Latin American Pay TV Services Market: Key Trends and Forecasts until 2017 Guilherme Faggion, Research Associate Telecom Services August 30, 2012 © 2012 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

Frost & Sullivan: Latin American Pay TV Services Market - Key Trends and Forecasts until 2017

Aug 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Latin American Pay TV Services Market: Key Trends and Forecasts until 2017

Guilherme Faggion, Research Associate

Telecom Services

August 30, 2012

© 2012 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

2

Today’s Presenter

Guilherme Faggion

Research Associate

Frost & Sullivan

São Paulo, Brazil

Specialties:

� Pay TV

� Broadband

� Fixed VoIP

� Multiple play

� Over-the-top

3

Focus Points

2

3

Forecasts

1 Market Overview

The Last Word

Market Overview

5

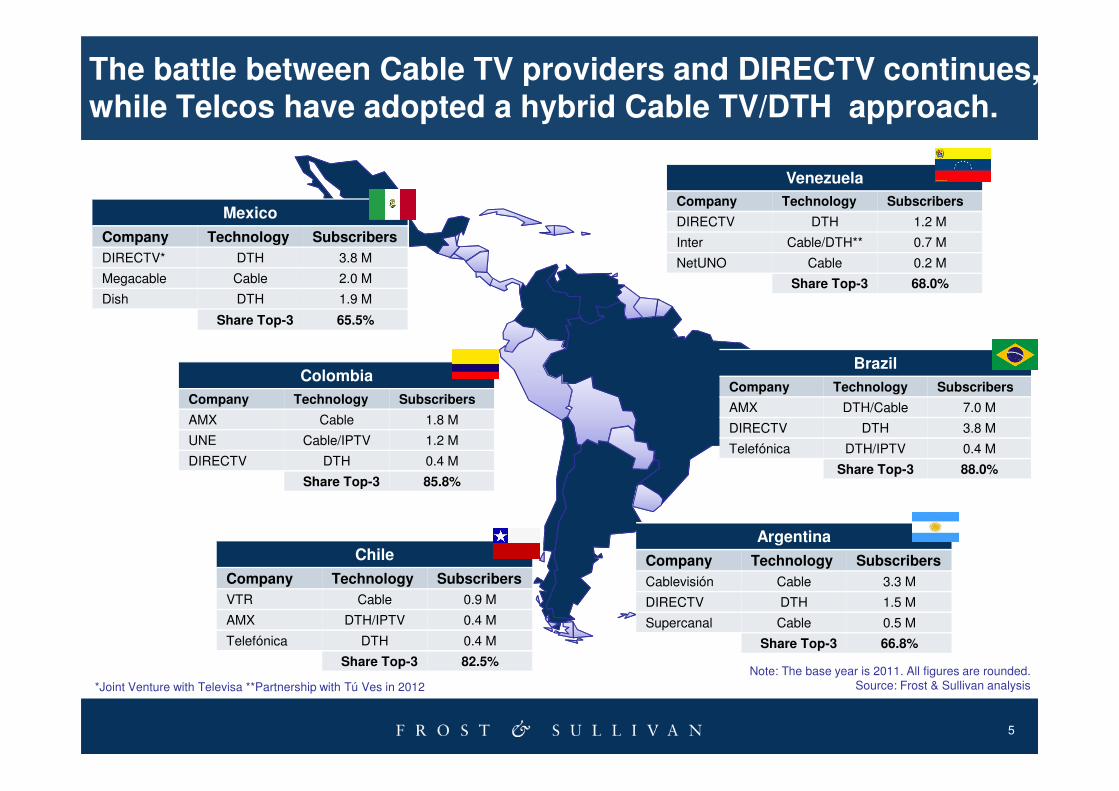

The battle between Cable TV providers and DIRECTV continues, while Telcos have adopted a hybrid Cable TV/DTH approach.

Venezuela

Company Technology Subscribers

DIRECTV DTH 1.2 M

Inter Cable/DTH** 0.7 M

NetUNO Cable 0.2 M

Share Top-3 68.0%

Brazil

Company Technology Subscribers

AMX DTH/Cable 7.0 M

DIRECTV DTH 3.8 M

Telefónica DTH/IPTV 0.4 M

Share Top-3 88.0%

Note: The base year is 2011. All figures are rounded.Source: Frost & Sullivan analysis

Mexico

Company Technology Subscribers

DIRECTV* DTH 3.8 M

Megacable Cable 2.0 M

Dish DTH 1.9 M

Share Top-3 65.5%

Colombia

Company Technology Subscribers

AMX Cable 1.8 M

UNE Cable/IPTV 1.2 M

DIRECTV DTH 0.4 M

Share Top-3 85.8%

Chile

Company Technology Subscribers

VTR Cable 0.9 M

AMX DTH/IPTV 0.4 M

Telefónica DTH 0.4 M

Share Top-3 82.5%

Argentina

Company Technology Subscribers

Cablevisión Cable 3.3 M

DIRECTV DTH 1.5 M

Supercanal Cable 0.5 M

Share Top-3 66.8%

*Joint Venture with Televisa **Partnership with Tú Ves in 2012

6

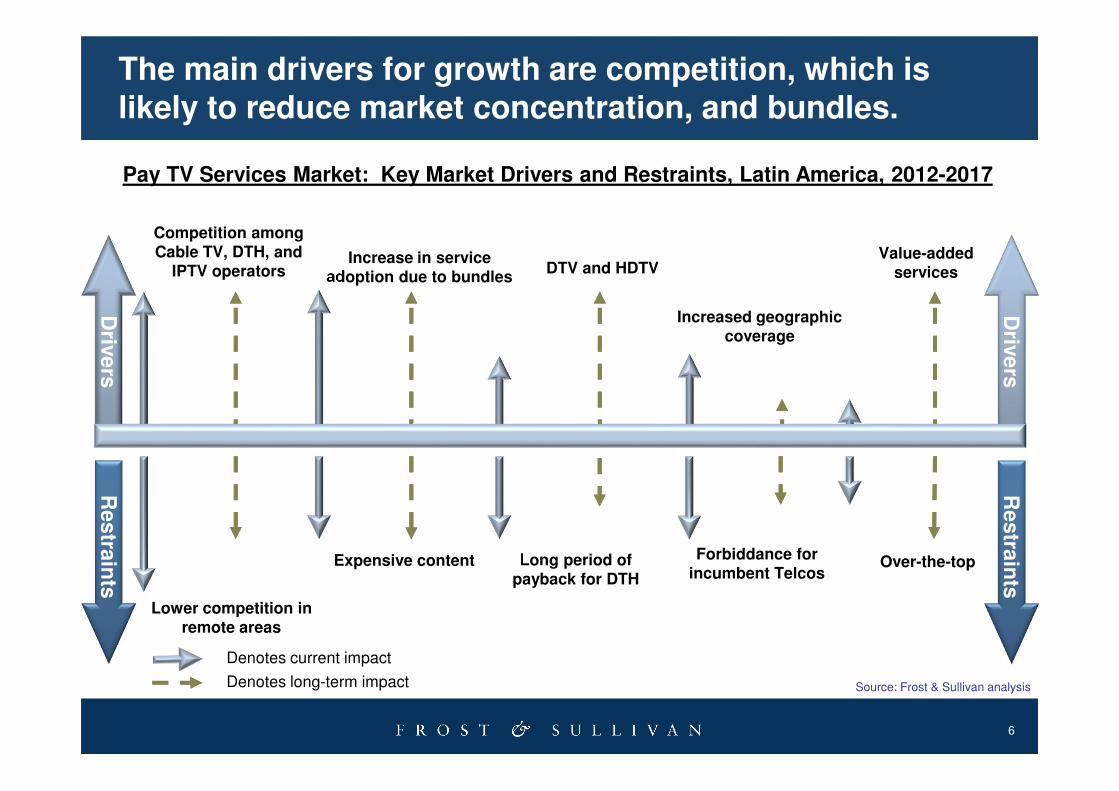

The main drivers for growth are competition, which is likely to reduce market concentration, and bundles.

Source: Frost & Sullivan analysisDenotes long-term impact

Denotes current impact

Driv

ers

Re

stra

ints

Driv

ers

Re

stra

ints

Competition among Cable TV, DTH, and

IPTV operatorsIncrease in service

adoption due to bundlesDTV and HDTV

Increased geographic coverage

Value-added services

Lower competition in remote areas

Long period of payback for DTH

Expensive content Forbiddance for incumbent Telcos

Over-the-top

Pay TV Services Market: Key Market Drivers and Restraints, Latin America, 2012-2017

7

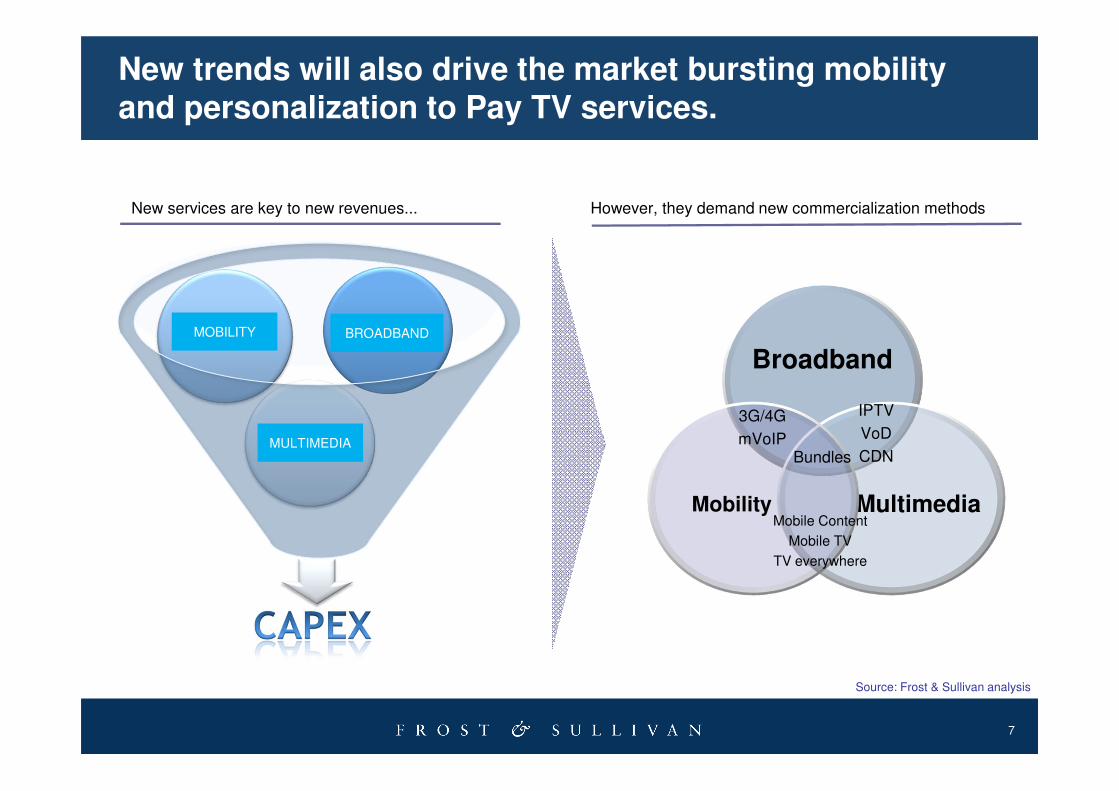

New trends will also drive the market bursting mobility and personalization to Pay TV services.

New services are key to new revenues... However, they demand new commercialization methods

Broadband

MultimediaMobility

3G/4G

mVoIP

Mobile Content

Mobile TV

TV everywhere

IPTV

VoD

CDNBundles

MOBILITY BROADBAND

MULTIMEDIA

Source: Frost & Sullivan analysis

8

Video-on-Demand and TV Everywhere are examples of mobility being used by Programmers and Pay TV providers.

• Muu is an online platform where the subscribers canenjoy video content from Globosat at any moment andplace using a VoD platform.

• Launched by Globosat, Muu service is available just forpay TV subscribers from NET and CTBC (Brazilianservice providers).

• In Argentina, Red Intercable offers it service Diboxthrough a partnership with Moviecity Play.

• This offering has the purpose of decreasing churn ratesand can be a competitive service against other largercable TV operator.

• ESPN Play, Turner and HBO are expected to join theplatform in the short-term.

Source: Frost & Sullivan analysis

9

Over-the-top offerings are being launched by Telcos when unable to offer pay TV or as an add-on by service providers.

Competitor

CountriesArgentina Argentina Argentina Brazil Brazil Mexico

Brand

Launch date Oct/2011 Apr/2011 Nov/2011 Feb/2012 Aug/2011 Sep/2011

Subscribers in Dec/2011

11,000* 30,000 n/a n/a n/a n/a

Content> 2,500

titles> 3,000

titles530 to

1,000 titlesn/a

> 2,000 hours

>3,000 titles

Cost per month

$9.30 $9.30$4.60 to $8.40

$8.00 Freemium$10.70

Restrictions

• Only clients

• Speed > 3Mbps

• Only clients

• Speed > 1Mbps

• Only clients

• Speed > 1Mbps

• Only clients

• Speed > 2Mbps

• Only NET’s Cable TV clients

• Only clients

• Speed > 500Kbps

ScreensPCs and TV sets

PCs and TV sets

Multiscreen PCs Multiscreen Multiscreen

Over-the-top offerings by Telcos and Pay TV stakeholders, Latin America, June 2012

Source: Frost & Sullivan analysis

Forecasts

11

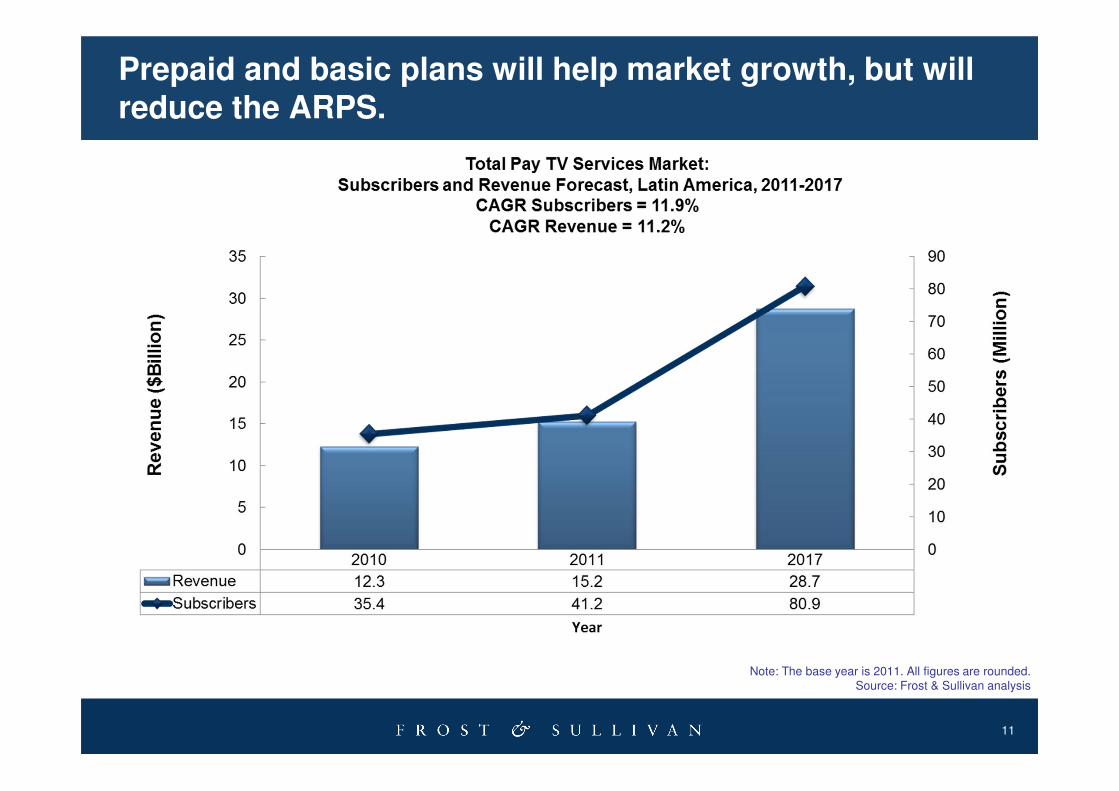

Prepaid and basic plans will help market growth, but will reduce the ARPS.

Note: The base year is 2011. All figures are rounded.Source: Frost & Sullivan analysis

12

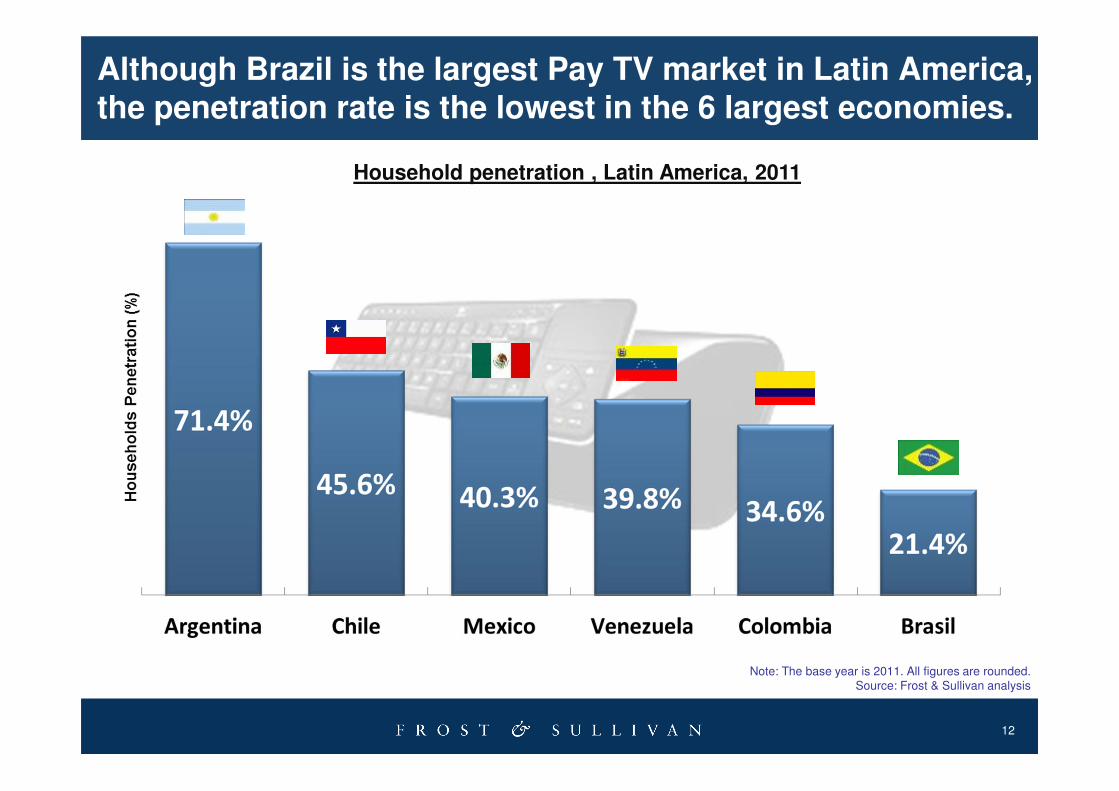

Although Brazil is the largest Pay TV market in Latin America, the penetration rate is the lowest in the 6 largest economies.

Note: The base year is 2011. All figures are rounded.Source: Frost & Sullivan analysis

Household penetration , Latin America, 2011

13

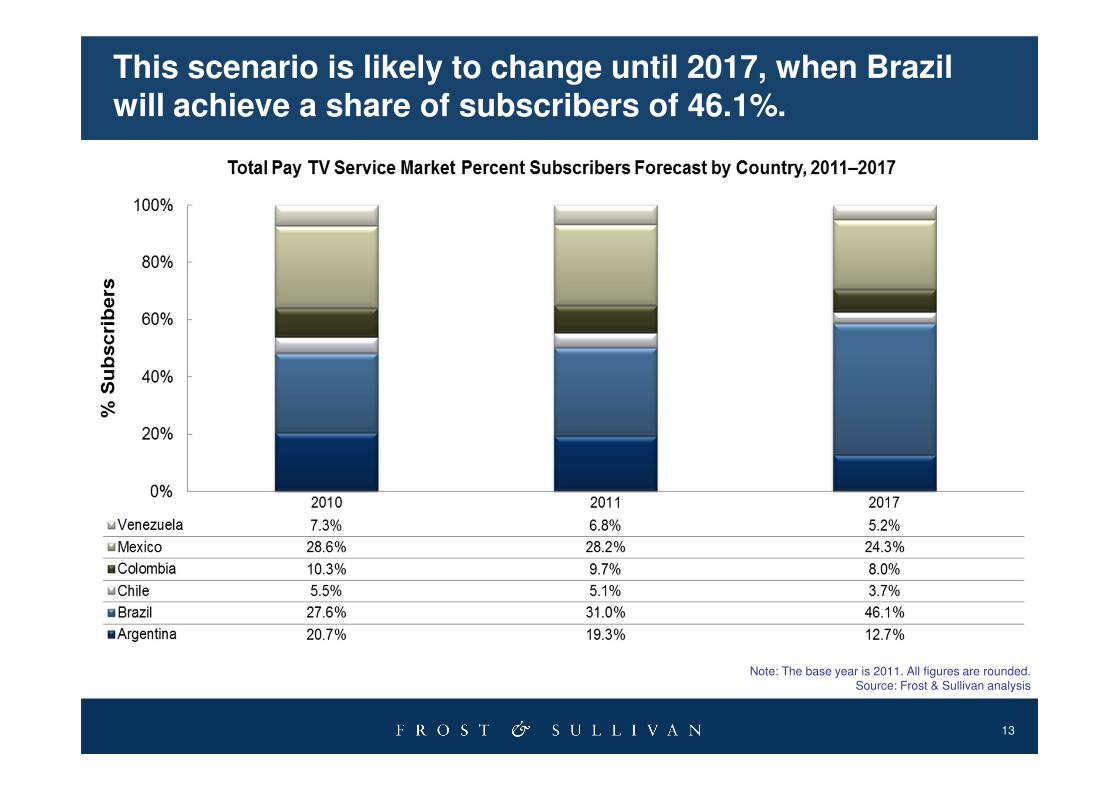

This scenario is likely to change until 2017, when Brazil will achieve a share of subscribers of 46.1%.

Note: The base year is 2011. All figures are rounded.Source: Frost & Sullivan analysis

14

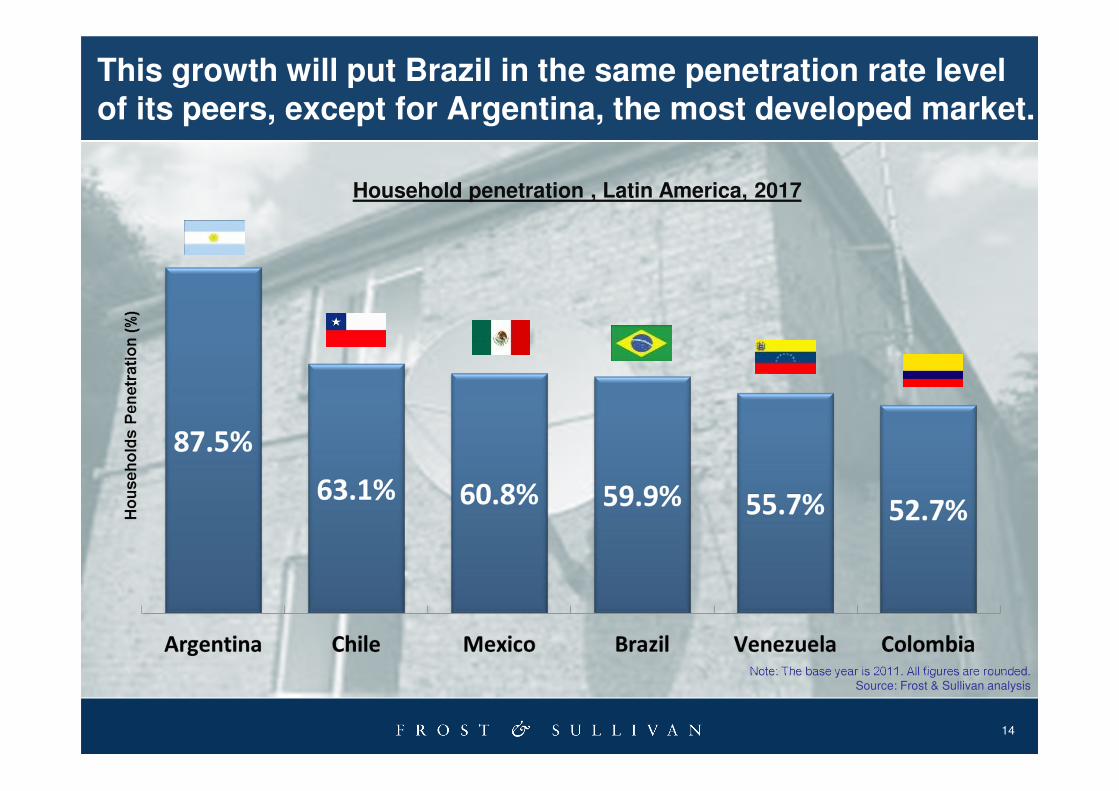

This growth will put Brazil in the same penetration rate level of its peers, except for Argentina, the most developed market.

Note: The base year is 2011. All figures are rounded.Source: Frost & Sullivan analysis

Household penetration , Latin America, 2017

15

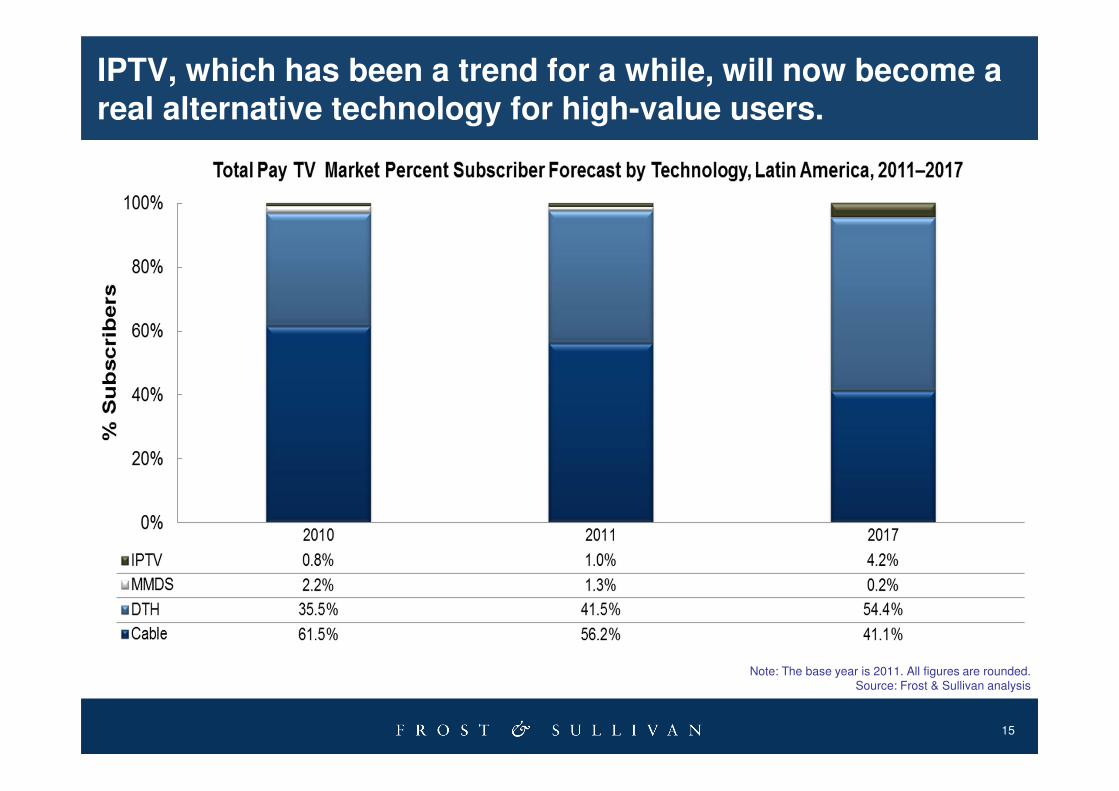

IPTV, which has been a trend for a while, will now become a real alternative technology for high-value users.

Note: The base year is 2011. All figures are rounded.Source: Frost & Sullivan analysis

16

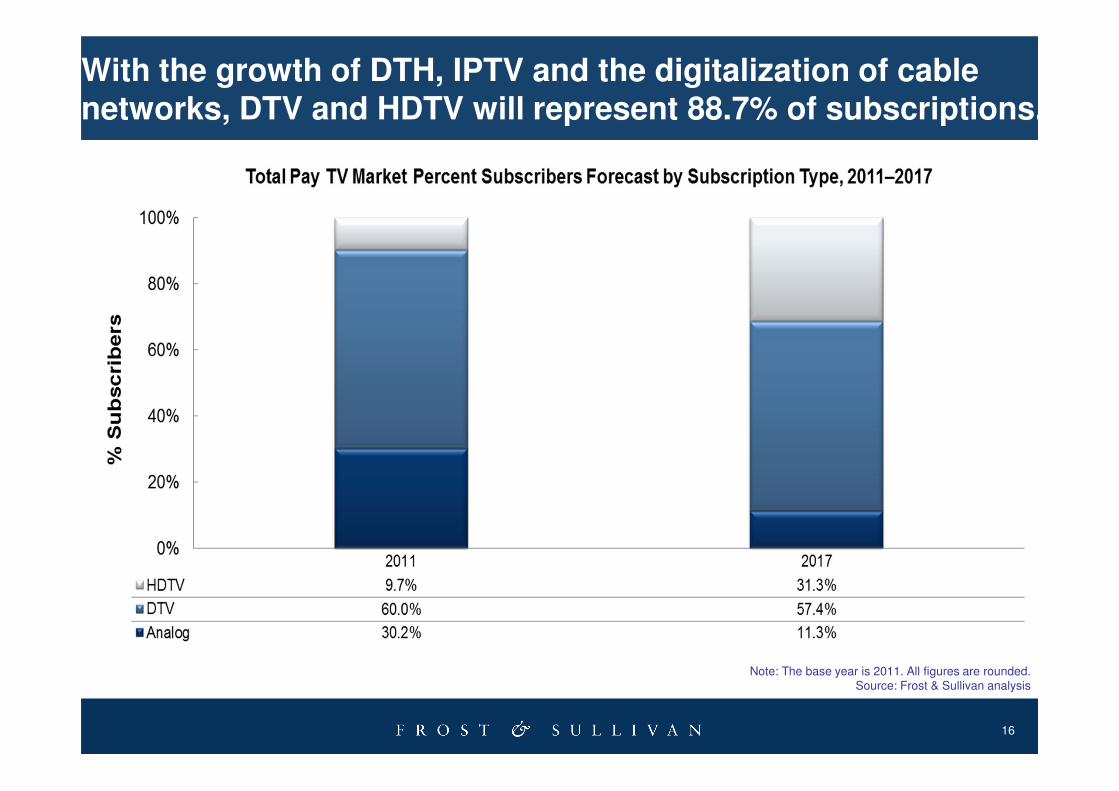

With the growth of DTH, IPTV and the digitalization of cable networks, DTV and HDTV will represent 88.7% of subscriptions.

Note: The base year is 2011. All figures are rounded.Source: Frost & Sullivan analysis

The Last Word

18

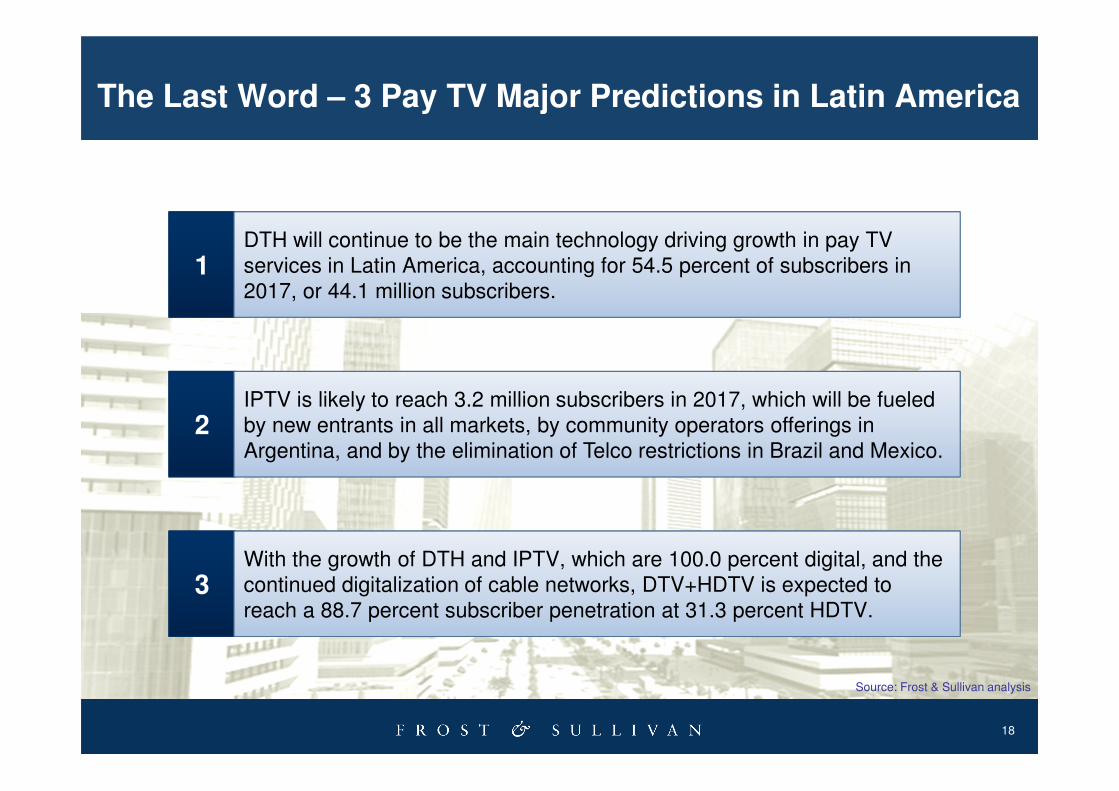

The Last Word – 3 Pay TV Major Predictions in Latin America

Source: Frost & Sullivan analysis

2IPTV is likely to reach 3.2 million subscribers in 2017, which will be fueled by new entrants in all markets, by community operators offerings in Argentina, and by the elimination of Telco restrictions in Brazil and Mexico.

3With the growth of DTH and IPTV, which are 100.0 percent digital, and the continued digitalization of cable networks, DTV+HDTV is expected to reach a 88.7 percent subscriber penetration at 31.3 percent HDTV.

1DTH will continue to be the main technology driving growth in pay TV services in Latin America, accounting for 54.5 percent of subscribers in 2017, or 44.1 million subscribers.

19

Next Steps

Develop Your Visionary and Innovative SkillsGrowth Partnership Service Share your growth thought leadership and ideas or

join our GIL Global Community

Join our GIL Community NewsletterKeep abreast of innovative growth opportunities

20

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

What would you like to see from Frost & Sullivan?

21

http://twitter.com/frost_sullivan

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

22

For Additional Information

Francesca Valente

Corporate Communications

Latin America

Related Documents