LATEST TRENDS COFI FT 14th Session The fourteenth session of the Sub-Committee on Fish Trade of the Committee on Fisheries (COFI FT) was held in Bergen, Norway, from 24 to 28 February 2014. The Session was attended by 53 member countries of the Food and Agriculture Organization (FAO) of the United Nations, one Associate Member, by representatives from two Specialized Agencies of the United Nations and by observers from 12 intergovernmental and international non-governmental organizations. Key topics discussed by the participants included the role of the fish trade for income generation and in promoting fish consumption, issues of market access for developing country producers and small-scale fishers, strategies for the development and empowerment of the small-scale sector, and various ongoing projects and focus areas related to sustainability and conservation. Amongst the latter discussions were the effects of ecolabelling schemes on fisheries, a review of the draft best practice traceability guidelines, the desirability of developing catch documentation schemes as called for by the UN fisheries resolution on sustainable fisheries and an update on activities related to the Convention on International Trade in Endangered Species of Wild Flora and Fauna (CITES). The fifteenth session of COFI FT will be held in Morocco in 2016. Issue 03/2014 March 2014 INDEX FOR PRICES Groundfish 10 Flatfish 11 Tuna 12 Small Pelagics 12 Cephalopods 13 Crustaceans 13 Bivalves 15 Salmon 15 Trout 16 Freshwater fish 16 Non Traditional Species 16 Seabass-Seabream- Meagre 17 The European Fish Price Report, based on information supplied by industry correspondents, aims to provide guidance on broad price trends. Price information is indicative and should be used only for forecasting medium- and long-term trends. FAO is not responsible for any errors or omissions.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LATEST TRENDS

COFI FT 14th Session

The fourteenth session of the Sub-Committee on Fish Trade of the Committee on Fisheries (COFI FT) was held in Bergen, Norway, from 24 to 28 February 2014. The Session was attended by 53 member countries of the Food and Agriculture Organization (FAO) of the United Nations, one Associate Member, by representatives from two Specialized Agencies of the United Nations and by observers from 12 intergovernmental and international non-governmental organizations. Key topics discussed by the participants included the role of the fish trade for income generation and in promoting fish consumption, issues of market access for developing country producers and small-scale fishers, strategies for the development and empowerment of the small-scale sector, and various ongoing projects and focus areas related to sustainability and conservation. Amongst the latter discussions were the effects of ecolabelling schemes on fisheries, a review of the draft best practice traceability guidelines, the desirability of developing catch documentation schemes as called for by the UN fisheries resolution on sustainable fisheries and an update on activities related to the Convention on International Trade in Endangered Species of Wild Flora and Fauna (CITES). The fifteenth session of COFI FT will be held in Morocco in 2016.

Issue 03/2014 March 2014

INDEX FOR PRICES

Groundfish 10

Flatfish 11

Tuna 12

Small Pelagics 12

Cephalopods 13

Crustaceans 13

Bivalves 15

Salmon 15

Trout 16

Freshwater fish 16

Non Traditional Species 16

Seabass-Seabream- Meagre 17

The European Fish Price Report, based on information supplied by industry correspondents, aims to provide guidance on broad price trends.

Price information is indicative and should be used only for forecasting medium- and long-term trends.

FAO is not responsible for any errors or omissions.

2

NASF 2014 Following COFI FT, this year Bergen also hosted the 9th annual North Atlantic Seafood Forum (NASF), with a range of presentations, seminars and industry networking events taking place over three days from 4-6 March. In total, 650 delegates from 35 countries (and all 5 continents), and more than 300 companies attended the 9th NASF this year. Topics included the retail sector, whitefish, salmon, small pelagics, policy and sustainability. FAO representatives included the Assistant Director-General, Mr Árni M. Mathiesen, who spoke on the global state of fisheries and aquaculture and its role in food security and nutrition, and Mr Audun Lem, branch chief of the Fish Products, Trade and Markets Branch (FIPM), who gave a presentation on the outlook for small pelagics sector and its contribution to global food supplies. Following these introductory overviews, a number of company executives, together with other expert speakers, gave their views on the current direction of the industry and the challenges to be faced in the future. An important theme during the retail sector session was the relatively low ranking of sustainability in the list of factors influencing the average consumer’s purchasing decisions. Meanwhile, representatives from the whitefish sector emphasized the need to follow the salmon industry’s lead of consolidation to maintain competitiveness, while the salmon session focused on the implications of the limits on supply growth and the struggle against sea lice.

GROUNDFISH A new arrangement on the management of shared fish stocks in the North Sea was concluded on 12 March in London between the European Union and Norway for 2014. Total allowable catches (TACs) and quotas for the shared stocks in the North Sea were established and an agreement was also reached on the exchange of reciprocal fishing possibilities in each other's waters. This arrangement involves an increase of 5% in the TAC for North Sea cod and of 15% for North Sea plaice compared with 2013. However, the TACs for North Sea haddock, saithe and whiting have been reduced by 15%.

According to the Norwegian Seafood Council, Norwegian exports of cod, saithe and haddock amounted to more than NOK 1.15 billion in February, representing an increase in value of 48% compared with February last year. In volume, exports of all codfish increased by 33%, at prices somewhat higher than last year’s.

In Europe, the price trend for wet-salted cod fillets (Gadus Macrocephalus) is now stable after the increase of past months. Importer stocks remain low, but supply is slightly improving. For wet-salted cod fillets (Gadus Morhua) from fresh raw material, demand is very strong from Spain for the traditional consumption of the Lent period while the Italian market is slowing down. The production of stockfish in Lofoten Island is expected to be lower compared with last year, although present weather conditions are favourable for the drying process. Both production and demand for ling are reported to be somewhat low at the moment.

Barents Sea cod prices have risen this month, because of a break in supply from fishing companies to industrials. The lack of stocks is due mainly to a change in supply policy, to financial problems and/or good sales of cod. Consequently, should 2014 catches not be as good as previous years, industrials may have difficulties finding stocks this year.

3

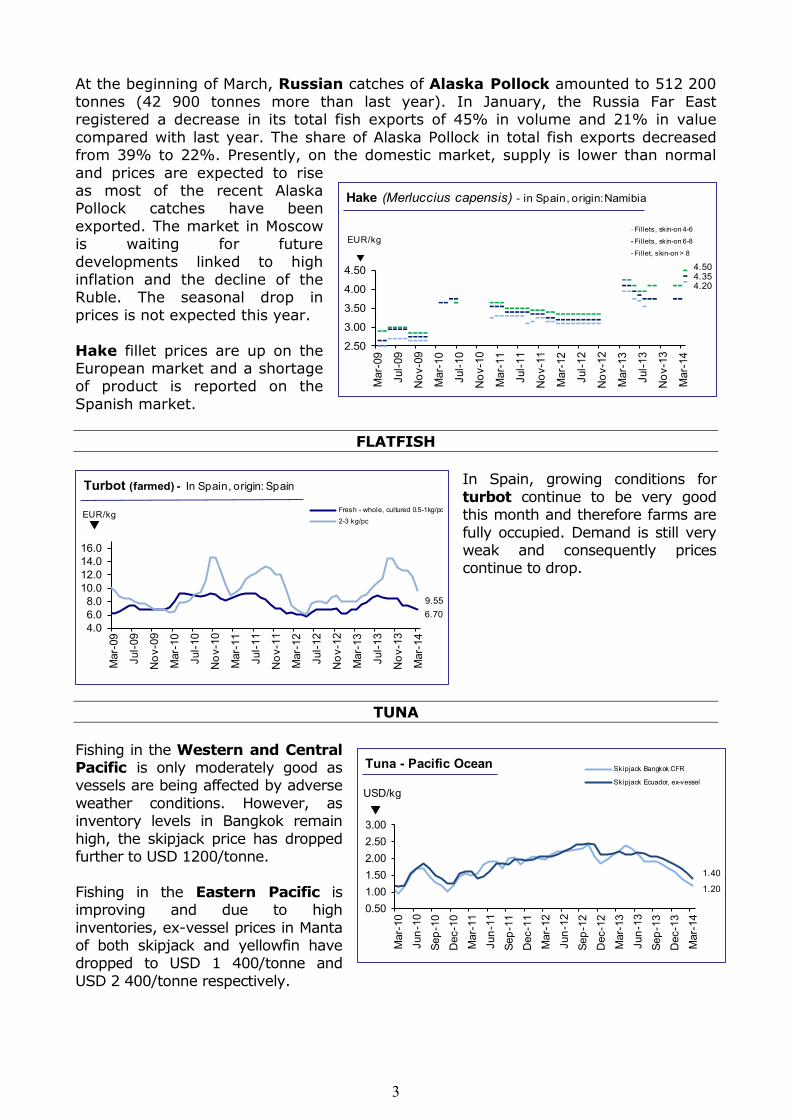

At the beginning of March, Russian catches of Alaska Pollock amounted to 512 200 tonnes (42 900 tonnes more than last year). In January, the Russia Far East registered a decrease in its total fish exports of 45% in volume and 21% in value compared with last year. The share of Alaska Pollock in total fish exports decreased from 39% to 22%. Presently, on the domestic market, supply is lower than normal and prices are expected to rise as most of the recent Alaska Pollock catches have been exported. The market in Moscow is waiting for future developments linked to high inflation and the decline of the Ruble. The seasonal drop in prices is not expected this year. Hake fillet prices are up on the European market and a shortage of product is reported on the Spanish market.

FLATFISH In Spain, growing conditions for turbot continue to be very good this month and therefore farms are fully occupied. Demand is still very weak and consequently prices continue to drop.

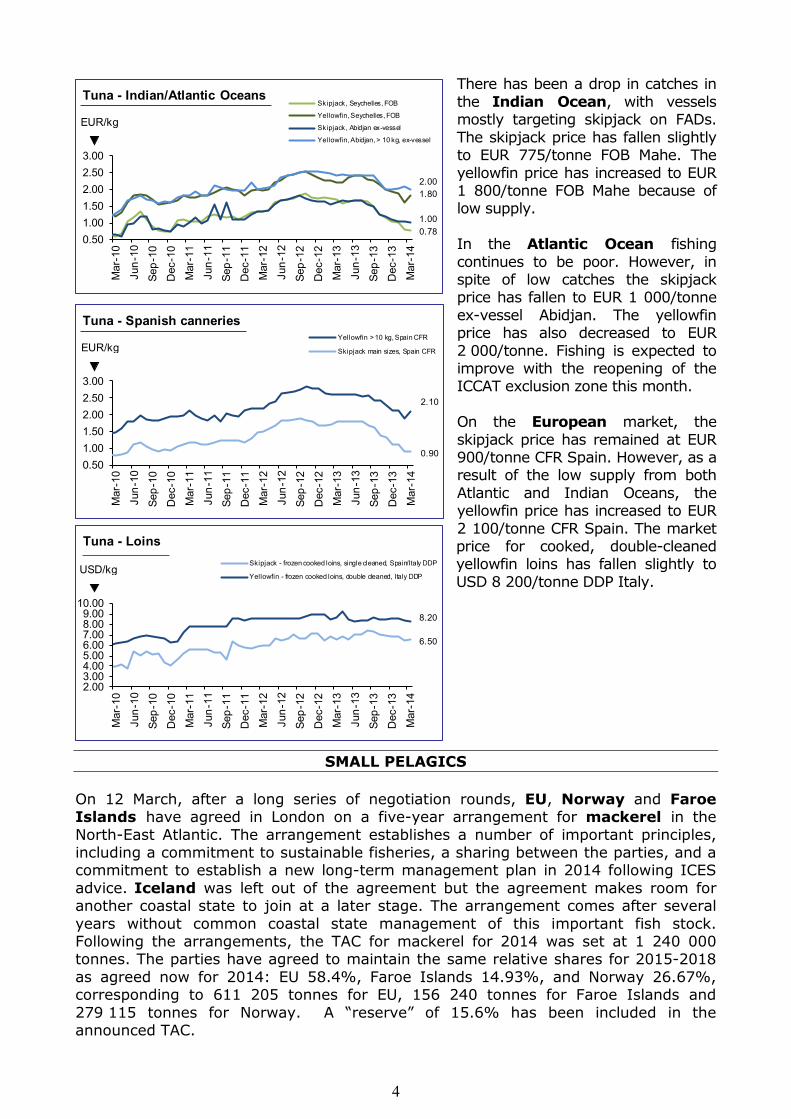

TUNA Fishing in the Western and Central Pacific is only moderately good as vessels are being affected by adverse weather conditions. However, as inventory levels in Bangkok remain high, the skipjack price has dropped further to USD 1200/tonne. Fishing in the Eastern Pacific is improving and due to high inventories, ex-vessel prices in Manta of both skipjack and yellowfin have dropped to USD 1 400/tonne and USD 2 400/tonne respectively.

4.354.20

4.50

2.50

3.00

3.50

4.00

4.50

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Fillets, skin-on 4-6

Fillets, skin-on 6-8

Fillet, skin-on > 8

EUR/kg

Hake (Merluccius capensis) - in Spain, origin: Namibia

6.709.55

4.06.08.0

10.012.014.016.0

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Turbot (farmed) - In Spain, origin: Spain

Fresh - whole, cultured 0.5-1kg/pc2-3 kg/pc

EUR/kg

1.40

1.20

0.501.001.502.002.503.00

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Skipjack Bangkok CFR

Skipjack Ecuador, ex-vessel

USD/kg

Tuna - Pacific Ocean

4

There has been a drop in catches in the Indian Ocean, with vessels mostly targeting skipjack on FADs. The skipjack price has fallen slightly to EUR 775/tonne FOB Mahe. The yellowfin price has increased to EUR 1 800/tonne FOB Mahe because of low supply. In the Atlantic Ocean fishing continues to be poor. However, in spite of low catches the skipjack price has fallen to EUR 1 000/tonne ex-vessel Abidjan. The yellowfin price has also decreased to EUR 2 000/tonne. Fishing is expected to improve with the reopening of the ICCAT exclusion zone this month. On the European market, the skipjack price has remained at EUR 900/tonne CFR Spain. However, as a result of the low supply from both Atlantic and Indian Oceans, the yellowfin price has increased to EUR 2 100/tonne CFR Spain. The market price for cooked, double-cleaned yellowfin loins has fallen slightly to USD 8 200/tonne DDP Italy.

SMALL PELAGICS On 12 March, after a long series of negotiation rounds, EU, Norway and Faroe Islands have agreed in London on a five-year arrangement for mackerel in the North-East Atlantic. The arrangement establishes a number of important principles, including a commitment to sustainable fisheries, a sharing between the parties, and a commitment to establish a new long-term management plan in 2014 following ICES advice. Iceland was left out of the agreement but the agreement makes room for another coastal state to join at a later stage. The arrangement comes after several years without common coastal state management of this important fish stock. Following the arrangements, the TAC for mackerel for 2014 was set at 1 240 000 tonnes. The parties have agreed to maintain the same relative shares for 2015-2018 as agreed now for 2014: EU 58.4%, Faroe Islands 14.93%, and Norway 26.67%, corresponding to 611 205 tonnes for EU, 156 240 tonnes for Faroe Islands and 279 115 tonnes for Norway. A “reserve” of 15.6% has been included in the announced TAC.

0.78

1.80

1.00

2.00

0.501.001.502.002.503.00

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Skipjack, Seychelles, FOB

Yellowfin, Seychelles, FOB

Skipjack, Abidjan ex-vessel

Yellowfin, Abidjan, > 10 kg, ex-vessel

EUR/kg

Tuna - Indian/Atlantic Oceans

6.50

8.20

2.003.004.005.006.007.008.009.00

10.00

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Skipjack - frozen cooked loins, single cleaned, Spain/Italy DDP

Yellowfin - frozen cooked loins, double cleaned, Italy DDPUSD/kg

Tuna - Loins

2.10

0.900.501.001.502.002.503.00

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Yellowfin > 10 kg, Spain CFR

Skipjack main sizes, Spain CFREUR/kg

Tuna - Spanish canneries

5

Following the conclusion of the above new coastal state mackerel agreement, another agreement was reached on 13 March between the European Union and the Faroe Islands on reciprocal exchanges of fishing opportunities in each other’s waters for 2014. This agreement follows a period of four years during which time the parties had not concluded arrangements, due to the long-standing mackerel dispute. So far, Russian catches of Pacific herring have decreased this year compared with 2013 because of a reduced number of fishing vessels. However, it is reported that in January the proportion of herring in total fish exports increased from 51.7% to 61.2% compared with January 2013. On the domestic market in Vladivostok the Pacific herring price is stable at EUR 0.36-0.44/kg for 200-300 gr/pc and EUR 0.65-0.69/kg for >300 gr/pc. At the wholesale market in Moscow the price is at EUR 0.56/kg for >250 gr/pc.

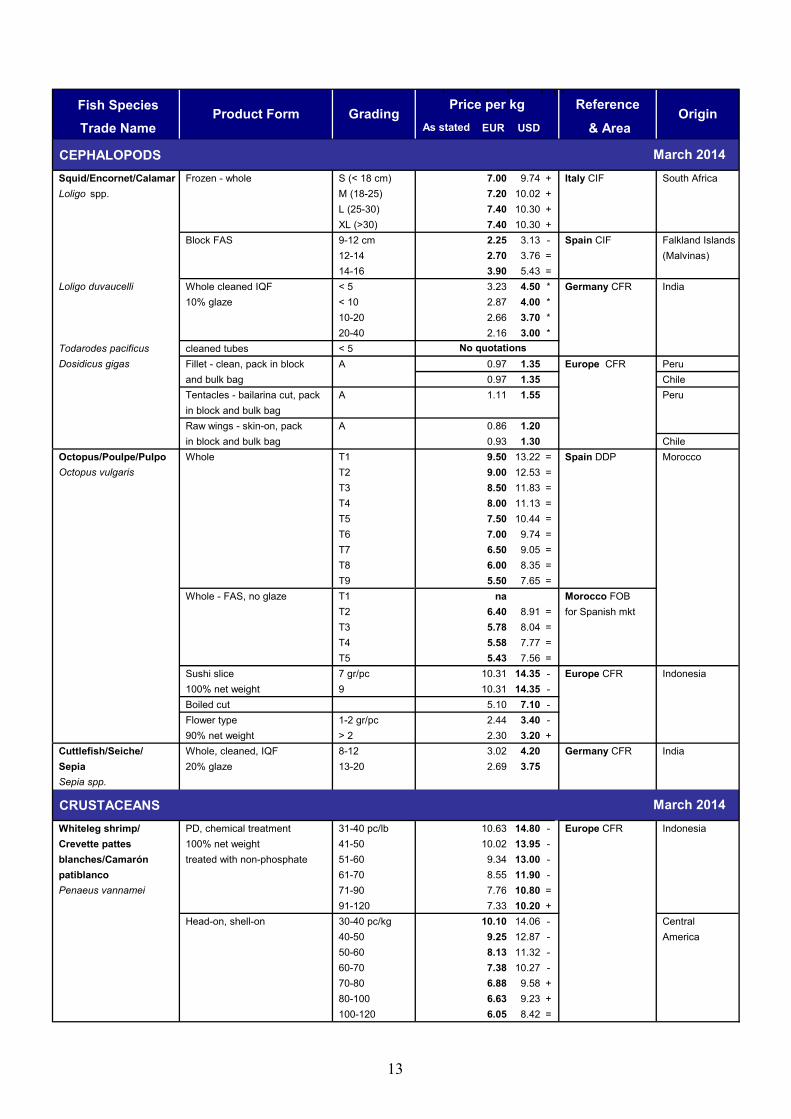

CEPHALOPODS In South African inshore waters, a season of fishing closure has been decided on for squid during the period April, May and June in order to try and encourage juvenile squid to settle on the spawning grounds. Presently local stocks are almost nil and prices are based on very low volumes.

CRUSTACEANS American lobster is out of season until 1 May and stocks are very low. Landings of European-caught crustaceans, such as Cancer pagurus and Homarus gammarus, have been very poor in February because of exceptionally difficult weather conditions and record-breaking wind forces. With low supply, prices remain consequently high.

7.20

3.004.005.006.007.008.00

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Squid - In Italy, origin: South Africa

Squid - Whole, FAS, size M EUR/kg

11.0013.5016.0018.5021.0023.50

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

- 11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

< 400 gr/pc

> 400CAN/kg

American Lobster - in Europe, origin: Canada

out

of

season

2.70

1.001.502.002.503.003.504.004.505.00

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul -1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

400-600 - 600-800 kg/pcEUR/kg

Crab (Cancer pagurus), origin: France

24.50

10.00

15.00

20.00

25.00

30.00

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

400-600/600-800 gr/pcEUR/kg

European Lobster, in Europe, origin Ireland

6

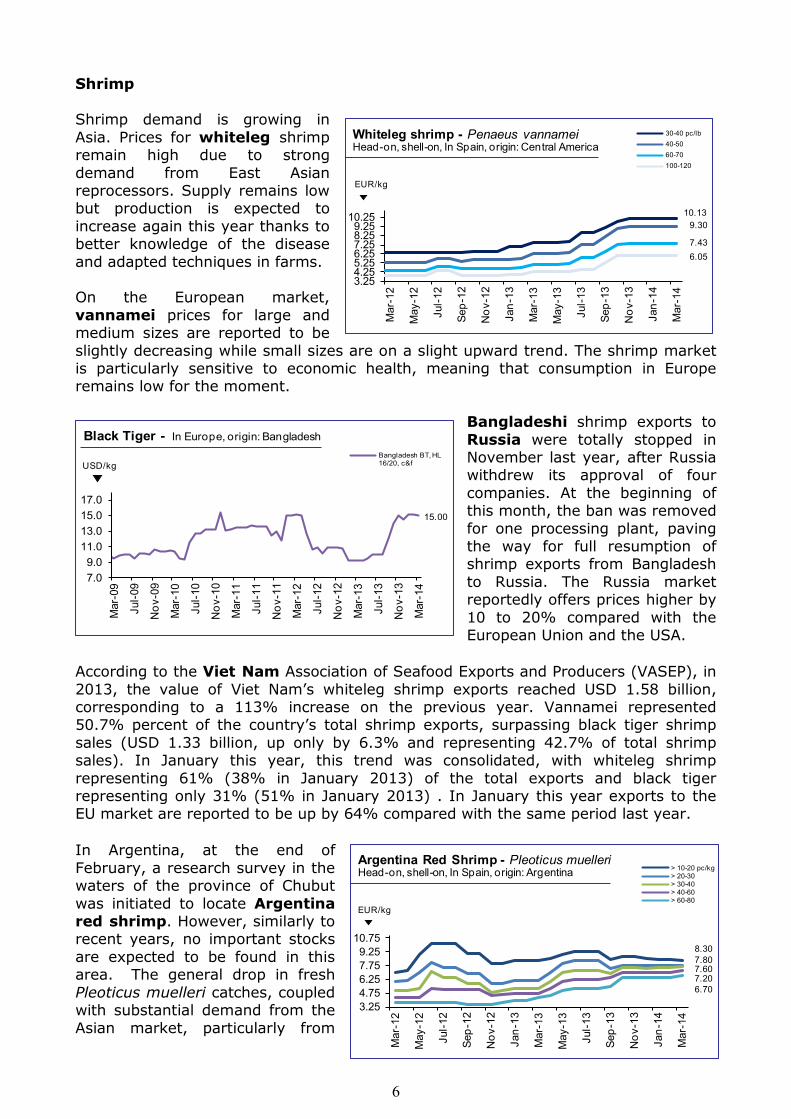

Shrimp Shrimp demand is growing in Asia. Prices for whiteleg shrimp remain high due to strong demand from East Asian reprocessors. Supply remains low but production is expected to increase again this year thanks to better knowledge of the disease and adapted techniques in farms. On the European market, vannamei prices for large and medium sizes are reported to be slightly decreasing while small sizes are on a slight upward trend. The shrimp market is particularly sensitive to economic health, meaning that consumption in Europe remains low for the moment.

Bangladeshi shrimp exports to Russia were totally stopped in November last year, after Russia withdrew its approval of four companies. At the beginning of this month, the ban was removed for one processing plant, paving the way for full resumption of shrimp exports from Bangladesh to Russia. The Russia market reportedly offers prices higher by 10 to 20% compared with the European Union and the USA.

According to the Viet Nam Association of Seafood Exports and Producers (VASEP), in 2013, the value of Viet Nam’s whiteleg shrimp exports reached USD 1.58 billion, corresponding to a 113% increase on the previous year. Vannamei represented 50.7% percent of the country’s total shrimp exports, surpassing black tiger shrimp sales (USD 1.33 billion, up only by 6.3% and representing 42.7% of total shrimp sales). In January this year, this trend was consolidated, with whiteleg shrimp representing 61% (38% in January 2013) of the total exports and black tiger representing only 31% (51% in January 2013) . In January this year exports to the EU market are reported to be up by 64% compared with the same period last year.

In Argentina, at the end of February, a research survey in the waters of the province of Chubut was initiated to locate Argentina red shrimp. However, similarly to recent years, no important stocks are expected to be found in this area. The general drop in fresh Pleoticus muelleri catches, coupled with substantial demand from the Asian market, particularly from

10.139.30

7.436.05

3.254.255.256.257.258.259.25

10.25

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

30-40 pc/lb40-5060-70100-120

EUR/kg

Whiteleg shrimp - Penaeus vannameiHead-on, shell-on, In Spain, origin: Central America

15.00

7.09.0

11.013.015.017.0

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Black Tiger - In Europe, origin: BangladeshBangladesh BT, HL 16/20, c&fUSD/kg

8.307.807.607.206.70

3.254.756.257.759.25

10.75

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

> 10-20 pc/kg> 20-30> 30-40> 40-60> 60-80

EUR/kg

Argentina Red Shrimp - Pleoticus muelleriHead-on, shell-on, In Spain, origin: Argentina

7

China and Japan, has pushed prices up at origin. In Europe, although the market is presently sluggish, sales of Argentina red shrimp are expected to resume soon in view of the Easter season. The shortage of supply - with only limited quantities of land-frozen shrimp - is anticipated to cause a price increase on the EU market when demand resumes.

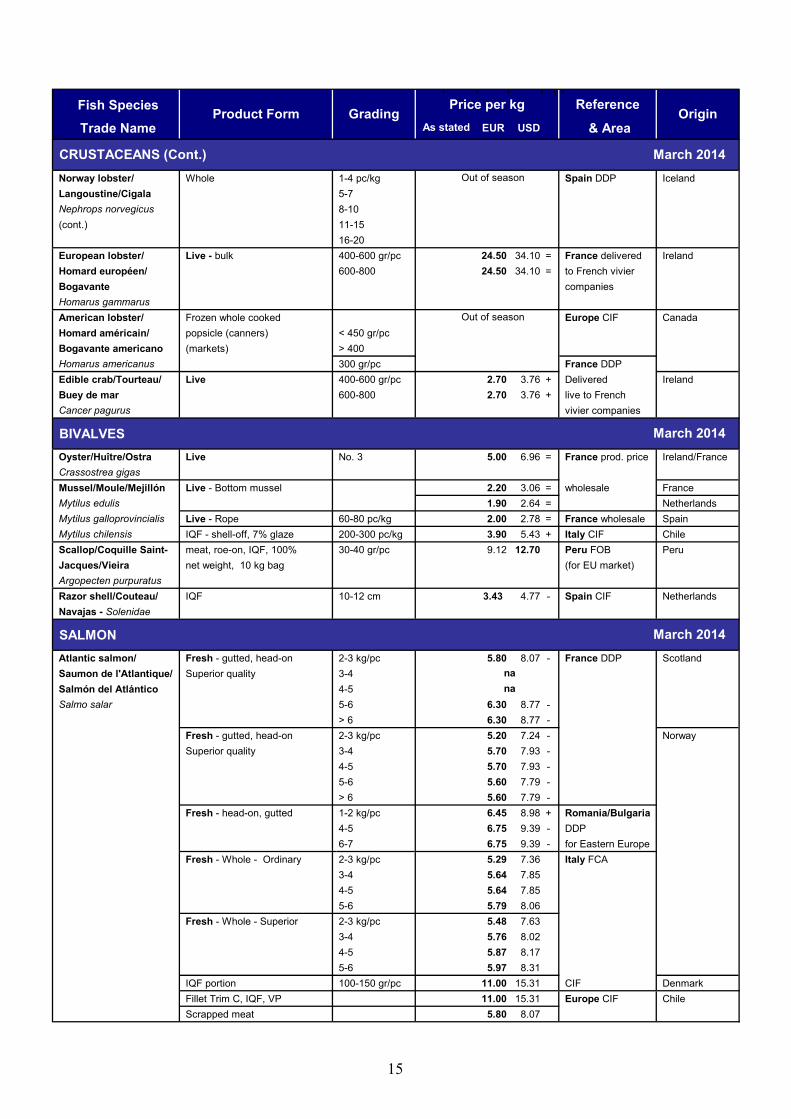

BIVALVES On the French market, a predominance of Dutch, Irish and Spanish mussels is reported as the French Bouchot season has come to an end. Oyster prices remain strong on the European market due to the decrease in supply as a consequence of the devastating herpes virus. However, the Spanish Agrifood Research and Technology Institute (owned by the Government of Catalonia) has recently developed oyster seeds free of the virus on the Ebro Delta waters which are expected to have higher survival rates compared with the spat which used to be imported from France.

SALMON

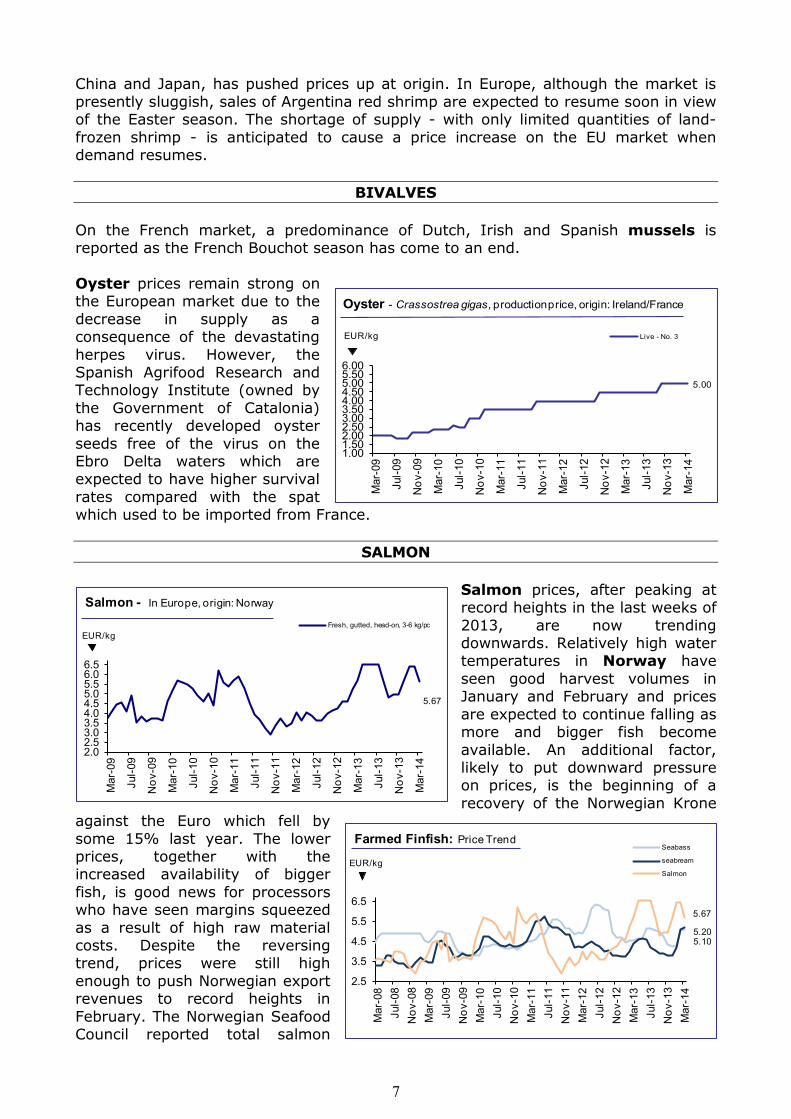

Salmon prices, after peaking at record heights in the last weeks of 2013, are now trending downwards. Relatively high water temperatures in Norway have seen good harvest volumes in January and February and prices are expected to continue falling as more and bigger fish become available. An additional factor, likely to put downward pressure on prices, is the beginning of a recovery of the Norwegian Krone

against the Euro which fell by some 15% last year. The lower prices, together with the increased availability of bigger fish, is good news for processors who have seen margins squeezed as a result of high raw material costs. Despite the reversing trend, prices were still high enough to push Norwegian export revenues to record heights in February. The Norwegian Seafood Council reported total salmon

5.00

1.001.502.002.503.003.504.004.505.005.506.00

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Live - No. 3EUR/kg

Oyster - Crassostrea gigas, production price, origin: Ireland/France

5.67

2.02.53.03.54.04.55.05.56.06.5

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Salmon - In Europe, origin: Norway

Fresh, gutted, head-on, 3-6 kg/pcEUR/kg

5.205.10

5.67

2.5

3.5

4.5

5.5

6.5

Mar

-08

Jul-0

8N

ov-0

8M

ar-0

9Ju

l-09

Nov

-09

Mar

-10

Jul-1

0N

ov-1

0M

ar-1

1Ju

l-11

Nov

-11

Mar

-12

Jul-1

2N

ov-1

2M

ar-1

3Ju

l-13

Nov

-13

Mar

-14

Farmed Finfish: Price TrendSeabass

seabream

SalmonEUR/kg

8

exports worth NOK 3.3 billion, 35% higher than February 2013, following on from a similarly record-breaking January figure. In terms of markets, the EU saw good year-on-year growth in February and Asian countries spent 48% more on Norwegian salmon than in February 2013. The USA also absorbed higher volumes at higher prices, while a 12% drop in volume to Russia still saw a 13% increase in value. Meanwhile UK salmon exports have increased four times in the last 5 years, for a total of GBP 200 million in 2013.

TROUT Growth in the salmon market is being largely mirrored by demand for trout, as the Norwegian Seafood Council reported exports of Norwegian trout increased by NOK 62 million or 45%, to a total of NOK 201 million in February 2014. Meanwhile, volumes were up by 5% compared with February 2013. Russia was the biggest market for Norwegian trout in February. In Southern Europe, the trout sector remains for the most part a domestic industry targeted at domestic consumers. In Turkey, which has become the largest trout producer in Europe, consolidation is now under way with more focus on value-added products for both domestic and international markets.

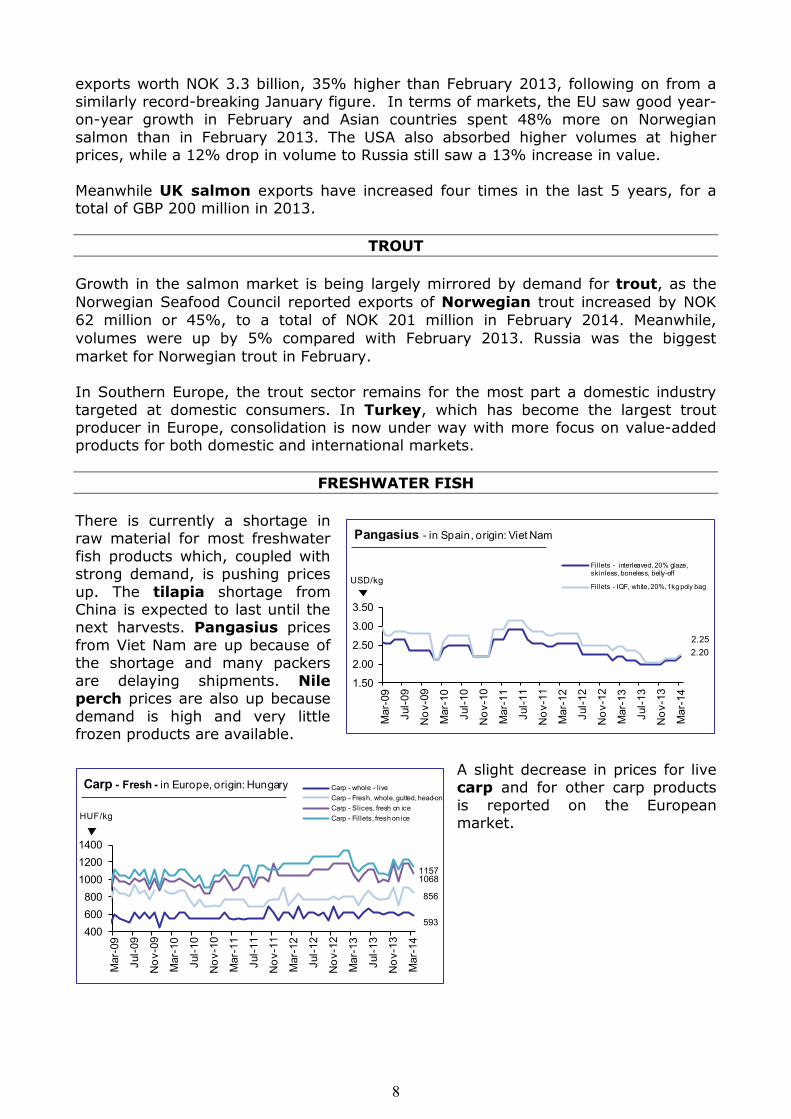

FRESHWATER FISH There is currently a shortage in raw material for most freshwater fish products which, coupled with strong demand, is pushing prices up. The tilapia shortage from China is expected to last until the next harvests. Pangasius prices from Viet Nam are up because of the shortage and many packers are delaying shipments. Nile perch prices are also up because demand is high and very little frozen products are available.

A slight decrease in prices for live carp and for other carp products is reported on the European market.

2.202.25

1.50

2.00

2.50

3.00

3.50

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Fillets - interleaved, 20% glaze, skinless, boneless, belly-off

Fillets - IQF, white, 20%, 1kg poly bagUSD/kg

Pangasius - in Spain, origin: Viet Nam

593

856

10681157

400600800

100012001400

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Carp - whole - liveCarp - Fresh, whole, gutted, head-onCarp - Slices, fresh on iceCarp - Fillets, fresh on iceHUF/kg

Carp - Fresh - in Europe, origin: Hungary

9

SEABASS/SEABREAM/MEAGRE

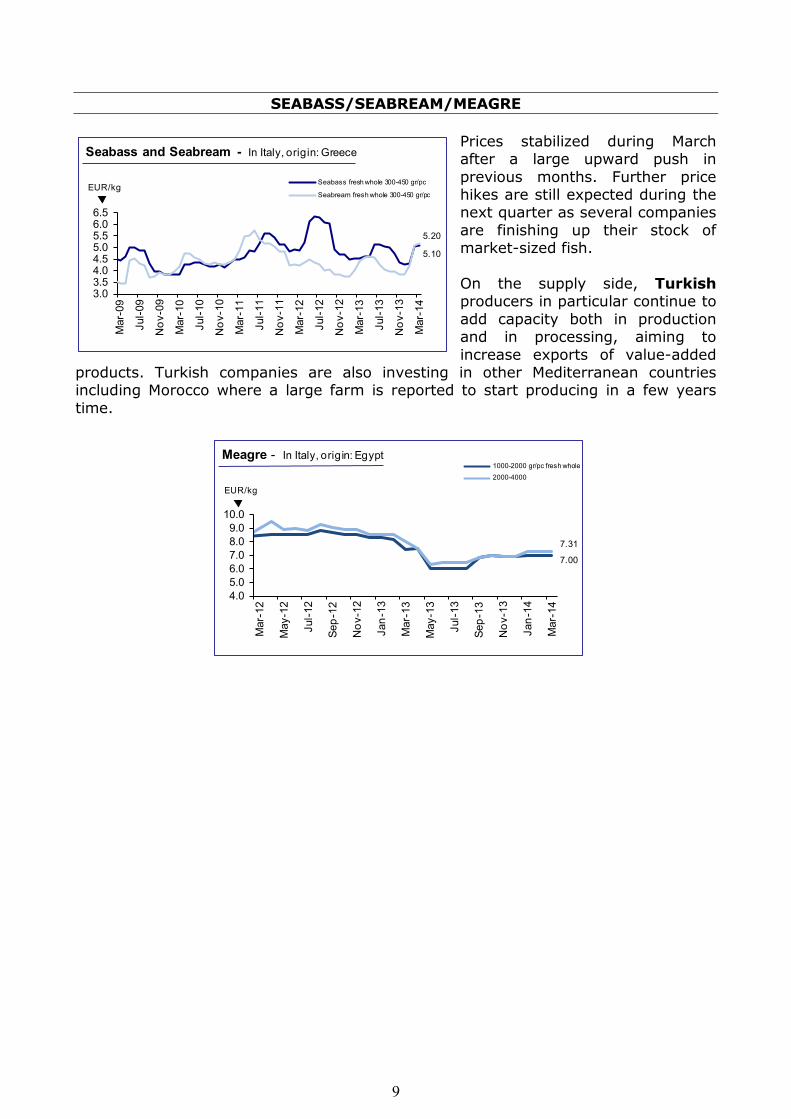

Prices stabilized during March after a large upward push in previous months. Further price hikes are still expected during the next quarter as several companies are finishing up their stock of market-sized fish. On the supply side, Turkish producers in particular continue to add capacity both in production and in processing, aiming to increase exports of value-added

products. Turkish companies are also investing in other Mediterranean countries including Morocco where a large farm is reported to start producing in a few years time.

5.20

5.10

3.03.54.04.55.05.56.06.5

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

- 11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Seabass and Seabream - In Italy, origin: Greece

Seabass fresh whole 300-450 gr/pc

Seabream fresh whole 300-450 gr/pcEUR/kg

7.00

7.31

4.05.06.07.08.09.0

10.0

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

Meagre - In Italy, origin: Egypt1000-2000 gr/pc fresh whole2000-4000

EUR/kg

10

Fish Species

Trade Name EUR USD & Area

Cod/Cabillaud, Morue/ Fresh gutted 1.24 1.73 - Poland FOB Baltic SeaBacalao IQF portion, single frozen 100-150 gr/pc 5.90 8.21 = Italy CIF IcelandGadus morhua Fresh - fillet 100-200 gr/pc 4.96 6.90 CPT Denmark

200-400 6.53 9.09Fresh - Whole 1-2 kg/pc 4.74 6.60

2-4 5.36 7.46Fillet - IQF - light salted 2.08 2.90 = Spain CFR Chinadouble frozen, 20% glazeFillet 4-8 oz 4.15 5.78 + FOB Russia

4-8 oz 4.60 6.40 + CIF Spain 8-16 4.60 6.40 + (origin: Barent16-32 4.40 6.12 + Sea)

H&G 1-3 kg/pc 2.20 3.06 FOB RussiaFillet - wet salted - 1st quality 700-1000 gr/pc 7.70 10.72 = Italy DDP Icelandproduced from fresh raw materialStockfish 700 gr/pc 16.00 22.27 - Norway

Gadus macrocephalus Fillet - wet salted - 1st quality 400-700 gr/pc 6.65 9.26 = CIP Denmarkproduced from frozen raw material

Hake/Merlu/Merluza B&P block Spain FOB Spain Merluccius capensis (origin: Barent

Sea)Minced block 1.58 2.20 = Namibia FOB Namibia

for Spanish marketFillet - skin-on, plate, 2-4 oz/pc 3.75 5.22 + Spain DDPlandfrozen 4-6 4.20 5.85 +

6-8 4.35 6.05 +8-12 4.50 6.26 +

IQF portion, trapeze 90-110 gr/pc 5.50 7.65 = Italy CIFMerluccius productus Fillet, PBO 2.42 3.37 = Spain CIF USA

Minced block 1.33 1.85 =Merluccius gayi H&G 100-200 gr/pc 1.08 1.50 Peru FOB Peru

0.93 1.30 (for EU market) EcuadorHoki - Grenadier/ Block Spain CIF ChileGrenadier/Merluza Block - PBO ArgentinaMacruronus magellanicusMacruronus Pieces block CIF New Zealandnovaezelandiae Fillet block 2.48 3.45 =Alaska pollack/Lieu Fillet (for baby food) Europe DAP USAde l'Alaska/Colínde AlaskaTheragra chalcogrammaSurimi (Alaska pollack) Stick - Paprika 250 gr/pc 2.41 3.35 France CFR SpainSaithe/Lieu noir/ Minced A Europe DDP NorwayCarbonero (Pollock, Coley) (for baby food)Pollachius virens Fillet - skinless, PBI, interleaved 16-35 oz 3.80 5.29 + Spain DDP IcelandMonkfish/Baudroie/ Fresh - Tail 0.3-0.5 kg/pc 11.09 15.43 Italy CPT UKRape 0.5-1 11.80 16.42Lophius spp. 1-2 12.22 17.01

> 2 12.58 17.51Fresh - whole 0.5-1 kg/pc 5.40 7.52 FCA France

1-2 5.50 7.65Tails, skin-off, IWP 100-250 gr/pc 5.75 8.00 = Spain DDP Namibia

250-500 6.75 9.39 +500-1000 8.00 11.13 +> 1000 8.75 12.18 +

Product Form GradingReference

GROUNDFISH

Price per kg

No quotations

No quotations

No quotations

March 2014

Origin

na

As stated

11

Fish Species

Trade Name EUR USD & AreaProduct Form Grading

ReferencePrice per kgOrigin

As stated

Haddock/Eglefin/Eglofino H&G < 0.8 kg/pc NOK 22.00 2.65 3.69 Sweden FCA Norway/Melanogrammus DenmarkaeglefinusLing/Lingue franche/ Fillet - wet salted 1-1.5 kg/pc 4.80 6.68 - Italy DDP Faeroe IslandsMaruca Produced from fresh raw materialMolva molva high quality

Turbot/Rodaballo Fresh - whole 0.5-1 kg/pc 6.70 9.32 - Spain CIF Spain Psetta maxima cultured 1-2 7.30 10.16 -

2-3 9.55 13.29 -3-4 13.40 18.65 -

Fresh - whole 0.5-1 kg/pc 10.90 15.17 - Netherlandswild 1-2 11.60 16.14 -

2-3 12.50 17.40 -3-4 15.80 21.99 -4-6 17.80 24.77 -> 6 20.30 28.25 -

Fresh - whole 0.8-1 kg/pc 7.00 9.74 Italy FCA Spain1.5-2 8.30 11.551-1.5 7.70 10.722-2.5 10.20 14.200.5-1 kg/pc 8.76 12.19 Netherlands0.7-1 10.20 14.201-2 11.70 16.28> 3 13.20 18.37

Sole/Sole/ Fresh - whole < 170 gr/pc 8.60 11.97 - Spain CIFLenguado wild 160-220 8.70 12.11 -Solea vulgaris 210-300 9.60 13.36 -

300-400 10.80 15.03 -400-600 14.70 20.46 -600-800 15.20 21.16 -800-1000 13.80 19.21 -

Fresh - whole No. 1 4.50 6.26 -No. 2 3.30 4.59 -No. 3 3.30 4.59 -No. 4 3.20 4.45 -

Fresh - whole No. 3 10.95 15.24 Italy CIFNo. 4 9.75 13.57

Fresh - gutted No. 2 14.10 19.62 FCANo. 3 10.93 15.21No. 4 9.44 13.14No. 5 7.63 10.62

European plaice/ Fresh - whole 150-300 gr/pc Spain CIFPlie d'Europe/ 300-400Solla europea 400-600Pleuronectes platessa IQF, white skin-on, 25% glaze No. 2 3.90 5.43 = Netherlands FOB

IQF skin-off, 25% glaze 4.20 5.85 = for Italian marketEuropean Flounder/ Fresh - whole 1.49 2.07 Italy CPT DenmarkFlet d'Europe/Platija europeaPlatichthys flesus Fillet CIF Netherlands

Fresh - whole 1.90 2.64 FCA

March 2014

FLATFISH

No quotations

na

GROUNDFISH (Cont.)

March 2014

12

Fish Species

Trade Name EUR USD & AreaProduct Form Grading

ReferencePrice per kgOrigin

As stated

Tuna/Thon/Atún Skipjack - whole main size 0.86 1.20 - Bangkok CFR Western/CentralThunnus spp. Pacific Ocean

Skipjack - whole 1.01 1.40 - Ecuador Eastern TropicalYellowfin - whole 1.72 2.40 * ex-vessel Pacific OceanSkipjack - whole main size 0.78 1.08 - Seychelles Indian OceanYellowfin - whole 1.80 2.51 + FOBSkipjack - whole 1.00 1.39 - Abidjan Atlantic OceanYellowfin - whole > 10 kg 2.00 2.78 - ex-vesselSkipjack - whole 1.8-3.4 kg/pc 0.90 1.25 = Spanish Various originsYellowfin - whole > 10 kg 2.10 2.92 + Canneries CFRSkipjack - cooked & cleaned single cleaned 4.67 6.50 + Italy DDP Solomon Islandsloins - vacuum packedYellowfin - cooked & cleaned double cleaned 5.89 8.20 - Ghana/Mauri-loins - vacuum packed tius/Solomon Is.Yellowfin - in olive oil, glass jar 190 gr net weight 1.70 2.37 CFR Portugalproduced from fresh raw material 130 gr drained weight (Azores Islands)Yellowfin - whole > 10 kg/pc na Spain CIF Eastern PacificBigeye - whole > 10 kg 1.80 2.51 = DAT Indian OceanSkipjack - whole > 1.8 kg/pc 1.00 1.39 * Atlantic OceanYellowfin - whole 3-10 kg/pc 1.50 2.09 - DAT

> 10 2.10 2.92 *Yellowfin - loins 5.40 7.52 + CIF Eastern PacificSkipjack - loins 4.20 5.85 - OceanSkipjack - pre-cooked loins 3.59 5.00 Ecuador FOB EcuadorYellowfin - pre-cooked loins single cleaning 4.10 5.70 (for European mkt)

double cleaning 4.53 6.30Skipjack - whole, raw material 1.9-3.4 kg/pc 1.11 1.55 *

3.5-5 1.15 1.60 *Skipjack - canned 170 gr net weight 20.65 28.75 *chunks in brine 120 gr drained weight

Skipjack - canned 185 gr net weight 28.23 39.30 *chunks in brine 130 gr drained weight

Skipjack - canned 170 gr net weight 25.86 36.00 *shredded in soyabean oil 120 gr drained weight

Skipjack - canned 185 gr net weight 28.74 40.00 *shredded in soyabean oil 130 gr drained weight

Skipjack - canned 170 gr net weight 16.88 23.50 *shredded in soyabean oil 120 gr drained weight

Skipjack - canned 195 gr net weight 34.05 47.40 * Germany CFRsolid pack in brine 150 gr drained weight

Swordfish/Espadon/ Seafrozen 30-50 kg/pc 5.00 6.96 + Spain FOT SpainPez espada 50-70 5.10 7.10 +Xiphias gladius

Mackerel/Maquereau/ Fresh - whole 2.24 3.12 Italy CPT FranceCaballa Whole 200-400 gr/pc na Netherlands FOB UKScomber scombrus 300-500 1.50 2.09 = for Eastern EuropeHerring/Hareng/Arenque Fresh - fillet 2.83 3.94 Italy CPT DenmarkClupeidae Fresh - whole 70-100 gr/pc 0.43 0.60 = Poland FOB BalticSprat/Sprat/Espadín 0.32 0.44 =Sprattus sprattusSardine/Sardine/ Fresh - whole 1.08 1.50 Italy CPT CroatiaSardina 1.35 1.88 SpainSardina pilchardus

per jar

SMALL PELAGICS

TUNAS/BILLFISHES March 2014

March 2014

13

Fish Species

Trade Name EUR USD & AreaProduct Form Grading

ReferencePrice per kgOrigin

As stated

CEPHALOPODSSquid/Encornet/Calamar Frozen - whole S (< 18 cm) 7.00 9.74 + Italy CIF South AfricaLoligo spp. M (18-25) 7.20 10.02 +

L (25-30) 7.40 10.30 +XL (>30) 7.40 10.30 +

Block FAS 9-12 cm 2.25 3.13 - Spain CIF Falkland Islands12-14 2.70 3.76 = (Malvinas)14-16 3.90 5.43 =

Loligo duvaucelli Whole cleaned IQF < 5 3.23 4.50 * Germany CFR India10% glaze < 10 2.87 4.00 *

10-20 2.66 3.70 *20-40 2.16 3.00 *

Todarodes pacificus cleaned tubes < 5Dosidicus gigas Fillet - clean, pack in block A 0.97 1.35 Europe CFR Peru

and bulk bag 0.97 1.35 ChileTentacles - bailarina cut, pack A 1.11 1.55 Peruin block and bulk bagRaw wings - skin-on, pack A 0.86 1.20in block and bulk bag 0.93 1.30 Chile

Octopus/Poulpe/Pulpo Whole T1 9.50 13.22 = Spain DDP MoroccoOctopus vulgaris T2 9.00 12.53 =

T3 8.50 11.83 =T4 8.00 11.13 =T5 7.50 10.44 =T6 7.00 9.74 =T7 6.50 9.05 =T8 6.00 8.35 =T9 5.50 7.65 =

Whole - FAS, no glaze T1 na Morocco FOBT2 6.40 8.91 = for Spanish mktT3 5.78 8.04 =T4 5.58 7.77 =T5 5.43 7.56 =

Sushi slice 7 gr/pc 10.31 14.35 - Europe CFR Indonesia100% net weight 9 10.31 14.35 -Boiled cut 5.10 7.10 -Flower type 1-2 gr/pc 2.44 3.40 -90% net weight > 2 2.30 3.20 +

Cuttlefish/Seiche/ Whole, cleaned, IQF 8-12 3.02 4.20 Germany CFR IndiaSepia 20% glaze 13-20 2.69 3.75Sepia spp.

CRUSTACEANSWhiteleg shrimp/ PD, chemical treatment 31-40 pc/lb 10.63 14.80 - Europe CFR IndonesiaCrevette pattes 100% net weight 41-50 10.02 13.95 -blanches/Camarón treated with non-phosphate 51-60 9.34 13.00 -patiblanco 61-70 8.55 11.90 -Penaeus vannamei 71-90 7.76 10.80 =

91-120 7.33 10.20 +Head-on, shell-on 30-40 pc/kg 10.10 14.06 - Central

40-50 9.25 12.87 - America50-60 8.13 11.32 -60-70 7.38 10.27 -70-80 6.88 9.58 +80-100 6.63 9.23 +100-120 6.05 8.42 =

No quotations

March 2014

March 2014

14

Fish Species

Trade Name EUR USD & AreaProduct Form Grading

ReferencePrice per kgOrigin

As stated

Whiteleg shrimp/ Head-on, shell-on 30-40 pc/kg 7.97 11.10 South/Central EcuadorCrevette pattes 40-50 6.90 9.60 America FOBblanches/Camarón 50-60 6.18 8.60 for European mainpatiblanco 60-70 5.89 8.20 portsPenaeus vannamei 70-80 5.68 7.90(cont.) Headless, shell-on 26-30 Germany CFR

IQF, 25% glazePD,100% net weight 60-80 kg/pc 7.90 11.00 India

70.90 7.62 10.6090-110 7.33 10.20

Argentine red shrimp/ Head-on, shell-on > 10-20 pc/kg 8.30 11.55 - Spain EXW ArgentinaSalicoque rouge/ > 20-30 7.80 10.86 =d'Argentine/Camarón > 30-40 7.60 10.58 +langostín argentino > 40-60 7.20 10.02 +Pleoticus muelleri > 60-80 6.70 9.32 +

FAS 10-20 8.00 11.13 = CIF20-30 7.75 10.79 +30-40 7.30 10.16 +40-60 6.70 9.32 =

Black tiger/Crevette Head-on, shell-on < 10 18.03 25.10 * Europe CFR Viet Namtigrée/Camarón tigre 100% net weight < 12 17.46 24.30 *Penaeus monodon < 15 14.87 20.70 *

Head-on, shell-on 6-8 kg/pc 10.13 14.10 * Bangladesh25% glaze 8-12 9.27 12.90 *

13-15 8.69 12.10 *16-20 7.62 10.60 *21-30 6.83 9.50 *31-40 6.14 8.55 *

Headless 16-20 10.78 15.00 *20% glaze, IQF 21-25 10.06 14.00 *

26-30 9.20 12.80 *31-40 8.62 12.00 *41-50 7.97 11.10 *51-80 7.40 10.30 *

Norway lobster/ Fresh - Whole 21-30 pc/kg 11.05 15.38 - Spain DDP NetherlandsLangoustine/Cigala 4X1.5 kg 16-20 12.80 17.81 -Nephrops norvegicus 10-15 15.30 21.29 -

8-12 18.80 26.17 -6-9 23.80 33.12 -4-7 29.30 40.78 *3-5 na> 40 pc/kg 8.20 11.41 Scotland31-40 9.50 13.2221-30 11.70 16.2816-20 14.20 19.7610-15 17.20 23.946-10 21.80 30.34

Whole 00 11.85 16.49 = CIF0 10.20 14.20 =1 9.15 12.73 =2 8.15 11.34 =3 7.15 9.95 =4 5.85 8.14 =5 5.15 7.17 =

CRUSTACEANS (Cont.) March 2014

No quotations

15

Fish Species

Trade Name EUR USD & AreaProduct Form Grading

ReferencePrice per kgOrigin

As stated

Norway lobster/ Whole 1-4 pc/kg Spain DDP IcelandLangoustine/Cigala 5-7Nephrops norvegicus 8-10(cont.) 11-15

16-20European lobster/ Live - bulk 400-600 gr/pc 24.50 34.10 = France delivered IrelandHomard européen/ 600-800 24.50 34.10 = to French vivierBogavante companiesHomarus gammarusAmerican lobster/ Frozen whole cooked Europe CIF CanadaHomard américain/ popsicle (canners) < 450 gr/pcBogavante americano (markets) > 400Homarus americanus 300 gr/pc France DDPEdible crab/Tourteau/ Live 400-600 gr/pc 2.70 3.76 + Delivered IrelandBuey de mar 600-800 2.70 3.76 + live to FrenchCancer pagurus vivier companies

BIVALVESOyster/Huître/Ostra Live No. 3 5.00 6.96 = France prod. price Ireland/FranceCrassostrea gigasMussel/Moule/Mejillón Live - Bottom mussel 2.20 3.06 = wholesale FranceMytilus edulis 1.90 2.64 = NetherlandsMytilus galloprovincialis Live - Rope 60-80 pc/kg 2.00 2.78 = France wholesale SpainMytilus chilensis IQF - shell-off, 7% glaze 200-300 pc/kg 3.90 5.43 + Italy CIF ChileScallop/Coquille Saint- meat, roe-on, IQF, 100% 30-40 gr/pc 9.12 12.70 Peru FOB PeruJacques/Vieira net weight, 10 kg bag (for EU market)Argopecten purpuratusRazor shell/Couteau/ IQF 10-12 cm 3.43 4.77 - Spain CIF NetherlandsNavajas - Solenidae

SALMONAtlantic salmon/ Fresh - gutted, head-on 2-3 kg/pc 5.80 8.07 - France DDP ScotlandSaumon de l'Atlantique/ Superior quality 3-4Salmón del Atlántico 4-5Salmo salar 5-6 6.30 8.77 -

> 6 6.30 8.77 -Fresh - gutted, head-on 2-3 kg/pc 5.20 7.24 - NorwaySuperior quality 3-4 5.70 7.93 -

4-5 5.70 7.93 -5-6 5.60 7.79 -> 6 5.60 7.79 -

Fresh - head-on, gutted 1-2 kg/pc 6.45 8.98 + Romania/Bulgaria4-5 6.75 9.39 - DDP6-7 6.75 9.39 - for Eastern Europe

Fresh - Whole - Ordinary 2-3 kg/pc 5.29 7.36 Italy FCA3-4 5.64 7.854-5 5.64 7.855-6 5.79 8.06

Fresh - Whole - Superior 2-3 kg/pc 5.48 7.633-4 5.76 8.024-5 5.87 8.175-6 5.97 8.31

IQF portion 100-150 gr/pc 11.00 15.31 CIF DenmarkFillet Trim C, IQF, VP 11.00 15.31 Europe CIF ChileScrapped meat 5.80 8.07

CRUSTACEANS (Cont.) March 2014

nana

Out of season

March 2014

March 2014

Out of season

16

Fish Species

Trade Name EUR USD & AreaProduct Form Grading

ReferencePrice per kgOrigin

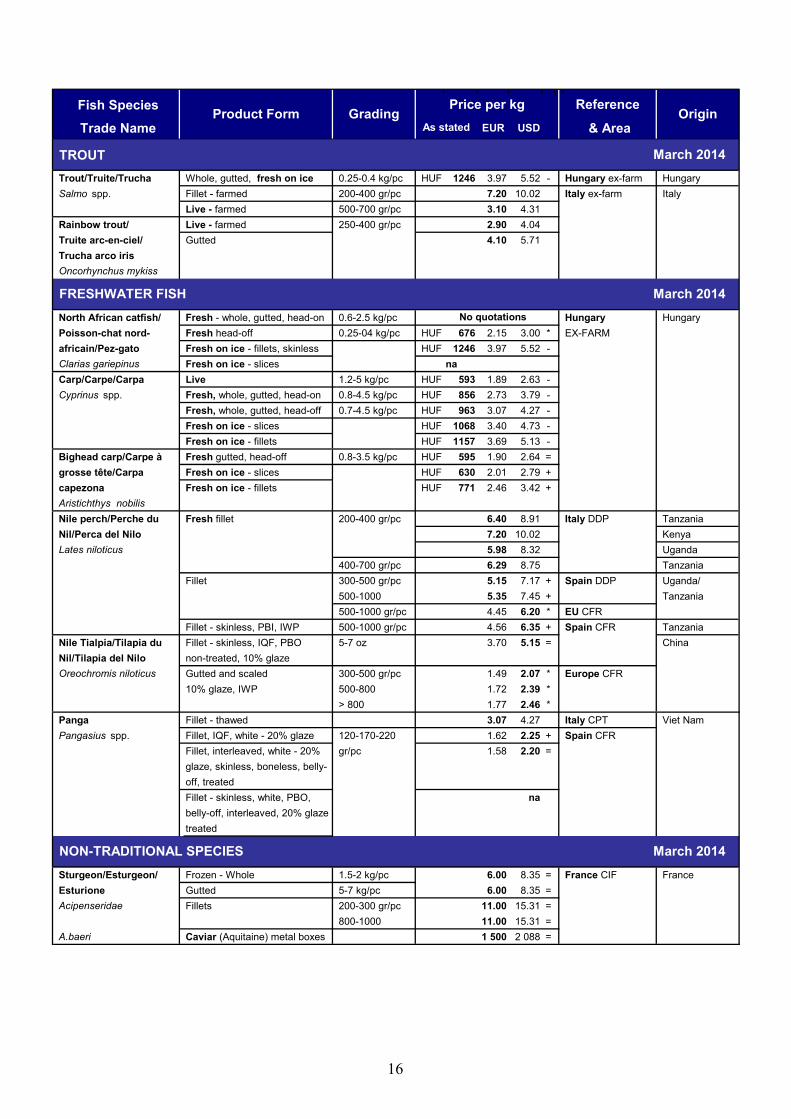

As stated

TROUTTrout/Truite/Trucha Whole, gutted, fresh on ice 0.25-0.4 kg/pc HUF 1246 3.97 5.52 - Hungary ex-farm HungarySalmo spp. Fillet - farmed 200-400 gr/pc 7.20 10.02 Italy ex-farm Italy

Live - farmed 500-700 gr/pc 3.10 4.31Rainbow trout/ Live - farmed 250-400 gr/pc 2.90 4.04Truite arc-en-ciel/ Gutted 4.10 5.71Trucha arco irisOncorhynchus mykiss

North African catfish/ Fresh - whole, gutted, head-on 0.6-2.5 kg/pc Hungary HungaryPoisson-chat nord- Fresh head-off 0.25-04 kg/pc HUF 676 2.15 3.00 * EX-FARMafricain/Pez-gato Fresh on ice - fillets, skinless HUF 1246 3.97 5.52 -Clarias gariepinus Fresh on ice - slices naCarp/Carpe/Carpa Live 1.2-5 kg/pc HUF 593 1.89 2.63 -Cyprinus spp. Fresh, whole, gutted, head-on 0.8-4.5 kg/pc HUF 856 2.73 3.79 -

Fresh, whole, gutted, head-off 0.7-4.5 kg/pc HUF 963 3.07 4.27 -Fresh on ice - slices HUF 1068 3.40 4.73 -Fresh on ice - fillets HUF 1157 3.69 5.13 -

Bighead carp/Carpe à Fresh gutted, head-off 0.8-3.5 kg/pc HUF 595 1.90 2.64 =grosse tête/Carpa Fresh on ice - slices HUF 630 2.01 2.79 +capezona Fresh on ice - fillets HUF 771 2.46 3.42 +Aristichthys nobilisNile perch/Perche du Fresh fillet 200-400 gr/pc 6.40 8.91 Italy DDP TanzaniaNil/Perca del Nilo 7.20 10.02 KenyaLates niloticus 5.98 8.32 Uganda

400-700 gr/pc 6.29 8.75 TanzaniaFillet 300-500 gr/pc 5.15 7.17 + Spain DDP Uganda/

500-1000 5.35 7.45 + Tanzania500-1000 gr/pc 4.45 6.20 * EU CFR

Fillet - skinless, PBI, IWP 500-1000 gr/pc 4.56 6.35 + Spain CFR TanzaniaNile Tialpia/Tilapia du Fillet - skinless, IQF, PBO 5-7 oz 3.70 5.15 = ChinaNil/Tilapia del Nilo non-treated, 10% glazeOreochromis niloticus Gutted and scaled 300-500 gr/pc 1.49 2.07 * Europe CFR

10% glaze, IWP 500-800 1.72 2.39 *> 800 1.77 2.46 *

Panga Fillet - thawed 3.07 4.27 Italy CPT Viet NamPangasius spp. Fillet, IQF, white - 20% glaze 120-170-220 1.62 2.25 + Spain CFR

Fillet, interleaved, white - 20% gr/pc 1.58 2.20 =glaze, skinless, boneless, belly-off, treatedFillet - skinless, white, PBO, nabelly-off, interleaved, 20% glazetreated

Sturgeon/Esturgeon/ Frozen - Whole 1.5-2 kg/pc 6.00 8.35 = France CIF FranceEsturione Gutted 5-7 kg/pc 6.00 8.35 =Acipenseridae Fillets 200-300 gr/pc 11.00 15.31 =

800-1000 11.00 15.31 =A.baeri Caviar (Aquitaine) metal boxes 1 500 2 088 =

FRESHWATER FISH March 2014

March 2014 NON-TRADITIONAL SPECIES

No quotations

March 2014

17

Fish Species

Trade Name EUR USD & AreaProduct Form Grading

ReferencePrice per kgOrigin

As stated

Seabass/Bar, Fresh - whole 200-300 gr/pc 4.15 5.78 = Greece FOB GreeceLoup/Lubina farmed 300-450 4.90 6.82 +Dicentrarchus labrax 400-600 5.30 7.38 +

600-800 6.75 9.39 +800-1000 8.75 12.18 +> 1000 9.75 13.57 +

200-300 gr/pc 4.35 6.05 = Italy CIF

300-450 5.10 7.10 +450-600 5.50 7.65 +600-800 6.95 9.67 +800-1000 8.95 12.46 +> 1000 9.95 13.85 +200-300 gr/pc 4.40 6.12 = France CIF300-450 5.15 7.17 +450-600 5.55 7.72 +600-800 7.00 9.74 +800-1000 9.00 12.53 +> 1000 10.00 13.92 +200-300 gr/pc 4.39 6.11 = Spain CIF300-450 5.14 7.15 +450-600 5.54 7.71 +600-800 6.99 9.73 +800-1000 8.99 12.51 +> 1000 9.99 13.90 +200-300 gr/pc 4.42 6.15 = Germany CIF300-450 5.17 7.20 +450-600 5.57 7.75 +600-800 7.02 9.77 +800-1000 9.02 12.55 +> 1000 10.02 13.95 +200-300 gr/pc 4.40 6.12 = Portugal CIF300-450 5.15 7.17 +450-600 5.55 7.72 +600-800 7.00 9.74 +800-1000 9.00 12.53 +

> 1000 10.00 13.92 +

200-300 gr/pc 4.58 6.37 = UK CIF300-450 5.33 7.42 +450-600 5.73 7.97 +600-800 7.18 9.99 +800-1000 9.18 12.78 +

> 1000 10.18 14.17 +

Fresh - whole 200-300 gr/pc 3.80 5.29 + Greece EXWfarmed 300-400 4.90 6.82 + for Eastern Europe

400-600 5.50 7.65 +600-800 6.70 9.32 =800-1000 11.60 16.14 => 1000 12.60 17.54 =

Fresh - whole - wild 600-800 10.17 14.15 Italy CPT EgyptMediterranean 800-1000 10.25 14.27

1000-2000 10.83 15.07> 2000 11.25 15.66

SEABASS/SEABREAM/MEAGRE March 2014

18

Fish Species

Trade Name EUR USD & AreaProduct Form Grading

ReferencePrice per kgOrigin

As stated

Gilthead seabream/ Fresh - whole 200-300 gr/pc 4.55 6.33 - Greece FOB GreeceDorade royale/Dorada farmed 300-450 5.00 6.96 =Sparus aurata 450-600 5.00 6.96 -

600-800 5.45 7.59 =800-1000 7.20 10.02 =

> 1000 8.05 11.20 =

200-300 gr/pc 4.75 6.61 - Italy CIF300-450 5.20 7.24 =450-600 5.20 7.24 -600-800 5.65 7.86 =800-1000 7.40 10.30 => 1000 8.25 11.48 =200-300 gr/pc 4.80 6.68 - France CIF300-450 5.25 7.31 =450-600 5.25 7.31 -600-800 5.70 7.93 =800-1000 7.45 10.37 =

> 1000 8.30 11.55 =

200-300 gr/pc 4.79 6.67 - Spain CIF300-450 5.24 7.29 =450-600 5.24 7.29 -600-800 5.69 7.92 =800-1000 7.44 10.35 => 1000 8.29 11.54 =200-300 gr/pc 4.82 6.71 - Germany CIF300-450 5.27 7.33 =450-600 5.27 7.33 -600-800 5.72 7.96 =800-1000 7.47 10.40 => 1000 8.32 11.58 =200-300 gr/pc 4.80 6.68 - Portugal CIF300-450 5.25 7.31 =450-600 5.25 7.31 -600-800 5.70 7.93 =800-1000 7.45 10.37 =

> 1000 8.30 11.55 =

200-300 gr/pc 4.98 6.93 - UK CIF300-450 5.43 7.56 =450-600 5.43 7.56 -600-800 5.88 8.18 =800-1000 7.63 10.62 =

> 1000 8.48 11.80 =

200-300 gr/pc 5.00 6.96 + Greece EXW300-400 5.00 6.96 + for Eastern Europe400-600 5.00 6.96 +600-800 5.30 7.38 +800-1000 7.20 10.02 -> 1000 na

Fresh - whole - wild 800-1000 gr/pc 12.81 17.83 Italy FCA MoroccoAtlantic 1000-2000 14.64 20.38

> 2000 13.49 18.78

SEABASS/SEABREAM/MEAGRE (cont.) March 2014

19

Fish Species

Trade Name EUR USD & AreaProduct Form Grading

ReferencePrice per kgOrigin

As stated

Gilthead seabream/ Fresh - whole 600-800 gr/pc 10.00 13.92 Italy CPT EgyptDorade royale/Dorada farmed 800-1000 8.86 12.33Sparus aurata 1000-2000 10.00 13.92Meagre/Maigre Fresh - Whole - wild 800-1000 gr/pc 6.53 9.09commun/Corvina 1000-2000 7.00 9.74Argyrosomus regius 2000-4000 7.31 10.17

3000-5000 8.00 11.13farmed 800-1000 gr/pc na FCA Greece

1000-1200 6.00 8.35> 2000 6.30 8.771000-2000 gr/pc 6.00 8.35 = CIF> 2000 7.50 10.44 =

SEABASS/SEABREAM/MEAGRE (cont.) March 2014

All rights reserved. No part of FAO/GLOBEFISH European Fish Price Report may be reproduced, stored in a retrieval system, or transmitted in any form or by any means (electronic, mechanical, photocopying or otherwise), without prior permission. Requests for use of this material (including purpose and extent) should be addressed to: GLOBEFISH - Fisheries and Aquaculture Department - Food and Agriculture Organization, Viale delle Terme di Caracalla, 00153 Rome, Italy.

The European Fish Price Report is a monthly GLOBEFISH publication, prepared by Karine Boisset, Felix Dent and Audun Lem.

It can be ordered from the FISH INFONetwork:

FAO GLOBEFISH (Network coordinator) Viale delle Terme di Caracalla 00153 Rome - Italy Tel: (39) 06 57055188 Fax: (39) 06 57053020 E-mail: [email protected] Web site: www.globefish.org

INFOPESCA (Latin America) Julio Herrera y Obes 1296 11200 Montevideo - Uruguay Tel: (598) 2 9028701 Fax: (598) 2 9030501 E-mail: [email protected] Web site: www.infopesca.org

EUROFISH (Central and Eastern Europe) H.C. Andersens Blvd 44-46 1553 Copenhagen - Denmark Tel: (45) 33377755 Fax: (45) 33377756 E-mail: [email protected] Web site: www.eurofish.dk

INFOFISH (Asia/Pacific) 1st Floor, Wisma LKIM Jalan Desaria - Pulau Meranti 47120 Puchong, Selangor DE Malaysia Tel: (603) 80649282/80649169 Fax: (603) 2078 6804 E-mail: [email protected] Web site: www.infofish.org

INFOPECHE (Africa) Tour C, 19éme étage, Cité Administrative Abidjan 01 - Côte d’Ivoire Tel: (225) 20228980 Fax: (225) 20218054 E-mail: [email protected] Web site: www.infopeche.ci

INFOYU (China) Room 514, Nongfeng Building No. 96 East Third Ring Road Chaoyang District Beijing 100122 – P.R. China Tel: (86-10) 59199614 Fax: (86-10) 59199614 E-mail: [email protected] Web site: www.infoyu.net

INFOSAMAK (Arab Region) 71 blvd Rahal El Meskini Casablanca 20 000 - Morocco Tel: (212) 522540856 Fax: (212) 522540855 E-mail: [email protected] Web site : www.infosamak.org

INFOSA - sub-office INFOPECHE (Southern Africa) 89, John Meinert Street- West Windhoek -Namibia Tel: (264) 61279430 Fax: (264) 61279434 E-mail:[email protected] Web site: www.infosa.org.na

PRICE REFERENCE (INCOTERMS 2010) EXW ex works FCA free carrier FAS free alongside ship FOB free on board CFR cost and freight CIF cost, insurance and freight CPT carriage paid to CIP carriage and insurance paid to DDP delivered duty paid DAT (new) delivered at terminal DAP (new) delivered at place (DAF, DES, DEQ and DDU have been cancelled) PRODUCT FORM IQF individually quick frozen IWP individually wrapped pack PBI pinbone in PBO pinbone off C&P cooked and peeled H&G headed and gutted FAS PD

frozen at sea peeled and deveined

PUD peeled, undeveined

SYMBOLS

Price increased in original currency since last report

- Price decreased in original currency since last report

= Updated but unchanged price * New insertion Not updated since last issue

CURRENCY RATES USD EUR Canada CAD 1.11 1.54 Hungary HUF 225.61 313.89 Norway NOK 5.97 8.30 USA USD 1.39 EU EUR 0.72 Denmark DKK 5.37 7.46

Exchange Rates: 14/03/14

GLOBEFISH Market Reports

are available from the GLOBEFISH web site: www.globefish.org

Related Documents