing annuities from The Prudential Insurance Company of America for those retirees and beneficiaries who do not elect the lump sum or were not eligible for the lump sum offer.

GM expects to issue lump sum payments to electing retirees in 2012.

Eligible retirees will be able to choose from up to three alternative payment forms. In addition to maintaining their existing benefit, or receiving their entire benefit in a single lump sum payment, some eligible retirees will be able to change their current annuity payment form from single life to joint & survivor or from joint & survivor to single life.

GM will create a new plan for salaried active (and, presumably, deferred vested) participants. Subsequently, they will voluntarily terminate the remaining salaried retiree and beneficiary plan and purchase annuities for the retirees and beneficiaries who did not receive a lump sum payment.

GM, in its press release, acknowledged the need for $3.5 to $4.5 billion in additional cash funding “to help fund the purchase of the group annuity contract and to improve the funded status of the pension plan for active salaried employees.” Further it disclosed special charges of $2.5 to $3.5 billion associated with the program, presumably for pension settlement accounting. An unfavorable impact to annual ongoing earnings of $200 million due to a decrease in pension income was also mentioned.

In the United States, the entire volume of pension liabilities annuitized in recent years has not exceeded $1 billion per year, and no single annuity transaction has exceeded $1 billion since the 1980s. By contrast, GM is expected to annuitize a significant portion of the $26 billion in this single transaction with Prudential.

Aon Hewitt 2

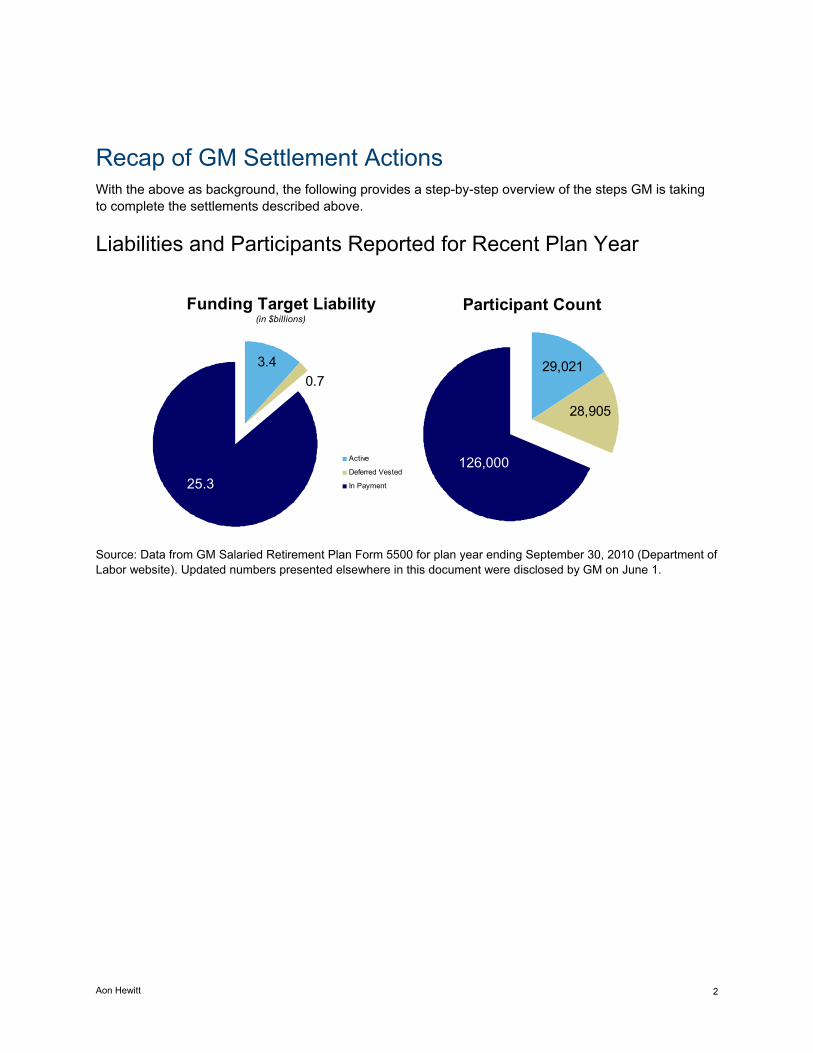

Recap of GM Settlement Actions With the above as background, the following provides a step-by-step overview of the steps GM is taking to complete the settlements described above.

Liabilities and Participants Reported for Recent Plan Year

Source: Data from GM Salaried Retirement Plan Form 5500 for plan year ending September 30, 2010 (Department of Labor website). Updated numbers presented elsewhere in this document were disclosed by GM on June 1.

Funding Target Liability(in $billions)

0.73.4

25 3

Active

Deferred Vested

In Payment

Participant Count

28,905

29,021

126,00025.3

126,000

Aon Hewitt 3

ActiveDeferred VestedRetirees—Not Lump Sum EligibleRetirees—Lump Sum Eligible

ActiveDeferred VestedRetirees to be Annuitized

Lump Sum Distributions

ActiveDeferred Vested

Lump Sum Distributions

Annuity Purchases

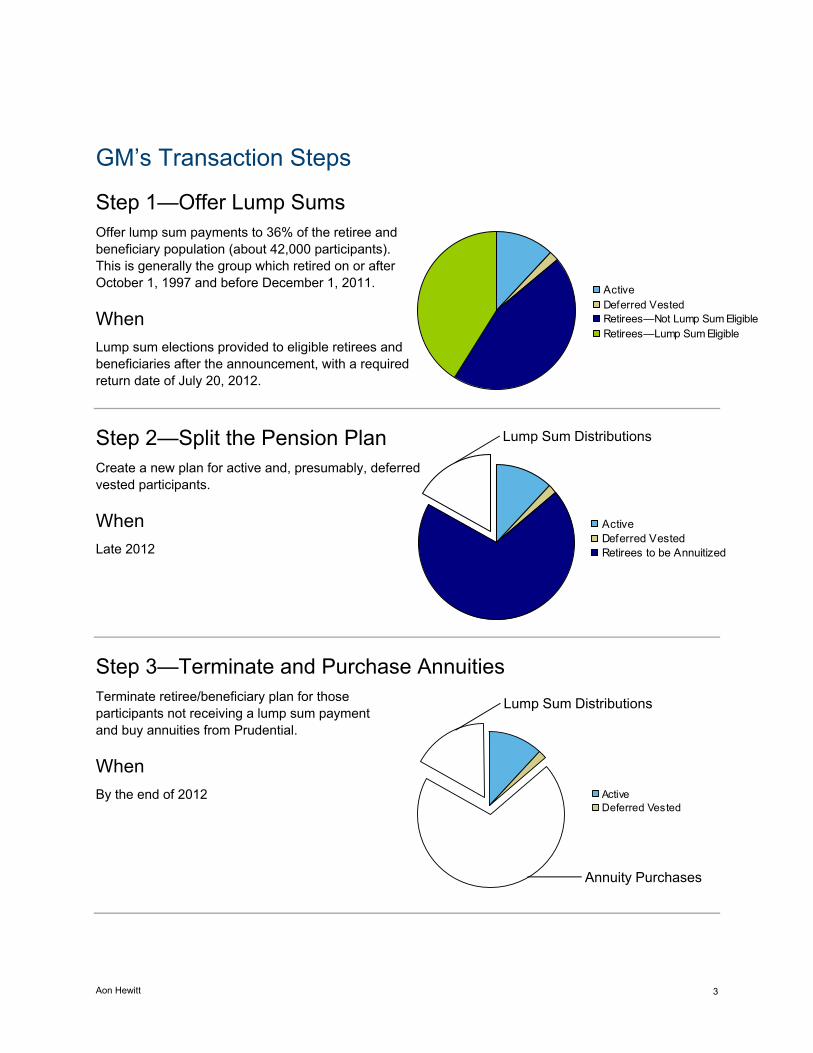

GM’s Transaction Steps

Step 1—Offer Lump Sums Offer lump sum payments to 36% of the retiree and beneficiary population (about 42,000 participants). This is generally the group which retired on or after October 1, 1997 and before December 1, 2011.

When Lump sum elections provided to eligible retirees and beneficiaries after the announcement, with a required return date of July 20, 2012.

Step 2—Split the Pension Plan Create a new plan for active and, presumably, deferred vested participants.

When Late 2012

Step 3—Terminate and Purchase Annuities Terminate retiree/beneficiary plan for those participants not receiving a lump sum payment and buy annuities from Prudential.

When By the end of 2012

Aon Hewitt 4

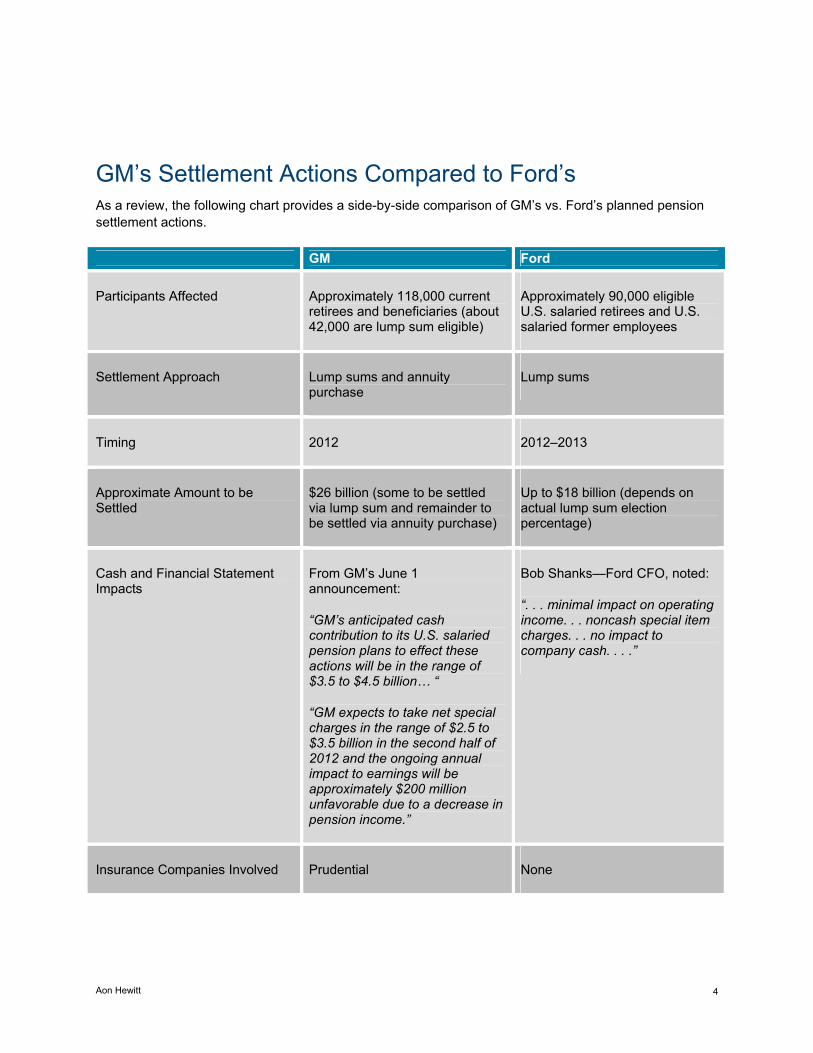

GM’s Settlement Actions Compared to Ford’s As a review, the following chart provides a side-by-side comparison of GM’s vs. Ford’s planned pension settlement actions.

GM Ford

Participants Affected Approximately 118,000 current retirees and beneficiaries (about 42,000 are lump sum eligible)

Approximately 90,000 eligible U.S. salaried retirees and U.S. salaried former employees

Settlement Approach Lump sums and annuity purchase

Lump sums

Timing 2012 2012–2013

Approximate Amount to be Settled

$26 billion (some to be settled via lump sum and remainder to be settled via annuity purchase)

Up to $18 billion (depends on actual lump sum election percentage)

Cash and Financial Statement Impacts

From GM’s June 1 announcement:

“GM’s anticipated cash contribution to its U.S. salaried pension plans to effect these actions will be in the range of $3.5 to $4.5 billion… “

“GM expects to take net special charges in the range of $2.5 to $3.5 billion in the second half of 2012 and the ongoing annual impact to earnings will be approximately $200 million unfavorable due to a decrease in pension income.”

Bob Shanks—Ford CFO, noted:

“. . . minimal impact on operating income. . . noncash special item charges. . . no impact to company cash. . . .”

Insurance Companies Involved Prudential None

Aon Hewitt 5

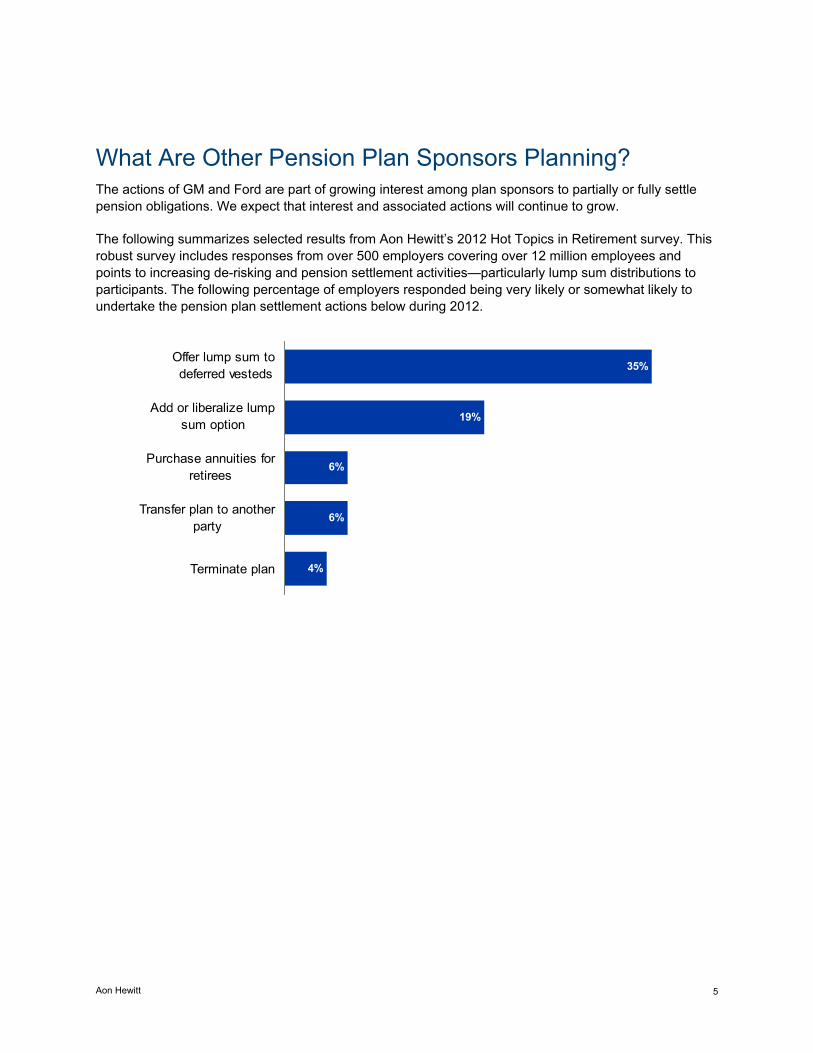

What Are Other Pension Plan Sponsors Planning? The actions of GM and Ford are part of growing interest among plan sponsors to partially or fully settle pension obligations. We expect that interest and associated actions will continue to grow.

The following summarizes selected results from Aon Hewitt’s 2012 Hot Topics in Retirement survey. This robust survey includes responses from over 500 employers covering over 12 million employees and points to increasing de-risking and pension settlement activities—particularly lump sum distributions to participants. The following percentage of employers responded being very likely or somewhat likely to undertake the pension plan settlement actions below during 2012.

35%

19%

6%

6%

4%

Offer lump sum to deferred vesteds

Add or liberalize lumpsum option

Purchase annuities forretirees

Transfer plan to anotherparty

Terminate plan

Aon Hewitt 6

Additional Considerations Associated with Pension Settlement Strategies As plan sponsors consider pension settlement strategies such as those recently announced by GM and Ford, it is important to study the various implications. The following is a brief discussion of issues for plan sponsors’ consideration.

Financial Issues

“Fully-Loaded” Liabilities As plan sponsors consider pension settlement options, it is important to first understand the level of fully-loaded pension liabilities. The additional costs to be recognized in this fully loaded scenario include mortality improvements, administrative and investment fees, PBGC premiums, anti-selection, and credit costs (i.e., the risk of default on fixed income investments). An understanding of these fully loaded costs, which can be more than 10% larger than the Projected Benefit Obligation (PBO) disclosed to investors, is critical when analyzing the range of pension settlement options available.

Anti-Selection Risk

This risk is real and represents the possibility that participant elections in lump sum offerings will ultimately increase plan sponsor costs as participants elect options more financially advantageous to themselves at the plan’s expense. Our analysis suggests that these anti-selection risks can increase costs by 5 to 15%, depending on the demographics of the affected population and the lump sum acceptance rate.

Asset Decisions and Allocations Before Settlement Actions Structuring a plan’s assets for settlement programs like those being undertaken by GM and Ford is one of the most complex strategic concerns, as the plan must generate liquidity for potentially billions of dollars of lump sum payments while simultaneously hedging significant interest rate exposure. This challenge can be exacerbated by under- or over-estimating the lump sum take rate. Additionally, the transfer of such a large premium to an insurance company typically requires a well-defined and complex portfolio of assets, known as an “in-kind” portfolio.

Low Interest Rates Today’s interest rates are at historically low levels, including 10-year U.S. Treasury yields currently around 1.50%. Many plan sponsors are reluctant to de-risk plan investments or settle pension obligations believing that interest rates will increase in the future. That said, many investors also believe that interest rates will be kept at low levels by the Federal Reserve, which announced in January 2012 that it planned to keep short-term interest rates near zero until at least 2014.

Aon Hewitt 7

If plan sponsors believe now isn’t the time to actively pursue plan settlement options due to low interest rates, we believe it is still worth preparing for future actions at this point. These preparations can include the development of triggers for plan investments and plan settlement options, an analytic structure which can be reviewed periodically by management to determine if plan settlement is a viable option, and data clean-up activities, including an effort to locate missing participants. Moreover, now is the time for plan fiduciaries to begin preparing for how they may approach any decision by the employer to provide for a lump sum window program, or to provide for annuity payments from a third-party insurer.

Settlement Accounting Many companies have expressed concerns about settlement accounting charges. These result from the immediate recognition of a portion of unrecognized losses (and gains) when plan liabilities are settled. These concerns over settlement charges have historically been voiced because of their impact on ongoing earnings levels, and resulting impacts on bonuses and other earnings-related rewards.

Countering these concerns over settlement accounting has been a trend toward mark-to-market pension accounting, which generally results in the immediate recognition of unrecognized losses as of some date, with regular and ongoing mark-to-market charges based on future plan experience. In a sense, settlement charges can be viewed as one-time, non-cash mark-to-market adjustments.

We are seeing fewer concerns with settlement charges by managers and investors as this mark-to-market pension accounting trend continues. In Ford’s investor call during which they discussed their pension settlement strategy, they noted that their actions result in “non-cash special item charges to profits.” Ford received no questions on settlement accounting from analysts during the call.

Participant Communications and Administration As plan sponsors consider various pension settlement options, including lump sum distributions, it is important to understand the various communications and administrative activities necessary to produce a positive outcome—for both participants and the company. First, there is a significant need for comprehensive and clear communications as retirees and other plan participants contemplate a major change in their financial futures. These communications need to be clear and concise, multi-channel (print communications, call centers, etc.), and unbiased. Working with retirees, as well as locating and effectively communicating with former employees (i.e., terminated vested participants) can take up to 10 times longer than supporting pension administration and related decisions for an ongoing “steady state” plan.

Aon Hewitt 8

In addition to these activities, the following lists the major administrative activities associated with significant pension settlement efforts like those being undertaken by GM and Ford.

Project management

Additional benefit calculations related to the lump sum offer

Data clean-up, including address and missing participant searches

IT support and necessary system changes

Production and fulfillment of decision and administrative support materials

Call centers

Paperwork processing

Access to unbiased financial advice

File preparation—for trustees, actuaries, and records

Plan Compliance and Settlor/Fiduciary Risk Management In order to mitigate the legal or regulatory risks associated with pursuing a pension settlement option, there are a number of decisions that will need to be made as the program is designed. Some of these are business decisions made by the employer, such as the decision to amend or terminate the plan. These are referred to as ‘settlor’ decisions. Fiduciary decisions, such as how the plan investments are to be managed, or which insurers offer the ‘safest available’ annuity, are made on behalf of plan participants.

From both a settlor and fiduciary perspective, careful planning and attention to tax, ERISA, fiduciary and plan governance requirements early on and throughout the process are necessary to minimize the risk of adverse claims or legal/regulatory findings. Among many others, the issues to be considered include:

The need for independent expertise and assistance in evaluating possible annuity providers and other settlement strategies;

Nondiscrimination testing requirements;

The potential need for a private letter ruling; and

Treatment of expenses—paid by general company or plan assets.

Copyright Aon 2012 9

Contact Information For more information, please contact:

Byron Beebe U.S. Retirement Consulting Market Leader [email protected] 216.573.9700

Rick Jones Leader of Retirement Consulting National Practices [email protected] 847.295.5000

About Aon Hewitt Aon Hewitt is the global leader in human capital consulting and outsourcing solutions. The company partners with organizations to solve their most complex benefits, talent and related financial challenges, and improve business performance. Aon Hewitt designs, implements, communicates and administers a wide range of human capital, retirement, investment management, health care, compensation and talent management strategies. With more than 29,000 professionals in 90 countries, Aon Hewitt makes the world a better place to work for clients and their employees. For more information on Aon Hewitt, please visit www.aonhewitt.com.

Related Documents