Roundtable Part 2: Our panelists name their top investment ideas for 2021. PAGE 22 Picks From the Pros > 63142 VOL. CI NO. 4 JANUARY 25, 2021 $5.00 WHAT BIDEN MEANS FOR THE MARKETS • PAGES 6, 12 MSGS MSFT Madison Square Garden Sports Microsoft GAN NEP SBGI AGR Avangrid GAN NextEra Energy Partners Sinclair Broadcast Group WLKP VIV NOC GLD ASIX PM DHI MPACX D.R. Horton Matthews Asia Growth Westlake Chemical Partners Telefônica Brasil Northrop Grumman SPDR Gold Shares AdvanSix Philip Morris International SCOTT BLACK SONAL DESAI MARIO GABELLI RUPAL J. BHANSALI

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Roundtable Part 2: Our panelists name their top investment ideas for 2021. PAGE 22

Picks From the Pros

>

63142

VOL. CI NO. 4 JANUARY 25, 2021 $5.00

WHAT BIDEN MEANS FOR THE MARKETS • PAGES 6, 12

MSGS

MSFT

Madison Square Garden Sports

Microsoft

GANNEP SBGIAGRAvangrid GAN

NextEra Energy Partners Sinclair Broadcast Group

WLKP

VIV

NOCGLD ASIX

PMDHIMPACXD.R. HortonMatthewsAsia Growth Westlake Chemical Partners

Telefônica Brasil

Northrop GrummanSPDRGold Shares AdvanSix

PhilipMorris International

SCOTT BLACKSONAL DESAI

MARIOGABELLI

RUPALJ.BHANSALI

C O N T E N T S 0 1 . 2 5 . 2 1 VO L . C I NO . 4

Index P.4

Review&Preview P.10

Mailbag P.39

InsideScoop P.M7

ChartingtheMarket P.M9

Winners&Losers P.M10

ResearchReports P.M11

MarketView P.M12

Cover Illustrations byHelen Green

© 2021 Dow Jones & Company, Inc. All Rights Reserved.

Our newspapers are 100% sourced from sustainable certified mills.

BARRON’S (USPS 044-700) (ISSN 1077-8039) Published everyMonday. Editorial and Publication Headquarters: 1211 Avenue ofthe Americas, New York, N.Y. 10036. Periodicals postage paid atChicopee, MA and other mailing offices. Postmaster: Send addresschanges to Barron’s, 200 Burnett Rd., Chicopee, MA 01020

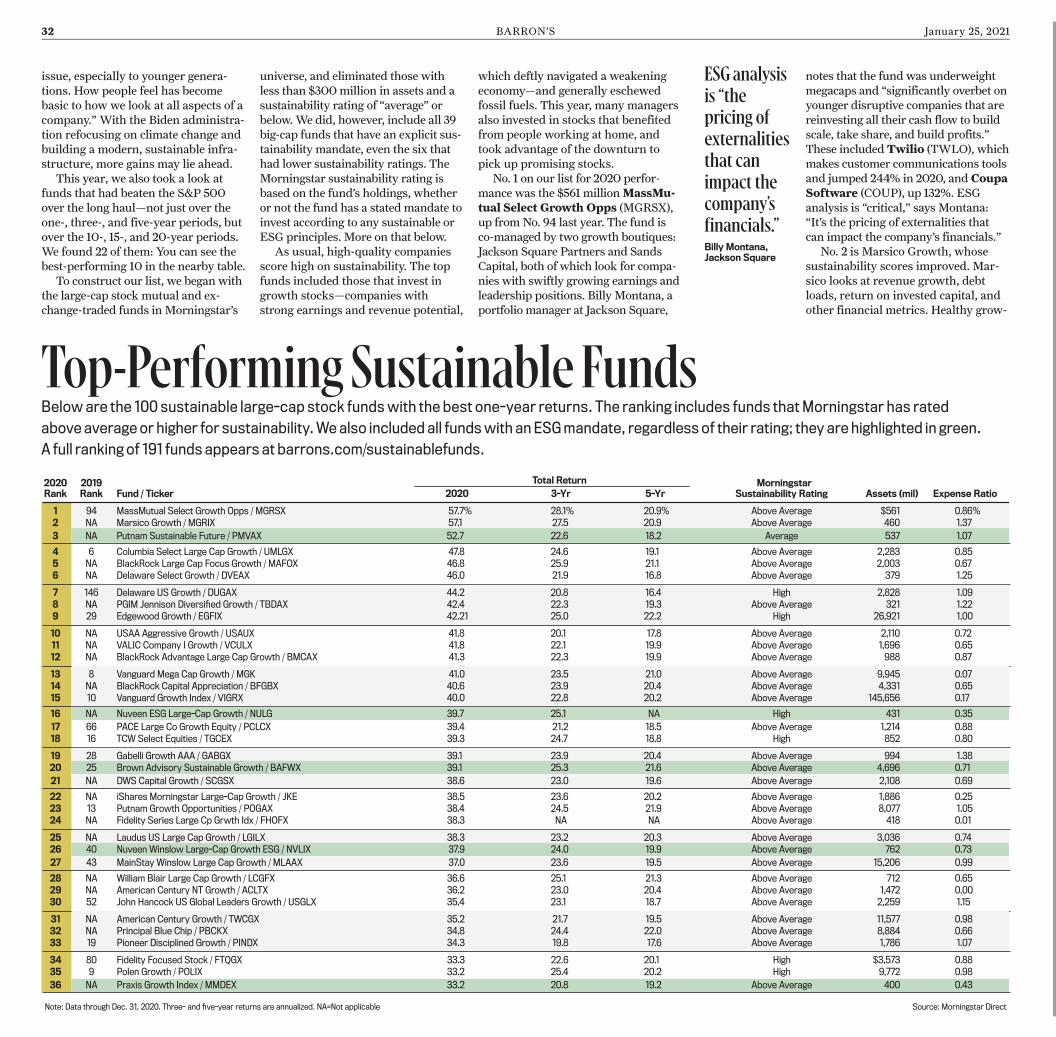

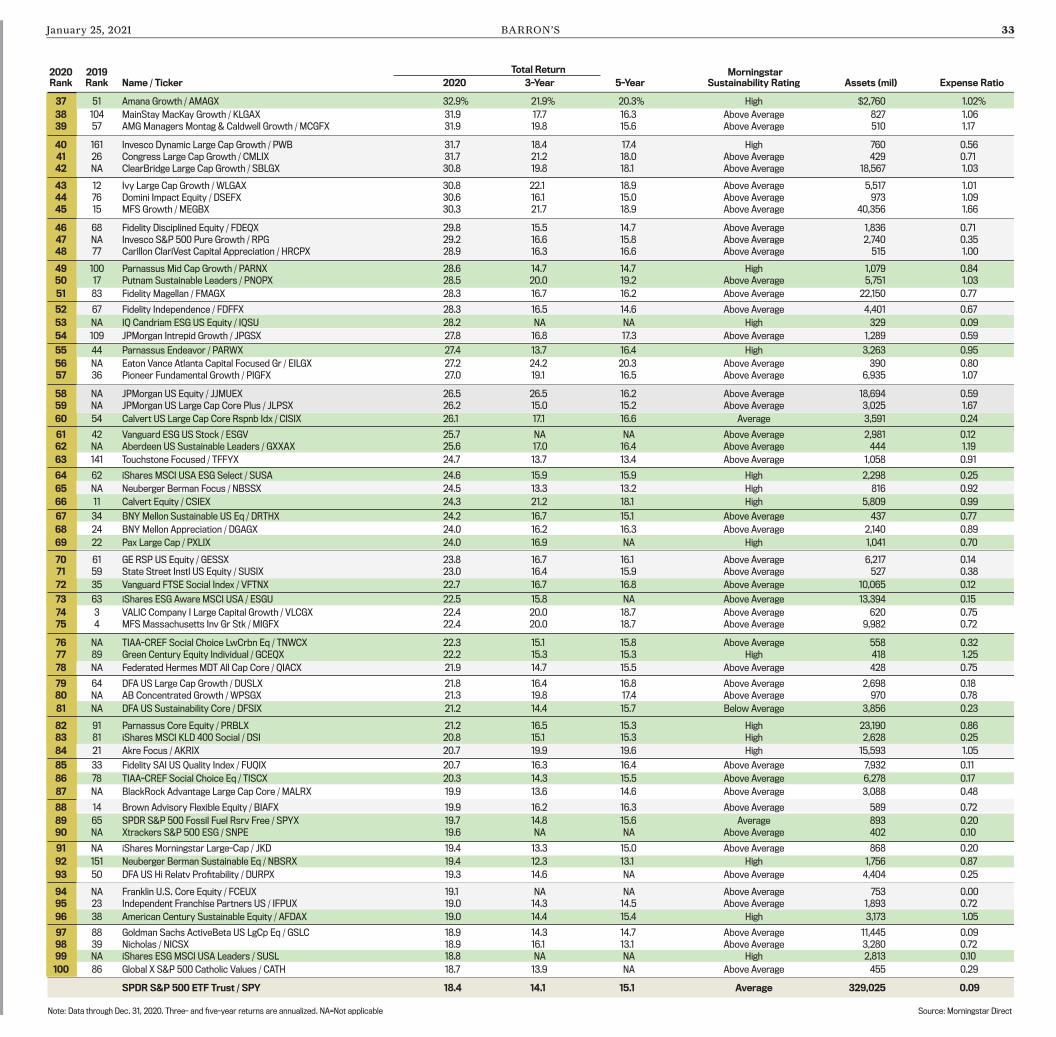

MassMutual Select Growth Opps2019 RANK: 94 TICKER: MGRSX 2020 TOTAL RETURN: 57.7%

Marsico Growth2019 RANK: NA TICKER: MGRIX 2020 TOTAL RETURN: 57.1%

Putnam Sustainable Future2019 RANK: NA TICKER: PMVAX 2020 TOTAL RETURN: 52.7%

Columbia Select Large Cap Growth2019 RANK: 6 TICKER: UMLGX 2020 TOTAL RETURN: 47.8%

BlackRock Large Cap Focus Growth2019 RANK: NA TICKER: MAFOX 2020 TOTAL RETURN: 46.8%

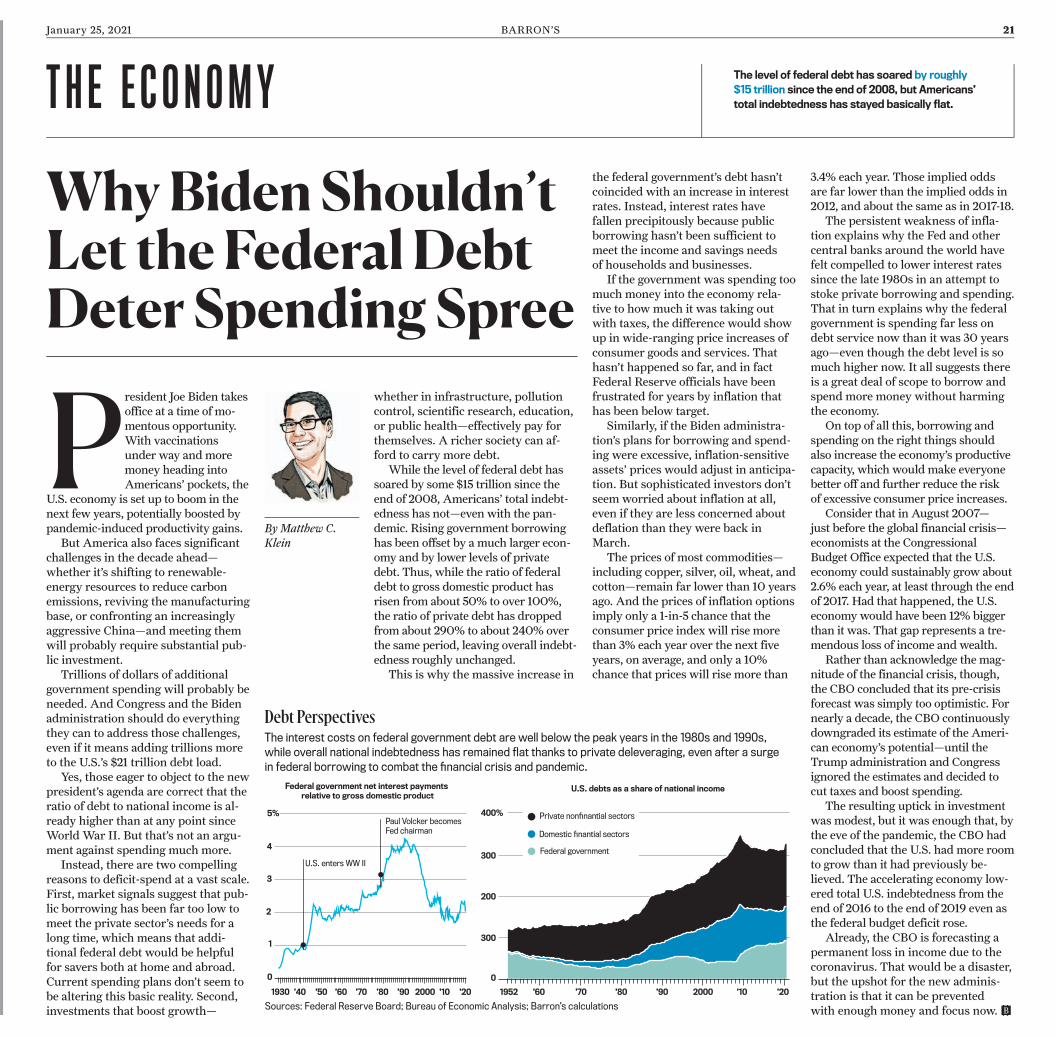

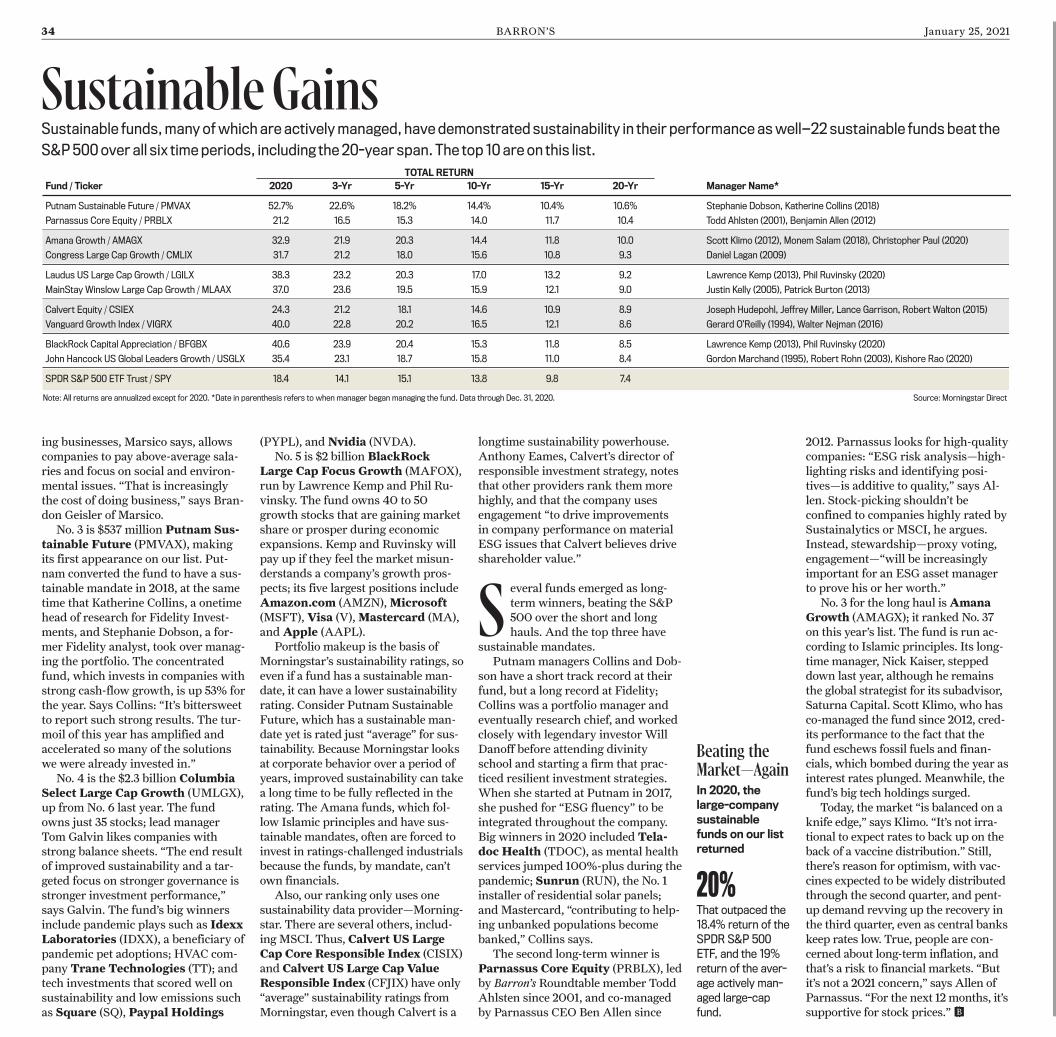

The 191 sustainable funds on our list returned 20% last year, on average, outpacingthe S&P 500 index’s 18% gain. Many funds did far better.

Trouncing the Market

Source: Morningstar DirectNA=Not applicable

2345

1

P.31

The Top Sustainable FundsOur fifth annual ranking reinforces the value of investing in companies that prioritizeenvironmental, social, and governance, or ESG, factors. ByLESLIEP.NORTON

Also: Investing in China can be problematic. Focusing on ESG can help. P. 35

P.6

Up & Down Wall Street:Speculation ReturnsThe buying frenzy in stocks suchas GameStop and megacap technames points to a market peak.Take a cue from the smart money.ByRANDALLW.FORSYTH

P.9

Streetwise: ScreenTime to the RescuePandemic lockdowns have ledto an explosion in videogaming—and upstart companies arerushing to get in on the action.ByJACKHOUGH

P. 12

Biden Isn’t Likely toEase Up on ChinaFollow-Up: Despite a reset onU.S.-China policy, investorsbetting on China’s rapid growthstill need to tread carefully.ByRESHMAKAPADIA

P. 13

A Corner of TechSet to Play Catch-UpRising spending on digitalinfrastructure makes these fourtower and data-center stockssavvy bets for the year to come.ByDARENFONDA

P. 15

Auto-Parts SupplierLKQ Is Purring AgainThe pandemic has prompted theused-parts specialist to make thefixes needed to get its profits—andstock price—moving higher.ByTERESARIVAS

P. 16

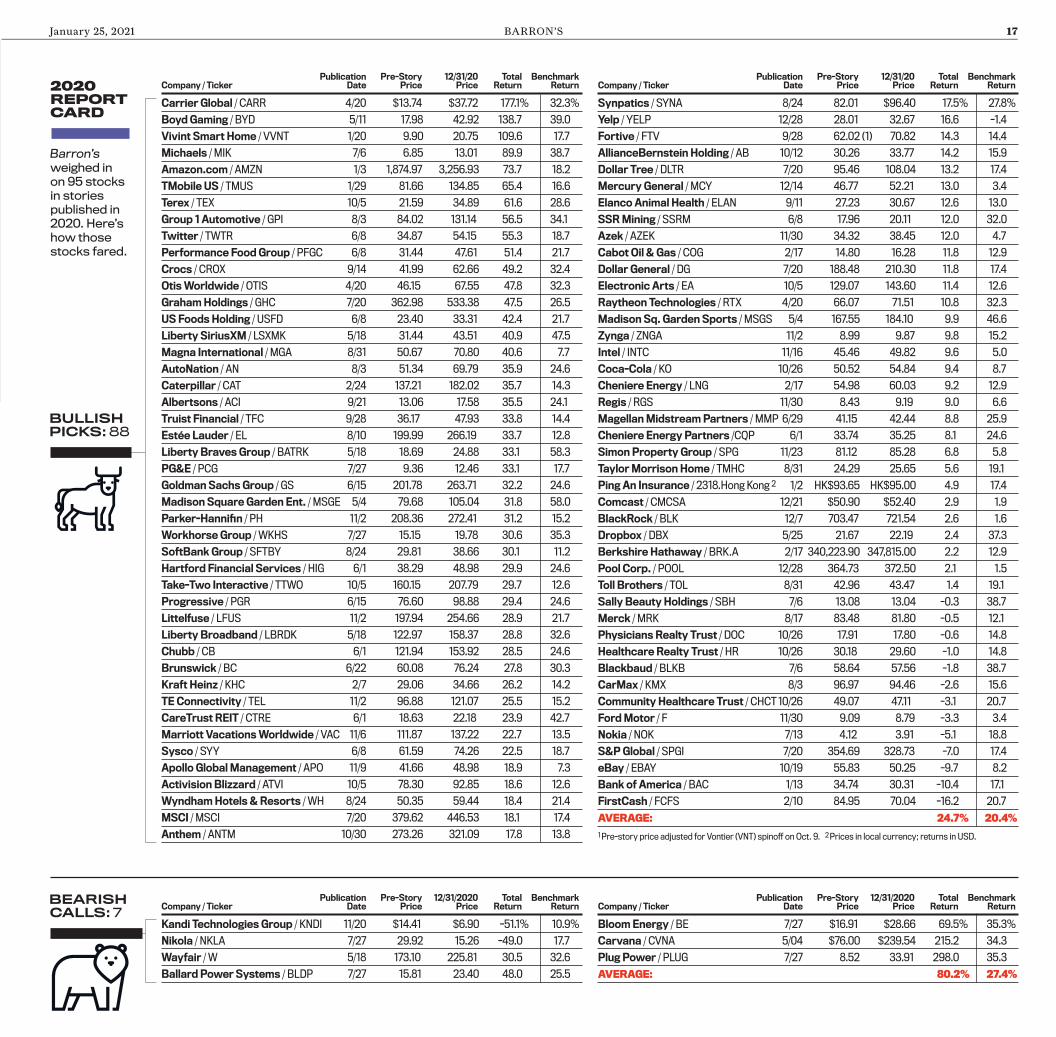

Our Stock Picks Beatthe Market in 2020Readers who followed our advice tobuy names such as Carrier Global,Boyd Gaming, and Michaels lastyear were well rewarded.ByAVI SALZMAN

P. 19

Income: Patience PaysWith Dividend FundsFunds that focus on stocks withabove-average payouts tend toshine when the going gets tough.Here are six to consider.ByLAWRENCEC.STRAUSS

P.22

Roundtable, Part 2:Place Your BetsCover Story: This installmenthighlights 28 investment ideasfrom Scott Black, Mario Gabelli,Rupal J. Bhansali, and Sonal Desai.ByLAURENR.RUBLIN

P.21

Economy: Don’t LetDebt Deter SpendingByMATTHEWC.KLEIN

P.36

Tech Trader: A NetflixNaysayer No MoreByERIC J.SAVITZ

P.38

Other Voices:Seafarer RestrictionsImperil Supply ChainsByGUYPLATTEN

P.M1

Trader: Spring CouldBring Market BargainsByBENLEVISOHN

P.M4

Euro Trader: A BrightOutlook for PolymetalByRUPERTSTEINER

P.M4

Emerging Markets:Investors OverlookObstacles in IndiaByCRAIGMELLOW

P.M5

Striking Price: WhyTesla Is a Perfect Fitfor Options TradingBySTEVENM.SEARS

P.M6

Commodities: LumberPrices Are WhittledDown as Supply GrowsByMYRAP.SAEFONG

Barron’s Roundtableon Fox BusinessWatch our TV show Fridays at 10p.m. or 11:30 p.m. ET; Saturdays at10 a.m. or 11:30 a.m.; or Sundaysat 7 a.m., 10 a.m., or 11:30 a.m.This week, we look at PresidentBiden’s policy priorities with GregValliere, AGF Investments chiefU.S. policy strategist, and gaininsights on 2021 stock picks fromMario Gabelli, chairman of GamcoInvestors.

Roundtable Part 2: Our panelists name their top investment ideas for 2021. PAGE 22

Picks From the Pros

>

63142

VOL. CI NO. 4 JANUARY 25, 2021 $5.00

WHAT BIDEN MEANS FOR THE MARKETS • PAGES 6, 12

MSGS

MSFT

Madison Square Garden Sports

Microsoft

GANNEP SBGIAGRAvangrid GAN

NextEra Energy Partners Sinclair Broadcast Group

WLKP

VIV

NOCGLD ASIX

PMDHIMPACXD.R. HortonMatthewsAsia Growth Westlake Chemical Partners

Telefônica Brasil

NorthropGrummanSPDRGold Shares AdvanSix

Philip Morris International

SCOTT BLACKSONAL DESAI

MARIOGABELLI

RUPALJ.BHANSALI

January 25, 2021 BARRON’S 3

The Refinitiv Lipper Fund Awards are based on the Lipper Leader for Consistent Return rating, which is a risk-adjusted performance measure calculated over 36, 60 and 120 months. Lipper Leaders fund ratings do not constitute and are not intended to constitute investment advice or an offer to sell or thesolicitation of an offer to buy any security of any entity in any jurisdiction. For more information, see lipperfundawards.com. Lipper Fund Awards from Refinitiv, ©2021 Refinitiv. All rights reserved. Used under license. The award is based on a review of risk-adjusted performance of 33 companies for 2020.The award pertains only to the Nuveen funds in the fixed-income category. Certain funds have fee waivers in effect. Without such waivers ratings could be lower.Past performance does not guarantee future results. This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided doesnot take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Before investing, carefully consider fund investment objectives, risks, charges and expenses. For this and other information that should be read carefully,please request a prospectus or summary prospectus from your financial professional or Nuveen at 800.752.8700 or visit nuveen.com.Nuveen Securities, LLC, member FINRA and SIPC. 20854 GAD-1134692CR-W0420X

Income strategies asdeep as our heritage

• Over 120 years as an income provider

• Expertise across municipal bonds,taxable fixed income and real assets

• Awarded 2020 Best Fixed IncomeLarge Fund Company

nuveen.com/income

4 BARRON’S January 25, 2021

A Abbott Laboratories . . . . . . . . . . . . . . . . . . . . . . . 11Activision Blizzard . . . . . . . . . . . . . . . . . . . . . . . . . . 9Advance Auto Parts . . . . . . . . . . . . . . . . . . . . . . . . 15Advanced Micro Devices . . . . . . . . . . . . . . . . . . . 11AdvanSix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Alcoa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . M9Alibaba Group Holding . . . . . . . . . . . . . . . . . . . M9Altria Group . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11,25Amazon.com . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16AMC Entertainment . . . . . . . . . . . . . . . . . . . . . . M9American Airlines Group . . . . . . . . . . . . . . . . . . . 11American Express . . . . . . . . . . . . . . . . . . . . . . . . . 11American Tower . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Anthem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11A.P. Moeller-Maersk . . . . . . . . . . . . . . . . . . . . . . . 11Apple . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11,19,28AT&T . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11AutoZone . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Avangrid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

B Bally's . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30Bank of America . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Bayerische Motoren Werke . . . . . . . . . . . . . . . . 28Best Buy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Bicycle Therapeutics . . . . . . . . . . . . . . . . . . . . . .M7BioNTech . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Boeing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Boyd Gaming . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

C Capital One Financial . . . . . . . . . . . . . . . . . . . . . . 11Carnival . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . M7Carrier Global . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Carvana . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Caterpillar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Charter Communications . . . . . . . . . . . . . . . . 11,13Chevron . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11China Construction Bank . . . . . . . . . . . . . . . . . . 35China Mobile . . . . . . . . . . . . . . . . . . . . . . . . . . . .12,26Clearwater Paper . . . . . . . . . . . . . . . . . . . . . . . . M11Coherent . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Colgate-Palmolive . . . . . . . . . . . . . . . . . . . . . . . . . . 11Comcast . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11,13Copart . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15CoreSite Realty . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Cosco Shipping Holdings . . . . . . . . . . . . . . . . . . . 11Crown Castle International . . . . . . . . . . . . . . 11,13

D Danaher . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11DermTech . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . M7Deutsche Telekom . . . . . . . . . . . . . . . . . . . . . . . . . 29DISH Network . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Dow . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11D.R. Horton . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

E Electronic Arts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Eli Lilly . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Entain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30,M11Enzo Biochem . . . . . . . . . . . . . . . . . . . . . . . . . . . . M7Equinix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

F Facebook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Fastenal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15FirstCash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Flutter Entertainment . . . . . . . . . . . . . . . . . . . . . 29Ford Motor. . . . . . . . . . . . . . . . . . . . . . . . . .10,28,M2Formula One Group . . . . . . . . . . . . . . . . . . . . . . . . 29Fox . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

G GAN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30GCP Applied Technologies . . . . . . . . . . . . . . . . . 29General Electric . . . . . . . . . . . . . . . . . . . . . . . . . . . 11General Motors . . . . . . . . . . . . . . . . . . . . . . . . . 10,28Genuine Parts . . . . . . . . . . . . . . . . . . . . . . . . . . . 15,29Gevo . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .M9

Gritstone Oncology . . . . . . . . . . . . . . . . . . . . . . . M9

H Home Depot . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Honeywell International . . . . . . . . . . . . . . . . . 11,26Hyster-Yale Materials Handling . . . . . . . . . . . . 24Hyundai Motor . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

I IAC/InterActiveCorp. . . . . . . . . . . . . . . . . . . . . . . 30Iberdrola . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29IBM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10,M9Inditex . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35Intel . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10,M9Invesco . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

J Johnson & Johnson . . . . . . . . . . . . . . . . . . . . . . . . 11

K Kandi Technologies Group . . . . . . . . . . . . . . . . . 16Kimball Electronics . . . . . . . . . . . . . . . . . . . . . . . . 27Kimberly-Clark . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Koninklijke Philips . . . . . . . . . . . . . . . . . . . . . . 11,27

L Lam Research . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Liberty Braves . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29LKQ. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Lockheed Martin . . . . . . . . . . . . . . . . . . . . . . . . . . 11Lumentum Holdings . . . . . . . . . . . . . . . . . . . 10,M9

MMadison Square Garden Sports . . . . . . . . . . . . 29Magna International . . . . . . . . . . . . . . . . . . . . . . . 28Mastercard . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

McDonald's . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Meituan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35MGM Resorts International . . . . . . . . . . . 30,M11Microsoft . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11,24,M1Mondelez International . . . . . . . . . . . . . . . . . . . . 11MSCI . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Muenchener Rueckversicherungs-Gesellschaft24

N Netflix . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10,26,36,M1News Corp . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Nexteer Automotive Group. . . . . . . . . . . . . . . . .27NextEra Energy. . . . . . . . . . . . . . . . . . . . . . . . . . . 29NextEra Energy Partners . . . . . . . . . . . . . . . . . 29Nikola . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Nintendo . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Norfolk Southern . . . . . . . . . . . . . . . . . . . . . . . . . . 11Northrop Grumman . . . . . . . . . . . . . . . . . . . . . 11,24

O O'Reilly Automotive . . . . . . . . . . . . . . . . . . . . . . . . 15Otis Worldwide . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

P PayPal Holdings . . . . . . . . . . . . . . . . . . . . . . . . . . . 34PDC Energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . M11Pfizer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .M11Philip Morris International . . . . . . . . . . . . . . . . 25Playtika Holding . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Plug Power . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29PNM Resources . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Prologis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

R Raytheon Technologies . . . . . . . . . . . . . . . . . . . . . 11RH . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . M11Riot Blockchain . . . . . . . . . . . . . . . . . . . . . . . . . . .M9

S Salesforce.com . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26SBA Communications . . . . . . . . . . . . . . . . . . . . . . 13ServiceNow . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Signature Bank . . . . . . . . . . . . . . . . . . . . . . . . . . M11Sinclair Broadcast Group . . . . . . . . . . . . . . . . . . 29Snam . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24SoftBank Group . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Sony . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Southwest Airlines . . . . . . . . . . . . . . . . . . . . . . . . . 11SPDR Gold Shares . . . . . . . . . . . . . . . . . . . . . . . . 30Square. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .34Starbucks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Stellantis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Stryker . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11SunPower. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .M9

T Take-Two Interactive Software . . . . . . . . . . . . . 9Telecom Italia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25Telefonica Brasil . . . . . . . . . . . . . . . . . . . . . . . . . . . 25Tencent Holdings . . . . . . . . . . . . . . . . . . . . . . . . . . 35Tenneco . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . M7Tesla . . . . . . . . . . . . . . . . . . . . . . . 10,11,16,24,M3,M5Texas Instruments . . . . . . . . . . . . . . . . . . . . . . . . . 113M. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11T-Mobile US . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13,25Toyota Motor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . M3Triton International . . . . . . . . . . . . . . . . . . . . . . . . 11T. Rowe Price Group . . . . . . . . . . . . . . . . . . . . . . . 11Twitter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

V Verizon Communications . . . . . . . . . . . . . . . . . . . 11Viatris . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . M11Visa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

WWestlake Chemical Partners . . . . . . . . . . . . . . . 27Westwater Resources . . . . . . . . . . . . . . . . . . . . . M9

I N D E X Our index lists significant companies mentioned in stories and columns,plus Research Reports, and Corrections & Amplifications. The referencesare to the first page of the item in which the company is mentioned.

For Customer Service, call 1 (800) 544-0422, or go tocustomercenter.barrons.com. For reprints of articles,call 1 (800) 843-0008, or go to djreprints.com.

EXECUTIVEEDITOR BobRose SENIORMANAGINGEDITOR LaurenR.Rublin

DEPUTYEDITOR AlexEule DEPUTYEDITOR BenLevisohnEDITORIALDIRECTOR, INVESTING&ASSETMANAGEMENT BeverlyGoodman

EDITORIALDIRECTOR,MAGAZINE Phil Roosevelt

MANAGINGEDITOR,DIGITAL Matt Bemer MANAGINGEDITOR, FEATURES JeffreyCaneMANAGINGEDITOR, ENTERPRISEBrianHershberg

ASSISTANTMANAGINGEDITORS MaryRomano, Robert Sabat

ASSOCIATEEDITORS AndrewBary, RandallW. Forsyth, JackHough,ReshmaKapadia, Eric J. Savitz

SENIORWRITERS BillAlpert,DarenFonda,MatthewC.Klein, Leslie P.Norton,AlRoot, Avi Salzman,Alexandra Scaggs, LawrenceC. Strauss

REPORTERS LisaBeilfuss,MaxA.Cherney,CarletonEnglish,Nicholas Jasinski, Evie Liu,JoshNathan-Kazis, TeresaRivas, Connor Smith, Jacob Sonenshine, BenWalsh

STORYEDITORS HenryCutter, EdLin, ErinMcCarthy

COPYDESK Michael J. Burlingham,RichardRescigno, Robert Teitelman

IDEASEDITOR Matt Peterson

DEPUTYDIGITALMANAGINGEDITOR Zoe Szathmary

SENIORAUDIOMANAGER Mette Lützhøft DIGITALPRODUCERS Robert Cushing, ClareMcKeen

DESIGNDIRECTOR ChrisMihal ARTDIRECTORS Robert Connolly, NickHallam, SueNgDIRECTOROFPHOTOGRAPHY Sarina Finkelstein PHOTOEDITORS SamKelly, Nicole Silver

RESEARCHDIRECTOR PaulineYuelys RESEARCHER DanLam

STATISTICSMANAGER Michael T. Kokoszka STATISTICIAN DarrenChima

MANAGER,ADVERTISINGSERVICES JamesH. Balmer ASSOCIATEMANAGER WardS.McGuinessNEWS [email protected] STATISTICS [email protected] CUSTOMERSERVICE 800-544-0422

GLOBALHEAD,WEALTH&ASSETMANAGEMENT JackOtter

Barron’s is a trademark of Dow Jones and its affiliates. Barron’s (USPS 044-700) (ISSN 1077-8039) Published every Monday. Editorial and PublicationHeadquarters: 1211 Avenue of the Americas, New York, N.Y. 10036. Periodicals postage paid at Chicopee, MA and other mailing offices. RegularU.S. subscription rate: one year, $223. Entire editorial content of this publication copyrighted by Dow Jones & Co., Inc. and must not be reproducedin whole or in part without special permission. Unsolicited manuscripts should be accompanied by self-addressed envelope with proper postage. Alladvertising published in Barron’s is subject to the applicable rate card, copies of which are available from the Advertising Director, 1211 Avenue of the

Americas, New York, N.Y. 10036. Barron’s reserves the right not to accept an advertiser’s order. Only publication of an advertisement shall constitute acceptanceof the advertiser's order. Postmaster: Send address changes to Barron’s, 200 Burnett Rd., Chicopee, MA 01020.

RupertMurdochExecutive Chairman,News CorpRobert ThomsonCEO,News Corp Almar LatourCEO,Dow Jones

SENIORVICEPRESIDENT, BARRON’SGROUPMaeM.ChengASSOCIATEPUBLISHER, BARRON’SGROUPDanShar

MANAGINGEDITORS, BARRON’SGROUP DuncanMavin, Dave PettitHEADOF INTERNATIONAL, BARRON’SGROUP FrancescoGuerrera

w00

4_p2

bw02

5000

_0_w

0040

0_1_

____

___x

a202

1_01

123

-Jan

-21

04:3

4:49

January 25, 2021 BARRON’S 5

“New York Life Investments” is both a service mark, and the common trade name, of certain investment advisors affiliated with New York Life Insurance Company.

The products and services of New York Life Investments' boutiques are not available in all jurisdictions or regions where such provision would be contrary to

local laws or regulations. 1824398

We invest in our clients, identifying new ideas and opportunities.

Where there are risks, we do our best to manage them.

This is how we work with you and for you.

Strategies intended to deliver real outcomes and build long-term wealth.

We see investing as a mutual effort—one that works only if we all succeed.

We’re in it together to move forward together. That’s how it works.

That’s how it has worked for our parent, New York Life, for over 175 years.

And how it’ll continue to work. That’s our promise.

We believe in you and in us.

Relationships built for the long term but relevant for the times we live in today.

In the power of what we can do together.

More than capital alone. More than algorithms or optimistic forecasts.

Building equity in something far bigger than just a portfolio.

And that is what makes us different.

More than investing. Invested.

6 BARRON’S January 25, 2021

U P & D OWN WA L L S T R E E T A short squeeze helped boost GameStop 80% atone point Friday before trading in the videogameseller’s stockwas halted. Still, it closed up 50%.

Speculative Frenzy’sUnlikely Poster Child:GameStop Shares

A return to normalcy orsnafu? The formerrecalls the presidencyofWarren G. Harding,inaugurated a centuryago, after the upheavalsofWorldWar I and the

flu pandemic of 1918. The latter refers toan acronym fromWorldWar II, whichroughly translates to “Situation normal,all fouled up” in its PG version.

Snafu rather than normalcy seemsmore apt to describe the speculativefrenzy in certain quarters of the finan-cial markets. Frenetic trading in stocksand options of no apparent worth haserupted anew, a classic sign of specula-tion that often coincides with tops inthe market.

The new poster child for this crazi-ness isGameStop (ticker: GME),which frankly I had forgotten still ex-ists. The bricks-and-mortar retailer ofvideogames, both new and used, shut-teredmy local store, which had been afew doors down fromwhat once was aBlockbuster Video outlet. I thoughtboth had been supplanted by onlinedelivery of content. Ditto for the youn-gest member of the Forsyth household,an avid gamer, whose powerful PClacks a DVD drive for physical content.

Yet traders have piled intoGameStop, sending the stock soaringmore than 80% Friday before beinghalted; it ultimately closed upmorethan 50%. Not coincidentally, theshares have been heavily shorted andhave been prominently featured byAndrew Left, the head of Citron Re-search, who posted his assessment ofthe extreme overvaluation of GameStopin a YouTube video that fanned only

contempt from the stock’s fans.The speculative froth also has been

visible in other corners of the market.Ironically, the cooling of the frenzy inBitcoin—back to around $32,000 froma recent peak over $40,000, followingits surge from around $24,000—hasshifted the speculative crowd back tothe action in megacap tech stocks. Butinstead of slices of these shares withprices in the hundreds or thousands ofdollars, they’re playing the low-priceoptions on these names, says JulianEmanuel, BTIG’s chief equity and de-rivatives strategist.

Specifically, the punters are buyingbullish call options on some of the big-gest of the FAANGs (he’s not allowed to

name names, but you know the stocksthat are covered by the famous acro-nym). More important, they’re playingcheap calls with strike prices that arefar out of the money andwith weeklyexpirations with only a few days to run.

The bottom line: These bets on high-price shares can be bought literally forpennies. Inevitably, they will expireworthless. But before that, the optionsmight rise a cent or two, making for bigpercentage moves for players who arequick to cash in.

This sort of action was prevalentlast August, just before the big techsthat drive the Nasdaq topped out,Emanuel notes. Now it’s back—a cau-tion signal for the short term.

The frenetic buying of bullish calloptions has kept implied volatilities—the key determinant of optionsprices—above their actual realizedvolatilities, he adds. Usually, buyingput options to protect portfolios fromdeclines pushes up implied volatility,which is most widely measured in theCboe Volatility Index, or VIX, themarket’s so-called fear gauge. Itclosed Friday at 21.91, well above theteens, where it might be expected tobe—with the Nasdaq Composite end-ing the holiday-shortened week upover 4% and at a record, and with

By Randall W.Forsyth

A shopperleaves a GameStopstore with the newPlay Station 5gaming consolelast Black Friday.

other averages near their peaks.But the mostly well-heeled and expe-

rienced clientele of Interactive Brokersare taking the opposite tack, writesThomas Peterffy, the firm’s founder, inan email. They are writing, or selling,call options against their substantialpositions in the expensive stocks onwhich they have big, accumulated prof-its. That generates current income,whichmight be why the smart moneygets that name.

More scary is the opprobriumheaped on GameStop’s detractors, whohave been objects of online attacks.“There is a consistent stridence to ma-jor market peaks,” writes Peter Atwa-ter, an adjunct professor of economicsat the College ofWilliam &Mary, in hisFinancial Insyghts newsletter. A returnto normalcy would be indeed welcome.

T he U.S. stock market endedInauguration Day at a recordhigh, but the connection isstrained. For fans of presi-

dential trivia, theWilshire 5000 totalstock market index’s gain that day of1.25%, or about $525 billion, put it upby nearly 72%, or $18.8 trillion, fromthe previous Inauguration Day, Jan. 20,2017. But this broad measure of theU.S. market has risen even more—some 82%, or $19.3 trillion—sinceMarch 23, when the Federal Reserve letloose its array of aggressive monetarymeasures to arrest the economic effectsof the coronavirus pandemic.

Since then, the bull market hasbeen built on hopes that the triumvi-rate of monetary and fiscal spurs plusvaccines will return the economy andthe world to something approachingnormalcy. But if past is prologue, theroad ahead could be bumpy for stocks.

February historically is the worstmonth for equities in a new president’sfirst year, according to a report fromStrategas Research Partners’Washing-ton research team, led by Dan Clifton.From 1927 to 2017, the S&P 500, onaverage, fell 4% in suchmonths. How-ever, that record is heavily skewed bythe steep drops in February 2009 at theheight of the financial crisis at the be-ginning of Barack Obama’s initial term,and in February 2001 during the reces-sion at the outset of GeorgeW. Bush’s A

imeeDilg

er/SOPA

Images/G

ettyIm

ages

January 25, 2021 BARRON’S 7

first term, after the dot-com bubble burst.For now, much of the bullishness is a

product of fiscal actions, taken or antici-pated. The $900 billion measure enactedat the end of 2020 provides $600 checksfor most Americans, while a massive $1.9trillion plan proposed by President JoeBiden’s administration would add another$1,400, for a total of $2,000.

But the February just after a new presi-dent takes up residence in the WhiteHouse brings “governing into focus,” theStrategas team writes. That could meanthat the Biden program’s high expecta-tions get scaled back. Some critics contendthat $1.9 trillion is more than needed, es-pecially if the full effects of the stimulushit the economy in the second half, just asenough Americans are vaccinated to fi-nally release the pent-up demand forgoods and services built up over nearly 1½years of curtailed activity.

Jim Paulsen, chief investment strategist atthe Leuthold Group, further contends thatthe fiscal andmonetary thrusts already aresubstantially greater than in past timeswhen joblessness was at levels similar tonow. The 11.7%U6 “under-employment”rate (which includes part-timers whowant afull-time job, plus people marginally at-tached to the labor market) is in line withthose of the recoveries that followed the1982, 1990, and 2007-09 recessions. More-over, he adds, the latest rebound has beenfar quicker.

In addition, he continues, policy ismuch more stimulative this time. Thebroad M2 money supply was growing at a25.1% annual rate in December, four timesas fast as in September 2014, when U6 wasat the current level. The fiscal deficit, at15.2% of gross domestic product, was fourtimes greater than in November 1993. Andthe 10-year Treasury yield, at 0.90% inDecember, was one-seventh the level inDecember 1986.

All this adds up to “too much cowbell,”as in the classic Saturday Night Live sketch.Paulsen says that could produce muchhigher inflation, possibly forcing the Fedand fiscal authorities to tighten policies,rekindling recession. (For another view,see Matthew Klein’s Economy column,page 21.)

The Fed, however, has stated its willing-ness to let inflation rise considerably overits 2% target to make up for previous short-falls. The projections released at the De-cember Federal Open Market Committeemeeting show a consensus calling for thefederal-funds target rate to remain near thecurrent 0% to 0.25% through 2023. So pre-

mature tightening seems unlikely.A more proximate worry for stocks

should be that, after the anticipated fiscallargess of up to $1.9 trillion from the Bidenteam, tax increases are likely for infra-structure and clean-energy initiatives.

That won’t necessarily result in a fullrepeal of the Trump tax cuts, former FedChair Janet Yellen, Biden’s Treasury Secre-tary nominee, said at her confirmationhearing on Tuesday, notes Ian Katz of Cap-ital Alpha Partners in a client note. Oncethe pandemic is no longer depressing theeconomy, Yellen said, the administrationwould propose repealing parts of the taxact “that benefited the highest-incomeAmericans and large companies.”

The Strategas research team thinks thecurrent corporate tax rate of 21% could belifted to 28%, halfway back to the 35% thatprevailed prior to the Tax Cut and Jobs Actof 2017. (For S&P 500 companies, the ef-fective rate actually fell to 17.7% in 2018from 24.4% in 2017, the researchersfound.) But, they add, it doesn’t seem thata future corporate tax hike has been dis-counted by the market, based on the rela-tive price action of stocks of more highlytaxed companies.

Very high-income investors could alsoface increased levies on dividends and capi-tal gains, the Strategas team points out. Un-der the Biden plan, capital gains and divi-dends could be taxed at a total federal rate of43.4% for those earningmore than $1 mil-lion a year. The capital-gains rate hasn’tbeen over 30% since 1978. Cap-gains rateincreases also result in fewer investors cash-ing in realized gains, they add.

The Biden proposal also would lift theeffective tax rate on dividends to 60% from40% (after taking into account the doubletaxation of payouts at the corporate andpersonal levels). Since the 2003 tax cut,which effectively lowered the effective fed-eral rate to 45% from 60%, a 25-year de-cline in the total of companies paying divi-dends has reversed.

As for stock repurchases—a more tax-efficient way to return cash to sharehold-ers—Strategas points out that Biden hasbeen critical of these since he was a sena-tor. The administration might tighten ruleson buybacks, while requiring more disclo-sure and shareholder approval.

Whatever the politics of higher taxes onwell-heeled investors, the economics sug-gests they aren’t positive for stock prices, allelse being equal. WhatWashington givethin stimulus, it might taketh in taxes. B

email: [email protected]

Up & Down Wall Street Continued

Serving our clients for over 30 years

DUE DILIGENCEBackground investigations

LITIGATION SUPPORTInternal investigations

Forensic and cyber investigations

SECURITYAssessments and travel

For further information contact:[email protected]

212-308-8500

Upgradeyour advisor.Get advice on managing your wealthand connect with a top advisor at

barrons.com/directory

©2020 DowJones & Company. All Rights Reserved. 2E205

8 BARRON’S January 25, 2021

QQQINVESCONASDAQ NEXTGEN 100 ETF

QQQINVESCONASDAQ 100 ETF

IVNQXINVESCONASDAQ 100MUTUAL FUND

Three new ways to access the growth potential of the Nasdaq;three new ways to seek growth for your clients.

NOT A DEPOSIT NOT FDIC INSURED NOT GUARANTEED BY THE BANK MAY LOSE VALUE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY

There are risks involved with investing in ETFs, including possible loss of money. ETFs are subject to risks similar to those of stocks. Investments focused in a particular sector, such as technology, are subject to greater risk, and are moregreatly impacted by market volatility, than more diversified investments. An investment cannot be made directly into any index.

BEFORE INVESTING,CONSIDERTHEFUND’SINVESTMENTOBJECTIVES,RISKS,CHARGESANDEXPENSES.VISITINVESCO.COM/FUNDPROSPECTUSFOR A PROSPECTUS CONTAINING THIS INFORMATION. READ IT CAREFULLY BEFORE INVESTING.Invesco Distributors, Inc. NA 9,595

Innovationloves company.Meet the three newmembers of theInvesco QQQ family.

January 25, 2021 BARRON’S 9

S T R E E TW I S E If there is a spoiler, it might be a comingwave ofinitial public offerings that could flood the marketwith videogame shares.

Roblox, Videogaming,And the Boom MarketIn Desperate Parents

M y bad parent-ing is aboutto get its ownstock listing.Ticker symbol:RBLX. Techni-cally, that’s for

a company called Roblox, but it’smore or less the same thing.

See, I used to be a solid B- as a dad,bribing my kids with M&Ms to doextra math drills and forcing theminto overmanaged sports leagues toburn off the calories. Then the pan-demic shut down in-person activitiesand turned my home into a daytimeturf war between the Zoom SchoolGang and the Department of HomeOffice Security. Evenings bring sweetrelief, my wife and I have discovered,so long as we allow our kids to raisethemselves as feral videogamers.Their favorite habitat is Roblox ontheir iPads.

Scold me if you must, but my familyisn’t alone. Roblox says its users in-clude two-thirds of U.S. children ages9 to 12. During the first nine monthsof 2020, the number of daily users rose82%, to 31 million. Hours played morethan doubled, to 22 billion.

That’s nothing compared withwhat happened to the company’svalue. Consider: The best-sellingvideogame property of all time is theGrand Theft Auto franchise, and itsowner, Take-Two Interactive Soft-ware (ticker: TTWO), has enjoyeda stock gain of more than 1,500%over the past decade, its recent valueat $23 billion. Roblox’s value, mean-while, has jumped to $30 billion from$4 billion over the past year, judging

by the terms of funding rounds ear-lier this month and last February.

Roblox was first launched for per-sonal computers in 2006, and is to-day played on Apple and Androidmobile devices, Xbox One gamingmachines, and Oculus Rift virtual-reality headsets. It’s not one game butrather millions of them—a “humanco-experience platform,” as the com-pany puts it. The games are made bysome seven million player-develop-ers, of whom nearly a million makemoney for their efforts. Graphics areblocky and cartoonish.

Games are free to play, but develop-ers can charge for things like a weaponthat launches eight pumpkins at once,or a “Doge hat” to give a player’s avatarthe head of a dog from a past internetmeme. Let your children onto Robloxand there will soon be incessant re-quests for the in-game currencyRobux, bought with real money. Theremight also be a sharp increase in in-stances of the littlest one trying to callyou “dude,” my field work indicates.Players can meet up in games withtheir real-world friends and commu-

nicate through a chat feature. Robloxfilters these messages for inappropri-ate content, not always thoroughly,and employs a small army of gamemonitors.

The company had planned aninitial public offering last year, butdelayed it, and then announced thismonth that it would instead pursuea direct listing, whereby companiesbegin trading but don’t issue newshares or raise money. The stockcould begin trading next month.

Roblox isn’t yet profitable, in partbecause it recognizes revenue fromin-game purchases little by little overthe gaming lives of its users. Revenuerose 68%, to $589 million, in the firstnine months of last year. Bookings,a simpler measure of money comingin, jumped 171%, to $1.24 billion.

MKM Partners analyst Eric Han-dler estimates that Roblox has re-cently been averaging $100 million infree cash flow a quarter. Assume thatfigure could quickly double and youcan make a case for Roblox’s valuationresembling that of Take-Two, the pric-iest of the legacy videogame makers,at 39 times projected free cash flow.Activision Blizzard (ATVI) trades at29 times and Electronic Arts (EA),23 times. All three stocks soared lastyear, as time playing videogames ex-ploded.

And it’s not just kids. Adults 45to 54 increased their game time by59% last year, according to the NPDGroup, a market researcher. Spend-ing rose faster. Last year, the globalvideogame business took in an esti-mated $180 billion. That’s about $80billion more than the movie businessat its peak.

Could now be as good as it gets forinvestors? “What’s so fascinatingabout this fiscal year for us, as greatas it has been...is it is still a very lightrelease year,” Take-Two CEO StraussZelnick told me this past week. “Thebulk of the titles that made up theyear existed previously, and havebeen ongoing consumer experiences.”Over the next five years, he expects torelease more than 90 new titles,which he says is double the pipelinethat Take-Two had a few years ago.

M KM’s Handler likes Ac-tivision Blizzard for itspromising release calen-dar, including Call of

Duty: Mobile, which came out inChina on Christmas. He says it couldbe a $500 million to $600 milliongame this year. He also likes Elec-tronic Arts for its recent acquisitionof Codemasters, which makes racinggames that haven’t yet added muchrecurring revenue from in-gameservices.

If there is a spoiler, it might be acoming wave of initial public offer-ings, which will generate excitementbut could also flood the market withvideogame shares. Playtika Holding(PLTK), a maker of casual casino-type games, came public earlier thismonth, and was recently valued atclose to $13 billion. Beyond Roblox,candidates for going public this yearinclude mobile game makers App-Lovin and Scopely, which couldbe valued at several billion dollarsapiece, and Epic Games, maker of theshoot-’em-up blockbuster Fortnite,which was valued in an August fund-ing round at more than $17 billion.

That should give bulls pause. Also,the long-term outlook for videogam-ing is bright—but near term, oncegroup activities resume, I might haveto start parenting again. That willmean switching my kids from Robloxto their previous human co-experi-ence platforms, like Little League,which has a chat feature called yell-ing stuff, and where players can altertheir in-game appearance for free bysliding in dirt. B

email: [email protected]

Barron’s StreetwiseIn a weekly podcast by Barron’s, columnist Jack Hough looks

at the companies, people, and trends you should be watching.

This is Wall Street like you’ve never heard before. Subscribe

to Barron’s Streetwise on Spotify, Apple Podcasts,

or your favorite listening app.

BARRONS.COM/PODCASTS

By Jack Hough

10 BARRON’S January 25, 2021

R E V I EW 30,996.98Dow Industrials: +182.72

511.02Dow Global Index: +7.87

1.09%10-year treasury note: -0.01

PROSPECTS FOR STELLANTIS

Inauguration HighsU.S. markets were closed for MartinLuther King’s Birthday, but stocks rosearound the world.With earnings roll-ing out in earnest, U.S. indexes hit newhighs as the new president was (peace-fully) sworn in. The rally was fueled byhopes for a jumbo relief measure andby huge numbers fromNetflix. TheDow and S&P 500 slipped on Friday,weighed down by concerns about oldtech: IBM and Intel. On the week, theDow industrials edged up 0.6%, to30,996.98; the S&P 500 rose 1.9%, to3841.47; and the Nasdaq Compositegained 4.2%, to 13,543.06.

TransitionsFormer President Trump left theWhite House and flew to Mar-a-Lago,the first outgoing president to refuseto greet his successor in 150 years.Security in Washington, D.C., wastight as President Biden was sworn in,speaking of unity and civility. Law-en-forcement officials continued toround up suspects alleged to haveparticipated in the Capitol riot. Fewthreats, however, materialized againststate capitols or Washington, D.C.

Biden: First MovesBiden signed a stack of executiveorders on Day One, and kept on sign-ing, targeting dozens of Trump poli-cies: killing the Muslim ban, rejoiningthe Paris climate accord andWorldHealth Organization, canceling theKeystone XL pipeline, and seeking toreunite children separated at the bor-der. He also outlined big initiatives—further Covid relief, steps to boost theeconomy, and immigration reform—and liberated Dr. Anthony Fauci.

Pardons and ImpeachmentsTrump signed 143 pardons and com-mutations before exiting, including forformer adviser Steve Bannon, GOPdonor Elliott Broidy, singer Lil Wayne,convicted Republican officials, andothers. Not on the list were his chil-dren, anyone involved in the Capitolriot, lawyer Rudolph Giuliani, or him-self. In Congress, GOP Leader MitchMcConnell said Trump “provoked” theCapitol riot, while the House said itwould send an impeachment article to

Old BrandsOn Tesla TurfPoof—and a giant auto company emerges. It’s mysteri-ously called Stellantis, and it’s the product of Fiat Chrys-ler’s merger with Peugeot. Stellantis is, by marriage, one ofthe once-dominant Detroit Three auto makers, withGen-eralMotors and FordMotor.

A lot has changed since the D-3 ruled. Chryslermerged, demerged, merged again. General Motors wentbankrupt in the financial crisis. Today, electric-vehiclestart-upTesla is the world’s most valuable auto maker.Tesla has been around for 17 years, but compared withthe D-3, it’s a pup. Tesla shipped some 500,000 vehiclesin 2020, Stellantis eight million, making it the third- orfourth-largest auto maker on the planet. Volumes fell formost car makers in 2020—but not for Tesla.

Still, the stock looks promising. J.P. Morgan’s Jose Asu-mendi began covering Stellantis last week with a Buy andan 18 euro ($21.90) price target. That’s a 35% implied gainon the current $16.15. He believes the two legacy firmscomplement each other. Fiat lost money in Europe; Peu-geot will help with that. Peugeot wasn’t a big player inNorth America; Chrysler is. He says the larger entity cancut costs and streamline capital spending, eventually pro-ducing annual savings in excess of €5 billion.

About 70% of analysts covering the stock rate it Buy.The average Buy ratio for Dow Jones Industrial stocks is57%. Stellantis is down 11%, year to date, in contrast toGM, up 33%, and Ford, up 31%. Investors are starting tovalue those companies’ autonomous and EV investmentsmore highly.With the merger closed, Stellantis shouldstart talking about its EV plans. —Al Root

25%Percentage of Americans livingin their home for more than 20years, a figure that’s been risingsteadily. Average stay: 13 years.

100.1%U.S. debt, at $21.6 trillion, togross domestic product at theend of 2020.

37 MNumber of new Netflix sub-scribers in 2020, a record, for atotal of 204 million at year-end.

$82 BAmount raised by special-pur-pose acquisition companies in2020, more than all other years’combined.

To get Numbers by Barron’sdaily, sign up whereveryou listen to podcasts or atBarrons.com/podcasts

THE NUMBERS

HE SAID

“We’re in anational emergency,and it’s time wetreated it like one.”President JoeBiden in announcinghis pandemic-responseplan

the Senate onMonday.

The 100-Day Vaccine GoalBiden has set as a goal 100million vacci-nations in the first 100 days. The head oftheWorld Health Organization warned ofa “catastrophic moral failure” as poorernations struggle to get vaccines. Mean-while, the U.S. death toll breached400,000, and some 900,000workersfiled for unemployment.

Navalny Returns to JailRussian dissident Alexei Navalny wasarrested when he and his wife flew fromGermany to Russia after recovering froman assassination attempt by poisoning.The arrest spurred international de-mands to release him and Navalny urgedsupporters to take to the streets.

Annals of Deal-MakingOptical components maker LumentumHoldings agreed to buy laser maker Co-herent for $5.7 billion….MytheresaGroup, the Munich-based luxury e-com-merce company and former NeimanMarcus subsidiary, went public, valuedat $2.2 billion. Mytheresa had been sub-ject of a creditor dispute after a spinoffand Neiman’s bankruptcy. Ill

ustrationbyElia

sSte

in;PatrickSemansky/P

ool/G

ettyIm

ages

January 25, 2021 BARRON’S 11

P R E V I EW

SPIRALING CONTAINER COSTS

Sign up for the Review &Preview daily newsletter atBarrons.com/reviewpreview

Monday 1/25Kimberly-Clark and Philips reportquarterly results.

The Federal Reserve Bank of Chi-cago releases its National Activity in-dex for December. Consensus estimateis for a 0.10 reading, below December’s0.27 figure. The recent data for theindex suggest a slightly above-averagegrowth rate for the economy after apowerful third-quarter rebound.

Tuesday 1/263M,Advanced Micro Devices,American Express, Capital OneFinancial, General Electric, In-vesco, Johnson & Johnson, Lock-heed Martin,Microsoft, Prologis,Raytheon Technologies, Star-bucks, Texas Instruments, and Ve-rizon Communications announceearnings.

The Conference Board releases itsConsumer Confidence index for Janu-ary. Economists forecast a 91.6 read-ing, three points more than in Decem-ber. Consumer confidence remainswell below prepandemic levels.

Wednesday 1/27Abbott Laboratories,Anthem,AT&T, Boeing, Crown Castle Inter-national,General Dynamics, LamResearch,Norfolk Southern, Ser-viceNow, and Stryker report quar-terly results.

The Federal OpenMarket Commit-tee announces its monetary-policydecision. The central bank is all butassured to keep the federal-funds rateunchanged at near zero. ButWallStreet is interested to learn if andwhen the Fed will consider paring itsbond purchases, currently at $120billion a month.

The Census Bureau releases thedurable goods report for December.New orders for manufactured durablegoods are expected to rise 0.8%month

over month to $246 billion.

Thursday 1/28Altria Group,American AirlinesGroup, Comcast,Danaher,Dow,Mastercard,McDonald’s,MondelezInternational,MSCI,NorthropGrumman, Southwest Airlines,T. Rowe Price Group, andVisaannounce earnings.

The Bureau of EconomicAnalysisreports its advance estimate for fourth-quarter gross domestic product. Con-sensus estimate is for the economy tohave grown at a seasonally adjustedannual rate of 4.3%, after a record paceof 33.4% in the third quarter.

Friday 1/29Caterpillar, Charter Communica-tions, Chevron, Colgate-Palmolive,Eli Lilly, andHoneywell Interna-tional host conference calls to discussquarterly results.

The BEA reports personal incomeand spending data for December. Econ-omists forecast both personal incomeand expenditures to tick down 0.1%month over month. In November, in-come fell 1.1%; spending declined 0.4%.

Coming EarningsConsensusEstimate Yearago

M

AGNC Investment (Q4) $2.58 $0.48

T

3M (Q4) 2.15 1.95

AdvancedMicroDevices (Q4) 0.47 0.32

AlaskaAir (Q4) -2.86 1.46

AmericanExpress (Q4) 1.30 2.03

C.H.RobinsonWorldwide (Q4) 0.97 0.73

MoreEarningsonPageM36.

Consensus EstimateDay ConsensusEst LastPeriod

T JanuaryConsumerConfidence 89.2 88.6

TH Q4GDP 4.3% 33.4%

DecemberWholesale Inventories 0.20% 0.0%

DecemberNewHomeSales 850,000 841,000

F DecemberPersonal Income 0.00% -1.1%

JanuaryMichiganSentiment - f 79.2 79.2

Unlessotherwise indicated, timesareEastern. a-Advanced;f-Final; p-Preliminary; r-Revised Source: FactSet

Formore informationabout comingeconomic reports- andwhat theymean - go toBarron’s freeEconomicCalendar atwww.barrons.com

Half of the six largest U.S. companies bymarket cap report results. Apple, Facebook,

and Tesla will also host calls to discuss their earnings after the market close.

Wednesday

Will ShippingFuel Inflation?Locked-down consumers are spending more on goods—mostly made overseas and transported on container ships—than on services. That, plus pandemic-related shipping dis-ruptions, have sent costs spiraling. The Baltic Dry Index, ameasure of rates to move dry goods, is up 128% in a year andnearly 60% since early December, boosted by China, theworld’s largest exporter, reopening its industrial economy.

That has been a boon for shipping lines, which have seenprofit margins widen. Shares ofMaersk and Cosco Ship-ping Holdings are up 92% and 195%, respectively, over thepast year, andTriton International, the world’s largestlessor of containers, has seen a 36.5% total return in a year.

Normally, higher shipping costs mean higher retail pricesand inflation. Bond yields have risen to price in higher infla-tion since the fall. But shipping is unlikely to ignite cost-push inflation. “First, the increase in shipping costs is likelyto be partially absorbed within wholesale and retail mar-gins,” writes Capital Economics group chief economist NeilShearing. “Second, while it’s difficult to be precise, the mostaffected goods are likely to account for a relatively smallshare of the overall [consumer price index] basket.”

Shearing estimates shipping costs at only 5% of retailprices. So, the past eight months’ doubling has added onlyabout that much to the cost of goods, with consumers proba-bly seeing only some of that. Aweaker dollar also offsetshigher shipping costs for non-U.S .importers. Then there’sthe upcoming Chinese NewYear, when factories shut downand exports fall. That could ease upward pressure on rates.The biggest relief? An end to the pandemic, with consumersspending again on services. —Nicholas Jasinski

Carrying TradeBig global shippers have prosperedas trade in goods has surged andshipping rates have followed.

Sources: FactSet; Bloomberg

High TideShipping rates fell as Covid emerged,then more than doubled as trade andChina recovered.

Cosco Shipping HoldingsA.P. Moeller-MaerskSeries ATriton Holding

Feb. 2020 ’21

-100

0

100

200

300%

Maersk, Cosco Holdings,Triton Holdings, Last 12 Months

Baltic Exchange Dry Index,Last 12 months

Feb. 2020 ’21

0

500

1000

1500

2000

IllustrationbyElia

sSte

in

12 BARRON’S January 25, 2021

F O L L OW - U P While China policy may be less volatile, investorsshould brace for continued complexities based ona changing relationship between the two nations.

Expect Biden to TakeTough Stance on China

Exchange to delist some of the stocks,including telecoms like China Mobile(ticker: 941.Hong Kong). Though in-vestors have until November to divest,many have already struggled to selltheir shares.

Adding to the uncertainty, the Chi-nese telecoms on Friday asked theNYSE to reconsider the delisting. Asthe new administration reviews recentTrump administration orders, it couldrein in some provisions or removecompanies from the list if they decidethe rationale to ban them was weak.

More broadly, the Biden China ap-proach is likely to be clearer, more mul-tilateral, and less ad-hoc. The selectionof Kurt Campbell, the top Asia diplo-mat in the Obama administration, for anew role as Indo-Pacific coordinatorsignals that the new team is thinkingabout more coherent policies, bothdomestically and among U.S. allies,that would have a better chance to sur-vive, says Scott Kennedy, senior advi-sor and trustee chair in Chinese Busi-ness and Economics at the Center forStrategic and International Studies.

Delisting threats could persist, butfund managers still see a chance U.S.

and Chinese regulators may compro-mise on legislation delisting Chinesecompanies if they fail to comply withU.S. audit rules within three years.

Another reason for investor cau-tion: The State Department on Tues-day just before Biden took office de-termined that China had committed“genocide and crimes against human-ity,” against the Uighurs, a Muslimminority group in Xianjiang prov-ince—a view shared by Secretary ofState nominee Anthony Blinken.

That may pave the way for sanc-tions or technology restrictions. Con-gress may also reintroduce a bill put-ting the burden on companies toprove no connection to goods made by

As President Joe Biden fillsChina-related positions in hisadministration, investors ex-pect a continued tough stance

against the country, especially on hu-man rights issues, along with a reviewof recent Trump administration exec-utive orders.

While policy may be less volatile,investors should brace for continuedcomplexities as they adjust portfoliosbased on a changing relationship be-tween the two countries.

Cabinet nominees in confirmationhearings made clear that the relation-ship with China would continue to bea major focus, with Janet Yellen, nomi-nated for Treasury Secretary, empha-sizing a willingness to use an array oftools to address what the former Fed-eral Reserve chair described asChina’s abusive and illegal practices.

But fund managers still favorChina, despite confusion around aNovember executive order banningU.S. investment in companies the Pen-tagon says have ties to the Chinesemilitary. That led the New York Stock

By RESHMA KAPADIA

New voices on China: President Biden, Kurt Campbell, left, and Anthony Blinken.

forced labor in Xianjiang, says AnnaAshton, vice president of governmentaffairs for the U.S.-China BusinessCouncil

For now, fund managers are hedg-ing their bets. “We don’t expect Bidento be soft on China, but we think wewill have a situation where it will be amore multilateral approach that willtake down the volatility and reducethe equity risk premium,” says JoanneIrving, co-manager of the $5.3 billionAberdeen Emerging Markets fund(ABEMX), which is overweightChina, but has favored Hong Konglistings over American depositaryreceipts when making new pur-chases. B P

hoto

IllustrationbyNicole

Fara

Silv

er;

refe

renceGetty(3

)

Risks: Mutual fund investing involves risk. Principal loss is possible. The funds invest in foreign securities, which involve greater volatility and political, economic and currency risks and differences in accounting methods.Each fund seeks long-term capital appreciation and current income.Each fund’s investment objectives, risk charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtainedby calling 877-485-8586. Read the prospectus carefully before investing.Distributed by ALPS Distributors, INC.

For further information, please contact 212.644.1800, [email protected] or visit www.cullenfunds.com

CHDVXCULLEN HIGH DIV IDEND EQUITY FUND

January 25, 2021 BARRON’S 13

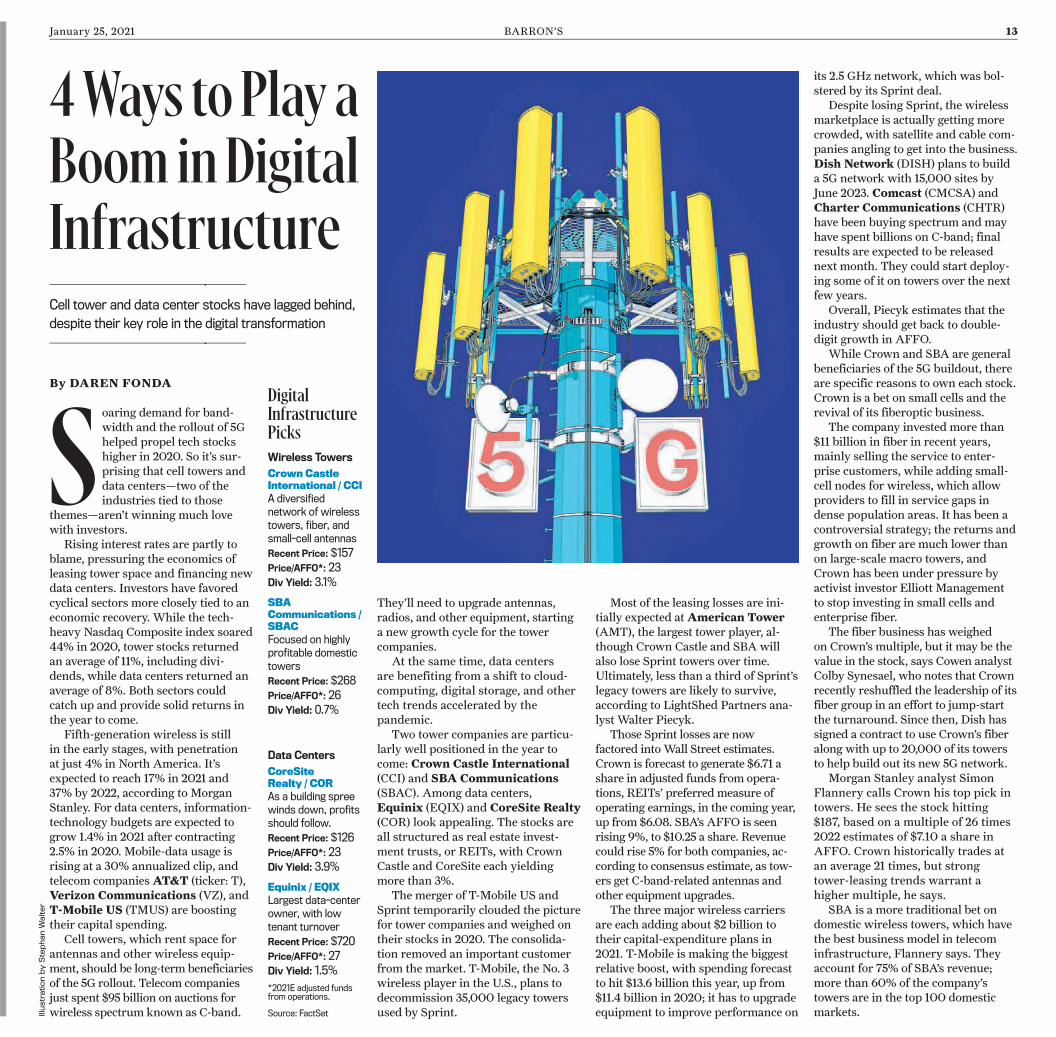

They’ll need to upgrade antennas,radios, and other equipment, startinga new growth cycle for the towercompanies.

At the same time, data centersare benefiting from a shift to cloud-computing, digital storage, and othertech trends accelerated by thepandemic.

Two tower companies are particu-larly well positioned in the year tocome: Crown Castle International(CCI) and SBA Communications(SBAC). Among data centers,Equinix (EQIX) and CoreSite Realty(COR) look appealing. The stocks areall structured as real estate invest-ment trusts, or REITs, with CrownCastle and CoreSite each yieldingmore than 3%.

The merger of T-Mobile US andSprint temporarily clouded the picturefor tower companies and weighed ontheir stocks in 2020. The consolida-tion removed an important customerfrom the market. T-Mobile, the No. 3wireless player in the U.S., plans todecommission 35,000 legacy towersused by Sprint.

Most of the leasing losses are ini-tially expected atAmerican Tower(AMT), the largest tower player, al-though Crown Castle and SBA willalso lose Sprint towers over time.Ultimately, less than a third of Sprint’slegacy towers are likely to survive,according to LightShed Partners ana-lyst Walter Piecyk.

Those Sprint losses are nowfactored intoWall Street estimates.Crown is forecast to generate $6.71 ashare in adjusted funds from opera-tions, REITs’ preferred measure ofoperating earnings, in the coming year,up from $6.08. SBA’s AFFO is seenrising 9%, to $10.25 a share. Revenuecould rise 5% for both companies, ac-cording to consensus estimate, as tow-ers get C-band-related antennas andother equipment upgrades.

The three major wireless carriersare each adding about $2 billion totheir capital-expenditure plans in2021. T-Mobile is making the biggestrelative boost, with spending forecastto hit $13.6 billion this year, up from$11.4 billion in 2020; it has to upgradeequipment to improve performance on

its 2.5 GHz network, which was bol-stered by its Sprint deal.

Despite losing Sprint, the wirelessmarketplace is actually getting morecrowded, with satellite and cable com-panies angling to get into the business.Dish Network (DISH) plans to builda 5G network with 15,000 sites byJune 2023. Comcast (CMCSA) andCharter Communications (CHTR)have been buying spectrum and mayhave spent billions on C-band; finalresults are expected to be releasednext month. They could start deploy-ing some of it on towers over the nextfew years.

Overall, Piecyk estimates that theindustry should get back to double-digit growth in AFFO.

While Crown and SBA are generalbeneficiaries of the 5G buildout, thereare specific reasons to own each stock.Crown is a bet on small cells and therevival of its fiberoptic business.

The company invested more than$11 billion in fiber in recent years,mainly selling the service to enter-prise customers, while adding small-cell nodes for wireless, which allowproviders to fill in service gaps indense population areas. It has been acontroversial strategy; the returns andgrowth on fiber are much lower thanon large-scale macro towers, andCrown has been under pressure byactivist investor Elliott Managementto stop investing in small cells andenterprise fiber.

The fiber business has weighedon Crown’s multiple, but it may be thevalue in the stock, says Cowen analystColby Synesael, who notes that Crownrecently reshuffled the leadership of itsfiber group in an effort to jump-startthe turnaround. Since then, Dish hassigned a contract to use Crown’s fiberalong with up to 20,000 of its towersto help build out its new 5G network.

Morgan Stanley analyst SimonFlannery calls Crown his top pick intowers. He sees the stock hitting$187, based on a multiple of 26 times2022 estimates of $7.10 a share inAFFO. Crown historically trades atan average 21 times, but strongtower-leasing trends warrant ahigher multiple, he says.

SBA is a more traditional bet ondomestic wireless towers, which havethe best business model in telecominfrastructure, Flannery says. Theyaccount for 75% of SBA’s revenue;more than 60% of the company’stowers are in the top 100 domesticmarkets.

4Ways to Play aBoom inDigitalInfrastructureCell tower and data center stocks have lagged behind,despite their key role in the digital transformation

Soaring demand for band-width and the rollout of 5Ghelped propel tech stockshigher in 2020. So it’s sur-prising that cell towers anddata centers—two of theindustries tied to those

themes—aren’t winning much lovewith investors.

Rising interest rates are partly toblame, pressuring the economics ofleasing tower space and financing newdata centers. Investors have favoredcyclical sectors more closely tied to aneconomic recovery. While the tech-heavy Nasdaq Composite index soared44% in 2020, tower stocks returnedan average of 11%, including divi-dends, while data centers returned anaverage of 8%. Both sectors couldcatch up and provide solid returns inthe year to come.

Fifth-generation wireless is stillin the early stages, with penetrationat just 4% in North America. It’sexpected to reach 17% in 2021 and37% by 2022, according to MorganStanley. For data centers, information-technology budgets are expected togrow 1.4% in 2021 after contracting2.5% in 2020. Mobile-data usage isrising at a 30% annualized clip, andtelecom companiesAT&T (ticker: T),Verizon Communications (VZ), andT-Mobile US (TMUS) are boostingtheir capital spending.

Cell towers, which rent space forantennas and other wireless equip-ment, should be long-term beneficiariesof the 5G rollout. Telecom companiesjust spent $95 billion on auctions forwireless spectrum known as C-band.

By DAREN FONDADigitalInfrastructurePicksWireless Towers

Crown CastleInternational / CCIA diversifiednetwork of wirelesstowers, fiber, andsmall-cell antennasRecent Price: $157Price/AFFO*: 23Div Yield: 3.1%

SBACommunications /SBACFocused on highlyprofitable domestictowersRecent Price: $268Price/AFFO*: 26Div Yield: 0.7%

Data Centers

CoreSiteRealty / CORAs a building spreewinds down, profitsshould follow.Recent Price: $126Price/AFFO*: 23Div Yield: 3.9%

Equinix / EQIXLargest data-centerowner, with lowtenant turnoverRecent Price: $720Price/AFFO*: 27Div Yield: 1.5%

*2021E adjusted fundsfrom operations.

Source: FactSetIllustrationbySte

phanWalter

w013_p2bw

025000_0_w01300_1________xa2021_w

-opt_01.pdf1

23-Jan-21 08:11:26

14 BARRON’S January 25, 2021

The C-band auctions should be a “signif-icant driver” of leasing in the second halfof 2021, Brendan Cavanagh, SBA’s chieffinancial officer, recently told investors.

“U.S. towers are the gold standard, andSBA has the most exposure to the busi-ness,” says MoffettNathanson analyst NickDel Deo, who calls SBA his top tower pick.He expects the stock to hit $320 in the next12 months, from a recent $272.

While tower companies are poised tobenefit from our ever-growing wirelessconnectivity, data centers are the facilita-tors of our addiction to data. Tech trendssuch as cloud computing, outsourcing ofcorporate servers, and increased demandfor data analytics are driving demand.

Cloud capex is expected to grow 16%in the first half of the year and 10% in thesecond half, according to Morgan Stanley.

CoreSite has actually missed potentialbusiness in recent years as the companyran short of inventory. But it’s now comingoff a building spree in core markets such asthe San Francisco Bay Area, Northern Vir-ginia, and Los Angeles. AFFO growth isexpected to jump from 5.4% this year to7.3% in 2022.

“They generate the best returns on in-vested capital, but the stock trades in linewith the group,” Del Deo says. At a recent$126, CoreSite trades at 23 times AFFOestimates for 2021. Del Deo has a pricetarget of $142 on the stock.

Equinix trades at a premium to CoreSite,at 27 times Wall Street’s estimate for 2021AFFO—but it’s the largest and arguablybest-positioned data-center owner. Tenantturnover is low, and the company’s globalportfolio of facilities in urban areas can’tbe easily replicated. Equinix has a largedevelopment pipeline, including expansionplans in India, and it has built strategicalliances with several tech giants, includingMicrosoft (MSFT),Amazon.com(AMZN), and Cisco Systems (CSCO).

Credit Suisse analyst Sami Badri hasOutperform ratings on Equinix and Core-Site. “Both companies have built highlyconnected ecosystems that offer key advan-tages to their customers versus other datacenters,” he says.

Badri has a $915 target on Equinix, nearthe top of Wall Street estimates. That maybe a stretch, and would require the stock toexpand its already premium multiple. Butearnings growth alone could drive gains inthe year to come. At a consistent 27 timesAFFO, the stock could hit $800 in a year,an 11% gain.

Towers and data centers may be thesleepy part of the technology market. Butthey could also be the least volatile part oftech in the coming year. In 2021, it’s worthpaying up for some stability. B

HOW DO YOU MANAGERISK WHEN THE WORLD IS

UPS IDE DOWN?

We can't control what's next, but we can help navigate it. CME Group provides 24-houraccess to trading opportunities in every investable asset class, allowing market participantsworldwide to manage risk and capture opportunities. For every economic twist and turn,when the new normal is anything but… CME Group.

V IS IT CMEGROUP.COM/ACT ION

Derivatives are not suitable for all investors and involve the risk of losing more than the amount originally deposited and any profit you might have made. Thiscommunication is not a recommendation or offer to buy, sell or retain any specific investment or service. Copyright © 2020 CME Group Inc. All rights reserved.

January 25, 2021 BARRON’S 15

lot on a muffler or rearviewmirror.The stock dropped 1.3% last year as

Covid-19 led to fewer miles driven formany people—meaning less wear andtear on vehicles and fewer accidents,causing scrap-metal prices to increase.

But most of LKQ’s problems havebeen self-inflicted. For years, LKQwas a consolidation story, snappingup smaller players and building adominant business, both in the U.S.and Europe. Yet the synergies thatshould have resulted from thisacquisition binge never emerged. Thecompany’s operating margins declinedeach year from 2015 to 2019, andexpenses were higher than theyshould have been. Covid-19 has forcedLKQ to get leaner—and that couldallow the stock to benefit from thereopening of the economy in 2021.

“LKQ, like a lot of other companies,realized that they can do more withless” during the pandemic, says JoshWein, a portfolio manager at HennessyFunds, which bought the stock inOctober. “Companies use it as anexcuse to do what they should havedone anyway—get rid of some fat.”

Disappointment has been the nameof the game for LKQ in recent years.The stock has been range-bound atabout $20 to $43 since late 2012 asmetrics such as return on assets andreturn on equity fell and debt rose. Ithas become easy to doubt an LKQturnaround. “We’ve owned the stocksince 2014, and it has been a perennialdisappointment,” says Lamar Villere,partner and portfolio manager atVillere & Co., which recently sold thestock. “The problem is, it’s six yearslater and [things are] moving moreslowly than hoped.”

S till, 2021 might be the year thatLKQ finally lives up to thepromises it made. The stock hasalready gained more than 6%

this year, putting it on course to finallybreak out of its trading range.

The company has reduced oper-ating expenses by about 6% in thefirst nine months of 2020, and LKQ’sstreamlined operations mean thatmargins are also a major focus. Bothnet margins and earnings beforeinterest and taxes, or Ebit, at 4.3% and7.8%, respectively, were lower in 2019than they were five years prior. Yetanalysts expect these to improve in2020, to 6.2% and 9%, both above thecompany’s five-year average.

Moreover, after years of mergersand acquisitions, LKQ has pulled backfromM&A, unlocking free cash flowand allowing the company to paydown debt and repurchase stock.Analysts expect that net debt will fallsome $600 million in 2021 to $3.5billion, on free cash flow of $859million, roughly double the levels itsaw from 2015 to 2018.

“LKQ is in the early-to-middleinnings of a multiyear plan, and theimprovement in profitability, coupledwith a return to [sales] growth nextyear, should drive multiple expan-sion,” says Stephens analyst DanielImbro, who points to the recent stringof better-than-expected earningsreports from the company.

Consensus estimates call for LKQ’searnings per share to have edged upjust 2.5% year over year in 2020 to$2.43, with revenue dipping 7.5%, to

$11.56 billion. Yet 2021 looks brighter,with earnings per share expected tojump 13% to a record $2.7forced ittoget leaner 5 on a 5.8% rise in sales to$12.22 billion.

Despite the positive outlook, LKQ’sprice/earnings ratio fell from about 20times at the beginning of 2020 to 14.5times at the end of the year, at a timewhen the S&P 500’s multiple rosefrom roughly 21 times to 31 times. Thegood news is that the low expectationsembedded in the multiple could workin LKQ’s favor, especially if it managesto right its European division.

The stock is cheap: At 13.7 times2021 earnings, it’s trading below itsfive-year average of 14.4 times, andbelow the P/E of peers like GenuineParts (GPC) andO’Reilly Auto-motive (ORLY), whose multiples arein the high teens, and Copart (CPRT)and Fastenal (FAST), which changehands for more than 30 times thisyear’s earnings.

“As execution improves, you’regoing to see the multiple recover,” saysImbro. He has a $44 price target onLKQ stock, up 17% fromWednesday’sclose of $37.60.

None of this takes into account theeconomic factors that should helpLKQ in 2021. The pandemic will end,and the reopening will unleash pent-up demand from motorists eager totravel again. And Americans, stilldealing with an uncertain economicoutlook, could be motivated to fix,rather than replace, damaged cars.

If 2020 taught us anything, it’s toexpect the unexpected. That includesa longtime lemon finally moving intothe fast lane. B

Auto-Parts SupplierLKQGets Into GearThe company spent years and took on a lot of debt trying to consolidate the

business. Then the pandemic forced it to get leaner and more profitable.

“LKQ, like alot of othercompanies,realizedthat theycan domorewith less”during thepandemic.Josh Wein,Hennessy Funds

Auto-parts supplier LKQhas been stuck in neutralfor years, but 2021 couldsee things turn around forthe company as thepandemic forces it to takesteps that some say it

should have taken long ago.Although LKQ (ticker: LKQ)

distributes car parts, don’t think of it asanotherAdvance Auto Parts (AAP)orAutoZone (AZO). The company,which takes its name from “like, kind,and quality,” the three criteria thatinsurers require for vehiclereplacement parts, buys used cars andwrecks, salvages them for reusableparts, and scraps the rest. It’s whereyou go when you don’t want to spend a

By TERESA RIVAS

IllustrationbyBenMounsey-W

ood

Shifting GearsLKQ stock could be ready to pick upthe pace.

Source: FactSet

40%

20

0

-20

-40

-60

-80

Feb. 2020 ’21

S&P 500LKQ Corp.

16 BARRON’S January 25, 2021

end of the year, versus 20.4% for thebenchmarks they are tracked against.It was the second straight year that webeat the benchmarks, after a three-year drought.

That said, Barron’s didn’t do aswell with its bearish picks. On aver-age, those rose more than their bench-marks, meaning that investors whoavoided stocks based on our reportingmight have missed out on gains—or ifthey shorted the stocks, they mighthave lost money.

Barron’s tracks the performance ofstock picks every year in an attempt ataccountability. It’s an imperfect pro-

cess, but one that hopefully showswhere we have succeeded and wherewe can improve. We track only articlesthat chose three stocks or fewer, sothat larger sector bets aren’t part ofthe tally. And the stocks chosen incolumns like Tech Trader aren’tincluded, either.

If Barron’swriters change theiropinion on a stock in a follow-up, thegain or loss is locked in on the date ofthe follow-up, similar to when an in-vestor decides to liquidate a position.As for benchmarks, we track large-caps against the S&P 500, mid-capsagainst the S&PMidCap 400, andsmall-caps against the Russell 2000.

Although wemissedTesla (ticker:TSLA), which rose 743% in 2020, Bar-ron’s found some special situations thatpaid off handsomely for investors.

In April, Andrew Bary wrote aboutthe two companies that had spun offfrom United Technologies—CarrierGlobal (CARR) andOtisWorldwide(OTIS)—and the company thatemerged from the merger, RaytheonTechnologies (RTX). The first two ofthose stocks had enormous gainsthrough the end of the year. Carrier,which makes air-conditioning andheating systems, returned 177%through the end of the year. Its prod-ucts have become crucial for trans-porting the Covid-19 vaccine producedby Pfizer (PFE) and BioNTech(BNTX), which must be kept inextremely cold temperatures.

Otis, an elevator maker, has prof-ited from the success of its servicesbusiness, which accounts for about80% of earnings. Its stock has re-turned 48%.

Boyd Gaming (BYD) more thandoubled after Barron’s recommendedthe gambling stock in May. With casi-nos closed, the stock had tumbled inthe weeks before, but Lawrence C.Strauss predicted that Boyd wouldrebound because a lot of its profitscome from regional casinos thatwould attract people who might notwant to get on a plane.

Tech stocks drove much of lastyear’s rally, and they helped our re-sults, as well. Sales atAmazon.com(AMZN) boomed as Americansbought more online instead of goinginto stores. We had recommended iteven before the pandemic began todevastate bricks-and-mortar retailers.Shares rose 74% after Jack Hough’sJanuary call.

Another winner wasTwitter(TWTR), which had fallen 3% over

the prior year when Bill Alpert wroteabout it in a June cover story. Twitterwas in a battle with President DonaldTrump at the time over warning labelson his tweets regarding factual accu-racy and violence. It has since barredTrump entirely. But the company’simproving ad services and its ability todominate conversation have kept itrelevant and helped propel the stock to55% gains through the end of the year.

Other picks didn’t do as well.FirstCash (FCFS), the nation’s largestoperator of pawnshops, tends to dowell during recessions, but the latestone was an exception—the corona-virus downturn was bad for just aboutevery retail business. An evictionmoratorium, meanwhile, meant thatpeople could delay selling off posses-sions at pawnshops.

Another pick, Bank of America(BAC), slumped as low interest rateshurt returns. That said, Bank ofAmerica is already up 5% this year, aslong-term interest rates have trendedhigher and banks are back in favor.

Our bearish picks performedpoorly—or rather they did too well,on average. It was the first time in thepast six years that our bearish picksrose more than their benchmarks, onaverage. They returned some 80%,even as their benchmarks returned27%. One problem might have beenthat there were just seven negativecalls last year.

Of those, two did correctly warninvestors about coming turbulence. AChinese electric-auto maker namedKandi Technologies Group (KNDI)lost 51% after we pointed out the chal-lenges that the company faces in get-ting Americans to buy its cars.

AndNikola (NKLA) fell as doubtsgrew about the highflying electric-truck company’s prospects. FounderTrevor Milton resigned in September.

Negative Barron’s pieces on otherstocks—some of them also richlyvalued—didn’t come to fruition duringthe year. Plug Power (PLUG), whichdevelops hydrogen fuel-cell systems,kept rising after our skeptical Julyarticle, and it has kept rocketinghigher, nearly doubling since the startof this year. That is despite the com-pany still being unprofitable.

A skeptical take on online used-cardealer Carvana (CVNA) also hasn’tpanned out. Carvana rose as Ameri-cans went online to buy cars amid thepandemic. That success hasn’t yetturned into profits, but investors areclearly optimistic about the future. B