GAAR Dileep Kumar Anumula

GAAR Dileep Kumar Anumula. Aim Combating Impermissible tax avoidance.

Dec 27, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

GAARDileep Kumar Anumula

Aim

• Combating Impermissible tax avoidance

Do we have this concept already in Act???

• Yes!

• Act already notified SAAR

Ex:

1. S. 40A(2) – Excessive/Un reasonable pymts to Related parties.

2. S. 80IA(8) – Transactions with Tax exempt entities

3. S. 92 to 92F – TP Provisions.

4. S. 2(22)(e) -Deemed Dividend.

When GAAR Comes in to Picture???

• As name suggests it comes in to picture, when there is a reduction of Tax liability by way of acts which are forbidden by law.

• Reduction of Tax liability can be made by many ways. But the all the ways can be clubbed in to three major catagories

Three Categories

Tax Evasion Tax Avoidance Tax Planning

Gen result of Illegality, Mis rep. or Fraud.

Result of Actions none of which are forbidden by law

Result of Tax incentives made avbl by the Act

Not Applies

Applies

Not Applies

Legal Enforcement

• Fin. Act, 2012 inserted new chapter, CH XA containing S. 95 to S. 102

• W.E.F AY 2014-15

• Later based on Shome Committee postponed to 2yrs

• Hence now GAAR comes in to force W.E.F 1/4/2016.

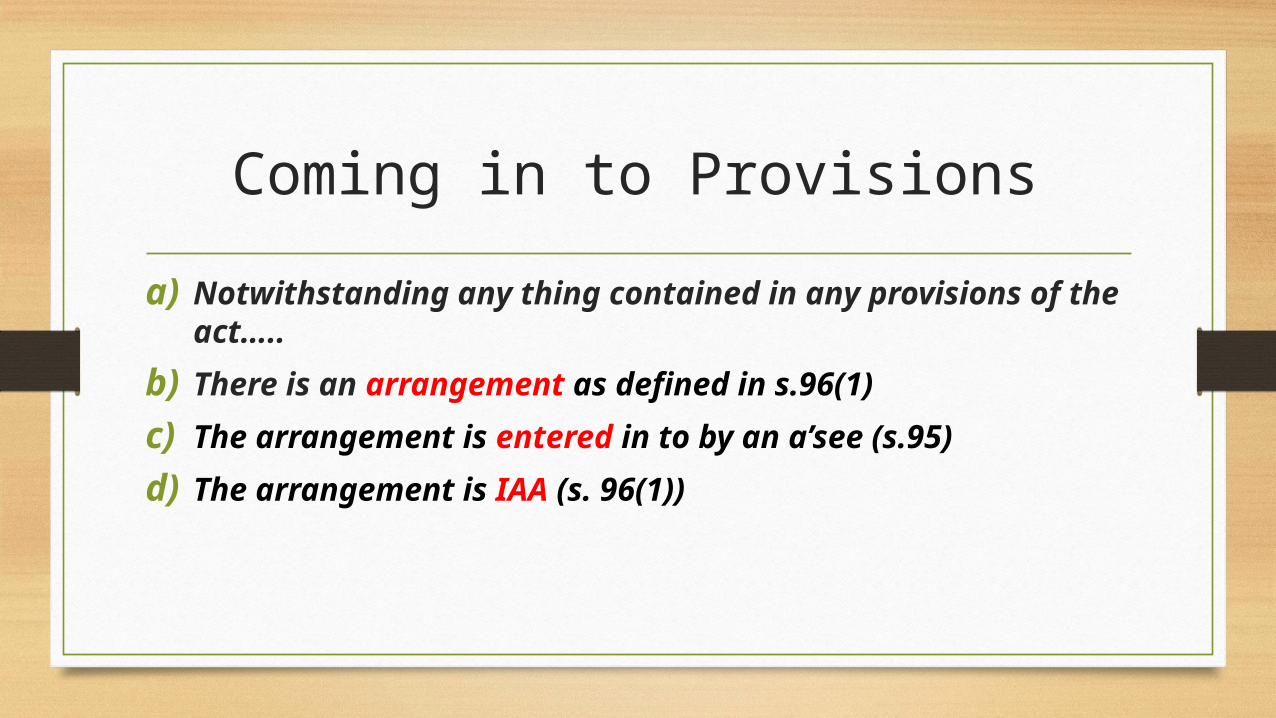

Coming in to Provisions

a) Notwithstanding any thing contained in any provisions of the act…..

b)There is an arrangement as defined in s.96(1)

c) The arrangement is entered in to by an a’see (s.95)

d)The arrangement is IAA (s. 96(1))

If the above (a) to (d) are satisfied, then

i. The arrangement may be declared to be an IAA, sub to the prov of the CH XA.

ii. The consequences in relation to tax arising there from may be determined based on S. 95 to S. 98

Inference of the above reading:

• Provisions shall be:

i. Applicable in addition to (or) in lieu of, any other basis for determination of tax liability (s. 100)

ii. Applied in acc with guidelines sub to such conditions & the manner as may be prescribed in S.101

iii. Applicable to all ( Ind/HUF/Firm/Coy)

iv. Applicable irrespective of Res. Status

Prime Definitions

Arrangement (Exhaustive):

Any step in or a part (or) whole of, any transaction, operation, scheme, agreement or understanding, whether enforceable or not, and includes alienation of any property in such transaction, operation, scheme, agreement o understanding. (none of these are defined in the act)

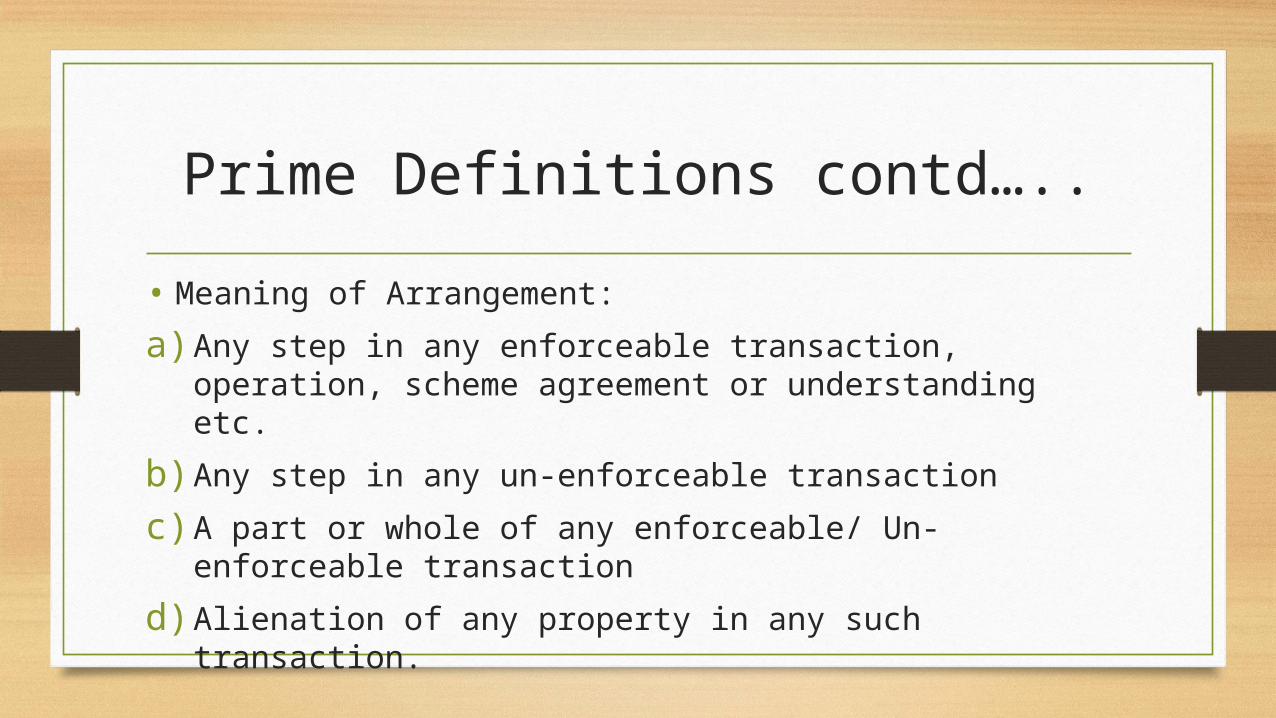

Prime Definitions contd…..

• Meaning of Arrangement:

a) Any step in any enforceable transaction, operation, scheme agreement or understanding etc.

b) Any step in any un-enforceable transaction

c) A part or whole of any enforceable/ Un-enforceable transaction

d) Alienation of any property in any such transaction.

Impermissible Avoidance Agreement (IAA)

There is an arrangement

The main purpose is to obtain Tax benefit

The arrangement satisfies any one of the following……..

IAA contd….

a) It creates rights/obligations which are not ordinarily created b/w persons dealing at ALP.

b) It results directly or Indirectly, in the Misuse/abuse of provisions of the act

c) It lacks commercial substance in whole or in part.

d) It is deemed to lack commercial substance in whole or in part with in the meaning of S.97

e) It is entered in to by means or in a manner which are not ordinarily employed for bonafide purpose.

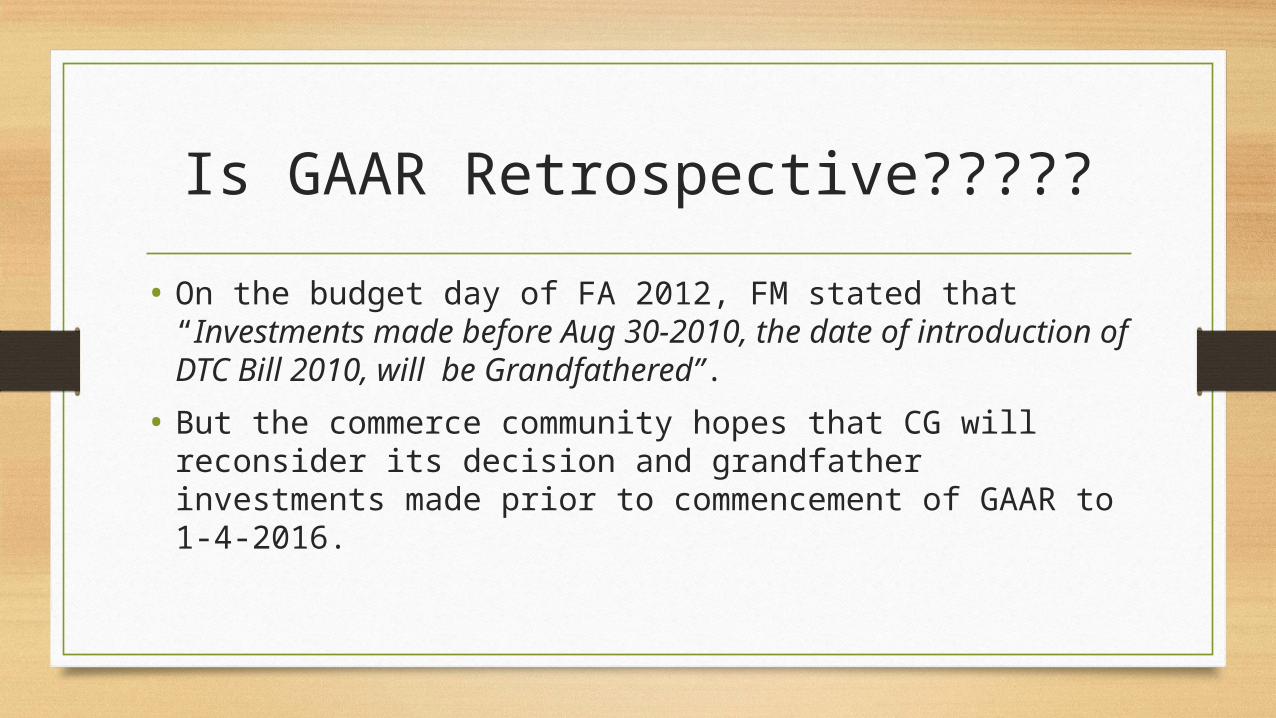

Is GAAR Retrospective?????

• On the budget day of FA 2012, FM stated that “Investments made before Aug 30-2010, the date of introduction of DTC Bill 2010, will be Grandfathered”.

• But the commerce community hopes that CG will reconsider its decision and grandfather investments made prior to commencement of GAAR to 1-4-2016.

Any monetary Threshold limit…..?

• Yes!

• The final Report of Expert committee recommended that a monetary threshold limit of Rs. 3 cr. Of tax benefit, to a taxpayer in a year should be used for the applicability of GAAR provisions.

Applicability of GAAR in SAAR cases…

• GAAR has no role of application where SAAR is available in the Act already.

• However Govt Press release dt. 14-1-2013 states that, “where GAAR & SAAR are both in force, only one of them will apply to a given case, and guidelines will be made regarding the applicability of one or the other”

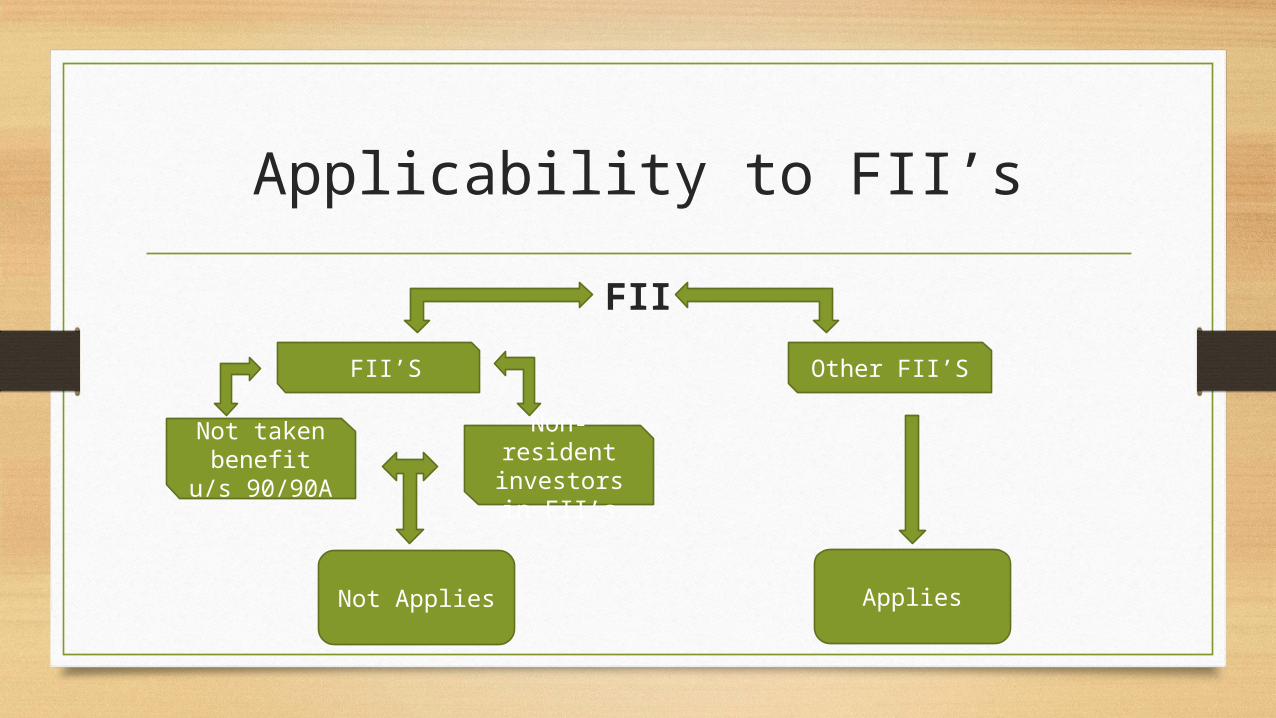

Applicability to FII’s

FII

Other FII’S FII’S

Not taken benefit u/s

90/90A

Non-resident

investors in FII’s

Not Applies Applies

Applying GAAR Procedure…..

• AO Can’t issue order without CIT approval.

At Any stage of Assessment or Re-assessment

Having regard to evidence & Material avbl

Makes ref. to CIT. CIT on receipt of ref, if CH-XA is to be invoked,

GAAR Procedure….. Contd…

Issues notices setting out of reasons, basis of opinion after providing OBH, with in 60 days.

Assesse’s Reaction

Assesse

Objects

CIT SatisfiesCIT Not Satisfies

Doesn’t Objects

CIT shall issue such directions as he deems

fit in respect of declaration of

arrangement to be an IAA

Shall not Invoke

Shall Invoke by making

ref. to Approving

panel

Related Documents

![Economic Substance and Abusive Tax avoidance · The Economic Substance Doctrine and GAAR: A Critical and Comparative Perspective [DRAFT] Jinyan Li* Written for the GAAR Symposium](https://static.cupdf.com/doc/110x72/5b0681297f8b9ad1768ce6d0/economic-substance-and-abusive-tax-avoidance-economic-substance-doctrine-and-gaar.jpg)

![GAAR Draft Guidelines 280612 [1]](https://static.cupdf.com/doc/110x72/577ce7b11a28abf103959850/gaar-draft-guidelines-280612-1.jpg)