Financial accounting practice is governed by concepts and rules known as generally accepted accounting principles (GAAP). Generally Accepted Accounting Principles Relevant Information Affects the decision of its users. Reliable Information Is trusted by users. Comparable Information Used in comparisons across years & companies. 1-1

Generally Accepted Accounting Principles

Dec 30, 2015

Relevant Information. Affects the decision of its users. Reliable Information. Is trusted by users. Comparable Information. Used in comparisons across years & companies. Generally Accepted Accounting Principles. - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financial accounting practice is governed by concepts and rules known as generally accepted accounting principles (GAAP).

Financial accounting practice is governed by concepts and rules known as generally accepted accounting principles (GAAP).

Generally Accepted Accounting Principles

Relevant Information

Relevant Information

Affects the decision of its users.

Affects the decision of its users.

Reliable InformationReliable Information Is trusted by users.

Is trusted by users.

Comparable Information

Comparable Information

Used in comparisons across years & companies.

Used in comparisons across years & companies.

1-1

Principles and Assumptions of Accounting

Measurement principle (also called cost principle) means that accounting information is based on actual cost.

Going-concern assumption means that accounting information reflects a presumption the business will continue operating.

Monetary unit assumption means we can express transactions in money.

Revenue recognition principle provides guidance on when a company must recognize revenue.

Business entity assumption means that a business is accounted for separately from its owner or other business entities.

Matching principle (expense recognition) prescribes that a company must record its expenses incurred to generate the revenue.

Full disclosure principle requires a company to report the details behind financial statements that would impact users’ decisions.

1-2

Time period assumption presumes that the life of a company can be divided into time periods, such as months and years.

AssetsLiabilities + Equity

Accounting Equation

LiabilitiesLiabilities EquityEquityAssetsAssets = +

1-3

LandLand

EquipmentEquipment

BuildingsBuildings

CashCash

VehiclesVehicles

Store Supplies

Store Supplies

Notes Receivable

Notes Receivable

Accounts Receivable

Accounts Receivable

Resources owned or controlled

by a company

Resources owned or controlled

by a company

Assets

1-4

Taxes Payable

Taxes Payable

Wages Payable

Wages Payable

Notes Payable

Notes Payable

Accounts Payable

Accounts Payable

Creditors’ claims on

assets

Creditors’ claims on

assets

Liabilities

1-5

Owner’sclaim on

assets

Owner’sclaim on

assets

DividendsDividends

Contributed Capital

Contributed Capital

Retained Earnings

Retained Earnings

Equity

1-6

LiabilitiesLiabilities EquityEquityAssetsAssets = +

Expanded Accounting Equation

RevenuesRevenues ExpensesExpensesContributed

CapitalContributed

CapitalDividendsDividends__ ++ __

Retained Earnings

LiabilitiesLiabilities EquityEquityAssetsAssets = +

1-7

Transaction Analysis

Business activities can be described in terms of transactions and events. External transactions are exchanges of value between two entities, which yield changes in the accounting equation. Internal transactions are exchanges within any entity; they can also affect the accounting equation. Events refer to happenings that affect an entity’s accounting equation and can be reliably measured. Transaction analysis is defined as the process used to analyze transactions and events.

1-8

Transaction Analysis

J. Scott invests $20,000 cash to start the business in return for stock.

1-9

Transaction Analysis

Purchased supplies paying $1,000 cash.

1-10

Transaction Analysis

Purchased equipment for $15,000 cash.

1-11

Transaction Analysis

Purchased Supplies of $200 and Equipment of $1,000 on account.

1-12

Transaction Analysis

Borrowed $4,000 from 1st American Bank.

1-13

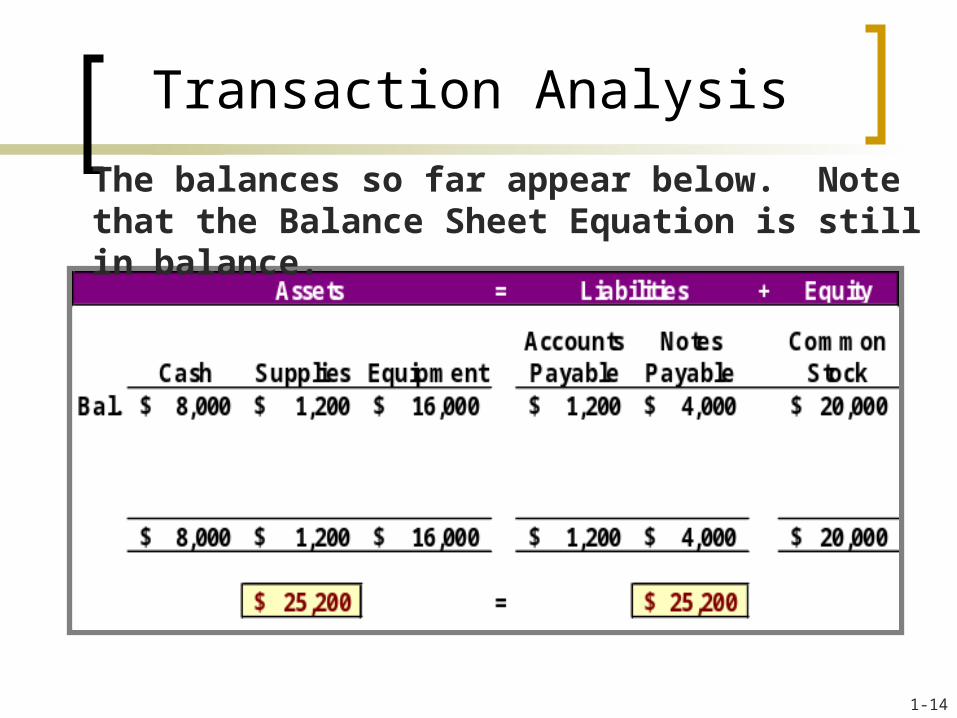

Transaction Analysis

The balances so far appear below. Note that the Balance Sheet Equation is still in balance.

1-14

Transaction Analysis

Now, let’s look at transactions involving revenue, expenses and

dividends.

1-15

Transaction Analysis

Provided consulting services receiving $3,000 cash.

1-16

Transaction Analysis

Remember that expenses decrease equity.

Paid salaries of $800 to employees.

1-17

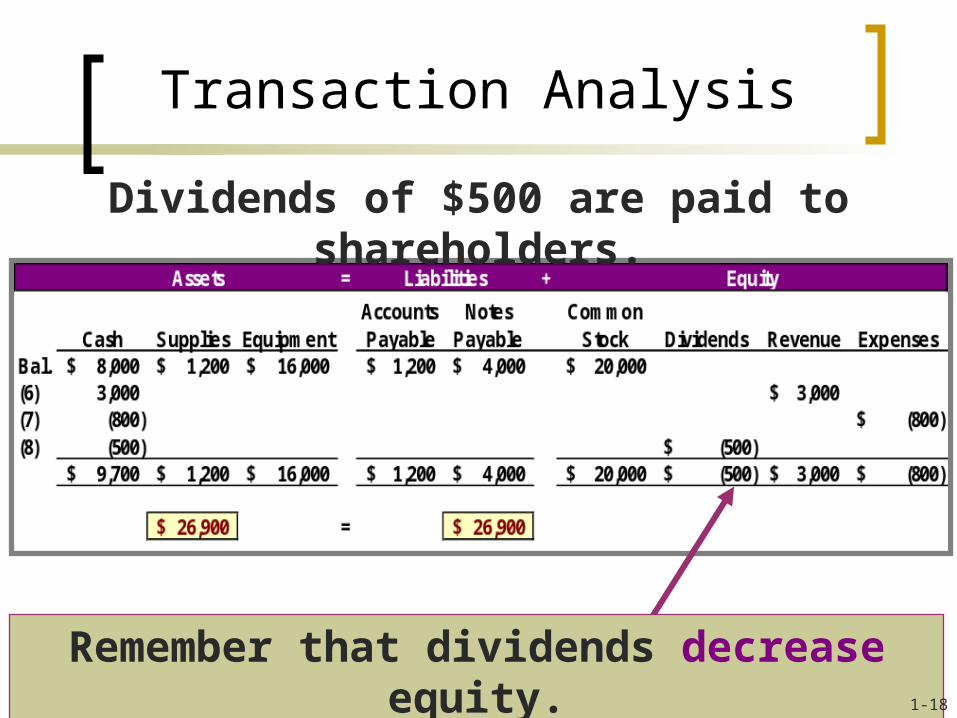

Transaction Analysis

Remember that dividends decrease equity.

Dividends of $500 are paid to shareholders.

1-18

Financial Statements

Let’s prepare the Financial Statements reflecting the transactions we have recorded.

1. Income Statement

2. Statement of Retained Earnings

3. Balance Sheet

4. Statement of Cash Flows

1. Income Statement

2. Statement of Retained Earnings

3. Balance Sheet

4. Statement of Cash Flows

1-19

Net income is the difference between

Revenues and Expenses.

Net income is the difference between

Revenues and Expenses.

The income statement describes a company’s revenues and expenses along with the resulting net income or loss over a period of time due to earnings activities.

The income statement describes a company’s revenues and expenses along with the resulting net income or loss over a period of time due to earnings activities.

Income Statement

1-20

The Balance Sheet describes a company’s financial position at a point in time.

The Balance Sheet describes a company’s financial position at a point in time.

Balance Sheet

1-21

22

Account Name

(Left Side) Debit

(Right Side) Credit

Tool to analyze and determine the balance in a given account

T-Account

23

Debit CreditDebit Credit

AssetsAssets

+ + --

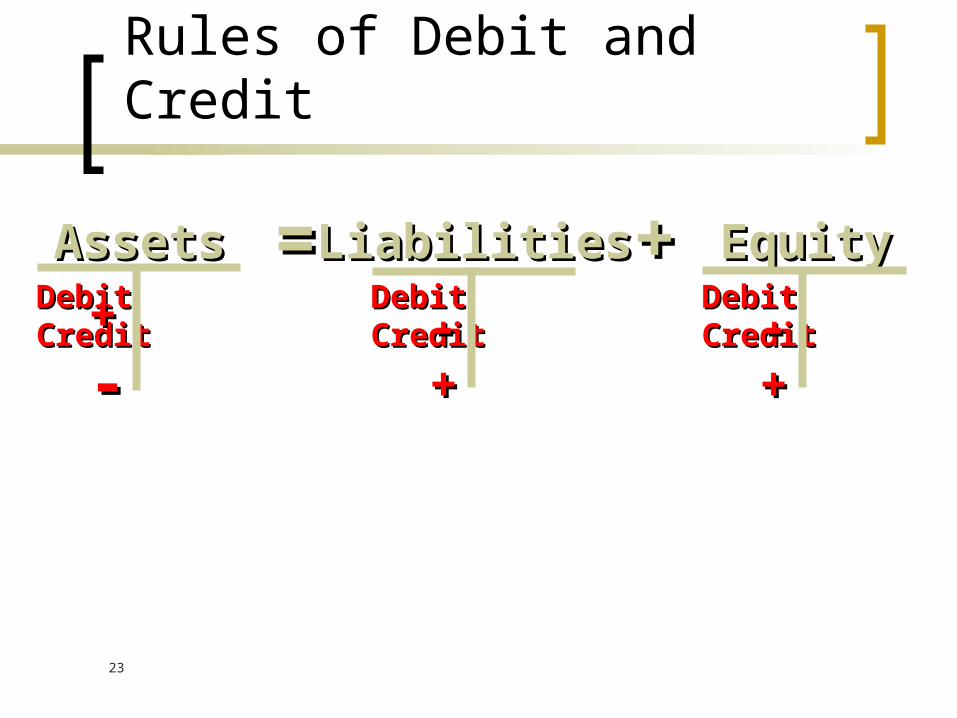

Rules of Debit and Credit

LiabilitiesLiabilities EquityEquity== ++Debit CreditDebit Credit - +- +

Debit CreditDebit Credit - +- +

24

Rules of Debit and Credit

Owner’s EquityOwner’s EquityDebit CreditDebit Credit - +- +

RevenuesRevenues

- +- +Debit CreditDebit Credit

Owner’s Owner’s CapitalCapital

Debit CreditDebit Credit - +- +

Owner’s Owner’s WithdrawalsWithdrawals

Debit CreditDebit Credit + + --

ExpensesExpenses

Debit CreditDebit Credit

+ + --

25

RevenuesRevenues ExpensesExpensesOwner’s Owner’s CapitalCapital

Owner’s Owner’s WithdrawalsWithdrawals

__ ++ __

Expanding the Rules of Debit and Credit

Owner’s Equity

Debit CreditDebit Credit - +- +

Debit CreditDebit Credit

- +- +Debit CreditDebit Credit + + --

Debit CreditDebit Credit + + --

26

Remember: Just ask ALICE!

Debit Credit

+ A = Assets -

- L = Liabilities +

- I = Income* +

- C = Capital +

+ E = Expenses -

* Really, this is revenues, but “r” just doesn’t fit in!

The first and the last are increased

with a debit

The middle three are increased with

credits

27

Journalizing Transactions

Identify accounts affected and its type

Determine whether each account is increased or decreased. Apply the rules of debit and credit

Record transaction in journal. Debit side of entry is entered first Total debit $ must = Total credit $

28

General Journal

Journal Page 1

Date Description Debit Credit

Jul 1 Cash 45,000

Lange, Capital 45,000

Investment from owner

Accounts AffectedAccounts Affected

Dollar amount of debits and credits

Dollar amount of debits and credits

Optional: Explanation of transaction

Optional: Explanation of transaction

Transaction Date

Transaction Date

29

General Journal

Debits are ALWAYS entered 1st.

Credits are INDENTED and listed after the debit accounts or accounts.

Do not use dollar signs.

SKIP A LINE between each entry

30

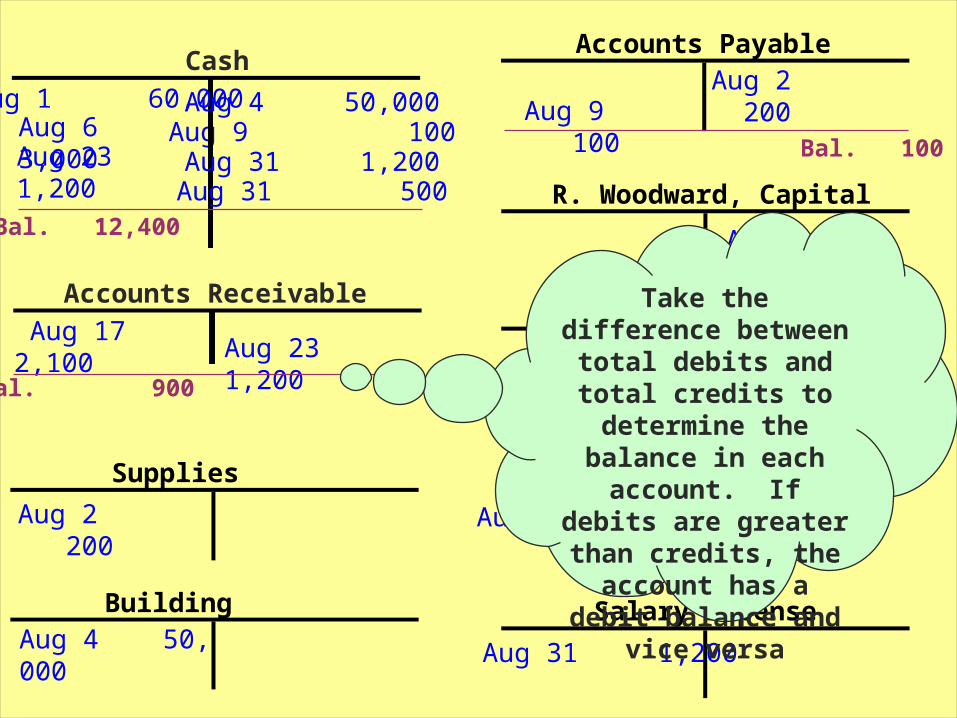

Exercise 2-19Aug 9 100

Cash

Aug 1 60,000 Aug 4 50,000Aug 6 3,000

Accounts Receivable

Aug 17 2,100Service Revenue

Aug 6 3,000

Bal. 12,400

BuildingAug 4 50, 000

R. Woodward, Capital

Aug 1 60,000

Rent Expense

Salary Expense

Aug 2 200

Supplies

Aug 2 200Accounts Payable

Aug 9 100Bal. 100

Aug 17 2,100

Aug 23 1,200

Aug 23 1,200

Aug 31 1,200Aug 31 500

Bal. 900Bal. 5,100

Aug 31 1,200

Aug 31 500

Take the difference between total debits and total credits to

determine the balance in each account. If

debits are greater than credits, the account has a debit balance

and vice versa

31

Revenue Principle

When is revenue recognized (entered

into the accounting records) ? When it is earned Not necessarily when cash is received

How much revenue is recognized? Cash value of item transferred to

customer

32

The Matching Principle

Measure all expenses incurred during the accounting period

When are expenses recognized? Match the expenses against the

revenues earned during the period

33

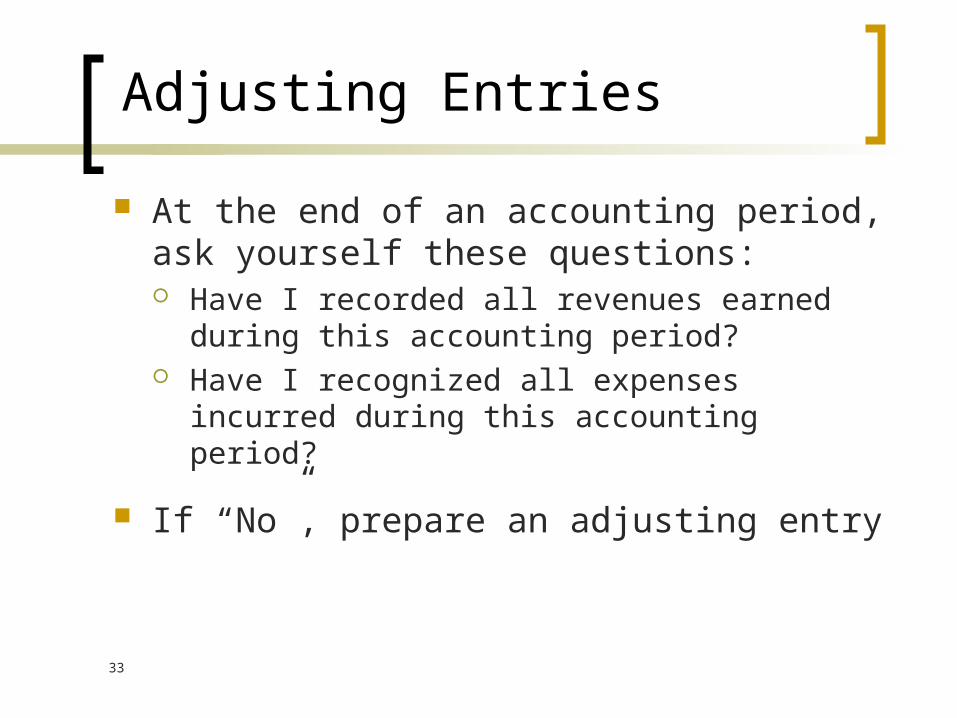

Adjusting Entries

At the end of an accounting period, ask yourself these questions: Have I recorded all revenues earned

during this accounting period? Have I recognized all expenses incurred

during this accounting period?

If “No”, prepare an adjusting entry

34

Adjusting Entries

Prepared at end of an accounting period

Recorded to bring an asset or liability account balance to its proper amount Recognize all revenues when earned Recognize all expenses incurred

35

Adjusting Prepaid Expenses

Resources paid for prior to receiving the actual benefits

Prepaid AssetPrepaid Asset

Used up portion = Expense

Used up portion = Expense

Unused portion = Prepaid

Unused portion = Prepaid

36

Depreciation - process of allocating the cost of a plant asset to expense over its expected useful life

Straight-LineDepreciation Expense

= Asset Cost

Useful Life

Adjusting for Depreciation

Long term plant assets except for land are

depreciated

37

Depreciation

Depreciation, for accounting purposes, has NOTHING to do with market value, resale value or insurance value of an asset.

It is a way to allocate the cost of the asset to each period that asset helps earn revenue

Accumulated Depreciation A contra asset account … it is the amount of

depreciation on that asset taken to date,

38

Tips

An adjusting entry will NEVER involve a debit or credit to Cash.

Each adjusting entry will affect at least one balance sheet account and one income statement account

Related Documents