German Tax Reform German Tax Reform Vienna, 30 May 2008 Vienna, 30 May 2008

German Tax Reform Vienna, 30 May 2008. Ebner, Stolz & Partner locations in Germany, over 540 employees Kiel Hamburg Hanover Berlin Munich Leipzig Stuttgart.

Dec 30, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

German Tax ReformGerman Tax ReformVienna, 30 May 2008Vienna, 30 May 2008

Ebner, Stolz & Partner locations in Germany, over 540 employees

Kiel

Hamburg

HanoverBerlin

Munich

Leipzig

Stuttgart

Reutlingen

Frankfurt

Agenda

I. Reduction of tax rate

II. Counter financing

III. Anti-Treaty Shopping rules

IV. Outlook

I. Reduction of tax rate

• 15% corporate tax rate (ex 25%)• Applicable for FY starting 2008• Solidarity surcharge of 5,5% on top of the tax rate

remains• Trade tax remains, but changes• Total burden app. 29.5%

Trade tax

• Not deductible as tax expense any more

• Basic factor reduced from 5 to 3,5%

• Factor multiplied by regional rate

• Base expanded by stricter rules in respect of financing costs

Expansion of trade tax base for financing costs

Calculation scheme

100 % For interests, pension, silent partners

20 % For rent and leasing of moveable goods

25 % For license fees

75 % For rent and leasing of immovable goods

= Total of financing costs

./. Allowance 100.000 €

= Increase of profit for trade tax purposes by 25 %

Effective tax cost

100 EUR financing

3,50 EUR

0,70 EUR

0,88 EUR

2,63 EUR

Example for a German corporation

Comperisation of total tax burden

Trade tax rate 300 % 400 % 420 % 490 %

Profit 100,00 100,00 100,00 100,00

Trade Tax - 10,50 - 14,00 - 14,70 - 17,15

Corporate Tax - 15,00 - 15,00 - 15,00 - 15,00

Solidarity surcharge - 0,83 - 0,83 - 0,83 - 0,83

Tax from FY 2008 - 26,33 - 29,83 - 30,53 - 32,98

Tax in the past- 35,98 - 38,65 - 39,15 - 40,86

Tax reduction 9,65 8,82 8,62 7,88

Reduction in % 26,83 % 22,82 % 22,04 % 19,30 %

II. Counter financing

• Overview

• Interest ceiling

• Loss limitation

• Exit taxation

• Base shifting

Overview

• Budget impact of the tax reform should be limited to EUR 5 billion

• Therefore, a couple of rules have been changed and implement for counter financing

• The following tools seem to be the most relevant, but do not provide a complete picture

Interest ceiling

• Old safe-haven rule dismissed (Art. 8a CTA)

• Introduction of complete new scheme of imposing a limit on deductibility of interest

• Covers all kind of financing

• Applicable for FY starting 1 June 2007

Interest ceiling - New concept

• Interest on borrowed capital will be tax deductible without restriction only up to an amount of EUR 1 mio

• If the limit is exceeded, interest is permitted to offset only by a percentage of EBITDA

• Percentage rate is 30%

• Any not tax deductible interest to be carried forward

Interest ceiling - Exceptions

• The interest ceiling rule does not apply if

(1) The business has net interest expenses of less than EUR 1 mio in a given FY or

(2) The business neither belongs to a consolidated group for accounting purposes nor is under common control with other businesses or

(3) The business can demonstrate that its indebtedness does not exceed the group indebtedness (by more than 1%)

Interest ceiling - Check list

Interest expense./. income ≤ 0

Difference < EUR 1 mio

Difference ≤ 30 % EBITDA

INTEREST CEILINGOnly 30 % of EBITDARemaining interests to be carried forward

Interest expenses fully tax deductible

No

No

No

Group-clause

Escape-clause:

No

No

No debt financing by shareholder

+

A

T1-Corp T2-Corp T3-Corp

B

100 %loan 1

loan 3100 % 100 % 70 % 30 %

M-Corp

loan 2

loan 1 and loan 3 are under tax risk

loan 2 is not under risk as it is consolidated

GROUP

Example

Loss limitation rules

• Tax losses of a merged company are not transferable any longer to the acquiring company

• Transfer of shares within a 5-year period:– If > 50% the carry-forward will cease to exist– If > 25% the carry-forward will expire on a pro rata basis– Injection of new assets isn’t risky any longer

Exit taxation

• If an asset is moved cross-border into a PE and the German taxation right is excluded or limited, a capital gain has to be taxed

• If a person owning at least 1% of any share holding moves and the German taxation right is excluded or limited, a capital gain has to be taxed

• The payment can be deferred until the realization of a sale if it happens within the European Community

Base shifting

• Background

• Definition

• Evaluation

• Price correction

• Base shifting

Base shifting - Background

R&D Patent registration

and invoicing

Transfer of

the project

Base shifting - Definition

• Shifting of business tasks inclindung functions and risks• Examples

– Transfer of whole business– Involvement of a contract manufacturer– Conversion of a sales person to a commissioner– Conversion of a contract manufacturer to a production entity– Secondment of staff in case of transfer of functions

• Copying of a successful business model was under heavy discussion and has been excluded unless it is a hidden base shifting

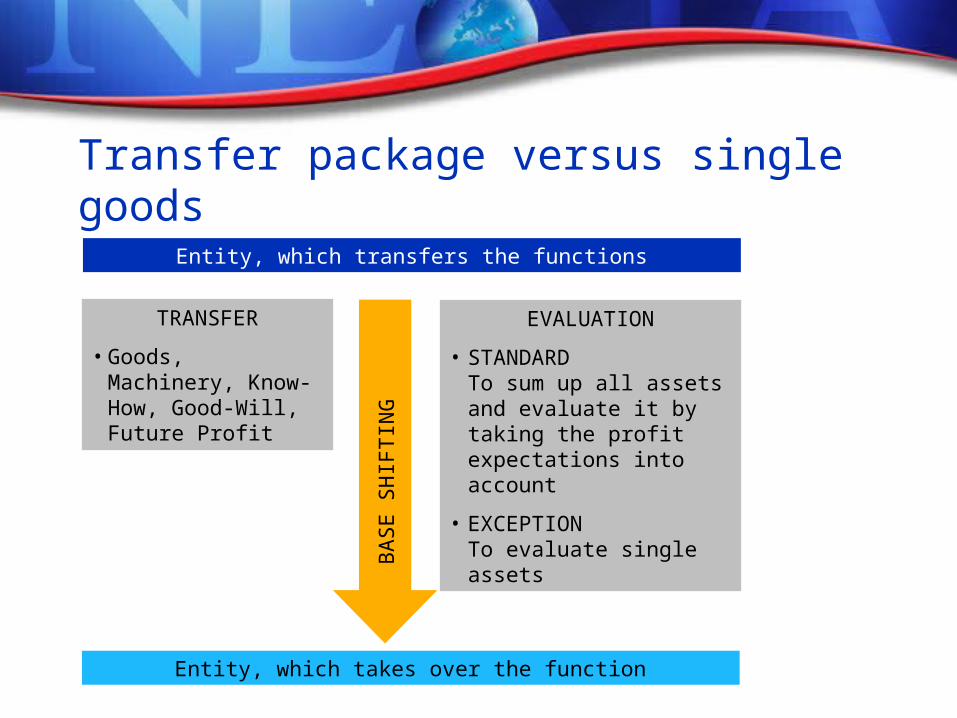

Entity, which transfers the functions

TRANSFER

• Goods, Machinery, Know-How, Good-Will, Future Profit

EVALUATION

• STANDARDTo sum up all assets and evaluate it by taking the profit expectations into account

• EXCEPTIONTo evaluate single assets

Entity, which takes over the function

BA

SE

SH

IFT

ING

Transfer package versus single goods

Evaluation of future profit (1)

Entity, which transfers the

function

Entity, which takes over the function

Profit potential

Expected profit before base shifting

./. Expected profit after base shifting

= Difference

x Factor for capitalization

= Minimum selling price

Expected profit after base shifting

./. Expected profit before base shifting

= Difference

x Factor for capitalization

= Maximum purchase price

Evaluation of future profit (2)

Most likely price

PRICE

Agree upon area

Entity, which transfer the function

4 mio 5 mio

Entity, which takes over the function

Price shifting clause

• Tax legislator works with an assumption that– There are uncertainties at the time of making the

arrangement and

– Third parties would have agreed on a price shifting clause. • Important in case the profit develops different from the planning

• Shall allow price corrections within 10 years period by the tax authority

Three-row-model

VALUEOF

TRANSFER PACKAGE

RETRO-ACTIVEPRICE

CORRECTION

INFO-

SUPPORTBY THE

TAX PAYER

BASE SHIFTING

TAXTREATMENT

III. Anti-Treaty-Shopping rules

• Tax Bill 2007 has introduced tightened domestic Anti-Treaty shopping rules

• First practical experience available

• Domestic subject to tax clause introduced

Stricter conditions (Art. 50d 3 ITA)

• Foreign holding exempt from WHT only if shareholders are entitled to the same benefit or the 3-Factor-Test is met:

+ Sufficient resources to conduct business+ Proof of non-tax reason for the structure+ 10% of gross revenues from own business

activities

Application of the rules

• German entity or the applicant has to complete a long and detailed questionnaire providing evidence about the shareholder and its background

• Old applications still valid, but extension requires the same questionnaire

Domestic subject to tax clause

• No “white” income any more? • If foreign source income is not subject to taxation abroad, it

shall be subject to taxation in Germany (Art. 50d 9 ITA)• The reason for the non-taxation abroad needs to be

analyzed, e. g. – different treatment of non-residents– DTT qualification conflict (hybrid structures)

IV. Outlook

• Flat tax of 25% to certain capital income and capital gains

• Reform of inheritance and gift tax

Flat tax of 25% from 2009

• Applicable to– Private income from capital, such as dividends

and interests– Private income from capital gains

• Restructuring of investments underway, which needs to be completed by 31.12.08

Example for German corporation and shareholder

Private Business old

Profit before tax 100,00 100,00 100,00

Tax at corporation level -29,83 -29,83 -38,65

Dividend distribution 70,18 70,18 61,35

Taxable dividends 70,18 42,11 30,68

Flat tax 25% -17,54 --- ---

Income tax (45 %) --- -18,95 -13,80

Solidarity surcharge -0,96 -1,04 -0,76

Tax at shareholder level -18,51 -19,99 -14,56

Total tax -48,33 -49,81 -53,21

Inheritance and gift tax reform

• Driven by the decision of the German Federal Constitutional Court, which declare current rules as non-constitutional

• Heavy ongoing discussion

• To completed by the end of 2008

Thanks for your attention

Our profile

Audit Tax advisory services Consultancy services in commercial law Business consultancy services

The best solution is our priority Our organization is focused on our clients requirements. A partner and his team guarantee for high quality services based on

the know how of our specialists Comprehensive knowledge and a flat organisational structure are the

base for flexible and integrated solutions

Specialists and their teams work as entrepreneurs for your enterprise Take advantage of an established institution of professional experts We apply our broad know how with full engagement to meet your

needs As a service company entrepreneurial partnership is important to us

More than 30 years we focus an middle sized companies With more than 540 employees we are independent and are one of

the most the established companies within our business field in Germany

Our offices are in Stuttgart, Hamburg, Hanover, Berlin, Frankfurt, Leipzig and Munich

Our international network is NEXIA., one of the leading worldwide associations

Who we are

Our serivce

Our operation

Partner

• Restructuring and reorganization

• Financial Advisory

• IT/Process Organisation

• Provisional Management

• Controlling

Ebner, Stolz & Partner

• International tax advisory

• Company succession

• Legal structuring

• Acquisition of companies

• Supporting of tax audits

• On-going consultancy

• Preparation of annual financial statements

Auditing

• Auditing of financial statements and con-solidated financial statements (legal Peer Review passed in 2005)

• Preparation and auditing of financial statements corresponding to US-GAAP or IFRS

• Due Diligence-reviews

• Audit of Internal control

• Valuation of companies

Tax advisory Services

• Consultancy together with taxation and auditing

• Company bylaws

• contracts for establishing companies, legal structuring, etc.

• Company

Succession

Commercial lawconsultancy

Business Consultancy

Services

Our services

Centers of Competence – Combination of generalists and specialists

• Internationalaccounting

• Due diligence

• Valuation of companies

• Risk management systems

• Financial services business

• Rating advisory

• All services and coordination from one source

• Audit and consultancy services by one team

• Providing integrated solutions

• Access to centers of competence

Centre of Competence Auditing

International taxation

company succession

legal structuring

Acquisition of companies

VAT

Fortune and taxes

First-class solutions

Client Contact TeamCentre of Competence

Taxation

Sten Günsel Professional background:

University of Halle/Wittenberg School of Law, Mandatory Legal Clerkship – Focus on Tax LawFrom 1995 – 2000 PwC Hanover, 1999 qualification as tax advisoraccording to German lawFrom 2000 – 2005 PwC Czech Republic, Brno/Prague, Leader of the German tax deskFrom 2005 – 2006 Leitner & Leitner, Czech Republic, PartnerSince 2006 Ebner, Stolz & Partner, Stuttgart – works in his capacity as tax advisor and attorney

Main Areas of Focus:International taxation, Expatriate taxation, Tax structuring, Central and Eastern Europe

Business Sectors:Investment - Service - Distribution – Manufacturer - Automotive

German Tax advisor – Attorney at Law

[email protected]: +49 711 2049 1258Fax: +49 711 2049 3258

Dr. Markus EmmrichProfessional background:

Studied business administration at the University of BayreuthResearch assistant to the Professional Chair for Economics Tax Law and Auditing at the University of BayreuthCompleted his Doctorate (Dr. rer. pol.)Appointed Certified Tax Consultant in 1999Employee at Mönning & Partner since 1999Since 2001 teaching appointment, lecturing in Conversion Tax Law at the University of Bayreuth European Chairman of SC International from 2002 until 2007From December 2007 Board member of NEXIA International and Deputy Chairman NEXIA Europe2002Partner at Mönning & Partner / Ebner, Stolz, Mönning GmbH Works in his capacity as Tax Consultant

Main Areas of Focus:Group RestructuringAcquisitions and Sale of Companies Company SuccessionConcepts focusing an International Tax Law

German Tax advisor

[email protected]: +49 40 37097-177Fax: +49 40 37097-599

Related Documents