Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos Primary Credit Analyst: Isabel Plaza, Madrid (34) 91-7887203; [email protected] Secondary Contact: Virginie Couchet, London (44) 20-7176-3897; [email protected] Table Of Contents €1 Billion Floating-Rate Notes Transaction Summary Notable Features Strengths, Concerns, And Mitigating Factors Transaction Structure Collateral Description Priority Of Payments Credit Analysis Cash Flow Analysis Scenario Analysis Surveillance Related Criteria And Research September 15, 2010 www.standardandpoors.com/ratingsdirect 1 820429 | 300131137

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Presale:

GC FTPYME Sabadell 8 Fondo deTitulización de ActivosPrimary Credit Analyst:Isabel Plaza, Madrid (34) 91-7887203; [email protected]

Secondary Contact:Virginie Couchet, London (44) 20-7176-3897; [email protected]

Table Of Contents

€1 Billion Floating-Rate Notes

Transaction Summary

Notable Features

Strengths, Concerns, And Mitigating Factors

Transaction Structure

Collateral Description

Priority Of Payments

Credit Analysis

Cash Flow Analysis

Scenario Analysis

Surveillance

Related Criteria And Research

September 15, 2010

www.standardandpoors.com/ratingsdirect 1

820429 | 300131137

Presale:

GC FTPYME Sabadell 8 Fondo de Titulizaciónde Activos

€1 Billion Floating-Rate Notes

This presale report is based on information as of Sept. 15, 2010. The ratings shown are preliminary. This report does not constitute a recommendation to buy, hold, or

sell securities. Subsequent information may result in the assignment of final ratings that differ from the preliminary ratings.

Class Prelim rating*Prelim amount (mil.

€)Available credit support

(%) Interest Legal final maturity

A1(G)¶ AAA (sf) 250 29 Three-month EURIBOR plus 130bps

January 2045

A2(G)¶ AAA (sf) 390 29 Three-month EURIBOR plus 135bps

January 2045

A3 AAA (sf) 160 29 Three-month EURIBOR plus 140bps

January 2045

B BB (sf) 200 9 Three-month EURIBOR plus 150bps

January 2045

Cash reserve — 90 — — —

*The rating on each class of securities is preliminary as of Sept. 15, 2010, and subject to change at any time. Initial credit ratings are expected to be assigned on the

closing date subject to a satisfactory review of the transaction documents and legal opinions. Standard & Poor's ratings address timely interest and ultimate principal.

¶The Kingdom of Spain will act as guarantor for the class A1(G) and A2(G) notes. The stand-alone preliminary ratings on the class A1(G) and A2(G) notes are 'AAA (sf)'.

EURIBOR—European interbank offered rate.

Transaction Participants

Originator Banco de Sabadell, S.A.

Trustee Gesticaixa S.G.F.T., S.A.

Arrangers Banco de Sabadell, S.A.

Servicer Banco de Sabadell, S.A.

Interest swap counterparty Banco de Sabadell, S.A.

Bank account provider Banco de Sabadell, S.A.

Paying agent Banco de Sabadell, S.A.

Underwriters Banco de Sabadell, S.A. and West LB AG

Subordinated loan provider Banco de Sabadell, S.A.

Supporting Ratings

Institution/role Ratings

Banco de Sabadell, S.A. as bank account provider, interest swap counterparty, servicer, and paying agent A/Negative/A-1

Transaction Key Features*

Closing date September 2010

Collateral Loans granted to Spanish SMEs and self-employed borrowers

Principal outstanding (€) 1,114,071,586.52

Country of origination Spain

Standard & Poor’s | RatingsDirect on the Global Credit Portal | September 15, 2010 2

820429 | 300131137

Transaction Key Features* (cont.)

Concentration Largest 10 obligors (8.08% of preliminary pool and 9.00% over the issue amount). Regional concentration: Catalonia(48.48%), Madrid (15.24%), Valencia (6.16%), Andalucía (5.5%), and Asturias (4.87%). Industrial concentration: Real

estate (22.36%) and construction (11.48%)

Average current loan size balance(€)

289,745.54

Weighted-average interest rate(%)

3.50

Arrears At closing, a maximum of 1% of loans in arrears for less than 66 days and an additional maximum of 5% of loans inarrears for less than 30 days

Redemption profile Amortizing (98.36%) and bullet (1.64%)

Cash reserve (%) 9.00

*Preliminary pool data as of Aug. 30, 2010. SME—Small and midsize enterprise.

Transaction Summary

Standard & Poor's Ratings Services has assigned preliminary credit ratings to the asset-backed floating-rate notes to

be issued by GC FTPYME Sabadell 8, Fondo de Titulización de Activos (GC FTPYME Sabadell 8).

The originator is Banco de Sabadell S.A. (Banco Sabadell), which at closing will sell to GC FTPYME Sabadell 8 a €1

billion closed portfolio of secured and unsecured loans granted to Spanish small and midsize enterprises (SMEs) and

self-employed borrowers based in Spain.

To fund this purchase, Gesticaixa S.G.F.T., S.A., the trustee, will issue four classes of floating-rate, quarterly paying

notes, on the issuer's behalf.

The class A1(G) and A2(G) notes will benefit from an irrevocable and unconditional guarantee for principal and

interest payments from the Kingdom of Spain (AA/Negative/A-1+).On receipt of a notice of a shortfall in the

available funds to meet either the interest or principal repayment obligations, or both, the Spanish Treasury must

cover the shortfall at the relevant payment date. The guarantee was implemented under the annual FTPYME

program administered by the Spanish Treasury. The stand-alone preliminary ratings on the class A1(G) and A2(G)

notes are 'AAA (sf)'.

The preliminary ratings on GC FTPYME Sabadell 8's notes reflect the subordination of the respective classes of

notes below them, the reserve fund, the presence of the interest rate swap (which provides excess spread of 60 bps),

and comfort provided by various other contracts.

Banco Sabadell will act as bank account provider, servicer, swap counterparty, and paying agent.

Our preliminary ratings reflect our analysis of the ability of the servicer, Banco Sabadell, to fulfill its role in the

transaction, and the cash flow mechanics of the transaction assuming various stress scenarios.

This report includes a scenario analysis for the transaction designed to show the likely impact of changes to a

number of collateral performance drivers on our cash flow analysis and ratings (see "Scenario Analysis" below).

This is part of a broad series of measures that we announced in 2008 to enhance our analytics and dissemination of

information (see "A Listing Of S&P's New Actions Aimed At Strengthening The Ratings Process," published on

Feb. 7, 2008).

www.standardandpoors.com/ratingsdirect 3

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

Notable Features

This transaction will be Banco Sabadell's 14th public SME securitization in Spain. The transaction follows a similar

structure to the previous transactions, the main difference being the split between the series A notes and the way

they amortize. Banco Sabadell's objective is to create ECB (European Central Bank)-eligible assets, increasing the

bank's liquidity cushion, and it intends to sell class A1(G) and A2(G) notes to investors.

The series A notes are divided into three sub-tranches: The class A1(G), A2(G), and A3 notes. Class A2(G) features a

lockout period from closing, lasting 18 months before it starts amortizing.

As in other Spanish transactions, interest and principal from the underlying assets are combined into a single priority

of payments, with cumulative default triggers and asset-liability test triggers in the payment of the interest, to protect

senior noteholders.

Strengths, Concerns, And Mitigating Factors

Strengths

• Banco Sabadell is an experienced originator and servicer, with 14 SME transactions.

• In our view, credit enhancement adequately covers the various stresses we applied to the transaction. Credit

enhancement comprises subordination, the available excess spread, the rating on the servicer, and the

subordinated loan that will fully fund the reserve fund on the closing date.

• Of the preliminary pool, 50.68% represents mortgage loans which carry a higher level of recoveries than

unsecured loans.

• The swap structure provides support to the rated notes. We have given credit for this in our cash flow analysis

(see "Interest swap agreement").

Concerns and mitigating factors

• There is borrower concentration risk, as the top 10 borrowers represent 8.08% of the preliminary pool and the

biggest borrower represents 1.35% of the amount to be issued. We took borrower concentrations into account in

our credit analysis when stressing the default rates at each rating level.

• A percentage of the loans have a higher level of risk due to their amortization profile: 1.64% of the loans in the

securitized pool follow a bullet amortization profile. Borrowers on this type of loan repay principal due in one

lump sum at maturity. We took into account loan amortization profiles in our credit and cash flow analysis.

• There is one interest deferral trigger that is more protective toward senior noteholders than subordinated

noteholders in cases of poor transaction performance. This feature is seen in the priorities of payments that

combine interest and principal. Hitting an interest deferral trigger would lead to the issuer using interest from the

junior notes to repay the most senior notes. This interest deferral trigger structure is typical in Spanish

securitization transactions and we size credit enhancement accordingly for the junior notes (see "Priority Of

Payments").

• The reserve fund can start amortizing after three years if it reaches 18% of the outstanding balance of the class

A1(G), A2(G), A3, and B notes, subject to a floor of half of its initial value, certain conditions need to be met to

amortize the reserve fund (see "Reserve fund").

Standard & Poor’s | RatingsDirect on the Global Credit Portal | September 15, 2010 4

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

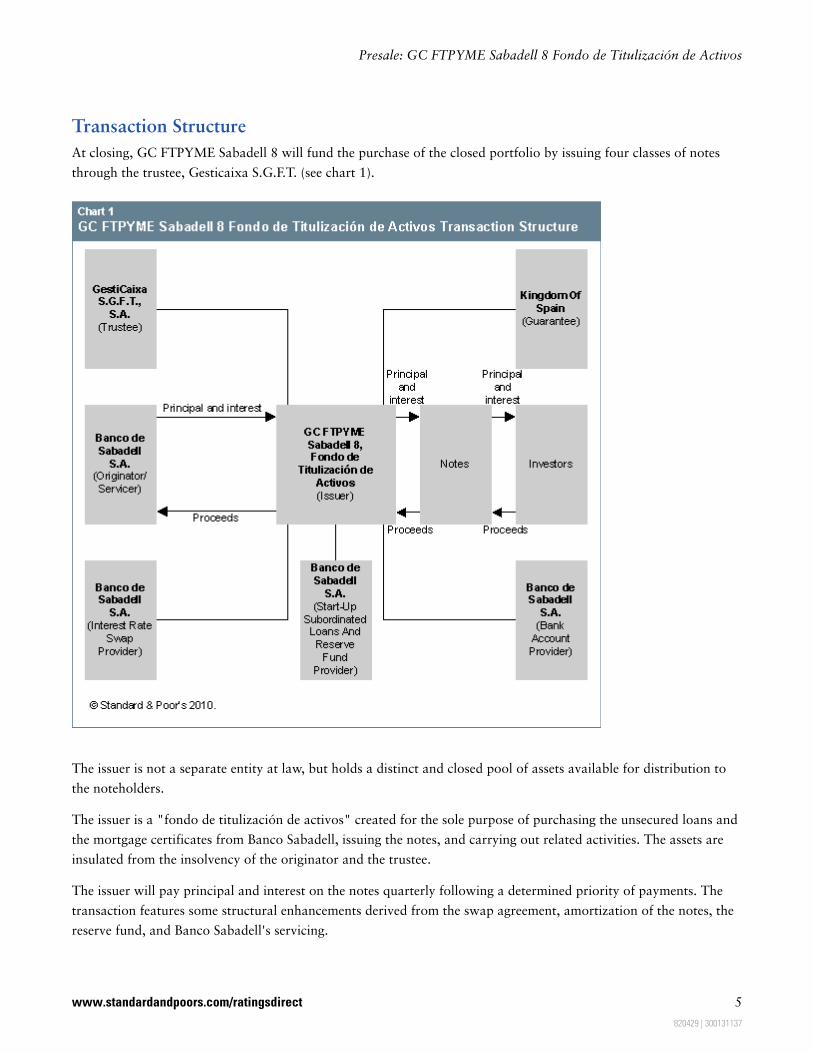

Transaction Structure

At closing, GC FTPYME Sabadell 8 will fund the purchase of the closed portfolio by issuing four classes of notes

through the trustee, Gesticaixa S.G.F.T. (see chart 1).

The issuer is not a separate entity at law, but holds a distinct and closed pool of assets available for distribution to

the noteholders.

The issuer is a "fondo de titulización de activos" created for the sole purpose of purchasing the unsecured loans and

the mortgage certificates from Banco Sabadell, issuing the notes, and carrying out related activities. The assets are

insulated from the insolvency of the originator and the trustee.

The issuer will pay principal and interest on the notes quarterly following a determined priority of payments. The

transaction features some structural enhancements derived from the swap agreement, amortization of the notes, the

reserve fund, and Banco Sabadell's servicing.

www.standardandpoors.com/ratingsdirect 5

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

As in other Spanish transactions, interest and principal from the underlying assets will be combined into a single

priority of payments. A cumulative default ratio test (defaults are defined as loans in arrears for more than 12

months) will protect senior noteholders by subordinating the payment of junior interest further down the priority of

payments.

Collateral Description

As of Aug. 30, 2010, the preliminary pool comprised 3,845 secured and unsecured loans, and the total number of

borrowers was3,643. The preliminary pool was originated between March 1999 and February 2010, and the

weighted-average seasoning was 19.8 months.

The largest obligor represents 1.21% of the preliminary pool and 1.35% of the final amount to be issued. The

largest 10 obligors represent 8.08% of the preliminary pool and 9.00% of the final amount to be issued.

Loans in the preliminary pool can follow three different amortization profiles. 87.29% of the loans follow a normal

amortizing schedule, while a further 11.07% have an initial grace period where only interest will be paid. The

remaining 1.64% of the pool are loans with a bullet amortization schedule, where the entire principal is paid at

maturity.

The weighted-average remaining life of the preliminary pool is 93 months. With a weighted-average seasoning of

19.8 months, 77.54% of the loans were originated more than 12 months ago (see chart 2).

Chart 2

The preliminary pool is exposed to different Spanish regions (see chart 3).

Standard & Poor’s | RatingsDirect on the Global Credit Portal | September 15, 2010 6

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

Chart 3

The largest industry concentration is real estate, which represents 22.36% of the preliminary pool. The

second-highest concentration is construction (11.48%), followed by wholesale trade, except of motor vehicles and

motorcycles (9.07%).

Of the outstanding amount of the preliminary pool, 50.68% is secured by mortgages over properties, commercial

premises, land, etc., in Spain. The average loan-to-value (LTV) ratio of these loans is 44.47%.

Of the preliminary pool, 84.35% is indexed to floating rates. The weighted-average interest of the preliminary pool

is 3.50% and 78.69% of the loans pay monthly installments.

Table 1 shows the distribution of the preliminary pool by size of company and by type of collateral.

Table 1

Preliminary Pool Distribution

Distribution between type of security

Turnover Secured (%) Unsecured (%) % of outstanding portfolio

Self-employed 5.13 4.18 4.66

€<300,000 32.81 12.37 22.73

€300,000 to €900,000 17.30 9.01 13.21

€900,000 to €6 million 28.62 26.06 27.36

€6 million to €30 million 12.40 24.82 18.52

€30 million to €100 million 3.74 23.56 13.51

www.standardandpoors.com/ratingsdirect 7

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

Cash-collection arrangements

Banco Sabadell, as servicer, will collect the amounts due under the loans and transfer them daily to the issuer

account held at Banco Sabadell.

The minimum rating required to be the bank account provider is 'A-1', so if Banco Sabadell is downgraded below

'A-1', it should take remedy actions following our "Revised Framework For Applying Counterparty And Supporting

Party Criteria" (see "Related Criteria And Research").

Commingling reserve

To protect against commingling risk, if Banco Sabadell is downgraded below a short-term rating of 'A-2', then:

• Within 30 calendar days, the servicer should find an eligible guarantor with at least a short-term rating of 'A-1'.

The guarantor should provide the issuer with a first-demand, unconditional, and irrevocable guarantee equal to

the commingling reserve amount to be applied to pay any amounts the servicer fails to pay to the issuer for the

loans. This amount, if required to be paid, would be deposited in an issuer bank account in accordance with the

bank account and cash management agreements. We would expect to review the guarantee at the time the

downgrade occurs; or

• Within 10 calendar days, the servicer should deposit in the issuer's bank account an amount equal to the

commingling reserve amount to be applied to pay any amounts the servicer fails to pay the issuer for the loans.

Alternatively, we encourage the servicer to request our written confirmation that the ratings on the notes would not

be adversely affected.

On the date this commingling reserve is required, the initial amount should be a sufficient proportion of the

principal amount outstanding to avoid affecting the ratings on the notes.

Cash reserve

The structure will benefit from a cash reserve fund. On the closing date, a subordinated loan will fully fund the

reserve fund, which will be fixed for the first three years and which the issuer will use on each payment date to pay

the different items of the priority of payments described below.

The reserve fund required on each payment date is the minimum of:

• 9% of the original total balance of classes A1(G), A2(G), A3, and B; and

• 18% of the outstanding total balance of classes A1(G), A2(G), A3, and B.

After three years have elapsed, the cash reserve account will amortize if the following conditions are met:

• The outstanding balance of the loans in the pool with any payment in arrears for more than 90 days is lower than

1% of the outstanding balance of the non-delinquent loans (loans in arrears for more than 90 days) in the pool;

or

• The reserve fund is at the required level on the previous payment date.

The minimum reserve fund level can never be lower than 4.5% of the initial total balance of the class A1(G), A2(G),

A3, and B notes.

Standard & Poor’s | RatingsDirect on the Global Credit Portal | September 15, 2010 8

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

Interest swap agreement

On the issuer's behalf, the trustee will enter into a swap agreement with Banco Sabadell. This swap will provide

protection against adverse interest rate resetting and movements.

The issuer will pay to the swap counterparty the interest due on the non-defaulted loans during the calculation

period and the interest received from the amortization account during the first 18 months of the transaction. The

issuer will receive from the swap counterparty an amount equivalent to the weighted-average coupon on the notes

plus 60 bps per year over a notional, which will be the outstanding balance of the notes, and the servicing fee

amount.

This type of swap not only provides a hedge for the interest rate risk, but it also provides credit support to the

transaction, given that it covers the substitute servicing fee, the weighted-average coupon on the notes, and also

guarantees a spread of 60 bps in the transaction.

If an ineligible counterparty is not replaced within the remedy period, we may lower the ratings on the notes to

levels that could be supported by the counterparty's then-current rating. We will take into consideration the amount

of collateral in analyzing the transaction after the counterparty is downgraded. Our analysis assumes that a

replacement of the ineligible counterparty will occur. However, given the bespoke nature of this swap, it may be

difficult to find a replacement. Therefore, the market should understand and consider the risk of downgrade to the

transaction if a replacement is not found.

Under the transaction documentation, any counterparty replacement or guarantee is subject to our rating

confirmation. The downgraded counterparty bears all the costs of the remedies.

Redemption of the notes

Amortization occurs for the:

• Class A1(G) notes, from the first payment date until fully amortized;

• Class A2(G) notes, from the payment date that occurs 18 months after closing (soft-bullet). It will amortize from

this date, even though class A1(G) has not amortized in full;

• Class A3 notes, once the class A1(G) and A2(G) notes are fully redeemed, unless the pro rata conditions are met;

and

• Class B notes, once the class A1(G), A2(G), and A3 notes are fully redeemed, unless some pro rata conditions are

met.

From the first payment date, 40% of the amortization amount will go to class A1(G) and 60% to class A2(G). Until

18 months after the closing date, this 60% will be kept in an amortization account.

Pro rata amortization conditions: Classes A1(G), A2(G), and A3

If the proportion of: (i) the outstanding balance of non-delinquent loans plus the amounts received from the assets

during that period, and (ii) the net outstanding balance of the class A1(G), A2(G), and A3 notes, is less than or equal

to 1, classes A1(G), A2(G), and A3 will amortize pro rata.

Pro rata amortization conditions: Classes A and B

The conditions for the pro rata amortization of the class B notes are that they amortize pro rata with the class A

notes if:

www.standardandpoors.com/ratingsdirect 9

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

• Pro rata amortization for classes A1(G), A2(G), and A3 is not been applied.

• The reserve fund it is at its required level.

• The outstanding balance of the series A and B notes is equal to or higher than 10% of the original amount.

• The outstanding balance of the class B notes has doubled by percentage over the outstanding balance of the notes

they represented at closing, over the original balance.

• The outstanding balance of loans in arrears is lower than 1.25% of the outstanding balance of the non-defaulted

loans for class B.

Priority Of Payments

On each quarterly interest payment date, the issuer will pay in arrears the interest due to the noteholders. To make

the payments, the issuer's available funds will include the proceeds of the interest swap, the reserve fund, principal

received under the loans, and any other proceeds received in connection with the loans.

The issuer can mix all interest and principal received to pay principal and interest due under the notes in the

following order:

• Fees;

• Administration fees;

• Net payments under the swap agreement (other than swap termination payments due to a default or breach of

contract by the swap counterparty);

• Interest on the class A1(G), A2(G), and A3 notes; and reimbursement of any amount owed to the Kingdom of

Spain under the guarantee program to pay interest on the class A1(G) and A2(G) notes;

• Interest on the class B notes if not deferred;

• Amortization of the notes and reimbursement of any amount owed to the Kingdom of Spain under the guarantee

program to pay principal on the class A1(G) and A2(G) notes;

• Interest on the class B notes if deferred;

• Replenishment of the cash reserve;

• Interest and principal payments under the subordinated loan, established to fund the cash reserve;

• Swap termination payments, if any, when the issuer is not the defaulting party;

• Interest payments and principal repayments under the subordinated start-up loan; and

• Cash back to Banco Sabadell.

A trigger aims to ensure that in a stressful economic environment, the more senior notes amortize before the issuer

pays interest on the subordinated class of notes.

Interest on the class B notes will be subject to a deferral on a given payment date to a lower position in the priority

of payments in the following situation. If the cumulative ratio of defaulted loans (the outstanding balance of the

loans when qualified as defaulted, divided by the balance of the pool at closing) is greater than 25%, interest on the

class B notes will pay in a lower position in the priority of payments, until the class A notes, and then the class B

notes, redeem.

Standard & Poor’s | RatingsDirect on the Global Credit Portal | September 15, 2010 10

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

Credit Analysis

Default rate

We used a stochastic approach to assess the pool's credit risk. We then sized the required credit support for each

class of rated notes using Standard & Poor's CDO Evaluator. In sizing the portfolio default and loss rates, CDO

Evaluator took into account our mapped rating for each small and midsize enterprise (SME), the correlation within

and between industries, the maturity of each exposure, and transaction-specific recovery rates.

We entered the mapped SME ratings into CDO Evaluator to determine the portfolio's expected default frequency.

CDO Evaluator computed the cumulative default rates for each rating level along the capital structure using Monte

Carlo simulations based on the Credit Risk Tracker credit estimate of each asset in the portfolio.

The scenario default rates derived by using CDO Evaluator identify the maximum level of portfolio defaults that

each tranche should be able to withstand during the life of the transaction at its respective rating level without

defaulting.

Recoveries

To obtain the base-case recovery rate, we examine loss given defaults (LGDs) on a loan-level basis, the average

recovery rate from previous Spanish SME transactions with similar concentrations of secured and unsecured loans,

and historical recovery data of the Banco Sabadell loan book. We then applied a haircut to obtain the loss severity

for different scenarios.

Cash Flow Analysis

Prepayments

We stressed the annual prepayment rate up to 24.0% and down to 0.5%.

Yield

We modeled the spread guaranteed by the asset swap.

Commingling

We did not model any commingling stress in the structure, as there is downgrade language to set up the foundation

of a contingent commingling reserve if the servicer is downgraded below 'A-2' (see "Commingling reserve" above).

Timing of defaults

We assume defaults occur periodically in amounts calculated as a percentage of the default rate. We have applied

seven different default curves in our analysis (see tables 2 and 3 below).

Table 2

Timing Of Defaults

Percentage of DR(equal)

Months whenapplied

Percentage of DR (slow)(%)

Months whenapplied

Percentage of DR (fast)(%)

Months whenapplied

1/3 1 5 7 30 1

1/3 13 5 13 30 7

1/3 25 10 19 20 13

— — 20 25 10 19

— — 30 31 5 25

www.standardandpoors.com/ratingsdirect 11

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

Table 2

Timing Of Defaults (cont.)

— — 30 37 5 31

DR—Default rate.

Table 3

Timing Of Defaults

Percentage of DR(standard back)(%)

Monthswhen

applied

Percentage of DR(standard front)

(%)

Monthswhen

applied

Percentage of DR(standard 5 years

even) (%)

Monthswhen

applied

Percentage of DR(standard 4 years

even) (%)

Monthswhen

applied

15 1 40 7 20 7 25 7

30 7 20 13 20 13 25 13

30 13 20 19 20 19 25 19

15 19 10 25 20 25 25 25

10 25 10 31 20 31 — —

DR—Default rate.

Timing of recoveries

For this transaction, we assume that the issuer would regain 150% of recoveries 42 months after a payment default.

The value of recoveries at each rating level is 100% minus the loss severity assumed at each rating level.

Interest and prepayments rate

We modeled three interest rate scenarios—up, down, and flat—using both high and low prepayment assumptions.

Interest rates were 0.65% at the time of modeling and we modeled them to rise by 2% a month to a cap of 12%

("up" scenario) and a floor of 0% ("down" scenario).

Scenario Analysis

As part of a broad series of measures that we announced in 2008 to enhance our analytics and dissemination of

information, we have committed to provide a "what-if" scenario analysis in rating reports to explain our key rating

assumptions and the potential effect of positive or negative events on the ratings.

This scenario analysis section incorporates:

• A description of our methodology and scenario stresses;

• Results of the effects of the stresses on ratings; and

• Results of the effects of the stresses on our cash flow analysis.

Methodology

When rating European asset-backed securities (ABS) transactions, we have developed a scenario analysis and

sensitivity-testing model framework. This demonstrates the likely effect of scenario stresses on the ratings in a

transaction over a one-year outlook horizon. For this asset class, we consider scenario stresses over a one-year

horizon to be appropriate given the relatively short weighted-average life of the assets backing the notes. For these

types of securities, there are many factors that could cause the downgrade and default of a rated note, including

asset performance and structural features. However, for the purposes of this analysis we focused on the three

fundamental drivers of collateral performance, namely:

Standard & Poor’s | RatingsDirect on the Global Credit Portal | September 15, 2010 12

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

• Gross default rate;

• Recovery rate; and

• Prepayment rate.

Given current economic conditions, the stress scenarios proposed reflect negative events for each of these variables.

Increases in gross default rates could arise from a number of factors, including rises in unemployment and company

insolvencies, together with falls in house prices and a reduction in the availability of credit. In addition, these effects

would most likely cause collateral recovery rates to fall as the structural imbalance between supply and demand

leads to reductions in asset prices. In this environment, we also expect prepayment rates to fall as fewer refinancing

options leave obligors unable to prepay finance agreements and demand for replacement vehicles falls.

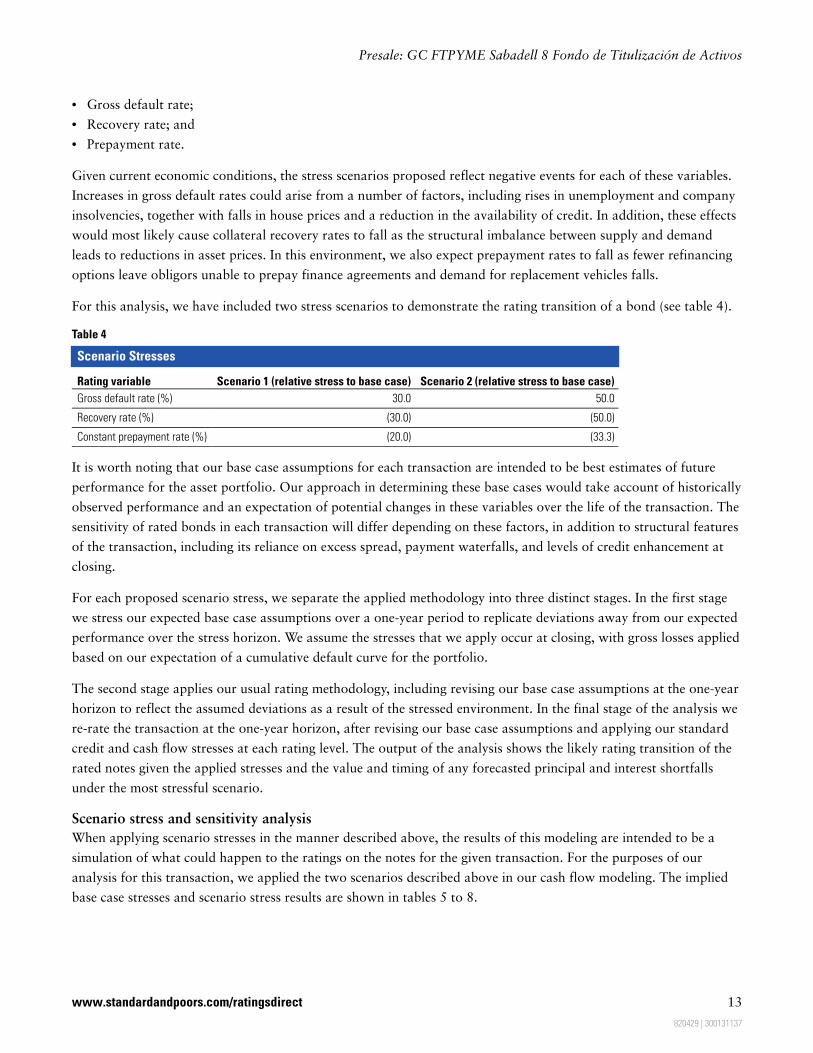

For this analysis, we have included two stress scenarios to demonstrate the rating transition of a bond (see table 4).

Table 4

Scenario Stresses

Rating variable Scenario 1 (relative stress to base case) Scenario 2 (relative stress to base case)

Gross default rate (%) 30.0 50.0

Recovery rate (%) (30.0) (50.0)

Constant prepayment rate (%) (20.0) (33.3)

It is worth noting that our base case assumptions for each transaction are intended to be best estimates of future

performance for the asset portfolio. Our approach in determining these base cases would take account of historically

observed performance and an expectation of potential changes in these variables over the life of the transaction. The

sensitivity of rated bonds in each transaction will differ depending on these factors, in addition to structural features

of the transaction, including its reliance on excess spread, payment waterfalls, and levels of credit enhancement at

closing.

For each proposed scenario stress, we separate the applied methodology into three distinct stages. In the first stage

we stress our expected base case assumptions over a one-year period to replicate deviations away from our expected

performance over the stress horizon. We assume the stresses that we apply occur at closing, with gross losses applied

based on our expectation of a cumulative default curve for the portfolio.

The second stage applies our usual rating methodology, including revising our base case assumptions at the one-year

horizon to reflect the assumed deviations as a result of the stressed environment. In the final stage of the analysis we

re-rate the transaction at the one-year horizon, after revising our base case assumptions and applying our standard

credit and cash flow stresses at each rating level. The output of the analysis shows the likely rating transition of the

rated notes given the applied stresses and the value and timing of any forecasted principal and interest shortfalls

under the most stressful scenario.

Scenario stress and sensitivity analysis

When applying scenario stresses in the manner described above, the results of this modeling are intended to be a

simulation of what could happen to the ratings on the notes for the given transaction. For the purposes of our

analysis for this transaction, we applied the two scenarios described above in our cash flow modeling. The implied

base case stresses and scenario stress results are shown in tables 5 to 8.

www.standardandpoors.com/ratingsdirect 13

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

Table 5

Scenario Stresses (Series A, 'AAA' Rating)Stress horizon—12 months

Rating variable Base case Scenario 1 Scenario 2

Gross loss rate (%) 35.16 45.71 52.74

Loss Severity (%) 70.00 79.00 85.00

Constant prepayment rate (%) 10.00 8.00 6.67

Table 6

Scenario Stress Analysis—Rating Transition Results

Scenario stress Class Initial rating Scenario stress rating

Scenario 1 A1(G), A2(G), and A3 AAA A

Scenario 2 A1(G), A2(G), and A3 AAA A

Table 7

Scenario Stresses (Class B, 'BB' Rating)Stress horizon—12 months

Rating variable Base case Scenario 1 Scenario 2

Gross loss rate (%) 15.96 20.75 23.94

Loss severity (%) 57.50 70.25 78.75

Constant prepayment rate (%) 10.00 8.00 6.67

Table 8

Scenario Stress Analysis—Rating Transition Results

Scenario stress Class Initial rating Scenario stress rating

Scenario 1 B BB BB

Scenario 2 B BB CCC

Where interest or principal shortfalls occur under the most senior notes, the holders of these notes and/or the trustee

can call an event of default. This could lead to multiple events, such as the senior fees of the transaction stepping up,

the swap terminating (with the issuer needing to make termination payments), and application of the

post-enforcement priority of payments. All of these events have an effect on the transaction cash flows.

For the purposes of the analysis above, we make a simplified assumption that the trustee will not call an event of

default.

Surveillance

We maintain continual surveillance on the transaction until the notes mature or are otherwise retired. To do this, we

analyze regular servicer reports detailing the performance of the underlying collateral, monitor supporting ratings,

assess pool cuts, and make regular contact with the servicer to ensure that minimum servicing standards are

sustained and that any material changes in the servicer's operations are communicated and assessed.

Key performance indicators for this transaction include:

• Rating migration of the collateral and default levels;

• Different concentrations of the collateral;

Standard & Poor’s | RatingsDirect on the Global Credit Portal | September 15, 2010 14

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

• Collateral prepayment levels;

• The evolution of the ratings on the supporting parties; and

• Increases in credit enhancement for the notes.

Related Criteria And Research

• Preliminary Ratings Assigned To GC FTPYME Sabadell 8's Spanish ABS Of SMEs Transaction, Sept. 15, 2010

• Revised Framework For Applying Counterparty And Supporting Party Criteria, May 8, 2007

• European Legal Criteria for Structured Finance Transactions, Aug. 28, 2008

• Global Interest Rate and Currency Swaps: Calculating the Collateral Required Amount, Feb. 26, 2004

• Standard & Poor's Global Interest Rate and Swap Counterparty Rating Criteria Expanded, Dec. 17, 2003

• Standard & Poor's Rating Methodology for CLOs Backed by European Small- and Midsize-Enterprise Loans,

Jan. 30, 2003

• Securitizing Spanish-Originated Loans to Small and Midsize Enterprises, April 7, 2003

• Spanish SME Performance Report: Delinquencies For Spanish SME Asset-Backed Securities Transactions Reach A

New High, July 23, 2009

• Spanish SME ABS Collateral Deterioration Focused On Construction Sector And Coastal Regions, Dec. 17, 2009

Related articles are available on RatingsDirect. Criteria, presales, servicer evaluations, and ratings information can

also be found on Standard & Poor's Web site at www.standardandpoors.com. Alternatively, call one of the

following Standard & Poor's numbers: Client Support Europe (44) 20-7176-7176; London Press Office (44)

20-7176-3605; Paris (33) 1-4420-6708; Frankfurt (49) 69-33-999-225; Stockholm (46) 8-440-5914; or Moscow (7)

495-783-4011.

Additional Contact:Structured Finance Europe; [email protected]

www.standardandpoors.com/ratingsdirect 15

820429 | 300131137

Presale: GC FTPYME Sabadell 8 Fondo de Titulización de Activos

S&P may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the rightto disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), andwww.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributed through other means, including via S&P publications and third-partyredistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result,certain business units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain theconfidentiality of certain non-public information received in connection with each analytical process.

Credit-related analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact orrecommendations to purchase, hold, or sell any securities or to make any investment decisions. S&P assumes no obligation to update the Content following publication in anyform or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/orclients when making investment and other business decisions. S&P's opinions and analyses do not address the suitability of any security. S&P does not act as a fiduciary oran investment advisor. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence orindependent verification of any information it receives.

No content (including ratings, credit-related analyses and data, model, software or other application or output therefrom) or any part thereof (Content) may be modified,reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of S&P. The Contentshall not be used for any unlawful or unauthorized purposes. S&P, its affiliates, and any third-party providers, as well as their directors, officers, shareholders, employees oragents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors oromissions, regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content isprovided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OFMERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONINGWILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to anyparty for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, withoutlimitation, lost income or lost profits and opportunity costs) in connection with any use of the Content even if advised of the possibility of such damages.

Copyright © 2010 by Standard & Poor's Financial ,<FONT COLOR="BLUE">Services LLC (S&P)</FONT>, a subsidiary of The McGraw-Hill Companies,

Standard & Poor’s | RatingsDirect on the Global Credit Portal | September 15, 2010 16

820429 | 300131137

Related Documents