Globalisation and Competition: The New World of Cities Cities Research Center I 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Globalisation and Competition:The New World of Cities

Cities Research Center I 2015

Globalisation and Competition: The New World of Cities 2 JLL

Foreword

The size, shape and metabolism of our cities are undergoing a metamorphosis. Urban form, urban life and the mechanics of our cities are having to respond to technological surprises, the demands of rising populations and the shifting geography of commerce. At the same time, cities face pressures of balancing quality of life and sustainability with productivity and growth. Underlying these pressures is a sense of urgency and of the need for unabated momentum if cities are to avoid getting locked into models that are unsustainable, uncompetitive or unliveable.

Many cities are using innovative approaches to tackle such serious demands, but there remains intense strain on infrastructure, squeezed funding, suboptimal land use, and a lack of clarity on future strategy in many urban landscapes. All of these deficits are part of the competitive framework between cities across the world. But while attention has been focused on how individual cities are dealing with such rapid and sweeping changes, what has become startlingly apparent is that a redefinition of city style, objectives, purpose and capabilities is taking place and is altering our understanding of the traditional city hierarchy. No longer does size determine growth, or industrial profile drive success, or history govern attractiveness. Rather, as this report clearly highlights, in seeking competitive advantage cities are describing themselves in ways that speak to their distinct purposes and different intentions.

‘Established World Cities’ will fight to maintain position while modernising; ‘Emerging World Cities’ are keen to prove strength in speed of change; and ‘New World Cities’ are promoting a new model of what it means to be both global and liveable.

This study seeks to reset our thinking on the future world of cities and uses detailed analysis of the very wide range of metrics and indices to guide us into a fresh understanding of city success and its implications for urban form and real estate dynamics.

Rosemary FeenanInternational DirectorGlobal Research Programmes,JLL

Globalisation and Competition: The New World of Cities 3 JLL

Contents

Globalisation and Competition: The New World of Cities 4 JLL

Executive Summary

We are in a new era of city competition. The rigid global urban hierarchy is breaking down as cities increasingly specialise in niche markets, enabling more cities than ever to ‘go global’. This is fundamentally changing the geography of commercial property and has deep implications for real estate formats, assets and opportunities.This paper, produced jointly by JLL and The Business of Cities, offers a fresh approach to understanding city performance and prospects. A new typology of cities is presented, with a focus on the trends, challenges and real estate implications in three broad categories of city:

Established World CitiesThese are the highly globalised and competitive metropolitan economies with the deepest and most settled concentrations of firms, capital and talent. Six cities stand out. The ‘Big Six’ include the traditional ‘super cities’ of London, New York, Paris and Tokyo, but more recently this quartet has been joined by Hong Kong and Singapore. They have significant competitive advantages, but nonetheless are vulnerable to other dynamic gateway cities that are well positioned to capture spill-over demand, notably Seoul, Toronto and Sydney and, over the longer term, Shanghai.

'Established World Cities' have been hugely successful in attracting real estate capital, and such is their attraction for sovereign wealth funds, institutions and high-net-worth individuals that the ‘Big Six’ alone account for more than one-fifth of total global activity. Yet to retain their competitive advantage, these cities will need to execute bold urban transformation plans (such as the ambitious ‘Grand Paris’ project) to support the shift to new modes of economic activity and to ensure the efficient recycling of land. Affordability has become a critical issue for cities such as London, New York and Hong Kong, where there are pressing requirements for appropriately-priced and flexible urban business space for the expanding innovation economy. A major boost to new residential supply and to delivery solutions is also crucial for maintaining their competitive edge.

Emerging World CitiesThese are the business and political capitals of large or medium-sized emerging economies that function as gateways for international firms, trade and investment. Cities such as Shanghai, Beijing, Istanbul and Sao Paulo are among the most recognisable ‘Emerging World Cities’ and are firmly on the path to becoming bona fide 'World Cities'. However, the rise of ‘Emerging World Cities’ is very uneven – Shenzhen, Dubai and Bangalore, for example, are globalising at breakneck speed; Jakarta, Manila and Sao Paulo are making notable improvements in key competitiveness measures; but others like Dhaka are struggling to cope with the pace of global change.

To support rapid urbanisation, cities such as Shanghai, Mexico City and Istanbul are witnessing massive expansion of their real estate inventory through the construction of impressive mixed-use schemes and trophy developments, which are seen as the hallmark of a modern city. But as these cities move to the next phase in their evolution, the real estate sector will play a more pivotal role in creating a ‘sense of place’ and contributing to city identity, uniqueness and well-being. As these are some of the world’s most environmentally-challenged cities, real estate will be a key driver of more sustainable urban models. Improvements in real estate transparency also need to progress at much greater speed, not only to attract new capital, but to enhance the business operating environment and contribute to the quality of life of its citizens.

Globalisation and Competition: The New World of Cities 5 JLL

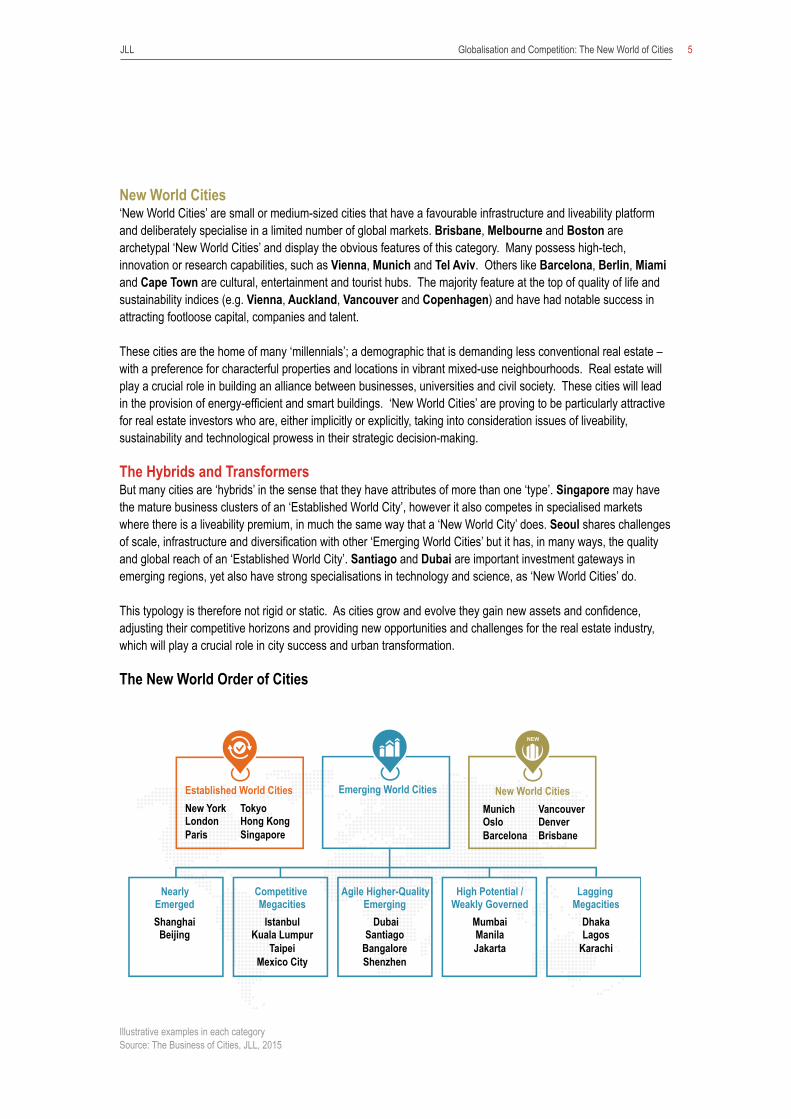

New World Cities‘New World Cities’ are small or medium-sized cities that have a favourable infrastructure and liveability platform and deliberately specialise in a limited number of global markets. Brisbane, Melbourne and Boston are archetypal ‘New World Cities’ and display the obvious features of this category. Many possess high-tech, innovation or research capabilities, such as Vienna, Munich and Tel Aviv. Others like Barcelona, Berlin, Miami and Cape Town are cultural, entertainment and tourist hubs. The majority feature at the top of quality of life and sustainability indices (e.g. Vienna, Auckland, Vancouver and Copenhagen) and have had notable success in attracting footloose capital, companies and talent.

These cities are the home of many ‘millennials’; a demographic that is demanding less conventional real estate – with a preference for characterful properties and locations in vibrant mixed-use neighbourhoods. Real estate will play a crucial role in building an alliance between businesses, universities and civil society. These cities will lead in the provision of energy-efficient and smart buildings. ‘New World Cities’ are proving to be particularly attractive for real estate investors who are, either implicitly or explicitly, taking into consideration issues of liveability, sustainability and technological prowess in their strategic decision-making.

The Hybrids and TransformersBut many cities are ‘hybrids’ in the sense that they have attributes of more than one ‘type’. Singapore may have the mature business clusters of an ‘Established World City’, however it also competes in specialised markets where there is a liveability premium, in much the same way that a ‘New World City’ does. Seoul shares challenges of scale, infrastructure and diversification with other ‘Emerging World Cities’ but it has, in many ways, the quality and global reach of an ‘Established World City’. Santiago and Dubai are important investment gateways in emerging regions, yet also have strong specialisations in technology and science, as ‘New World Cities’ do.

This typology is therefore not rigid or static. As cities grow and evolve they gain new assets and confidence, adjusting their competitive horizons and providing new opportunities and challenges for the real estate industry, which will play a crucial role in city success and urban transformation.

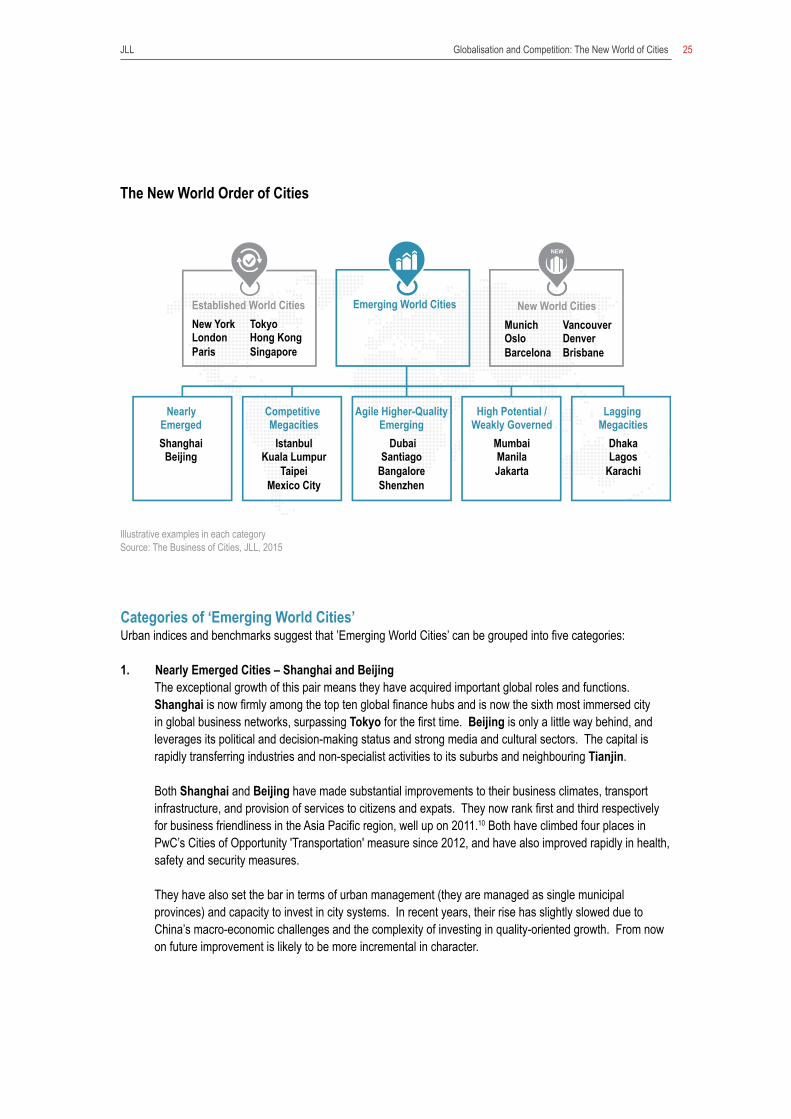

The New World Order of Cities

Established World Cities New World Cities New York London Paris

Munich Oslo Barcelona

Nearly Emerged

Lagging Megacities

Shanghai Beijing

Dhaka Lagos

Karachi

Tokyo Hong Kong Singapore

Vancouver Denver Brisbane

Competitive Megacities

High Potential / Weakly Governed

Istanbul Kuala Lumpur

Taipei Mexico City

Mumbai Manila Jakarta

Agile Higher-Quality Emerging

Santiago Bangalore Shenzhen

Dubai

Emerging World Cities

Illustrative examples in each category Source: The Business of Cities, JLL, 2015

Globalisation and Competition: The New World of Cities 6 JLL

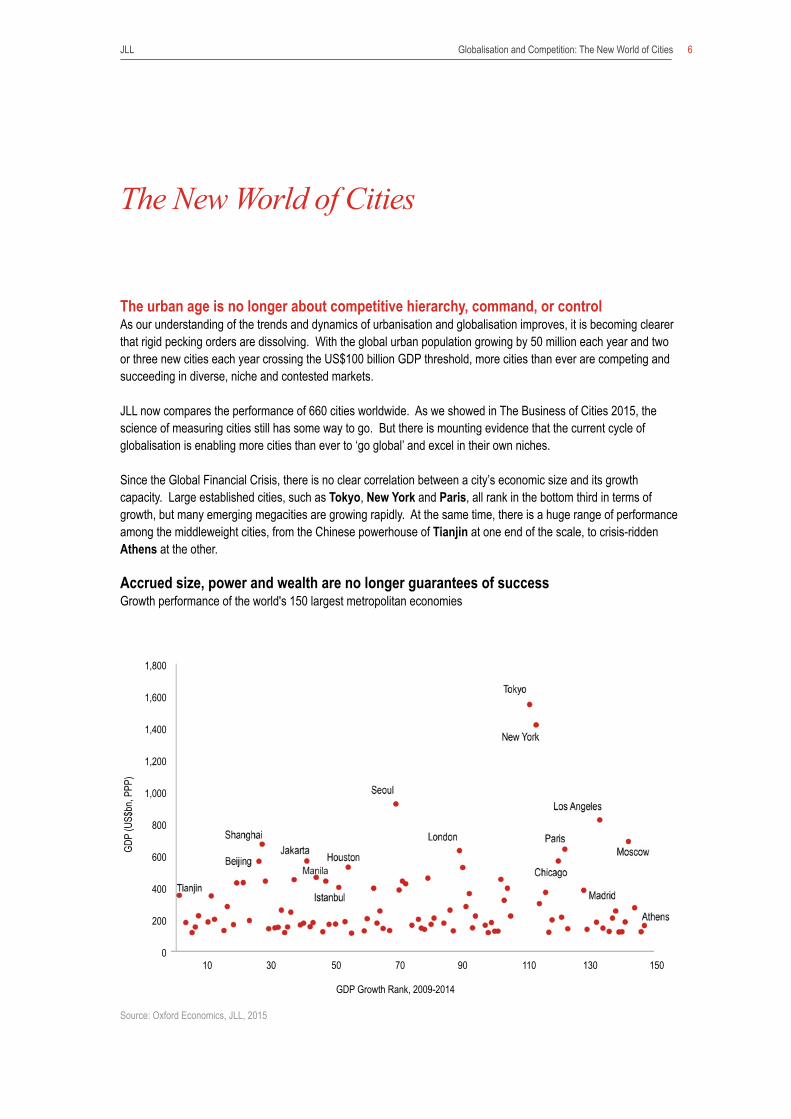

The urban age is no longer about competitive hierarchy, command, or control As our understanding of the trends and dynamics of urbanisation and globalisation improves, it is becoming clearer that rigid pecking orders are dissolving. With the global urban population growing by 50 million each year and two or three new cities each year crossing the US$100 billion GDP threshold, more cities than ever are competing and succeeding in diverse, niche and contested markets.

JLL now compares the performance of 660 cities worldwide. As we showed in The Business of Cities 2015, the science of measuring cities still has some way to go. But there is mounting evidence that the current cycle of globalisation is enabling more cities than ever to ‘go global’ and excel in their own niches.

Since the Global Financial Crisis, there is no clear correlation between a city’s economic size and its growth capacity. Large established cities, such as Tokyo, New York and Paris, all rank in the bottom third in terms of growth, but many emerging megacities are growing rapidly. At the same time, there is a huge range of performance among the middleweight cities, from the Chinese powerhouse of Tianjin at one end of the scale, to crisis-ridden Athens at the other.

Accrued size, power and wealth are no longer guarantees of successGrowth performance of the world's 150 largest metropolitan economies

The New World of Cities

New York, USA

Source: Oxford Economics, JLL, 2015

1,800

1,600

1,400

1,200

1,000

800

600

400

200

0 10 30 50 70 90 110 130 150

GDP Growth Rank, 2009-2014

GDP

(US$

bn, P

PP)

Globalisation and Competition: The New World of Cities 7 JLL

Towards a new typology of citiesLooking at a range of over 200 diverse city indices suggests that it no longer makes sense to understand all cities as being in competition with every other city. There is not one singular system of cities. When we look at these indices in finer-grained detail, we see a pattern that shows that individual cities typically share similar classes of assets, challenges and trajectories with a small cluster of other similarly endowed cities.

The benchmarking of cities in the same class may be a much more effective and revealing approach as we try to understand the performance and prospects of cities. One way to achieve this is to develop typologies of cities based on their inherited attributes and strategic positioning.

In this paper we pursue this ‘typology approach’ by reviewing the trends and challenges in three broad categories of city:

I. Established World Cities: highly globalised and competitive metropolitan economies with the deepest and most settled concentrations of firms, capital and talent.II. Emerging World Cities: business and political capitals of large or medium-sized emerging economies that function as gateways for international firms, trade and investment.III. New World Cities: small or medium-sized cities that have an attractive infrastructure and liveability platform and deliberately specialise in a limited number of global markets.

There are many exemplary examples of each ‘type’ of city. London and New York are textbook ‘Established World Cities’. Shanghai, Istanbul and Sao Paulo are immediately recognisable as ‘Emerging World Cities’. Melbourne, Brisbane, Barcelona and Boston have many of the obvious features of ‘New World Cities’.

Hybrids and transformersBut many cities are ‘hybrids’ in the sense that they have attributes of more than one ‘type’. Singapore may have the mature business clusters of an ‘Established World City’, however it also competes in specialised and contested markets where there is a liveability premium, in much the same way that a ‘New World City’ does. Seoul shares challenges of scale, infrastructure and diversification with other ‘Emerging World Cities’ but having become an upper-income city it has in many ways the quality and global reach of an ‘Established World City’. Santiago and Dubai are important investment gateways in emerging regions, yet also have strong specialisations in technology and science, as ‘New World Cities’ do.

This typology is therefore not rigid or static. As cities grow and evolve they gain new assets and confidence, adjusting their competitive horizons. Thus, at various stages, cities have elements of more than one ‘type’ of city.Globalisation and urbanisation also drive the emergence of other types of city. Some rely and compete first and foremost on their quality of life, and the ability to attract talent and entrepreneurs. Vancouver and Geneva are the obvious candidates. Others – like Busan or Hamburg – leverage their ports or airports to build logistics, trade and science functions. We also see cities competing as visitor destinations, with examples including Las Vegas, Macau and Prague. These are just some of the wide range of typologies that cities can fit into.

Globalisation and Competition: The New World of Cities 8 JLL

Broad Types of Globalising Cities

Source: The Business of Cities, 2015

High quality of life

Specialised centres

Port & airport cities

Visitor destinations

Knowledge hub

Re-emerging capital cities

New gateway cities

New World Cities

Established World Cities

Emerging World Cities

Globalisation and Competition: The New World of Cities 9 JLL

Source: fDi Intelligence, 2014

What are ‘Established World Cities’?Analysis of 200 city indices over the last five years reveals that there is a small and distinct cluster of uniquely globalised ‘world cities’ with their own class of assets and challenges. These cities have had open and internationalised economies for at least three business cycles. Business in these cities is typically conducted in several languages and currencies, and across several jurisdictions and time zones. They combine proficient corporate clusters with global reach, strong infrastructure platforms and an enduring cultural appeal.

In the leading global indices, six cities stand out. They include the traditional ‘super cities’ of London, New York, Paris and Tokyo, as defined by JLL’s Commercial Attraction Index.1 This quartet has been more recently joined by Hong Kong and Singapore. This group, known as the ‘Big Six’, were once often described as the “command and control” centres of the world economy. That framework has become outdated as new forms of power, influence and success have emerged, but these established global centres retain a range of unique competitive assets.2

The concentration and depth of globally trading companies marks the ‘Big Six’ apart The ‘Big Six’ are not all the largest city economies by scale or by prosperity, but have absorbed the biggest shares of financial and business services activity.3 London, New York, Paris and Tokyo have been leaders for several business cycles, whereas Hong Kong and Singapore broke clear of the chasing pack in the 1990s after pursuing an unusually strategic and co-ordinated approach to their economic development.

Foreign direct investment into these six cities remains very strong. London has dominated in recent years but Paris, Singapore, Hong Kong and New York have also excelled. Only Beijing and Shanghai are consistently as competitive in investment attraction. Across multiple indices, the ‘Big Six’ are compelling thanks to their customer markets, political stability, legal and regulatory frameworks, and their institutional credibility.

Specifically, Singapore and Hong Kong are considered the most business friendly cities in the world. Tokyo and Paris remain magnetic despite their rigidities, because of their infrastructure platforms and talent pools.4 Paris, in particular, has proven highly successful at attracting investment from across Europe and North America since 2013, especially into its software, IT and business services sectors.5

The 'Big Six' are among the world's most attractive investment destinationsNumber of greenfield investment projects, 2014

Established World Cities

Toronto

Amsterdam

MelbourneParis

San Fr

ancisco

DublinToky

oBeijin

g

Bangalore

Sydney

Hong Kong

New YorkDubai

Shangh

ai

London

Singa

pore

50

150

250

350

450

Globalisation and Competition: The New World of Cities 10 JLL

London and New York dominate commercial real estate investmentIn terms of commercial real estate investment, London and New York stand head and shoulders above other cities, typically accounting for between 10% and 15% of total global investment. Their scale, liquidity, transparency and ‘safe haven’ attributes are attracting significant capital from sovereign wealth funds, global institutions and high-net-worth individuals. Investment activity in Tokyo has recently strengthened as it secures its position as the world’s third most active market. Singapore and Hong Kong remain some way behind due to the existence of policies which have recently restrained investment.

The 'Big Six' account for 22% of global real estate investmentTop 30 cities for direct commercial real estate investment, Q3 2012 - Q2 2015

(US$ billions)Source: JLL, 2015

London 1 129

Los Angeles 5 46

New York 2 110

Paris 4 55

Tokyo 3 66

Chicago 6 38

Washington 7 34

Boston 8 30

Singapore 9 28

San Francisco 10 27

Seoul 11 27

Sydney 12 27

Hong Kong 13 26

Shanghai 14 24

Seattle 15 21

San Jose 16 21

Dallas 17 20

Atlanta 18 17

Houston 19 17

Munich 20 17

Toronto 21 16

Frankfurt 22 15

Stockholm 23 15

Melbourne 24 15

Beijing 25 14

Phoenix 26 14

Denver 27 13

San Diego 28 13

Berlin 29 13

Moscow 30 12

Globalisation and Competition: The New World of Cities 11 JLL

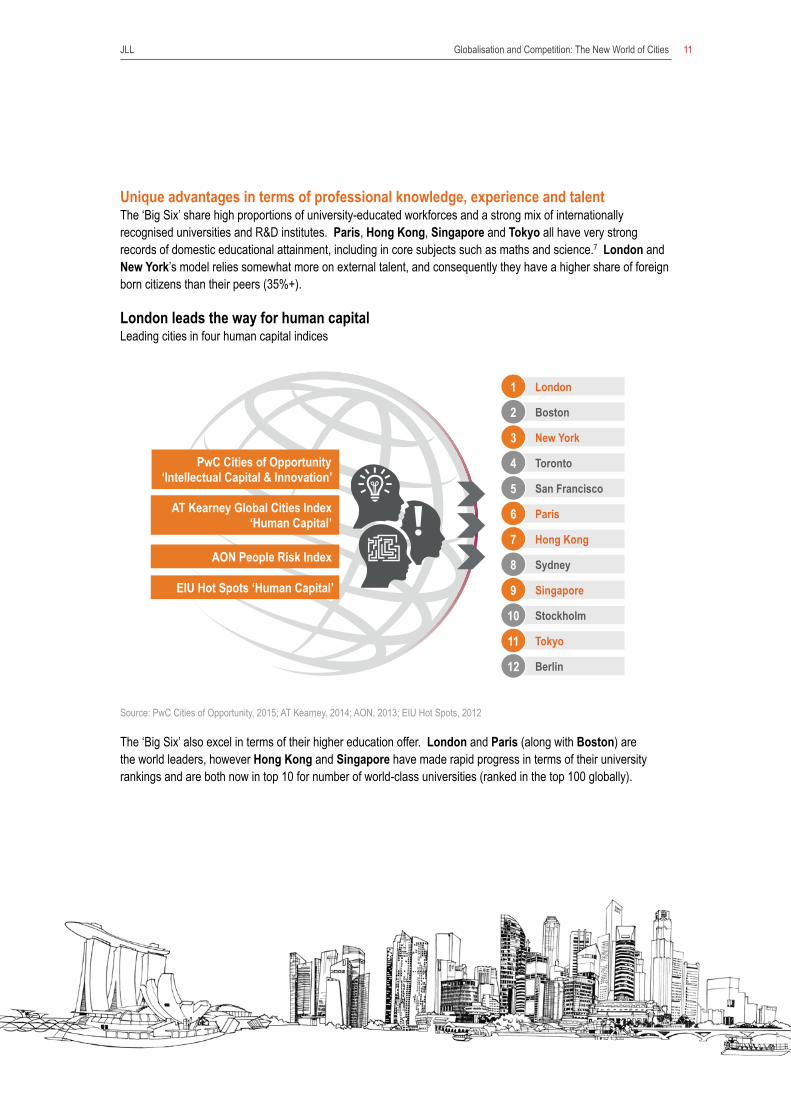

Unique advantages in terms of professional knowledge, experience and talent The ‘Big Six’ share high proportions of university-educated workforces and a strong mix of internationally recognised universities and R&D institutes. Paris, Hong Kong, Singapore and Tokyo all have very strong records of domestic educational attainment, including in core subjects such as maths and science.7 London and New York’s model relies somewhat more on external talent, and consequently they have a higher share of foreign born citizens than their peers (35%+).

London leads the way for human capitalLeading cities in four human capital indices

Source: PwC Cities of Opportunity, 2015; AT Kearney, 2014; AON, 2013; EIU Hot Spots, 2012

The ‘Big Six’ also excel in terms of their higher education offer. London and Paris (along with Boston) are the world leaders, however Hong Kong and Singapore have made rapid progress in terms of their university rankings and are both now in top 10 for number of world-class universities (ranked in the top 100 globally).

PwC Cities of Opportunity ‘Intellectual Capital & Innovation’

AT Kearney Global Cities Index ‘Human Capital’

AON People Risk Index

EIU Hot Spots ‘Human Capital’

London 1

Boston 2

New York 3

Toronto 4

San Francisco 5

Paris 6

Hong Kong 7

Sydney 8

Singapore 9

Stockholm 10

Tokyo 11

Berlin 12

Globalisation and Competition: The New World of Cities 12 JLL

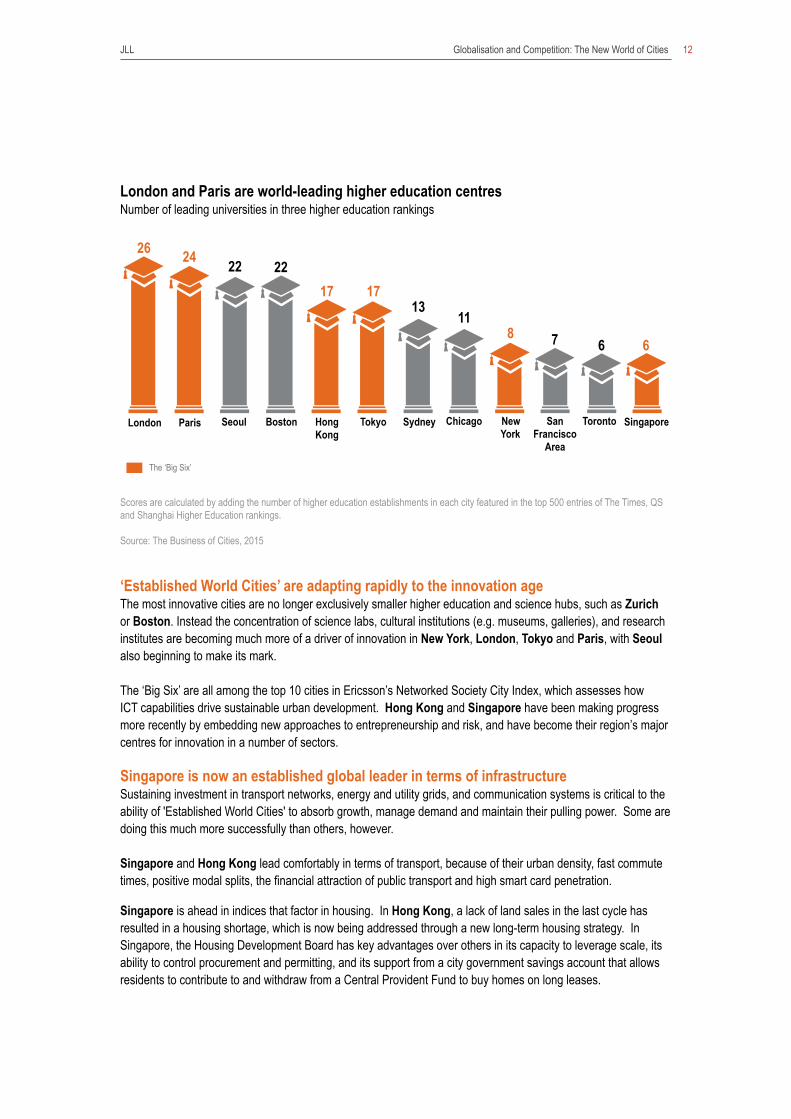

‘Established World Cities’ are adapting rapidly to the innovation ageThe most innovative cities are no longer exclusively smaller higher education and science hubs, such as Zurich or Boston. Instead the concentration of science labs, cultural institutions (e.g. museums, galleries), and research institutes are becoming much more of a driver of innovation in New York, London, Tokyo and Paris, with Seoul also beginning to make its mark.

The ‘Big Six’ are all among the top 10 cities in Ericsson’s Networked Society City Index, which assesses how ICT capabilities drive sustainable urban development. Hong Kong and Singapore have been making progress more recently by embedding new approaches to entrepreneurship and risk, and have become their region’s major centres for innovation in a number of sectors.

Singapore is now an established global leader in terms of infrastructure Sustaining investment in transport networks, energy and utility grids, and communication systems is critical to the ability of 'Established World Cities' to absorb growth, manage demand and maintain their pulling power. Some are doing this much more successfully than others, however.

Singapore and Hong Kong lead comfortably in terms of transport, because of their urban density, fast commute times, positive modal splits, the financial attraction of public transport and high smart card penetration.

Singapore is ahead in indices that factor in housing. In Hong Kong, a lack of land sales in the last cycle has resulted in a housing shortage, which is now being addressed through a new long-term housing strategy. In Singapore, the Housing Development Board has key advantages over others in its capacity to leverage scale, its ability to control procurement and permitting, and its support from a city government savings account that allows residents to contribute to and withdraw from a Central Provident Fund to buy homes on long leases.

Scores are calculated by adding the number of higher education establishments in each city featured in the top 500 entries of The Times, QS and Shanghai Higher Education rankings.

Source: The Business of Cities, 2015

London Paris Chicago Boston Seoul Hong Kong

Sydney Tokyo Singapore New York

Toronto San Francisco

Area

26 24 22 22 17 17

13 11

8 7 6 6

The ‘Big Six’

London and Paris are world-leading higher education centresNumber of leading universities in three higher education rankings

Globalisation and Competition: The New World of Cities 13 JLL

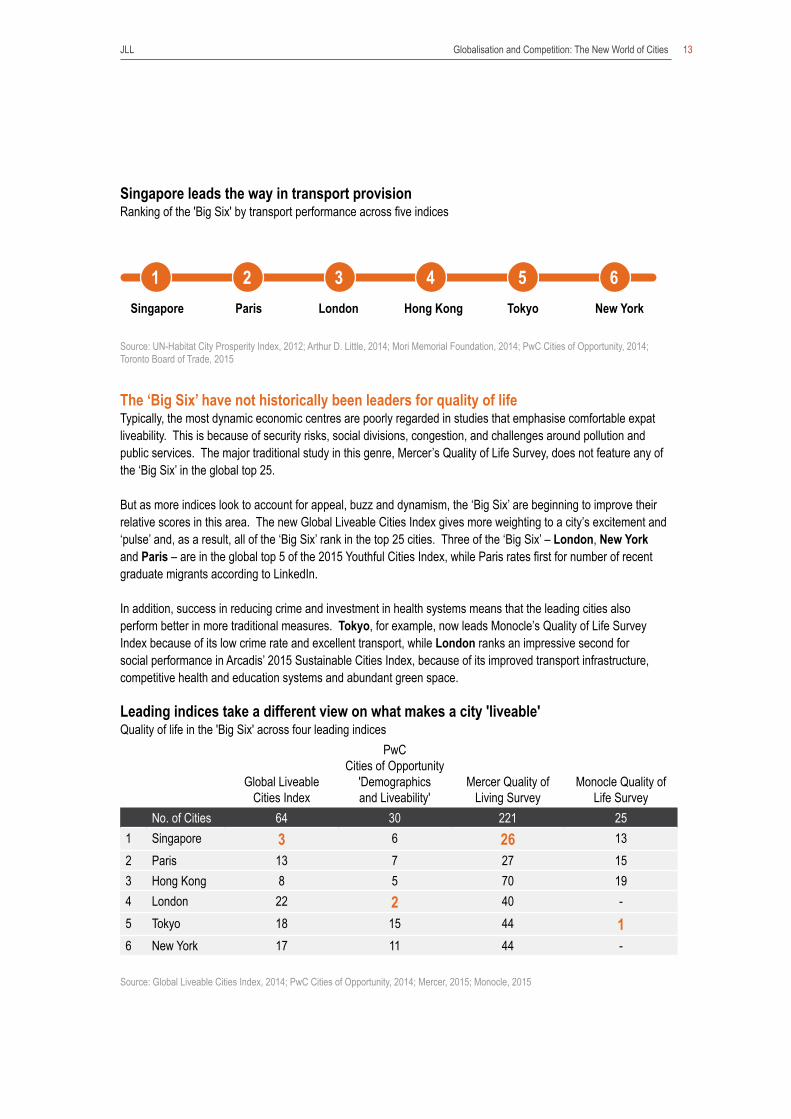

Singapore leads the way in transport provisionRanking of the 'Big Six' by transport performance across five indices

Source: UN-Habitat City Prosperity Index, 2012; Arthur D. Little, 2014; Mori Memorial Foundation, 2014; PwC Cities of Opportunity, 2014; Toronto Board of Trade, 2015

The ‘Big Six’ have not historically been leaders for quality of lifeTypically, the most dynamic economic centres are poorly regarded in studies that emphasise comfortable expat liveability. This is because of security risks, social divisions, congestion, and challenges around pollution and public services. The major traditional study in this genre, Mercer’s Quality of Life Survey, does not feature any of the ‘Big Six’ in the global top 25.

But as more indices look to account for appeal, buzz and dynamism, the ‘Big Six’ are beginning to improve their relative scores in this area. The new Global Liveable Cities Index gives more weighting to a city’s excitement and ‘pulse’ and, as a result, all of the ‘Big Six’ rank in the top 25 cities. Three of the ‘Big Six’ – London, New York and Paris – are in the global top 5 of the 2015 Youthful Cities Index, while Paris rates first for number of recent graduate migrants according to LinkedIn.

In addition, success in reducing crime and investment in health systems means that the leading cities also perform better in more traditional measures. Tokyo, for example, now leads Monocle’s Quality of Life Survey Index because of its low crime rate and excellent transport, while London ranks an impressive second for social performance in Arcadis’ 2015 Sustainable Cities Index, because of its improved transport infrastructure, competitive health and education systems and abundant green space.

Leading indices take a different view on what makes a city 'liveable'Quality of life in the 'Big Six' across four leading indices

Global Liveable Cities Index

PwCCities of Opportunity

'Demographics and Liveability'

Mercer Quality of Living Survey

Monocle Quality of Life Survey

No. of Cities 64 30 221 251 Singapore 3 6 26 132 Paris 13 7 27 153 Hong Kong 8 5 70 194 London 22 2 40 -5 Tokyo 18 15 44 16 New York 17 11 44 -

Source: Global Liveable Cities Index, 2014; PwC Cities of Opportunity, 2014; Mercer, 2015; Monocle, 2015

Singapore Paris London Hong Kong Tokyo New York

1 2 3 4 5 6

Globalisation and Competition: The New World of Cities 14 JLL

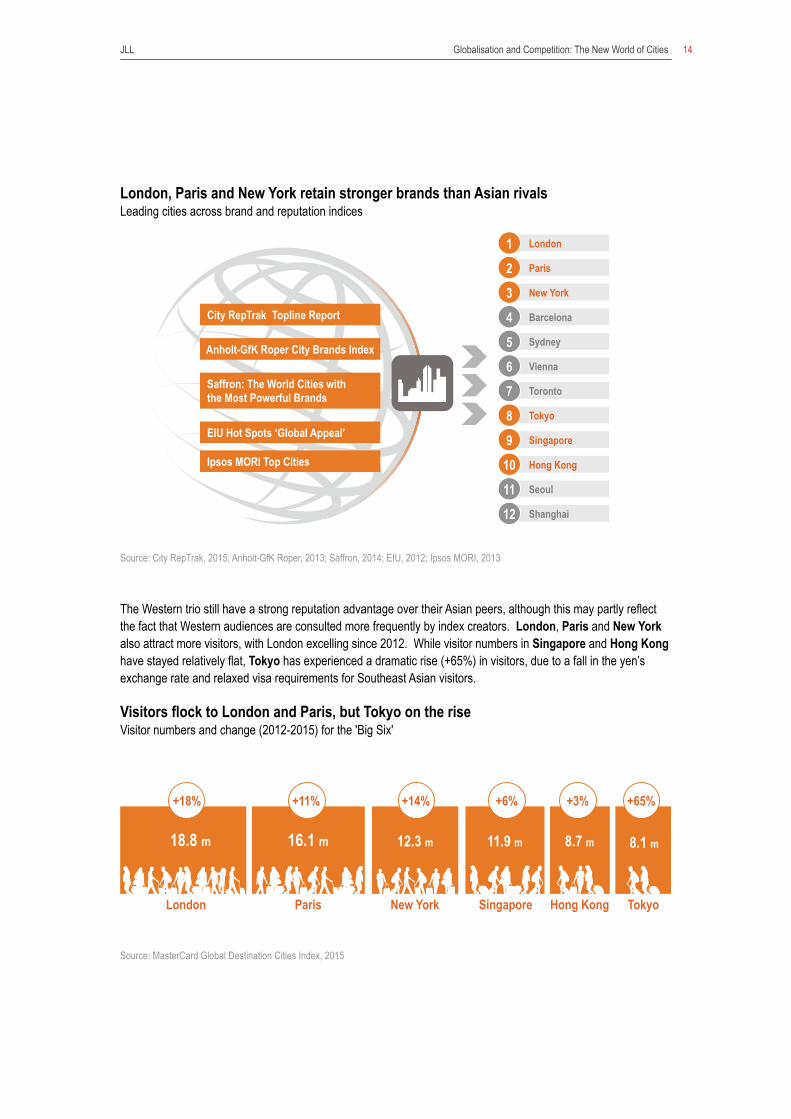

London, Paris and New York retain stronger brands than Asian rivalsLeading cities across brand and reputation indices

Source: City RepTrak, 2015; Anholt-GfK Roper, 2013; Saffron, 2014; EIU, 2012; Ipsos MORI, 2013

The Western trio still have a strong reputation advantage over their Asian peers, although this may partly reflect the fact that Western audiences are consulted more frequently by index creators. London, Paris and New York also attract more visitors, with London excelling since 2012. While visitor numbers in Singapore and Hong Kong have stayed relatively flat, Tokyo has experienced a dramatic rise (+65%) in visitors, due to a fall in the yen’s exchange rate and relaxed visa requirements for Southeast Asian visitors.

Visitors flock to London and Paris, but Tokyo on the riseVisitor numbers and change (2012-2015) for the 'Big Six'

Source: MasterCard Global Destination Cities Index, 2015

City Rep Trak Topline Report

Anholt-GfK Roper City Brands Index

Saffron: The World Cities with the Most Powerful Brands

EIU Hot Spots ‘Global Appeal’

Ipsos MORI Top Cities

London 1 Paris 2 New York 3 Barcelona 4 Sydney 5 Vienna 6 Toronto 7 Tokyo 8 Singapore 9 Hong Kong 10 Seoul 11 Shanghai 12

London

18.8 m

Paris

16.1 m

New York

12.3 m 11.9 m

Singapore Hong Kong

8.7 m

Tokyo

8.1 m

+18% +11% +14% +6% +3% +65%

Globalisation and Competition: The New World of Cities 15 JLL

Singapore and Tokyo are moving ahead when it comes to sustainability Singapore ranks 7th in the environmental dimension of Arcadis' Sustainable Cities Index because its city systems, energy consumption and waste management are better managed than in the other less comprehensively planned metropolitan areas. Meanwhile, Tokyo is rated the safest city in the world by the Economist Intelligence Unit in 2015, because of the protection of its infrastructure, digital and technology assets. These results are consistent with other indices in recent years which show that these cities are leaders in the sustainable and smart city space.

By contrast, the remaining four cities in the ‘Big Six’ continue to record modest or weak scores in a number of assessments on environment and resilience. Paris is rated relatively poorly for digital and personal security. New York is rated the most vulnerable to climate disasters of the ‘Big Six’, but is first globally for its policy approach to addressing resilience, at least at the city level.8

The ‘Big Six’ is not a closed shopDespite the group’s advantages, there is increasing competition from cities which have upgraded their infrastructure and connectivity more rapidly. The 'Big Six's' dominance is therefore vulnerable to younger cities that can learn from their mistakes and capture the spill-overs from excess demand. It is likely that the ‘Big Six’ will grow over the next ten years, perhaps into a new ‘Big Eight’ or ‘Big Ten’.

Based on index results since 2013, there are three main candidates to join and expand the ‘Big Six’. Seoul, Toronto and Sydney are now in their fourth cycle of global engagement and adjustment, and have acquired some of the financial, headquarter and institutional critical mass. This trio are strategically located gateways to large and relatively high-growth markets (Seoul is now fourth in the world for international visitor spend). They also have wide international reach, access to pools of talent, and increasingly visible liveability advantages that make them attractive to a mobile workforce.

Equally, medium-term trends suggest that the size and success of ‘Established World Cities’ is creating negative externalities that are hard to solve quickly – such as congestion, demographic pressure, unmet demand for housing and two-speed economies. Improvements are complex, incremental and costly. In many respects, four of the ‘Big Six’ are relying on their national governments to help deliver key reforms that will address these deficits: fiscal devolution and investment in London; airport investment in New York; business friendly National Strategic Special Zones in Tokyo; and regional infrastructure in Paris.

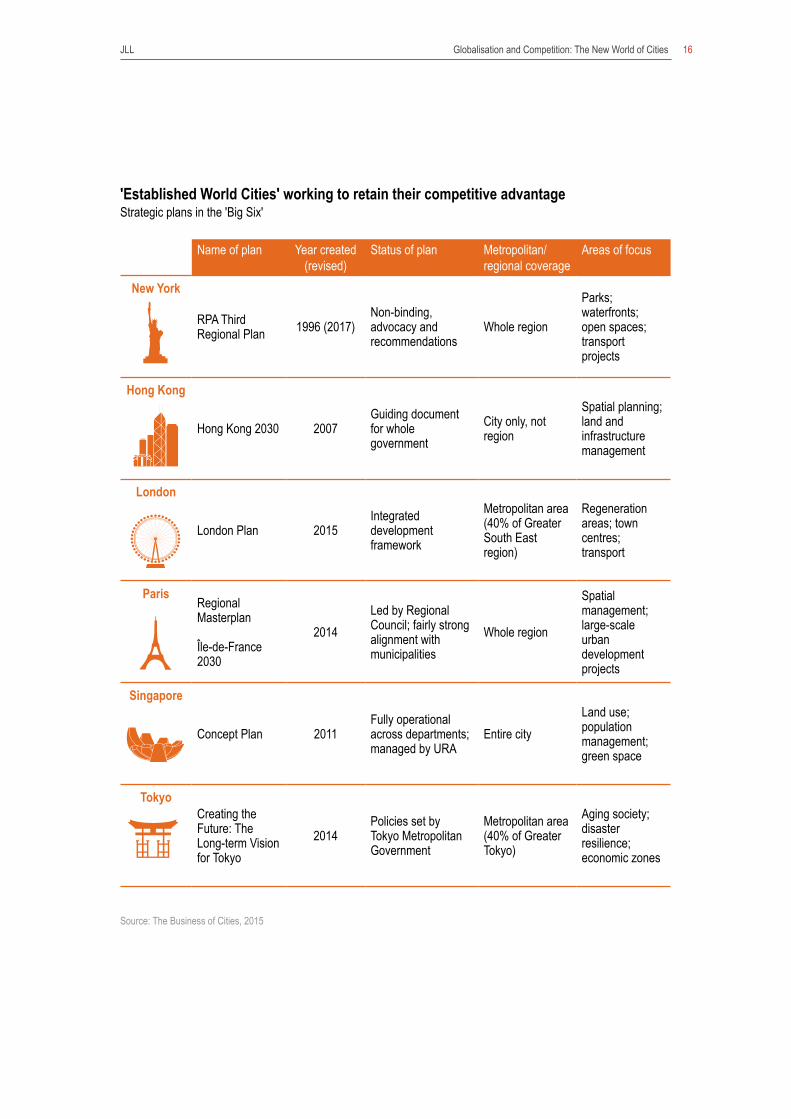

Globalisation and Competition: The New World of Cities 16 JLL

'Established World Cities' working to retain their competitive advantageStrategic plans in the 'Big Six'

Name of plan Year created (revised)

Status of plan Metropolitan/regional coverage

Areas of focus

New York

RPA Third Regional Plan 1996 (2017)

Non-binding, advocacy and recommendations

Whole region

Parks; waterfronts; open spaces; transport projects

Hong Kong

Hong Kong 2030 2007Guiding document for whole government

City only, not region

Spatial planning; land and infrastructure management

London

London Plan 2015Integrated development framework

Metropolitan area (40% of Greater South East region)

Regeneration areas; town centres; transport

Paris Regional Masterplan

Île-de-France 2030

2014Led by Regional Council; fairly strong alignment with municipalities

Whole region

Spatial management; large-scale urban development projects

Singapore

Concept Plan 2011Fully operational across departments; managed by URA

Entire cityLand use; population management; green space

TokyoCreating the Future: The Long-term Vision for Tokyo

2014Policies set by Tokyo Metropolitan Government

Metropolitan area (40% of Greater Tokyo)

Aging society; disaster resilience; economic zones

Source: The Business of Cities, 2015

Globalisation and Competition: The New World of Cities 17 JLL

‘Emerging World Cities’ are integrating into the global economyCity index trends since the Global Financial Crisis reveal that major cities in the fastest growing, larger economies are becoming key gateways and engines of international economic activity. In the current cycle of globalisation, they are rapidly gaining the attributes of major cities in developed nations. They are on the path to becoming bona fide ‘world cities’.

The latest indices and benchmarks observe and track this new type of city. The ongoing Globalisation and World Cities (GaWC) studies reveal big changes in the number and type of cities that are taking on international functions. Today of the 100 most globalised cities according to GaWC data, 44 are middle-income and lower-income cities with real GDP per capita of below US$25,000.

Nearly half of the cities that are driving the process of globalisation are located in so-called ‘developing’ countries. They vary considerably in size, political context and development path. Their per capita income (by PPP) diverges significantly – cities such as Warsaw and Moscow are beginning to enter upper-middle or upper income status, while Indian and some Chinese cities are still closer to US$5,000 per annum. But the signs are that they all becoming rapidly integrated into the global economy, and their economic performance has become closely indexed to global demand.

Emerging World Cities

Globalisation and Competition: The New World of Cities 18 JLL

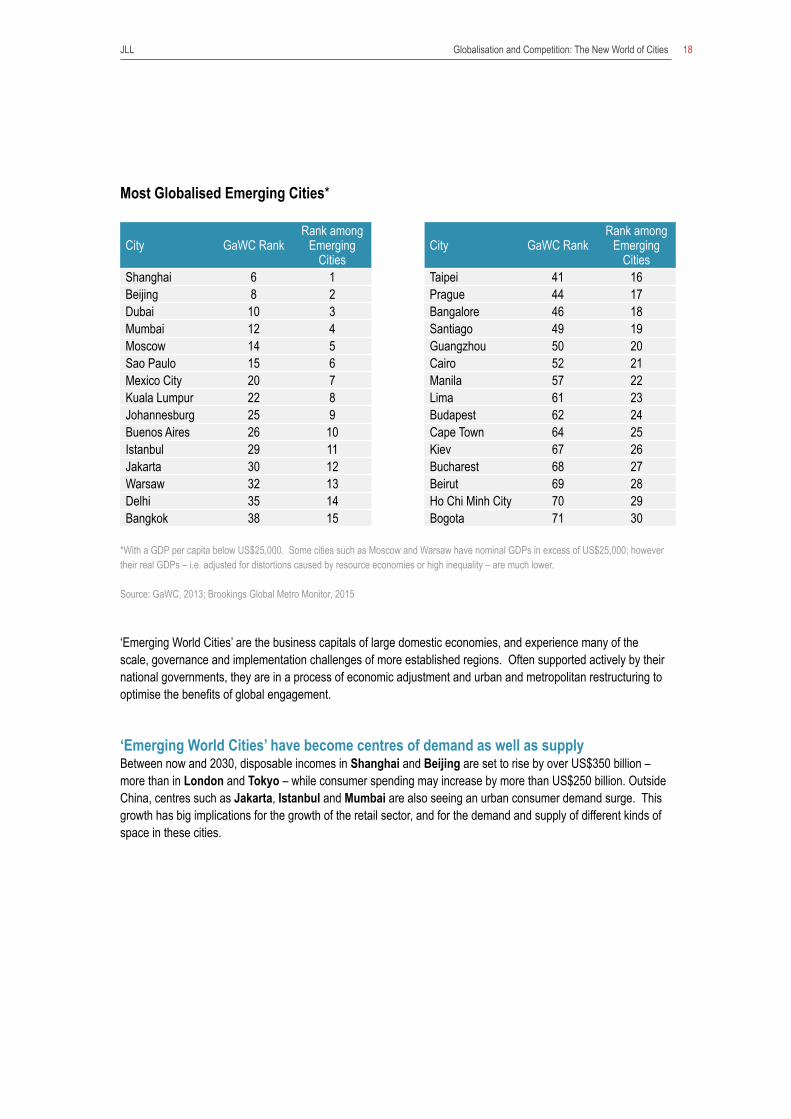

Most Globalised Emerging Cities*

City GaWC RankRank among

Emerging Cities

City GaWC RankRank among

Emerging Cities

Shanghai 6 1 Taipei 41 16Beijing 8 2 Prague 44 17Dubai 10 3 Bangalore 46 18Mumbai 12 4 Santiago 49 19Moscow 14 5 Guangzhou 50 20Sao Paulo 15 6 Cairo 52 21Mexico City 20 7 Manila 57 22Kuala Lumpur 22 8 Lima 61 23Johannesburg 25 9 Budapest 62 24Buenos Aires 26 10 Cape Town 64 25Istanbul 29 11 Kiev 67 26Jakarta 30 12 Bucharest 68 27Warsaw 32 13 Beirut 69 28Delhi 35 14 Ho Chi Minh City 70 29Bangkok 38 15 Bogota 71 30

*With a GDP per capita below US$25,000. Some cities such as Moscow and Warsaw have nominal GDPs in excess of US$25,000; however their real GDPs – i.e. adjusted for distortions caused by resource economies or high inequality – are much lower.

Source: GaWC, 2013; Brookings Global Metro Monitor, 2015

‘Emerging World Cities’ are the business capitals of large domestic economies, and experience many of the scale, governance and implementation challenges of more established regions. Often supported actively by their national governments, they are in a process of economic adjustment and urban and metropolitan restructuring to optimise the benefits of global engagement.

‘Emerging World Cities’ have become centres of demand as well as supply Between now and 2030, disposable incomes in Shanghai and Beijing are set to rise by over US$350 billion – more than in London and Tokyo – while consumer spending may increase by more than US$250 billion. Outside China, centres such as Jakarta, Istanbul and Mumbai are also seeing an urban consumer demand surge. This growth has big implications for the growth of the retail sector, and for the demand and supply of different kinds of space in these cities.

Globalisation and Competition: The New World of Cities 19 JLL

Surge in disposable incomes expected in Asian megacitiesIncreases in disposable income by 2030 across developed and emerging cities

Source: Oxford Economics, 2015

'Established World Cities' used to host the overwhelming share of large global firms, but the picture is rapidly changing. 26% of firms with revenue above US$1 billion are now based in ‘Emerging World Cities', potentially reaching 50% by 2025.9

A changing urban landscapeThe leading ‘Emerging World Cities’, those that have successfully organised and embraced new opportunities, have begun to close the gap across a range of indicators. More than 24 emerging cities have appeared in the last three editions of AT Kearney’s Global Cities Index, and cities such as Guangzhou and Bangalore have moved rapidly into the top 100 most globalised cities.

Emerging cities globalising at breakneck speedMost rapidly globalising cities according to GaWC

GaWC 2000Rank

GaWC 2012Rank

Change +

Doha 177 83 94Shenzhen 200 120 80Guangzhou 109 50 59Hanoi 147 100 47Dubai 54 10 44Bangalore 81 46 35Cape Town 94 64 30Beijing 36 8 28Lagos 123 97 26Chennai 102 77 25Shanghai 31 6 25Almaty 143 119 24Moscow 34 14 20Riyadh 95 75 20Lima 80 61 19

Source: GaWC, 2013

0

50

100

150

200

250

300

350

400

450

500

New Yo

rk

London

Tok

yo

Shangha

i Beiji

ng

Chongqi

ng

Jakarta

Tian

jin

Guangzh

ou

Istanbu

l

Shenzhe

n

Sao Paul

o

Donggua

n

Moscow

Mumbai

Luanda

Delh

i

Mexico

City

Chengdu

Lim

a

US$ billions

Globalisation and Competition: The New World of Cities 20 JLL

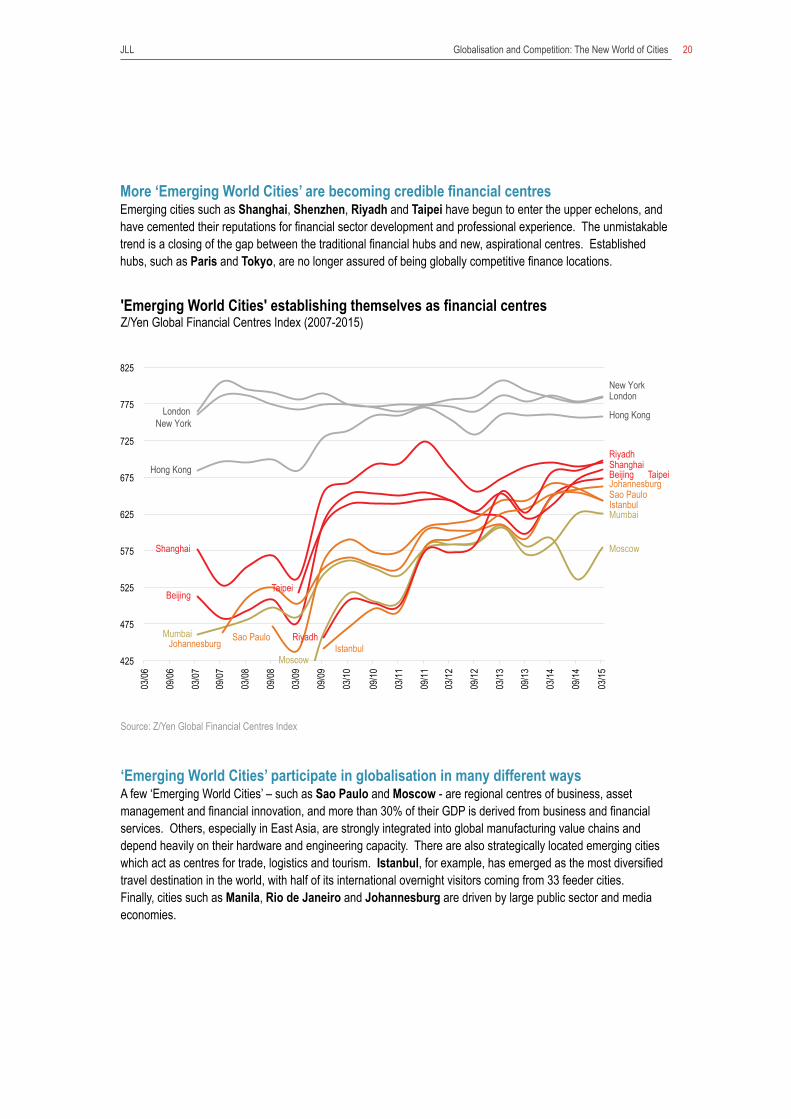

Source: Z/Yen Global Financial Centres Index

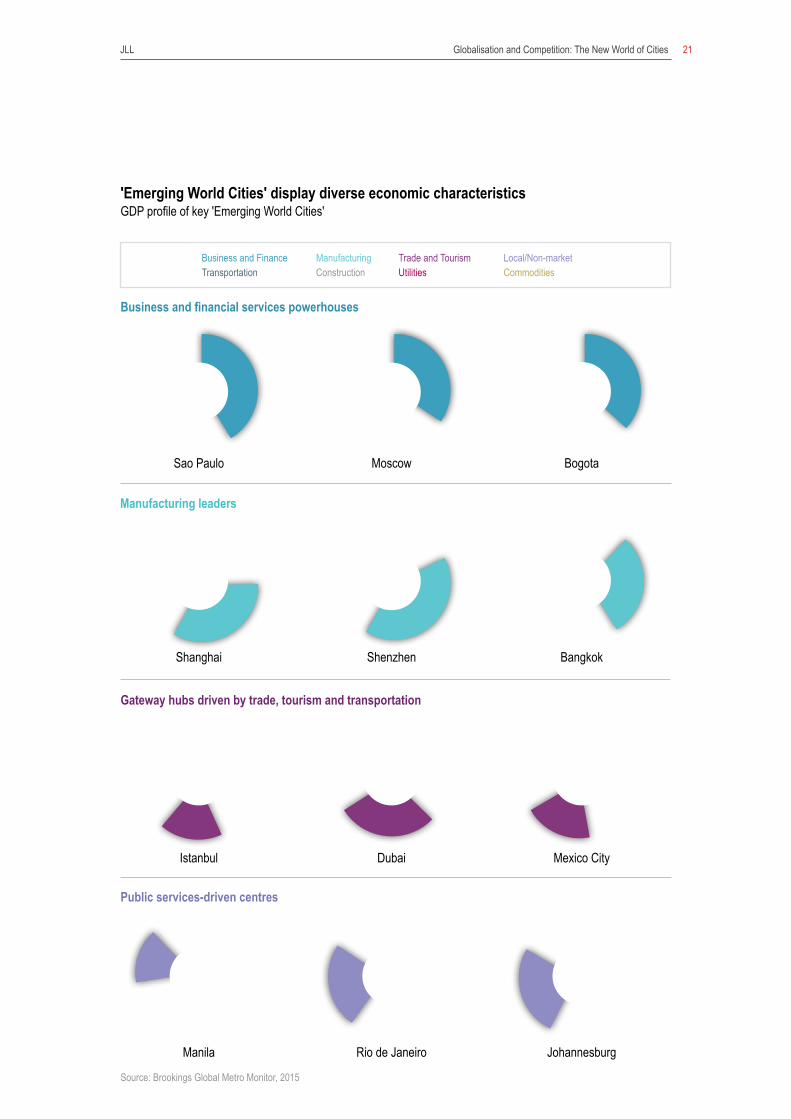

‘Emerging World Cities’ participate in globalisation in many different waysA few ‘Emerging World Cities’ – such as Sao Paulo and Moscow - are regional centres of business, asset management and financial innovation, and more than 30% of their GDP is derived from business and financial services. Others, especially in East Asia, are strongly integrated into global manufacturing value chains and depend heavily on their hardware and engineering capacity. There are also strategically located emerging cities which act as centres for trade, logistics and tourism. Istanbul, for example, has emerged as the most diversified travel destination in the world, with half of its international overnight visitors coming from 33 feeder cities. Finally, cities such as Manila, Rio de Janeiro and Johannesburg are driven by large public sector and media economies.

'Emerging World Cities' establishing themselves as financial centresZ/Yen Global Financial Centres Index (2007-2015)

425

475

525

575

625

675

725

775

825

03/06

09/06

03/07

09/07

03/08

09/08

03/09

09/09

03/10

09/10

03/11

09/11

03/12

09/12

03/13

09/13

03/14

09/14

03/15

London

New York

Hong Kong

Shanghai

Moscow

Mumbai

Sao Paulo

Beijing

Johannesburg

Istanbul

Taipei

London

New York

Hong Kong

Shanghai Riyadh

Riyadh

Moscow

Sao Paulo

Mumbai

Johannesburg

Istanbul

Beijing

Taipei

More ‘Emerging World Cities’ are becoming credible financial centres Emerging cities such as Shanghai, Shenzhen, Riyadh and Taipei have begun to enter the upper echelons, and have cemented their reputations for financial sector development and professional experience. The unmistakable trend is a closing of the gap between the traditional financial hubs and new, aspirational centres. Established hubs, such as Paris and Tokyo, are no longer assured of being globally competitive finance locations.

Globalisation and Competition: The New World of Cities 21 JLL

'Emerging World Cities' display diverse economic characteristicsGDP profile of key 'Emerging World Cities'

Manufacturing leaders

Public services-driven centres

Sao Paulo Moscow Bogota

Shanghai Shenzhen Bangkok

Manila Rio de Janeiro Johannesburg

Business and Finance Manufacturing Trade and Tourism Local/Non-market Transportation Construction Utilities Commodities

Gateway hubs driven by trade, tourism and transportation

Istanbul Dubai Mexico City

Source: Brookings Global Metro Monitor, 2015

Business and financial services powerhouses

Globalisation and Competition: The New World of Cities 22 JLL

Physical infrastructure is perhaps the most urgent deficit in 'Emerging World Cities'Taipei is the highest ranked emerging centre at 25th overall among 120 cities according to the EIU’s Hot Spots index, and 22nd of 50 in Grosvenor’s study on urban infrastructure resilience. Beijing and Shanghai are still rarely ranked in the top third of global studies on infrastructure, despite their spectacular levels of investment, because total coverage remains modest by Western standards, while housing and telecommunications are not always of the highest quality. Istanbul and Santiago both have stronger transport systems than other cities in their regions, while Mumbai, Buenos Aires and Manila consistently rate near the bottom. These cities have demand for physical capital investments, which will not only improve the day-to-day functionality of cities, but also make these cities more ‘investment-ready’.

The ability of emerging cities to occupy more lucrative roles in global value chains depends on their capacity to develop and attract talent. Innovation and skills are essential to building durable clusters. Some emerging cities have invested heavily in their higher education offer, such as Shanghai and Moscow, while indices show that cities like Buenos Aires, Bangkok and Kuala Lumpur have gained more skilled workforces in recent years. Sao Paulo, Mumbai and Istanbul have even become regional hubs of innovation, and are beginning to leverage and commercialise this capacity at scale for the first time.

'Emerging World Cities' building their higher education offerNumber of universities in the major higher education rankings

Scores are calculated by adding the number of higher education establishments in each city featured in the top 100 and 500 entries of The Times, QS and Shanghai Higher Education rankings.

Source: The Business of Cities, 2015

0

2

4

6

8

10

12

14

16

Beijing

Taipei

Shangha

i

Moscow

Buenos

Aires

Istanbu

l

Sao Paul

o

Santiag

o

Bogota

Prague

Guangzh

ou Tian

jin

St Petersb

urg

Warsaw

Cape To

wn

Kuala L

umpur

Bangkok

Johann

esburg

Rio de J

aniero

Delh

i

Top 100 Top 500

London Paris Toky

o

Hong Kong

New York

Singapo

re

18

20

22

24

26

28‘Big Six'

Globalisation and Competition: The New World of Cities 23 JLL

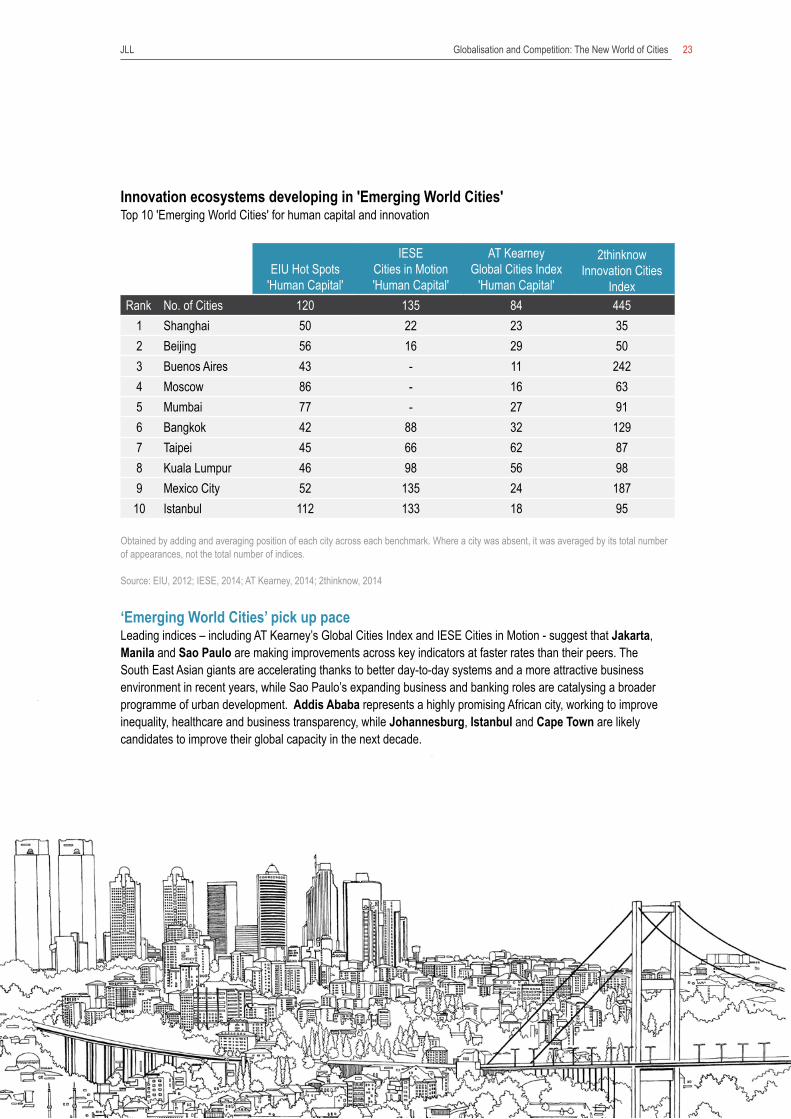

Innovation ecosystems developing in 'Emerging World Cities'Top 10 'Emerging World Cities' for human capital and innovation

EIU Hot Spots 'Human Capital'

IESE Cities in Motion 'Human Capital'

AT KearneyGlobal Cities Index

'Human Capital'

2thinknow Innovation Cities

IndexRank No. of Cities 120 135 84 445

1 Shanghai 50 22 23 352 Beijing 56 16 29 503 Buenos Aires 43 - 11 2424 Moscow 86 - 16 635 Mumbai 77 - 27 916 Bangkok 42 88 32 1297 Taipei 45 66 62 878 Kuala Lumpur 46 98 56 989 Mexico City 52 135 24 18710 Istanbul 112 133 18 95

Obtained by adding and averaging position of each city across each benchmark. Where a city was absent, it was averaged by its total number of appearances, not the total number of indices.

Source: EIU, 2012; IESE, 2014; AT Kearney, 2014; 2thinknow, 2014

‘Emerging World Cities’ pick up paceLeading indices – including AT Kearney’s Global Cities Index and IESE Cities in Motion - suggest that Jakarta, Manila and Sao Paulo are making improvements across key indicators at faster rates than their peers. The South East Asian giants are accelerating thanks to better day-to-day systems and a more attractive business environment in recent years, while Sao Paulo’s expanding business and banking roles are catalysing a broader programme of urban development. Addis Ababa represents a highly promising African city, working to improve inequality, healthcare and business transparency, while Johannesburg, Istanbul and Cape Town are likely candidates to improve their global capacity in the next decade.

Globalisation and Competition: The New World of Cities 24 JLL

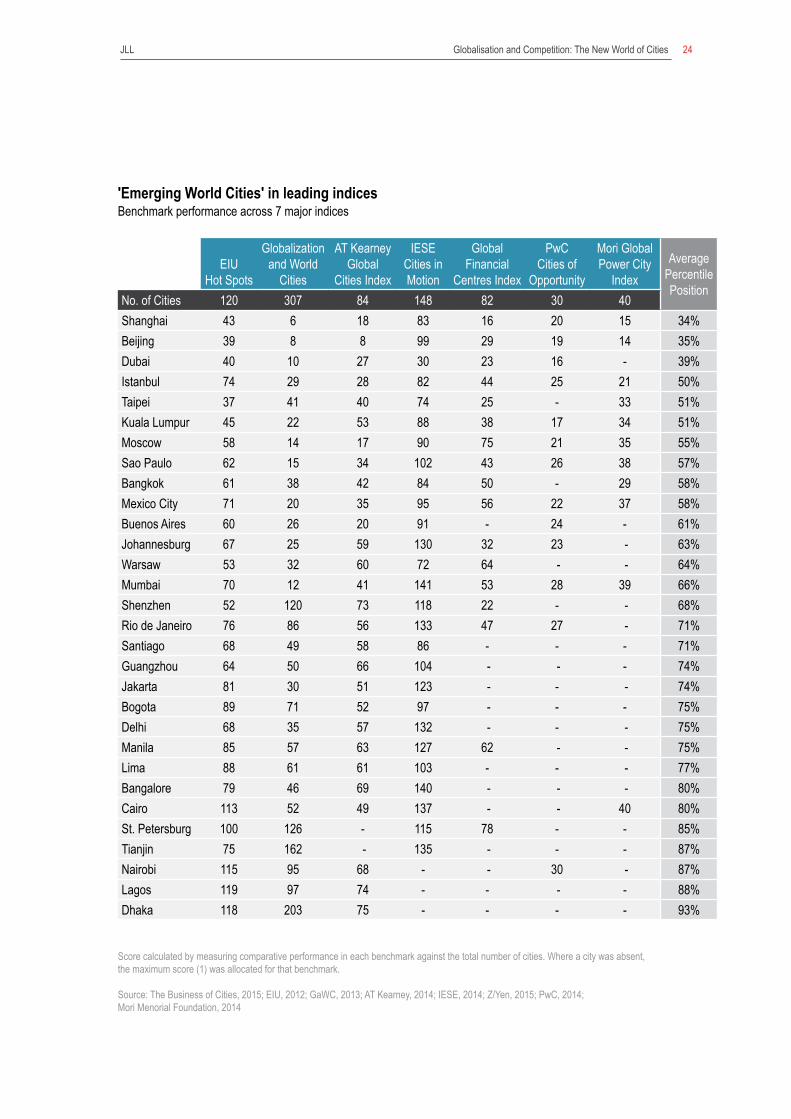

'Emerging World Cities' in leading indicesBenchmark performance across 7 major indices

EIU Hot Spots

Globalization and World

Cities

AT Kearney Global

Cities Index

IESE Cities in Motion

Global Financial

Centres Index

PwC Cities of

Opportunity

Mori Global Power City

IndexAverage

Percentile Position

No. of Cities 120 307 84 148 82 30 40Shanghai 43 6 18 83 16 20 15 34%Beijing 39 8 8 99 29 19 14 35%Dubai 40 10 27 30 23 16 - 39%Istanbul 74 29 28 82 44 25 21 50%Taipei 37 41 40 74 25 - 33 51%Kuala Lumpur 45 22 53 88 38 17 34 51%Moscow 58 14 17 90 75 21 35 55%Sao Paulo 62 15 34 102 43 26 38 57%Bangkok 61 38 42 84 50 - 29 58%Mexico City 71 20 35 95 56 22 37 58%Buenos Aires 60 26 20 91 - 24 - 61%Johannesburg 67 25 59 130 32 23 - 63%Warsaw 53 32 60 72 64 - - 64%Mumbai 70 12 41 141 53 28 39 66%Shenzhen 52 120 73 118 22 - - 68%Rio de Janeiro 76 86 56 133 47 27 - 71%Santiago 68 49 58 86 - - - 71%Guangzhou 64 50 66 104 - - - 74%Jakarta 81 30 51 123 - - - 74%Bogota 89 71 52 97 - - - 75%Delhi 68 35 57 132 - - - 75%Manila 85 57 63 127 62 - - 75%Lima 88 61 61 103 - - - 77%Bangalore 79 46 69 140 - - - 80%Cairo 113 52 49 137 - - 40 80%St. Petersburg 100 126 - 115 78 - - 85%Tianjin 75 162 - 135 - - - 87%Nairobi 115 95 68 - - 30 - 87%Lagos 119 97 74 - - - - 88%Dhaka 118 203 75 - - - - 93%

Score calculated by measuring comparative performance in each benchmark against the total number of cities. Where a city was absent, the maximum score (1) was allocated for that benchmark.

Source: The Business of Cities, 2015; EIU, 2012; GaWC, 2013; AT Kearney, 2014; IESE, 2014; Z/Yen, 2015; PwC, 2014; Mori Menorial Foundation, 2014

Globalisation and Competition: The New World of Cities 25 JLL

Categories of ‘Emerging World Cities’ Urban indices and benchmarks suggest that ’Emerging World Cities’ can be grouped into five categories:

1. Nearly Emerged Cities – Shanghai and BeijingThe exceptional growth of this pair means they have acquired important global roles and functions. Shanghai is now firmly among the top ten global finance hubs and is now the sixth most immersed city in global business networks, surpassing Tokyo for the first time. Beijing is only a little way behind, and leverages its political and decision-making status and strong media and cultural sectors. The capital is rapidly transferring industries and non-specialist activities to its suburbs and neighbouring Tianjin.

Both Shanghai and Beijing have made substantial improvements to their business climates, transport infrastructure, and provision of services to citizens and expats. They now rank first and third respectively for business friendliness in the Asia Pacific region, well up on 2011.10 Both have climbed four places in PwC’s Cities of Opportunity 'Transportation' measure since 2012, and have also improved rapidly in health, safety and security measures.

They have also set the bar in terms of urban management (they are managed as single municipal provinces) and capacity to invest in city systems. In recent years, their rise has slightly slowed due to China’s macro-economic challenges and the complexity of investing in quality-oriented growth. From now on future improvement is likely to be more incremental in character.

The New World Order of Cities

Established World Cities New World Cities New York London Paris

Munich Oslo Barcelona

Nearly Emerged

Lagging Megacities

Shanghai Beijing

Dhaka Lagos

Karachi

Tokyo Hong Kong Singapore

Vancouver Denver Brisbane

Competitive Megacities

High Potential / Weakly Governed

Istanbul Kuala Lumpur

Taipei Mexico City

Mumbai Manila Jakarta

Agile Higher-Quality Emerging

Santiago Bangalore Shenzhen

Dubai

Emerging World Cities

Illustrative examples in each category Source: The Business of Cities, JLL, 2015

Globalisation and Competition: The New World of Cities 26 JLL

2. Competitive Megacities This group of 8-10 cities has entered a key cycle of internationalisation. Usually rated among the 40 most globalised cities and in the top 75 for all-round performance, they are gateways to large domestic or regional markets and have important decision-making functions. They record high investment rates, and have an impressive infrastructure project pipeline that augurs well for their capacity to absorb growth at a metropolitan scale.

Kuala Lumpur, Taipei and Istanbul are the strongest examples of this type of city. All three benefit from a highly strategic location and dynamic labour markets as they upgrade into higher value sectors. Moscow is also among the top group, while Sao Paulo, Mexico City and Buenos Aires continue to be evenly matched in Latin America. Collectively they face big quality of life, infrastructure and governance challenges, which will become more acute as they continue to attract talent and firms. Most have strong relationships with national governments at the moment, but will need continued support for governance and fiscal reforms that will enable them to optimise their assets and escape growth rigidities (e.g. mono-centric development) during periods of slower growth.

3. Agile Higher Quality Emerging CitiesAgile higher quality emerging cities such as Warsaw and Santiago have attractive business environments, extensive development opportunities and comparatively well-educated populations that are allowing them to find niches in global supply chains. Chinese cities like Shenzhen and Guangzhou are also in this category, as are Colombo and Chengdu, which have been two of the fastest growing destination cities in the world since 2009.11 Many have effectively leveraged property taxes, local user fees, and the monetisation of public land to invest in public services. These medium-sized emerging cities have some low-income housing and transport challenges, but fewer of the sprawling slum problems of other larger emerging centres. Typically, they are actively building international functions within the wider knowledge economy.

Dubai occupies a unique niche on the world stage. The emirate combines many characteristics of both established and emerging cities, thanks to its meteoric and unprecedented rise. Overall, however, the city's attractive business environment and international profile, alongside its finance and knowledge-based strengths, mark it out as an agile higher quality emerging city.

4. High Potential but Weakly Governed Megacities Manila, Mumbai and Jakarta are performing well at attracting real estate investment and outsourcing activities, but also have more chronic infrastructure supply challenges than the cities above. Transnational firms find these cities attractive as they expand their operations in South and South East Asia, because of low costs and huge consumer market opportunities; however they face considerable urban infrastructure shortages.

For these types of cities to capitalise on their potential, their first priorities remain leadership, governance and co-ordination – all prerequisites to quality of life and economic ambitions. They need to reduce the complexity of preparing, assembling and executing projects, which prevents capital investment budgets from being fully deployed on a year-by-year basis. They also rely on national policy to devise more effective plans for the national ‘system of cities’, and formal recognition from the national level of the unique burden of being a large globalising metropolitan area.

Globalisation and Competition: The New World of Cities 27 JLL

5. Lagging MegacitiesFinally, there is a group of lagging megacities, such as Dhaka and Karachi, which are struggling to cope with the pace of population growth, fragmented governance and a lack of inward investment. They are not fully integrated in global value chains and have huge issues of tackling youth unemployment and consumer demand. Often their ability to attract investment is hampered by weak local capacity and political instability. Most larger sub-Saharan African cities feature in this group but a few cities, like Lagos and Nairobi, are rising above the parapet and beginning to attract significant investment and corporate activity.12

The rise of ‘Emerging World Cities’ is already uneven The rise of ‘Emerging World Cities’ is already uneven and will become more so as each city prepares differently for the next cycle of growth. Many face the dilemmas that ‘Established World Cities’ first tried to address 50 years ago - car-dependence, demographic strain, infrastructure deficits and environmental imbalances. But given their size and demographics, the challenges are principally those of pace and scale, whether in upgrading housing supply, core utilities, or transport systems.

There is a strong correlation between the index performance of ‘Emerging World Cities’ and the capacity they have to invest in their growth. Chinese cities have had comparatively wide opportunities, while cities with weaker fiscal tools such as Cairo and Mexico City have struggled.13 Given that infrastructure investments in emerging cities need to be in the range of 4-6% of urban GDP by 2025 – around US$20 billion annually in a city like Istanbul – they urgently need independent financing mechanisms and, in some cases, fairer tax and fiscal arrangements vis-à-vis the rest of the country.14

‘Emerging World Cities’ therefore need to solve three major barriers to growth and success:i. how to build and sustain multiple sources of investment for infrastructure and development; ii. how to attract talent and bridge local skills gaps; and iii. how to organise and co-ordinate the metropolitan space.

Without systems and strategies to address these, ’Emerging World Cities’ will struggle to manage their growth effectively and succeed with economic development.

Success of ‘Emerging World Cities’ linked to clear, bold and durable leadership structures Taipei is by far the highest ranked emerging city for institutional effectiveness, at 28th according to the EIU’s Hot Spots Index. Among emerging cities (excluding city-states and emirates), only Taipei, Johannesburg, Durban, Cape Town and Warsaw make the top 60 cities. The most strongly governed cities in the next tier are Kuala Lumpur, Santiago and Buenos Aires. Because of this, City RepTrak’s 2014 index on urban reputations finds only Taipei and Warsaw in the top 50, at 47th and 49th, while other emerging cities struggle - Sao Paulo (73rd), Istanbul (75th) and Moscow (94th).

Not all ‘Emerging World Cities’ will automatically evolve into ‘Established World Cities’. Their potential as sites of global production, innovation, consumption or investment depends on decisions and strategies made around infrastructure, quality of life and economic development by city and national governments.

Globalisation and Competition: The New World of Cities 28 JLL

New World Cities

The rise of smaller, specialised, globally-oriented citiesThe current cycle of globalisation has seen the rise of many smaller, more specialised, but highly globally-oriented, cities. This group of cities are neither ‘established’ nor ‘emerging’. They are smaller, high-income cities with efficient infrastructure, an attractive quality of life, and fewer social, environmental or economic externalities such as crime, pollution, congestion, high costs or inequality. Unlike ‘Emerging’ or ‘Established World Cities’, they are often not the primary city in their national or regional system of cities.

These ‘New World Cities’ have begun to internationalise their economies based on a small number of specialisms derived from their comparative advantages as smaller, more liveable and attractive centres. Several are knowledge, cultural or entertainment hubs, but many also possess hi-tech, innovation or research capabilities that make them important cities in the convention and higher education economies.

Because they do not often possess major political or institutional functions, ‘New World Cities’ are more agile than their nearest ‘Established World Cities’. They are becoming specialised centres for decision-making, knowledge-intensive sectors and quality of life. They now compete openly in contested global markets (e.g. for tourism, higher education, events, R&D, summits, medicine).

Defining a ‘New World City’

Scale and productivity US$100-400 billion metropolitan economy, 1-8 million populationInternationalisation Top 120 for global economic connectivityInvestibility Top 100 for commercial investmentAppeal and opportunity Top 50 for knowledge, visitors or brandSpecialisation Highly competitive (top 20) in at least one index areaFirst cycles of development Absent from the top 40 of 3 or more index areas

There are a number of drivers that give rise to ‘New World Cities’:i. The global economic centre of gravity is shifting east and south. This creates new opportunities for

cities that were more peripheral, such as Brisbane, as well as imperatives for cities that must fight to remain relevant and influential, like Helsinki. The changing economic geography brings new market opportunities.

ii. The mobility and global reach of the new global middle classes means that there is a much wider and deeper reservoir of demand, whether for education, experiences or economic opportunity. ‘New World Cities’ that have attractive climates, urban design or commercial clusters are now on the radar of 3 or 4 billion people. This is why a medium-sized city like Houston is the fastest growing visitor destination in North America since 2009, and why Hamburg is Europe’s second fastest growing destination, behind only Istanbul.

iii. Global urbanisation reshapes the economic and spatial balance of nations. Although some nations have seen benefits accrued mainly to the largest or capital city, second or third-tier centres have absorbed some of the excess demand, or have benefited from national policies to disperse and re-distribute growth. National ‘systems of cities’ have emerged where different cities gain complementary specialisations, allowing medium-sized cities to become more internationally oriented and competitive.

Globalisation and Competition: The New World of Cities 29 JLL

iv. New and emerging business sectors are internationalising. The footloose nature of sectors such as digital media, clean technology, design, tradable urban services, film, TV, and life sciences means ‘New World Cities’ can offer agile businesses an excellent eco-system for growth and global trade and investment.

v. Technology is driving new systems of production and integration. A new generation of products, services and innovation means that supply chains and value chains have become more complex. More cities can offer opportunities for businesses to invent, test and commercialise. The digitisation of business provides the flexibility to select from a wider range of city locations, while the sharing economy favours cities.

'New World Cities' attract a disproportionate share of global investment Relative to their size, ‘New World Cities’ attract a disproportionate share of global investment as investors look for value beyond the core group of ‘Established’ and ‘Emerging World Cities’. Munich, Melbourne and Denver, for example, are not in the top 50 largest cities but are regularly in the global top 30 for direct commercial real estate investment flows and attractiveness.15 The top ranks of the JLL Investment Intensity Index, which compares the volume of direct real estate investment relative to the economic size of a city, is dominated by ‘New World Cities’ such as Oslo, Auckland and Austin.16 These cities all have robust technology sectors supported by a high quality of life and strong environmental credentials, factors which are increasingly being incorporated, either explicitly or implicitly, into real estate investment strategies.

Melbourne, Miami, Vancouver, Vienna, Barcelona and Seattle all regularly feature among the top 15 candidates for foreign investment in their respective regions,17 while even less established cities such as Brisbane and Auckland excel for their investment strategies.18

'New World Cities' dominate JLL's Investment Intensity IndexJLL Investment Intensity Index - Global Top 20

3-year rolling total direct real estate investment volumes to Q2 2015Source: JLL, September 2015

London 1

Munich2

Sydney3

Oslo4

Honolulu 5

Auckland6

Frankfurt 7

Copenhagen 8

Stockholm 9

San Jose10

San Francisco 11

Austin 12

Melbourne13

Dublin14

Paris15

Gothenburg16

New York17

Boston18

Warsaw20

Brisbane19

Total Real Estate Investment as a Proportion of City GDP

Globalisation and Competition: The New World of Cities 30 JLL

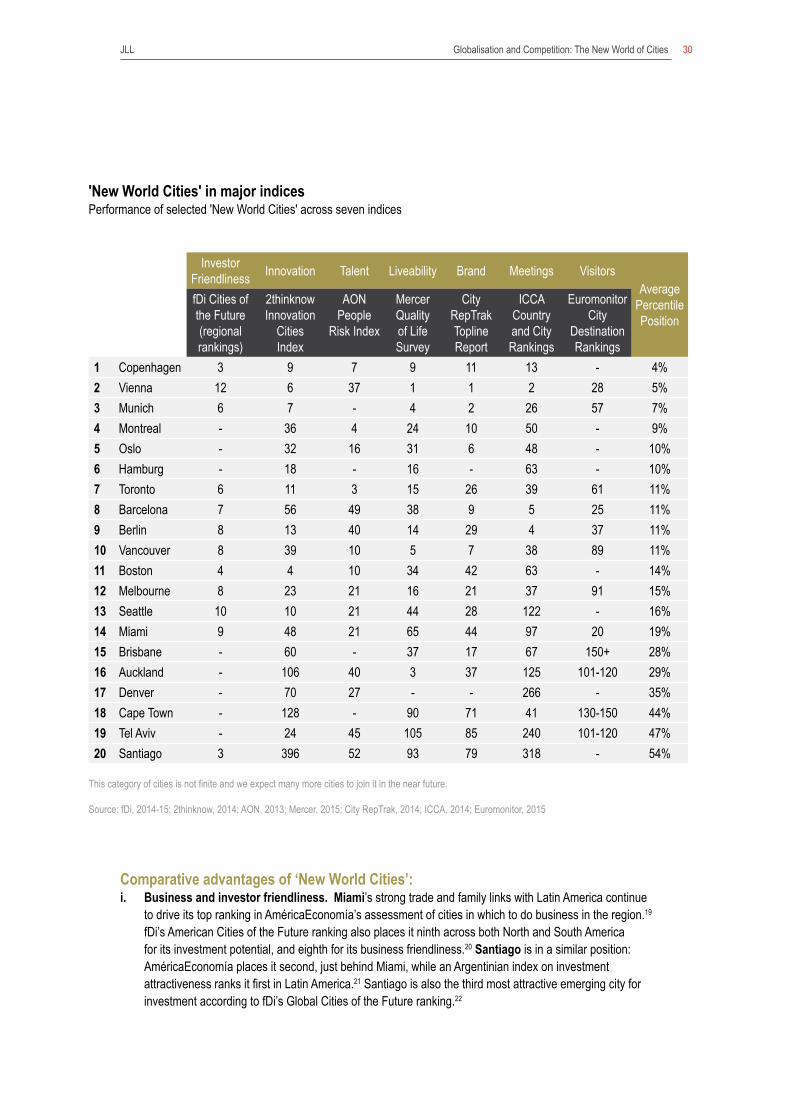

'New World Cities' in major indicesPerformance of selected 'New World Cities' across seven indices

Investor Friendliness Innovation Talent Liveability Brand Meetings Visitors

Average Percentile Position

fDi Cities of the Future (regional rankings)

2thinknow Innovation

Cities Index

AON People

Risk Index

Mercer Quality of Life Survey

City RepTrak Topline Report

ICCA Country and City Rankings

Euromonitor City

Destination Rankings

1 Copenhagen 3 9 7 9 11 13 - 4%2 Vienna 12 6 37 1 1 2 28 5%3 Munich 6 7 - 4 2 26 57 7%4 Montreal - 36 4 24 10 50 - 9%5 Oslo - 32 16 31 6 48 - 10%6 Hamburg - 18 - 16 - 63 - 10%7 Toronto 6 11 3 15 26 39 61 11%8 Barcelona 7 56 49 38 9 5 25 11%9 Berlin 8 13 40 14 29 4 37 11%10 Vancouver 8 39 10 5 7 38 89 11%11 Boston 4 4 10 34 42 63 - 14%12 Melbourne 8 23 21 16 21 37 91 15%13 Seattle 10 10 21 44 28 122 - 16%14 Miami 9 48 21 65 44 97 20 19%15 Brisbane - 60 - 37 17 67 150+ 28%16 Auckland - 106 40 3 37 125 101-120 29%17 Denver - 70 27 - - 266 - 35%18 Cape Town - 128 - 90 71 41 130-150 44%19 Tel Aviv - 24 45 105 85 240 101-120 47%20 Santiago 3 396 52 93 79 318 - 54%

This category of cities is not finite and we expect many more cities to join it in the near future.

Source: fDi, 2014-15; 2thinknow, 2014; AON, 2013; Mercer, 2015; City RepTrak, 2014; ICCA, 2014; Euromonitor, 2015

Comparative advantages of ‘New World Cities’:i. Business and investor friendliness. Miami’s strong trade and family links with Latin America continue

to drive its top ranking in AméricaEconomía’s assessment of cities in which to do business in the region.19 fDi’s American Cities of the Future ranking also places it ninth across both North and South America for its investment potential, and eighth for its business friendliness.20 Santiago is in a similar position: AméricaEconomía places it second, just behind Miami, while an Argentinian index on investment attractiveness ranks it first in Latin America.21 Santiago is also the third most attractive emerging city for investment according to fDi’s Global Cities of the Future ranking.22

Globalisation and Competition: The New World of Cities 31 JLL

ii. Innovation and tech sector leadership. More than half of the 20 most innovative cities in the world are ‘New World Cities’. Centres such as Melbourne and Toronto have seen their economies thrive around their ability to incubate and commercialise new ideas. Melbourne is ranked as the second best student city in the world and Toronto is ninth, not only because of their concentration of leading universities, but also their capacity to attract students from across their respective continents.23 Toronto is 11th of over 400 on 2thinknow’s innovation benchmark, while Melbourne is 23rd, both outperforming their size.24 Leaders in ‘New World Cities’ also focus on reducing the burden on business as much as possible. Toronto is rated the third least risky city to relocate to, according to AON’s People Risk Index of 130 cities, while Boston and Melbourne also excel.25 High investment in education, enterprise and diversity has also seen ‘New World Cities’ enter the top 10 for human capital in many indices.26 Both Toronto and Melbourne also come out strongly on AT Kearney’s ‘Human Capital’ sub-index, with Toronto ranked 8th and Melbourne 12th, thanks to high graduate concentrations and their diverse demographic profiles.

iii. Attractiveness, lifestyle and brand. Many ‘New World Cities’ leverage their natural and inherited assets in order to build global profile. Today, nearly two-thirds of the top 20 most trusted and admired cities are ‘New World Cities’, according to the Reputation Institute’s major study. Auckland, a city which has made it an ambition to become the most liveable city in the world, is now third on Mercer’s survey and is becoming a more attractive cultural and work destination.27 New Zealand’s business capital is an impressive third of 69 cities on the UN-Habitat’s ‘Environment’ sub-index.28 Barcelona is another 'New World City' whose dynamic visitor brand means it is now in the top 10 of two major brand indices, because of its perceived charm and vibrancy, as well as the top 5 for international conventions and conferences. These ‘New World Cities’ are experiencing high demand in many markets.

Maintaining competitive advantage‘New World Cities’ need to adapt their model of success in order to sustain their progress. Often there is a danger that a city becomes seen as a ‘one-trick pony’, or that it fails to live up to its brand promise due to the strains of a whole cycle of growth.

As a result, many city and metropolitan leadership organisations now work actively to limit the externalities that this demand creates on their appeal, and generate the conditions that will expand their innovation economy.29 Projects such as the Greater Sydney Commission, Barcelona Global Talent Programme, and the Project Oslo Region all reflect a new impetus to create the scale and maintain the quality to compete.

Many areas for improvement for ‘New World Cities’ are visible and trackable in city indices. A lot of ’New World Cities’ – such as Munich, Miami and Sydney – fall short in terms of their digital systems, measured in terms of broadband quality, affordability and market development.30 Most are also in the bottom half – and falling - of indices that track road congestion. And at least 10 ‘New World Cities’ are now at least as expensive as ‘Established World Cities’, mainly because of food, clothes and entertainment costs.31

Globalisation and Competition: The New World of Cities 32 JLL

'New World Cities' exhibit a diverse range of strengthsComparative advantages of selected 'New World Cities'

City Key Strengths

Index Performance

Auckland Urban Environment and Visitor Appeal

3rd in Mercer Quality of Living Survey; 3rd in UN-Habitat Environment Index

Barcelona Culture and Tourism 14th in AT Kearney Global Cities Index ‘Cultural Experience’; 11th in MasterCard Global Destination Cities

Boston Tech and Human Capital 4th in 2thinknow Innovation Cities Index; 7th in AT Kearney Global Cities Index ‘Human Capital’

Brisbane Quality of Life 20th in EIU Liveability Index

Berlin Culture and Innovation 3rd in Youthful Cities Index;13th in 2thinknow Innovation Cities Index

Cape Town Attractiveness and Visitor Appeal

52nd in ICCA Country and City Rankings;1st in African Green City Index

Copenhagen Quality of Life and Talent 9th in Mercer Quality of Living Survey; 7th in AON People Risk Index

Denver Tech and Lifestyle27th in Milken Institute’s Best-Performing Cities 'High Tech GDP Concentration'; 18th in Gallup/Healthways Well-being Index

Hamburg Liveability and Commercial Innovation

16th in Mercer Quality of Living Survey;18th in 2thinknow Innovation Cities Index

Melbourne Human Capital 12th in AT Kearney Global Cities Index ‘Human Capital’

Miami Business Friendliness 1st in AméricaEconomía Places to do Business in Latin America

Montreal Human Capital and Reputation

4th in AON People Risk Index;10th in City RepTrak

Munich Brand, Innovation and Productivity

2nd in City Reptrak; 7th in Innovation Cities Index; 1st in ‘Economic Potential’ among large cities, fDi European Cities of the Future

Oslo Infrastructure Platform 3rd in European Green City Index;1st in UN-Habitat Infrastructure Index

Santiago Investment Openness 2nd in AméricaEconomía Places to do Business in Latin America

Seattle Human Capital 10th in 2thinknow Innovation Cities Index; 8th in EIU Hot Spots ‘Human Capital’

Tel Aviv Digital Technology 2nd in Start-up Genome

Toronto Talent and Innovation5th in PwC Cities of Opportunity ‘Intellectual Capital and Innovation’;11th in 2thinknow Innovation Cities Index

Vancouver Sustainability and Quality of Life

3rd in EIU Liveability Index;2nd in North American Green City Index

Vienna Lifestyle, Visitor Appeal and Reputation

1st in Mercer Quality of Living Survey;1st in City RepTrak

Source: Business of Cities, 2015

Globalisation and Competition: The New World of Cities 33 JLL

The current cycle of globalisation is enabling more cities than ever to ‘go global’. The rigid pecking order is breaking down as cities increasingly specialise in certain niche markets. This is fundamentally changing the geography of commercial real estate and, dependent on the ‘type’ of city, will have deep implications for real estate formats, assets and opportunities:

Established World Cities aim to capture footloose services, corporations and world-class talent. These cities have been hugely successful in attracting real estate capital and, such is their attraction for sovereign wealth funds, institutions and high-net-worth individuals, that the ‘Big Six’ alone (London, New York, Tokyo, Paris, Singapore and Hong Kong) account for more than one-fifth of total global activity. Yet to retain their competitive advantage, these cities will need to execute bold urban transformation plans (such as the ambitious ‘Grand Paris’ project) to support the shift to new modes of economic activity and to ensure the efficient recycling of land. Affordability has become a critical issue for cities such as London, New York and Hong Kong, where there are pressing requirements for appropriately-priced and flexible urban business space for the expanding innovation economy. A major boost to new residential supply and to delivery solutions is also crucial for maintaining their competitive edge.

Emerging World Cities are looking to attract catalytic foreign investment, as well as to nurture indigenous industries and services. To support rapid urbanisation, cities like Shanghai, Mexico City and Istanbul are witnessing massive expansion of their real estate inventory through the construction of impressive mixed-use schemes and trophy developments, which are seen as the hallmark of a modern city. But as these cities move to the next phase in their evolution, the real estate sector will play a more pivotal role in creating a ‘sense of place’ and contributing to city identity, uniqueness and well-being. As these are some of the world’s most environmentally challenged cities, real estate will be a key driver of more sustainable urban models. Improvements in real estate transparency also need to progress at much greater speed, not only to attract new capital, but to enhance the business operating environment and contribute to the quality of life of its citizens.

New World Cities are striving to attract mobile entrepreneurs, students, conventions and young institutions. These cities are the home of many ‘millennials’; a demographic that is demanding less conventional real estate – with a preference for characterful properties and locations in vibrant mixed-use neighbourhoods. Real estate will play a crucial role in building an alliance between businesses, universities and civil society. These cities will lead in the provision of energy-efficient and smart buildings. 'New World Cities' are proving to be particularly attractive for real estate investors who are, either implicitly or explicitly, taking into consideration issues of liveability, sustainability and technological prowess in their strategic decision-making.

Globalisation, urbanisation and technological advancement are creating sweeping changes to urban form, to urban living and to urban challenges. The true value of real estate for all types of cities is in providing the infrastructure and environment for productive activity that facilitates creativity, innovation and entrepreneurship, while at the same time fostering a sense of community and well-being for its citizens.

A Real Estate Perspective

Globalisation and Competition: The New World of Cities 34 JLL

Each city typology faces unique challengesStrategic imperatives for three different kinds of world city

Established World Cities Emerging World Cities New World Cities

Population Maintain population growth from international in-migration.

Implement a more managed approach to population growth and to rural migration.

Build an alliance around talent attraction.

Housing Boost new supply in housing markets and confront NIMBY-ist tendencies.

Provide attractive entry level housing efficiently and quickly enough.

Monitor housing range and affordability to suit under 35s.

Inequality Address challenges of urban under-class.

Tackle polarisation of income and service access.

Ensure a strong focus on inclusive growth via skills development and mixed-use housing.

Sustainability Tackle climate change adaptation and resilience.

Reduce vulnerability to climate change, flooding, earthquakes.

Active leadership on energy efficiency and mix, low pollution, green economy, resilience.

Land Undertake big redevelopment efforts to shift from old to new modes and recycle land effectively.

Rationalise land use and spatial governance to achieve coherent urban and metropolitan forms.

Agreed spatial strategy managed by lead agency. Ensure projects are investment ready.

Business framework

Maintain competitive business climate and tax regime and IP environment.

Improve productivity and business climate, especially legal and regulatory framework. Focus on transparency and confidence.

Improve information and co-ordination. Foster start-up growth.

Talent Maintain public support for openness, especially at national level.

Ensure openness to international talent, while fostering cosmopolitanism and multi-lingualism.

Gain visibility among international talent and entrepreneurs. Maintain affordability.

Infrastructure Undertake infrastructure modernisation, e.g. transport, water, waste, energy.

Tackle major infrastructure and basic housing deficits

Enhance international air and port links, especially to growth markets. Focus on digital connectivity.

Economic development

Ensure affordability for new entrants in the emerging innovation economy.

Give sufficient support to new entrants and emerging sectors.

Expert specialisation, innovation, digital and science. Leverage big events.

Brand and identity Maintain clear identity in highly competitive environment.

Establish identity and live up to brand promise.

Build a business and investor brand to complement its other stronger brands. Improve work-life balance.

Metro governance Promote networked and collaborative governance across the functional region.

Promote maturity of institutions, municipal governments’ capacity and tools.

A broader leadership platform, involving business, universities and civil society. Embrace the metropolitan agenda.

Inter-governmental relationships

Improve fiscal arrangements with national government.

Attain recognition of urban agenda and spatial economy by national government.

Build story from scratch and gain active support for internationalisation programme.

Source: The Business of Cities, 2015

Globalisation and Competition: The New World of Cities 35 JLL

Dubai, UAE