Global Indirect Taxes - May 2013 - Issue 03 1 May 2013 Issue 03 Content Introduction to the Nexia Global Indirect Taxes newsletter GST considerations for overseas entities making taxable supplies in Singapore Criminal prosecution still possible in Germany for VAT tax evasion in other member states of the EU Indian Goods and Service Tax regime - reality or distant dream Coming to America - A guide to navigating the high seas of State and local sales taxes Non-residents and electronic commerce in Canada 1 2 3 4 6 7 Tax Special Interest Groups Global Indirect Taxes Introduction to the Nexia Global Indirect Taxes newsletter Welcome to the latest edition of the Nexia Global Indirect Taxes newsletter. Since the last edition writing we have seen further evidence of the “coming together” of direct and indirect taxes on a global level. As previously mentioned in articles, the global reduction in corporate tax rates means that governments have to look elsewhere to gather taxes to support their economies and this has led to a widening of the indirect tax base and an increase in VAT/GST rates around the world. In February the OECD published a discussion paper for comment on International VAT/ GST Guidelines. The document addresses a number of points, but mainly focuses on “place of supply issues”. We see this very much as a precursor for the gradual integration of indirect taxes into the OECD model tax treaty over a period of time. This will require detailed discussion with interested parties in order to rationalise the different direct and indirect tax approaches currently adopted to issues such as permanent establishment, taxing rights, branch versus single legal entity etc. If the taxes are to “come together” it would be nonsense to work with differing definitions for these important tax concepts. This is likely to be a long debate! This newsletter contains articles from Singapore aimed at non-resident business intending to trade in Singapore. An article from Germany highlighting the strict approach their tax authorities take to failures by businesses to comply, not just in Germany but all around the EU. An article outlining the delays in India to implementing GST and a reminder from America that they also have their State and local sales taxes which should not be forgotten by inbound businesses and are an equally important part of tax planning. Finally, an article from Cliff Beneroff on Canadian electronic commerce. I would also like to welcome Ellen McCabe from CliftonLarsonAllen who has joined the Nexia Global Indirect taxes committee. John Voyez, VAT Partner, Smith & Williamson LLP, UK

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Global Indirect Taxes - May 2013 - Issue 03 1

May 2013Issue 03

ContentIntroduction to the Nexia Global Indirect Taxes newsletter

GST considerations for overseas entities making taxable supplies in Singapore

Criminal prosecution still possible in Germany for VAT tax evasion in other member states of the EU

Indian Goods and Service Tax regime - reality or distant dream

Coming to America - A guide to navigating the high seas of State and local sales taxes

Non-residents and electronic commerce in Canada

1

2

3

4

6

7

Tax Special Interest Groups

Global Indirect Taxes

Introduction to the Nexia Global Indirect Taxes newsletterWelcome to the latest edition of the Nexia Global Indirect Taxes newsletter.

Since the last edition writing we have seen further evidence of the “coming together” of direct and indirect taxes on a global level. As previously mentioned in articles, the global reduction in corporate tax rates means that governments have to look elsewhere to gather taxes to support their economies and this has led to a widening of the indirect tax base and an increase in VAT/GST rates around the world.

In February the OECD published a discussion paper for comment on International VAT/GST Guidelines. The document addresses a number of points, but mainly focuses on “place of supply issues”. We see this very much as a precursor for the gradual integration of indirect taxes into the OECD model tax treaty over a period of time. This will require detailed discussion with interested parties in order to rationalise the different direct and indirect tax approaches currently adopted to issues such as permanent establishment, taxing rights, branch versus single legal entity etc. If the taxes are to “come together” it would be nonsense to work with differing definitions for these important tax concepts. This is likely to be a long debate!

This newsletter contains articles from Singapore aimed at non-resident business intending to trade in Singapore. An article from Germany highlighting the strict approach their tax authorities take to failures by businesses to comply, not just in Germany but all around the EU. An article outlining the delays in India to implementing GST and a reminder from America that they also have their State and local sales taxes which should not be forgotten by inbound businesses and are an equally important part of tax planning. Finally, an article from Cliff Beneroff on Canadian electronic commerce. I would also like to welcome Ellen McCabe from CliftonLarsonAllen who has joined the Nexia Global Indirect taxes committee.

John Voyez, VAT Partner, Smith & Williamson LLP, UK

2 Global Indirect Taxes - May 2013 - Issue 03

GST considerations for overseas entities making taxable supplies in SingaporeSingapore has for some years been recognised as an international commercial hub. Political stability, a business-friendly environment, low taxation and a robust legal framework contribute to making it the destination of choice for many foreign multinationals seeking to trade or invest in this region.

While Singapore prides itself on a relatively simple and transparent tax regime in comparison with many other locations, overseas businesses and multinationals seeking to exploit commercial opportunities here should still be mindful of potential pitfalls when considering the Goods and Services Tax (GST) implications of their business and investment decisions. This is especially true for overseas traders seeking to sell their products or services in Singapore, either to final customers or within the context of a larger business value chain.

GST is a broad-based consumption tax imposed on the supply of goods and services in Singapore and on the importation of goods into Singapore. Any business (including an overseas entity) that has made taxable supplies in excess of SGD1 million in Singapore for the past four quarters or expects to make taxable supplies in excess of SGD1m in Singapore in the next 12 months is required to be registered for GST purposes and charge GST at the appropriate rate. So what constitutes a taxable supply? There are essentially two main categories of taxable supplies for GST purposes – standard-rated items (which cover most domestic supplies of goods and services) attract the rate of 7% and zero-rated items (covering exports and international services) are subject to a 0% rate. Exempt

items would comprise financial services and residential property transactions.

An overseas trader, for instance a car parts manufacturer in Thailand, selling products to a local Singaporean buyer, could very easily find itself making taxable supplies in Singapore and having to account for GST on the supply of the parts if the value crosses the SGD1 million threshold. This is especially true if ownership of the car parts transfers to the Singaporean buyer subsequent to the importation of the goods into Singapore. Typically, the parts would first need to be cleared through customs at which point it would be subject to GST on importation. Being GST registered would enable the overseas trader to recover the GST incurred on importation as it would be able to charge GST on the onward sale of the car parts to the local buyer. Indeed, GST registration would be compulsory at this point if the SGD1 million threshold is broken given that the sale would constitute a local supply. Without the ability to charge GST on the subsequent sale, there would be no means of recovering the GST paid on importation resulting in it being an additional business cost to the overseas trader.

An alternative scenario would be where the overseas trader appoints what is known as a Section 33(2) agent to do the importation of the parts on its behalf. The GST registered agent would in effect act as the principal (ie the overseas trader) for the importation of, as well as the onward supply of the parts, reporting the input and output GST on its own returns. In such a case, the overseas trader need not register itself for GST purposes and is largely unaffected by the cash flow implications otherwise faced.

An overseas supplier of services currently does not face the same predicament encountered by an overseas trader of goods as in the above case. This is mainly due to the fact that the place of supply of services is determined by where the supplier belongs (unlike in the case of goods where it is dependent on the where the goods are located at the time of the supply) and the fact that the importation of services is to date not subject to GST. Overseas suppliers providing services in Singapore are also currently not subject to any reverse charge mechanisms to account for GST.

Global Indirect Taxes - May 2013 - Issue 03 3

It is worthwhile noting that a failure to comply with the GST registration requirements can entail hefty penalties. Any person who fails to register for GST, potentially faces a fine of up to SGD10,000 as well as a penalty equal to 10% of the tax due for each year from the date on which the person was required to apply for registration. In the case of a continuing offence, the person faces a further fine of SGD50 for each day the offence continues after conviction. These provisions apply equally to domestic as well as overseas traders.

With the above in mind, the blanket of comfort one derives from being an overseas trader often masks the less obvious risks of either crossing the registration threshold when making taxable supplies in Singapore or being unwittingly ensnared in the GST net with no possibility of relief. This is another reason why overseas businesses and traders who trade significantly with Singapore should give serious thought to the extent that they should be formalising their presence within the country.

[Editor’s note – the GST system in Singapore closely mirrors many of the rules in the EU, particularly regarding registration rules and the requirement to register for supplies of goods, although the EU does apply a “reverse charge” obligation on recipients of services.]

Contributed byLam Fong Kiew, Nexia TS, [email protected]

Criminal prosecution still possible in Germany for VAT tax evasion in other member states of the EUNormally, the German state prosecutors will only pursue tax evasion in Germany. The nationality or state of residence of the (alleged) criminal is of no consequence. However, since the end of 2010, German prosecutors have been permitted to pursue a criminal case beyond the borders of Germany, even for VAT levied by another EU member state.

If, regardless of nationality or state of residence, a taxpayer fails to register in another member state of the EU as required, or cross-border supplies, consignment stores or real estate sales are not properly declared in another member state of the EU, the German prosecutor can prosecute in addition to any case brought by the respective member state. To what extent cases may be brought by both the German authorities and the authorities of the respective member state have not been conclusively clarified. However, the fact that the other EU member states levy the taxes and possibly a fine, does not prevent the German authorities levying their own punishment, provided that primacy is given to redressing the cash benefit from the failure to pay the tax and the focus is not on the punishment. Moreover, it is not ruled out that the same conduct by a person can be prosecuted under the national law of another member state and also under German national law. This too does not constitute a breach of the ne bis in idem principle. Together with our respective national Nexia partners, we are publishing a guideline on the penalties levied by a selection of EU member states on the Nexia webpage.

4 Global Indirect Taxes - May 2013 - Issue 03

Indian Goods and Service Tax regime – Reality or distant dreamThe concept of Goods and Services Tax, commonly known as GST, was first mooted in the budget 2006 – 2007 whereby it was to be introduced from 1 April 2010. GST was intended to subsume most of the current indirect taxes (like excise duty, service tax, entry tax etc.) that are imposed on all goods and services. The motive for the introduction of GST is to simplify India’s tax structure, broaden the tax base and to create a single unified market in the interest of the economy as well as corporate business.

However, the GST rollout is already delayed by 3 years from its original deadline. The first discussion paper issued in November 2009 provided the design and roadmap for GST, with a dual structure for both Central (CGST) and State Government (SGST), both having the right to levy tax. The tax structure is multi-tiered ie taxes at federal level are governed by Central Government, while at State level they are governed by State Government. A two-rate structure was proposed for goods – a lower rate for necessary items of basic importance, a standard rate for goods in general and a single rate for services for both CGST and SGST was proposed by the First Discussion Paper.

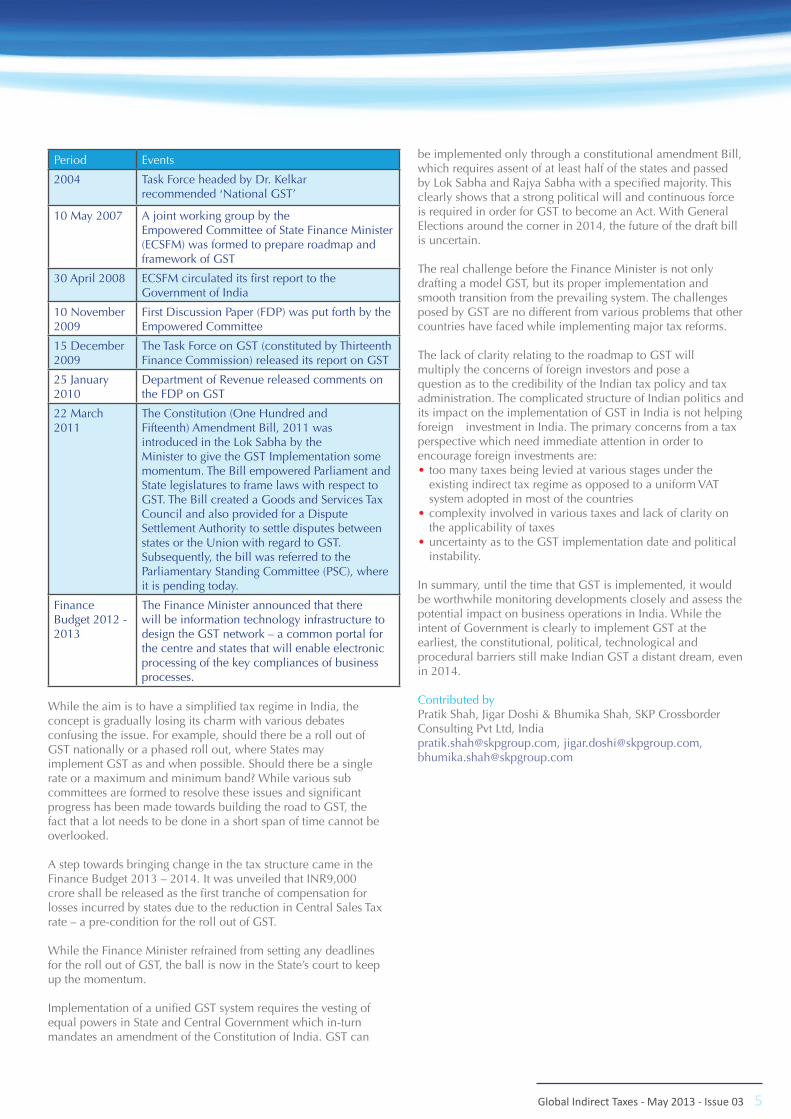

The following page provides a timetable for the events that took place, leading up to the implementation of GST and provides an insight on developments.

This illustrates a dilemma: due to the vulnerability of VAT law to abuse, EU law is becoming tighter and tighter. For companies, particularly those in the production sector, most of which trade throughout Europe, there is a need to address the VAT requirements of each respective EU member state to avoid tax and criminal proceedings that could arise upon failure. There are still many differences in the way the law is implemented at national level despite the uniform VAT legislation at EU level.

For this reason, businesses should consider setting up a functioning EU-wide tax compliance system. Nexia firms work together to clarify all the relevant VAT issues throughout the EU to allow businesses to steer their way around any unseen traps under VAT law and avoid the ensuing criminal proceedings.

[Editor’s note – German VAT legislation and the legislation of a number of EU member states, treat certain failures by a business as a criminal matter and therefore considerable caution should be exercised. A number of other member states eg UK treat most general failures as a civil matter.]

Contributed byAlexander Michelutti, Ebner Stolz Mönning Bachem, [email protected]

Global Indirect Taxes - May 2013 - Issue 03 5

Period Events

2004 Task Force headed by Dr. Kelkar recommended ‘National GST’

10 May 2007 A joint working group by the Empowered Committee of State Finance Minister (ECSFM) was formed to prepare roadmap and framework of GST

30 April 2008 ECSFM circulated its first report to the Government of India

10 November 2009

First Discussion Paper (FDP) was put forth by the Empowered Committee

15 December 2009

The Task Force on GST (constituted by Thirteenth Finance Commission) released its report on GST

25 January 2010

Department of Revenue released comments on the FDP on GST

22 March 2011

The Constitution (One Hundred and Fifteenth) Amendment Bill, 2011 was introduced in the Lok Sabha by the Minister to give the GST Implementation some momentum. The Bill empowered Parliament and State legislatures to frame laws with respect to GST. The Bill created a Goods and Services Tax Council and also provided for a Dispute Settlement Authority to settle disputes between states or the Union with regard to GST. Subsequently, the bill was referred to the Parliamentary Standing Committee (PSC), where it is pending today.

Finance Budget 2012 - 2013

The Finance Minister announced that there will be information technology infrastructure to design the GST network – a common portal for the centre and states that will enable electronic processing of the key compliances of business processes.

While the aim is to have a simplified tax regime in India, the concept is gradually losing its charm with various debates confusing the issue. For example, should there be a roll out of GST nationally or a phased roll out, where States may implement GST as and when possible. Should there be a single rate or a maximum and minimum band? While various sub committees are formed to resolve these issues and significant progress has been made towards building the road to GST, the fact that a lot needs to be done in a short span of time cannot be overlooked.

A step towards bringing change in the tax structure came in the Finance Budget 2013 – 2014. It was unveiled that INR9,000 crore shall be released as the first tranche of compensation for losses incurred by states due to the reduction in Central Sales Tax rate – a pre-condition for the roll out of GST.

While the Finance Minister refrained from setting any deadlines for the roll out of GST, the ball is now in the State’s court to keep up the momentum.

Implementation of a unified GST system requires the vesting of equal powers in State and Central Government which in-turn mandates an amendment of the Constitution of India. GST can

be implemented only through a constitutional amendment Bill, which requires assent of at least half of the states and passed by Lok Sabha and Rajya Sabha with a specified majority. This clearly shows that a strong political will and continuous force is required in order for GST to become an Act. With General Elections around the corner in 2014, the future of the draft bill is uncertain.

The real challenge before the Finance Minister is not only drafting a model GST, but its proper implementation and smooth transition from the prevailing system. The challenges posed by GST are no different from various problems that other countries have faced while implementing major tax reforms.

The lack of clarity relating to the roadmap to GST will multiply the concerns of foreign investors and pose a question as to the credibility of the Indian tax policy and tax administration. The complicated structure of Indian politics and its impact on the implementation of GST in India is not helping foreign investment in India. The primary concerns from a tax perspective which need immediate attention in order to encourage foreign investments are:• too many taxes being levied at various stages under the

existing indirect tax regime as opposed to a uniform VAT system adopted in most of the countries

• complexity involved in various taxes and lack of clarity on the applicability of taxes

• uncertainty as to the GST implementation date and political instability.

In summary, until the time that GST is implemented, it would be worthwhile monitoring developments closely and assess the potential impact on business operations in India. While the intent of Government is clearly to implement GST at the earliest, the constitutional, political, technological and procedural barriers still make Indian GST a distant dream, even in 2014.

Contributed by Pratik Shah, Jigar Doshi & Bhumika Shah, SKP Crossborder Consulting Pvt Ltd, [email protected], [email protected], [email protected]

6 Global Indirect Taxes - May 2013 - Issue 03

which a company has sales tax links may result in hefty taxes, interest and penalty assessments. Sales taxes are not easily avoided, survive bankruptcy and may result in personal officer liability. Since sales taxes may substantially alter the desired course of a company, its course must be carefully planned and plotted before sailing into U.S. ports.

Some courses are safer than others and quality solutions exist. Compliance solutions vary depending on whether a company desires minimal assistance or turn-key solutions. Many companies outsource their sales tax compliance functions such as registration, monitoring rate changes, preparing and filing returns, handling the funds required to satisfy tax liabilities and managing tax assessments as they arise. Sales tax return compliance services are usually priced on a per return basis, set fee or hourly basis. An advantage of outsourcing sales tax return compliance is the ability to avoid costly and lengthy license agreements for individual software packages.

If a full service solution is not desired, a company may license compliance software itself from a software provider. Once software is integrated into a company’s own reporting system, which can in some cases be difficult to accomplish, it can be used to help a company fulfill filing requirements. Unfortunately, no software package alone will provide all the tools needed to steer a company clear of sales tax icebergs. Just like choosing the most reliable vessel, a company should choose its navigational system and resources carefully to improve its chances of survival when, like a 40 foot wave, a state or local taxing jurisdiction comes crashing down.

Contributed byTom Chrzanowski, CliftonLarsonAllen, [email protected]

Coming to America – A guide to navigating the high seas of State and local sales taxesIn the 1980s, “Coming to America” conjured up images of Neil Diamond belting out lyrics to his famous song. Today, it creates a feeling of overwhelming dread of how to navigate the stormy seas of state and local sales taxes. Conducting business in America without navigating state and local sales tax is like setting sail in the Pacific Ocean in a rowing boat. You are unlikely to survive and if you do, you will wish you hadn’t.

For companies expanding in America, sales tax compliance is too dangerous and costly to ignore. Sales tax compliance encompasses making correct tax decisions and filing proper sales tax returns in more than 7,500 taxing jurisdictions. No two local taxing jurisdictions are the same when it comes to rules and regulations concerning registration, taxation, exemptions and rates. Although local areas set and maintain their own tax rates, most follow state rules when determining taxation. The United States does not have VAT, GST or even a federal sales tax. Instead, each state and “locality” imposes its own sales tax as it sees fit. Before sailing unchartered waters, you need to understand the rules and regulations established by each taxing authority.

Failure to properly register and file in states and localities in

Global Indirect Taxes - May 2013 - Issue 03 7

Non-residents and electronic commerce in CanadaIt is generally accepted that a resident of Canada who carries on their business and makes taxable supplies in the course of a commercial activity, is required to register for and to collect, Canada’s Goods and Services Tax (GST) or Harmonised Sales Tax (HST). Subject to the small-supplier threshold, a non-resident person who carries on business in Canada and who makes taxable supplies in the course of a commercial activity, is likewise required to register and is subject to all of the obligations of a registrant. The parameters of non-registrant VAT registration in Canada were the subject of an article published in the October 2012 edition of Nexia International’s Global Indirect Taxes newsletter.

While the notion of “carrying on business in Canada” is often unavoidably subjective, case law and administrative policy concentrate on the long-held traditional view that “carrying on business” in a place requires some physical presence. In an era of virtual online businesses and virtual marketplaces, many non-resident businesses that nonetheless leave an economic footprint in the Canadian market are not required to become GST/HST registrants and therefore do not collect Canadian value-added taxes.

The GST/HST legislation easily accommodates supplies made by unregistered non-resident businesses. A supply of personal property or a service made by a non-resident person that might otherwise be considered to have been made in Canada is deemed to be made outside Canada unless the supply is made by a person who has registered for GST/HST purposes or unless it is made in the course of a business carried out in Canada by that person.

There is no reverse charge obligation imposed on the Canadian customer of an unregistered non-resident supplier, if the customer would otherwise have been entitled to claim a full input tax credit in respect of the supply. This fact may therefore create a slight bias towards non-resident vendors, if only to improve one’s cash flow. On the other hand, other persons who are not entitled to full input tax credits, including consumers, have an obligation to “self-assess” the tax they would have had to pay to a registered supplier if the supply were made in Canada.

There is likely little concern for tax leakage as it concerns the online sale of merchandise for delivery in Canada. Goods that will physically enter Canada must do so at a border entry point, at which time and place the GST or HST will be collected by the Canada Border Services Agency. The GST at the rate of 5% is collected on commercial imports regardless of the province to which the goods are being shipped, whereas the GST or HST will be collected at the rate in effect for that province for casual importations. There is, however, no border to monitor the taxation of inbound services or intangible property. Such supplies may include the electronic ordering and downloading

of digitised products, software maintenance contracts, website hosting and data warehousing, internet access, subscriptions to databases and websites and information provided by electronic means.

The Canada Revenue Agency clearly distinguishes the use by a non-resident of a third-party server located in Canada to host its data or applications, from that of the ownership by that non-resident of a server that is physically located in Canada. In the latter case, the server itself may be regarded as tangible personal property located in Canada through which the non-resident carries out its business, which could attribute to the non-resident having a permanent establishment in Canada.

Whereas the potential for tax leakage exists at the international level, there is often the same concern expressed at the inter-provincial level. For example, Quebec has its own value-added tax system that applies alongside the GST. However, an online vendor in Alberta that does not carry out business in Quebec would not be required to register for purposes of the Quebec Sales Tax (QST) and thus, could not be compelled to collect the QST. Likewise, some provinces in western Canada have a separate retail sales tax system that faces similar challenges. In this regard, for the purposes of the recently re-enacted British Columbia provincial sales tax, a rule affecting out-of-province vendors stipulates that such vendors are required to register if they solicit orders for the sale of taxable goods through advertising in the province or through a website that targets consumers in the province.

Supplies made to non-residentsWhen a non-resident is the recipient of a taxable supply made by GST/HST-registered Canadian suppliers through electronic means, such supplies may often be zero-rated.

For example, a supply of intellectual property made to an unregistered non-resident person is zero-rated. Thus, a supply of a software license would be zero-rated under this rule.

A supply of intangible personal property made to an unregistered non-resident person is also zero-rated, subject to restrictions. Specifically, the supply is not zero-rated if it is made to an individual who is not outside Canada at the time the supply is made. An online supplier through a website must therefore not only reasonably determine whether a customer is factually a non-resident of Canada but also whether the customer is physically present in Canada at a particular time. The zero-rating of supplies of intangible property is further restricted in scope to exclude such supplies when they relate to real property located in Canada, tangible personal property ordinarily situated in Canada or a service the supply of which is not a zero-rated supply.

Nevertheless, a prudent supplier must first determine whether a supply is actually a supply of intangible property and not a supply of other goods or services, such as a telecommunication service, an advertising service or a professional service, among others, each of which may be subject to a different set of rules.

Contributed by Clifford Benderoff, Nexia Friedman LLP, [email protected]

This update was edited by John Voyez, Smith & Williamson LLP, UK. If you have any comments about the articles contained in this publication please contact:

John VoyezSmith & Williamson LLP, UKEmail: [email protected]

Mike Adams, Tax DirectorNexia International SecretariatEmail: [email protected]

Nexia International4 Harley StreetLondon, WIG 9PB, UKTelephone: +44 (0) 20 7436 1114

www.nexia.com

Nexia International does not accept any responsibility for the commission of any act, or omission to act by, or the liabilities of, any of its members. Nexia International does not accept liability for any loss arising from any action taken, or omission, on the basis of this publication. Professional advice should be obtained before acting or refraining from acting on the contents of this publication.

Membership of Nexia International, or associated umbrella organisations, does not constitute any partnership between members, and members do not accept any responsibility for the commission of any act, or omission to act by, or the liabilities of, other members.

Nexia International is the trading name of Nexia International Limited, a company registered in the Isle of Man. Company registration number: 53513C. Registered office: 2nd floor, Sixty Circular Road, Douglas, Isle of Man, IM1 1SA.

Related Documents