FX Options(II) : Engineering New Risk Management Products Dr. J. D. Han King’s College, UWO

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FX Options(II) : Engineering New Risk Management Products

Dr. J. D. HanKing’s College, UWO

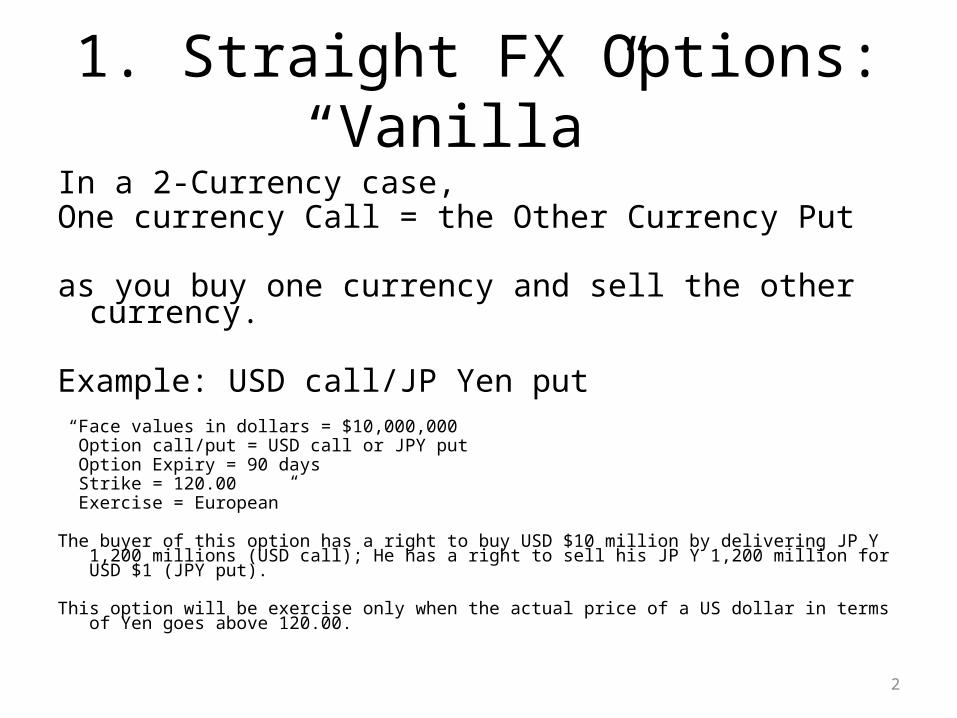

1. Straight FX Options: “Vanilla” In a 2-Currency case, One currency Call = the Other Currency Put

as you buy one currency and sell the other currency. Example: USD call/JP Yen put “Face values in dollars = $10,000,000 Option call/put = USD call or JPY put Option Expiry = 90 days Strike = 120.00 Exercise = European”

The buyer of this option has a right to buy USD $10 million by delivering JP Y 1,200 millions (USD call); He has a right to sell his JP Y 1,200 million for USD $1 (JPY put).

This option will be exercise only when the actual price of a US dollar in terms of Yen goes above 120.00.

2

2. Creating New Products

• Combining existing instruments

• Restructuring existing instruments

• Applying existing instruments to new

markets

3

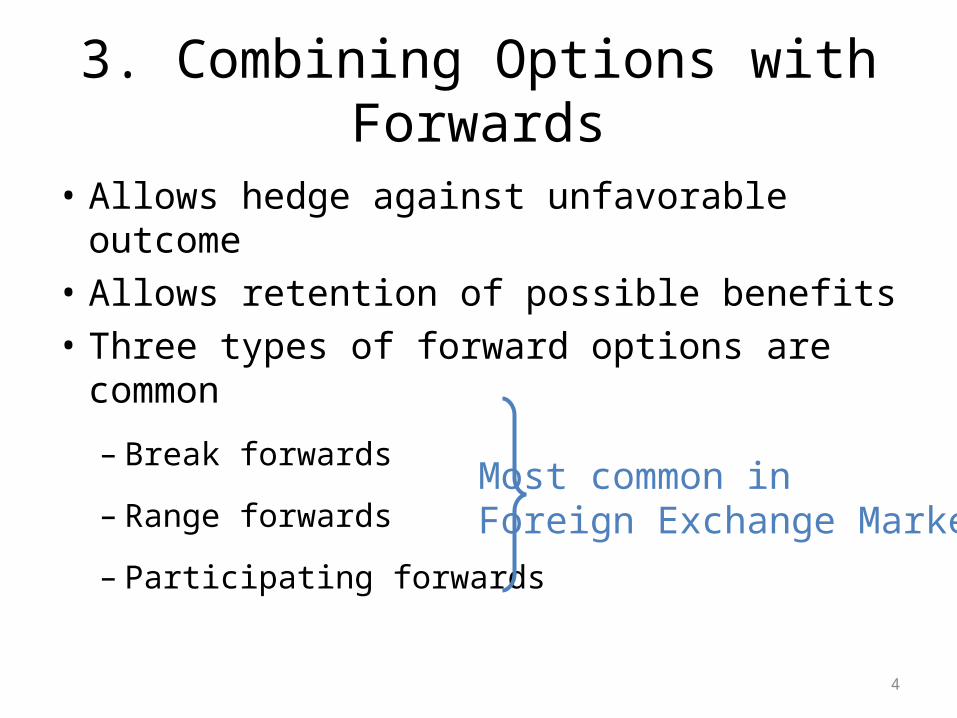

3. Combining Options with Forwards

• Allows hedge against unfavorable outcome• Allows retention of possible benefits• Three types of forward options are common

– Break forwards

– Range forwards

– Participating forwards

4

Most common in Foreign Exchange Markets

1) Break Forwards

• Modifies forward to have features of a Call Option

• Premium is paid “implicitly”

• The buyer can ‘break’ or ‘unwind’ the forward contract at a position where St+1 < X.

5

Break Forward Payoff

6

$/£1.40 1.45 1.50 1.55 1.60

Break Forward

Contract Rate

Price where owner may ‘break’ (unwind)

Typical ForwardContract Rate

2) Range Forward

• A forward contract with limited gain & loss• Major merit: Low Cost• Also known as – A flexible forward– Forward band– Collar Cylinder

• Long Put + Short Call

7

8

Which one to choose depends on the Initial FX risk of the hedger.

Long Range Forward

9

Short Call

Long Put

S1

Short Range-Forward

• A collar is an interesting strategy that is often employed by major investment banks and corporate executives.

• This position is made by selling a call option at one strike price and using the proceeds to purchase a put option at a lower price. The cost to the investor to make this trade, therefore, is low or close to zero.

• It is called Cylinder = Option fence = collar = range forward.

10

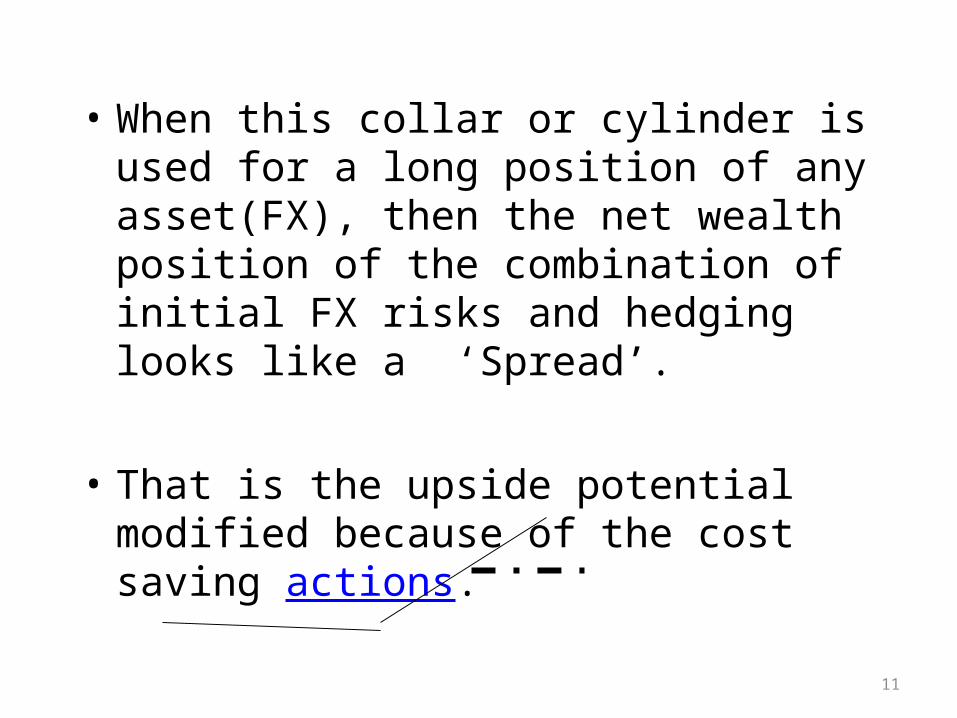

• When this collar or cylinder is used for a long position of any asset(FX), then the net wealth position of the combination of initial FX risks and hedging looks like a ‘Spread’.

• That is the upside potential modified because of the cost saving actions.

11

3) Participating Forward

• Way to eliminate the “up-front” premium• Combine Short Forward position with Long out-of-money Call• Short fraction of in-money put

12

Participating Forward Diagram

13

P

V

Sell 1/2 Put

Buy 1 Call

CombinedOption Payoff

Inherent Risk

ResultingExposure

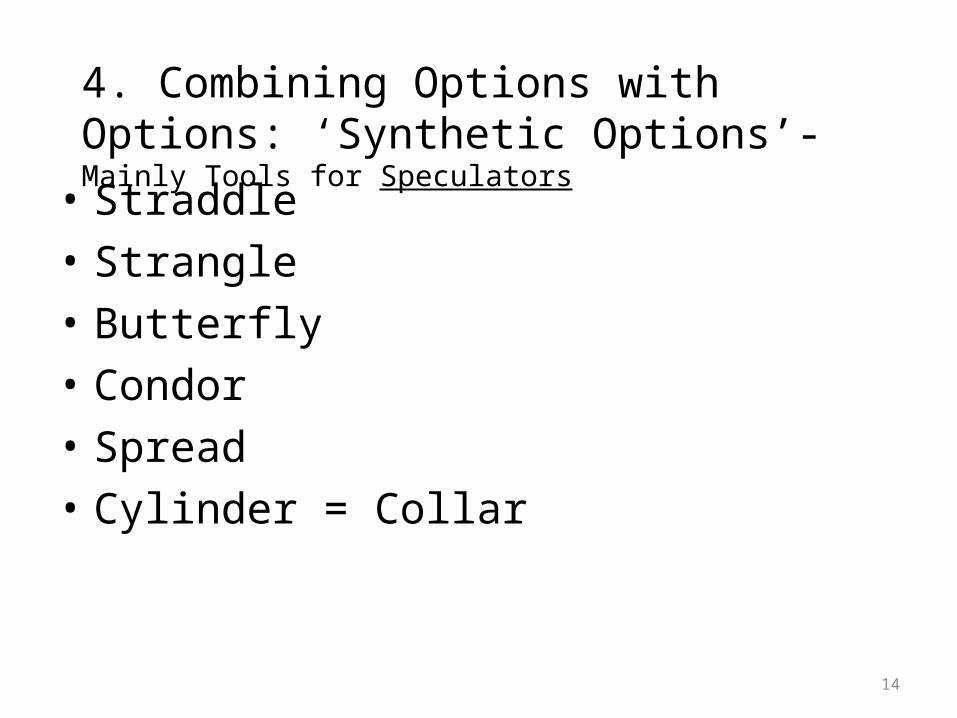

4. Combining Options with Options: ‘Synthetic Options’- Mainly Tools for Speculators

• Straddle• Strangle• Butterfly• Condor• Spread• Cylinder = Collar

14

1) Long “Straddle”

15

Use: Betting on an Increased Price Volatility

Construction: Long Call and Long Put at the same Strike Price

2) Long ‘Strangle’

16

Use: the same as ‘Straddle’ but a lower premium

Construction: long call and long put at different strike prices

3) Long ‘Butterfly’

17

4) Long ‘Condor’

18

5) Spread: ‘Low or Zero Cost Options’

19

(1) Bull Spread

Long Call at X1 and Short Call at X2

X2

X1

Sell call option and use the premium to buy another call option at a lower strike price:

X1 > X2

•* The farther the two X’s, the larger the upside potential of the bear spread :

• Compare the two cases:

20

(2) Bear Spread: Buy Put at X1 and sell Put at X2

21

Short put

Long put

Use the premium from short Put in order to buy another Put at a higher strike price

X2>X1

X1

X2

(5) Collar

• A collar is an options trading strategy that is constructed by holding shares of the underlying stock while simultaneously buying protective puts and selling call options against that holding. The puts and the calls are both out-of-the-money options having the same expiration month and must be equal in number of contracts.

22

5. Option Maker by J.D. Han

• Click here to make the above options by using my option maker(copy-righted)

23

Related Documents