Global Development Finance 2007 The Globalization of Corporate Finance in Developing Countries May, 2007 T H E W O R L D B A N K

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Global Development Finance 2007

The Globalization of Corporate Finance in Developing Countries

May, 2007T H E W O R L D B A N K

Key Messages

Slowdown in global growth is likely to reverse the benign financial conditions facing developing countries

Private capital flows have continued to expand in 2006, but many low-income countries depend on development assistance

Developing countries gain from financial globalization of the corporate sector

A soft landing is expected; yet downside risks remain

Outlook for the global economy

The U.S. slowdown is only having a limited effect on European and developing country growth

Outlook for the global economy

The U.S. slowdown is only having a limited effect on European and developing country growth

Low long-term interest rates favor a soft landing led by robust developing country growth

Outlook for the global economy

The U.S. slowdown is only having a limited effect on European and developing country growth

Low long-term interest rates favor a soft landing led by robust developing country growth

Slower growth will help reduce global imbalances and inflationary pressures

Outlook for the global economy

The U.S. slowdown is only having a limited effect on European and developing country growth

Low long-term interest rates favor a soft landing led by robust developing country growth

Slower growth will help reduce global imbalances and inflationary pressures

But downside risks (U.S. recession, revaluation of risk, overheating) mean a more abrupt slowdown is possible.

A sharp decline in the U.S. housing sector

-25

-20

-15

-10

-5

0

5

10

15

20

25

1999Q1 2000Q1 2001Q1 2002Q1 2003Q1 2004Q1 2005Q1 2006Q1 2007Q1

Quarterly growth of residential investments in constant prices (saar)

Source: World Bank

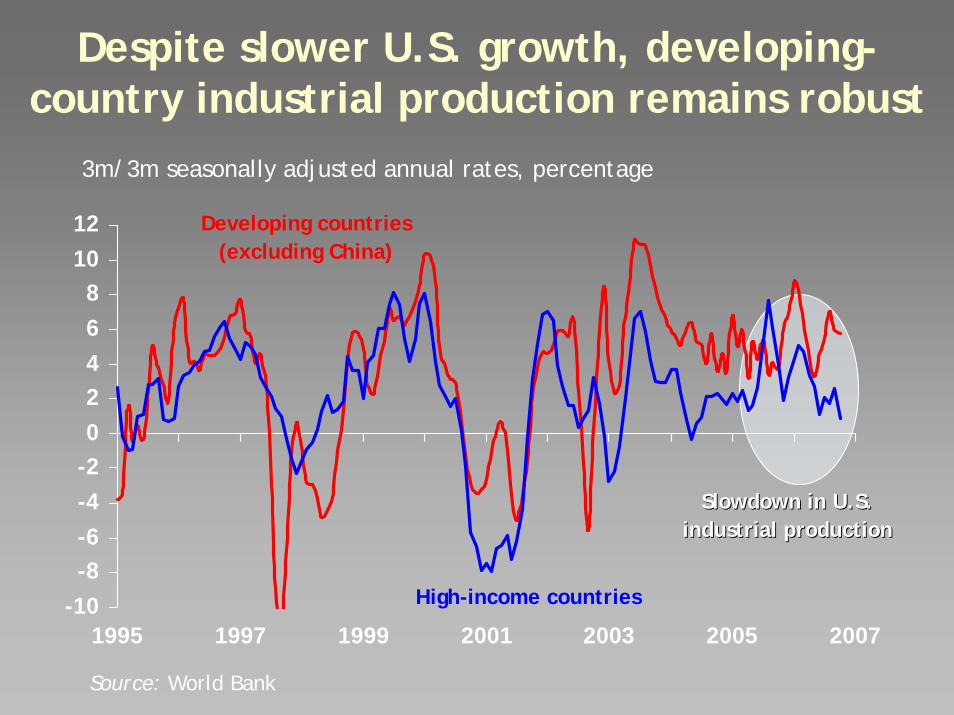

Despite slower U.S. growth, developing-country industrial production remains robust

-10-8-6-4-202468

1012

1995 1997 1999 2001 2003 2005 2007

Source: World Bank

High-income countries

Slowdown in U.S.Slowdown in U.S.industrial productionindustrial production

3m/3m seasonally adjusted annual rates, percentage

-10-8-6-4-202468

1012

1995 1997 1999 2001 2003 2005 2007

Source: World Bank

High-income countries

Developing countries(excluding China)

Slowdown in U.S.Slowdown in U.S.industrial productionindustrial production

3m/3m seasonally adjusted annual rates, percentage

Despite slower U.S. growth, developing-country industrial production remains robust

-10-8-6-4-202468

1012

1995 1997 1999 2001 2003 2005 2007

Source: World Bank

High-income countries

Developing countries(excluding China)

Developing countryDeveloping countryoutput stable oroutput stable or

acceleratingaccelerating

Despite slower U.S. growth, developing-country industrial production remains robust

3m/3m seasonally adjusted annual rates, percentage

Outlook for the global economy

The U.S. slowdown is only having a limited effect on European and developing country growth

Low long-term interest rates favor a soft landing led by robust developing country growth

Slower growth will help reduce global imbalances and inflationary pressures

But downside risks (U.S. recession, revaluation of risk, overheating) mean a more abrupt slowdown is possible.

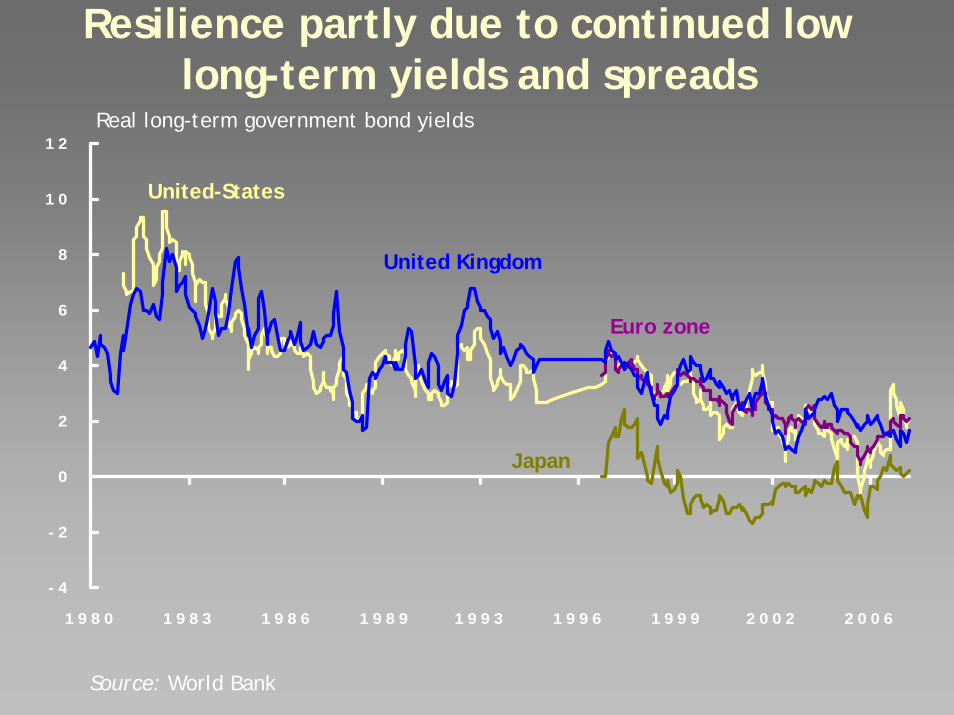

Resilience partly due to continued low long-term yields and spreads

- 4

- 2

0

2

4

6

8

1 0

1 2

1 9 8 0 1 9 8 3 1 9 8 6 1 9 8 9 1 9 9 3 1 9 9 6 1 9 9 9 2 0 0 2 2 0 0 6

United-States

United Kingdom

Source: World Bank

Japan

Euro zone

Real long-term government bond yields

-1

1

2

3

4

5

6

7

8

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

Forecast

Developing

2009

Weaker but still robust prospects

Real GDP annual percent change

Source: World Bank

-1

1

2

3

4

5

6

7

8

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

Forecast

Developing

2009

Developing ex. China & India

Weaker but still robust prospects

Real GDP annual percent change

Source: World Bank

-1

1

2

3

4

5

6

7

8

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

Forecast

Developing

High-income

2009

Developing ex. China & India

Weaker but still robust prospects

Real GDP annual percent change

Source: World Bank

Regional Growth Trends

2

3

4

5

6

7

8

9

10

East-Asia &Pacific

Europe &Central Asia

Latin America& Caribbean

Middle-East &North Africa

South Asia Sub-SaharanAfrica

20052006200720082009

Percent change in GDP

Source: World Bank

Some Africa Specific slides

-2

-1

1

2

3

4

5

6

7

8

1981 1984 1987 1990 1993 1996 1999 2002 2005 2008

Forecast

The acceleration in Africa reflects a decade long trend…

Real GDP annual percent change

Source: World Bank.

..that has been broadly-based

0

5

10

15

20

25

1980s 1990s 2000-06

Number of African countries

Note: Poor performers are countries with a per capita GDP decline of 3% or more;

Laggards are countries with a per capita GDP growth between -1% and 1%;

Good performers are countries with a per capita GDP growth between 1% and 3%;

Strong performers are countries with a per capita GDP growth above 3%.

Poor Poor performersperformers

Mediocre Mediocre performersperformers

Good performersGood performers

StrongStrong

performersperformers

Some ECA Specific slides

Rising inflation in a number of countries in the Europe and Central Asia region

0

2

4

6

8

10

Czech

RepArm

enia

Lithuan

iaHunga

ryEsto

niaSlov

ak Rep

Kyrgyz

RepBulgaria

Kazakh

stan

Turkey

2005 2006

CPI, year-over-year percentage change

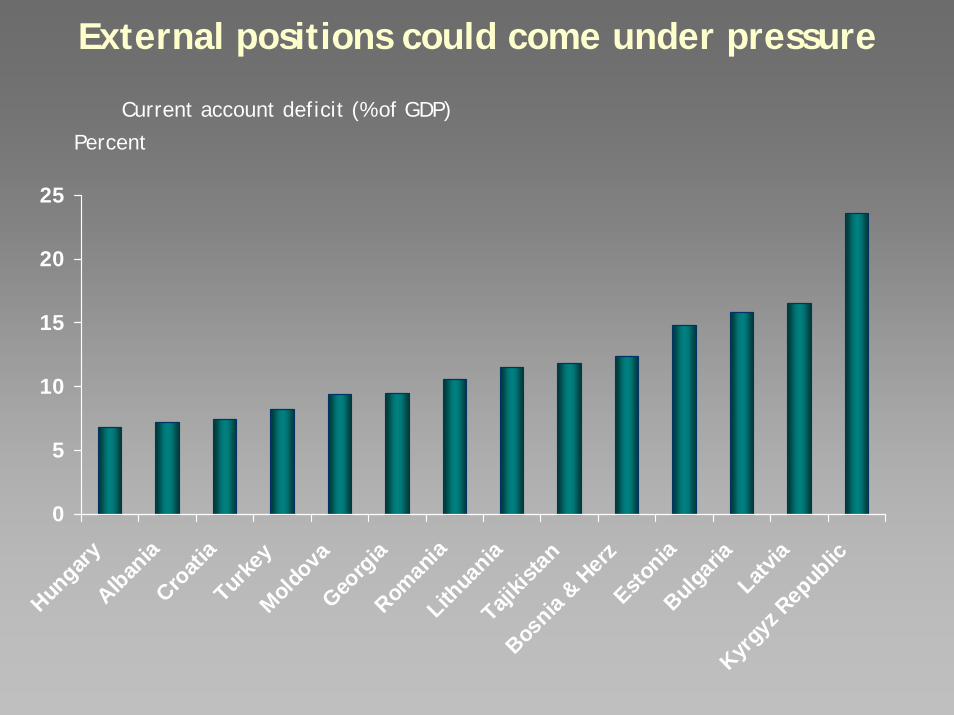

External positions could come under pressure

0

5

10

15

20

25

Hungary

Albania

Croati

aTur

key

Moldova

Georg

iaRom

ania

Lithua

niaTaji

kistan

Bosnia

& Herz

Estonia

Bulgari

aLatv

ia

Kyrgyz

Rep

ublic

Current account deficit (% of GDP)

Percent

External positions could come under pressure

0

510

15

2025

30

3540

45

Kazak

hstan

Hungary

Turke

yLith

uania

Croati

aTaji

kistan

Latvia

Moldova

Estonia

Roman

iaBos

nia & H

erzPercent

Debt servicing charges as a percent of export revenues

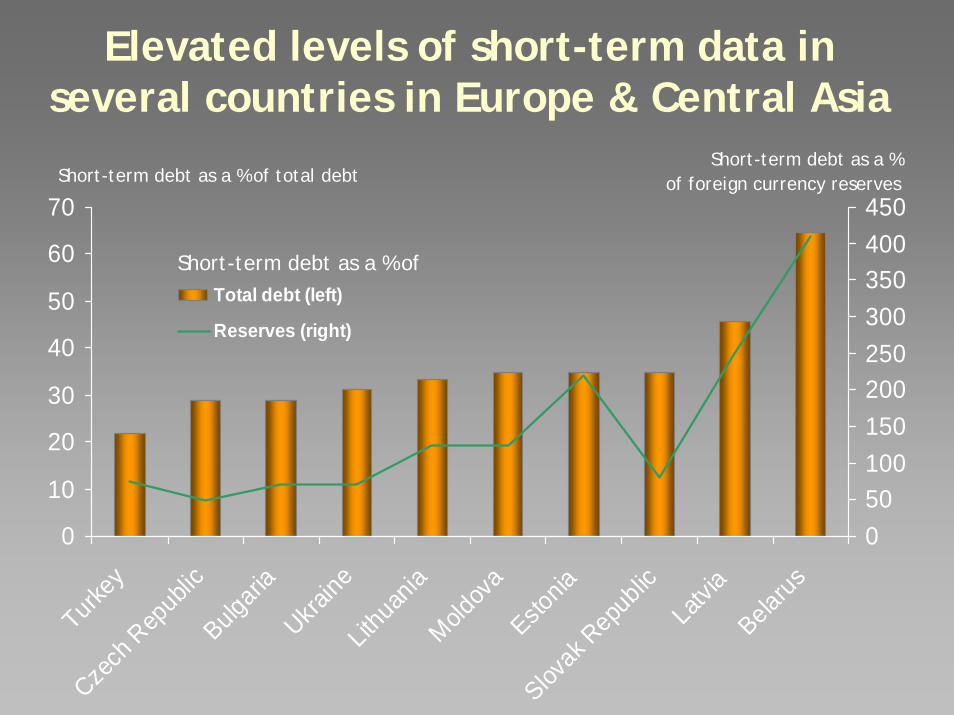

Elevated levels of short-term data in several countries in Europe & Central Asia

0

10

20

30

40

50

60

70

Turkey

Czech

Rep

ublic

Bulgari

aUkra

ineLit

huan

iaMold

ova

Estonia

Slovak

Rep

ublic

Latvi

aBela

rus

050100150200250300350400450

Total debt (left)

Reserves (right)

Short-term debt as a % of total debtShort-term debt as a %

of foreign currency reserves

Short-term debt as a % of

Back to the main presentation

African per capita growth rates approach levels of the 1960s

-2

-1

0

1

2

3

4

5

6

Low-income Middle-income Sub-Saharan Africa

1960

s

1970

s 1980

s

1990

s20

01/6

Average annual per capita income growth

Source: World Bank

Outlook for the global economy

The U.S. slowdown is only having a limited effect on European and developing country growth

Low long-term interest rates favor a soft landing led by robust developing country growth

Slower growth will help reduce global imbalances and inflationary pressures

But downside risks (U.S. recession, revaluation of risk, overheating) mean a more abrupt slowdown is possible.

Core inflation in high-income countries

-2-1.5

-1-0.5

00.5

11.5

22.5

33.5

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07

United Kingdom

United States

Japan

Euro zone

Oil and metal prices have peaked

Index, Jan. 2003 = 100

50

100

150

200

250

300

350

2000M1 2001M1 2002M1 2003M1 2004M1 2005M1 2006M1 2007M1

Metals & minerals

Agricultural products

Energy

Source: World Bank, Datastream

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

2002Q1 2003Q1 2004Q1 2005Q1 2006Q1 2007Q

OtherOPECFSUWorld

Source: International Energy Agency

OPEC as swing producer

Non-OPEC supply is coming on stream

Change in oil deliveries (y/y millions of barrels per day)

U.S. trade balance improving

-7

-6

-5

-4

-3

-2Q4 2001 Q4 2002 Q4 2003 Q4 2004 Q4 2005 Q4 2006

Oil balanceNon-oil balance

Source: U.S. Department of Commerce.

Balance on goods, oil and non-oil (%GDP)

Unwinding global imbalances

Factors favoring an unwindingIncreased U.S. household savingsDecreased U.S. government deficitExpected decline in oil pricesDepreciation of currency increases USD value of external earnings

Factors tending to slow the unwindingLarge gap between value of imports and exportsIncreasing payments on U.S. external debt

A Start to Orderly Adjustment?

Current account balance, Percent World GDP

Source: World Bank

-2

-1.5

-1

-0.5

0

0.5

1

USA Europe Japan Other HIC East Asia &Pacific (ex

China)

China Europe &Central Asia

Otherdevelopingimporters

Oilexporters

Oil importers

2002

2006

2009

Outlook for the global economy

The U.S. slowdown is only having a limited effect on European and developing country growth

Low long-term interest rates favor a soft landing led by robust developing country growth

Slower growth will help reduce global imbalances and inflationary pressures

But downside risks (U.S. recession, revaluation of risk, overheating) mean a more abrupt slowdown is possible.

3

4

5

6

7

8

197

0Q1

197

4Q1

197

8Q1

198

2Q1

198

6Q1

199

0Q1

199

4Q1

199

8Q1

200

2Q1

200

6Q1

Source: World Bank

Further adjustment needed in U.S?

Residential investment (%GDP)

Nominal

Real

Long-term average (nominal)

-1 1 3 5 7 9 11 13 15 17

Burkina FasoChile

MalaysiaMoroccoLithuania

EstoniaBarbados

South AfricaIndia

KazakhstanBotswana

PakistanTurkey

UgandaArgentina

UkraineMauritius

Egypt, ArabParaguay

Kenya

Consumer price inflation, year-over-year percent change

2004 Inflation Inflation end 2006

Source: World Bank

Inflation is up in several developing countries

Financial Flows

Capital flows have continued to expand, but at a slower pace.

Corporate borrowing up strongly in middle-income countries

Official development assistance stagnated

Some countries vulnerable to market correction

$ billions

0

100

200

300

400

500

600

700

1990 1993 1996 1999 2002 2005

0

1

2

3

4

5

6Percent of GDP (right axis)5.8% in 2005-6

Percent

$647 billion in 2006

Net private capital flows to developing countries

Private capital flows have leveled off

More capital is going to East Europe and Central Asia and to East Asia and Pacific regions

Europe & Central Asia

26%

Latin America & Caribbean

47%

East Asia & Pacific

15%

Sub-Saharan Africa

5%South Asia5%Middle East &

North Africa2%

2000 2006

Total net private capital flows to developing countries

Latin America & Caribbean

14%

Middle East & North Africa

4%

South Asia6%

Sub-Saharan Africa

6%

East Asia & Pacific

28%

Europe & Central Asia

42%

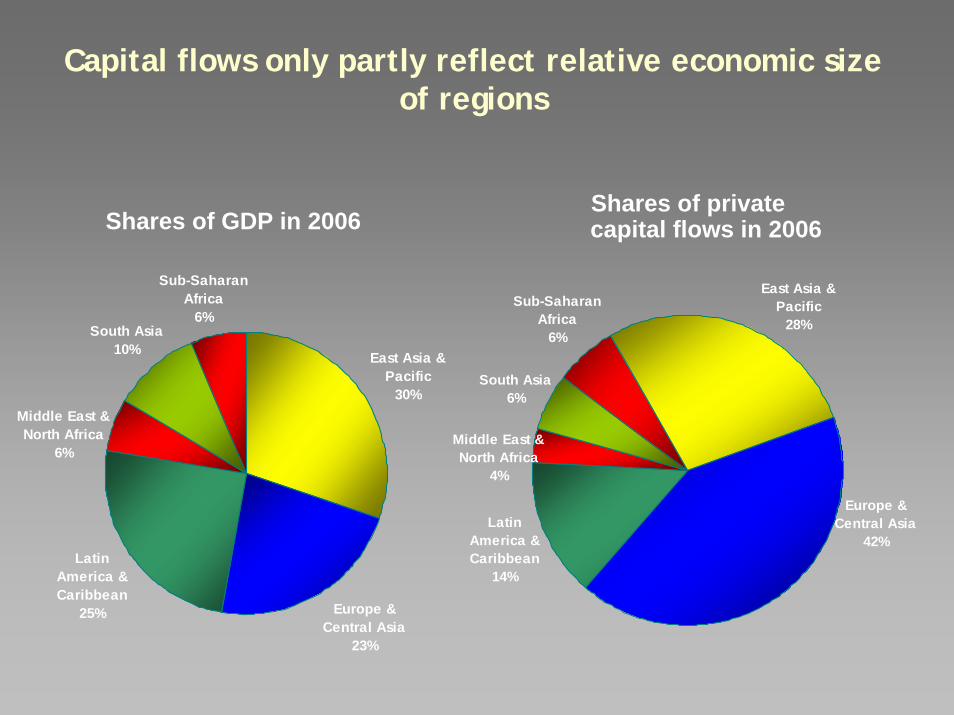

Capital flows only partly reflect relative economic size of regions

Europe & Central Asia

23%

Latin America & Caribbean

25%

East Asia & Pacific

30%

Sub-Saharan Africa

6%South Asia

10%

Middle East & North Africa

6%

Shares of GDP in 2006Shares of private capital flows in 2006

Latin America & Caribbean

14%

Middle East & North Africa

4%

South Asia6%

Sub-Saharan Africa

6%

East Asia & Pacific

28%

Europe & Central Asia

42%

-100

0

100

200

300

400

500

600

700

1990 1992 1994 1996 1998 2000 2002 2004 2006

Debt

Portfolio equity

FDI

$ billions

$234

$94

$325

Net private flows $647 billion in 2006

Equity flows account for the lion share

DebtDebt36 %36 %

EquityEquity64 %64 %

$ billionsNet private debt flows to developing countries

Bank lending dominates the expansion in private debt flows

-100

-50

0

50

100

150

200

250

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Short-term debt flowsBank lendingBond flowsNet private debt flows

0

20

40

60

80

100

1998 1999 2000 2001 2002 2003 2004 2005 2006

$94 billion

$ billions

Portfolio equity flows surged

Net portfolio equity inflows to developing countries

0

15

30

45

60

75

2002 2003 2004 2005 2006

$ billions

OtherCountries

China

$71 billion

Capital raised through Initial Public Offerings (IPOs) by companies in developing countries

Record expansion in IPO transactions led by China

-50

-40

-30

-20

-10

0

10

20

30

2000 2001 2002 2003 2004 2005 2006

World BankIMFParis Club and others

$ billions

Some countries made large repayments to Paris Club creditors and the IMF

Net official flows to developing countries

-$47.7 billion-$25.1 billion

-$2.4 billion

0

2

4

6

8

10

Brazil Mexico Venezuela Peru Others*

$ billions

20

25

30

35

40

1998 1999 2000 2001 2002 2003 2004 2005 2006

Percent

Total value of public external debt buyback operations in 2006

Public external debt as a share of GDP in developing countries

* Including Philippines, Nigeria, Colombia, Panama, and Uruguay

Governments have continued to reduce their external debt…

39% in 1999

23% in 2006

…while increasing their domestic debt

Source: World Bank staff calculations based on JP Morgan

0

10

20

30

40

1998 1999 2000 2001 2002 2003 2004 2005 2006

External DomesticPercent

Public debt as a share of GDP in 28 emerging market economies

Foreign participation in domestic debt market has increased significantly in some countries

Source: World Bank staff estimates.

0

10

20

30

Brazil Malaysia Mexico Indonesia Zambia Poland Hungary

2002 2006

PercentShare of domestic debt held by nonresidents in selected countries

$ billions

0

1

2

3

4

2000 2001 2002 2003 2004 2005 2006

Percent

Migrant remittance flows Migrant remittance flows / GDP

Steady expansion in migrant remittance flows

0

50

100

150

200

2000 2001 2002 2003 2004 2005 2006

Middle-income countriesLow-income countries

Low-income countries

Middle-income countries

$200 billion

Source: World Bank staff estimates.

$ billions $ billions

Middle-income countries Low-income countries

The volume of migrant remittance flows is comparable to aid flows to low-income countries

0

25

50

75

100

125

150

2000 2001 2002 2003 2004 2005 2006

Migrant remittance flowsOfficial development assistance

0

25

50

75

100

125

150

2000 2001 2002 2003 2004 2005 2006

Migrant remittance flowsOfficial development assistance

Source: World Bank staff estimates.

Financial Flows

Capital flows have continued to expand, but at a slower pace.

Corporate borrowing up strongly in middle-income countries

Official development assistance stagnated in 2006

High asset valuation and low risk premiums are a source of vulnerability

Increased internationalization of emerging market firms ..

0

100

200

300

400

500

600

700

800

1990 1993 1996 1999 2002 2005

ServicesManufacturingPrimary

0

10

20

30

40

50

60

70

80

90

100

1990 1993 1996 1999 2002 2005

ServicesManufacturingPrimary

400

250

50

$ billion$ billionNumber of deals

Cross-border M&A transaction by developing countries

Total value of deals

$56

$32

$13

..and closer integration of emerging financial markets

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

36-month rolling correlation of returns

Jan.1995 Jan.1998 Jan.2001 Jan.2004 Jan.2007

Emerging markets/World

Emerging markets/Europe, Australia, Asia

Emerging markets/U.S.

..have driven the globalization of corporate finance

0

50

100

150

200

250

300

350

400

450

1998 1999 2000 2001 2002 2003 2004 2005 2006

Syndicated bank loansBond issues

Equity offerings

$ billion

Oversea capital raised

$245 billion

$88 billion

$68 billion

0

20

40

60

80

100

120

140

1998 1999 2000 2001 2002 2003 2004 2005 2006

Corporate

Sovereign

$ billions

$88 billion

$43 billion

Bond issuance by developing countries

Corporate bond issuance now exceeds sovereign borrowing

0

50

100

150

200

250

300

2002 2003 2004 2005 2006

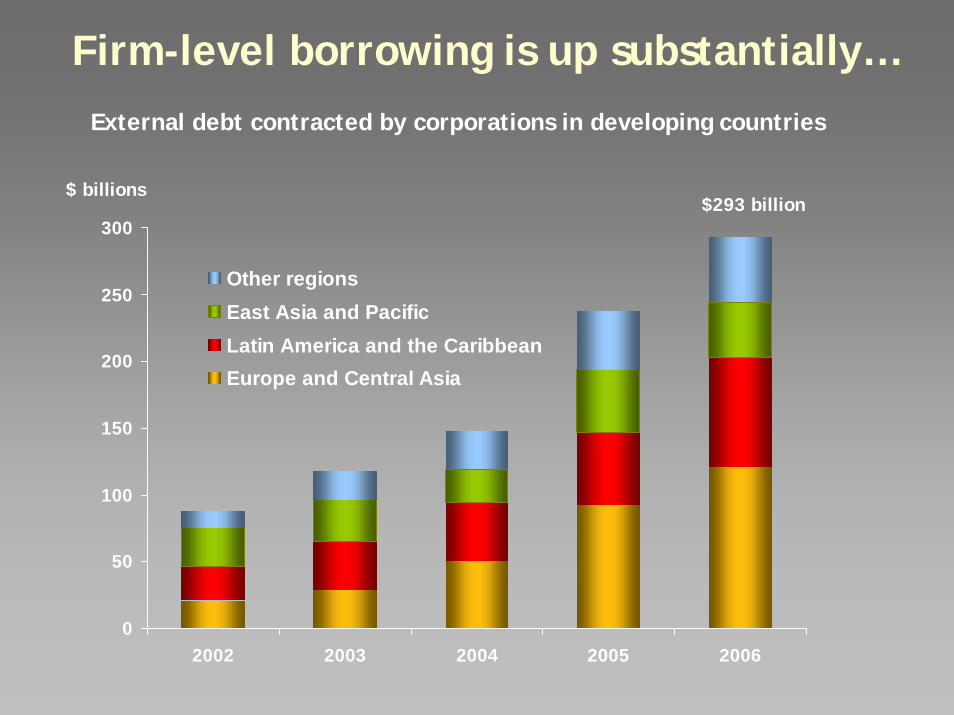

Other regionsEast Asia and PacificLatin America and the CaribbeanEurope and Central Asia

$293 billion

Firm-level borrowing is up substantially…

$ billions

External debt contracted by corporations in developing countries

0

50

100

150

200

250

300

2002 2003 2004 2005 2006

Other sectors

Finance

Oil & Gas

Construction

Telecom

$293 billion

Firm-level borrowing is up substantially…

$ billions

External debt contracted by corporations in developing countries

Financial Flows

Capital flows have continued to expand, but at a slower pace.

Corporate borrowing up strongly in middle-income countries

Official development assistance stagnated in 2006

High asset valuation and low risk premiums are a source of vulnerability

0

20

40

60

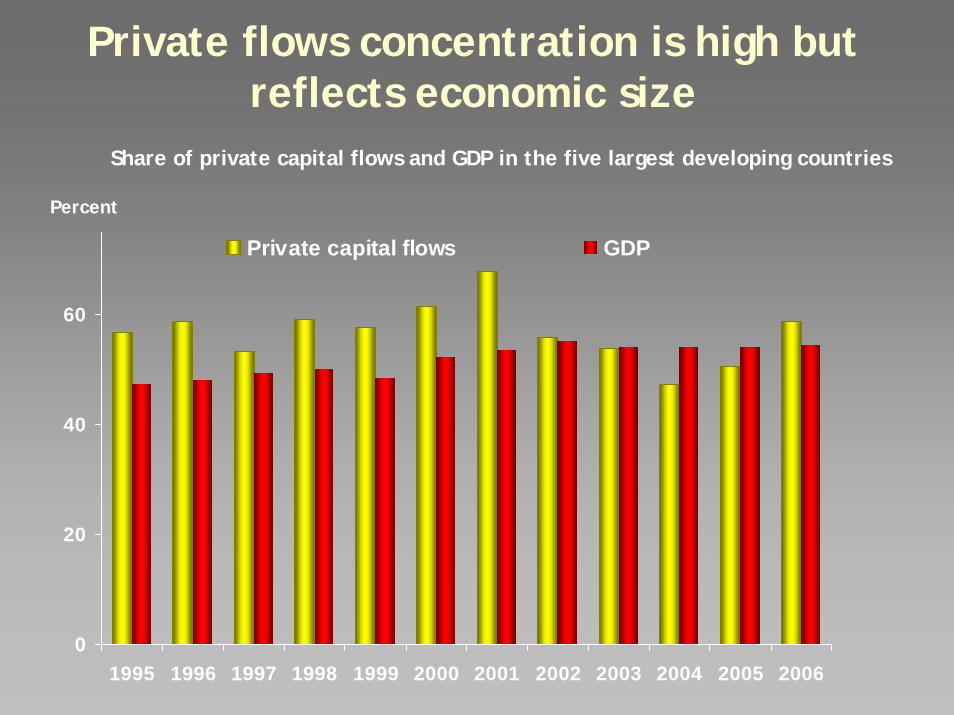

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Private capital flows GDP

Percent

Private flows concentration is high but reflects economic size

Share of private capital flows and GDP in the five largest developing countries

0

25

50

75

100

1990 1992 1994 1996 1998 2000 2002 2004 20060

0.1

0.2

0.3

$ billions Percent

ODA / GNI (right scale)

Source: OECD Development Assistance Committee (DAC)

Official Development Assistance (ODA) stagnated in 2006

ODA less debt relief(left scale)

Debt relief

Net ODA disbursements by DAC donors

0

10

20

30

40

50

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

$ billionsODA allocated to Sub-Saharan Africa in real terms ($2004)

$32 billion in 2005(incl. debt relief)

$24 billion in 2005(excl. debt relief)

$50 billion in 2010(commitment)

Source: World Bank staff calculations based on OECD Development Assistance Committee (DAC).

Donors need to increase aid significantly in order to meet commitments

Financial Flows

Capital flows have continued to expand, but at a slower pace.

Corporate borrowing up strongly in middle-income countries

Official development assistance stagnated in 2006

High asset valuation and low risk premiums are a source of vulnerability

Sharp increase in some emerging market equity prices could be a signal of asset overvaluation

MSCI equity price index (Jan. 2000 = 100)

0

40

80

120

160

200

240

280

320

2000M1 2001M1 2002M1 2003M1 2004M1 2005M1 2006M1 2007M1

EM Europe

Latin America

Global Composite

EM Asia

0 200 400 600 800 1000 1200 1400 1600

MalaysiaChina

Korea, Rep.Thailand

PolandColombia

CroatiaTurkey

PanamaArgentina

PeruMexico

Brazil

Apr-07

Sep-98

Jun-97

Emerging market bond spreads may have moved into complacent territory

JP Morgan EMBI Global Bond Spreads

Basis points

Key challenge ahead: managing the risk of an abrupt turn in the credit cycle

Consequences would be severe in some countries

Risk under-priced in markets with large imbalances and/or incipient inflation?

Inadequate information relating to new instruments, borrowers and creditors

Structured financial products & hedge funds/private equity

External debt increasingly in corporate sector

Borrowing by low-income countries on non-concessional terms could endanger debt sustainability

Related Documents