Global Imbalances Warwick J. McKibbin Center for Applied Macroeconomic Analysis (CAMA) RSPAS Australian National University &The Lowy Institute for International Policy & The Brookings Institution Presentation at Oxford University, 16 May 2006

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Global Imbalances

Warwick J. McKibbin

Center for Applied Macroeconomic Analysis (CAMA) RSPAS

Australian National University

&The Lowy Institute for International Policy

& The Brookings Institution

Presentation at Oxford University, 16 May 2006

Based on

• Lee, McKibbin and Park (2006) “Transpacific Trade Imbalances: Causes and Cures” World Economy vol 29

• McKibbin and Stoeckel (2005) The United States current account

deficits and world markets www.economicscenarios.com

• Forthcoming paper with Jong-Wha Lee on “Global Imbalances”

• McKibbin (2006) “The Global Macroeconomic Consequences of a Demogrphic Transition” Asian Economic Papers, MIT Press

Overview

• What are the macroeconomic imbalances? • Sources of current account imbalances• Quantifying Possible policies and shocks that can affect

current accounts• The Role of Demographics• Summary and Conclusion

Two Aspects of Global Imbalances

• Global Savings in excess of global investment which shows up as low long term real interest rates

• National savings and investment imbalances which show up as current account imbalances between countries

– Countries with national savings greater than national investment run current account surpluses

– Countries with national investment greater than national savings run current account deficits

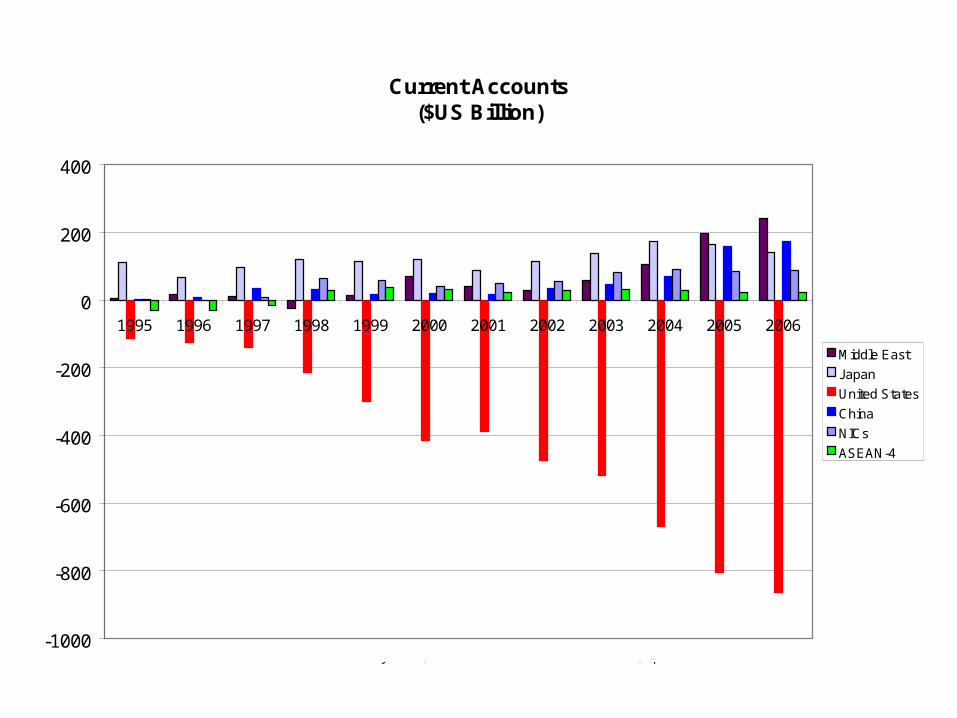

Current Accounts ($US Billion)

-1000

-800

-600

-400

-200

0

200

400

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Middle East

Japan

United States

China

NICs

ASEAN-4

International Monetary Fund, World Economic Outlook Database, April 2006

Global Current accounts

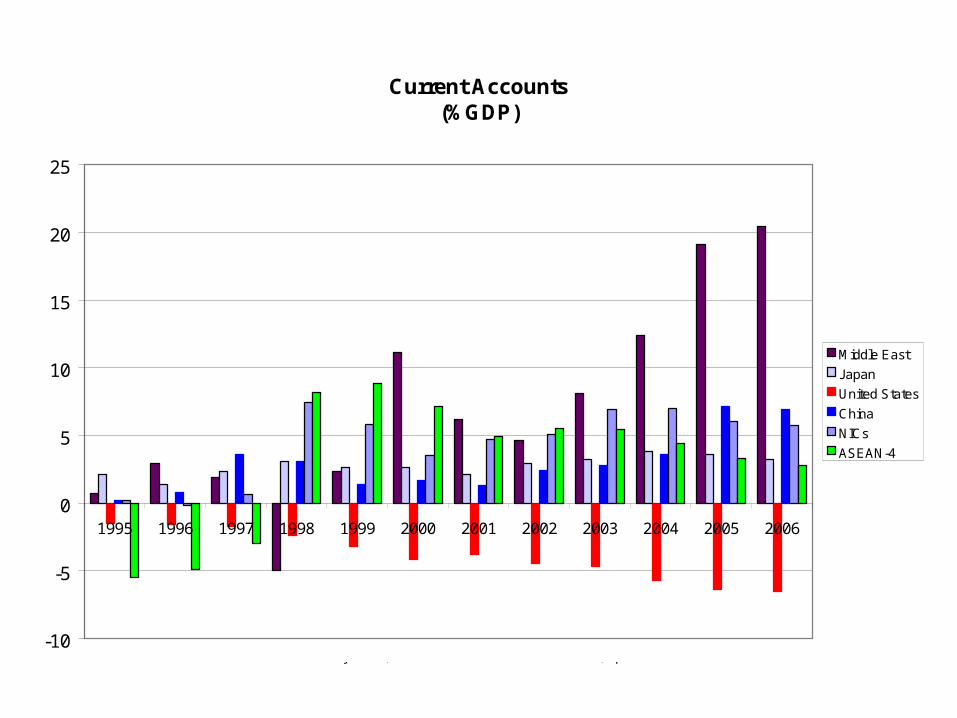

Current Accounts (%GDP)

-10

-5

0

5

10

15

20

25

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Middle East

Japan

United States

China

NICs

ASEAN-4

International Monetary Fund, World Economic Outlook Database, April 2006

Number of Real Factors and not a Single cause

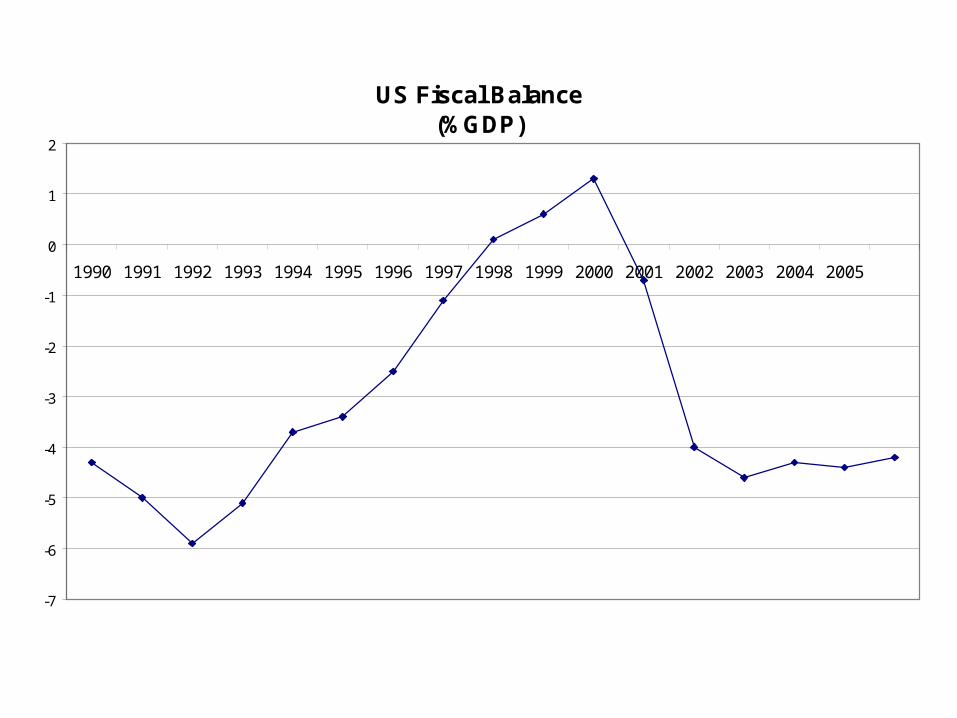

• Pull– US fiscal deficits– Decline in household saving– Strong productivity growth

• Push– Decline in Asian investment rates (except China)– Rising corporate and household saving in China– Oil revenue recycling by Oil Exporters

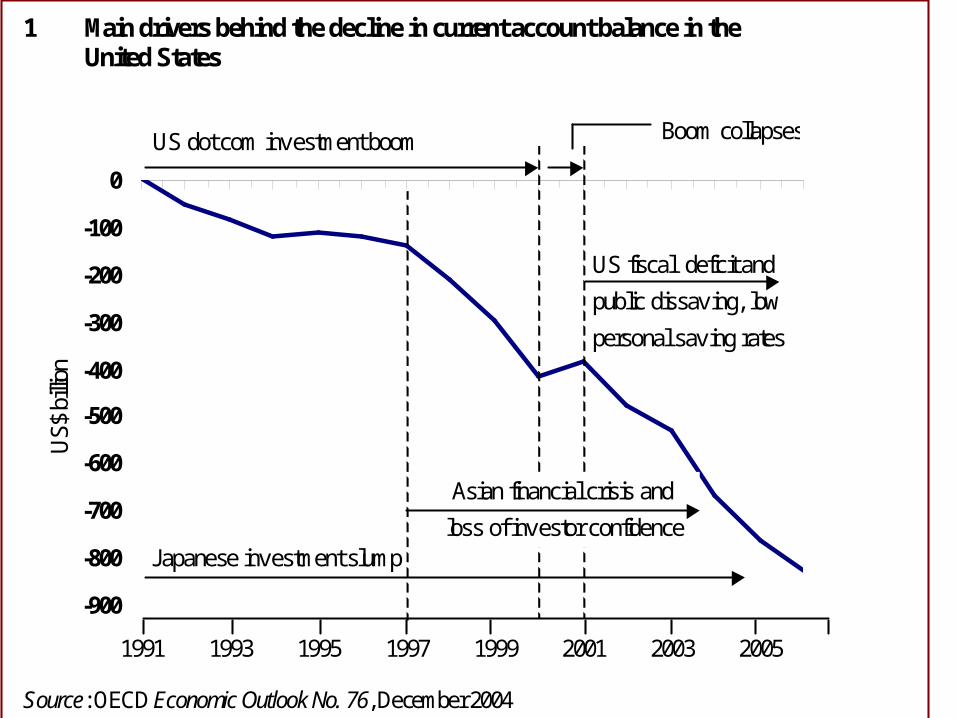

1 Main drivers behind the decline in current account balance in the United States

-900

-800

-700

-600

-500

-400

-300

-200

-100

0

1991 1993 1995 1997 1999 2001 2003 2005

US$

billi

on .

..

US fiscal deficit and

public dissav ing, low

personal sav ing rates

Japanese inv estment slump

US dot com inv estment boom Boom collapses

Asian financial crisis and

loss of inv estor confidence

Source: OECD Economic Outlook No. 76, December 2004

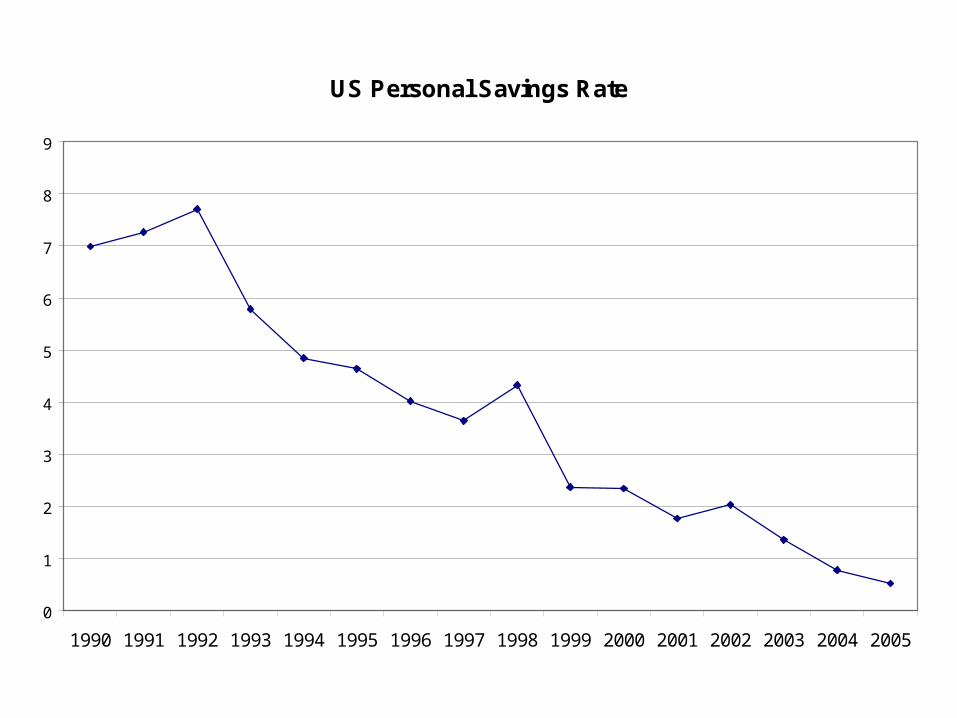

US Personal Savings Rate

0

1

2

3

4

5

6

7

8

9

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

US Fiscal Balance(%GDP)

-7

-6

-5

-4

-3

-2

-1

0

1

2

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Source: IMF WEO database 2005

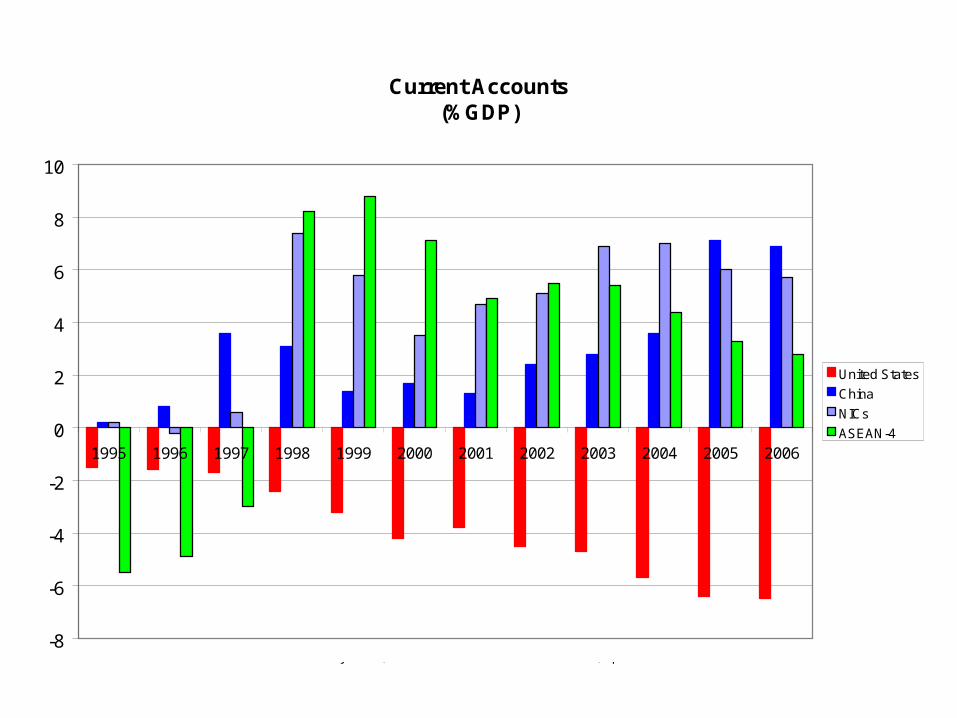

Current Accounts (%GDP)

-8

-6

-4

-2

0

2

4

6

8

10

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

United States

China

NICs

ASEAN-4

International Monetary Fund, World Economic Outlook Database, April 2006

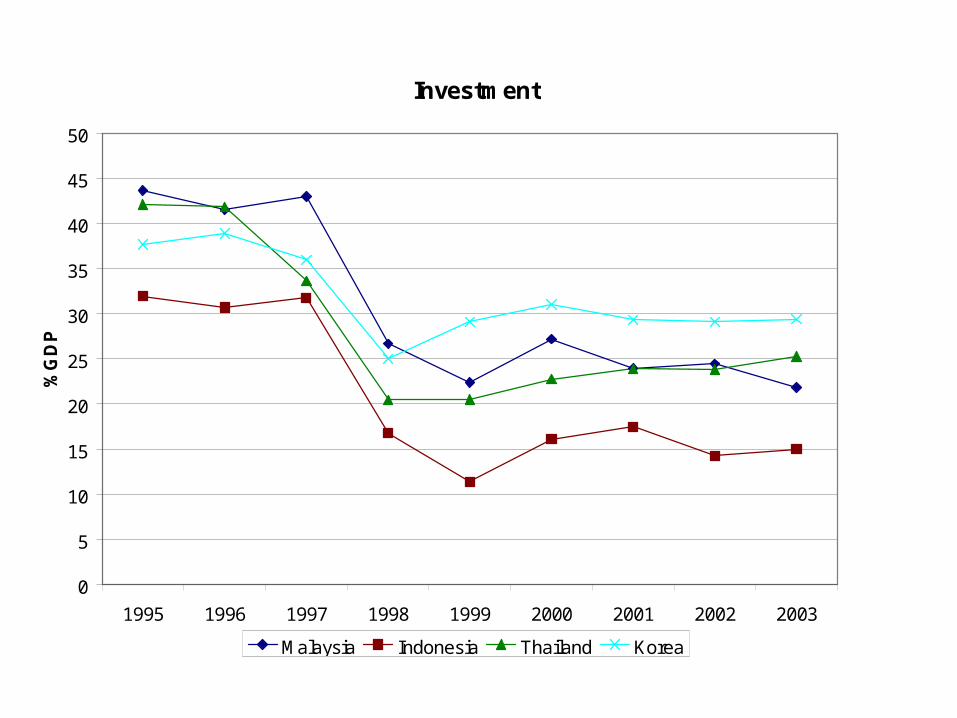

Investment

0

5

10

15

20

25

30

35

40

45

50

1995 1996 1997 1998 1999 2000 2001 2002 2003

%G

DP

Malaysia Indonesia Thailand Korea

Change in Asian Current accounts

• Large fall in Investment except China• Rise in Chinese corporate and household savings

Implication of various shocks for Current accounts

Using the G-Cubed (Asia Pacific Model)

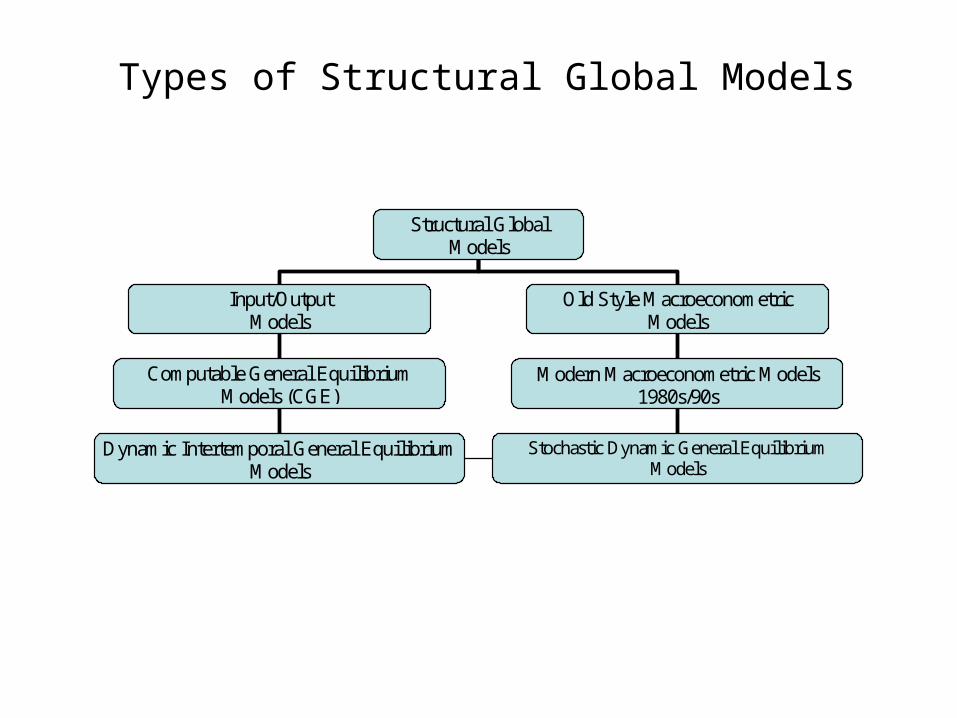

Types of Structural Global Models

Structural Global Models

Input/Output Models

Old Style Macroeconometric Models

1960s/70s

Computable General Equilibrium Models (CGE)

Models

Dynamic Intertemporal General Equilibrium Models

Modern Macroeconometric Models 1980s/90s

Stochastic Dynamic General Equilibrium Models

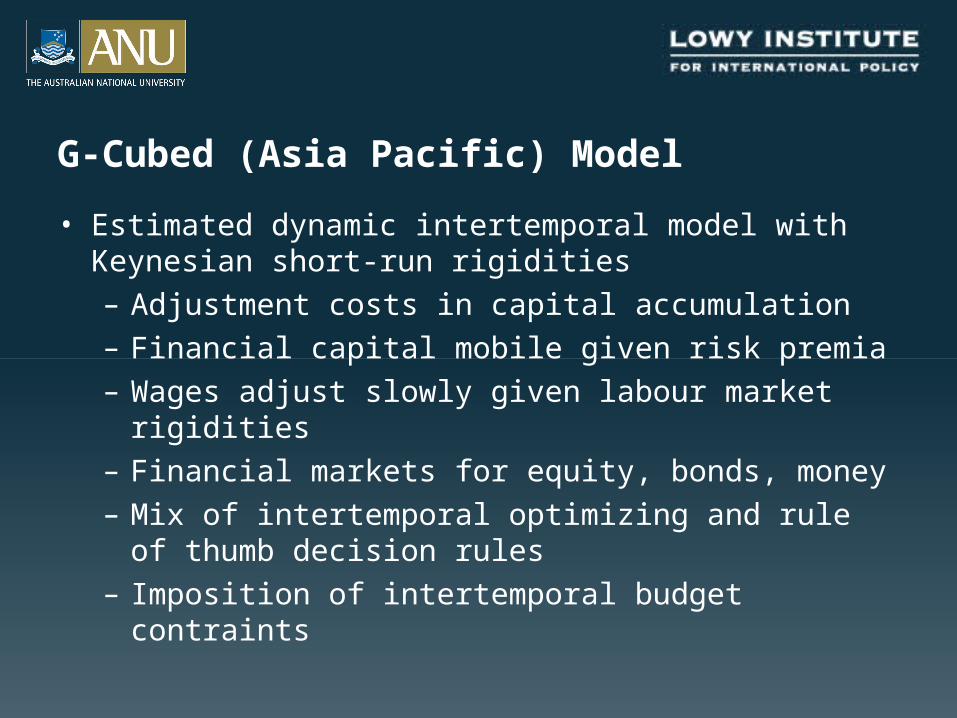

G-Cubed (Asia Pacific) Model

• Estimated dynamic intertemporal model with Keynesian short-run rigidities– Adjustment costs in capital accumulation– Financial capital mobile given risk premia– Wages adjust slowly given labour market rigidities– Financial markets for equity, bonds, money– Mix of intertemporal optimizing and rule of thumb

decision rules– Imposition of intertemporal budget contraints

Countries

• United States Japan• United Kingdom Europe• Canada Australia• New Zealand • China India • Korea Taiwan• Singapore Hong Kong• Malaysia Thailand • Indonesia Philippines • Oil Exporting Developing Countries • Eastern Europe and the former Soviet Union • Other Developing Countries

Sectors

• Energy

• Mining

• Agriculture

• Durable Manufacturing

• Non-Durable Manufacturing

• Services

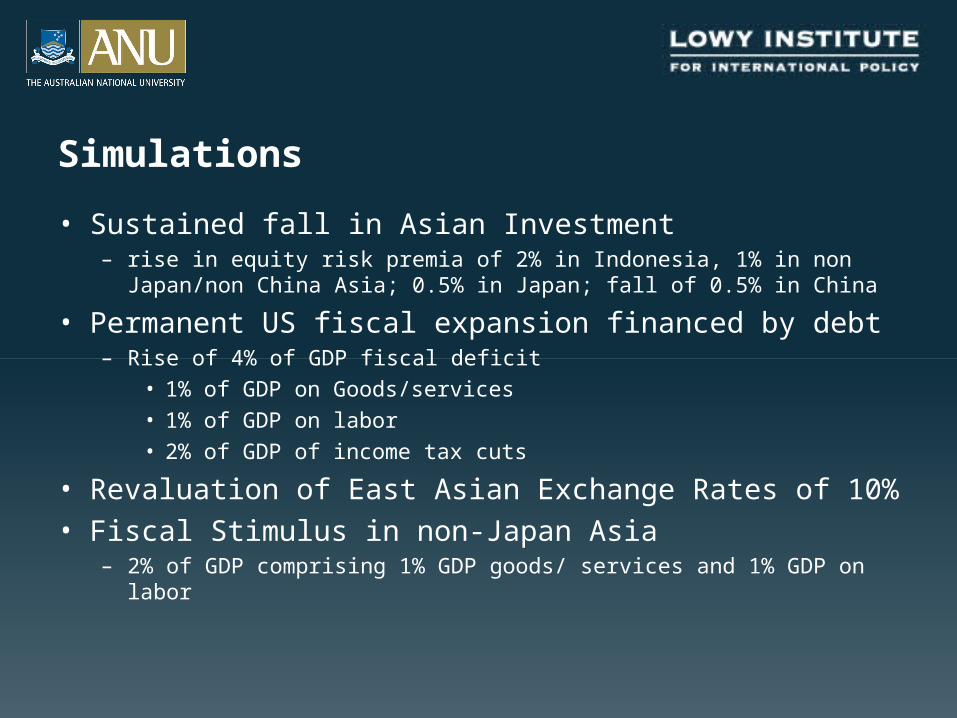

Simulations

• Sustained fall in Asian Investment – rise in equity risk premia of 2% in Indonesia, 1% in non Japan/non

China Asia; 0.5% in Japan; fall of 0.5% in China

• Permanent US fiscal expansion financed by debt – Rise of 4% of GDP fiscal deficit

• 1% of GDP on Goods/services

• 1% of GDP on labor

• 2% of GDP of income tax cuts

• Revaluation of East Asian Exchange Rates of 10%• Fiscal Stimulus in non-Japan Asia

– 2% of GDP comprising 1% GDP goods/ services and 1% GDP on labor

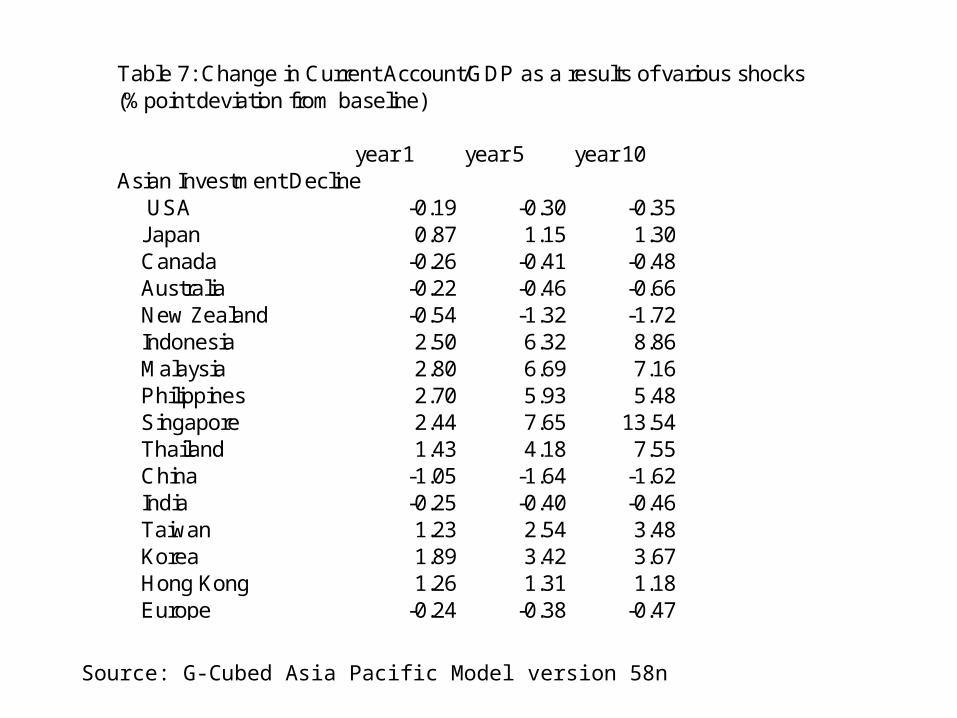

Adjustment Story: Asian Investment Decline

• Rise in equity risk premium implies rate of return on capital must rise above other assets– Capital stock must fall to generate the higher return– Investment declines– Portfolio holders substitute out of equities into bonds

(r falls), into housing (housing prices rise) and into foreign assets (capital outflow)

– Real exchange rate depreciates and GDP falls• raising exports and lowering imports

– Consistent with excess savings relative to investment• Current account improves

Source: G-Cubed Asia Pacific Model version 58n

Table 7: Change in Current Account/GDP as a results of various shocks(%point deviation from baseline)

year 1 year 5 year 10Asian Investment Decline USA -0.19 -0.30 -0.35 Japan 0.87 1.15 1.30 Canada -0.26 -0.41 -0.48 Australia -0.22 -0.46 -0.66 New Zealand -0.54 -1.32 -1.72 Indonesia 2.50 6.32 8.86 Malaysia 2.80 6.69 7.16 Philippines 2.70 5.93 5.48 Singapore 2.44 7.65 13.54 Thailand 1.43 4.18 7.55 China -1.05 -1.64 -1.62 India -0.25 -0.40 -0.46 Taiwan 1.23 2.54 3.48 Korea 1.89 3.42 3.67 Hong Kong 1.26 1.31 1.18 Europe -0.24 -0.38 -0.47

Adjustment Story: US Fiscal Policy

• Basic Mundell-Fleming story except intertemporal overlay and asset adjustment

• Higher spending/lower taxes initially raises GDP but over time GDP falls as resources are extracted from the private sector to finance the fiscal deficit

• Partial Ricardian adjustment in Consumption but long term real interest rates rise to free up resources from the private sector to finance the deficit

• Net capital inflow which initially appreciates the US real exchange rate– Exports fall, imports rise

Adjustment Story: US Fiscal Policy

• Investment rises initially but then falls, private saving rises but total savings falls by more than investment– US Current account deteriorates

• High long term real interest rates lowers global investment improving Asian current accounts

Source: G-Cubed Asia Pacific Model version 58n

Table 7: Change in Current Account/GDP as a results of various shocks(%point deviation from baseline)

US Fiscal policy USA -1.58 -1.89 -1.95 Japan 0.95 0.94 1.00 Canada 1.04 1.36 1.41 Australia 1.00 1.11 1.21 New Zealand 1.57 2.57 2.67 Indonesia 0.56 1.24 1.22 Malaysia 1.03 2.10 1.75 Philippines 2.54 2.94 2.20 Singapore -0.40 0.34 1.51 Thailand 1.31 2.09 2.32 China 0.24 0.48 0.38 India 0.52 0.82 0.71 Taiwan 0.43 0.73 0.89 Korea 1.10 1.59 1.33 Hong Kong 5.14 4.53 3.57 Europe 0.67 0.61 0.66

Adjustment Story: East Asia Revaluation

• Monetary policy regimes differ across countries

• Fixed exchange rates in China and Hong Kong• Other countries follow a modified Henderson-McKibbin

Rule with an additional weight on a desired nominal exchange rate relative to the $US– Shock is a change in the desired bilateral rate with the

$US.

Adjustment Story: East Asia Revaluation

• Real exchange rate initially appreciates– Over time prices rise less quickly and the real exchange

eventually returns to base– GDP in appreciating countries fall relative to base

• Chinese GDP falls relative to base by 4% in the first year– Exports less competitive but domestic slowdown reduces

imports• Trade balance worsens slightly

– GDP in other countries ambiguous depending on competition with China and East Asia versus fall in Asian demand from trading partners

– Overall impact on US/Asia trade balances is small

Source: G-Cubed Asia Pacific Model version 58n

Table 7: Change in Current Account/GDP as a results of various shocks(%point deviation from baseline)

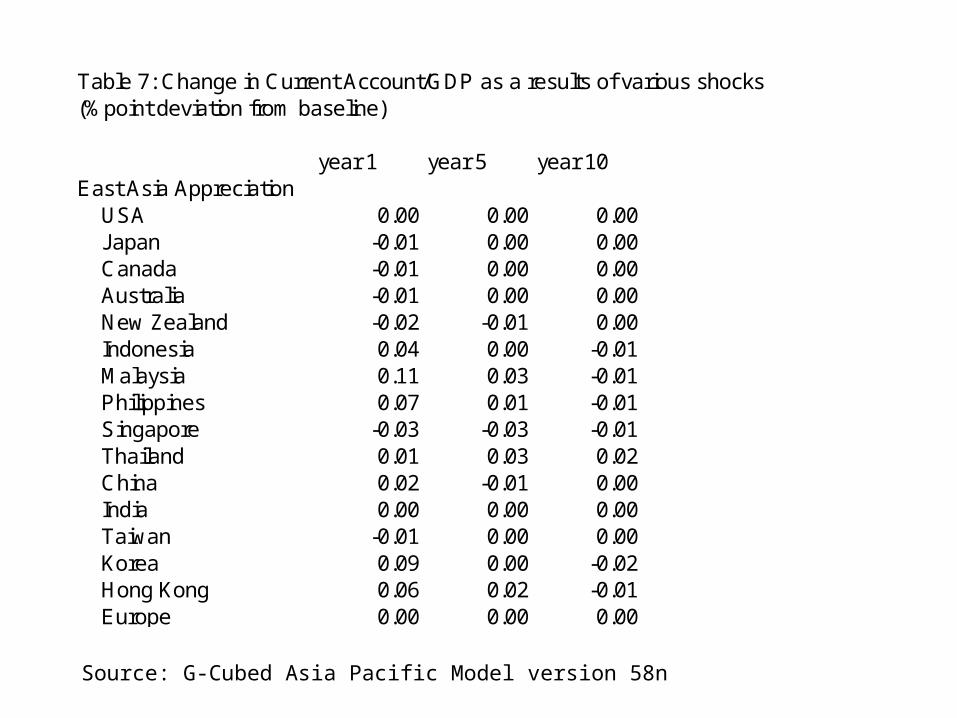

year 1 year 5 year 10East Asia Appreciation USA 0.00 0.00 0.00 Japan -0.01 0.00 0.00 Canada -0.01 0.00 0.00 Australia -0.01 0.00 0.00 New Zealand -0.02 -0.01 0.00 Indonesia 0.04 0.00 -0.01 Malaysia 0.11 0.03 -0.01 Philippines 0.07 0.01 -0.01 Singapore -0.03 -0.03 -0.01 Thailand 0.01 0.03 0.02 China 0.02 -0.01 0.00 India 0.00 0.00 0.00 Taiwan -0.01 0.00 0.00 Korea 0.09 0.00 -0.02 Hong Kong 0.06 0.02 -0.01 Europe 0.00 0.00 0.00

Source: G-Cubed Asia Pacific Model version 58n

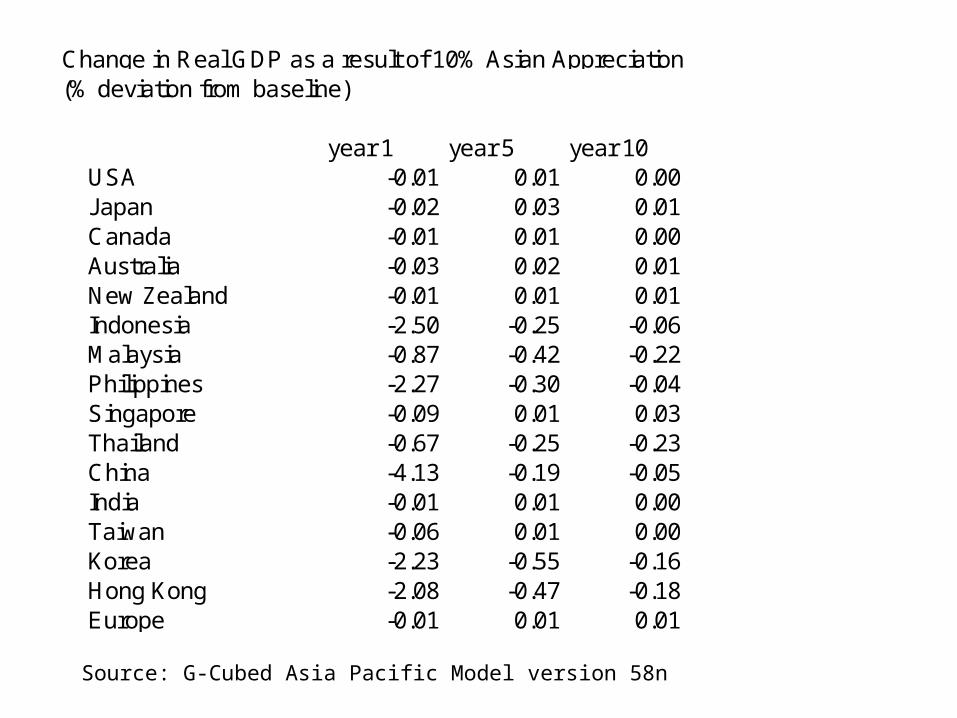

Change in Real GDP as a result of 10% Asian Appreciation(% deviation from baseline)

year 1 year 5 year 10 USA -0.01 0.01 0.00 Japan -0.02 0.03 0.01 Canada -0.01 0.01 0.00 Australia -0.03 0.02 0.01 New Zealand -0.01 0.01 0.01 Indonesia -2.50 -0.25 -0.06 Malaysia -0.87 -0.42 -0.22 Philippines -2.27 -0.30 -0.04 Singapore -0.09 0.01 0.03 Thailand -0.67 -0.25 -0.23 China -4.13 -0.19 -0.05 India -0.01 0.01 0.00 Taiwan -0.06 0.01 0.00 Korea -2.23 -0.55 -0.16 Hong Kong -2.08 -0.47 -0.18 Europe -0.01 0.01 0.01

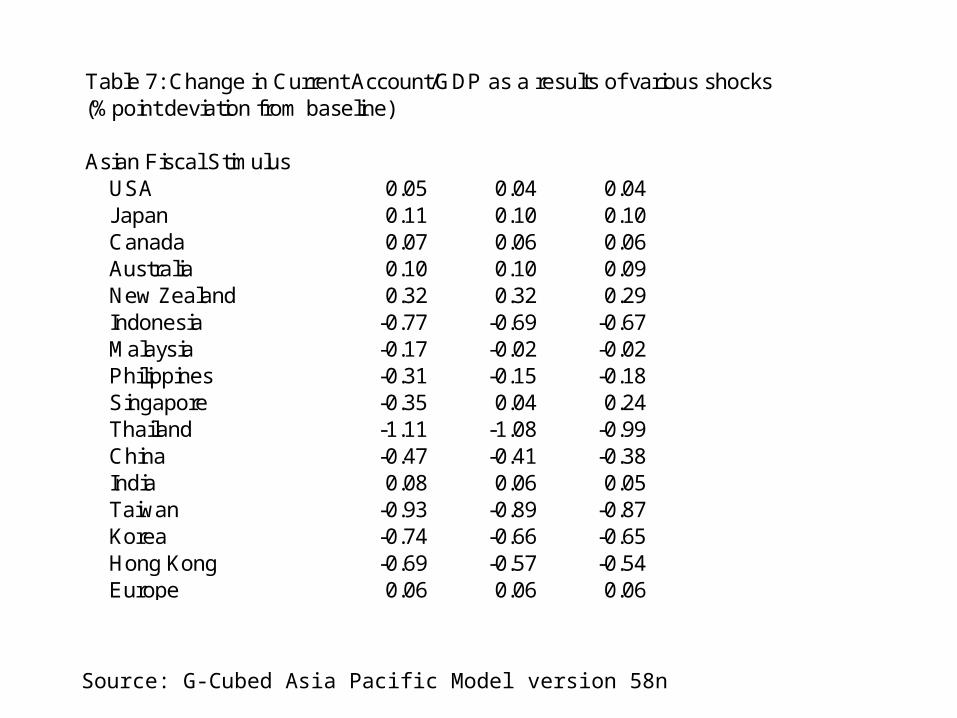

Adjustment Story: Asian Fiscal Stimulus

• Similar story to US policy except partial exchange rate targeting in some countries causes larger rises in GDP in Asia

• Less impact on long term real interest rates because of economic size and less crowding out of foreign investment

• Capital flows in to finance the fiscal deficit• Real exchange rate appreciation

– Trade balance deteriorates

Source: G-Cubed Asia Pacific Model version 58n

Table 7: Change in Current Account/GDP as a results of various shocks(%point deviation from baseline)

Asian Fiscal Stimulus USA 0.05 0.04 0.04 Japan 0.11 0.10 0.10 Canada 0.07 0.06 0.06 Australia 0.10 0.10 0.09 New Zealand 0.32 0.32 0.29 Indonesia -0.77 -0.69 -0.67 Malaysia -0.17 -0.02 -0.02 Philippines -0.31 -0.15 -0.18 Singapore -0.35 0.04 0.24 Thailand -1.11 -1.08 -0.99 China -0.47 -0.41 -0.38 India 0.08 0.06 0.05 Taiwan -0.93 -0.89 -0.87 Korea -0.74 -0.66 -0.65 Hong Kong -0.69 -0.57 -0.54 Europe 0.06 0.06 0.06

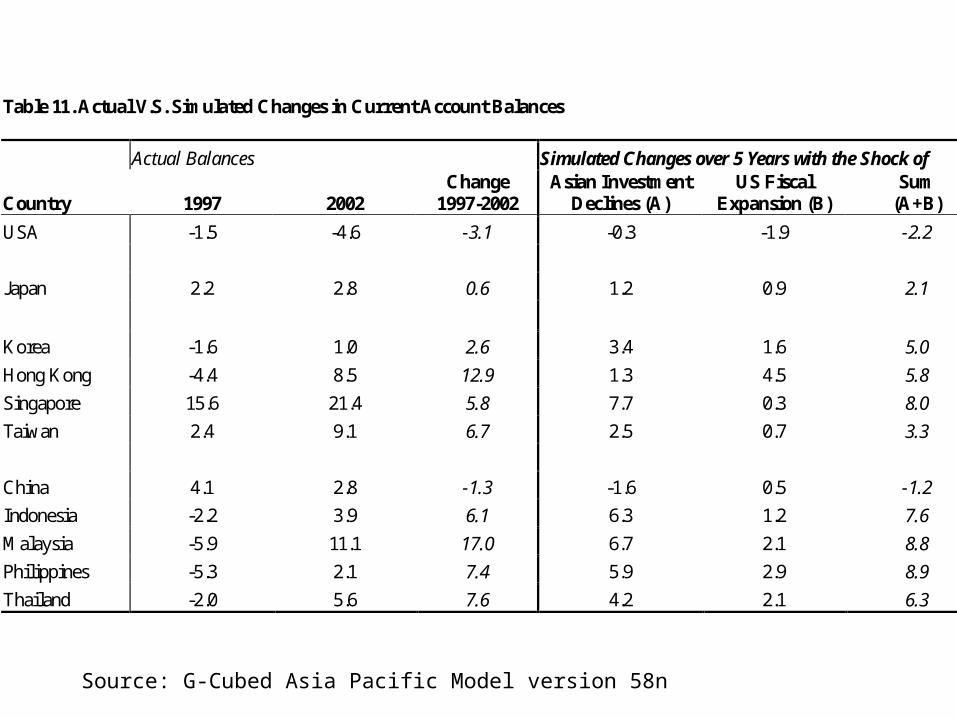

Source: G-Cubed Asia Pacific Model version 58n

Table 11. Actual V.S. Simulated Changes in Current Account Balances

Actual Balances Simulated Changes over 5 Years with the Shock of

Country 1997 2002 Change

1997-2002 Asian Investment

Declines (A) US Fiscal

Expansion (B) Sum

(A+B)

USA -1.5 -4.6 -3.1 -0.3 -1.9 -2.2

Japan 2.2 2.8 0.6 1.2 0.9 2.1

Korea -1.6 1.0 2.6 3.4 1.6 5.0

Hong Kong -4.4 8.5 12.9 1.3 4.5 5.8

Singapore 15.6 21.4 5.8 7.7 0.3 8.0

Taiwan 2.4 9.1 6.7 2.5 0.7 3.3

China 4.1 2.8 -1.3 -1.6 0.5 -1.2

Indonesia -2.2 3.9 6.1 6.3 1.2 7.6

Malaysia -5.9 11.1 17.0 6.7 2.1 8.8

Philippines -5.3 2.1 7.4 5.9 2.9 8.9

Thailand -2.0 5.6 7.6 4.2 2.1 6.3

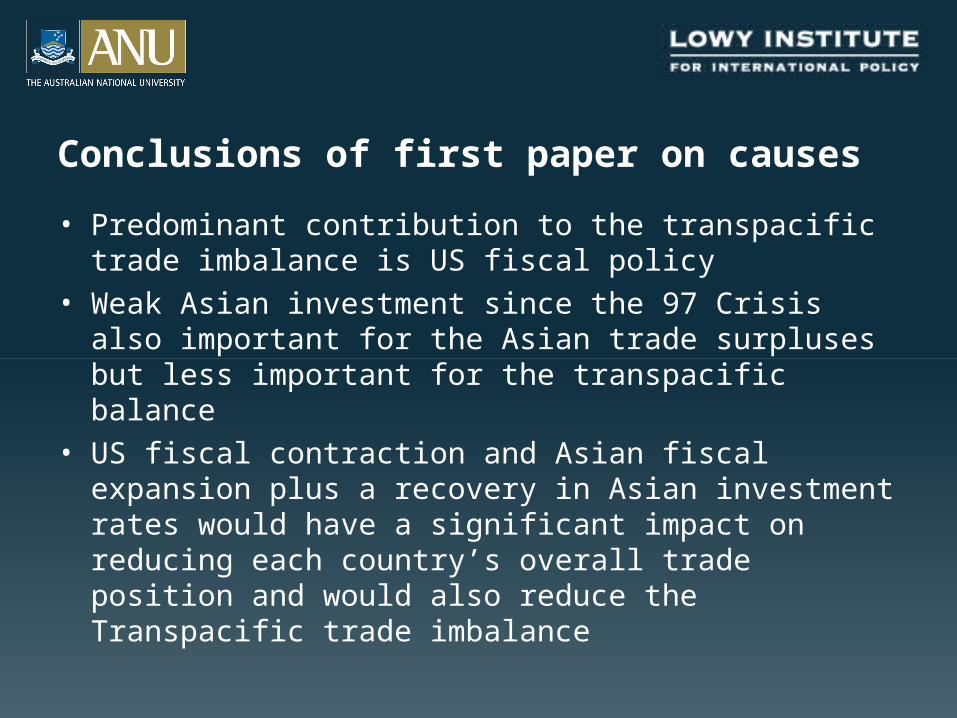

Conclusions of first paper on causes

• Predominant contribution to the transpacific trade imbalance is US fiscal policy

• Weak Asian investment since the 97 Crisis also important for the Asian trade surpluses but less important for the transpacific balance

• US fiscal contraction and Asian fiscal expansion plus a recovery in Asian investment rates would have a significant impact on reducing each country’s overall trade position and would also reduce the Transpacific trade imbalance

Conclusions

• East Asia exchange rate revaluation has significant effects on slowing East Asia for a year but not in changing global trade balances

• The worsening in East Asian competitiveness plus weaker East Asian growth tends to offset each other in the spillover to other countries and have a minor impact on the relative saving and investment balances across the region.

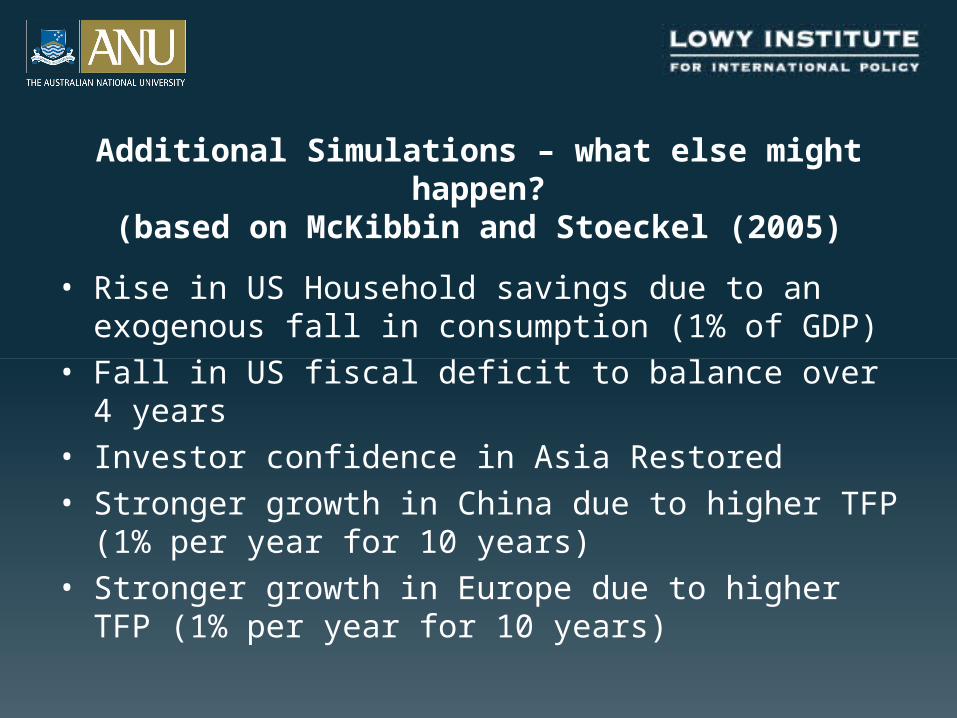

Additional Simulations – what else might happen?(based on McKibbin and Stoeckel (2005)

• Rise in US Household savings due to an exogenous fall in consumption (1% of GDP)

• Fall in US fiscal deficit to balance over 4 years• Investor confidence in Asia Restored• Stronger growth in China due to higher TFP (1% per

year for 10 years)• Stronger growth in Europe due to higher TFP (1% per

year for 10 years)

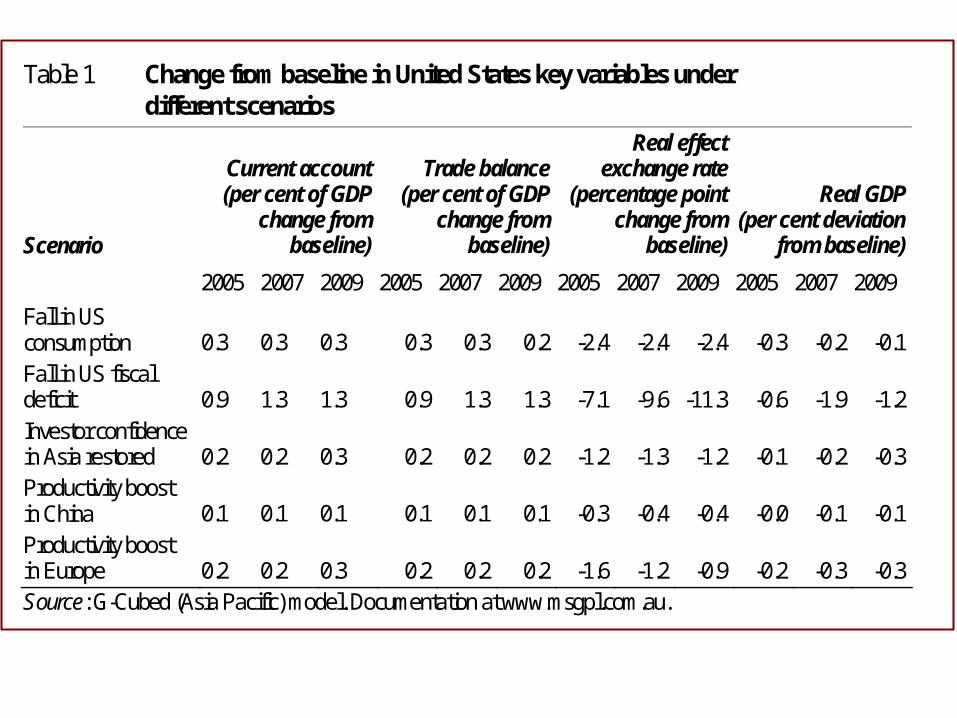

Table 1 Change from baseline in United States key variables under different scenarios

Scenario

Current account (per cent of GDP

change from baseline)

Trade balance (per cent of GDP

change from baseline)

Real effect exchange rate

(percentage point change from

baseline)

Real GDP (per cent deviation

from baseline)

2005 2007 2009 2005 2007 2009 2005 2007 2009 2005 2007 2009 Fall in US consumption 0.3 0.3 0.3 0.3 0.3 0.2 -2.4 -2.4 -2.4 -0.3 -0.2 -0.1 Fall in US fiscal deficit 0.9 1.3 1.3 0.9 1.3 1.3 -7.1 -9.6 -11.3 -0.6 -1.9 -1.2 Investor confidence in Asia restored 0.2 0.2 0.3 0.2 0.2 0.2 -1.2 -1.3 -1.2 -0.1 -0.2 -0.3 Productivity boost in China 0.1 0.1 0.1 0.1 0.1 0.1 -0.3 -0.4 -0.4 -0.0 -0.1 -0.1 Productivity boost in Europe 0.2 0.2 0.3 0.2 0.2 0.2 -1.6 -1.2 -0.9 -0.2 -0.3 -0.3 Source: G-Cubed (Asia Pacific) model. Documentation at www.msgpl.com.au.

Is there a demographic story behind the imbalances?

The Global Macroeconomic Consequences of a Demographic

Transition

Warwick J McKibbin

Centre for Applied Macroeconomic Analysis, RSPAS, ANU;Lowy Institute for International Policy, Sydney

The Brookings Institution, Washington DC;

Prepared for a seminar at the Bank of Korea, Seoul Wednesday May 10 2006

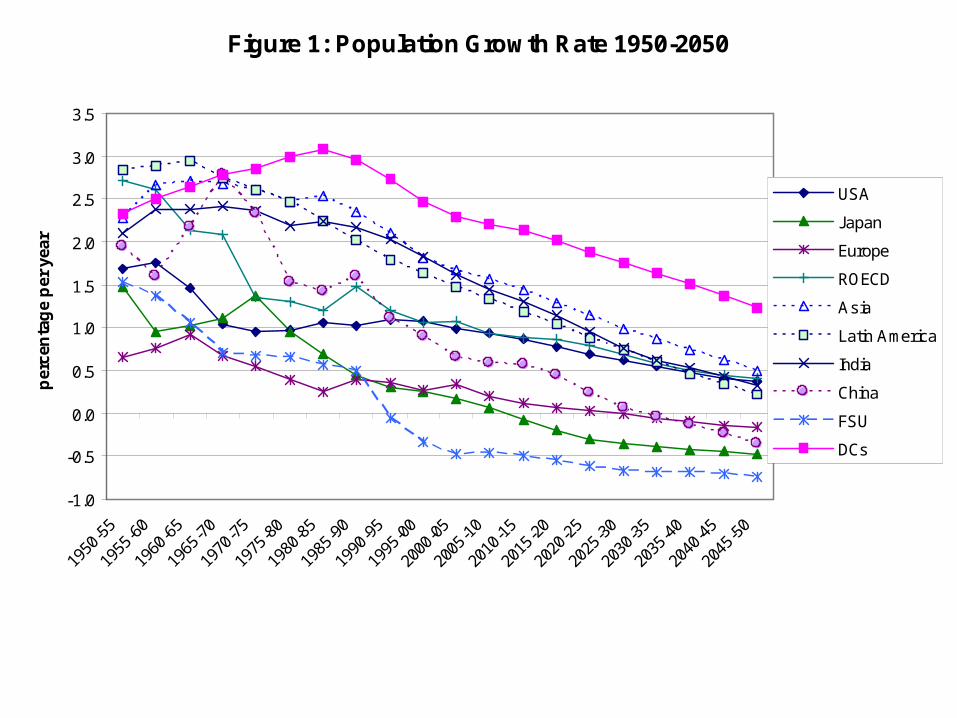

Figure 1: Population Growth Rate 1950-2050

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1950

-55

1955

-60

1960

-65

1965

-70

1970

-75

1975

-80

1980

-85

1985

-90

1990

-95

1995

-00

2000

-05

2005

-10

2010

-15

2015

-20

2020

-25

2025

-30

2030

-35

2035

-40

2040

-45

2045

-50

per

cen

tag

e p

er y

ear

USA

Japan

Europe

ROECD

Asia

Latin America

India

China

FSU

DCs

Source: UN, World Population Prospects: The 2004 Revision (Medium Variant)

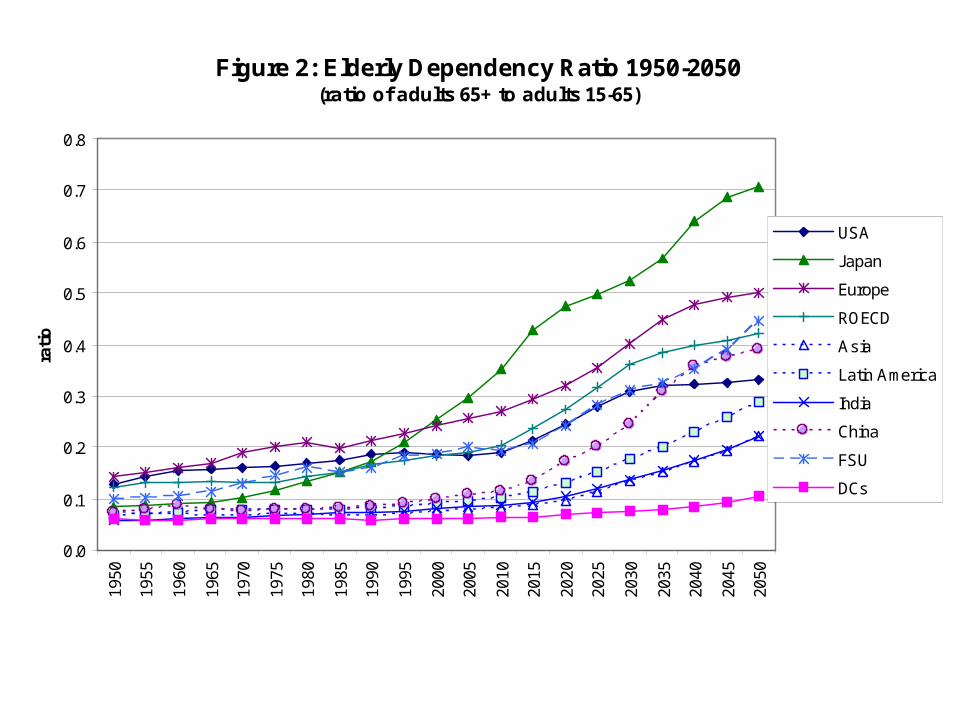

Figure 2: Elderly Dependency Ratio 1950-2050(ratio of adults 65+ to adults 15-65)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

rati

o

USA

Japan

Europe

ROECD

Asia

Latin America

India

China

FSU

DCs

Source: UN, World Population Prospects: The 2004 Revision (Medium Variant)

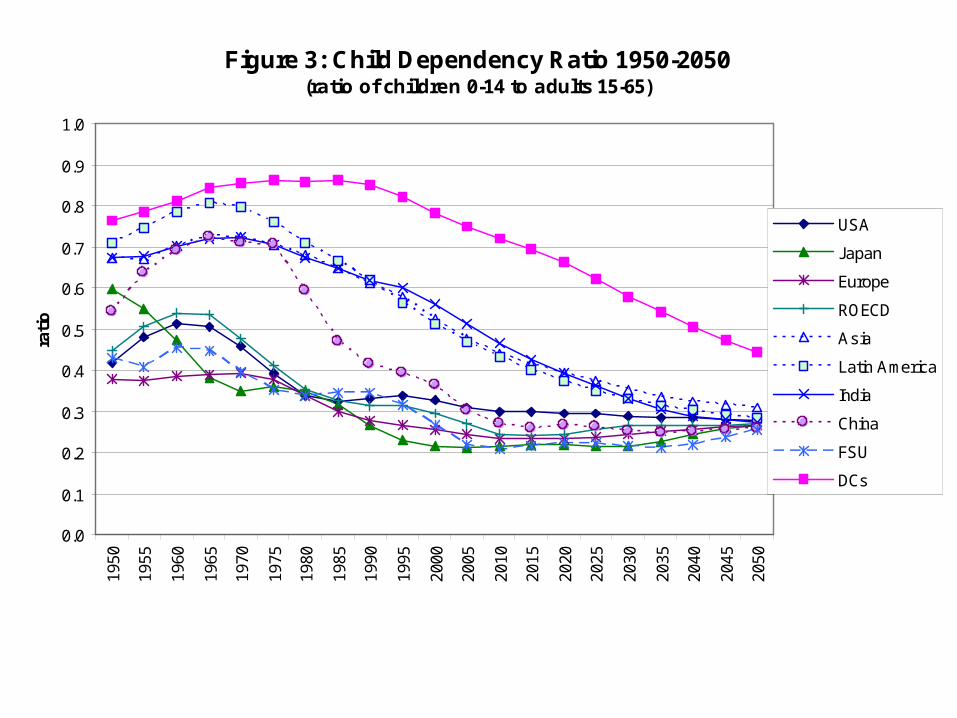

Figure 3: Child Dependency Ratio 1950-2050(ratio of children 0-14 to adults 15-65)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.019

50

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

rati

o

USA

Japan

Europe

ROECD

Asia

Latin America

India

China

FSU

DCs

Source: UN, World Population Prospects: The 2004 Revision (Medium Variant)

Figure 12: Contribution to Current Accounts of Own versus Global Demographic

Change US Current Account/GDP

(relative to no demographic transi tion)

-1

-0.5

0

0.5

1

1.5

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

% p

oin

t ch

ang

e

global ow n

Japan Current Account/GDP(relative to no demographic transi tion)

0

1

2

3

4

5

2005

2009

2013

2017

2021

2025

2029

2033

2037

2041

2045

2049

% p

oin

t ch

ang

e

global ow n

China Current Account/GDP(relative to no demographic transi tion)

00.10.2

0.30.40.50.6

0.70.8

2005

2009

2013

2017

2021

2025

2029

2033

2037

2041

2045

2049

% p

oin

t ch

ang

e

global ow n

Latin America Current Account/GDP(relative to no demographic transi tion)

-1

-0.5

0

0.5

1

1.5

2005

2009

2013

2017

2021

2025

2029

2033

2037

2041

2045

2049

% p

oin

t ch

ang

e

global ow n

Overall Conclusion

• US current account deficit and corresponding current account surpluses in other countries caused by a variety of factors that affect– Savings and investment changes in the United States

China, East Asia and rest of world

• Exchange rate policy has little to do with changing current account balances which reflect real rather than monetary factors – This is unlikely to be a solution (especially for China)

because it has minor effect on US savings and investment

Background Papers

www.sensiblepolicy.com

www.gcubed.com

Related Documents