Future of Wealth Management March 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Future of Wealth Management

March 2016

© 2016 Deloitte Consulting Pte Ltd 2

Agenda

Context

Forces of change and implications

© 2016 Deloitte Consulting Pte Ltd 3

Context

Current industry challenges

� Increasing regulatory / tax burden: Need for enhancement in controls, compliance and transparency

� Customer acquisition: Competition between onshore and offshore wealth centers, coupled with challenges in cracking the onshore market

� Revenue mix: The battle for non-capital market solutions is intensifying

� Efficiency: Cost-to-income ratio under pressure as Hong Kong and Singapore become too expensive as booking centers

� Digital: 80% of Asian HNWIs prefer their wealth management relationships to be digital by 2018

� Inter-generational wealth transfer: 80% of the Asian wealth to be transferred in the next 15 year

� Understand current and emerging trends impacting the industry and your bank

� Plan for uncertainties that will potentially influence the industry and your bank

� Establish framework for recognizing and adapting to change over time—ahead of time

Growth Imperatives

Source: RBC Wealth Report; Hubbis

© 2016 Deloitte Consulting Pte Ltd 4

Agenda

Context

Forces of change and implications

© 2016 Deloitte Consulting Pte Ltd 5

There are two types of forces of change outside the organization that will shape future dynamics in predictable and unpredictable ways

Two Types of Driving Forces

Predetermined Trends

� Forces of change that are relatively certain within the relevant timeframe, such as population aging

� It is a given that predetermined elements will play out in the future, though how they interact with and impact other variables remain uncertain

Uncertainties

Predictable Unpredictable

� Unpredictable driving forces, such as public opinion or the state of the economy, that will impact the environment and/or market conditions but whose outcomes are highly uncertain or unknown in the planning timeframe

� How uncertainties may unfold form the basis of a divergent set of scenarios

© 2016 Deloitte Consulting Pte Ltd 6

EXPONENTIAL

IMPROVEMENT OF

TECHNOLOGY

4

5

AGING

ASIA

EMPOWERED

WOMEN

SHARING

ECONOMY

URBANIZ-

ATION

LOCAL

CHAMPIONS

RISE OF THE

GLOBAL CITIZEN

1

2

3

4

5

6

7

Looking ahead to 2025, the wealth management industry will be impacted by seven predetermined trends and may be shaped by six uncertainties in the environment

Uncertainties

Predetermined trends

PRESSURES

ON

COMPANIES

2

3FRAGMENT-

ATIONCONCENTRAT-

ION

1

6

Source: Deloitte – “Hero’s journey through the landscape of the future”

© 2016 Deloitte Consulting Pte Ltd 7

Today, we will discuss implications of selected predetermined trends and uncertainty scenarios on how Service Providers will and should operate in the future

Focus of today’s discussion

1. Pressures on companies

2. Pressures on individuals

3. Barriers to entry, commercialization and learning

4. Fragmentation

5. Concentration

6. Mobilizers

1

2

3

4

5

6

1. Exponential improvement of technology

2. Aging Asia

3. Empowered women

4. Sharing economy

5. Urbanization

6. Local champions

7. Rise of the global citizen

4

5

6

7

3

2

1

Predetermined Trends Uncertainties

© 2016 Deloitte Consulting Pte Ltd 8

In a sharing economy, Service Providers need to enhance product and value propositions to differentiate their platforms (RMs, advice, products)

4

Illustrative impact of predetermined trends on WM i ndustry and Service Providers

Strategic questions for Service ProvidersImpact on WM industry

Predetermined trend: Sharing economy

How to win?

Where to play?

� Value proposition: – How can Service Providers rethink

relationship model to co-create and co-produce with clients or foster collaboration amongst clients?

– How can Service Providers support clients to distill information and in decision making in a world of information and choice overload?

� Profit management: How can Service Providers compete with lower cost providers that rely on crowdsourced ideas rather than cost-intensive proprietary insights?

� Growing interest in interactions and collaboration amongst HNW peers, e.g. co-investments

� Industry competitiveness and cost pressures intensify as FinTechs enter the wealth management space, leveraging virtual networks and crowdsourcing to provide services to clients and to Service Providers

Service provided Example FinTechs

HNW networking

Co-investing

Structured product super mart

� Erosion of exclusivity of opportunities traditionally only available to HNWIs, e.g. ownership of hospitality assets, early stage investing

� Proliferation of investment ideas and advice due to sharing

� Products: What exclusive investment opportunities can Service Providers offer that are unavailable to crowd investors?

� Shared creation, production and consumption of goods and services by people and organizations

� 78% of consumers in Asia are willing to participate in the sharing economy vs. 68% globally

Examples

Source: Tech in Asia; Deloitte Analysis

How can Service Providers achieve differentiation w ith greater transparency and availability of altern ative platforms?

© 2016 Deloitte Consulting Pte Ltd 9

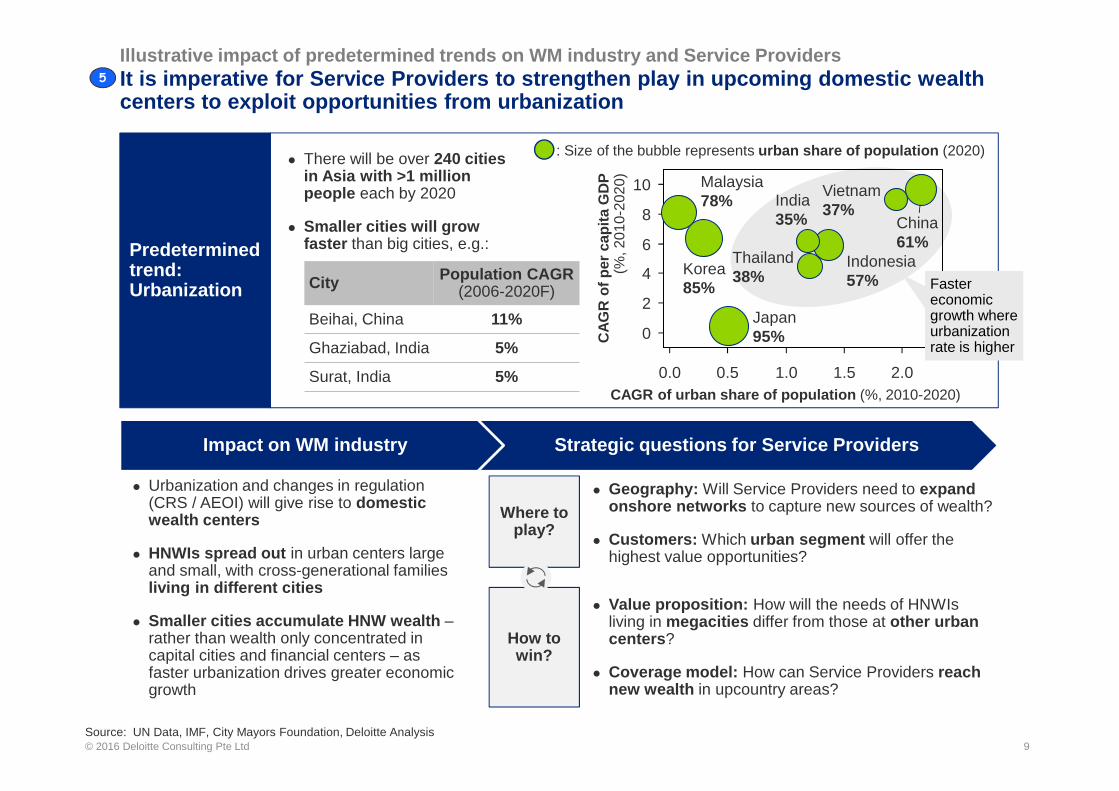

It is imperative for Service Providers to strengthen play in upcoming domestic wealth centers to exploit opportunities from urbanization

Illustrative impact of predetermined trends on WM i ndustry and Service Providers

Strategic questions for Service ProvidersImpact on WM industry

Predetermined trend: Urbanization

� Urbanization and changes in regulation (CRS / AEOI) will give rise to domestic wealth centers

� HNWIs spread out in urban centers large and small, with cross-generational families living in different cities

� Smaller cities accumulate HNW wealth –rather than wealth only concentrated in capital cities and financial centers – as faster urbanization drives greater economic growth

5

10

6

4

2

0

2.0

8

1.51.00.50.0

95%

85%Korea

78%Malaysia

Thailand

Japan

57%Indonesia

35%37%

61%China

38%

VietnamIndia

: Size of the bubble represents urban share of population (2020)

CA

GR

of

per

cap

ita

GD

P(%

, 201

0-20

20)

CAGR of urban share of population (%, 2010-2020)

� There will be over 240 cities in Asia with >1 million people each by 2020

� Smaller cities will grow faster than big cities, e.g.:

Faster economic growth where urbanization rate is higher

� Geography: Will Service Providers need to expand onshore networks to capture new sources of wealth?

� Customers: Which urban segment will offer the highest value opportunities?

� Value proposition: How will the needs of HNWIs living in megacities differ from those at other urban centers?

� Coverage model: How can Service Providers reach new wealth in upcountry areas?

How to win?

Where to play?

Source: UN Data, IMF, City Mayors Foundation, Deloitte Analysis

City Population CAGR(2006-2020F)

Beihai, China 11%

Ghaziabad, India 5%

Surat, India 5%

© 2016 Deloitte Consulting Pte Ltd 10

In a scenario of mounting pressures on individuals, Service Providers need to rethink what clients to focus on and how

2

Potential scenario: Mounting pressures on individuals

Conditions:

� Average lifespan of skills decreases

� Mid-skilled workers are replaced by outsourcing and automation

� Companies resort to layoffs and outsourcing to combat intensified competition

Strategic questions for Service ProvidersImpact on WM industry

How individuals may react / be affected

How to win?

Where to play?

� Value proposition: How can Service Providers effectively redesign the relationship model to serve clients with less time?

� Defensible advantage: How can Service Providers address talent shortage – improve talent management, engage freelancers, automate for efficiency, or establish capabilities-led partnerships (e.g. research)?

� Risk and cost management: How can Service Providers ensure compliance and manage cost with increased regulatory requirements?

� Intensified skill shortage (In 2013, demand for private bankers already outstrips supply by 1,600 bankers in Asia)

� Demanding nature of running own business leads to less time to meet RMs and less time for wealth management

� Individuals prefer self-employment as traditional benefits of employment (e.g. job stability, pension) are eroded

� Compensation gap widens as mid-skilled workers are laid off to be replaced by automation or outsourcing

� Concentration of wealth– less HNWs but UHNWs get richer

� Pressure on governments to scrutinize tax evasionby the privileged

� Customers: With increased intelligence of clients and shorter tenure of PB skills, do Service Providers need to rethink what clients to focus on?

Illustrative impact of uncertainty scenarios on WM industry and Service Providers

High

Low

Pressures on individuals

Source: Deloitte – “Hero’s journey through the landscape of the future”, David Autor – “U.S. Labor Market Challenges over the Longer Term”

© 2016 Deloitte Consulting Pte Ltd 11

Where fragmentation and concentration coexist, Service Providers need to redefine their roles to become niche operators, infrastructure providers, aggregators or agents

5,6

How to win?

� FinTechs commoditize tailored investment advice (e.g. SigFig)

� HNWs demand private banking services when they want it where they want it

� Given more choices, HNWs demand transparency on product features, risks and pricing

� Service Providers forced to adopt one of four new roles: niche operator, infrastructure provider, aggregation platform or agent business

� What should Service Providers become?

Where to play?

� Business model: will depend on which option Service Providers choose

Impact on WM industry

Strategic questions for Service Providers

What are the dynamics in this new ecosystem

� Provide personalized, localized products and services

� Compete on specialization and customization

Niche operators

� Provide physical infrastructure, digital aggregation, or mass agent capability

� Compete on scale and scope

Scale and scope operators

Illustrative impact of uncertainty scenarios on WM industry and Service Providers

Potential scenario: Fragmentation and concentration coexist

Conditions:

� Parts of the economy fragment while other parts concentrate

� More niche operators driven by desire for autonomy and increased ease of managing a business of any scale

� Concentration driven by need for infrastructure, platforms, and agents to support niche operators

Some level of fragmentation and concentration

Fra

gm

enta

tio

n High

LowCo

nce

ntr

atio

n

High

Low

Source: Deloitte – “Hero’s journey through the landscape of the future”

Infrastructure providers: deliver high-volume, routine process services

Aggregation platforms: connect clients with resources and vendors

Agents: serve as a trusted advisor to clients

or

or

or

Niche operators: offer goods and services that fit very specific preferences

Important notice

This document has been prepared by Deloitte Consulting Southeast Asia (as defined below) for the sole purpose of providing a proposal to the parties to whom it is addressed in order that they may evaluate the capabilities of Deloitte Consulting Southeast Asia to supply the proposed services.

The information contained in this document has been compiled by Deloitte Consulting Southeast Asia and includes material which may have been obtained from information provided by various sources and discussions with management but has not been verified or audited. This document also contains confidential material proprietary to Deloitte Consulting Southeast Asia. Except in the general context of evaluating our capabilities, no reliance may be placed for any purposes whatsoever on the contents of this document or on its completeness. No representation or warranty, express or implied, is given and no responsibility or liability is or will be accepted by or on behalf ofDeloitte Consulting Southeast Asia or by any of its partners, members, employees, agents or any other person as to the accuracy, completeness or correctness of the information contained in this document or any other oral information made available and any such liability is expressly disclaimed.

This document and its contents are confidential and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person in whole or in part without our prior written consent.

This document is not an offer and is not intended to be contractually binding. Should this proposal be acceptable to you, and following the conclusion of our internal acceptance procedures, we would be pleased to discuss terms and conditions with you prior to our appointment.

In this document, references to Deloitte are references to Deloitte Consulting Southeast Asia which is an affiliate of Deloitte Southeast Asia Ltd, a member firm of Deloitte & Touche Tohmatsu Limited.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 210,000 professionals are committed to becoming the standard of excellence.

About Deloitte Southeast AsiaDeloitte Southeast Asia Ltd – a member firm of Deloitte Tohmatsu Limited comprising Deloitte practices operating in Brunei, Cambodia, Guam, Indonesia, Lao PDR, Malaysia, Myanmar, Philippines, Singapore, Thailand and Vietnam – was established to deliver measurable value to the particular demands of increasingly intra-regional and fast growing companies and enterprises.

Comprising over 270 partners and 6,300 professionals in 24 office locations, the subsidiaries and affiliates of Deloitte Southeast Asia Ltd combine their technical expertise and deep industry knowledge to deliver consistent high quality services to companies in the region.

All services are provided through the individual country practices, their subsidiaries and affiliates which are separate and independent legal entities.

Disclaimer

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2015 Deloitte Consulting Southeast Asia

Related Documents