GLENDALE COMMUNITY COLLEGE DISTRICT ANNUAL FINANCIAL REPORT JUNE 30, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

GLENDALE COMMUNITYCOLLEGE DISTRICT

ANNUAL FINANCIAL REPORT

JUNE 30, 2016

GLENDALE COMMUNITY COLLEGE DISTRICT

TABLE OF CONTENTSJUNE 30, 2016

FINANCIAL SECTIONIndependent Auditor's Report 2Management's Discussion and Analysis 5Basic Financial Statements - Primary Government

Statement of Net Position 13Statement of Revenues, Expenses, and Changes in Net Position 14Statement of Cash Flows 15Fiduciary Funds

Statement of Net Position 17Statement of Changes in Net Position 18

Notes to Financial Statements 19

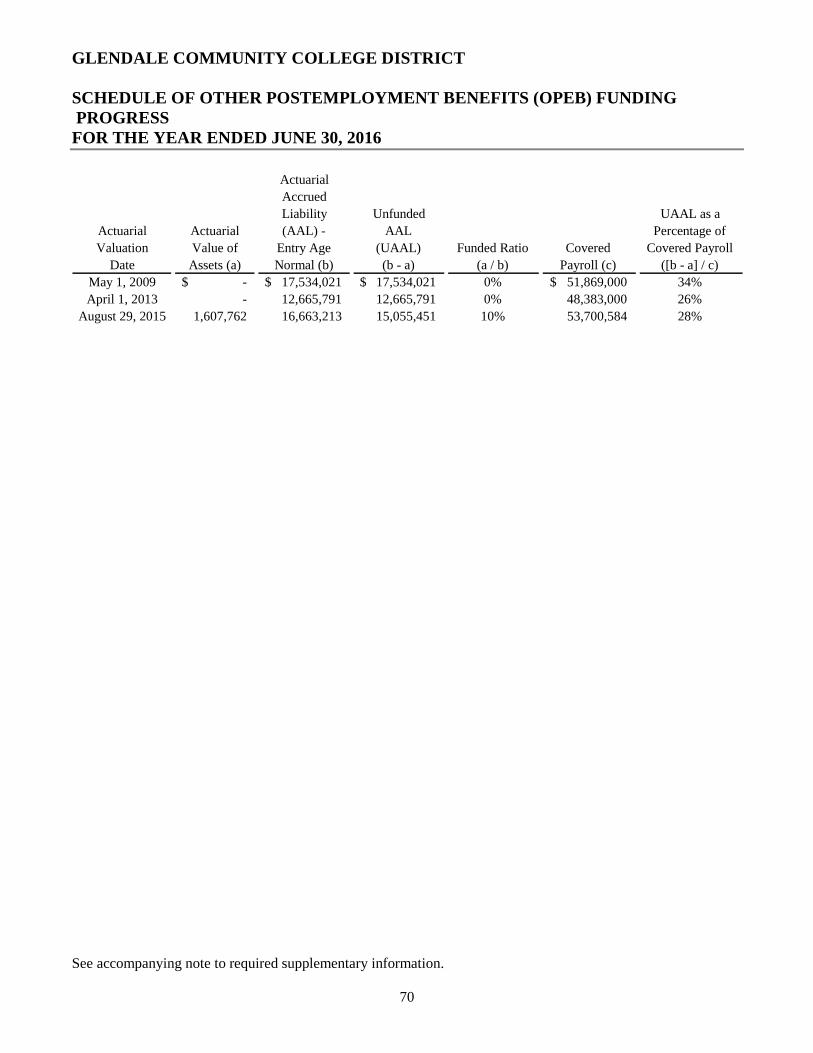

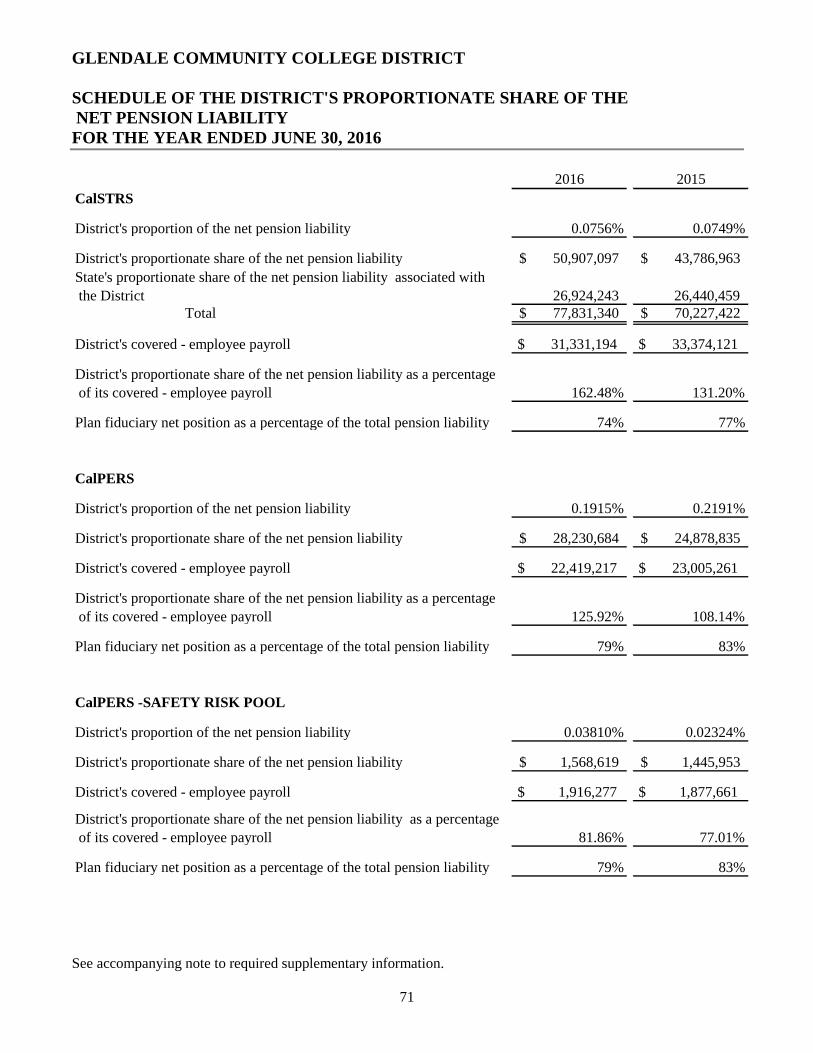

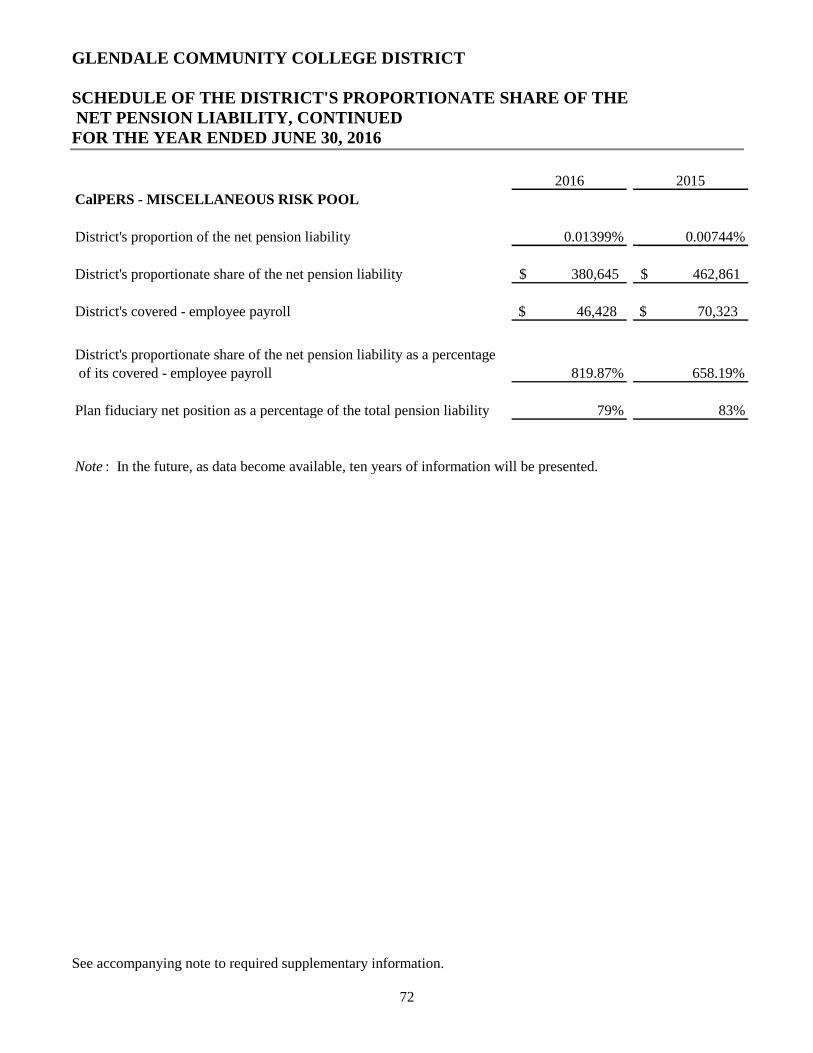

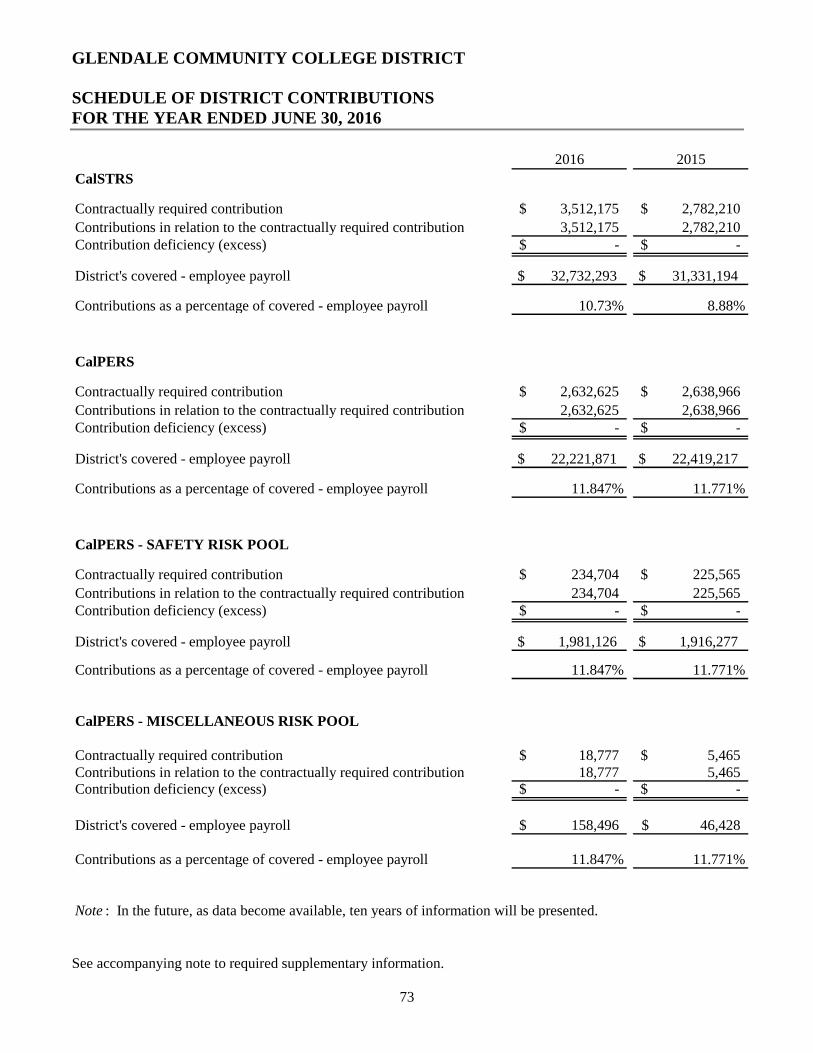

REQUIRED SUPPLEMENTARY INFORMATIONSchedule of Other Postemployment Benefits (OPEB) Funding Progress 70Schedule of the District's Proportionate Share of the Net Pension Liability 71Schedule of District Contributions 73Note to Required Supplementary Information 74

SUPPLEMENTARY INFORMATIONDistrict Organization 76Schedule of Expenditures of Federal Awards 77Schedule of Expenditures of State Awards 79Schedule of Workload Measures for State General Apportionment 80Reconciliation of Education Code 84362 (50 Percent Law) Calculation 81Reconciliation of Annual Financial and Budget Report (CCFS-311) With theFinancial Statements 83Proposition 30 Education Protection Act (EPA) Expenditure Report 84Reconciliation of Governmental Funds to the Statement of Net Position 85Note to Supplementary Information 87

INDEPENDENT AUDITOR'S REPORTSReport on Internal Control Over Financial Reporting and on Compliance and OtherMatters Based on an Audit of Financial Statements Performed in Accordance WithGovernment Auditing Standards 90

Report on Compliance for Each Major Program and on Internal Control OverCompliance Required by the Uniform Guidance 92

Report on State Compliance 95

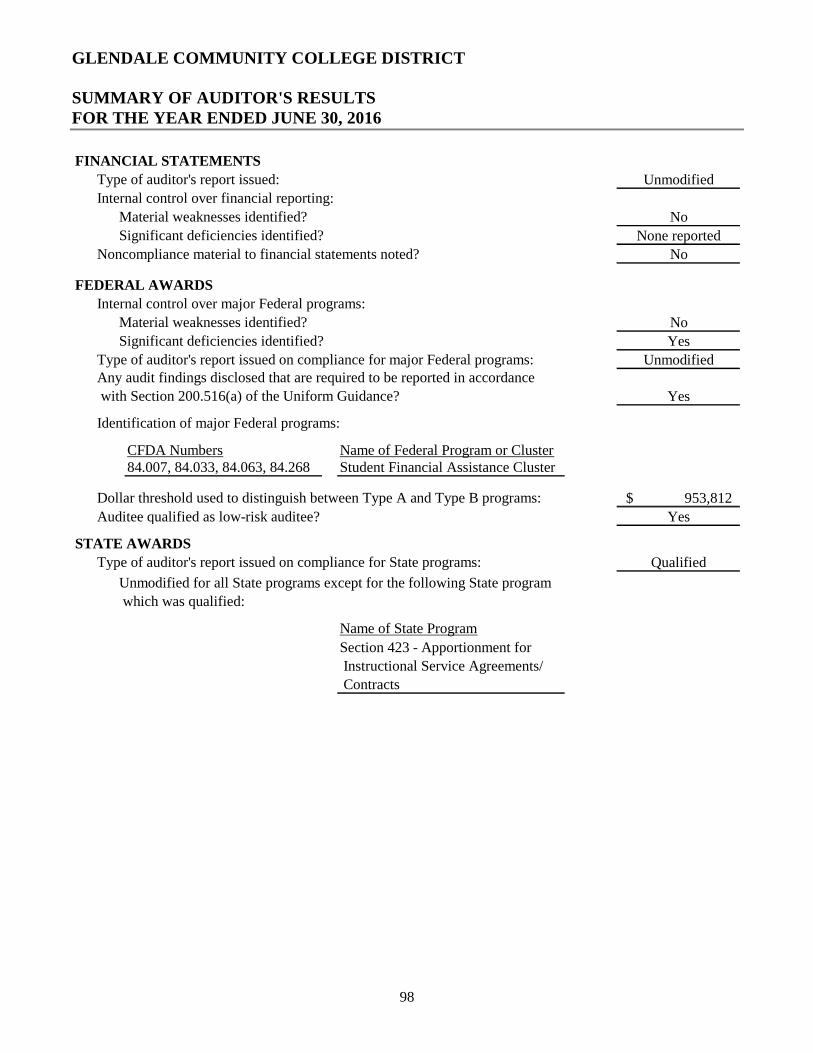

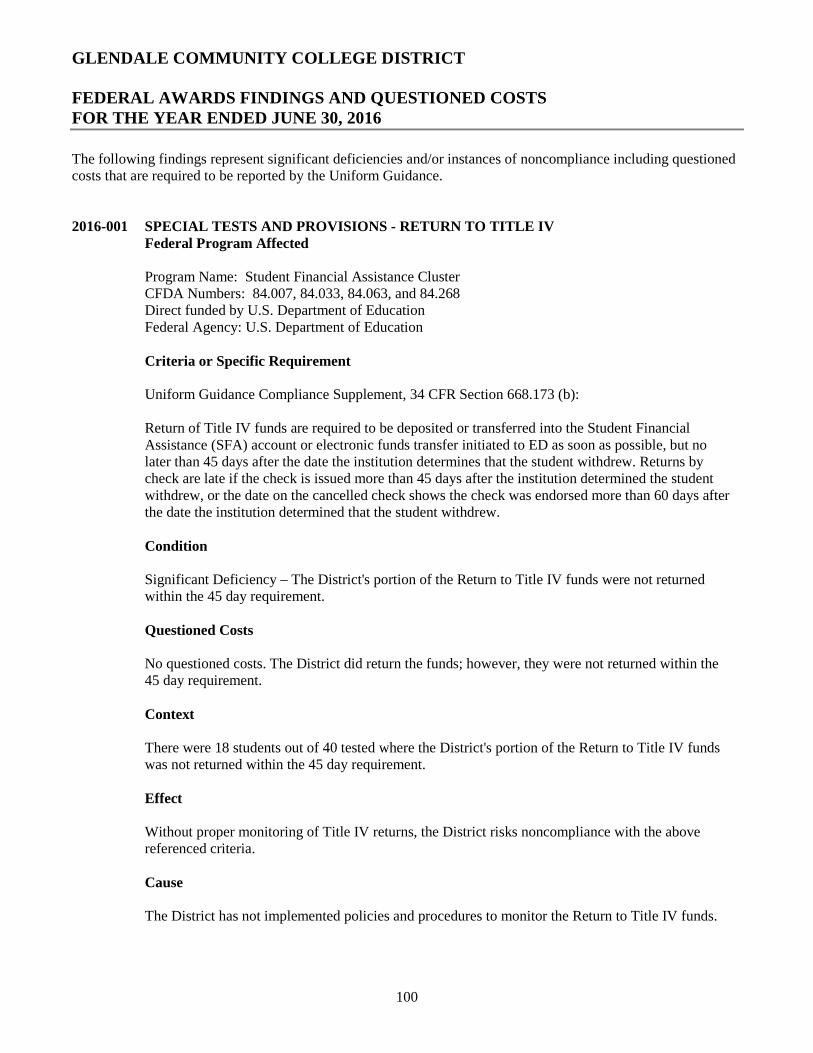

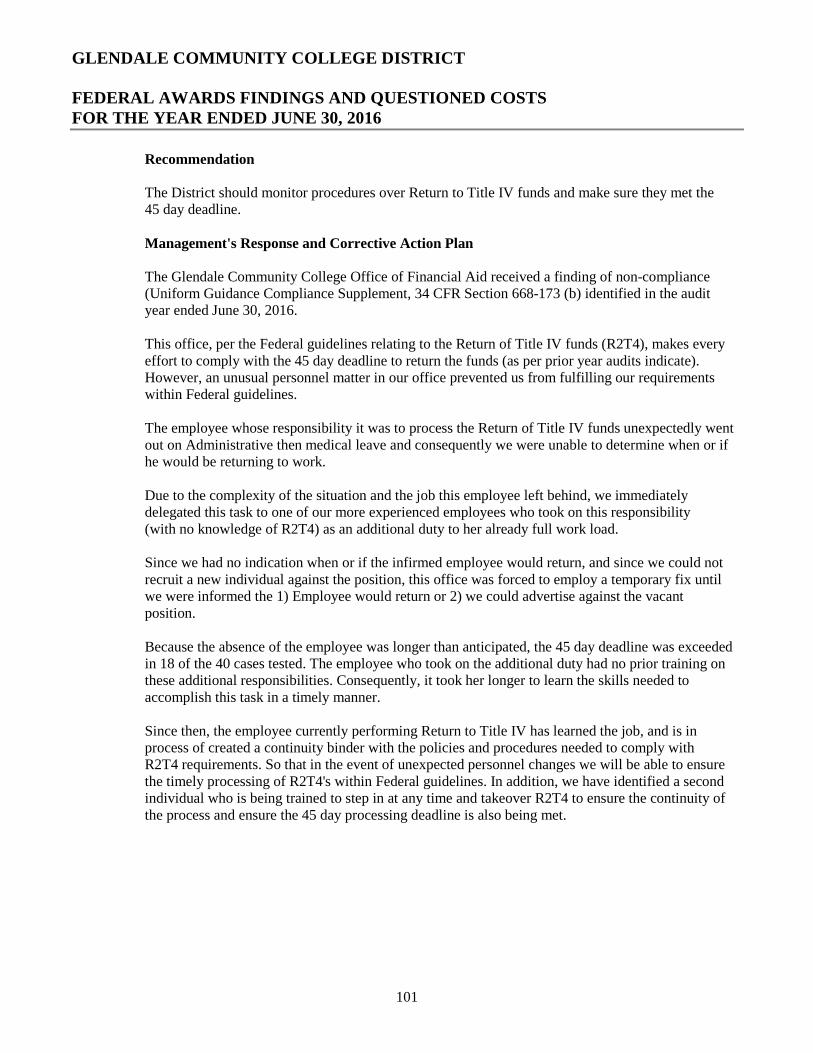

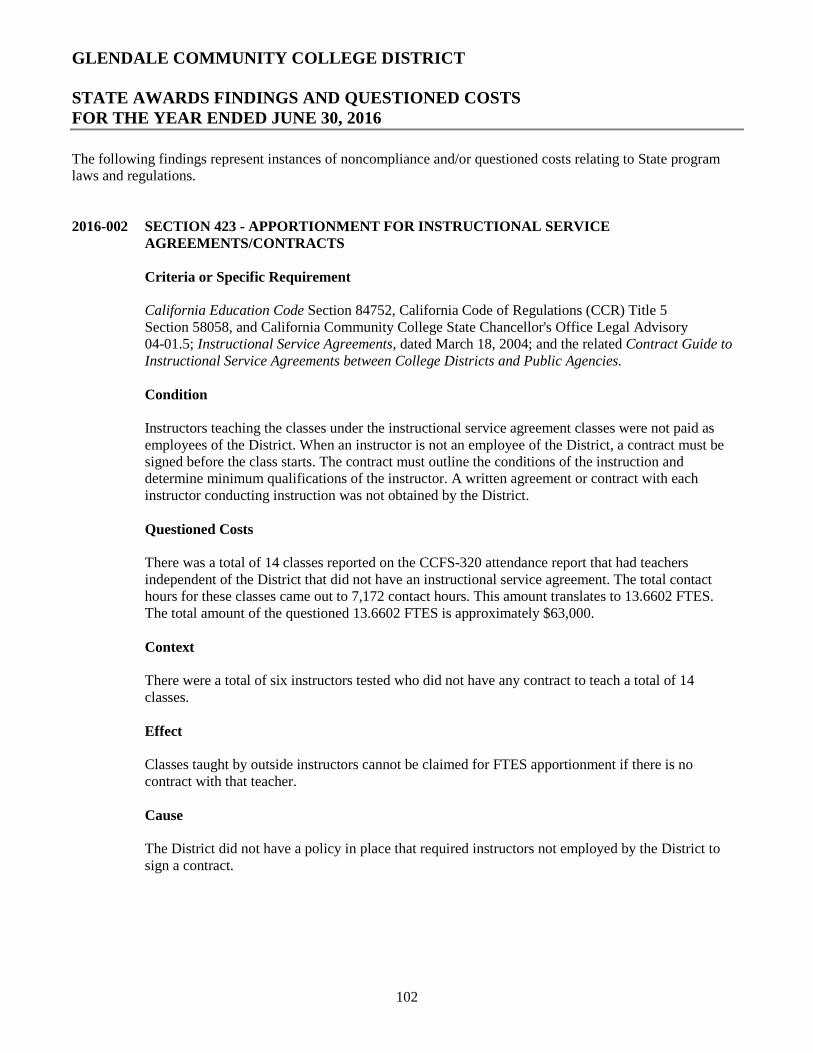

SCHEDULE OF FINDINGS AND QUESTIONED COSTSSummary of Auditor's Results 98Financial Statement Findings and Recommendations 99Federal Awards Findings and Questioned Costs 100State Awards Findings and Questioned Costs 102Summary Schedule of Prior Audit Findings 104

1

FINANCIAL SECTION

10681 Foothill Blvd., Suite 300 Rancho Cucamonga, CA 91730 Tel: 909.466.4410 www.vtdcpa.com Fax: 909.466.4431

Vavrinek, Trine, Day & Co., LLPCertified Public Accountants

VALUE THE D IFFERENCE

2

INDEPENDENT AUDITOR'S REPORT

Board of TrusteesGlendale Community College DistrictGlendale, California

Report on the Financial Statements

We have audited the accompanying financial statements of the business-type activities and the aggregateremaining fund information of Glendale Community College District (the District) as of and for the year endedJune 30, 2016, and the related notes to the financial statements, which collectively comprise the District's basicfinancial statements as listed in the Table of Contents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordancewith accounting principles generally accepted in the United States of America; this includes the design,implementation, and maintenance of internal control relevant to the preparation and fair presentation of financialstatements that are free from material misstatements, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted ouraudit in accordance with auditing standards generally accepted in the United States of America and the standardsapplicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General ofthe United States, and the 2015-2016 Contracted District Audit Manual, issued by the California CommunityColleges Chancellor's Office. Those standards require that we plan and perform the audit to obtain reasonableassurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in thefinancial statements. The procedures selected depend on the auditor's judgment, including the assessment of therisks of material misstatement of the financial statements, whether due to fraud or error. In making those riskassessments, the auditor considers internal control relevant to the District's preparation and fair presentation of thefinancial statements in order to design audit procedures that are appropriate in the circumstances, but not for thepurpose of expressing an opinion on the effectiveness of the District's internal control. Accordingly, we expressno such opinion. An audit also includes evaluating the appropriateness of accounting policies used and thereasonableness of significant accounting estimates made by management, as well as evaluating the overallpresentation of the financial statements.

We believe the audit evidence we have obtained is sufficient and appropriate to provide a basis for our auditopinion.

3

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the respectivefinancial position of the business-type activities and the aggregate remaining fund information of the District as ofJune 30, 2016, and the respective changes in financial position and cash flows thereof for the year then ended inaccordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require the Management's Discussionand Analysis on pages 5 through 12, the Schedule of Other Postemployment Benefits (OPEB) Funding Progress onpage 70, the Schedule of the District's Proportionate Share of the Net Pension Liability on pages 71 through 72,and the Schedule of District Contributions on page 73 be presented to supplement the basic financial statements.Such information, although not a part of the basic financial statements, is required by the GovernmentalAccounting Standards Board, who considers it to be an essential part of financial reporting for placing the basicfinancial statements in an appropriate operational, economic, or historical context. We have applied certain limitedprocedures to the required supplementary information in accordance with auditing standards generally accepted inthe United States of America, which consisted of inquiries of management about the methods of preparing theinformation and comparing the information for consistency with management's responses to our inquiries, the basicfinancial statements, and other knowledge we obtained during our audit of the basic financial statements. We donot express an opinion or provide any assurance on the information because the limited procedures do not provideus with sufficient evidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectivelycomprise the District's basic financial statements. The accompanying supplementary information listed in theTable of Contents, including the Schedule of Expenditures of Federal Awards, as required by Title 2 U.S. Code ofFederal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and AuditRequirements for Federal Awards, is presented for purposes of additional analysis and is not a required part of thebasic financial statements.

The accompanying supplementary information is the responsibility of management and was derived from andrelates directly to the underlying accounting and other records used to prepare the basic financial statements.Such information has been subjected to the auditing procedures applied in the audit of the basic financialstatements and certain additional procedures, including comparing and reconciling such information directly tothe underlying accounting and other records used to prepare the basic financial statements or to the basic financialstatements themselves, and other additional procedures in accordance with auditing standards generally acceptedin the United States of America. In our opinion, the accompanying supplementary information is fairly stated, inall material respects, in relation to the basic financial statements as a whole.

4

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated December 21, 2016, onour consideration of the District's internal control over financial reporting and on our tests of its compliance withcertain provisions of laws, regulations, contracts, grant agreements, and other matters. The purpose of that reportis to describe the scope of our testing of internal control over financial reporting and compliance and the results ofthat testing, and not to provide an opinion on the internal control over financial reporting or on compliance. Thatreport is an integral part of an audit performed in accordance with Government Auditing Standards in consideringthe District's internal control over financial reporting and compliance.

Rancho Cucamonga, CaliforniaDecember 21, 2016

Dr. David ViarSuperintendent/President

BOARD OF TRUSTEESAnita Quinonez Gabrielian

Dr. Armine HacopianDr. Vahé Peroomian

Ann H. RansfordAnthony P. Tartaglia

1500 North Verdugo Road • Glendale, CA 91208-2894 • 818-240-1000 • fax: 818-549-9436 • www.glendale.edu

5

In June 1999, the Governmental Accounting Standards Board (GASB) issued Statement No. 34, Basic FinancialStatements and Management's Discussion and Analysis for State and Local Governments, which established anew reporting format for annual financial statements of governmental entities. In November 1999, GASBreleased Statement No. 35, Basic Financial Statements and Management's Discussion and Analysis for PublicColleges and Universities, which applies the new reporting standards to public colleges and universities.

The California Community Colleges Chancellor's Office has recommended that all State community collegesfollow the Business-Type Activity (BTA) model for financial statement reporting purposes.

The following discussion and analysis complies with the GASB standard and provides an overview of GlendaleCommunity College District's (the District) financial position and activities for the year ended June 30, 2016, withselected comparative information for the year ended June 30, 2015. This discussion has been prepared bymanagement and should be read in conjunction with the financial statements and the notes which follow thissection. Responsibility for the completeness and accuracy of this information rests with the District management.

As required by generally accepted accounting principles, the annual report consists of three basic financialstatements that provide information on the District as a whole:

The Statement of Net Position

The Statement of Revenue, Expenses, and Changes in Net Position

The Statement of Cash Flows

Each of these statements will be discussed.

FINANCIAL AND ENROLLMENT HIGHLIGHTS

Reported enrollment at the District decreased in 2015-2016. Credit enrollment decreased about 0.9 percent.Noncredit enrollment decreased about 0.96 percent from 2014-2015.

Nonresident enrollment increased almost 3.0 percent in 2015-2016.

The District ended the year with an unrestricted General Fund balance of $11.1 million. This was an increaseof approximately $6.4 million from the prior year due to one-time State allocations.

The District ending fund balance increased from 5.63 percent to 11.96 percent due to one-time Stateallocations.

GLENDALE COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2016

6

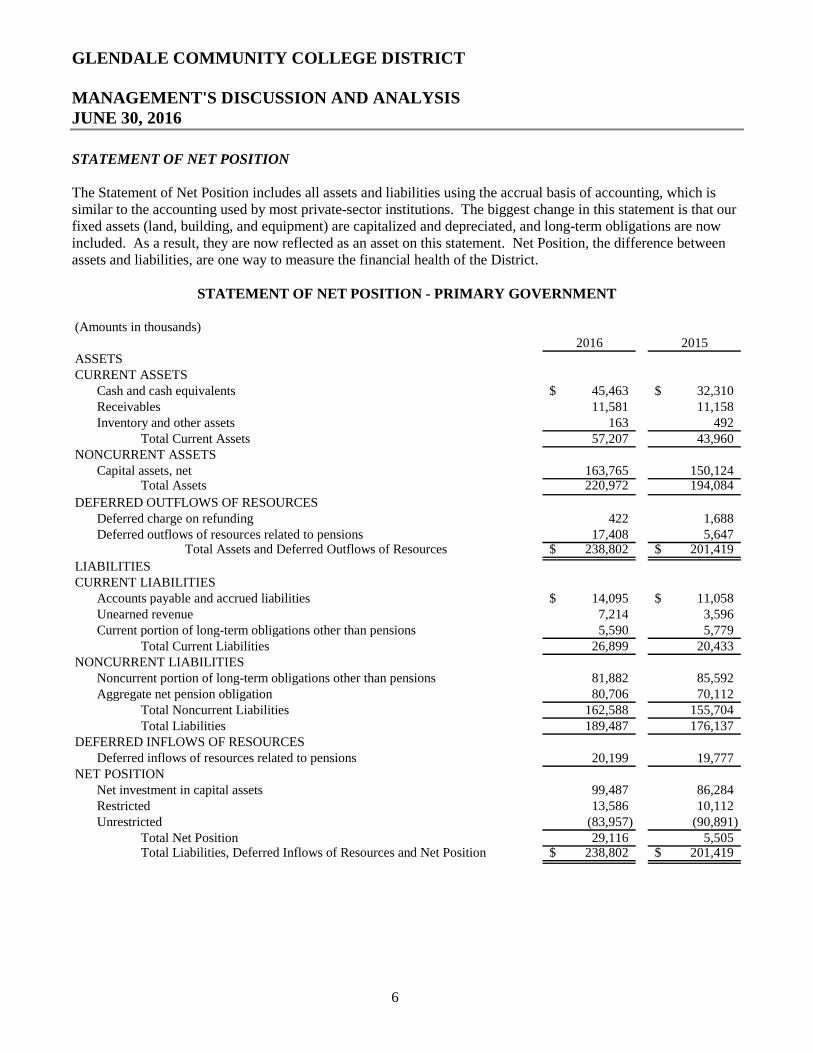

STATEMENT OF NET POSITION

The Statement of Net Position includes all assets and liabilities using the accrual basis of accounting, which issimilar to the accounting used by most private-sector institutions. The biggest change in this statement is that ourfixed assets (land, building, and equipment) are capitalized and depreciated, and long-term obligations are nowincluded. As a result, they are now reflected as an asset on this statement. Net Position, the difference betweenassets and liabilities, are one way to measure the financial health of the District.

STATEMENT OF NET POSITION - PRIMARY GOVERNMENT

(Amounts in thousands)2016 2015

ASSETSCURRENT ASSETS

Cash and cash equivalents 45,463$ 32,310$Receivables 11,581 11,158Inventory and other assets 163 492

Total Current Assets 57,207 43,960NONCURRENT ASSETS

Capital assets, net 163,765 150,124Total Assets 220,972 194,084

DEFERRED OUTFLOWS OF RESOURCESDeferred charge on refunding 422 1,688Deferred outflows of resources related to pensions 17,408 5,647

Total Assets and Deferred Outflows of Resources 238,802$ 201,419$

LIABILITIESCURRENT LIABILITIES

Accounts payable and accrued liabilities 14,095$ 11,058$Unearned revenue 7,214 3,596Current portion of long-term obligations other than pensions 5,590 5,779

Total Current Liabilities 26,899 20,433NONCURRENT LIABILITIES

Noncurrent portion of long-term obligations other than pensions 81,882 85,592Aggregate net pension obligation 80,706 70,112

Total Noncurrent Liabilities 162,588 155,704Total Liabilities 189,487 176,137

DEFERRED INFLOWS OF RESOURCESDeferred inflows of resources related to pensions 20,199 19,777

NET POSITIONNet investment in capital assets 99,487 86,284Restricted 13,586 10,112Unrestricted (83,957) (90,891)

Total Net Position 29,116 5,505Total Liabilities, Deferred Inflows of Resources and Net Position 238,802$ 201,419$

GLENDALE COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2016

7

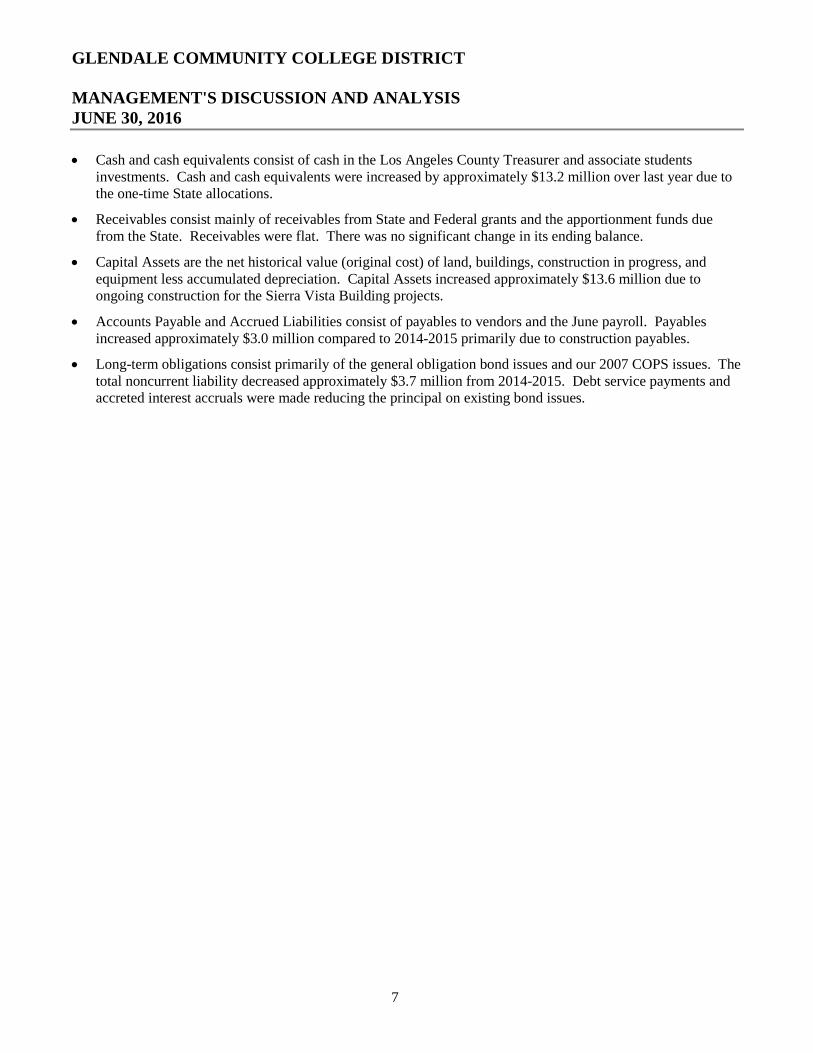

Cash and cash equivalents consist of cash in the Los Angeles County Treasurer and associate studentsinvestments. Cash and cash equivalents were increased by approximately $13.2 million over last year due tothe one-time State allocations.

Receivables consist mainly of receivables from State and Federal grants and the apportionment funds duefrom the State. Receivables were flat. There was no significant change in its ending balance.

Capital Assets are the net historical value (original cost) of land, buildings, construction in progress, andequipment less accumulated depreciation. Capital Assets increased approximately $13.6 million due toongoing construction for the Sierra Vista Building projects.

Accounts Payable and Accrued Liabilities consist of payables to vendors and the June payroll. Payablesincreased approximately $3.0 million compared to 2014-2015 primarily due to construction payables.

Long-term obligations consist primarily of the general obligation bond issues and our 2007 COPS issues. Thetotal noncurrent liability decreased approximately $3.7 million from 2014-2015. Debt service payments andaccreted interest accruals were made reducing the principal on existing bond issues.

GLENDALE COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2016

8

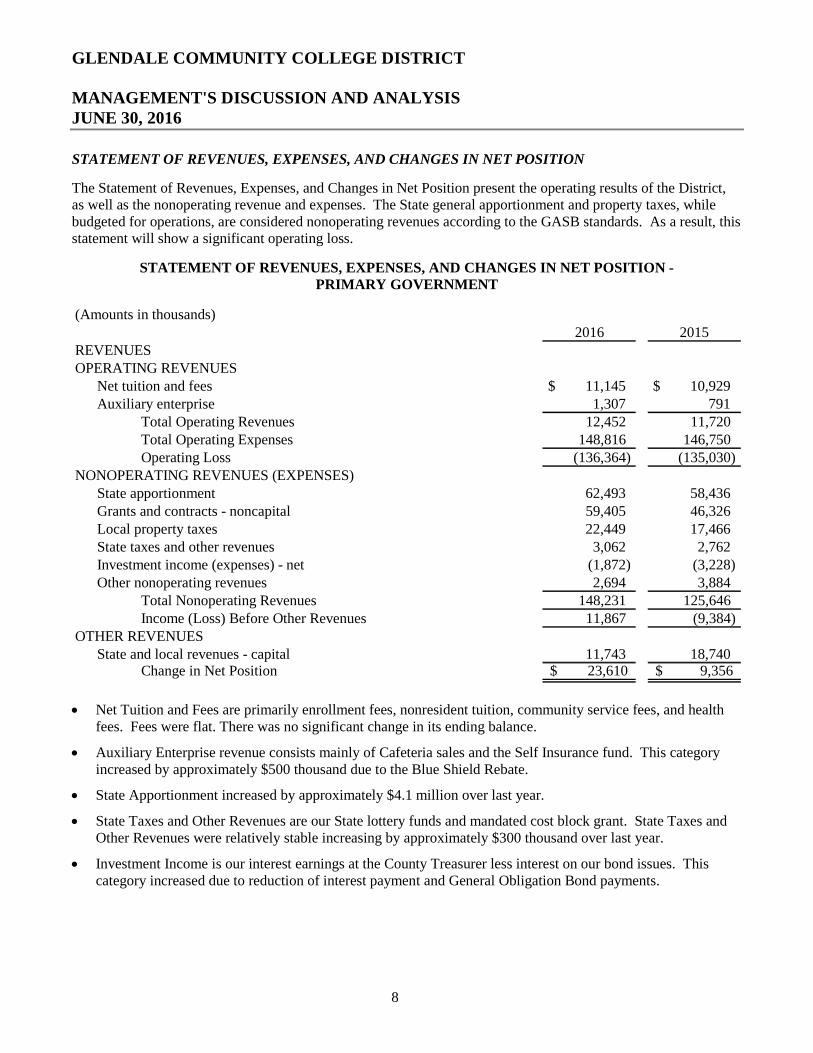

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION

The Statement of Revenues, Expenses, and Changes in Net Position present the operating results of the District,as well as the nonoperating revenue and expenses. The State general apportionment and property taxes, whilebudgeted for operations, are considered nonoperating revenues according to the GASB standards. As a result, thisstatement will show a significant operating loss.

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION -PRIMARY GOVERNMENT

(Amounts in thousands)2016 2015

REVENUESOPERATING REVENUES

Net tuition and fees 11,145$ 10,929$Auxiliary enterprise 1,307 791

Total Operating Revenues 12,452 11,720Total Operating Expenses 148,816 146,750Operating Loss (136,364) (135,030)

NONOPERATING REVENUES (EXPENSES)State apportionment 62,493 58,436Grants and contracts - noncapital 59,405 46,326Local property taxes 22,449 17,466State taxes and other revenues 3,062 2,762Investment income (expenses) - net (1,872) (3,228)Other nonoperating revenues 2,694 3,884

Total Nonoperating Revenues 148,231 125,646Income (Loss) Before Other Revenues 11,867 (9,384)

OTHER REVENUESState and local revenues - capital 11,743 18,740

Change in Net Position 23,610$ 9,356$

Net Tuition and Fees are primarily enrollment fees, nonresident tuition, community service fees, and healthfees. Fees were flat. There was no significant change in its ending balance.

Auxiliary Enterprise revenue consists mainly of Cafeteria sales and the Self Insurance fund. This categoryincreased by approximately $500 thousand due to the Blue Shield Rebate.

State Apportionment increased by approximately $4.1 million over last year.

State Taxes and Other Revenues are our State lottery funds and mandated cost block grant. State Taxes andOther Revenues were relatively stable increasing by approximately $300 thousand over last year.

Investment Income is our interest earnings at the County Treasurer less interest on our bond issues. Thiscategory increased due to reduction of interest payment and General Obligation Bond payments.

GLENDALE COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2016

9

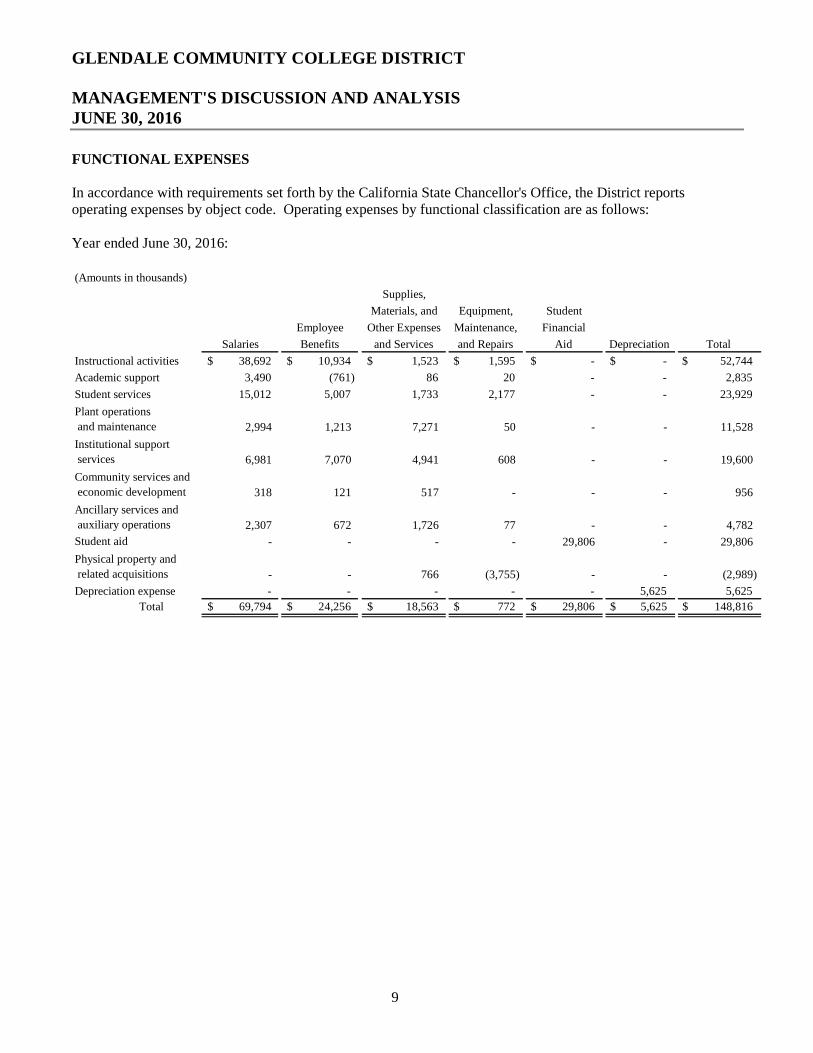

FUNCTIONAL EXPENSES

In accordance with requirements set forth by the California State Chancellor's Office, the District reportsoperating expenses by object code. Operating expenses by functional classification are as follows:

Year ended June 30, 2016:

(Amounts in thousands)

Supplies,

Materials, and Equipment, Student

Employee Other Expenses Maintenance, Financial

Salaries Benefits and Services and Repairs Aid Depreciation Total

Instructional activities 38,692$ 10,934$ 1,523$ 1,595$ -$ -$ 52,744$

Academic support 3,490 (761) 86 20 - - 2,835

Student services 15,012 5,007 1,733 2,177 - - 23,929

Plant operations

and maintenance 2,994 1,213 7,271 50 - - 11,528

Institutional support

services 6,981 7,070 4,941 608 - - 19,600

Community services and

economic development 318 121 517 - - - 956

Ancillary services and

auxiliary operations 2,307 672 1,726 77 - - 4,782

Student aid - - - - 29,806 - 29,806

Physical property and

related acquisitions - - 766 (3,755) - - (2,989)

Depreciation expense - - - - - 5,625 5,625

Total 69,794$ 24,256$ 18,563$ 772$ 29,806$ 5,625$ 148,816$

GLENDALE COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2016

10

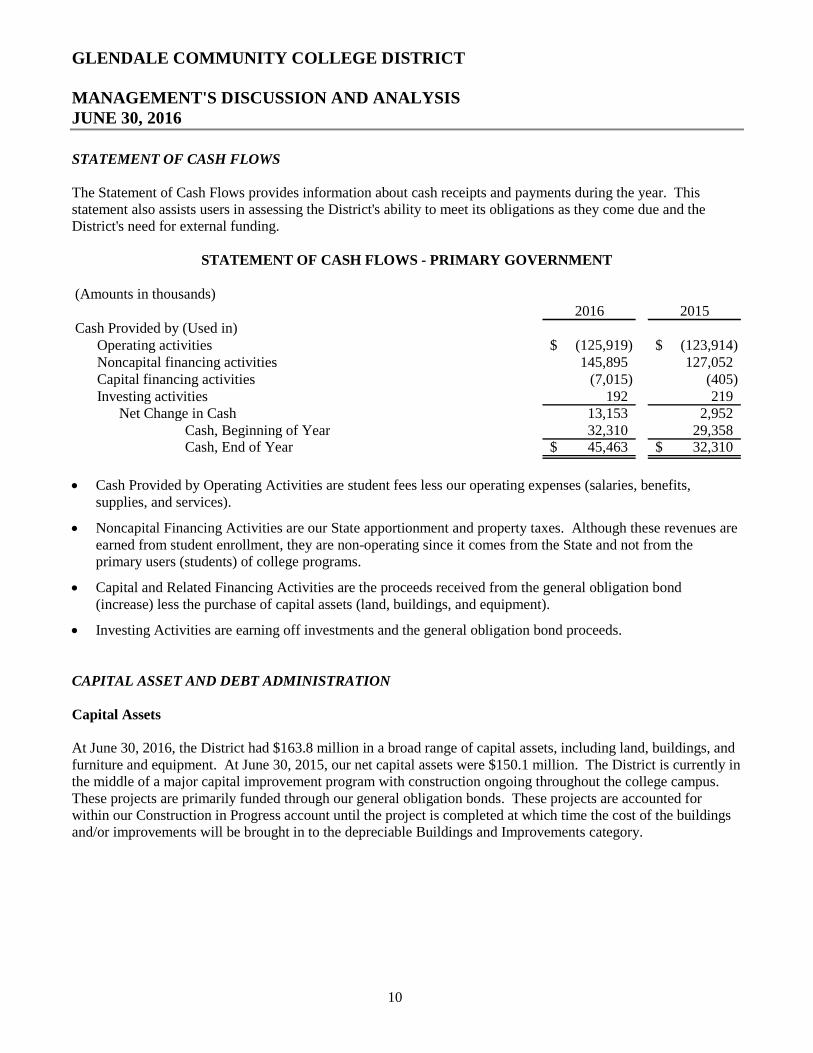

STATEMENT OF CASH FLOWS

The Statement of Cash Flows provides information about cash receipts and payments during the year. Thisstatement also assists users in assessing the District's ability to meet its obligations as they come due and theDistrict's need for external funding.

STATEMENT OF CASH FLOWS - PRIMARY GOVERNMENT

(Amounts in thousands)2016 2015

Cash Provided by (Used in)Operating activities (125,919)$ (123,914)$Noncapital financing activities 145,895 127,052Capital financing activities (7,015) (405)Investing activities 192 219

Net Change in Cash 13,153 2,952Cash, Beginning of Year 32,310 29,358Cash, End of Year 45,463$ 32,310$

Cash Provided by Operating Activities are student fees less our operating expenses (salaries, benefits,supplies, and services).

Noncapital Financing Activities are our State apportionment and property taxes. Although these revenues areearned from student enrollment, they are non-operating since it comes from the State and not from theprimary users (students) of college programs.

Capital and Related Financing Activities are the proceeds received from the general obligation bond(increase) less the purchase of capital assets (land, buildings, and equipment).

Investing Activities are earning off investments and the general obligation bond proceeds.

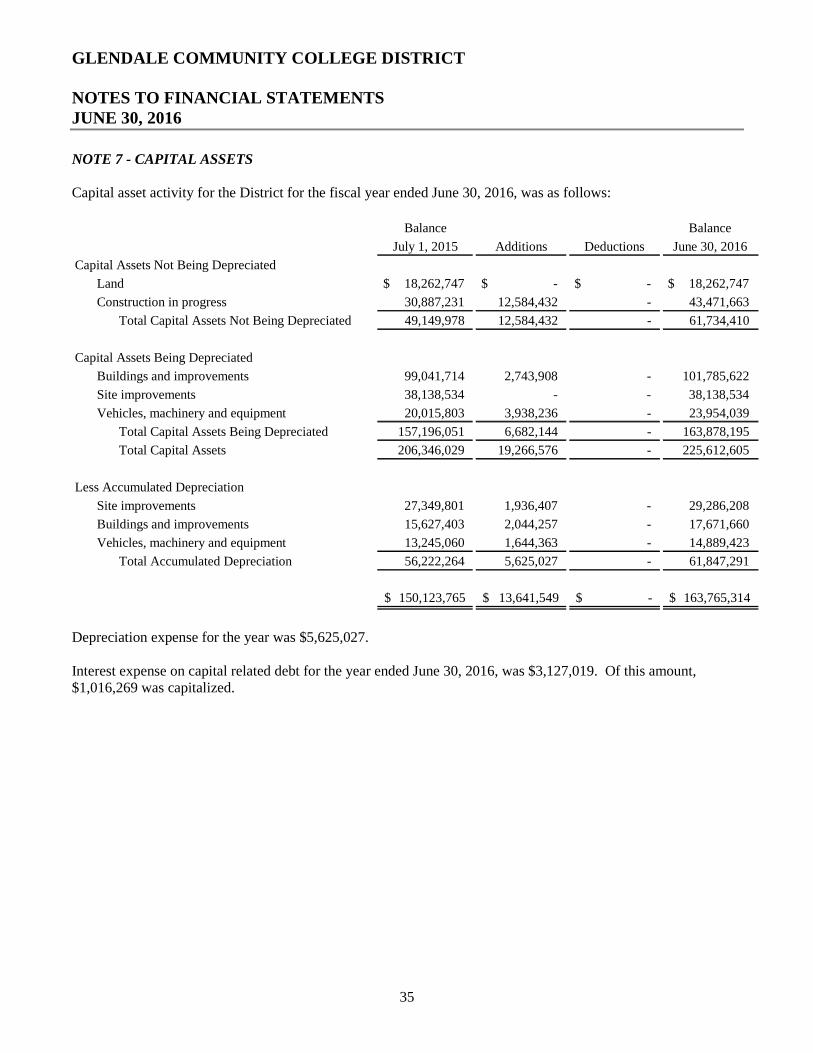

CAPITAL ASSET AND DEBT ADMINISTRATION

Capital Assets

At June 30, 2016, the District had $163.8 million in a broad range of capital assets, including land, buildings, andfurniture and equipment. At June 30, 2015, our net capital assets were $150.1 million. The District is currently inthe middle of a major capital improvement program with construction ongoing throughout the college campus.These projects are primarily funded through our general obligation bonds. These projects are accounted forwithin our Construction in Progress account until the project is completed at which time the cost of the buildingsand/or improvements will be brought in to the depreciable Buildings and Improvements category.

GLENDALE COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2016

11

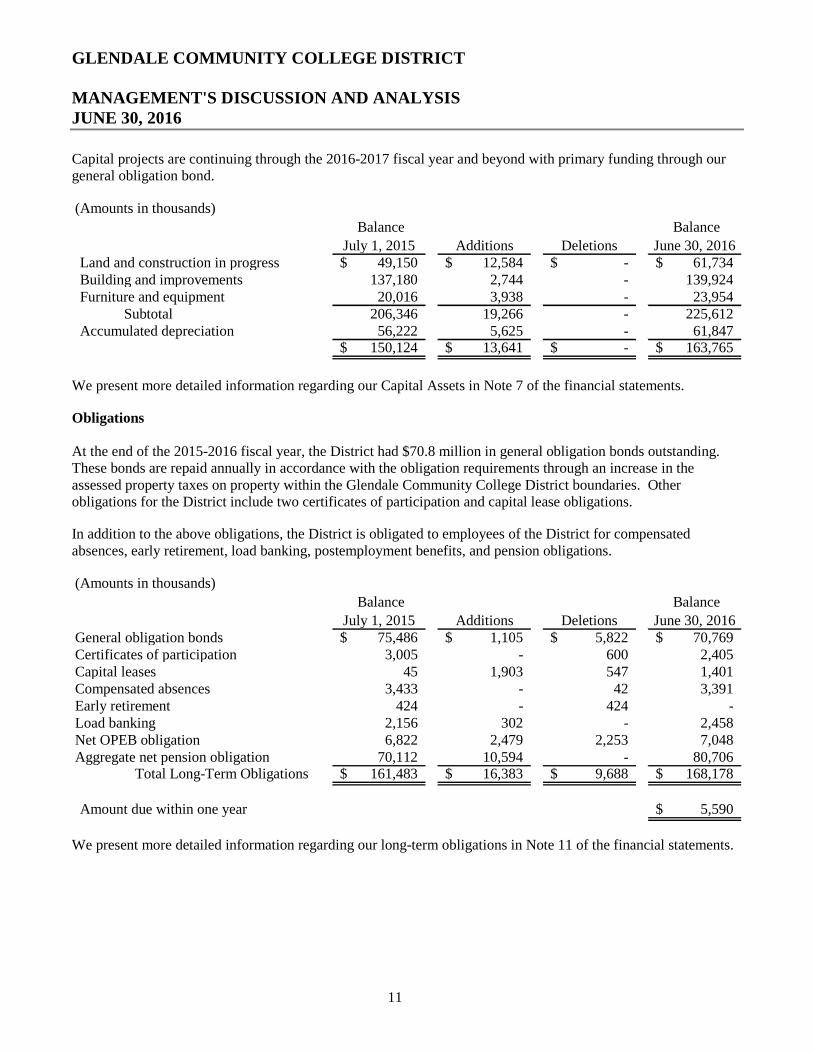

Capital projects are continuing through the 2016-2017 fiscal year and beyond with primary funding through ourgeneral obligation bond.

(Amounts in thousands)

Balance

July 1, 2015 Additions Deletions

Balance

June 30, 2016Land and construction in progress 49,150$ 12,584$ -$ 61,734$Building and improvements 137,180 2,744 - 139,924Furniture and equipment 20,016 3,938 - 23,954

Subtotal 206,346 19,266 - 225,612Accumulated depreciation 56,222 5,625 - 61,847

150,124$ 13,641$ -$ 163,765$

We present more detailed information regarding our Capital Assets in Note 7 of the financial statements.

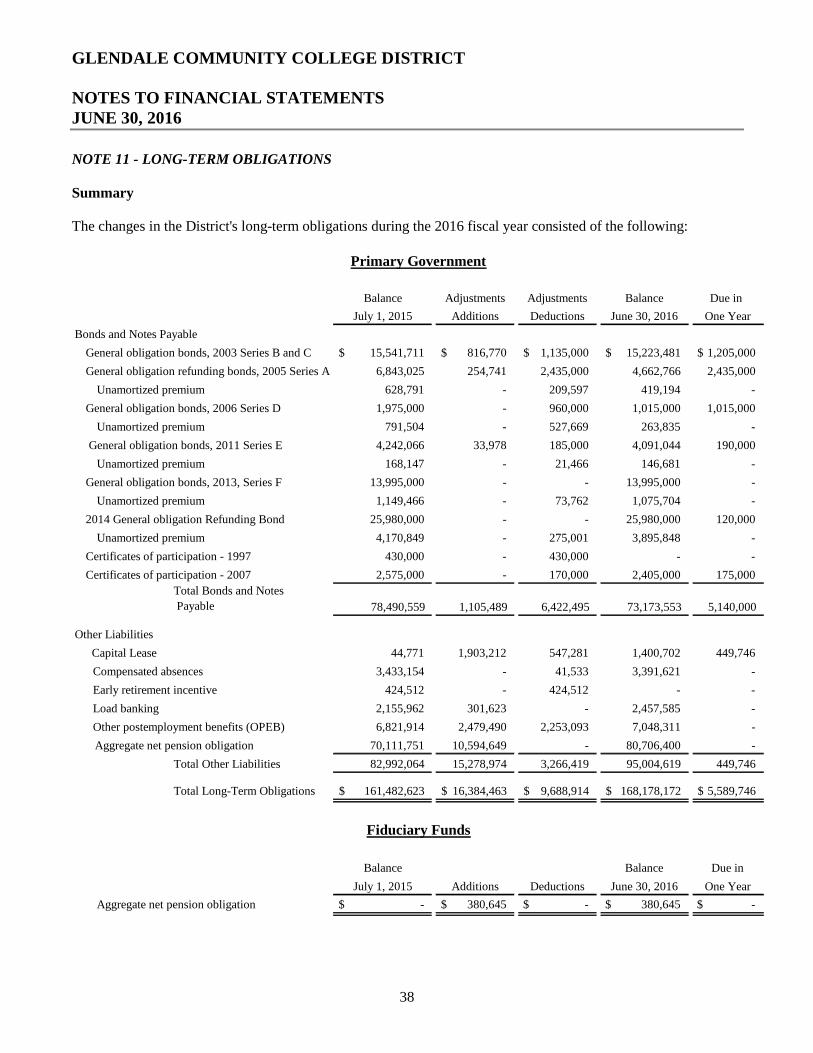

Obligations

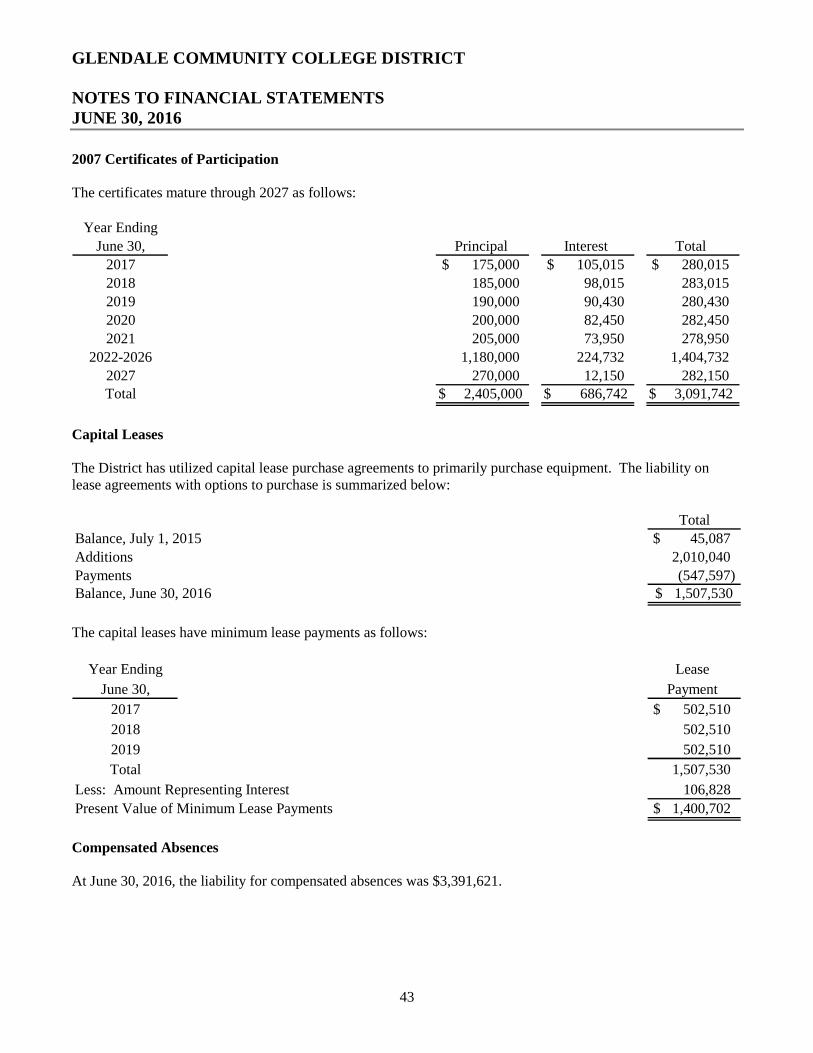

At the end of the 2015-2016 fiscal year, the District had $70.8 million in general obligation bonds outstanding.These bonds are repaid annually in accordance with the obligation requirements through an increase in theassessed property taxes on property within the Glendale Community College District boundaries. Otherobligations for the District include two certificates of participation and capital lease obligations.

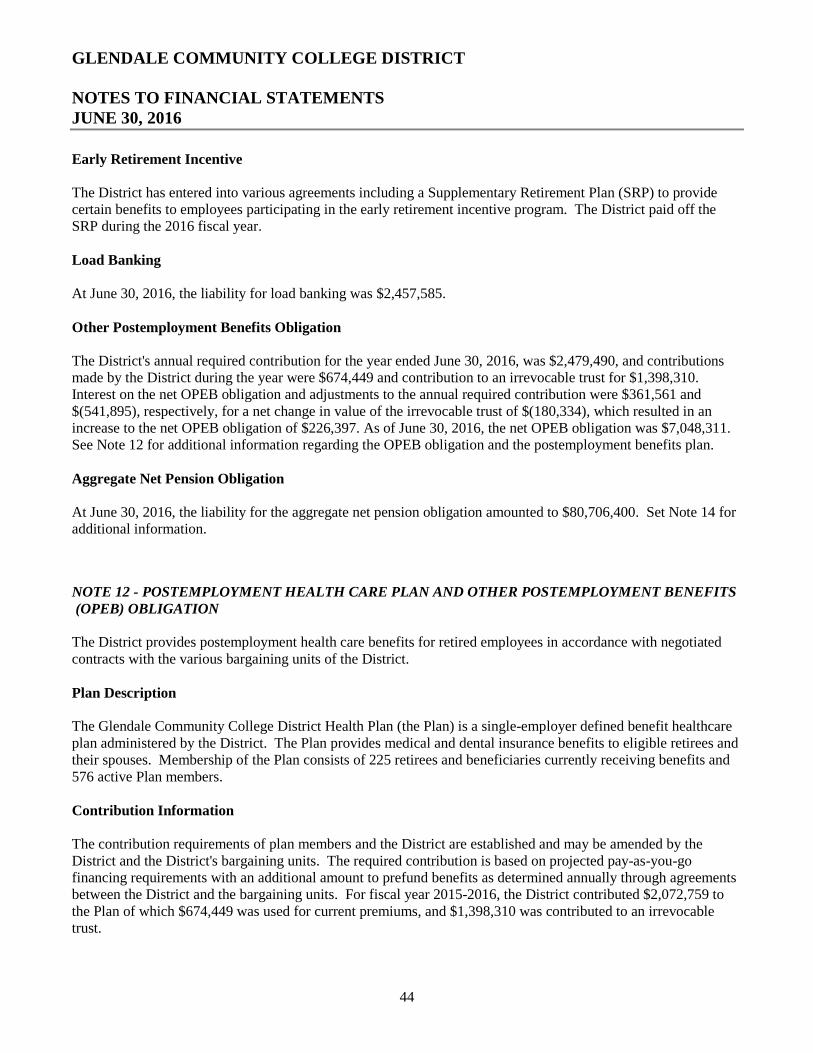

In addition to the above obligations, the District is obligated to employees of the District for compensatedabsences, early retirement, load banking, postemployment benefits, and pension obligations.

(Amounts in thousands)

Balance

July 1, 2015 Additions Deletions

Balance

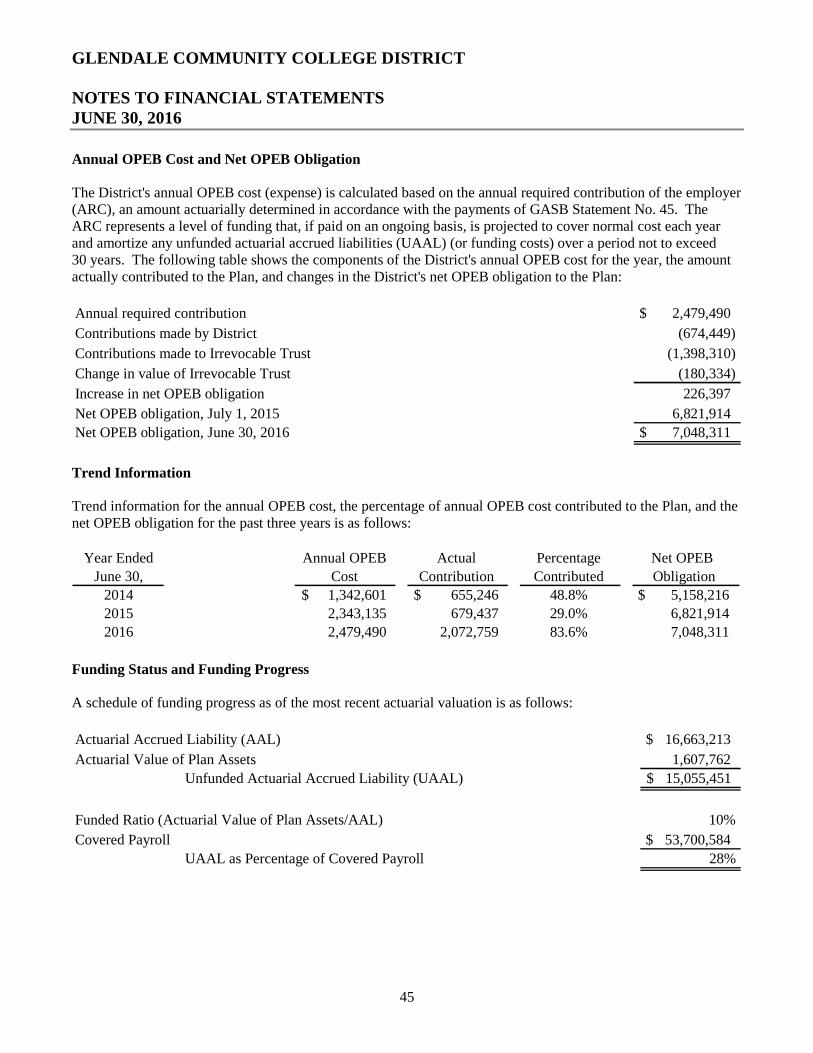

June 30, 2016General obligation bonds 75,486$ 1,105$ 5,822$ 70,769$Certificates of participation 3,005 - 600 2,405Capital leases 45 1,903 547 1,401Compensated absences 3,433 - 42 3,391Early retirement 424 - 424 -Load banking 2,156 302 - 2,458Net OPEB obligation 6,822 2,479 2,253 7,048Aggregate net pension obligation 70,112 10,594 - 80,706

Total Long-Term Obligations 161,483$ 16,383$ 9,688$ 168,178$

Amount due within one year 5,590$

We present more detailed information regarding our long-term obligations in Note 11 of the financial statements.

GLENDALE COMMUNITY COLLEGE DISTRICT

MANAGEMENT'S DISCUSSION AND ANALYSISJUNE 30, 2016

12

ECONOMIC FACTORS THAT MAY AFFECT THE FUTURE

The November 8, 2016 election had several positive outcomes for the Glendale Community College District(GCCD). The extension of Proposition 30 (income tax), after it expires on December 31, 2018, will continue for12 additional years in the form of Proposition 55. This extension will provide continual access to approximately$13 million dollars per year to support instructional costs. In addition, the approval of Proposition 51 included$2 billion dollars earmarked for Community Colleges. GCCD will be able to submit construction projects tocompete for those financial resources. Finally, GCCD's local GC Bond was approved by 73 percent of the voters.This local bond measure totals $325 million dollars. These monies will be used to improve the GCCD campusesand facilities as stated in the bond ballot language.

Although the one-quarter of percent sales tax increase which was also initiated by the Governor's tax initiative(Proposition 30) will sunset at the end of 2016, Proposition 2 (Governor's Rainy Day Fund) could be used by theGovernor to cover revenue short falls. The Governor has expressed caution even with the improved State economy,there are still concerns with the loss of $4-$5 billion when sales tax rates revert back to the pre-Proposition 30level.

The State's economy continues to improve with tax receipts far exceeding initial estimates. As a result, the StateBudget provides significant increases for access, student success, and student equity. The Governor hasappropriated the new funding as "ONE-TIME". The District will be strategically prudent in the allocation of itsone-time funds to avoid any financial problems in the future years.

All of these resources will be used to continually enhance a learning environment to attract new students as well asprovide student support services that will encourage persistence of the existing student body. These activitiescould lead to higher enrollment numbers that could yield larger resource allocations to GCCD from the StateChancellors Office. Enrollment is the biggest concern with the college's budget. Enrollment was flat in 2014-2015and 772 FTEs from Summer 2015 were shifted to the 2014-2015 fiscal year to maximize revenue. The college willcontinue to use this State Chancellor's Office approved method of shifting FTES through 2018-2019. The collegehas implemented a strategic touchpoint strategy as it continues to look into ways to become more effective in itsenrollment management.

CONTACTING THE DISTRICT'S FINANCIAL MANAGEMENT

This financial report is designed to provide our citizens, taxpayers, students, and investors and creditors with ageneral overview of the District's finances and to demonstrate the District's accountability for the money itreceives. If you have any questions about this report or need additional financial information, contact the Districtat: Glendale Community College District, 1500 North Verdugo Road, Glendale, CA 91208.

GLENDALE COMMUNITY COLLEGE DISTRICT

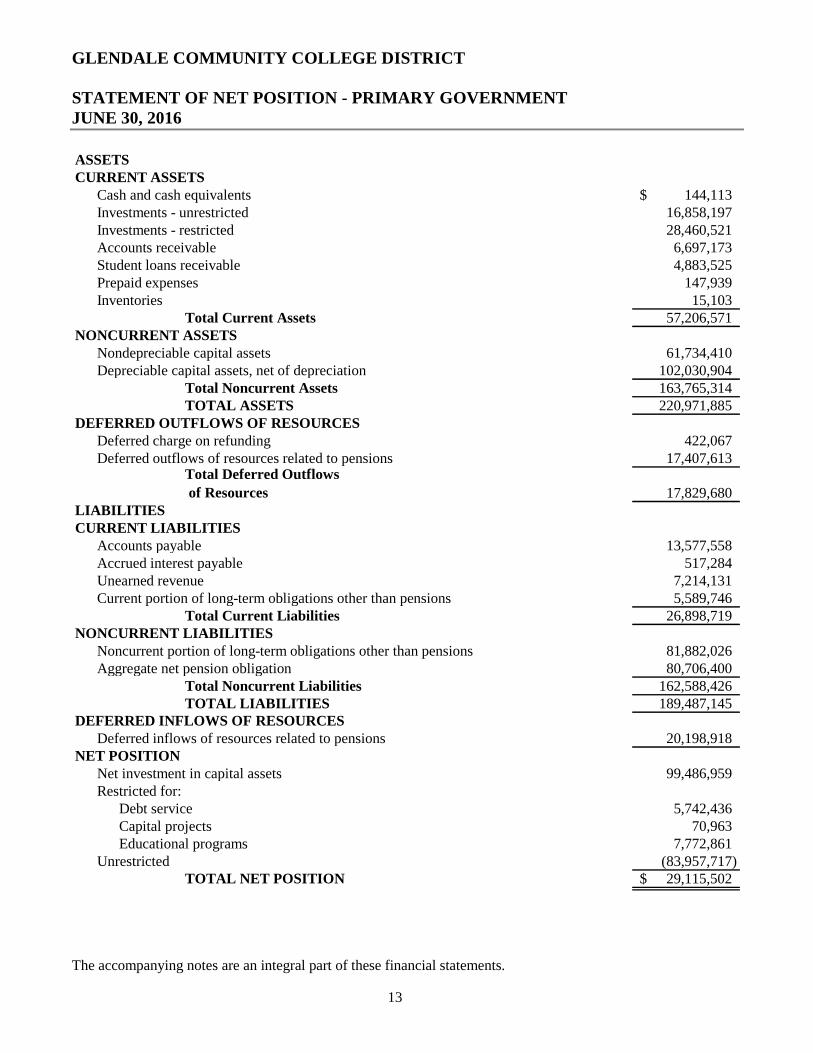

STATEMENT OF NET POSITION - PRIMARY GOVERNMENTJUNE 30, 2016

The accompanying notes are an integral part of these financial statements.

13

ASSETSCURRENT ASSETS

Cash and cash equivalents 144,113$Investments - unrestricted 16,858,197Investments - restricted 28,460,521Accounts receivable 6,697,173Student loans receivable 4,883,525Prepaid expenses 147,939Inventories 15,103

Total Current Assets 57,206,571NONCURRENT ASSETS

Nondepreciable capital assets 61,734,410Depreciable capital assets, net of depreciation 102,030,904

Total Noncurrent Assets 163,765,314TOTAL ASSETS 220,971,885

DEFERRED OUTFLOWS OF RESOURCESDeferred charge on refunding 422,067Deferred outflows of resources related to pensions 17,407,613

Total Deferred Outflows

of Resources 17,829,680LIABILITIESCURRENT LIABILITIES

Accounts payable 13,577,558Accrued interest payable 517,284Unearned revenue 7,214,131Current portion of long-term obligations other than pensions 5,589,746

Total Current Liabilities 26,898,719NONCURRENT LIABILITIES

Noncurrent portion of long-term obligations other than pensions 81,882,026Aggregate net pension obligation 80,706,400

Total Noncurrent Liabilities 162,588,426TOTAL LIABILITIES 189,487,145

DEFERRED INFLOWS OF RESOURCESDeferred inflows of resources related to pensions 20,198,918

NET POSITIONNet investment in capital assets 99,486,959Restricted for:

Debt service 5,742,436Capital projects 70,963Educational programs 7,772,861

Unrestricted (83,957,717)TOTAL NET POSITION 29,115,502$

GLENDALE COMMUNITY COLLEGE DISTRICT

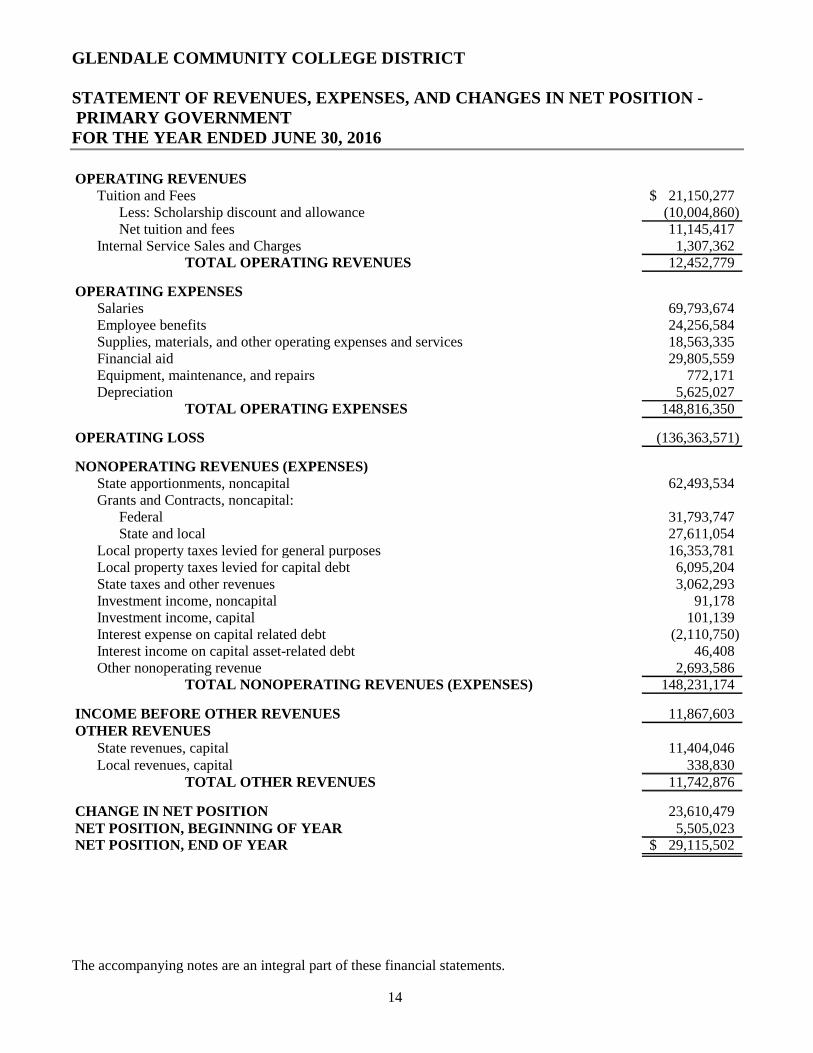

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION -PRIMARY GOVERNMENT

FOR THE YEAR ENDED JUNE 30, 2016

The accompanying notes are an integral part of these financial statements.

14

OPERATING REVENUESTuition and Fees 21,150,277$

Less: Scholarship discount and allowance (10,004,860)Net tuition and fees 11,145,417

Internal Service Sales and Charges 1,307,362TOTAL OPERATING REVENUES 12,452,779

OPERATING EXPENSESSalaries 69,793,674Employee benefits 24,256,584Supplies, materials, and other operating expenses and services 18,563,335Financial aid 29,805,559Equipment, maintenance, and repairs 772,171Depreciation 5,625,027

TOTAL OPERATING EXPENSES 148,816,350

OPERATING LOSS (136,363,571)

NONOPERATING REVENUES (EXPENSES)State apportionments, noncapital 62,493,534Grants and Contracts, noncapital:

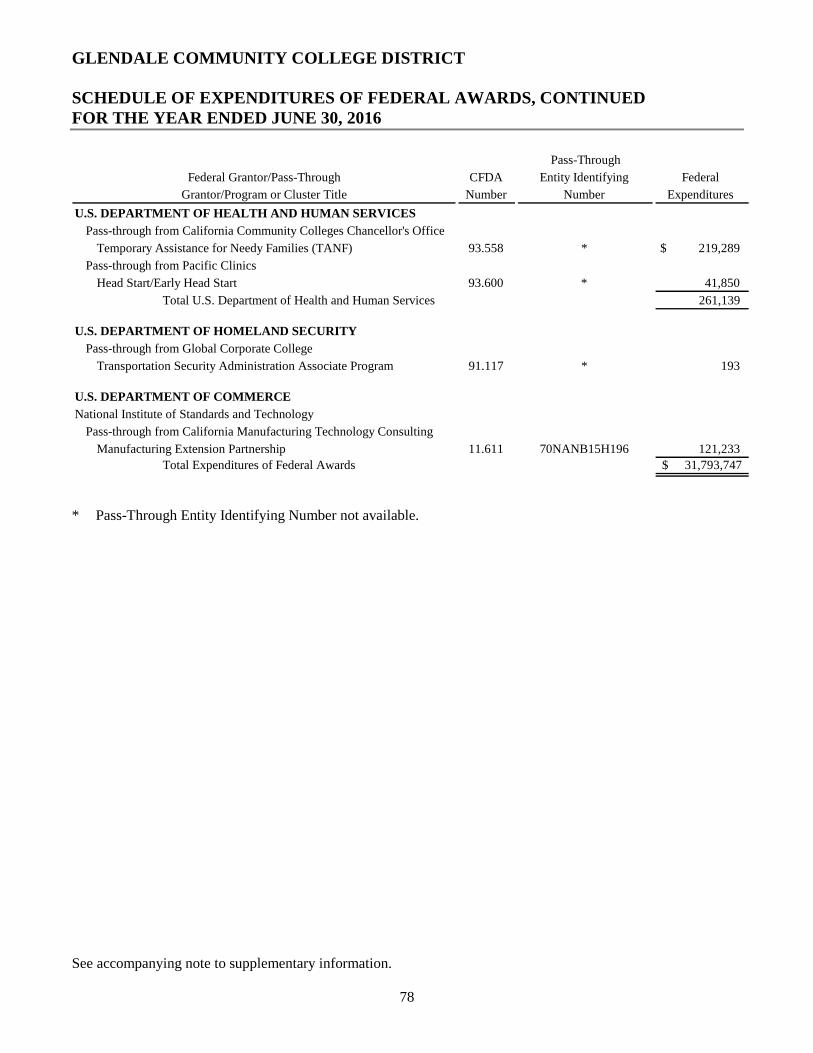

Federal 31,793,747State and local 27,611,054

Local property taxes levied for general purposes 16,353,781Local property taxes levied for capital debt 6,095,204State taxes and other revenues 3,062,293Investment income, noncapital 91,178Investment income, capital 101,139Interest expense on capital related debt (2,110,750)Interest income on capital asset-related debt 46,408Other nonoperating revenue 2,693,586

TOTAL NONOPERATING REVENUES (EXPENSES) 148,231,174

INCOME BEFORE OTHER REVENUES 11,867,603OTHER REVENUES

State revenues, capital 11,404,046Local revenues, capital 338,830

TOTAL OTHER REVENUES 11,742,876

CHANGE IN NET POSITION 23,610,479NET POSITION, BEGINNING OF YEAR 5,505,023NET POSITION, END OF YEAR 29,115,502$

GLENDALE COMMUNITY COLLEGE DISTRICT

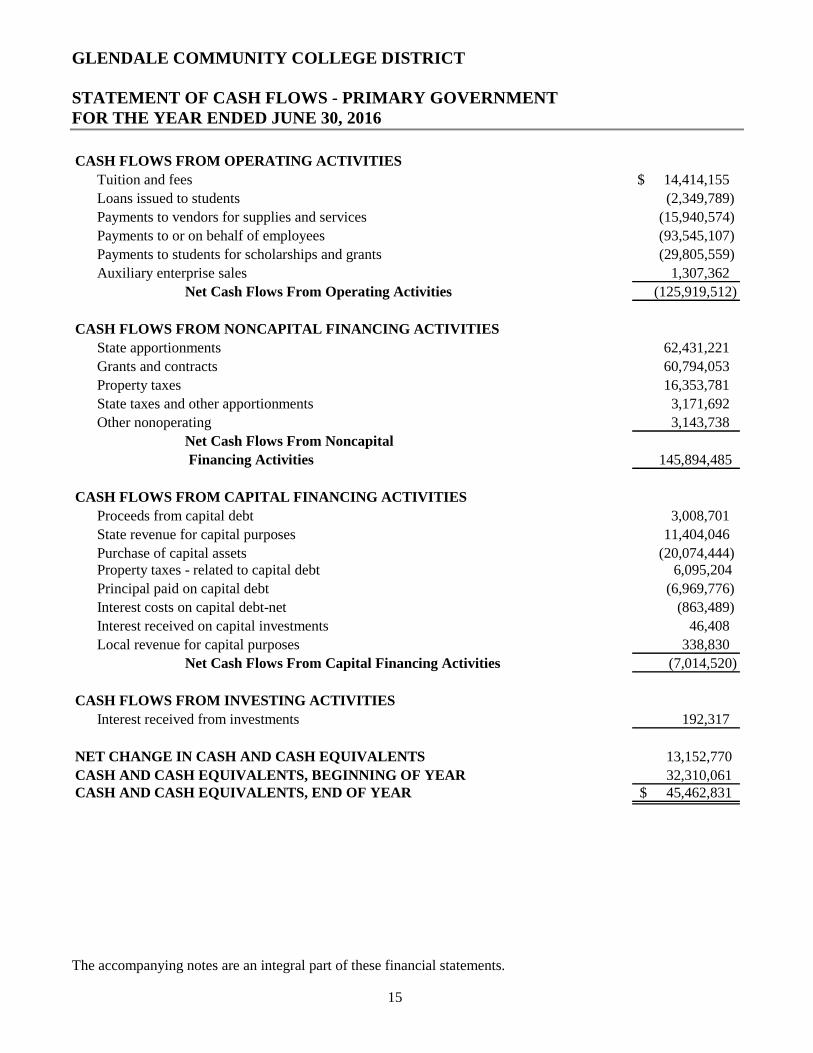

STATEMENT OF CASH FLOWS - PRIMARY GOVERNMENTFOR THE YEAR ENDED JUNE 30, 2016

The accompanying notes are an integral part of these financial statements.

15

CASH FLOWS FROM OPERATING ACTIVITIES

Tuition and fees 14,414,155$

Loans issued to students (2,349,789)

Payments to vendors for supplies and services (15,940,574)

Payments to or on behalf of employees (93,545,107)

Payments to students for scholarships and grants (29,805,559)

Auxiliary enterprise sales 1,307,362

Net Cash Flows From Operating Activities (125,919,512)

CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIES

State apportionments 62,431,221

Grants and contracts 60,794,053

Property taxes 16,353,781

State taxes and other apportionments 3,171,692

Other nonoperating 3,143,738

Net Cash Flows From Noncapital

Financing Activities 145,894,485

CASH FLOWS FROM CAPITAL FINANCING ACTIVITIES

Proceeds from capital debt 3,008,701

State revenue for capital purposes 11,404,046

Purchase of capital assets (20,074,444)Property taxes - related to capital debt 6,095,204

Principal paid on capital debt (6,969,776)

Interest costs on capital debt-net (863,489)

Interest received on capital investments 46,408

Local revenue for capital purposes 338,830

Net Cash Flows From Capital Financing Activities (7,014,520)

CASH FLOWS FROM INVESTING ACTIVITIES

Interest received from investments 192,317

NET CHANGE IN CASH AND CASH EQUIVALENTS 13,152,770

CASH AND CASH EQUIVALENTS, BEGINNING OF YEAR 32,310,061CASH AND CASH EQUIVALENTS, END OF YEAR 45,462,831$

GLENDALE COMMUNITY COLLEGE DISTRICT

STATEMENT OF CASH FLOWS - PRIMARY GOVERNMENT, CONTINUEDFOR THE YEAR ENDED JUNE 30, 2016

The accompanying notes are an integral part of these financial statements.

16

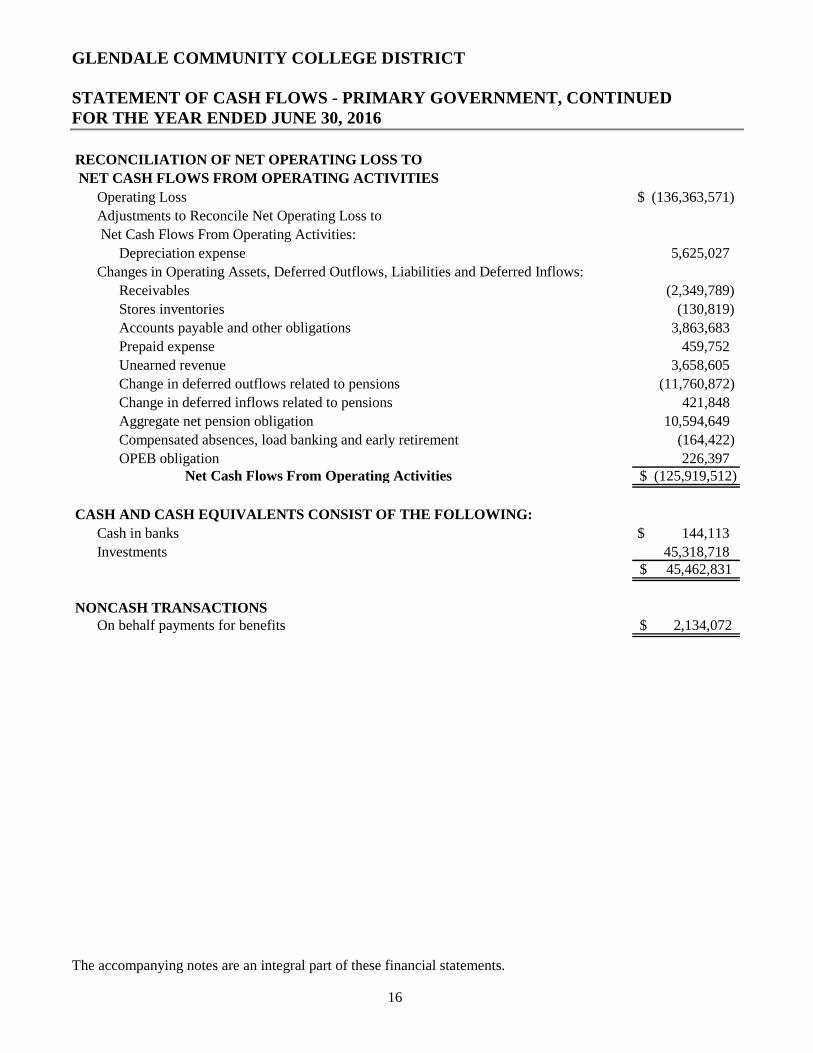

RECONCILIATION OF NET OPERATING LOSS TO

NET CASH FLOWS FROM OPERATING ACTIVITIES

Operating Loss (136,363,571)$

Adjustments to Reconcile Net Operating Loss to

Net Cash Flows From Operating Activities:

Depreciation expense 5,625,027

Changes in Operating Assets, Deferred Outflows, Liabilities and Deferred Inflows:

Receivables (2,349,789)

Stores inventories (130,819)

Accounts payable and other obligations 3,863,683

Prepaid expense 459,752

Unearned revenue 3,658,605

Change in deferred outflows related to pensions (11,760,872)

Change in deferred inflows related to pensions 421,848

Aggregate net pension obligation 10,594,649

Compensated absences, load banking and early retirement (164,422)

OPEB obligation 226,397Net Cash Flows From Operating Activities (125,919,512)$

CASH AND CASH EQUIVALENTS CONSIST OF THE FOLLOWING:

Cash in banks 144,113$

Investments 45,318,71845,462,831$

NONCASH TRANSACTIONSOn behalf payments for benefits 2,134,072$

GLENDALE COMMUNITY COLLEGE DISTRICT

STATEMENT OF FIDUCIARY NET POSITIONJUNE 30, 2016

The accompanying notes are an integral part of these financial statements.

17

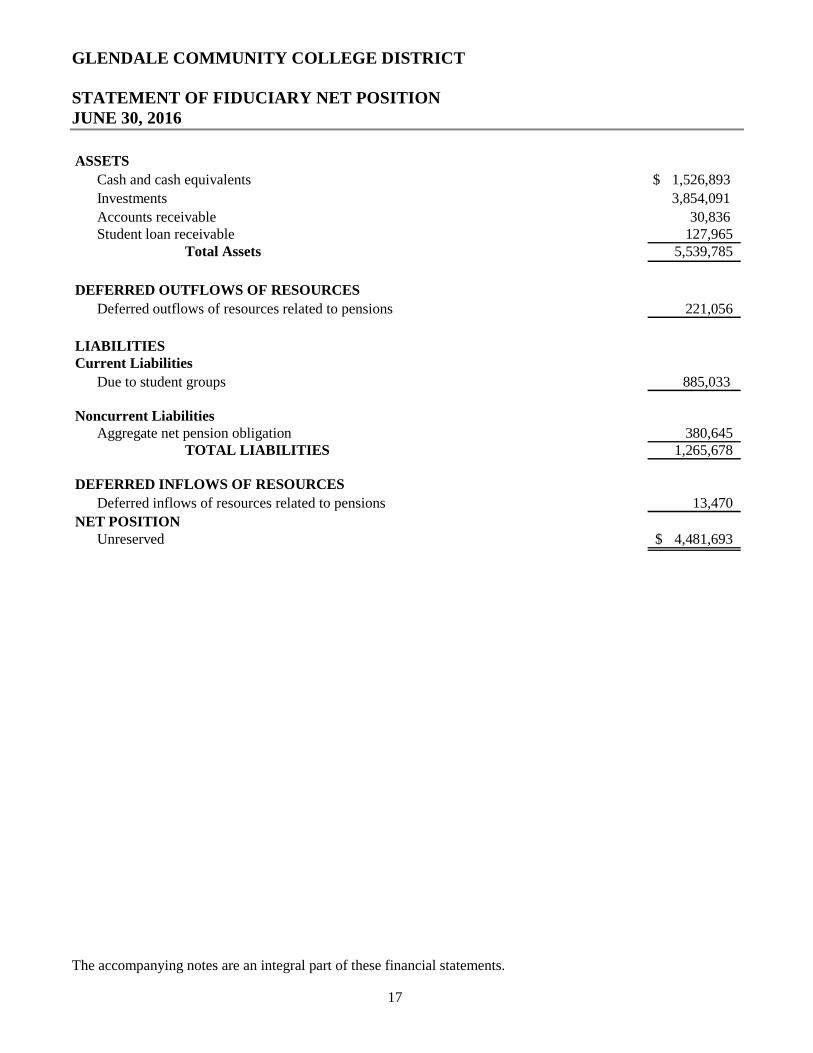

ASSETS

Cash and cash equivalents 1,526,893$

Investments 3,854,091

Accounts receivable 30,836Student loan receivable 127,965

Total Assets 5,539,785

DEFERRED OUTFLOWS OF RESOURCES

Deferred outflows of resources related to pensions 221,056

LIABILITIESCurrent Liabilities

Due to student groups 885,033

Noncurrent LiabilitiesAggregate net pension obligation 380,645

TOTAL LIABILITIES 1,265,678

DEFERRED INFLOWS OF RESOURCES

Deferred inflows of resources related to pensions 13,470

NET POSITIONUnreserved 4,481,693$

GLENDALE COMMUNITY COLLEGE DISTRICT

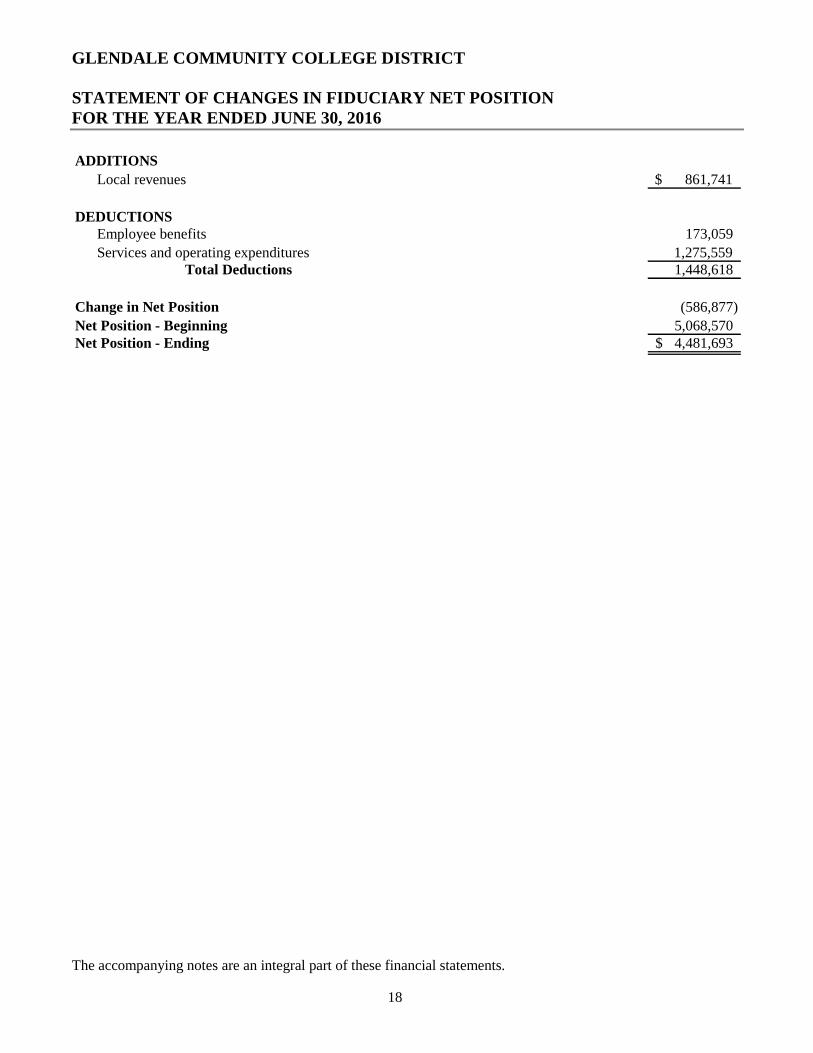

STATEMENT OF CHANGES IN FIDUCIARY NET POSITIONFOR THE YEAR ENDED JUNE 30, 2016

The accompanying notes are an integral part of these financial statements.

18

ADDITIONS

Local revenues 861,741$

DEDUCTIONSEmployee benefits 173,059

Services and operating expenditures 1,275,559Total Deductions 1,448,618

Change in Net Position (586,877)

Net Position - Beginning 5,068,570Net Position - Ending 4,481,693$

GLENDALE COMMUNITY COLLEGE DISTRICT

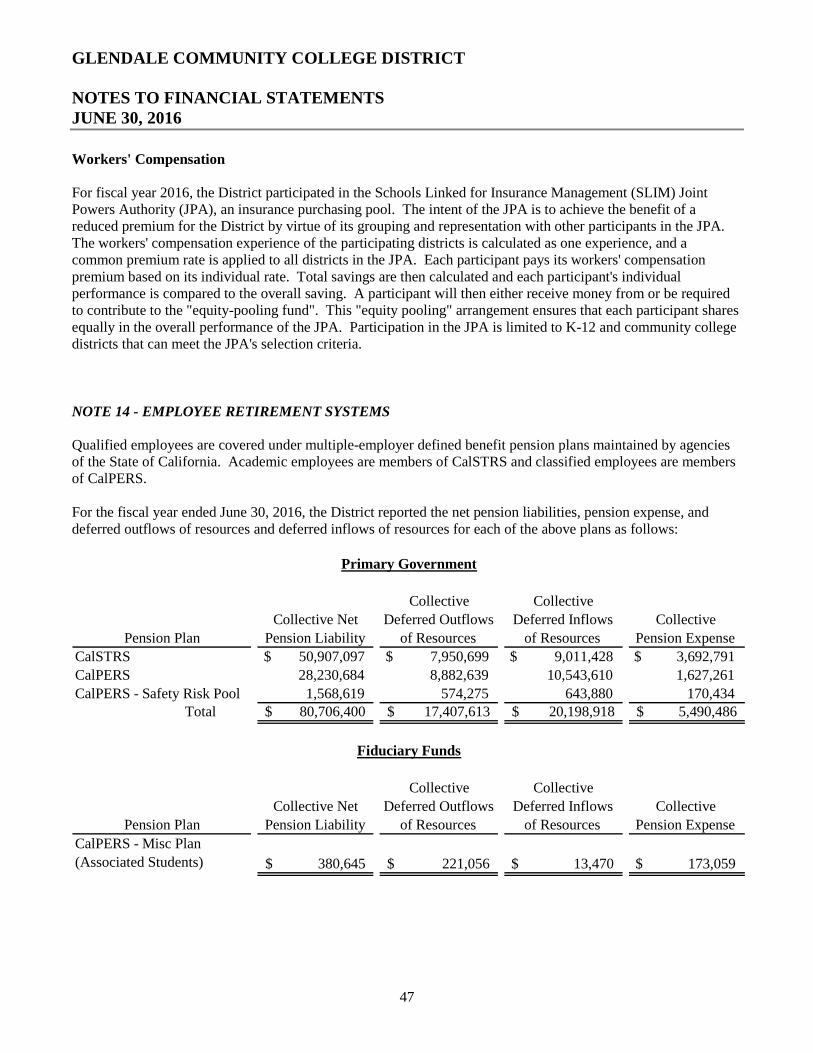

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

19

NOTE 1 - ORGANIZATION

The Glendale Community College District (the District) was established in 1983 as a political subdivision of theState of California and is a comprehensive, public, two-year institution offering educational services to residentsof the surrounding area. The District operates under a locally elected five-member Board of Trustees form ofgovernment, which establishes the policies and procedures by which the District operates. The Board mustapprove the annual budgets for the General Fund, special revenue funds, and capital project funds, but thesebudgets are managed at the department level. Currently, the District operates one community college and onecenter located in Glendale, California. While the District is a political subdivision of the State of California, it islegally separate and is independent of other State and local governments, and it is not a component unit of theState in accordance with the provisions of Governmental Accounting Standards Board (GASB) Statement No. 61.The District is classified as a Public Educational Institution under Internal Revenue Code Section 115 and is,therefore, exempt from Federal taxes.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Financial Reporting Entity

The District has adopted GASB Statement No. 61, Determining Whether Certain Organizations are ComponentUnits. This statement amends Statement No. 14, The Financial Reporting Entity, to provide additional guidanceto determine whether certain organizations, for which the District is not financially accountable, should bereported as component units based on the nature and significance of their relationship with the District. The threecomponents used to determine the presentation are: providing a "direct benefit", the "environment and ability toaccess/influence reporting", and the "significance" criterion. As defined by accounting principles generallyaccepted in the United States of America and established by the Governmental Accounting Standards Board, thefinancial reporting entity consists of the primary government, the District, and the following component unit:

The Los Angeles County Schools Regionalized Business Service Corporation

The Los Angeles County Schools Regionalized Business Service Corporation (the Corporation) is a legallyseparate organization and a component unit of the District. The Corporation was formed to issue debtspecifically for the acquisition and construction of capital assets for the District. The financial activity hasbeen "blended" or consolidated within the financial statements of the District as if the activity was theDistrict's. The activity is included as the Other Debt Service Fund. Certificates of participation issued by theCorporation are included as long-term obligations of the District. Individually-prepared financial statementsare not prepared for the Los Angeles County Schools Regionalized Business Service Corporation.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

20

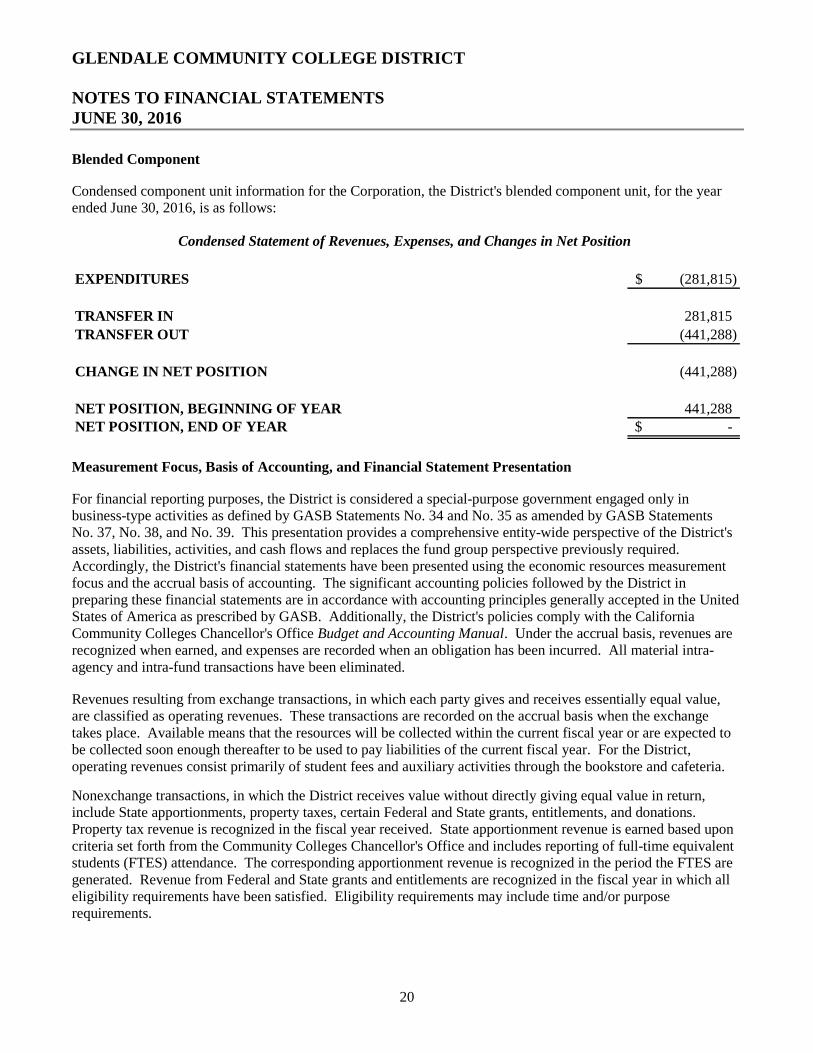

Blended Component

Condensed component unit information for the Corporation, the District's blended component unit, for the yearended June 30, 2016, is as follows:

EXPENDITURES (281,815)$

TRANSFER IN 281,815

TRANSFER OUT (441,288)

CHANGE IN NET POSITION (441,288)

NET POSITION, BEGINNING OF YEAR 441,288NET POSITION, END OF YEAR -$

Condensed Statement of Revenues, Expenses, and Changes in Net Position

Measurement Focus, Basis of Accounting, and Financial Statement Presentation

For financial reporting purposes, the District is considered a special-purpose government engaged only inbusiness-type activities as defined by GASB Statements No. 34 and No. 35 as amended by GASB StatementsNo. 37, No. 38, and No. 39. This presentation provides a comprehensive entity-wide perspective of the District'sassets, liabilities, activities, and cash flows and replaces the fund group perspective previously required.Accordingly, the District's financial statements have been presented using the economic resources measurementfocus and the accrual basis of accounting. The significant accounting policies followed by the District inpreparing these financial statements are in accordance with accounting principles generally accepted in the UnitedStates of America as prescribed by GASB. Additionally, the District's policies comply with the CaliforniaCommunity Colleges Chancellor's Office Budget and Accounting Manual. Under the accrual basis, revenues arerecognized when earned, and expenses are recorded when an obligation has been incurred. All material intra-agency and intra-fund transactions have been eliminated.

Revenues resulting from exchange transactions, in which each party gives and receives essentially equal value,are classified as operating revenues. These transactions are recorded on the accrual basis when the exchangetakes place. Available means that the resources will be collected within the current fiscal year or are expected tobe collected soon enough thereafter to be used to pay liabilities of the current fiscal year. For the District,operating revenues consist primarily of student fees and auxiliary activities through the bookstore and cafeteria.

Nonexchange transactions, in which the District receives value without directly giving equal value in return,include State apportionments, property taxes, certain Federal and State grants, entitlements, and donations.Property tax revenue is recognized in the fiscal year received. State apportionment revenue is earned based uponcriteria set forth from the Community Colleges Chancellor's Office and includes reporting of full-time equivalentstudents (FTES) attendance. The corresponding apportionment revenue is recognized in the period the FTES aregenerated. Revenue from Federal and State grants and entitlements are recognized in the fiscal year in which alleligibility requirements have been satisfied. Eligibility requirements may include time and/or purposerequirements.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

21

Operating expenses are costs incurred to provide instructional services including support costs, auxiliary services,and depreciation of capital assets. All other expenses not meeting this definition are reported as nonoperating.Expenses are recorded on the accrual basis as they are incurred, when goods are received, or services arerendered.

The District reports are based on all applicable GASB pronouncements, as well as applicable FinancialAccounting Standards Board (FASB) pronouncements issued on or before November 30, 1989, unless thosepronouncements conflict or contradict GASB pronouncements. The District has not elected to apply FASBpronouncements after that date.

The financial statements are presented in accordance with the reporting model as prescribed in GASB StatementNo. 34, Basic Financial Statements and Management's Discussion and Analysis for State and Local Governments,and GASB Statement No. 35, Basic Financial Statements and Management's Discussion and Analysis for PublicColleges and Universities, as amended by GASB Statements No. 37, No. 38, and No. 39. The business-typeactivities model followed by the District requires the following components of the District's financial statements:

Management's Discussion and Analysis Basic Financial Statements for the District as a whole including:

o Statements of Net Position - Primary Governmento Statements of Revenues, Expenses, and Changes in Net Position - Primary Governmento Statements of Cash Flows - Primary Governmento Financial Statements for the Fiduciary Funds including:

o Statements of Fiduciary Net Positiono Statements of Changes in Fiduciary Net Position

Notes to the Financial Statements

Cash and Cash Equivalents

The District's cash and cash equivalents are considered to be unrestricted cash on hand, demand deposits, andshort-term unrestricted investments with original maturities of three months or less from the date of acquisition.Cash equivalents also include unrestricted cash with county treasury balances for purposes of the Statement ofCash Flows. Restricted cash and cash equivalents represent balances restricted by external sources such as grantsand contracts or specifically restricted for the repayment of capital debt.

Investments

In accordance with GASB Statement No. 31, Accounting and Financial Reporting for Certain Investments andExternal Investment Pools, investments held at June 30, 2016, are stated at fair value. Fair value is estimatedbased on quoted market prices at year-end. Short-term investments have an original maturity date greater thanthree months, but less than one year at time of purchase. Long-term investments have an original maturity ofgreater than one year at the time of purchase.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

22

Restricted Assets

Restricted assets arise when restrictions on their use change the normal understanding of the availability of theasset. Such constraints are either imposed by creditors, contributors, grantors, or laws of other governments orimposed by enabling legislation. Restricted assets are classified on the Statement of Net Position because theiruse is limited by enabling legislation, applicable bond covenants, and other laws of other governments. Also,resources have been set aside to satisfy certain requirements of the bonded debt issuance and to fund certaincapital asset projects.

Accounts Receivable

Accounts receivable include amounts due from the Federal, State, and/or local governments or private sources, inconnection with reimbursement of allowable expenditures made pursuant to the District's grants and contracts.Accounts receivable also consist of tuition and fee charges to students and auxiliary enterprise services providedto students, faculty, and staff, the majority of each residing in the State of California. Management has analyzedthese accounts and believes all amounts are fully collectable.

Prepaid Expenses

Prepaid expenses represent payments made to vendors and others for services that will benefit periods beyondJune 30, 2016.

Inventories

Inventories consist primarily of bookstore merchandise and cafeteria food and supplies held for resale to thestudents and faculty of the colleges. Inventories are stated at cost, utilizing the weighted average method. Thecost is recorded as an expense as the inventory is consumed.

Capital Assets and Depreciation

Capital assets are long-lived assets of the District as a whole and include land, construction in progress, buildings,leasehold improvements, and equipment. The District maintains an initial unit cost capitalization threshold of$5,000 and an estimated useful life greater than one year. Assets are recorded at historical cost, or estimatedhistorical cost, when purchased or constructed. The District does not possess any infrastructure. Donated capitalassets are recorded at estimated fair market value at the date of donation. Improvements to buildings and land thatsignificantly increase the value or extend the useful life of the asset are capitalized; the costs of routinemaintenance and repairs that do not add to the value of the asset or materially extend an asset's life are charged asan operating expense in the year in which the expense was incurred. Major outlays for capital improvements arecapitalized as construction in progress as the projects are constructed.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

23

Depreciation of capital assets is computed and recorded utilizing the straight-line method. Estimated useful livesof the various classes of depreciable capital assets are as follows: buildings, 25 to 50 years; improvements,20 years; equipment, 5 to 15 years; vehicles, 5 to 10 years.

Accrued Liabilities and Long-Term Obligations

All payables, accrued liabilities, and long-term obligations are reported in the entity-wide financial statements.

Debt Issuance Costs, Premiums, and Discounts

Debt premiums and discounts, as well as issuance costs related to prepaid insurance costs, are amortized over thelife of the bonds using the straight-line method.

Deferred Charge on Refunding

Deferred charge on refunding is amortized using the straight-line method over the remaining life of the new debt.

Deferred Outflows/Inflows of Resources

In addition to assets, the Statement of Net Position also reports deferred outflows of resources. This separatefinancial statement element represents a consumption of net position that applies to a future period and so will notbe recognized as an expense or expenditure until then. The District reports deferred outflows of resources fordeferred charges on refunding of debt and for pension related items.

In addition to liabilities, the Statement of Net Position reports a separate section for deferred inflows of resources.This separate financial statement element represents an acquisition of net position that applies to a future periodand so will not be recognized as revenue until then. The District reports deferred inflows of resources for pensionrelated items.

Pensions

For purposes of measuring the net pension liability and deferred outflows/inflows of resources related to pensionsand pension expense, information about the fiduciary net position of the California State Teachers' RetirementSystem (CalSTRS) and the California Public Employees' Retirement System (CalPERS) plan for schools(the Plans) and additions to/deductions from the Plans' fiduciary net position have been determined on the samebasis as they are reported by CalSTRS and CalPERS. For this purpose, benefit payments (including refunds ofemployee contributions) are recognized when due and payable in accordance with the benefit terms. Membercontributions are recognized in the period in which they are earned. Investments are reported at fair value.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

24

Compensated Absences

Accumulated unpaid employee vacation benefits are accrued as a liability as the benefits are earned. The entirecompensated absence liability is reported on the entity-wide financial statements. The current portion of unpaidcompensated absences is recognized upon the occurrence of relevant events such as employee resignation andretirements that occur prior to year end that have not yet been paid within the fund from which the employeeswho have accumulated the leave are paid. The District also participates in "load banking" with eligible academicemployees whereby the employee may teach extra courses in one period in exchange for time off in anotherperiod. The liability for this benefit is reported on the entity-wide financial statements.

Sick leave is accumulated without limit for each employee based upon negotiated contracts. Leave with pay isprovided when employees are absent for health reasons; however, the employees do not gain a vested right toaccumulated sick leave. Employees are never paid for any sick leave balance at termination of employment orany other time. Therefore, the value of accumulated sick leave is not recognized as a liability in the District'sfinancial statements. However, retirement credit for unused sick leave is applicable to all classified members whoretire after January 1, 1999. At retirement, each member will receive .004 year of service credit for each day ofunused sick leave. Retirement credit for unused sick leave is applicable to all academic employees and isdetermined by dividing the number of unused sick days by the number of base service days required to completethe last school year, if employed full time.

Unearned Revenue

Unearned revenue arises when potential revenue does not meet both the "measurable" and "available" criteria forrecognition in the current period or when resources are received by the District prior to the incurrence ofqualifying expenditures. In subsequent periods, when both revenue recognition criteria are met, or when theDistrict has a legal claim to the resources, the liability for unearned revenue is removed from the combinedbalance sheet and revenue is recognized. Unearned revenue includes (1) amounts received for tuition and feesprior to the end of the fiscal year that are related to the subsequent fiscal year and (2) amounts received fromFederal and State grants received before the eligibility requirements are met.

Noncurrent Liabilities

Noncurrent liabilities include bonds and notes payable, compensated absences, capital lease obligations, earlyretirement, load banking, OPEB obligations, and net pension obligation with maturities greater than one year.

Net Position

GASB Statements No. 34 and No. 35 report equity as "Net Position" and represent the difference between assetsand liabilities. The net position is classified according to imposed restrictions or availability of assets forsatisfaction of District obligations according to the following net asset categories:

Net Investment in Capital Assets consists of capital assets, net of accumulated depreciation and outstandingprincipal balances of debt attributable to the acquisition, construction, or improvement of those assets. To theextent debt has been incurred, but not yet expended for capital assets, such accounts are not included as acomponent of net investment in capital assets.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

25

Restricted: Net position is reported as restricted when there are limitations imposed on their use, eitherthrough enabling legislation adopted by the District, or through external restrictions imposed by creditors,grantors, or laws or regulations of other governments. The District first applies restricted resources when anexpense is incurred for purposes for which both restricted and unrestricted resources are available.

Unrestricted: Net position that is not subject to externally imposed constraints. Unrestricted net positionmay be designated for specific purposes by action of the Board of Trustees or may otherwise be limited bycontractual agreements with outside parties.

When both restricted and unrestricted resources are available for use, it is the District's practice to use restrictedresources first and the unrestricted resources when they are needed. The entity-wide financial statements report$13,586,260 of restricted net position.

State Apportionments

Certain current year apportionments from the State are based on financial and statistical information of theprevious year. Any corrections due to the recalculation of the apportionment are made in February of thesubsequent year. When known and measurable, these recalculations and corrections are accrued in the year inwhich the FTES are generated.

Property Taxes

Secured property taxes attach as an enforceable lien on property as of January 1. The County Assessor isresponsible for assessment of all taxable real property. Taxes are payable in two installments on November 1 andFebruary 1 and become delinquent on December 10 and April 10, respectively. Unsecured property taxes arepayable in one installment on or before August 31. The County of Los Angeles bills and collects the taxes onbehalf of the District. Local property tax revenues are recorded when received.

The voters of the District passed a General Obligation Bond in March 2002 for the acquisition, construction, andremodeling of certain District property. As a result of the passage of the bond, property taxes are assessed on theproperty within the District specifically for the repayment of the debt incurred. The taxes are assessed, billed, andcollected as noted above and remitted to the District when collected.

Scholarships, Discounts, and Allowances

Student tuition and fee revenue is reported net of scholarships, discounts, and allowances. Fee waivers approvedby the Board of Governors are included within the scholarships, discounts, and allowances in the Statement ofRevenues, Expenses, and Changes in Net Position. Scholarship discounts and allowances represent the differencebetween stated charges for enrollment fees and the amount that is paid by students or third parties makingpayments on the students' behalf.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

26

Federal Financial Assistance Programs

The District participates in federally funded Pell Grants, SEOG Grants, and Federal Work-Study programs, as well asother programs funded by the Federal government. Financial aid to students is either reported as operating expensesor scholarship allowances, which reduce revenues. The amount reported as operating expense represents the portionof aid that was provided to the student in the form of cash. Scholarship allowances represent the portion of aidprovided to students in the form of reduced tuition. These programs are audited in accordance with Title 2 U.S. Codeof Federal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and AuditRequirements for Federal Awards.

Estimates

The preparation of the financial statements in conformity with accounting principles generally accepted in theUnited States of America requires management to make estimates and assumptions that affect the amountsreported in the financial statements and accompanying notes. Actual results may differ from those estimates.

Interfund Activity

Interfund transfers and interfund receivables and payables for governmental activities are eliminated during theconsolidation process in the Primary Government and Fiduciary Funds' financial statements, respectively.

Change in Accounting Principles

In February 2015, the GASB issued Statement No. 72, Fair Value Measurement and Application. This Statementaddresses accounting and financial reporting issues related to fair value measurements. The definition of fairvalue is the price that would be received to sell an asset or paid to transfer a liability in an orderly transactionbetween market participants at the measurement date. This Statement provides guidance for determining a fairvalue measurement for financial reporting purposes. This Statement also provides guidance for applying fairvalue to certain investments and disclosures related to all fair value measurements.

The District has implemented the provisions of this Statement as of June 30, 2016.

In June 2015, the GASB issued Statement No. 73, Accounting and Financial Reporting for Pensions and RelatedAssets That Are Not within the Scope of GASB Statement 68, and Amendments to Certain Provisions of GASBStatements 67 and 68. The objective of this Statement is to improve the usefulness of information about pensionsincluded in the general purpose external financial reports of State and local governments for making decisions andassessing accountability. This Statement results from a comprehensive review of the effectiveness of existingstandards of accounting and financial reporting for all postemployment benefits with regard to providingdecision-useful information, supporting assessments of accountability and inter-period equity, and creatingadditional transparency.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

27

This Statement establishes requirements for defined benefit pensions that are not within the scope of StatementNo. 68, Accounting and Financial Reporting for Pensions—an amendment to GASB Statement No. 27, as well asfor the assets accumulated for purposes of providing those pensions. In addition, it establishes requirements fordefined contribution pensions that are not within the scope of GASB Statement No. 68. It also amends certainprovisions of GASB Statement No. 67, Financial Reporting for Pension Plans—an amendment toGASB Statement No. 25, and GASB Statement No. 68 for pension plans and pensions that are within theirrespective scopes.

The provisions in this Statement, effective as of June 30, 2016, include the provisions for assets accumulated forpurposes of providing pensions through defined benefit plans and the amended provisions of GASB StatementsNo. 67 and No. 68. The District has implemented these provisions as of June 30, 2016. The provisions in thisStatement related to defined benefit pensions that are not within the scope of GASB Statement No. 68 areeffective for periods beginning after June 15, 2016.

In June 2015, the GASB issued Statement No. 76, The Hierarchy of Generally Accepted Accounting Principlesfor State and Local Governments. The objective of this Statement is to identify—in the context of the currentgovernmental financial reporting environment—the hierarchy of generally accepted accounting principles(GAAP). The "GAAP hierarchy" consists of the sources of accounting principles used to prepare financialstatements of State and local governmental entities in conformity with GAAP and the framework for selectingthose principles. This Statement reduces the GAAP hierarchy to two categories of authoritative GAAP andaddresses the use of authoritative and non-authoritative literature in the event that the accounting treatment for atransaction or other event is not specified within a source of authoritative GAAP.

This Statement supersedes GASB Statement No. 55, The Hierarchy of Generally Accepted Accounting Principlesfor State and Local Governments.

The District has implemented the provisions of this Statement as of June 30, 2016.

In December 2015, the GASB issued Statement No. 79, Certain External Investment Pools and Pool Participants.This Statement addresses accounting and financial reporting for certain external investment pools and poolparticipants. Specifically, it establishes criteria for an external investment pool to qualify for making the electionto measure all of its investments at amortized cost for financial reporting purposes. An external investment poolqualifies for that reporting if it meets all of the applicable criteria established in this Statement. The specificcriteria address (1) how the external investment pool transacts with participants; (2) requirements for portfoliomaturity, quality, diversification, and liquidity; and (3) calculation and requirements of a shadow price.Significant noncompliance prevents the external investment pool from measuring all of its investments atamortized cost for financial reporting purposes. Professional judgment is required to determine if instances ofnoncompliance with the criteria established by this Statement during the reporting period, individually or in theaggregate, were significant.

If an external investment pool does not meet the criteria established by this Statement, that pool should apply theprovisions in paragraph 16 of GASB Statement No. 31, Accounting and Financial Reporting for CertainInvestments and for External Investment Pools, as amended. If an external investment pool meets the criteria inthis Statement and measures all of its investments at amortized cost, the pool's participants also should measuretheir investments in that external investment pool at amortized cost for financial reporting purposes. If anexternal investment pool does not meet the criteria in this Statement, the pool's participants should measure theirinvestments in that pool at fair value, as provided in paragraph 11 of GASB Statement No. 31, as amended.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

28

This Statement establishes additional note disclosure requirements for qualifying external investment pools thatmeasure all of their investments at amortized cost for financial reporting purposes and for governments thatparticipate in those pools. Those disclosures, for both the qualifying external investment pools and theirparticipants, include information about any limitations or restrictions on participant withdrawals.

The District has implemented the provisions of this Statement as of June 30, 2016.

New Accounting Pronouncements

In June 2015, the GASB issued Statement No. 74, Financial Reporting for Postemployment Benefit Plans OtherThan Pension Plans. The objective of this Statement is to improve the usefulness of information aboutpostemployment benefits other than pensions (other postemployment benefits or OPEB) included in the generalpurpose external financial reports of State and local governmental OPEB plans for making decisions andassessing accountability. This Statement results from a comprehensive review of the effectiveness of existingstandards of accounting and financial reporting for all postemployment benefits (pensions and OPEB) with regardto providing decision-useful information, supporting assessments of accountability and inter-period equity, andcreating additional transparency.

This Statement replaces GASB Statements No. 43, Financial Reporting for Postemployment Benefit Plans OtherThan Pension Plans, as amended, and No. 57, OPEB Measurements by Agent Employers and AgentMultiple-Employer Plans. It also includes requirements for defined contribution OPEB plans that replace therequirements for those OPEB plans in GASB Statements No. 25, Financial Reporting for Defined Benefit PensionPlans and Note Disclosures for Defined Contribution Plans, as amended, No. 43, and No. 50, PensionDisclosures.

The requirements of this Statement are effective for financial statements for periods beginning after June 15, 2016.Early implementation is encouraged.

In June 2015, the GASB issued Statement No. 75, Accounting and Financial Reporting for PostemploymentBenefits Other Than Pension. The primary objective of this Statement is to improve accounting and financialreporting by State and local governments for postemployment benefits other than pensions (other postemploymentbenefits or OPEB). It also improves information provided by State and local governmental employers aboutfinancial support for OPEB that is provided by other entities. This Statement results from a comprehensivereview of the effectiveness of existing standards of accounting and financial reporting for all postemploymentbenefits (pensions and OPEB) with regard to providing decision-useful information, supporting assessments ofaccountability and inter-period equity, and creating additional transparency.

This Statement replaces the requirements of GASB Statements No. 45, Accounting and Financial Reporting byEmployers for Postemployment Benefits Other Than Pensions, as amended, and No. 57, OPEB Measurements byAgent Employers and Agent Multiple-Employer Plans, for OPEB. GASB Statement No. 74, Financial Reportingfor Postemployment Benefit Plans Other Than Pension Plans, establishes new accounting and financial reportingrequirements for OPEB plans.

The requirements of this Statement are effective for financial statements for periods beginning after June 30, 2017.Early implementation is encouraged.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

29

In August 2015, the GASB issued Statement No. 77, Tax Abatement Disclosures. This Statement requiresgovernments that enter into tax abatement agreements to disclose the following information about the agreements:

Brief descriptive information, such as the tax being abated, the authority under which tax abatements areprovided, eligibility criteria, the mechanism by which taxes are abated, provisions for recapturing abatedtaxes, and the types of commitments made by tax abatement recipients

The gross dollar amount of taxes abated during the period Commitments made by a government, other than to abate taxes, as part of a tax abatement agreement

The requirements of this Statement are effective for financial statements for periods beginning afterDecember 15, 2015. Early implementation is encouraged.

In December 2015, the GASB issued Statement No. 78, Pensions Provided through Certain Multiple-EmployerDefined Benefit Pension Plans. The objective of this Statement is to address a practice issue regarding the scopeand applicability of GASB Statement No. 68, Accounting and Financial Reporting for Pensions—an amendmentto GASB Statement No. 27. This issue is associated with pensions provided through certain multiple-employerdefined benefit pension plans and to State or local governmental employers whose employees are provided withsuch pensions.

Prior to the issuance of this Statement, the requirements of GASB Statement No. 68 applied to the financialstatements of all State and local governmental employers whose employees are provided with pensions throughpension plans that are administered through trusts that meet the criteria in paragraph 4 of that Statement.

This Statement amends the scope and applicability of GASB Statement No. 68 to exclude pensions provided toemployees of State or local governmental employers through a cost-sharing multiple-employer defined benefitpension plan that (1) is not a State or local governmental pension plan; (2) is used to provide defined benefitpensions both to employees of State or local governmental employers and to employees of employers that are notState or local governmental employers; and (3) has no predominant State or local governmental employer(either individually or collectively with other State or local governmental employers that provide pensionsthrough the pension plan). This Statement establishes requirements for recognition and measurement of pensionexpense, expenditures, and liabilities; note disclosures; and required supplementary information for pensions thathave the characteristics described above.

The requirements of this Statement are effective for reporting periods beginning after December 15, 2015. Earlyimplementation is encouraged.

In January 2016, the GASB issued Statement No. 80, Blending Requirements for Certain Component Units—anamendment to GASB Statement No. 14. The objective of this Statement is to improve financial reporting byclarifying the financial statement presentation requirements for certain component units. This Statement amendsthe blending requirements established in paragraph 53 of GASB Statement No. 14, The Financial ReportingEntity. The additional criterion requires blending of a component unit incorporated as a not-for-profit corporationin which the primary government is the sole corporate member. The additional criterion does not apply tocomponent units included in the financial reporting entity pursuant to the provisions of GASB StatementNo. 39, Determining Whether Certain Organizations Are Component Units—an amendment to GASB StatementNo. 14.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

30

The requirements of this Statement are effective for reporting periods beginning after June 15, 2016. Earlyimplementation is encouraged.

In March 2016, the GASB issued Statement No. 81, Irrevocable Split-Interest Agreements. The objective of thisStatement is to improve accounting and financial reporting for irrevocable split-interest agreements by providingrecognition and measurement guidance for situations in which a government is a beneficiary of the agreement.

This Statement requires that a government that receives resources pursuant to an irrevocable split-interestagreement recognize assets, liabilities, and deferred inflows of resources at the inception of the agreement.Furthermore, this Statement requires that a government recognize assets representing its beneficial interests inirrevocable split-interest agreements that are administered by a third party, if the government controls the presentservice capacity of the beneficial interests. This Statement requires that a government recognize revenue whenthe resources become applicable to the reporting period.

The requirements of this Statement are effective for financial statements for periods beginning afterDecember 15, 2016, and should be applied retroactively. Early implementation is encouraged.

In March 2016, the GASB issued Statement No. 82, Pension Issues—an amendment of GASB Statements No. 67,No. 68, and No. 73. The objective of this Statement is to address certain issues that have been raised with respectto GASB Statement No. 67, Financial Reporting for Pension Plans—an amendment to GASB Statement No. 25,GASB Statement No. 68, Accounting and Financial Reporting for Pensions—an amendment to GASB StatementNo. 27, and GASB Statement No. 73, Accounting and Financial Reporting for Pensions and Related Assets ThatAre Not within the Scope of GASB Statement 68, and Amendments to Certain Provisions of GASB Statements 67and 68. Specifically, this Statement addresses issues regarding (1) the presentation of payroll-related measures inrequired supplementary information; (2) the selection of assumptions and the treatment of deviations from theguidance in an Actuarial Standard of Practice for financial reporting purposes; and (3) the classification ofpayments made by employers to satisfy employee (plan member) contribution requirements.

The requirements of this Statement are effective for reporting periods beginning after June 15, 2016, except forthe requirements of this Statement for the selection of assumptions in a circumstance in which an employer'spension liability is measured as of a date other than the employer's most recent fiscal year end. In thatcircumstance, the requirements for the selection of assumptions are effective for that employer in the firstreporting period in which the measurement date of the pension liability is on or after June 15, 2017. Earlyimplementation is encouraged.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

31

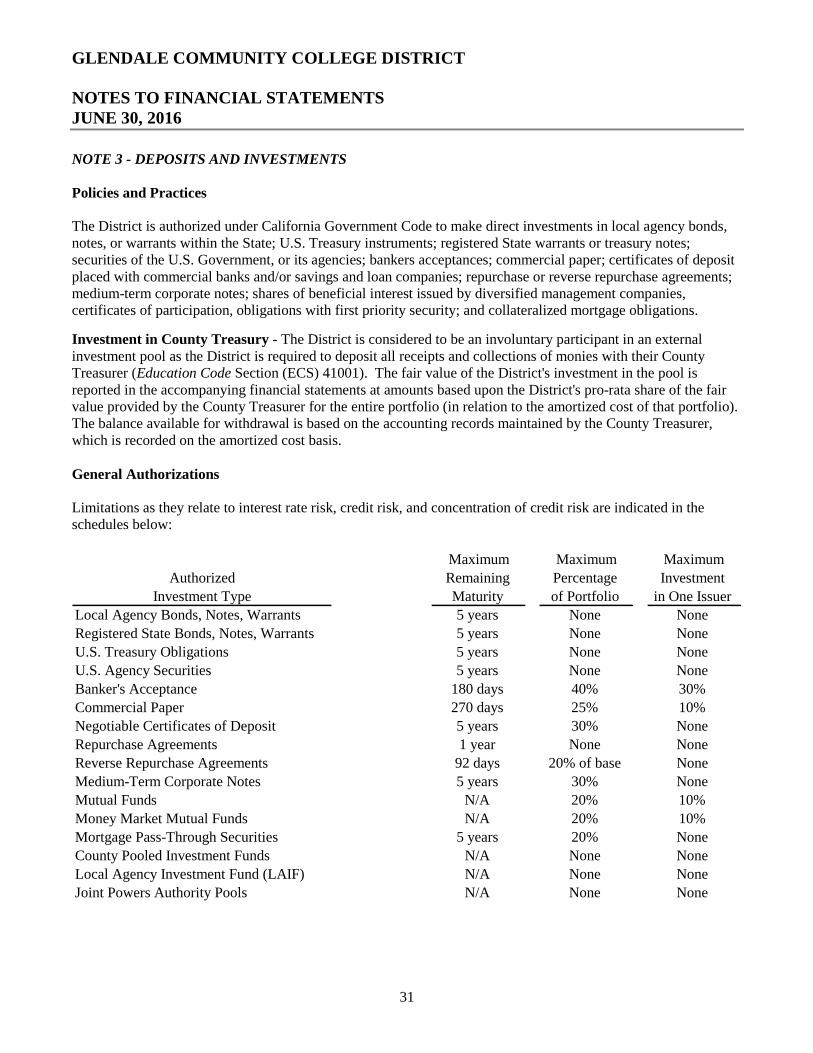

NOTE 3 - DEPOSITS AND INVESTMENTS

Policies and Practices

The District is authorized under California Government Code to make direct investments in local agency bonds,notes, or warrants within the State; U.S. Treasury instruments; registered State warrants or treasury notes;securities of the U.S. Government, or its agencies; bankers acceptances; commercial paper; certificates of depositplaced with commercial banks and/or savings and loan companies; repurchase or reverse repurchase agreements;medium-term corporate notes; shares of beneficial interest issued by diversified management companies,certificates of participation, obligations with first priority security; and collateralized mortgage obligations.

Investment in County Treasury - The District is considered to be an involuntary participant in an externalinvestment pool as the District is required to deposit all receipts and collections of monies with their CountyTreasurer (Education Code Section (ECS) 41001). The fair value of the District's investment in the pool isreported in the accompanying financial statements at amounts based upon the District's pro-rata share of the fairvalue provided by the County Treasurer for the entire portfolio (in relation to the amortized cost of that portfolio).The balance available for withdrawal is based on the accounting records maintained by the County Treasurer,which is recorded on the amortized cost basis.

General Authorizations

Limitations as they relate to interest rate risk, credit risk, and concentration of credit risk are indicated in theschedules below:

Maximum Maximum Maximum

Authorized Remaining Percentage Investment

Investment Type Maturity of Portfolio in One Issuer

Local Agency Bonds, Notes, Warrants 5 years None None

Registered State Bonds, Notes, Warrants 5 years None None

U.S. Treasury Obligations 5 years None None

U.S. Agency Securities 5 years None None

Banker's Acceptance 180 days 40% 30%

Commercial Paper 270 days 25% 10%

Negotiable Certificates of Deposit 5 years 30% None

Repurchase Agreements 1 year None None

Reverse Repurchase Agreements 92 days 20% of base None

Medium-Term Corporate Notes 5 years 30% None

Mutual Funds N/A 20% 10%

Money Market Mutual Funds N/A 20% 10%

Mortgage Pass-Through Securities 5 years 20% None

County Pooled Investment Funds N/A None None

Local Agency Investment Fund (LAIF) N/A None None

Joint Powers Authority Pools N/A None None

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

32

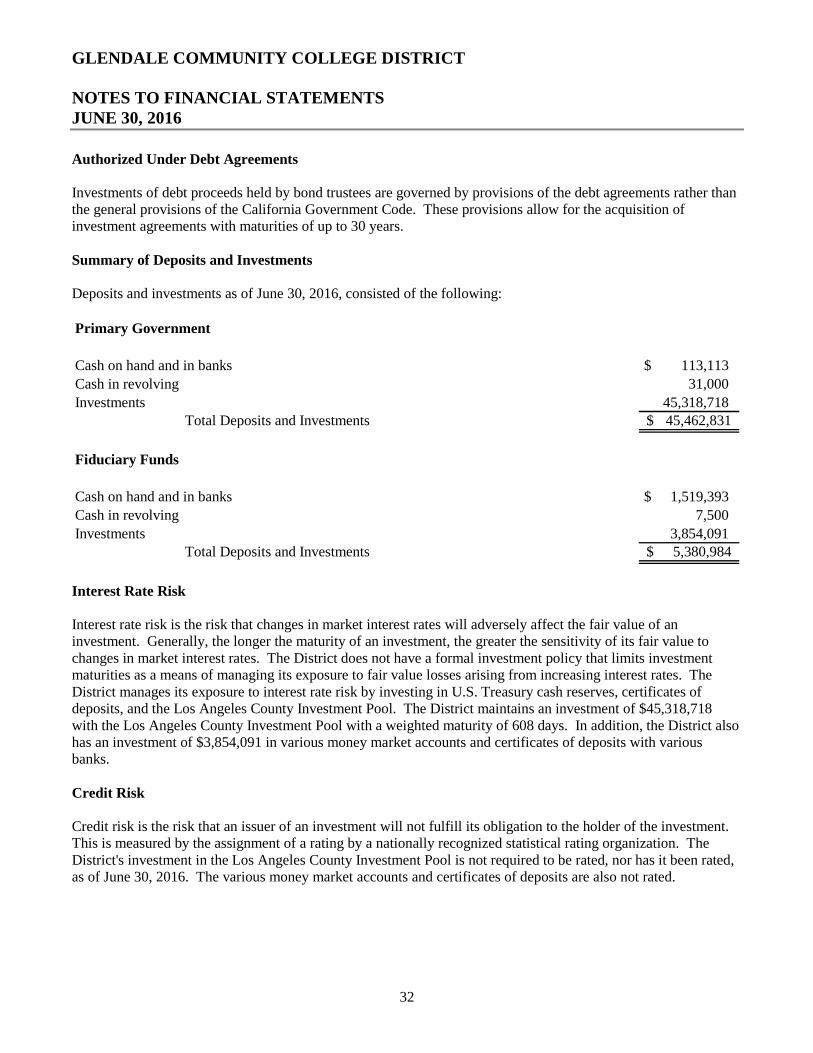

Authorized Under Debt Agreements

Investments of debt proceeds held by bond trustees are governed by provisions of the debt agreements rather thanthe general provisions of the California Government Code. These provisions allow for the acquisition ofinvestment agreements with maturities of up to 30 years.

Summary of Deposits and Investments

Deposits and investments as of June 30, 2016, consisted of the following:

Primary Government

Cash on hand and in banks 113,113$

Cash in revolving 31,000

Investments 45,318,718Total Deposits and Investments 45,462,831$

Fiduciary Funds

Cash on hand and in banks 1,519,393$

Cash in revolving 7,500

Investments 3,854,091Total Deposits and Investments 5,380,984$

Interest Rate Risk

Interest rate risk is the risk that changes in market interest rates will adversely affect the fair value of aninvestment. Generally, the longer the maturity of an investment, the greater the sensitivity of its fair value tochanges in market interest rates. The District does not have a formal investment policy that limits investmentmaturities as a means of managing its exposure to fair value losses arising from increasing interest rates. TheDistrict manages its exposure to interest rate risk by investing in U.S. Treasury cash reserves, certificates ofdeposits, and the Los Angeles County Investment Pool. The District maintains an investment of $45,318,718with the Los Angeles County Investment Pool with a weighted maturity of 608 days. In addition, the District alsohas an investment of $3,854,091 in various money market accounts and certificates of deposits with variousbanks.

Credit Risk

Credit risk is the risk that an issuer of an investment will not fulfill its obligation to the holder of the investment.This is measured by the assignment of a rating by a nationally recognized statistical rating organization. TheDistrict's investment in the Los Angeles County Investment Pool is not required to be rated, nor has it been rated,as of June 30, 2016. The various money market accounts and certificates of deposits are also not rated.

GLENDALE COMMUNITY COLLEGE DISTRICT

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2016

33

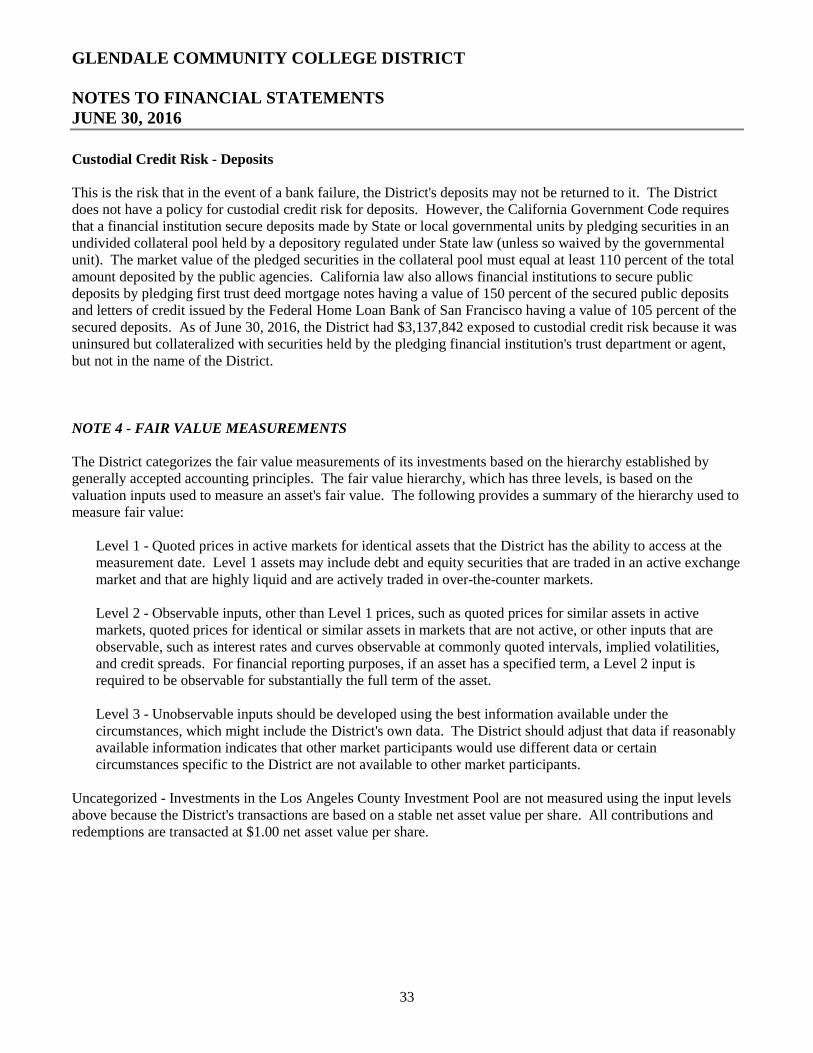

Custodial Credit Risk - Deposits

This is the risk that in the event of a bank failure, the District's deposits may not be returned to it. The Districtdoes not have a policy for custodial credit risk for deposits. However, the California Government Code requiresthat a financial institution secure deposits made by State or local governmental units by pledging securities in anundivided collateral pool held by a depository regulated under State law (unless so waived by the governmentalunit). The market value of the pledged securities in the collateral pool must equal at least 110 percent of the totalamount deposited by the public agencies. California law also allows financial institutions to secure publicdeposits by pledging first trust deed mortgage notes having a value of 150 percent of the secured public depositsand letters of credit issued by the Federal Home Loan Bank of San Francisco having a value of 105 percent of thesecured deposits. As of June 30, 2016, the District had $3,137,842 exposed to custodial credit risk because it wasuninsured but collateralized with securities held by the pledging financial institution's trust department or agent,but not in the name of the District.

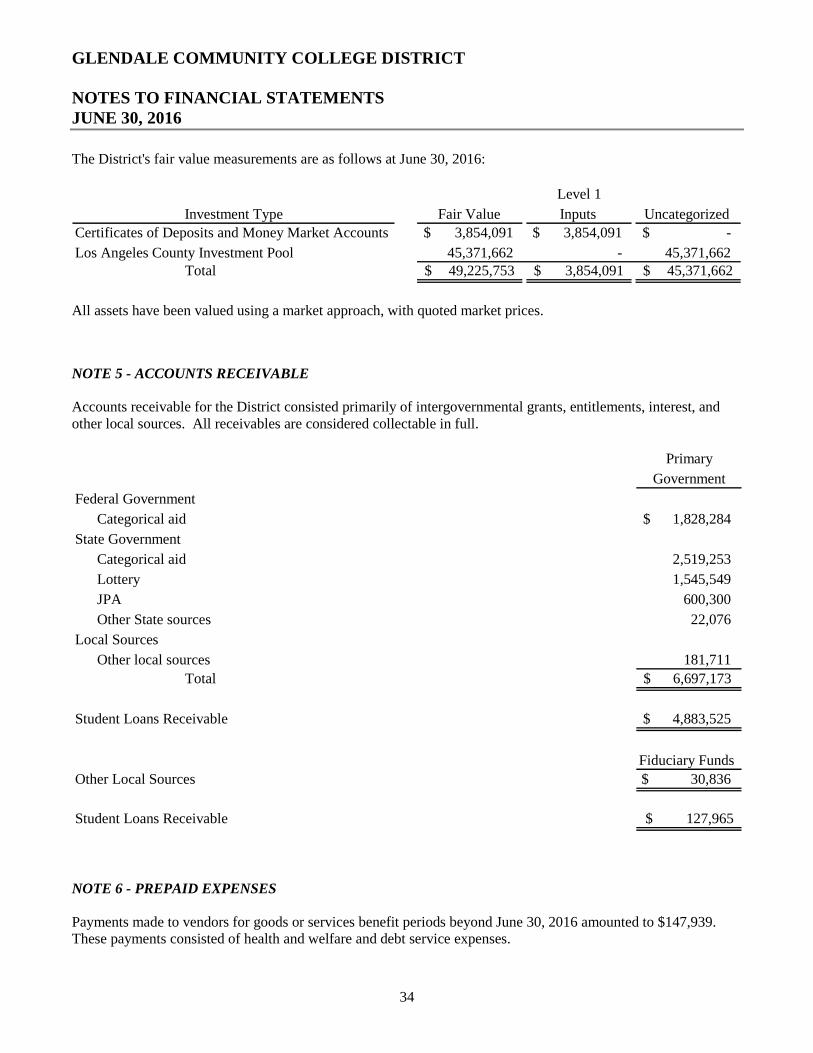

NOTE 4 - FAIR VALUE MEASUREMENTS

The District categorizes the fair value measurements of its investments based on the hierarchy established bygenerally accepted accounting principles. The fair value hierarchy, which has three levels, is based on thevaluation inputs used to measure an asset's fair value. The following provides a summary of the hierarchy used tomeasure fair value:

Level 1 - Quoted prices in active markets for identical assets that the District has the ability to access at themeasurement date. Level 1 assets may include debt and equity securities that are traded in an active exchangemarket and that are highly liquid and are actively traded in over-the-counter markets.

Level 2 - Observable inputs, other than Level 1 prices, such as quoted prices for similar assets in activemarkets, quoted prices for identical or similar assets in markets that are not active, or other inputs that areobservable, such as interest rates and curves observable at commonly quoted intervals, implied volatilities,and credit spreads. For financial reporting purposes, if an asset has a specified term, a Level 2 input isrequired to be observable for substantially the full term of the asset.