RESULTS REVIEW 1QFY15 13 AUG 2014 GAIL NEUTRAL Tough times GAIL reported all round weak results and adj EBITDA was at Rs 14.8bn (-27% YoY). Lower adj gas transmission tariff (Rs 0.9/scm, -41%), drop in adj gas trading margins (Rs 0.2/scm, -42%), oil UR sharing (Rs 5bn, -27%) and higher LNG usage led to dismal performance. APAT was Rs 9.2bn (-29% YoY). There are multiple negative triggers lined up for GAIL (1) Spot LNG prices are trading below LT prices, hence trading margins will remain weak (2) Tariff revision for Vadodara pipelines is due, we believe that there will be further retrospective hit (3) GAIL will be made to share oil UR of ~Rs 5bn in Q2, we believe the same will stop only after the gas price hike (4) Increase in gas prices from H2 will impact petchem/LPG margins (5) Capitalisation of petchem Pata-II (~Rs 81bn 4QFY15) will increase depreciation/interest cost, whereas returns will be muted due to higher gas cost. Our SOTP target for GAIL is Rs 418/sh (~6.4x FY16E EV/EBITDA and Rs 106/sh from investments). Maintain NEUTRAL. 1QFY15 highlights Natural gas transmission : Volumes 97mmscmd (-2% YoY), reported tariff Rs 0.66/scm (-58%) due to non recognised revenues of Rs 2.4bn on account of tariff revision for five pipelines, adjusted tariff Rs 0.94/scm (- 41%), reported EBIT Rs 2.2bn (-79%). Gas Trading : Volumes 77mmscmd (-6% YoY), margins - Rs 0.04/scm (vs 0.4) due to (1) Rs 1.9bn imbalance on the sale of gas from different sources, will be recovered in Q2 (2) Rs 1bn hit due to fall in spot LNG prices, reported EBIT -Rs 0.4bn. Petrochemicals : Volumes 87kt (-28% YoY) due to maintenance shutdown and power supply interruption, EBITDA margin Rs 16.9/kg (-58% YoY, 70-75% of LNG in gas mix). LPG and LHC : Oil under recovery sharing was Rs 5bn (flat QoQ, -29% YoY), volumes 324 kT (-7% YoY, +12% QoQ) due to higher domestic gas allocation, EBIT at Rs 5bn (flat QoQ). FINANCIAL SUMMARY (STANDALONE) Year Ending March (Rs bn) 1QFY15 1QFY14 YoY (%) 4QFY14 QoQ (%) FY13 FY14 FY15E FY16E Net Sales 138.04 134.00 3.0 145.67 (5.2) 475.23 575.08 736.06 931.62 EBITDA 14.77 20.08 (26.5) 14.40 2.6 64.69 67.01 63.39 73.02 PAT 9.24 13.08 (29.4) 9.72 (5.0) 40.22 40.99 38.54 44.20 Diluted EPS (Rs) 7.3 10.3 (29.4) 7.7 (5.0) 31.7 32.3 30.4 34.8 P/E (x) 13.1 12.8 13.6 11.9 EV / EBITDA (x) 7.6 7.4 7.8 6.8 RoE (%) 17.5 16.0 13.7 14.4 Source: Company, HDFC sec Inst Research INDUSTRY OIL & GAS CMP (as on 12 Aug 2014) Rs 413 Target Price Rs 418 Nifty 7,727 Sensex 25,881 KEY STOCK DATA Bloomberg/Reuters GAIL IN/GAIL.BO No. of Shares (mn) 1,268 MCap (Rs bn) / ($ mn) 524/8,579 6m avg traded value (Rs mn) 709 STOCK PERFORMANCE (%) 52 Week high / low Rs 475/272 3M 6M 12M Absolute (%) 7.7 15.9 37.7 Relative (%) (2.2) (10.7) 1.2 SHAREHOLDING PATTERN (%) Promoters 56.11 FIs & Local MFs 21.29 FIIs 18.77 Public & Others 3.83 Source : BSE Satish Mishra [email protected] +91-22-6171-7334 HDFC securities Institutional Research is also avail able on Bloomberg HSLB <GO> & Thomson Reuters

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/11/2019 Gail - 1qfy15 - Hdfc Sec

http://slidepdf.com/reader/full/gail-1qfy15-hdfc-sec 1/9

RESULTS REVIEW 1QFY15 13 AUG 2014

GAIL

NEUTRAL

Tough timesGAIL reported all round weak results and adj EBITDA

was at Rs 14.8bn (-27% YoY). Lower adj gas

transmission tariff (Rs 0.9/scm, -41%), drop in adj gas

trading margins (Rs 0.2/scm, -42%), oil UR sharing (Rs

5bn, -27%) and higher LNG usage led to dismal

performance. APAT was Rs 9.2bn (-29% YoY).

There are multiple negative triggers lined up for GAIL

(1) Spot LNG prices are trading below LT prices, hence

trading margins will remain weak (2) Tariff revision

for Vadodara pipelines is due, we believe that there

will be further retrospective hit (3) GAIL will be made

to share oil UR of ~Rs 5bn in Q2, we believe the same

will stop only after the gas price hike (4) Increase in

gas prices from H2 will impact petchem/LPG margins

(5) Capitalisation of petchem Pata-II (~Rs 81bn

4QFY15) will increase depreciation/interest cost,

whereas returns will be muted due to higher gas cost.

Our SOTP target for GAIL is Rs 418/sh (~6.4x FY16E

EV/EBITDA and Rs 106/sh from investments).

Maintain NEUTRAL.

1QFY15 highlights

Natural gas transmission : Volumes 97mmscmd (-2%

YoY), reported tariff Rs 0.66/scm (-58%) due to non

recognised revenues of Rs 2.4bn on account of tariff

revision for five pipelines, adjusted tariff Rs 0.94/scm (-

41%), reported EBIT Rs 2.2bn (-79%).

Gas Trading : Volumes 77mmscmd (-6% YoY), margins -

Rs 0.04/scm (vs 0.4) due to (1) Rs 1.9bn imbalance on

the sale of gas from different sources, will be recoveredin Q2 (2) Rs 1bn hit due to fall in spot LNG prices,

reported EBIT -Rs 0.4bn.

Petrochemicals : Volumes 87kt (-28% YoY) due to

maintenance shutdown and power supply interruption,

EBITDA margin Rs 16.9/kg (-58% YoY, 70-75% of LNG in

gas mix).

LPG and LHC : Oil under recovery sharing was Rs 5bn

(flat QoQ, -29% YoY), volumes 324 kT (-7% YoY, +12%

QoQ) due to higher domestic gas allocation, EBIT at Rs

5bn (flat QoQ).

FINANCIAL SUMMARY (STANDALONE)

Year Ending March (Rs bn) 1QFY15 1QFY14 YoY (%) 4QFY14 QoQ (%) FY13 FY14 FY15E FY16E

Net Sales 138.04 134.00 3.0 145.67 (5.2) 475.23 575.08 736.06 931.62

EBITDA 14.77 20.08 (26.5) 14.40 2.6 64.69 67.01 63.39 73.02

PAT 9.24 13.08 (29.4) 9.72 (5.0) 40.22 40.99 38.54 44.20

Diluted EPS (Rs) 7.3 10.3 (29.4) 7.7 (5.0) 31.7 32.3 30.4 34.8

P/E (x) 13.1 12.8 13.6 11.9

EV / EBITDA (x) 7.6 7.4 7.8 6.8

RoE (%) 17.5 16.0 13.7 14.4

Source: Company, HDFC sec Inst Research

INDUSTRY OIL & GAS

CMP (as on 12 Aug 2014) Rs 413

Target Price Rs 418

Nifty 7,727

Sensex 25,881

KEY STOCK DATA

Bloomberg/Reuters GAIL IN/GAIL.BO

No. of Shares (mn) 1,268

MCap (Rs bn) / ($ mn) 524/8,579

6m avg traded value (Rs mn) 709

STOCK PERFORMANCE (%)

52 Week high / low Rs 475/272

3M 6M 12M

Absolute (%) 7.7 15.9 37.7

Relative (%) (2.2) (10.7) 1.2

SHAREHOLDING PATTERN (%)

Promoters 56.11

FIs & Local MFs 21.29FIIs 18.77

Public & Others 3.83

Source : BSE

Satish Mishra

[email protected]+91-22-6171-7334

HDFC securities Institutional Research is also available on Bloomberg HSLB <GO> & Thomson Reuters

8/11/2019 Gail - 1qfy15 - Hdfc Sec

http://slidepdf.com/reader/full/gail-1qfy15-hdfc-sec 2/9

GAIL : RESULTS REVIEW 1QFY15

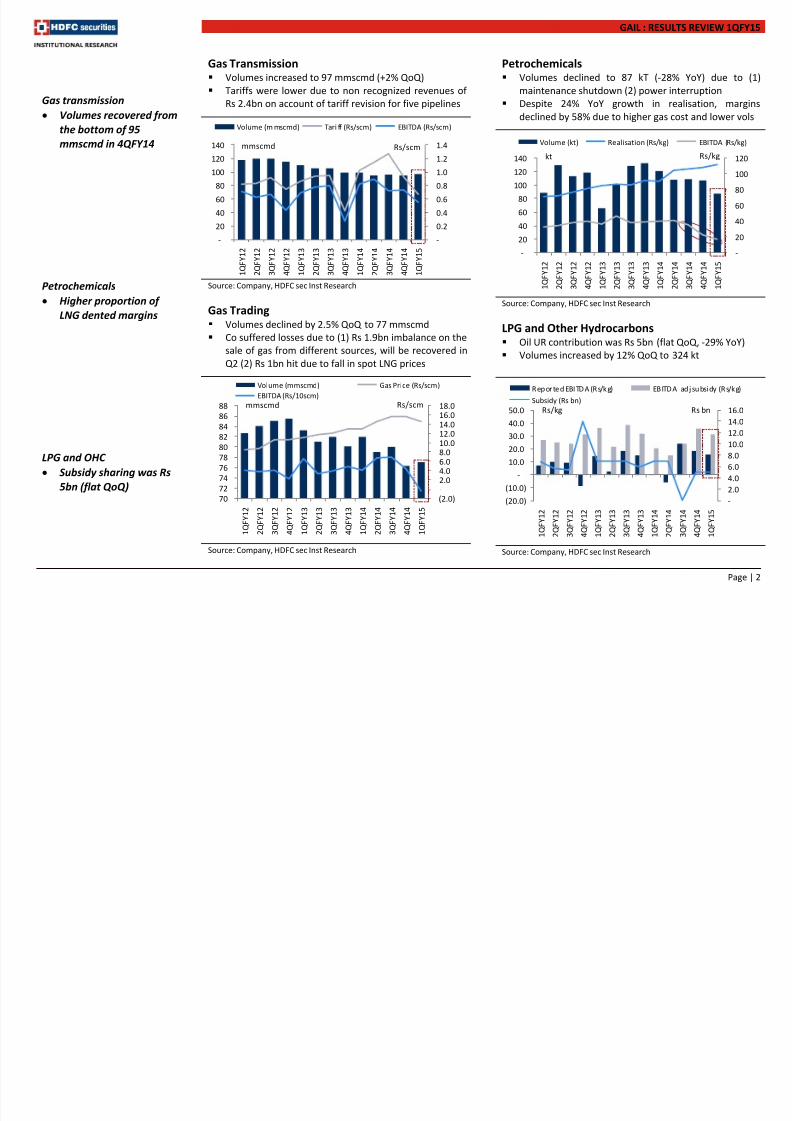

Gas Transmission Volumes increased to 97 mmscmd (+2% QoQ)

Tariffs were lower due to non recognized revenues of

Rs 2.4bn on account of tariff revision for five pipelines

Source: Company, HDFC sec Inst Research

Gas Trading Volumes declined by 2.5% QoQ to 77 mmscmd

Co suffered losses due to (1) Rs 1.9bn imbalance on the

sale of gas from different sources, will be recovered in

Q2 (2) Rs 1bn hit due to fall in spot LNG prices

Source: Company, HDFC sec Inst Research

Petrochemicals Volumes declined to 87 kT (-28% YoY) due to (1)

maintenance shutdown (2) power interruption

Despite 24% YoY growth in realisation, margins

declined by 58% due to higher gas cost and lower vols

Source: Company, HDFC sec Inst Research

LPG and Other Hydrocarbons Oil UR contribution was Rs 5bn (flat QoQ, -29% YoY)

Volumes increased by 12% QoQ to 324 kt

Source: Company, HDFC sec Inst Research

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

-

20

40

60

80

100

120

140

1 Q

F Y 1 2

2 Q

F Y 1 2

3 Q

F Y 1 2

4 Q

F Y 1 2

1 Q

F Y 1 3

2 Q

F Y 1 3

3 Q

F Y 1 3

4 Q

F Y 1 3

1 Q

F Y 1 4

2 Q

F Y 1 4

3 Q

F Y 1 4

4 Q

F Y 1 4

1 Q

F Y 1 5

Volume (m mscmd) Tari ff (Rs/scm) EBITDA (Rs/scm)

mmscmd Rs/scm

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

(20.0)

(10.0)

-

10.0

20.0

30.0

40.0

50.0

1 Q F Y 1 2

2 Q F Y 1 2

3 Q F Y 1 2

4 Q F Y 1 2

1 Q F Y 1 3

2 Q F Y 1 3

3 Q F Y 1 3

4 Q F Y 1 3

1 Q F Y 1 4

2 Q F Y 1 4

3 Q F Y 1 4

4 Q F Y 1 4

1 Q F Y 1 5

Rep orted EBITDA (Rs/kg) EB ITDA ad j su bsidy (Rs/kg)

Subsidy (Rs bn)

Rs/kg Rs bn

Gas transmission

• Volumes recovered from

the bottom of 95mmscmd in 4QFY14

Petrochemicals

• Higher proportion of

LNG dented margins

LPG and OHC

• Subsidy sharing was Rs

5bn (flat QoQ)

-

20

40

60

80

100

120

-

20

40

60

80

100

120

140

1 Q F Y 1

2

2 Q F Y 1

2

3 Q F Y 1

2

4 Q F Y 1

2

1 Q F Y 1

3

2 Q F Y 1

3

3 Q F Y 1

3

4 Q F Y 1

3

1 Q F Y 1

4

2 Q F Y 1

4

3 Q F Y 1

4

4 Q F Y 1

4

1 Q F Y 1

5

Volume (kt) Realisation (Rs/kg) EBITDA (Rs/kg)

kt Rs/kg

(2.0)-2.04.06.08.010.012.014.016.018.0

70

72

74

76

78

80

82

84

8688

1 Q F Y 1 2

2 Q F Y 1 2

3 Q F Y 1 2

4 Q F Y 1 2

1 Q F Y 1 3

2 Q F Y 1 3

3 Q F Y 1 3

4 Q F Y 1 3

1 Q F Y 1 4

2 Q F Y 1 4

3 Q F Y 1 4

4 Q F Y 1 4

1 Q F Y 1 5

Volume (mmscmd) Gas Price (Rs/scm)

EBITDA (Rs/10scm)

mmscmd Rs/scm

Page | 2

8/11/2019 Gail - 1qfy15 - Hdfc Sec

http://slidepdf.com/reader/full/gail-1qfy15-hdfc-sec 3/9

GAIL : RESULTS REVIEW 1QFY15

QUARTERLY FINANCIALS SNAPSHOT (STANDALONE)

(Rs bn) 1QFY15 1QFY14 YoY (%) 4QFY14 QoQ (%)

Revenues 138.04 134.00 3.0 145.67 (5.2)

Raw Material Expenses 4.51 6.72 (32.8) 7.09 (36.3)

Trading Expenses 106.65 96.47 10.5 109.90 (3.0)Employee Expenses 2.27 2.00 13.4 2.26 0.7

Other Operating Expenses 9.84 8.72 12.8 12.02 (18.1)

EBITDA 14.77 20.08 (26.5) 14.40 2.6

Depreciation 2.34 2.81 (16.8) 3.06 (23.6)

Other Income 1.72 0.58 198.9 4.11 (58.0)

PBIT 14.16 17.85 (20.7) 15.45 (8.4)

Interest Cost 0.93 0.61 52.3 1.06 (11.7)

PBT 13.22 17.24 (23.3) 14.39 (8.1)

Tax 3.99 4.16 (4.2) 4.67 (14.7)

APAT 9.24 13.08 (29.4) 9.72 (5.0)

Exceptional 2.89 - - - -

RPAT 6.34 13.08 (51.5) 9.72 (34.7)

AEPS (Rs/sh) 7.3 10.3 (29.4) 7.7 (5.0)

Source: Company, HDFC sec Inst Research

MARGIN ANALYSIS

1QFY15 1QFY14 YoY (bps) 4QFY14 QoQ (bps)

Material Expenses as % of Net Sales 3.3 5.0 (174) 4.9 (160)

Trading Expenses as % of Net Sales 77.3 72.0 526 75.4 181

Employee Expenses as % of Net Sales 1.6 1.5 15 1.6 10

Other Expenses as % of Net Sales 7.1 6.5 62 8.3 (112)

EBITDA Margin (%) 10.7 15.0 (429) 9.9 81

Net Profit Margin (%) 6.7 9.8 (307) 6.7 2

Tax Rate (%) 30.1 24.1 602 32.5 (233)

Source: Company, HDFC sec Inst Research

Profitability declined in all

the major segments (gas

transmission, gas trading,

petchem)

Page | 3

8/11/2019 Gail - 1qfy15 - Hdfc Sec

http://slidepdf.com/reader/full/gail-1qfy15-hdfc-sec 4/9

GAIL : RESULTS REVIEW 1QFY15

SEGMENTAL PERFORMANCE

(Rs bn) 1QFY15 1QFY14 YoY (%) 4QFY14 QoQ (%) FY14

Revenues

Natural Gas Transmission 5.87 14.27 (58.9) 7.87 (25.4) 38.29

LPG Transmission 1.11 0.94 18.1 1.15 (3.5) 4.18

Gas Trading 102.45 96.82 5.8 107.76 (4.9) 426.22

Petrochemicals 9.74 10.97 (11.2) 11.60 (16.0) 45.37

LPG & Other Liquid Hydro Carbons 12.60 10.04 25.5 14.86 (15.2) 54.63

Total 133.37 133.56 (0.1) 144.64 (7.8) 572.45

PBIT

Natural gas transmission 2.23 10.54 (78.8) 2.60 (14.2) 18.02

LPG transmission 0.69 0.55 25.4 0.58 19.2 2.15

Gas trading (0.35) 3.03 (111.7) 2.85 (112.4) 15.80

Petrochemicals 1.25 4.38 (71.5) 1.96 (36.4) 13.61

LPG & Other hydrocarbons 4.96 (0.11) (4,633.9) 4.98 (0.5) 10.21

Total 9.39 18.13 (48.2) 12.98 (27.7) 59.85

SEGMENTAL KEY DATA

Physical performance 1QFY15 1QFY14 YoY (%) 4QFY14 QoQ (%) FY14

TRANSMISSION

Natural Gas (mmscmd) 97 99 (2.4) 95 2.0 96

Tariff (Rs/kscm) 664 1,575 (57.8) 1,149 (42.2) 1,090

LPG (kT) 832 699 19.0 729 14.1 3,146

Tariff (Rs/kg) 1.3 1.3 (0.8) 1.3 0.1 1.3

SALES

Natural Gas (mmscmd) 77 82 (6.1) 79 (2.5) 79

Realisation (Rs/scm) 14.6 12.9 12.7 15.5 (5.8) 14.7

Margin (Rs/scm) (0.04) 0.40 (109.1) 0.43 (108.7) 0.55

Petrochemicals (kT) 87 121 (28.1) 108 (19.4) 445

Realisation (Rs/kg) 112 91 23.5 104 7.2 102

EBITDA (Rs/kg) 16.9 40.0 (57.8) 40.5 (58.2) 34.6

LPG + LHC (kT) 324 350 (7.4) 289 12.1 1,308

Subsidy Contribution (Rs mn) 5,000 7,000 (28.6) 5,000 - 19,000

Source: Company, HDFC sec Inst Research

Gas transmission revenues

were lower due to nonrecognition of revenues

worth Rs 2.4bn on account

of tariff revision for five

pipelines

GAIL accounted for under

recovery of Rs 1.9bn due to

imbalance on account of

the sale of gas fromdifferent sources in the

trading segment, will be

recovered in 2QFY15

QoQ increase in gas

transmission volumes is

encouraging

We expect ~Rs 5bn/qtr oil

UR sharing to continue until

there is an increase in gas

price

Page | 4

8/11/2019 Gail - 1qfy15 - Hdfc Sec

http://slidepdf.com/reader/full/gail-1qfy15-hdfc-sec 5/9

GAIL : RESULTS REVIEW 1QFY15

ASSUMPTIONS

FY12 FY13 FY14 FY15E FY16E FY17E

TRANSMISSION

Gas Volumes (mmscmd) 118 105 96 101 110 129

Tariff (Rs/scm) 0.8 0.9 1.1 0.9 1.0 1.0

LPG Volumes (kT) 3,362 3,136 3,145 3,161 3,177 3,177

Tariff (Rs/kg) 1.4 1.3 1.3 1.3 1.3 1.3

SALES

Natural Gas (mmscmd) 84 82 79 81 88 103

Realisation (US$/mmbtu) 5.1 5.5 6.4 8.2 9.5 10.0

EBITDA Margin (Rs/scm) 0.35 0.47 0.55 0.41 0.37 0.34

Petrochemicals (kT) 448 427 445 540 810 855

Realisation (US$/t) 1,573 1,611 1,685 1,685 1,685 1,685

Feed Gas Cost (US$/mmbtu) 5.4 5.5 8.1 9.0 10.5 10.7

LPG (kT) 1,124 1,075 1,030 1,030 1,030 1,030

Other LHC (kT) 315 296 277 298 298 298

OTHERS

INR-US$ 48.0 54.4 60.5 60.0 60.0 60.0

Subsidy Contribution (Rs bn) 31.8 26.9 19.0 10.0 - -

Source: Company, HDFC sec Inst Research

SOTP VALUATION (BASED ON FY16E)

EBITDA (Rs bn) Multiple EV (Rs bn) Value/sh Basis

Gas Transmission 25.7 8.0 206 162 x FY16E EBITDA

LPG Transmission 2.6 7.0 18 15 x FY16E EBITDA

Gas Trading 12.0 4.0 48 38 x FY16E EBITDA

Petchem 17.6 4.5 79 62 x FY16E EBITDA

LPG & Other Hydrocarbons 22.4 5.0 112 88 x FY16E EBITDA

Standalone wt avg 6.4

Less : Net Debt (Mar-14) 68.8 69 54

Standalone Value 311

Investments

ONGC 0.8 77 61 20% disc. to our TP

Petronet LNG 0.8 14 11 20% disc. to our TP

IGL 0.8 10 8 20% disc. to our TP

Others 1.0 34 27 1x BV

Value per share 418

Source : HDFC sec Inst Research

Key events for GAIL

(1)

Increase in gas

transmission volumes

(2) Increase in gas cost

(3) No subsidy sharing post

gas price hike

Lower multiple to petchem,

LPG and trading biz due to

rising gas cost andregulatory risk

Page | 5

8/11/2019 Gail - 1qfy15 - Hdfc Sec

http://slidepdf.com/reader/full/gail-1qfy15-hdfc-sec 6/9

GAIL : RESULTS REVIEW 1QFY15

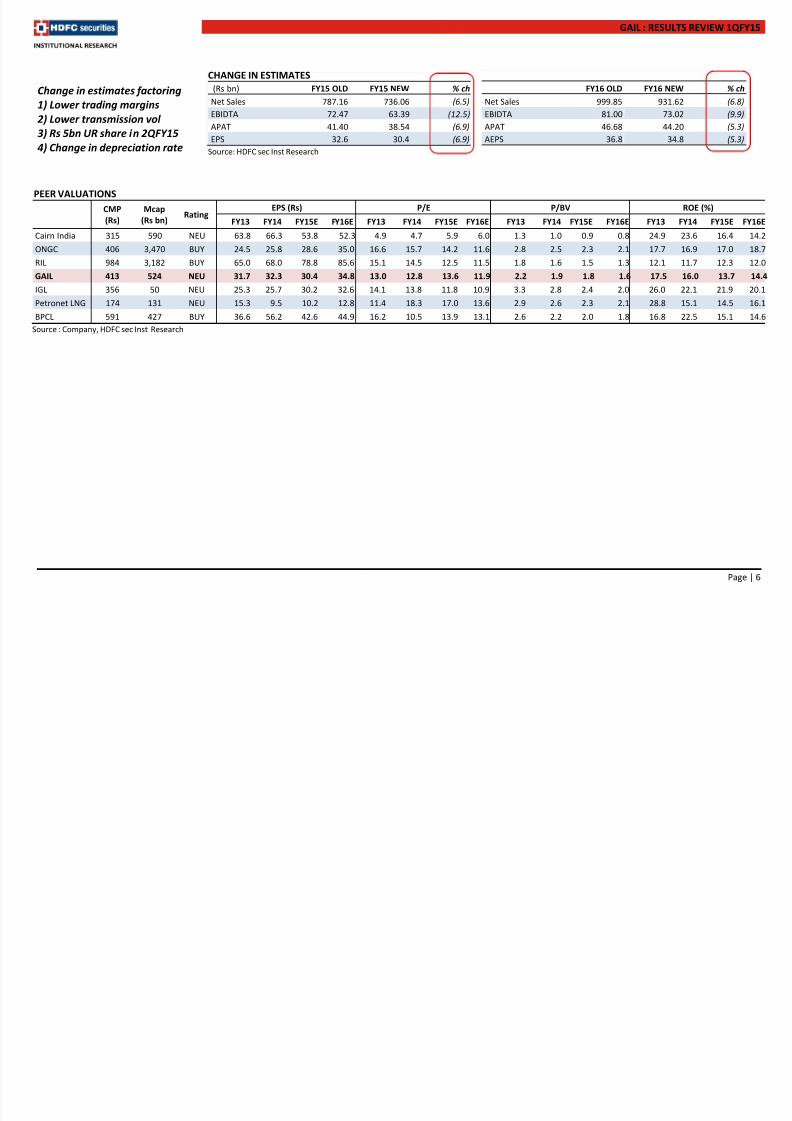

CHANGE IN ESTIMATES

(Rs bn) FY15 OLD FY15 NEW % ch

Net Sales 787.16 736.06 (6.5)

EBIDTA 72.47 63.39 (12.5)

APAT 41.40 38.54 (6.9)

EPS 32.6 30.4 (6.9)

FY16 OLD FY16 NEW % ch

Net Sales 999.85 931.62 (6.8)

EBIDTA 81.00 73.02 (9.9)

APAT 46.68 44.20 (5.3)

AEPS 36.8 34.8 (5.3)

Source: HDFC sec Inst Research

PEER VALUATIONS

CMP

(Rs)

Mcap

(Rs bn) Rating

EPS (Rs) P/E P/BV ROE (%)

FY13 FY14 FY15E FY16E FY13 FY14 FY15E FY16E FY13 FY14 FY15E FY16E FY13 FY14 FY15E FY16E

Cairn India 315 590 NEU 63.8 66.3 53.8 52.3 4.9 4.7 5.9 6.0 1.3 1.0 0.9 0.8 24.9 23.6 16.4 14.2

ONGC 406 3,470 BUY 24.5 25.8 28.6 35.0 16.6 15.7 14.2 11.6 2.8 2.5 2.3 2.1 17.7 16.9 17.0 18.7

RIL 984 3,182 BUY 65.0 68.0 78.8 85.6 15.1 14.5 12.5 11.5 1.8 1.6 1.5 1.3 12.1 11.7 12.3 12.0

GAIL 413 524 NEU 31.7 32.3 30.4 34.8 13.0 12.8 13.6 11.9 2.2 1.9 1.8 1.6 17.5 16.0 13.7 14.4

IGL 356 50 NEU 25.3 25.7 30.2 32.6 14.1 13.8 11.8 10.9 3.3 2.8 2.4 2.0 26.0 22.1 21.9 20.1

Petronet LNG 174 131 NEU 15.3 9.5 10.2 12.8 11.4 18.3 17.0 13.6 2.9 2.6 2.3 2.1 28.8 15.1 14.5 16.1

BPCL 591 427 BUY 36.6 56.2 42.6 44.9 16.2 10.5 13.9 13.1 2.6 2.2 2.0 1.8 16.8 22.5 15.1 14.6

Source : Company, HDFC sec Inst Research

Change in estimates factoring

1) Lower trading margins

2) Lower transmission vol

3) Rs 5bn UR share in 2QFY154) Change in depreciation rate

Page | 6

8/11/2019 Gail - 1qfy15 - Hdfc Sec

http://slidepdf.com/reader/full/gail-1qfy15-hdfc-sec 7/9

GAIL : RESULTS REVIEW 1QFY15

STANDALONE INCOME STATEMENT

(Rs bn) FY12 FY13 FY14 FY15E FY16E

Revenues 404.41 475.23 575.08 736.06 931.62

Growth % 24.6 17.5 21.0 28.0 26.6

Raw Material 25.86 36.47 42.17 55.54 83.38

Gas Trading 284.40 333.97 412.34 559.88 712.79

Employee Cost 6.50 7.85 8.48 9.16 9.89

Other expenses 31.65 32.24 45.08 48.09 52.53

EBITDA 55.99 64.69 67.01 63.39 73.02

EBITDA growth % 2.3 15.5 3.6 (5.4) 15.2

EBITDA Margin % 13.8 13.6 11.7 8.6 7.8

Depreciation 7.91 9.81 11.76 10.90 12.54

Other income 6.48 7.65 8.99 8.67 9.02

EBIT 54.56 62.53 64.24 61.16 69.50

Interest Cost 1.16 1.95 3.66 4.06 4.01

Exceptional items - - 3.45 - -

PBT 53.40 60.58 64.02 57.10 65.49

Taxes 16.86 20.36 20.27 18.56 21.28

RPAT 36.54 40.22 43.75 38.54 44.20

APAT 36.54 40.22 40.99 38.54 44.20

APAT Growth % 2.6 10.1 1.9 (6.0) 14.7

AEPS 28.8 31.7 32.3 30.4 34.8

EPS Growth % 2.6 10.1 1.9 (6.0) 14.7

Source: Company, HDFC sec Inst Research

STANDALONE BALANCE SHEET

(Rs bn) FY12 FY13 FY14 FY15E FY16E

SOURCES OF FUNDS

Share capital 12.68 12.68 12.68 12.68 12.68

Reserves and surplus 203.57 229.59 258.04 281.04 308.96

Net Worth 216.26 242.28 270.72 293.72 321.65

LT Loans 48.89 81.41 95.26 85.26 75.26

ST Loans - 2.24 - - -

Total Debt 48.89 83.65 95.26 85.26 75.26

Deferred tax liability 17.69 23.00 25.66 27.95 27.95

Other LT Liabilities 2.77 6.85 7.71 7.71 7.71

Long term provisions 3.38 3.60 4.04 4.04 4.04

Total liabilities 288.98 359.37 403.40 418.68 436.61

APPLICATION OF FUNDS

Net fixed assets 158.58 197.07 205.29 282.94 295.10

Capital WIP 79.42 89.78 106.75 53.64 58.94

LT Investments 26.72 36.80 41.03 41.03 41.03

LT Loans and Advances 31.75 25.91 25.35 25.35 25.35

Other non current assets 2.72 6.73 7.18 7.18 7.18

Inventory 14.20 15.35 22.55 27.62 34.98

Debtors 19.04 25.51 28.12 35.23 44.62

Cash and Cash Equivalent 9.41 23.97 26.51 24.61 21.53

Loans and advances 19.66 25.56 35.14 26.07 26.33

Other current assets 0.01 0.15 0.18 0.18 0.18

Total current assets 62.33 90.54 112.50 113.72 127.65Trade Payables 25.10 31.04 39.75 50.18 63.55

Other Current Liabiliites 36.55 42.08 40.48 40.48 40.48

Provisions 10.88 14.35 14.49 14.53 14.62

Total current Liabilities 72.53 87.47 94.71 105.18 118.65

Net current assets (10.20) 3.07 17.79 8.54 9.00

Total Assets 288.98 359.37 403.40 418.68 436.61

Source: Company, HDFC sec Inst Research

Page | 7

8/11/2019 Gail - 1qfy15 - Hdfc Sec

http://slidepdf.com/reader/full/gail-1qfy15-hdfc-sec 8/9

8/11/2019 Gail - 1qfy15 - Hdfc Sec

http://slidepdf.com/reader/full/gail-1qfy15-hdfc-sec 9/9

Related Documents