1 BANKING ON INNOVATION: UNCOVERING THE POLITICAL BARRIERS TO INNOVATIVE FINANCIAL SERVICES John Fearn Interel Financial Services June 2014

Future of Financial Services - Banking on Innovation - Final Paper

Aug 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

BANKING ON INNOVATION: UNCOVERING THE POLITICAL

BARRIERS TO INNOVATIVE

FINANCIAL SERVICES

John Fearn

Interel Financial Services

June 2014

2

Contents

Introduction ........................................................................................................ 3

Scope and methodology ................................................................................. 3

A vision for future financial services .................................................................... 4

Why now? ....................................................................................................... 5

Political risk ..................................................................................................... 8

Sector analysis ................................................................................................. 10

Alternative finance ........................................................................................ 10

Payments and commerce ............................................................................. 18

High street financial services ........................................................................ 22

Conclusions ...................................................................................................... 26

About Interel ..................................................................................................... 27

Contacts ....................................................................................................... 27

3

Introduction Radical change in any sector of the economy poses challenges to politicians and

regulators but nowhere is this more apparent than in financial services.

The pace of innovation and the emergence of disruptive new models is leaving

policy-makers behind. In an age when consumer protection is an overriding

priority for authorities, it is not easy to craft policies and regulations that do not

overly inhibit diversity and competition.

In such an environment, the dominant perception of a product, service or

business can be critical to influencing the rules under which firms have to

operate. This is why Interel has conducted its own research to benchmark the

attitudes of political stakeholders towards some of the newer services against

more traditional providers.

By doing so, we have been able to determine the political reputations of different

providers and identify the challenges that these firms face in influencing their

own regulatory environment.

Scope and methodology

Our political audit covers a wide range of retail services including alternative

finance providers, payments services, and the high street bank and mutual

sectors. We believe that such a broad scope is necessary if we are to

understand the political views of the future industry as a whole.

The findings in this paper are based on two main forms of primary research:

Parliamentary opinion polling conducted in partnership with Populus, and first-

hand interviews with various stakeholders.

4

A vision for future financial services What does the future hold for financial services? Will we tell our driverless cars

to take us to our local bank branch? And when we plug in and recharge our car

on the way to the bank, how will we pay? Will cash still be king? Where will we

get the loan for our intelligent automobile?

It is tempting either to make hyperbolic suggestions about the future of financial

services, or to dismiss radical thinking on the basis that change is always slower

and more incremental than the blue-sky thinkers would like. It is the accepted

wisdom that consumers are inherently cautious, particularly where finance is

concerned and there is a historic record of consumer satisfaction/apathy (delete

as appropriate depending on your point of view) to support this stance. However,

it is possible to envisage in the near future a retail financial services market that

is radically different to that in operation over the past 30 years.

Here are some predictions for the UK market:

Banks and building societies won’t disappear from our high streets but

branch networks will be pared back drastically and the average customer

will only visit for major transactions such as mortgages.

Partnerships between banks and supermarkets or other retail chains in

order to address financial exclusion will increase but are not here to stay.

The overwhelming majority of everyday transactions will be conducted

digitally. Physical debit and credit cards become almost entirely

redundant but not extinct, in the same way that cheques remain popular

among certain consumer groups.

Mobile payments take off significantly – coffee houses, retail chains and

public transport in the forefront. Mobile and ‘wearables’ add another layer

of security to overcome trust issues.

The provision of banking services will become fragmented:

o Providers, products and services in traditional areas like current

accounts, overdrafts and personal loans diversifies.

o Customers create bespoke accounts with third-parties providing

smart money management services, simple but powerful

5

comparison tools, and reward-based retail relationship

management.

o Tech, retail and other service firms merge into the finance

industry to meet consumer demand for seamless transaction

experiences in their everyday life.

20% of consumer and SME lending will be through alternative lenders.

Financial advice effectively becomes crowd sourced as social media use

brings a return to ‘word-of-mouth’ endorsements (despite the best

intentions of the regulator).

Why now?

Many leading FinTech firms that are attracting headlines and major investment

are not start-ups, they are established firms; Zopa, for example, was set up back

in 2005. Equally, it has been apparent for some time that competition in the

traditional retail markets had not yet delivered genuine alternatives to satisfy

consumer demand. There have been four separate official reviews of the

personal current account market since 2000, all of which have come to the same

basic conclusions. In the savings market, price comparison websites have led to

a plethora of providers competing hard against each other but essentially

offering the same products. As a Bank of England official recently commented,

for too long diversification has been mistaken for diversity.

Throughout this paper we will talk about the role of technology in creating a new

financial services landscape but if innovation is a constant process what is

different now that enables radical change?

It is a combination of two factors: take up of mobile technology and the impact of

the 2007-09 financial crisis.

Firstly, consumer habits have been irreversibly changed with the widespread

adoption of smart mobile devices and the exponential growth in accompanying

services. Customers are no longer tied to a physical entity chosen because of its

convenient location so they are choosing the services that best meet their needs.

This change is affecting financial services but the big financial brands are mostly

responding to it rather than shaping it because this shift in consumer demand is

being driven by others. Some of the large banks have responded better than

others – Barclay’s mobile banking app and Pingit services have won awards and

6

customers – but as Paul Purcell, a leading US investor in consumer FinTech,

says everyday commerce has been influential:

“The nature of commerce is fundamentally changing. Online has

deconstructed the whole retail process, empowering customers by giving

them choice and changing their expectations across all sectors.

Commercial success becomes about how you deal with consumers now,

how well to you meet their exact need, and how easy you make it.

Customers now expect great service and frictionless transactions at a

minimum – areas in which traditional financial services providers have

not typically excelled.”

Mobile commerce continues to grow and the emergence of the app both as retail

portal and revenue generator through in-app micro transactions clearly has

consequences for the payments industry and the need for physical bank

networks but it is also symptomatic of a consumer base that is increasingly

comfortable trusting alternative providers offering diversity through novel

products or compelling services.

The second factor is directly related to the global financial crisis. The effects of

the credit crunch on personal and SME finance are still being felt despite a range

of government initiatives aimed at increasing the flow of funding to the real

economy. The dichotomous nature of financial services policy – regulate to

prevent a recurrence of the last crisis while promoting lending to SMEs and

homebuyers – hasn’t helped, especially when the ‘stick’ for non-compliance with

capital requirements is much more feared than the negative publicity received for

not lending to small firms. Furthermore, authorities’ actions to stabilise the

financial sector and increase liquidity has depressed yields in many classes of

securities like gilts and bonds. For example, in the UK quantitative easing and

the Funding for Lending scheme has given banks easy access to funding so

investors searching for better returns are being forced to look elsewhere.

7

Lending to UK businesses Lending to SMEs

Lending to consumers Source: Bank of England Trends in Lending Report April 2014

It has often been asserted that consumers and businesses are shunning banks

because of ethical concerns and residual anger for the role ‘big finance’ played

in causing the financial crash and ensuing recession. This sentiment is

undoubtedly in abundance among indebted individuals or small businessmen

who have been denied finance as well as more activist-minded people, and a

general but widespread antipathy towards to ‘banks’ still lingers. It is important to

understand customers’ motivations: people who are more open to alternatives

because their trust in the established sector has been damaged will be looking

for a product, a service or a supplier that offers a fresh ‘non-bank-like’

experience while those who have been denied by banks might be from the riskier

end of the borrower spectrum and are looking for any way to get the finance they

need.

This is not the place to examine in detail banks’ lending volumes or pricing. Even

though the main banks are still by far the largest lenders to consumers and

SMEs the alternative finance sector received a shot in the arm when they

curtailed their lending.

8

Political risk

So if consumers’ needs are being met and new firms are bringing innovation to

the market, creating competition and driving diversity, are there any clouds on

the horizon?

Innovation is almost always used in a positive sense but just because something

is innovative or new does not mean it is automatically without problems. Firms

often consider risk from a commercial or legal stance, and overcoming these

issues on the way to market can be a significant effort. We consider political risk

to be one of the most important factors in business planning yet it is all too often

overlooked until it is too late.

Political risk can manifest itself in a variety of ways from damaging publicity to

regulatory enforcement action. Sources of political risk also vary: partisan

attitudes towards certain industries, a lack of political and regulatory

understanding of new products and services, flaws in firms’ business models,

regulatory reform programmes, conduct scandals and even elections generate

risk. Sometimes the very reason for a model’s success opens it up to political

and regulatory censure and quite often, difficulties in one sector or one firm can

affect the outlook for a whole industry.

In the UK, the Financial Conduct Authority (FCA) has recognised the importance

of understanding innovative business models before they reach the market at

scale. It has launched a new programme, dubbed Project Innovate, that aims to

ensure positive developments in areas such as mobile banking, online

investment or money transfer are supported by the regulatory environment.

Under the auspices of this project the FCA will provide compliance expertise to

firms developing new models or products, and provide an ‘incubator’ to “support

innovative, small financial businesses getting ready for authorisation”.

The Government has also expressed its official enthusiasm for more diversity

and innovation in financial services. The Treasury recently consulted on plans to

force UK banks to direct customers whose loan applications they reject to

alternative finance providers. In 2013 the Government agreed to lend to SMEs

through FundingCircle and in February 2014 allocated £40m of funding from the

9

British Business Bank to be distributed through the peer-to-peer lending

platform1.

However, there are some cautionary tales showing how innovation is not without

its challenges. Consider the example of ClearAccount2, a firm that offers an

automatic top-up service designed to stop current account holders going into

overdraft. In theory, one can see the merit in such a service, and ClearAccount

was licensed by the Office of Fair Trading under the previous consumer credit

regime and is now authorised by the FCA.

However, two elements of the ClearAccount model were always likely to attract

attention at a time when political focus is on the short-term, high cost credit

market. First, the rate of interest charged on the top-up loans puts them into the

same bucket as payday lenders, and second, the firm requested customers’

online banking details in order to know when to put credit into their accounts.

ClearAccount says it is providing an attractive alternative to higher cost

unauthorised overdraft charges; Stella Creasy PM, the shadow consumer affairs

spokesperson and longstanding campaigner on fair finance, said “automatically

topping up someone’s finances is a new low”. Media and regulatory

investigations have followed.

The example shows that firms offering new services or products have to be

aware of the political context in which they operate. Regulatory authorisation

does not confer immunity from political risk, which in turn can have real impact

on revenues.

The rest of the paper explores the reputation of financial services providers

among political audiences and provides an assessment of the political risk faced

by each sector as technological developments quicken the pace of change.

1 Department for Business, Innovation and Skills 2 www.clearaccount.com

10

Sector analysis

Alternative finance

Scope

Peer-to-peer lending

Crowdfunding

Invoice trading

Small sum, short-term lending

Sector summary

‘Alternative finance’ is probably the hottest subject in financial services at

present yet the term covers such a diverse range of products and providers that

it is worth sketching out some of the core components before commenting on

their role in the landscape of future financial services and their appeal to political

stakeholders.

The excellent benchmarking report ‘The Rise of Future Finance’3 sets out a

taxonomy of alternative finance models that includes peer-to-peer lending (P2P);

debt, equity and rewards crowdfunding; microfinance and community shares;

and invoice trading. The industry covers both consumer and business credit. In

practice there is some blurring between the above categories because of the

diversity of innovative business models employed by firms. New firms sometimes

bring a novel model to market that does not sit entirely comfortably in one

category or another while sometimes the choice of one label or another depends

on a very technical, regulatory classification.

There is some debate over whether short-term, small sum lending, including but

not exclusively so-called payday products, should be included in this category;

payday lenders are an alternative to traditional credit institutions and serving a

customer base that is often excluded from mainstream products and services4.

As such, we have included short-term lenders in our research though we note

that payday has its own unique model and does not share many of the important

3 The Rise of Future Finance: the UK Alternative Finance Benchmarking Report – December 2013 – Liam Collins (Nesta), Richard Swart (University of California, Berkeley), Bryan Zhang (University of Cambridge) 4 Note also that some payday consumer credit lenders have entered the short-term SME finance market. For example WDFC UK, best known for its Wonga subsidiary, rebranded its Wonga for Business arm as Everline in 2013.

11

characteristics of the other types of alternative finance mentioned above,

particularly the open or ‘democratic’ nature of P2P and crowdfunding. Therefore

we clearly differentiate this sub-sector from other alternative finance providers.

Political perceptions

There is an emerging feeling among the industry that the UK Government is

becoming more aware of the potential of alternative finance. Considerable

investments have now been made through P2P platforms via the Business

Investment Bank, a Cabinet Office working-group is to be convened to

coordinate departmental positions on crowdfunding, the Bank of England has

now dedicated resources to studying and liaising with the sector, and the FCA

has adopted a public stance of being “on the right side of progress”.

While the Bank and the regulator are reacting to a growing part of the financial

services industry, the appeal of the sector for the Government is clear. The

alternative sector offers an attractive vision of socially useful finance at a time

when lending to businesses by mainstream lenders is curtailed, faith in banks is

only starting to recover, and it is not politically expedient to be seen to support

the established order too closely.

But while understanding grows at an official level, alternative finance retains a

very low profile among politicians. Perhaps unsurprisingly given the sector’s

relative youth and size, no other sector reported such a low level of

understanding among politicians in our exclusive polling.

Awareness and understanding

Crowdfunding, P2P and invoice trading were the only categories which reported

MPs who have never heard of the providers. At 11%, this is a significant

minority.

A large portion of all respondents (35%) had either never

heard of, or had a fairly poor understanding of

crowdfunding and peer-to-peer lending. This low level of

understanding is particularly pronounced among older

and less-recently elected MPs: 43% for MPs over the age

of 555 and 56% for MPs elected between 1992 and 1997.

Regionally, there are significant variations: 62% of

5 The average age of MPs in this Parliament is 50.

12

Scottish MPs6 and 43% of MPs in south west England reported a very low level

of understanding, while among the English regions respondents from the

Midlands were more likely to have never heard of crowdfunding and P2P.

Putting these figures into context, 90% of MPs claimed a good or excellent

understanding of the traditional high street banking business model, with 86%

reporting the same for building societies.

Breaking down the results, our polling by political party shows that levels of low

awareness and understanding were broadly similar across the three main

parties, although a much higher percentage of Liberal Democrat MPs were well-

informed about the sector7.

Predictably, younger MPs were far more likely to have better knowledge of this

industry, with 57% of MPs aged between 18-44 and 46% of MPs elected in 2010

reporting a good or excellent understanding. Female MPs were also more likely

to have greater knowledge of alternative finance providers.

We also used another metric to gauge the relative profiles of crowdfunding and

peer-to-peer lending among parliamentary audiences versus banks and payday

firms. The graph below shows the Parliamentary ‘occasions’8 in which these four

terms were mentioned. One can clearly see that crowdfunding and P2P have not

received much parliamentary time over the past four and a half years when

compared to banks and payday lenders.

6 32% of Scottish respondents had not heard of the services 7 63% of Lib Dem respondents reported a good understanding of the sector 8 I.e. a Westminster Hall debate on crowdfunding counts as one occasion, as does a written parliamentary question.

13

An analysis of social media over the last 18 months shows that alternative

finance services are also not featuring strongly in political stakeholder

conversations online.

Quantitative analysis does not reveal how positive or negative these mentions

were but a sample study of the results mentioning crowdfunding shows the vast

majority of tweets were promoting awareness of a specific project; the term

crowdfunding was not the main subject matter but used instead to garner interest

in the projects themselves.

0

20

40

60

80

100

120M

ay-1

0

Jul-

10

Sep

-10

No

v-1

0

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep

-11

No

v-1

1

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Occ

asio

ns

DatePayday Peer-to-Peer Banks Crowdfunding

The amount of times each were mentioned on social media

14

Trust

A lack of understanding influences opinions on questions of trust and regulation.

The alternative finance9 sector’s negative rating on the question of whether MPs

would trust platforms to act in their customers’ interests is very low compared to

all mainstream providers except building societies and credit unions. This means

that fewer MPs actively distrust the firms in the sector than they do for high street

banks, new entrants to retail banking and card issuers such as Visa and

MasterCard. But nearly 50% of MPs are unsure about whether alternative

finance providers are trustworthy and the sector still lags behind all others except

payday for positive trust ratings: 43% versus 57% for new banking entrants, 63%

for established high street banks, 73% for card issuers and 90% and 93% for

building societies and credit unions respectively. However, from that percentage

only 2% “definitely trusted”10 crowdfunding and P2P, compared to 9% for

established high street banks, 5% for new entrants to banking, 11% for card

issuers, 28% for building societies and 43% for credit unions.

Of MPs from the three main parties, the Liberal Democrats had the firmest views

though their opinion was split. A large percentage of the respondents from the

Conservative and Labour parties (42% and 41% respectively) simply didn’t yet

know whether the platforms’ interests, particularly crowdfunding and P2P, were

aligned with those of consumers.

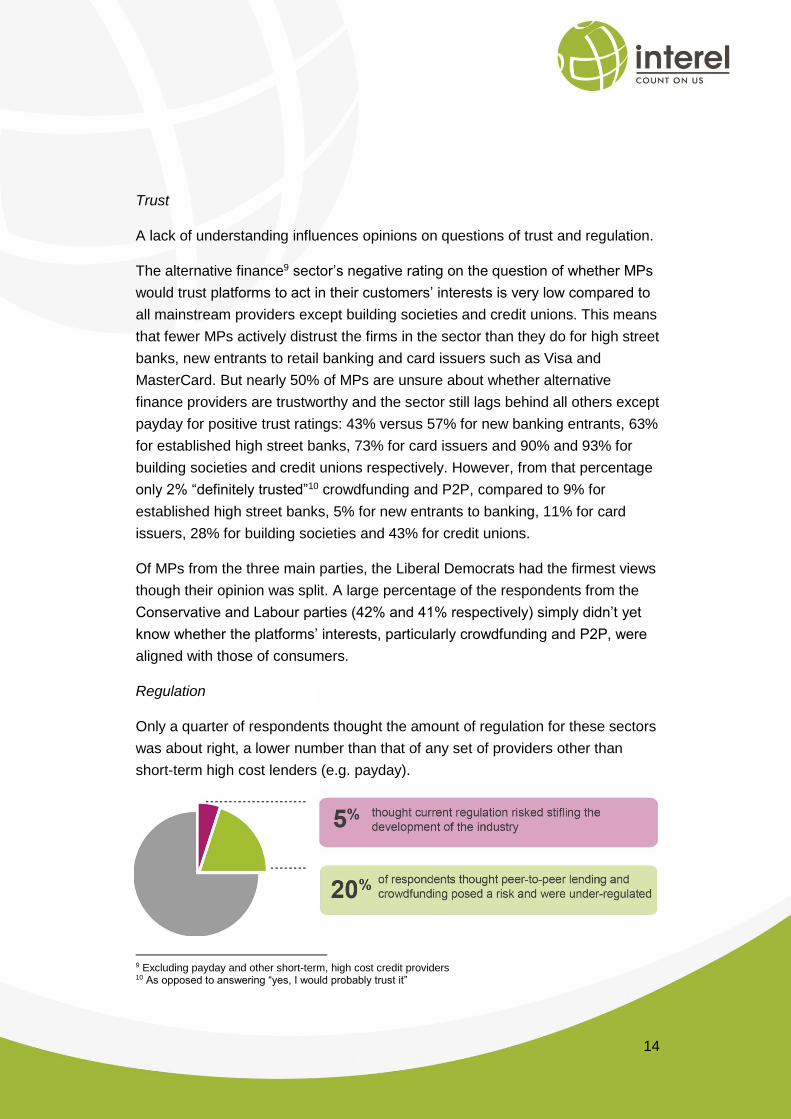

Regulation

Only a quarter of respondents thought the amount of regulation for these sectors

was about right, a lower number than that of any set of providers other than

short-term high cost lenders (e.g. payday).

9 Excluding payday and other short-term, high cost credit providers 10 As opposed to answering “yes, I would probably trust it”

15

MPs that claimed good or excellent understanding of the sector were highly likely

to also give a positive response to questions about trust but attitudes among

those same MPs towards regulation of the sector was much more even: 38%

believed the regulatory regime achieved a good balance but 31% thought it was

too light touch and the sector posed a risk. Furthermore, while younger MPs had

greater knowledge of the businesses and might have been expected to be more

favourable towards new innovations, over a quarter of respondents aged

between 18 and 44 believed such alternative forms of finance were under-

regulated. The qualitative polling results and first-hand interviews do not suggest

that older MPs are more inclined to a positive view of current regulation; rather

they have not yet formed an impression of the nature of the industry and the

required form of regulation.

Sector outlook (political risk assessment)

The alternative finance market, as defined in the Nesta report, is in an excellent

starting position: it is experiencing astonishing growth rates, funding through

platforms is increasing as large mainstream institutions become more engaged

as they hunt for yield in a low rate environment, partnerships between banks and

peer-to-peer lenders are emerging, and Government ministers are offering

enthusiastic endorsement to the sector. The role for P2P and crowdfunding in a

diverse future financial services market could be very significant.

Yet there are challenges ahead, particularly when the enthusiasm at high levels

within government and regulatory bodies does not translate into accommodating

action at official level.

There is, for example, some concern among P2P providers about the bundling

together of P2P and crowdfunding by the FCA and European Commission in

recent policy statements. We have also heard anecdotal evidence that there are

technical problems with the regulator’s approach that suggests it is trying to fit

these alternatives into its existing paradigm rather than taking a broader and

more flexible view. One example is the use of a the Financial Services and

Markets Act 2000 to clamp down on ‘illegal financial promotions’ on social media

platforms like Twitter and Facebook. Industry participants complain that the out-

dated legislation (enacted before social media’s arrival) is hampering start-ups’

and other substitutes’ ability to promote their enterprises.

We have also heard there are problems arising in the relationship between the

banks, the platforms and the borrowers. For example, some platforms are finding

16

it hard to access payments systems while crowdfunded start-ups are being

denied business bank accounts.

The essence of the alternative finance concept – connecting borrowers and

lenders that would otherwise be locked out of a closed market dominated by big

investors – is the biggest weapon the sector can deploy to stave off business

and political risk, and ensure it continues to grow. Undermining or blocking that

central element will not just limit the size of one particular sector of modern

financial services, but inhibit entrepreneurship and hamper the move towards a

more transparent, inclusive and democratic shareholder community.

In addition to the current regulatory and business issues, we see two main

challenges for the sector as it continues to grow:

Create awareness and better understanding in order to foster a

constructive regulatory structure, help the sector withstand reputational

shocks (such as conduct crises or the failure of a major platform), and

weather political turbulence at national, European and global levels.

Maintain the essence of alternative finance, the things that make these

products different, while gaining scale and moving to the mainstream.

It is a big task but it is also a huge opportunity for the industry.

A note on the ‘payday’ sector

One could have easily anticipated that politicians would have negative feelings

towards the high cost, short-term consumer finance industry. However, the scale

of hostility towards the industry is striking.

MPs awareness of claimed knowledge of payday lenders is very high: three-

quarters of respondents said they had a good or excellent understanding of the

industry. However, great understanding does not equal a positive view of the

sector: 75% of MPs (including all Labour MPs) think there is too little regulation

of payday while 90% probably or definitely would not trust payday lenders to act

in their customers’ interests.

However, there is a clear division on party lines: 41% of Conservative

respondents felt that the regulatory regime was ‘about right’, perhaps given the

Government’s role in creating the new regime, but no MPs from any other party

agreed. And it was only MPs from the Conservative party that ‘would probably

17

trust’ payday lenders to act in their customers’ interests, though the amount was

much smaller at 16%.

Despite this minority view it is clear that there is a chronic breakdown in the

short-term high cost credit industry’s relationship with parliamentarians. Given

this political opposition and the media interest in the problems associated with

the product, it is likely that we will continue to see the sector under pressure from

MPs and the regulator for the foreseeable future, especially should Labour win

the general election in 2015.

18

Payments and commerce

Scope

Mobile payments

Card companies and new entrants

Big Data, big rewards and the relationship with the customer

Sector summary

The payments industry may not attract as many headlines or twitter mentions as

other parts of financial services but it is no less important. As the ‘rails’ of

commerce and financial services, what happens in the payments space has an

enormous impact on other issues, particularly diversity and competition. Much of

the speculation about technology companies and other new entrants moving into

banking comes directly from their presence in payments.

Payments are tightly regulated and access to the systems is not easy to achieve.

Substitutes have to fit within the existing system, which for the large part favours

the banks and the card issuers but the number of players in the industry is large

and growing.

Online retailers and major content providers such as Apple and Google have

dipped their toes into the water but it is mostly smaller firms that are creating

innovative services that respond to demands for cheaper, more flexible and

more value-accretive payments platforms. In the US firms like Square and

LevelUp have emerged to meet specific need: Square offers small businesses

and would be merchants the opportunity to take card payments via their

smartphones, turning any iPhone into a point of sale. LevelUp provides

merchants with a means of taking payment via mobile phone QR scans – not

only is the service quicker for the customer to use and lower cost for the

merchant, it allows businesses to build relationships with individual consumers

by targeting them with relevant promotions, rewards, reminders or special offers.

LevelUp has also recently announced it would provide support to merchants

using Apple’s iBeacon, a Bluetooth-enabled device that ‘pings’ nearby

customers. In an era when data is king, these types of services offer a much

greater value proposition for businesses, especially small or new ones, than that

delivered in the past by traditional payments providers.

19

Some innovations will emerge and disappear without ever reaching the required

scale. Electronic wallets, for example, are likely to have a very short life span.

O2 and Square both recently withdrew wallet apps from the market because of a

lack of consumer engagement. Even Google has not worked out yet how to

create a compelling offer.

However, mobile payments will continue to grow in popularity and will reach

mass acceptance in the (relatively) near future. It will not be banks or card

issuers making this happen; it will be coffee shops and restaurants, buses and

trains. In the US, 1 in 10 transactions at Starbucks are now via mobile payments.

In the UK the Harris & Hoole coffee chain recently launched its own mobile

payments app that you can use to order before you even reach the counter. At a

local level, perhaps the biggest single step will be when Transport for London

phases out the Oyster card and introduces NFC and mobile payments in its

place. At a stroke the technology will be promoted to 8 million Londoners and

countless other visitors.

We believe that mass adoption of new forms of payments and a sector-wide shift

away from solely processing payments towards data-driven ID assurance will

have far-reaching consequences for other financial services. Consider the use of

the M-Pesa payments in Africa; with no historic payment system in place and no

antiquated technology to update, payments in the African continent has

leapfrogged the West but to the exclusion of banks altogether.

Political perceptions

Taking the political community as a whole, the most prominent issue in the UK

has been encouraging faster processing of payments. There is a relatively high

level of awareness of the problems posed by delays to consumers, particularly

those who might be considered financially vulnerable. It is also an issue that fits

within a widely-believed narrative that says the large banks serve themselves

first before their customers.

If one disaggregates government and regulators from the wider political

environment one can see that a great deal of attention has focused on payments

recently. However, a general political audience finds other aspects of payments

esoteric and there is a lack of understanding about how this sector affects other

politically important subjects such as supporting SME growth and increasing

competition in retail financial services.

20

Trust & regulation

There is also scepticism about innovations in the market, almost solely based

upon concerns about fraud, data security and ID theft. In this regard, political

audiences are no different in terms of sentiment from the general public.

Research by YouGov11 found that over half of people who didn’t yet possess

contactless cards or NFC/mobile phones said they would not be interested in

using them in the future to make payments. Some of the main reasons were ‘fear

of losing’ the card/device, concerns over security, and a belief that ‘too much can

go wrong’.

In this context it is unsurprising that the major card companies are widely trusted

by politicians because of the role they play in everyday financial transactions.

These findings suggest that there is actually a great deal of comfort with current

services; Visa and MasterCard are seen as important contributors to a stable

and secure payments system12, which gives them a privileged position in public

policy debates as well as in business.

We note that consumer sentiment towards payment service providers for online

transactions is more positive towards alternatives. For example, according to the

Future Foundation’s m-commerce13 report, PayPal is the most trusted to take

payments ahead of card companies, banks, mobile telephony companies etc.

Additional research could perhaps shed light on whether politicians’ attitudes

towards providers shift when just considering online but on the basis of existing

evidence we suspect that the established providers14 would remain in pole

11 YouGov, September 2013 12 However, just under a quarter said they would probably or definitely not trust them – like the other established sectors, there is not much of a grey area in MPs’ views on the card companies. 13 http://www.monitise.com/insights/2013/10/01/mcommerce-future-foundation-report 14 One could rightly argue that PayPal should now be considered as one of the established providers.

21

position. Put simply, new entrants are just not as trusted as the established

banks and traditional service providers, regardless of how much the financial

crisis and conduct scandals have undermined faith in the present order.

Sector outlook

Paul Purcell of Continental Advisors, an investor in LevelUp among others, says

radical change in the market is still in its early stage and the opportunities are

hugely exciting but there are also obstacles:

“The power of the mobile handset in giving retailers huge amounts of

data and connecting them directly to their customers, and at a lower cost,

makes it a dangerous time for banks and card companies.

“Real innovation is coming from the fringe players, not even Google or

Facebook can innovate like these guys, and they can make things work

because they get around the competition problems. But you still have to

have access to the payments system somewhere, and that has a cost

attached.”

In 2015 a new payment services regulator will be set up and one of its objectives

will be to foster competition and innovation. The FCA’s ‘incubator’ service should

also help start-ups and new entrants. The way that the new regulatory body is

implemented and its interpretation of its mandate will have a critical effect on the

development of payment services here. Reforms taking place in the US and at

the European level will also influence which new technologies or services make

it to mass market.

It is important that the regulatory regime does not create a bias against new

firms who are trying to do new things that challenge the regulator because of

their unfamiliarity. Concerns about fraud and security should not overrule change

by default. In fact, mobile payments can increase security – people are now far

more attached to their phone than their wallet – but the firms bringing radical

products to market still have a job to do in educating stakeholders about the

benefits of their innovations.

22

High street financial services

Scope

Future role of high street banks, building societies and credit unions.

Market structure

Competition or diversity

Sector summary

The most visible parts of financial services for the average consumer are the

high street banks and the building societies. 93% of UK adults have a personal

current account (PCA) while 90% of borrowers taking out a mortgage obtain

credit from either a bank or a building society.

Concerns about the banking market go back to before the financial crisis and

have, to a large degree, focused on market structure. In the UK retail banking

services are highly concentrated15: the big five banks16 have 85% of the PCA

market, 67% of the mortgage market, and the biggest four have a SME lending

market share of about 80%. The personal savings market more fragmented but

there is no doubt that the banks are the biggest game in town.

The mutual sector is often promoted as the ‘ethical alternative’ but the sector has

had a mixed record in the aftermath of the crisis. Credit unions are growing in

number but still make up a tiny proportion of the market when compared to other

countries.

The financial crisis and following conduct issues have exacerbated fears that the

banking market is not working well; overdraft charges and the PPI mis-selling

scandal allow critics to paint banks as actively working against their customers’

interests, while the taxpayer bail-out of Lloyds and RBS crystallised the ‘too-big-

to-fail’ dilemma as the Government stepped into stabilise the market at the

expense of moral hazard.

There are signs that the structure of the market is starting to change with a

number of new banks (Metro, Virgin Money, Aldermore, Handelsbanken,

Paragon and Shawbrook among others) entering the market, retail brands such

as Marks & Spencer and Tesco launching new services, and some old banking

15 The UK is far from unique as in many industrialised countries banking is a highly concentrated industry. 16 Lloyds Banking Group, Barclays, RBS, HSBC, Santander

23

names such as TSB and Williams & Glyn returning as part of bigger groups’

divestments.

Political perceptions

Understanding

Unsurprisingly, MPs reported a very high level understanding of the established

banking sector; 90% said they had a good or excellent understanding of these

business models, the highest of any sector in the survey. Building societies were

close behind.

Simple brand profile explains this familiarity and politicians, like any other

average consumer, have personal interactions with these banks. It is probable

that all MPs have used one or more of these firms for saving or borrowing

services.

Furthermore, the banks have barely been out of the political spotlight since the

global financial crisis of 2007/08 and the ensuing economic crash. First, they

needed to be rescued with vast sums of taxpayer cash; then they had to be

fixed, split up and simplified before being criticised for contracting lending to

SMEs, paying staff huge bonuses and fixing benchmark rates. Even now in April

2014 the shareholder revolt against pay packages at Barclays and RBS is more

newsworthy than companies in almost any sector.

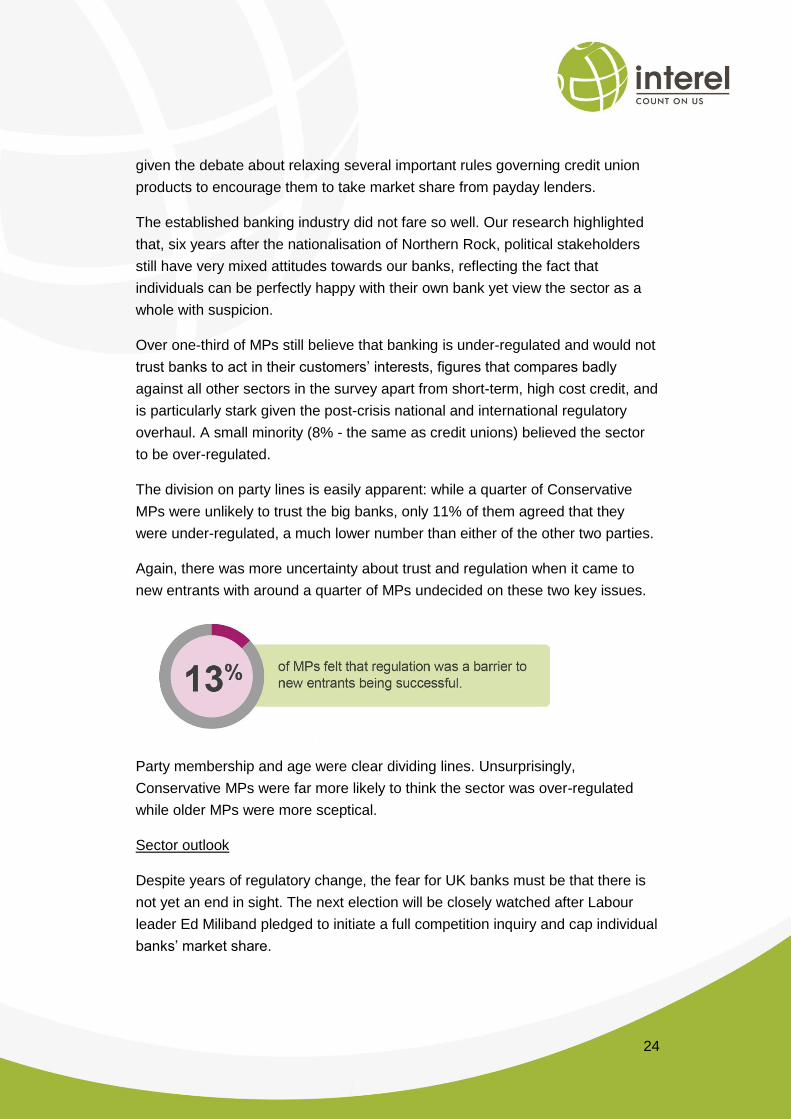

However, there was some uncertainty about new entrants to high street banking

with only 41% confident they understood these firms’ businesses (the second

lowest positive rating after crowdfunding and P2P) though that figure was much

higher among younger MPs.

Conservative MPs were much more likely than Labour MPs

to claim a good or excellent knowledge of new entrants but

nearly a quarter of female MPs surveyed across all parties

‘did not understand [this sub-sector] at all”.

Trust & regulation

Building societies and credit unions scored very highly on trust and the majority

of MPs thought the regulatory regime for these two sectors was about right (83%

and 76% respectively). The latter result for credit unions is somewhat surprising

24

given the debate about relaxing several important rules governing credit union

products to encourage them to take market share from payday lenders.

The established banking industry did not fare so well. Our research highlighted

that, six years after the nationalisation of Northern Rock, political stakeholders

still have very mixed attitudes towards our banks, reflecting the fact that

individuals can be perfectly happy with their own bank yet view the sector as a

whole with suspicion.

Over one-third of MPs still believe that banking is under-regulated and would not

trust banks to act in their customers’ interests, figures that compares badly

against all other sectors in the survey apart from short-term, high cost credit, and

is particularly stark given the post-crisis national and international regulatory

overhaul. A small minority (8% - the same as credit unions) believed the sector

to be over-regulated.

The division on party lines is easily apparent: while a quarter of Conservative

MPs were unlikely to trust the big banks, only 11% of them agreed that they

were under-regulated, a much lower number than either of the other two parties.

Again, there was more uncertainty about trust and regulation when it came to

new entrants with around a quarter of MPs undecided on these two key issues.

Party membership and age were clear dividing lines. Unsurprisingly,

Conservative MPs were far more likely to think the sector was over-regulated

while older MPs were more sceptical.

Sector outlook

Despite years of regulatory change, the fear for UK banks must be that there is

not yet an end in sight. The next election will be closely watched after Labour

leader Ed Miliband pledged to initiate a full competition inquiry and cap individual

banks’ market share.

25

So far this Government has been content to try to create the conditions for more

competition rather than force solutions on the market. Change will inevitably be

slow but that is unappealing politically, especially after both Sir John Vickers and

the Andrew Tyrie-led parliamentary commission have warned that drastic action

would be necessary if conditions did not improve.

The big banks have to prove that they can once again provide the social utility

that is now expected of them. They will have to do so while still responding to

shifts in the economic model of retail banking. For example, the rise of mobile

banking means that large scale branch networks are becoming more costly and

more unnecessary but there is a significant political attachment to branches,

especially in rural or deprived areas and where financial exclusion is more

prevalent. Similarly, Lloyds and RBS have recently reversed their decisions to

limit their basic bank account customers to using proprietary cash machines after

widespread opposition to the move.

For new entrants, the challenge is one of education and differentiation while

pursuing growth strategies that give them a strong presence in the market. Many

of the murky cross-subsidies that allow for free access to cash machines act as

a barrier to entry or growth for newer firms, and while there is a growing number

of banks that now charge customers who deposit less than a minimum amount

per month in their current account, the widespread adoption of monthly charges

seems some way off partly because of concerns about financial exclusion. The

bigger institutions must fear a political backlash and/or a customer revolt if they

try to change the status quo.

26

Conclusions

1. Political paradigm favours the status quo

It is very encouraging that the Government and the regulators have woken up to

potential of innovation but the wider political community is behind the curve of

financial innovation. The prevailing paradigm remains one centred on the large

high street institutions. Understanding of the alternatives, and how they can help

move the UK towards a more diverse and customer-orientated market, is low

and this translates into policy. For example, Labour has promised to shake up

the banking market by capping a bank’s market share and forcing the big banks

to divest themselves of more branches. Notwithstanding the practical difficulties

of doing so, and the fact that only one bank has an individual PCA market share

above 16%, one cannot help but think that the aim of the policy is wrong.

Creating more institutions that operate on very similar business models and offer

almost identical products does not encourage diversity.

2. Political focus should move away from ‘what are we afraid of’ towards

‘what benefits do we want to see’

Trust continues to be an issue, both for novel business models and the

established players. For less-familiar brand names it is a question of building

awareness and an understanding of how new services can fit into a diverse,

competitive and (relatively) stable market. There is comfort in the current system

and this puts some firms in a privileged position; new entrants need to make a

compelling case for the benefits that innovation can bring to the wider economy.

3. The outcome of the 2015 general election will be important for the

industry

Our research provides evidence that the make-up of the next Government will

have a significant impact on the prospects for the financial services industry.

Labour and Liberal Democrat MPs are more sceptical about the industry in

general but they are strong supporters of the mutual sector. Younger MPs

coming into Parliament in 2015 might be seen as natural advocates for new

entrants but it is apparent from our research that youth, and the more inherent

connection to new technologies, is no guarantee of a favourable attitude.

27

About Interel Interel is a leading owner-managed fully integrated international consultancy

specialising in strategic communications, public affairs and association

management

We are headquartered in Brussels with own offices in London, Paris, Berlin,

Washington, D.C. and Delhi (coming soon: Beijing)

We are at the centre of a global partnership of independent, best-in class public

affairs specialists in more than 40 countries, with a total 1000 consultants

serving clients around the globe

Over 200 blue chip companies, institutional investors, trade associations and

governments count on us

Contacts

George McGregor

Managing Partner UK and Group Head of Public Affairs

e: [email protected] t: +44 (0) 20 7592 3804

Stephen Edwards

Deputy Managing Partner and Group Head of Technology

e: [email protected] t: +44 (0) 20 7592 3800

John Fearn

Director and UK Head of Financial and Business Services

e: [email protected] t: +44 (0) 20 7592 3809

Related Documents