www.nicsa.org | #WebinarWednesdays “Glocal" Distribution Strategies Wednesday, November 29 | 10:00am – 11:00am ET

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.nicsa.org | #WebinarWednesdays

“Glocal" Distribution Strategies

Wednesday, November 29 | 10:00am – 11:00am ET

www.nicsa.org | #WebinarWednesdays

Scott Brady - ModeratorVice President,

Head of Product

Development & Strategy

Columbia Threadneedle Investments, US

Diana MackayCEO

MackayWIlliams

Angelos GousiosDirector,

European Retail Research

Cerulli Associates Europe

Presenters

www.nicsa.org | #WebinarWednesdays

Confidential. Not for re-distribution.

Global Fund Distribution

By: Angelos Gousios, Director of European Retail Research

29 November, 2017

www.nicsa.org | #WebinarWednesdays

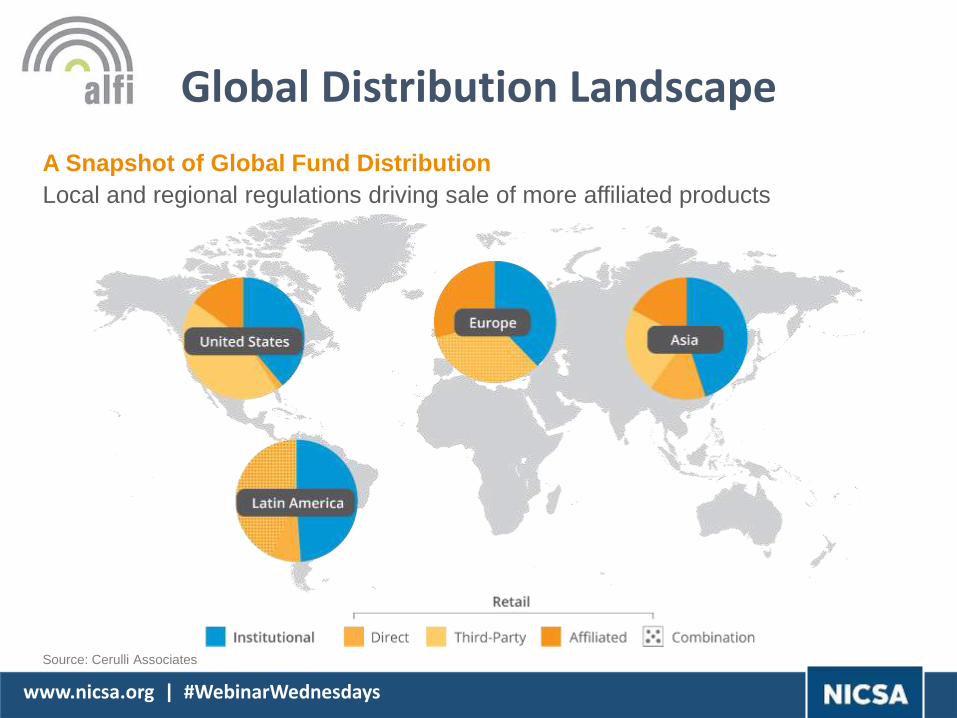

Global Distribution Landscape

www.nicsa.org | #WebinarWednesdays

Global Asset Management Industry Assets Under Management by

Region, 2012–2021E (US$ trillions)

U.S. marketshare gradually being eroded by Asia and Europe

60.366.2

72.3 75.479.3

84.389.2

94.5100.2

106.3

45.6%

44.6%

46.1%

47.7% 47.8%48.4%

49.0%49.5%

50.1%50.7%

44%

46%

48%

50%

52%

US$0

US$20

US$40

US$60

US$80

US$100

US$120

2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021E

Global Non-US (% of global)

50.1%

United States

Analyst Note: We have attempted to remove double-counting wherever data transparency allows us to do so. Some minor restatement occasionally

occurs between review periods. ¹Includes Canada, Latin America, and other assets.

Source: Cerulli Associates, The Cerulli Report - Global Markets 2017: How to Succeed Internationally

www.nicsa.org | #WebinarWednesdays

Local and regional regulations driving sale of more affiliated products

Source: Cerulli Associates

A Snapshot of Global Fund Distribution

Global Distribution Landscape

www.nicsa.org | #WebinarWednesdays

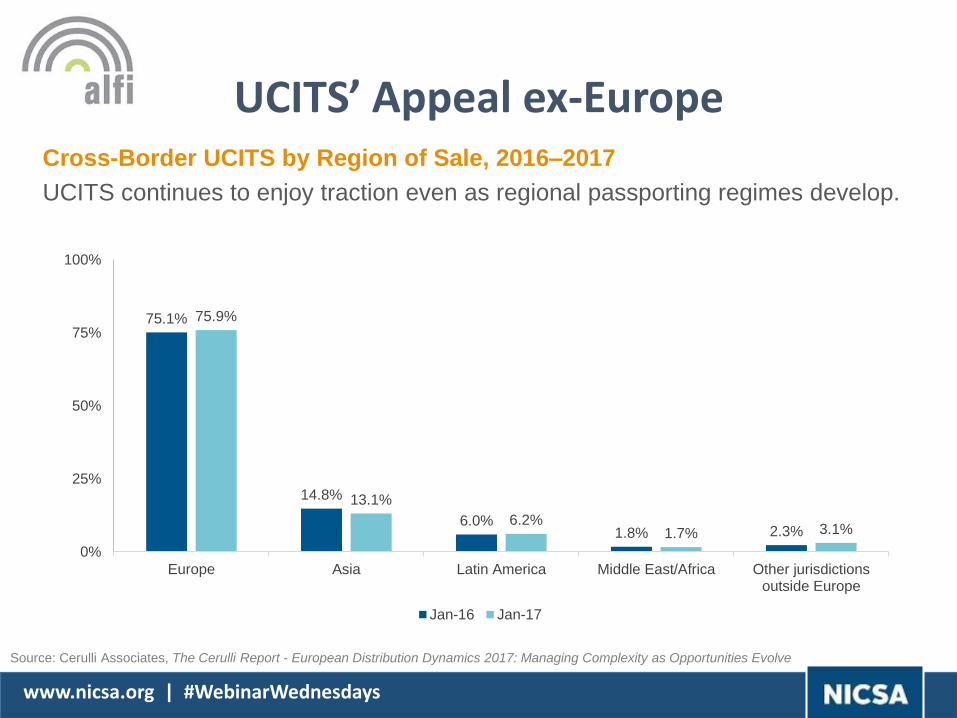

Cross-Border UCITS by Region of Sale, 2016–2017

UCITS continues to enjoy traction even as regional passporting regimes develop.

Source: Cerulli Associates, The Cerulli Report - European Distribution Dynamics 2017: Managing Complexity as Opportunities Evolve

75.1%

14.8%

6.0%1.8% 2.3%

75.9%

13.1%

6.2%1.7% 3.1%

0%

25%

50%

75%

100%

Europe Asia Latin America Middle East/Africa Other jurisdictionsoutside Europe

Jan-16 Jan-17

UCITS’ Appeal ex-Europe

www.nicsa.org | #WebinarWednesdays

Asia ex-Japan

www.nicsa.org | #WebinarWednesdays

Asia Ex-Japan Mutual Fund Assets Under Management by Country, 2012–2021E (US$

billions)

Source: Cerulli Associates, The Cerulli Report – Global Markets 2017: How to Succeed Internationally

Country 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021E

CAGR2016-2021E

China 387.5 418.7 634.6 1,171.7 1,251.1 1,442.4 1,649.6 1,872.2 2,106.8 2,348.0 13.4%

Korea 158.0 153.9 166.1 180.0 178.7 186.3 195.7 205.9 217.2 229.9 5.2%

Taiwan 131.9 137.3 154.5 153.3 148.9 160.9 171.7 182.7 193.3 203.8 6.5%

India 109.5 119.5 152.2 184.6 236.9 291.7 341.6 399.0 465.2 539.8 17.9%

Hong Kong 93.8 108.1 123.5 122.7 130.9 144.8 159.1 174.6 189.9 204.1 9.3%

Singapore 36.7 48.0 56.4 58.5 60.3 64.3 68.6 73.6 79.1 85.3 7.2%

Total 917.4 985.5 1287.3 1870.8 2006.8 2290.4 2586.3 2908 3251.5 3610.9 12.5%

Asia ex-Japan

www.nicsa.org | #WebinarWednesdays

Asia Ex-Japan Mutual Fund Assets Under Management by Distribution

Channel, 2014–2016

Efforts underway to diversify fund distribution channels but banks likely to retain tight control

Analyst Note: 1Includes mutual fund sales through ILPs and direct sales.

Source: Cerulli Associates, The Cerulli Report - Asian Distribution Dynamics 2017: New Horizons Await—Venturing into Overseas Markets

17%24% 27%

48%41%

40%

15% 14% 12%

13% 15% 15%

7% 6% 6%

0%

20%

40%

60%

80%

100%

2014 2015 2016

Direct Banks Securities companies Independent financial advisors/Platforms Insurance companies(1)

Asia ex-Japan

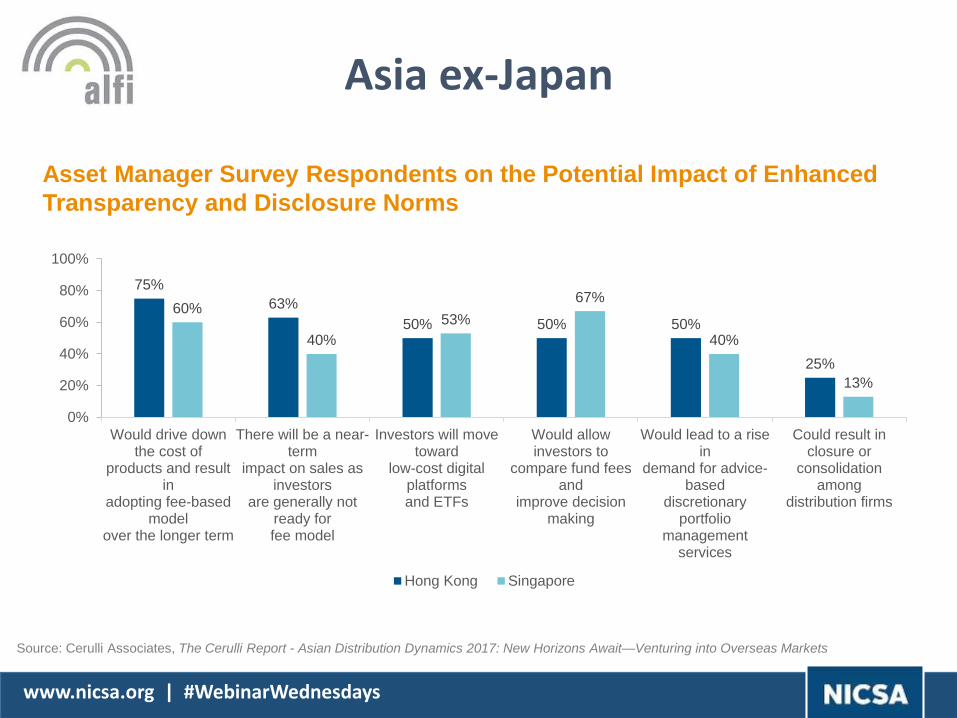

www.nicsa.org | #WebinarWednesdays

Asset Manager Survey Respondents on the Potential Impact of Enhanced

Transparency and Disclosure Norms

Source: Cerulli Associates, The Cerulli Report - Asian Distribution Dynamics 2017: New Horizons Await—Venturing into Overseas Markets

75%

63%

50% 50% 50%

25%

60%

40%

53%

67%

40%

13%

0%

20%

40%

60%

80%

100%

Would drive downthe cost of

products and resultin

adopting fee-basedmodel

over the longer term

There will be a near-term

impact on sales asinvestors

are generally notready forfee model

Investors will movetoward

low-cost digitalplatformsand ETFs

Would allowinvestors to

compare fund feesand

improve decisionmaking

Would lead to a risein

demand for advice-based

discretionaryportfolio

managementservices

Could result inclosure or

consolidationamong

distribution firms

Hong Kong Singapore

Asia ex-Japan

www.nicsa.org | #WebinarWednesdays

Asia Ex-Japan Exchange-Traded Fund Assets Under Management,

2012–2016 (US$ billions)

Analyst Note: Locally domiciled only.

Source: Cerulli Associates, The Cerulli Report - Asian Distribution Dynamics 2017: New Horizons Await—Venturing into Overseas Markets

23.4 23.1

36.4

66.2

52.1

12.216.1 16.3 17.9

20.8

4.5 4.3 5 6.2 8

2 1.5 2 2.65.1

26.424

35.1 34.9

29.2

1.5 1.3 1.5 1.5 1.6

$0

$20

$40

$60

$80

2012 2013 2014 2015 2016

China Korea Taiwan India Hong Kong Singapore

Asia ex-Japan

www.nicsa.org | #WebinarWednesdays

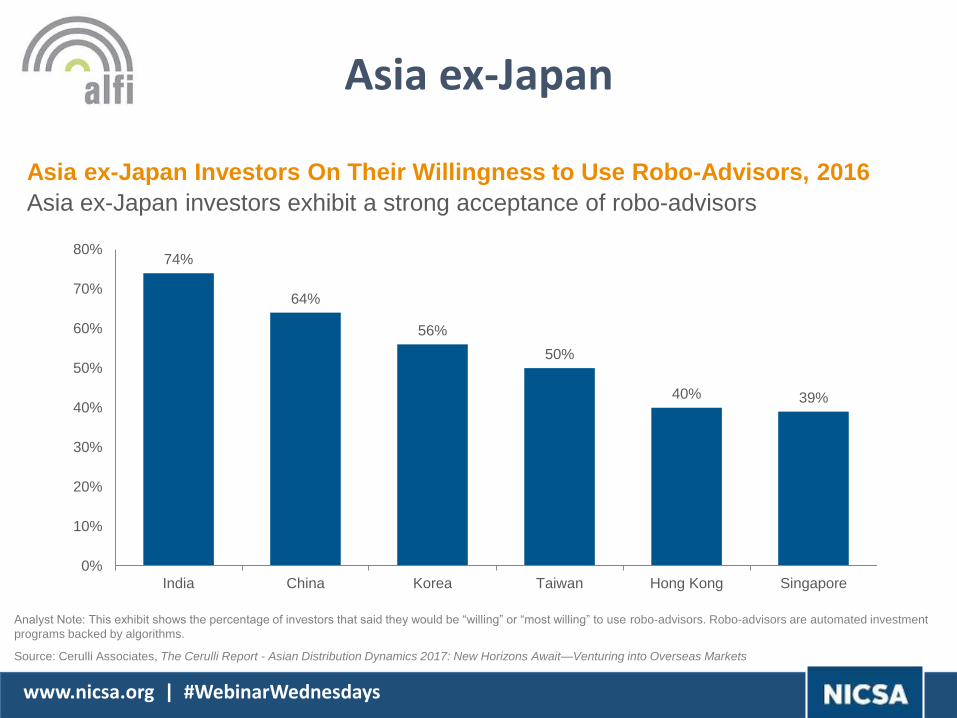

Asia ex-Japan Investors On Their Willingness to Use Robo-Advisors, 2016

Asia ex-Japan investors exhibit a strong acceptance of robo-advisors

Analyst Note: This exhibit shows the percentage of investors that said they would be “willing” or “most willing” to use robo-advisors. Robo-advisors are automated investment

programs backed by algorithms.

Source: Cerulli Associates, The Cerulli Report - Asian Distribution Dynamics 2017: New Horizons Await—Venturing into Overseas Markets

74%

64%

56%

50%

40% 39%

0%

10%

20%

30%

40%

50%

60%

70%

80%

India China Korea Taiwan Hong Kong Singapore

Asia ex-Japan

www.nicsa.org | #WebinarWednesdays

Europe –entering a new age of distribution

Diana Mackay, CEO MackayWilliams LLP

www.nicsa.org

www.nicsa.org | #WebinarWednesdays

Mapping out the European

landscape;

New dynamics in distribution;

Disruption

Agenda

www.nicsa.org | #WebinarWednesdays

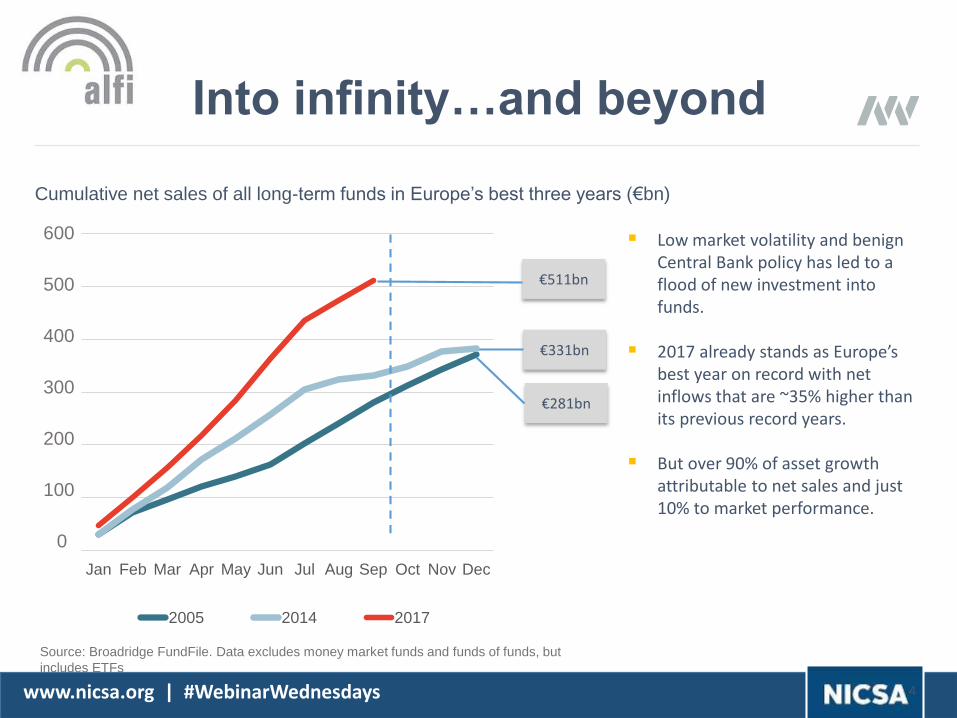

€331bn

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2005 2014 2017

€511bn

Into infinity…and beyond

Cumulative net sales of all long-term funds in Europe’s best three years (€bn)

Source: Broadridge FundFile. Data excludes money market funds and funds of funds, but

includes ETFs

4

200

300

400

500

600

100

0

€281bn

Low market volatility and benign Central Bank policy has led to a flood of new investment into funds.

2017 already stands as Europe’s best year on record with net inflows that are ~35% higher than its previous record years.

But over 90% of asset growth attributable to net sales and just 10% to market performance.

www.nicsa.org | #WebinarWednesdays

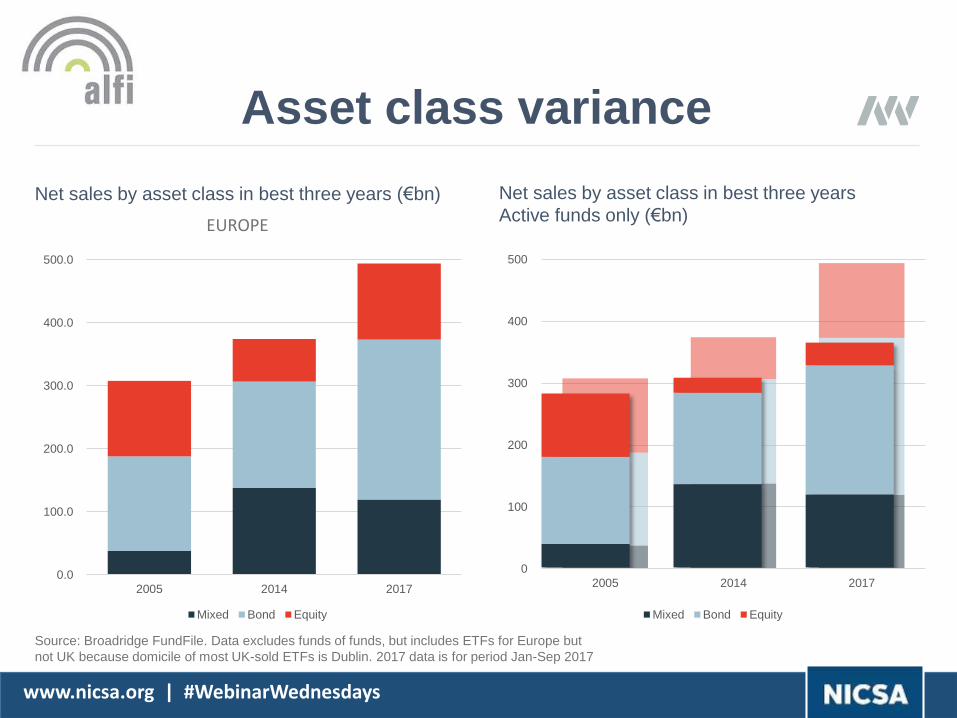

Asset class variance

Net sales by asset class in best three years (€bn)

EUROPE

Source: Broadridge FundFile. Data excludes funds of funds, but includes ETFs for Europe but

not UK because domicile of most UK-sold ETFs is Dublin. 2017 data is for period Jan-Sep 2017

Net sales by asset class in best three years

Active funds only (€bn)

0.0

100.0

200.0

300.0

400.0

500.0

2005 2014 2017

Mixed Bond Equity

0

100

200

300

400

500

2005 2014 2017

Mixed Bond Equity

www.nicsa.org | #WebinarWednesdays

A period of extraordinary sales growth

18

-100,000

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2013

2014

2015

2016

2017

Mixed Asset Bond Equity

• Investors chase safety in bonds fuelled by central bank QE initiatives;

• Mixed assets outrun equities, boosted by demand for absolute return and diluted exposure to risk;

• Core active equity funds struggle to prove their added value.

5 yr cumulative monthly net sales by asset class (€m)

Source: MackayWilliams analysis of Broadridge FundFile data

Data excludes money market funds and funds of funds

€742bn

€631bn

€324bn

www.nicsa.org | #WebinarWednesdays

Taking account of the changing world

But … regulation is changing industry dynamics

Source: MackayWilliams

Impact of the financial crisis and Central

Bank policies to flood liquidity into markets,

and terminally low interest rates;

New mood of optimism amongst investors,

including mainstream consumers;

In Continental Europe, bank focus on

building profits rather than boosting cash

reserves;

Search for alpha or uncorrelated investment

options set against context of robust

provision of beta via low-cost passives.

www.nicsa.org | #WebinarWednesdays

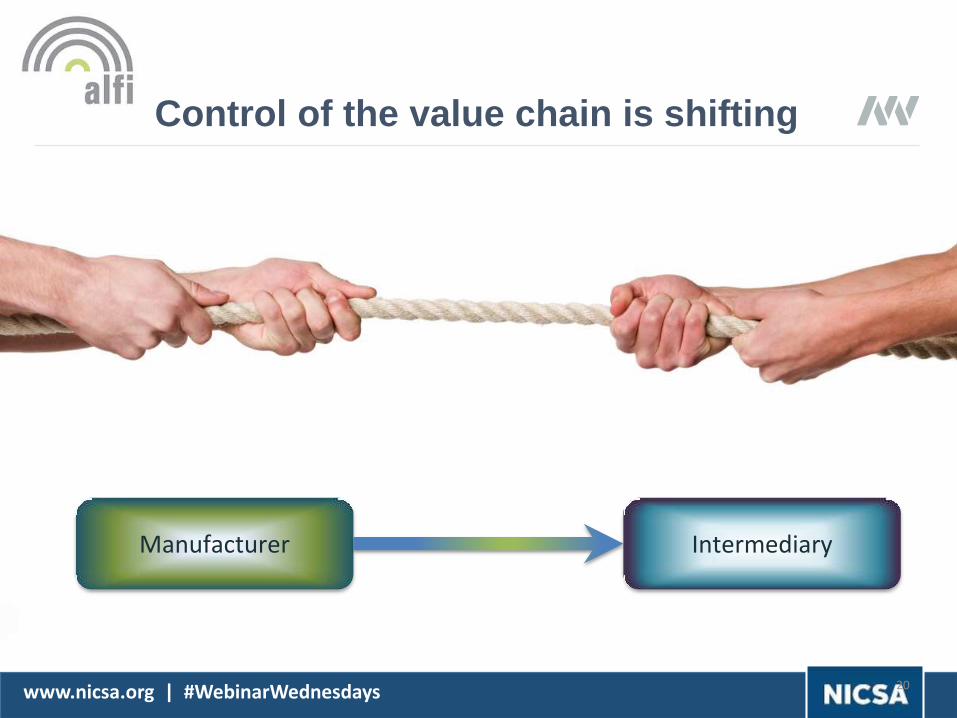

Control of the value chain is shifting

20

Manufacturer Intermediary

www.nicsa.org | #WebinarWednesdays

Apocalypse…

Passive will take over

Winner takes all, the squeezed middle and product proliferation

A race to the bottom on prices

Client engagement

Competition from newcomers

www.nicsa.org | #WebinarWednesdays

Threats – real or

imagined

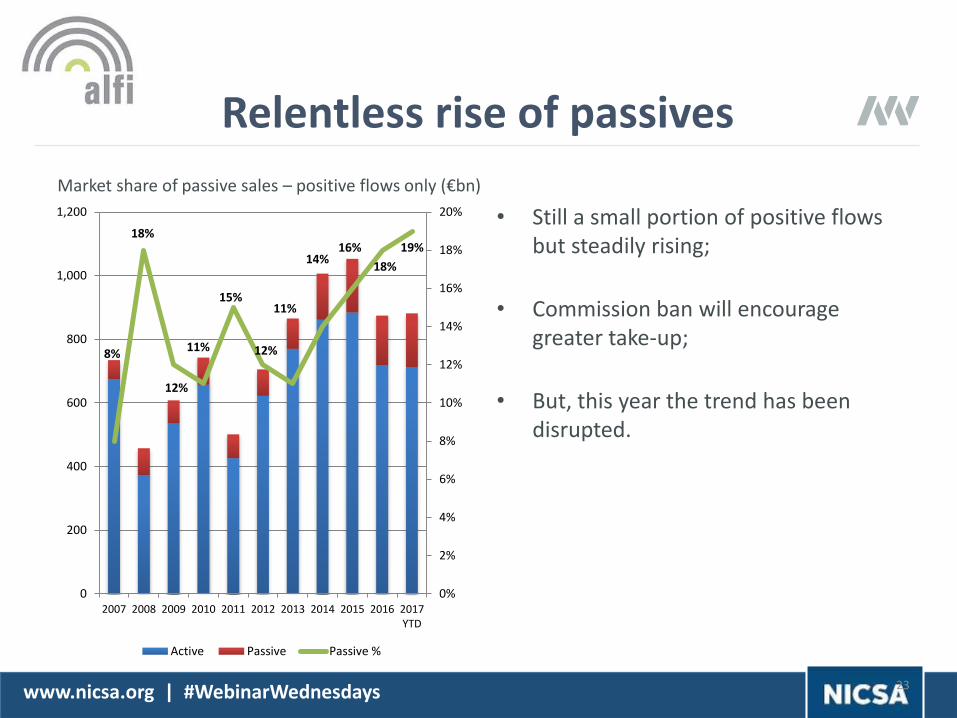

www.nicsa.org | #WebinarWednesdays 23

• Still a small portion of positive flows but steadily rising;

• Commission ban will encourage greater take-up;

• But, this year the trend has been disrupted.

8%

18%

12%

11%

15%

12%

11%

14%16%

18%

19%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

200

400

600

800

1,000

1,200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017YTD

Active Passive Passive %

Market share of passive sales – positive flows only (€bn)

Relentless rise of passives

www.nicsa.org | #WebinarWednesdays

Net sales 2005 2014 2017

7 5 4Annual net sales of….. €10bn+

€0m+€1bn

73 83 79€1bn-€10bn

Number of groups in each net sales band – active funds only (€bn)

% sales taken by top fund

2005 2014 2017

1% 2% 7%

793 958 927

Winner takes all?

www.nicsa.org | #WebinarWednesdays

Race to the bottom on pricing

The move towards

passive investments is

creating downwards

pressure on fund prices

generally, but I expect

that good active

managers will be able to

demonstrate that they

can produce and

sustain their

performance over timeDiscretionary portfolio manager

Source: MackayWilliams, Fund Buyer Focus distributor interviews

The distributor discussion has shifted from

‘what retrocession are you offering?’ to ‘how do

you justify the fee that you want to charge?’.

Pricing pressure is being felt most in the

commoditised passive arena.

In active funds, demand is growing for access

to the lowest priced share class but good

performance outweighs fees.

Performance fees are generally disliked, but if

implemented they must be simple and easy to

explain to clients.

www.nicsa.org | #WebinarWednesdays

Client engagement

‘Selling’ advisory services will play an important role

for providers in the future, which is why we have to

concentrate, expand and broaden our expertise. I

hope for good co-operation with our fund providers

in terms of joint customer events and presentations

but also for an effective communication of

investment ideas.

Discretionary portfolio manager

Product is the traditional core of the asset management offer, butthe future is in operating as a service industry

Source: MackayWilliams, Fund Buyer Focus distributor interviews

www.nicsa.org | #WebinarWednesdays

Competition from newcomers

I have noticed that fund

companies are trying to

pursue new business

lines and cooperation

agreements rather than

just offer products. I

have come across

attempts to set up joint

wealth managements

and Robo-Advice.

Discretionary portfolio

manager

Source: MackayWilliams, Fund Buyer Focus distributor interviews

The rise of the trusted adviser and its

conversion to asset manager;

Attractions of robo-advice

www.nicsa.org | #WebinarWednesdays

Disruption

www.nicsa.org | #WebinarWednesdays

Changing product mix

Rotation – not from bond to equity but…

From developed markets to emerging markets;

From niche to generalist;

From single strategies to solutions;

From active to passive

www.nicsa.org | #WebinarWednesdays

Developed to emerging

Source: Broadridge FundFile. Data excludes funds of funds. Graphic based on ‘super-sector’ so

all EM-based sectors merged. 2017 data is for period Jan-Sep 2017

-50,000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2002 2004 2006 2008 2010 2012 2014 2016

Cumulative net sales history –Bond (€m)

Bonds Emerging Markets Bonds Global Currencies

-100,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

300,000

2002 2004 2006 2008 2010 2012 2014 2016

Cumulative net sales history – Equities (€m)

Eq Europe Eq Global Eq Emerging Markets

EM Bond is Europe’s 16th largest sector but

ranks 3rd for net inflows EM Equity is Europe’s 6th largest sector but

ranks 11th for net inflows

Financial crisis Financial crisis

www.nicsa.org | #WebinarWednesdays

Single strategies to solutions

-200

0

200

400

600

800

1,000

1,200

DevelopedEquity

Outcomes Higher RiskBonds

Core Bonds EM and AsiaEquity

Other Theme Equity

Total net sales by style, Sep ‘07 – Aug ‘17 (€bn)

Source: MackayWilliams analysis of Broadridge FundFile data, excluding money market funds and funds of funds. ‘Outcomes’ consists of mixed asset, alternative,

and bonds global currencies sectors.

Many of the most popular

sectors of the past decade

focus on ‘outcomes’.

But the bond category has

also undergone an important

transformation, diversifying

into riskier areas.

www.nicsa.org | #WebinarWednesdays

Active to passive

Source: MackayWilliams analysis of Broadridge FundFile data. Data excludes money market funds and funds of funds

Asset class Active (€bn) Passive (€bn)

Equity -92 415

Bond 648 218

Mixed Asset 755 1

Equity Bond

-300

-200

-100

0

100

200

300

400

500

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017YTD

Active Passive

-300

-200

-100

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017YTD

Active Passive

Cumulative flows by asset class over the last 10 years (€bn)

Mixed asset funds unaffected by rotation

Q&AQUESTIONS & ANSWERS SESSION

www.nicsa.org | #WebinarWednesdays

Related Documents