Lessons Learned from the Financial Crisis the Financial Crisis What happened and where are we What happened and where are we now? Julie L. Stackhouse Senior Vice President The views expressed in this presentation are the views of Julie Stackhouse and not necessarily the views of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Lessons Learned from the Financial Crisisthe Financial Crisis

What happened and where are weWhat happened and where are we now?

Julie L. StackhouseSenior Vice President

The views expressed in this presentation are the views of Julie Stackhouse and not necessarily the views of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

Pre‐poll question:The financial crisis led to the passage of sweeping legislation in June 2010 that

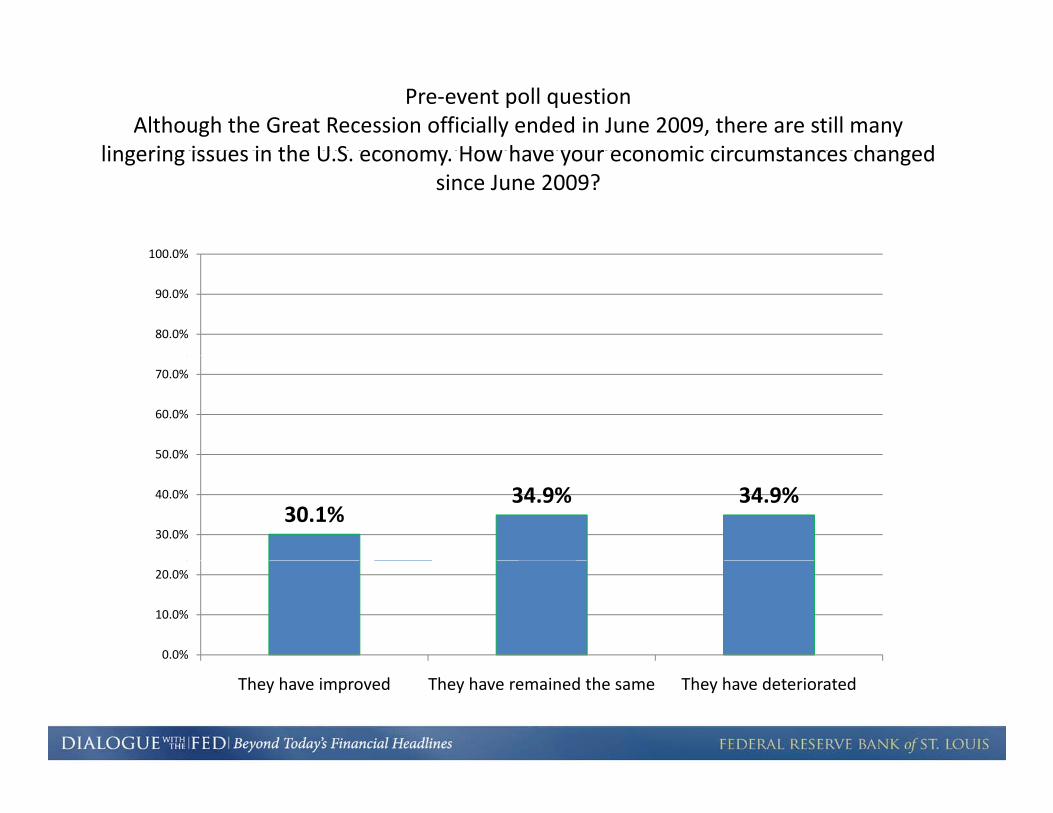

Pre‐event poll questionAlthough the Great Recession officially ended in June 2009, there are still many

lingering issues in the U S economy How have your economic circumstances changedThe financial crisis led to the passage of sweeping legislation in June 2010 that overhauled many aspects of our financial regulatory system. As a result of the changes, how confident are you that the U.S. can avoid or at least lessen the impact of future

shocks to our financial system?

lingering issues in the U.S. economy. How have your economic circumstances changed since June 2009?

100 0%

80.0%

90.0%

100.0%

80.0%

90.0%

100.0%

50 0%

60.0%

70.0%

50.0%

60.0%

70.0%

31.3% 33.7%

22.9%30.0%

40.0%

50.0%

30.1%34.9% 34.9%

30.0%

40.0%

50.0%

1.2%

12.0%

0.0%

10.0%

20.0%

0.0%

10.0%

20.0%

2

Very confident Slightly more confident

Neither more nor less confident

Slightly less confident

Not confident at all

They have improved They have remained the same They have deteriorated

Pre‐event poll question:The financial crisis led to the passage of sweeping legislation in June 2010 that overhauled many aspects of our financial regulatory system As a result of the changes how confidentmany aspects of our financial regulatory system. As a result of the changes, how confident

are you that the U.S. can avoid or at least lessen the impact of future shocks to our financial system?

80.0%

90.0%

100.0%

50 0%

60.0%

70.0%

31.3% 33.7%

22.9%30.0%

40.0%

50.0%

1.2%

12.0%

0.0%

10.0%

20.0%

3

Very confident Slightly more confident

Neither more nor less confident

Slightly less confident

Not confident at all

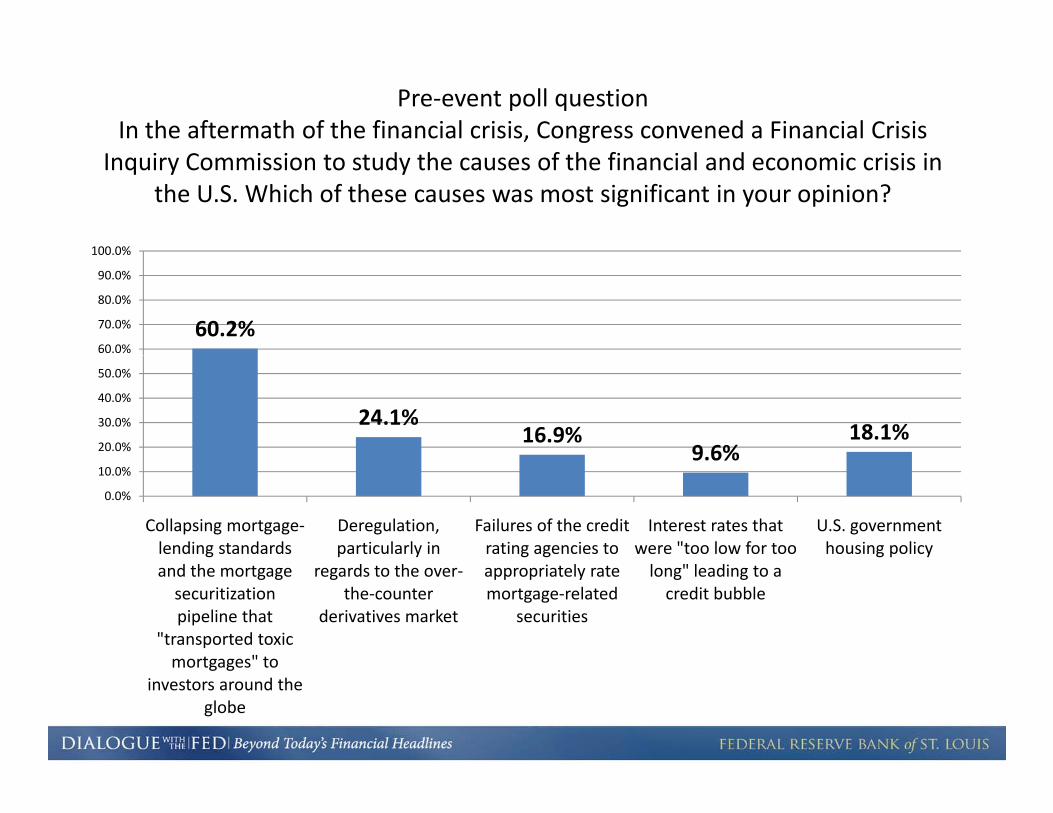

Pre‐event poll questionIn the aftermath of the financial crisis, Congress convened a Financial Crisis

Inquiry Commission to study the causes of the financial and economic crisis in the U.S. Which of these causes was most significant in your opinion?

100 0%

60.2%60.0%

70.0%

80.0%

90.0%

100.0%

24.1%16.9%

9.6%18.1%

20.0%

30.0%

40.0%

50.0%

9.6%

0.0%

10.0%

Collapsing mortgage‐lending standards

Deregulation, particularly in

Failures of the credit rating agencies to

Interest rates that were "too low for too

U.S. government housing policy

and the mortgage securitization pipeline that

"transported toxic mortgages" to

regards to the over‐the‐counter

derivatives market

appropriately rate mortgage‐related

securities

long" leading to a credit bubble

4

mortgages to investors around the

globe

We’ve learned a little about you. Now let’s talk about the Federal Reserve!Federal Reserve!

The Fed is the Central Bank of the United States. It was founded by Congress in 1913 to provide the nation with a safer, more flexible, and more stable monetary and financial system Over the years its role in banking and the economy hasand financial system. Over the years, its role in banking and the economy has expanded. Today, the Federal Reserve's duties fall into four general areas:

Conducting the nation’s monetary policy by influencing the monetary and credit conditions in the economy in pursuit of maximum employment stable prices andconditions in the economy in pursuit of maximum employment, stable prices and moderate long‐term interest rates

Supervising and regulating banking institutions to ensure the safety and soundness of p g g g g ythe nation’s banking system and to protect the rights of consumers

Maintaining the stability of the financial system and containing systemic risk that may g y y g y yarise in financial markets

Providing financial services to depository institutions, the U.S. government, and foreign official institutions including playing a major role in operating the nation’s payments

5www.federalreserve.gov

official institutions, including playing a major role in operating the nation’s payments system

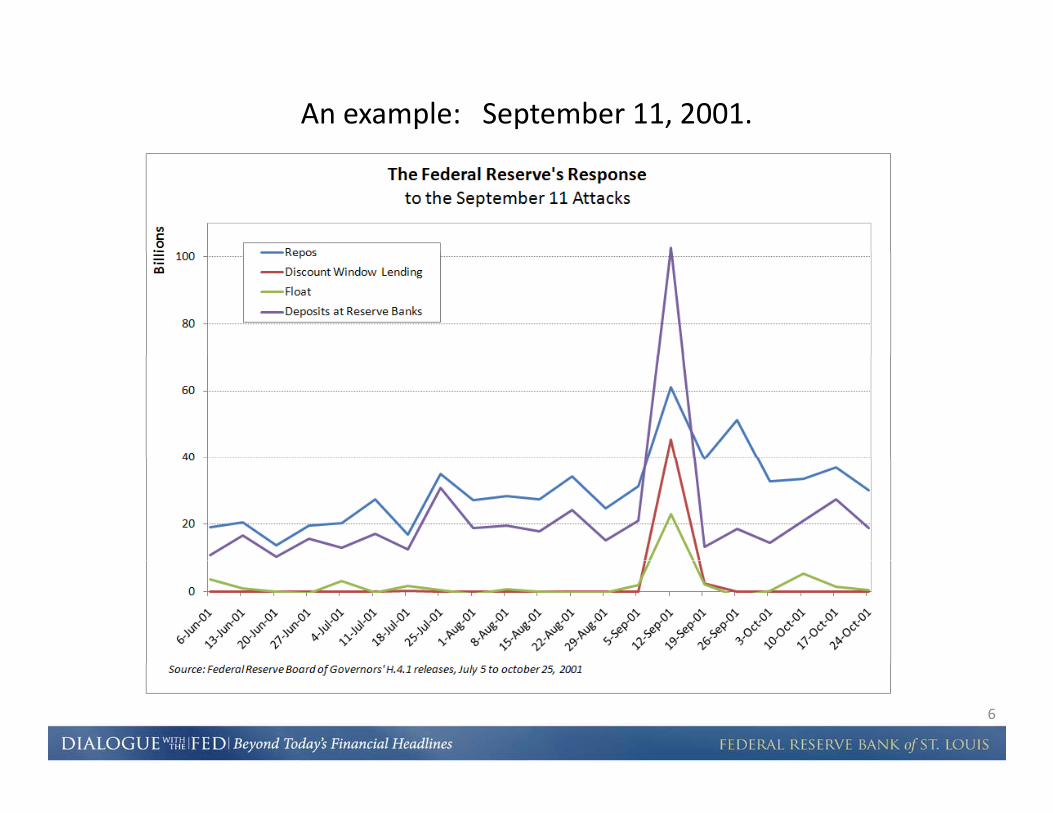

An example: September 11, 2001.

6

The Federal Reserve also played a major role in addressing the financial crisis of 2008.

“The financial crisis that gripped the United States last fall* was unprecedented in type and magnitude It began with anwas unprecedented in type and magnitude. It began with an asset bubble in housing, expanded into the subprime mortgage crisis, escalated into a severe freeze‐up of the interbank l di k t d l i t d i i t ti b th U it dlending market, and culminated in intervention by the United States and other industrialized countries to rescue their banking systems.”

Congressional Oversight Report on the Troubled Asset Relief Program, December 9, 2009

* Reference is to the fall of 2008

7

* Reference is to the fall of 2008

Let’s look back at what happened. Favorable mortgage rates d it i t h hmade it easier to purchase a home.

Mortgage Originations4000

s of d

olla

rs

Mortgage Originations

Prime Home-Equity Lines/Loans

3000

Bill

ions Alt A

Subprime

1000

2000Prime Jumbo

Prime Conventional/

02001 2002 2003 2004 2005 2006 xx 2007 Q2 Q3 Q4 2008 Q2 Q3 Q4

Conforming

FHA/VA

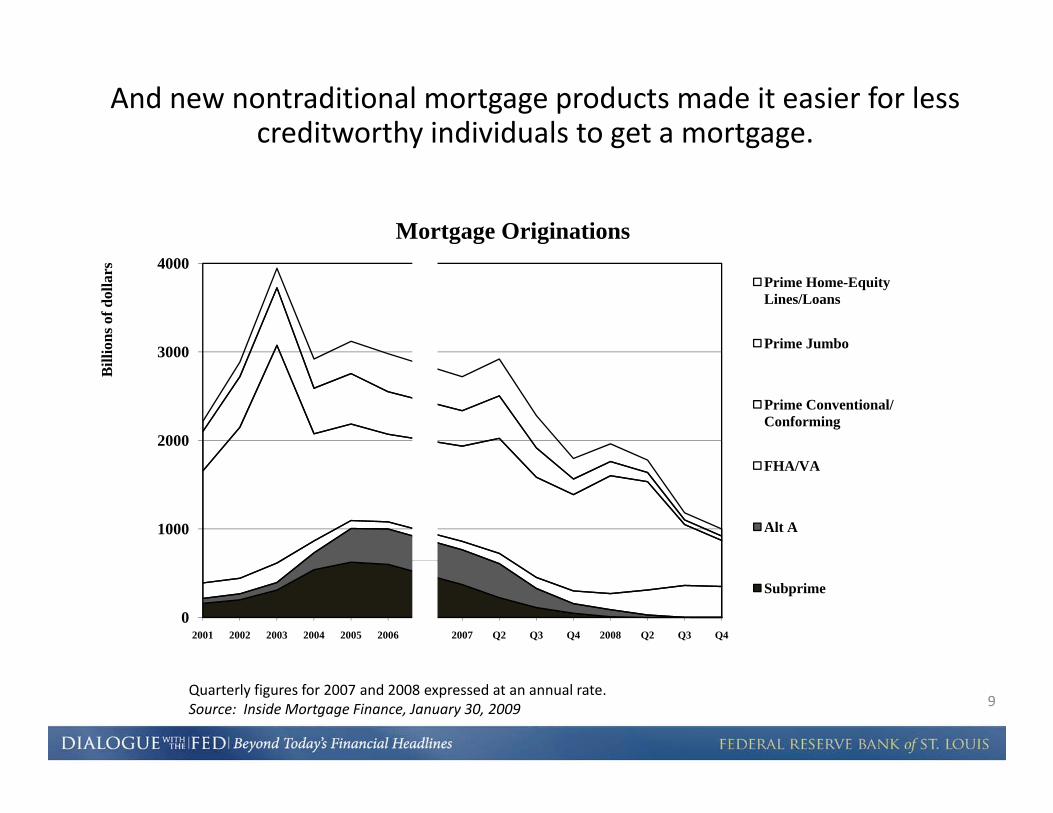

8Quarterly figures for 2007 and 2008 expressed at an annual rate.Source: Inside Mortgage Finance, January 30, 2009.

2001 2002 2003 2004 2005 2006 xx 2007 Q2 Q3 Q4 2008 Q2 Q3 Q4

And new nontraditional mortgage products made it easier for less creditworthy individuals to get a mortgage.

Mortgage Originations

3000

4000

lions

of d

olla

rs

Prime Home-Equity Lines/Loans

Prime Jumbo

2000

3000

Bill

Prime Conventional/ Conforming

1000

FHA/VA

Alt A

02001 2002 2003 2004 2005 2006 2007 Q2 Q3 Q4 2008 Q2 Q3 Q4

Subprime

9Quarterly figures for 2007 and 2008 expressed at an annual rate.Source: Inside Mortgage Finance, January 30, 2009

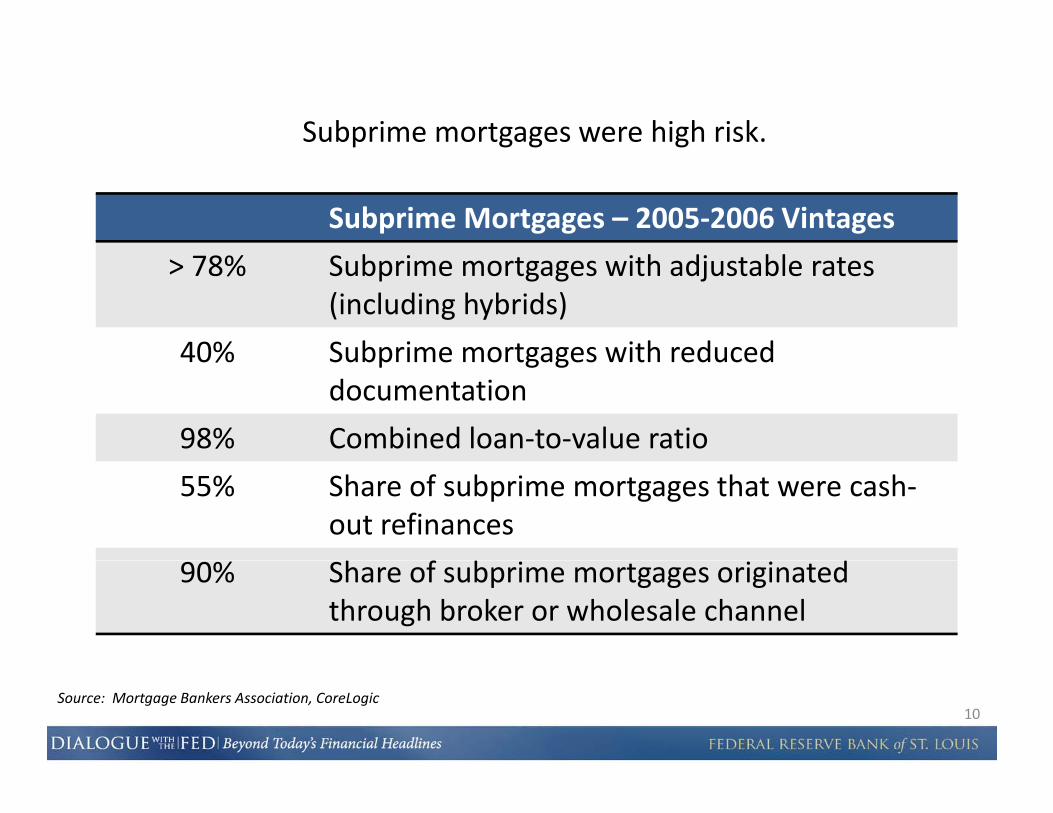

Subprime mortgages were high risk.

Subprime Mortgages – 2005‐2006 Vintages

> 78% Subprime mortgages with adjustable rates (including hybrids)

40% Subprime mortgages with reduced40% Subprime mortgages with reduced documentation

98% Combined loan‐to‐value ratio

55% Share of subprime mortgages that were cash‐out refinances

h f b90% Share of subprime mortgages originated through broker or wholesale channel

10Source: Mortgage Bankers Association, CoreLogic

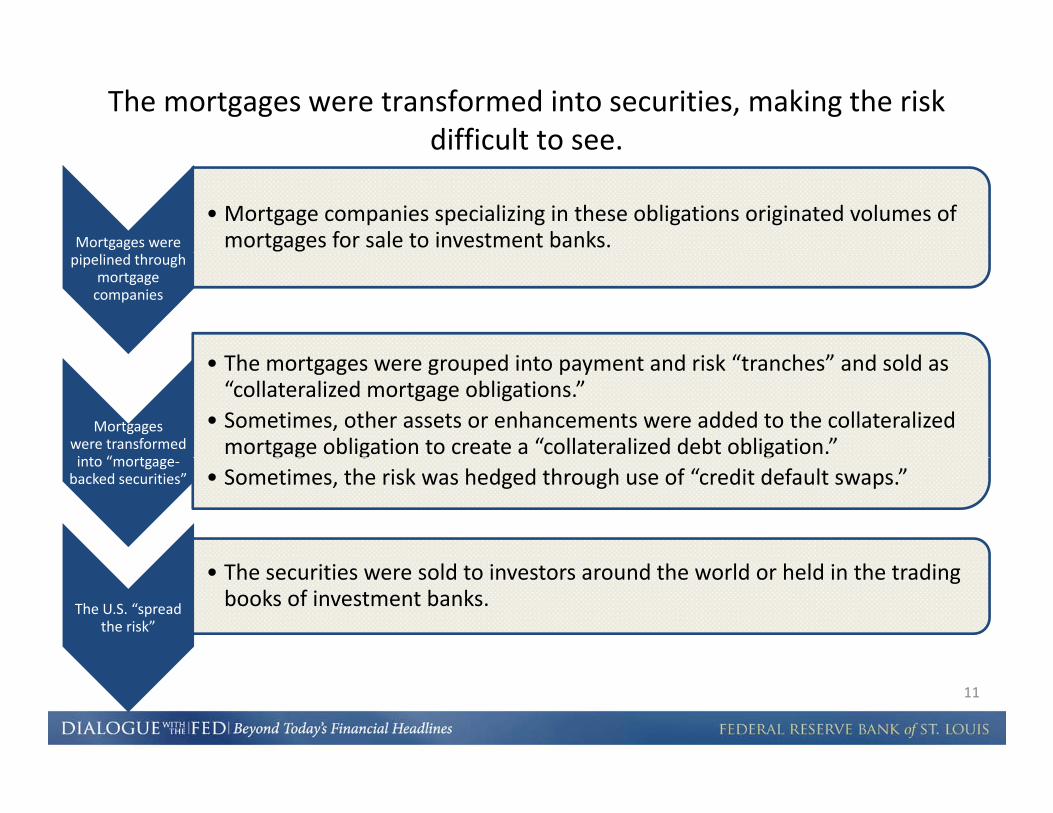

The mortgages were transformed into securities, making the risk difficult to see.

Mortgages were

• Mortgage companies specializing in these obligations originated volumes of mortgages for sale to investment banks.

pipelined through mortgage companies

h d i d i k “ h ” d ld

Mortgages were transformed i t “ t

• The mortgages were grouped into payment and risk “tranches” and sold as “collateralized mortgage obligations.”

• Sometimes, other assets or enhancements were added to the collateralized mortgage obligation to create a “collateralized debt obligation.”

into “mortgage‐backed securities”

g g g g• Sometimes, the risk was hedged through use of “credit default swaps.”

The U.S. “spread the risk”

• The securities were sold to investors around the world or held in the trading books of investment banks.

11

Cash‐out refinance options and home equity loans also accelerated and reduced the amount of equity in the home.

Total Home Equity Cashed Out in Freddie Mac Mortgage RefinancesBillions of dollars

375 375

300 300

225

150

225

150

75

0

75

0

12

10050095

Source: Federal Home Loan Mortgage Corporation /Haver Analytics

Easy credit fueled demand for houses, causing prices to rise at an unsustainable pace, especially in 2005 and 2006.

Loan Performance House Price Index (HPI)Nominal Loan Performance HPI (including distress sales),

deflated by Core Consumer Price IndexIndex = 1 at Start of Decade

1.5

1.7

1.9

1.1

1.3

1.5

0.5

0.7

0.9

00 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100

105

110

115

120

Months into Decade (120 Months in a Decade)

1980s 1990s 2000s 2010s

13

Months into Decade (120 Months in a Decade)

Source: BLS and Loan Performance/ Haver Analytics

Bank lending followed the housing boom.

Construction and Land Development Loans / Total Loans

14

16

18

8

10

12

Percen

t

4

6

8P

Chicago MSA Banks

All Banks in the U S

0

2All Banks in the U.S.

14Source: Call Reports

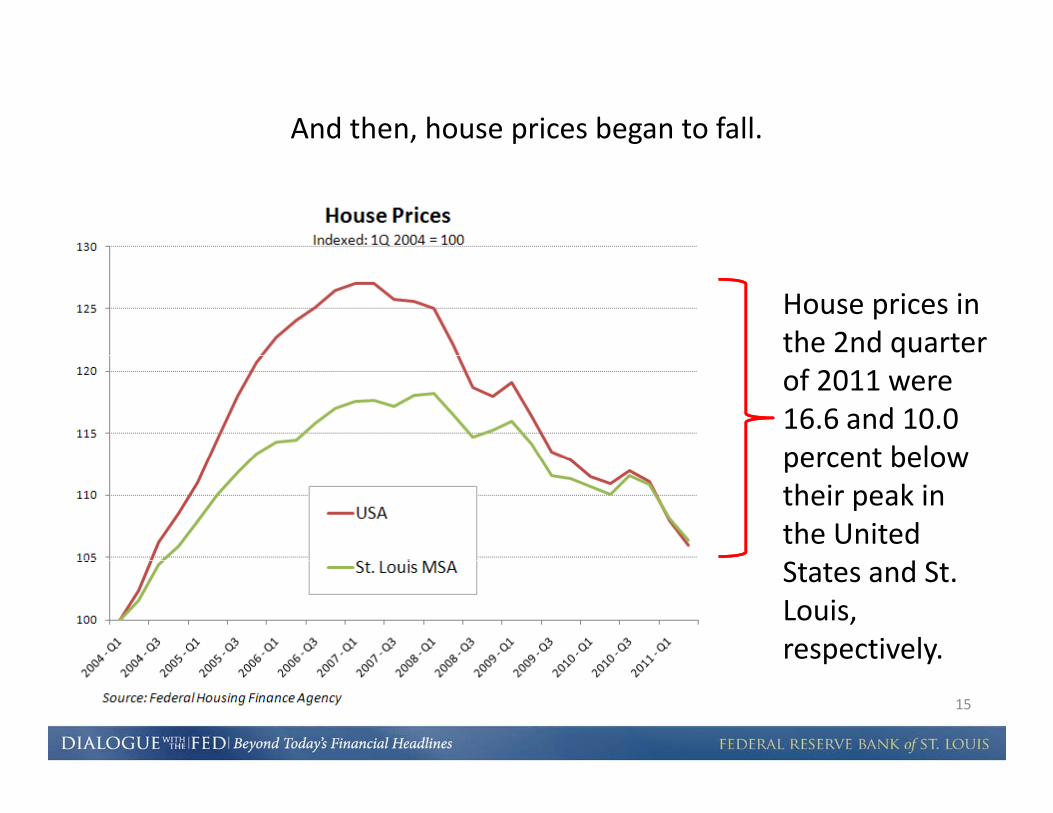

And then, house prices began to fall.

House prices in the 2nd quarter qof 2011 were 16.6 and 10.0 percent belowpercent below their peak in the United

dStates and St. Louis, respectively.

15

p y

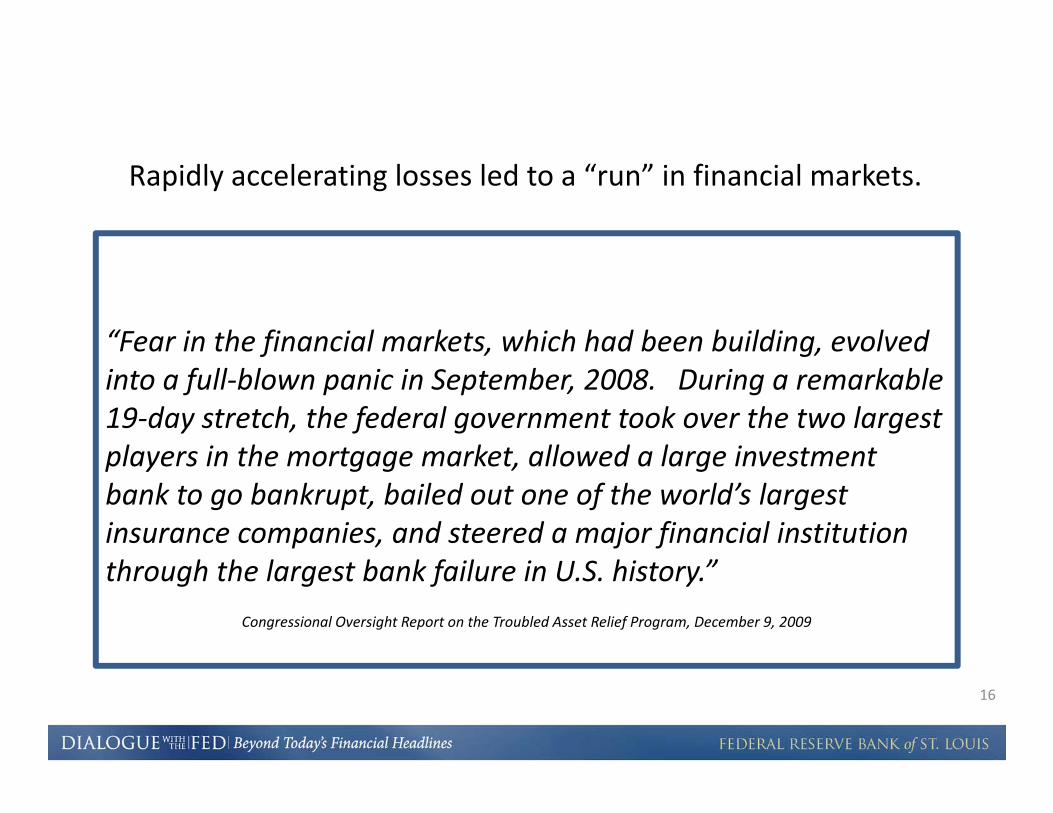

Rapidly accelerating losses led to a “run” in financial markets.

“Fear in the financial markets, which had been building, evolved f , g,into a full‐blown panic in September, 2008. During a remarkable 19‐day stretch, the federal government took over the two largest players in the mortgage market allowed a large investmentplayers in the mortgage market, allowed a large investment bank to go bankrupt, bailed out one of the world’s largest insurance companies, and steered a major financial institution h h h l b k f il i hi ”through the largest bank failure in U.S. history.”

Congressional Oversight Report on the Troubled Asset Relief Program, December 9, 2009

16

By September 2008 the country faced the most significant financialBy September 2008, the country faced the most significant financial crisis since the Great Depression.London Interbank Offered Rate (LIBOR) and Overnight Indexed Swap (OIS)

Interest Rate Spread Weekly January 2007 August 2011 inbasis points

3.5

4

Weekly, January 2007 ‐August 2011, in basis points

2

2.5

3

0.5

1

1.5

0

171 Month 3 Month

Source: British Bankers Associations and Reuters

The crisis required a massive response.

Federal Reserve

• Provided funds (liquidity) to stabilize financial markets.

United States

• Funded the Troubled Asset Relief Program, the $800 billion economic

First responders to United States

Government stimulus, Cash for Clunkers, Homebuyer Tax Credit, extended unemployment benefits.

pthe financial

crisis

Federal Deposit Insurance

• Raised bank deposit insurance limits and provided other bank

18Corporation

provided other bank debt guarantees.

A picture of the Federal Reserve’s actions.Federal Reserve Credit Easing Policy Tools

2,500,000

3,000,000

Federal Reserve Credit Easing Policy ToolsWeekly, January 2007 ‐August 2011, in millions of dollars

1,500,000

2,000,000

‐

500,000

1,000,000

Traditional Security Holdings Securities Lent to Dealers Repurchase Agreements

Other Fed Assets Currency Swaps Term Auction CreditOther Fed Assets Currency Swaps Term Auction Credit

Primary/Other Broker Dealer Primary Credit Secondary Credit

Seasonal Credit Maiden Lane 1 Maiden Lane 2

Maiden Lane 3 Asset‐Backed Commercial Paper Net Portfolio Holdings Comm Paper

Other Credit Credit to AIG Mortgage‐backed Securities

19Federal Agency Debt Securities Term Asset‐Backed Securities Long Term Treasury Purchases

Source: Federal Reserve Board.

While these actions avoided a collapse of the financial system…London Interbank Offered Rate (LIBOR) and Overnight Indexed Swap (OIS)

Interest Rate SpreadWeekly, January 2007 - August 2011, in basis points

300

350

400

150

200

250

0

50

100

-50

0

JAN07

JUN07

DEC07

JUN08

DEC08

JUN09

DEC09

JUN10

DEC10

JUN11

201 Month 3 Month

Source: British Bankers Associations and Reuters

we did not avoid a “Great Recession.”

10

Growth Real GDPPercent Change from Quarter A Year Ago,

NBER Recession Shaded in Grey

6

8

0

2

4

‐4

‐2

0

‐6

21Source: BEA

Source: Bureau of Economic Analysis

Home prices have collapsed in some markets

Geographic Area Market Peak Market TroughPeak to Current

Home prices have collapsed in some markets.

Geographic Area Market Peak Market TroughPercent Decline

Boston November 2005 April 2009 15.6

Chicago March 2007 April 2011 32.0

Denver March 2006 February 2009 10.9

Las Vegas April 2006 June 2011 59.2

Los Angeles April 2006 May 2009 37.8Los Angeles April 2006 May 2009 37.8

Miami May 2006 February 2011 49.8

New York City May 2006 March 2011 23.1

S Di M h 2006 M 2009 38 6San Diego March 2006 May 2009 38.6

San Francisco March 2006 May 2009 38.9

Washington, D.C. March 2006 March 2009 27.9

22Source: Case‐Shiller, through August 2011 release

Challenges remain in the housing market.Seriously delinquent or in‐foreclosure mortgages are backlogged and must work through the pipeline.

July 2011

23Source: Lender Processing Services (LPS) and Federal Housing Finance Agency (FHFA)

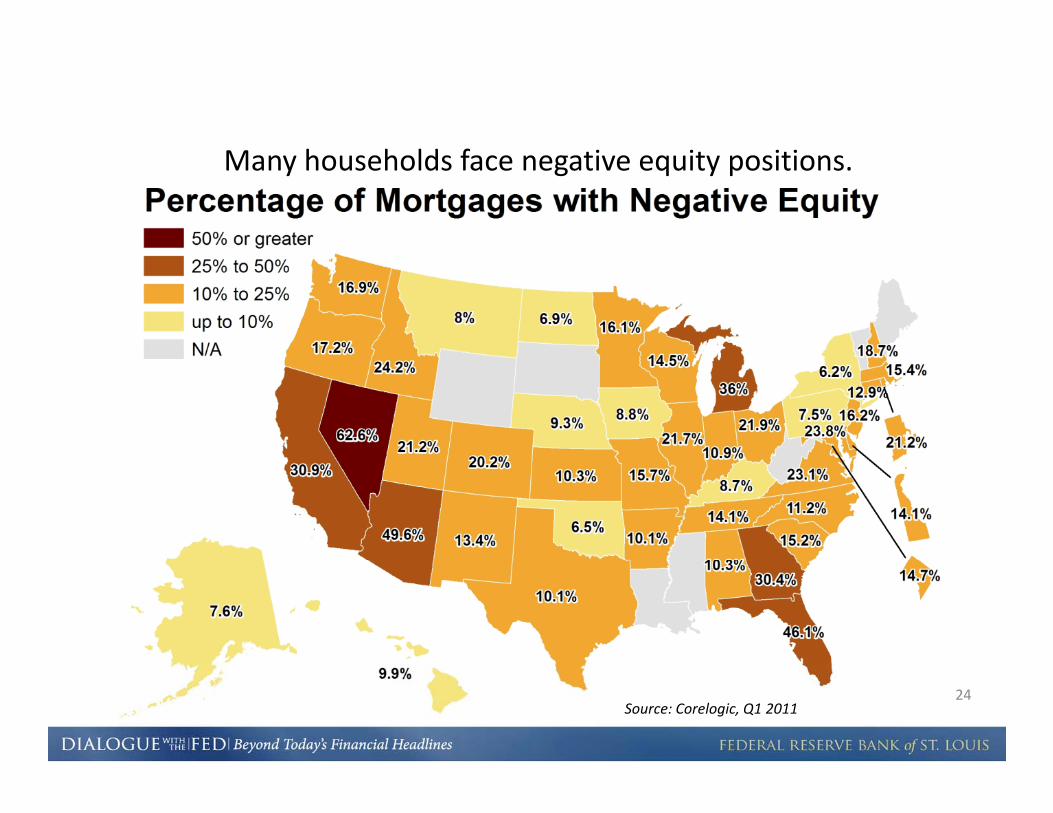

M h h ld f i i i iMany households face negative equity positions.

24Source: Corelogic, Q1 2011

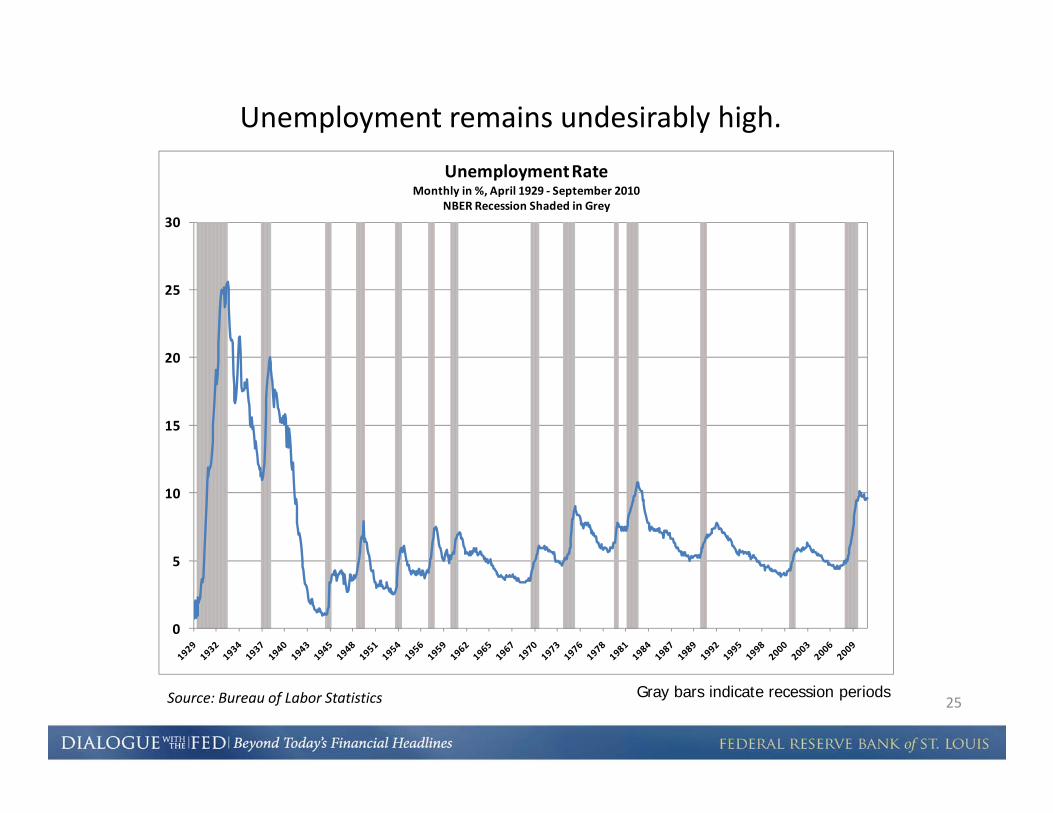

Unemployment remains undesirably high.

30

Unemployment Rate Monthly in %, April 1929 ‐ September 2010

NBER Recession Shaded in Grey

20

25

15

20

5

10

0

5

25Source: Bureau of Labor Statistics Gray bars indicate recession periods

On the other hand, mortgage financing options have quickly d Th b i k h l lcorrected. The subprime mortgage market has largely

disappeared.

250

Trends in Subprime Mortgage Originations and OutstandingsIndex, January 2005 = 100

150

200

50

100

Subprime Originations

SubprimeOutstandings

0

Subprime Outstandings

26Source: Calculations based on data from Lender Processing Service (LPS) Inc

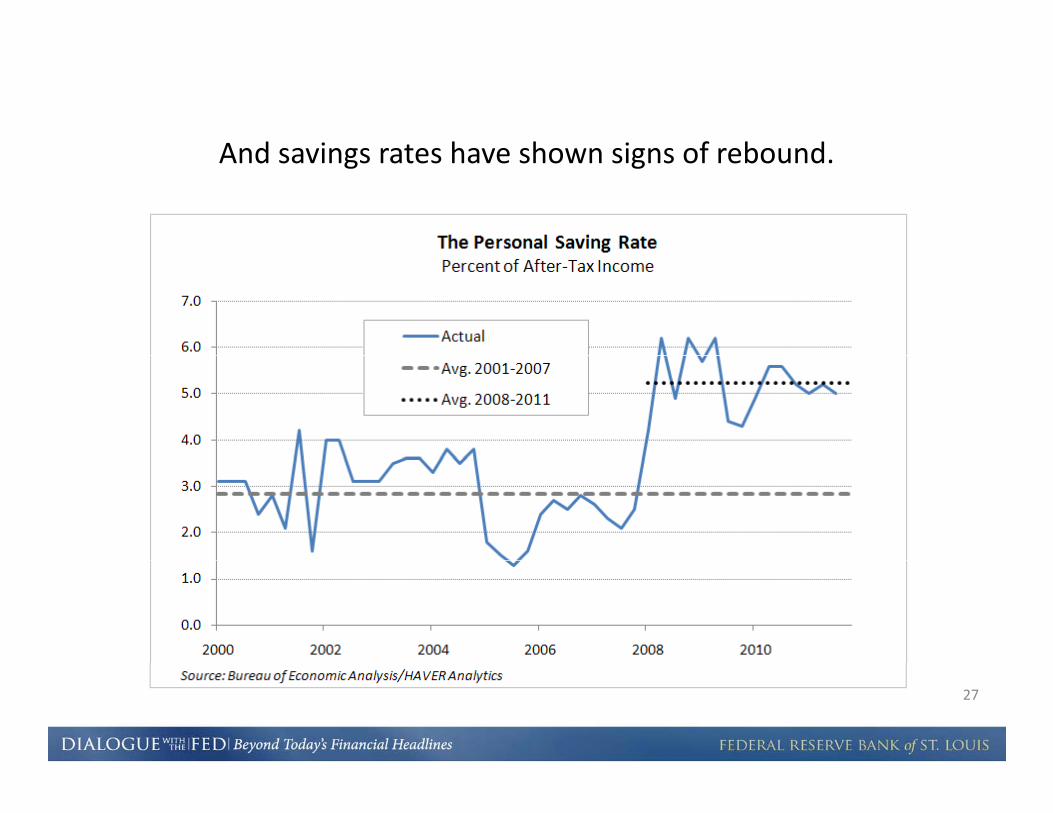

And savings rates have shown signs of reboundAnd savings rates have shown signs of rebound.

27

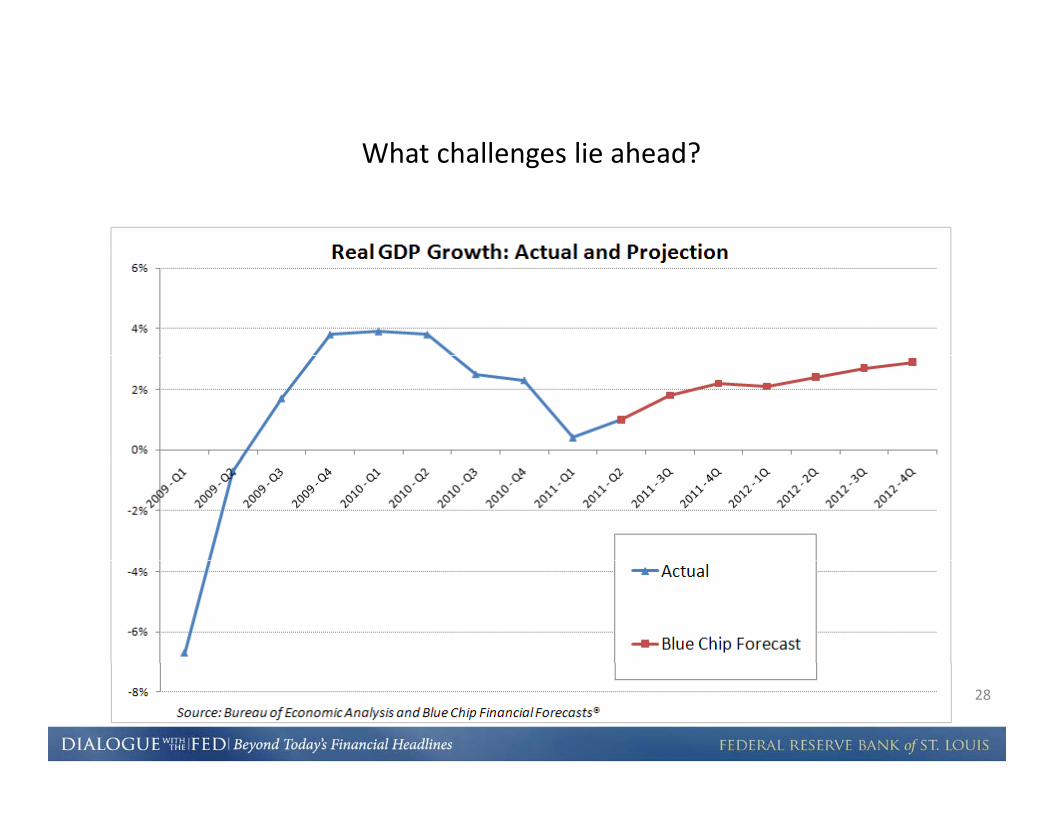

What challenges lie ahead?What challenges lie ahead?

28

What challenges lie ahead?

180

Gross Government Debt‐to‐GDPYearly, in %

120

140

160

180

80

100

120

20

40

60

0

China Greece Italy Spain United Kingdom United States

29Source: International Monetary Fund

The perspective of Fed Chairman Bernanke

“The growth fundamentals of the United States do not appear to have been permanently altered by the shocks of the pastto have been permanently altered by the shocks of the past four years. It may take some time, but we can reasonably expect to see a return to growth rates and employment levels

i t t ith th d l i f d t l ”consistent with those underlying fundamentals.”

Jackson Hole, Wyoming, August 26, 2011

30

What have we learned?

High levels of debt, uncertain ability of borrowers to repay debt, and an expectation that housing prices will always increase (among other factors) created a comfort level that wasincrease (among other factors) created a comfort level that was misguided.

Spreading risk outside of the insured banking system and useSpreading risk outside of the insured banking system and use of “insurance” policies such as credit default swaps did not result in risk diversification. Risk needs to be understood across all parts of the financial system – banks and nonbanksacross all parts of the financial system banks and nonbanks. The Dodd‐Frank Act provides a means to do so.

Choices made in the short‐run may have long‐run consequences that need to be carefully considered.

31

Questions tonight will be taken by:

• Julie Stackhouse

• Dr. William Emmons, Assistant Vice President and Economist

• Dr Silvio Contessi Economist• Dr. Silvio Contessi, Economist

• Mary H. Karr, Senior Vice President and General Counsel

32

Related Documents