Gemeinsam zum Handeln anregen Zurich Insurance Group Geschäftsbericht 2021

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Gemeinsam zum Handeln anregenZurich Insurance GroupGeschäftsbericht 2021

Konzernüberblick

Unser Geschäft 3

Brief des Verwaltungsratspräsidenten 10

Brief des Group CEO 12

Unser Geschäftsmodell 16

Unsere Strategie 18

Unsere Anspruchsgruppen 21

Governance

Mitteilung des Verwaltungsratspräsidenten zur Corporate Governance 40

Bericht über die Corporate Governance 42

Mitteilung des Vorsitzenden des Vergütungsausschusses 84

Vergütungsbericht 86

Integrated sustainability disclosure

Executive message on sustainability 120

Integrated sustainability disclosure 122

Risk review

Message from our Group Chief Risk Officer 184

Risk review 186

Financial review

Message from our Group Chief Financial Officer 218

Financial overview 220

Message from our Group Chief Investment Officer 230

Consolidated financial statements 232

Holding company 354

Shareholder information 368

Glossar 370

Kontakt 373

Zurich Insurance Group (Zurich) ist eine führende Mehrspartenversicherung, die über 55 Millionen Kunden – sowohl Privatpersonen als auch Unternehmen – in mehr als 210 Ländern und Gebieten betreut. Vor 150 Jahren gegründet, treibt Zurich heute den Wandel in der Versicherungsbranche voran. Die Gruppe bietet neben Versicherungsschutz zunehmend auch Präventionsdienstleistungen an, die beispielsweise das Wohlbefinden fördern und die Klimaresilienz stärken.

Im Einklang mit dem Ziel «gemeinsam eine bessere Zukunft zu gestalten» strebt Zurich danach, eines der verantwortungs und wirkungsvollsten Unternehmen der Welt zu sein. Die Gruppe beabsichtigt, bis 2050 NettoNullEmissionen zu erreichen, und ist gemäss dem S&P Global Corporate Sustainability Assessment einer der nachhaltigsten Versicherer weltweit. Im Jahr 2020 lancierte Zurich das Projekt «Zurich Forest», um die Wiederaufforstung und Wiederherstellung der Biodiversität in Brasilien zu unterstützen.

Die Gruppe hat ihren Hauptsitz in Zürich, Schweiz, und beschäftigt rund 56’000 Mitarbeitende. Zurich Insurance Group AG (ZURN) ist an der SIX Swiss Exchange kotiert und verfügt über ein Level I American Depositary Receipt Programm (ZURVY), das ausserbörslich an der OTCQX gehandelt wird. Weitere Informationen über Zurich sind verfügbar unter www.zurich.com.

Wenn wir zusammenarbeiten, erreichen wir mehr. Lernen Sie einige der Menschen kennen, die mit oder für Zurich arbeiten und dazu beitragen, das Unternehmen zu dem zu machen, was es heute ist. Erfahren Sie etwas über ihre Ansichten und wie sie andere dazu inspirieren, es ihnen gleichzutun und sich für wichtige Anliegen einzusetzen. Wir ziehen Bilanz aus 150 Jahren Innovation und blicken in eine Zukunft, in der sich Zurich weiter anpassen und wachsen wird – im Interesse des Unternehmens, seiner Kunden, Mitarbeitenden, Partner und des Planeten.

Zurich Insurance Group Geschäftsbericht 2021

Zum Handeln anregen

Zurich pflanzt zusammen mit dem lokalen NonProfitUnternehmen Instituto Terra eine Million Bäume im Atlantischen Regenwald in Brasilien, einem BiodiversitätsHotspot (siehe Titelbild). Das acht Jahre dauernde Projekt zielt nicht nur auf die Wiederherstellung der einheimischen Flora und Fauna ab, sondern auch darauf, die Mitarbeitenden von Zurich dazu anzuregen, umweltbewusster zu werden. Für den Fotografen Sebastião Salgado und seine Frau Lélia Wanick Salgado, die 1998 das Instituto Terra gegründet haben, ist es von entscheidender Bedeutung, gemeinsam an der Wiederherstellung unseres Planeten zu arbeiten. «Eine Idee zu haben, ist sehr wichtig. Aber das reicht nicht», sagt Sebastião Salgado. «Man muss auch Partner haben.»

Sebastião Salgado und Lélia Wanick SalgadoGründer des Instituto Terra

Um das Bewusstsein für den Verlust der Artenvielfalt zu schärfen, ist Zurich die globale Hauptpartnerin von Salgados «Amazônia» Ausstellungstournee und KonzertenSeite 34

Die Saat des Wandels säen

Zurich Insurance Group Geschäftsbericht 2021

1 Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Zum Handeln anregen

Widerstandsfähigkeit aufbauenAls Global Head for Climate Resilience Services beraten Amar Rahman und sein Team von Risk Engineers bei Zurich Resilience Solutions Kunden beim Aufbau von Widerstandsfähigkeit gegenüber Naturkatastrophen mit massgeschneiderten Erkenntnissen und Lösungen.

Zu diesen Kunden gehört der Automobilhersteller AUDI AG (Volkswagen Group). Als 2016 ein Produktionswerk der AUDI AG (Volkswagen Group) im südwestdeutschen Neckarsulm überschwemmt wurde und die Produktion zum Erliegen kam, beschloss der Automobilhersteller Massnahmen zur Verbesserung des Hochwasserschutzes zu ergreifen. Es wurde eine Reihe innovativer Schutzmassnahmen ergriffen, wie beispielsweise aufblasbare Wasserbarrieren, die nicht nur das Werk, sondern auch die Mitarbeitenden und die umliegenden Gemeinden vor Flutwellen schützen.

«Eine Verbesserung der Klimaresilienz beinhaltet auch, dass Unternehmen sofort in Anpassungen investieren und nicht auf neue Daten oder Regierungsvorschriften warten, bevor sie handeln», sagt Amar Rahman. «Wenn man wartet, wird es zu spät sein, um Lösungen zu entwickeln und umzusetzen.»

Die Bewährungsprobe folgte im Juni 2021, als heftige Regenfälle das Werk in Neckarsulm heimsuchten. Der Schaden am Standort war gering. Der Automobilhersteller will nun die gewonnenen Erkenntnisse und Erfahrungen auf andere Standorte der Volkswagen Group übertragen.

Amar RahmanGlobal Head Climate Change Resilience Services, Zurich Insurance Group

2 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unser Geschäft

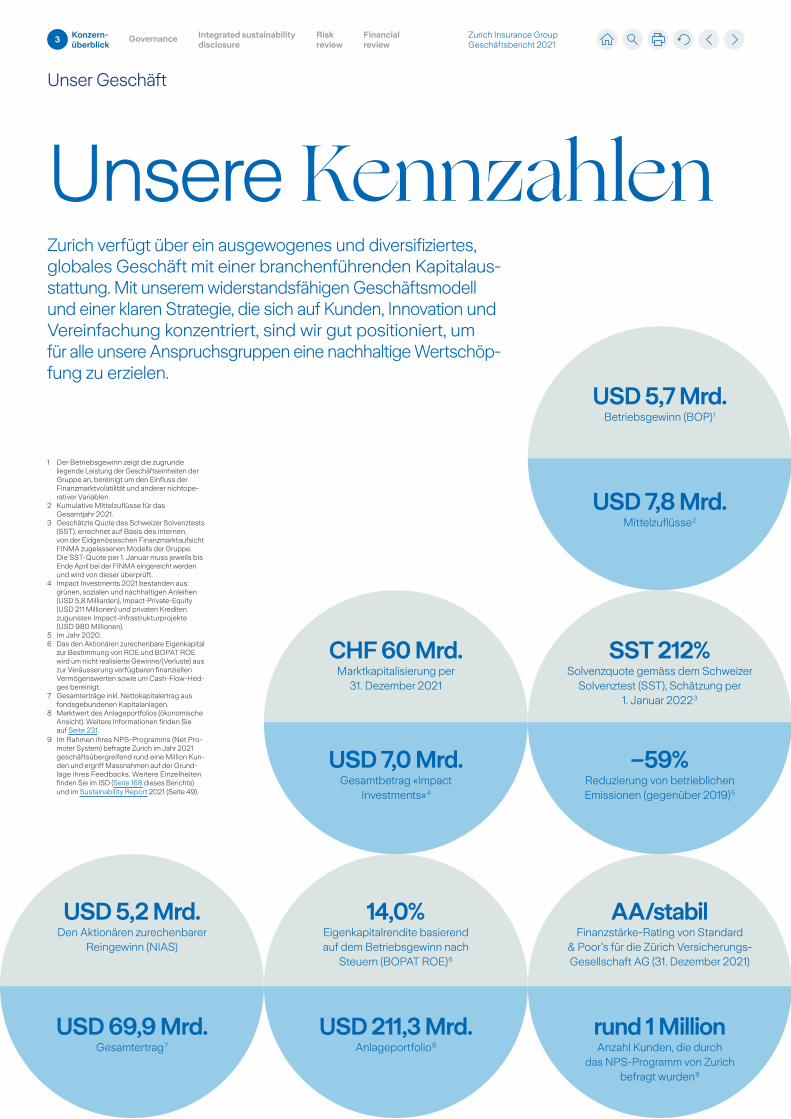

Unsere KennzahlenZurich verfügt über ein ausgewogenes und diversifiziertes, globales Geschäft mit einer branchenführenden Kapitalausstattung. Mit unserem widerstandsfähigen Geschäftsmodell und einer klaren Strategie, die sich auf Kunden, Innovation und Vereinfachung konzentriert, sind wir gut positioniert, um für alle unsere Anspruchsgruppen eine nachhaltige Wertschöpfung zu erzielen.

1 Der Betriebsgewinn zeigt die zugrunde liegende Leistung der Geschäftseinheiten der Gruppe an, bereinigt um den Einfluss der Finanzmarktvolatilität und anderer nichtoperativer Variablen.

2 Kumulative Mittelzuflüsse für das Gesamtjahr 2021.

3 Geschätzte Quote des Schweizer Solvenztests (SST), errechnet auf Basis des internen, von der Eidgenössischen Finanzmarktaufsicht FINMA zugelassenen Modells der Gruppe. Die SSTQuote per 1. Januar muss jeweils bis Ende April bei der FINMA eingereicht werden und wird von dieser überprüft.

4 Impact Investments 2021 bestanden aus: grünen, sozialen und nachhaltigen Anleihen (USD 5,8 Milliarden), ImpactPrivateEquity (USD 211 Millionen) und privaten Krediten zugunsten ImpactInfrastrukturprojekte (USD 980 Millionen).

5 Im Jahr 2020.6 Das den Aktionären zurechenbare Eigenkapital

zur Bestimmung von ROE und BOPAT ROE wird um nicht realisierte Gewinne/(Verluste) aus zur Veräusserung verfügbaren finanziellen Vermögenswerten sowie um CashFlowHedges bereinigt.

7 Gesamterträge inkl. Nettokapitalertrag aus fondsgebundenen Kapitalanlagen.

8 Marktwert des Anlageportfolios (ökonomische Ansicht). Weitere Informationen finden Sie auf Seite 231.

9 Im Rahmen ihres NPSProgramms (Net Promoter System) befragte Zurich im Jahr 2021 geschäftsübergreifend rund eine Million Kunden und ergriff Massnahmen auf der Grundlage ihres Feedbacks. Weitere Einzelheiten finden Sie im ISD (Seite 168 dieses Berichts) und im Sustainability Report 2021 (Seite 49).

USD 5,7 Mrd.Betriebsgewinn (BOP) 1

USD 5,2 Mrd.Den Aktionären zurechenbarer

Reingewinn (NIAS)

14,0%Eigenkapitalrendite basierend auf dem Betriebsgewinn nach

Steuern (BOPAT ROE) 6

USD 7,8 Mrd.Mittelzuflüsse 2

USD 69,9 Mrd.Gesamtertrag 7

USD 211,3 Mrd.Anlageportfolio 8

CHF 60 Mrd.Marktkapitalisierung per

31. Dezember 2021

SST 212%Solvenzquote gemäss dem Schweizer

Solvenztest (SST), Schätzung per 1. Januar 2022 3

AA/stabilFinanzstärkeRating von Standard

& Poor’s für die Zürich VersicherungsGesellschaft AG (31. Dezember 2021)

USD 7,0 Mrd.Gesamtbetrag «Impact

Investments» 4

–59%Reduzierung von betrieblichen Emissionen (gegenüber 2019) 5

rund 1 MillionAnzahl Kunden, die durch

das NPSProgramm von Zurich befragt wurden 9

3 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unser Geschäft (fortgesetzt)

1.

2.

3.

4.

5.

Business mix2021 Bruttoprämien und Policengebühren per Geschäftsbereich (%)2

1. Motor 20%

2. Property 38%

3. Liability 17%

4. Special lines 17%

5. Worker injury 8%

Business mix2021 Bruttoprämien, Policengebühren und Beiträge mit Anlagecharakter per Geschäftsbereich (%)2

1.

2.3.

4.

1. Protection 41%

2. Corporate pension 7%

3. Unit-linked 21%

4. Savings & annuity 30%

Business mix2021 Bruttoprämien per Geschäftsbereich (%)2

1. Auto 47%

2. Home 28%

3. Speciality 13%

4. Business insurance 10%

5. Other 2%

1.

2.

3.

4.5.

Dynamisch, agil und ausgewogenWir sind eine führende Mehrspartenversicherung, die Dienstleistungen für Kunden in globalen und lokalen Märkten erbringt. Wir bieten eine umfassende Palette von Produkten und Dienstleistungen in über 210 Ländern und Gebieten an. Zu unseren Kunden gehören Einzelpersonen, kleine, mittlere und grosse Unternehmen sowie multinationale Konzerne.

Schaden- und UnfallversicherungVersicherung, Dienstleistungen und Risikoanalysen

USD 3,1 Mrd.Betriebsgewinn 1

USD 40,1 Mrd.Bruttoprämien und Policengebühren

LebensversicherungLebensversicherungen, Kapitalanlagen, Spar und Vorsorgelösungen

USD 1,8 Mrd.Betriebsgewinn 1

USD 28,4 Mrd.Bruttoprämien, Policengebühren und Beiträge mit Anlagecharakter

Farmers Group, Inc.3

Eine hundertprozentige Tochtergesellschaft, die bestimmte Dienstleistungen für die Exchanges erbringt.3

USD 1,6 Mrd.Betriebsgewinn 1

USD 4,3 Mrd.Managementgebühren und verbundene Erträge

Farmers Exchanges3

– Zurich ist ein führender, globaler Firmenkundenversicherer mit einem profitablen Privatkundengeschäft. Mit der verbesserten Portfolioqualität im Firmenkundengeschäft sind wir gut positioniert, um über den gesamten Zyklus hinweg erfolgreich zu sein.

– Der SchadenKostenSatz in der Schaden und Unfallversicherung – eine Kennzahl für die Rentabilität – war mit 94,3 Prozent auf dem niedrigsten Stand der letzten 15 Jahre.

– Das Firmenkundengeschäft generiert etwa zwei Drittel der Bruttoprämien in der Schaden und Unfallversicherung der Gruppe.

Mehr zu Schaden- und UnfallversicherungSeiten 222–223

– Zurich verfolgt eine langfristige Strategie mit Fokus auf Vorsorgelösungen und Sparprodukten mit geringer Kapitalbindung. Damit ist das Lebensversicherungsgeschäft gut für das derzeitige Niedrigzinsumfeld positioniert.

– 2021 machten Vorsorgelösungen, fondsgebundene Produkte und das Kollektivlebenversicherungsgeschäft 90 Prozent des Neugeschäfts aus.

Mehr zu LebensversicherungSeiten 224–225

– Zurich hält keine Eigentumsanteile an den Farmers Exchanges 3, die Eigentum ihrer Versicherungsnehmer sind. Die Exchanges sind ein führender Privatkundenversicherer in den USA.

– Die Farmers Exchanges 3 konzentrieren sich darauf, den Kundenkreis durch Ausweitung und Diversifizierung des Vertriebs zu vergrössern.

Mehr zu Farmers Group, Inc. und Farmers Exchanges 3

Seite 226

1 Der Betriebsgewinn zeigt die zugrunde liegende Leistung der Geschäftseinheiten der Gruppe an, bereinigt um den Einfluss der Finanzmarktvolatilität und anderer nichtoperativer Variablen.2 Summe der gerundeten Prozentsätze kann von 100 abweichen.3 Die Zurich Insurance Group hält keine Eigentumsanteile an den Farmers Exchanges. Die Farmers Group, Inc., eine hundert prozentige Tochtergesellschaft der Gruppe, erbringt als Bevoll mäch tigte

bestimmte nicht auf die Schadenabwicklung bezogene Dienstleistungen und Nebendienstleistungen für die Farmers Exchanges und erhält hierfür eine Gebühr.

4 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

5 Konzern-überblick

Financial review

Risk review

Governance Integrated sustainability disclosure

Zum Handeln anregen

Zum Handeln anregen

Vertrauen gewinnenAls Assistentin in der Schadenabwicklung von Zurich setzt Carriane Chan unsere kundenorientierte Strategie täglich um. Bei jeder Schadenanfrage setzt Carriane Chan darauf, Vertrauen zu den Kundinnen und Kunden aufzubauen, indem sie ihnen zuhört, ihre Bedürfnisse erkennt und sie vor allem als Menschen behandelt. «Es ist wichtig, dass wir uns in die Situation unserer Kundinnen und Kunden hineinversetzen», sagt Carriane Chan, die in Hongkong arbeitet. «Indem wir uns auf die Einzigartigkeit und nicht auf die Gemeinsamkeiten jeder einzelnen Schadenanfrage konzentrieren, können wir unseren Kundinnen und Kunden eine bessere Erfahrung bieten – und wenn sie zufriedener sind, sind auch wir zufriedener mit unserer Arbeit.»

Carriane ChanClaims Service Assistant, Zurich Hong Kong

Für etwas einstehen«Mit kleinen Veränderungen und gemeinsamem Handeln lässt sich viel bewirken», sagt Amy Meek, Mitbegründerin der britischen gemeinnützigen Organisation Kids Against Plastic. Amy Meek gründete die Organisation zusammen mit ihrer Schwester Ella im Jahr 2016, als sie gerade 12 und 10 Jahre alt waren. Kids Against Plastic weckt das Bewusstsein für die mit der Plastikverschmutzung verbundenen Umweltprobleme und inspiriert die Menschen dazu, Plastikabfälle zu vermeiden. Amy Meek sprach kürzlich auf der Youth Against Carbon Conference, die von Zurich UK organisiert wurde, um jungen Menschen eine Stimme in der Debatte über Massnahmen zur Bekämpfung des Klimawandels zu geben. Sie spielte auch eine Schlüsselrolle in der globalen Markenkampagne des Unternehmens, in der sie als «Klimaheldin» agierte, um zu inspirieren und die geballte Kraft des gemeinsamen Handelns zu zeigen.

Amy MeekAktivistin und Mitbegründerin von Kids Against Plastic

Zurich Insurance Group Geschäftsbericht 2021

Zum Handeln anregen

Ein blaues Spielzeugauto, ein Mittel gegen Kater und ein Golfschlägerset reihen sich aneinander, zusammen mit Unmengen von Prämien, Schadensfällen und Ausgaben von den 1880er bis zu den 1980erJahren. Willkommen in den Archiven des Unternehmens: eine Sammlung von Akten und Gegenständen aus der 150jährigen Geschichte von Zurich. Der Unternehmenshistoriker Thomas Inglin ist der Verwalter dieser Artikel und wählt zusammen mit seinem Team aus, welche Objekte erhalten werden sollen.

«Zurich hat mehr Erfahrung und mehr Wissen als einzelne Individuen, und es ist wichtig, dass künftige Generationen dieses Wissen nutzen», sagt Thomas Inglin, der im Jahr 1995, als er zu Zurich stiess, mit dem Aufbau des Archivs begann. Für ihn ist das archivierte Material, das sich insgesamt über 2’600 Meter erstrecken würde, eine «unendliche Quelle der Inspiration».

Thomas InglinHead of Corporate Archives, Zurich Insurance Group

150 Jahre und darüber hinaus

6 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unser Geschäft (fortgesetzt)

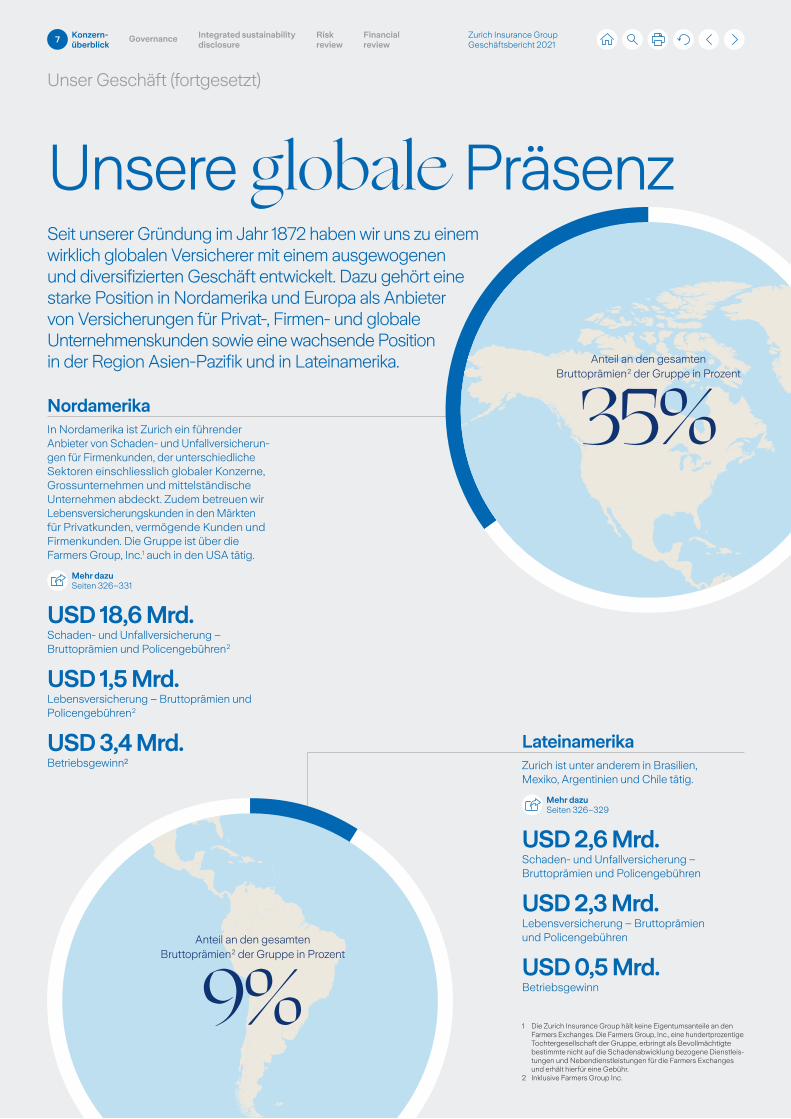

Unsere globale PräsenzSeit unserer Gründung im Jahr 1872 haben wir uns zu einem wirklich globalen Versicherer mit einem ausgewogenen und diversifizierten Geschäft entwickelt. Dazu gehört eine starke Position in Nordamerika und Europa als Anbieter von Versicherungen für Privat, Firmen und globale Unternehmenskunden sowie eine wachsende Position in der Region AsienPazifik und in Lateinamerika.

NordamerikaIn Nordamerika ist Zurich ein führender Anbieter von Schaden und Unfallversicherungen für Firmenkunden, der unterschiedliche Sektoren einschliesslich globaler Konzerne, Grossunternehmen und mittelständische Unternehmen abdeckt. Zudem betreuen wir Lebensversicherungskunden in den Märkten für Privatkunden, vermögende Kunden und Firmenkunden. Die Gruppe ist über die Farmers Group, Inc.1 auch in den USA tätig.

Mehr dazuSeiten 326–331

USD 18,6 Mrd.Schaden und Unfallversicherung – Bruttoprämien und Policengebühren 2

USD 1,5 Mrd.Lebensversicherung – Bruttoprämien und Policengebühren 2

USD 3,4 Mrd.Betriebsgewinn�

Anteil an den gesamten Bruttoprämien 2 der Gruppe in Prozent

35%

Lateinamerika Zurich ist unter anderem in Brasilien, Mexiko, Argentinien und Chile tätig.

Mehr dazuSeiten 326–329

USD 2,6 Mrd.Schaden und Unfallversicherung – Bruttoprämien und Policengebühren

USD 2,3 Mrd.Lebensversicherung – Bruttoprämien und Policengebühren

USD 0,5 Mrd.Betriebsgewinn

1 Die Zurich Insurance Group hält keine Eigentumsanteile an den Farmers Exchanges. Die Farmers Group, Inc., eine hundertprozentige Tochtergesellschaft der Gruppe, erbringt als Bevollmächtigte bestimmte nicht auf die Schadenabwicklung bezogene Dienstleistungen und Nebendienstleistungen für die Farmers Exchanges und erhält hierfür eine Gebühr.

2 Inklusive Farmers Group Inc.

Anteil an den gesamten Bruttoprämien 2 der Gruppe in Prozent

9%

7 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unser Geschäft (fortgesetzt)

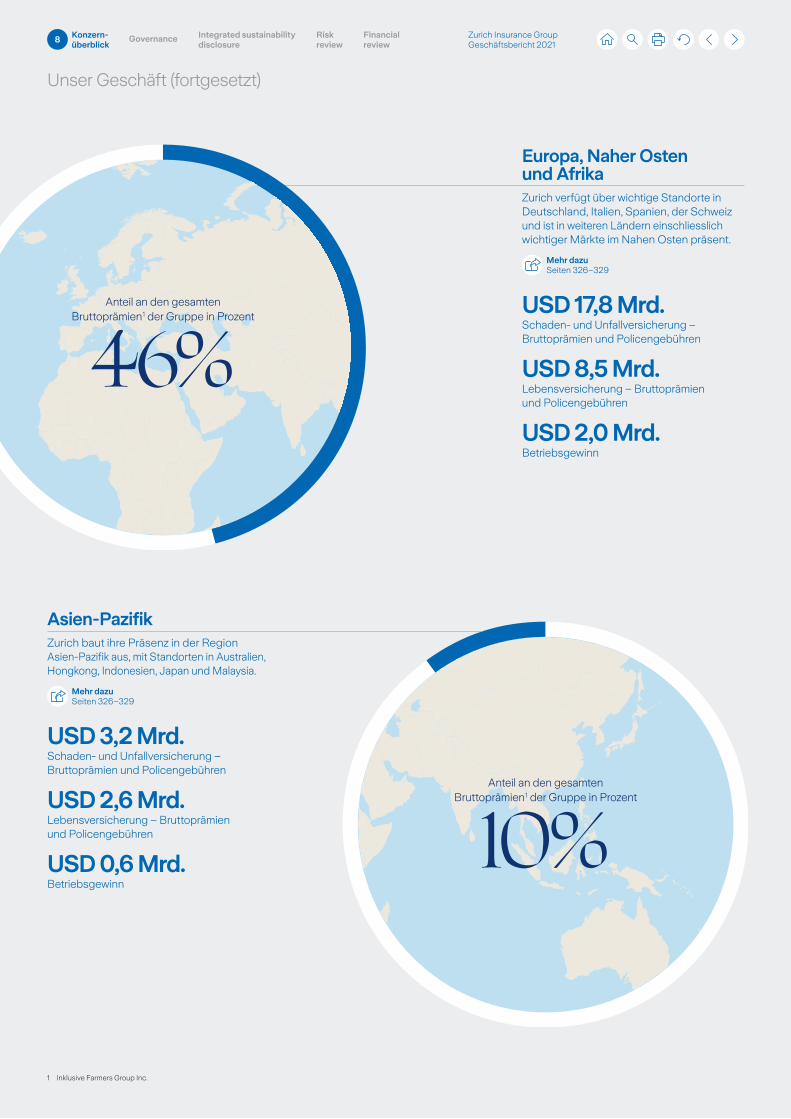

Asien-PazifikZurich baut ihre Präsenz in der Region AsienPazifik aus, mit Standorten in Australien, Hongkong, Indonesien, Japan und Malaysia.

Mehr dazuSeiten 326–329

USD 3,2 Mrd.Schaden und Unfallversicherung – Bruttoprämien und Policengebühren

USD 2,6 Mrd.Lebensversicherung – Bruttoprämien und Policengebühren

USD 0,6 Mrd.Betriebsgewinn

1 Inklusive Farmers Group Inc.

Europa, Naher Osten und Afrika Zurich verfügt über wichtige Standorte in Deutschland, Italien, Spanien, der Schweiz und ist in weiteren Ländern einschliesslich wichtiger Märkte im Nahen Osten präsent.

Mehr dazuSeiten 326–329

USD 17,8 Mrd.Schaden und Unfallversicherung – Bruttoprämien und Policengebühren

USD 8,5 Mrd.Lebensversicherung – Bruttoprämien und Policengebühren

USD 2,0 Mrd.Betriebsgewinn

Anteil an den gesamten Bruttoprämien 1 der Gruppe in Prozent

10%

Anteil an den gesamten Bruttoprämien 1 der Gruppe in Prozent

46%

8 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Zum Handeln anregen

«Returnships» bieten qualifizierten Frauen die Möglichkeit, nach einer beruflichen Auszeit ins Berufsleben zurückzukehren. Dies ist nur ein Beispiel dafür, wie Zurich unterschiedlichste Talente anzieht und für sich gewinnt. Im Rahmen eines ReturnshipProgramms konnte Gabriela Reynolds nach einer zweijährigen Auszeit von ihrer Tätigkeit als Anwältin eine Festanstellung bei Zurich finden und dabei von einem Onthejob Training sowie von vielfältigen Vernetzungsmöglichkeiten profitieren.

Gabriela arbeitet jetzt in der Abteilung Human Resources und hofft, dass ihre Geschichte andere dazu inspiriert, die Vorteile eines ReturnshipProgramms bei Zurich zu nutzen. «Es handelt sich um eine WinwinSituation für die Teilnehmenden und das Unternehmen», sagt Gabriela. «Für die Teilnehmenden geht es darum, das Beste aus der Erfahrung zu machen: das Unternehmen und die Menschen kennenlernen und die eigenen Kompetenzen ausbauen, um für zukünftige berufliche Chancen darauf aufbauen zu können. Für das Unternehmen ist es eine wunderbare Gelegenheit, Menschen mit Energie, Leidenschaft und einer frischen Perspektive willkommen zu heissen.»

Gabriela ReynoldsHR Program Manager, Zurich Insurance Group

Ein Comeback starten

9 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Brief des Verwaltungsratspräsidenten

Zum Handeln anregen

Das Fundament für unsere ehrgeizigen Ziele legenIch bin stolz darauf, dem Verwaltungsrat eines Unternehmens vorzustehen, das auch in schwierigen Zeiten seine Verpflichtung erfüllt, für die Menschen und den Planeten einzustehen und für alle Anspruchsgruppen Vorteile zu erzielen.

Michel M. LièsPräsident des Verwaltungsrats

10 Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Zurich Insurance Group Geschäftsbericht 2021

Brief des Verwaltungsratspräsidenten (fortgesetzt)

Das Fundament für unsere ehrgeizigen Ziele legen

Es ist kaum zu glauben, dass es zwei Jahre her ist, seit COVID19 zur Pandemie erklärt wurde. Wir haben einen langen Kampf geführt, um das Virus einzudämmen, Leben zu retten, unsere mentale Gesundheit zu erhalten, Existenzen zu sichern, Bildung zu ermöglichen und unseren Alltag weiterhin so gut wie möglich zu bewältigen.

Ebenso wie der Rest der Welt mussten wir bei Zurich uns ständig an die sich verändernden Umstände anpassen. Dennoch hat unser Unternehmen seine Widerstandsfähigkeit bewahrt, und dafür danke ich all unseren 56’000 Mitarbeitenden. Sie haben eine anstrengende und turbulente Zeit hinter sich, und ich habe tiefes Mitgefühl mit denen, die durch die Pandemie persönliches Leid erfahren haben.

Ebenso wie 2020 war auch das letzte Jahr für unsere Kunden wieder eine Herausforderung. Unsere Mitarbeitenden haben Stärke, Flexibilität und Einfallsreichtum gezeigt, damit die Kunden weiterhin an erster Stelle stehen. Ihr Engagement hat mich wirklich inspiriert.

Robuste Ziele und Werte Es überrascht mich nicht, dass unsere Mitarbeitenden der Herausforderung gewachsen sind. Es gehört zur DNA unseres Unternehmens, ein Verständnis dafür zu haben, dass wir für unsere Kunden da sein müssen, wenn sie uns am dringendsten brauchen, selbst in diesen sehr besonderen Zeiten.

Unsere DNA wird unterstützt durch eine ehrgeizige Zielsetzung, robuste Werte und einen glaubwürdigen Verhaltenskodex. Ich bin stolz darauf, dem Verwaltungsrat eines Unternehmens vorzustehen, das auch in schwierigen Zeiten seine Verpflichtung erfüllt, für die Menschen und den Planeten einzustehen und für alle Anspruchsgruppen Vorteile zu erzielen – Kunden, Mitarbeitende, Investoren und Gemeinschaften.

Als Verwaltungsrat nehmen wir auch unsere Verantwortung für die Aufrechterhaltung und Einbettung unserer Strategie für Umwelt, Soziales und Governance (ESG) sehr ernst, die ständiger Veränderung unterliegt und uns die Möglichkeit gibt, auf kritische Risiken in diesen Bereichen zu reagieren – von Klimawandel und Verlust der Biodiversität bis zu sozialer Ungleichheit und der anhaltenden Pandemie (siehe Seiten 40–41).

Widerstandsfähigkeit bildet das Fundament für ehrgeizige ZieleZu Beginn des letzten Jahres unseres dreijährigen Strategiezyklus liegt die Gruppe weiterhin auf Kurs, um unsere Ziele für 2022 zu erreichen. Unsere Massnahmen zur Digitalisierung unseres Geschäfts haben Zurich leistungsfähiger, schneller und widerstandsfähiger als je zuvor gemacht. Das verleiht uns ein starkes Fundament, um ehrgeizige Ziele für einen neuen dreijährigen Strategiezyklus festzulegen, die wir im November präsentieren werden.

Im Jahr 2022 werden wir zudem unser 150jähriges Bestehen feiern. Ich hoffe, dass dies ein Jahr sein wird, in dem wir uns darauf konzentrieren können, die Welt zu einem besseren Ort für alle zu machen.

Michel M. LièsPräsident des Verwaltungsrats

Zurich Insurance Group Geschäftsbericht 2021

Integrated sustainability disclosure

Governance Risk review

Financial review

Konzern-überblick

11

Brief des Group CEO

Zum Handeln anregen

Unsere Leistung zeigt einmal mehr, dass sich unsere Disziplin auszahlt. Im Firmenkundengeschäft konnten wir in den letzten Jahren durch unsere Bemühungen zur Neuausrichtung und Verbesserung der Qualität des Geschäftsportfolios stark von den steigenden Preisen profitieren. Durch unsere konsequente Ausrichtung auf die Kundinnen und Kunden wächst auch unser Privatkundengeschäft.

Mario GrecoGroup Chief Executive Officer

Bemerkenswerte Fortschritte

12 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Brief des Group CEO (fortgesetzt)

Erfüllende Karrieren anbieten

Menschen sind die treibende Kraft hinter unserem Geschäft, und wir sind der Auffassung, dass unsere

Mitarbeitenden ihre eigenen Karrieren vorantreiben sollten. Wir unterstützen unsere Mitarbeitenden

dabei, ihre Weiterbildung und Umschulung sowie ihre berufliche Entwicklung selbst in die Hand zu nehmen.

Durch Investitionen in unsere Mitarbeitenden können wir sicherstellen, dass wir die besten Talente anziehen

und halten.

Für den PlanetenWir bei Zurich sind der Meinung, dass erfolgreich sein

und Gutes tun Hand in Hand geht. Aus diesem Grund suchen wir nach Möglichkeiten, unseren Kundinnen und

Kunden umweltfreundlichere Versicherungslösungen anzubieten: von der nutzungsbasierten Autoversicherung

bis zur branchenweit ersten klimaneutralen Anlageoption für die Kundinnen und Kunden fondsgebundener

Lebensversicherungen.

Sich auf neue Regeln der Finanzberichterstattung

vorbereitenZurich ist dabei, die Umsetzung der

Rechnungslegungsstandards IFRS17 und IFRS9 – zwei der bedeutendsten Änderungen der globalen

Finanzberichterstattung in der jüngeren Vergangenheit – abzuschliessen. Unser Fokus liegt nun darauf, die Dynamik

der finanziellen Performance und der Kennzahlen im Rahmen der neuen Standards vollständig zu bewerten und unsere

wichtigsten Anspruchsgruppen im Hinblick auf die Berichterstattung nach den neuen Regeln im Jahr 2023

zu informieren.

Sich wandelnde Kundenbedürfnisse

Individuell, einfach und jederzeit verfügbar. Zurich definiert die globale Kundenerfahrung neu und schafft innovative

Lösungen sowohl für bestehende Kundinnen und Kunden als auch für die nächste Generation.

Immer einen Schritt voraus sein

Unternehmen aller Grössen konzentrieren sich zunehmend auf Risikoprävention, Risikominderung und Widerstandsfähigkeit. Mit Zurich Resilience Solutions

bieten wir Dienstleistungen an, die über den traditionellen Versicherungsrisikotransfer hinausgehen. Mit unseren Lösungen helfen wir Unternehmen, die Risiken ihres

Kerngeschäfts zu steuern, und stellen ein Frühwarnsystem sowie schnelle, praktische Hilfe zur Verfügung.

Leben in einer digitalen Welt

Unser Leben wird immer digitaler – von der Kommunikation über die Arbeit bis hin zum Abschluss von Versicherungen.

Wir investieren in unsere digitalen Fähigkeiten, um auf die Bedürfnisse unserer Kundinnen und Kunden einzugehen

und ihr bevorzugter Anbieter zu bleiben. Ausserdem nutzen wir die Digitalisierung dazu, die Zusammenarbeit mit

unseren Kundinnen und Kunden nicht unnötig kompliziert zu machen.

Auf ein sich änderndes Geschäftsumfeld reagieren:Tiefgreifende Veränderungen wie der digitale Fortschritt, Versicherungslösungen von neuen,

nichttraditionellen Anbietern und höhere Kundenerwartungen haben Auswirkungen auf uns alle. Wir stellen sicher, dass wir das richtige Fachwissen haben, um erfolgreich zu sein, und gewährleisten,

dass Zurich für zukünftige Herausforderungen gut gerüstet ist.

Unsere Leistung im Jahr 2021Wir haben 2021 bemerkenswerte Fortschritte gemacht: neue Kundinnen und Kunden gewonnen, die Rentabilität verbessert und unser Geschäft vereinfacht in einem Jahr, das von anhaltenden Beeinträchtigungen durch COVID19 und schweren Auswirkungen von Naturkatastrophen geprägt war.

Diese Leistung basiert auf einem tiefen Risikoverständnis. Seit 150 Jahren schützt Zurich diejenigen, die ihr Vertrauen in uns setzen, und hat sich auch in Zeiten grosser Veränderungen erfolgreich behauptet. Unser 150. Jubiläum in diesem Jahr bietet Gelegenheit, eine Bestandsaufnahme unserer Stärken zu machen und uns vor Augen zu führen, was wir bisher erreicht haben – und mit Zuversicht in die Zukunft zu blicken.

Die heutigen Herausforderungen erinnern uns daran, dass wir, aufbauend auf unserem Vermächtnis, unsere Widerstandsfähigkeit weiter stärken und unser Unternehmen, unsere Mitarbeitenden sowie unsere Gemein schaf ten auf eine nachhaltige Zukunft vorbereiten müssen.

Kundenbedürfnisse erfüllenUnsere Ergebnisse im Jahr 2021 zählen zu den besten in unserer Geschichte. Unser den Aktionären zurechenbare Reingewinn von USD 5,2 Milliarden und der Betriebsgewinn von USD 5,7 Milliarden waren die höchsten seit 2007. Diese Ergebnisse sind der Lohn für die harte Arbeit eines hervorragenden Teams, und ich möchte allen meinen Kolleginnen und Kollegen für ihren Beitrag danken.

Unsere Leistung zeigt einmal mehr, dass sich unsere Disziplin auszahlt. Im Firmenkundengeschäft konnten wir in den letzten Jahren durch unsere Bemühungen zur Neuausrichtung und Verbesserung der Qualität des Geschäftsportfolios stark von den steigenden Preisen profitieren.

Durch unsere konsequente Ausrichtung auf die Kundinnen und Kunden wächst auch unser Privatkundengeschäft. Allein im letzten Jahr konnten wir netto 2,2 Millionen Privatkunden 1 hinzugewinnen, weil wir flexibel sind, uns schnell an die sich ändernden Kundenbedürfnisse anpassen und Technologien einsetzen, um die Kundenerfahrung zu verbessern, die Interaktionen zu optimieren und unser Angebot von dem unserer Mitbewerber zu differenzieren.

Bemerkenswerte Fortschritte

1 Basierend auf acht Privatkundenmärkten: Australien, Brasilien, Deutschland, Japan, Italien, Santander JV, Spanien, Schweiz.

13 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Brief des Group CEO (fortgesetzt)

Unser 150-jähriges JubiläumWir von Zurich wollen Vertrauen in die Zukunft wecken. Seit 1872 helfen wir jeden Tag Unternehmen, Familien und Gemeinschaften dabei, erfolgreich zu sein und zu wachsen.

Im Rahmen unseres 150jährigen Jubiläums feiern wir unsere Vergangenheit und unsere Gegenwart, unsere Kundinnen und Kunden, unsere Gemeinschaften und unsere Mitarbeitenden – all jene, die uns so weit gebracht haben.

Zu den Feierlichkeiten gehören globale Town Halls, spezielle Veranstaltungen und die Veröffentlichung eines Jubiläumsbuchs im EBookFormat. Der Höhepunkt wird die offizielle Jubiläumsfeier im Oktober sein (siehe Seite 32).

Seit mehr als 150 Jahren setzt Zurich positive Akzente. Wir haben bewiesen, dass wir auf Herausforderungen richtig reagieren und uns anpassen können, und wir blicken zuversichtlich auf die Zukunft.

Nur wenige Monate nach Bekanntgabe unserer Ziele für 2020–2022 stellte die Pandemie unsere Pläne auf den Kopf, worauf wir schnell reagierten und einen neuen Kurs einschlugen. Zwei Jahre später sind wir auf dem besten Weg, unsere Ziele zu erreichen, und wir sind bereit, uns neue Ziele für den nächsten Strategiezyklus im November zu setzen.

Risiken in Chancen verwandelnDas Versicherungsgeschäft hat sich seit der Gründung von Zurich im Jahr 1872 – des Zeitalters von Dampfmaschinen, Pferden und Telegrafen – drastisch verändert. Die heutigen Risiken sind komplexer, miteinander verknüpft und global. Wir unterstützen unsere Kundinnen und Kunden, unsere Geschäftspartner und unsere Gemeinschaften aktiv dabei, ihre Widerstandsfähigkeit gegenüber unerwünschten Ereignissen zu stärken, bevor diese eintreten, und ergänzen damit den traditionellen Risikotransfer, der die Kosten deckt, wenn etwas schiefgeht.

Durch unsere enge Beziehung zu unseren Kundinnen und Kunden und unsere 150jährige Erfahrung können wir ihnen spezifische Erkenntnisse und Instrumente an die Hand geben, um sie bei der Steuerung traditioneller und neuer Risiken zu unterstützen, sei es im Zusammenhang mit dem Klimawandel, den Lieferketten oder der Cybersicherheit. Das gehört zur Rolle einer Versicherung in der Gesellschaft: Wir helfen, Risiken zu verringern und nachhaltiges Verhalten zu fördern.

Wir reagieren auch auf die Komplexität und den rasanten Wandel unserer Zeit, indem wir unseren Mitarbeitenden helfen, sich in diesem Umfeld zurechtzufinden. Nachhaltige Arbeitsgestaltung ist für uns zentral, daher unterstützen wir unsere Kolleginnen und Kollegen unter anderem dabei, ihre Fähigkeiten ständig weiterzuentwickeln, und der beste Beweis für unseren Erfolg ist, dass zwei Drittel der offenen Stellen bei Zurich mit internen Kandidatinnen und Kandidaten besetzt werden.

Zum Handeln anregenUm die Risiken des Klimawandels, der Digital isierung und der sozialen Ungleichheit zu bewältigen, ist gemeinsames Handeln gefragt – von Regierungen, Unternehmen und Einzelpersonen. Wir wollen unsere Kundinnen und Kunden, unsere Mitarbeitenden, unsere Partner und die Gemeinschaften, in denen wir tätig sind, dabei unterstützen, das zu tun, was für sie am wichtigsten ist.

Unser Projekt «Zurich Forest» trägt zum Beispiel dazu bei, das Umweltbewusstsein unserer Mitarbeitenden zu stärken. In Zusammenarbeit mit dem gemeinnützigen Instituto Terra unterstützen wir die artenreiche Aufforstung des atlantischen Regenwalds in Brasilien. Seit September 2020 sind mehr als 200’000 Setzlinge gepflanzt worden. Die Mitarbeitenden können sich einen Baum aussuchen und danach den Prozess der Wiederaufforstung Schritt für Schritt verfolgen.

Im Jahr 2021 zeigten die Geschäftseinheiten, die Mitarbeitenden, die Kundinnen und Kunden sowie die Vertriebspartner von Zurich im Rahmen der grössten Spendenaktion der Z Zurich Foundation 1 seit ihrer Gründung im Jahr 1973, was man mit vereinten Kräften erreichen kann. Die im Zuge der Spendenaktion gesammelten Mittel ermöglichen der UNICEF, mehr als 1,7 Millionen besonders gefährdeten Personen jeweils zwei Dosen COVID19Impfstoff zu verabreichen.

1 Die Z Zurich Foundation ist eine gemeinnützige Stiftung mit Sitz in der Schweiz, die von verschiedenen Mitgliedern der Gruppe finanziert wird. Sie ist das wichtigste Vehikel zur Umsetzung der globalen Investitionsstrategie von Zurich zugunsten von Gemeinschaften.

14 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Brief des Group CEO (fortgesetzt)

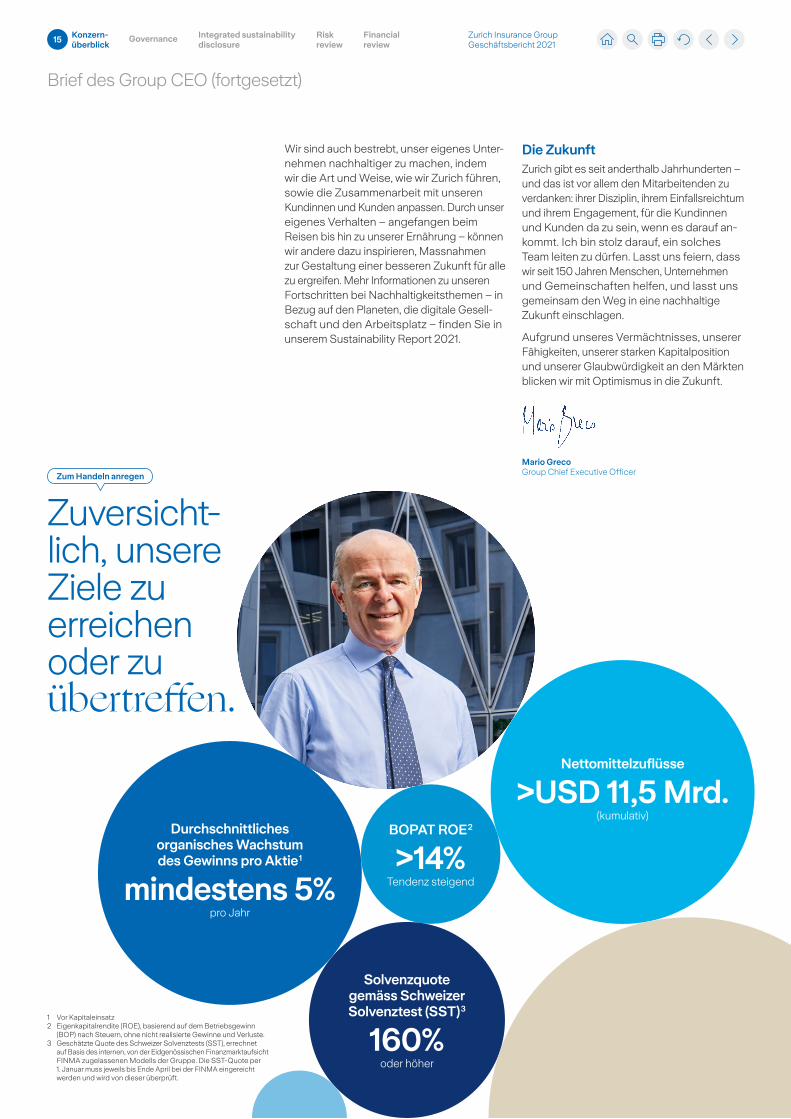

Nettomittelzuflüsse

>USD 11,5 Mrd.(kumulativ)

1 Vor Kapitaleinsatz2 Eigenkapitalrendite (ROE), basierend auf dem Betriebsgewinn

(BOP) nach Steuern, ohne nicht realisierte Gewinne und Verluste.3 Geschätzte Quote des Schweizer Solvenztests (SST), errechnet

auf Basis des internen, von der Eidgenössischen Finanzmarktaufsicht FINMA zugelassenen Modells der Gruppe. Die SSTQuote per 1. Januar muss jeweils bis Ende April bei der FINMA eingereicht werden und wird von dieser überprüft.

BOPAT ROE 2

>14%Tendenz steigend

Durchschnittliches organisches Wachstum des Gewinns pro Aktie 1

mindestens 5%pro Jahr

Solvenzquote gemäss Schweizer Solvenztest (SST) 3

160%oder höher

Zuversichtlich, unsere Ziele zu erreichen oder zu

bertreffen.

Wir sind auch bestrebt, unser eigenes Unternehmen nachhaltiger zu machen, indem wir die Art und Weise, wie wir Zurich führen, sowie die Zusammenarbeit mit unseren Kundinnen und Kunden anpassen. Durch unser eigenes Verhalten – angefangen beim Reisen bis hin zu unserer Ernährung – können wir andere dazu inspirieren, Massnahmen zur Gestaltung einer besseren Zukunft für alle zu ergreifen. Mehr Informationen zu unseren Fortschritten bei Nachhaltigkeitsthemen – in Bezug auf den Planeten, die digitale Gesellschaft und den Arbeitsplatz – finden Sie in unserem Sustainability Report 2021.

Die ZukunftZurich gibt es seit anderthalb Jahrhunderten – und das ist vor allem den Mitarbeitenden zu verdanken: ihrer Disziplin, ihrem Einfallsreichtum und ihrem Engagement, für die Kundinnen und Kunden da zu sein, wenn es darauf ankommt. Ich bin stolz darauf, ein solches Team leiten zu dürfen. Lasst uns feiern, dass wir seit 150 Jahren Menschen, Unternehmen und Gemeinschaften helfen, und lasst uns gemeinsam den Weg in eine nachhaltige Zukunft einschlagen.

Aufgrund unseres Vermächtnisses, unserer Fähigkeiten, unserer starken Kapitalposition und unserer Glaubwürdigkeit an den Märkten blicken wir mit Optimismus in die Zukunft.

Mario GrecoGroup Chief Executive OfficerZum Handeln anregen

15 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unser Geschäftsmodell

Schaden- und Unfallversicherung

Lebensversicherung

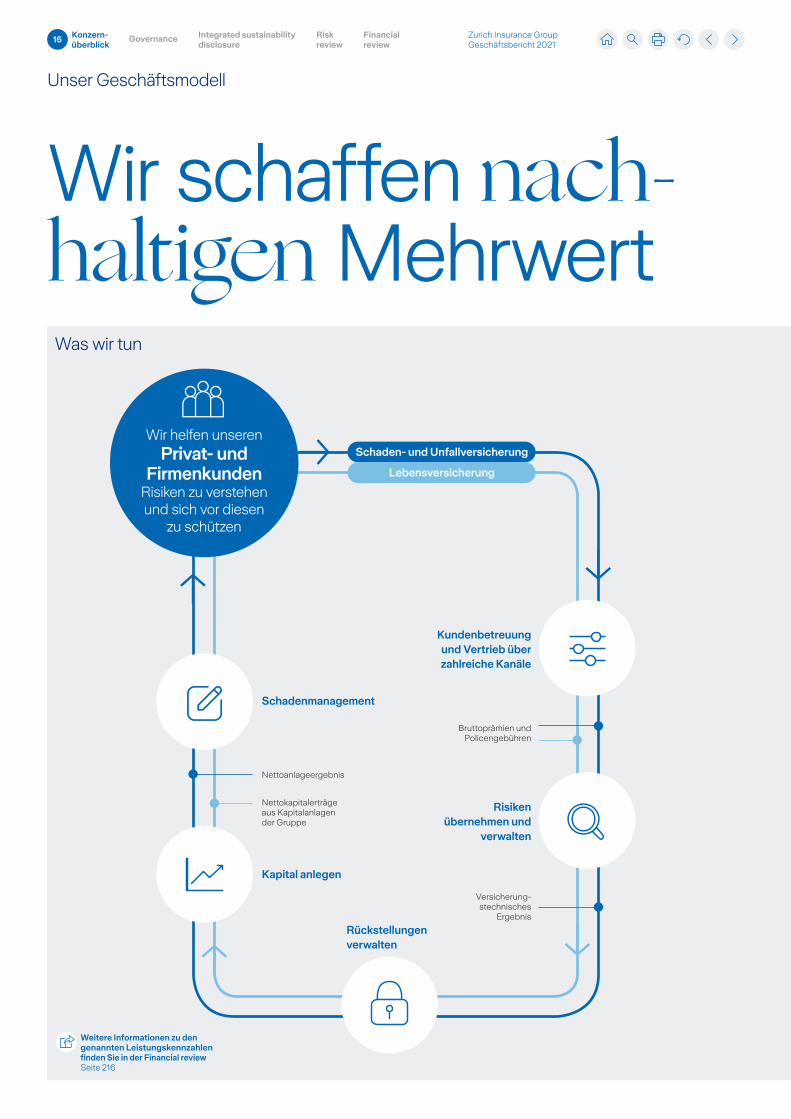

Wir schaffen nachhaltigen MehrwertWas wir tun

Kundenbetreuung und Vertrieb über zahlreiche Kanäle

Risiken übernehmen und

verwalten

Rückstellungen verwalten

Kapital anlegen

Schadenmanagement

Bruttoprämien und Policengebühren

Nettoanlageergebnis

Nettokapitalerträge aus Kapitalanlagen der Gruppe

Versicherungstechnisches

Ergebnis

Wir helfen unseren Privat- und

Firmenkunden Risiken zu verstehen und sich vor diesen

zu schützen

Weitere Informationen zu den genannten Leistungskennzahlen finden Sie in der Financial reviewSeite 216

16 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unser Geschäftsmodell (fortgesetzt)

Rückstellungen verwalten

Unsere konzernweite Richtlinie, der «Zurich Way of Reserving» für die Bildung von Rückstellungen mit genau definierten konservativen Normen, bildet die Grundlage für unsere Berechnungen der Verbindlichkeiten aus dem Versicherungsgeschäft. Die Bildung von Rückstellungen wird bei uns durch eine starke Governance unterstützt, zu der auch umfangreiche interne und externe Überprüfungen gehören.

Kapital anlegen

Unsere Einnahmen beinhalten Erträge aus investierten Prämien, Policengebühren und Einlagen. Unser Geschäftserfolg ist sowohl für diejenigen wichtig, die darauf vertrauen, dass wir Schäden zuverlässig bezahlen, als auch für Anleger, die von uns erwarten, dass wir Erträge auf Sparguthaben erzielen und unser Geschäft verantwortungsbewusst führen.

Schadenmanagement

Um sicherzustellen, dass wir unseren Kunden positive Erfahrungen bieten, schenken wir ihnen über unser NetPromoterSystemProgramm (NPS) konsequent Gehör – nicht nur im Rahmen unseres Schadenabwicklungsprozesses, sondern an allen Kundenschnittstellen.

EinführungWährend anderthalb Jahrhunderten haben wir unser Geschäftsmodell weiterentwickelt, um das Beste aus unseren Ressourcen herauszuholen und einen Mehrwert für alle unsere Anspruchsgruppen zu schaffen. Unsere Mitarbeitenden helfen unseren Privat und Firmenkunden, Risiken zu verstehen und sich vor diesen zu schützen.

Kundenbetreuung und Vertrieb über zahlreiche Kanäle

Durch verlängerte und neue Vertriebsvereinbarungen wird der Pool der erreichbaren Kunden erweitert. Unsere Produkte und Lösungen stehen den Kunden mit einer klaren Ausrichtung auf hervorragenden Kundenservice über zahlreiche Kanäle zur Verfügung: direkt oder indirekt über Makler, über Vorsorgeberater und in Kooperation mit Dritten, einschliesslich Banken, Reiseanbietern, Einzelhändlern, Autovermietern und händlern.

Risiken übernehmen und verwalten

Die Übernahme und das Management von Risiken sind für unsere Geschäftstätigkeit von zentraler Bedeutung. Risiken zu verstehen, zu messen und zu modellieren, hilft uns, den Risiken angemessene Preise zuzuordnen und unseren Kunden, die auch auf unsere Kompetenz zur Risiko minderung setzen, wettbewerbsfähige Prämien anzubieten.

Farmers Group Inc. und Farmers ExchangesFarmers Group, Inc. (FGI) ist eine hundertprozentige Tochtergesellschaft der Gruppe. FGI erbringt als Bevollmächtigte bestimmte, nicht auf die Schadenabwicklung bezogene Dienstleistungen und Nebendienstleistungen für die Farmers Exchanges und erhält hierfür eine Gebühr. Zu diesen Dienstleistungen gehören unter anderem Underwriting, Policenverwaltung, Prämieninkasso, Investment Management sowie Rechnungslegung und Berichterstattung.

Die Zurich Insurance Group hält keine Eigentumsanteile an den Farmers Exchanges, die Eigentum ihrer Versicherungsnehmer sind. Die Farmers Exchanges tragen das versicherungstechnische Risiko und wickeln die Schadensfälle ab. Ausserdem sind sie Eigentümer der Marke Farmers und der Vertriebsressourcen wie beispielsweise Exklusivagenten und direkte Callcenter. Die an FGI gezahlten Gebühren für Dienstleistungen werden als Prozentsatz der verdienten Bruttoprämien berechnet.

Unsere Anspruchsgruppen

Mehr dazuSeiten 21–37

Kunden

Mitarbeitende

Investoren

PlanetGemeinschaften und Gesellschaft

17 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

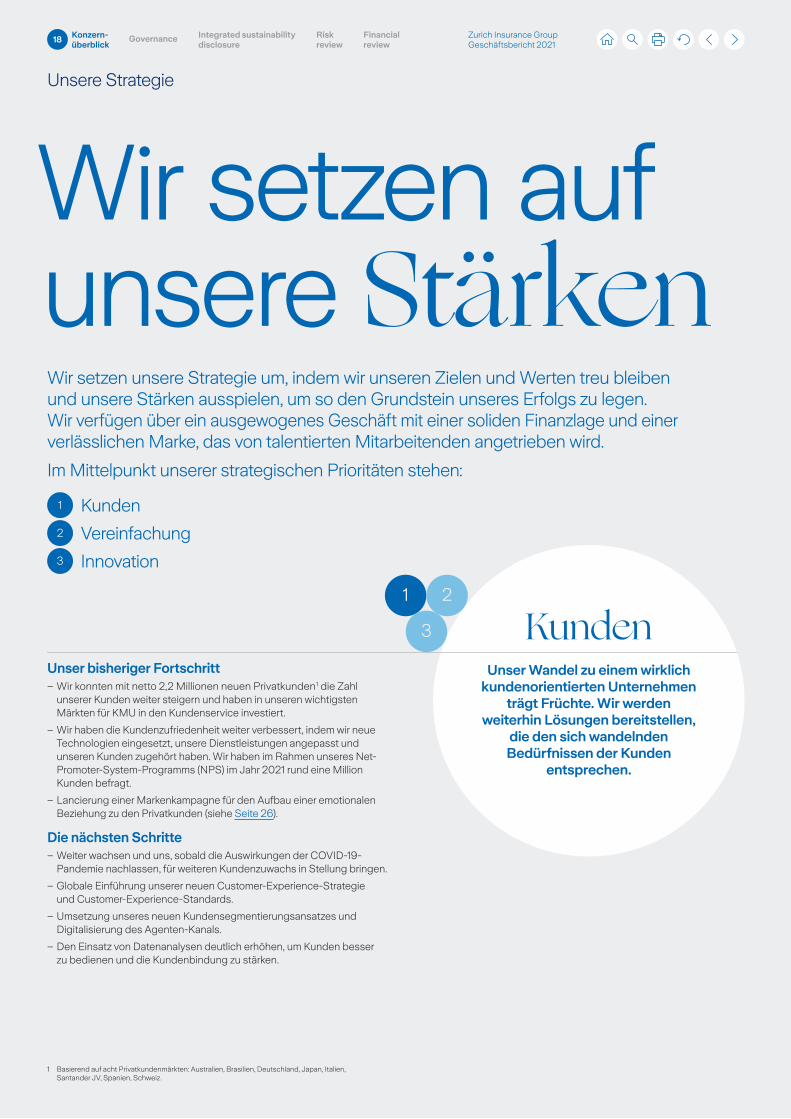

Unsere Strategie

KundenUnser Wandel zu einem wirklich

kundenorientierten Unternehmen trägt Früchte. Wir werden

weiterhin Lösungen bereitstellen, die den sich wandelnden Bedürfnissen der Kunden

entsprechen.

Unser bisheriger Fortschritt – Wir konnten mit netto 2,2 Millionen neuen Privatkunden 1 die Zahl unserer Kunden weiter steigern und haben in unseren wichtigsten Märkten für KMU in den Kundenservice investiert.

– Wir haben die Kundenzufriedenheit weiter verbessert, indem wir neue Technologien eingesetzt, unsere Dienstleistungen angepasst und unseren Kunden zugehört haben. Wir haben im Rahmen unseres NetPromoterSystemProgramms (NPS) im Jahr 2021 rund eine Million Kunden befragt.

– Lancierung einer Markenkampagne für den Aufbau einer emotionalen Beziehung zu den Privatkunden (siehe Seite 26).

Die nächsten Schritte – Weiter wachsen und uns, sobald die Auswirkungen der COVID19Pandemie nachlassen, für weiteren Kundenzuwachs in Stellung bringen.

– Globale Einführung unserer neuen CustomerExperienceStrategie und CustomerExperienceStandards.

– Umsetzung unseres neuen Kundensegmentierungsansatzes und Digitalisierung des AgentenKanals.

– Den Einsatz von Datenanalysen deutlich erhöhen, um Kunden besser zu bedienen und die Kundenbindung zu stärken.

Wir setzen unsere Strategie um, indem wir unseren Zielen und Werten treu bleiben und unsere Stärken ausspielen, um so den Grundstein unseres Erfolgs zu legen. Wir verfügen über ein ausgewogenes Geschäft mit einer soliden Finanzlage und einer verlässlichen Marke, das von talentierten Mitarbeitenden angetrieben wird.

Im Mittelpunkt unserer strategischen Prioritäten stehen:

1 Kunden

2 Vereinfachung

3 Innovation

Wir setzen auf unsere St rken

1 Basierend auf acht Privatkundenmärkten: Australien, Brasilien, Deutschland, Japan, Italien, Santander JV, Spanien, Schweiz.

18 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

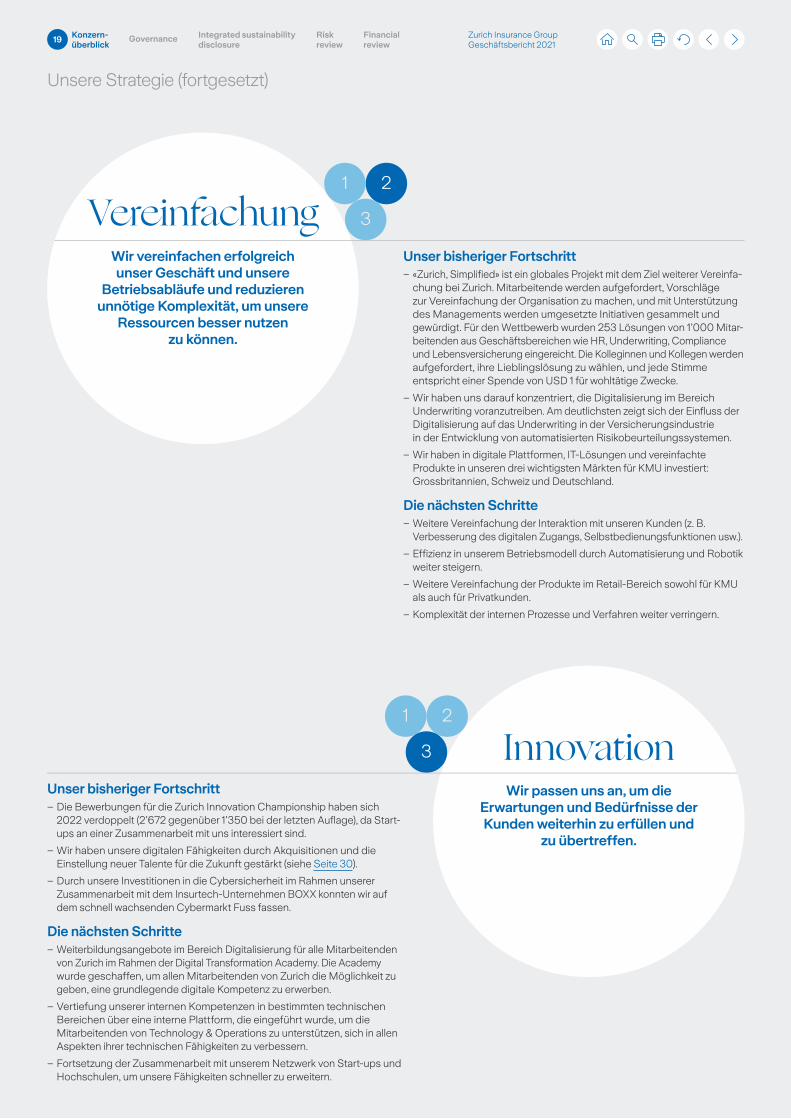

Unsere Strategie (fortgesetzt)

VereinfachungWir vereinfachen erfolgreich unser Geschäft und unsere

Betriebsabläufe und reduzieren unnötige Komplexität, um unsere

Ressourcen besser nutzen zu können.

Unser bisheriger Fortschritt – «Zurich, Simplified» ist ein globales Projekt mit dem Ziel weiterer Vereinfachung bei Zurich. Mitarbeitende werden aufgefordert, Vorschläge zur Vereinfachung der Organisation zu machen, und mit Unterstützung des Managements werden umgesetzte Initia tiven gesammelt und gewürdigt. Für den Wettbewerb wurden 253 Lösungen von 1’000 Mitarbeitenden aus Geschäftsbereichen wie HR, Underwriting, Compliance und Lebensversicherung eingereicht. Die Kolleginnen und Kollegen werden aufgefordert, ihre Lieblingslö sung zu wählen, und jede Stimme entspricht einer Spende von USD 1 für wohltätige Zwecke.

– Wir haben uns darauf konzentriert, die Digitalisierung im Bereich Underwriting voranzutreiben. Am deutlichsten zeigt sich der Einfluss der Digitalisierung auf das Underwriting in der Versicherungsindustrie in der Entwicklung von automatisierten Risikobeurteilungssystemen.

– Wir haben in digitale Plattformen, ITLösungen und vereinfachte Produkte in unseren drei wichtigsten Märkten für KMU investiert: Grossbritannien, Schweiz und Deutschland.

Die nächsten Schritte – Weitere Vereinfachung der Interaktion mit unseren Kunden (z. B. Verbesserung des digitalen Zugangs, Selbstbedienungsfunktionen usw.).

– Effizienz in unserem Betriebsmodell durch Automatisierung und Robotik weiter steigern.

– Weitere Vereinfachung der Produkte im RetailBereich sowohl für KMU als auch für Privatkunden.

– Komplexität der internen Prozesse und Verfahren weiter verringern.

InnovationWir passen uns an, um die

Erwartungen und Bedürfnisse der Kunden weiterhin zu erfüllen und

zu übertreffen.

Unser bisheriger Fortschritt – Die Bewerbungen für die Zurich Innovation Championship haben sich 2022 verdoppelt (2’672 gegenüber 1’350 bei der letzten Auflage), da Startups an einer Zusammenarbeit mit uns interessiert sind.

– Wir haben unsere digitalen Fähigkeiten durch Akquisitionen und die Einstellung neuer Talente für die Zukunft gestärkt (siehe Seite 30).

– Durch unsere Investitionen in die Cybersicherheit im Rahmen unserer Zusammenarbeit mit dem InsurtechUnternehmen BOXX konnten wir auf dem schnell wachsenden Cybermarkt Fuss fassen.

Die nächsten Schritte – Weiterbildungsangebote im Bereich Digitalisierung für alle Mitarbeitenden von Zurich im Rahmen der Digital Transformation Academy. Die Academy wurde geschaffen, um allen Mitarbeitenden von Zurich die Möglichkeit zu geben, eine grundlegende digitale Kompetenz zu erwerben.

– Vertiefung unserer internen Kompetenzen in bestimmten technischen Bereichen über eine interne Plattform, die eingeführt wurde, um die Mitarbeitenden von Technology & Operations zu unterstützen, sich in allen Aspekten ihrer technischen Fähigkeiten zu verbessern.

– Fortsetzung der Zusammenarbeit mit unserem Netzwerk von Startups und Hochschulen, um unsere Fähigkeiten schneller zu erweitern.

19 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Strategie (fortgesetzt)

Unsere Ziele umsetzen…Wir sind ein ausgewogenes und vielfältiges Unternehmen mit einzigartigen Fähigkeiten. Wir nutzen unsere Stärken, um Mehrwert für unsere Anspruchsgruppen zu generieren und unsere Ziele zu erreichen:

Solide FinanzlageDie Bilanz der Gruppe ist nach wie vor sehr stark, was durch die FinanzstärkeRatings AA und Aa3 mit stabiler Prognose von S&P und Moody’s für die Zürich VersicherungsGesellschaft AG bestätigt wird. Durch unsere solide Finanzlage haben unsere Kunden die Gewissheit, dass wir imstande sind, ihre Schadenansprüche jederzeit zu erfüllen, und unsere Aktionäre können darauf vertrauen, dass wir über die notwendige finanzielle Stabilität verfügen. Sie verleiht uns zudem zu Recht eine hohe Reputation als Unternehmen und Arbeitgeber und hilft uns, in zukünftiges Wachstum zu investieren.

Ausgewogenes GeschäftUnser Geschäft ist sowohl geografisch als auch im Hinblick auf die Produkte und Kundensegmente ausgewogen. Dank unseres starken Privat und Firmenkundengeschäfts und unseres flexiblen Betriebsmodells können wir Konjunktur und Marktschwankungen überstehen und Veränderungen in der Branche nutzen.

Wir bleiben unserem Unternehmensziel und unseren Werten treu.Gewinne zu erwirtschaften ist nur ein Teil dessen, was heutzutage ein Unternehmen ausmacht. Unser Ziel ist es, eines der verantwortungsbewusstesten und wirkungsvollsten Unternehmen der Welt zu sein und dadurch positive Ergebnisse für die Menschen und den Planeten zu erzielen. Wir wollen dies durch die Zusammenarbeit mit unseren Mitarbeitenden, Investoren, Kunden und den Gemeinschaften, in denen wir leben und arbeiten, erreichen und so gemeinsam eine bessere Zukunft gestalten.

Verlässliche Marke mit talentierten MitarbeitendenWir verstehen die Risiken unserer Kunden und können unsere Angebote so strukturieren, dass sie deren Bedürfnisse erfüllen. Dies stärkt unsere globale Marke, die es uns zusammen mit unserer guten Reputation ermöglicht, weltweit die besten Talente zu gewinnen.

20 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Anspruchsgruppen

Zurich setzt sich dafür ein, für all ihre Anspruchsgruppen nachhaltigen Mehrwert zu schaffen. Lernen Sie auf den folgenden Seiten unsere Anspruchsgruppen kennen und erfahren Sie, wie sie andere dazu anregen, gemeinsam Massnahmen zu ergreifen – zum Wohle unserer Kunden, Mitarbeitenden, Investoren und unseres Planeten.

21 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Anspruchsgruppen (fortgesetzt)

PlanetZum Handeln anregen

Erfolgreich sein und Gutes tun

Bei Zurich sind wir überzeugt, dass es nicht nur möglich, sondern auch notwendig ist, langfristigen und nachhaltigen Mehrwert zu schaffen, indem wir gut wirtschaften und dabei Gutes tun. Responsible Investment Analyst Danielle Brassel trägt durch ihre Zusammenarbeit mit unseren weltweiten internen Anlageteams und externen Vermögensverwaltern dazu bei, unsere robusten Prinzipien für verantwortungsbewusstes Anlegen zu verankern. Dadurch erzielen wir Ergebnisse, die den Menschen und dem Planeten langfristig zugutekommen.

Danielle Brassel und das Responsible Investment Team ermöglichen es Zurich, drei spezifische Ergebnisse zu erzielen: bis 2050 eine vollständige Dekarbonisierung unseres Anlageportfolios zu erreichen, einen Beitrag zur Vermeidung von 5 Millionen metrischen Tonnen CO2äquivalenter Emissionen pro Jahr zu leisten und durch unsere Impact Investments das Leben von 5 Millionen Menschen jährlich zu verbessern. «Prinzipien für verantwortungsbewusstes Anlegen einzuführen, ist der erste und leichteste Schritt», sagt Danielle Brassel. «Die grössere und wichtigere Herausforderung besteht darin, die positiven Auswirkungen der Kapitalanlagen zu messen.»

Danielle BrasselResponsible Investment Analyst, Zurich Insurance Group

22 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Anspruchsgruppen (fortgesetzt)

PlanetZum Handeln anregen

Ein LichtblickEine neue hochmoderne Solaranlage soll mehr als 70% des Stromverbrauchs unseres Hauptgebäudes auf der Isle of Man decken. Der Zurich Internal Carbon Fund stellte einen Teil der Vorlaufkosten bereit, um das Projekt zu lancieren. Das Projekt soll sich durch Energieeinsparungen im Laufe von zehn Jahren amortisieren. Mit den eingesparten Mitteln werden weitere Nachhaltigkeitsinitiativen vorangetrieben. «Ich liebe meine Tätigkeit und ermutige die Belegschaft, sich ebenfalls zu engagieren», betont Jason Buckley, Facilities Manager auf der Isle of Man. Er hat sich selbst das ehrgeizige persönliche Ziel gesetzt, bis Ende 2022 für den Firmensitz Emissionsfreiheit zu erreichen.

Jason BuckleyFacilities Manager, Zurich Isle of Man

FallstudieGrüne Anlageentscheidungen anregen Zurich führte die branchenweit erste klimaneutrale Anlageoption für die Kunden fondsgebundener Lebensversicherungen ein. Der Zurich Carbon Neutral World Equity Fund investiert in emissionsarme Unternehmen und Spitzenreiter im Bereich saubere Technologien. Die auf den Fonds entfallenden Emissionen belaufen sich nur auf 9 Tonnen CO2 pro investierter USD 1 Million im Vergleich zu 68 Tonnen bei traditionellen Anlagestrategien. Die verbleibenden Emissionen werden von Zurich durch Investitionen im Biodiversitätsreservat Rimba Raya in Indonesien ausge glichen. Der Fonds ist in Deutschland, Italien, Portugal, in der Schweiz und bei Zurich International verfügbar.

–85%Ungefähre Reduzierung des CO2Fussabdruck des Fonds 1 gegenüber traditionellen Investmentstrategien 2.

1 Scope 1+2 Treibhausgasemissionen.2 Basierend auf dem MSCI World Index per 31. Dezember 2021.

23 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Anspruchsgruppen (fortgesetzt)

Q A mit Sierra Signorelli

Wir sehen sowohl neue Risiken als auch neue Chancen.Sierra SignorelliCEO Commercial Insurance, Zurich Insurance Group

Welche Aufgaben bringt diese Position mit sich?Meine Aufgabe ist es, unser globales Firmenkundengeschäft so zu leiten, dass wir unsere strategischen Ziele erreichen. Dazu muss ich mich auf unsere Kunden, unsere Mitarbeitenden und unsere finanzielle Leistung konzentrieren. Mein Ziel ist es, die Kompetenzen sowie die Produkte und Dienstleistungen, mit denen wir unsere Kunden unterstützen, laufend zu erweitern, um das zu schützen, was für sie am wichtigsten ist, und zu vermeiden, dass Schäden ihr Geschäft beeinträchtigen. Ich möchte zudem sicherstellen, dass wir den grossartigen Mitarbeitenden von Commercial Insurance ein Arbeitsumfeld bieten, in dem sie sich entwickeln und erfolgreich sein können. Für unseren Erfolg ist entscheidend, dass wir durch gutes Management unserer Portfolios unsere Rentabilität erhalten, sodass wir langfristig ein beständiger und berechenbarer Partner bleiben.

Warum ist diese Zeit interessant für die Versicherung von Firmenkunden?Wir erleben gerade Veränderungen in vielen Bereichen, und es entwickeln sich neue Risiken und Chancen. Wir bauen unsere Fähigkeiten weiter aus, um bessere Erkenntnisse zu gewinnen und weiterzugeben. So können wir Schäden für unsere Kunden und für Zurich besser vorhersagen und vermeiden, und unsere Kunden zeigen zunehmend Interesse daran, nicht nur Risiken zu versichern, sondern auch Schäden abzuwenden. Es gibt nur sehr wenige Versicherer, die ihre Kunden mit der gleichen globalen Reichweite, Erfahrung und Fachkompetenz unterstützen können, die ihnen ausreichend Sicherheit geben, um heutige Schäden zu vermeiden und zukünftige Chancen zu nutzen. Die nächsten Jahre bieten uns eine einzigartige Möglichkeit, an der Entwicklung von Lösungen für zukünftige Herausforderungen mitzuwirken.

Welche grösseren Erfolge hat Zurichs Commercial Insurance 2021 erzielt?Im Jahr 2021 zahlte sich die harte Arbeit aus, die wir in den letzten Jahren in Zusammenhang mit der Neugewichtung unseres Portfolios geleistet haben, die wichtig ist, um ein beständiger und berechenbarer Partner zu bleiben. Die starke Kundenbindung in unserem bestehenden Geschäft und das Wachstum unseres Portfolios zeigen, dass unsere Kunden mit uns zufrieden sind und wir darüber hinaus in der Lage sind, neue Kunden zu gewinnen. Wir haben auf unseren Stärken aufgebaut und Zurich Resilience Solutions ins Leben gerufen, um unsere Kunden bei der Weiterentwicklung ihrer heutigen und zukünftigen Widerstandsfähigkeit zu unterstützen.

Wenn Sie sich den Markt betrachten, sehen Sie dann Chancen oder Herausforderungen?Chancen natürlich! Wir bauen auf einem sehr starken Fundament langfristiger Beziehungen zu Kunden und Maklern auf. Diese Beziehungen helfen uns, weiterhin zu den richtigen Ergebnissen für unsere Kunden, unsere Maklerpartner und für Zurich zu gelangen. Zudem bietet sich uns die grosse Chance, unsere Präsenz im Mittelstandssegment auszubauen und unsere Dienstleistungen zur Risikoprävention und minderung auszuweiten. Der Markt birgt jedoch auch grosse Herausforderungen wie Naturkatastrophen, soziale Inflation, Cyber und Lieferkettenrisiken. Bei den Naturkatastrophen stellen wir zunehmend fest, dass die Gesellschaft auf solche Ereignisse nicht vorbereitet ist. Diese Herausforderung kann nur durch den gemeinsamen Einsatz von Einzelpersonen, Regierungen und Organisationen bewältigt werden, und Zurich trägt dazu bei, diesen Wandel voranzutreiben.

CEO Commercial Insurance

24 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Anspruchsgruppen (fortgesetzt)

KundenZum Handeln anregen

Träume verwirklichenDie Gründung des österreichischen Startups riskine – ehemaliger Teilnehmer der Zurich Innovation Championship – beruht auf einer einfachen Prämisse: Menschen wollen sich sicher fühlen, gegen Risiken geschützt sein und ihre Träume verwirklichen. Bei diesen Zielen spielen ihre Finanzen eine zentrale Rolle.

«Vielen fehlt ein klarer Überblick über ihre Risiken und finanziellen Bedürfnisse sowie das entsprechende Verständnis. Dies ist jedoch ausschlaggebend, um die geeigneten Finanzprodukte zu finden», betont Ralf Widtmann, Chief Executive Officer von riskine. «Jeder sollte in der Lage sein, fundierte Entscheidungen zu treffen.»

Das Startup analysiert die objektiven Risiken der Kunden, ihre Risikopräferenzen sowie ihre Wünsche und Träume mittels Algorithmus. Die Daten sollen Kunden helfen, sachkundige Finanzentscheidungen zu treffen: von der Bewusstseinsbildung und Beratung bis hin zum Kauf eines Produkts.

Zurich arbeitet seit der zweiten Auflage der Zurich Innovation Championship im Jahr 2020 mit riskine zusammen. Der Wettbewerb fordert Startups dazu auf, kühne Ideen zu präsentieren, die zur Gestaltung der Zukunft der Versicherung beitragen können.

Ralf WidtmannChief Executive Officer, riskine

Durch Corporate Life & Pension, Zurich International, CoverMore, LiveWell und andere, konzentrierte sich Zurich Global Ventures im Jahr 2021 auf die Bedürfnisse der Kunden in den Bereichen Employee Benefits, Reisen, Gesundheit und Wohlbefinden und Cyber.

Jack HowellCEO Zurich Global Ventures

Fallstudie

Innovation durch Zurich Global VenturesZurich Global Ventures ist ein Zusammenschluss unabhängiger Geschäftsbereiche, die Innovationen vorantreiben, um globale Dienstleistungen und Produkte anzubieten, die über die traditionelle Versicherung hinausgehen.

Unter der Leitung von Jack Howell wird die Einheit Zurich ermöglichen, ihren Kunden näherzukommen, indem sie Privatkunden und Unternehmen massgeschneiderte, ansprechende und digitale Erfahrungen bietet. Dies soll die Kunden befähigen, sich besser für die Zukunft zu wappnen.

25 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Anspruchsgruppen (fortgesetzt)

Fallstudie

Was kann gut gehen?Versicherungsgesellschaften konzentrieren sich in der Kundenkommunikation traditionell auf die Frage, was schiefgehen kann. Sie heben die möglichen Unfälle, Risiken und Katastrophen des täglichen Lebens hervor, um auf die Notwendigkeit der Versicherungsdeckung aufmerksam zu machen. Bei Zurich haben wir dieses veraltete Konzept auf den Kopf gestellt. Es ist an der Zeit, dass Versicherungen eine optimistischere Haltung einnehmen und fragen: Was kann gut gehen?

Die Frage: «Was kann gut gehen?» steht im Zentrum unserer ersten globalen Markenkampagne seit sieben Jahren. Wir haben uns mit Klimaaktivisten aus aller Welt, wie dem Fotografen Sebastião Salgado (siehe Seite 1) und der Umweltaktivistin Amy Meek (siehe Seite 5), zusammengetan, um eine äusserst ansprechende SocialMediaKampagne zu entwickeln, die über 150 Millionen Kunden erreicht.

Im Rahmen der Kampagne stellen wir eine emotionale Verbindung zu unseren Kunden her, indem wir Themen aufgreifen, die sie betreffen.

Anlässlich der UNKlimakonferenz (COP26) vermittelten wir diesen Optimismus, indem wir in Glasgow eine Statue für all jene errichteten, die Massnahmen zum Klimaschutz ergreifen. Sie besteht aus sechs Figuren und lädt die Menschen ein, sich einzureihen und sich zum Schutz unseres Planeten zu verpflichten. Stellen Sie sich vor, was gut gehen kann, wenn jeder individuelle Massnahmen ergreift, um den Klimawandel anzugehen.

Die Statue dient jedoch nicht nur als Symbol und Inspiration für Klimamassnahmen, sie stellt auch eine Innovation dar, die zur Bekämpfung der globalen Erwärmung beitragen kann. Das Material für die Statue besteht aus gebundenem Kohlendioxid. Zur Herstellung wurde eine Technologie eingesetzt, die bei der Reduktion der CO2Emissionen eine wichtige Rolle spielen kann.

Unsere Markenkampagne stellt unsere Kunden weiterhin ins Zentrum unseres Handelns; gleichzeitig erfüllt sie unseren Zweck, «gemeinsam eine bessere Zukunft zu gestalten».

Durch den Kontakt zu unseren Kunden können wir bedeutungsvolle Beziehungen aufbauen. Dies zeigt sich an den rekordhohen Zahlen der akquirierten Privatkunden. Allein im Jahr 2021 gewannen wir netto 2,2 Millionen neue Privatkunden 1.

Und alles beginnt mit der optimistischen Frage: Was kann gut gehen?

Es ist an der Zeit, unseren Blickwinkel zu ändern.Conny KalcherGroup Chief Customer Officer, Zurich Insurance Group

1 Basierend auf acht Privatkundenmärkten: Australien, Brasilien, Deutschland, Japan, Italien, Santander JV, Spanien, Schweiz.

26 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Anspruchsgruppen (fortgesetzt)

Zum Handeln anregen MitarbeitendeZum Handeln anregen

Wenn es etwas gibt, das Samantha Chow während ihrer Tätigkeit bei Brand Marketing and Communications, Zurich Malaysia, gelernt hat, dann, dass Taten mehr sagen als Worte.

«Es bringt nichts, über etwas nur zu sprechen», sagt Samantha. «Man muss bereit sein, sich die Hände schmutzig zu machen. Menschen inspiriert man am besten zum Handeln, indem man es selbst tut und mit gutem Beispiel vorangeht.»

Seit ihrem Eintritt in das Unternehmen im Jahr 2020 beschäftigt sie sich mit Kampagnen in den Bereichen Klima, Nachhaltigkeit und Wohlbefinden. Sie schätzt das Engagement von Zurich, eine Kultur zu fördern, in der die Mitarbeitenden ermutigt werden, sowohl am Arbeitsplatz als auch in der Gemeinschaft etwas zu bewirken. Für das Jahr 2022 haben wir uns zum Ziel gesetzt, dass unsere Mitarbeitenden insgesamt 150’000 Stunden ehrenamtliche Arbeit leisten.

Was Samantha wirklich Hoffnung gibt, ist das Potenzial jedes Einzelnen, etwas zu bewirken.

«Manchmal haben wir vielleicht das Gefühl, dass unsere Bemühungen nichts bewirken, aber wenn alle dasselbe denken, dann wird auch nichts geschehen. Es gibt Menschen, die im Alleingang einen ganzen Wald gepflanzt haben. Wenn diese gedacht hätten, dass sie als einzelne Person ohnehin nichts bewirken könnten und nicht den ersten Baum gepflanzt hätten, gäbe es keinen Wald.»

Wenn Samantha selber Zuspruch braucht, weiss sie genau, an wen sie sich wenden kann. «Mein Vater ist das beste Beispiel für Widerstandsfähigkeit, Bescheidenheit und Intelligenz und die erste Person, die ich anrufe, wenn ich bei wichtigen Entscheidungen Hilfe brauche.»

Samantha ChowBrand Marketing and Communications, Zurich Malaysia

Mit gutem Beispiel vorangehen.

27 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Anspruchsgruppen (fortgesetzt)

PlanetZum Handeln anregen

Wir alle können etwas bewirken«Jeder Einzelne von uns kann etwas bewirken, jeden Tag, an dem wir leben.» So lautete die Botschaft der Hoffnung und der Ermächtigung der britischen Primatenforscherin und Umweltschützerin Dr. Jane Goodall in der ersten Runde der Gesprächsreihe ZTalks by Zurich, bei der die Bekämpfung des Klimawandels im Mittelpunkt stand.

Die am globalen Hauptsitz von Zurich stattfindende Gesprächsreihe ZTalks by Zurich besteht aus vier LiveEvents. Zu diesen Veranstaltungen kommen Vordenker, Akademiker, Aktivisten, Nichtregierungsorganisationen (NGOs) und Führungskräfte von Unternehmen zusammen, um die dringendsten aktuellen Themen zu erörtern. Dabei geht es unter anderem um den Klimawandel, die psychische Gesundheit und die digitale Transformation (siehe Foto auf Seite 29). Die Gesprächsreihe unterstreicht das Ziel von Zurich, eines der verantwortungsbewusstesten und wirkungsvollsten Unternehmen der Welt zu sein.

Jane Goodall, PhD, DBE Gründerin des Jane Goodall Institute und UNFriedensbotschafterin

Fallstudie

Ein kleiner Pieks mit grosser WirkungEs ist wahrscheinlich das coolste Impfzentrum der Stadt und befindet sich an unserem neuen globalen Hauptsitz, dem Quai Zurich Campus. Das eher an eine Flughafenlounge als an eine Klinik erinnernde Impfzentrum steht den Mitarbeitenden sowie ihren Familien und Freunden und unseren Lieferanten zur Verfügung.

«Es geht darum, die Gemeinschaft zu unterstützen», betont Yves K. Leuenberger, Head of Group Property & Innovation bei Zurich. «Da die Wirksamkeit der Impfprogramme von der Höhe der Beteiligung abhängt, kann mit einem kleinen Schritt eine grosse Wirkung erzielt werden.»

Es ist eines von mehreren Impfzentren, die Zurich 2021 in verschiedenen Ländern Asiens, Europas und Amerikas für Mitarbeitende einrichtete, um die staatlichen Kampagnen zur Beschleunigung der COVID19Impfung zu

unterstützen. Das Zentrum, das Mitarbeitenden des Corporate Centers kostenlosen und leich ten Zugang zu Impfstoffen gewähren soll, bietet neben den COVID19 und BoosterImpfungen auch Grippeimpfungen an. Die Dienstleistung kann mit und ohne Terminvereinbarung in Anspruch genommen werden.

Es wurde bewusst die Atmosphäre einer BusinessLounge geschaffen. Mitarbeitende können einen Snack einnehmen, sich impfen lassen, bequem auf den Checkup eines Arztes warten und dann an den Arbeitsplatz zurückkehren.

«Wir wollen unseren Beitrag zum Kampf gegen COVID19 leisten», sagt Yves Leuenberger. «Wir verfügen über die Einrichtungen sowie die Mittel zur Einstellung medizinischer Fachkräfte und wir können die von den öffentlichen Behörden bereitgestellten Dienste ergänzen.»

Vom 14. September 2021 bis 31. Januar 2022 haben mehr als 1’000 Personen das Impfzentrum in Anspruch genommen.

28 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Anspruchsgruppen (fortgesetzt)

Wir alle können etwas bewirken

Fallstudie

Zurich und BASF: eine langfristige und nachhaltige Beziehung Der deutsche Chemieriese BASF ist seit den 1980erJahren ein Kunde von Zurich. Die Beziehung wurde in den letzten Jahren noch vertieft, da das Chemieunternehmen den Übergang zur Nachhaltigkeit eingeleitet hat.

«Das Wichtigste für mich ist die Zuverlässigkeit. Wir brauchen einen zuverlässigen Partner für diesen Transformationsprozess», so Patrick Fiedler, Senior Vice President bei BASF. «Man braucht einen Versicherer, der die branchenspezifischen Herausforderungen versteht, an den Herausforderungen interessiert ist und bereit ist, zu helfen und Teil der Lösung zu sein.»

Zurich setzt sich im Rahmen der Zusammenarbeit mit ihren Kunden dafür ein, sie beim Übergang zu NettoNullEmissionen und bei der Anpassung ihrer Geschäftsmodelle für eine nachhaltigere Zukunft zu unterstützen. Wie Zurich hat sich auch BASF verpflichtet, im Einklang mit den Zielen des Pariser Klimaschutzabkommens bis 2050 ein Unternehmen mit NettoNullEmissionen zu werden.

Zurich hilft den Kunden, die physischen Risiken infolge des Klimawandels zu verstehen, und bietet Beratung zur Risikominderung und prävention. Dies erfolgt zum Beispiel über die im Jahr 2020 gegründete Einheit Zurich Climate Change Resilience Services.

«Aufgrund des Klimawandels besteht nun ein höheres Risiko für Überschwemmungen, schwere Regenfälle und so weiter», bemerkt Patrick Fiedler, der zusammen mit seinem weltweiten Team von rund 40 Kollegen alle versicherbaren Risiken bei BASF bewirtschaftet. «Zurich hilft BASF, die erhöhten Risiken zu erkennen und die richtigen Massnahmen zur Minderung des Risikos zu identifizieren.»

Aber selbst bei Geschäftsbeziehungen zwischen Grossunternehmen kommt es laut Patrick Fiedler im Grunde genommen auf die Menschen, das Verständnis und das Vertrauen an.

«Es geht um einzelne Menschen sowie ihre Bereitschaft, zu verstehen und zu helfen», sagt er. «Auch in dieser Hinsicht leistet Zurich meines Erachtens wirklich gute Arbeit.»

Kurz gesagt, ist es eine nachhaltige Beziehung.

Patrick Fiedler nahm am ersten LiveEvent der Gesprächsreihe ZTalks by Zurich unter dem Titel «Future Planet» teil (siehe Abbildung unten).

Die Folge können Sie hier abrufen:www.zurich.com/en/ztalksbyzurich

Man braucht einen Versicherer, der die branchenspezifischen Herausforderungen versteht.Patrick FiedlerSenior Vice President, BASF

29 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Anspruchsgruppen (fortgesetzt)

Fallstudie

Unsere digitalen Fähigkeiten stärken Technologie ist in vielen Branchen ein wichtiger Differenzierungsfaktor, so auch im Versicherungswesen. Die COVID19Pandemie hat die Digitalisierung und die Einführung neuer Technologien beschleunigt und damit den Bedarf an erstklassigen Lösungen in den Bereichen Cybersicherheit und Datenverwaltung erhöht. Zurich stärkt ihre digitalen Fähigkeiten, um Kunden beim Umgang mit diesen komplexen Risiken zu helfen, unnötige Komplexität zu reduzieren und personalisierte Produkte zu entwickeln, die die technisch versierten Kunden von heute wollen und brauchen.

Mit Computern sprechenIm Jahr 2021 übernahm Zurich das in Estland ansässige Unternehmen AlphaChat, eines der fortschrittlichsten Startups im Bereich dialogfähiger künstlicher Intelligenz (KI), mit einem Team aus erfahrenen Unternehmern und Spezialisten für maschinelles Lernen. Durch die Übernahme kann Zurich die steigende Nachfrage ihrer Kundinnen und Kunden nach perso nalisierten und jederzeit verfügbaren Produkten und Dienstleistungen abdecken. Insbesondere soll dadurch ein einheitlicher und effizienter Ansatz für die Entwicklung intelligenter virtueller Assistenten in allen Ge schäftsbereichen sichergestellt werden – sowohl für interne als auch für externe Zwecke.

Tech TalentZurich hat ihre digitale Transformation mit der Einführung von zwei neuen Funktionen im Jahr 2021 weiter gestärkt. Peter Kasahara wurde zum Group Chief Data Officer ernannt. In dieser Position ist er für alle Aspekte des Datenmanagements zuständig und bringt Zurich ihrem Ziel, ein führendes Unternehmen im verantwortungsvollen Umgang mit Daten zu werden, einen Schritt näher. In seiner Funktion als Group Chief Platform Officer konzentriert sich Frank Verkerk darauf, in enger Zusammenarbeit mit Zurich Global Ventures (siehe Fallstudie auf Seite 25) die Entwicklung digitaler und modularer Dienstleistungen voranzutreiben, um die sich rasant verändernden Bedürfnisse der Kunden abzudecken.

CybersicherheitDie zunehmende Einführung digitaler Geschäftsmodelle und der Einsatz von Technologie in unserem Alltag haben Vorteile gebracht – aber auch neue Risiken. Cyberrisiken nehmen zu und können zu Cyberattacken, Betriebsunterbrechungen, Umsatzverlusten und regulatorischen Datenschutzmassnahmen führen. Im Jahr 2021 gab Zurich eine globale Zusammenarbeit mit dem InsurtechUnternehmen BOXX Insurance mit Sitz in Toronto bekannt, das vollständig integrierte Cybersecurity und Versicherungslösungen für kleine bis mittlere Unternehmen, Konsumenten und Familien anbietet. Durch die Zusammenarbeit und den auf Prävention aus gerichteten Ansatz von BOXX kann Zurich ihr Ziel erreichen, Vertrauen in eine digitale Gesellschaft zu schaffen und gleichzeitig die schnell wachsende Nachfrage nach Cybersicherheitslösungen zu befriedigen.

Schutz abseits von RichtlinienZurich Resilience Solutions (siehe Fallstudie auf Seite 35) wurde 2021 gegründet und bietet Dienstleistungen an, die Firmenkunden beim Umgang mit einem der schwierigsten Risiken für ein modernes Unternehmen unterstützen: Cyberrisiken. Zurich Cyber Security Services bietet neben Versicherungspolicen auch Dienstleistungen in den Bereichen Cyber Risk Engineering und Beratung sowie, zusammen mit dem CybersecurityUnternehmen CYE, eine Lösung zur kontinuierlichen Bewertung der Cybersicherheit. Zurich Cyber Security Services hilft Kunden, CyberBedrohungen einen Schritt voraus zu sein, indem sie unbekannte Sicherheitslücken schliesst und proaktiven Schutz für kritische Unternehmensanlagen gewährleistet.

Die Bedürfnisse der Kunden entwickeln sich rasant weiter.Frank VerkerkGroup Chief Platform Officer, Zurich Insurance Group

Wir legen grossen Wert auf Transparenz.Peter KasaharaGroup Chief Data Officer, Zurich Insurance Group

30 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Unsere Anspruchsgruppen (fortgesetzt)

Q A mit Ericson ChanWas motiviert Sie morgens beim Aufstehen?Als Ingenieur aus Leidenschaft begeistert mich die Zusammenarbeit mit Gleichgesinnten, um neue, digitale Lösungen zu finden und dadurch das Angebot für unsere Kunden zu verbessern. Die schnelle Weiterentwicklung von Technologien und Daten gibt uns noch mehr Möglichkeiten, kreativ auf die Bedürfnisse und Erwartungen der Kunden zu reagieren.

Was hat Sie im Jahr 2021 besonders stolz gemacht?Aussergewöhnliche Produkte und Dienstleistungen fangen mit aussergewöhnlichen Teams an. Wir haben unser grossartiges Team weiter verstärkt mit zwei erfahrenen Experten in leitenden Funktionen (siehe Seite 30).

Mithilfe unserer neu eingerichteten Digital Academy haben wir zudem unsere Mitarbeitenden durch 15’000 Stunden Lernen und durch Zertifizierungen weitergebildet, damit sie auf dem neuesten Wissenstand bleiben. Und wir haben mehr als 100 neue Technologieexperten eingestellt und marktführende Startups wie AlphaChat ins Boot geholt, um künstliche Intelligenz mit modernen Konversationsfähigkeiten zu nutzen.

Wie fördern Sie eine Start-up-Mentalität bei Zurich?Wir fühlen uns bereits wohl in der Zusammenarbeit mit Startups, und die dritte und beliebteste Auflage unserer Zurich Innovation Championship ist in vollem Gang. Startups sind bestrebt, kundenorientierte Produkte und Dienstleistungen bereitzustellen, und ich möchte, dass unsere Mitarbeitenden mit der gleichen Energie arbeiten.

Wir ermutigen Kolleginnen und Kollegen auf der ganzen Welt, ihre digitalen Lösungen und deren Vorteile für Kunden in unserer internen Digital League vorzustellen. Unabhängig von der Funktion können alle Mitarbeitenden innovative, skalierbare Kundenlösungen präsentieren, die einen echten Nutzen und Mehrwert bieten. Es ist sehr wichtig, agil zu bleiben, den Markttrends voraus zu sein und schnell zu handeln.

Wie wichtig sind Daten und Digitalisierung für das Kundenerlebnis?In den letzten zwei Jahren, als die «Boomer» zu «Zoomern» wurden, haben sich das Verhalten und die Erwartungen der Kunden verändert. Wir müssen die Bedürfnisse der Kunden vorhersehen und innovative und höchst personalisierte Lösungen anbieten. Zu diesem Zweck binden wir Digitalisierung, Daten und Plattformen in all unsere Aktivitäten ein, damit unsere Leistungen durch digitale Automatisierung nahtlos bereitstehen, durch Dateneinblicke bedürfnisorientiert sind und den Kunden durch offene Plattformen zur richtigen Zeit am richtigen Ort angeboten werden.

Was ist das nächste grosse Ding, das Sie im Bereich der Versicherungstechnologie erwarten? Bedeutungsvollere, natürlichere und regelmässigere Interaktionen mit unseren Kunden anstelle des üblichen Austauschs einmal im Jahr. Mit den neuesten Technologien – künstliche Intelligenz, Blockchain, Cloud und Big Data – können wir ein neues Geschäftsmodell schaffen, um überzeugende digitale Leistungen im richtigen Mass bereitzustellen. Das bedeutet, dass wir neben dem Verkauf einer Police zur finanziellen Absicherung an erster Stelle auch wertsteigernde Leistungen anbieten, wie den ganzheitlichen WellbeingService von LiveWell und die Risk Advisor App von Zurich für unsere Firmenkunden.

Es ist wichtig, dass wir die Bedürfnisse der Kunden vorhersehen, um überzeugende und personalisierte Lösungen anbieten zu können.Ericson Chan Group Chief Information and Digital Officer,Zurich Insurance Group

Group Chief Information and Digital Officer

31 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Zum Handeln anregen

150jähriges Jubil umAuf dem Quai Zurich Campus, unserem neuen globalen Hauptsitz am Zürichsee in der Schweiz, treffen öffentliche und private Räume zusammen. Mitarbeitende, Ortsansässige und Besucher der Schweizer Stadt können die idyllischen Innenhöfe des Campus geniessen oder sich bei einem Kaffee im Quai Café entspannen, das von der Züricher Innenarchitektin Iria Degen (Bild) entworfen wurde. Unsere engen und langjährigen Beziehungen zur lokalen Gemeinschaft werden in unserem EBook «Quai Zurich Campus – in good company» beleuchtet, das anlässlich der Eröffnung des Campus im Jahr 2021 veröffentlicht wurde und auf unserer Website erhältlich ist. Unsere Pläne für die Feier des diesjährigen 150Jahre Jubiläums in Zürich stehen ebenfalls im Zeichen der Gemeinschaft und beinhalten die Ausstellung Amazônia (siehe Seiten 14 und 34).

Iria Degen Gründerin Iria Degen Interiors

Unsere Anspruchsgruppen (fortgesetzt)

32 Zurich Insurance Group Geschäftsbericht 2021

Konzern-überblick

Integrated sustainability disclosure

Governance Risk review

Financial review

Fallstudie