Assignment submitted to Crawford School of Public Policy (June 2014) ‘Future of India-China relationship: alternative scenarios for 2030’ Introduction The focus of this paper is the bilateral relationship between India and China in 2030 and is directed at the Indian audience. This paper takes an economic interdependence perspective to analyse possible variations in this bilateral relationship 15 years from now. It is important because the gradual decline of the West is associated with the unprecedented economic growth of these two giants and how it folds out in future affects the global balance of power. It discusses scenarios on India’s future with respect to China’s continued economic growth prospects and their mutual involvement in regional trade agreements. The bilateral relationship between China and India exhibits a mix of contention and interdependence. China and India has historical security issues such as, border disputes, issues on Tibet and Kashmir, China’s military support to Pakistan, US’s increasing ties with India and China’s deepening interest in the Indian Ocean (Small 2014, p.5). Over the last decade however, China and India has increased their economic interdependence with rapidly growing trade between the two nations (GoI 2014). In terms of global affairs, China and India appear to converge on issues that 0

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Assignment submitted to Crawford School of Public Policy

(June 2014)

‘Future of India-China relationship: alternative scenarios for 2030’

Introduction

The focus of this paper is the bilateral relationship

between India and China in 2030 and is directed at the

Indian audience. This paper takes an economic

interdependence perspective to analyse possible variations

in this bilateral relationship 15 years from now. It is

important because the gradual decline of the West is

associated with the unprecedented economic growth of these

two giants and how it folds out in future affects the

global balance of power. It discusses scenarios on India’s

future with respect to China’s continued economic growth

prospects and their mutual involvement in regional trade

agreements.

The bilateral relationship between China and India exhibits

a mix of contention and interdependence. China and India

has historical security issues such as, border disputes,

issues on Tibet and Kashmir, China’s military support to

Pakistan, US’s increasing ties with India and China’s

deepening interest in the Indian Ocean (Small 2014, p.5).

Over the last decade however, China and India has increased

their economic interdependence with rapidly growing trade

between the two nations (GoI 2014). In terms of global

affairs, China and India appear to converge on issues that

0

Assignment submitted to Crawford School of Public Policy

(June 2014)have potential of affecting their growth and trade such as

‘climate negotiations, the Doha trade talks and in the

context of BRICS’ (Small 2014, p.5).

China became the largest trading partner of India in 2011

accounting for a total of US$ 73.9 billion (Varma 2012).

Accordingly, in financial year 2013/14, China became the

top country of import for India, with a share of 11.47 per

cent of total imports while during the same period, India’s

export to China consisted only 4.83 per cent of total

exports incurring a huge trade deficit with China (GoI

2014). On the contrary, for China, India ranked 15th in

terms of bilateral trade volume in 2012 with a share of

1.72 per cent of China’s overall trade, comprising a 2.33

per cent of total Chinese exports and with a share of 1.1

per cent in overall imports by China, ranked 19th among

countries exporting to China (EoI n.d.). China is an

important trade partner for India but for China, India

appears to be less important compared to other countries.

In terms of export alone, interestingly, for both

countries, the top export destinations are US and EU with a

share of 29.6 per cent of total export for India and 33.5

per cent for China (WTO 2014). This could change with

mutual trade based on comparative advantage.

In current bilateral economic relationship between India

and China, India appears to be vulnerable in terms of

relative bilateral trade volume and its increasing

dependence on cheap Chinese exports. This could however

1

Assignment submitted to Crawford School of Public Policy

(June 2014)change in future if national and regional policies move in

a positive direction beneficial to both the countries. With

election of forward looking economy focused Prime Minister

Narendra Modi, India has a huge potential to tap on its

demographic dividend by developing its manufacturing sector

and benefiting from regional trade agreements.

Driver 1: Economic growth as a driver of relationship

Trade ties between the two countries is fuelled by both

countries’ high economic growth ambitions. As bigger

economies have varied import and export base, the bilateral

trade created an economic interdependence (Gupta & Wang

2009). Chinese and Indian economic growth has increasingly

gained global and regional attention such as in the Asia-

Pacific Economic Cooperation (APEC) forum and in the G-20

(Wolf et al. 2011, p.37) as the unfolding of their

relationship would affect global economy in future. The

current economic growth experienced by India and China has

attracted global focus as these countries continue to

expand its GDP and increase its global share. Even though

international trade gradually increased with liberalisation

policies, the bilateral trade between India and China took

off only after 2001 when China acceded to WTO (Mohanty

2013, p.48). India has recorded gradual decline from 10.3%

growth rate in FY2010/11 but is expected to gradually

increase through FY2014/15 (Times of India 2014).

2

Assignment submitted to Crawford School of Public Policy

(June 2014)Currently, India has not been performing well in

manufacturing sector. It has stagnated at 16 per cent of

the GDP and constitutes only about 2 per cent in global

manufacturing share (Bhunia 2014). Failure in increasing

manufacturing sector is considered the biggest failure with

respect to growth (Times of India 2014). Between 2005 and

2011, India’s manufacturing sector grew by about 10 per

cent Compound Annual Growth Rate (CAGR) but decreased after

that; however, government officials have recognized its

importance for growth and have been taking steps to revive

the manufacturing industry (Das 2014). With Narendra Modi

as prime minister, India could revive its manufacturing

sector with its multiplier effect and can contribute to and

sustain its economic growth. According to a study by global

management consulting firm McKinsey and Company, India’s

manufacturing sector may exceed US$ 1 trillion by 2025,

mainly due to rising demand within the country and

establishment of low-cost plants by multinational companies

(IBEF 2014). This will have a significant impact in the

economy with creation of jobs and increased investment.

This will further increase the total exports and help

sustain the economic growth.

On the other hand, if India fails to develop its

manufacturing industry due to ‘high manufacturing cost

because of its failure to do labour reforms’ (Mohanty 2013,

p.56), then it will have a tremendous effect on economic

growth of the nation.

3

Assignment submitted to Crawford School of Public Policy

(June 2014)

Driver 2: Regional economic integration through Regional

Comprehensive Economic Partnership (RCEP)

China and India both concur with a view that regional trade

can be augmented through regional platform. RCEP represents

30 per cent of world GDP and makes up 29 per cent of world

trade (Wignaraja 2013). For India, RCEP is a realisation of

India’s farsighted pursuit of ‘Look East’ policy since 1990

with potential pragmatic benefits. While bilateral free

trade agreements with ASEAN exists for both India and

China, RCEP will further lower trade barriers and custom

duties throughout the region once it finalises in 2015

(China Briefing 2012). The association of India into RCEP

therefore would serve its long-term economic interests

better. India would be able to gain from export industry

which currently is not performing very well. RCEP would not

only generate trade opportunities, it would also maximise

welfare gains when ASEAN+6 countries get integrated into it

(Mohanty 2013, p.119). Contrarily, China had already been

interacting with ASEAN countries through ASEAN+3 (APT)

framework. In the East Asia Summit, China suggested

preference of APT as a regional framework rather than

ASEAN+6 where India would also be a member through RCEP

process. India’s presence in the RCEP however presents with

significant welfare gains to the whole region, which could

amount to US$502.8 billion depending on the level of

liberalisation (Mohanty 2013, p.108).

4

Assignment submitted to Crawford School of Public Policy

(June 2014)The negotiation for RCEP is due to end by 2015. The future

of Asia-Pacific and the China-India relationship rests

significantly on how this process ends. After 2015, the

RCEP process might conclude with the inclusion of both

India and China with ramifications for regional trade for

both countries. On the other hand, it may not conclude

successfully or may get extended into future, in which

case, India run the risk of not being integrated into the

regional trade, which might come with a cost for its

economy as a whole.

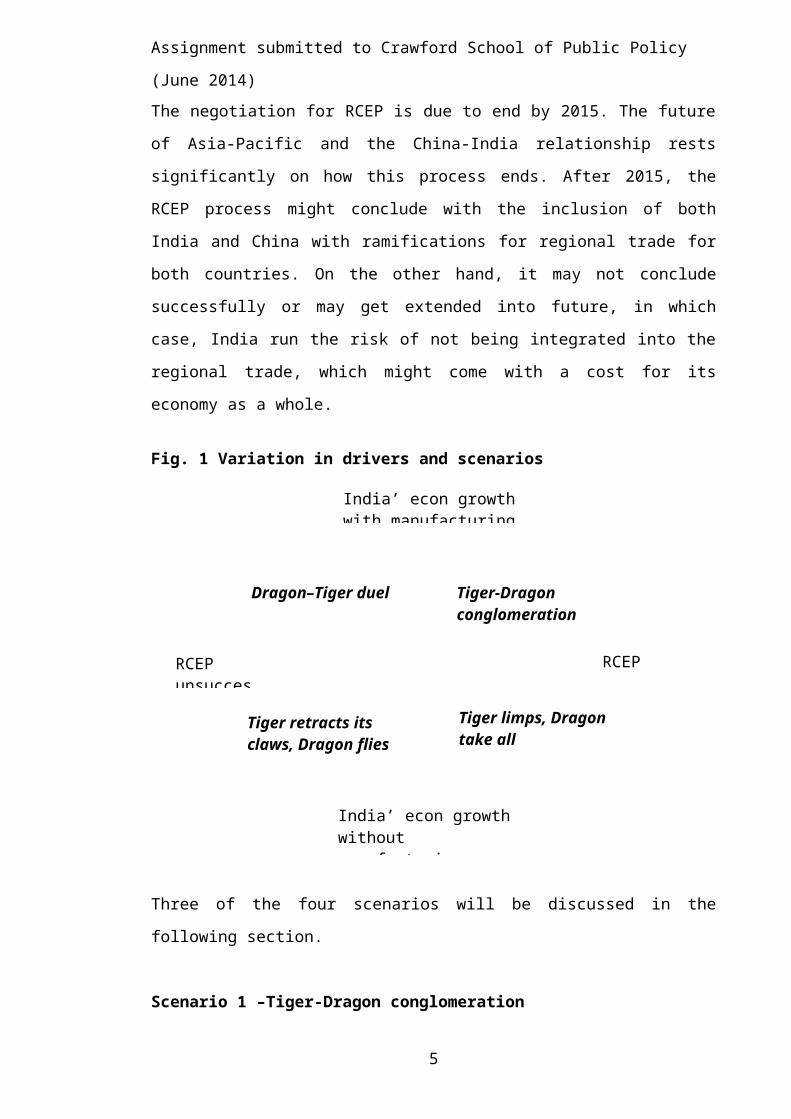

Fig. 1 Variation in drivers and scenarios

Three of the four scenarios will be discussed in the

following section.

Scenario 1 –Tiger-Dragon conglomeration

5

RCEP unsucces

Dragon–Tiger duel

India’ econ growthwithout manufacturing

India’ econ growthwith manufacturing

RCEP successful

Tiger-Dragon conglomeration

Tiger limps, Dragon take all

Tiger retracts its claws, Dragon flies

Assignment submitted to Crawford School of Public Policy

(June 2014)India’s high economic growth fuelled by development of

manufacturing industry and realization of ‘Look East’

policy through successful Regional Comprehensive Economic

Partnership has paved way to the rise of India as the third

largest economy in the world. Both India and China are

experiencing 8 to 10 per cent annual growth rates (Wolf et

al 2011, p.38). There is a strong economic interdependence

between India and China. A decade in the office (Stobdan

2014), Indian Prime Minister Narendra Modi boosted the

economy as anticipated by general public with his first win

in 2013/14 (Tellis 2014) with development of

infrastructures, reformulation of labour policies, opening

up of economy and increasing trade ties with China and

placed a benchmark to fuel economic growth in manufacturing

industries. India’s manufacturing sector exceeded US$1

trillion as predicted by McKinsey and Company (IBEF 2014).

The cost of production is low due to policy reforms adding

to the cost competitiveness of India products vis-à-vis

Chinese products. This created numerous jobs for the

increasing youth population, enabling India to cash on

demographic dividend. On the other hand, President Xi

Jinping and Premier Li Keqiang’s also continued to hold

their office in China (Stobdan 2014), which resulted in

continuous growth in Chinese economy. As forecasted by Wolf

et al. (2011), Chinese total GDP amounts to $30 trillion

and India’s GDP totals $12 trillion (p.54). As the largest

economies, the two countries increase their bilateral trade

playing on comparative advantages of each country. Export

specialization has taken place and differences in export

6

Assignment submitted to Crawford School of Public Policy

(June 2014)sector is visible. As argued by Aziz et al. (2006), India’s

exports are now concentrated in natural textiles and

garments industry and China exports manmade fibres (p.277).

China has shifted its focus on high-tech manufacturing such

as electronics and telecommunications while India has

boomed labour-intensive manufacturing in combination with

boom in pharmaceutical, chemical, and automobile industry.

The successful integration of China and India through RCEP

process opened up ASEAN markets for their products. RCEP

placed both China and India into a high growth path that

made these two countries the largest economies. RCEP has

been trade creating in nature with absolute increase in

welfare gains amounting to US$502 billion per annum as

forecasted by Mohanty (2013, p.109). The economic

integration in combination with the growth in manufacturing

sector in India compensated for the trade deficit that

India was long experiencing. While trade between India and

China increased multi-fold, trade diversification in terms

of exports into ASEAN countries in addition to domestic

growth through manufacturing industry shielded both the

countries from shocks in global financial market. This

further contributed towards sustained and long-term

economic growth. The economic growth in India will make the

bilateral relationship stronger but sensitive, as both

countries now exert similar economic power and one cannot

afford to forego the other. The strong economic

interdependence paves way to a new chapter in history where

7

Assignment submitted to Crawford School of Public Policy

(June 2014)two giants, ‘the dragon’ and ‘the tiger’ conglomerate to

influence the world.

Policy Recommendations:

With a strong bilateral relationship with China and better

positioning globally, India should focus on sustaining the

economic growth. India should continue to explore its

export competitiveness globally, and China in particular,

for varieties of products to fuel export led growth

together with domestic demand-led growth. Pursuing export-

led growth would heighten economic integration with ASEAN

through RCEP (Mohanty 2013, p.19-20). India should continue

to invest in agricultural commodities, iron ore and natural

fibres to export to China. India should perform education

reforms as part of structural reform to sustain its high

economic growth. The growing youth and urban population

would demand increased jobs, so India should explore

opportunities to create jobs within the nation. According

to McKinsey & Company estimates, India will need to spend

US$1.2 trillion on urban infrastructure by 2030, which is

eight times higher than its spending on infrastructure in

2011(Wignaraja 2011)

Rising per capita income might demand a shift from labour-

intensive industries to high paying high-tech and skilled

industries. Necessary transitioning environment should be

developed by India to accommodate such transition. The

balance between trade and political rivalry with China

8

Assignment submitted to Crawford School of Public Policy

(June 2014)should be handled cautiously so as not jeopardise bilateral

economic relationships.

Early Warning Indicators:

The indicator for strong economic interdependence between

India and China will start to be visible with their

increased growth in bilateral trade and decreasing trade

deficit, with successful negotiation of RCEP and with

formulation of labour reform policies in India. By 2020,

China-India trade would be greater than US$400 billion

(Gupta & Wang 2009). The composition of export and import

items will start to change. The subsequent growth in

manufacturing industry in India will signal unprecedented

future growth which calls for acting on comparative

advantage to complement with China’s growth. Influx of

infrastructure projects would be another indicator that

high and sustainable economic growth is near.

Scenario 2: Tiger limps, Dragon take all

India has fallen back from its economic growth path, which

suffered due to its inability to develop manufacturing

sector, which is mainly due to lack of infrastructure and

labour reform policies. However, India successfully got

integrated into the RCEP process through negotiations which

ended in 2015. Against peoples’ aspiration, Prime Minister

Narendra Modi could not deliver growth to the Indian

economy as he got into a turmoil on Hinduism debate. He did

9

Assignment submitted to Crawford School of Public Policy

(June 2014)not stay in the office for full-term. He was forced to

resign due to vote of no confidence within his own party.

India’s exports suffered due to inability of exporters to

take advantage of opening up of market and less developed

manufacturing sector. FY 2013/14 was the worst year for

manufacturing industry in India, when it experienced a

decline of 0.2% (Das 2014). This trend was not able to be

reversed even after change of subsequent governments mainly

due to peoples’ loss of confidence in domestic

manufacturing. The high-tech manufacturing sector, which

was 28 per cent of total manufacturing (Dhar & Rao 2014,

p.43), fell significantly after the global financial crisis

and are now dominated by cheap yet branded Chinese exports.

India was not prepared to take advantage from the

opportunities created by regional integration through RCEP.

In fact, China and ASEAN countries have surged their

exports to India, further deteriorating its manufacturing

sector. The need to revitalise the manufacturing sector had

been well articulated in 2011 by then finance minister,

Pranab Mukherjee with adoption of National Manufacturing

Policy (Dhar & Rao 2014, p.43). The subsequent Prime

Minister Narendra Modi with his forward looking growth-

focused vision attempted to materialise the policy but

could not do so due to inability to implement policies that

added domestic value, enhanced technological depth and

ensured sustainability of growth with creation of jobs.

China on the other hand is experiencing double digit growth

at 10 per cent annually due to its integration into RCEP

10

Assignment submitted to Crawford School of Public Policy

(June 2014)and expansion of market into countries and areas where

India failed to develop.

Policy recommendations:

India should retrace its steps and think of the mistakes it

has made. To boost manufacturing sector, India should

change its indirect taxes, including cutting the excise

duty on selected capital goods and consumer goods including

electrical and construction to 10 per cent as well as

automobile industry (Das 2014). Devolution of power to

states is key to allow individual states to grow and

prosper taking its local advantage. India should focus on

development of infrastructure at strategic locations first,

followed by gradual expansion to other areas. India should

work on the comparative advantage based on natural and

human resources it has and target export sectors. Clarity

in policies to develop and strengthen the manufacturing

base will not only enhance its investment, it will also

result in consumption that is needed to fuel growth.

Similarly, products with comparative advantage will have

comfortable availability of market in China and the ASEAN

region. India should attract FDIs in infrastructure

development and in sectors where Indian investors are

unwilling to invest.

Early warning indicators:

11

Assignment submitted to Crawford School of Public Policy

(June 2014)India’s continued slump in economic growth over the last

two years should gradually pass by and with Modi into power

and with his economic growth-focused vision, India should

start to see year-on-year growth in economy in the first

half of the decade. The development of labour reform

policies and initiation of infrastructure projects

especially roads, will be another indicator to notice. If

these policies are not placed within next few years, then

it is an ingredient for the scenario to pass by 2030.

Scenario 3: Dragon-Tiger duel starts

India attains high economic growth with development of

manufacturing sector and but failed to negotiate

successfully in RCEP process. The successful development of

manufacturing sector with its multiplier effect results in

high economic growth rate at 8 per cent annually as

predicted in Global Trends 2030 by National Intelligence

Council (NIC 2012, p.16). Economic growth is generated due

to boosting investment and boosting domestic consumption as

argued by Vuving (2012, p.405). But due to the failure of

RCEP process, India is not integrated into the ASEAN

region. And the greater Asian economy. As a result, India

has lost the US$ 75 billion which it could have benefited

from regional trade if it had been integrated with ASEAN

through RCEP (Mohanty 2013, p.119). India’s economic growth

is mostly fuelled by domestic demand and the rising middle-

income class, but it is still challenged to find jobs for

the huge youth population, with rising inequality,

12

Assignment submitted to Crawford School of Public Policy

(June 2014)disparities in regional infrastructure development and

educational differences (NIC 2012, p.78). The textile

industry is performing very well but the wage rate is

rising and the rising middle class now expects better

paying and skilled jobs. There is fear that domestic

political stability might be dampened and China might make

an economic invasion into the Indian market. The export

sector is not performing well. Failure to tap into Asian

market and competition with China for limited Indian

products in Western market has placed India into a position

where sustaining economic growth is a year-on-year effort.

Even the domestic market is flushed with a surge of cheap

Chinese imports that has a brand recognition globally.

These Chinese imports have not allowed Indian high-tech

sector to grow such that India is highly dependent on

imports for high tech electronics, mobile phones and

technology.

On the other hand, China enjoys regional economic

integration through APT. Both China and ASEAN benefit from

this regional integration. Chinese exports have gotten high

brand recognition both in the Western market as well as in

the Asian market. China easily outpaces India when

competing for similar products and most of the Indian

exports consist only of raw materials. While export sector

is not developed very well, India struggles to get into the

regional market and with trade barriers and tariffs, Indian

products get treated differently than Chinese products in

the ASEAN region. China’s total working-age population has

13

Assignment submitted to Crawford School of Public Policy

(June 2014)declined from 994 million to 961 million (NIC 2012, p16),

but due to the change in industrial policy in 2015 and

shifting more to high-tech intensive products from labour

intensive products, this demographic change made little

impact to the overall growth of the economy of China.

Reformed national policies in combination with regional

economic integration through RCEP makes China continue to

experience growth at around 8 per cent annually.

The economic interdependence between India and China is

therefore of contention and rivalry. This has little

potential to fuel military conflict, as liberal theorists

argue the ‘economics’ win over the politics. The economic

interdependence here is of competition for India and

domination for China in international market. China

continues to seek opportunities to expand its exports into

the India market by supplying cheap branded Chinese high-

tech electronic products and increase FDI in India, while

India tries to safeguard its domestic market from Chinese

invasion.

Policy recommendations:

India should reconsider its State-Centre relations and

devolve central power to states as much as possible as

argued by Debroy, Tellis and Trevor in their forthcoming

book ‘Getting India Back on Track: An Action Agenda for

Reform’. Because high economic growth is attributed mostly

to domestic demand-led growth, the challenge for fast

14

Assignment submitted to Crawford School of Public Policy

(June 2014)growing economy like India is to insulate this domestic

growth from taking its share by foreign markets. As local

conditions vary and known best by the states, India should

provide sufficient decisive capacity for its state

governments to deal with the challenges that arise from

high economic growth. A forward-looking regulatory

mechanisms need to be developed to deal with the high

corruption (Vaishnav & Kapur 2014).

A combination of structural reform and education reform

policies need to be developed and implemented. Increased

wage rate and heightening inflation should be dealt with

appropriate monetary policies. India should continue its

dialogue with China and ASEAN towards regional integration

as preferential access to the Chinese and ASEAN market

would be beneficial to India (Berry 2011). Historically the

rivalry between India and China begins with their goal of

acquiring same things at the same time (Malik 2012, p.347).

As such, India should work on its comparative advantage to

penetrate both Chinese market as well as global market.

Additionally, bold structural and macro policies such as

product market liberalisation and labour market reforms can

enhance growth and reduce any imbalances (Johansson 2012,

p.27)

Early warning indicators:

India should see this scenario coming with completion of

RCEP negotiation in 2015. Succesful realisation of Modi’s

15

Assignment submitted to Crawford School of Public Policy

(June 2014)long-term vision playing into practice with reform and

growth-focused policies during his term in the office

should also signal high growth for the India economy. More

focus on domestic demand-led growth and less focus on

export-led growth will be visible through national periodic

plans in order to make an educated guess of whether the

scenario is going to pass.

16

Assignment submitted to Crawford School of Public Policy

(June 2014)References

Aziz, J, Dunaway, S & Prasad, E 2006, China and India: learningfrom each other: refoms and policies for sustained growth, InternationalMonetary Fund, Washington.

Berry, S 2011, ‘The India China strategic economicdialogue’, East Asia Forum, viewed 22 May 2014, <http://www.eastasiaforum.org/2011/09/26/the-india-china-strategic-economic-dialogue/>.

Bhunia, A 2014, ‘Why India must revive its manufacturingsector’, The Diplomat, 25 February, viewed 21 April 2014,< http://thediplomat.com/2014/02/why-india-must-revive-its-manufacturing-sector/>.

China Briefing 2012, ‘China to join RCEP, creating massive free trade area with ASEAN, India, and Japan’, China Briefing,9 November, viewed 31 May 2014,<www.china-briefing.com/news/2012/11/09/china-to-join-rcep-creating-massive-free-trade-area-with-asean-india-and-japan.html>.

Das, G 2014, ‘The wheels are off’, Business Today, 16 March,viewed 19 April 2014,<http://businesstoday.intoday.in/story/manufacturing-sector-is-dragging-down-india-economic-growth/1/203616.html>.

Dhar, B & Rao, C 2014, India’s current account deficit:causes and cures, Economic and Political Weekly, vol. 49, no. 21,pp.41-45.

EoI, see Embassy of India

Embassy of India n.d., Trade and commercial relations,India-China bilateral relations, Embassy of India, Beijing,viewed 31 May 2014,< http://www.indianembassy.org.cn/DynamicContent.aspx?MenuId=3&SubMenuId=0>

GoI, See Government of India

17

Assignment submitted to Crawford School of Public Policy

(June 2014)Government of India 2014, System on Foreign Trade Performance Analysis (FPTA), Ministry of Commerce and Industry, Department of Commerce, viewed 16 April 2014, <http://commerce.nic.in/ftpa/cntq.asp>.

Gupta, AK & Wang, H 2009, ‘China and India: greater economic integration’, China Business Review, viewed 23 May2014,<www.chinabusinessreview.com/china-and-india-greater-economic-integration/>.

IBEF 2014, ‘Manufacturing: brief introduction’, India BrandEquity Foundation, viewed 19 April 2014,< http://www.ibef.org/industry/manufacturing-sector-india.aspx>.

Johansson, A, Guillemette, Y, Murtin, F, Turner, D,Nicoletti, G, Maisonneuve, C, Bagnoli, P, Bousquet, G &Spinelli, F 2012, ‘Looking to 2060: long-term global growthprospects’, OECD Economic Policy Paper Series no. 03, OECD.

Malik, M 2012, India balances China, Asian Politics and Policy, vol. 4, no. 3, pp.345–376.

Mohanty, SK 2013, ‘India-China bilateral trade relationship’, Reserve Bank of India, viewed 16 April 2014,<http://rbidocs.rbi.org.in/rdocs/Publications/PDFs/PRSICBT130613.pdf>.

NIC, see National Intelligence Council

National Intelligence Council 2012, Global trends 2030: alternative worlds, National Intelligence Council, viewed 30 May 2014,< http://info.publicintelligence.net/GlobalTrends2030.pdf>.

Small, A 2014, Regional dynamics and strategic concerns inSouth Asia: China’s role, Background paper of the CSISProgram on Crisis, Conflict, and Cooperation, Center forStrategic & International Studies, viewed 11 April 2014,<http://csis.org/files/publication/140127_Small_RegionalDynamics_China_Web.pdf>.

18

Assignment submitted to Crawford School of Public Policy

(June 2014)

Stobdan, P 2014, ‘Indo-China ties and economics’, Agenda,The Pioneer, 25 May, viewed 31 May 2014,<http://www.dailypioneer.com/sunday-edition/agenda/foreign-policy-special-issue/indo-china-ties-and-economics.html>.

Tellis, AJ 2014, ‘Productive but joyless? Narendra Modi andUS-India relations’, Carnegie Endowment for InternationalPeace, viewed 20 May 2014,<carnegieendowment.org/2014/05/12/productive-but-joyless-narendra-modi-and-u.s.-india-relations/han1>.

Times of India 2014, ‘Indian manufacturing stagnates due topeculiar labour laws: Meghnad Desai’, Times of India, 21March, viewed 19 April 2014,<http://timesofindia.indiatimes.com/business/india-business/Indian-manufacturing-stagnates-due-to-peculiar-labour-laws-Meghnad-Desai/articleshow/32424439.cms>.

Vaishnav, M & Kapur, D 2014, ‘Strengthening India’s rule oflaw’, Carnegie Endowment for International Peace, viewed 29May 2014,< http://carnegieendowment.org/2014/05/27/strengthening-india-s-rule-of-law/hbpa>.

Varma, KJM 2012, ‘2011: India-China Trade Hits All TimeHigh of $ 73.9 Bn’, Outlook (online), 29 January, viewed 17April 2014,<http://news.outlookindia.com/items.aspx?artid=749460>.

Vuving, AL 2012, The future of China's rise: how China'seconomic growth will shift the Sino‐US balance of power,2010–2040, Asian Politics & Policy, vol. 4, no. 3, pp.401-423.

Wignaraja, G 2013, ‘Why the RCEP matters for Asia and theworld’, East Asia Forum, viewed 20 May 2014,<http://www.eastasiaforum.org/2013/05/15/why-the-rcep-matters-for-asia-and-the-world/>.

Wignaraja, G 2011, ‘Can India really surpass China’, EastAsia Forum, viewed 20 May 2014,< http://www.eastasiaforum.org/2011/09/28/can-india-really-surpass-china/>.

19

Assignment submitted to Crawford School of Public Policy

(June 2014)

Wolf Jr, W, Dalal, S, DaVanzo, J, Larson, EV, Akhmedjonov,A, Dogo, H, Huang, M & Montoya, S 2011, China and India, 2025: acomparative assessment, RAND Corporation, Santa Monica.

WTO, see World Trade Organization

World Trade Organization 2014, Trade profiles, Statisticsdatabase, World Trade Organization, viewed 30 May 2014,<http://stat.wto.org/CountryProfile/WSDBCountryPFView.aspx?Language=E&Country=CN%2cIN>.

20

Related Documents