Connect with Vanguard > vanguard.com • Equities not domiciled in the United States accounted for 51% of the global equity market as of December 31, 2013, 1 reflecting a significant opportunity for portfolio diversification. • Despite the size of non-U.S. markets, U.S. mutual fund investors held, on average, only 27% of their total equity allocation in non-U.S.-domiciled funds as of year-end 2013, according to Morningstar. • This paper concludes that although no one answer fits all investors, empirical and practical considerations suggest a reasonable starting allocation to non-U.S. stocks of 20%, with an upper limit based on global market capitalization, subject to the investor’s perspective on the short- and long-term trade-offs. Vanguard research February 2014 Note: This paper is an update of a paper by the same author published in 2012 and titled Considerations for investing in non-U.S. equities. 1 Sources: Thomson Reuters Datastream and MSCI, as of December 31, 2013. Global equities: Balancing home bias and diversification Author Christopher B. Philips, CFA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Connect with Vanguard > vanguard.com

• EquitiesnotdomiciledintheUnitedStatesaccountedfor51%oftheglobalequitymarketasofDecember31,2013,1reflectingasignificantopportunityforportfoliodiversification.

• Despitethesizeofnon-U.S.markets,U.S.mutualfundinvestorsheld,onaverage,only27%oftheirtotalequityallocationinnon-U.S.-domiciledfundsasofyear-end2013,accordingtoMorningstar.

• Thispaperconcludesthatalthoughnooneanswerfitsallinvestors,empiricalandpracticalconsiderationssuggestareasonablestartingallocationtonon-U.S.stocksof20%,withanupperlimitbasedonglobalmarketcapitalization,subjecttotheinvestor’sperspectiveon theshort-andlong-termtrade-offs.

Vanguard research February 2014

Note: This paper is an update of a paper by the same author published in 2012 and titled Considerations for investing in non-U.S. equities.

1 Sources: Thomson Reuters Datastream and MSCI, as of December 31, 2013.

Globalequities:Balancinghomebiasanddiversification

Author

Christopher B. Philips, CFA

2

AsofDecember31,2013,U.S.equitiesaccountedfor49%oftheglobalequitymarket.Non-U.S.equities,includingthoseofdevelopedcountriessuchasGermany,Japan,andtheUnitedKingdom,plusthoseofemergingcountriessuchasBrazil,India,andChina,accountedfortheremaining51%.AsshowninFigure 1,the2013U.S.marketcapitalizationwasbelowtherecenthighof55%oftheglobalequitymarket,reachedinMarch2003,butremainedsignificantlyabovetheall-timelowof29%,reachedatthepeakoftheJapanesestockmarketruninthelate1980s.AportfolioinvestingsolelywithintheU.S.stockmarketthusautomaticallyexcludesoverone-halfoftheglobalopportunityset.

The case for investing in non-U.S. stocks

Beyondtheopportunitytoinvestacrossabroadermarket,non-U.S.equitieshavediversifiedthe returnsofU.S.equities,onaverage,acrosstime.Therationalefordiversificationisclear—U.S.stocksareexposedtoU.S.economicandmarketforces,whilestocksdomiciledoutsideoftheUnitedStatesofferexposuretoawiderarrayofeconomicand

marketforces.Thesedifferingeconomiesandmarketsproducereturnsthatcanvaryfromthose ofU.S.stocks.Figure 2a,onpage4,showsthat, allelsebeingequal,aU.S.investorshouldrealize adiversificationbenefitfrominvestinggloballybecausetheequitymarketsofotherdevelopedeconomiesareless-than-perfectlycorrelatedwith theU.S.equitymarket.

Atahighlevel,thebenefitofglobaldiversificationcanbeshownbycomparingthevolatilityofaglobalindexwiththatofindexesfocusedoneithertheU.S.marketornon-U.S.marketsinisolation.InFigure 2b,onpage4,thebenefitofdiversificationisclear:AlthougheachindividualcountryhasexperiencedgreatervolatilitythanthatoftheUnitedStates,thebroadMSCIWorldIndexexUSA,whichfocusesondevelopedmarkets,hasexperiencedvolatilitymoresimilartothatoftheUnitedStates.Andwhentakenonestepfurther,thebroadestglobalindex—representingthecombinedMSCIUSAIndex,thedevelopedmarketsindex,andtheMSCIEmergingMarketsIndex—hasrealizedthelowestaveragevolatility.

Notesonrisk:Allinvestmentsaresubjecttorisk,includingpossiblelossofprincipal.Diversificationdoesnotensureaprofitorprotectagainstalossinadecliningmarket.Investmentsinsecuritiesissuedby non-U.S.companiesaresubjecttorisksincludingcountry/regionalriskandcurrencyrisk.Theserisksareespeciallyhighinemergingmarkets.

Past performance is not a guarantee of future results. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

3

Figure 1. Historical mix of global equity market capitalization

Notes: U.S. market represented by MSCI USA Index; non-U.S. market represented by MSCI World Index ex USA from 1969 through 1987 and MSCI All Country World Index ex USA thereafter. Data as of December 31, 2013.

Sources: Thomson Reuters Datastream and MSCI.

Mar

ket

capi

taliz

atio

n

0

20

40

60

80

100%

U.S. market

Non-U.S. market

1969 1973 1977 1981 1985 1989 1993 1997 2001 2005 2009 2013

Can multinational corporations provide enough exposure?

Onecommonquestionregardingexposureto non-U.S.stocksiswhetherenoughcoverage offoreignmarketsisembeddedintheprices ofU.S.-domiciledmultinationalcompaniessuch asMcDonald’s,Amazon.com,orExxonMobil. Thethinkinggoesthatbecausemanylargefirmsgenerateasignificantportionoftheirrevenuefromforeignoperations,thediversificationbenefitsofglobalinvestingarealreadyreflectedinthepricesandperformanceoflargeU.S.firms.

Whilethisaspectofglobalizationcannotbeignored(andcertainlycanhaveanimpactoninvestors’portfolios),webelieveitstillmakessenseforinvestorstoholdnon-U.S.-domiciledinvestments,forseveralreasons.First,simplyfocusingonU.S.-domiciledcompaniesmeansan

investorhasnostakeinleading,globalcompaniesthataredomiciledinothercountriessuchasSamsung,Toyota,orNestlé.Second,manyfirmsseektohedgeawaycurrencyfluctuationsoftheirforeignoperations.Althoughthiscanhelptosmoothrevenuestreams,foreignexchange canbeadiversifierforU.S.investors.Lastly,aportfoliomadeupsolelyofU.S.firms,whicharemoreconcentratedinbiotechnology,computerequipment,informationtechnologyandITservices,andsoftware,wouldbeunderweightedin“oldworld”industriessuchaselectricalequipment,durablehouseholdgoods,andautomobiles.Inotherwords,anall-U.S.portfoliowouldlosenotjustinvestmentopportunitiesbutalsothediversificationbenefitsofaportfoliothat’smoreevenlydistributedacrossindustries.

4

Given global exposure, how much?

Thedecisiontoinvestgloballyisonlythefirst step.Thenextstepistodetermineanappropriateallocation.Thestandardfinancial-theoryapproach,whetherforallocatinggloballyorwithinaspecificcountryormarket,istoinvestproportionallyaccordingtomarketcapitalization.Thismethodassumesthatmarketsarereasonablyefficientandthatstockpricesreflectalltheavailableinformation,investmentpositions,andexpectationsoftheinvestingcommunity.AsshowninFigure1,U.S.equitiescurrentlymakeupapproximately49%of theglobalmarket.Accordingtothistheory,then,U.S.investorswouldcurrentlyhave51%oftheirequityportfolioinnon-U.S.equities,andthisweightwouldfluctuatewithmarketperformance.However,fewinvestorsfollowthisapproachtotheletter;instead,theymoreoftenchooseasetallocation andthenperiodicallyrebalancetothatlevel.

Formanyinvestorssuchanapproachrepresents areasonabletrade-offbetweentheopportunity fordiversificationandtherealitiesoftheglobalequitymarkets.Forexample,despiteincreasingefficiencies,globalmarketsarenotyetfullyandseamlesslyintegrated.Thefactremainsthat costssuchasexpenseratios,bid-askspreads,frictionalcosts,andevenmarket-impactcostscontinuetobehigherformarketsoutside oftheUnitedStates.

Inaddition,localinvestorsacrosstheworld (includingintheUnitedStates)areinfluencedbyembeddedhomebiases,probablyaresultboth ofregulatoryconstraints,suchasexplicitlimitsonpublicpensionfunds’allocations,andbehavioraltendencies.Forexample,accordingtoPhilips,Kinniry,andDonaldson(2012),U.S.investorsmaintainedanallocationtoU.S.stocksthat wasapproximately1.7xthemarketcapof

Figure 2.

a. Correlations of returns in foreign equity markets with U.S. equity markets

Correlations and volatility of equity returns of countries and regions

Notes: Country returns represented by MSCI country indexes; emerging markets represented by MSCI Emerging Markets Index; developed markets represented by MSCI World Index ex USA; global market, including both developed and emerging markets, represented by MSCI All Country World Index. Emerging market data begin in 1988; all data through December 31, 2013.

Sources: Vanguard, Thomson Reuters Datastream, and MSCI.

b. Volatility of returns for country and regional indexes

Cor

rela

tion

coef

ficie

nt

0

0.2

0.4

0.6

0.8

1

Aus

tral

iaA

ustr

iaB

elgi

umC

anad

aD

enm

ark

Fran

ceG

erm

any

Ital

yJa

pan

Net

herla

nds

Nor

way

Spa

inSw

eden

Switz

erla

ndU

.K.

Em

ergi

ng m

arke

ts

Ave

rage

Hon

g Ko

ng

Uni

ted

Sta

tes

Aus

tral

iaA

ustr

iaB

elgi

umC

anad

aD

enm

ark

Fran

ce

Ital

yH

ong

Kong

Japa

nN

ethe

rland

sN

orw

ayS

pain

Em

ergi

ng m

arke

tsD

evel

oped

mar

kets

Swed

enSw

itzer

land

U.K

.

Glo

bal

mar

ket

Ger

man

y

0

10

20

30

40%

Ann

ualiz

ed s

tand

ard

devi

atio

n

5

U.S.stocks,whilethenext-closestinvestorsintermsofbiastohomemarketcapwerethoseintheUnitedKingdom,whomaintainedarelativehomebiasofabout6.25xthemarketcapofU.K.stocks.Whatevertheunderlyingdriver,thelocalhomebiasesofinvestorsineachcountryaggregatetoformaglobalmarketthatisnotfullyrepresentativeofthetheoreticalfree-floatinginvestorexperience,whichwouldbetheobjectiveofafullymarket-proportionalportfolio.Asaresult,acasecouldbemadeforadedicatedallocationtonon-U.S.stocksthatdiffersfromtheglobalmarket-weightedportfoliosimplybasedonawarenessoflocalandglobalbiases(whetherjustifiedornot).

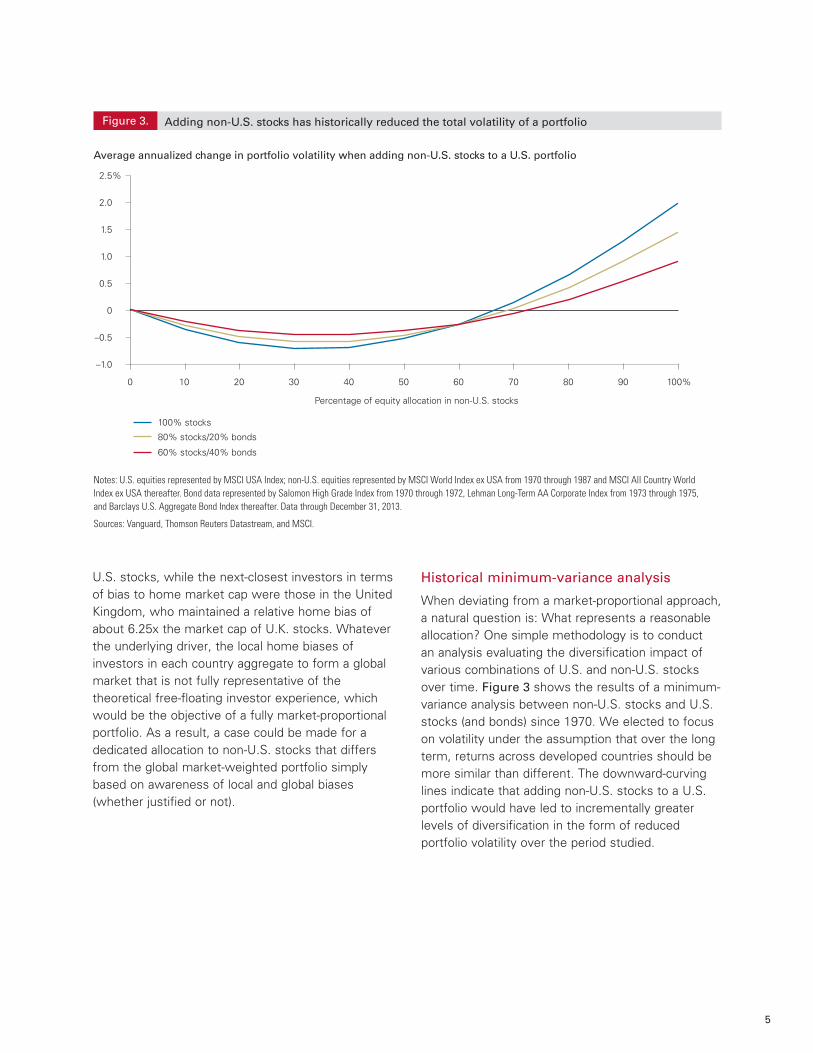

Historical minimum-variance analysis

Whendeviatingfromamarket-proportionalapproach,anaturalquestionis:Whatrepresentsareasonableallocation?Onesimplemethodologyistoconduct ananalysisevaluatingthediversificationimpactofvariouscombinationsofU.S.andnon-U.S.stocksovertime.Figure 3showstheresultsofaminimum-varianceanalysisbetweennon-U.S.stocksandU.S.stocks(andbonds)since1970.Weelectedtofocusonvolatilityundertheassumptionthatoverthelongterm,returnsacrossdevelopedcountriesshouldbemoresimilarthandifferent.Thedownward-curvinglinesindicatethataddingnon-U.S.stockstoaU.S.portfoliowouldhaveledtoincrementallygreaterlevelsofdiversificationintheformofreducedportfoliovolatilityovertheperiodstudied.

Figure 3.

Average annualized change in portfolio volatility when adding non-U.S. stocks to a U.S. portfolio

Adding non-U.S. stocks has historically reduced the total volatility of a portfolio

Notes: U.S. equities represented by MSCI USA Index; non-U.S. equities represented by MSCI World Index ex USA from 1970 through 1987 and MSCI All Country WorldIndex ex USA thereafter. Bond data represented by Salomon High Grade Index from 1970 through 1972, Lehman Long-Term AA Corporate Index from 1973 through 1975, and Barclays U.S. Aggregate Bond Index thereafter. Data through December 31, 2013.

Sources: Vanguard, Thomson Reuters Datastream, and MSCI.

100% stocks

80% stocks/20% bonds

60% stocks/40% bonds

0 10 30 40 50 60 8070 90 100%20

Percentage of equity allocation in non-U.S. stocks

–1.0

–0.5

0

0.5

1.0

1.5

2.0

2.5%

6

What’sstrikingaboutFigure3isthatU.S.investorswouldhaveobtainedsubstantial(relative)diversi-ficationbenefitsfromallocationstonon-U.S.stocksfarshortofthecurrentmarket-proportionalportfolio(nowabout51%andhistoricallyapproximately50%,onaverage).Infact,whenreferringbacktoFigure2,thenetimpactofafullygloballymarket-proportionalportfolioacrosshistoryhasbeenapproximately35basispointsinlowerannualvolatilityrelativetoa100%U.S.equityportfolio(representedinFigure3bythex-axis)—thesameimpactasa10%staticallocationtonon-U.S.stocks.Lookingattheblue lineinFigure3,whichrepresentsaportfoliocomposedentirelyofequities,themaximumhistoricaldiversificationbenefitwouldhavebeenachievedbyallocatingapproximately30%ofanequityportfoliotonon-U.S.equities(althoughthedifferencebetween30%non-U.S.and40%non-U.S.iswithin0.02%),withanetreductioninvolatilityof71basispoints.Allocating20%ofanequityportfoliotonon-U.S.stockswouldhavecaptured60ofthose71basispoints,orabout85%ofthemaximumpossiblebenefit.Forinvestorsinterestedindeviatingfromtheglobalmarketcap,it’shelpfultounderstandthathistoricallyithasbeenpossibletoobtainsimilardiversificationbenefitswhilemitigatingtheimpact ofhighercostsandsomeofthebehavioralhurdlesoflargerglobalallocations.

Althoughsuchoptimizationcanserveasareferencepoint,asignificantweaknessofthisanalysisisthat itisbackward-lookingandparticularlydependentonthetimeperiodexamined.Forexample,atdifferentobservationdates,the“optimal”allocationtonon-U.Sstockshasbeenaslowas20%orashighas70%.Asrecentlyasyear-end2005,thebottomofthe“U”patterninFigure3fellbetween40%and50%;throughbothyear-end2008andyear-end2013,however,thecurveclearlybottomedoutbetween30%and40%.Andevenmorerecentlyovershortertimeperiods,wehaveseennon-U.S.stocksfailtoreducethevolatilityofaportfolioat anyallocation.Further,whenevaluatingportfoliosdiversifiedacrossmultipleassetclasses,theresults

mayalsochange.Forexample,theminimum-volatilityportfolioinFigure3,givena40%allocationtobonds,hasdifferedfromanequity-onlyallocation.Thisisthereasonwedonotfocussolelyonsuchoptimizationtechniquestoformportfolios,butinsteadcombineanevaluationoftheinvestmenttrade-offswithfactorssuchascostandbehavioralrealities.

Qualitative considerations

Real-worldconsiderationsmayfurthersupport alowerallocationtonon-U.S.equitiesthanthatrecommendedbymarketproportions.Broadly, suchconsiderationsinvolvebarrierstoinvestment,suchaslimitationsontherepatriationofinvestmentincomeandhighertransactionandfrictioncosts (forinstance,commissions,opportunitycosts, andmarket-impactcosts).

Althoughbarrierstocross-borderinvestment havebeenfallingovertime,transactionandinvestmentcostsgenerallyremainproportionallyhigherinforeignmarketsthanintheUnitedStates.Thisisprimarilyaresultofliquiditydifferencesandrelativelylowermarketparticipation.Forexample,bid-askspreadstendtobewider,andmanagementfeesandfrictioncoststendtobehigher,for foreignmarkets.

Finally,ourempiricalanalysisreliesonmonthlyreturndatafordevelopedmarketsthatextendbacktoonly1970anddataforemergingmarketsthatextendto1985.Alongertimeseriesofreturns, ifitexisted,mightprovidemorerobustempiricalresultsbecauseitwouldspanmorefinancial,economic,andpoliticalcycles.However,investorsmightalsoconsidermorerecentexperiencestobemorerepresentativeofthefutureasglobalmarketsbecomemoreintegratedandinformationflowsmoreseamlessly.Wediscusstheimplicationsofsuchaviewinthenextseveralsections.

7

Ever-changing impact of global diversification

AlthoughFigure3showstheimpactofdiversificationovertheentire1970–2013period,fewinvestorsactuallyrealizesuchanextendedtimehorizonwithoutmakingchangestotheirportfolios.Therefore,itmakessensetoevaluatethediversificationimpact ofcombiningU.S.andnon-U.S.equitiesovershortertimewindows.Figure 4showstheproportionofthemaximumpossiblediversificationbenefitachieved atvariousallocationstonon-U.S.stocksoverrollingten-yearwindows.Forexample,overthetenyearsendedDecember1979,a10%allocationtonon-U.S.equitieswouldhaveprovided39%ofthemaximumpossiblediversificationbenefit.A30%allocationtointernationalequitieswouldhaveprovided90%ofthemaximumdiversificationbenefit.

However,it’simportanttonotehowtheimpactofdiversificationcanchangeovertimeasthereturns,volatilities,andcorrelationsbetweenU.S.andnon-

U.S.stockschange.Forexample, Figure4showsthatduringseveralperiods,oneormoreofthelinesbumpupagainstthetopofthechart—atthe100%limit.Overtheseperiods,investorswouldhave beenbetteroffholdingalowerallocationtonon-U.S.stocks(assumingloweraveragevolatilitywastheirprimarymotivationforholdingnon-U.S.equities). Forinstance,forthetenyearsendedDecember31,1997,a20%allocationwouldhaveprovidedthemaximumdiversificationbenefit,meaningthoseinvestorswhoheldallocationsgreaterthan20%wouldhavefoundthemselvesonthebacksideof theUpatterninFigure3—withastillloweraveragevolatilitythanaportfolioof100%U.S.equities,butwithgreatervolatilitythanthatofaportfoliowitha20%allocationtonon-U.S.equities.Ontheotherhand,a40%allocationwouldhaveprovidedaround90%ofthemaximumvolatilityreductionfortheten-yearperiodsendedintheearly2000s,buta60%allocationwouldhavebeenrequiredtoreapthemaximumvolatilityreduction.

Figure 4.

Proportion of maximum volatility reduction achieved by including non-U.S. stocks

On average, dedicating 30% of equities to non-U.S. stocks has provided most of the maximum possible diversification benefit

Notes: U.S. equities represented by MSCI USA Index; non-U.S. equities represented by MSCI World Index ex USA from 1970 through 1987 and MSCI All Country World Index ex USA thereafter. Data through December 31, 2013.

Sources: Vanguard, Thomson Reuters Datastream, and MSCI.

10% international

20% international

30% international

40% international

Tota

l per

cent

age

ofm

axim

um v

olat

ility

red

uctio

n

0

20

40

60

80

100% Since the ten yearsended 10/31/2008, any allocation to non-U.S. stocks has increased average volatility.

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 20132010

Ten years ended December 31:

2 That said, international equity correlations should remain less than perfect. Consider, for instance, that several studies (e.g., Stock and Watson, 2003) have found minimal evidence of increased international synchronization of business cycles, despite increases in international trade flows, developed-market integration, and the introduction of the euro.

8

Althoughtherehasbeensignificantdisparityin theincrementalbenefitdeliveredbyallocationstonon-U.S.stocksovertime,Figure4showsthat,onaverage,a20%allocationofadomesticportfoliotonon-U.S.equitieshasprovided70%ofthemaximumdiversificationbenefit.Aninvestorwhoallocated30%tonon-U.S.equitieshasaveraged90%ofthemaximumdiversificationbenefitacrossallperiods.Theseresultsindicatethatinvestorscanbenefitsubstantiallyfromexposuretonon-U.S.equitieswhileremainingsensitivetothepotentiallyhighercostsandrisksofaportfoliowhoseallocationsarebasedonglobalmarketcapitalizationacrossmanydifferenttimeperiods.

Finally,it’simportanttonotethatinrecentperiodsdiversifyingintonon-U.S.stockshasnotreducedvolatilityinanequityportfolio.Weillustratethis ontherightportionofFigure4,whereeventhe 10%allocationlinemergeswiththetopofthe chart.Infact,sincethetenyearsendedOctober31, 2008,investorswouldhaverealizedlowervolatilitybybeinginvestedsolelyinU.S.stocks.Ofcourse,becauseFigure4onlyaccountsforvolatilityimpact,returndifferentialsarenotevaluated,whichisanotherpotentialmotivationfordiversification andsomethingweaddressinalatersection.

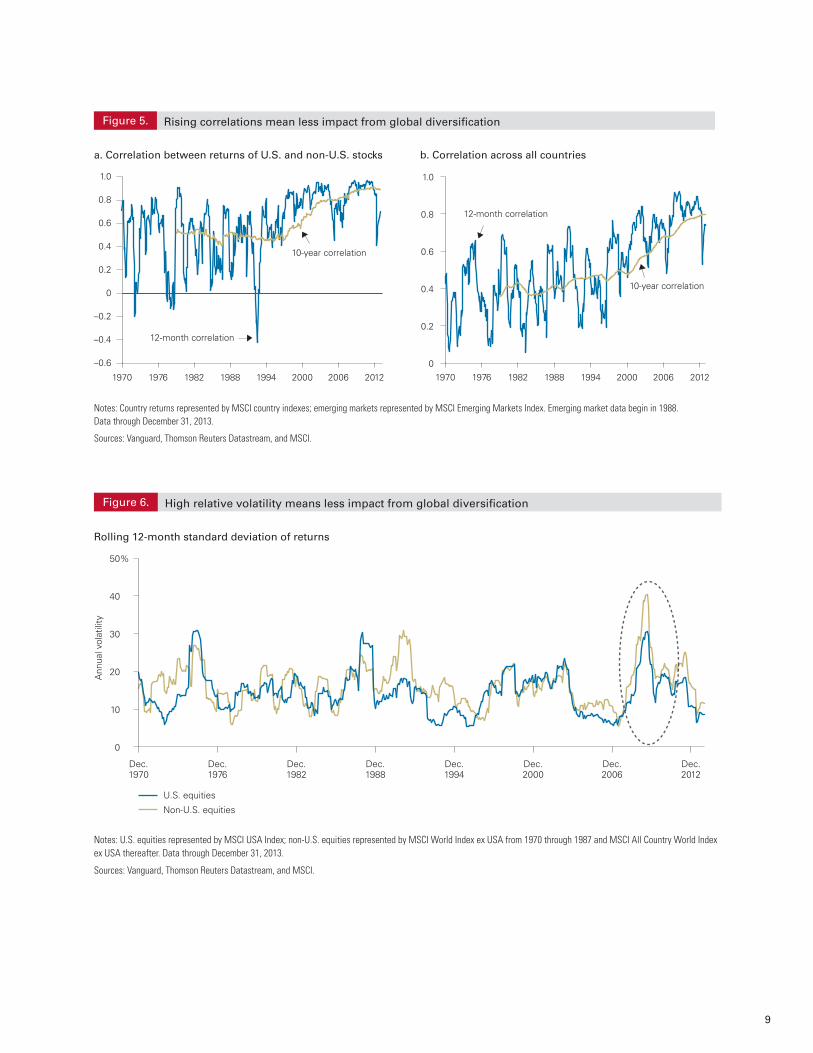

Challenges facing investors today

Therearetwoprimarydriversofthisrecentdivergencefromlong-termhistory.Thefirstdriverhasbeenhigheraveragecorrelationsacrossglobalequitymarkets.Figure 5ashowsthatthecorrelationbetweenU.S.andnon-U.S.stockshasincreasedovertime,andnotablysosincethemid-1990s.Infact,althoughlonger-termcorrelationswerestablethroughthe1980sandearly1990s,recentyearshaveshownasignificantrise.Onefactorfortheincreasedcorrelationhasbeenthesteadydecline intheimportanceofthePacificregionsince1989.Historically,EuropeanmarketshavebeenmorecloselycorrelatedtoU.S.marketsthanPacificmarketshavebeentoU.S.markets.Inother words,Pacificmarkets,andespeciallyJapan,

havehistoricallybeenasignificantsourceofdiversificationforglobalportfolios.But,sincethe1980s,Europe’smarketcapitalizationhasdoubled, attheexpenseofthePacificregion.Asaresult, thestrongdiversifyingeffectofthePacificregionhasdiminished.

Inaddition,individualmarketsacrosstheworldhavebecomemoresynchronized.AsshowninFigure 5b,correlationsacrossindividualcountrieshavealsoincreasedsignificantly,fromapproximately0.35inthe1980sto0.77asof2013.Whetherthesetrendswillcontinueisopenfordebate;however,itisnotunreasonabletoanticipatethatthefuturecorrelationbetweennon-U.S.andU.S.equitieswillmorecloselyresemblethatoftherecentpast,ratherthanthe1970sand1980s,particularlygiventhatcorrelationtrendsareslowtoshift.2

Theseconddriverforthereversalindiversificationbenefitswasasignificantspikeinrelativevolatilityfornon-U.S.stockssince2007.Figure 6showsthetrailing12-monthstandarddeviationofreturnsforbothU.S.andnon-U.S.stocks.ItisnotablethatthespikeinvolatilityfromSeptember2007through2011actuallyincreasedthelong-termaveragevolatilityofnon-U.S.marketsbynearlyafullpercentagepoint,from16.47%to17.27%.Thehighervolatility,combinedwithrisingcorrelations,servedtomutetheimpactofagloballydiversifiedportfolio.Itisinterestingthattherehavebeenpriorperiodsinwhichnon-U.S.stockshaveexperiencedsignificantlyhighervolatilitythanU.S.stocks—forexample,1990–91and1972–74.However,thekeydifferenceinthoseperiodswasthatcorrelationsacrossglobalmarketswerelowerthantheyhavebeenrecently.Ofcourse,despiteperiodicspikesinrelativevolatility,moreoftenthannot,U.S.andnon-U.S.stockshaveexperiencedsimilarvolatility.Assuch,wewouldnotexpectthehighrelativevolatilityobservedinrecentperiodstopersistindefinitely. Allelsebeingequal,lowerrelativevolatilityfor non-U.S.stockswouldincreasethediversificationbenefitsofglobalequityallocations.

9

a. Correlation between returns of U.S. and non-U.S. stocks

Figure 5.

b. Correlation across all countries

Rising correlations mean less impact from global diversification

Notes: Country returns represented by MSCI country indexes; emerging markets represented by MSCI Emerging Markets Index. Emerging market data begin in 1988. Data through December 31, 2013.

Sources: Vanguard, Thomson Reuters Datastream, and MSCI.

–0.6

–0.4

–0.2

0

0.2

0.4

0.6

0.8

1.0

1970 1976 1982 1988 1994 2000 2006 2012

12-month correlation

10-year correlation

0

0.2

0.4

0.6

0.8

1.0

1970 1976 1982 1988 1994 2000 2006 2012

12-month correlation

10-year correlation

12-month correlation

10-year correlation

12-month correlation

10-year correlation

Figure 6.

Rolling 12-month standard deviation of returns

High relative volatility means less impact from global diversi�cation

Notes: U.S. equities represented by MSCI USA Index; non-U.S. equities represented by MSCI World Index ex USA from 1970 through 1987 and MSCI All Country World Index ex USA thereafter. Data through December 31, 2013.

Sources: Vanguard, Thomson Reuters Datastream, and MSCI.

0

10

20

30

40

50%

Ann

ual v

olat

ility

U.S. equities

Non-U.S. equities

Dec.1970

Dec.1976

Dec.1988

Dec.1994

Dec.2000

Dec.2006

Dec.2012

Dec.1982

10

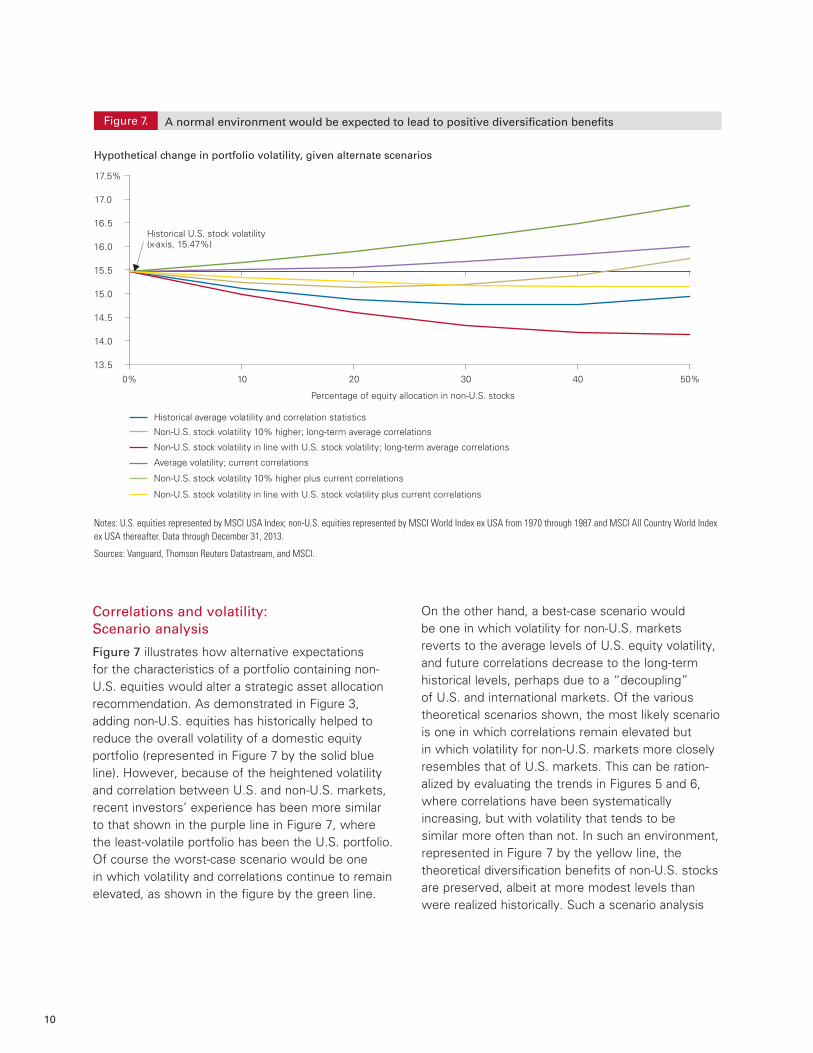

Correlations and volatility: Scenario analysis

Figure 7illustrateshowalternativeexpectations forthecharacteristicsofaportfoliocontainingnon-U.S.equitieswouldalterastrategicassetallocationrecommendation.AsdemonstratedinFigure3,addingnon-U.S.equitieshashistoricallyhelpedtoreducetheoverallvolatilityofadomesticequityportfolio(representedinFigure7bythesolidblueline).However,becauseoftheheightenedvolatilityandcorrelationbetweenU.S.andnon-U.S.markets,recentinvestors’experiencehasbeenmoresimilartothatshowninthepurplelineinFigure7,wheretheleast-volatileportfoliohasbeentheU.S.portfolio.Ofcoursetheworst-casescenariowouldbeone inwhichvolatilityandcorrelationscontinuetoremainelevated,asshowninthefigurebythegreenline.

Ontheotherhand,abest-casescenariowould beoneinwhichvolatilityfornon-U.S.marketsrevertstotheaveragelevelsofU.S.equityvolatility,andfuturecorrelationsdecreasetothelong-termhistoricallevels,perhapsduetoa“decoupling” ofU.S.andinternationalmarkets.Ofthevarioustheoreticalscenariosshown,themostlikelyscenarioisoneinwhichcorrelationsremainelevatedbut inwhichvolatilityfornon-U.S.marketsmorecloselyresemblesthatofU.S.markets.Thiscanberation-alizedbyevaluatingthetrendsinFigures5and6,wherecorrelationshavebeensystematicallyincreasing,butwithvolatilitythattendstobe similarmoreoftenthannot.Insuchanenvironment,representedinFigure7bytheyellowline,thetheoreticaldiversificationbenefitsofnon-U.S.stocksarepreserved,albeitatmoremodestlevelsthanwererealizedhistorically.Suchascenarioanalysis

Figure 7.

Hypothetical change in portfolio volatility, given alternate scenarios

A normal environment would be expected to lead to positive diversification benefits

Notes: U.S. equities represented by MSCI USA Index; non-U.S. equities represented by MSCI World Index ex USA from 1970 through 1987 and MSCI All Country World Index ex USA thereafter. Data through December 31, 2013.

Sources: Vanguard, Thomson Reuters Datastream, and MSCI.

13.5

14.0

14.5

15.0

15.5

16.0

16.5

17.0

17.5%

0% 10 20 30 40 50%

Percentage of equity allocation in non-U.S. stocks

Historical average volatility and correlation statistics

Non-U.S. stock volatility 10% higher; long-term average correlations

Non-U.S. stock volatility in line with U.S. stock volatility; long-term average correlations

Average volatility; current correlations

Non-U.S. stock volatility 10% higher plus current correlations

Non-U.S. stock volatility in line with U.S. stock volatility plus current correlations

Historical U.S. stock volatility(x-axis, 15.47%)

11

canhelpinvestorsquantifyfutureexpectations andassessthepotentialimpactthatarangeofallocationstointernationalequitieswouldhave ontheirportfolios.Foradditionalperspectiveoncorrelationsduringrecessions,seeDavisand Aliaga-Díaz(2009).

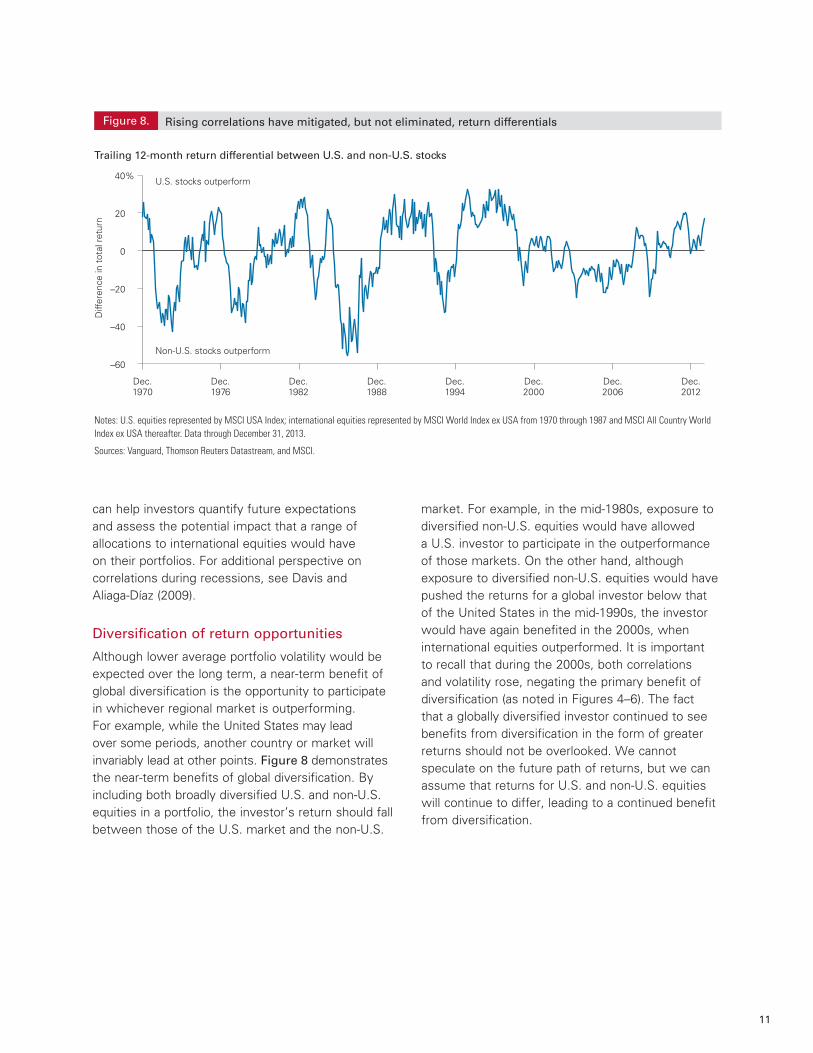

Diversification of return opportunities

Althoughloweraverageportfoliovolatilitywouldbeexpectedoverthelongterm,anear-termbenefitofglobaldiversificationistheopportunitytoparticipateinwhicheverregionalmarketisoutperforming. Forexample,whiletheUnitedStatesmaylead oversomeperiods,anothercountryormarketwillinvariablyleadatotherpoints.Figure 8 demonstratesthenear-termbenefitsofglobaldiversification.ByincludingbothbroadlydiversifiedU.S.andnon-U.S.equitiesinaportfolio,theinvestor’sreturnshouldfallbetweenthoseoftheU.S.marketandthenon-U.S.

market.Forexample,inthemid-1980s,exposuretodiversifiednon-U.S.equitieswouldhaveallowed aU.S.investortoparticipateintheoutperformanceofthosemarkets.Ontheotherhand,althoughexposuretodiversifiednon-U.S.equitieswouldhavepushedthereturnsforaglobalinvestorbelowthatoftheUnitedStatesinthemid-1990s,theinvestorwouldhaveagainbenefitedinthe2000s,wheninternationalequitiesoutperformed.Itisimportant torecallthatduringthe2000s,bothcorrelations andvolatilityrose,negatingtheprimarybenefitofdiversification(asnotedinFigures4–6).Thefact thatagloballydiversifiedinvestorcontinuedtoseebenefitsfromdiversificationintheformofgreaterreturnsshouldnotbeoverlooked.Wecannotspeculateonthefuturepathofreturns,butwecanassumethatreturnsforU.S.andnon-U.S.equitieswillcontinuetodiffer,leadingtoacontinuedbenefitfromdiversification.

Figure 8.

Trailing 12-month return differential between U.S. and non-U.S. stocks

Rising correlations have mitigated, but not eliminated, return differentials

Notes: U.S. equities represented by MSCI USA Index; international equities represented by MSCI World Index ex USA from 1970 through 1987 and MSCI All Country World Index ex USA thereafter. Data through December 31, 2013.

Sources: Vanguard, Thomson Reuters Datastream, and MSCI.

Diff

eren

ce in

tot

al r

etur

n

–60

–40

–20

0

20

40% U.S. stocks outperform

Non-U.S. stocks outperform

Dec.1970

Dec.1976

Dec.1988

Dec.1994

Dec.2000

Dec.2006

Dec.2012

Dec.1982

12

Impact of currency exposure

Investmentsinforeignmarketsareexposedtofluctuationsinforeignexchangerates.Figure 9 illustratesthatcurrencyfluctuationshaveperiodicallyaddedtoorsubtractedfromthereturnforU.S.investorsofinternationalinvestments.Forexample,currencymovementssubtracted17%fromthe12-monthreturnsofinternationalstocksin1984 andthenadded35%in1986.3

Althoughcurrencymovementstendtobeunpredictableandcanbelarge,theyhavehistoricallybeenuncorrelatedtomovementsinstockprices.4 Asaresult,overtime,currencymovementshavehelpedtoreducethecorrelationbetweennon-U.S.

equitiesandU.S.equities,thuscontributingto thediversificationbenefitsofforeignholdings. Forexample,since1970,thecorrelationofforeignstocksdenominatedintheirlocalcurrencyto U.S.stockswas0.71,higherthanthecorrelation offoreignstocksdenominatedinU.S.dollarsto U.S.stocks(0.64).However,currencymovementsalsoincreasedthevolatilityofnon-U.S.equitiesbyapproximately2.7percentagepointsfrom1970through2013(from14.6%to17.3%).Allelsebeingequal,wewouldexpectcurrencytocontinueto beadiversifierfornon-U.S.investmentsfrom thestandpointthatcurrencymovementsdirectlyinfluencethereturndifferentialsshowninFigure8,alongwiththecorrelationpropertiesamongcountries.

3 The theory of purchasing-power parity states that real returns will be the same across countries, as exchange-rate movements and inflation differentials should be identical. Interest rate parity is based on the notion that the interest rate differential between the home and foreign markets will determine the change in the exchange rate. There is considerable empirical support for these theories in the long run, but substantial research documents significant departures from a currency’s “fair value” in the short run.

4 Of course, although this statement is generally true, there are cases in which commodity-based economies such as those of Australia and Canada have had a positive correlation with foreign stock prices—see, for example, LaBarge (2010).

Figure 9.

Annualized contribution of U.S. dollar to non-U.S. equity returns

Exposure to currency can further affect return differentials

Cur

renc

y re

turn

Notes: Contribution of the U.S. dollar calculated by subtracting the returns of non-U.S. stocks denominated in local currency from the returns of non-U.S. stocks denominated in U.S. dollars. Non-U.S. equities represented by MSCI World Index ex USA from 1970 through 1987 and MSCI All Country World Index ex USA thereafter. Data through December 31, 2013.

Sources: Vanguard, Thomson Reuters Datastream, and MSCI.

–20

–10

0

10

20

30

40%

Dec.1970

Dec.1976

Dec.1988

Dec.1994

Dec.2000

Dec.2006

Dec.2012

Dec.1982

13

Role of emerging markets

Emergingmarketsareeconomiesormarketsthatarejustenteringtheglobalarenaordonotmeetcriteriatobeconsidereddevelopedeconomies. Forexample,theWorldBankclassifiesemergingmarketsaseconomiesbelowtheupper-middle-incomethreshold.5MSCI,FTSE,andotherbenchmarkprovidersmayconsideradditional criteriasuchasthematurityoffinancialmarkets, thestructureoftransactionsettlement,andthefreedomofcapital,amongothers.Manycountries(amongthebetter-knownonesareChina,India,Brazil,andRussia)maymeetoneormoreofthesecriteriabutnotall.Thosethatsuccessfullydevelopeconomically,politically,andfinancially(suchastheUnitedStatesfromthe1800sthroughthe1900s)wouldbeexpectedtoenjoystronglong-termreturns.However,thosethatdonotdevelopmayseetheirfinancialmarketslanguish.

Becauseofhighlyspecializedpolitical,economic, andfinancialrisks,investinginindividualemerging-marketcountriescanbeextremelyrisky.However,becauseindividualemergingmarketsarerelativelyuncorrelatedamongeachother,theriskofinvestingacrossallcountriesismuchless.Inaddition,theuniquedevelopmentpatternsoftheseemergingmarketshelpthemtodiversifythereturnsofdevelopedinternationalmarketsandU.S.markets—correlationsbetweendevelopedmarketsandemergingmarketshaveaveraged0.66since1985.Andemergingmarketshavedeliveredhigheraveragereturns—withcommensuratelyhighervolatility—thanthoseofdevelopedmarkets.From1985through2013,emergingmarketsproduced anaverageannualreturnof12.7%withanaveragevolatilityof24.0%,versusaverageannualreturns fordevelopedmarketsoverthesameperiodof 9.9%withanaveragevolatilityof17.6%.This overallpatternofrelativeperformancemighthavebeenexpected,giventheoverallcharacteristicsof

emergingeconomiesormarkets.Thecombination ofhigherexpectedreturns,higherexpectedvolatility,andmoderatecorrelationsbetweenemerginganddevelopedmarketssuggeststhatamodestallocationtoemergingmarketsiswarranted.Formostinvestors,amarket-weightedallocationviaafund orexchange-tradedfundthatisinvestedacross allnon-U.S.marketsisthebestwaytoincludeemergingmarketsinadiversifiedportfolio.Such anallocationwouldensureconstantinvestmentatthemarketweighting,andwouldhelptoinsulateinvestorsfromemergingmarkets’potentiallysevereswingsinperformance.

Conclusion

Inlightofquantitativeanalysisandqualitativeconsiderations,wehavedemonstratedthat domesticinvestorsshouldconsiderallocating partoftheirportfoliostointernationalsecurities, andthata20%allocationmaybeareasonablestartingpoint.Althoughfinancetheorydictates thatanupperassetallocationlimitshouldbebasedontheglobalmarketcapitalizationforinternationalequities(currentlyapproximately51%),wehavedemonstratedthatinternationalallocationsexceeding40%havenothistoricallyaddedsignificantadditionaldiversificationbenefits,particularlyaccountingforcosts.Formanyinvestors,anallocationbetween20%and40%shouldbeconsideredreasonable,giventhehistoricalbenefitsofdiversification.Allocationscloserto40%maybesuitablefor thoseinvestorsseekingtobeclosertoamarket-proportionalweightingorforthosewhoarehopingtoobtainpotentiallygreaterdiversificationbenefitsandarelessconcernedwiththepotentialrisksandhighercosts.Ontheotherhand,allocationscloser to20%maybeviewedasofferingagreaterbalanceamongthebenefitsofdiversification,therisksofcurrencyvolatilityandhigherU.S.tonon-U.S.stockcorrelations,investorpreferences,andcosts.

5 Countries are ranked by the World Bank each July and divided into four income groups (based on gross national income per capita). The groups are: low income, $1,005 or less; lower middle income, $1,006–$3,975; upper middle income, $3,976–$12,275; and high income, $12,276 or more.

14

References

Davis,JosephH.,andRogerAliaga-Díaz,2009. The Global Recession and International Investing. ValleyForge,Pa.:TheVanguardGroup.

LaBarge,KarinPeterson,2010.Currency Management: Considerations for the Equity Hedging Decision.ValleyForge,Pa.: TheVanguardGroup.

Philips,ChristopherB.,FrancisM.KinniryJr.,andScottJ.Donaldson,2012.The Role of Home Bias in Global Asset Allocation Decisions.ValleyForge,Pa.:TheVanguardGroup.

Stock,JamesH.,andMarkW.Watson,2003.Understanding Changes in International Business Cycle Dynamics.NBERWorkingPaperNo.9859.Cambridge,Mass.:NationalBureauofEconomicResearch.

Vanguard research > Vanguard Center for Retirement Research Vanguard Investment Strategy Group

E-mail > [email protected]

For more information about Vanguard funds, visit vanguard.com, or call 800-662-2739, to obtain a prospectus. Investment objectives, risks, charges, expenses, and other important information about a fund are contained in the prospectus; read and consider it carefully before investing.

CFA® is a trademark owned by CFA Institute.

P.O.Box2600 ValleyForge,PA19482-2600

© 2014 The Vanguard Group, Inc. All rights reserved. Vanguard Marketing Corporation, Distributor.

ISGGEB 022014

Connect with Vanguard® > vanguard.com

Related Documents