www.mergers-alliance.com Global Consumer Goods Sector Report 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.mergers-alliance.com

Global Consumer GoodsSector Report 2012

1Consumer Goods - Contents

Report 2

Introduction 3

Report Highlights 4

Deal Focus by Country

Contacts 38

Transactions 40

AmericasBrazil 8

Mexico 10

USA 12

Asia, Africa and Middle EastChina 14

India 16

Japan 18

Turkey 20

EuropeFrance 22

Germany 24

Italy 26

The Netherlands 28

Poland 30

Russia 32

Spain 34

United Kingdom 36

Sector Report 2012

Contents

2

Report

Consumer Goods - Report

Sector Report 2012

About the report

Deal Focus

This sector report was edited byAndre Johnston of the MergersAlliance central team. To compileour findings we conductedinterviews with our sector expertsfrom each member firm within theMergers Alliance partnership. Wealso surveyed owners and seniorexecutives within consumer goodsector organisations and privateequity investors worldwide.

For more information on thisreport please contact AndreJohnston, Mergers AllianceResearch Manager.

Andre JohnstonMergers Alliance+44 207 881 [email protected]

Other sector reports availableto download from mergers-alliance.com include:

Global Cleantech Report

Global Engineering Review

Global Food & Drink

European Plastic Packaging

Within each country’s Deal Focuswe review merger and acquisition(M&A) activity, focusing on keydeals and trends within theconsumer goods sector with anemphasis on branded goods.

We have included tables ofrecent transactions where thetarget company is located inthe country under review.Additionally, we provide an

overview of the consumer goodssector as a whole, highlighting themarket structure as well ascommenting on the key trendsand the factors influencing M&A.

We provide our own insight onhow we think the market mightplay out over the coming 18months and attempt to identifykey investment opportunities.

Key terminology: FMCG (Fastmoving consumer goods)CF+T (Cosmetics, fragrancesand toiletries) y-o-y (year onyear), CAGR (Compound annualgrowth rate) BRIC (Brazil, China,India, Russia). All deal values arein US dollars unless otherwisestated.

DisclaimerThis publication contains general informationand is not intended to be comprehensive norto provide financial, investment, legal, tax orother professional advice or services. Thispublication is not a substitute for suchprofessional advice or services, and it should

not be acted on or relied upon or used as abasis for any investment or other decision oraction that may affect you or your business.Before taking any such decision you shouldconsult a suitably qualified professionaladviser. Whilst reasonable effort has beenmade to ensure the accuracy of theinformation contained in this publication,

this cannot be guaranteed and neitherMergers Alliance nor any of its member firmsor other related entity shall have any liabilityto any person or entity which relies on theinformation contained in this publication,including incidental or consequentialdamages arising from errors of omissions.Any such reliance is solely at the user’s risk.

p

3Consumer Goods - Introduction

IntroductionSector Report 2012

As you will see from our report,mergers and acquisitions (M&A)activity in the sector has beenprogressively rising since thenadir of the global downturn in2009. The report highlights thatdespite very challenging marketstransactions are being completedin many different consumersegments and geographies.In addition a large proportionof these deals are cross-bordertransactions reflecting theincreasingly global characteristicsof the sector.

Our report also contains a greatdeal of market-leading insight intothe key issues facing the sector in

2012 and beyond: how emergingmarkets are critical to consumerproduct company growth; whymulti-channel sales strategies aredriving investment activity andhow companies at the value,premium and luxury ends ofconsumer markets are benefitingfrom those operating in themiddle of the market. Our workalso highlights the level of privateequity investment in the sectorand how mid-cap companies andglobal corporates are shapingtheir acquisition strategies.

As the global recovery takes hold,we at Mergers Alliance are ideallyplaced to help you. Whether you

seek growth through acquisitions,wish to restructure or realise valuein your business, our internationaladvisors are in a unique positionto help you. Our member firmshave a prominent position inboardrooms across the world andare renowned for delivering anaward-winning partner-ledadvisory service with seamlessinternational cooperation.

We hope you find our reportenlightening and welcome anyfeedback on our observationsand conclusions.

Andy CurrieChairman of Mergers AllianceManaging Partner of Catalyst Corporate Finance LLP+ 44 207 881 [email protected]

Caution and uncertainty continue to affect the majoreconomies and depress consumer confidence levels,especially in the US and Europe. Whilst the consumerproduct industry has been particularly exposed to theprevailing economic conditions we are optimistic thatconfidence will improve in 2012, creating newopportunities across all consumer markets.

4

Report Highlights

Consumer Goods - Report Highlights

Sector Report 2012

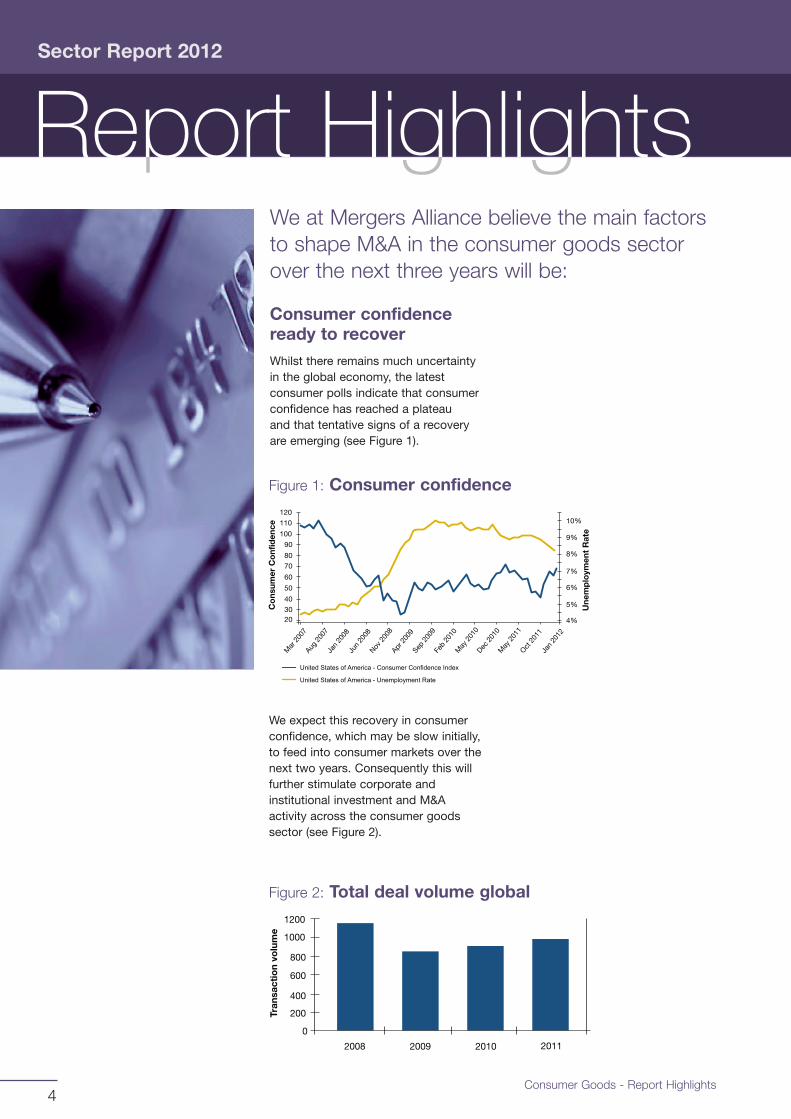

Consumer confidenceready to recoverWhilst there remains much uncertaintyin the global economy, the latestconsumer polls indicate that consumerconfidence has reached a plateauand that tentative signs of a recoveryare emerging (see Figure 1).

We expect this recovery in consumerconfidence, which may be slow initially,to feed into consumer markets over thenext two years. Consequently this willfurther stimulate corporate andinstitutional investment and M&Aactivity across the consumer goodssector (see Figure 2).

We at Mergers Alliance believe the main factorsto shape M&A in the consumer goods sectorover the next three years will be:

p

United States of America - Consumer Confidence Index

United States of America - Unemployment Rate

40

30

50

110

60

120

20

100

90

80

70

4%

5%

6%

7%

8%

9%

10%Oct

2011

Jan

2012

May

2011

Dec20

10

May

2010

Feb

2010

Sep20

09

Apr20

09

Nov20

08

Jun

2008

Jan

2008

Aug20

07

Mar

2007

Co

nsum

erC

onf

iden

ce

Une

mp

loym

ent

Rat

e

200

400

800

600

1000

1200

0

2008 2009 2010 2011

Tran

sact

ion

volu

me

Figure 2: Total deal volume global

Figure 1: Consumer confidence

g g

5Consumer Goods - Report Highlights

Emerging markets risingConsumer goods companies haverecognised that emerging markets area requisite for growth rather than justa complementary source of revenue.We expect this corporate focus to drivemore Western investment into emergingeconomies directly through acquisitionsor joint ventures.

Our research shows the rise ofconsumer sector M&A in emergingmarkets and in particular Asia. Since2008, the proportion of M&A in theseeconomies has increased by over a fifthto represent 30% of all deals globally(see Figure 3).

The deal flow is two way. Indianconsumer companies Godrej andGitanjali have been among the ten mostactive acquirers globally over the pastthree years, having completed 15 dealsbetween them. As with other BRICheadquartered multinationals, they haveset ambitious growth plans and haveacquired branded goods companies inboth developed and other developingcountries.

10

20

30

40

60

70

50

90

80

100

0

M&A Volume 2009 M&A Volume 2011

Europe and North America

Rest of World

1%4%

25%

Africa and the Middle EastAsia PacificLatin America & Caribbean

M&

AD

eal V

olu

me

Figure 3: Emerging markets

6

Report Highlights

Consumer Goods - Report Highlights

Sector Report 2012

Adoption of multi-channelsales approach drivingM&AAlmost all consumer productcompanies have adopted a multi-channel retail distribution model, whichincluded high street retail, online, mailorder and television distribution. Onlineshopping accounted for the majority ofoverall retail sales growth in a numberof developed markets during 2011 andis set to continue to dominate growth.

Companies in the US, UK, Germanyand the Netherlands have beenparticularly active in acquiring onlinebusinesses and we expect furtherconsolidation to occur across thedeveloped economies.

The Chinese market is forecast tobecome the biggest home shoppingmarket globally – the B2C e-commercemarket growing at 75% CAGR up to2014. It is inevitable that successfullocal online businesses will be targetsof both acquisitive overseas andlocal buyers.

Pressure on brandshas intensifiedConsumers in developed markets havebeen increasingly focused on price andbrand equity. Whilst this has meantgrowth at both the premium end andvalue end of the branded goodsspectrum, there has been intensecompetition and margin pressure inthe middle. Many of these brands havefound themselves competing directlyagainst their distribution networks,which have developed private labelsofferings – currently growing at 10%in the US and 6% in Europe.

This has created a number of‘distressed’ sales and both corporateand private equity investors such asSun Capital have capitalised on theseopportunities. We expect furtherdistressed opportunities to emergein the short term.

Private equity continuesits love affair withconsumer brandsThe private equity industry has anestablished track record of workingwith private businesses to expand thedistribution of consumer brandedproducts in most developed countries.This trend has continued through theeconomic downturn although the focushas moved away from single channelretail distribution to multi-channeldistributed products.

Some of the more well known specialistsector investors such as L Capital andChange Capital have been activerecently as well as global players likeCarlyle Group, Oaktree Capital, Eurazeoand Blackstone Group.

High prices paid forhigh-end brandsDuring the past three years corporateand private equity activity in the luxuryand premium segment has risen toreflect the increase in demand forpremium goods from Asia, Russiaand South America.

European luxury brands have been inparticular demand and commandedhigh prices. The leading French luxuryconglomerate LVMH has made sevenacquisitions since 2008 including Italianjewellery maker Bulgari. Jimmy Choo,the iconic British lifestyle brand, wasacquired for c. $930m by Labelux, theAustrian firm, which includes Bally andBelstaff amongst its portfolio. VF Corp,the leading US branded apparelconglomerate, acquired Timberlandfor $2.2bn, at a valuation of 12.3xhistoric EBITDA.

M&A is now one of themain growth strategiesfor consumercompanies domiciledin mature economies.

“”

p g g

7Consumer Goods - Report Highlights

We expect to see the luxury andpremium brand conglomeratescontinue to consolidate the marketand provide the best exit route forinvestors, who would have consideredan IPO in previous years.

Companies in lowergrowth, matureeconomies needto acquireM&A is now one of the main growthstrategies for consumer companiesdomiciled in mature economies.Companies that have reached a

ceiling in terms of organic growth dueto the mature and consolidated natureof their respective markets, will becompelled to pursue globalisationstrategies.

The larger multinationals already haveglobal sales and distribution operations,and are generally the first to acquire inemerging markets however, we expectto see more mid sized businessesacquire in BRIC countries as the risksbecome more understood and the M&Aapproach more accepted.

Consumer powerA consumer tidal wave is on its wayin the form of the BRIC countries.Whilst the economies in each countryvary significantly, their consumermarkets are characterised by a largelyuntapped rural consumer population,expanding middle classes and the highincome disparities between the ruraland urban populations. It is estimatedthat one billion more consumers willemerge in less than 15 years.

Whilst the consumption of basic goodssuch as food, beverages and clothinghave grown most in line with GDP, theconsumption mix is changing. Certainsub-sectors, such as skin-care in Chinaand India and cosmetics and babydiapers in Brazil, are growing fasterthan GDP. As a result, competitionfor local brands is intensifying andacquirers are paying high premiums asconsolidation takes place. We expectpremiums to remain high as demandfor these brands and companiesexceed supply.

200

400

800

600

1000

1200

1400

1600

0

Year 2009 Year 2025

250

1,350

OthersBrazil

India

China

One billion new middle class consumers

Source: McKinsey & Company

8

“With the risein consumerincome andthe emergence

of 30 million newconsumers, theBrazilian consumermarket has attractedglobal attention.Despite substantialconsolidation in recentyears there are stillplenty of M&Aopportunities.”Felipe Monaco,Broadspan

Brazil

Deal Focus - Brazil

A BRIC success

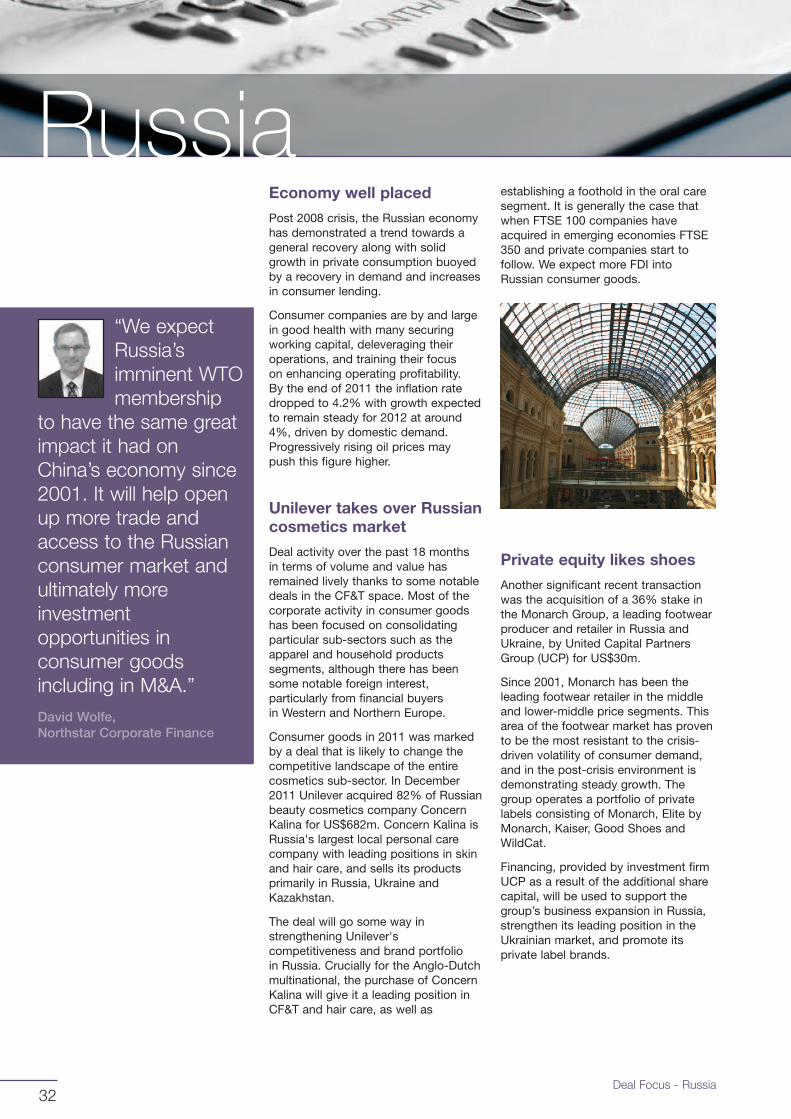

Brazil’s appeal to investors grows dayby day and is quickly becoming oneof the most appealing of the BRIC’sthanks to its booming economy andimproving business conditions.

Brazilian GDP grew 7.5% in 2010 andis estimated to expand by 3.4% in2012, mainly driven by its internalmarket, which benefits from record highemployment and rising income levels.This social migration process isreaching over 30 million people who areeither joining the consumer base or areincreasing their consumption habits.

The upper, middle and lower-middle(or A-B-C) income segments nowrepresent 74% of the population vs.49% in 2005 thanks to the sharpincrease in lower income consumerspending power. A strong commitmentto economic stability, along with astructurally sound financial sector, hascontributed to consumer confidenceand capital expansion which shouldhave a positive effect on generaleconomic growth.

Population increasedriving diaper market

Multinationals are becomingincreasingly attracted to the babydiaper segment. In September 2011personal care giants Svenska CellulosaAktiebolaget (SCA) acquired babydiapers and wet wipes specialistsPro Descart Indústria E Comérciofor US$71m.

Domestic consolidation is also takingplace, in August 2010 multi-billiondollar Brazilian conglomerateHypermarcas acquired the Brazil baseddiapers, tissues and feminine careproducer Mabesa from Grupo PI Mabein a US$195m transaction whichrepresented an estimated 8.5 x EVto EBITDA ratio. Hypermarcas alsoacquired two other leading diaperBrazilian companies (Pom Pom inNovember 2009 for US$173m andSapeka in March 2010 for US$211m)establishing its national leadership witha 35% market share.

The baby diapers segment hasexperienced double digit growth overthe past few years - a trend that isexpected to continue due to theincreasing purchasing powerof the consumer and relativelyhigh birth rates.

Footwear IPO alerts sellers

Arezzo, Brazil’s leading footwearcompany that holds an 11% marketshare and operates through franchisesas well as its own stores, went public inJanuary 2011 raising US$339m. A largechunk of the proceeds (roughly 35%)will be used to acquire smaller brands.It has been reported that other localfootwear companies are also currentlyseeking acquisitions both domesticallyand overseas. Expect substantialconsolidation activity in this sub-sectorover the next 18 months.

Strong private equityinvolvement

Private equity involvement in theLatin American market is becomingincreasingly evident.

The Carlyle Group looked to expand itsconsumer portfolio by acquiring a 51%stake in Scalina, Brazil’s largestmanufacturer and retailer of women’shosiery and lingerie, for approximatelyUS$160m. In the last five years, theBrazilian lingerie market has outpacedGDP growth by circa 100%; a figurethat can be attributed to theproliferation of the middle class andthe rising number of women withexpendable incomes.

9

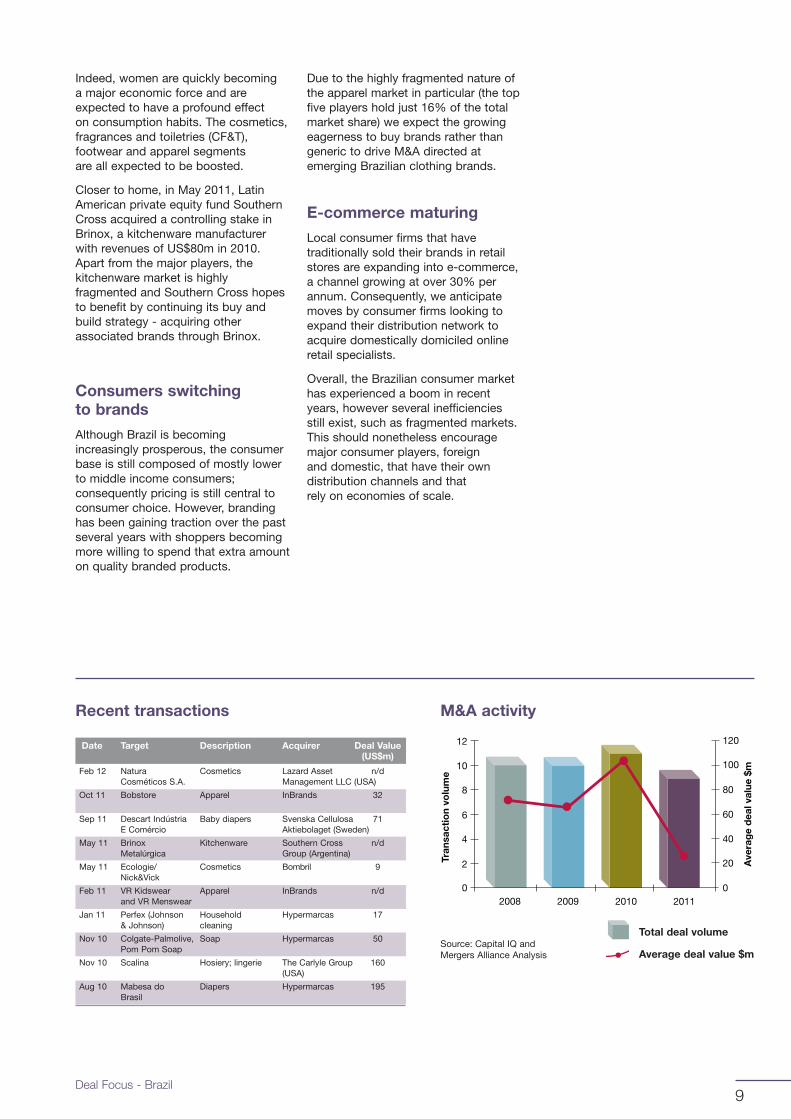

Date Target Description Acquirer Deal Value(US$m)

Feb 12 Natura Cosmetics Lazard Asset n/dCosméticos S.A. Management LLC (USA)

Oct 11 Bobstore Apparel InBrands 32

Sep 11 Descart Indústria Baby diapers Svenska Cellulosa 71E Comércio Aktiebolaget (Sweden)

May 11 Brinox Kitchenware Southern Cross n/dMetalúrgica Group (Argentina)

May 11 Ecologie/ Cosmetics Bombril 9Nick&Vick

Feb 11 VR Kidswear Apparel InBrands n/dand VR Menswear

Jan 11 Perfex (Johnson Household Hypermarcas 17& Johnson) cleaning

Nov 10 Colgate-Palmolive, Soap Hypermarcas 50Pom Pom Soap

Nov 10 Scalina Hosiery; lingerie The Carlyle Group 160(USA)

Aug 10 Mabesa do Diapers Hypermarcas 195Brasil

Recent transactions

Indeed, women are quickly becominga major economic force and areexpected to have a profound effecton consumption habits. The cosmetics,fragrances and toiletries (CF&T),footwear and apparel segmentsare all expected to be boosted.

Closer to home, in May 2011, LatinAmerican private equity fund SouthernCross acquired a controlling stake inBrinox, a kitchenware manufacturerwith revenues of US$80m in 2010.Apart from the major players, thekitchenware market is highlyfragmented and Southern Cross hopesto benefit by continuing its buy andbuild strategy - acquiring otherassociated brands through Brinox.

Consumers switchingto brands

Although Brazil is becomingincreasingly prosperous, the consumerbase is still composed of mostly lowerto middle income consumers;consequently pricing is still central toconsumer choice. However, brandinghas been gaining traction over the pastseveral years with shoppers becomingmore willing to spend that extra amounton quality branded products.

Due to the highly fragmented nature ofthe apparel market in particular (the topfive players hold just 16% of the totalmarket share) we expect the growingeagerness to buy brands rather thangeneric to drive M&A directed atemerging Brazilian clothing brands.

E-commerce maturing

Local consumer firms that havetraditionally sold their brands in retailstores are expanding into e-commerce,a channel growing at over 30% perannum. Consequently, we anticipatemoves by consumer firms looking toexpand their distribution network toacquire domestically domiciled onlineretail specialists.

Overall, the Brazilian consumer markethas experienced a boom in recentyears, however several inefficienciesstill exist, such as fragmented markets.This should nonetheless encouragemajor consumer players, foreignand domestic, that have their owndistribution channels and thatrely on economies of scale.

Deal Focus - Brazil

4

2

6

10

8

12

0

20

40

60

80

100

120

02008 2009 2010 2011

Tran

sact

ion

volu

me

Ave

rag

ed

eal v

alue

$m

Source: Capital IQ andMergers Alliance Analysis

Total deal volume

Average deal value $m

M&A activity

10

“Thedevelopmentpriority ofmany firms has

been outward of late totake advantage of therapidly growing middleclass. Solid macrofundamentals alongwith the increase inconsumer credit, rolledout by both departmentand specialist stores,has led to a surge inMexican consumerism.With this, Mexicoremains one of themore attractiveemerging marketpropositions.”Christian Garcini Garcia,Sinergia Capital

Mexico

Deal Focus - Mexico

Sound fundamentals

The Mexican consumer goods sectorswept through the global economicdownturn unimpeded, experiencing6% compound annual growth over thepast three years.

Consumer growth is expected to atleast equal GDP growth which iscurrently at 4%. Indeed, a rising middleclass may push growth in consumergoods higher still. Other positive indicesinclude a relatively low inflation rate(at 3.14%) and stable consumerconfidence levels. Moreover,consumer credit is recovering aftera sharp contraction in 2009 and isexpected to reach 2007 levels in 2012.

Overall deal volume in consumer goodshas traditionally been low relative to thegeneral market; however, it has beensteadily rising since 2009.

Multinationals investingin Mexico

Large multinationals have sought tocapitalise on concentrated sectorgrowth. One such firm was SvenskaCellulosa Aktiebolaget, the Swedishconsumer goods giant and owner ofbrands such as Bodyform and Tempo.In July 2010 it agreed to acquireCopamex S.A, a baby diaper businessthat targets the Mexican and CentralAmerican market, for US$50m. Thedeal involves the rights to the brandsTessy Babies and Dry Kids amongothers and will take advantage of thegrowing Mexican and Central Americanbaby diaper market.

Brand integration

An increasingly common theme inMexican consumer oriented M&Ahas been for diversified consumercompanies to buy smaller brandsto then incorporate into theirproduct lines.

In October 2010, Genomma LabInternacional SAB, a Mexico baseddeveloper and marketer of over-the-counter pharmaceutical and personalcare products, agreed to acquire thePomada de la Campana, Galaflex,Affair, Vanart and Sante Haircare brandsfor a total consideration of US$85m.The brands, that reported combinedannual sales of US$38m in 2009, will beincorporated into Genomma’s alreadyextensive portfolio of over 90 brands

Largest luxury marketin Latin America

The luxury goods market is the secondmost important in Mexico after themass segment. Indeed, Mexico ratesabove Argentina and Brazil with 55% ofthe total sales of luxury goods in LatinAmerica. According to AC Nielsen,6,4 million Mexicans will have annualincomes of over US$60,000 by 2030.A number of major international luxurybrands rely on the affluent Mexicanconsumer as much as they do theEuropean. Hugo Boss for examplederives c. 15% of its global salesfrom Mexico.

Apparel acquisitionopportunities

We expect the trend of Mexican brandsbeing bought with the intention of beingintegrated into the buying company’sproduct line to continue. We expect thistrend to take place in the apparel sectorin particular, where a number ofsuccessful local brands haveemerged. These include:

11

Date Target Description Acquirer Deal Value(US$m)

Oct 11 Scientific-Atlanta Set-top boxes PCE Paragon 45de Mexico Solutions kft (Hungary)

Aug 11 Moda Holding Footwear Nexxus Capital, n/dS.A.P.I. de C.V. S.C. developer

Aug 11 Various Brands Various brands Genomma Lab 85Internacional SAB

Jul 11 Toshiba Electronics Just International n/dElectromex Ltd. (Taiwan)

Oct 10 Colgate-Palmolive Personal care Genomma Lab 29(Mexican brands) Interacional SAB

Jul 10 Copamex, S.A. Personal care Svenska Cellulosa 50de C.V. Aktiebolaget (Sweden)

Mar 10 Laboratorios KSK Natural products Takashi Tsuru n/dcompany Kayaba

Mar 10 Impco, S. de Household Sylvan Holdings n/dR.L. de C.V. appliances Pte. Ltd (Singapore)

Jan 09 Iconix Brand Various brands New Brands 6Group, Inc Americas LLC (USA)

Aug 08 Barajas y Naipes Leisure equipment Cartamundi NV; n/dde Mexico Copag da Amazônia S.A.

Recent transactions

2

1

3

4

6

5

7

010

30

50

60

90

80

70

120

0

20

40

2008 2009 2010 2011

Tran

sact

ion

volu

me

Ave

rag

ed

eal v

alue

$m

Source: Capital IQ andMergers Alliance Analysis

Total deal volume

Average deal value $m

M&A activity

Julio: Quality clothing at low prices.It currently has 48 stores and 15franchises in Mexico.

Ivonne: The brand has positioneditself as one of the leadingcompanies in selling fashion andaccessories to a wide segment ofthe female population. Has recentlyopened its first stores in the US.

Marsel: It currently has 20 storesin shopping malls across thecountry, Marsel has beenexpanding at a fast pace.

Highlife: Clothing for men; one ofthe market leaders in the sector.

Andrea: Catalogue sales of shoeswith a large share of the Mexicanmarket.

In our view the above present a goodopportunity for foreign firms looking toinvest in the infrastructure of some wellestablished and potentially high growthMexican brands.

Deal Focus - Mexico

The luxury goodsmarket is the secondmost important inMexico after the masssegment. Indeed,Mexico rates aboveArgentina and Brazilwith 55% of thetotal sales of luxurygoods in LatinAmerica.

“

”

12

“The USconsumerproducts M&Aactivity has

proven to be ratherresilient in this volatileenvironment. Giventhe strong corporatebalance sheets, andbacklog of agingowners of privately-heldCP companies, we arebracing for a strongsurge of M&A activityover the next few years.”Brian Mulvaney,Headwaters MB

USA

Deal Focus - USA

Strategies change onmacro deterioration

As goes the consumer so goes theconsumer products industry and theconsumers throughout the world arestill recovering from the local and globalrecession and personal deleveraging.

The US consumers buying behaviourhas fundamentally changed from themid-2000’s and consumer goodsmanufacturers and the retail channelswill continue to have to adjust to thisnew buying paradigm.

The continued contraction of creditavailability to the consumer (be it fromcredit cards, home equity loans, 401k)combined with declining assets,dropping consumer confidence andincreased unemployment, has madethe US consumer more price sensitive,decrease discretionary spending andbecome more willing to consideralternative channels for key purchases.

The consumer goods manufacturershave also faced a dramaticallychanging environment in the US.Rising inflation on the back of monetarystimulus has meant that companieshave faced rising commodity priceswhile at the same time being pressuredto maintain, if not lower, its retailpricing. Many branded companiesfaced new competition from privatelabel offerings. In addition, companiesremain challenged by tight creditmarkets, a volatile dollar and increasingemployee benefit costs.

Stable M&A levels

Despite volatile economic conditionsaffecting the consumer space, theannual number of transactions has

remained relatively constant since2008 through the end of 2011at approximately 200 reportedtransactions per annum. While most ofthe deals had undisclosed value andterms, the ones that did discloseexhibited an increased averagetransaction size from a low in 2008through 2010. This increase in theaverage deal size was reflective of thefinancial turmoil in 2008 in which manyof the sellers were "distressed" andbuyers had limited sources of capital.Average deal size spiked in 2010 asthere were five US$1bn+ transactionsincluding NBTY and Alberto-Culver forUS$4bn each, whereas the largestdisclosed deal in 2008 was onlyUS$500m.

Approximately 13% of the companiesacquired in the US have been boughtby a non-US based entity. In 2011,there was an increase in cross-bordertransactions which was driven by theweak dollar and a desire for Europeanand Chinese companies seeking"foothold" acquisitions in the US.

Large deals and hostiletakeovers

VF Corp, one of the leading ownersof branded apparel companies, addedTimberland to its portfolio in June 2011in a US$2.2bn deal. This valuation wasa 40% premium to Timberlands recentstock price, 1.2 x revenue and 12.3 xEBITDA.

Timberland, which was publicly tradedbut family managed, had suffered adecline in profitability and was facinginvestor criticism. By being acquired byVF, Timberland’s cost structure shouldimprove and sales will benefit from VF’sglobal distribution network. VF, whichowns such brands as Vans, North Face,JanSport, Reef, Wrangler and Lee hasstated that it will continue to look tobuild its brand portfolio in all of itscategories both in the US andoverseas.

13

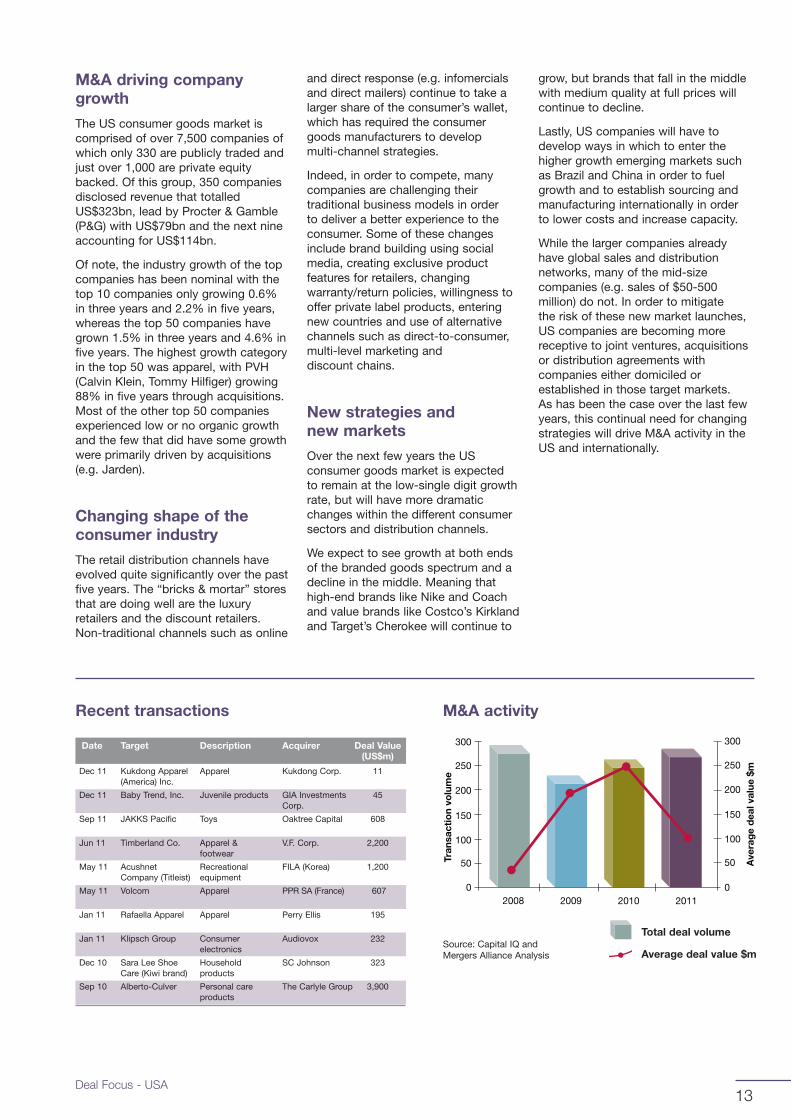

Date Target Description Acquirer Deal Value(US$m)

Dec 11 Kukdong Apparel Apparel Kukdong Corp. 11(America) Inc.

Dec 11 Baby Trend, Inc. Juvenile products GIA Investments 45Corp.

Sep 11 JAKKS Pacific Toys Oaktree Capital 608

Jun 11 Timberland Co. Apparel & V.F. Corp. 2,200footwear

May 11 Acushnet Recreational FILA (Korea) 1,200Company (Titleist) equipment

May 11 Volcom Apparel PPR SA (France) 607

Jan 11 Rafaella Apparel Apparel Perry Ellis 195

Jan 11 Klipsch Group Consumer Audiovox 232electronics

Dec 10 Sara Lee Shoe Household SC Johnson 323Care (Kiwi brand) products

Sep 10 Alberto-Culver Personal care The Carlyle Group 3,900products

Recent transactions

M&A driving companygrowth

The US consumer goods market iscomprised of over 7,500 companies ofwhich only 330 are publicly traded andjust over 1,000 are private equitybacked. Of this group, 350 companiesdisclosed revenue that totalledUS$323bn, lead by Procter & Gamble(P&G) with US$79bn and the next nineaccounting for US$114bn.

Of note, the industry growth of the topcompanies has been nominal with thetop 10 companies only growing 0.6%in three years and 2.2% in five years,whereas the top 50 companies havegrown 1.5% in three years and 4.6% infive years. The highest growth categoryin the top 50 was apparel, with PVH(Calvin Klein, Tommy Hilfiger) growing88% in five years through acquisitions.Most of the other top 50 companiesexperienced low or no organic growthand the few that did have some growthwere primarily driven by acquisitions(e.g. Jarden).

Changing shape of theconsumer industry

The retail distribution channels haveevolved quite significantly over the pastfive years. The “bricks & mortar” storesthat are doing well are the luxuryretailers and the discount retailers.Non-traditional channels such as online

and direct response (e.g. infomercialsand direct mailers) continue to take alarger share of the consumer’s wallet,which has required the consumergoods manufacturers to developmulti-channel strategies.

Indeed, in order to compete, manycompanies are challenging theirtraditional business models in orderto deliver a better experience to theconsumer. Some of these changesinclude brand building using socialmedia, creating exclusive productfeatures for retailers, changingwarranty/return policies, willingness tooffer private label products, enteringnew countries and use of alternativechannels such as direct-to-consumer,multi-level marketing anddiscount chains.

New strategies andnew markets

Over the next few years the USconsumer goods market is expectedto remain at the low-single digit growthrate, but will have more dramaticchanges within the different consumersectors and distribution channels.

We expect to see growth at both endsof the branded goods spectrum and adecline in the middle. Meaning thathigh-end brands like Nike and Coachand value brands like Costco’s Kirklandand Target’s Cherokee will continue to

grow, but brands that fall in the middlewith medium quality at full prices willcontinue to decline.

Lastly, US companies will have todevelop ways in which to enter thehigher growth emerging markets suchas Brazil and China in order to fuelgrowth and to establish sourcing andmanufacturing internationally in orderto lower costs and increase capacity.

While the larger companies alreadyhave global sales and distributionnetworks, many of the mid-sizecompanies (e.g. sales of $50-500million) do not. In order to mitigatethe risk of these new market launches,US companies are becoming morereceptive to joint ventures, acquisitionsor distribution agreements withcompanies either domiciled orestablished in those target markets.As has been the case over the last fewyears, this continual need for changingstrategies will drive M&A activity in theUS and internationally.

Deal Focus - USA

50

100

150

200

250

300

0

100

150

250

200

300

0

50

2008 2009 2010 2011

Tran

sact

ion

volu

me

Ave

rag

ed

eal v

alue

$m

Source: Capital IQ andMergers Alliance Analysis

Total deal volume

Average deal value $m

M&A activity

14

“China is themost significantprize in theconsumer

goods sector. Themiddle-class in Chinais increasingly becominga wealthy one with agrowing appetite forconsumer goods.Companies, bothdomestic and foreign,will vie for marketshare through M&A.”Andre Johnston,Mergers Alliance

China

Deal Focus - China

Steady shift to a moreconsumer driven economy

The Chinese consumer class, riding onthe wave of constant macroeconomicgrowth, has been expanding at arapid rate.

Just seven years ago 4.2 millionhouseholds were earning US$10,000a year, that household figure has sincerisen to just over 20 million and rising.Despite this, consumption still onlymakes up 35% of GDP comparedto 70% in the US. It is clear that theconsumption capacity of the Chinesehas not come close to realising itsfull potential. Indeed, analysts expectChina’s consumer market to grow tothree times the size of the US marketover the next two decades.

China’s 12th five year plan, which runsuntil 2015, places an emphasis onbalancing the economy to be morehigher-value-add consumer drivenand less reliant on cheap exports.Even with this, China will remain arelatively frugal state relative to itswestern counterparts and saving willremain firmly entrenched in the culture;an economic dynamic that can onlyprove supportive to the long termhealth of the economy.

Large interest in homeappliances

China has been a fairly active hub ofconsumer goods M&A in recent yearsand although there was a contractionin 2010, 2011 surpassed the peaksin both volume and average dealvalue. Interestingly, over half of alltransactions over the past three yearshave been cross-border.

Recent among them was renownedSwedish outdoor recreational brandHestra-Handsken’s acquisition of a50% stake in outdoor sportswear andequipment firm Zhejiang PinghuHuashen in February 2011 for anundisclosed sum. In the same monthFrench electrical appliances companySEB Internationale acquired a 20%stake in kitchenware appliances brandZhejiang Supor for US$526m.

Indeed, the past three years hasseen M&A targeted at home applianceelectronics firms gather pace; furtherdeals included the purchase ofShenzhen based United Opto-Electronics, a firm engaged in thedesign and manufacturing of projectiontelevisions and related products, bykeypad specialists Karce InternationalHoldings for US$346m and the majoritystake purchase of Hefei RoyalstarIndustrial, by its domestic peer WuxiLittle Swan for US$78m.

Homegrown brands taketo the world stage

China is home to a number ofmultibillion dollar brands, some ofwhich have had more exposure toWestern markets than others.The brands range from electronicsto sporting goods and top among themis multinational computer firm Levono.The company manufactures andmarkets desktop, tablet and notebookcomputers. Currently the world'snumber two PC brand, the companyhas already been active in global M&Awith its acquisition of IBM’s personalcomputer division in 2005 being itsmost high-profile deal. Looking aheadit recently stated that it is looking foroverseas acquisitions to expand itsnascent mobile device division.

The next two biggest non food anddrink consumer companies are Antaand Li-Ning, both sporting goodsfirms that design sports apparel andequipment under their own brandnames. Li-Ning surpassed Adidasdomestically in 2009 to become thesecond largest sports brand by marketshare (after Nike). In the same year itbought Hong Kong based sportswearfirm Kason Sports for US$24m. Antameanwhile has ambitiously declared itsintention to open 10,000 new storesacross China.

15

Date Target Description Acquirer Deal Value(US$m)

Dec 11 Shanghai Watches Watches Shenzhen Fiyta 7Company Limited Holdings Ltd

Dec 11 Shenzhen Consumer Sichuan Changhong 32Changhong electronics Electronics Group

Nov 11 Yiwu Nengdali Apparel China Fashion n/dGarments Co.,Ltd. Holdings Ltd.

Aug 11 Parel Cosmetics Ming Fai Holdings 5Cosmetics Ltd. Limited

Aug 11 BSW Household Electornics Bosch and Siemens 19Appliances Home Appliances (Ger)

Aug 11 FAB Enterprise Electronics Wizzard Software 15

Mar 11 Zhejiang Putian Household Elica SpA (Italy) 42Electric appliances

Feb 11 Zhejiang Supor Housewares and SEB SA (France) 526specialties

Feb 11 Zhejiang Pinghu Sportswear and Hestra-Handsken n/dHuashen equipment AB (Sweden)

Apr 08 United Opto- Electronics Karce International 346Electronics Holdings

Recent transactions

Personal care opensits borders

Due to its substantial growth prospectsone industry that has been more activethan most in M&A has been the CF&T(cosmetics, fragrances and toiletries)segment.

In December 2010 Coty Inc, the world’slargest fragrance companyheadquartered in Paris and New Yorkand privately owned by German holdingcompany Joh. A. Benckiser, acquired amajority stake in TJoy Holdings, aJiangsu Province based brand thatmanufactures skin care products, forUS$400m. Although Tjoy has negligiblemarket share (estimated at 1%) Cotywas attracted to one of the Chinesefirm's lucrative skin whitening and maleskincare products lines. These productshave been experiencing high doubledigit growth in recent years.

In 2008 Johnson & Johnson ChinaInvestment Co, a subsidiary of NewJersey based Johnson & Johnson,bought Beijing Dabao Cosmetics, oneof China’s best known cosmetic brands(the firm had previously been majoritystate owned). The purchase has so farfacilitated Johnson & Johnson’s entryinto the Chinese market throughDabao’s 3,000 mainland outlets.

Interestingly, there has been notableoutbound involvement as well; ChinaInvestment Corporation investedUS$50m into French beauty and homeproducts firm L'Occitane Internationalduring its floatation.

Luxury sensibilities

By 2015 China is set to overtake theUS and Japan to become the world’slargest luxury market. Heavy tariffslevied on certain consumer goods suchas a 50% duty on cosmetics and a30% duty on high-end watches are tobe repealed with further reductions onimport tariffs to follow. Such a movemay actually discourage China targetedM&A by foreign luxury companies ashome advantage no longer becomes aprerequisite to penetrating the market.

Currently, only a small fraction of thepopulation can afford premium goods,most of whom are confined to themajor cities, however, prosperityand goods are now swelling intothe second and third tier cities.

Monetary policy couldinfluence M&A

If the Chinese government stopsartificially suppressing its currency andallows the RNB to float freely (whichmay happen sooner than anticipateddue to domestic inflation concerns) theconsumer’s purchasing power will risesharply. Not only will this enable theChinese to outbid foreign consumerson products they themselves make,it will also provide Chinese firms withthe additional purchasing power toparticipate in outbound M&A moreaggressively.

Deal Focus - China

10

20

30

40

50

60

0

20

30

50

40

60

0

10

2008 2009 2010 2011

Tran

sact

ion

volu

me

Ave

rag

ed

eal v

alue

$m

Source: Capital IQ andMergers Alliance Analysis

Total deal volume

Average deal value $m

M&A activity

16

“Consumercompanieshave oftenstruggled to

penetrate the disparateand often volatileIndian market asmodern retail chainsare relatively weak andthe majority ofconsumer goods aresold in traditionalshops. Entering thesemarkets requirespowerful independentdistribution networks,therefore, most wouldbe better off acquiringor partnering with localestablished brands.”Sujay Kotak,Singhi Advisors

India

Deal Focus - India

Growing middle classboosts M&A

India is one the world’s most lucrativeconsumer markets and there is stillample room for expansion in a countrywhere, similar to China, consumptionmakes up less than half of the totalGDP.

A number of multinational consumergiants have had a presence in India fordecades: Unilever initially entered theIndian market in 1930 and Procter &Gamble commenced its first operationsin the 1950’s.

M&A participation in the sectoralthough always evident, has increasedover the past five years thanks tofavourable consumer drivers includinghigh GDP growth, a growing middleclass (which is expected to swell toaround 500 million by 2025) and arise in per capita income for ruralinhabitants.

High valuations inpersonal care

India’s personal care market is growingrapidly thanks to the rise in thepopulation’s purchasing power andincreasing health awareness. The sectorhas attracted many overseas cash richbuyers. Unfortunately, the numberof brands for sale has not satisfieddemand which has contributed tothe high multiples being paid.

This was illustrated by the biddingwar, involving both multinational anddomestic players, for ParasPharmaceuticals, a household andpersonal care company. The auctionwas eventually won by UK basedReckitt Benckiser who bid a sizableUS$725m (price/sales multiple of over8 x). Reckitt is the world's largestproducer of personal and householdproducts boasting global brands suchas Durex and Vanish. As well asextending these brands alreadydiscernable presence in India, theacquisition will allow Reckitt to expandits product line through Paras’ ownextensive portfolio which includesbrands such as D’Cold, Moor andDermicool.

Foreign private equityinterest in Indian apparel

Disposable income in India is growingat 5% annually; yearly growth of theapparel sector however is c. 13%. Thisfigure can be partly attributed to moremoney being in the hands of youngpeople and an increase in demand foroffice wear by both men and women.

The past three years have seen thegrowth in apparel reflected in the M&Amarket where many of the consumertransactions took place.

A number of financial funds competedto invest in Genesis Colors, a companythat owns a variety of premium fashionlabels. Investors included L Capital,the private equity arm of luxuryconglomerate LVMH, who recentlyacquired a 40% stake. Previously, UKbased Henderson Global Investorsacquired a 12% stake for US$17m andUS based venture capital firms SequoiaCapital and Mayfield Fund contributedUS$26m. The new funds have beenused to open new branches, marketone of its flagship brands, Satya Paul,and fund future acquisitions.

In 2010 private equity firms BainCapital and TPG Capital purchasedundisclosed stakes in Indian kids-wearfirm Lilliput for US$86m. The newfunds will allow one of India’s mostrecognisable kids-wear brands toextend its product range as well as itsstore footprint. The deal is also seen asa precursor to its initial share offeringthat is said to be taking place over thenext 12 months.

Seeking global coverage

A growing number of Indian firms areseeking international exposure to bothhedge against domestic competitionand to capitalise on some of thelucrative diaspora market. Historically,Indian firms have sold identical productlines in the targeted overseas marketsto the ones sold locally, however, firmsare now customising their brandportfolio to better suit the tastes ofinternational consumers. M&A hashelped facilitate the cross-over and onesuch example was the acquisition ofUK based CF&T company Keyline

17

Date Target Description Acquirer Deal Value(US$m)

Sep 11 Genesis Colors Apparel L Capital, Henderson 43Mayfield (Various)

Jun 11 Darling Group Hair care Godrej Consumer 100Holdings Products Ltd.

Apr 11 Henkel India Ltd. Fabric care Jyothy 170Laboratories Ltd.

Apr 11 Weekender Apparels for Madhusudan 21Clothing children Securities (Vietnam)

Jan 11 Maya Appliances Household Koninklijke Philips n/dIndustry appliances Electronics (Egypt)

Dec 10 Naturesse Hair care Godrej Consumer n/dConsumer Care Products

Dec 10 Paras Healthcare Reckitt Benckiser 725Pharmaceuticals (UK)

Dec 10 Essence Consumer Fabric care Godrej Consumer n/dCare Products Products

Dec 10 Bachi Shoes Footwear Tata International 26India Private

Sep 10 Lilliput Kids apparel Bain Capital, 86TPG Capital (USA)

Recent transactions

Brands by Godrej Consumer Products,the consumer division of the Indianconglomerate. The buy enabled Godrejto introduce new product ranges to theUK and Europe as well bring Keyline’sbrands to the Indian market. Indeed,Godrej has been one of the world’smost acquisitive consumer companiesover the past three years. A trend thatwe expect to continue as firms inemerging markets go out of theirway to achieve global coverage.

Outlook

The majority of the rural population willemerge from subsistence consumptionto a level that consistently consumestailored, though still affordable,products. The market potential in termsof volume for mass premium productsand FMCG’s is considerable. Webelieve this holds true for productsin beauty and skin care products inparticular and this is where we expectfurther M&A activity to take place overthe next three years.

Despite its eclectic language structureand vast landmass, the current Indianconsumer climate is relativelyhomogenous. Nonetheless, a rise inpurchasing power and an increase inscale will necessitate more complexbusiness models with regards tobranding and general operations.An effort than can be facilitated byforeign expertise.

Deal Focus - India

“At Godrej Consumer Products wehave a financial goal of what we call10x10, which essentially means 10times the size in 10 years. We expectto grow organically by around 15-20% over the next 10 years both in

India and through our global operations.On top of that, we expect a 10%compounded annual growth rate fromacquisitions. This would be financed bythe surpluses generated each year andby maintaining a debt equity ratio ofabout 1:1.

10 times in 10 years is a compoundedannual growth rate of about 27%,which we fully expect to achieve.Ultimately our growth aspirations areindicative of the Indian consumermarket as a whole.”

The Godrej Group is an Indianconglomerate headquartered inMumbai, India and has a turnoverof US$2.6bn. Godrej ConsumerProducts is a leader among India'sFMCG companies, with leadinghousehold and personal careproducts.

Industry insight

Name: Vivek GambhirCompany: Godrej GroupPosition: Chief Strategy Officer

5

10

15

20

30

25

35

0

20

30

90

80

70

6050

40

100

010

2008 2009 2010 2011

Tran

sact

ion

volu

me

Ave

rag

ed

eal v

alue

$m

Source: Capital IQ andMergers Alliance Analysis

Total deal volume

Average deal value $m

M&A activity

18

“The flatJapanesepopulationgrowth and

shrinking consumergoods market in Japanis underpinning M&Aactivity in this sector.We expect to see moreconsolidation ofmarginal localconsumer productscompanies along withMBOs and privateequity investment, whilethe stronger companieslook abroad to thehigher growth marketsin the BRICs, SouthEast Asia and Africa.”Tomoki Tanaka,IBS Yamaichi Securities Co Ltd

Japan

Deal Focus - Japan

Factors determining M&A

Major economic drivers of M&A inthe consumer goods sector in Japaninclude demographics, deflation andthe strong yen to name a few.According to the 2010 census, thepopulation of Japan in 2010 was 128million, virtually the same as in 2005.

The percentage of the population aged65 and over reached 23%, the highestin the world, followed by Germany andItaly at 20%. Mature and shrinkingmarkets in Japan have led toconsolidation among domesticconsumer goods companies. Deflationin Japan has created price competitionputting pressure on margins, furtherforcing players to consolidate to findcost synergies. The strong yen has alsolevelled the domestic playing fieldattracting foreign global players to themarket. Global consumer brands suchas H&M and Zara in apparel and Ikeain furniture have been successfulin Japan.

At the same time these factors havealso been drivers for outbound M&Aas Japanese consumer companiesseek faster growing markets abroad.

Great East Japanearthquake impacts M&A

Prior to the impact of the Lehmanshock, Japan saw a number of majormid and large-sized consumer deals.Panasonic acquired Sanyo electric in adeal worth US$12bn. Moreover, foreignbuyers made selective acquisitionssuch as Newell Rubbermaids purchaseof the baby stroller company Aprica. In2009 consumer sector deals declinedon the back of the market uncertaintyfollowing the global credit crunch.

In 2010 deal volumes and valuesquickly rebounded from a realisationthat the consumer market was relativelyunaffected compared to otherdeveloped economies. However, thischanged dramatically in March 2011with the Great East Japan earthquake

as deal value plunged briefly onceagain reflecting the uncertaintysurrounding the after-effects of theearthquake. In 2011, Japanesecorporations turned to outbound M&Aas a risk diversification measure and totake advantage of the strengtheningyen against major foreign currencies.

Reorganisation of Japaneseelectronics takes place

The much predicted reorganisation ofJapan’s consumer electronics industrywas realised in 2008 with the start ofthe acquisition of Sanyo Electric byPanasonic Corporation.

The initial 50.2% stake in the listedSanyo Electric amounted to overUS$12bn. With major electriccompanies like Hitachi, Toshiba andMitsubishi surging domestically, Sanyocould not compete by itself in many ofits product areas. In 2011, Haier GroupCompany of China, acquired ninesubsidiaries of Sanyo which mainlyproduced washing machines andrefrigerators in Japan and Asia.

M&A was not limited to domesticplayers seeking consolidation. In 2008,Bain Capital saw a brand enhancingopportunity in the Japanese audioelectronics market by acquiring theTokyo Stock Exchange listed D&MHoldings for US$686m. Bain purchasedthe stakes of RHJ International andPhillips and D&M was delisted fromthe stock exchange. D&M holds audioelectronic brands such as Denon,Marantz, and McIntosh.

Strong yen driving foreignexpansion

Given the strong yen and healthy cashbalances, Japanese corporations areincreasingly seeking M&A opportunitiesin growing markets outside Japan tobuild up existing overseas networks inEurope and North America and diversifytheir brand offerings.

p

19

Date Target Description Acquirer Deal Value(US$m)

Dec 11 Asty, Inc. Cosmetics Kenkou Corporation n/d

Dec 11 Wave International Apparel brand Tokyo Style 13Co. Ltd.

July 11 SANYO Electric Kitchen goods Haier Group n/dCo, 9 Subsidiaries

July 11 Pentax Ricoh Digital cameras Ricoh n/dImaging

May 11 Kawashima Curtains, JS Group 180Selkon Textile home interior

Jan 11 Prime Japan Inc. Wedding jewellery Baring P.E. Asia n/d(Hong Kong)

Oct 10 Kasco Corp. Golf products Mamiya-OP Co. Ltd. 26

Oct 10 Sanei International Apparel TSI Holdings 315

Jun 09 Kracie Holdings Toiletries & Hoyu Co. Ltd. 261cosmetics

Dec 08 SANYO Electric Electronics Panasonic Corp. 1,230

Recent transactions

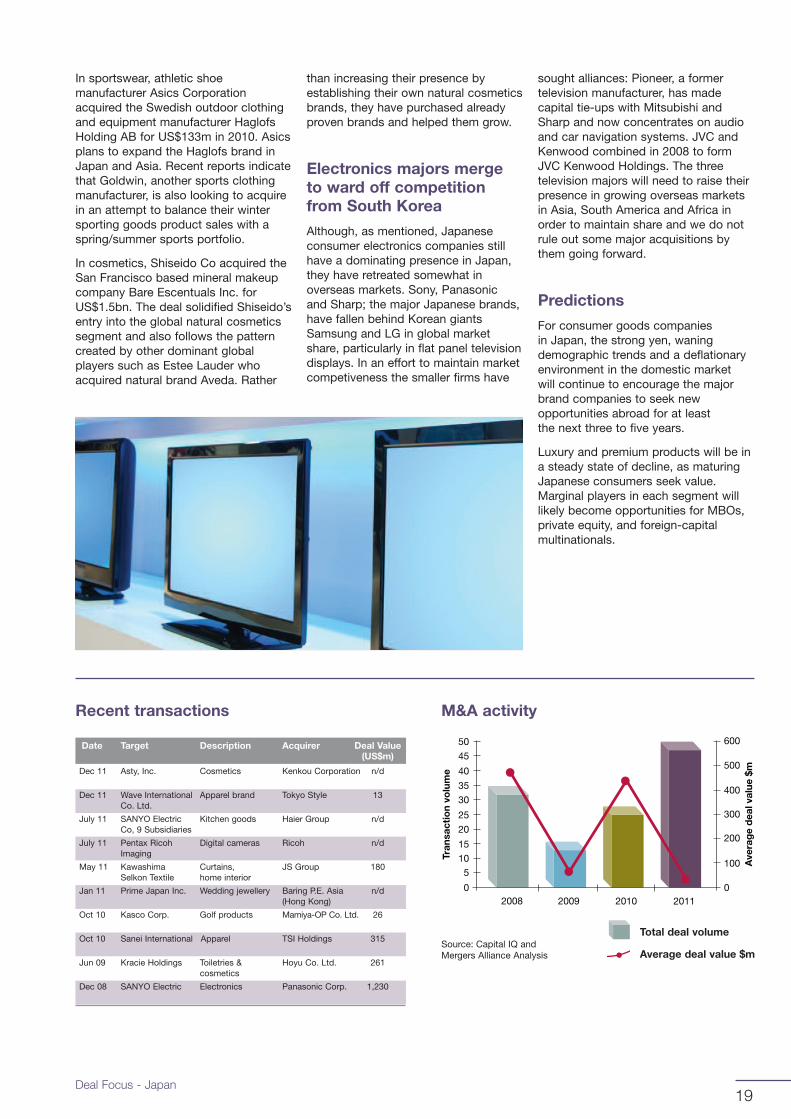

In sportswear, athletic shoemanufacturer Asics Corporationacquired the Swedish outdoor clothingand equipment manufacturer HaglofsHolding AB for US$133m in 2010. Asicsplans to expand the Haglofs brand inJapan and Asia. Recent reports indicatethat Goldwin, another sports clothingmanufacturer, is also looking to acquirein an attempt to balance their wintersporting goods product sales with aspring/summer sports portfolio.

In cosmetics, Shiseido Co acquired theSan Francisco based mineral makeupcompany Bare Escentuals Inc. forUS$1.5bn. The deal solidified Shiseido’sentry into the global natural cosmeticssegment and also follows the patterncreated by other dominant globalplayers such as Estee Lauder whoacquired natural brand Aveda. Rather

than increasing their presence byestablishing their own natural cosmeticsbrands, they have purchased alreadyproven brands and helped them grow.

Electronics majors mergeto ward off competitionfrom South Korea

Although, as mentioned, Japaneseconsumer electronics companies stillhave a dominating presence in Japan,they have retreated somewhat inoverseas markets. Sony, Panasonicand Sharp; the major Japanese brands,have fallen behind Korean giantsSamsung and LG in global marketshare, particularly in flat panel televisiondisplays. In an effort to maintain marketcompetiveness the smaller firms have

sought alliances: Pioneer, a formertelevision manufacturer, has madecapital tie-ups with Mitsubishi andSharp and now concentrates on audioand car navigation systems. JVC andKenwood combined in 2008 to formJVC Kenwood Holdings. The threetelevision majors will need to raise theirpresence in growing overseas marketsin Asia, South America and Africa inorder to maintain share and we do notrule out some major acquisitions bythem going forward.

Predictions

For consumer goods companiesin Japan, the strong yen, waningdemographic trends and a deflationaryenvironment in the domestic marketwill continue to encourage the majorbrand companies to seek newopportunities abroad for at leastthe next three to five years.

Luxury and premium products will be ina steady state of decline, as maturingJapanese consumers seek value.Marginal players in each segment willlikely become opportunities for MBOs,private equity, and foreign-capitalmultinationals.

Deal Focus - Japan

5

10

15

45

40

25

30

20

35

50

0

500

400

300

200

600

0

100

2008 2009 2010 2011

Tran

sact

ion

volu

me

Ave

rag

ed

eal v

alue

$m

Source: Capital IQ andMergers Alliance Analysis

Total deal volume

Average deal value $m

M&A activity

20

“The Turkishconsumergoods sectoris quickly

becoming highlyattractive to investors.This has beenespecially evident inthe ready wear/apparelsector. Although dealvolume has been lowin the past, there arenumerous active dealsin the market and inthe pipeline.”Ozkan Yavasal,Daruma Corporate Finance

Deal Focus - Turkey

Turkish consumer market inan advantageous position

Eurozone uncertainty and trouble inthe Middle East have not preventedthe rapid growth of the Turkishconsumer market.

Factors such as rapid urbanisation; anincreasingly organised retail segment(318 shopping malls by the end of2012); an influx of foreign brandscreating conducive competitiveconditions; and highly favourabledemographics, that are increasinglytrending towards more westernlifestyles, are all benefitingthe consumer sector.

European multinationalstarget personal care market

French CF&T giant L’Oréal expandedits presence in the fast growing Turkishpersonal care market with the purchaseof Canan, one of Turkey’s leading haircare companies. Most of Canan’sUS$26m turnover comes from its Ipekbrand. Closing the deal the consumerproducts president for L’Oréal noted:

“The Turkish cosmetics market isexpanding strongly and has a very largegrowth potential. The acquisition ofCanan will bolster our positions inhair-care products, the largestsegment in the market.”

It is reported that L’Oréal is looking topursue further M&A in high growthemerging markets with Turkey stillhigh on its radar.

Elsewhere, Svenska CellulosaAktiebolaget continued its trend oftargeting personal care companies inemerging markets with its acquisitionsof San Saglik Urunleri SanTic andKomili Kagit ve Kisisel Bakim Uretim.The former is an adult diaper and underpads company whilst the latterspecialises in baby diaper andfeminine care products.

The acquisitions are in line with SCA’sstrategy of pursuing inorganic growth inEurope and in other parts of the world.

Investors look to livelyapparel market

The rise in the appetite for clothingbrands has been significant, however,it is only recently that investors havelooked to M&A as a means ofcapitalising on this demand. InDecember 2010 the owner of Turkishfootwear company Yesil Kundura,purchased a majority share in CeylanGiyim in a deal worth US$101m. CeylanGiyim’s primary activities are theproduction and marketing of adultsportswear and fashion wears.It operates 54 retail stores andtwo online stores.

Private equity activity in this space hasalso been apparent: In October 2010newly-formed private equity fundEurasia Capital Partner (a fundfocused on equity and equity-relatedinvestments in Turkish companies)along with the Balkan Accession Fund,acquired a 50% share in Wenice Kids,a children’s clothing brand that sells inmore than 300 shops in 46 countries.The investors hope to help realiseWenice’s ambitious intention of enteringanother 40 markets by the end of 2012and establishing itself as one of theworld’s top ten children’s clothingbrands.

Consumer spendingreaching new heights

Turkey has quickly become one of themost dynamic and fastest growingconsumer markets. It should be notedthat such rapid growth may slow nextyear if the macro conditions in Europeworsen (Turkeys biggest export marketis the EU, and by some margin).

Nonetheless, Turkey’s estimatedconsumer spending level of US$6.9bnin 2010 is expected to almost doubleto US$13bn by 2014. These growthexpectations have stemmed from thegrowth of the retail sector, increasingaffluence and the emergence ofdomestic brands to complimentthe influx of foreign players.

Turkeyy

21

Date Target Description Acquirer Deal Value(US$m)

Dec 11 Sanpan Isitma Decorative Zehnder Group n/dSistemleri San products AG (Swi)

Aug 11 San Saglik Personal products Svenska Cellulosa 15Urunleri San.Tic. Aktiebolaget (Swe)

Jun 11 Komili Kagit ve Baby diapers, Svenska Cellulosa 49Kisisel Bakim feminine care Aktiebolaget (Swe)

Dec 10 Ceylan Giyim Ready-wear Kamil Engin Yeşil 101apparel (Private individual)

Nov 10 �pek Giyim Apparel CarrefourSA 30Mağazaları

Oct 10 Wenice Kids Childrens apparel Eurasia Capital n/dPartners

Jul 10 Hobi Cosmetics Cosmetics Dabur Group 68(India)

Recent transactions

In parallel with this rise in consumerspending (which has already surpassedpre-crisis levels) we expect to see anincrease in M&A movements.

Deal Focus - Turkey

Although the majorityof investments havebeen channelled intodurables, Dabur’sUS$68m acquisitionof Hobi Cosmeticsillustrates that theTurkish consumerbrands market is notlimited to sub-sectorssuch as apparel.

“

”

2

1

3

7

4

5

6

8

0

40

50

30

20

60

0

10

2008 2009 2010 2011

Tran

sact

ion

volu

me

Ave

rag

ed

eal v

alue

$m

Source: Capital IQ andMergers Alliance Analysis

Total deal volume

Average deal value $m

M&A activity

22

“The Frenchconsumerbrand M&Amarket will be

driven by the luxurysector where multiplesare ever-increasing asa consequence ofsector characteristics(high growth, profitableand non cyclical) andthe increasing appetiteof Asian strategicbuyers generatinghigher competitionwith establishedworld leaders.”Michel Degryck,Capital Partner

France

Deal Focus - France

Luxury goods leadingthe M&A market

France is well known for its luxurybrands with global leaders such asLVMH, PPR, Hermès, Chanel andL’Oréal (but also numerous small andmid-sized independent companies)prospering. As such, transactionsfeaturing luxury brand companies areover-represented, and strongly fuel theM&A market.

The market is considered very attractivedue to its profitable, fast growing andnoncyclical characteristics. Moreover,French global market leaders are nowcompeting with new strategic buyersfrom emerging countries like China. Asa consequence, premium assets are inhigh demand and transaction multiplesare surging.

Recent activity included the acquisitionof Bulgari by LVMH, the IPO ofL’Occitane on the Chinese StockExchange and the battle betweenLVMH and the Hermès Family forthe control of Hermès. LVMH, theworld's largest luxury goods company,unveiled a US$5.2bn all-share deal totake over Italian jeweller Bulgari. Thecompany acquired 50.4% of Bulgari,issuing 16.5 million shares in exchangefor 152.5 million shares held by theBulgari family.

The French firm also bought the rest ofBulgari’s shares at 12.25 Euros a share- a premium of about 60%. As part ofthe deal, the Bulgari family became thesecond-biggest family shareholderof LVMH.

Luxury giants seeking newbrands and routes to clients

LVMH, PPR and L’Oréal are lookingtowards consolidation on a global scaleand are actively surveying mid-marketopportunities to strengthen their brandportfolio.

They are also looking to reinforcetheir distribution networks in the BRICeconomies, where they hope to growat a multiple to local GDP thanks to

the emerging middle classes and theincreasing number of high wealthindividuals.

Luxury brands are also adjusting toan environment where buying poweris shifting to emerging markets.Furthermore, consumers in developedregions are making luxury purchasesacross a widening range of distributionformats, including outlet stores andonline.

Private equity buyersvery active

M&A in the consumer goodssector has been very active over thepast two years, fuelled by the cashstockpiles held by the global leadingplayers and private equity firms thathave sought to make deals andspend their cash after two years ofmacroeconomic uncertainty and limitedaccess to financial leverage.

Recent deals of particular interestincluded the sale of Spotless, theFrench maker of laundry and cleaningproducts, to BC Partners, a UK-basedprivate equity group, in a deal valuingthe company at about US$826m. Axaprivate equity, which built Spotless upthrough six bolt-on acquisitions overfive years, has more than doubled itsinitial equity investment in the company.BC Partners saw off competition forSpotless from rival buy-out groupsBridgepoint and Lion Capital.

The Spotless transaction illustrates theappetite for French brands and the highproportion of deals completed byprivate equity houses offeringvaluations comparable to strategicindustrial players. 2011 was especiallyproductive for private equity dueto the banking leverage that wasavailable until August of that year,which enabled LBO France and LFPIGestion to acquire men's underwearmaker Eminence, L Capital to acquireCaptain Tortue and EDRIP to finalisean MBO for children’s apparelbrand Sun City.

23

Date Target Description Acquirer Deal Value(US$m)

Jan 12 Briconord Sarl Home improvement Evolem n/dproducts

Aug 11 Captain Tortue Door to door L Capital 83sales apparel

Jul 11 Paul ka High end apparel Change Capital 69(UK)

Jul 11 Sun City Childrens apparel Edrip + Management 69

Jun 11 Le Tanneur Leather goods Qatar Luxury Group 40et Cie (Qatar)

Jun 11 Eminence Underwear brand LBO France 206

Jun 11 The Kooples Fashion apparel LBO France n/d

Feb 11 Sergent Major Childrens apparel Edrip + Siparex n/d

Sep 10 Sandro Maje Fashion apparel L Capital and Florac n/dClaudie Pierlot

Feb 09 Spotless Laundry/ cleaning BC Partners 826branded products (UK)

Recent PE transactions

Development of own-brandranges by mass-retail

Many of the mass market brandsare now competing against theirdistribution networks, which areincreasing their margins throughdeveloping their own product rangesand private labels. Decathlon (40%market share of the French sportinggoods retail market) epitomises thisnew trend. It is increasingly selling itsown-branded products and carryingout self-innovation rather than simplyretailing third-party branded products.

Corporates likely to spurM&A activity in 2012

The consumer branded goods marketwill be affected in the coming monthsby the downgraded growth forecastsand a tough debt market. We thereforeexpect private equity activity to belimited and the market to be supportedby industrial players which have soundbalance sheets and a strong inclinationto further expand into emergingmarkets.

The sector attractiveness, combinedwith the increasing appetite of Asianstrategic acquirers, is generating highercompetition for M&A transactions andpressure for higher multiples.

Deal Focus - France

1020

30

60

90

80

50

40

70

100

02008 2009 2010 2011

Tran

sact

ion

volu

me

Source: Capital IQ andMergers Alliance Analysis Total deal volume

M&A activity

24

“We expectmany familyownedmid-size

companies to triggerfurther consolidationand be the mainparticipant in consumergoods M&A. Despitethe challenging currenteconomic climate, M&Aactivity in the sectorshould remain stable.”Stefan Constantin,C.H. Reynolds CorporateFinance

Germany

Deal Focus - Germany

A balanced and stableconsumer market

Following the stuttering globaleconomic recovery in 2010 and firsthalf of 2011, macroeconomic risksrose again in Q3 2011.

With sovereign balance sheets saddledby debt burdens, financial marketinstability and deteriorating marketconfidence (amplified by “high-spread”countries) the growth prospects inadvanced European economies remainuncertain. Germany’s performance inthis context has been above-average:Price adjusted GDP growth for 2011was 2.7% with real wages growing by1.9%. Consumer spending increasedby 1.6% while inflation remainsrelatively low at 2.3%. Moreover, theunemployment rate experienced a slightdecrease of 0.6% to level at 6.6%.

Generally, rather robust consumerspending throughout 2008-2011ensured relative stability in consumergoods M&A.

Private equity investorsactive

As mentioned, through 2008 to 2011the number of transactions in theconsumer goods industry in Germanyremained generally stable, averaging50 deals per year.

During 2011 there were a notablenumber of large-scale cross-borderdeals that were supported byfavourable financing conditions forfinancial investors at the time.

In July 2011, Blackstone Group agreedto acquire Jack Wolfskin, the functionalapparel and equipment brand, fromBarclays Private Equity (UK) andQuadriga Capital Services (Germany)for US$982m - equivalent to a multipleof 2 x 2011 sales and 8 x theacquisition price paid in 2005 byBarclays. The transaction underpins thecontinuing high growth expectations ofthe outdoor sector driven by changinglifestyle trends in developed countriesand the ongoing internationalisation ofthe industry.

In the mid-market, UK based 3i Grouprecently acquired Amor GmbH in asecondary buyout. The supplier ofjewellery, marketed internationally underthe Amor brand, was acquired fromPamplona Capital for an estimatedUS$140m. This implied a multiple ofapproximately 6.3 x EBITDA 2010.3i Group intends to extend Amor’sdistribution channels internationallyand strengthen its brand position.

Also in the mid-market, ACapitalrecently acquired the family ownedMustang, the fashion brand for anundisclosed amount.

Made in Germany

Germany is home to a number of globalpower brands, included among themare: Adidas AG, Bosch & Siemens,Beiersdorf AG (Nivea), Puma SE andHugo Boss. Their products range fromsportswear to home appliances, fromskin care to high-end clothing. All thesefirms are pursuing targeted M&Astrategies to support their ambitiousgrowth plans.

From 2008 to 2011 sports and lifestyleapparel companies Adidas and Pumacompleted several cross-border dealsfocused on both the extension of theirexisting brand portfolio and theconsolidation of the companiesposition in foreign markets.

Both companies have been targetingsales growth of up to 50% by 2015,partially supported by inorganicexpansion. This was exemplified byAdidas’ acquisition of Ashworth Inc,the listed US based retailer of golfapparel. They also recently acquired US

y

25

Date Target Description Acquirer Deal Value(US$m)

Dec 11 Run & Style GmbH Sports apparel Maier Sports GmbH n/d& Co. KG & Co. KG

Oct 11 Mustang - Fashion apparel ACapital n/dBekleidungswerke

Jul 11 Jack Wolfskin Outdoor apparel Blackstone 982Ausruestung fuer and footwear Group L.P. (UK)

Jun 11 Medion AG Electronics Lenovo Group 261and IT Limited (HGK)

Apr 11 SLV Elektronik Lighting systems Cinven Ltd. 772GmbH (UK)

Apr 11 d&b Electronics Odewald & n/daudiotechnik GmbH Compagnie

Feb 11 Siteco Lighting solutions Osram GmbH n/d

Feb 11 Weco Furniture under Mebelplast S.A. n/dPolstermoebel WECO brand (Poland)

Jan 11 PAIDI Moebel Furniture for DZ Equity n/dGmbH children Partner GmbH

Dec 10 Amor GmbH Jewellery 3i Group PLC (UK) 140manufacturing/ retail

Recent transactions

performance sports brand Five Ten.Puma SE meanwhile acquired theCobra Golf brand from AcushnetCompany; in addition they purchasedDobotex International, the Dutchexclusive licensing partner of a varietyof fashion, sports and sports-lifestylebrands.

During the same period, Beiersdorf AGlaid out its strategic intention to focuson its core brands – primarily Nivea,Eucerin and La Prairie – whilestreamlining and partially divestingits non-core brands.

In the textile segment HUGO Bossacquired 15 mono-brand stores andrelated assets of the Moss Bros Group(the listed UK fashion retailer) in Q12011 to further expand their storenetwork.

Opportunities abounddespite power brandsdominance

The total sales volume of Germanconsumer goods is estimated atUS$50bn, with the top five brandsaccounting for US$27.7bn.

The industry’s sub-sectors generallyhave their distinctive market leaders(the aforementioned power brands),while the rest of the market ispopulated by a broad array of mid tosmall-cap players (many family-owned)leaving room for consolidationopportunities.

This was illustrated in 2009 whenstrategic investors acquired assets ofinsolvent consumer companies as wellas underperforming assets atfavourable valuations (this wasparticularly evident in the apparelindustry e.g. Baeumler AG andRosner GmbH & Co).

Factors determiningfuture M&A

Cross-border M&A activity involvingGerman consumer goods companiesbuying foreign targets has been largelytriggered by companies striving tointernationalise their distributionnetworks but also by their need toupscale and to secure additionalgrowth platforms (e.g. premiumbrands targeting emerging markets).

Domestic growth opportunities in theGerman consumer goods market stemprimarily from the ongoing life-stylechanges and rising environmentalconsciousness of the consumer. Tocapitalise on these trends, companiesneed stringent brand positioning anddistinctive brand value propositions,as well as efficient distribution andcommunication channels - often aprerogative of the larger market players.We expect these factors to supportconsolidation trends going forward.

Deal Focus - Germany

10

20

50

40

70

30

60

80

0

40

120

100

80

60

140

0

20

2008 2009 2010 2011

Tran

sact

ion

volu

me

Ave

rag

ed

eal v

alue

$m

Source: Capital IQ andMergers Alliance Analysis

Total deal volume

Average deal value $m

M&A activity

26

“Householdspendingcapability,already

undermined by theglobal recession, hasbeen further hit by theincrease in VAT onconsumer goods,drawing consumerstowards low costproducts. Mid-rangebrands are sufferingand are being targetedby stronger competitorslooking for acquisitionsat convenient multiples.”Nuccia Cavalieri,Ethica Corporate Finance

Italy

Deal Focus - Italy

Consumer confidencenosedives

A European debt crisis and contagionconcerns have put a damper oneconomic growth in Italy and hasforced the government’s hand toinitiate broad austerity measures.

There are now real fears thatanother recession is imminent asItalian firms struggle to regaincompetitiveness.

To compound these sentiments themost recent local statistics show Italianconsumer confidence fell to its lowestlevel in over three years. Spending willlikely remain static over the next sixmonths with growth (if any) beingachieved on the back of industrialexpansion.

Firesale prices for brands

Although there has been a y-o-y dip indeal volume due to deteriorating macroconditions (although 2011 saw a slightrecovery), consumer goods led M&Ahas remained relatively active owing toa plethora of esteemed local brands(actively involved in the market) andenthusiastic international participation.

There has also been substantial privateequity involvement in Italian brands aswell as a number of important IPOs -Prada, Ferragamo. Conspicuous bytheir absence however are local tradebuyers, which can be attributed to thesmall to mid-sized Italian companieslacking the required financial strengthto support M&A.

Another characteristic has been thehigh valuations; Moncler, Moleskine,Coin and Braccialini all had at leastnine times EBITDA valuation multiples.It should be noted, disruptedeconomic conditions have alsoled to opportunities involving buyingunderperforming marquee brands atdiscounted prices - the bankruptcy ofMariella Burani and Ittierre groups ledto the firesale of the GianfrancoFerrè, Mandarina Duck, Maloand Arcte brands.

Luxury reigns supreme asinternational markets upthe stakes

Similar to France, internationalawareness for premium local brandsis as high as ever thanks to an evergrowing affluent class in thedeveloping world.

One of the most high profile globaldeals over the past 18 months was theacquisition of Italian luxury consumergroup Bulgari by its French counterpartLouis Vuitton Moët Hennessy (LVMH) inan all-share transaction for US$5.2bn.The mega deal will reinforce LVMH’sworldwide growth aspirations and allowit to double its jewellery and watchesbusinesses while improving itspurchasing and distribution operations.The high purchase price, which was ata 60% premium to Bulgari's averageshare price, was partly due to multiplebidders and partly due to the currentfavourable conditions of the luxurymarket.

Another recent premium transactionwas the acquisition of the MoglianoVeneto based apparel firm Belstaffby the Swiss luxury holding companyLabelux for US$161m in June 2011.The rationale behind the purchase ofthe predominantly menswear firm wasto extend Labelux’s coverage in Asia,particularly China where menswear isone of the country’s fastest growingluxury sectors.

Private equity eager toacquire luxury

Interestingly, private equityinvolvement has been focused in theluxury/premium segments due to themass segments heavy working capital,high debts and low barriers to entry.One of the most high profile deals wasthe minority stake sale of the high-endbrands holding group Moncler SpA toEurazeo private equity fund forUS$572m. The 45% equity acquisitionwill support Moncler’s entry intomarkets such as China and the US.Its brands include Moncler, MarinaYachting and Henry Cotton.

y

27

Date Target Description Acquirer Deal Value(US$m)

Dec 11 Coccinelle S.p.A. Fashion E.Land World 20accessories Company Ltd. (Kor)

Sep 11 Omas Srl Writing instruments Ming Fung Jewelry 51(HK)

Aug 11 DIT Group Jewellery Gitanjali Gems 11(India/ Corporate)

Aug 11 Bulgari Jewellery LVMH 2,470(France)

Aug 11 Moncler Sportswear Eurazeo 572(France)

Jul 11 Braccialini Leather NEM 36accessories

Jul 11 Toy Watch Jewellery J.Hirsch & Co n/d

Jul 11 Mandarina Duck Leather E-Land Co 66accessories (S. Korea)

Feb 11 Gianfranco Fashion Paris Group (UAE) n/dFerrè

Dec 10 Cantieri Navali Luxury yachts Nauticstar Marine 18Lavagna (China)

Jul 10 Barovier & Toso Glass accessories AVM Private Equity 17

Recent transactions

Outbound deals prevail

Outbound deals have been moreprevalent compared to domesticconsolidation over the past threeyears with heavy involvement bysome of the world’s most importantconsumer companies.

Luxottica, the world’s largest eyewearcompany (Ray-Ban, Oakley) was busyfinalising acquisitions in Mexico, NewZealand, Israel and Turkey; while GiochiPreziosi, the world’s fifth largesttoymaker, acquired a 25% stake inFrance based toy distributor KingJouet. Elsewhere, furniture firmElica SpA acquired three companiesin China and India.

Underlying currents of theconsumer brand market

The Italian consumer products industryis relatively fragmented with thousandsof companies with turnovers rangingfrom US$1-100m. The industry as awhole still has a family owned flavourto it. Curiously, there are a distinct lackof domestically based mass marketbrands as most have been bought outby foreign players.

Moving to mass-premium, most smallto mid-sized Italian companies arestruggling to position themselves in anincreasingly value conscious consumermarket. There has been an ongoingdisconnect between what a companysells a product for and its actual marketvalue. Price points have both beenlower to increase volume or higher tomake up for lost volume. Even withthese adjustments, margins haveremained low.

Cross-border willremain king

Given the propensity for large Italiancompanies to look for growthopportunities abroad (rather thanacting as consolidators domestically),we expect the current trend of foreignbig cap companies raiding the countryfor strong historical premium brands tocontinue. The acquisition mood will bedriven by undisputed brand equityon one side and by opportunismon the other.

In terms of valuations, we expectmultiples to remain in the high rangeand for bargains to be few and farbetween.

Deal Focus - Italy

10

20

50

80

40

30

60

70

90

0

100

300

250

200

150