Prepared by Netscribes (Research on Global Markets) Proprietary and Confidential, Copyright © 2017, Netscribes, Inc. All Rights Reserved The content of this document is confidential and meant for the review of the recipient. Disclaimer: The names or logos of other companies and products mentioned herein are the trademarks of their respective owners Global Telematics Market (2014-2022) December, 2017 Sample pages

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Prepared by Netscribes (Research on Global Markets)

Proprietary and Confidential, Copyright © 2017, Netscribes, Inc. All Rights Reserved

The content of this document is confidential and meant for the review of the recipient.

Disclaimer: The names or logos of other companies and products mentioned herein are the trademarks of their respective owners

Global Telematics Market (2014-2022)

December, 2017

Sample pages

Chapter 1: Executive Summary

2

3

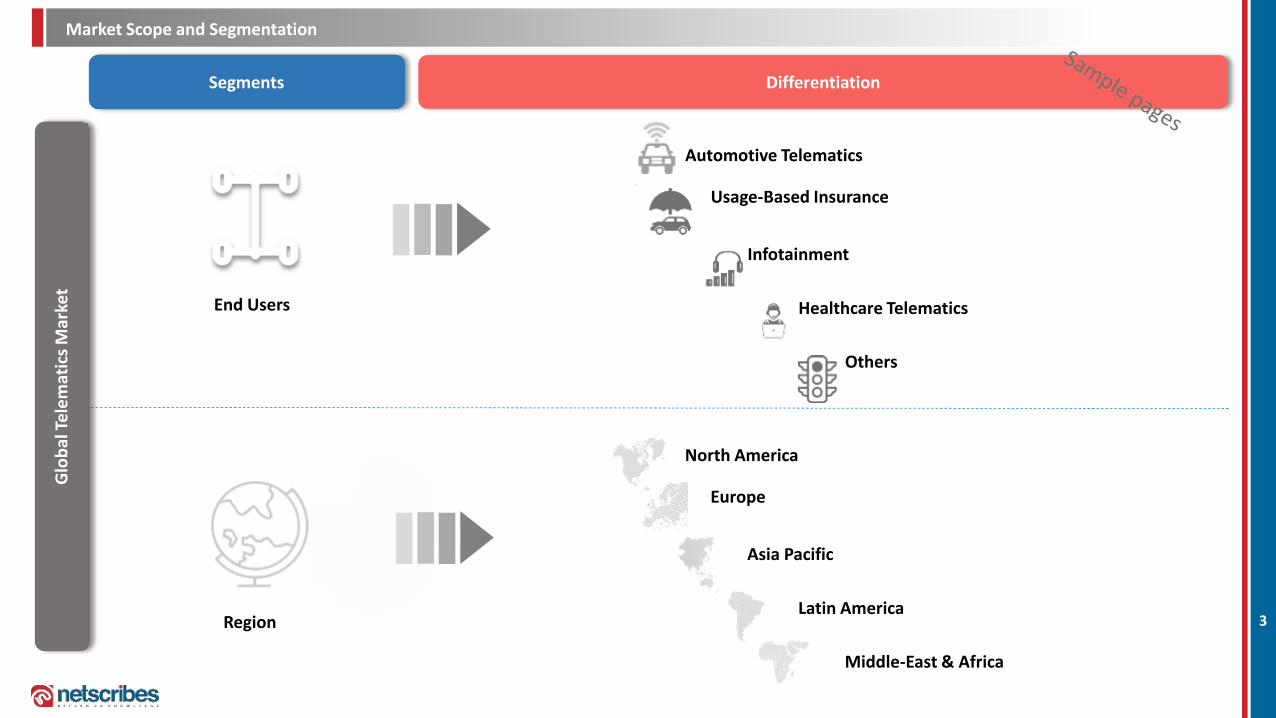

Market Scope and Segmentation

Glo

bal

Te

lem

atic

s M

arke

tSegments Differentiation

End Users

Region

North America

Europe

Latin America

Middle-East & Africa

Asia Pacific

Automotive Telematics

Usage-Based Insurance

Healthcare Telematics

Others

Infotainment

4

Key Questions Answered in This Study

Inte

rve

nti

on

al C

ard

iolo

gy M

arke

t

What is the overview of the Global Telematics Market?

What was the market size in the past, and what is the current and the forecasted size for

the Global Automotive Telematics market (Fleet telematics and connected car market),

Usage-Based Insurance, Infotainment, Healthcare Telematics and Others sectors?

What was the market size in the past, and what is the current and forecasted regional

(North America, Europe, Asia Pacific, Latin America, Middle East & Africa) market size for

Global Automotive Telematics, Usage-Based Insurance, Infotainment, Healthcare Telematics

and other sectors?

Who are the stakeholders and technology ecosystem in telematics for different segments?

What are the major drivers and challenges affecting the Global Telematics Market and

Automotive Telematics, Usage-Based Insurance, Infotainment, Healthcare Telematics and

Others sectors?

What is the competitive landscape and profiles of major public and private players

operating in the market, this include companies which provide vehicle tracking system,

telematics device and GPS fleet tracking system?

What are the recent key developments in Automotive Telematics, Usage-Based Insurance,

Infotainment, Healthcare Telematics and Others sectors.?

What are the market trends in Automotive Telematics, Usage-Based Insurance,

Infotainment, Healthcare Telematics and Others sectors.?

5

Executive Summary – Global Telematics Market

Ove

rvie

w

Trends2014 2017 2022

$ bn

• Global Telematics Market is expected to grow at a CAGR of X.X% between 2017 and 2022, from USD XX.XX billion (2017) to USD XX.XX billion (2022). Similarly,

• Automotive Telematics generates along with Infotainment and UBI generates XX.XX% revenue and the rest is generates from health market and government initiatives(others).

• North America and Europe are pioneers in telematics usage. Customers’ awareness is high in these regions and market is stable. However, Asia Pacific is adapting faster dueto factors like safety, security, fuel cost , environment protection and government regulation. However, Latin America and Middle East & Africa faces challenges likeeconomic slowdown, political instability and lack of telematics infrastructure.

Increasing requirement to track vehicles on a real-time basis and observe drivers’ behavior (monitoring health, temperament while driving, therequirement for Others or knowledge about government laid down regulations) is leading to growing usage of telematics technology.

Reduce cost of claims by 40% and policy management by 50%, which in turn would minimize the acquisition cost leading to effective policy pricing

Shift in demand from simple music systems to value-added services, technology embedded devices and applications in vehicles.

Growing demands for telemedicine applications used by health professionals for remote consultation and also for collaborative medical assistance isexpected in near future

Augmenting demand for Big Data analytics is opening up revenue generation stream for both service and retail based organizations.

Companies are introducing Crash and Claim programs which would play a significant role in driving the UBI market.

Complete medical records can be collected across providers and when data from electronic medical records system and consumer wearable are merged,it is possible to process data faster

Collecting Toll Tax from vehicles through telematics based technology has been one of the biggest achievement

• Lack of awareness among individual car owners and resistance to additional expenditure for installation of new devices in old cars or vehicles

• Customers' for whom privacy is extremely important do not prefer UBI companies’ tracking their daily movements.

• Software updates may become problematic and space problems in devices may hinder automatic software update.

• Lack of innovation in healthcare insurance industry and customers awareness towards technology based insurance solutions

• Telematics device installation cost, mobile data fees, employee training and monitoring report data is a complex and costly set of activity for the Government

Chapter 2: Introduction: Market Overview

7

Market Definition

Telematics Automotive Telematics

Others

Healthcare Telematics

Others

Usage Based Insurance

TELEMATICS

HEALTHCARE TELEMATICS

AUTOMOTIVE TELEMATICS

MEDIA AND ENTERTAINMENT

Healthcare Telematics

OTHERS

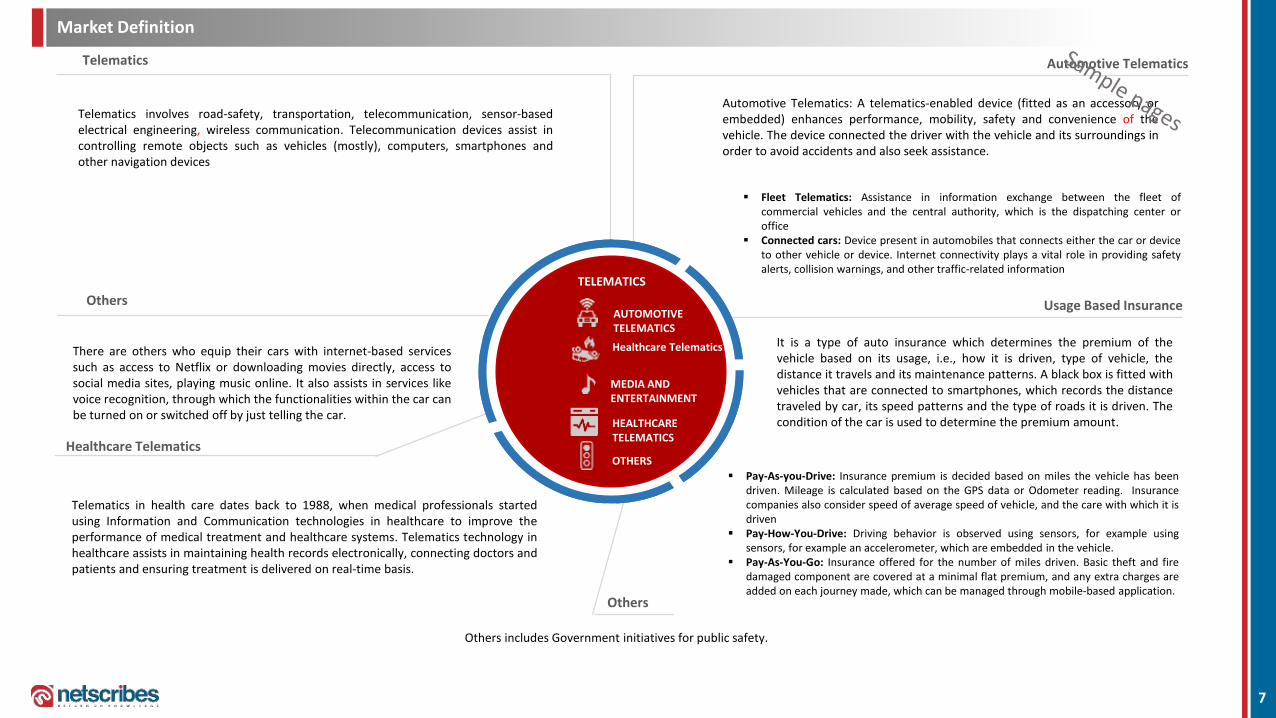

Telematics involves road-safety, transportation, telecommunication, sensor-basedelectrical engineering, wireless communication. Telecommunication devices assist incontrolling remote objects such as vehicles (mostly), computers, smartphones andother navigation devices

Automotive Telematics: A telematics-enabled device (fitted as an accessory orembedded) enhances performance, mobility, safety and convenience of thevehicle. The device connected the driver with the vehicle and its surroundings inorder to avoid accidents and also seek assistance.

Fleet Telematics: Assistance in information exchange between the fleet ofcommercial vehicles and the central authority, which is the dispatching center oroffice

Connected cars: Device present in automobiles that connects either the car or deviceto other vehicle or device. Internet connectivity plays a vital role in providing safetyalerts, collision warnings, and other traffic-related information

There are others who equip their cars with internet-based servicessuch as access to Netflix or downloading movies directly, access tosocial media sites, playing music online. It also assists in services likevoice recognition, through which the functionalities within the car canbe turned on or switched off by just telling the car.

Telematics in health care dates back to 1988, when medical professionals startedusing Information and Communication technologies in healthcare to improve theperformance of medical treatment and healthcare systems. Telematics technology inhealthcare assists in maintaining health records electronically, connecting doctors andpatients and ensuring treatment is delivered on real-time basis.

It is a type of auto insurance which determines the premium of thevehicle based on its usage, i.e., how it is driven, type of vehicle, thedistance it travels and its maintenance patterns. A black box is fitted withvehicles that are connected to smartphones, which records the distancetraveled by car, its speed patterns and the type of roads it is driven. Thecondition of the car is used to determine the premium amount.

Pay-As-you-Drive: Insurance premium is decided based on miles the vehicle has beendriven. Mileage is calculated based on the GPS data or Odometer reading. Insurancecompanies also consider speed of average speed of vehicle, and the care with which it isdriven

Pay-How-You-Drive: Driving behavior is observed using sensors, for example usingsensors, for example an accelerometer, which are embedded in the vehicle.

Pay-As-You-Go: Insurance offered for the number of miles driven. Basic theft and firedamaged component are covered at a minimal flat premium, and any extra charges areadded on each journey made, which can be managed through mobile-based application.

Others includes Government initiatives for public safety.

8

Global - Market Trend

On

line

app

Re

gula

tio

ns

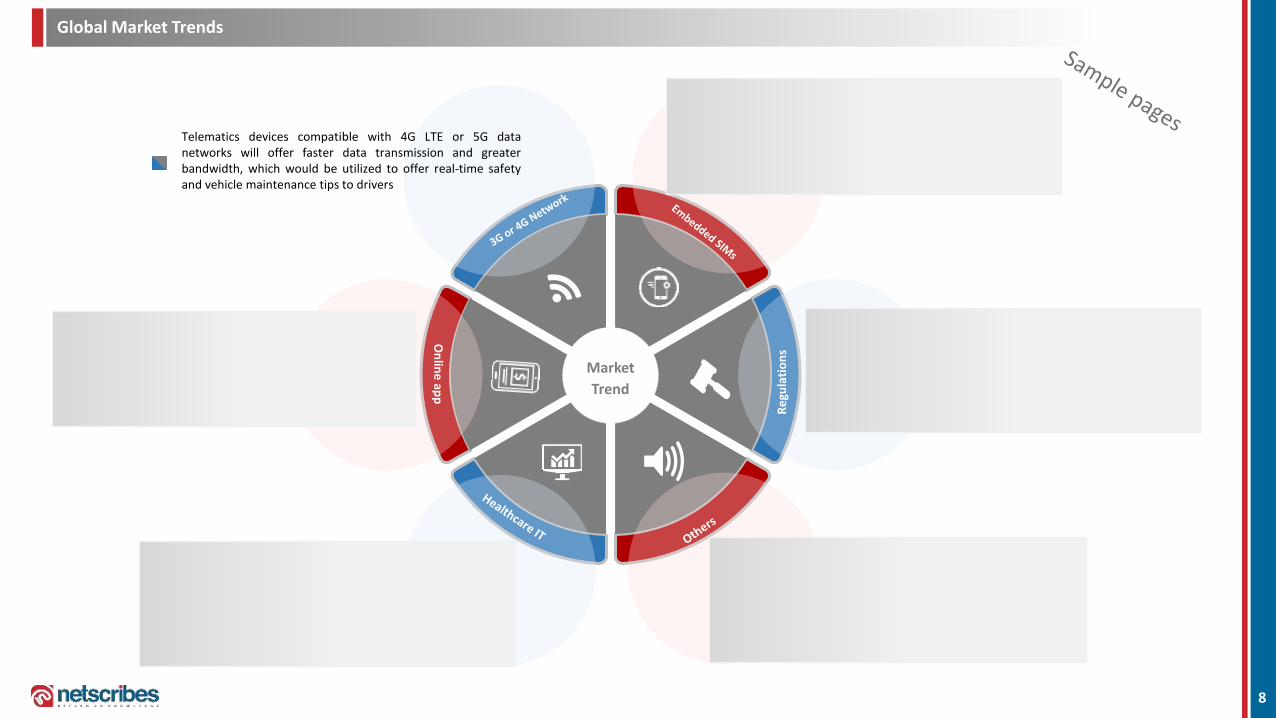

Telematics devices compatible with 4G LTE or 5G datanetworks will offer faster data transmission and greaterbandwidth, which would be utilized to offer real-time safetyand vehicle maintenance tips to drivers

Companies are offering tethering technology based onlineapplications, for instance, Apple is offering CarPlay, andGoogle is providing Android Auto for vehicles

Market

Trend

Vehicles are being manufactured with embedded SIMs to availtelematics based services such as UBI products which can beaccessed through smartphones or pre-installed screens in thevehicles

Government in most developed and developing nations aremaking it mandatory for Fleets to come up with embeddedtelematics devices such as navigation devices or black-box forreal-time position tracking and maintenance

Automotive companies are focusing towards embedded voicerecognition systems for cars, which will take Others offeringsto next level. Smartphone enabled car control system isalready used by individual car owners as well as connectedcars for commercial purposes. Auto theft can be minimizedthrough this

Global Market Trends

Increasing usage of Telematics based healthcare servicesby individual patients apart from only hospitals or healthprofessionals. It is offering various benefits such aselectronic insurance cards, auto-update of software andonline renewal of insurance cards. It is offering not onlymedical assistance to patients but also simultaneouslyhelping them in understanding the process of their medicaltreatment.

9

Global – Market Overview

XX.XXX.X

53.6

2014 2015 2016

XX.XXX.X

XX.X

XX.X

XX.X

XX.X

2017 2018 2019 2020 2021 2022

Global historical market revenue (US$ bn)

Global forecasted market revenue (US$ bn)

CAGR (2014-2016): X.X%

CAGR (2017-2025): X.X%

Geography wise market revenue (US$ bn)

No

rth

Am

eri

ca

Euro

pe

Asi

a P

acif

ic

Lati

n A

me

rica

MEA

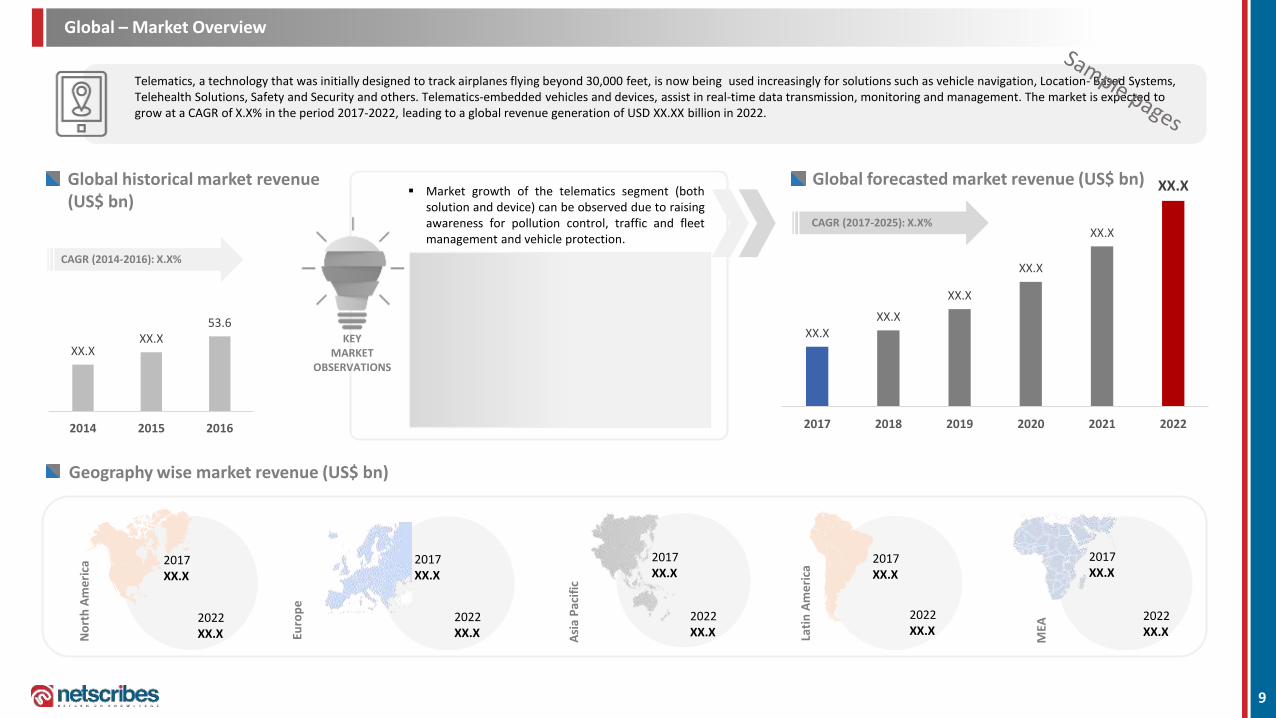

Telematics, a technology that was initially designed to track airplanes flying beyond 30,000 feet, is now being used increasingly for solutions such as vehicle navigation, Location- Based Systems, Telehealth Solutions, Safety and Security and others. Telematics-embedded vehicles and devices, assist in real-time data transmission, monitoring and management. The market is expected to grow at a CAGR of X.X% in the period 2017-2022, leading to a global revenue generation of USD XX.XX billion in 2022.

2017XX.X

2022XX.X

2017XX.X

2022XX.X

2017XX.X

2022XX.X

2017XX.X

2022XX.X

2017XX.X

2022XX.X

Market growth of the telematics segment (bothsolution and device) can be observed due to raisingawareness for pollution control, traffic and fleetmanagement and vehicle protection.

Increasing requirement to track vehicles on a real-time basis and observe drivers’ behavior(monitoring health, temperament while driving,the requirement for Others or knowledge aboutgovernment laid down regulations) is leading togrowing usage of telematics technology.

Plunging cost of cellular-based data charges isshifting focus from device based telematicssolutions to data-enabled smartphonesapplications for cost-effective, easy access.

KEY MARKET

OBSERVATIONS

Chapter 3: Automotive Telematics

11

Automotive Telematics- Fleet Telematics

Purchase Decision Service offered Market Trends Advantages

Global Regional

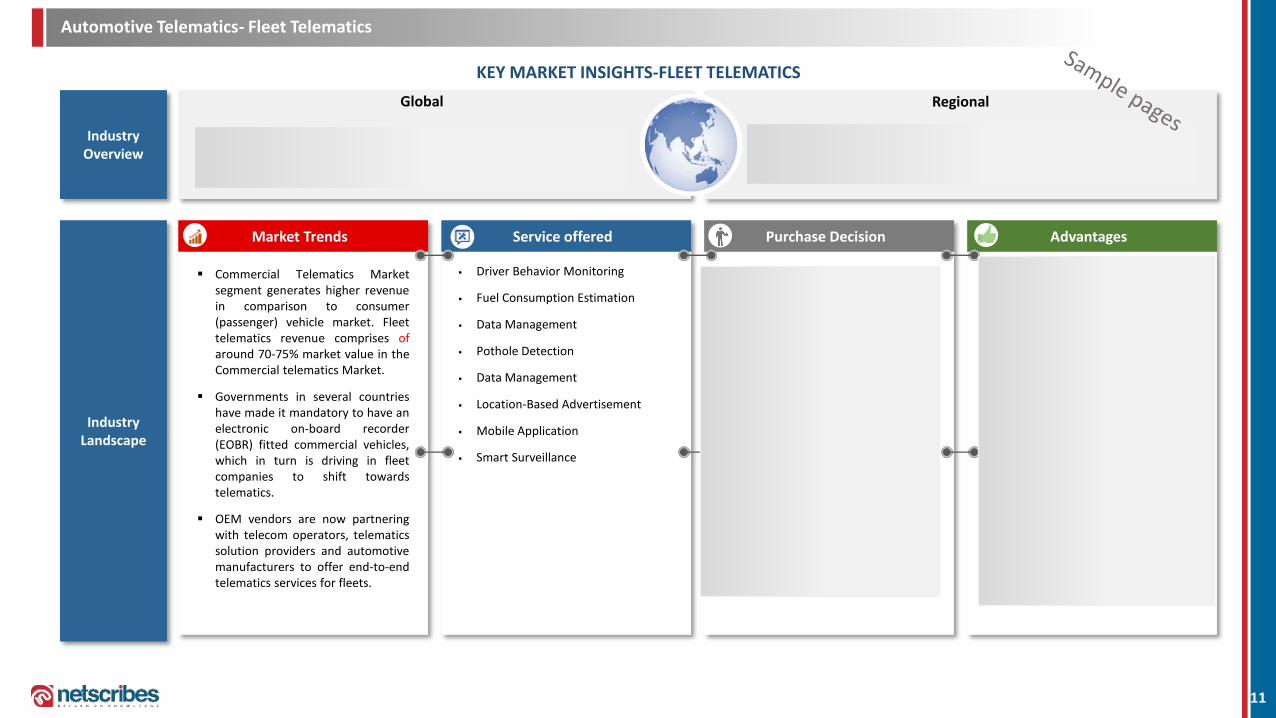

Driver Behavior Monitoring

Fuel Consumption Estimation

Data Management

Pothole Detection

Data Management

Location-Based Advertisement

Mobile Application

Smart Surveillance

The workload of fleet managers havereduced as vehicle monitoring anddriving patterns are taken care of bythe telematics companies on theirbehalf.

Vehicle safety has augmented andfuel consumption has reduced,further decreasing the operatingcost of fleet companies.

Smartphone based application hasmostly eliminated the requirementfor additional expenditure on deviceinstallation and maintenance.

Telematics solutions are beinglaunched keeping in mindgovernment regulations, which assistfleet drivers to avoid transit hassles.

Non-automotive companies areintroducing innovative solutionportfolios, providing fleet companiesvaried options to choose.

KEY MARKET INSIGHTS-FLEET TELEMATICS

Industry Overview

Industry Landscape

Commercial Telematics Marketsegment generates higher revenuein comparison to consumer(passenger) vehicle market. Fleettelematics revenue comprises ofaround 70-75% market value in theCommercial telematics Market.

Governments in several countrieshave made it mandatory to have anelectronic on-board recorder(EOBR) fitted commercial vehicles,which in turn is driving in fleetcompanies to shift towardstelematics.

OEM vendors are now partneringwith telecom operators, telematicssolution providers and automotivemanufacturers to offer end-to-endtelematics services for fleets.

Fleet Telematics segment accounts for ~60% of Automotive Telematics market. It canbe estimated that telematics revenue in fleet management is growing at a CAGR of ~29% (2017-2022), from $17.53 bn. (2017) to $67.53 bn. (2022)

North American and European government has made it mandatory to install vehicletracking systems (EOBR) or e-call in commercial vehicles from 2016. However, inCountries like Brazil, Russia and other countries, in spite of government regulation,fleets companies are reluctant aggressive adoption of fleet telematics

Purchase Decision of buyers (fleetcompanies/ fleet managers) depends oncertain criteria

Fleet Owners in case of smallbusinesses: Preference is towardssolution cost, value-added servicesand effective after sales services.

Fleet Managers in case of largelogistics organization: They prefer tohave a solution from a company whichhas high brand value and visibility.

Government agents: Multiple servicesoffering in a single solution portfolio ishighly preferred by large load haulers,who want visibility at all times

Others: Companies offering highreturn on investment and real-timesales support to fleet

Automotive Telematics- Connected Cars

Scope of the Battle Card Deck

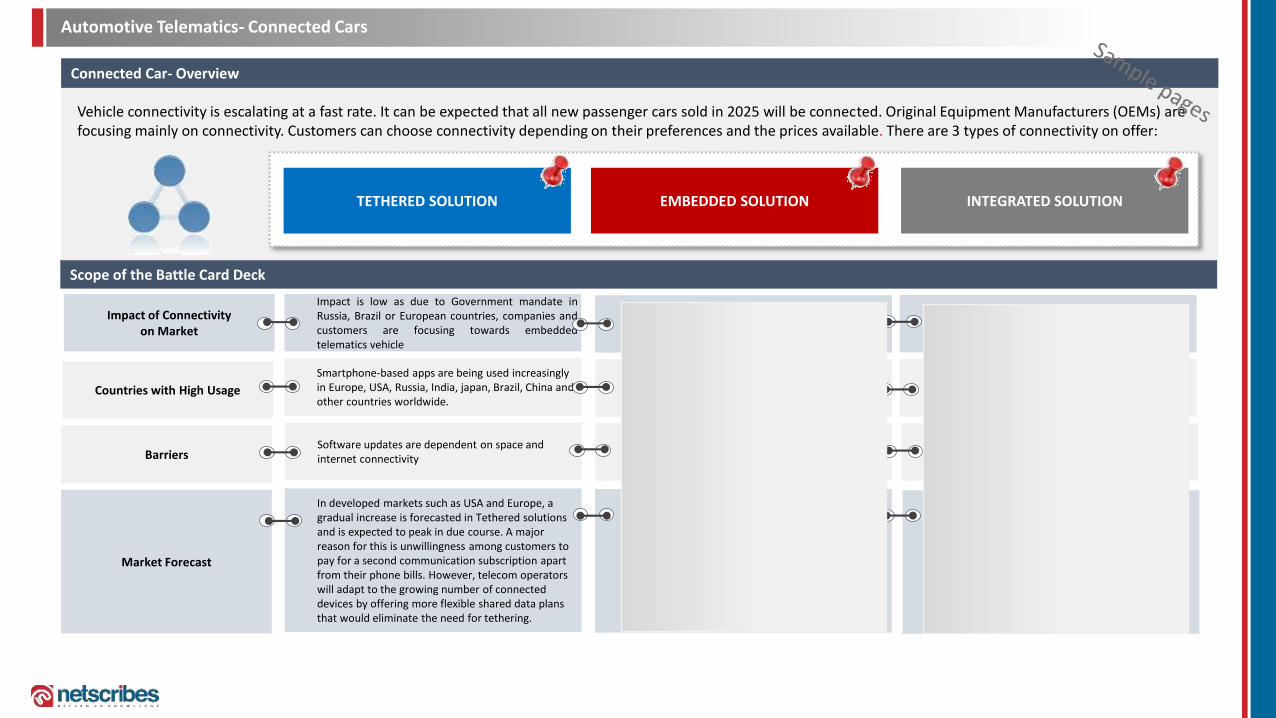

Vehicle connectivity is escalating at a fast rate. It can be expected that all new passenger cars sold in 2025 will be connected. Original Equipment Manufacturers (OEMs) are focusing mainly on connectivity. Customers can choose connectivity depending on their preferences and the prices available. There are 3 types of connectivity on offer:

Connected Car- Overview

Market Forecast

In developed markets such as USA and Europe, a gradual increase is forecasted in Tethered solutions and is expected to peak in due course. A major reason for this is unwillingness among customers to pay for a second communication subscription apart from their phone bills. However, telecom operators will adapt to the growing number of connected devices by offering more flexible shared data plans that would eliminate the need for tethering.

EMBEDDED SOLUTIONTETHERED SOLUTION INTEGRATED SOLUTION

Impact of Connectivity on Market

Impact is low as due to Government mandate inRussia, Brazil or European countries, companies andcustomers are focusing towards embeddedtelematics vehicle

Countries with High Usage

Smartphone-based apps are being used increasingly in Europe, USA, Russia, India, japan, Brazil, China and other countries worldwide.

Impact is highest as it can be expected that by 2025 all the cars would be pre-fitted with telematics devices.

European countries have high embedded telematics usage, followed by Brazil and Russia. India, China and other countries have medium to low usage.

The USA dominates embedded telematics sales, However, it can be expected that within five years the USA will only signify a fraction of the total market share. Countries like Brazil, Russia and Europe has issued regulatory norms to use embedded telematics for every vehicle. It can be expected that China will introduce a similar mandate for telematics, due to increase in car sales.

The impact in this case would be low as apps are no longer restricted to smartphones.

European countries, USA, Japan have high integrated telematics usage, in comparison to China, Brazil, India, Russia and other countries.

Integrated telematics solutions are estimated to proliferate in the next ten years due to increasing usage of smartphones and Apps. It can be expected that within a decade the add-ons of these solutions might reach 100% by 2020, in markets such as USA and China. However, web-based Apps would be developed which can function without smartphone integration, that might lead to decline in integrated telematics after 2020.

BarriersSoftware updates are dependent on space and internet connectivity

Cost of hardware is high,, which in turn is increasing the price of the vehicle.

Frequent-usage services and high-bandwidth is required for services such as infotainment and navigation, that entails additional subscriptions

13

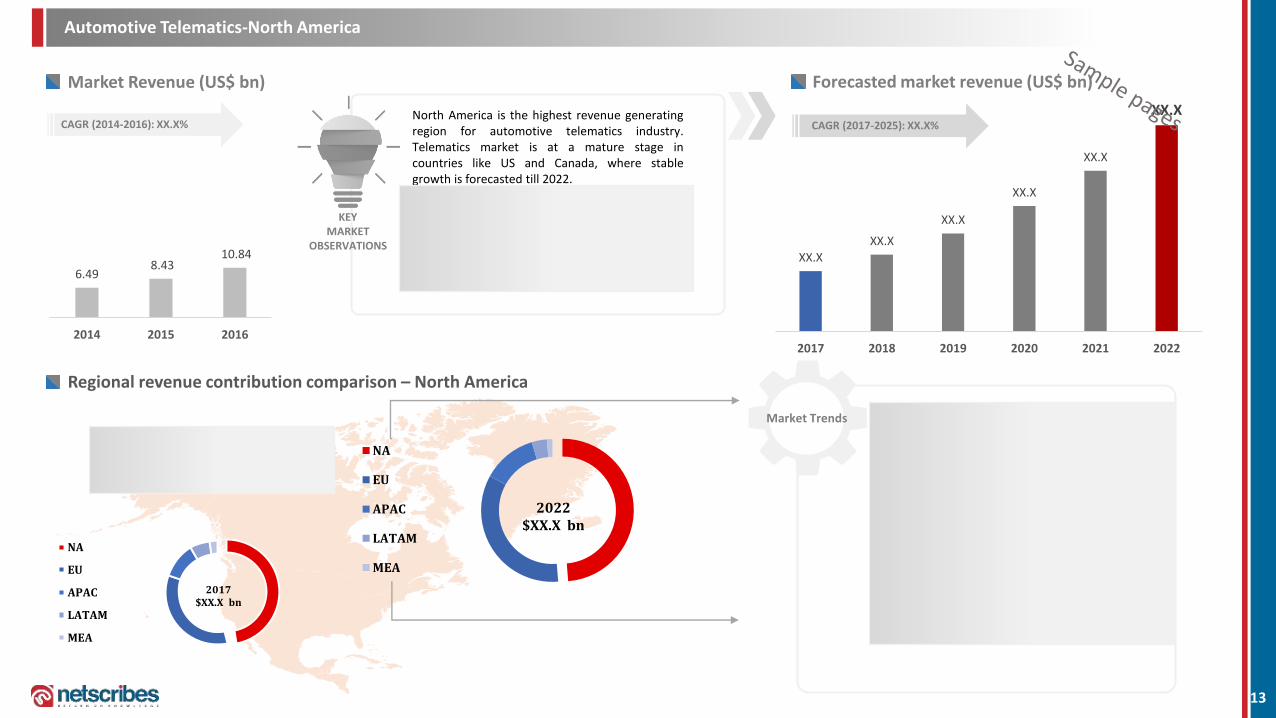

Automotive Telematics-North America

6.498.43

10.84

2014 2015 2016

Market Revenue (US$ bn) Forecasted market revenue (US$ bn)

CAGR (2014-2016): XX.X% CAGR (2017-2025): XX.X%

NA

EU

APAC

LATAM

MEA

2017 $XX.X bn

NA

EU

APAC

LATAM

MEA

2022 $XX.X bn

Regional revenue contribution comparison – North America

North America Automotive telematics market generates 47% market revenue in 2017

North America is the highest revenue generatingregion for automotive telematics industry.Telematics market is at a mature stage incountries like US and Canada, where stablegrowth is forecasted till 2022.

However, innovative solutionand device, increasing security for customers’data and optimum product pricing would increasetelematics penetration in untapped pockets ofthe North American market.

Market Trends Augmenting demand for Big Data analytics isopening up revenue generation stream for bothservice and retail based organizations. Dataanalytics companies and retail players arepartnering with telematics companies to utilizedatabases to design new solutions.

The concept of Driverless car is grabbing attentionof potential customers, which will create massivedemand for telematics technology. Companies likeUber see their future investment in driverless cars,which would give them an edge over theircompetitors, considering aspects like droppingcustomers on time and finding free parking spacein populated cities worldwide.

KEY MARKET

OBSERVATIONS XX.X

XX.X

XX.X

XX.X

XX.X

XX.X

2017 2018 2019 2020 2021 2022

14

North America - Market Overview

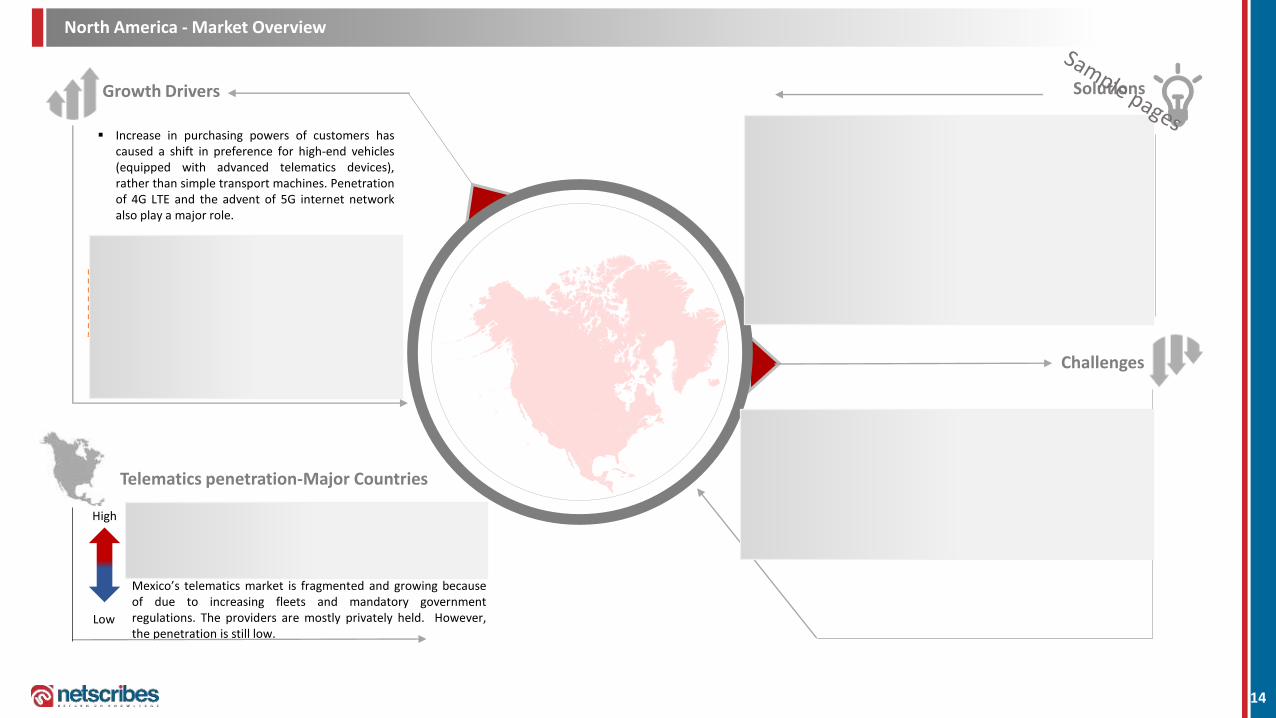

Growth Drivers

Challenges

Increase in purchasing powers of customers hascaused a shift in preference for high-end vehicles(equipped with advanced telematics devices),rather than simple transport machines. Penetrationof 4G LTE and the advent of 5G internet networkalso play a major role.

mber of automobiles in developed nations like theUSA, Canada or populated countries like Mexicohave augmented the need for road assistance andvehicle crash management.

Octo’s First Notice of Loss (FNOL) crash detectionservice has been validating an average of 417,000crashes yearly and offering accident responses withaid from Agero Inc., that manages more than900,000 accident recovery services per year

Vehicles connected on the same network can behacked and controlled, which might result in damageor accidents

Lack of awareness among individual car owners andresistance to additional expenditure for installation ofnew devices in old cars or vehicles

Fleet Solutions

Companies like OCTO North America offers Fleet Lite offers self-installed telematics solution for fleets. Similarly, MiX Telematics NAoffers (SaaS) Software-as-a-Service for fleet management to maintainand evaluate fleet data

Connected CarFord Motor Company with Lyft is leveraging ride-hailing facility(open platform) to offer self-driving cars. They would be utilizing BigData and fleet telematics technology to bring about a change inmobility and transportation for the fleets and commercialconnected car segment

Solutions

USA and Canada have highest telematics penetration in NorthAmerica for mandates like published ELD (electronic loggingdevice) and regulation for oil and gas fleets for lone-workertechnology

Mexico’s telematics market is fragmented and growing becauseof due to increasing fleets and mandatory governmentregulations. The providers are mostly privately held. However,the penetration is still low.

Telematics penetration-Major Countries

High

Low

Chapter 5: Infotainment

15

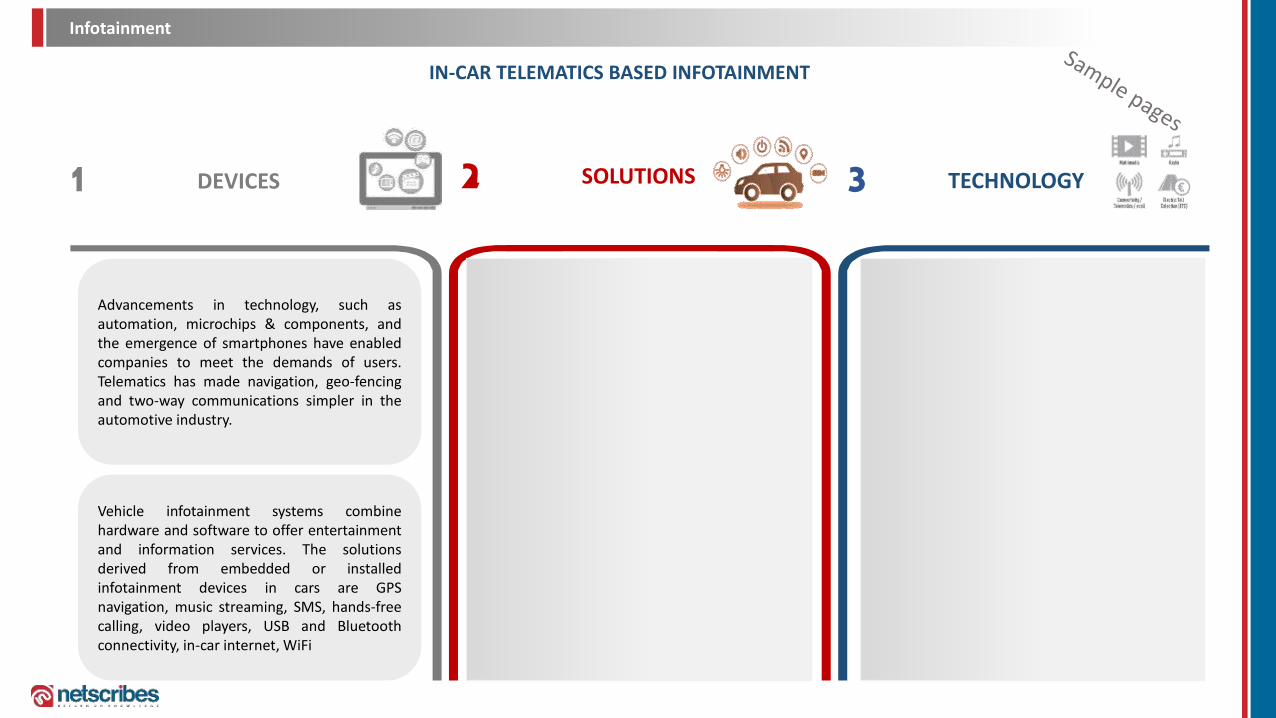

Infotainment

Offers real-time outlook of traffic which includes entire session, capture buffer, a user-selectable

volume that can be reset at any time.

GPS device based navigation solutions offeredturn-by-turn navigation direction through text orspeech. However, now smartphone enabled GPSsoftware is hassle-free and does not requiredevice installation.

In-vehicle Infotainment (IVI) features includethe head-up display, handset integration,infotainment systems for driver assistance,interior personalization and Cloud-basedinfotainment.

Integrating technology also support multiplefeatures or systems. Many automotivecomponent suppliers are involved in integratingthe existing car navigation system with the caraudio and the mobile phone, using a hands freekit or Bluetooth.

Consumers demand PC-like responsiveness,power and human-machine interface fromevery device on the go. Infotainment devicesare hardware devices that offer solutions suchas navigation, audio & visual connectivity.

Vehicle infotainment systems combinehardware and software to offer entertainmentand information services. The solutionsderived from embedded or installedinfotainment devices in cars are GPSnavigation, music streaming, SMS, hands-freecalling, video players, USB and Bluetoothconnectivity, in-car internet, WiFi

Advancements in technology, such asautomation, microchips & components, andthe emergence of smartphones have enabledcompanies to meet the demands of users.Telematics has made navigation, geo-fencingand two-way communications simpler in theautomotive industry.

Virtual space cubes and Sonic curtains areinstalled to eliminate noise and make VRsystems more effective within the car. This assistin watching movies or listing to music withoutinterruption.

Automakers supply fully incorporated suites such as Fiat's Blue&Me and Ford's SYNC, which provide a infotainment interface to most of the

car's electronic functions.

IN-CAR TELEMATICS BASED INFOTAINMENT

1 2 3DEVICES SOLUTIONS TECHNOLOGY

17

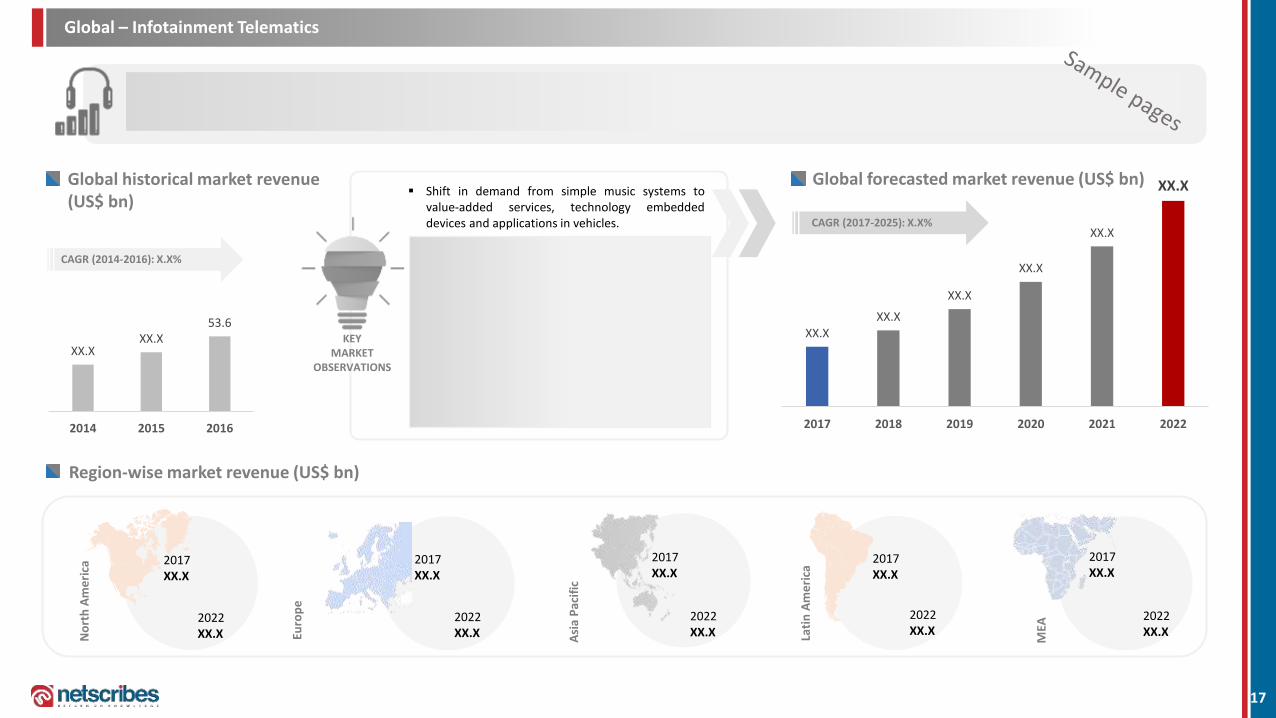

Global – Infotainment Telematics

XX.XXX.X

53.6

2014 2015 2016

XX.XXX.X

XX.X

XX.X

XX.X

XX.X

2017 2018 2019 2020 2021 2022

Global historical market revenue (US$ bn)

Global forecasted market revenue (US$ bn)

CAGR (2014-2016): X.X%

CAGR (2017-2025): X.X%

Region-wise market revenue (US$ bn)

No

rth

Am

eri

ca

Euro

pe

Asi

a P

acif

ic

Lati

n A

me

rica

MEA

Telematics, a technology that was initially designed to track airplanes flying beyond 30,000 feet, is now being increasing used for solutions such as vehicle Navigation, Location Based Systems, Telehealth Solutions, Safety and Security and Others. Telematics embedded vehicle or device, assist in real-time data transmission, monitoring and management. The market is expected to grow at CAGR of X.X% in a span of 2017-2022 leading to a global revenue generation of USD XX.XX billion in 2022.

2017XX.X

2022XX.X

2017XX.X

2022XX.X

2017XX.X

2022XX.X

2017XX.X

2022XX.X

2017XX.X

2022XX.X

Shift in demand from simple music systems tovalue-added services, technology embeddeddevices and applications in vehicles.

Increasing requirement to track vehicles on a real-time basis and observe drivers’ behavior(monitoring health, temperament while driving,the requirement for Others or knowledge aboutgovernment laid down regulations) is leading togrowing usage of telematics technology.

Plunging cost of cellular-based data charges isshifting focus from device based telematicssolutions to data-enabled smartphonesapplications for cost-effective, easy access.

KEY MARKET

OBSERVATIONS

Chapter 8: Stakeholders and Technology Analysis

19

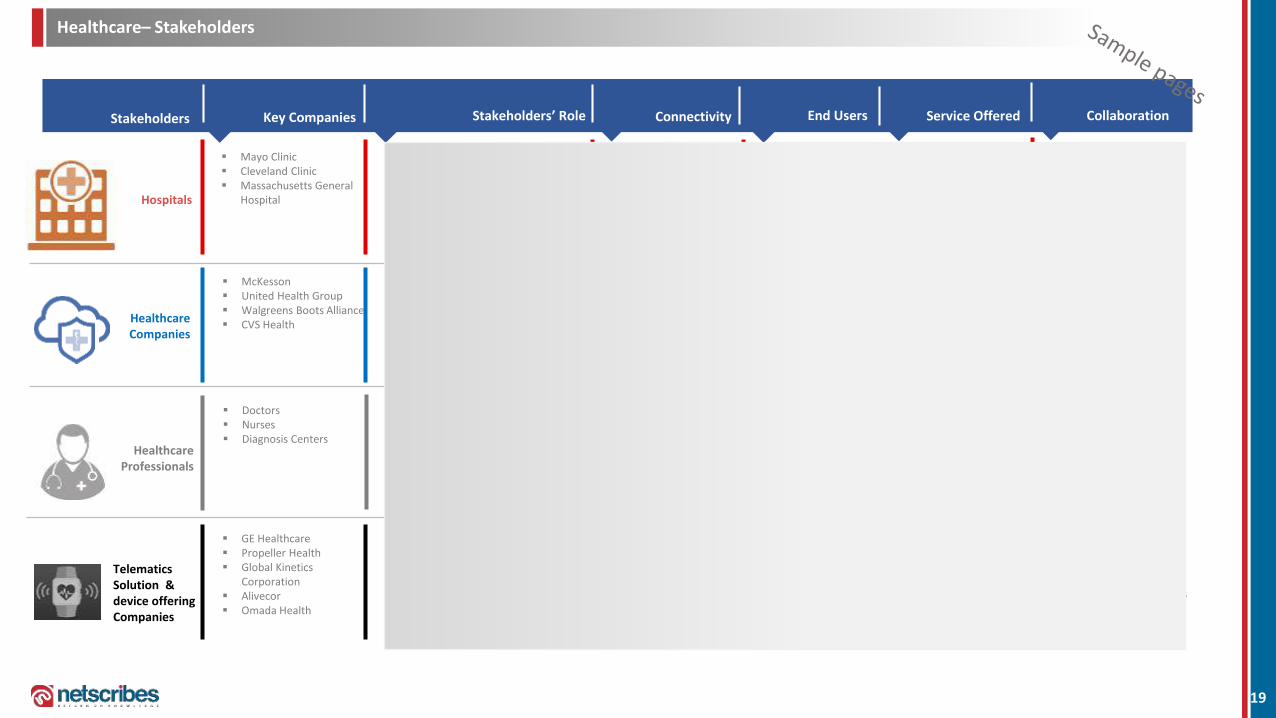

Healthcare– Stakeholders

Hospitals

Healthcare Companies

Mayo Clinic Cleveland Clinic Massachusetts General

Hospital

Stakeholders Key Companies ConnectivityStakeholders’ Role

Hospitals are using telematics formaintaining Electronic Healthrecords, offering e-Alert applicationsfor patients’ and healthcareproviders. Monitoring patients withless human assistance has becomepossible.

Telematics Solution & device offering Companies

Doctors Nurses Diagnosis Centers

Healthcare professionals can not onlymonitor patients without being in thehospital premise but also consult otheronline doctors to treat critical patientsSurgeries can be performed withdoctors; assistance from othercountries

Integrated or Tethered Solutions

Healthcare companies in assistancewith IT infrastructure is developingtelematics enabled applications andmedical devices, which are providinginitial health assistance to patients,monitoring their vital status forfaster treatment and diagnosis

McKesson United Health Group Walgreens Boots Alliance CVS Health

Healthcare Professionals

End Users Collaboration

GE Healthcare Propeller Health Global Kinetics

Corporation Alivecor Omada Health

Telematics solution providers mostly have collaboration with telecom companies and device providers because they offer end-to-end service portfolio to their clients. Telematics companies offer device integrated or embedded healthcare solutions

Tethered solutions

Tethered Solutions

Integrated or Tethered or

Embedded Solutions

Service Offered

Patients, Healthcare professionals (Doctors, nurses, others), Diagnostics centers

HospitalsPharmaceutical companiesDoctorsInsurance Companies

Patients, Hospitals

Government, HospitalsDoctors and other healthcare professionals, Pharmaceutical companies, Patients , Life Insurance Companies

Real-time vehicle data collection and monitoring

Treatment and emergency health assistance

Hassel-free and cost effective treatment

Hospital management software

Real-time patient monitoring solutions

Artificial intelligence based services

Maintenance of electronic medical history

Online health assistance

Real-time monitoring & assistance

Emergency Healthcare Assistance

Electronic medical record

Telemedicine

Telematics solution providers

Healthcare companies Telecom operators IT companies and

networking solution providers

Hospitals Pharmaceutical

companies IT companies for

software framework

Hospitals Telematics solution

providers

Hospitals Healthcare Companies Medical Professionals Telecom Operators Networking Companies

20

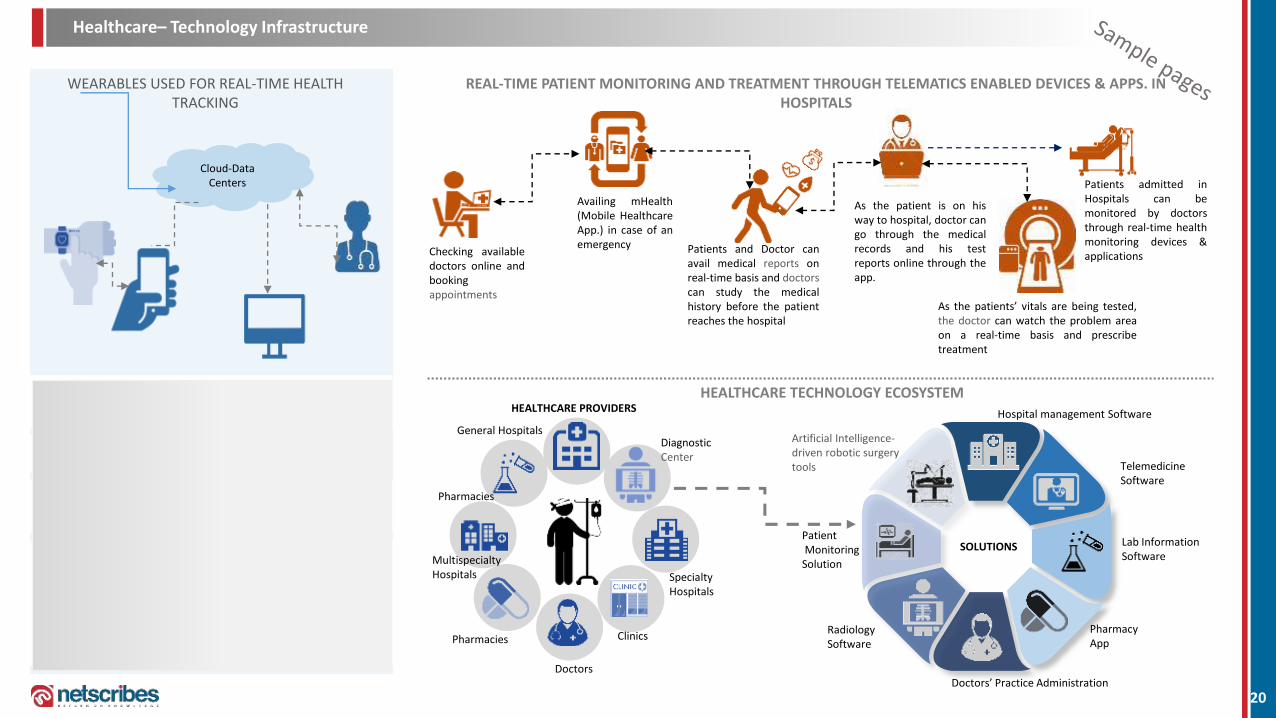

Cloud-Data Centers

Healthcare– Technology Infrastructure

WEARABLES USED FOR REAL-TIME HEALTH TRACKING

Checking availabledoctors online andbookingappointments

Availing mHealth(Mobile HealthcareApp.) in case of anemergency Patients and Doctor can

avail medical reports onreal-time basis and doctorscan study the medicalhistory before the patientreaches the hospital

As the patient is on hisway to hospital, doctor cango through the medicalrecords and his testreports online through theapp.

As the patients’ vitals are being tested,the doctor can watch the problem areaon a real-time basis and prescribetreatment

Patients admitted inHospitals can bemonitored by doctorsthrough real-time healthmonitoring devices &applications

Smartphones are connected to wearable (such as FitBit), which aretracking and monitoring heart rate, footsteps walked, caloriesburnt, etc.

Health professionals in hospitals, who keep updated heath recordof patients, also consider information from wearable to offermedical assistance along with electronic health records

Information get recorded in the smartphone based applicationthrough the smart watch or health trackers

REAL-TIME PATIENT MONITORING AND TREATMENT THROUGH TELEMATICS ENABLED DEVICES & APPS. IN HOSPITALS

HEALTHCARE TECHNOLOGY ECOSYSTEM

SOLUTIONS

Hospital management Software

PharmacyApp

Doctors’ Practice Administration

Lab InformationSoftware

TelemedicineSoftware

RadiologySoftware

PatientMonitoring

Solution

Artificial Intelligence-driven robotic surgery tools

HEALTHCARE PROVIDERS

Clinics

SpecialtyHospitals

MultispecialtyHospitals

General Hospitals

Doctors

Pharmacies

Pharmacies

DiagnosticCenter

Life insurance companies are adopting new methods of datacollection for their customers. Focus is shifting from just medicaltest to real-time health tracking of customers through wearabledevices, which is also giving a vivid idea about the lifestyle (activeor sedentary) of the insure.

However, the aspect is still at a nascent stage ascustomers are not willing to buy wearable separately apart frompremium.

Chapter 9: Company Profiles

21

22

Company Profile

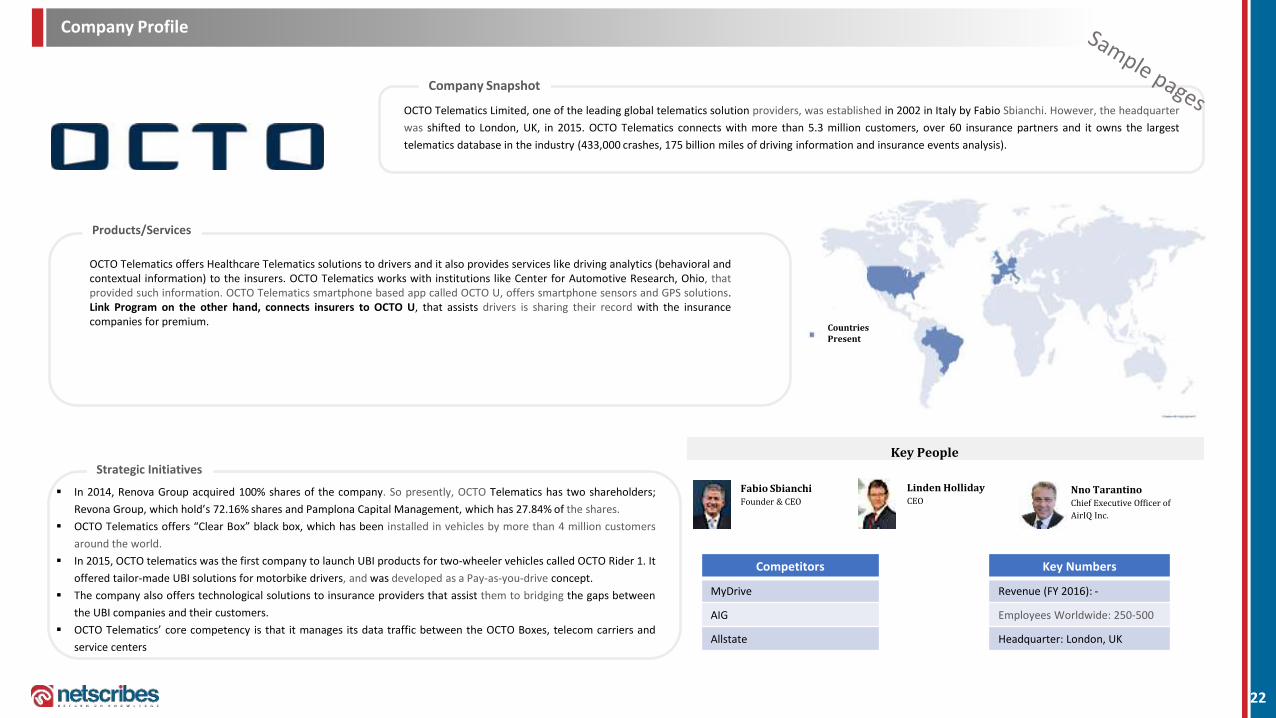

Company Snapshot

OCTO Telematics Limited, one of the leading global telematics solution providers, was established in 2002 in Italy by Fabio Sbianchi. However, the headquarter

was shifted to London, UK, in 2015. OCTO Telematics connects with more than 5.3 million customers, over 60 insurance partners and it owns the largest

telematics database in the industry (433,000 crashes, 175 billion miles of driving information and insurance events analysis).

Products/Services

Countries Present

OCTO Telematics offers Healthcare Telematics solutions to drivers and it also provides services like driving analytics (behavioral andcontextual information) to the insurers. OCTO Telematics works with institutions like Center for Automotive Research, Ohio, thatprovided such information. OCTO Telematics smartphone based app called OCTO U, offers smartphone sensors and GPS solutions.Link Program on the other hand, connects insurers to OCTO U, that assists drivers is sharing their record with the insurancecompanies for premium.

Strategic Initiatives

In 2014, Renova Group acquired 100% shares of the company. So presently, OCTO Telematics has two shareholders;

Revona Group, which hold’s 72.16% shares and Pamplona Capital Management, which has 27.84% of the shares.

OCTO Telematics offers “Clear Box” black box, which has been installed in vehicles by more than 4 million customers

around the world.

In 2015, OCTO telematics was the first company to launch UBI products for two-wheeler vehicles called OCTO Rider 1. It

offered tailor-made UBI solutions for motorbike drivers, and was developed as a Pay-as-you-drive concept.

The company also offers technological solutions to insurance providers that assist them to bridging the gaps between

the UBI companies and their customers.

OCTO Telematics’ core competency is that it manages its data traffic between the OCTO Boxes, telecom carriers and

service centers

Nno TarantinoChief Executive Officer of

AirIQ Inc.

Fabio SbianchiFounder & CEO

Linden HollidayCEO

Key People

Competitors

MyDrive

AIG

Allstate

Key Numbers

Revenue (FY 2016): -

Employees Worldwide: 250-500

Headquarter: London, UK

Chapter 10: Start-up Company Profiles

24

Start-Up Profile

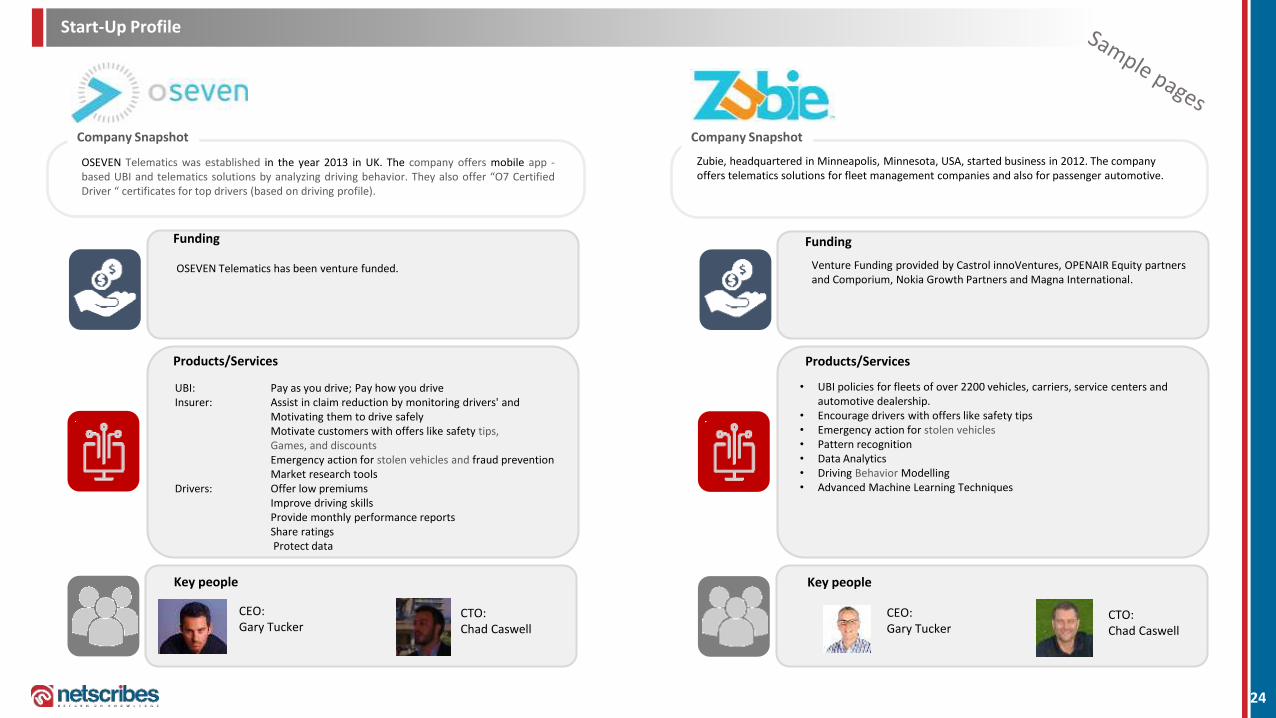

Company Snapshot Company Snapshot

Funding

Products/Services

Key people

OSEVEN Telematics was established in the year 2013 in UK. The company offers mobile app -based UBI and telematics solutions by analyzing driving behavior. They also offer “O7 CertifiedDriver “ certificates for top drivers (based on driving profile).

Zubie, headquartered in Minneapolis, Minnesota, USA, started business in 2012. The company offers telematics solutions for fleet management companies and also for passenger automotive.

UBI: Pay as you drive; Pay how you driveInsurer: Assist in claim reduction by monitoring drivers' and

Motivating them to drive safely Motivate customers with offers like safety tips, Games, and discounts Emergency action for stolen vehicles and fraud prevention Market research tools

Drivers: Offer low premiums Improve driving skills Provide monthly performance reports Share ratings Protect data

OSEVEN Telematics has been venture funded.

CEO: Gary Tucker

CTO: Chad Caswell

Venture Funding provided by Castrol innoVentures, OPENAIR Equity partners and Comporium, Nokia Growth Partners and Magna International.

Funding

• UBI policies for fleets of over 2200 vehicles, carriers, service centers and automotive dealership.

• Encourage drivers with offers like safety tips • Emergency action for stolen vehicles• Pattern recognition• Data Analytics• Driving Behavior Modelling• Advanced Machine Learning Techniques

Products/Services

Key people

CEO: Gary Tucker

CTO: Chad Caswell

Appendix

25

Research Methodology

The study begins with identifying the right research question(s). The question depends on what we are going to achieve by conducting the research or what we wantto convey to the prospective customers through this research. Next, we identify the logical steps to arrive needed to arrive at the answers to the question(s). Theselogical steps form our research objectives. The research objectives provide us a guideline regarding what information we need to conduct analysis. We stronglybelieve that well-defined objectives will lead to clear results about the given market

The next stage of the research is conducted utilizing the secondary sources of information, using a process called desk/secondary research. Netscribes Inc. has aconsiderable volume of information in both quantitative and qualitative forms, across all major industries and its sectors. Also, we conduct an in-depth study of themarket, understanding its key stakeholders, drivers, trends, challenges and global opportunities covering major regions such as North America, Latin America, Europe,Asia Pacific, and Middle East & Africa. The key sources referred to for this research includes (but not limited to) the following: Financial reports published by the key market players Government and other official sources including the National Statistics National and International trade associations Paid databases Other reliable sources

Primary research complements the secondary research as it helps us gain insights from the industries directly by communicating with the senior executives, keyopinion leaders and independent consultants who are experts in their industries or specific industry sectors. Such interviews are conducted across the value chain ofthe market in question. A survey questionnaire is usually prepared for conducting any primary interview or survey. The questionnaire is developed with utmost care tofulfil the key research objectives and also to validate the assumptions about the market. This supplements the information otherwise unaddressed via secondaryresearch. The primary data collection is done by expert interviewers who have specific industry knowledge. Linguists are hired to conduct interviews in therespondent’s native language. Only paid interviews are conducted to incentivize the respondents and ensure that there is no shift of focus. Some of the primaryresearch methods applied at Netscribes include the following: In-depth Interviews Executive Interviews Expert Panels

The qualitative and quantitative findings from the above stages are brought together by specialists to perform a rigorous analysis. The regional market trends, drivers,and opportunities obtained during the analysis is compared with regional economic indicators, sector growth rates, population index, etc. to ensure data consistency.After ensuring the consistency, these historical and present indicators help us to understand how the market will perform in future. Our proprietary forecasting modelfactors in all these indicators to predict the future market accurately.

Appendix

26

Assumptions

The regional split of automobile Telematics Industry has been considered, taking into account the market of fleet telematics andconnected car segment in both commercial and passenger car segment. As per secondary sources, North America being the largest andmost stable market, has the highest market share in terms of revenue generation, followed by Europe and Asia Pacific. However, AsiaPacific has a high CAGR as countries like China, Japan and Korea are well equipped with technological knowledge. Latin America is still asmall market, though Government norms regarding use of connected cars and telematics devices in countries like Brazil are leading theregion in adopting telematics faster than before. MEA is still at the nascent stage and has the smallest market in telematics. Refer to theworking sheet for sources or other calculations.

The regional split in Usage Based Insurance has been considered based on the number of policy holders in different regions. Theconcept of Usage-Based Insurance is still quite new inmost of the regions. The largest market is North America (USA, Canada, Mexico),Europe (Italy, UK, Germany, France, Norway). Asia Pacific, Latin America are slowly understanding the concept and advantages of UBI,while Middle East & Africa has negligible share as far as UBI is concern.

Healthcare telematics is growing at the fastest pace in Asia Pacific countries. However, North America and Europe is a mature market.Due to financial constraints, healthcare institutions in many Latin America and Middle East & Africa countries have still not adoptedhealthcare telematics solutions. The regional market value has been assumed based on these estimates.

Based on the secondary sources, the share of in-car infotainment services have high share in North America, followed by Europe andAsia Pacific, which has been considered to estimate the regional value for media and entertainment.

No unexpected changes in the external factors have been considered that could change the global scenario of the market in the future.

Appendix

27

About Netscribes Inc.

MBA

28%

Graduates

22%

BE

20%

BCA/MCA

12%

CPA/CA/CFA

8%

Others

10%

Well-qualified Team

Netscribes provides end-to-end research-driven solutions that help clients meet their growth objectives by collaboratively transforming information into business advantage.

In-house Research Data VisualizationGlobal CoveragePanel Expertise Premium Databases

Specialized panel of senior executives, analysts and

practitioners

Extensive experience of working on various premium databases

Ability to conduct research across the globe in multiple

languages

Ability to present complex data insights in crisp, easy-

to-understand visuals

Global market intelligence and content

management firm –services across the

research and information value chain

Venture-funded by US and Singapore private

equity firms

725+ member delivery team across Mumbai,

Kolkata and Gurgaon, and sales presence in USA, UK,

Singapore, Dubai and Israel

Revenue composition:

USA: 45%Europe/MENA: 45%

APAC: 10%

ISO 9001:2008 certified by DNV GL

since 2014

Owns:– Inrea Research– OnSense– Research on Global

Markets

We utilize an in-house resource model to provide our clients

with actionable insights

Thank You for Your Attention

28

Global Telematics Market report is part of Netscribes’ ICT Industry Series.

For any queries or customized research requirements, contact us at:

Phone: +91 (33) 4027 6251 | E-Mail: [email protected]

Research on Global Markets is a leading source of research reports on worldwide markets. Sourced fromleading publishers, our reports cover a broad range of industries across international markets to helpcustomers make informed business decisions. With Research on Global Markets, you can be assured ofrelevant, comprehensive market research reports and analysis, as you need it.

Disclaimer: This report is published for general information only. Although high standards have been used in the preparation, “Netscribes” is not responsible for any loss or damage arising from use of this document. This document is the sole property of Netscribes and prior permission is required for guidelines on reproduction.

Related Documents