Fundamentals of investing: Why invest? D. Scott Phillips Wells Fargo Advisors, LLC

Fundamentals of investing: Why invest? D. Scott Phillips Wells Fargo Advisors, LLC.

Dec 27, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Fundamentals of investing: Why invest?D. Scott PhillipsWells Fargo Advisors, LLC

The Value of Money

From Barter to Pay We no longer trade beaver skins, we trade money.

Money has value Supply and demand

Inflation never sleeps

Philosophy of money

Spend

Loan

Own

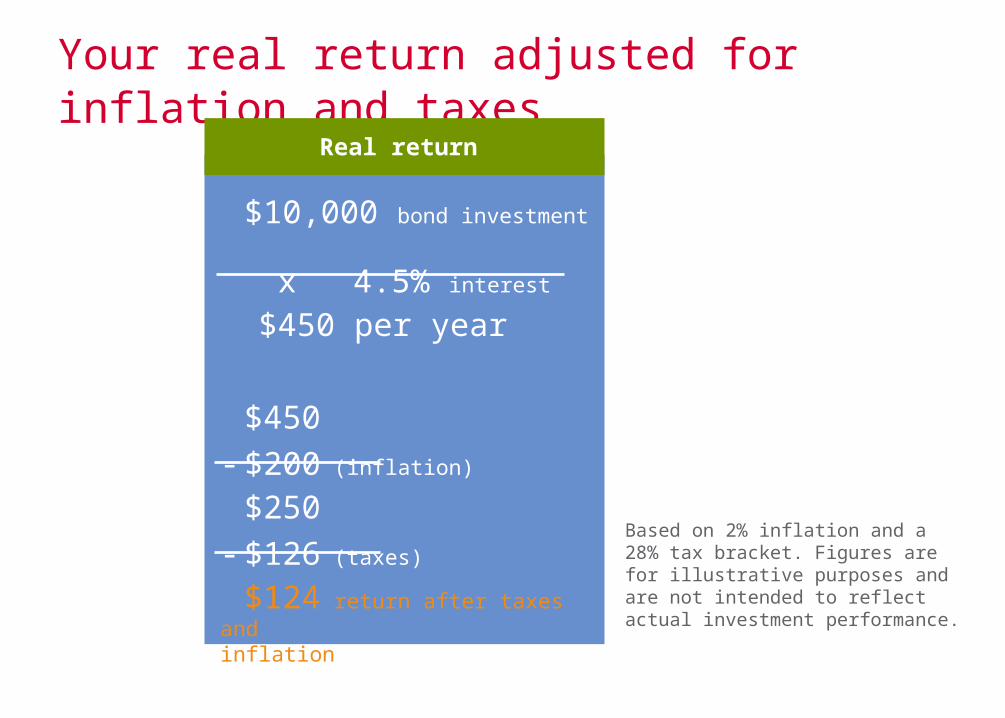

Based on 2% inflation and a 28% tax bracket. Figures are for illustrative purposes and are not intended to reflect actual investment performance.

Your real return adjusted for inflation and taxes

Taxable

$10,000 bond investment

x 4.5% interest

$450 per year

$450- $200 (inflation)

$250 - $126 (taxes)

$124 return after taxes and inflation

Real return

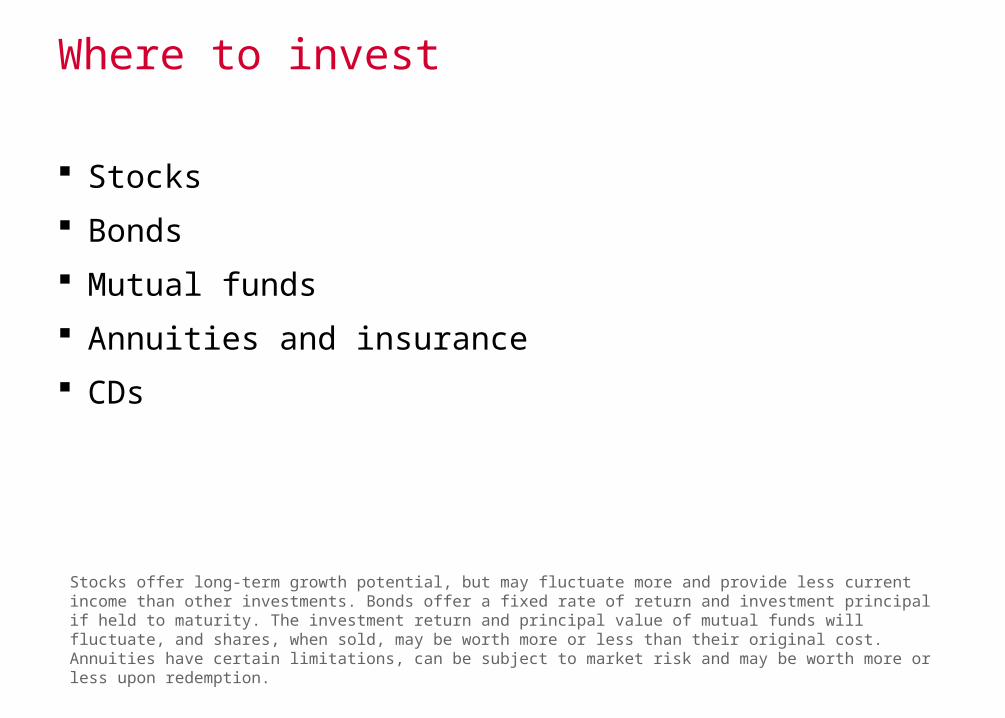

Where to invest

Stocks

Bonds

Mutual funds

Annuities and insurance

CDs

Stocks offer long-term growth potential, but may fluctuate more and provide less current income than other investments. Bonds offer a fixed rate of return and investment principal if held to maturity. The investment return and principal value of mutual funds will fluctuate, and shares, when sold, may be worth more or less than their original cost. Annuities have certain limitations, can be subject to market risk and may be worth more or less upon redemption.

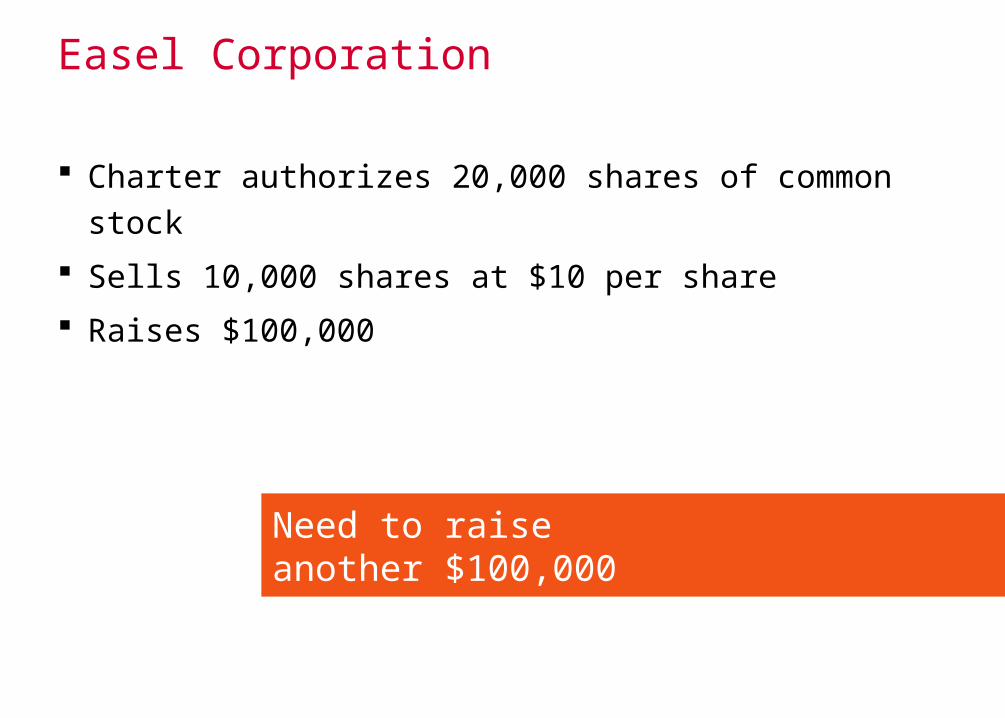

Easel Corporation

Charter authorizes 20,000 shares of common stock

Sells 10,000 shares at $10 per share

Raises $100,000

Need to raiseanother $100,000

Easel Corporation

Issue corporate bonds to “borrow” $100,000– Secured bonds

– Unsecured bonds

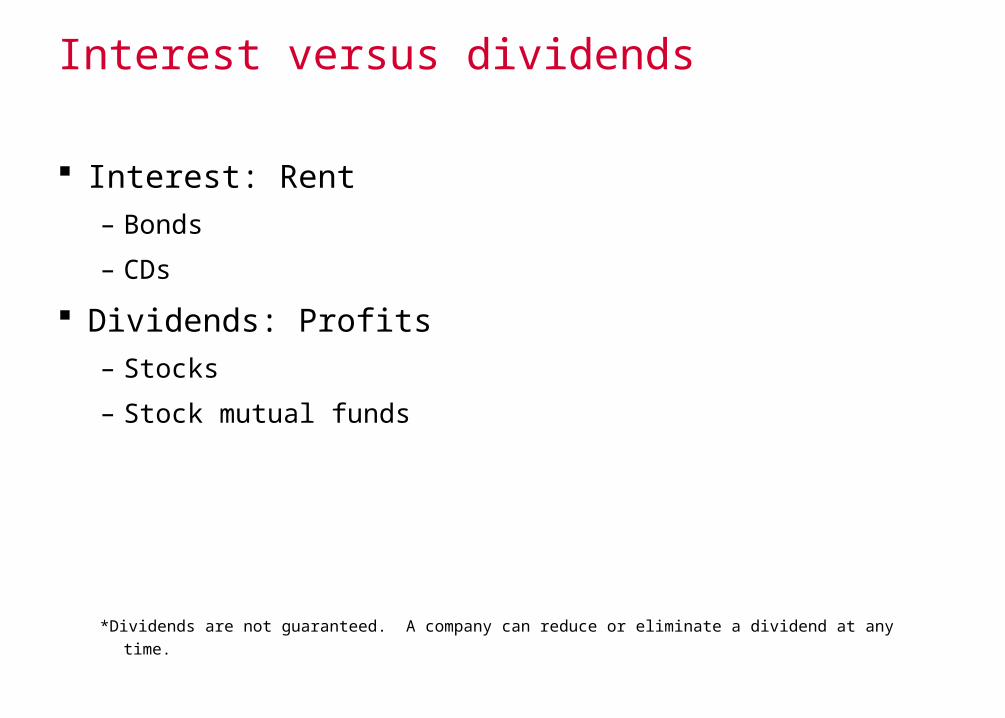

Interest versus dividends

Interest: Rent– Bonds

– CDs

Dividends: Profits– Stocks

– Stock mutual funds

*Dividends are not guaranteed. A company can reduce or eliminate a dividend at any time.

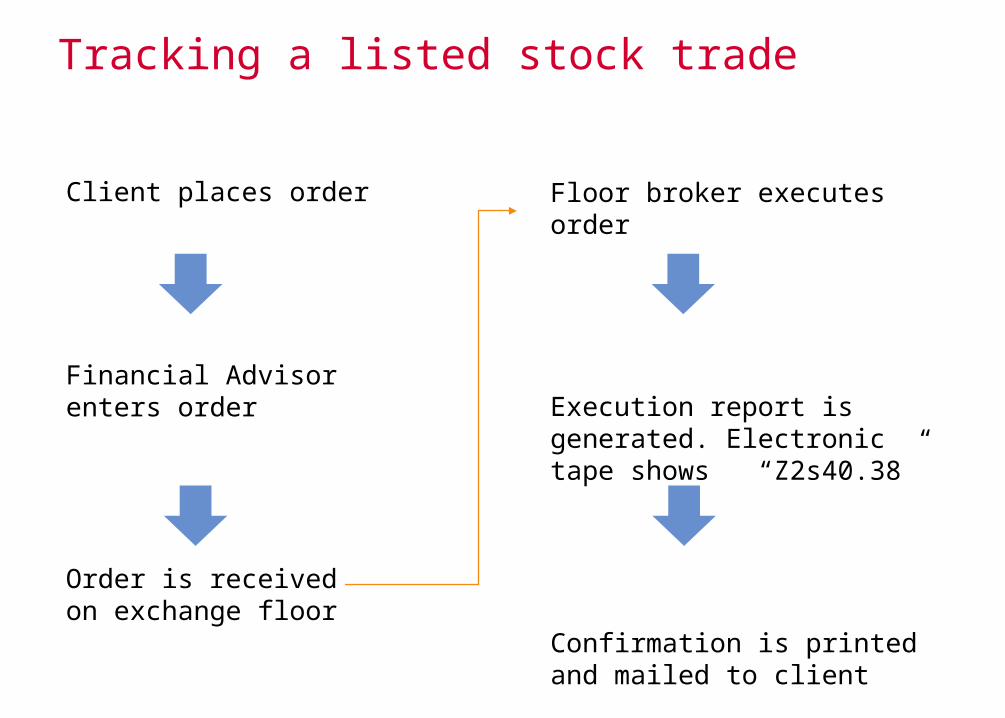

Tracking a listed stock trade

Client places order

Financial Advisor enters order

Order is received on exchange floor

Tracking a listed stock trade

Floor broker executes order

Execution report is generated. Electronic tape shows “Z2s40.38”

Confirmation is printed and mailed to client

Client places order

Financial Advisor enters order

Order is received on exchange floor

Three-day settlement rule

Keep money on deposit with brokerage firm

Money market funds

Liquid

Fluctuating interest

Check writing

An investment in any of the money market funds is neither insured nor guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the fund seeks to preserve the value of your investment at one dollar per share, it is possible to lose money by investing in the fund

Asset allocation

The blending of stocks, bonds and cash in your portfolio

Simple interest

$1,000 x 1.05$1,050

$1,000 x 1.05$1,050

Year 2

$1,000 x 1.05$1,050

Year 1 Year 3

Compound interest

$1,050 x 1.05$1,103

$1,103 x 1.05 $1,158

$1,000 x 1.05$1,050

Year 1 Year 2 Year 3

$1,158 x 1.05$1,216

$1,216 x 1.05$1,277

Year 4 Year 5

For illustrative purposes only and not intended to reflect actual performance of any particular investment. This illustration does not include the effect that taxes and investment expenses may have had on the outcome.

A dollar per day from ages 25 to 65 years old

72/5 = 14.4 72

For illustrative purposes only and not intended to reflect actual performance of any particular investment. This is a general investment rule of thumb that assumes the investment’s principal value and rate of return remain constant and that all interest and/or dividends are reinvested annually at the same rate of return.

Rule of 72

72 yrs.

55.418

14.412

108

64

3

24% 18% 12% 9% 7.2% 6% 5% 4% 1.3% 1%

14.4

5 72

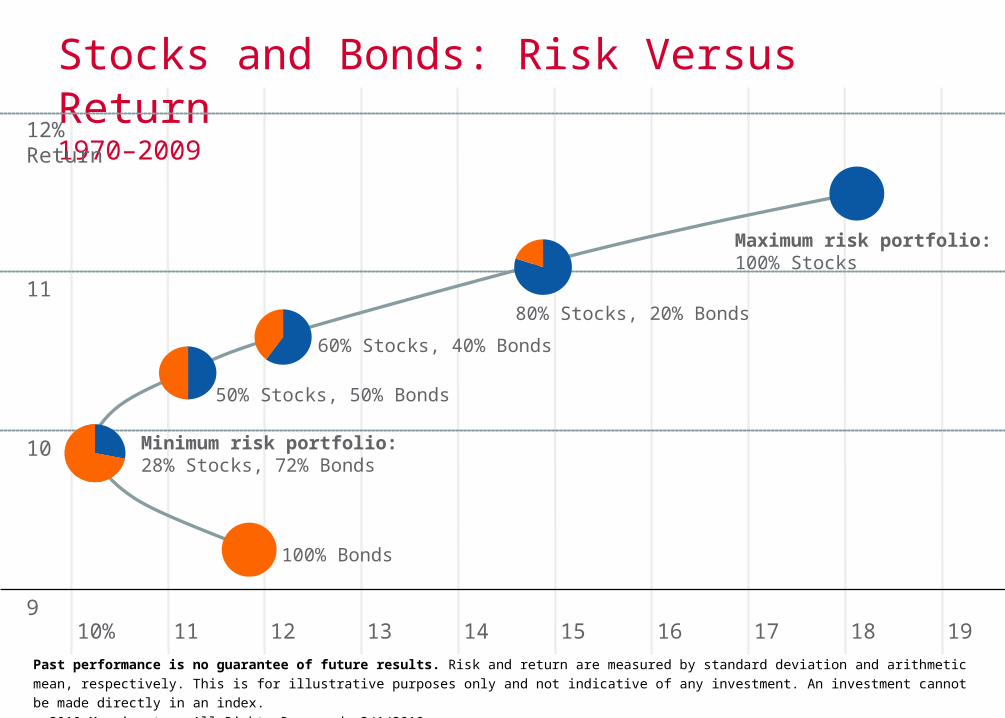

Stocks and Bonds: Risk Versus Return1970–2009

Past performance is no guarantee of future results. Risk and return are measured by standard deviation and arithmetic mean, respectively. This is for illustrative purposes only and not indicative of any investment. An investment cannot be made directly in an index. © 2010 Morningstar. All Rights Reserved. 3/1/2010

12% Return

11

10

9

Maximum risk portfolio:100% Stocks

60% Stocks, 40% Bonds

50% Stocks, 50% Bonds

100% Bonds

Minimum risk portfolio:28% Stocks, 72% Bonds

11 12 13 14 15 16 1917 1810%

80% Stocks, 20% Bonds

Inflation’s powerful effects

Source: Consumer Price Index

One dollar today Five years from now Ten years from now Twenty years from now

Why invest in stocks?

Inflation hedge

Growth potential

May issue dividends

Total-return potential

Facts about stock ownership

Stock investors own shares of a company

Almost half (47%) of all U.S. households own individual stocks*

There are a number of ways to invest in stocks: Individually

Mutual funds

Defined portfolios

Variable annuities

Private money managers

*Source: “Equity and Bond Ownership in America, 2008”. Investment Company Institute and the Securities Industry and Financial Markets Association survey, 2008.

Dividends

Portion of company’s profits paid to shareholders

Income investors choose companies with consistent dividend payments

Yield

= Current yieldAnnual cash dividend

Current stock price

Yield

Earnings per share (EPS)

Key number in determining a company’s investment value

= EPSNet income

Common stock outstanding

Payout ratio

Important number for income investors

Dividend-to-EPS ratio

Ex-dividend date

Ex-dividend date means “without the current dividend”

Ex-dividend

Ex-dividend date

Ex-dividend date means “without the current dividend”

If you buy stock after the ex-dividend date, the former owner will receive the current dividend

Ex-dividendBought stock

without dividend

Record date

Stock split

Before split: 100 shares at $100 = $10,000

After 4-for-1 split: 400 shares at $25 = $10,000

How to invest in stocks

Establish goals

Establish your risk tolerance

Determine what to buy

Bonds

You are a lender to the company

You earn interest on the money you lend

Bonds

Were first issued in coupon form

Bonds

Were first issued in coupon form

Moved toward issuing bonds registered with the owner’s name on certificate

Bonds

Were first issued in coupon form

Moved toward issuing bonds registered with the owner’s name on certificate

Finally, issued in book-entry form

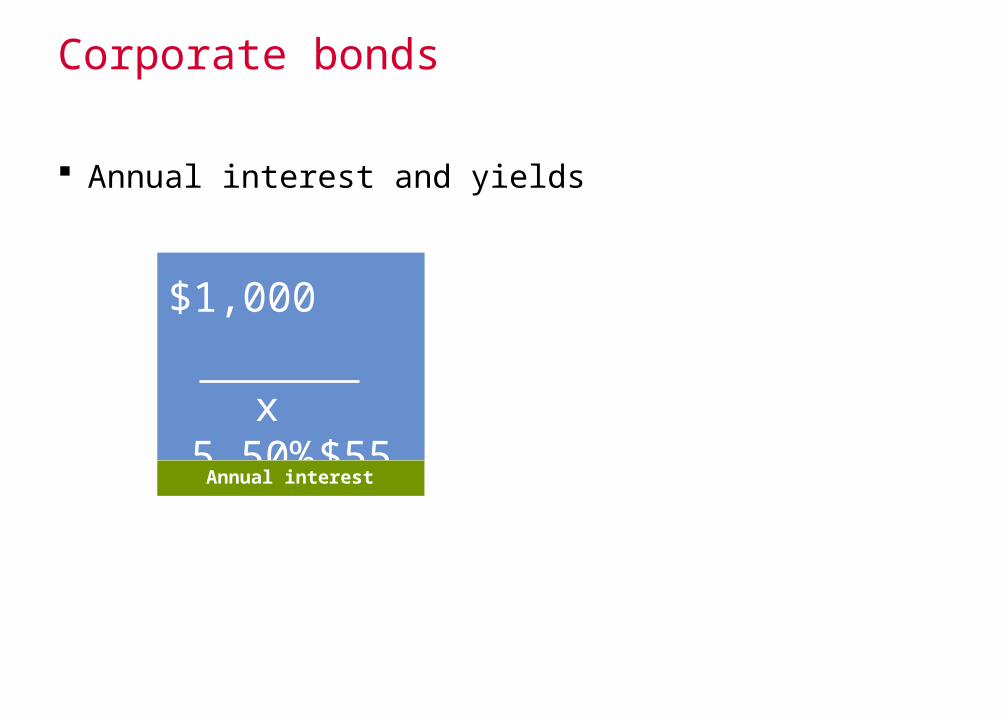

Corporate bonds

Annual interest and yields

Annual interest

$1,000 x 5.50%

$55

Annual interest

Corporate bonds

Annual interest and yields

$55 ÷ $1,030 = 5.34% current yield

$1,050

Annual interest

$1,000 x 5.50%

$55

Bond yields

Example: 10 years to maturity

5.50% coupon rate

Paid $30 premium over par $1,000

Callable in five years for $1,000

5.11% = yield to maturity

4.81% = yield to call

Government bonds

$5,000 and $10,000 denominations

Guaranteed by the U.S. government as to timely payment of interest and principal

State-tax-free

Municipal bonds

Free from federal taxes* and sometimes state taxes

$5,000 denominations

* Subject to amount

Municipal bonds

General obligation

Revenue

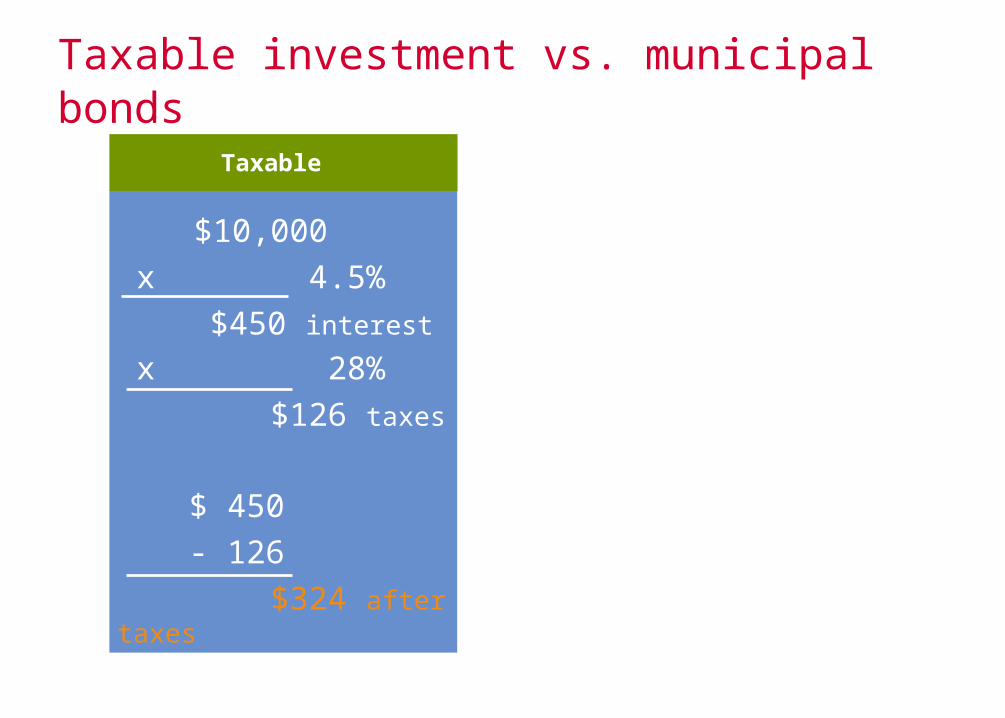

Taxable investment vs. municipal bonds

$10,000 x 4.5%

$450 interest

x 28% $126 taxes

$ 450 - 126 $324 after taxes

Taxable

Taxable investment vs. municipal bonds

$10,000 x 3.5%

$350 interest

x 28% $98 taxes

$ 350 - 0 $350 after taxes

Municipal

$10,000 x 4.5%

$450 interest

x 28% $126 taxes

$ 450 - 126 $324 after taxes

Taxable

Taxable-equivalent yield

100 x Tax-exempt yield

100% - Investor’s tax bracket = Taxable-equivalent yield

Example:

100 x 3.5% = 3.5

100 - 28% = 72

=4.86%

Investment-grade bond ratings

S&P (+ or -)

Moody’s (1, 2 or 3)

Superior AAA Aaa

Excellent AA Aa

Favorable A A

Average BBB Baa

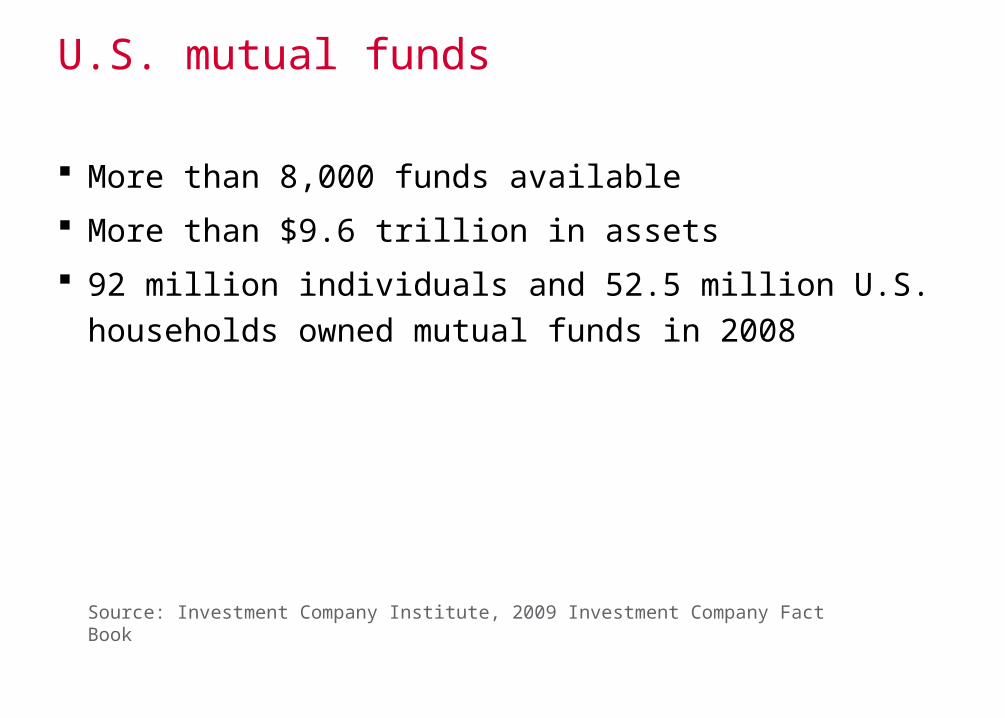

U.S. mutual funds

More than 8,000 funds available

More than $9.6 trillion in assets

92 million individuals and 52.5 million U.S. households owned mutual funds in 2008

Source: Investment Company Institute, 2009 Investment Company Fact Book

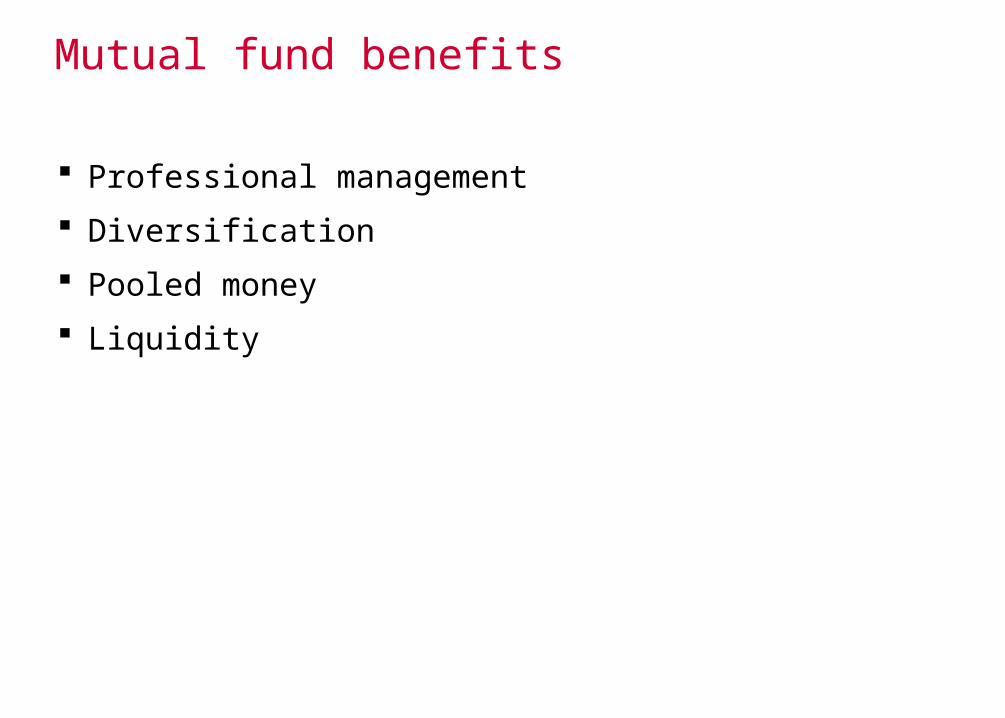

Mutual fund benefits

Professional management

Diversification

Pooled money

Liquidity

Did you know?

Mutual funds cannot hold money

Mutual funds cannot hold securities

Mutual fund pricing

Front-end load

Back-end load

No load

All funds have management fees

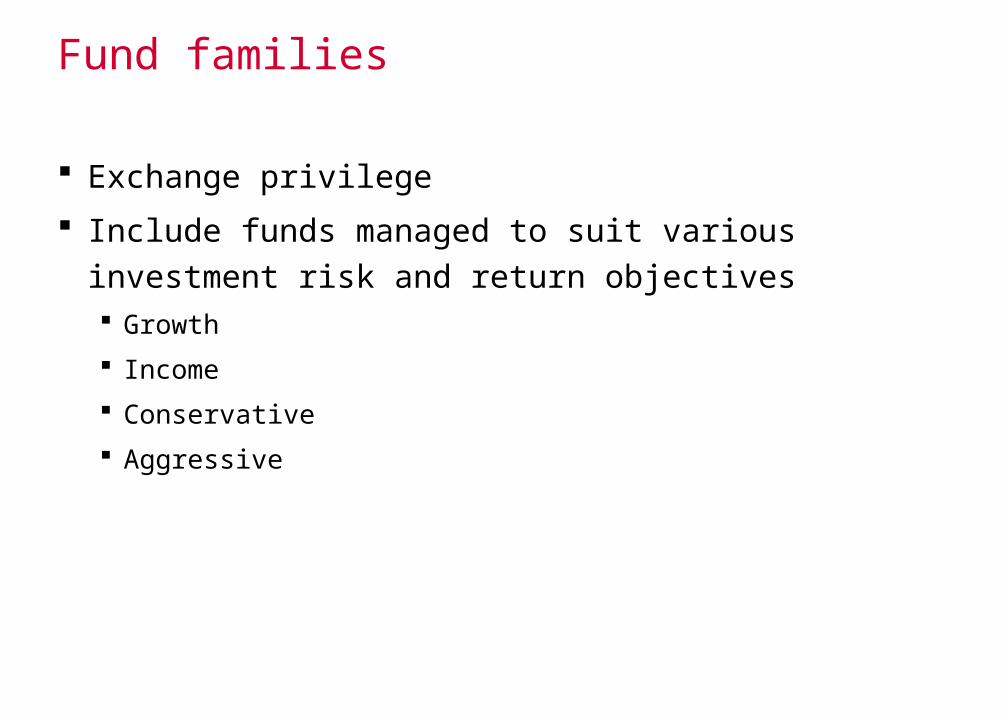

Fund families

Exchange privilege

Include funds managed to suit various investment risk and return objectives Growth

Income

Conservative

Aggressive

Taxation of mutual funds

Dividends — taxed as they occur

Trading profits — taxed as they occur

Exchange-traded funds (ETFs)

Index fund

Track one specific index

Buy/sell like stocks

Price set by underlying index

Matching asset allocation with where you are: Builders

Cruisers

Coasters

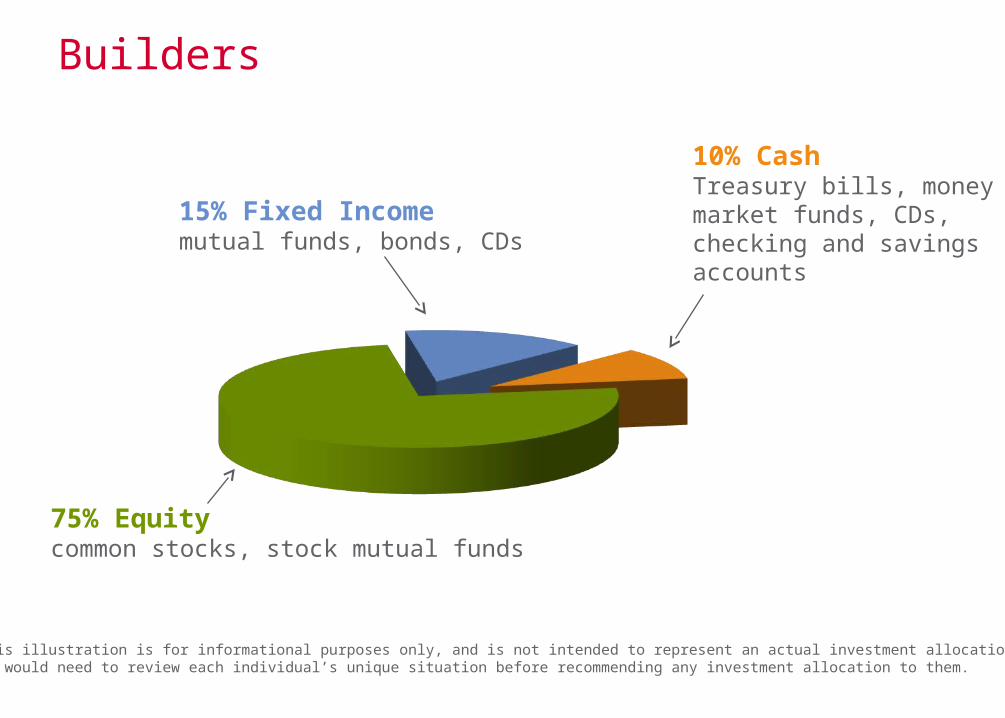

Builders

75% Equitycommon stocks, stock mutual funds

10% CashTreasury bills, money market funds, CDs, checking and savings accounts

15% Fixed Incomemutual funds, bonds, CDs

This illustration is for informational purposes only, and is not intended to represent an actual investment allocation. We would need to review each individual’s unique situation before recommending any investment allocation to them.

Cruisers

40% Fixed Incomeintermediate-term Treasurysecurities, mortgage-backed securities, municipal bonds, etc.

50% Equitycommon stocks, stock mutual funds

10% CashTreasury bills, money market funds, CDs, checking and savings accounts

This illustration is for informational purposes only, and is not intended to represent an actual investment allocation. We would need to review each individual’s unique situation before recommending any investment allocation to them.

Coasters

60% Fixed Incomeintermediate-term Treasury securities, mortgage-backed securities, municipal bonds, etc.

30% Equitycommon stocks, stock mutual funds

10% CashTreasury bills, money market funds, CDs, checking and savings accounts

This illustration is for informational purposes only, and is not intended to represent an actual investment allocation. We would need to review each individual’s unique situation before recommending any investment allocation to them.

5656

©2010 Wells Fargo Advisors, LLC. All rights reserved. 0410-2337A [25326-v12] e6757 4/10

Wells Fargo Advisors is the trade name used by two separate, registered broker-dealers: Wells Fargo Advisors, LLC and Wells Fargo Advisors Financial Network, LLC, Members SIPC, non-bank affiliates of Wells Fargo & Company.

Insurance products are offered through nonbank insurance agency affiliates of Wells Fargo & Company and are underwritten by unaffiliated insurance companies.

Securities and Insurance Products:

Not Insured by FDIC or any Federal Government Agency

May Lose ValueNot a Deposit of or Guaranteed by a

Bank or Any Bank Affiliate

Related Documents