ed: KK/ sa: MR/ AS / CS / AH BUY (Initiating Coverage) Last Traded Price ( 15 Jan 2020): P1.45 (PCOMP : 7,664.40) Price Target 12-mth: P2.00 (38% upside) Analyst Regional Research Team [email protected] Price Relative Forecasts and Valuation FY Dec (P m) 2018A 2019F 2020F 2021F Revenue 1,579 1,981 2,650 3,484 EBITDA 202 279 409 544 Pre-tax Profit 140 180 298 407 Net Profit 100 129 213 292 Net Pft (Pre Ex.) 93.9 129 213 292 Net Pft Gth (Pre-ex) (%) (45.7) 37.4 65.5 36.7 EPS (P) 0.06 0.06 0.10 0.14 EPS Pre Ex. (P) 0.06 0.06 0.10 0.14 EPS Gth Pre Ex (%) (46) 3 66 37 Diluted EPS (P) 0.06 0.06 0.10 0.14 Net DPS (P) 0.0 0.01 0.02 0.03 BV Per Share (P) 0.23 0.68 0.76 0.87 PE (X) 23.1 24.0 14.5 10.6 PE Pre Ex. (X) 24.7 24.0 14.5 10.6 P/Cash Flow (X) 16.7 13.3 8.6 6.6 EV/EBITDA (X) 11.7 7.7 5.2 3.7 Net Div Yield (%) 0.0 1.0 1.3 2.1 P/Book Value (X) 6.3 2.1 1.9 1.7 Net Debt/Equity (X) 0.1 CASH CASH CASH ROAE (%) 29.2 14.2 13.9 16.8 GIC Industry : Consumer Staples GIC Sector: Food & Staples Retailing Principal Business: Fruitas Holdings, Inc. is the holding company of one of the largest food and beverage kiosk operators in the Philippines, which serves various product offerings for low- to middle-income markets such as fresh fruit shakes and juices, lemonade, cooler Source of all data on this page: Company, DBS Bank Bloomberg Finance L.P. At A Glance Issued Capital (m shrs) 533.7 Mkt. Cap (Pm/US$m) 774 / 15.3 Major Shareholders (%) Lester Yu 21.1 Rai Properties 13.1 Free Float (%) 65.8 3m Avg. Daily Val (US$m) 1.8 DBS Group Research . Equity Regional Company Focus Fruitas Holdings, Inc. Bloomberg: FRUIT PM | Reuters: FRUIT.PS Refer to important disclosures at the end of this report 16 Jan 2020 Scaling up and branching out • Versatile business model geared to navigate a competitive and agile operating environment • Favourable exposure to the Philippines’ food service landscape • Earnings growth driven by aggressive store rollouts and scale efficiencies • Initiating coverage with a BUY rating and TP of P2.00 Initiating coverage on Fruitas Holdings, Inc. (Fruitas; FRUIT PM) with a BUY call and target price (TP) of P2.00. Fruitas Holdings, Inc. is the Philippines’ fastest growing diversified food and beverage kiosks operator, serving mostly snack items and fresh refreshments for low- to middle-income markets across the country. With over 17 years in operations, FRUIT has been apt in navigating a competitive and agile operating environment. It has a versatile business model that: a) generates value through strategic differentiation with a multi-branded and diversified product offering supported by a centralised commissary system and, b) has a rapidly expanding store network, enabled by its flexible store formats and backed by an in-house logistics and distribution infrastructure. We are of the view that FRUIT is well- positioned to expand brand visibility, accessibility, and reach, leading the growth of an industry that benefits from positive demographic trends, rising regional incomes, increasing food & beverage (F&B) spend, and growing demand for convenience. Where we differ: We expect robust earnings per share (EPS) growth of 29.7% in the next three years driven by aggressive store rollouts and margin expansion on scale efficiencies. Potential catalysts: (i) Upgrades in commissary, (ii) product and brand innovation, (iii) value-adding acquisitions and, (iv) expansion of food park. Valuation: Initiating coverage with BUY call and TP of P2.00. We have a fair value estimate of P4.4bn on the company, pegged to P/E of 20x on FY20 EPS of P0.10. There is a case for FRUIT to trade at par with peers given its industry leadership among local food stalls and kiosks operators. We have yet to factor in other growth strategies such as upgrade in commissaries, product innovation, value-adding M&A, and expansion of food park business. Key Risks to Our View: (i) Store network concentration risk – 50% in Metro Manila, (ii) unfavourable store network split and high operating leverage – 82% of outlets are company-owned, (iii) substitution risk from other food service options, (iv) inventory risk, (v) contamination risk and quality control mishaps. 57 77 97 117 137 157 177 197 217 1.0 1.1 1.2 1.3 1.4 1.5 1.6 1.7 1.8 1.9 Nov-19 Relative Index P Fruitas Holdings, Inc. (LHS) Relative PCOMP (RHS)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ed: KK/ sa: MR/ AS / CS / AH

BUY (Initiating Coverage)

Last Traded Price ( 15 Jan 2020): P1.45 (PCOMP : 7,664.40) Price Target 12-mth: P2.00 (38% upside)

Analyst

Regional Research Team

Price Relative

Forecasts and Valuation

FY Dec (P m) 2018A 2019F 2020F 2021F

Revenue 1,579 1,981 2,650 3,484 EBITDA 202 279 409 544 Pre-tax Profit 140 180 298 407 Net Profit 100 129 213 292 Net Pft (Pre Ex.) 93.9 129 213 292 Net Pft Gth (Pre-ex) (%) (45.7) 37.4 65.5 36.7 EPS (P) 0.06 0.06 0.10 0.14 EPS Pre Ex. (P) 0.06 0.06 0.10 0.14 EPS Gth Pre Ex (%) (46) 3 66 37 Diluted EPS (P) 0.06 0.06 0.10 0.14 Net DPS (P) 0.0 0.01 0.02 0.03 BV Per Share (P) 0.23 0.68 0.76 0.87 PE (X) 23.1 24.0 14.5 10.6 PE Pre Ex. (X) 24.7 24.0 14.5 10.6 P/Cash Flow (X) 16.7 13.3 8.6 6.6 EV/EBITDA (X) 11.7 7.7 5.2 3.7 Net Div Yield (%) 0.0 1.0 1.3 2.1 P/Book Value (X) 6.3 2.1 1.9 1.7 Net Debt/Equity (X) 0.1 CASH CASH CASH ROAE (%) 29.2 14.2 13.9 16.8

GIC Industry : Consumer Staples GIC Sector: Food & Staples Retailing Principal Business: Fruitas Holdings, Inc. is the holding company of one of the largest food and beverage kiosk operators in the Philippines, which serves various product offerings for low- to middle-income markets such as fresh fruit shakes and juices, lemonade, cooler

Source of all data on this page: Company, DBS Bank

Bloomberg Finance L.P.

At A Glance Issued Capital (m shrs) 533.7

Mkt. Cap (Pm/US$m) 774 / 15.3

Major Shareholders (%)

Lester Yu 21.1

Rai Properties 13.1

Free Float (%) 65.8

3m Avg. Daily Val (US$m) 1.8

DBS Group Research . Equity

Regional Company Focus

Fruitas Holdings, Inc. Bloomberg: FRUIT PM | Reuters: FRUIT.PS

Refer to important disclosures at the end of this report

16 Jan 2020

Scaling up and branching out• Versatile business model geared to navigate a

competitive and agile operating environment • Favourable exposure to the Philippines’ food service

landscape• Earnings growth driven by aggressive store rollouts and

scale efficiencies• Initiating coverage with a BUY rating and TP of P2.00

Initiating coverage on Fruitas Holdings, Inc. (Fruitas; FRUIT PM) with a BUY call and target price (TP) of P2.00. Fruitas Holdings, Inc. is the Philippines’ fastest growing diversified food and beverage kiosks operator, serving mostly snack items and fresh refreshments for low- to middle-income markets across the country. With over 17 years in operations, FRUIT has been apt in navigating a competitive and agile operating environment. It has a versatile business model that: a) generates value through strategic differentiation with a multi-branded and diversified product offering supported by a centralised commissary system and, b) has a rapidly expanding store network, enabled by its flexible store formats and backed by an in-house logistics and distribution infrastructure. We are of the view that FRUIT is well-positioned to expand brand visibility, accessibility, and reach, leading the growth of an industry that benefits from positive demographic trends, rising regional incomes, increasing food & beverage (F&B) spend, and growing demand for convenience.

Where we differ: We expect robust earnings per share (EPS) growth of 29.7% in the next three years driven by aggressive store rollouts and margin expansion on scale efficiencies.

Potential catalysts: (i) Upgrades in commissary, (ii) product and brand innovation, (iii) value-adding acquisitions and, (iv) expansion of food park.

Valuation: Initiating coverage with BUY call and TP of P2.00. We have a fair value estimate of P4.4bn on the company, pegged to P/E of 20x on FY20 EPS of P0.10. There is a case for FRUIT to trade at par with peers given its industry leadership among local food stalls and kiosks operators. We have yet to factor in other growth strategies such as upgrade in commissaries, product innovation, value-adding M&A, and expansion of food park business.

Key Risks to Our View: (i) Store network concentration risk – 50% in Metro Manila, (ii)

unfavourable store network split and high operating leverage – 82% of outlets are company-owned, (iii) substitution risk from other food service options, (iv) inventory risk, (v) contamination risk and quality control mishaps.

57

77

97

117

137

157

177

197

217

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

Nov-19

Relative IndexP

Fruitas Holdings, Inc. (LHS) Relative PCOMP (RHS)

Page 2

Company Focus

Fruitas Holdings, Inc.

Table of Contents

Investment Thesis 3

Valuation 6

SWOT Analysis 7

The Company 8

Key Management 9

Business Model 10

Competitive Strengths 13

Growth Strategies 16

Key Risks 16

Industry Analysis 17

Key Assumptions 21

Income Statement 22

Balance Sheet 23

Cash Flow Statement 24

Page 3

Company Focus

Fruitas Holdings, Inc.

Investment Thesis

FRUIT is the Philippines’ fastest growing chained food stalls and

kiosks operator with a national footprint spanning 949 outlets

as of June 2019. The company is equipped with a versatile

business model, geared to navigate a competitive and agile

operating environment. We are of the view that FRUIT has the

potential to lead the growth of an industry that stands to

benefit from a growing market’s increasing F&B per capita

spend, as well as rising demand for convenience. We expect

robust EPS growth in the next three years driven by aggressive

store rollouts and margin expansion on scale efficiencies.

Versatile business model geared to navigate a competitive and

agile operating environment

We believe that FRUIT’s business model can adapt to a highly

competitive industry marked by low barriers to entry and high

buyer bargaining power. On one hand, its differentiation

strategy allows the Group to boost value per outlet while

operating efficiently. On the other, investments in centralised

commissary and logistics infrastructure lay the ground for

scaling up and expanding reach to areas that are underserved

by chained stalls and kiosks.

#1 Generating value through strategic differentiation. Local

food stalls and kiosks engage in a highly competitive trade.

Low barriers to entry and minimal switching costs among

consumers have conferred a price-sensitive market with low

brand loyalty. Amid these market conditions, FRUIT has

propelled itself as the country’s fastest growing and more

profitable chained food stalls and kiosks operators through the

following:

A multi-branded and diversified product portfolio…. through

which FRUIT can appropriate suitable concepts depending on its

target market’s preferences. Currently, the Group competes in

seven categories for mainstream customers. It serves niche

markets with unique offerings through its company-operated

food parks. Acquisitions such as De Original Jamaican Pattie and

Sabroso Lechon continue to lead their respective categories in

terms of market share and growth.

Moreover, FRUIT’s array of complementary product offerings

can be sold in multi-branded outlets. We believe this is an

effective strategy in generating value. On one hand, brands can

leverage on scope economies as facilities are shared within the

same kiosk. On the other, this prevents customers from vetoing

purchases altogether, as outlets can provide more options than

competing operators with limited product offerings.

…supported by a centralised commissary system for key

offerings. This enables the Group to offer consistency and

quality to a wider market base. With standardised stock

keeping units (SKUs), the Group is able to grant its outlets

an aura of uniformity, allowing its brands to compete with

more established and higher-value chained food service

operators. FRUIT is able to generate a loyal following for

key products that are most visible and available to its target

consumers.

#2 Rapidly growing store network, furthering market

expanse and reach. With over 17 years in operations,

FRUIT’s management has grown apt to leveraging on the

agility of kiosk-type food service formats to locate in areas

that are unable to support full-scale operations. FRUIT’s

faster-than-industry store network growth is enabled by its

versatile outlet formats and backed by an efficient logistics

infrastructure, ultimately expanding brand visibility,

accessibility, and reach.

Versatile store formats. FRUIT can customise each outlet to

suit both ambience (upscale or economical) and available

selling area (as carts, kiosks, or larger in-line stalls) as

needed. This affords the Group the agility to locate itself in

areas with high foot traffic, most of which have limited

spaces, such as transport hubs and streets/walkways.

Improved brand visibility and accessibility enables FRUIT to

increase wallet shares in markets accustomed to proximity

and convenience.

In-house logistics and distribution infrastructure. Not only

does this enable the Group to maintain dependable service

levels for all its outlets, but more importantly it allows the

Group to advance its expanse and reach. We highlight this

as key to FRUIT’s rapid store expansion and to its distinctive

ability to stream down to areas currently dominated by

informal food service vendors, most of which are still

underserved by professionally managed chained operators.

These are the key strengths that enable the Group to

capitalise on the loosely regulated and spontaneous food

stalls and kiosks industry. With almost two decades of

operations, FRUIT has created a national footprint that

cannot be easily replicated. Its array of diversified yet

complementary brands makes for a valuable toolbox in

providing quality offerings and tailor-fitting outlets to each

market’s preferences. Moreover, through its efficient

logistics infrastructure, FRUIT can maintain consistent and

dependable service levels, especially in markets where

experience is just as important as prices.

Page 4

Company Focus

Fruitas Holdings, Inc.

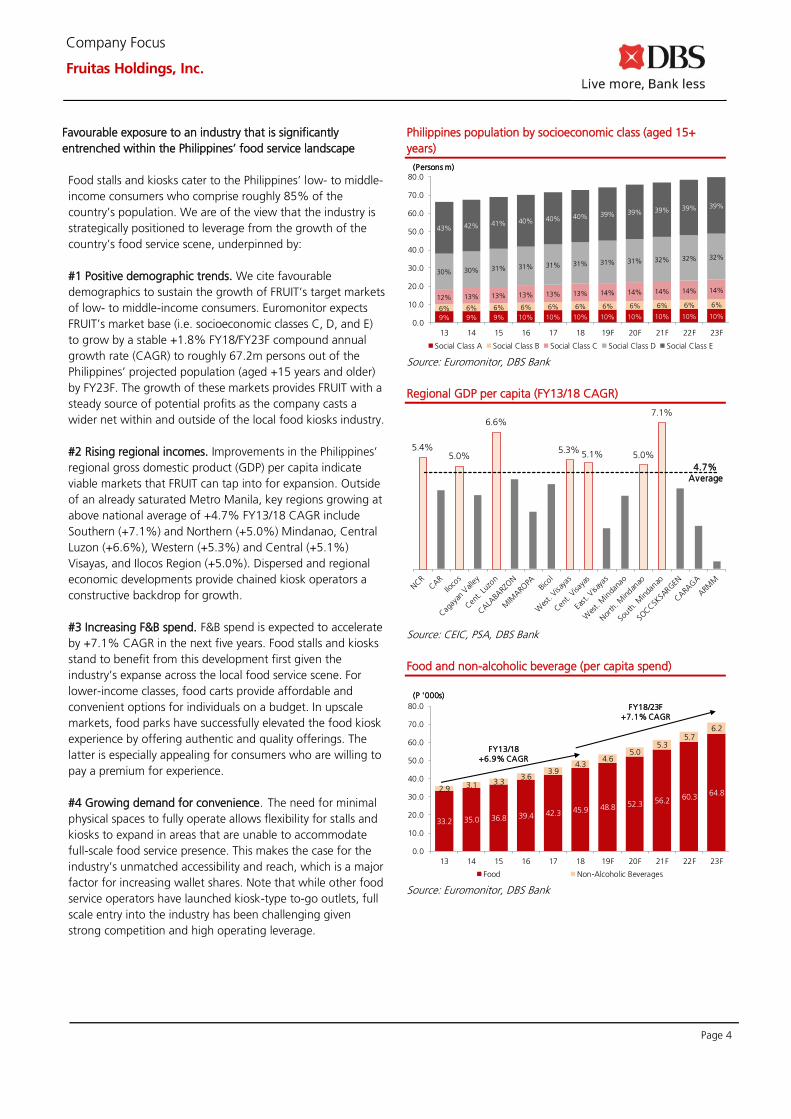

Favourable exposure to an industry that is significantly

entrenched within the Philippines’ food service landscape

Food stalls and kiosks cater to the Philippines’ low- to middle-

income consumers who comprise roughly 85% of the

country’s population. We are of the view that the industry is

strategically positioned to leverage from the growth of the

country’s food service scene, underpinned by:

#1 Positive demographic trends. We cite favourable

demographics to sustain the growth of FRUIT’s target markets

of low- to middle-income consumers. Euromonitor expects

FRUIT’s market base (i.e. socioeconomic classes C, D, and E)

to grow by a stable +1.8% FY18/FY23F compound annual

growth rate (CAGR) to roughly 67.2m persons out of the

Philippines’ projected population (aged +15 years and older)

by FY23F. The growth of these markets provides FRUIT with a

steady source of potential profits as the company casts a

wider net within and outside of the local food kiosks industry.

#2 Rising regional incomes. Improvements in the Philippines’

regional gross domestic product (GDP) per capita indicate

viable markets that FRUIT can tap into for expansion. Outside

of an already saturated Metro Manila, key regions growing at

above national average of +4.7% FY13/18 CAGR include

Southern (+7.1%) and Northern (+5.0%) Mindanao, Central

Luzon (+6.6%), Western (+5.3%) and Central (+5.1%)

Visayas, and Ilocos Region (+5.0%). Dispersed and regional

economic developments provide chained kiosk operators a

constructive backdrop for growth.

#3 Increasing F&B spend. F&B spend is expected to accelerate

by +7.1% CAGR in the next five years. Food stalls and kiosks

stand to benefit from this development first given the

industry’s expanse across the local food service scene. For

lower-income classes, food carts provide affordable and

convenient options for individuals on a budget. In upscale

markets, food parks have successfully elevated the food kiosk

experience by offering authentic and quality offerings. The

latter is especially appealing for consumers who are willing to

pay a premium for experience.

#4 Growing demand for convenience. The need for minimal

physical spaces to fully operate allows flexibility for stalls and

kiosks to expand in areas that are unable to accommodate

full-scale food service presence. This makes the case for the

industry’s unmatched accessibility and reach, which is a major

factor for increasing wallet shares. Note that while other food

service operators have launched kiosk-type to-go outlets, full

scale entry into the industry has been challenging given

strong competition and high operating leverage.

Philippines population by socioeconomic class (aged 15+

years)

Source: Euromonitor, DBS Bank

Regional GDP per capita (FY13/18 CAGR)

Source: CEIC, PSA, DBS Bank

Food and non-alcoholic beverage (per capita spend)

Source: Euromonitor, DBS Bank

9% 9% 9% 10% 10% 10% 10% 10% 10% 10% 10%6% 6% 6% 6% 6% 6% 6% 6% 6% 6% 6%

12% 13% 13% 13% 13% 13% 14% 14% 14% 14% 14%

30% 30% 31% 31% 31% 31% 31% 31% 32% 32% 32%

43% 42% 41% 40% 40% 40% 39% 39% 39% 39% 39%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

13 14 15 16 17 18 19F 20F 21F 22F 23F

Social Class A Social Class B Social Class C Social Class D Social Class E

(Persons m)

7.1%

5.0%5.1%5.3%

6.6%

5.0%5.4%

4.7%

Average

33.2 35.0 36.8 39.4 42.3 45.9 48.8 52.3 56.2 60.364.8

2.9 3.1 3.33.6

3.94.3

4.65.0

5.35.7

6.2

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

13 14 15 16 17 18 19F 20F 21F 22F 23F

Food Non-Alcoholic Beverages

(P '000s)

FY13/18+6.9% CAGR

FY18/23F+7.1% CAGR

Page 5

Company Focus

Fruitas Holdings, Inc.

Earnings growth driven by aggressive store rollouts and margin

expansion on scale efficiencies.

In the next three years, we are of the view that FRUIT can

deliver its planned store network rollout of roughly 750 stores

from FY20F to 22F. Additional stores should allow FRUIT to

reap further margins from scale efficiencies, generating faster-

than-peer earnings before interest, tax, depreciation and

amortisation (EBITDA) growth of 38.4% FY18-21F CAGR. We

forecast net profit margin to reach high single digits and ROE

at par with local/regional comparables.

We have yet to factor in FRUIT management’s other growth

strategies such as:

#1 Upgrade of commissary capacity. To accommodate

increased volumes, FRUIT plans to build two new facilities for

bottled juices by FY20F and an ice plant in FY21F.

#2 Product and brand innovation. FRUIT’s management is

always on the lookout for the next innovative concept in the

market. This is of utmost importance to stay relevant given

changing market preferences.

#3 Value-adding acquisitions with strategic fit. FRUIT remains

open to other viable acquisitions that can add value to the

company and further its goal of becoming the largest food

stalls and kiosks operator in the Philippines.

#4 Expand food park operations. FRUIT’s food parks are good

incubation grounds for novel and experimental concepts.

Through these, the company can test market reception of

new brands and product offerings without committing to

long term retail leases.

Sales trends

Source: DBS Bank

Profitability trends

Source: DBS Bank

Margin trends

Source: DBS Bank

1,152.6

1,579.2

1,981.1

2,649.7

3,484.3

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

17 18 19F 20F 21F

Sales, in P m

(P m)

0

50

100

150

200

250

300

350

400

450

17 18 19F 20F 21F

Operating Profit Pretax Profit Net Profit

(P m)

60.2

56.1 56.2 56.3 56.5

22.7

12.7 13.6 15.0 15.3

15.0

6.4 6.5 8.1 8.4

17 18 19F 20F 21F

Gross Margin EBITDA Margin Net Margin

Page 6

Company Focus

Fruitas Holdings, Inc.

Valuation Initiate coverage with a BUY and TP of P2.0. Our TP has an

upside of 35% and is pegged at a PE of 20.0x on FY20F EPS

of P0.10.

There is a case for FRUIT to trade at par to its peers given its

industry leadership among local food stalls and kiosks

operators. We expect robust EPS growth of 29.7% in FY18-

21F driven by aggressive store rollouts and margin expansion

on scale efficiencies. We forecast net profit margin to reach

high single digits and ROE at par with local/regional

comparables.

Peer comparison

Source: Refinitiv, DBS Bank

Mkt EPS CAGR EBITDA

Price Cap FY18-21F 20F 21F FY18-21F 20F 21F 20F 21F 20F 21F 20F 21F 20F 21F

Company Name Loca l$ US$m % x x CAGR % x x % % % % % % x x

ASEAN

Minor International PCL 34.5 5,280 17.4% 23.2 20.6 29.1% 12.2 11.4 9.0 9.9 5.8 6.3 1.7 1.8 2.0 1.9

MK Restaurant Group PCL 69.8 2,128 4.9% 22.8 21.6 11.0% 12.2 11.6 19.4 19.8 15.0 14.9 4.1 4.4 4.3 4.2

Central Plaza Hotel PCL 24.0 1,074 (4.6)% 18.6 17.1 3.4% 8.2 7.5 12.3 12.3 7.8 8.0 2.4 2.6 2.2 2.0

After You Public Co Ltd 10.4 281 29.2% 29.7 26.7 22.7% 21.0 19.2 25.0 24.6 21.3 23.6 1.9 1.9 NaN NaN

BreadTalk Group Ltd 0.7 272 1.0% 28.7 22.2 29.9% 5.7 5.1 10.2 12.3 1.9 2.4 3.2 3.4 2.6 2.4

Koufu Group Ltd 0.8 319 4.8% 14.5 14.0 43.6% 4.6 4.3 27.3 25.0 11.5 11.8 3.7 3.9 3.6 3.2

Kimly Ltd 0.2 206 1.5% 12.0 12.0 0.7% 7.1 6.8 23.8 23.1 9.8 9.9 4.2 4.2 3.0 2.7

Japan Foods Holding Ltd 0.5 58 (12.3)% 21.4 19.6 (6.8)% 11.4 10.2 10.0 11.2 4.7 5.4 4.7 4.7 2.4 2.4

JUMBO Group Ltd 0.4 181 8.9% 17.7 17.7 8.9% 9.2 8.4 19.1 18.6 8.1 8.3 3.5 3.2 3.1 2.9

Fast Food Indonesia Tbk PT 2,490.0 364 26.8% 13.6 11.5 25.3% 7.2 6.3 20.4 21.7 4.8 5.6 NaN NaN NaN NaN

Berjaya Food Bhd 1.3 125 41.4% 21.1 16.3 15.5% 7.7 7.5 6.8 7.8 3.3 3.7 3.2 3.5 1.3 1.3

Average 10.8% 20.3 18.1 16.7% 9.7 9.0 16.7 16.9 8.5 9.1 3.3 3.4 2.7 2.6

Phil ippines

Jollibee Foods Corp 212.0 4,594 (2.0)% 35.3 29.4 8.3% 16.2 14.6 11.9 13.4 3.2 3.4 1.1 1.3 4.1 3.8

Shakey's Pizza Asia Ventures Inc 9.4 284 11.6% 13.9 12.3 12.6% 10.1 9.0 17.5 17.3 11.0 11.2 1.7 1.9 2.4 2.0

Max's Group Inc 11.2 241 13.7% 11.3 9.8 11.9% 8.6 7.6 12.0 12.6 5.1 5.3 1.3 1.5 1.3 1.2

Average 7.8% 20.2 17.1 11.0% 11.7 10.4 13.8 14.4 6.4 6.6 1.4 1.6 2.6 2.3

Fruitas Holdings Inc 29.7% 20.0 14.6 38.4% 8.3 6.0 13.9 16.8 8.1 8.4 0.9 1.5 3.0 2.6

P/BkP/E EV/EBITDA ROE Net Margin Yie ld

Page 7

Company Focus

Fruitas Holdings, Inc.

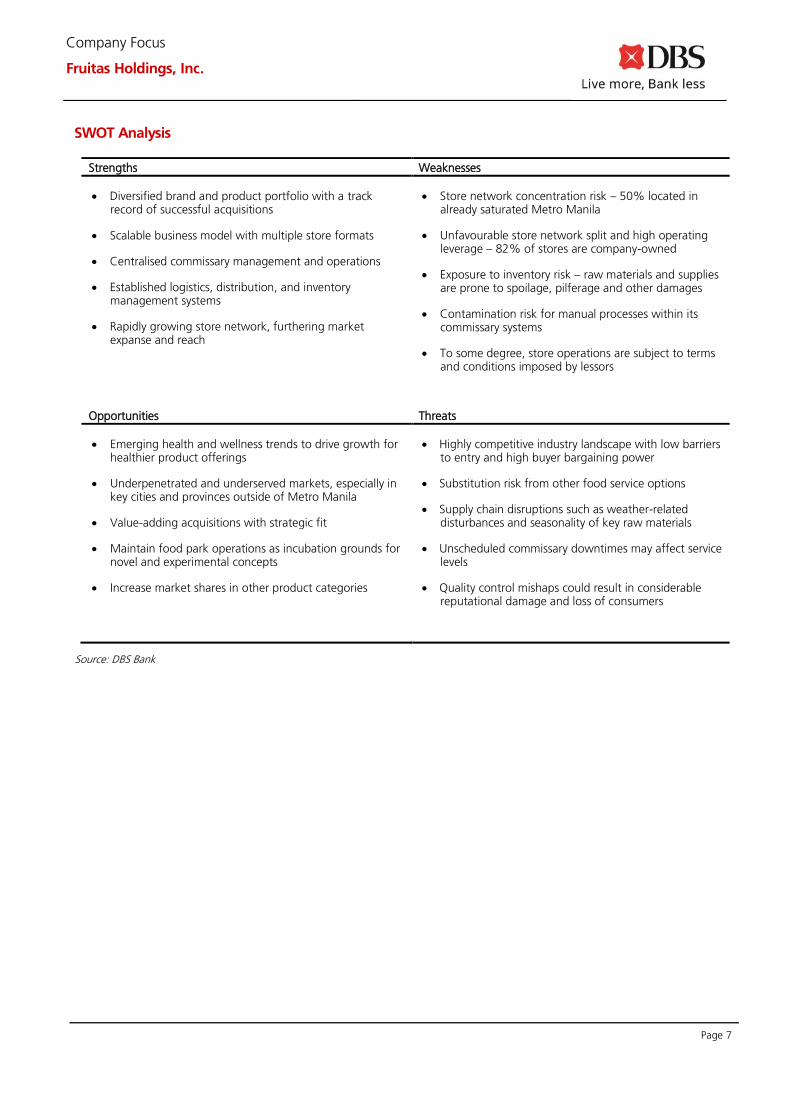

SWOT Analysis

Strengths Weaknesses

• Diversified brand and product portfolio with a track record of successful acquisitions

• Scalable business model with multiple store formats

• Centralised commissary management and operations

• Established logistics, distribution, and inventory management systems

• Rapidly growing store network, furthering market expanse and reach

• Store network concentration risk – 50% located in already saturated Metro Manila

• Unfavourable store network split and high operating leverage – 82% of stores are company-owned

• Exposure to inventory risk – raw materials and supplies are prone to spoilage, pilferage and other damages

• Contamination risk for manual processes within its commissary systems

• To some degree, store operations are subject to terms and conditions imposed by lessors

Opportunities Threats

• Emerging health and wellness trends to drive growth for healthier product offerings

• Underpenetrated and underserved markets, especially in key cities and provinces outside of Metro Manila

• Value-adding acquisitions with strategic fit

• Maintain food park operations as incubation grounds for novel and experimental concepts

• Increase market shares in other product categories

• Highly competitive industry landscape with low barriers to entry and high buyer bargaining power

• Substitution risk from other food service options

• Supply chain disruptions such as weather-related disturbances and seasonality of key raw materials

• Unscheduled commissary downtimes may affect service levels

• Quality control mishaps could result in considerable reputational damage and loss of consumers

Source: DBS Bank

Page 8

Company Focus

Fruitas Holdings, Inc.

The Company

Company background. FRUIT is the holding company of one of

the largest food and beverage kiosk operators in the

Philippines, which serves various product offerings for low- to

middle-income markets across its 949 stores nationwide (as of

June 2019). Menu items include fresh fruit shakes and juices,

lemonade, coolers, milk tea, desserts, meat-filled pastries, and

lechon (roasted pig), among others.

Corporate history. The Group traces its roots to Lush

Enterprises Corporation (LEC), which was incorporated by

founder Mr. Lester C. Yu in 2000. In 2002, its first store Fruitas

Fresh from Babot’s Farm opened at SM Manila. From 2004

through 2013, the Group launched and expanded its product

offerings and brands to include Juice Avenue, Buko ni Fruitas,

The Mango Farm, Black Pearl, Fruitas Ice Candy, Buko Loco,

Friends Fries, Tea-Rex, House of Desserts, and 7,107 Halo-Halo

Islands.

In 2015, The Lush Company, Inc. (later renamed to Fruitas

Holdings, Inc. or FHI) was incorporated. FRUIT has since been

reorganised to consolidate the Group’s operations, including

recent acquisitions (De Original Jamaican Pattie Shop and Juice

and Sabroso Lechon) and other new launches (such as Johnn

Lemon, Shou, House of Fruitas, among others). As of June

2019, FRUIT’s store network totalled 949 outlets nationwide. It

also operates two food parks (Uno Cinquenta and Le Village

Lifestyle Park) via its subsidiary, Fruitasgroup Incorporated.

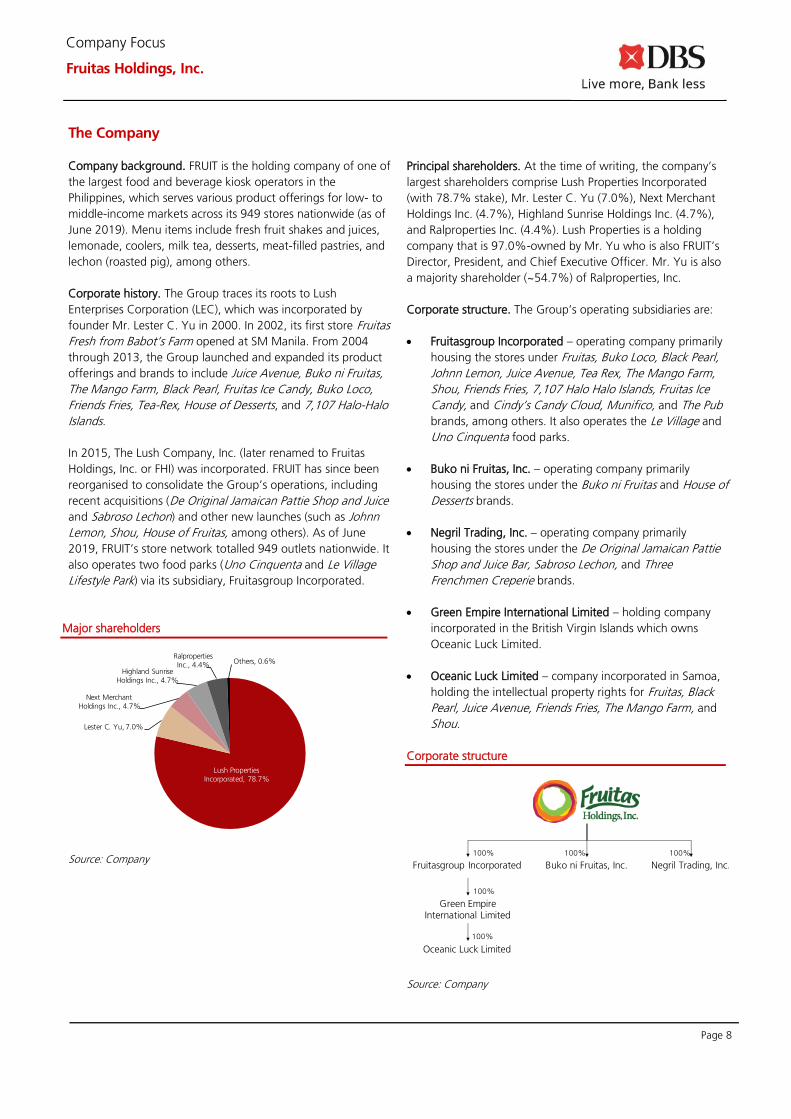

Major shareholders

Source: Company

Principal shareholders. At the time of writing, the company’s

largest shareholders comprise Lush Properties Incorporated

(with 78.7% stake), Mr. Lester C. Yu (7.0%), Next Merchant

Holdings Inc. (4.7%), Highland Sunrise Holdings Inc. (4.7%),

and Ralproperties Inc. (4.4%). Lush Properties is a holding

company that is 97.0%-owned by Mr. Yu who is also FRUIT’s

Director, President, and Chief Executive Officer. Mr. Yu is also

a majority shareholder (~54.7%) of Ralproperties, Inc.

Corporate structure. The Group’s operating subsidiaries are:

• Fruitasgroup Incorporated – operating company primarily

housing the stores under Fruitas, Buko Loco, Black Pearl,

Johnn Lemon, Juice Avenue, Tea Rex, The Mango Farm,

Shou, Friends Fries, 7,107 Halo Halo Islands, Fruitas Ice

Candy, and Cindy’s Candy Cloud, Munifico, and The Pub

brands, among others. It also operates the Le Village and

Uno Cinquenta food parks.

• Buko ni Fruitas, Inc. – operating company primarily

housing the stores under the Buko ni Fruitas and House of

Desserts brands.

• Negril Trading, Inc. – operating company primarily

housing the stores under the De Original Jamaican Pattie

Shop and Juice Bar, Sabroso Lechon, and Three

Frenchmen Creperie brands.

• Green Empire International Limited – holding company

incorporated in the British Virgin Islands which owns

Oceanic Luck Limited.

• Oceanic Luck Limited – company incorporated in Samoa,

holding the intellectual property rights for Fruitas, Black

Pearl, Juice Avenue, Friends Fries, The Mango Farm, and

Shou.

Corporate structure

Source: Company

Lush Properties Incorporated, 78.7%

Lester C. Yu, 7.0%

Next Merchant Holdings Inc., 4.7%

Highland Sunrise Holdings Inc., 4.7%

Ralproperties Inc., 4.4%

Others, 0.6%

Fruitasgroup Incorporated

Green Empire International Limited

Oceanic Luck Limited

Buko ni Fruitas, Inc. Negril Trading, Inc.

100% 100% 100%

100%

100%

Page 9

Company Focus

Fruitas Holdings, Inc.

Key Management Team

Current Position Previous Experience

Lester C. Yu Director, President, and

Chief Executive Officer

Mr. Yu has been Fruitas’ President and Chief Executive Officer since

its incorporation, concurrently serving as its Chairman from February

2015 through August 2019. He started his career with his family

business Janette Jewelry in 1989. Before founding the group, he

entered the banking industry and served as the youngest Branch

Manager for Westmont Bank. Mr. Yu gained his B.S. Industrial

Management Engineering degree from De La Salle University and a

Master of Business Administration from the University of the

Philippines.

Irene O. Chua Director, Chief Financial

Officer and Treasurer

Ms. Chua was appointed as Fruitas’ Chief Financial Officer and

Treasurer on August 2019. She has been with the Fruitas Group as a

consultant since March 2014. Prior to joining the Group, she was an

Assistant Vice President in the Philippine National Bank where she

worked for 34 years. She is also the President and Director of Sure

Jobs Academy, Inc. Ms. Chua holds a BS Business Administration

degree from the University of Santo Tomas.

Calvin F. Chua Director and Chief Financial

Adviser

Mr. Cua was elected as a Director and Chief Financial Adviser on

August 2019, serving as a consultant for the Group since May 2017.

Mr. Chua previously held roles as Director and consultant of ING

Bank N.V., Manila Branch. He received his degrees of BS

Management Engineering and BA Economics (Honors Program) from

Ateneo de Manila University.

Madelene T.

Sayson Chief Operating Officer

Ms. Sayson served as a Director of Fruitas from February 2015 to

August.2019. She is concurrently the Chairman and President of

Gyuma Fragrance Inc., and the Corporate Secretary and Director for

One Fifty Food Place, Inc., Lush Properties Inc., Negril Trading, Inc.,

Bamazeh Incorporated, Dough Matters, Inc., Sure Jobs Academy,

Inc., and Toyoda Technik Corporation. Ms. Sayson earned her BS

Accountancy degree from Garcia College of Technology.

Roselyn A. Legaspi Managing Director – Visayas

and Mindanao

Ms. Legaspi served as a Director of Fruitas from February 2015 to

August 2019. She is also the Vice President and Director of Negril

Trading, Inc., Bamazeh Inc., Lush Properties Incorporated,

Ralproperties Inc., and Sure Jobs Academy Inc. She is a Director for

Gyuma Fragrance Inc., Lush Harvest Manufacturing Inc.,

Themangofarm Corp., La Petite Parisienne, Inc., and Lush Enterprises

Corp. Ms. Legaspi is the Treasurer of Fruitasgroup Incorporated and

Buko ni Fruitas, Inc. Ms Legaspi holds a BS Accountancy degree. She

is currently taking up MBA at the University of San Carlos, Cebu City.

Marvin C. Yu Corporate Secretary

Mr. Yu was a consultant in the SMC Telco Project, Master Planning

Network Coverage Senior Manager for the Sun Cellular 2G and 3G

Project, and RF Network Planning, Design and Optimization Engineer

for Smart Communications Inc. Mr. Yu completed his education at

De La Salle University with a degree of BS Electronics and

Communications Engineering.

Source: Company

Page 10

Company Focus

Fruitas Holdings, Inc.

The Business

Fruitas Holdings, Inc. is one of the Philippines’ largest

diversified food and beverage kiosk operators, serving mostly

snack items and fresh refreshments for low- to middle-income

markets across the country.

Brands and menu offerings. The Group boasts of a multi-

branded portfolio of food stalls and kiosks, offering various

food and beverage items ranging from fresh fruit shakes and

juices, lemonade, coolers, milk tea, desserts, meat-filled

pastries, and lechon (roasted pig). Of its 24 active brands,

among the more popular ones are Fruitas for fruit shakes, Juice

Avenue for juices and smoothies, Buko Loco and Buko ni

Fruitas for coconut-based refreshments, Black Pearl for coolers,

Johnn Lemon for lemonade, De Original Jamaican Pattie for

meat-filled pastries, and Friends Fries for fries category.

According to UA&P Center for Food and Agribusiness, in 2018

FRUIT dominated as a major player in four major kiosk

categories (fruit shakes, lemonade, meat-filled pastries, and

coconut-based refreshments).

Store formats. Store formats vary depending on available

leasable spaces and market ambience. Among these are

smaller carts and kiosks as well as larger in-line food stalls.

Most outlets are located within densely populated areas such

as malls, schools, hospitals, food courts, and other commercial

establishments.

The company operates two food parks Uno Cinquenta (600

sqm) and Le Village Lifestyle Park (1,646 sqm), both located in

Quezon City, Metro Manila.

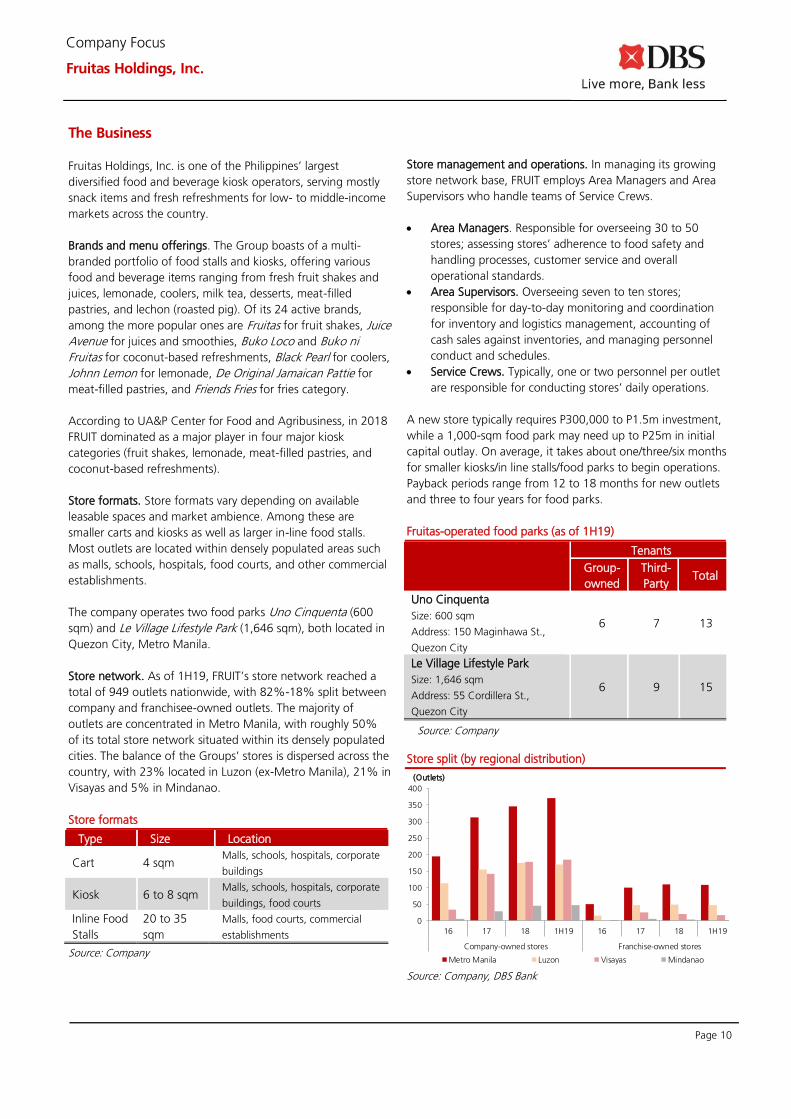

Store network. As of 1H19, FRUIT’s store network reached a

total of 949 outlets nationwide, with 82%-18% split between

company and franchisee-owned outlets. The majority of

outlets are concentrated in Metro Manila, with roughly 50%

of its total store network situated within its densely populated

cities. The balance of the Groups’ stores is dispersed across the

country, with 23% located in Luzon (ex-Metro Manila), 21% in

Visayas and 5% in Mindanao.

Store formats

Type Size Location

Cart 4 sqm Malls, schools, hospitals, corporate

buildings

Kiosk 6 to 8 sqm Malls, schools, hospitals, corporate

buildings, food courts

Inline Food

Stalls

20 to 35

sqm

Malls, food courts, commercial

establishments

Source: Company

Store management and operations. In managing its growing

store network base, FRUIT employs Area Managers and Area

Supervisors who handle teams of Service Crews.

• Area Managers. Responsible for overseeing 30 to 50

stores; assessing stores’ adherence to food safety and

handling processes, customer service and overall

operational standards.

• Area Supervisors. Overseeing seven to ten stores;

responsible for day-to-day monitoring and coordination

for inventory and logistics management, accounting of

cash sales against inventories, and managing personnel

conduct and schedules.

• Service Crews. Typically, one or two personnel per outlet

are responsible for conducting stores’ daily operations.

A new store typically requires P300,000 to P1.5m investment,

while a 1,000-sqm food park may need up to P25m in initial

capital outlay. On average, it takes about one/three/six months

for smaller kiosks/in line stalls/food parks to begin operations.

Payback periods range from 12 to 18 months for new outlets

and three to four years for food parks.

Fruitas-operated food parks (as of 1H19)

Tenants

Group-

owned

Third-

Party Total

Uno Cinquenta

Size: 600 sqm

Address: 150 Maginhawa St.,

Quezon City

6 7 13

Le Village Lifestyle Park

Size: 1,646 sqm

Address: 55 Cordillera St.,

Quezon City

6 9 15

Source: Company

Store split (by regional distribution)

Source: Company, DBS Bank

0

50

100

150

200

250

300

350

400

16 17 18 1H19 16 17 18 1H19

Company-owned stores Franchise-owned stores

Metro Manila Luzon Visayas Mindanao

(Outlets)

Page 11

Company Focus

Fruitas Holdings, Inc.

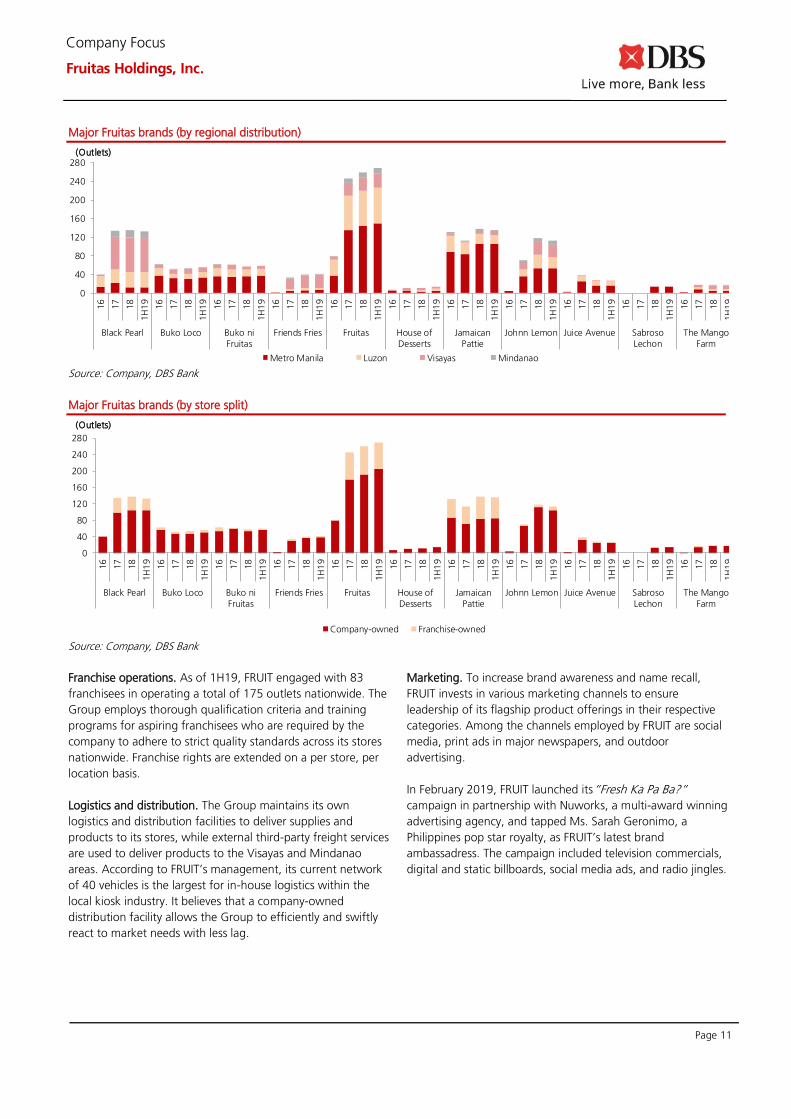

Major Fruitas brands (by regional distribution)

Source: Company, DBS Bank

Major Fruitas brands (by store split)

Source: Company, DBS Bank

Franchise operations. As of 1H19, FRUIT engaged with 83

franchisees in operating a total of 175 outlets nationwide. The

Group employs thorough qualification criteria and training

programs for aspiring franchisees who are required by the

company to adhere to strict quality standards across its stores

nationwide. Franchise rights are extended on a per store, per

location basis.

Logistics and distribution. The Group maintains its own

logistics and distribution facilities to deliver supplies and

products to its stores, while external third-party freight services

are used to deliver products to the Visayas and Mindanao

areas. According to FRUIT’s management, its current network

of 40 vehicles is the largest for in-house logistics within the

local kiosk industry. It believes that a company-owned

distribution facility allows the Group to efficiently and swiftly

react to market needs with less lag.

Marketing. To increase brand awareness and name recall,

FRUIT invests in various marketing channels to ensure

leadership of its flagship product offerings in their respective

categories. Among the channels employed by FRUIT are social

media, print ads in major newspapers, and outdoor

advertising.

In February 2019, FRUIT launched its”Fresh Ka Pa Ba?”

campaign in partnership with Nuworks, a multi-award winning

advertising agency, and tapped Ms. Sarah Geronimo, a

Philippines pop star royalty, as FRUIT’s latest brand

ambassadress. The campaign included television commercials,

digital and static billboards, social media ads, and radio jingles.

0

40

80

120

160

200

240

280

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

Black Pearl Buko Loco Buko niFruitas

Friends Fries Fruitas House ofDesserts

JamaicanPattie

Johnn Lemon Juice Avenue SabrosoLechon

The MangoFarm

Metro Manila Luzon Visayas Mindanao

(Outlets)

0

40

80

120

160

200

240

280

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

16

17

18

1H

19

Black Pearl Buko Loco Buko niFruitas

Friends Fries Fruitas House ofDesserts

JamaicanPattie

Johnn Lemon Juice Avenue SabrosoLechon

The MangoFarm

Company-owned Franchise-owned

(Outlets)

Page 12

Company Focus

Fruitas Holdings, Inc.

Commissary management and operations. FRUIT maintains

four commissaries to support its existing operations. These are:

• Fruitasgroup Inc (FGI) Commissary. Fruits are delivered

daily to the two FGI commissaries where FRUIT’s fresh

fruits requirements are delivered by different suppliers

daily. Initial quality checks are conducted to ensure

consistency of inputs to production. After processing,

finished goods are stored in the commissary until picked

up by company-owned trucks for delivery to stores.

• Negril Trading Inc (NTI-Sabroso) Commissary. For Sabroso

Lechon, partially cleaned carcasses are received and again

cleaned and rinsed to ensure quality and cleanliness of the

pigs. Subsequently, the carcasses are sorted according to

size before roasting. The stuffed carcasses are roasted for

a maximum of five hours. Temperature and oil drippings

are constantly monitored. A final quality check prior to

packaging is done before packing and delivering the

Lechon to retail and institutional clients.

• Negril Trading Inc (NTI-Jamaican Pattie) Commissary. As

with other commissaries, FRUIT’s facility for Jamaican

Pattie enforces quality checks at various stages of

production, from raw material (filling and dough)

preparation to filling to pattie labelling and baking. Two-

level checks for critical steps in ingredients mixing, as well

as food taste and visual checks for required product

attributes are conducted to ensure desired quality

standards.

Suppliers. The Group’s key suppliers include Aeroplast

Industries Inc., Multiplast Corporation, STC Vigour Packaging

Philippines Inc.; McBride Corporation for various packaging;

Westpac Meat Processing Corp. for meat; and Hermano Oil

Mfg. and Sugar Corp. and First Boundary Rider Trading Corp.

for sugar. The company employs local suppliers for its fruits

requirements. The Group currently does not have fixed price

contracts with any of its suppliers.

Employees. As of 1H19, FRUIT employed1,715 direct hires.

Depending on demand, management engages third-party

agencies to augment manpower requirements including

commissary staff, drivers, security personnel, and utility staff.

Competition. Major competitors of FRUIT in the local food

stall/kiosks industry include:

• JC Worldwide Franchise Inc. started in 2006 with Burger

Factory. Over the years, its brands expanded to include

Siopao “Da” King, Noodle House, Sgt. Sisig, and Siomai

King.

• Cinco Holdings Co. which launched its first Potato Corner

store back in 1992 and has since expanded to foreign

markets such as the United States, Australia, Singapore,

Hong Kong, and Thailand, among others. With its 27-year

track record, Cinco Holdings Co. has also won awards for

its branding and business model success.

• Duskin Co. Ltd. is a Japan-based franchisor in Asia which

started its first franchise “Mister Donut” in the Philippines

in 1982. Currently, its Mister Donut brand has at least

5500 stores worldwide with more than 700 outlets

located in the Philippines. Mister Donut has been a well-

known brand in the country because of its accessibility via

convenience stores.

• San Miguel Corporation’s Food Group also competes in

the kiosk industry with its famous “Purefoods Tender Juicy

Hotdogs,” and has about 530 stalls nationwide.

Page 13

Company Focus

Fruitas Holdings, Inc.

Competitive Strengths

Diversified brand and product portfolio, with a track record of

successful acquisitions. The Group offers the market a wide

array of brands and product offerings that cater to various

trends and consumer preferences.

Currently, the Group competes in seven categories; fruit

shakes (“Fruitas”), juices and smoothies (“Juice Avenue”),

buko-based drinks (“Buko Loco” and “Buko ni Fruitas”),

coolers (“Black Pearl”), lemonade (“Johnn Lemon”), meat-

filled pastries (“De Original Jamaican Pattie”), and fries

(“Friends Fries”). It serves niche markets with several other

unique offerings (“Munifico Pizzeria”, “The Pub”, and “Uva”,

among others). Its management also has a history of successful

acquisitions with the likes of De Original Jamaican Pattie and

Sabroso Lechon, which continue to lead the industry in terms

of market share and growth.

Subject to each outlet’s intended locale, FRUIT’s on-the-ground

personnel can determine which brands are suitable and will

likely generate optimal revenues for the Group. Social media

scanning is employed to gather market feedback for both

existing and newly introduced product offerings.

Diversified brand portfolio

Source: Company

Cost-efficient, multi-branded and versatile store formats.

Enabling the company’s broad national footprint are its three

store formats: carts (~4sqm), kiosks (~6 to 8 sqm), and in-line

stalls (~20 to 35 sqm). This allows for agility in locating to high

foot traffic areas, most of which have limited available selling

spaces such as transport terminals and streets/walkways,

adding accessibility and brand visibility for its consumers.

With FRUIT’s over 20 active brands, each outlet may be

tailored to host multi-branded offerings to fit the preferences

of each locale. This boosts value per outlet by encouraging

higher spend per transaction while reducing operating costs as

brands share facilities within the same kiosk.

Versatile store formats

Source: Company

Carts

Kiosks

In-Line Stalls

Page 14

Company Focus

Fruitas Holdings, Inc.

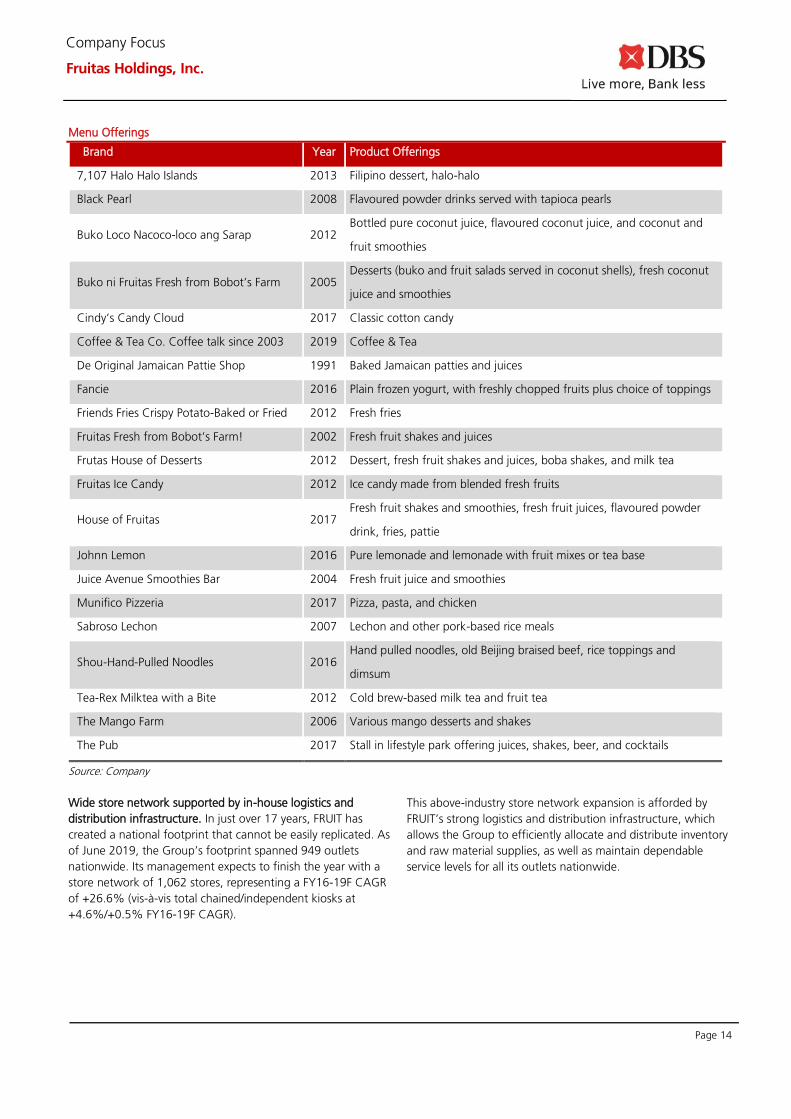

Menu Offerings

Brand Year Product Offerings

7,107 Halo Halo Islands 2013 Filipino dessert, halo-halo

Black Pearl 2008 Flavoured powder drinks served with tapioca pearls

Buko Loco Nacoco-loco ang Sarap 2012 Bottled pure coconut juice, flavoured coconut juice, and coconut and

fruit smoothies

Buko ni Fruitas Fresh from Bobot’s Farm 2005 Desserts (buko and fruit salads served in coconut shells), fresh coconut

juice and smoothies

Cindy’s Candy Cloud 2017 Classic cotton candy

Coffee & Tea Co. Coffee talk since 2003 2019 Coffee & Tea

De Original Jamaican Pattie Shop 1991 Baked Jamaican patties and juices

Fancie 2016 Plain frozen yogurt, with freshly chopped fruits plus choice of toppings

Friends Fries Crispy Potato-Baked or Fried 2012 Fresh fries

Fruitas Fresh from Bobot’s Farm! 2002 Fresh fruit shakes and juices

Frutas House of Desserts 2012 Dessert, fresh fruit shakes and juices, boba shakes, and milk tea

Fruitas Ice Candy 2012 Ice candy made from blended fresh fruits

House of Fruitas 2017 Fresh fruit shakes and smoothies, fresh fruit juices, flavoured powder

drink, fries, pattie

Johnn Lemon 2016 Pure lemonade and lemonade with fruit mixes or tea base

Juice Avenue Smoothies Bar 2004 Fresh fruit juice and smoothies

Munifico Pizzeria 2017 Pizza, pasta, and chicken

Sabroso Lechon 2007 Lechon and other pork-based rice meals

Shou-Hand-Pulled Noodles 2016 Hand pulled noodles, old Beijing braised beef, rice toppings and

dimsum

Tea-Rex Milktea with a Bite 2012 Cold brew-based milk tea and fruit tea

The Mango Farm 2006 Various mango desserts and shakes

The Pub 2017 Stall in lifestyle park offering juices, shakes, beer, and cocktails

Source: Company

Wide store network supported by in-house logistics and

distribution infrastructure. In just over 17 years, FRUIT has

created a national footprint that cannot be easily replicated. As

of June 2019, the Group’s footprint spanned 949 outlets

nationwide. Its management expects to finish the year with a

store network of 1,062 stores, representing a FY16-19F CAGR

of +26.6% (vis-à-vis total chained/independent kiosks at

+4.6%/+0.5% FY16-19F CAGR).

This above-industry store network expansion is afforded by

FRUIT’s strong logistics and distribution infrastructure, which

allows the Group to efficiently allocate and distribute inventory

and raw material supplies, as well as maintain dependable

service levels for all its outlets nationwide.

Page 15

Company Focus

Fruitas Holdings, Inc.

Highly scalable business model enabled by a centralised

commissary system. Further allowing its large and growing

scale are FRUIT’s commissaries. To service roughly 1,000

outlets across the country, FRUIT currently maintains four

commissaries: (a) two FGI Commissaries (bottled juices)

dedicated to the production of bottled fruit juices and buko-

based refreshments; (b) NTI Commissary (Jamaican Pattie) for

its category-leading meat-filled pastry brand, De Original

Jamaican Pattie; and (c) NTI Commissary (Sabroso) for its most

recent acquisition and newest product segment Sabroso

Lechon.

FRUIT’s investments for the bulk production of its key product

offerings are significant in keeping consistent quality while

allowing for the Group to reap economies of scale in its

production.

Page 16

Company Focus

Fruitas Holdings, Inc.

Growth Strategies

Expand national footprint, especially in key regions outside of

Metro Manila. The Group plans to expand its store network by

200 to 300 stores annually in the next three years. Roughly

65% of these will be in Metro Manila and Luzon, while the

balance will be set up in Visayas and Mindanao.

Outside of Metro Manila, among targeted cities and provinces

are La Union, Laoag, Bataan, Bulacan, Pampanga, and Cavite

for Luzon; Cebu, Ormoc, Bacolod, and Roxas for Visayas; and

Davao, Zamboanga, Butuan, and Ozamiz in Mindanao. FRUIT’s

management aims to maintain store network split between

company/franchise-owned stores at 80%-20%.

Upgrade commissary capacity. To accommodate increased

volumes, FRUIT is planning to build two new facilities for

bottled juices – one in Quezon City, Metro Manila (online by

1Q20) and another in Cebu, Visayas (by 2Q20). The new

commissary in Quezon City is expected to double current

volumes for bottled juices in Metro Manila and Luzon, while

the other in Cebu is expected to augment volumes for Visayas

and Mindanao.

FRUIT’s investment in an ice plant (1Q21) is estimated by its

management to lead to roughly 15% cost savings in the

production of ice.

Product and brand innovation. Despite having over 20 brands

in its portfolio, FRUIT remains on the lookout for the next

blockbuster food and/or beverage concept that will capture

wallet shares. We believe that consistent innovation is

important to maintain relevance amid changing market

preferences.

Seek value-adding acquisitions with strategic fit. The company

has successfully identified value-adding acquisitions in the past

with the likes of De Original Jamaican Pattie and Sabroso

Lechon. Moving forward, FRUIT’s management remains open

to other viable acquisitions that could further its goal of

becoming the largest food stalls and kiosks operator in the

Philippines. Roughly P300m is being allocated by FRUIT’s

management for two or more acquisitions in the next two

years.

Expand food park operations. We agree that food parks are

good incubation grounds for novel and experimental concepts.

This allows the company to try out new brands and product

offerings without committing to long term retail leases.

Currently, FRUIT’s management is evaluating possible locations

within Luzon. The option of leasing suitable spaces in existing

commercial establishments is also on the table, potentially

establishing FRUIT-operated food courts that will house the

Group’s brands.

Key Risks

Store network concentration risk. Roughly 50% of the Group’s

outlets are in Metro Manila. This exposes the company to

substantial competition, especially given current levels of

saturation in the country’s National Capital Region.

Store cannibalisation. The Group’s outlets, despite varying

brands and product offerings, cater to the same target market

and compete for the same share of wallet. This poses risks of

sales cannibalisation among stores, especially when redundant

product offerings are located in the same area.

Product substitution. Low switching cost among consumers

poses a palpable substitution risk for the company’s product

offerings vis-à-vis other food service alternatives.

High buyer bargaining power. FRUIT’s target market is

generally price-sensitive, marked by the absence of brand

loyalty. Investments in marketing and innovation are

paramount to remain relevant and sustain market shares,

although pricing flexibility and potential profits are limited due

to high buyer bargaining power.

High rental costs. Despite low physical space requirements for

FRUIT’s outlets, rental still comprises 14% of its annual sales

due to the Group’s large aggregate net selling area.

Logistical disruption. Weather-related disturbances, traffic and

other logistical challenges may negatively affect service levels

given FRUIT’s just-in-time delivery setup.

Quality control mishaps. This could result in considerable

reputational damage and loss of customers. We flag manual

processes of FRUIT’s commissary systems as having high risk of

contamination and human error due to potential mishandling

and processing of food items.

Inventory risk. Raw materials and supplies are prone to

spoilage, pilferage and other damages.

Page 17

Company Focus

Fruitas Holdings, Inc.

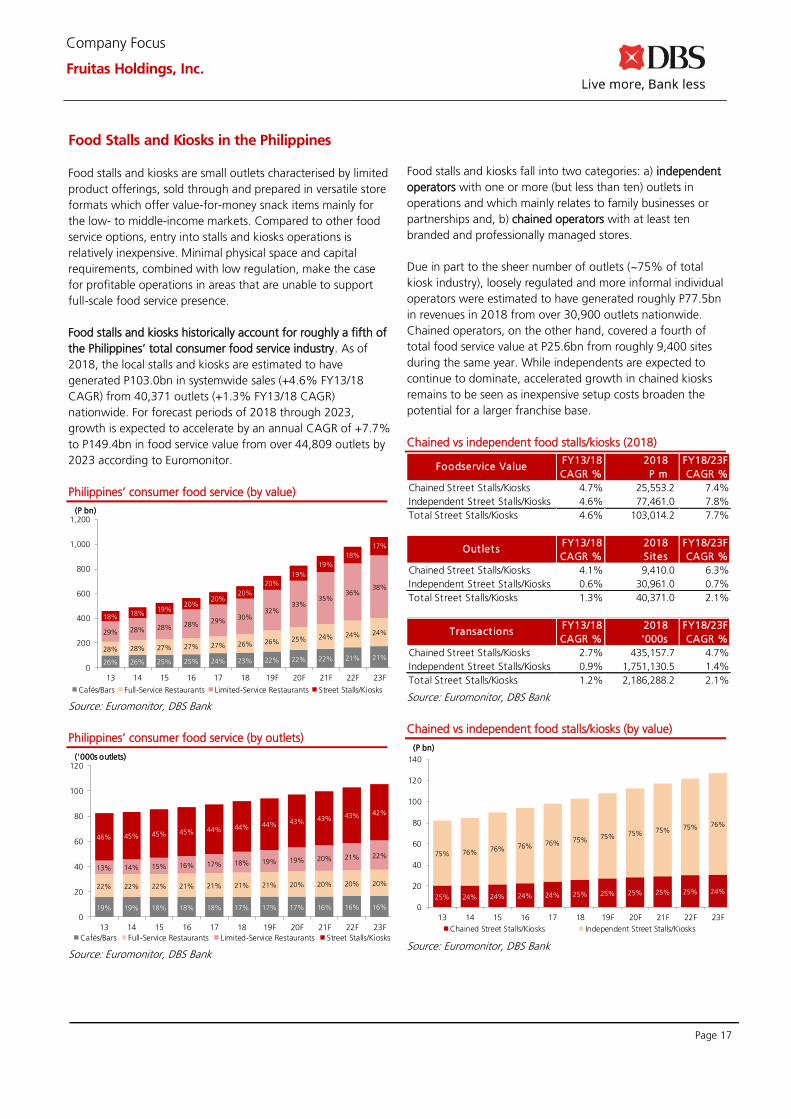

Food Stalls and Kiosks in the Philippines

Food stalls and kiosks are small outlets characterised by limited

product offerings, sold through and prepared in versatile store

formats which offer value-for-money snack items mainly for

the low- to middle-income markets. Compared to other food

service options, entry into stalls and kiosks operations is

relatively inexpensive. Minimal physical space and capital

requirements, combined with low regulation, make the case

for profitable operations in areas that are unable to support

full-scale food service presence.

Food stalls and kiosks historically account for roughly a fifth of

the Philippines’ total consumer food service industry. As of

2018, the local stalls and kiosks are estimated to have

generated P103.0bn in systemwide sales (+4.6% FY13/18

CAGR) from 40,371 outlets (+1.3% FY13/18 CAGR)

nationwide. For forecast periods of 2018 through 2023,

growth is expected to accelerate by an annual CAGR of +7.7%

to P149.4bn in food service value from over 44,809 outlets by

2023 according to Euromonitor.

Philippines’ consumer food service (by value)

Source: Euromonitor, DBS Bank

Philippines’ consumer food service (by outlets)

Source: Euromonitor, DBS Bank

Food stalls and kiosks fall into two categories: a) independent

operators with one or more (but less than ten) outlets in

operations and which mainly relates to family businesses or

partnerships and, b) chained operators with at least ten

branded and professionally managed stores.

Due in part to the sheer number of outlets (~75% of total

kiosk industry), loosely regulated and more informal individual

operators were estimated to have generated roughly P77.5bn

in revenues in 2018 from over 30,900 outlets nationwide.

Chained operators, on the other hand, covered a fourth of

total food service value at P25.6bn from roughly 9,400 sites

during the same year. While independents are expected to

continue to dominate, accelerated growth in chained kiosks

remains to be seen as inexpensive setup costs broaden the

potential for a larger franchise base.

Chained vs independent food stalls/kiosks (2018)

Source: Euromonitor, DBS Bank

Chained vs independent food stalls/kiosks (by value)

Source: Euromonitor, DBS Bank

26% 26% 25% 25% 24% 23% 22% 22% 22% 21% 21%28% 28% 27% 27% 27% 26% 26% 25% 24% 24% 24%29% 28% 28% 28%

29%30%

32%33%

35%36%

38%

18%18%

19%20%

20%20%

20%

19%

19%

18%

17%

0

200

400

600

800

1,000

1,200

13 14 15 16 17 18 19F 20F 21F 22F 23F

Cafés/Bars Full-Service Restaurants Limited-Service Restaurants Street Stalls/Kiosks

(P bn)

19% 19% 18% 18% 18% 17% 17% 17% 16% 16% 16%

22% 22% 22% 21% 21% 21% 21% 20% 20% 20% 20%

13% 14% 15% 16% 17% 18% 19% 19% 20% 21% 22%

46% 45% 45% 45% 44% 44% 44% 43% 43% 43% 42%

0

20

40

60

80

100

120

13 14 15 16 17 18 19F 20F 21F 22F 23F

Cafés/Bars Full-Service Restaurants Limited-Service Restaurants Street Stalls/Kiosks

('000s outlets)

FY13/18 2018 FY18/23F

CAGR % P m CAGR %

Chained Street Stalls/Kiosks 4.7% 25,553.2 7.4%

Independent Street Stalls/Kiosks 4.6% 77,461.0 7.8%

Total Street Stalls/Kiosks 4.6% 103,014.2 7.7%

FY13/18 2018 FY18/23F

CAGR % Sites CAGR %

Chained Street Stalls/Kiosks 4.1% 9,410.0 6.3%

Independent Street Stalls/Kiosks 0.6% 30,961.0 0.7%

Total Street Stalls/Kiosks 1.3% 40,371.0 2.1%

FY13/18 2018 FY18/23F

CAGR % '000s CAGR %

Chained Street Stalls/Kiosks 2.7% 435,157.7 4.7%

Independent Street Stalls/Kiosks 0.9% 1,751,130.5 1.4%

Total Street Stalls/Kiosks 1.2% 2,186,288.2 2.1%

Foodservice Value

Out let s

Transact ions

25% 24% 24% 24% 24% 25% 25% 25% 25% 25% 24%

75% 76% 76% 76% 76% 75% 75% 75% 75% 75% 76%

0

20

40

60

80

100

120

140

13 14 15 16 17 18 19F 20F 21F 22F 23F

Chained Street Stalls/Kiosks Independent Street Stalls/Kiosks

(P bn)

Page 18

Company Focus

Fruitas Holdings, Inc.

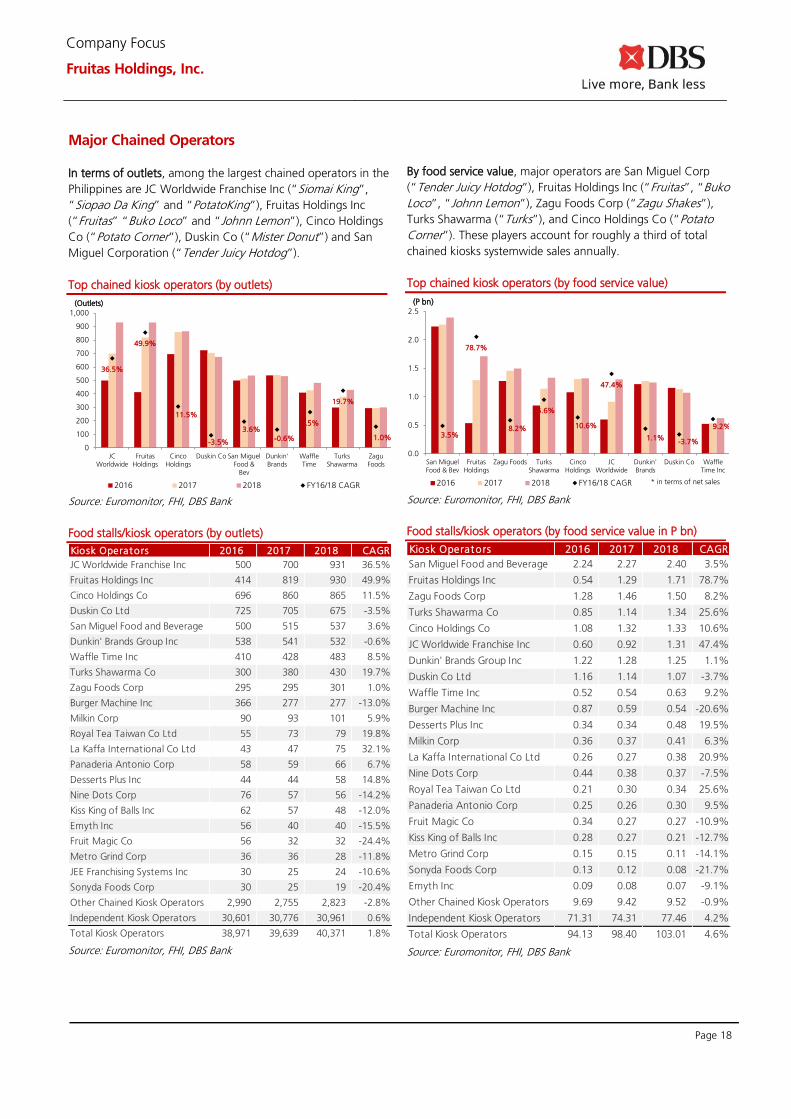

Major Chained Operators

In terms of outlets, among the largest chained operators in the

Philippines are JC Worldwide Franchise Inc (“Siomai King”,

“Siopao Da King” and “PotatoKing”), Fruitas Holdings Inc

(“Fruitas” “Buko Loco” and “Johnn Lemon”), Cinco Holdings

Co (“Potato Corner”), Duskin Co (“Mister Donut”) and San

Miguel Corporation (“Tender Juicy Hotdog”).

Top chained kiosk operators (by outlets)

Source: Euromonitor, FHI, DBS Bank

Food stalls/kiosk operators (by outlets)

Source: Euromonitor, FHI, DBS Bank

By food service value, major operators are San Miguel Corp

(“Tender Juicy Hotdog”), Fruitas Holdings Inc (“Fruitas”, “Buko

Loco”, “Johnn Lemon”), Zagu Foods Corp (“Zagu Shakes”),

Turks Shawarma (“Turks”), and Cinco Holdings Co (“Potato

Corner”). These players account for roughly a third of total

chained kiosks systemwide sales annually.

Top chained kiosk operators (by food service value)

Source: Euromonitor, FHI, DBS Bank

Food stalls/kiosk operators (by food service value in P bn)

Source: Euromonitor, FHI, DBS Bank

36.5%

49.9%

11.5%

-3.5%

3.6%

-0.6%

8.5%

19.7%

1.0%-10%

0%

10%

20%

30%

40%

50%

60%

0

100

200

300

400

500

600

700

800

900

1,000

JCWorldwide

FruitasHoldings

CincoHoldings

Duskin Co San MiguelFood &

Bev

Dunkin'Brands

WaffleTime

TurksShawarma

ZaguFoods

2016 2017 2018 FY16/18 CAGR

(Outlets)

Kiosk Operators 2016 2017 2018 CAGR

JC Worldwide Franchise Inc 500 700 931 36.5%

Fruitas Holdings Inc 414 819 930 49.9%

Cinco Holdings Co 696 860 865 11.5%

Duskin Co Ltd 725 705 675 -3.5%

San Miguel Food and Beverage 500 515 537 3.6%

Dunkin' Brands Group Inc 538 541 532 -0.6%

Waffle Time Inc 410 428 483 8.5%

Turks Shawarma Co 300 380 430 19.7%

Zagu Foods Corp 295 295 301 1.0%

Burger Machine Inc 366 277 277 -13.0%

Milkin Corp 90 93 101 5.9%

Royal Tea Taiwan Co Ltd 55 73 79 19.8%

La Kaffa International Co Ltd 43 47 75 32.1%

Panaderia Antonio Corp 58 59 66 6.7%

Desserts Plus Inc 44 44 58 14.8%

Nine Dots Corp 76 57 56 -14.2%

Kiss King of Balls Inc 62 57 48 -12.0%

Emyth Inc 56 40 40 -15.5%

Fruit Magic Co 56 32 32 -24.4%

Metro Grind Corp 36 36 28 -11.8%

JEE Franchising Systems Inc 30 25 24 -10.6%

Sonyda Foods Corp 30 25 19 -20.4%

Other Chained Kiosk Operators 2,990 2,755 2,823 -2.8%

Independent Kiosk Operators 30,601 30,776 30,961 0.6%

Total Kiosk Operators 38,971 39,639 40,371 1.8%

3.5%

78.7%

8.2%

25.6%

10.6%

47.4%

1.1%-3.7%

9.2%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

0.0

0.5

1.0

1.5

2.0

2.5

San MiguelFood & Bev

FruitasHoldings

Zagu Foods TurksShawarma

CincoHoldings

JCWorldwide

Dunkin'Brands

Duskin Co WaffleTime Inc

2016 2017 2018 FY16/18 CAGR

(P bn)

* in terms of net sales

Kiosk Operators 2016 2017 2018 CAGR

San Miguel Food and Beverage 2.24 2.27 2.40 3.5%

Fruitas Holdings Inc 0.54 1.29 1.71 78.7%

Zagu Foods Corp 1.28 1.46 1.50 8.2%

Turks Shawarma Co 0.85 1.14 1.34 25.6%

Cinco Holdings Co 1.08 1.32 1.33 10.6%

JC Worldwide Franchise Inc 0.60 0.92 1.31 47.4%

Dunkin' Brands Group Inc 1.22 1.28 1.25 1.1%

Duskin Co Ltd 1.16 1.14 1.07 -3.7%

Waffle Time Inc 0.52 0.54 0.63 9.2%

Burger Machine Inc 0.87 0.59 0.54 -20.6%

Desserts Plus Inc 0.34 0.34 0.48 19.5%

Milkin Corp 0.36 0.37 0.41 6.3%

La Kaffa International Co Ltd 0.26 0.27 0.38 20.9%

Nine Dots Corp 0.44 0.38 0.37 -7.5%

Royal Tea Taiwan Co Ltd 0.21 0.30 0.34 25.6%

Panaderia Antonio Corp 0.25 0.26 0.30 9.5%

Fruit Magic Co 0.34 0.27 0.27 -10.9%

Kiss King of Balls Inc 0.28 0.27 0.21 -12.7%

Metro Grind Corp 0.15 0.15 0.11 -14.1%

Sonyda Foods Corp 0.13 0.12 0.08 -21.7%

Emyth Inc 0.09 0.08 0.07 -9.1%

Other Chained Kiosk Operators 9.69 9.42 9.52 -0.9%

Independent Kiosk Operators 71.31 74.31 77.46 4.2%

Total Kiosk Operators 94.13 98.40 103.01 4.6%

Page 19

Company Focus

Fruitas Holdings, Inc.

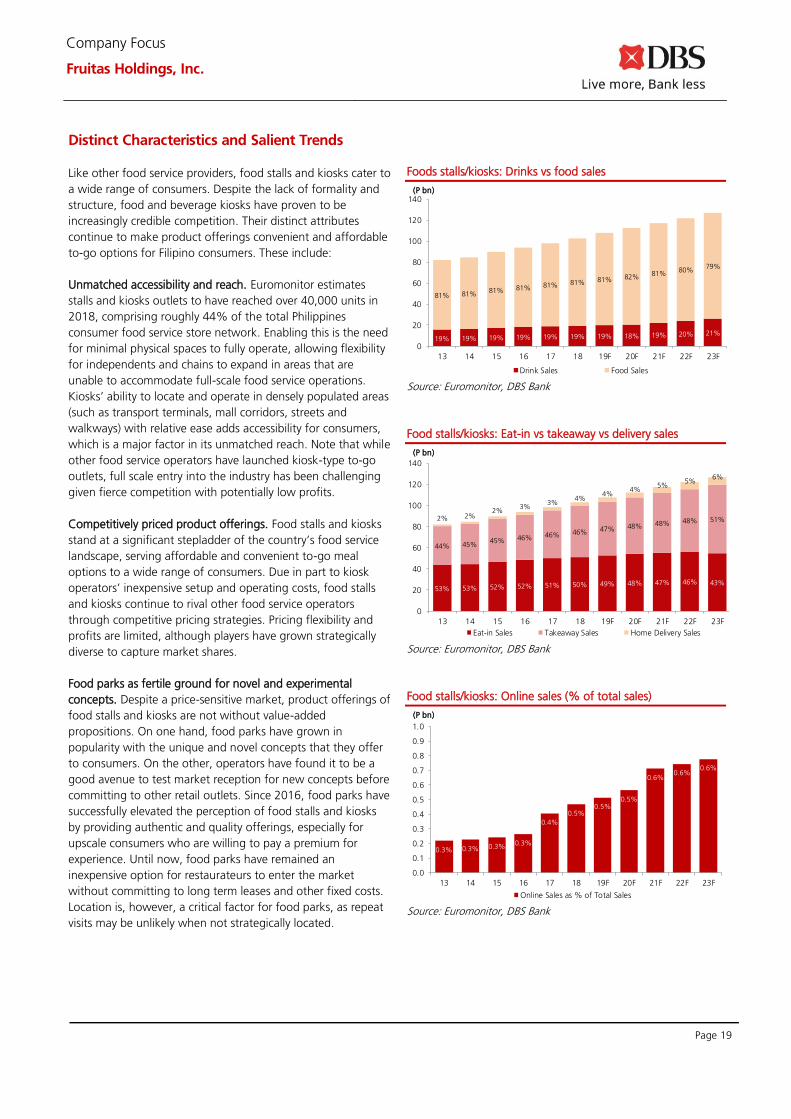

Distinct Characteristics and Salient Trends

Like other food service providers, food stalls and kiosks cater to

a wide range of consumers. Despite the lack of formality and

structure, food and beverage kiosks have proven to be

increasingly credible competition. Their distinct attributes

continue to make product offerings convenient and affordable

to-go options for Filipino consumers. These include:

Unmatched accessibility and reach. Euromonitor estimates

stalls and kiosks outlets to have reached over 40,000 units in

2018, comprising roughly 44% of the total Philippines

consumer food service store network. Enabling this is the need

for minimal physical spaces to fully operate, allowing flexibility

for independents and chains to expand in areas that are

unable to accommodate full-scale food service operations.

Kiosks’ ability to locate and operate in densely populated areas

(such as transport terminals, mall corridors, streets and

walkways) with relative ease adds accessibility for consumers,

which is a major factor in its unmatched reach. Note that while

other food service operators have launched kiosk-type to-go

outlets, full scale entry into the industry has been challenging

given fierce competition with potentially low profits.

Competitively priced product offerings. Food stalls and kiosks

stand at a significant stepladder of the country’s food service

landscape, serving affordable and convenient to-go meal

options to a wide range of consumers. Due in part to kiosk

operators’ inexpensive setup and operating costs, food stalls

and kiosks continue to rival other food service operators

through competitive pricing strategies. Pricing flexibility and

profits are limited, although players have grown strategically

diverse to capture market shares.

Food parks as fertile ground for novel and experimental

concepts. Despite a price-sensitive market, product offerings of

food stalls and kiosks are not without value-added

propositions. On one hand, food parks have grown in

popularity with the unique and novel concepts that they offer

to consumers. On the other, operators have found it to be a

good avenue to test market reception for new concepts before

committing to other retail outlets. Since 2016, food parks have

successfully elevated the perception of food stalls and kiosks

by providing authentic and quality offerings, especially for

upscale consumers who are willing to pay a premium for

experience. Until now, food parks have remained an

inexpensive option for restaurateurs to enter the market

without committing to long term leases and other fixed costs.

Location is, however, a critical factor for food parks, as repeat

visits may be unlikely when not strategically located.

Foods stalls/kiosks: Drinks vs food sales

Source: Euromonitor, DBS Bank

Food stalls/kiosks: Eat-in vs takeaway vs delivery sales

Source: Euromonitor, DBS Bank

Food stalls/kiosks: Online sales (% of total sales)

Source: Euromonitor, DBS Bank

19% 19% 19% 19% 19% 19% 19% 18% 19% 20% 21%

81% 81%81% 81% 81% 81% 81% 82%

81%80%

79%

0

20

40

60

80

100

120

140

13 14 15 16 17 18 19F 20F 21F 22F 23F

Drink Sales Food Sales

(P bn)

53% 53% 52% 52% 51% 50% 49% 48% 47% 46% 43%

44% 45%45% 46% 46% 46% 47% 48% 48% 48% 51%2% 2%2%

3%3%

4%4%

4%5%

5%6%

0

20

40

60

80

100

120

140

13 14 15 16 17 18 19F 20F 21F 22F 23F

Eat-in Sales Takeaway Sales Home Delivery Sales

(P bn)

0.3% 0.3% 0.3%0.3%

0.4%

0.5%0.5%

0.5%

0.6%0.6%

0.6%

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

13 14 15 16 17 18 19F 20F 21F 22F 23F

Online Sales as % of Total Sales

(P bn)

Page 20

Company Focus

Fruitas Holdings, Inc.

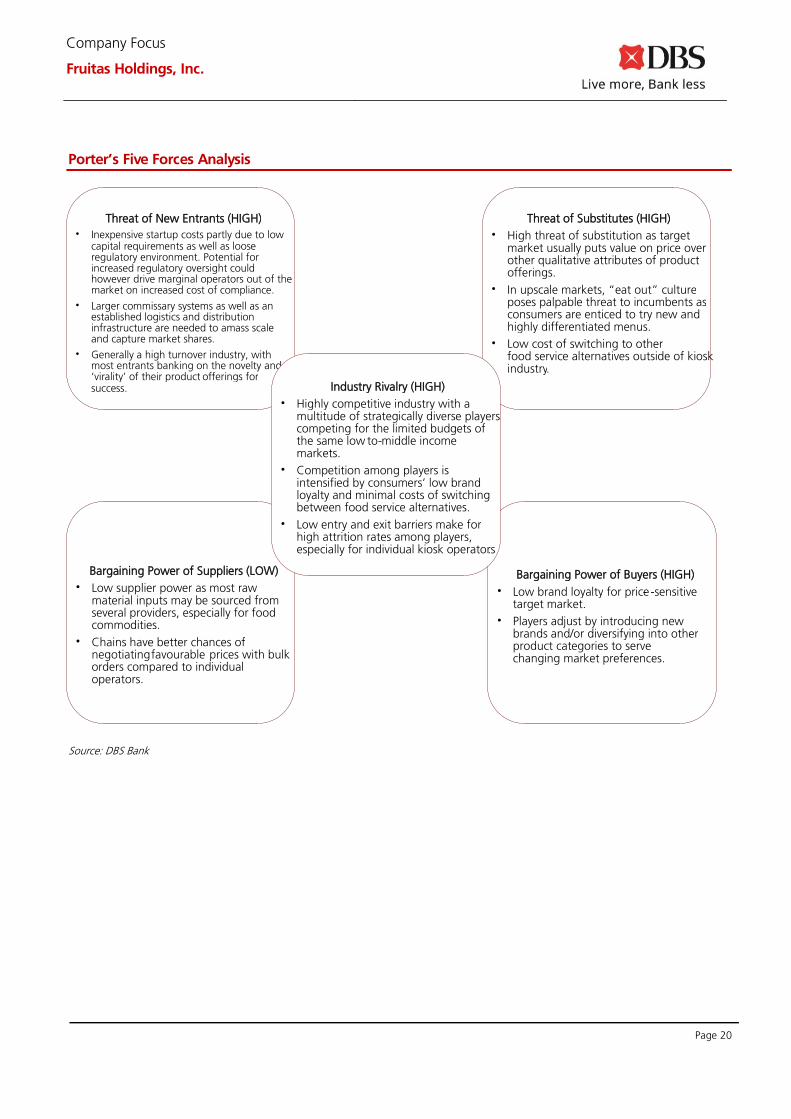

Porter’s Five Forces Analysis

Source: DBS Bank

Bargaining Power of Buyers (HIGH) • Low brand loyalty for price - -sensitive

target market. • Players adjust by introducing new

brands and/or diversifying into other product categories to serve changing market preferences.

Bargaining Power of Suppliers (LOW) • Low supplier power as most raw

material inputs may be sourced from several providers, especially for food commodities.

• Chains have better chances of negotiating favourable prices with bulk orders compared to individual operators.

Threat of New Entrants (HIGH) • Inexpensive startup costs partly due to low

capital requirements as well as loose regulatory environment. Potential for increased regulatory oversight could however drive marginal operators out of the market on increased cost of compliance.

• Larger commissary systems as well as an established logistics and distribution infrastructure are needed to amass scale and capture market shares.

• Generally a high turnover industry, with most entrants banking on the novelty and ‘virality’ of their product offerings for success.

Threat of Substitutes (HIGH) • High threat of substitution as target

market usually puts value on price over other qualitative attributes of product offerings.

• In upscale markets, “eat out” culture poses palpable threat to incumbents as consumers are enticed to try new and highly differentiated menus.

• Low cost of switching to other food service alternatives outside of kiosk industry .

Industry Rivalry (HIGH) • Highly competitive industry with a

multitude of strategically diverse players competing for the limited budgets of the same low to - middle income markets.

• Competition among players is intensified by consumers’ low brand loyalty and minimal costs of switching between food service alternatives.

• Low entry and exit barriers make for high attrition rates among players, especially for individual kiosk operators .

Page 21

Company Focus

Fruitas Holdings, Inc.

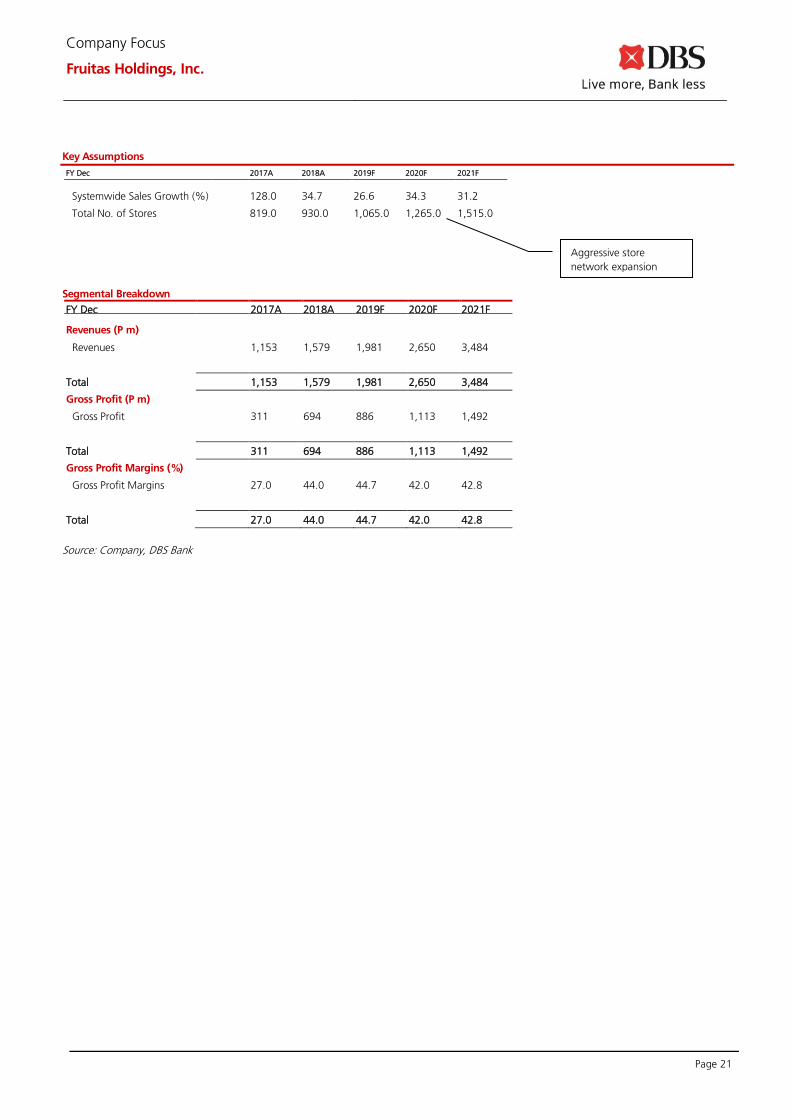

Key Assumptions

FY Dec 2017A 2018A 2019F 2020F 2021F

Systemwide Sales Growth (%) 128.0 34.7 26.6 34.3 31.2

Total No. of Stores 819.0 930.0 1,065.0 1,265.0 1,515.0

Segmental Breakdown

FY Dec 2017A 2018A 2019F 2020F 2021F Revenues (P m)

Revenues 1,153 1,579 1,981 2,650 3,484

Total 1,153 1,579 1,981 2,650 3,484

Gross Profit (P m)

Gross Profit 311 694 886 1,113 1,492

Total 311 694 886 1,113 1,492

Gross Profit Margins (%)

Gross Profit Margins 27.0 44.0 44.7 42.0 42.8

Total 27.0 44.0 44.7 42.0 42.8

Source: Company, DBS Bank

Aggressive store

network expansion

Page 22

Company Focus

Fruitas Holdings, Inc.

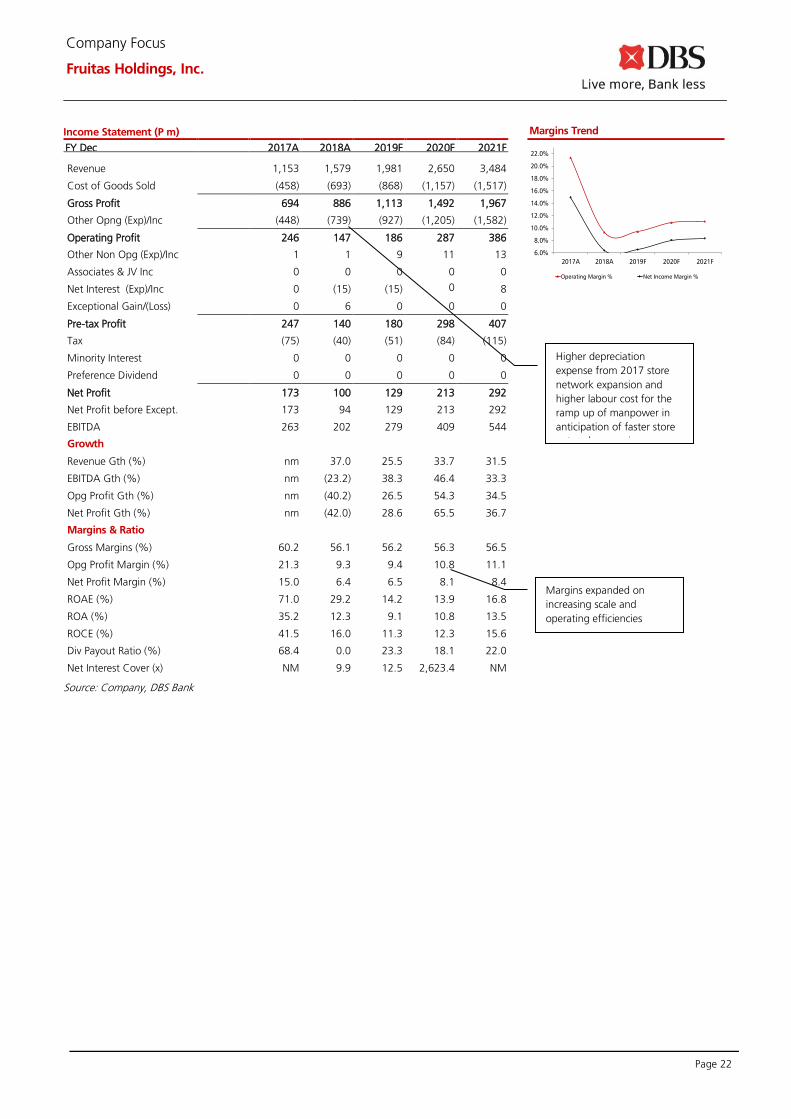

Income Statement (P m)

FY Dec 2017A 2018A 2019F 2020F 2021F Revenue 1,153 1,579 1,981 2,650 3,484

Cost of Goods Sold (458) (693) (868) (1,157) (1,517)

Gross Profit 694 886 1,113 1,492 1,967

Other Opng (Exp)/Inc (448) (739) (927) (1,205) (1,582)

Operating Profit 246 147 186 287 386

Other Non Opg (Exp)/Inc 1 1 9 11 13

Associates & JV Inc 0 0 0 0 0

Net Interest (Exp)/Inc 0 (15) (15) 0 8

Exceptional Gain/(Loss) 0 6 0 0 0

Pre-tax Profit 247 140 180 298 407

Tax (75) (40) (51) (84) (115)

Minority Interest 0 0 0 0 0

Preference Dividend 0 0 0 0 0

Net Profit 173 100 129 213 292

Net Profit before Except. 173 94 129 213 292

EBITDA 263 202 279 409 544

Growth

Revenue Gth (%) nm 37.0 25.5 33.7 31.5

EBITDA Gth (%) nm (23.2) 38.3 46.4 33.3

Opg Profit Gth (%) nm (40.2) 26.5 54.3 34.5

Net Profit Gth (%) nm (42.0) 28.6 65.5 36.7

Margins & Ratio

Gross Margins (%) 60.2 56.1 56.2 56.3 56.5

Opg Profit Margin (%) 21.3 9.3 9.4 10.8 11.1

Net Profit Margin (%) 15.0 6.4 6.5 8.1 8.4

ROAE (%) 71.0 29.2 14.2 13.9 16.8

ROA (%) 35.2 12.3 9.1 10.8 13.5

ROCE (%) 41.5 16.0 11.3 12.3 15.6

Div Payout Ratio (%) 68.4 0.0 23.3 18.1 22.0

Net Interest Cover (x) NM 9.9 12.5 2,623.4 NM

Source: Company, DBS Bank

Margins Trend

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

2017A 2018A 2019F 2020F 2021F

Operating Margin % Net Income Margin %

Margins expanded on

increasing scale and

operating efficiencies

Higher depreciation

expense from 2017 store

network expansion and

higher labour cost for the

ramp up of manpower in

anticipation of faster store

network expansion

Page 23

Company Focus

Fruitas Holdings, Inc.

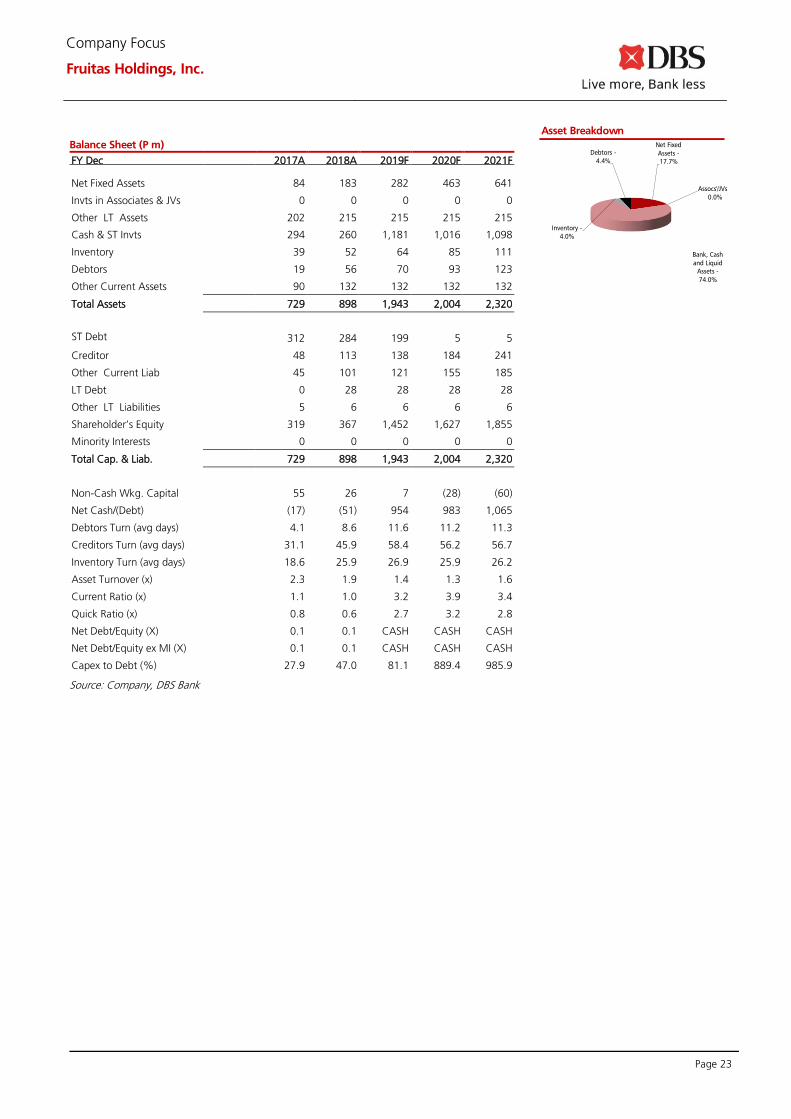

Balance Sheet (P m)

FY Dec 2017A 2018A 2019F 2020F 2021F Net Fixed Assets 84 183 282 463 641

Invts in Associates & JVs 0 0 0 0 0

Other LT Assets 202 215 215 215 215

Cash & ST Invts 294 260 1,181 1,016 1,098

Inventory 39 52 64 85 111

Debtors 19 56 70 93 123

Other Current Assets 90 132 132 132 132

Total Assets 729 898 1,943 2,004 2,320

ST Debt

312 284 199 5 5

Creditor 48 113 138 184 241

Other Current Liab 45 101 121 155 185

LT Debt 0 28 28 28 28

Other LT Liabilities 5 6 6 6 6

Shareholder’s Equity 319 367 1,452 1,627 1,855

Minority Interests 0 0 0 0 0

Total Cap. & Liab. 729 898 1,943 2,004 2,320

Non-Cash Wkg. Capital 55 26 7 (28) (60)

Net Cash/(Debt) (17) (51) 954 983 1,065

Debtors Turn (avg days) 4.1 8.6 11.6 11.2 11.3

Creditors Turn (avg days) 31.1 45.9 58.4 56.2 56.7

Inventory Turn (avg days) 18.6 25.9 26.9 25.9 26.2

Asset Turnover (x) 2.3 1.9 1.4 1.3 1.6

Current Ratio (x) 1.1 1.0 3.2 3.9 3.4

Quick Ratio (x) 0.8 0.6 2.7 3.2 2.8

Net Debt/Equity (X) 0.1 0.1 CASH CASH CASH

Net Debt/Equity ex MI (X) 0.1 0.1 CASH CASH CASH

Capex to Debt (%) 27.9 47.0 81.1 889.4 985.9

Source: Company, DBS Bank

Asset Breakdown

Net Fixed

Assets -17.7%

Assocs'/JVs -

0.0%

Bank, Cash

and Liquid Assets -

74.0%

Inventory -

4.0%

Debtors -

4.4%

Page 24

Company Focus

Fruitas Holdings, Inc.

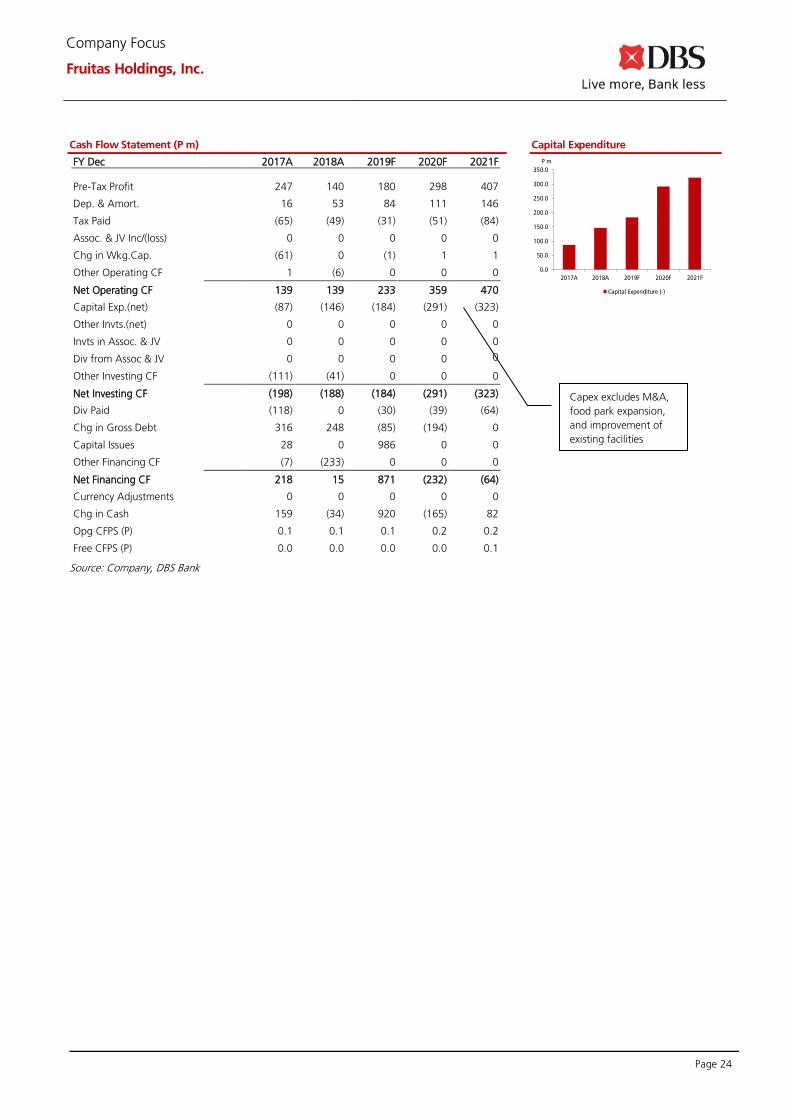

Cash Flow Statement (P m)

FY Dec 2017A 2018A 2019F 2020F 2021F

Pre-Tax Profit 247 140 180 298 407

Dep. & Amort. 16 53 84 111 146

Tax Paid (65) (49) (31) (51) (84)

Assoc. & JV Inc/(loss) 0 0 0 0 0

Chg in Wkg.Cap. (61) 0 (1) 1 1

Other Operating CF 1 (6) 0 0 0

Net Operating CF 139 139 233 359 470

Capital Exp.(net) (87) (146) (184) (291) (323)

Other Invts.(net) 0 0 0 0 0

Invts in Assoc. & JV 0 0 0 0 0

Div from Assoc & JV 0 0 0 0 0

Other Investing CF (111) (41) 0 0 0

Net Investing CF (198) (188) (184) (291) (323)

Div Paid (118) 0 (30) (39) (64)

Chg in Gross Debt 316 248 (85) (194) 0

Capital Issues 28 0 986 0 0

Other Financing CF (7) (233) 0 0 0

Net Financing CF 218 15 871 (232) (64)

Currency Adjustments 0 0 0 0 0

Chg in Cash 159 (34) 920 (165) 82

Opg CFPS (P) 0.1 0.1 0.1 0.2 0.2

Free CFPS (P) 0.0 0.0 0.0 0.0 0.1

Source: Company, DBS Bank

Capital Expenditure

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

2017A 2018A 2019F 2020F 2021F

Capital Expenditure (-)

P m

Capex excludes M&A,

food park expansion,

and improvement of

existing facilities

Page 25

Company Focus

Fruitas Holdings, Inc.

DBS Bank Ltd recommendations are based on an Absolute Total Return* Rating system, defined as follows:

STRONG BUY (>20% total return over the next 3 months, with identifiable share price catalysts within this time frame)

BUY (>15% total return over the next 12 months for small caps, >10% for large caps)

HOLD (-10% to +15% total return over the next 12 months for small caps, -10% to +10% for large caps)

FULLY VALUED (negative total return, i.e., > -10% over the next 12 months)

SELL (negative total return of > -20% over the next 3 months, with identifiable share price catalysts within this time frame)

*Share price appreciation + dividends Completed Date: 16 Jan 2020 10:46:09 (HKT)

Dissemination Date: 16 Jan 2020 14:41:43 (HKT)

Sources for all charts and tables are DBS Bank unless otherwise specified GENERAL DISCLOSURE/DISCLAIMER

This report is prepared by DBS Bank. This report is solely intended for the clients of DBS Bank Ltd, its respective connected and associated

corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii)

redistributed without the prior written consent of DBS Bank. The research set out in this report is based on information obtained from sources believed to be reliable, but we (which collectively refers to DBS

Bank Ltd, its respective connected and associated corporations, affiliates and their respective directors, officers, employees and agents

(collectively, the “DBS Group”) have not conducted due diligence on any of the companies, verified any information or sources or taken into

account any other factors which we may consider to be relevant or appropriate in preparing the research. Accordingly, we do not make any

representation or warranty as to the accuracy, completeness or correctness of the research set out in this report. Opinions expressed are subject

to change without notice. This research is prepared for general circulation. Any recommendation contained in this document does not have

regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This document is for the

information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate