Gluskin Sheff + Associates Inc. Investing Past the Seventh-Inning Stretch David A. Rosenberg November 2017 Invested in your prosperity

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Gluskin Sheff + Associates Inc.

Investing Past the Seventh-Inning Stretch

David A. Rosenberg

November 2017

Invested in your prosperity

Gluskin Sheff + Associates Inc.

Notes:

Source: New York Post (March 10, 2016) 1

Gluskin Sheff + Associates Inc.

2

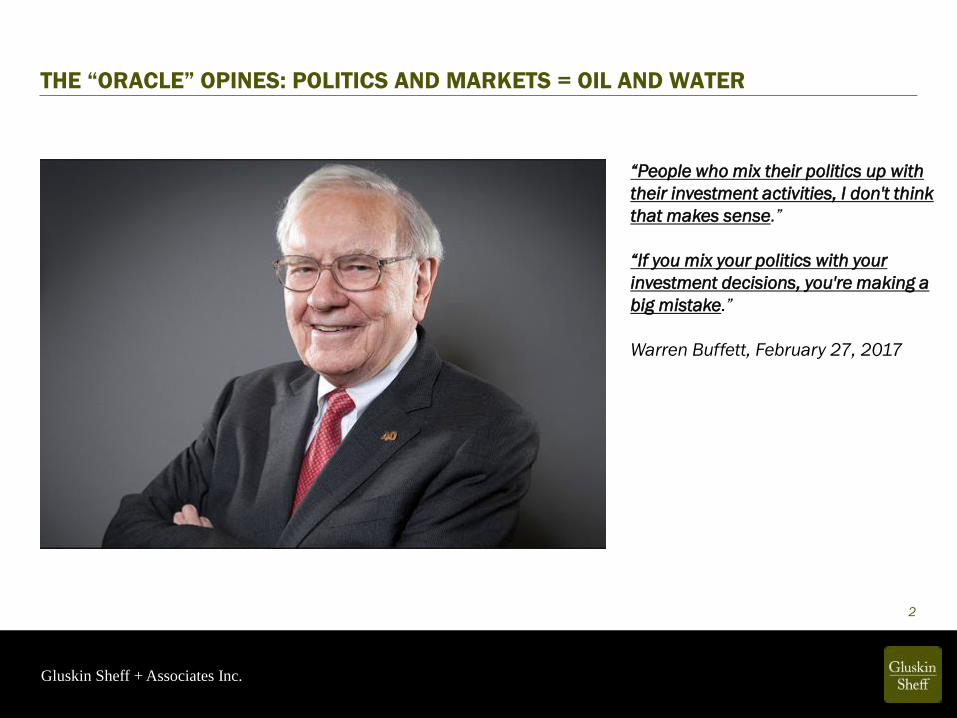

“People who mix their politics up with

their investment activities, I don't think

that makes sense.”

“If you mix your politics with your

investment decisions, you're making a

big mistake.”

Warren Buffett, February 27, 2017

THE “ORACLE” OPINES: POLITICS AND MARKETS = OIL AND WATER

Gluskin Sheff + Associates Inc.

3

WHAT YOU SEE ISN’T ALWAYS WHAT YOU GET

Election NarrativeWhat Actually

Happened

Ronald Reagan (1980-88)Deregulation, small government,

tax cuts, defense spending

Recession in first two years,

massive deficits, S&P 500 down

25% (the good stuff happened

later)

George H.W. Bush (1988-92)Extend the Reagan era (nothing

more)

Proposed tax hikes, Recession

within two years, one-term

president

Bill Clinton (1992-2000)Health care reform, socialist from

Arkansas

Eight-year expansion, stock market

tripled, deregulation, welfare reform

George W. Bush (2000-08)Deregulation, fiscal conservatism,

isolationism

Tax cuts, public spending, Iraq war,

35% stock market plunge

Barack Obama (2008-16)Health care reform, Main Street

over Wall Street, socialist from

Illinois

Obamacare, bank bailouts,

weakest recovery ever, record

income inequality, S&P 500 tripled

Gluskin Sheff + Associates Inc.

4Notes:

Source: Bloomberg Businessweek (February 6, 2017)

SO… HOW TO INVEST AROUND TRUMP? DON’T!!

Gluskin Sheff + Associates Inc.

5

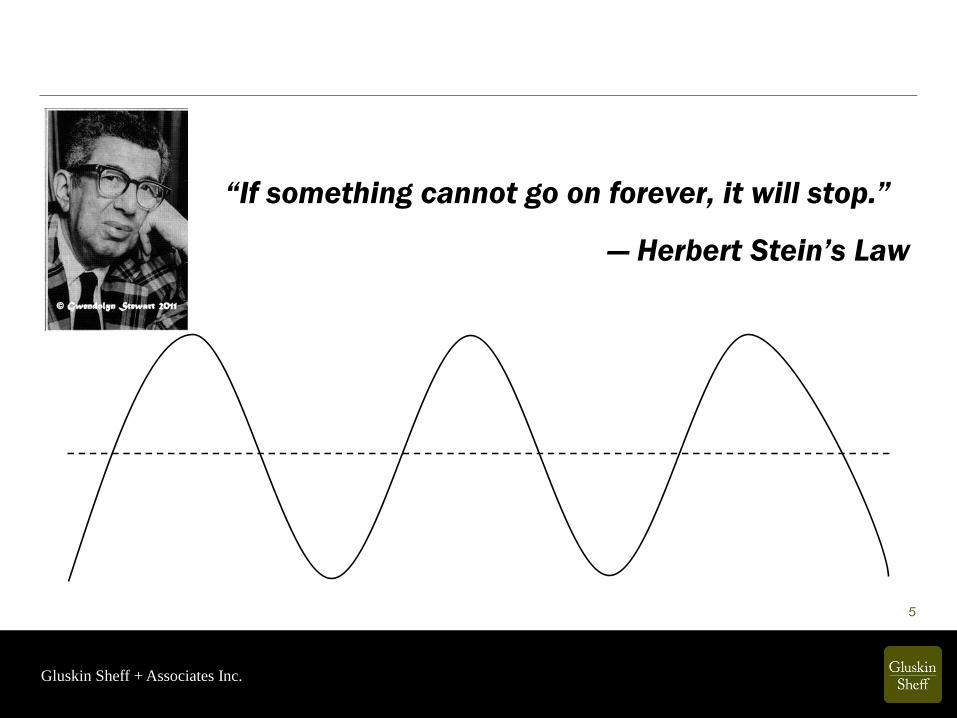

“If something cannot go on forever, it will stop.”

— Herbert Stein’s Law

Gluskin Sheff + Associates Inc.

(months)

6

Month of Economic Cycle Peak

Notes:

Source: National Bureau of Economic Research, Gluskin Sheff

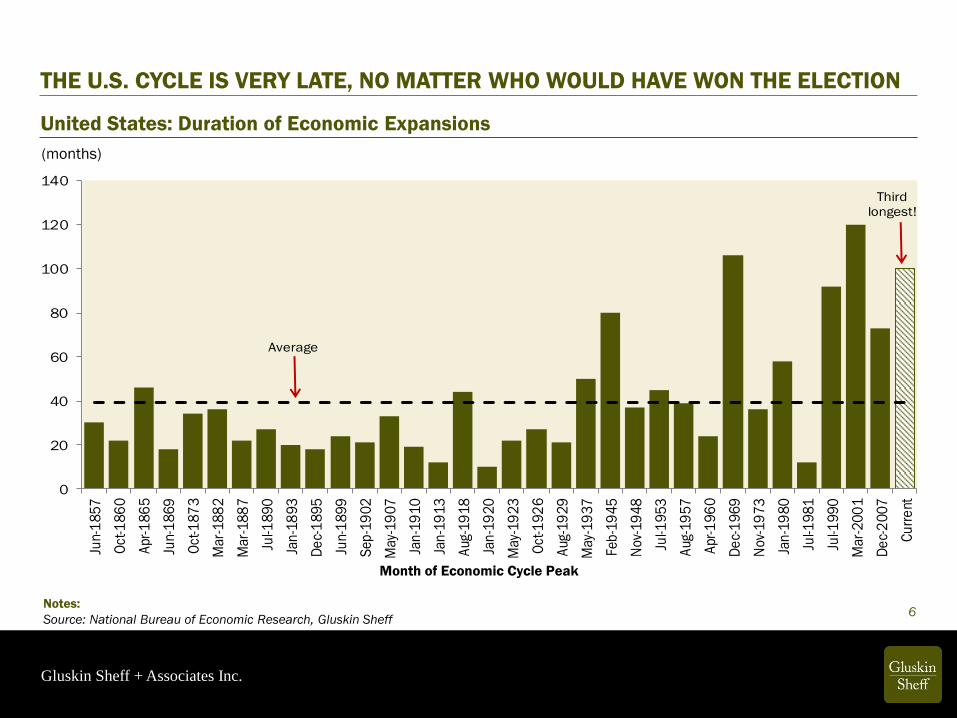

THE U.S. CYCLE IS VERY LATE, NO MATTER WHO WOULD HAVE WON THE ELECTION

United States: Duration of Economic Expansions

0

20

40

60

80

100

120

140

Jun

-18

57

Oct

-18

60

Ap

r-1

86

5

Jun

-18

69

Oct

-18

73

Ma

r-1

88

2

Ma

r-1

88

7

Jul-1

89

0

Jan

-18

93

De

c-1

89

5

Jun

-18

99

Sep

-19

02

Ma

y-1

90

7

Jan

-19

10

Jan

-19

13

Au

g-1

91

8

Jan

-19

20

Ma

y-1

92

3

Oct

-19

26

Au

g-1

92

9

Ma

y-1

93

7

Fe

b-1

94

5

No

v-1

94

8

Jul-1

95

3

Au

g-1

95

7

Apr

-19

60

De

c-1

96

9

No

v-1

97

3

Jan

-19

80

Jul-1

98

1

Jul-1

99

0

Ma

r-2

00

1

De

c-2

00

7

Cu

rre

nt

Third

longest!

Average

Gluskin Sheff + Associates Inc.

WHEN CONFIDENCE PEAKS — RECESSION A YEAR LATER!

United States: Consumer Confidence

(1985 = 100)

7

Notes:

Shaded regions represent periods of U.S. recession

Source: Haver Analytics, Gluskin Sheff

0

20

40

60

80

100

120

140

160

1967 1972 1977 1982 1987 1992 1997 2002 2007 2012 2017

peak

peakpeak

peak

peak

peak

peak

peak

Gluskin Sheff + Associates Inc.

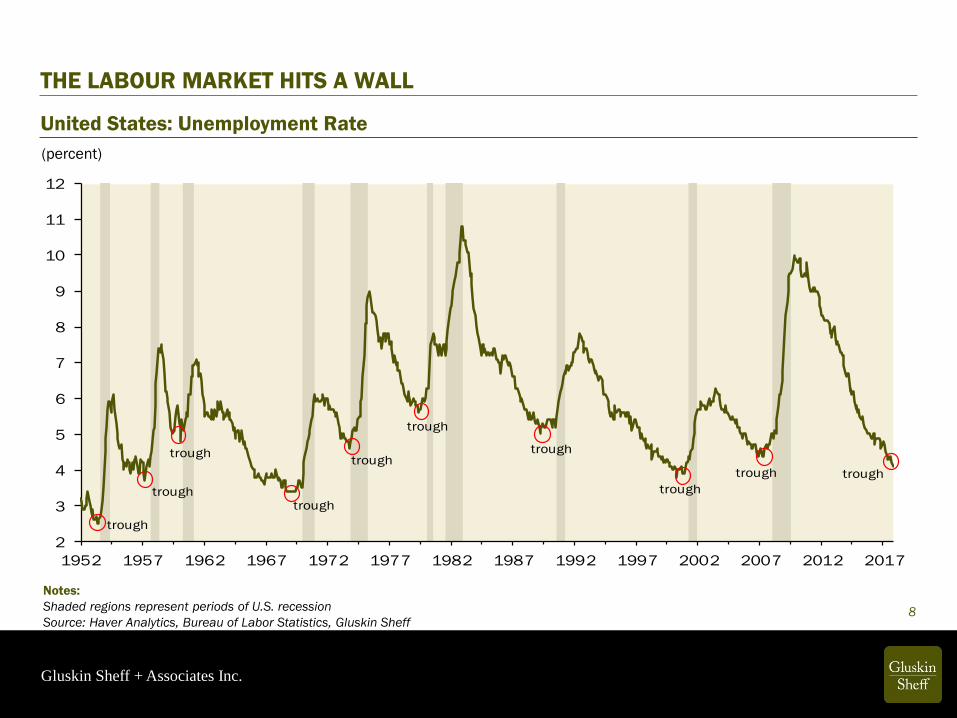

THE LABOUR MARKET HITS A WALL

United States: Unemployment Rate

(percent)

8

Notes:

Shaded regions represent periods of U.S. recession

Source: Haver Analytics, Bureau of Labor Statistics, Gluskin Sheff

2

3

4

5

6

7

8

9

10

11

12

1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012 2017

trough

trough

trough

trough

trough

trough

trough

trough

trough trough

Gluskin Sheff + Associates Inc.

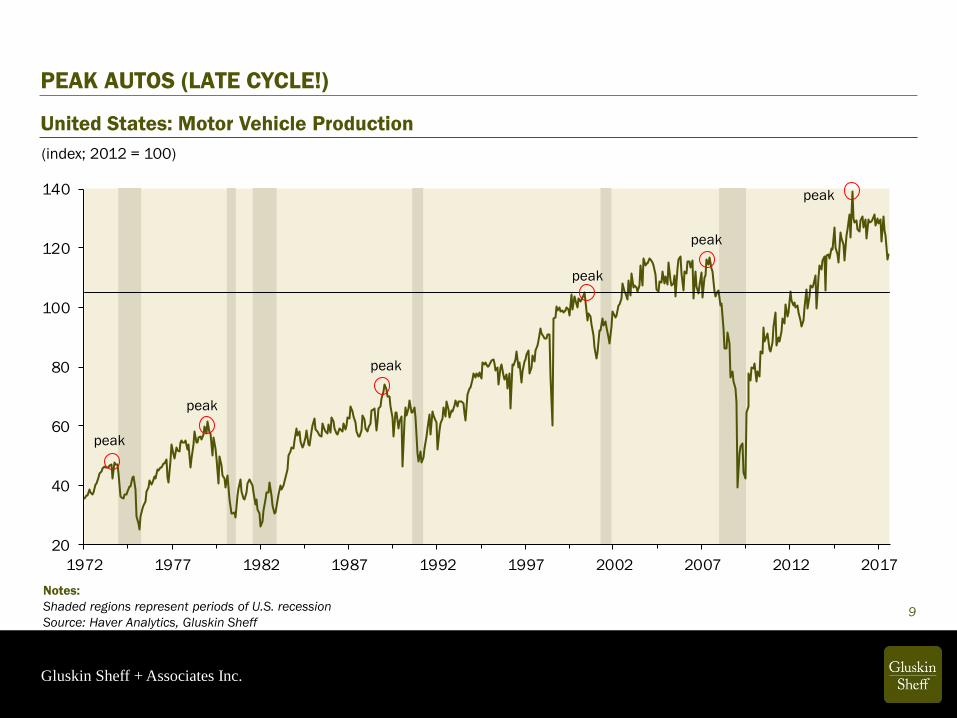

PEAK AUTOS (LATE CYCLE!)

United States: Motor Vehicle Production

(index; 2012 = 100)

9

Notes:

Shaded regions represent periods of U.S. recession

Source: Haver Analytics, Gluskin Sheff

20

40

60

80

100

120

140

1972 1977 1982 1987 1992 1997 2002 2007 2012 2017

peak

peak

peak

peak

peak

peak

Gluskin Sheff + Associates Inc.

PEAK HOUSING (LATE CYCLE!)

United States: Existing Home Sales

(millions of units)

10

Notes:

Shaded regions represent periods of U.S. recession

Source: Haver Analytics, Gluskin Sheff

1

2

3

4

5

6

7

1968 1973 1978 1983 1988 1993 1998 2003 2008 2013

peak

peak

peak

peak

peak

peakpeak

Gluskin Sheff + Associates Inc.

PEAK VALUATIONS

11

Notes:

Shaded regions represent periods of U.S. recession

Source: Haver Analytics, Gluskin Sheff

(ratio)

5x

10x

15x

20x

25x

30x

35x

40x

45x

50x

1979 1984 1989 1994 1999 2004 2009 2014

peak

peak

peak

peak

peak

peak?

United States: Cyclically Adjusted P/E Multiple

Gluskin Sheff + Associates Inc.

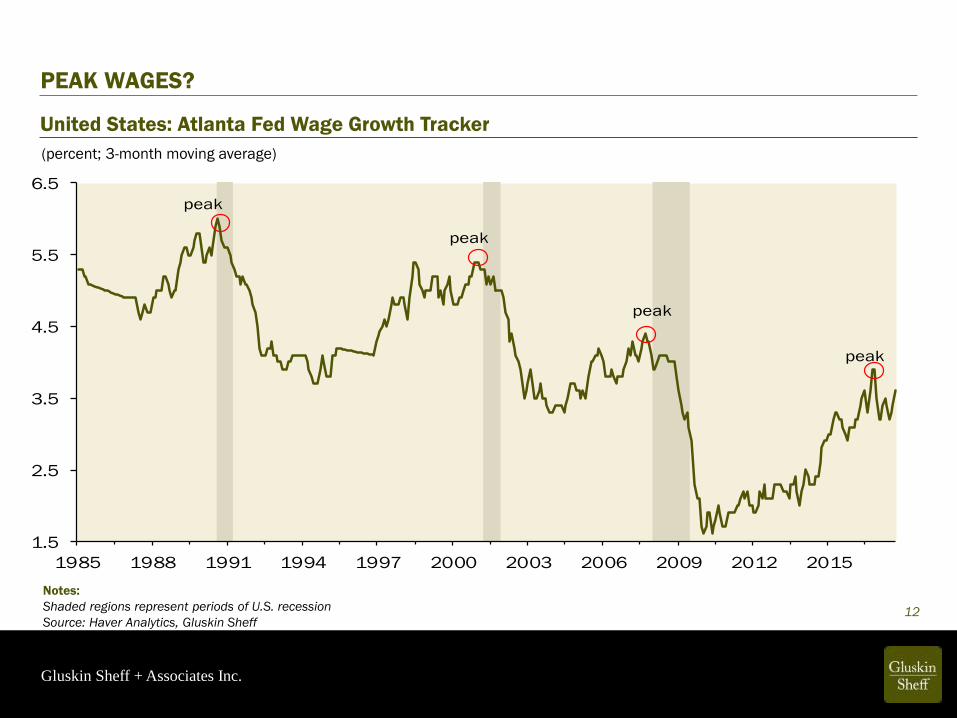

PEAK WAGES?

12

Notes:

Shaded regions represent periods of U.S. recession

Source: Haver Analytics, Gluskin Sheff

(percent; 3-month moving average)

United States: Atlanta Fed Wage Growth Tracker

1.5

2.5

3.5

4.5

5.5

6.5

1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

peak

peak

peak

peak

Gluskin Sheff + Associates Inc.

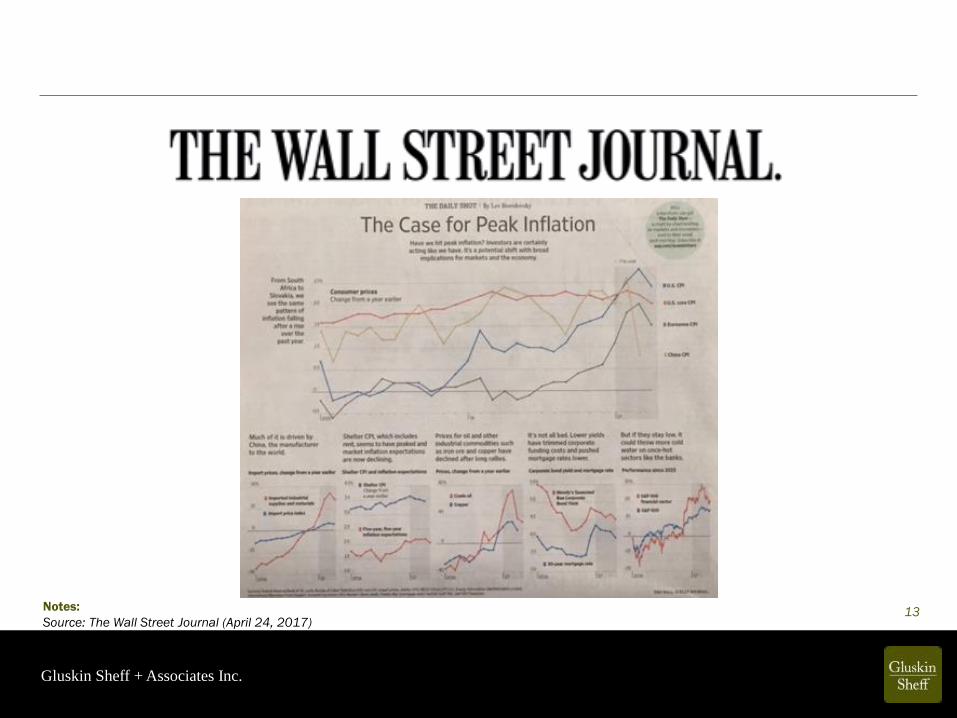

13Notes:

Source: The Wall Street Journal (April 24, 2017)

Gluskin Sheff + Associates Inc.

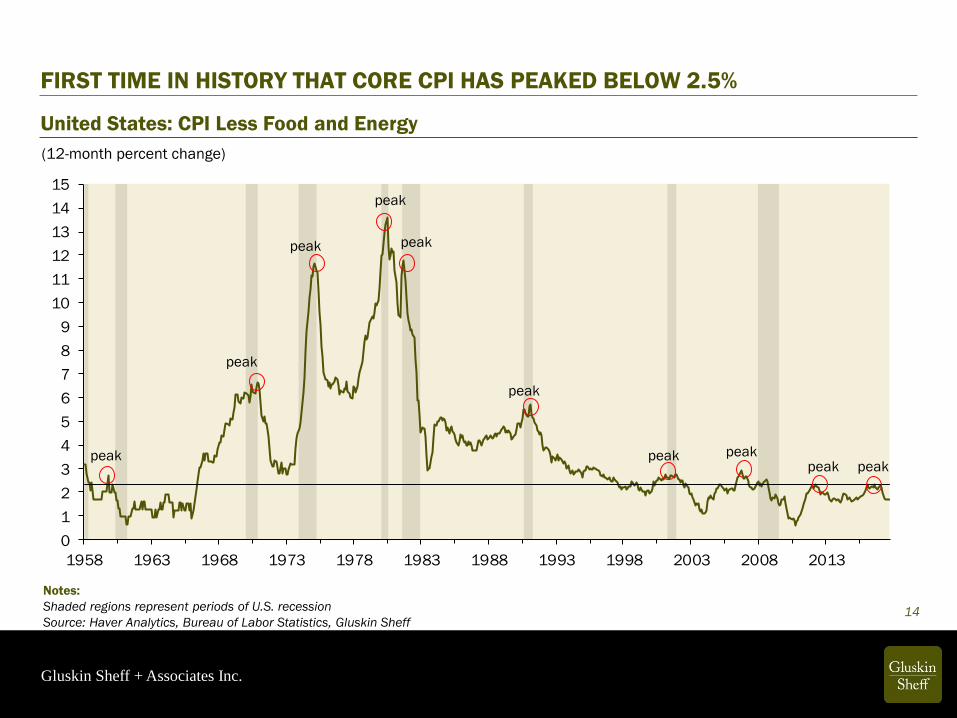

FIRST TIME IN HISTORY THAT CORE CPI HAS PEAKED BELOW 2.5%

United States: CPI Less Food and Energy

(12-month percent change)

14

Notes:

Shaded regions represent periods of U.S. recession

Source: Haver Analytics, Bureau of Labor Statistics, Gluskin Sheff

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

1958 1963 1968 1973 1978 1983 1988 1993 1998 2003 2008 2013

peak

peak

peak

peak peakpeak peak

peak

peak

peak

Gluskin Sheff + Associates Inc.

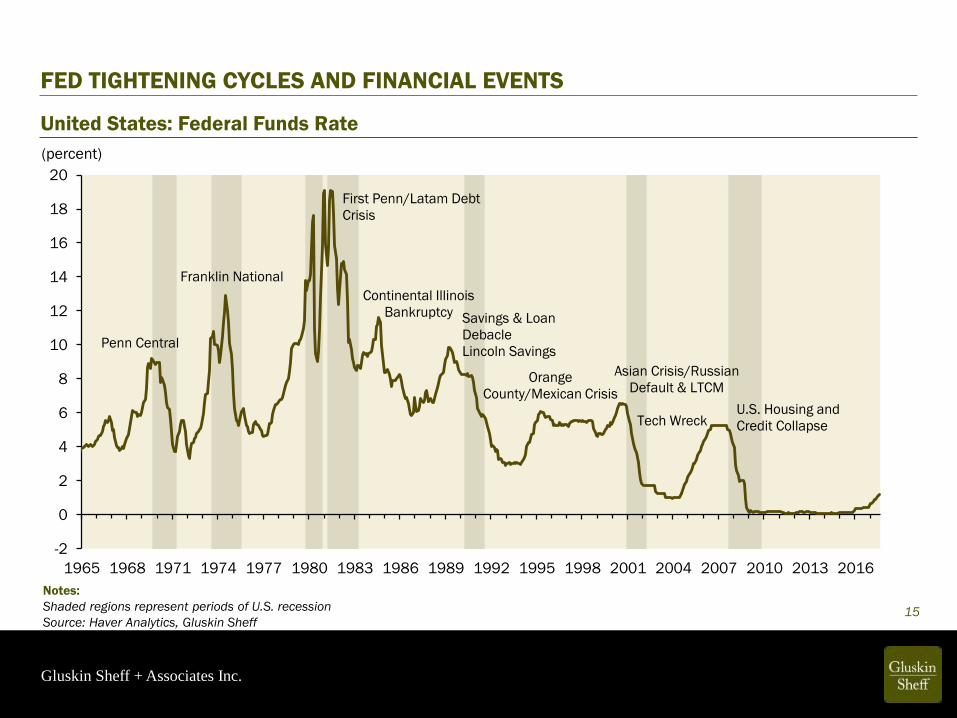

FED TIGHTENING CYCLES AND FINANCIAL EVENTS

15

Notes:

Shaded regions represent periods of U.S. recession

Source: Haver Analytics, Gluskin Sheff

(percent)

United States: Federal Funds Rate

-2

0

2

4

6

8

10

12

14

16

18

20

1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013 2016

First Penn/Latam Debt

Crisis

Asian Crisis/Russian

Default & LTCM

U.S. Housing and

Credit Collapse

Orange

County/Mexican Crisis

Penn Central

Continental Illinois

Bankruptcy

Franklin National

Savings & Loan

Debacle

Lincoln Savings

Tech Wreck

Gluskin Sheff + Associates Inc.

16

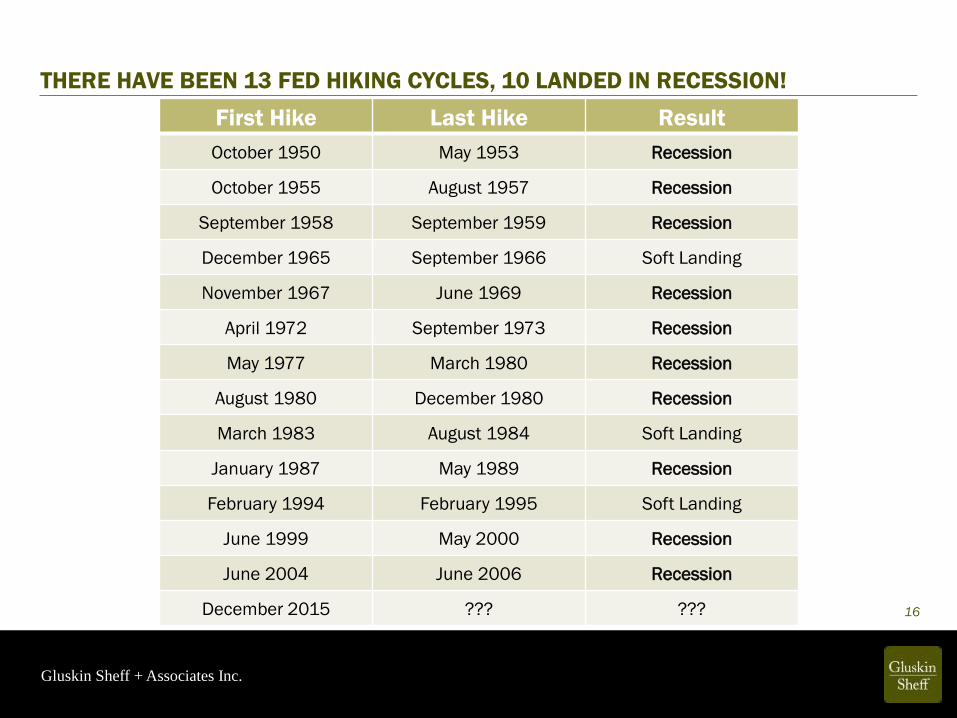

THERE HAVE BEEN 13 FED HIKING CYCLES, 10 LANDED IN RECESSION!

First Hike Last Hike Result

October 1950 May 1953 Recession

October 1955 August 1957 Recession

September 1958 September 1959 Recession

December 1965 September 1966 Soft Landing

November 1967 June 1969 Recession

April 1972 September 1973 Recession

May 1977 March 1980 Recession

August 1980 December 1980 Recession

March 1983 August 1984 Soft Landing

January 1987 May 1989 Recession

February 1994 February 1995 Soft Landing

June 1999 May 2000 Recession

June 2004 June 2006 Recession

December 2015 ??? ???

Gluskin Sheff + Associates Inc.

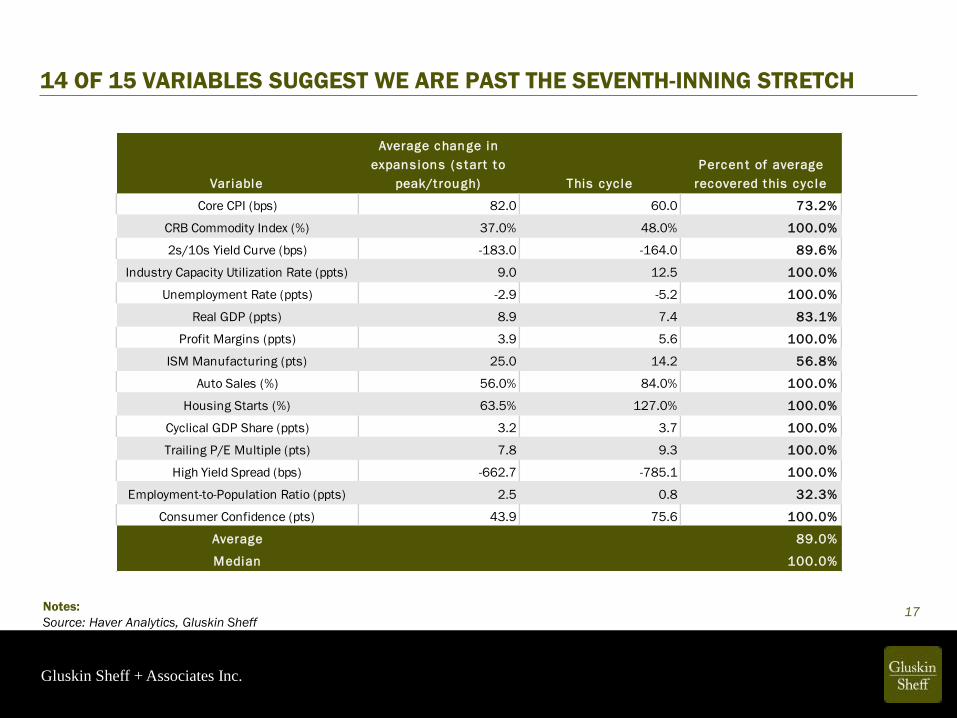

17Notes:

Source: Haver Analytics, Gluskin Sheff

Variable

Average change in

expans ions ( s tart to

peak/trough) This cyc le

Percent of average

recovered this cyc le

Core CPI (bps) 82.0 60.0 73.2%

CRB Commodity Index (%) 37.0% 48.0% 100.0%

2s/10s Yield Curve (bps) -183.0 -164.0 89.6%

Industry Capacity Utilization Rate (ppts) 9.0 12.5 100.0%

Unemployment Rate (ppts) -2.9 -5.2 100.0%

Real GDP (ppts) 8.9 7.4 83.1%

Profit Margins (ppts) 3.9 5.6 100.0%

ISM Manufacturing (pts) 25.0 14.2 56.8%

Auto Sales (%) 56.0% 84.0% 100.0%

Housing Starts (%) 63.5% 127.0% 100.0%

Cyclical GDP Share (ppts) 3.2 3.7 100.0%

Trailing P/E Multiple (pts) 7.8 9.3 100.0%

High Yield Spread (bps) -662.7 -785.1 100.0%

Employment-to-Population Ratio (ppts) 2.5 0.8 32.3%

Consumer Confidence (pts) 43.9 75.6 100.0%

Average 89.0%

Median 100.0%

14 OF 15 VARIABLES SUGGEST WE ARE PAST THE SEVENTH-INNING STRETCH

Gluskin Sheff + Associates Inc.

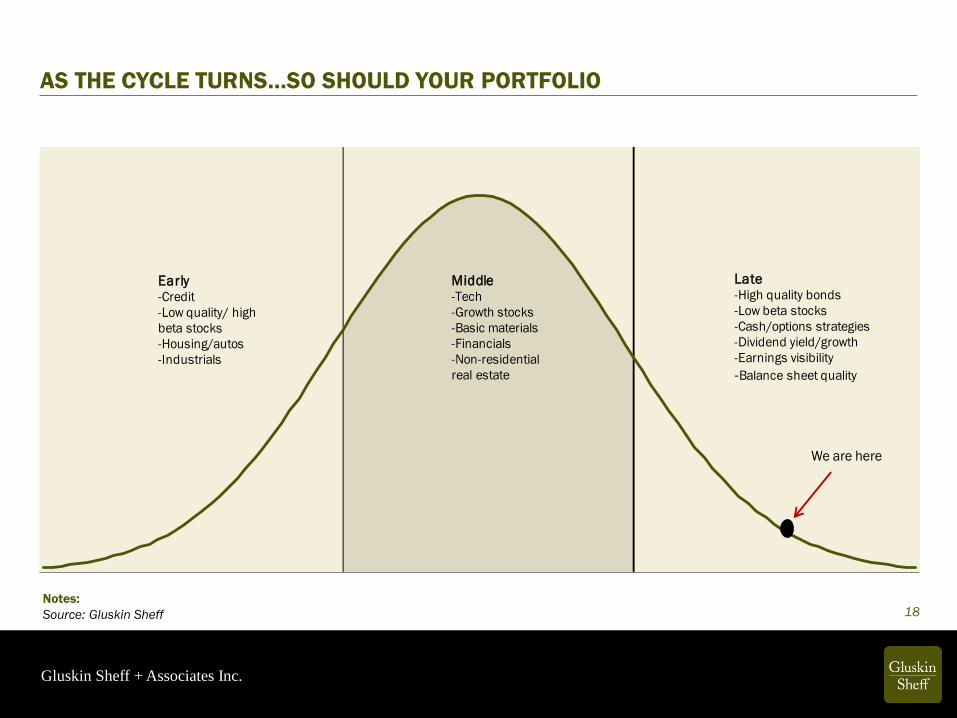

AS THE CYCLE TURNS…SO SHOULD YOUR PORTFOLIO

18

We are here

Early-Credit

-Low quality/ high

beta stocks

-Housing/autos

-Industrials

Middle-Tech

-Growth stocks

-Basic materials

-Financials

-Non-residential

real estate

Late-High quality bonds

-Low beta stocks

-Cash/options strategies

-Dividend yield/growth

-Earnings visibility

-Balance sheet quality

Notes:

Source: Gluskin Sheff

Gluskin Sheff + Associates Inc.

19

IT’S A BIG WORLD OUT THERE

Gluskin Sheff + Associates Inc.

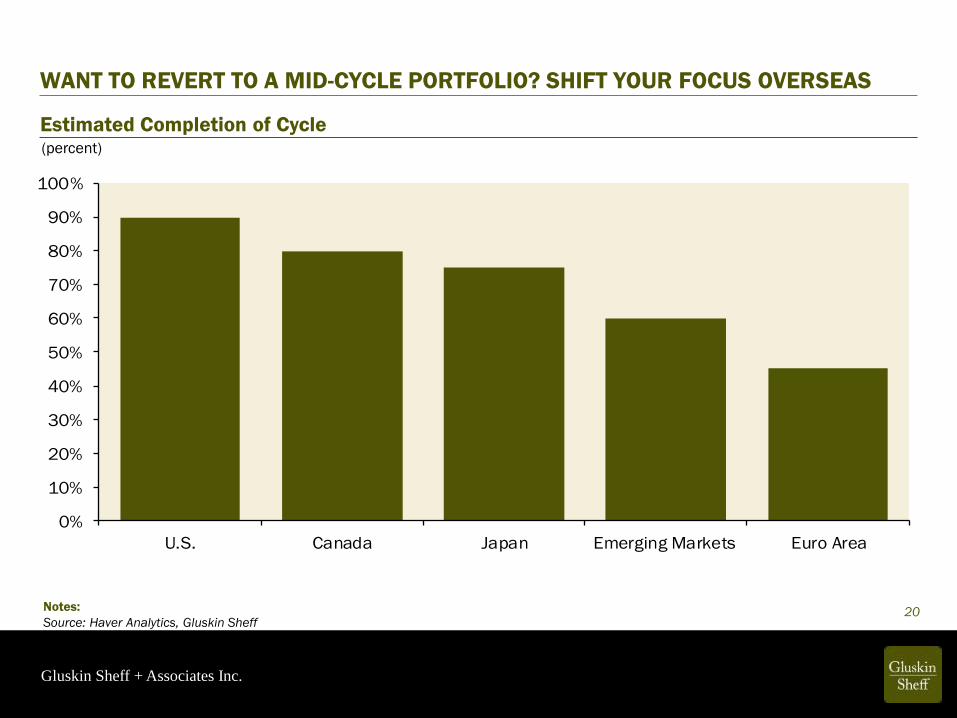

WANT TO REVERT TO A MID-CYCLE PORTFOLIO? SHIFT YOUR FOCUS OVERSEAS

Estimated Completion of Cycle

20Notes:

Source: Haver Analytics, Gluskin Sheff

(percent)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

U.S. Canada Japan Emerging Markets Euro Area

Gluskin Sheff + Associates Inc.

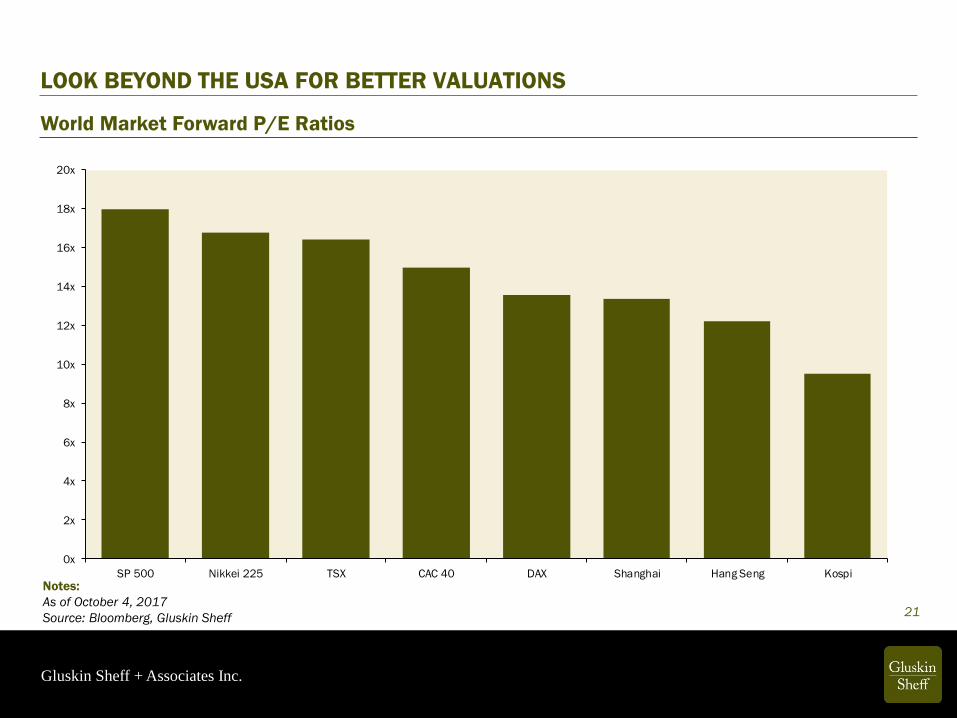

0x

2x

4x

6x

8x

10x

12x

14x

16x

18x

20x

SP 500 Nikkei 225 TSX CAC 40 DAX Shanghai Hang Seng Kospi

LOOK BEYOND THE USA FOR BETTER VALUATIONS

World Market Forward P/E Ratios

21

Notes:

As of October 4, 2017

Source: Bloomberg, Gluskin Sheff

Gluskin Sheff + Associates Inc.

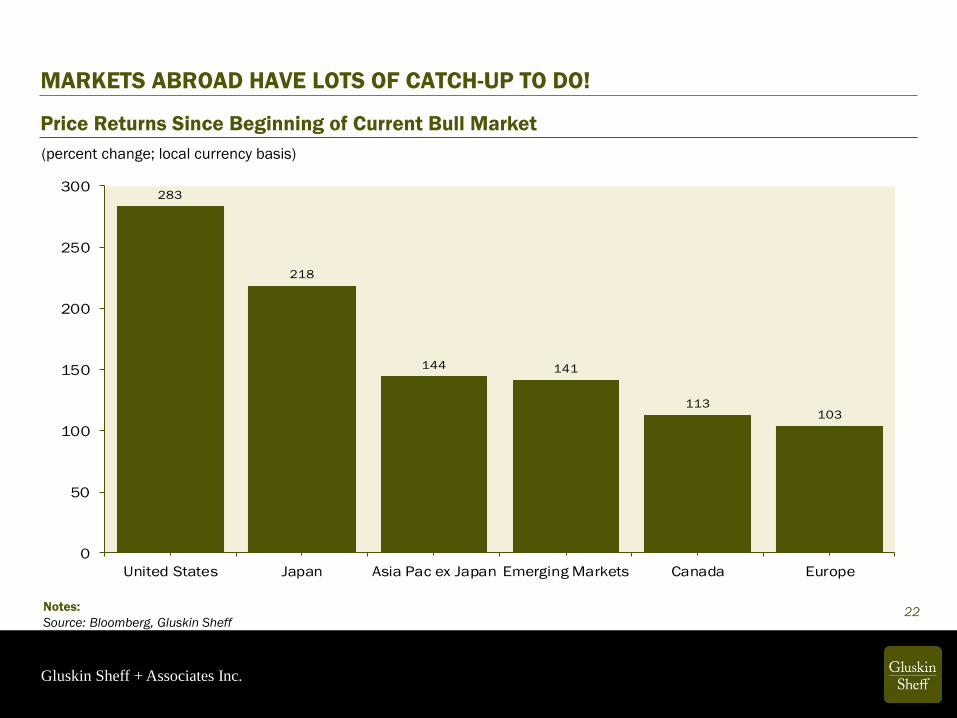

MARKETS ABROAD HAVE LOTS OF CATCH-UP TO DO!

Price Returns Since Beginning of Current Bull Market

(percent change; local currency basis)

22Notes:

Source: Bloomberg, Gluskin Sheff

283

218

144 141

113103

0

50

100

150

200

250

300

United States Japan Asia Pac ex Japan Emerging Markets Canada Europe

Gluskin Sheff + Associates Inc.

Notes:

Source: The Economist (June, 2017)23

Gluskin Sheff + Associates Inc.

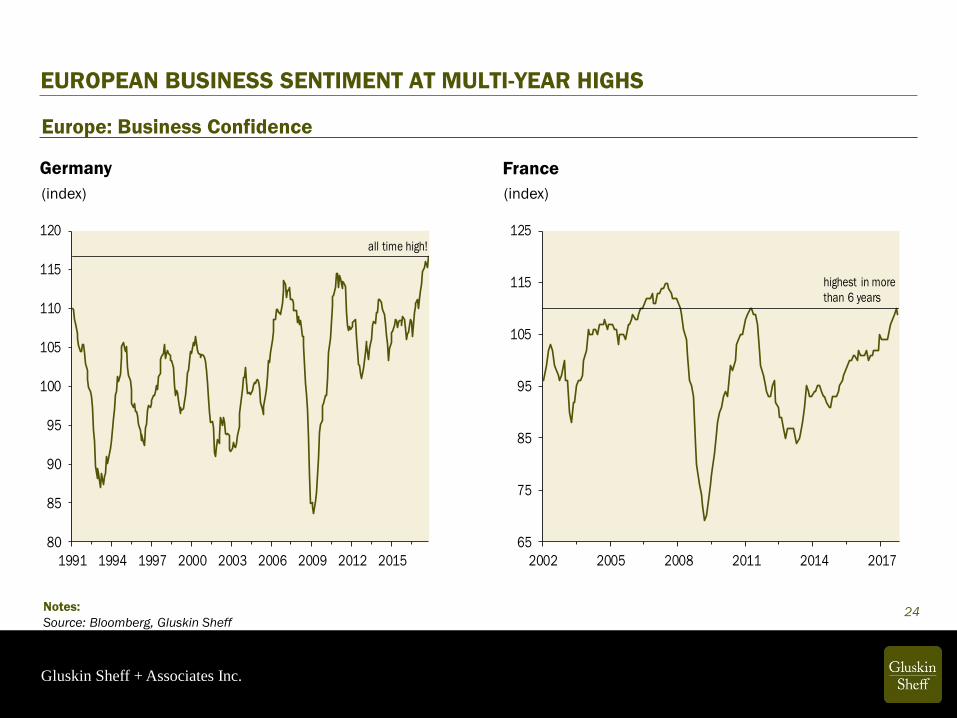

24

Europe: Business Confidence

(index) (index)

Germany France

EUROPEAN BUSINESS SENTIMENT AT MULTI-YEAR HIGHS

Notes:

Source: Bloomberg, Gluskin Sheff

80

85

90

95

100

105

110

115

120

1991 1994 1997 2000 2003 2006 2009 2012 2015

all time high!

65

75

85

95

105

115

125

2002 2005 2008 2011 2014 2017

highest in more

than 6 years

Gluskin Sheff + Associates Inc.

25

JAPAN…WAS ASLEEP FOR A LONG TIME!

Gluskin Sheff + Associates Inc.

26Notes:

Source: The Economist (May 18, 2013)

IT HAS AWAKENED UNDER SUPER-ABE!!

Gluskin Sheff + Associates Inc.

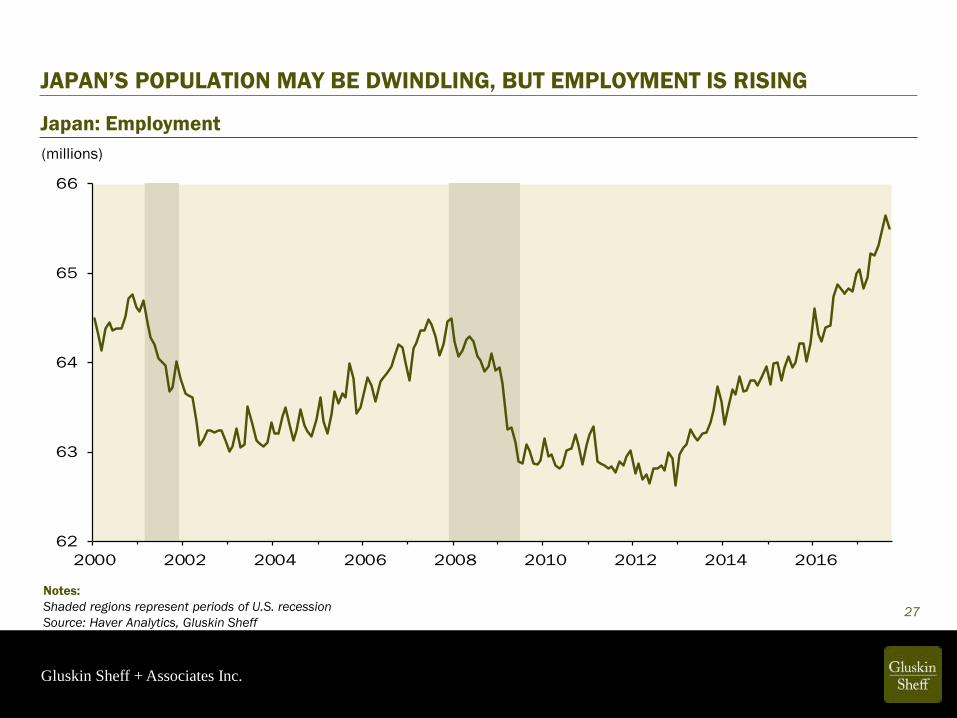

Japan: Employment

(millions)

27

Notes:

Shaded regions represent periods of U.S. recession

Source: Haver Analytics, Gluskin Sheff

JAPAN’S POPULATION MAY BE DWINDLING, BUT EMPLOYMENT IS RISING

62

63

64

65

66

2000 2002 2004 2006 2008 2010 2012 2014 2016

Gluskin Sheff + Associates Inc.

Notes:

Source: The Economist (Week of November 18, 2017)28

Gluskin Sheff + Associates Inc.

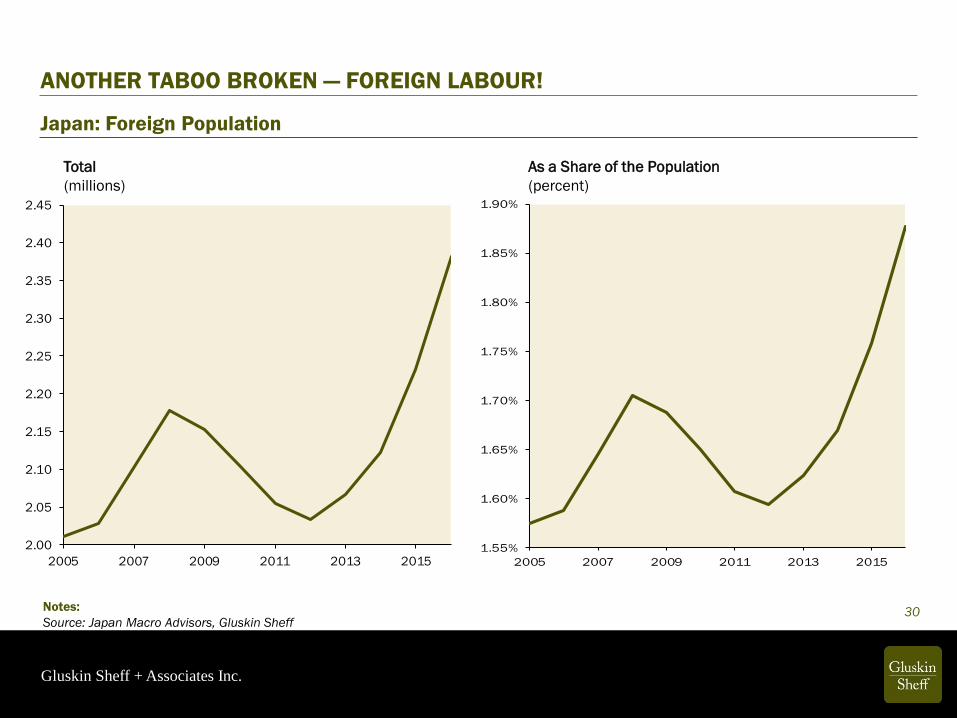

TABOOS BEING BROKEN!

29Notes:

Source: International Labour Organization, Gluskin Sheff

(percent)

Japan: Female Labour Force Participation Rate

48.0

48.5

49.0

49.5

50.0

50.5

51.0

1990 1995 2000 2005 2010 2015

Abe assumes

office

Gluskin Sheff + Associates Inc.

30Notes:

Source: Japan Macro Advisors, Gluskin Sheff

Japan: Foreign Population

2.00

2.05

2.10

2.15

2.20

2.25

2.30

2.35

2.40

2.45

2005 2007 2009 2011 2013 20151.55%

1.60%

1.65%

1.70%

1.75%

1.80%

1.85%

1.90%

2005 2007 2009 2011 2013 2015

Total As a Share of the Population

ANOTHER TABOO BROKEN — FOREIGN LABOUR!

(millions) (percent)

Gluskin Sheff + Associates Inc.

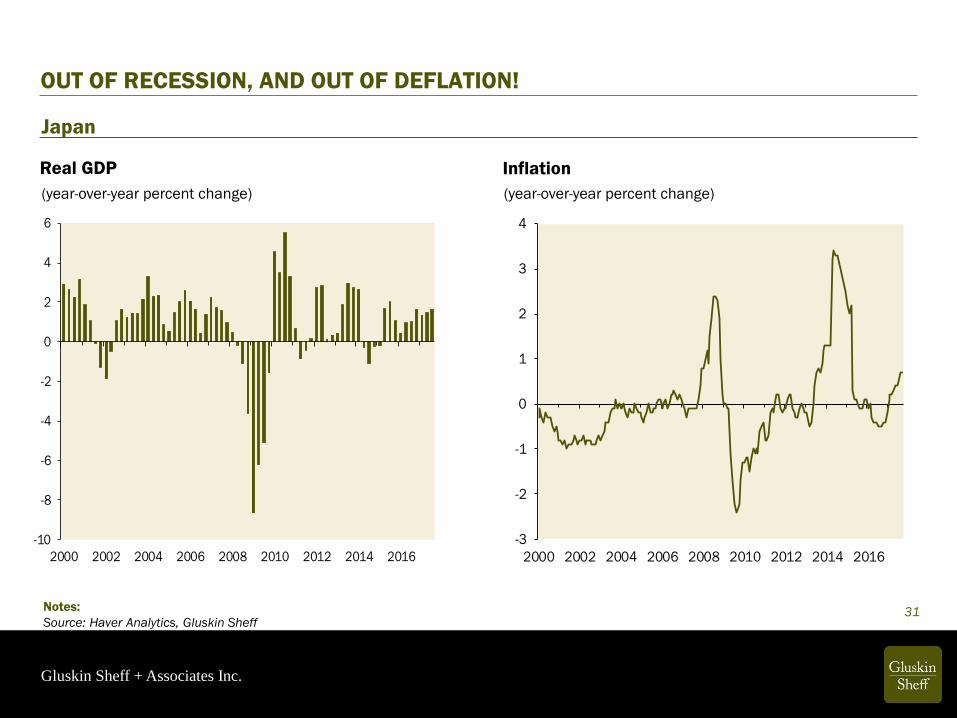

31

Japan

(year-over-year percent change) (year-over-year percent change)

Real GDP Inflation

OUT OF RECESSION, AND OUT OF DEFLATION!

Notes:

Source: Haver Analytics, Gluskin Sheff

-10

-8

-6

-4

-2

0

2

4

6

2000 2002 2004 2006 2008 2010 2012 2014 2016

-3

-2

-1

0

1

2

3

4

2000 2002 2004 2006 2008 2010 2012 2014 2016

Gluskin Sheff + Associates Inc.

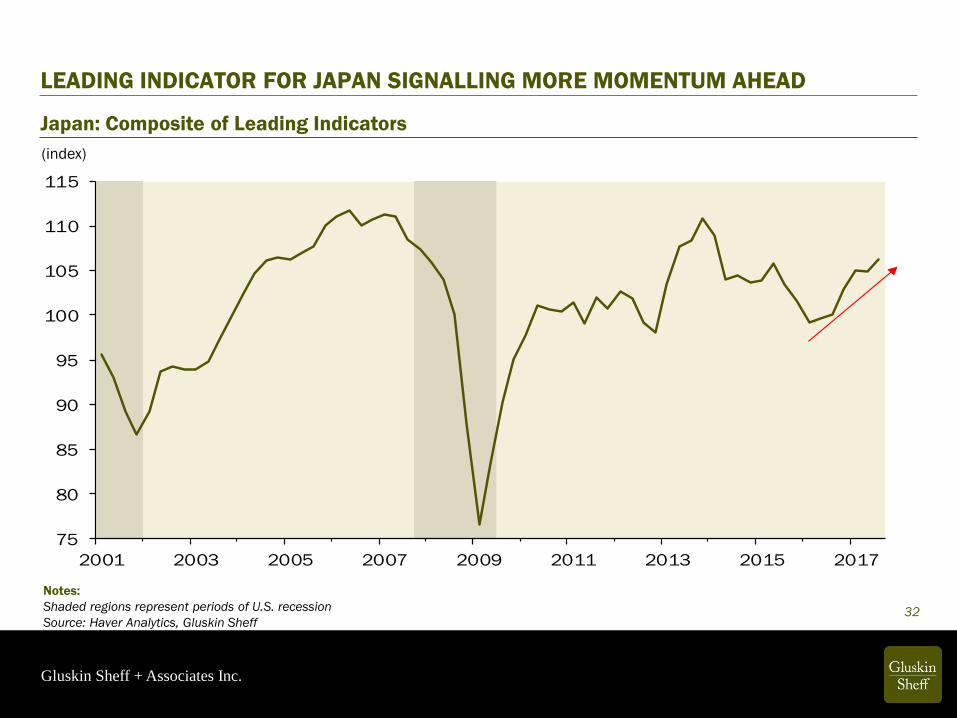

32

LEADING INDICATOR FOR JAPAN SIGNALLING MORE MOMENTUM AHEAD

Notes:

Shaded regions represent periods of U.S. recession

Source: Haver Analytics, Gluskin Sheff

Japan: Composite of Leading Indicators

75

80

85

90

95

100

105

110

115

2001 2003 2005 2007 2009 2011 2013 2015 2017

(index)

Gluskin Sheff + Associates Inc.

Notes:

Source: The Globe & Mail (November 3, 2017)33

Gluskin Sheff + Associates Inc.

34Notes:

Source: Bloomberg, Gluskin Sheff

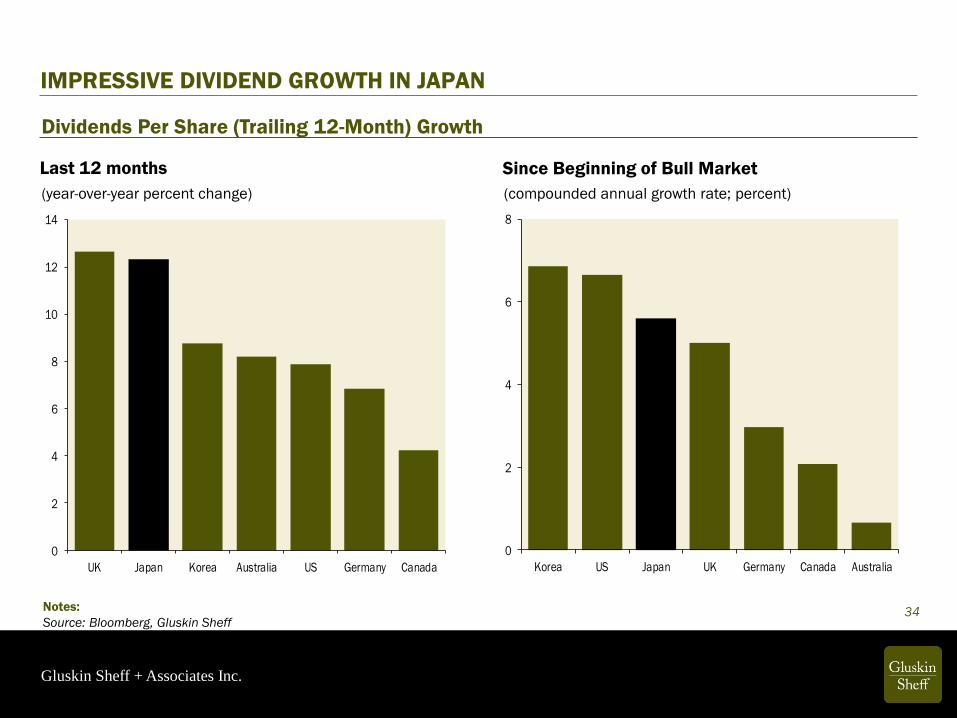

Dividends Per Share (Trailing 12-Month) Growth

(year-over-year percent change)

0

2

4

6

8

10

12

14

UK Japan Korea Australia US Germany Canada

0

2

4

6

8

Korea US Japan UK Germany Canada Australia

(compounded annual growth rate; percent)

Last 12 months Since Beginning of Bull Market

IMPRESSIVE DIVIDEND GROWTH IN JAPAN

Gluskin Sheff + Associates Inc.

35Notes:

Source: CLSA, Bloomberg, Gluskin Sheff

Current Year Expected Dividend Payout Ratios

17%

29%31%

39% 39%41%

50%53%

63%

0%

10%

20%

30%

40%

50%

60%

70%

Korea Japan India US Germany Hong Kong France Italy UK

AND BETTER DIVIDEND GROWTH PROSPECTS AS WELL

(percent)

Gluskin Sheff + Associates Inc.

36Notes:

Source: Haver Analytics, Gluskin Sheff

(percent)

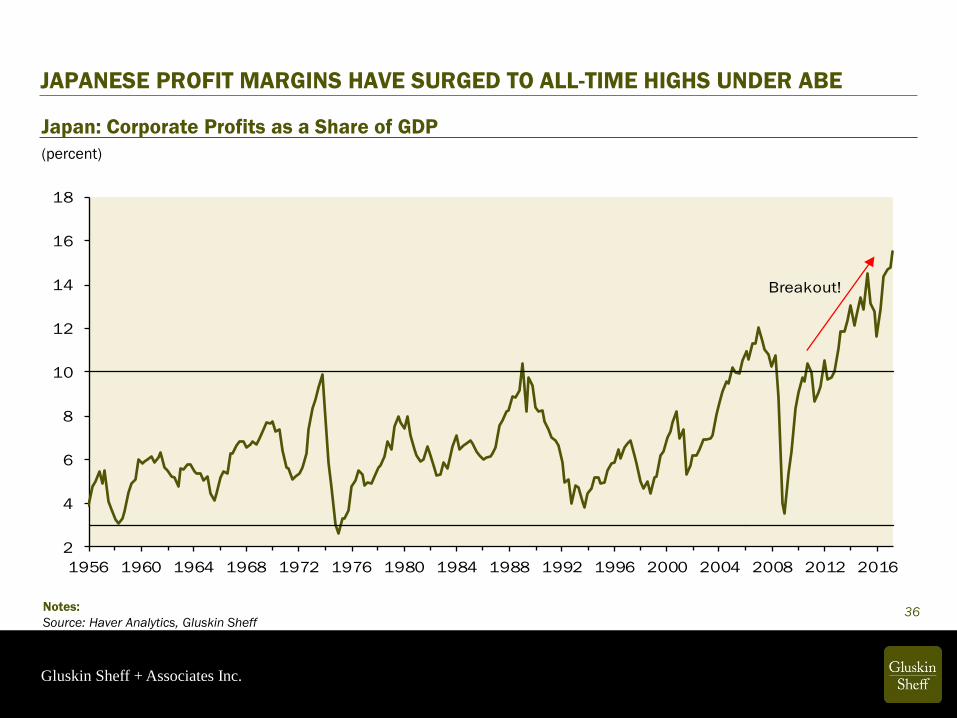

Japan: Corporate Profits as a Share of GDP

2

4

6

8

10

12

14

16

18

1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Breakout!

JAPANESE PROFIT MARGINS HAVE SURGED TO ALL-TIME HIGHS UNDER ABE

Gluskin Sheff + Associates Inc.

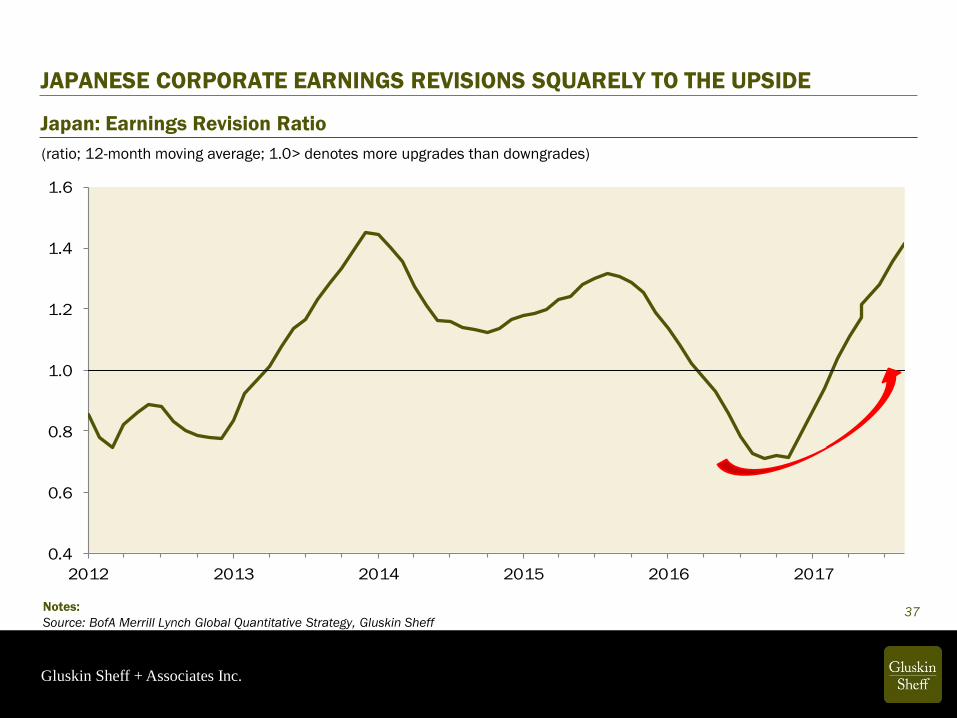

JAPANESE CORPORATE EARNINGS REVISIONS SQUARELY TO THE UPSIDE

37Notes:

Source: BofA Merrill Lynch Global Quantitative Strategy, Gluskin Sheff

Japan: Earnings Revision Ratio

0.4

0.6

0.8

1.0

1.2

1.4

1.6

2012 2013 2014 2015 2016 2017

(ratio; 12-month moving average; 1.0> denotes more upgrades than downgrades)

Gluskin Sheff + Associates Inc.

WHAT A DIFFERENCE A YEAR MAKES

38Notes:

Source: BofA Merrill Lynch Global Quantitative Strategy, Gluskin Sheff

World: 3-Month Earnings Revision Ratio

Today

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

Japan USA World Asia Pac ex.

Japan

Emerging

Markets

Europe

0.4

0.5

0.6

0.7

0.8

0.9

1.0

USA Europe Emerging

Markets

World Asia Pac ex.

Japan

Japan

One Year Ago

(ratio; 1.0> denotes more upgrades than downgrades)

Gluskin Sheff + Associates Inc.

39Notes:

Source: Haver Analytics, Gluskin Sheff

(index)

Japan: Nikkei 225

5000

10000

15000

20000

25000

30000

35000

40000

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

S&P 500 was 700

JAPANESE EQUITIES ARE BREAKING OUT

Gluskin Sheff + Associates Inc.

40Notes:

Source: Bloomberg, Gluskin Sheff

Japan: Market Cap Share of Total

(percent share)

6

7

8

9

10

11

12

13

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

average

IF YOU BELIEVE IN MEAN REVERSION, THIS IS THE MARKET TO BE IN

Gluskin Sheff + Associates Inc.

41Notes:

Source: National Post (November 3, 2017)

Gluskin Sheff + Associates Inc.

DISCLAIMER

The information, opinions, and other materials contained in this presentation is the

property of Gluskin Sheff + Associates Inc. and may not be reproduced in any way, in

whole or in part, without express authorization of the copyright holder in writing. The

statements and statistics contained herein have been prepared by Gluskin Sheff +

Associates Inc. based on information from sources considered to be reliable. We make

no representation or warranty, express or implied, as to its accuracy or completeness.

This publication is for the information of investors and business persons and does not

constitute an offer to sell or a solicitation to buy securities.

42

Related Documents

![^F mF n PoY[K v v h [ ! 5 V ^ [ Znoja/f.pdf · 9 2 X (9 < 5o =9 X ?> 1 @ BA & l X! G ? ? C: 9 9ED F: HG X G X G I !( "9 $ ! vj J $ q 9 5 j 9 & " jm K' Io"1] y. KL ` 6AM: 9 9ONQP](https://static.cupdf.com/doc/110x72/5ec40ffd9579f031121de05d/f-mf-n-poyk-v-v-h-5-v-z-nojafpdf-9-2-x-9-5o-9-x-1-ba.jpg)

![TI - unican.es · (IV) {isc1.m}:x [ n ]=!∞ k = −∞ x [ k ] δ [n − k ] ≡!∞ k = −∞ p k [n ]. p k [n ] ada x [k ] instante k. a p k [ n ] es v k [n ]= x [k ] h[n −](https://static.cupdf.com/doc/110x72/5e89c15993604a6d474be7b4/ti-iv-isc1mx-n-a-k-aa-x-k-n-a-k-aa-k-aa.jpg)